Download the latest CBSE Class 12 Accountancy Reconstitution Of Partnership Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner

To secure a higher rank, students should use these Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Revision Notes for Class 12 Accountancy

CHAPTER 3

Reconstitution of Partnership

Meaning of Reconstitution:

Any change in agreement of partnershipis called reconstitution of partnership firm. In following circumstances a partnership firm may be reconstituted:

1. Change in Profit Sharing Ratio

2. Admission of a partner

3. Retirement/Death of a partner

Change in profit sharing ratio among the existing partners

Meaning:

When all the partners of a firm agree to change their profit sharing ratio, the ratio may be changed. In this case one profit is purchasing a share of partner from another one. In other words, share of one partner may increase and share of another partner may decrease.

Accounting treatment of goodwill:

In case of change in profit sharing ratio, the gaining partner must compensate the sacrificing partner by paying the proportionate amount of goodwill.

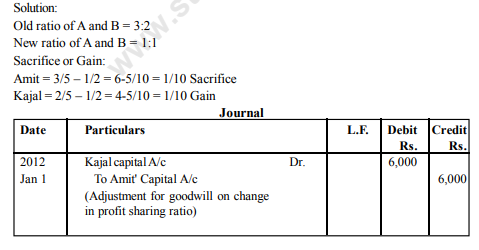

Illustration 1 Amit and Kajal were partners in a firm sharing profits in the ratio of 3:2. With effect from January 1,2012 they agreed to share profits equally. For this purpose the goodwill of the firm was valued at ‘60,000. Pass the necessary journal entry.

Accounting treatment of Reserves and Accumulated Profits: Case (i) When reserves and accumulated profits/losses are to be distributed At the time of change in profit sharing ratio, if there are some reserves or accumulated profits/losses existing in the books of the firm, these should be distributed to partners in their old profit sharing ratio.

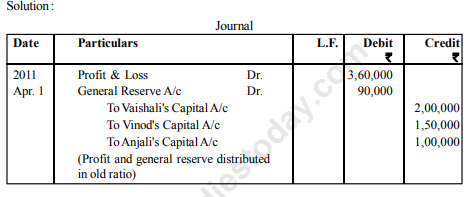

Illustration 2 : Vaishali, Vinod and Anjali are partners sharing profits in the ratio of 4:3:2. From April 1,2011, they decided to share the profits equally. On that date their books showed a credit balance of ‘3,60,000 in the profit and loss account and a balance of ‘ 90,000 in the General reserve. Record the journal entry for distribution of these profits and reserves.

Case (ii) When accumulated profits/losses are not be distributed at the time of change in ratio

Partners may decide that reserves and accumulated profits/losses will not be affected and remains in the books with same figure. In this case, the gaining partner must compensate the sacrificing partner by the share gained by him i.e. Gaining Partner's Capital A/c Dr.

To Sacrificing Partner's Capital A/c.

Illustration 4: Keshav, Meenakshi and Mohit sharing profit and losses in the ratio of 1:2:2,decide to share future profit equally with effect from April 1, 2011. On that date general reserve showed a balance of ` 2,40,000. Partners do not want to distribute the reserves. You are required to give the adjusting entry.

Solution: Keshav : Meenakshi : Mohit

Old ratio 1/5 : 2/5 : 2/5

New ratio 1/3 : 1/3 : 1/3

Sacrifice or Gain:

Keshav = 1/5 – 1/3 = 35/15 = 2/15 (Gain)

Meenakshi = 2/5 – 1/3 = 65/15 = 1/15 (Sacrifice)

Mohit = 2/5 – 1/3 = 65/15 = 1/15 (Sacrifice)

Illustration 5: Neha, Niharika, and Nitin are partners sharing profits and losses in the ratio of 2:3:4. They decided to change their ratio and their new ratio is 4:3:2. They also decided to pass a single journal entry to adjust the following without affecting their book values: ` Profit & Loss account 80,000

General Reserve 40,000

Advertisement Suspense A/c 30,000

You are required to give the single journal entry to adjust the above.

Solution:

Profit & Loss account 80,000

Add: General Reserve 40,000

1,20,000

Less: Advertisement Suspense 30,000

Total amount to be adjusted 90,000

Neha Niharika Nitn

Old ratio 2/9 3/9 4/9

New ration 4/9 3/9 2/9

Sacrifice or Gain :

Neha = 2/94/9=2/9 (Gain)

Niharika = 3/93/9=0 (No change)

Nitin = 4/92/9=2/9 (Sacrifice)

Accounting treatment for Revaluation of Assets and reassessment of Liabilities on change in Profit sharing ratio:

At the time of change in profit sharing ratio of existing partners, Assets and liabilities of a firm must be revalued because actual realizable value of assets and liabilities may be different from their book values. Change in the assets and liabilities belongs to the period prior to change in profit sharing ratio and therefore it must be shared in old profit sharing ratio.

Revaluation of assets and liabilities may be treated in two ways: (i) When revised values are to be shown in the books.

(ii) When revised values are not to be shown in the books

When revised values are to be shown in the books:

In this case revaluation of assets and liabilities is completed with the help of "Revaluation Account”. This account is also known as “Profit and Loss Adjustment Account”. All losses due to revaluation are shown in debit side of this account and all gains due to revaluation are shown in credit side of this account.

Note : (1) Increase in the value of an Asset and decrease in the value of a liability result in profit.

(2) Decrease in the value of any asset and Increase in the value of liability gives loss. Illustration 6:

Piyush, Puja and Praveen are partners sharing profits and losses in the ratio of 3:3:2. There balance sheet as on March 31st 2011 was as follows.

Partners decided that with effect from April 1, 2011, they would share profits and losses in the ratio of 4:3:2. It was agreed that:

(i) Stock be valued at ` 2,20,000.

(ii) Machinery is to be depreciated at 10%.

(iii) A provision for doubtful debts is to be made on debtors at 5%. (iv) Building is to be appreciatd by 20%.

(v) A liability for ` 5,000 included in sundry creditors is not likely to arise.

Partners agreed that the revised value are to be recorded in the books. You are required to prepare journal, revaluation account, partners capital account and revised balance sheet.

Please click the link below to download pdf file for CBSE Class 12 Reconstitution of Partnership.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Notes

Students can use these Revision Notes for Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Reconstitution Of Partnership Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Reconstitution Of Partnership Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Reconstitution Of Partnership Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Reconstitution Of Partnership Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Reconstitution Of Partnership Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.