Read and download the CBSE Class 10 Social Science Economics Money and Credit Assignment for the 2026-27 academic session. We have provided comprehensive Class 10 Economics school assignments that have important solved questions and answers for Understanding Economic Development Chapter 3 Money And Credit. These resources have been carefuly prepared by expert teachers as per the latest NCERT, CBSE, and KVS syllabus guidelines.

Solved Assignment for Class 10 Economics Understanding Economic Development Chapter 3 Money And Credit

Practicing these Class 10 Economics problems daily is must to improve your conceptual understanding and score better marks in school examinations. These printable assignments are a perfect assessment tool for Understanding Economic Development Chapter 3 Money And Credit, covering both basic and advanced level questions to help you get more marks in exams.

Understanding Economic Development Chapter 3 Money And Credit Class 10 Solved Questions and Answers

INTRODUCTION

Money acts as a medium of excahnge for goods and services. A person holding money can easily exchange it for any commodity or service that he or she might want. All the goods and services are bought and sold with the use of money .

The concept of money is not a recent phenomena. It gradually transformed from a medium of exchange to an important intermediate. Before the advent of money Barter System was in practise, but it had the problem of double coincidence of wants. To solve it, money was introduced.

IMPORTANCE OF MONEY

A person holding money can easily exchange it for any commodity or service that he or she might want. Everyone prefers to receive payments in money and then exchange the money for things that they want.

(a) Double coincidence of wants :

Double coincidence of wants mean both parties i.e., the buyer and the seller have to agree to sell and buy each others commodities. In a barter system where goods are directly exchanged without the use of money, double coincidence of want is an essential feature. In an economy where money is in use, money by providing the crucial intermediate step eliminates the need for double coincidence of wants.

(b) Money : as Medium of Exchange :

Since money acts as an intermediate in the exchange process, it is called a medium of exchange.

(i) Acts as an intermediary for the goods and services :

Medium of exchange is an important function of money. It means that money acts as an intermediary for the goods and services in an exchange of transaction. Use of money as a medium of exchange has removed the major difficulty of double coincidence of wants in the barter system.

(ii) Basis of time and place :

The medium of exchange, function of money has classified all transactions on the basis of time and place. Now, the seller of goods need not sell his goods at a particular time and place and buy goods of the same value as well.

(iii) Money facilitates multi-lateral trade :

The 'medium of exchange' function of money implies that money is generally acceptable by the people. They can buy goods and services they need using money. That is, money facilitates multi-lateral trade.

(iv) Economic freedom :

Money also offers economic freedom to the people.

(c) Role of money in an economy :

(i) Indispensable role :

Money plays an important role in the economy of a country. The use of money is at every step of life. In fact it would be hard to imagine life without money.

(ii) Facilitate the exchange of goods and services

The main function of money in an economic system is to facilitate the exchange of goods and services, i.e., to lessen the time and effect required to carry on trade.

(iii) Needs and requirements :

Without exchange of goods and services nobody can fulfill all his needs and requirements.

Without money, exchange is not easy. Barter system has many problems.

(iv) Usaye of money

We are living in world, with a very large group of countries and their population. As the group becomes larger and larger, problems begin to emerge more and more with the barter system.

(v) Specialisation :

Modern economies are highly specialized. There is specialization of firms, of business, of regions, of types of capital, etc. Such specialization allows the utilization of each person at the best of his or her ability and skill, each region to the maximum advantage, and the use of large amounts of specialized capital to reap economics of scale. The fruits of this are high standards of living and productivity. All this specialization will not be possible without an equal highly developed system of exchange and trade, i.e., the use of money.

(vi) Basic Factors :

Money serves the economy of the country performing the following four most important functions: (a) a unit of value (b) medium of exchange (c) a standard deferred payments and (d) store of value.

MODERN FORMS OF MONEY

(i) Paper notes and coins

Modern forms of money include currency- paper notes and coins. The modern currency is without any use of its own.

(ii) Gold, silver and copper

Traditional forms of money include gold, silver and copper. The traditional money had its own uses.

(a) Why currency is accepted as a medium of exchange ? :

(i) It is accepted as a medium of exchange because the currency is authorized by the government of the country.

(ii) The law legalizes the use of rupee as a medium of payment that cannot be refused in settling transactions in India. No individual in India can legally refuse a payment made in rupees.

(b) Monetary system adopted by India :

(i) Paper currency standard

India has adopted paper currency standard which is also referred as the managed currency standard.

(ii) Legal money

The monetary standard means the types of standard money used and the standard refers to legal money in which the government discharges its obligations. The monetary standard is thus synonymous with the standard money adopted. Thus in India paper currency is the unlimited legal tender i.e., it is used to settle debts and make payments to an unlimited amount.

(iii) Currency notes and coins

Reserve Bank of India issues all currency notes and coins except one rupee notes and coins which are issued by ministry of finance.

(iv) Reserve system

The system governing note issue is the minimum reserve system which means that we have kept a reserve of 200 crore and the Central Bank is permitted to issue notes to any extent.

(c) Deposits with Banks :

People who have extra money can deposit it with the banks by opening a bank account in their name. Banks accept the deposits and also pay an interest rate on the deposits. In this way people money is safe with the banks and earns an interest. People also have the provision to withdraw the money as and when they require. Since the deposits in the bank accounts can be withdrawn on demand these deposits are called demand deposits.

(d) Cheque and its advantages :

Demand deposits offer another interesting facility. Any person who has an account with the bank can make his payments through cheques. A cheque is a paper instructing the bank to pay a specific amount from the person's account to the person in whose name the cheque has been made.

(i) It is the safest mode of transactions.

(ii) It is easy to carry a cheque as compare to money.

(iii) The facility of cheques against demand deposits makes it possible to directly settle payments without the use of cash.

ROLE THE BANKS PLAY IN THE ECONOMY OF A COUNTRY

The banks play an important role in the economy of a country

(i) Safe custody

They keep the money of the people in safe custody otherwise people can become an easy prey of thieves or robber.

(ii) Income of the depositor

They give interest on the money deposited by the people. Thus they add to the income of the depositor. Many families survive on the bank interest.

(iii) Mendiation

The banks mediate between those who have surplus money and those who need money.

(iv) Cheap loans

Banks provide cheap loans to a large number of people.

(v) Agriculture loans

Banks promote agriculture by providing loans to the farmers who can increase their production by bringing new farm implements and make better arrangements for the irrigation of their fields without which they cannot survive.

(vi) Cheap loans to the industrialists

Banks boost the country's industry also by providing cheap loans to the industrialists etc.

(vii) The banks are the backbone of the country's trade also.

(viii) Employment

Banks employ a large number of people and as such they solve the employment problem also.

(a) Central Bank :

Is an apex institution in the banking and financial structure of a country. It plays a leading role in controlling, regulating, supervising and developing the banking and financial structure of the economy.

Function of a central bank

(i) It issues the currency notes.

(ii) It acts as a banker to the government.

(iii) Central bank acts as a banker of banks.

(iv) Central bank also functions as the custodian of foreign exchange reserve of a country.

(v) It controls credit.

(vi) It also performs developmental and promotional functions.

(vii) It maintains relation with the international organizations such as the World Bank, IMF, etc.

(viii) It conducts research studies and surveys and publishes reports.

(ix) It formulates an appropriate monetary policy for the country.

(x) It provides training facilities to the staff working in a various banking institutions in the country.

(b) Commercial banks :

A banking company is one which transacts the business of banking which means accepting deposits for the purpose of Indian companies lending or investment, deposits of money from the public, repayable on demand or otherwise withdrawable by cheque, draft etc. Commercial banks are also called joint stock banks because they are organized in the same manner as joint stock companies.

Main features of commercial banks are :-

(i) It deals with money; it accepts deposits and advances loans.

(ii) It also deals with credit. It has the power to create credit.

(iii) It is a commercial institution, whose aim is to earn profit.

(iv) It is a unique financial institution that creates demand.

(v) It deals with the general public.

(c) Loan activities of banks :

(i) Small proportion of their deposits

Banks keep only a small proportion of their deposits as cash with themselves. For example, banks in India these days hold about 15 percent of their deposits as cash. This is kept as a provision to pay the depositors who might come to withdraw money from the bank on any given day. Since, on any particular day, only some of its many depositors come to withdraw cash, the banks are able to manage with this cash.

(ii) Deposits to extend

Banks use the major portion of the deposits to extend loans. Banks make use of the deposits to meet the loan requirements of the people.

(iii) Madiation

In this way, banks mediate between those who have surplus funds (the depositors) and those who are in need of these funds (the borrowers)

(iv) Debt-trap. Credit

Informal sources charge a higher interest rate on loans than they offer on credit, thus instead of helping them in improving their earnings, leave those worse off. This is an example of what is commonly called debt-trap. Credit in this case pushes the borrower into a situation from which recovery is very painful.

(d) Role of credit for development :

(i) Development of a country

It plays a major role in the development of a country by creating better facilities for agricultural and industrial activities.

(ii) Earnings and support their families

Moreover, it helps people from all walks of life in setting up their business, increase their earnings and support their families.

(iii) Other Activities

To some people, loans help a lot in constructing their houses and get rid of monthly rents.

(iv) Social status

To others, loans or credit help a lot in raising their social status by enabling them to buy cars, scooters, televisions etc.

(e) Terms of Credit :

Interest rate, collateral and documentation requirement, and the mode of repayment together comprise what is called the terms of credit. The terms of credit vary substantially from one credit arrangement to another. They may vary depending on the nature of the lender and the borrower.

(f) Collateral :

Is an asset that the borrower owns (such as land, building, vehicle, livestock, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid. If the borrower fails to repay the loan, the lender has the right to sell the asset or collateral to obtain payment. Property such as land titles, deposits with banks, livestock are some common examples of collateral used for borrowing.

(g) Reasons when the banks might not be willing to lend to certain borrowers :

(i) Certificate

Some persons are not able to produce certificate of their earnings.

(ii) Documents

There are other people who are not able to produce documents of their employment.

(iii) Security/collateral

Some persons have nothing to give to the bank as security/collateral- no house, no land etc.

(iv) Witness

There are few others who fail to produce two persons who can stand as surety in case he is unable to repay the loan.

SECTORS OF CREDIT IN INDIA

The various types of loans can be conveniently grouped as

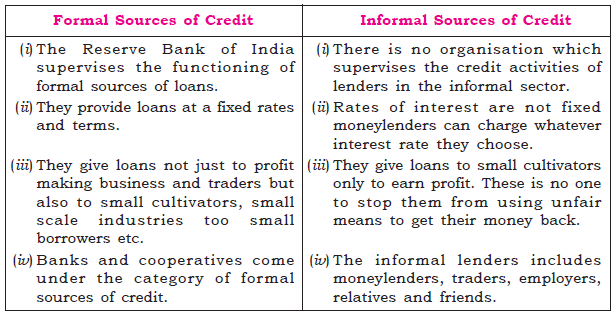

(a) Formal sector loans :

These resources work under the supervision of the Reserve Bank of India. The rate of interest is very low. Commercial banks, cooperative societies are the main source of formal source of credit.

(b) Informal sector loans :

These do not work under any government organization. The rate of interest is very high. Relatives, money lenders and landlords are the main source.

RESERVE BANK OF INDIA (RBI)

The Reserve Bank of India supervises the functioning of formal sources of loans. For instance, the banks maintain a minimum cash balance out of the deposits they receive. The RBI monitors that the banks actually maintain the cash balance. Similarly, the RBI sees that the banks give loans not just to profit making businesses and traders but also to small cultivators, small scale industries, to small borrowers etc. Periodically, banks have to submit information to the RBI on how much they are lending to whom, at what interest rate, etc. The supervision of RBI is necessary due to the following reasons:

(i) Safe deposits It is required to safe deposits of the peoples with the banks and the cooperative society.

(ii) Minimum cash balance It gives a power to RBI to force banks to maintain a minimum cash balance of the deposits they receives.

(iii) Supervision The RBI can check the other banks to loan only to honest and real needy people who are having capacity to repay the loan along with interest on time.

(iv) Checking policy RBI checks that all formal credit agencies are following the economic policy or guidelines laid down by the government of the country.

SELF-HELP GROUP FOR THE POOR

(i) A typical self help group can have 15 to 20 members usually belonging to the same village.

(ii) The main motive of self help group is to pool the savings of the poor people.

(iii) Saving per member can vary from Rs. 25 to Rs. 100 or more depending on the ability of the people and the strength of the group.

(iv) The self help groups provide loans to their members at a reasonable rate.

(v) After a year or two, if the group is regular in savings, it becomes eligible for bank loans.

(vi) Loan is sanctioned in the name of the group with the main motive to create self employment opportunities for the members.

(vii) In the recent years, many commercial and cooperative banks have provided loan to these self help groups for releasing mortgaged land, for meeting working capital needs, for housing materials, for acquiring assets like sewing machines, handlooms, cattle etc.

(viii) Most of the self help groups work in a democratic way i.e., it is the group which decides regarding the loans to be granted, interest to be charged, schedule etc.

(ix) A case of non-repayment of loan by any member is followed up seriously by other members in the group and because of this feature the commercial banks don't hesitate to lend loans to these groups.

(x) The most important feature of self help groups is that most of these groups are being organized by women. These are helping women to become financially self reliant. The regular meetings of the group provide a platform to discuss and act on a variety of social issues such as health, dowry, domestic violence, child marriage etc.

Example : Grameen Bank.

Choose the correct option

Question. What is the most important function of money?

(a) Used in banking transactions

(b) Payment of loans

(c) Medium of exchange

(d) Stock market exchange

Answer : C

Question. A person can withdraw money by issuing a cheque. What is a cheque?

(a) Loan taken by the bank.

(b) Loan taken by the depositor from the bank.

(c) Paper instructing the bank to pay a specific amount.

(d) Paper valid to withdraw money

Answer : C

Question. A substitute of cash and cheque is

(a) credit card

(b) coin

(c) currency

(d) demand deposit

Answer : A

Question. Which of the following is not a feature of Self Help Groups (SHGs)?

(a) It consists of 15-20 members or more.

(b) Here members pool their savings which acts as collateral.

(c) Loans are given at nominal rate of interest.

(d) It is an informal source of credit.

Answer : D

Question. Modern forms of money include which of the following?

(a) Currency notes and coins

(b) Cowrie shells and stones

(c) Gold and silver coins

(d) Grains and cattle

Answer : A

Question. Bank laying down norms for bank is

(a) RBI

(b) SBI

(c) syndicate bank

(d) all of these

Answer : A

Question. Percentage of formal sector in total credit in India in poor household is

(a) 15

(b) 20

(c) 70

(d) 80

Answer : A

Question. A system where goods were exchanged without using money is batter known as

(a) goods system

(b) exchange system

(c) barter system

(d) no-money system

Answer : C

Question. Raghav has surplus money so he opens a bank account and deposits in it. Whenever he needs money. he can go to his bank and withdraw from there. This kind of deposit with the banks are known as

(a) demand deposit

(b) term deposit

(c) fixed deposit

(d) surplus deposit

Answer : A

Question. All the banks act as mediator between .......... and .......... .

(a) rural people, urban people

(b) literates, illiterates

(c) people, government

(d) depositors, borrowers

Answer : D

Question. A porter making pots, wants to exchange pots for wheat. Lukily, he meets a farmer who has wheat and is willing to exchange it for the pots. What is this situation known as?

(a) Incidence of wants

(b) Double coincidence of wants

(c) Barter system of wants

(d) None of the above

Answer : B

Question. Chit fund come under

(a) organised credit

(b) unorganised credit

(c) discounted coupon

(d) none of these

Answer : B

Question. A trader provides farm inputs on credit on the

condition that farmers will sell their crop

produce to him at .......... prices so that he

could sell them at .......... prices in the market.

(a) high, medium

(b) low, high

(c) medium, high

(d) high, low

Answer : B

Question. In agricultural stage grains were used as

(a) money

(b) commodity

(c) ingredient

(d) none of these

Answer : A

Question. Money is based on

(a) double coincidence of wants

(b) single coincidence of wants

(c) Both a and b

(d) none of these

Answer : A

Question. Method of repayment of loan is called

(a) mode of payment

(b) method of payment

(c) mode of repayment

(d) none of these

Answer : C

Question. Banks give out loans and charge .......... on the loan amount from the borrower.

(a) rent

(b) wages

(c) interest

(d) money

Answer : C

Question. Ram and Shyam are small farmers. Ram has taken credit 1.5% per month on < 20000 from a trader while Shyam has taken credit at 8% per annum from bank on the same amount. Who is better off?

(a) Ram is better because he has to do no paperwork.

(b) Shyam is better because his interest payment is less.

(c) Ram is better because he has not paid any collateral.

(d) Both Ram and Shyam are equal so no one is better off.

Answer : B

Question. Money is a measured of

(a) currency

(b) value

(c) transfer

(d) all of these

Answer : A

Question. Which among the following lenders will possibly not ask the borrower to sign the terms of credit?

(a) Banks

(b) Moneylenders

(c) Cooperatives

(d) Private agencies

Answer : B

Question. Which among the following is not a feature of informal source of credit?

(a) It is supervised by the Reserve Bank of India.

(b) Rate of interest is not fixed.

(c) Terms of credit are very flexible.

(d) Traders, employers, friends, relatives, etc provide informal credit source.

Answer : A

Question. The problem of similar wants made exchange difficult, so a new medium of exchange was developed known as

(a) capital

(b) cost

(c) rent

(d) money

Answer : D

Question. Organised credit is also called

(a) informal credit

(b) formal credit

(c) cooperative credit

(d) none of these

Answer : B

Question. Which of the following is a reason for using money to buy goods and services?

(a) Money can be easily exchanged for any good or service a person wants.

(b) Money is more valuable than any good or service a person wants.

(c) Money cannot be put to any other use apart from transaction.

(d) Money is less valuable than any good or service a person wants so people easily give money for the goods and services.

Answer : A

Question. Ethnic tension between Serbs and Albanians resulted in disintegration of which of the following countries ?

(a) Sri Lanka

(b) Belgium

(c) Yugoslavia

(d) Bolivia

Answer : C

Question. A system where goods are exchanged for other good is called ______.

(a) barter system

(b) flexible exchange system

(c) fluctuating system

(d) rational trade system

Answer A

Question. Arrange the Sequence

(i) Bank money (ii) Commodity money

(iii) Metallic money (iv) Paper money

Options –

(a) iv-i-ii-iii

(b) ii-iii-iv-i

(c) iii-iv-ii-i

(d) iii-iv-i-ii

Answer : B

Question. Mohan produces ice creams and wants to sell it to people. He also requires sugar to make ice cream, so he wishes to buy sugar. Now, Mohan is unable to find a person who will exchange sugar for ice cream. Which of the following terms explain the problem that Mohan is facing?

(a) Lack of trade expertise

(b) Double coincidence of wants

(c) Irrational consumer behavior

(d) Future expectations

Answer : B

Question. Which of the following statement is true of banks?

(a) Banks mediate between those who want to sell one commodity in exchange of other commodity

(b) Banks use a major proportion of deposits to invest in mutual funds.

(c) Banks charge a lower interest rates on loan than the interest rate they offer on deposits.

(d) Banks use the deposits to fulfil loan requirements of the people.

Answer : D

Question. Because money acts as an intermediary in a transaction, it is referred to as _____.

(a) Unit of account

(b) Standard of deferred payment

(c) Medium of exchange

(d) Store of value

Answer : C

Question. Which of the following statement best describes the double coincidence of wants?

(a) A person must have money if he or she wishes to buy a good or service.

(b) A person should demand a great amount of a good or service so that another person is willing to produce it.

(c) Two individuals must agree to sell and buy each other’s commodities to conduct the trade.

(d) Two individuals must be able to produce all goods and services for the entire society.

Answer : C

Question. Which among the following issues currency notes on behalf of the Central Government ?

(a) State Bank of India

(b) Reserve Bank of India

(c) Commercial Bank of India

(d) Union Bank of India

Answer : B

Question. Which of the following statement best describes a debt trap?

(a) When a person takes credit but is unable to repay it and has to take more credit either to repay the previous credit, the person is in a debt trap.

(b) When a person takes credit for production process, earns good profit, returns the credit and again takes credit in the next production cycle, the person is in a debt trap.

(c) When a person takes loan from unorganized sector, the person is in a debt trap.

(d) When a person takes loan from a bank, the person is in a debt trap as the banks charge a very high interest rate on loans.

Anwer : A

Question. Which of the following statement best describes a demand deposit?

(a) The cash held by people which can be used as and when they require is called demand deposit.

(b) The cash deposited in a bank which can be withdrawn on demand is called demand deposit.

(c) The order to a bank to pay a certain sum from the drawer’s account is called demand deposit.

(d) The currency approved by international bodies to carry out trade practices is called demand deposit.

Answer : B

Question. A paper that instructs a bank to pay a specific amount from a person’s account to another person in whose name the paper is issued is called a ______.

(a) demand deposit

(b) time deposit

(c) bond

(d) cheque

Answer : D

Question. What is the most important function of the banks?

(a) Accept deposits and extend loans.

(b) Give loans to government.

(c) Open as many bank accounts as possible.

(d) Give loans to businesses.

Answer : A

Question. An example of cooperative society can be of

(a) farmers

(b) workers

(c) women

(d) all of these

Answer : D

Question. Who has the authority to issue the following currency note ?

(a) Central Government

(b) Reserve Bank of India

(c) Union Bank of India

(d) State Bank of India

Answer : B

True or False

Question. Since money acts as an intermediate in the exchange process, it is called a medium of exchange. (True/False)

Answer : True

Question. Money eliminates the need for double coincidence of wants. (True/False)

Answer : True

Question. In the barter system, when the demand of two persons for each other’s commodity is raised at the same time, it is called double coincidence of wants. (True/False)

Answer : True

Question. Transactions are made in money because it eliminates the inconvenience of barter system of exchange. (True/False)

Answer : True

Question. Paper notes are accepted as a medium of exchange because the currency is authorized by the government of the country. (True/False)

Answer : True

Match the following :

Answer : 1. (C), 2. (D), 3. (B), 4. (E), 5. (A)

Assertion and Reasoning Based Questions

Mark the option which is most suitable :

(a) If both assertion and reason are true and reason is the correct explanation of assertion.

(b) If both assertion and reason are true but reason is not the correct explanation of assertion.

(c) If assertion is true but reason is false.

(d) If both assertion and reason are false.

Question. Assertion : Banks keep only a small proportion of their deposits as cash with themselves.

Reason : Banks in India these days hold about 15 per cent of their deposits as cash.

Answer : (b) Banks keep only a small proportion of their deposits as cash with themselves because they use the major portion of the deposits to extend loans as there is a huge demand for loans for various economic activities.

Question. Assertion : In India, no individual can refuse to accept a payment made in rupees.

Reason : Rupee is the legal tender in India.

Answer : (a) The law legalises the use of rupee as a medium of payment that cannot be refused in settling transactions in India.

Question. Assertion : The facility of demand deposits makes it possible to settle payments without the use of cash.

Reason : Demand deposits are paper orders which make it possible to transfer money from one person’s account to another person’s account.

Answer : (d) The facility of cheques against demand deposits makes it possible to directly settle payments without the use of cash. Since demand deposits are accepted widely as a means of payment, along with currency, they constitute money in the modern economy.

Question. Assertion : The modern currency is used as a medium of exchange; however, it does not have a use of its own.

Reason : Modern currency is easy to carry

Answer : (b) The modern currency is used as a medium of exchange because it is accepted and authorised as a medium of exchange by a country’s government.

Question. Assertion : Banks charge a higher interest rate on loans than what they offer on deposits.

Reason : The difference between what is charged from borrowers and what is paid to depositors is their main source of income.

Answer : (a) Banks in India hold about 15 per cent of their deposits as cash as the remaining deposits are used to provide loans. The interest charged on loans is higher than the interest paid on deposits and the difference between the two interest rates is the major source of income for banks.

Question. Assertion : Collateral is an asset that the borrower owns (such as land, building, vehicle, livestock, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid.

Reason : Collateral is given as the lender can sell the collateral to recover the loan amount if the borrower fails to repay the loan.

Answer : (a) Property such as land titles, deposits with banks, livestock are some common examples of collateral used for borrowing. In case of failure of repayment of loan, the lender can sell the collateral to recover the loan amount.

Question. Assertion : Rohan took credit in the form of advance payment from a buyer and he delivered the goods to the buyer on time and also earned profit. The credit made Rohan better off in this situation.

Reason : Credit can never push a person into a debt trap.

Answer : (c) The credit made Rohan better off in this situation, however, Rohan would have been worse off if he had failed to deliver the goods on time or he had made a loss in the production process. The latter two situations may have caused Rohan to fall in a debt trap.

Question. Assertion : The Reserve Bank of India supervises the functioning of formal sources of loans.

Reason : The RBI sees that the banks give loans not just to profit-making businesses and traders but also to small cultivators, small scale industries, to small borrowers etc.

Answer : (b) The RBI oversees the functioning of commercial banks. The reason statement substantiates the assertion but it is not the explanation for the assertion.

Question. Assertion : If credit would be useful or not depends on the risk involved in a situation.

Reason : The chance of benefitting from credit is highest in agriculture sector.

Answer : (c) Whether credit would be useful or not depends on the risks in the situation and whether there is some support, in case of loss.

Question. Assertion : The terms of deposit are same for all credit arrangements.

Reason : Credit arrangements are very complex process so to remove the complexities same terms of deposits are used.

Answer : (d) The terms of credit vary substantially from one credit arrangement to another. They may vary depending on the nature of the lender and the borrower.

Source/Extract Based Questions

Read the extract given below and answer the questions that follow:

Salim, has received an order from a large trader in town for 3,000 pairs of shoes to be delivered in a month time. To complete production on time, Salim has to hire a few more workers for stitching and pasting work. He has to purchase the raw materials. To meet these expenses, Salim obtains loans from two sources. First, he asks the leather supplier to supply leather now and promises to pay him later. Second, he obtains loan in cash from the large trader as advance payment for 1000 pairs of shoes with a promise to deliver the whole order by the end of the month. At the end of the month, Salim is able to deliver the order, make a good profit, and repay the money that he had borrowed.

Answer the following MCQs by choosing the most appropriate option

1. The passage given above related to which of the following options?

(a) Different credit situations

(b) Trading and selling

(c) Smart manufacturing

(d) Complex show manufacturing

Answer : A

2. According to the given passage, which one of the followings was the benefit of taking credit?

(a) To meet the production expenses

(b) To complete production on time

(c) To increase his earnings

(d) All of the above

Answer : D

3. Salim was pushed to take credit because of _______ .

(a) Less work force and raw material

(b) Sudden high demand for shoes

(c) Both (a) and (b) are correct

(d) Both (a) and (b) are incorrect.

Answer : B

4. What could be the reason that Salim did not approach bank for loan?

(a) Lack of trust with bank

(b) No bank in the vicinity

(c) High Interest rate

(d) Leather supplier and trader are known to him

Answer : D

Read the passage and answer the following question –

Arun is supervising the work of one farm labourer. He has seven acres of land. He is one of the few persons in Sonpur to receive bank loan for cultivation. The interest rate on the Loan is 8.5 % per annum and can be repaid anytime in the next three years. He plans to repay the loan after harvest by selling a part of the crop.

1. What type of credit Arun has taken ?

Answer : Arun has taken credit from formal sector.

.2 At what rate of interest Arun gets loan ?

Answer : 8.5%

3. In how many years, he can pay the loan ?

Answer : 3 years

Read the sources given below and answer the questions that follow– Answer :

Source A – Currency

Currency includes paper notes and coins it is a modern form money. Unlike the things that were used as money earlier, modern currency is not made of precious metal such as gold, silver and copper. And unlike grain and cattle, they are neither of everyday use. The modern currency is without any use of its own.

Source B – Reserve Bank of India

In India, The RBI issues currency notes on behalf of the Central Government. As per Indian Law, no other individual or organisation is allowed to issue currency. Moreover, the law legalises the use of rupee as a medium of payment that can not be refused in selling transactions in India. Hence, the rupee is widely accepted as a medium of exchange.

Source C – Deposits with Bank

The other form in which people hold money as deposits with banks. At a point of time, people need only some currency for their day to day needs but beyond that need they deposit the money with the banks and banks pay interest on such deposits. People can withdrew money whenever they want to.

1. How modern form of money is different from the things used as money earlier ?

Answer : Modern form of money is not made of precious metal and neither it is of everyday use.

2. Can you refuse payment made in rupees ? Give reason for your answer.

Answer : We cannot refuse payment made in rupee in selling transactions in India as the law has legalises the use of rupee as a medium of exchange.

3. How can people hold money other than cash ?

Answer : People can hold money as deposits with bank other than cash. For this they get interest from bank.

Very Short Answer Type Questions

Question : Which segment of the society receives formal credit?

Answer : It is the richer segment of society which receives formal credit.

Question : Why do people in rural areas demand for credit?

Answer : They demand for credit for crop production.

Question : What do banks do with the money we deposit there?

Answer : Banks keep only a small proportion of their deposits as cash with themselves. They use the major portion of the deposits to extend loans.

Question : Which segment of the society depends on the formal sources?

Answer : The poor have to depend on the formal sources.

Question : What is the major source of revenue for the commercial banks?

Answer : Their major source of revenue is the difference between what is charged from borrowers and what is paid to depositors.

Question. What kind of economy is suitable for barter system?

Answer : Backward economy.

Question. Highlight the inherent problem in double coincidence of wants.

Answer : The inherent problem in double coincidence of wants is that both parties must agree to sell and buy each other’s commodities.

Question. Who issues currency in India?

Answer : The Reserve Bank of India.

Question. What are the two benefits of banks ?

Answer : (i) Banks accept deposits, i.e., surplus funds from the depositors.

(ii) Banks play an important role in economic development.

Question. What are the modern forms of money — currency and deposits associated with ?

Answer : Modern banking system.

Question. Why one cannot refuse a payment made in rupees in India ?

Answer : One cannot refuse a payment made in rupees in India because rupees is officially accepted as medium of exchange. The currency is authorised by the government of the country.

Question. How does money remove the difficulty of the double coincidence of wants ?

Answer : Money has removed the problem of double coincidence of wants by breaking a single exchange transaction for specific goods into two transactions of buying and selling by involving a medium of general acceptability, i.e., money. Everyone involved in a transaction may buy the good of his requirement from anybody who has got that thing. Now they don’t have to look for a person who desires to sell exactly what the other wishes to buy.

Question. What is demand deposit ?

Answer : Demand deposits are the deposits with the bank which are withdrawable by cheque. Since such deposits can be withdrawn by cheque on demand, that is why they are called demand deposits.

Question. Define Cheque.

Answer : A cheque is a credit instrument through which the depositor instructs the bank to pay a specific amount from the depositor’s account to the person in whose name the cheque has been issued.

Question. What is money ?

Answer : Money is anything which is generally acceptable as a medium of exchange.

Question. What are the functions of a bank ?

Answer : To accept deposit and providing loan.

Question. How does money remove the difficulty of the double coincidence of wants ?

Answer : Money has removed the problem of double coincidence of wants by breaking a single exchange transaction for specific goods into two transactions of buying and selling by involving a medium of general acceptability, i.e., money. Everyone involved in a transaction may buy the good of his requirement from anybody who has got that thing. Now they don’t have to look for a person who desires to sell exactly what the other wishes to buy.

Question. What is credit ?

Answer : Credit or loan refers to an agreement between a lender and a borrower in which the lender provides the borrower money, goods or services to be paid back by the borrower in the future.

Question. What is the full form of SHG?

Answer : Self Help Group.

Question. What is the main purpose of credit in rural areas ?

Answer : In rural areas, the main demand for credit is for crop production. Crop production involves expenses on seeds, fertilisers, pesticides, water, electricity, repair of equipment, etc.

Question. The main functions of money in an economic system facilitate.

Answer : The exchange of goods and Services

Question. Explain the main difficulty of Barter System.

Answer : The double coincidence of wants

Question. What in your opinion is the way to break the debt trap ?

Answer : The debt trap can be broken with the help of credit facilities on softer terms from the formal sector like banks, cooperative societies or self help groups.

Question. What is debt trap ?

Answer : A debt trap is a situation in which a debtor has to take more debts to pay back the previously taken loans and their interest liability.

Question. What things can be used as collateral ?

Answer : Land, building, jwellery, vehicle, livestocks, deposits with banks etc. can be used as collateral.

Question. Currency is accepted as a medium of exchange because the currency is authorised by ________ .

OR

________ is an asset that the borrower owns and uses this as a guarantee to a lender until the loan is repaid.

Answer : Government.

OR

Collateral.

Question. Complete the following table :

(Formal, Informal sector)

Answer : (i) Informal sector (ii) Formal sector

Question. Who supervises the functioning of formal sources of loans?

Answer : The Reserve Bank of India.

Question. Correct the following statement and rewrite :

Collateral is an assets and uses this as a guarantee until the loan is repaid and use this, that the borrower owns.

Answer : Collateral is an assets that the borrower owns and uses this as a guarantee to a lender until the loan is repaid.

Question. What are the two benefits of cooperatives ?

Answer : (i) Cooperatives help their members to acquire credit at reasonable terms.

(ii) It save the members from the exploitation of informal sources of credit like moneylenders.

Question. Recognize the situation when both the parties in a barter economy have to agree to sell and buy each other’s commodities? What is it called?

Answer : Double coincidence of wants.

Question. Explain the main function of money.

Answer : The medium of exchange.

Question. What are the purposes a farmers’ cooperative provides loans for ?

Answer : Farmers’ Cooperative provides loans to its members for the purchase of agricultural equipment, cultivation and agricultural trade, fishery loans, construction of houses and a variety of other expenses.

Short Answer Type Questions

Question : Give the meaning and functions of money.

Answer : Meaning of money: Money may be anything chosen by common consent as a medium of exchange and measure of value.

Functions of money:

(A) Primary functions:

(a) Medium of exchange (b) Medium of value

(B) Secondary functions:

(a) Store of value (b) Standard of deferred payments (c) Transfer of value

(C) Contingent functions:

(a) Basis of credit (b) Liquidity (c) Maximum utilization of resources

(d) Guarantor of solvency (e) Distribution of National Income

Question : What monetary system does India follow?

Answer : (a) India has adopted a representative paper currency or the managed currency standard.

(b) The monetary standard is synonymous with the standard money adopted. Paper currency in India is the unlimited legal tender i.e. it is used to settle debts and make payments against all transactions.

(c) RBI (The Reserve Bank of India) issues all currency notes and coins except one rupee notes and coins which are issued by the ministry of finance.

(d) The system governing note issues the minimum reserve system viz. certain quantity of gold is kept in reserve.

Question : What is banking? Give the main features of commercial banking.

Answer : Banking is defined as the accepting of deposits for the purpose of lending or investment of deposited money by the public, repayable on demand or otherwise and withdrawal by cheque, draft order or otherwise.

Main features of commercial banks are as follows:

(i) It deals with money, it accepts deposits and advances loans.

(ii) It also deals with credit, it has the power to create credit.

(iii) It is a commercial institution, whose aim is to earn profit.

(iv) It is a unique financial institution that creates demand.

(v) It deals with the general public.

Question : What are the two categories of sources of credit? Mention four features of each.

Answer :

Question : Explain any two features each of formal sector loans and informal sector loans.

Answer : Formal Sector Loans

(i) It provides loans at a fixed rates and terms.

(ii) It gives loans not just to profit-making businesses and traders but also to small cultivators, small-scale industries to small borrowers etc.

Informal Sector Loans

(i) Rates of interest are not fixed. Moneylenders can charge whatever interest rate they choose.

(ii) There is no one to stop them from using unfair means to get their money back.

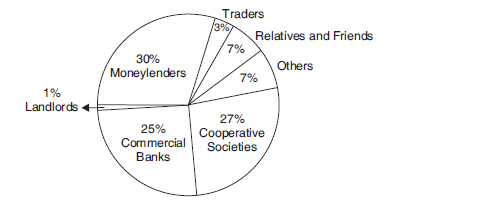

Question : Study the diagram given below and answer the following questions:

Answer : (i) Moneylenders and cooperative societies are the two major sources of credit for rural households in India.

(ii) Moneylenders are the most dominant sources of credit for rural households.

(iii) Moneylenders are the most dominant sources of credit for rural households because

(a) Rural households need not to produce certificate of their earning or documents of their employment while borrowing money from the money lenders.

(b) Neither they have to show any property or assets as collateral (security or guarantee)

Question. What are the functions of money?

Answer : • Money has solved the problem of barter system.

• Acts as medium of exchange

• Serves as a store of value.

• Serves as a measure of value.

Question. What are the advantages of depositing money in the banks?

Answer : • It is the safer place to keep money as compared to the house or a working place.

• People can earn interest on the deposited money.

• People have the provisions to withdrawn the money as and when they require.

• People can also make payment through cheques.

Question. Self Help Groups support has brought about a revolutionary change in the rural sector.

Answer : Which values according to you is it able to support.

• Women empowerment

• Team work

• Self sufficiency

• Eradication of poverty

Question. What is collateral?

Answer : • Collateral is an asset that the borrower owns (such as land, building, vehicles, livestock, deposits with banks) and uses this as a guarantee to a lender until the loan is repaid.

• If the borrower fails to repay the loan, the lender has the right to sell the asset or the collateral to obtain the payment.

• Property such as land, livestock etc are some of the common examples of collateral used for borrowing.

Question. What are the limitations of the barter system?

Answer : • Lack of double coincident

• Lack of divisibility

• Lack of measure of value.

• Problem of store of value.

Question. What do you understand by double coincidence of wants ?

Answer : Double coincidence of wants is a difficult situation involved in the barter system. Under the barter system, the transactions between two persons were executed through the mutual exchange of goods. For example, person A has got rice and wants a blanket while person B has blanket and wants rice. Both of them have the things which the other one wants. So the transaction here can take place easily. This is called double coincidence of wants, i.e., what a person desires to sell is exactly what the other wishes to buy.

Question. What happens when there is no one to supervise informal sector lending ?

Answer : This gives a kind of liberty to moneylenders to charge whatever interest rate they wish to charge, no matter how much high the rate is. Similarly, there is no one to stop them from using unfair means to get their money back.

Question. ‘‘Banks are efficient medium of exchange.’’ Support the statement with arguments.

Answer : We agree with the statement that banks are efficient medium of exchange.

(i) Demand deposits share the essential features of money.

(ii) The facility of cheque against demand deposit makes it possible to directly settle payment without use of cash.

(iii) Demand deposits are accepted widely as a medium of payment.

Question. How are deposits with the banks beneficial for individual as well as for the nation ? Explain with examples.

Answer : The deposits with banks are beneficial for individual as well as for nation :

(i) Banks accept deposit and also pay an amount as interest and in this way people earn money.

(ii) People’s money is safe with banks.

(iii) It is easy for individuals to get credit who have savings and current account in the banks.

(iv) Poor people who are engaged in production need credit.

(v) Credit provided by the banks for government projects helps in the development of the nation.

(vi) Banks provide loans for the promotion of International trade.

(vii) Development of infrastructure is undertaken with the loans provided by the banks.

Question. Why do lenders ask for ‘collateral’ while lending ? Analyse the reasons.

OR

Why do banks demand ‘collateral’ while issuing a loan ?

Answer : Lenders ask for collateral while lending to borrowers because—

(i) Lenders demand collateral (security) against loan. Collateral is an asset that the borrowers owns (such as land, building, vehicles, livestocks, deposits with Bank).

(ii) Every loan specifies an interest rate which the borrower must pay to the lender alongwith the repayment of the principal.

(iii) Lender use the collateral as a guarantee until the loan (with interest if applicable) is repaid.

(iv) If the borrower fails to repay the loan, the lender has a right to sell the asset or collateral to recover his payment.

Question. Explain any three loan activities of banks in India.

Answer : Activities of banks in India who are involved in providing loan :

(i) Banks in India these days want 15% to 20% from loan seeker to pay for their other resources and give balance money as loan on interest. For example,

if someone wants ` 1 lakh as loan for purchase of house, bank will pay around 80% of amount against hypothecation of property of equal amount.

(ii) Bank keeps a provision to pay the amount to loan seeker or depositor who might come for the money to the bank on any given day.

(iii) Bank uses the major portion of deposits to extend loan.

(iv) Difference between the interest rates, what bank pay to public for FD and what they charge from loan seeker is the main source of income of banks.

Question. Why are the poor people depend on informal sources of credit ?

Answer : Poor people depend on informal source of credit because banking facilities are not available everywhere in rural India. Even if they are available, it is much more difficult to get a loan from a bank than taking a loan from informal sources because of wide ranging difficulties. Non-availability of collateral and a guarantor also prevents the poor from getting bank loan :

Question. What are the main functions of a bank ?

Answer : Accepting deposits and providing loans are the main functions of a bank. Banks act as financial mediator or intermediaries between the savers and borrowers. Savers are the people who have surplus money which they do not require in the near future and they deposit

such money with banks. On the other hand, there are people who want credit for business requirements or meeting personal needs. Banks provide credit or loan to such people and charges interest on particular loan.

Question. In situations with high risks, credit might create further problems for the borrower. Explain.

Answer : A person takes credit or loan with the explicit or implicit understanding of returning that credit amount with interest to the lender. Sometimes it happens that the purpose for which loan has been taken by the borrower involves high risk in which the returns on the loan amount become uncertain. If the returns from the investment made out of loan amount happen to be negative then some or whole of the loan amount may be lost. If the borrower does not have any asset to compensate the lost amount then he may have to take fresh loan to expedite the loan or credit previously taken. This may lead to debt trap. Debt trap is a situation in which a person has to take new loans to pay the previously taken loans and this is a very serious problem for a person. Sometimes a person who gets into this trap and does not find ways to get out of that, may commit suicide. This has happened with various farmers and businessmen in India.

Question. “Poor households still depend on informal sources of credit.” Support the statement with examples.

Answer : Poor households even now prefer to get credit from informal sector rather than the formal sector due to the following reasons :

(i) Relatives and moneylenders are easily accessible. Still in India several rural areas do not have a bank closeby.

(ii) Norms or rules for lending out money is much strict in formal sector as compared to the informal sector.

(iii) Most poor households are still uneducated. The processes and formalities involved to get a loan sanctioned from formal sector often deter the poor to approach the bank.

Question. What are “Terms of Credit” ? Are they same for every borrower ?

Answer : Agreement regarding interest rate, collateral and documentation requirement and the mode of repayment etc. together constitute the “Terms of Credit”. The terms of credit vary substantially from borrower to borrower depending upon various factors like duration of credit, amount of credit, purpose of credit, past relationship between borrower and lender and risk involved in credit etc.

Question. “Focuses of currency have undergone several changes since early times.” Elucidate.

Answer : (i) Before the introduction of coins, a variety of objects were used as money.

(ii) For example, since the very early ages, Indians used grains and cattle as money.

(iii) Thereafter, the use of metallic coins–gold, silver, copper coins–a phase which continued well into the last century.

(iv) Modern forms of money include currency–paper notes and coins.

(v) Modern currency is not made of precious metal, it is without any use of its own.

Question. What are the prerequisites for the credit system in India to be successful for poor ?

Answer : In order to make the credit system successful in India, it is necessary that banks and cooperative societies expand their lending facilities particularly for poor people in the rural areas, so that their dependence on informal sources of credit reduces. These informal sources charge a very high interest rates from these people which left them with very little income and savings. Hence, credit must be available to this section on soft terms. Another problem which poor people face is that very few of them get the loan. Thus, it is also very necessary that everyone receives these loans so that they don’t have to depend on the informal sources.

Question. What is SHG ? What are the two benefits of SHG ?

Answer : Self Help Group is the association of poor people who pool their monetary resources for mutual monetary help in the form of soft term credit facilities to its members. Following are the two benefits of SHG:

(i) SHG helps its members to acquire credit at reasonable terms.

(ii) It saves the members from the exploitation of informal sources of credit like moneylenders.

Question. Look at a 10 rupee note. What is written on top ? Can you explain this statement ?

Answer : The top of the 10 rupee note presents the promise of the Governor of the Reserve Bank of India in these words – “I PROMISE TO PAY THE BEARER THE SUM OF TEN RUPEES.” This statement means that the RBI Governor promises to pay the value of ten rupee note in the form of other denominations of Indian currency equivalent to rupees ten. This promise of the Governor of RBI represents the legal status of the Government of India to this currency.

Question. How does the use of money make it easier to exchange things ? Given an example.

Answer : Money makes the things easier as :

(i) It is in the form of authorised paper currency which gives the guarantee of the mentioned price to the owner.

(ii) It has general acceptability.

(iii) Its price remains constant compared to other commodities.

(iv) Money can be stored easily and it doesn’t need much space.

Question. Describe the significance of the Reserve Bank of India.

Answer : The significances of the Reserve Bank of India are discussed below :

(i) It issues currency notes on behalf of the central government.

(ii) It supervises the functioning of formal source of loans. RBI monitors the banks and ensures that they maintain minimum reserves as per the guidelines of Central Bank.

(iii) It also sees that banks give loans not just for profit making to traders but also to small borrowers, small cultivators etc.

(iv) Periodically banks have to submit information to RBI on how much they are lending, to whom, at what interest rate, etc.

(v) When commerical bank fails to get financial accommodation from any where, it approaches Central Bank as a last resort. Central Bank

advances loan to such banks against approved securities. It ensure that the the banking system of the country does not suffer from any setback and

money market remains stable.

(vi) It acts as a banker to the government and is the custodian of the foreign exchange reserves of the economy.

Question. How do banks mediate between those who have surplus money and those who need money?

Answer : Banks act as financial mediator or intermediaries between the saver and borrowers. Savers are the people who have surplus money which they do not require in the near future. They deposit such money by opening an account in the bank. Banks give interest on such deposits. On the other hand there are people who want credit for business requirements or meeting their personal needs. Banks provide credit or loan to such people and charge interest on that. The banks charge a bit higher rate of interest on loans and pay a bit lower rate of interest on deposits. This difference between rates of interest become source of income for the banks.

Long Answer Type Questions :

Question. Distinguish between formal and informal credit sources.

Answer : Formal Sector

• These resources work under the supervision of the Reserve Bank of India (RBI).

• The rate of interest is very low.

• Commercial banks, cooperative societies etc. are the main sources of formal credit.

Informal Sector

• These do not work under any government organization.

• The rate of interest is very high.

• Relatives, money lenders and landlords are the main sources of informal credit.

Question. Why is barter system not suitable for a modern economy ? What are the merits of money ?

Answer : Barter system is the system of transaction between two persons which is executed through the mutual exchange of goods. For example, person A has got rice and wants a blanket while person B has blanket and wants rice. Both of them have the things which the other one wants. So the transaction here can take place easily. Such kind of system is suitable for an economy where people have very limited wants, there are few goods and people live in vicinity of each other. Such kind of economy is normally a backward economy. But in modern economy, people’s wants are numerous and innumerable goods and services are produced. Rather, the share of services is much higher in comparison of goods. In such an economy barter system cannot function. The problem of double coincidence of wants will become so complex that it will convert the modern economy into a backward economy. Money has solved this problem of double coincidence of wants. The various merits of money are following :

(i) It has made the buying and selling of goods easier.

(ii) It has removed the problem of double coincidence of wants inherent in barter system.

(iii) It has helped in the expansion of economy.

(iv) It has general acceptability because of legal sanction provided by the government.

(v) It has helped in the production of multiplicity of goods.

(vi) It has removed the problem of limited choice for consumer.

(vii) It has removed the compulsion from the people to accept whatever is available in exchange for goods.

(viii) It has helped in the determination of price of goods and the calculation of national income.

Question. Why is it necessary for the banks and cooperative societies to increase their lending facilities in rural areas ? Explain.

Answer : In the rural areas, people are often found to borrow from moneylenders which comprise the unorganised sector. This usually has higher cost of borrowing which means a larger part of the earnings of the borrowers is used to repay the loan. Hence, borrowers have less income left for themselves. This could lead to increasing debt. Thus, it is necessary that banks and cooperatives increase their lending particularly in the rural areas, so that the dependence on informal sources of credit reduces.

Borrowing from the organised sector like banks and co-operatives would lead to higher incomes and many people could then borrow cheaply for a variety of needs They could grow crops, do business, set up small-scale industries etc. They could set up new industries or trade in goods. Cheap and affordable credit is crucial for the country’s development. Thus, the formal sector loans need to expand, it is also necessary that everyone receives these loans :

Question. Analyse the role of credit for development.

OR

‘Credit has its own unique role for development’, justify the statement with argument.

OR

What is credit ? How does credit play a vital and positive role ? Explain with an example.

OR

Describe the vital and positive role of credit with example.

Answer : The credit facility is a boon for a country’s development. It

represents the expanded purchasing power in the hands of the borrowers to meet their various requirements. It is the sacrifice of the savers which help the borrowers to expand their production and income of the country. It helps in generating those productive resources which could not have been generated in the absence of purchasing power. We can see the practical examples of various business houses like Reliance and Tata who with the help of credit established big business houses and generated large employment. Similar examples may be seen all around us where the people have taken

loans to start various businesses, building homes and gaining education etc. All these have contributed a lot in the development of the country and raising the standard of living of the borrowers. But credit helps a borrower only when the terms of credit are reasonable.

Unfortunately, these terms of credit are not very much favourable in the informal sources of credit which lead to the exploitation of borrower which may be harmful for the development. Hence, it is for this reason that the formal sources of lending like banks and cooperatives must expand so that the positive contributions of credit may lead to overall development.

Question. Manav needs a loan to set up a small business. On what basis will Manav decide whether to borrow from the bank or the moneylender ? Discuss.

Answer : In order to decide whether to take loan from a bank or moneylender, Manav has to give attention to the following factors :

(i) Availability of banks in the area : Only when banks are available in the area, Manav can take loan from it. Otherwise he will have to resort to a moneylender.

(ii) Availability of necessary documents and collateral : If Manav has got necessary documents and collateral, only then he can take loan from the bank. Otherwise he will have to go to moneylender. Moneylenders may sometimes lend without collateral and documents if they know the borrower personally.

(iii) Rate of Interest : If Manav does not want to pay higher rate of interest then he will have to take loan from the bank because the moneylenders charge very high rate of interest.

(iv) Other terms and conditions : Other terms and conditions like time of loan, mode of repayment etc. are some other factors which he may have to consider before taking loans because banks may not be very flexible in terms and conditions while moneylenders may be.

Question. In India, about 80 per cent of farmers are small farmers, who need credit for cultivation.

(i) Why might banks be unwilling to lend to small farmers ?

(ii) What are the other sources from which the small farmers can borrow ?

(iii) Explain with an example how the terms of credit can be unfavourable for the small farmer.

(iv) Suggest some ways by which small farmers can get cheap credit.

Answer : (i) Banks need proper documentation and reasonable collateral to provide any kind of loan. Small farmers many not have necessary documentation and reasonable collateral because his collateral may already have been mortgaged or he may be a tenant on the land or may be very poor. In all these situations his chances of getting loans from the bank are very less.

(ii) The other sources through which the farmers can take loan from are the cooperative society, moneylenders, agricultural traders and self help groups etc.

(iii) Suppose, Gopal is a farmer who wants loan from a local moneylender for the purpose of crop production. Now the moneylender extends him loan on 5 % rate of interest per month on cumulative basis. As collateral the moneylender keeps the papers of his land. Another condition the moneylender puts before him is that after this crop season, Gopal will be allowed to use his land only when he repays the whole loan or repays loan by selling his land or does “Begar” for the money lender till he repays the entire loan.

(iv) Small farmers can get cheap credit from banks, cooperative societies or self help groups.

Question. What are the merits and demerits of credit ?

OR

‘‘Credit is useful as well as harmful, it depends on the risk involved.’’ Support the statement with examples.

Answer : Credit is a facility in which a lender extends a loan to a borrower to fulfill his needs with a promise from the borrower to return the borrowed money to the lender with predetermined interest. Such credit may be in terms of money as well as goods and services. The credit facility has following merits and demerits :

Merits :

(i) It provides much needed purchasing power to the borrower which he lacks.

(ii) It helps the borrower to mobilise the productive resources.

(iii) It helps to increase the production of the borrower and the country.

(iv) It helps to raise the income and standard of living of the borrower.

(v) It helps the lender to earn income in the form of interest.

(vi) It helps to utilise surplus money of lender which is not in immediate use.

Demerits :

(i) It puts a burden of payment of excess amount on the borrower. The excess amount refers to the sum of principal and interest.

(ii) It puts the borrower in stress of losing an asset or reputation if he fails to return the borrowed money on time.

(iii) If the borrower looses the loan amount and is not supported by the financial or asset backup, he may fall into the debt trap.

(iv) If the terms of credit are unfavourable, the borrower may face difficulties in carrying on with the credit.

Question. ‘‘The credit activites of the informal sector should be discouraged.’’ Support the statement with arguments.

Answer : The credit activities of the informal sector should be discouraged because

(i) 85% of loans taken by the poor households in the urban areas are from informal sources.

(ii) Informal lenders charge very high interest on their loans :

(iii) There are no boundaries and restrictions.

(iv) Higher cost of borrowing means a larger part of the earnings of the borrowers is used to repay the loan.

(v) In certain cases, the high interest rate for borrowing can mean that the amount to be repaid is greater than the income of the borrower.

(vi) This could lead to increasing debt and debt trap, therefore the credit activities of the informal sector should be discouraged.

Question. How can the formal sector loans be made beneficial for poor farmers and workers ? Suggest any five measures.

Answer : People obtained loans from various sources :

The various sources of loans is categorised into :

(i) Formal sector loan

(ii) Informal sector loan The formal sector loans are given by banks and cooperatives. Poor people and workers get much of their loans from the informal sectors, which is not only exploitative but also charges very high interest rate. These make the poor people and worker to fall back in poverty. The informal lenders include money- lenders, traders, employers, relatives, friends etc. The measures to make formal sector loan beneficial for poor farmers and workers are :

(i) The formal sector like banks and cooperatives should lend more to poor people and worker, particularly in rural areas.

(ii) The formal sector should provide cheap and affordable credit.

(iii) The formal sector should ensure that every one receives loan :

(iv) Providing self help group bank linkage.

(v) There should be more number of cooperatives and banks in rural areas.

Question. In what ways does the Reserve Bank of India supervise the functioning of banks ? Why is this necessary ?

OR

How does Reserve Bank of India play crucial role in controlling the formal sector loans.

Answer : Reserve Bank of India (RBI) supervises the functioning of the banks in the following manner :

(i) First of all RBI determines the necessary reserve ratios for the banks such as Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) to be maintained by them. The reserves are maintained by the banks to deal with the liquidity crunch if that may ever arise. These reserves are calculated on the basis of the deposits with the banks.

(ii) The banks have to periodically submit reports with RBI regarding the credit portfolio. They have to ensure that they do not breach any of the instructions given by RBI on the management of credit portfolio. This helps the RBI to contain any risk situations that may emerge due the lending practices of the banks.

(iii) RBI also ensures that the banks are not being partial in providing loans : It means that RBI ensures that the banks are lending not only to the big businessmens or companies but also taking care of the weaker sections of the society like small farmers and agricultural labourers in rural areas and small businessmen, labourers, small artisans etc. in urban areas. Lending to such weaker sections may be included in priority sector lending of the banks.

(iv) The RBI may supervise the expansion pattern of the banks in order to ensure that the banks are not only opening their branches in urban areas only but also expanding their facilities in rural and remote areas like hilly areas of the country.

Question. What steps do you think are necessary for banks to extend credit facilities to the poor sections of the society ?

Answer : Following steps are necessary for the expansion of credit facilities to the poor sections of the society :

(i) The banking facilities must be expanded to every corner of the country whether urban or rural, so that the banking facilities can cover all the families.

(ii) An awareness campaign must be run continuously so that the poor sections can become aware of the banking facilities.

(iii) Poor sections must be encouraged to open bank accounts and deposit money no matter how small that may be. This will develop a kind of banking habit among them. For this purpose, a bit higher interest rate may be offered to them.

(iv) Credit facility with softer terms must be designed for the poor sections.

(v) Process of credit must be made simpler for them.

(vi) Banks must provide as much as possible loans to cooperatives and self-help groups.

(vii) RBI must take steps to regularise the practices of informal sector.

Question. What is money ? What are the modern forms of money ? How has it removed the difficulties of barter system ?

OR

‘‘Money has made transactions easy.’’ Justify.

Answer : Money is anything which is generally acceptable as a medium of exchange. Money acts as an intermediary in the exchange process that is why it is called a medium of exchange. Currency (paper notes and coins) and demand deposits withdrawable by cheques are modern

forms of money. Money has removed the problem of double coincidence of wants involved in the barter system. Under the barter system, the transactions between two persons were executed through the mutual exchange of goods. For example, person A has got rice and wants a blanket while person B has blanket and wants rice. Both of them have the things which the other one wants. So the transaction here can take place easily. The situation becomes difficult when one of them wants something which the other one does not have. For example, person B has got blanket

but he wants milk instead of rice. Now he will have to search for a third person who has milk and wants rice. This becomes highly difficult. Money has made this situation easier by breaking a single exchange transaction for specific goods into two transactions of buying and selling by involving a medium of general acceptability, i.e., money. For example, person A may buy blanket from person B by giving him money while person B may buy milk from someone else who may or may not want rice by paying him that money any time. So the transactions become easier for everyone who does not have to care for mutual wants of goods.

Question. Write a note on the “Cooperative”.

Answer : Cooperative or the cooperative society is an organisation of persons which is based on the principle of mutual cooperation. The concept of cooperation refers to the superiority or unity of weaker sections or consumers over the exploitative powers of the lenders, traders or middlemen. It is generally an organisation of people from the same profession and not necessarily formed by poor people only. These are generally the registered bodies. The agriculturists and labourers may form such cooperative society for their welfare. The objective of such cooperative society may be to :

(i) Promote a sense of security among its members.

(ii) Stop the exploitation of the members from the exploitative practices of informal sector loans.

(iii) Provide a formal source of credit to its members.

(iv) Make available credit on favourable terms to its members. The capital of the cooperative society is generated by the contribution by members in the form of deposits. With these deposits as collateral, the cooperative can obtain a loan from the bank. These funds can be used to provide loans to members. Once these loans are repaid, another round of lending can take place. These loans can be provided to its members for the purchase of equipment, crop production, construction of houses etc.

Question. Why do you think that richer sections of the society has better access to formal sector loans while poor sections do not have ?

Answer : The richer sections of the society, whether urban or rural have better access to the formal sources of credit due to the following reasons :

(i) The richer sections of the society are comparatively better educated and they can understand very well the formal procedures of getting credit from the formal sources of credit. Poor people lack such understanding.

(ii) The richer sections of the society have proper documents, guarantees or collateral which they can offer to the bank or any other institution. Poor sections generally lack all such things.

(iii) The richer sections of the society have better repayment capacity. So their chances of back tracking on the repayment are lesser. In the case of poor sections such chances of failure of repayments may be higher.

(iv) The richer sections of society have regular interactions with the formal sector institutions interms of deposits and withdrawals. Such kind of interaction increases the trust of the formal sector in richer sections of the society. Poor sections of society lack such interaction and hence the trust too.

Question. What are Self Help Groups ? How do they work ? Explain.

Answer : Self Help Groups are the organisations of the rural poor, people of same socio-economic background to pool their savings and provide loans to their members.

Work of self-help groups :

(i) Generally self help groups consist of 15 – 20 members.

(ii) Members belong to one neighbourhood.

(iii) They meet regularly.