Download the latest CBSE Class 12 Accountancy Retirement Or Death Of A Partner Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner

To secure a higher rank, students should use these Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner Revision Notes for Class 12 Accountancy

CBSE Class 12 Retirement or Death of a Partner. Learning the important concepts is very important for every student to get better marks in examinations. The concepts should be clear which will help in faster learning. The attached concepts made as per NCERT and CBSE pattern will help the student to understand the chapter and score better marks in the examinations.

CHAPTER 5

Retirement/Death of a Partner

Introduction

Like admission and change in profit sharing ratio, in case of retirement or death also the existing partnership deed comes to an end and the new one comes into existence among the remaining partners. There is not much difference in the accounting treatment at the time of retirement or in the event of death.

Amount due to retiring deceased Partner

(To be credited to his capital account)

1. Credit Balance of his capital.

2. Credit Balance of his current account (if any)

3. Share of Goodwill.

4. Share of Reserves or Undistributed profits.

5. His share in the profit revaluation of assets and liabilities.

6. Share in profits upto the date of Retirement/Death.

7. Interest on capital if involved.

8. Salary if any

Deduction from the above sum (to be debited to the capital account)

1. Debit balance of his current account (if any)

2. Share of Goodwill to be written off.

3. Share of Accumulated loss.

4. Drawings and interest on drawings (if any)

5. Share of loss on account of Revaluation of assets and liabilities.

6. His share of business loss.

Accounting Treatement

1. Calculation of new profit sharing ration and gaining ratio

2. Treatment of goodwill.

3. Revaluation a/c preparation with the adjustment in the respect of unrecorded assets/ liabilities.

4. Distribution of reserves and accumulated profits/loss.

5. Ascertainment of share of profits/loss till the date of retirement/death.

6. Adjustment of capital if required

7. Settlement of the Accounts due to Retired/Deceased partner.

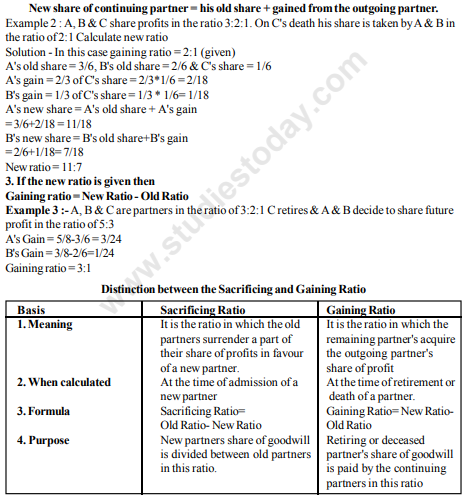

New Profit Sharing Ratio & Gaining Ratio

New Profit Sharing Ratio It is the ratio in which the remaining partners will share further profits after retirement/death.

Gaining ratio It is the ratio in which the continuing partners have acquired the share from the outgoing partner Calulation of the two ratios Following situations may arise.

1. When no information about new ratio or gaining ratio is given in the question In this case it is considered that the share of the retiring partner is acquired by the remaining partners in the old ratio. Then no need to calculate the new ratio/gaining ratio as it will be the same as before.

Example 1 :A

Band C are partners sharing profit and loss in the ratio of 3:2:1 then on retirement of the gaining ratio/new ratio will be

A2: 1

B3: 1

C3: 2

2. Gaining ratio is given which is different than the old ratio In this case

Treatment of Goodwill

According to accounting standard 10, Goodwill account can't be raised. Therefore only adjustment entry is done for goodwill.

Steps to be followed :

1. When old goodwill appears in the books then first of all this is written off in the old ratio. Remember Old Goodwill Old Ratio

All Partners' capital A/c Dr

To Good will A/c

2. After writing off old goodwill adjustment of retiring partner's share of goodwill will be made through the following journal entry.

Remaining Partner's Cap A/c Dr (in gaining ratio)

To Retiring/Deceased Partner's Cap A/c

Example 4 : M, N & P are partners in a firm. P retires & the goodwill of the firm is valued at Rs.30000. M & N decide to share future profits in the ratio of 3:2. Pass necessary adjustment entries.

1 If goodwill A/c already appears in teh books at Rs.18000

2. When no goodwill A/c appears in the books.

Solution : Old ratio of M, N & P = 1:1:1 (since profit sharing ratio is not given it is treated as equal) New ratio= 3:2

M's gain = 3/51/3= 4/15

N's gain = 2/51/3= 1/15

Gaining ratio = 4:1

P's shareof goodwill = 30,000*1/3 = 10,000

Case 1.

1. Old goodwill will be written off in the old ratio i.e. 1:1:1

M's Capital A/c Dr 6000

N's Capital A/c Dr. 6000

P's Capital A/c Dr 6000

To Goodwill A/c 18000

2. Adjustment entry will be done in gaining ratio

M's Capital A/c Dr.8000

N's Capital A/c Dr.2000

To P's Capital A/c 10,000

Case 2. When No goodwill already appears in the books then only second entry will be done. Hidden goodwill

Sometimes goodwill is not given in the question directly. But if a firm agrees to pay a sum which

is more than his balance in capital a/c after making all adjustment with respect to reserves, revaluation of assets and liabilities etc. then excess amount is treated as his share of goodwill (known as hidden goodwill)

EXAMPLE 5 : Let R, S & T are partners in a firm sharing profit & loss in the ratio of 2:2:1. T Retires and his balance in capital a/c after adjustment for reserve & revaluation of assets & liabilities comes out to be Rs.50000. R & S agree to pay him Rs.60000. Give journal entry for the adjustmnet of goodwill.

Solution

New ratio between R & S = gaining ratio = 2:2 or 1:1

T's share of goodwill (hidden) = Rs.6000050000=10000

Hence adjustment entry is

R's capital a/c Dr 5000

S's capital a/c Dr 5000

To T's capital a/c 10000

(T's share of goodwill adjusted in gaining ratio i.e. 1:1)

3. Revaluation of Assets and Reassessment Liabilities

Revaluation A/c is prepared in the same way as in the case of admission of a new partner. Profit and loss on revaluation is transferred among all the partners in old ratio.

4. Adjustment of Reserves and Surplus

(Profits) (Appearing in the Balance Sheet Liability Side)

(a) General Reseve A/c Dr.

Reserve Fund A/c Dr.

P& LA/c (Credit Balance) Dr.

To all partners Capital/Current A/c in old ratio.

Example 6 : X, Y and Z are partners in a firm sharing profits and losses in the ratio of 2:1:1, Y retires on 31st March, 2011. On that date, there was a balance of Rs.24,000 in general reserve and Rs.16,000 in profit and loss A/c of the firm. Give Journal entries.

Solution

General Reserve A/c Dr 24,000

P & L A/c Dr 16,000

To X's Cap A/c 20,000

To Y's Cap A/c 10,000

To Z's Cap A/c 10,000

(Reserve & Surplus amount distributed in old ratio on Y's retirement)

b) Specific Funds If the specific funds such as workmen's compensation fund or investment fluctuation fund are in excess of actual requirement, the excess will be transferred to the Capital A/c in old ratio.

Workment Compensation Fund A/c Dr

Investment Fluctuation Fund A/c Dr

To All Partner's Cap A/cs

Example 7 : P, Q and Rare partner's sharing profits and losses in the ration of 3:2:1. P retires and on that date there was workmen's compensation fund amount Rs.30,000 in the Balance Sheet. But actual liability on this account was for Rs.12,000 only on that date. Give Journal Entry.

Solution

Excess amount in Workmen's Compensation Fund = Rs.30,000Rs.12,000= Rs.18,000 (Cr)

This will be transferred to all partner's Capital A/c in old ratio

Journal Entry

1. W. Compensation Fund A/c Dr 18,000

To P's Cap A/c 9000

To Q's Cap A/c 6000

To R's Cap A/c 3000 (Excess amount in W. Comp. Fund istrfd to partner's Cap A/cs in old ratio)

c) For distributing accumulated losses

(I.e. P & L A/c debit balance shown on the Asset side of Balance Sheet

All partner's Cap/Current A/c Dr (in old ratio) To P & L A/c

Example 8 : A, B and C are equal partner's. A retires and on that date there was a debit balance of Rs.15,000 in P & LA/c. Give Journal entry. Solution

A's Cap A/c Dr 5,000

(Loss in P & L A/c written off in old ratio on A's retirement)

Solution

A's Cap A/c Dr 5,000

B's Cap A/c Dr 5,000

C's Cap A/c Dr 5,000

To P & L A/c 15,000

(Loss in P & L A/c written off in old ratio on A's retirement)

JLP means the policy taken by the firm on the lives of the partners. When any of teh partners dies the insurance company pays the whole amount which makes the payment easy to deceased partner's legal representatives in case of death.

5. Adjustmetn of Joint Life Policy (JLP)Introduction

Accounting treatment in case of retirement

Case1. . When premium paid is considered as Revenue Expenditure – In this case the premium paid is debited to P&L A/c and JLP A/c doesn’t appear in the balance sheet. In this case the Retiring partner's share in the surrender value of JLP will be debited to the remaining partners Cap A/c in

gaining ratio.

I.e. Remaining Partner’s Cap A/c Dr

To Retiring Partner’s Cap A/c

Example 9: D, E and F are partners in a firm sharing profit & losses in the ratio of

3:2:1. F retires on 31st March 2011. The firm had a JLP of Rs.80,000, the surrender value of which was Rs.18,000 on that date annual premium paid on the policy of Rs.10,000 which was debited to P&L A/c every Year. Give adjustment entry if no JLP A/c appears in the Balance Sheet.

Solution

F's share in the surrender value = 1/6*18000=Rs.3000

Gaining Ratio b/w D: E=3:2

Adjustment Entry

D's Cap A/c Dr1800

E's Cap A/c Dr1200

To F's Cap A/c 3000

(F’s share in the surrender value of JLP adjusted in gaining ratio)

Case2. . When premium paid is considered as Capital Expenditure In this case the JLP A/c will be already appearing in the Balance Sheet at surrender value. Then no further treatment is required because it means that the retiring partners share is already included in his Cap A/c.

Disposal of the Amount Due to the Retiring Partner

The outgoing partners A/c is settled as per the terms of partnership deed. Three cases maybe there as given below

When the retiring partner is paid full amount either in cash or by cheque. Retiring Partner’s Cap A/c Dr

2. When the retiring partner is paid nothing in cash then the whole amount due is trfd to his loan A/c.

Retiring Partner’s Cap A/c Dr

To retiring partner’s Loan A/c

3. When Retiring Partner is partly paid in cash and the remaining amount is treated as Loan.

Retiring Partner’s Cap A/c Dr (Total Amount due) To Cash/Bank A/c (Amount Paid) To Retiring Partner’s Loan A/c(Amount of Loan)

Settlement of Loan of the Retiring Partner

Loan of the retiring partner is disposed off according to the pre decided terms and conditions among the partners. Normally the Principal amount is paid in few equal installments. In such cases interest is credited to the Loan A/c on the basis of the amount outstanding at the beginning of each year and the amount paid is debited to loan A/c.The following Journal entries are done

a) For interest on Loan.

Interest A/c Dr

To Retiring partner’s Loan A/c

b) For the payment of installment.

Retiring Partner’s Loan A/c Dr

To Cash/ Bank A/c

Example 10: A, B, and C are partners in a firm. B retires from the firm on 1st Jan 2008. On the date of his retirement Rs.66, 000 were due to him. It was decided that the payment will be done in 3 equal yearly installments together with interest @ 10%p.a. on the unpaid balance. Prepare B’s Loan A/c.

To Cash or Bank A/c

Reconstitution Of Partnership: Retirement And Death Of A Partner

Basic Concepts

Meaning of Retirement: When a partner leaves or retires from the firm due to any reason, it is known as retirement of a partner. On retirement or death of a partner, the old partnership comes to an end and a new partnership comes into existence between the remaining partners. However the firm continues. Retirement involves a few preconditions that have been clearly laid down by Section 32(1) of the Indian Partnership Act, 1932. It states that a partner may retire:

- with the consent of all the partners

- in accordance with an express agreement amongst the partners.

- by issuing a notice in writing to all the partners stating the intention to retire (this occurs in cases where partnership is at will)

Adjustments Required: Following are the various matters that need adjustment at the time of retirement:

(i) Determination of new profit-sharing ratio.

(ii) Determination of gaining ratio.

(iii) Treatment of goodwill.

(iv) Revaluation of assets and Reassessment of liabilities.

(v) Adjustment of reserves and accumulated profits or losses.

(vi) Adjustment of capitals.

(vii) Determination of the amount payable to the retiring partner.

New Profit-sharing Ratio: The new profit-sharing ratio is the ratio in which the continuing partners will share profit. The share of each remaining partner will be the sum total of his old share of profit in the firm and the portion of the retiring partner's share of the profit acquired.

It is determined as:

New share = Old share + Acquired share

The new profit sharing ratio may be calculated as follows in the following circumstances:

Case 1: When no information is given about remaining partners' new share, new ratio will be the same as old ratio among them.

Case 2: When retiring partner's share is acquired by remaining partners in a specified ratio, the acquired share is added to their existing share to arrive at their new share in the firm.

Gaining Ratio: Gaining Ratio refers to the ratio in which the remaining partners gain the retiring or deceased partner's share of profit. It is calculated as:

Gaining Ratio = New share - Old Share

Calculation of Gaining Ratio under different cases:

Case I: No Agreement amongst Partners for New Profit-sharing Ratio

In case the partners have no express agreement, they continue to share it in their old profit-sharing ratio. Thus the gaining ratio is automatically their old profit-sharing ratio.

Case II: Agreement amongst Partners for New Profit-sharing Ratio

When there is an agreement to share the retiring partner's share amongst the remaining partners, the gaining ratio is governed by such an agreement.

Case III: Acquisition of Retiring Partner's Share only by One Partner

When the retiring partner's share is gained entirely by one partner, then only gaining partner provides for the share of goodwill of the retiring partner.

Difference between Sacrificing Ratio and Gaining Ratio

| S.No. | Basis | Sacrificing Ratio | Gaining Ratio |

|---|---|---|---|

| 1. | Definition | It is the proportion in which the old partners sacrifice their share in favour of a new partner. | It is the proportion in which the old partners acquire the outgoing (retired or deceased) partner's share. |

| 2. | Time of Calculation | Generally, it is calculated at the time of admission of a new partner. | Generally, it is calculated at the time of retirement or death of a partner. |

| 3. | Purpose | It is calculated to know how the old partners shall share the goodwill brought in by the new partner. | It is calculated to know how the remaining partners shall contribute towards the share of goodwill of the retiring partner. |

| 4. | Formula | Sacrificing Ratio = Old Share - New Share | Gaining Ratio = New Share - Old Share |

| 5. | Effect on Share of Profit of Old/Remaining Partners | The old partners' share decreases. | The remaining partners' share increases. |

| 6. | Effect on Capital Accounts | Old partners' capital accounts are credited for the share of goodwill in the sacrificing ratio. | Remaining partners' capital accounts are debited for the share of goodwill in the gaining ratio. |

Treatment of Goodwill: When a partner retires, the continuing partners gain his share of profit. They thus have to compensate the retiring partner for his share in the goodwill in the gaining ratio. Similarly when there is death of a partner, the continuing partners should bear the share of the goodwill due to the heirs of the deceased partner.

The accounting adjustments adopted to treat goodwill in the accounts depends directly on the fact whether goodwill already appears in the books or not.

Case I: When goodwill does not appear in the books of accounts

The share of goodwill of the retiring partner is credited to his capital account and continuing partners' capital accounts will be debited with share of goodwill of the retiring partner in gaining ratio.

In this case, following entry is passed:

Continuing Partners' Capital/Current A/cs Dr. (In gaining ratio)

To Retiring Partner's Capital/Current A/c

(Being goodwill adjusted in partners' capitals)

Note: If any of the remaining partners has also sacrificed a part of his share in profits of the firm on retirement or death of a partner, his capital/current account will also be credited with his proportion of sacrifice (i.e., Share of sacrifice × Firm's goodwill).

Case II: When goodwill exists in the accounting books.

When goodwill account already appears in books, write off the existing goodwill by debiting all the partners' capital accounts (in case of fluctuating capitals) or current accounts (in case of fixed capitals) in their old profit-sharing ratio and crediting the goodwill account.

All Partners' Capital/ Current A/cs Dr. (in old ratio)

To Goodwill A/c (existing value of goodwill)

(Being existing value of goodwill written off)

Later, credit the outgoing partners' capital/current account with his share of goodwill and debit the gaining partner(s) capital/current account in gaining ratio.

Remaining Partners' Capital/ Current A/cs Dr. (in gaining ratio)

To Outgoing Partner's Capital/Current A/c (goodwill share)

(Being goodwill adjusted on a partner's retirement)

Hidden Goodwill: If the firm has agreed to settle the account of retiring partner by paying him a lump-sum amount, then amount paid to him in excess of his adjusted capital shall be treated as his share of goodwill. For example A, B and C are partners. A retires, his capital account after making adjustment for reserves and profit on revaluation exists at Rs. 60,000, B and C have agreed to pay him Rs. 90,000 in full settlement of his claim. It implies that Rs. 30,000 (Rs. 90,000 - Rs. 60,000) is A's share of goodwill of the firm. This will be treated by debiting Rs. 30,000 in B and C's Capital Accounts in their gaining ratio and crediting A's Capital A/c.

Revaluation of Assets and Reassessment of Liabilities: Generally when a partner retires from a partnership firm, the assets and liabilities are revalued or adjusted on the date of retirement so that the retiring partner gets his fair share of the firm's assets. When the assets and liabilities of the firm are revalued, a Revaluation Account/Profit and Loss Adjustment Account is prepared in the same way as is prepared in the case of admission of a new partner. The only difference is that in case of retirement, any profit or loss on revaluation is divided amongst all the partners (including the retiring partner), whereas in case of admission of a new partner, the new partner does not share such profit or loss on revaluation.

Memorandum Revaluation Account: When the partners decide to give effect to revaluation of assets and reassessment of liabilities without affecting existing amounts of assets and liabilities, Memorandum Revaluation Account is prepared in the same manner as in case of admission of a partner. It should be remembered that first part of Memorandum Revaluation Account is transferred to Capital Accounts of all the partners including outgoing partner in their old profit-sharing ratio, while the second part of this account is transferred to the Capital Accounts of the continuing partners in their new profit-sharing ratio.

Treatment of Accumulated (Undistributed) Profits/Losses and Reserves: Upon retirement of a partner, if there are any undistributed profits or reserves, the same need to be divided amongst all the partners in their old profit-sharing ratio. Accumulated profits and reserves belong to all partners, hence, they should be credited to all partners' capital accounts in their old profit-sharing ratio. Alternatively, only the retiring partner's share may be transferred to his capital account if the other partners continue to share profits in their old ratio and want to still show reserves in the Balance Sheet. The following entry will be made for distributing accumulated profits or reserves.

Profit and Loss A/c (credit balance) Dr.

General Reserve A/c Dr.

Workmen Compensation Reserve A/c Dr. (Excess of Reserve over Actual Liability)

To All Partners' Capital/Current A/cs

(Being accumulated profits distributed amongst partners in their old profit-sharing ratio upon retirement of a partner.)

For distributing accumulated losses:

If there is a debit balance of Profit and Loss Account in the Balance Sheet on the date of retirement of a partner, it must be written off by all the partners in old profit-sharing ratio.

All Partners' Capital/Current A/cs Dr.

To Profit and Loss A/c (debit balance)

(Being accumulated losses distributed amongst partners in their old profit-sharing ratio upon retirement of a partner)

For distributing surplus of specific funds:

Workmen's Compensation Reserve A/c Dr. (Excess of Reserve over Actual Liability)

Investment Fluctuation Reserve A/c Dr. (Excess of Reserve over Difference between Book value and market value of Investment)

To All Partners' Capital A/cs (or Current A/cs)

(Being amounts in excess of actual requirement in specific reserves divided amongst partners in their old profit-sharing ratio upon retirement)

Final Payment to the Retiring Partner: The final amount payable to the retiring partner is determined by taking into accounts the following items:

- Opening balance of capital account and current account of the retiring partner.

- Retiring partner's share in revaluation profit.

- Retiring partner's share in reserves and accumulated profits.

- Retiring partner's share of profit till the date of retirement.

- Retiring partner's share of goodwill.

- Salary and/or interest on capital due to retiring partner.

The above mentioned items increase the amount payable to the retiring partner. The following items decrease the amount payable to the retiring partner.

- Drawings and interest on drawings.

- Retiring partner's share in the accumulated losses.

- Retiring partner's share of revaluation loss.

Methods of Payment:

Case I: Full settlement of account in one single (lumpsum) payment.

Retiring Partner's Capital A/c Dr.

To Cash/Bank A/c

(Being retiring partner's whole claim settled at the time of retirement).

Case II: Part payment of dues and balance transferred to loan account

Retiring Partner's Capital A/c Dr.

To Retiring Partner's Loan A/c

To Bank A/c

(Being retiring partner's claim partly settled through cash and the rest transferred to the loan account at the time of retirement)

Case III: Entire balance transferred to loan account and paid later in instalments.

Retiring Partner's Capital A/c Dr.

To Retiring Partner's Loan A/c

(Being retiring partner's whole claim transferred to the corresponding loan account at the time of retirement).

Note: If the question does not specify the treatment of settlement of retiring partners' account, the final payment due to him is transferred to his Loan Account.

When the loan account of a retired partner is settled through payment of instalments, the latter includes both the principal sum and interest.

For interest generated on retiring partner's loan

Interest A/c Dr.

To Retiring Partner's Loan A/c

(Being interest generated on loan transferred to the corresponding loan account of the retired partner)

Meaning Of Retirement

Question 1. What does retirement of a partner mean?

Answer: Retirement of a partner means ceasing to be a partner of the firm. A partner can retire in three ways: (i) with the consent of all the partners, (ii) by giving notice in writing to all other partners of his intention to retire, in case of partnership at will, or (iii) in accordance with the terms of agreement between the partners.

In simple words: Retirement means a partner stops being part of the business. It can happen if all partners agree, or if one partner writes to tell the others he wants to leave, or based on what the partnership agreement says.

Exam Tip: Remember the three ways a partner can retire - by consent, by notice (for partnership at will), or as per the agreement terms.

Liability Of A Partner

Question 2. What is the liability of a retiring partner for acts before retirement?

Answer: Under Section 32(2), a retiring partner stays liable for all the acts of the firm up to the date of his retirement. However, a retiring partner may be released from his liability by an agreement between himself, the third party, and the continuing partners.

In simple words: A retiring partner must pay for all the firm's actions until he leaves. But he can get out of this duty if all sides agree in writing.

Exam Tip: Distinguish between liability before and after retirement - before requires an agreement to discharge, after requires public notice.

Question 3. What is the liability of a retiring partner for acts after retirement?

Answer: Under Section 32(3), a retiring partner continues to be liable to third parties for the acts of the firm even after his retirement. This liability continues until a public notice of his retirement is given.

In simple words: Even after leaving, a retiring partner can still be held responsible for the firm's actions until the firm tells the public he has left.

Exam Tip: Public notice is key - without it, outsiders won't know the partner has left, so they can still hold him responsible.

Question 4. What are the various matters that need accounting adjustment at the time of retirement?

Answer: The various matters requiring accounting adjustment at retirement are: (i) Determination of new profit sharing ratio, (ii) Determination of gaining ratio, (iii) Treatment of goodwill, (iv) Revaluation of assets and liabilities, (v) Adjustment of accumulated profits and losses, (vi) Adjustment of capital, and (vii) Determination of the amount payable to the retiring partner.

In simple words: When a partner leaves, the firm must figure out the new profit split, how much goodwill to pay, revalue the assets, handle old profits and losses, fix each partner's capital, and calculate what the leaving partner gets.

Exam Tip: All seven adjustments must be addressed in order - this is the standard sequence followed in retirement questions.

New Profit Sharing Ratio

Question 5. What is the new profit sharing ratio?

Answer: The new profit sharing ratio is the ratio in which the continuing partners will share profits and losses after a partner retires. It is calculated by adding the old ratio of each continuing partner to the ratio in which the outgoing partner's share of profit is gained by that partner. The formula is: New Ratio = Old Ratio + Gaining Ratio.

In simple words: After a partner leaves, the remaining partners get a new split of profits. Each continuing partner's new share equals what they had before plus what they get from the retiring partner.

Exam Tip: Always remember the formula New Ratio = Old Ratio + Gaining Ratio when calculating new profit shares.

Gaining Ratio

Question 6. What is the gaining ratio?

Answer: The gaining ratio is the ratio in which the remaining or continuing partners have taken over the share from the retiring partner. It shows how much each continuing partner gains from the retiring partner's share. The formula is: Gaining Ratio = New Ratio - Old Ratio.

In simple words: The gaining ratio shows how much extra profit each staying partner picks up from the partner who leaves. It is found by subtracting each partner's old share from their new share.

Exam Tip: The gaining ratio is always calculated only for continuing partners, never for the retiring partner.

Difference Between Sacrificing Ratio And Gaining Ratio

| Basis | Sacrificing Ratio | Gaining Ratio |

|---|---|---|

| Meaning | The portion of profits or losses given up by the existing partner in favor of a new partner. | The portion of profits or losses gained by the remaining partners on leave of retired or died partner. |

| Why should we calculate | To find the ratio of profits or losses given up by the existing partner on account of a new partner. | To find the ratio of profits or losses gained by the remaining partners on account of retirement or death of the old partner. |

| When to be calculated | At the time of Admission of new partners. | At the time retirement or death of partners. |

| How to calculate | SR = Old ratio - New ratio. | GR = New ratio - Old ratio. |

| Its effect on respective partners. | The profit-sharing ratio of the existing partners is reduced. | The profit-sharing ratio of the existing partners is increased. |

Treatment Of Goodwill

Question 7. What is the treatment of goodwill when a partner retires?

Answer: Goodwill is a form of payment given to an outgoing partner and is paid by the remaining partners in their gaining ratio. The adjustment for the retiring partner's share of goodwill is made through the journal entry: Gaining Partners' Capital A/c Dr [Continuing partners in gaining ratio] To Sacrificing Partner's Capital A/c [Retiring partner]. If goodwill already shows in the old balance sheet, it must be written off in the old ratio using the entry: All Partners' Capital/Current A/c Dr To Goodwill A/c.

In simple words: Goodwill is extra money paid to the retiring partner. The staying partners pay it based on how much they gain. If the old balance sheet had goodwill listed, that old goodwill must be removed first.

Exam Tip: Remember two scenarios - when goodwill is new (paid to retiring partner) and when old goodwill exists (must be written off first).

Question 8. How is goodwill written off if it already appears in the old balance sheet?

Answer: If goodwill already shows in the old balance sheet, it must be written off in the old profit sharing ratio. The journal entry used is: All Partners' Capital/Current A/c Dr To Goodwill A/c. This removes the existing goodwill from the books at the time of retirement and clears it from all partners' accounts based on their old ratio.

In simple words: Old goodwill that was on the books gets removed and charged to all partners based on their old profit share. This clears the goodwill account completely.

Exam Tip: Always write off old goodwill BEFORE calculating the new goodwill payment to the retiring partner.

Revaluation Of Assets And Reassessment Of Liabilities

Question 9. How are assets and liabilities treated when a partner retires?

Answer: Revaluation of assets and reassessment of liabilities are done in the same way as in the case of admission of a new partner. Assets are valued at their current market value and liabilities are adjusted to their current fair value. Any gains or losses from revaluation are shared among all partners (including the retiring partner) in their old profit sharing ratio.

In simple words: At retirement, assets and liabilities are updated to show what they are worth now. Any profit or loss from this update is split among all partners based on their old profit share.

Exam Tip: Revaluation gains and losses are credited or debited to all partners' capital accounts in their old ratio.

Question 10. How are reserves and accumulated profits handled at retirement?

Answer: Adjustment for reserves and accumulated profits or losses is done in the same way as in the case of admission of a partner. All reserves and accumulated profits are shared among all partners (including the retiring partner) in their old profit sharing ratio. The retiring partner gets his share of reserves and accumulated profits as part of the settlement amount.

In simple words: Any money saved up (reserves) or old profits and losses that the firm kept are split among all partners based on their old profit share. The retiring partner receives his portion as part of his final payment.

Exam Tip: Reserves and accumulated profits are always divided in the OLD ratio among all partners, not the new ratio.

Settlement Of Amount Due To Retiring Partner

Question 11. What items are credited to the retiring partner's capital account?

Answer: The following items are credited to the retiring partner's capital account: (i) Opening balance of capital and current account of retiring partner, (ii) His share in the profit of the revaluation account, (iii) His share of reserve and accumulated profit, (iv) His share of goodwill of the firm, (v) His share of profit till the date of his retirement, and (vi) His salary and/or interest on capital due to him till the date of his retirement.

In simple words: The retiring partner gets credit for what he started with, his share of new asset values, old savings, goodwill, profit up to his last day, and any salary or interest owed to him.

Exam Tip: All six credit items must be carefully identified from the question data and added to calculate the total due.

Question 12. What items are debited to the retiring partner's capital account?

Answer: The following items are debited to the retiring partner's capital account: (i) Drawings and interest thereon, (ii) Share in the accumulated losses of past year/years, and (iii) Share in the loss of revaluation account. These items reduce the amount owed to the retiring partner.

In simple words: The retiring partner loses money from his final payment for money he took out (drawings), his share of old losses, and his share of any loss when assets were revalued down.

Exam Tip: Debits reduce the net amount payable - keep them separate from the credit items for clarity.

Question 13. What are the two ways to settle the amount due to the retiring partner?

Answer: The amount due to the retiring partner can be settled in two ways: (i) The amount is paid off immediately in full through cash or bank, or (ii) The amount is not paid immediately and is transferred to the retiring partner's loan account. If transferred to a loan account, it shows as a liability in the new firm's books until it is paid off completely. Interest may be provided on the loan, and payments are made in installments.

In simple words: The firm can pay the retiring partner all at once in cash, or it can give him an IOU (loan account) and pay him over time with interest.

Exam Tip: When the amount is transferred to a loan account, it becomes a liability and interest accrues until fully paid.

Question 14. What journal entry is passed if the retiring partner's amount is paid immediately?

Answer: If the amount due to the retiring partner is paid off immediately, the following journal entry is passed:

Retiring Partner's Capital A/c Dr

To Cash/Bank A/c

This entry shows that the retiring partner's capital account is closed and the cash or bank account is reduced by the amount paid out.

In simple words: The firm removes what it owes the retiring partner from his capital account and pays it out in cash or from the bank right away.

Exam Tip: This is a straightforward two-part entry - one debit and one credit, nothing more.

Question 15. What journal entries are passed if the retiring partner's amount is transferred to a loan account?

Answer: The following journal entries are passed if the amount is transferred to a loan account:

(a) For amount due, transferred to retiring partner's loan account:

Retiring Partner's Capital A/c Dr

To Retiring Partner's Loan A/c

(b) On interest being provided:

Interest on Loan A/c Dr

To Retiring Partner's Loan A/c

(c) On payment of installment with interest:

Retiring Partner's Loan A/c Dr

To Cash/Bank A/c

These entries show the transfer of the amount to a loan account, the accrual of interest, and the eventual payment of installments.

In simple words: First, the firm changes the retiring partner's capital into a loan he owes. Then interest builds up on that loan. Finally, when he gets paid, the loan goes down and cash goes out.

Exam Tip: Remember the three stages - transfer to loan, add interest, and payment - each with its own journal entry.

Question 16. What journal entry is passed if the retiring partner's amount is partly paid in cash and the remainder is treated as a loan?

Answer: If the amount is partly paid in cash and the remaining amount is treated as a loan, the following journal entry is passed:

Retiring Partner's Capital A/c Dr

To Cash/Bank A/c

To Retiring Partner's Loan A/c

This is a compound entry where the capital account is debited and split into two parts - one credited to cash/bank for the immediate payment and one credited to the loan account for the deferred amount.

In simple words: The firm pays part of what it owes right away in cash and sets up a loan for the rest that will be paid later.

Exam Tip: This is a three-part entry - one debit on the left and two credits on the right splitting the total amount.

Adjustment Of Capital

Question 17. When is capital adjustment required at the time of retirement?

Answer: Capital adjustment may be required at retirement when the continuing partners decide to adjust their capital contributions in their new profit sharing ratio. This ensures that each partner's capital is proportionate to his new share of profits. Capital adjustment is optional and depends on the partnership agreement or the partners' decision.

In simple words: After a partner leaves, the staying partners might want their capital amounts to match their new profit shares. This keeps everything fair and balanced.

Exam Tip: Capital adjustment is not mandatory - it only happens if the partnership agreement requires it or the partners choose to do it.

Question 18. What are the three cases for adjusting capital of continuing partners?

Answer: The three cases for adjusting the capital of continuing partners are: (i) Case I - When the total capital of the new firm is given, (ii) Case II - When the total capital of the new firm is not given, and (iii) Case III - When the outgoing partner is to be paid through cash brought by the continuing partners in such a way as to make their capitals proportionate to their new profit sharing ratio. Each case uses different steps to calculate and adjust the capital.

In simple words: Capital adjustment can happen three ways - when you know what the total capital should be, when you don't know the total, or when staying partners bring cash to pay the retiring partner and fix their capital ratio at the same time.

Exam Tip: Identify which case applies based on the information given in the question before attempting the calculation.

Question 19. What are the steps involved in Case I of capital adjustment?

Answer: The steps involved in Case I (when the total capital of the new firm is given) are: Step 1 - Calculate the adjusted old capitals of continuing partners (after all other adjustments). Step 2 - Calculate the new capitals of continuing partners based on the given total and their new profit sharing ratio. Step 3 - Calculate the surplus or deficit capital by comparing the new capital with the adjusted old capital. If there is a surplus, the partner brings in cash; if there is a deficit, cash is returned to the partner.

In simple words: First, fix what each partner's capital is now after all changes. Then, work out what it should be based on the new profit split. Finally, see if each partner needs to add money or take money out.

Exam Tip: Always compare Step 2 (new capital) with Step 1 (adjusted old capital) to find the surplus or deficit.

Question 20. What are the steps involved in Case II of capital adjustment?

Answer: The steps involved in Case II (when the total capital of the new firm is not given) are: Step 1 - Calculate the adjusted old capitals of continuing partners after all other adjustments. Step 2 - Calculate the total capital of the new firm by adding up the adjusted old capitals of all continuing partners. Step 3 - Calculate the new capitals of continuing partners based on the calculated total and their new profit sharing ratio. Step 4 - Calculate the surplus or deficit capital by comparing the new capital with the adjusted old capital.

In simple words: First, work out each staying partner's capital now. Add them up to get the total for the new firm. Then divide that total based on the new profit shares. Finally, see who needs to pay or get money back.

Exam Tip: The total capital in Case II is derived from the adjusted old capitals - it is not given like in Case I.

Question 21. What are the steps involved in Case III of capital adjustment?

Answer: The steps involved in Case III (when the outgoing partner is paid through cash brought by continuing partners) are: Step 1 - Calculate the adjusted old capitals of continuing partners after all other adjustments. Step 2 - Calculate the total capital of the new firm. Step 3 - Calculate the new capitals of continuing partners based on the new profit sharing ratio. Step 4 - Calculate the surplus or deficit by comparing the new capital with the adjusted old capital. The continuing partners bring in cash as a surplus to pay the retiring partner, or withdraw cash if there is a deficit.

In simple words: First, work out current capital. Find the total for the new firm. Work out what each partner should have based on new profit shares. Then staying partners add or pull out the difference to pay the retiring partner.

Exam Tip: Case III links capital adjustment with the payment to the retiring partner - the surplus brought in by continuing partners pays the outgoing partner.

Death Of A Partner

Question 22. What happens to a partnership when a partner dies?

Answer: When a partner dies, the partnership comes to an end immediately, although the firm may continue with the remaining partners. The deceased partner is entitled to receive his share in the firm as per the provision of the partnership agreement. His share in the firm is calculated in the same manner as in the case of a retiring partner.

In simple words: The partnership ends right away when a partner dies, but the business can keep going with the other partners. The dead partner's family gets what his share was worth, just like if he had retired.

Exam Tip: Death of a partner triggers the same settlement process as retirement, but the legal partnership automatically ends.

Question 23. How is the deceased partner's share of profit calculated?

Answer: If a partner dies on any date after the date of the balance sheet, his share of profit is calculated from the beginning of the year to the date of death. The calculation can be done on two bases: (A) On the basis of time - using the formula: Profit of the firm till the date of death = (Previous Year Profit or Average profit of a given number of past years / 12) × No's of months from last Balance Sheet to the date of death, then multiplied by the Deceased partner share. (B) On the basis of turnover (sale basis) - using the formula: Profit of the firm till the date of death = (Average profit of a given numbers of years or Profit of previous year / Sale of last year) × Sale from the date of last Balance Sheet till the date of death, then multiplied by the Deceased partner share.

In simple words: The dead partner gets his cut of profits earned from the start of the year until he died. You can count this two ways - by months or by sales amounts.

Exam Tip: Check the question to see whether time basis or sales basis should be used - the wording usually makes this clear.

Question 24. How is the amount due to a deceased partner ascertained?

Answer: The deceased partner's share is calculated in the same manner as in the case of the retiring partner. The amount due to a deceased partner is shown in his capital account after taking into account all credits and debits (including revaluation gains or losses, goodwill, accumulated reserves and profits, share of profit till death, salary, interest on capital, drawings, and accumulated losses). The amount due is then transferred to his executors' account by passing the journal entry: Deceased Partner's Capital A/c Dr To Deceased Partner's Executors A/c

In simple words: The dead partner's final due amount is figured out just like for a retiring partner - all credits go in, all debits come out. Then the total gets moved to an account for his family.

Exam Tip: The executors' account acts as a payable to the deceased partner's heirs - treat it like a liability.

Question 25. How is the amount due to the deceased partner settled?

Answer: The amount due to a deceased partner can be settled in two ways: (i) If payment is made in full or lump sum, the journal entry is: Deceased Partner's Executor's A/c Dr To Cash/Bank A/c. (ii) If payment is made in installments, two entries are passed: (a) Deceased Partner's Executor's A/c Dr To Deceased Partner's Executor's Loan A/c, and (b) Interest A/c Dr To Deceased Partner's Executor's Loan A/c. Interest is generally paid to the deceased partner's executor's at 6% per annum. Further payments of installments with interest are made using the entry: Deceased Partner's Executor's Loan A/c Dr To Cash/Bank A/c

In simple words: The family can be paid all at once in cash, or the firm can set up a loan to pay over time with interest added on (usually 6% a year).

Exam Tip: Always remember the 6% per annum interest rate on the loan to the deceased partner's executor unless stated otherwise.

Format Of Deceased Partner's Capital Account

Question 26. What is the format of a deceased partner's capital account?

Answer: A deceased partner's capital account is prepared in a T-format with debit and credit sides. On the debit side, entries include: To Revaluation A/c (Loss), To Profit and Loss Suspense A/c (Share of loss up to the date of death), To Accumulated Losses A/c, To Goodwill A/c (Written off), and To Partner Executor's A/c (Payment due - balancing figure). On the credit side, entries include: By Balance b/d, By Profit and Loss Suspense A/c (Share of profit up to the date of death), By Goodwill, By Reserves and Profits, By Revaluation A/c (gain), By Joint Life Policy A/c, By Interest on Capital A/c, By Salary A/c, and By Commission A/c. The balancing figure on the debit side represents the amount due to the executor.

In simple words: A dead partner's capital account looks like a normal account with two sides. Debits show costs and losses, credits show gains and income. The difference tells you how much his family gets.

Exam Tip: The balancing figure (on the side with fewer/smaller items) is the amount due to the executor - always check which side it falls on.

Please click the link below to download pdf file for CBSE Class 12 Retirement or Death of a Partner.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner Notes

Students can use these Revision Notes for Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 1 Chapter 3 Reconstitution of a Partnership Firm Retirement/Death of a Partner. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Retirement Or Death Of A Partner Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Retirement Or Death Of A Partner Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Retirement Or Death Of A Partner Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Retirement Or Death Of A Partner Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Retirement Or Death Of A Partner Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.