Download the latest CBSE Class 12 Accountancy Accounting For Debentures Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures

To secure a higher rank, students should use these Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 2 Chapter 2 Issue and Redemption of Debentures Revision Notes for Class 12 Accountancy

Accounting for Debentures

DEBENTURES :A debenture is a document that either creates a debt or acknowledges it. In corporate finance, the term is used for a mediumto longterm debt instrument used by large companies to borrow money. In some countries the term is used interchangeably with bond, loan stock or note. A debenture is thus like a certificate of loan or a loan bond evidencing the fact that the company is liable to pay a specified amount with interest and although the money raised by the debentures becomes a part of the company’s capital structure, it does not become share capital.

Note : Debenture is instrument that is not secured by physical asset or collateral In case of bond interest is not clared. Debentures are generally freely transferable by the debenture holder. Debenture holders have no rights to vote in the company’s general meetings of shareholders,The interest paid to them is a charge against profit in the company’s financial statements.

Types of debentures

Convertibility point of view : there are two types of debentures:

Convertible debentures, which are can be converted into equity shares of the issuing company after a predetermined period of time.

These may be Partly Convertible Debentures (PCD): A part of these instruments are converted into Equity shares in the future at notice of the issuer. The issuer decides the ratio for conversion. This is normally decided at the time of subscription.

•Fully convertible Debentures (FCD): These are fully convertible into Equity shares at the issuer’s notice. The ratio of conversion is decided by the issuer. Upon conversion the investors enjoy the same status as ordinary shareholders of the company.

Nonconvertible

debentures, which are simply regular debentures, cannot be converted into equity shares of the liable company. They are debentures without the convertibility feature, they usually carry higher interest rates than their convertible counterparts. On basis of Security, debentures are classified into:∙

Secured Debentures: These instruments are secured by a charge on the fixed assets of the issuer company. So if the issuer fails on payment of either the principal or interest amount, his assets can be sold to repay the liability to the investors

Unsecured Debentures: These instrument are unsecured in the sense that if the issuer defaults on payment of the interest or principal amount, the investor is treated like along other unsecured creditors of the company .

From redemption point of view

Redeemable Debentures:Redeemable debentures are those which are redeemed or paid off after the termination of fixed term. The amount paid off includes the principal amount and the current year’s interest. The company always has the option of either to redeem a specific number of debentures each year or redeem all the debentures at specified date.

Irredeemable or Perpetual Debentures:Irredeemable debentures are those debentures which do not have any fixed date of redemption. They are redeemed either in the event of winding up or at a very remote period of time. Irredeemable or perpetual debenture holders can never force the company to redeem their debentures.

Issue of Debentures :

Debentures can be issued in two ways

1 . for cash

2. for consideration other than cash

3. As collateral security

Terms of issue of: Debentures can be issued in two ways

1 .Issue of Debentures at Par

2. Issue of Debentures at Premium

Debentures payable in Instalments

1. First instalment paid along with application is called as application money

2. Second instalment paid on allotment is called as allotment money

3. Subsequent instalments paid are called as call money calls can be more than one and called First call, second call or as the case may be ISSUE OF Debentures FOR CASH AT PAR : This means shares are issued at face value

Example

Raj Ltd. Issued 2,000 12% Debentures of Rs.100 each at par payable Rs.25 on Application, Rs.50 on Allotment and the balance on first and final call. In all 3,000 application were received. Allotment was made to 2,000 applicants others were rejected. Give Journal entries.

Importan : If % of debenture is given then it must be written along with Debenture ISSUE OF DEBENTURES AT PREMIUM : It is issue of Debenture at more than face value Note : Premium is Presumed To be Demanded on Allotment Unless Specified and Credited to Securities Premium Account

Example Z Ltd. Invited applications for 5,000, 8% Debentures of Rs.100 each at a premium of 2%, Rs.40 were payable on Application and balance an allotment. Applications were received for 4,800 shares and accepted in full. All money duly received. Journalise the transactions.

Oversubscription of debentures : In such case excess application are rejected or partial or Prorata allotment is done or combination of both is carried on.

Ganga Ltd. issued 2,000 debentures of Rs.100 each at a premium of 10% payable Rs.25 on application Rs.40 (including premium) payable on allotment and balance on First and final Call. In all 3,500 application were received 500 application were rejected and allotment was made to applicants of 3,000 debentures on Prorata basis. The excess money was adjusted on allotment. Give journal entries

Please click the link below to download pdf file for CBSE Class 12 Accounting for Debentures.

Meaning of Debenture

The term 'debenture' has been taken from the Latin word "debre" which means "to borrow". Thus, it is a written document that confirms a debt under the common seal of the company and contains a contract for the repayment of the principal sum at a specified date and for the payment of interest (usually half-yearly) at a fixed rate percent until the principal sum is repaid.

"Debenture includes debenture stock, bonds and any other securities of a company whether constituting a charge on the assets of the company or not." - Section 2(12) of the Companies Act, 1956.

Bond

Bond, like debenture, is an acknowledgment of debt issued under the seal of a company and signed by an authorized signatory.

Charge

It means securing the loan by pledging a specific part of assets towards the loan. It means, if the company fails to meet its obligation, the lender can secure his payment from the assets mortgaged or in case of winding up of the company from the official liquidator.

The Companies Act, 1956 requires that all the charges be registered with the Registrar of Companies. Section 125 (4) of the Companies Act, 1956 requires that a charge when created on the following be got registered:

- For the purpose of securing any issue of debentures.

- On uncalled share capital of the company.

- On calls made but not paid.

- On any book debts of the company.

- On any immovable property, wherever situated, or any interest therein.

- On a ship or any share in the ship.

- On goodwill, on a patent or a license under a patent, on a trademark or on the copyright or a license under copyright.

Types of Debentures

There are two types of debentures:

Convertible Debentures - These can be changed into equity shares of the issuing company after a set period of time. These may be:

- Partly Convertible Debentures (PCD): A part of these instruments are changed into Equity shares in the future at notice of the issuer. The issuer decides the ratio for conversion. This is normally decided at the time of subscription.

- Fully Convertible Debentures (FCD): These are fully changeable into Equity shares at the issuer's notice. The ratio of conversion is decided by the issuer. Upon conversion the investors enjoy the same status as ordinary shareholders of the company.

Non-convertible Debentures - These are simply regular debentures, cannot be changed into equity shares. These are debentures without the convertibility feature; these usually carry higher interest rates than their convertible counterparts.

On Basis of Security, Debentures Are Classified Into:

Secured Debentures: These instruments are secured by a charge on the fixed assets of the issuer company. So if the issuer fails to pay off either the principal or interest amount, its assets can be sold to repay the liability towards debenture holders.

Unsecured Debentures: These instruments are unsecured in the sense that if the issuer defaults on payment of the interest or principal amount, the investor is treated like other unsecured creditors of the company.

From Redemption Point of View

Redeemable Debentures: Redeemable debentures are those which are redeemed or paid off after the termination of fixed term. The amount paid off includes the principal amount and the current year's interest. The company always has the option of either to redeem a specific number of debentures each year or redeem all the debentures at a specified date.

Irredeemable or Perpetual Debentures: Irredeemable debentures are those debentures which do not have any fixed date of redemption. They are redeemed either in the event of winding up or at a very remote period of time. Irredeemable or perpetual debenture holders can never force the company to redeem their debentures.

Distinguish Between a Share and Debenture

| Basis | Share | Debenture |

|---|---|---|

| Ownership | Shareholders are the owners of company | Debenture holders are the lenders of company |

| Form of return | Dividend | Interest |

| Security | Not secured | Secured by a charge on assets |

| Voting right | Equity shareholders have the voting right | No voting right in normal course of business |

| Risk | More risk as compared to Debentures | Risk Free due to secured Debentures |

Issue of Debentures

Debentures can be issued in following ways:

- For cash

- For consideration other than cash

- As collateral security

Terms of Issue

Debentures can be issued in following ways:

- Issue of Debentures at Par

- Issue of Debenture at Premium

- Issue of Debentures at Discount

Debenture Payable in Installments

- First installment paid along with the application is called application money.

- Second installment paid on allotment is called allotment money.

- Subsequent installments paid are called as call money calls can be more than one and called First call, second call or as the case may be.

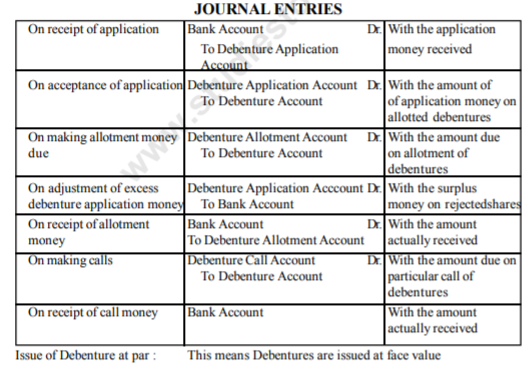

Issue of Debentures for Cash

(a) When Debentures amount received in lump sum with the application

| Event | Journal Entry | Remarks |

|---|---|---|

| On receipt of application money | Bank A/c Dr. To Debenture Application and Allotment A/c | With the application money received |

| On acceptance of application money | Debenture Application and Allotment A/c Dr. To X% Debentures A/c To Bank A/c | With Amount of application money on allotted debentures, and Excess amount refunded. |

(B) When Debentures amount received in installments.

In this case accounting entries will be same as at the time of issue of shares in instalments with small change in the name of term like - the share capital word replaced with the X% Debentures A/c, and Share word replaced with Debentures e.g. Equity share capital into 8% Debentures, Equity share application into Debentures Application and follows on.

AT Par: means debentures are issued at face value.

Issue of Debentures for Consideration Other Than Cash

When Debentures are issued for purchase of asset

| Scenario | Journal Entry | Remarks |

|---|---|---|

| When Debentures Issued for purchases Asset at par | Sundry Asset A/c Dr. To Vendor | With the purchases consideration |

| Vendor Dr. To Debenture Account | ||

| When Debentures are issued for purchases of asset at premium | Sundry Assets A/c Dr. To Vendor | With the purchases Consideration No. of debentures par value No. of debentures x premium |

| Vendor Dr. To Debenture A/c To Security Premium Reserve A/c |

When Business is Purchased

| Scenario | Journal Entry | Remarks |

|---|---|---|

| When Purchase consideration is equal to net value of assets | Sundry Assets A/c Dr. To Sundry Liabilities A/c To Vendor | Value of asset Value of liabilities Purchases considerationExcess of Purchase Value (B/F)Value of LiabilitiesPurchases Consideration |

| When Purchases consideration more than net value of assets | Goodwill Account Dr. To Sundry Liabilities A/cTo Vendor | |

| When Purchase Consideration is less than net value of asset | Sundry Assets Account Dr. To Sundry Liabilities A/c To Capital Reserve To Vendor | Value of Asset Value of liabilities Difference (B/F Purchases Consideration |

Collateral Security

Collateral security means security given to the lender in addition to the principal security. It is a subsidiary or secondary security. Whenever a company takes a loan from a bank or from any financial institution it may issue its debentures as secondary security which is in addition to the principal security. Such an issue of debentures is known as 'issue of debentures as collateral security'. The lender will have a right over such debentures only when the company fails to pay the loan amount and the principal security is exhausted. In case the need to exercise the right does not arise, debentures will be returned back to the company. No interest is paid on the debentures issued as collateral security because the company pays interest on loan.

In the accounting books of the company issue of debentures as collateral security can be credited in two ways:

First method: No Journal entry to be made in the books of accounts of the company for debentures issued as collateral security. A note of this fact is given in this case.

Second method: Entry to be made in the books of accounts of the company.

A journal entry is made on the issue of debentures as a collateral security, Debentures Suspense Account is debited because no cash is received for such an issue.

Following journal entry will be made

| Date | Particulars | L.F. | Debit (Rs.) | Credit (Rs.) |

|---|---|---|---|---|

| Debenture Suspense A/c Dr. To % Debentures A/c (Being the issue of Debentures of Rs... each issued as collateral security) |

Interest on Debentures

Interest on Debentures is calculated at a fixed rate on its face value and is usually payable half yearly and is paid even if the company is suffering from loss because it is charged on profit.

Income Tax is deducted from interest before payment to debenture holders. It is called T.D.S. (Tax deducted at source).

Journal Entries

| Event | Journal Entry | Remarks |

|---|---|---|

| 1. When interest is Due | Debentures Interest A/c Dr. To Debentures holder A/c To Income Tax Payable A/c | (Gross Interest) (Net Interest) (Income Tax Deducted) |

| 2. When Interest is paid | Debentures Holder A/c Dr. To Bank A/c | (With Interest) |

| 3. On payment of Income Tax to Government | Income Tax Payable A/c Dr. To Bank A/c | (Amount of Income) |

| 4. On Transfer of Interest on Debenture to statement of profit and Loss A/c | Statement of Profit and Loss Dr. To Debenture Interest A/c | (Tax deducted at source) (Amount of Interest) |

Redemption of Debentures

Redemption of debentures means repayment of the loan due on debentures to debenture holders. According to Section 117 C (3) of the Companies Act 1956, the debentures should be redeemed in accordance with the terms and conditions of their issue/ offer documents. The date, the terms, and the conditions are generally stated in the debenture certificate itself or in the trust deed.

On the due date or happening of the circumstances so specified, the company becomes liable to pay the principal amount to the debenture holder. A company may purchase its own debenture which then stands canceled.

In other words, the redemption of debentures means repayment of the number of debentures by the company. There are three aspects that a company should bear in mind regarding redemption, namely the time of redemption, the amount to pay, and the sources from which redemption will have to be carried out.

Methods of the Redemption of Debentures

The various methods of redemption of debentures are as under:

- Payment in Lump-Sum

- Payment in Installments

- Purchase in Open Market

- Conversion of existing Debenture into Shares or New Debentures.

1. Payment in Lump Sum

It means debentures can be redeemed by paying the debenture holders in one lump sum at the expiry of the agreed time or earlier at the option of the company. In this case, the time of repayment is known in advance and thus the company can plan its financial resources accordingly.

2. Payment in Installments

It means the redemption is made in annual installments. The amount of installment is worked out by dividing the total amount of debentures by the number of years it is to last. The number of debentures to be redeemed each year are selected by lottery. Thus, it is also known as drawing by lottery or draw of lots.

3. Purchase in Open Market

A company, if authorized by its Articles of Association, can purchase its own debenture in the open market. Debentures so purchased may be canceled and it means the debentures have been paid.

4. Conversion of Existing Debentures into Shares or New Debentures

It means the debenture holder can exchange their debenture either for shares or new debentures of the company and the debentures which carry such rights are called convertible debentures.

Sources of Funds for Redemption of Debentures

The redemption of debentures can be done either out of capital or out of profits.

(a) Redemption of Debenture Out of Capital

In this case, profits of the company are not utilized for the redemption of debentures, so the assets of the company are reduced by the amount paid. Normally the profits are transferred to Debenture Redemption Reserve for redemption. In case no profits have been transferred to Debenture Redemption Reserve and debentures are redeemed on the due date, it is regarded as redemption out of the capital. It is, however, presumed that the company has adequate funds to redeem the debentures.

Accounting Treatment:

(a) If debentures are to be redeemed at par

1. On debentures becoming due

Debentures A/c Dr.

To Debenture- holder A/c

2. On Redemption

Debenture Holder A/c Dr.

To Bank A/c

(b) If debentures are to be redeemed at a premium

1. On debentures becoming due

Debentures A/c Dr.

Premium on Redemption of Debenture A/c Dr.

To Debenture holder A/c

2. On Redemption

Debenture holder A/c Dr.

To Bank A/c

(b) Redemption of Debentures Out of Profits

Redemption of debentures out of profits means the amount equal to that utilized for repayment to debenture holders is transferred from Profit and Loss Appropriation A/c to a newly opened A/c called 'Debenture Redemption Reserve A/c' (DRR). The portion of the profits set aside may either be retained in the business or maybe invested.

The Companies Act (Amendment), 2000 Has Introduced Section 117 C Which Provides As Under:

(a) Where company-issued debentures after the commencement of this act, it shall create a DRR for the redemption of such debentures, to which an adequate amount shall be credited, from out of its profits every year until such debentures are redeemed.

(b) The amount credited to the DRR shall not be utilized by the company except for the purpose of the redemption of debentures.

SEBI's Guidelines

Securities and Exchange Board of India (SEBI) has provided some guidelines for the redemption of debentures. The focal points of these guidelines are:

1. Every company shall create a venture Redemption Reserve in case of issue of debenture redeemable after a period of more than 18 months from the date of issue.

2. The creation of Debenture Redemption Reserve is obligatory only for non-convertible debentures and a non-convertible portion of partly convertible debentures.

3. A company shall create a Debenture Redemption Reserve equivalent to at least 50% of the amount of debenture issue before starting the redemption of the debenture.

4. Withdrawal from Debenture Redemption Reserve is permissible only after 10% of the debenture liability has already been reduced by the company.

Exemption:

SEBI guidelines would not apply under the following situations:

(a) Infrastructure company (a company wholly Engaged in the business of developing, maintaining, and operating infrastructure facilities.)

(b) A company issuing debentures with a maturity period of not more than 18 months.

Clarifications Regarding Debenture Redemption Reserve

The Department of Company Affairs, Government of India, vide their circular No. 9/2002, dates 18.04.2002 has issued the following clarifications regarding the creation of Debenture Redemption Reserve (DRR):

(a) No DRR is required for debentures issued by All India Financial Institutions, by RBI and, Banking Companies for both public as well as privately placed debentures.

(b) No DRR is required in case of privately placed debentures.

(c) Section 117c will apply to debentures issued and pending to be redeemed and, therefore, DRR will also be created for debentures issued prior to 13.12.2000 and pending redemption.

(d) Section 117c will apply to the non-convertible portion of debentures issued whether they are fully or partly paid.

Journal Entries

Debenture A/c

To Debentureholders A/c

Debenture holder A/c

To Bank A/c

Profit and Loss Appropriation A/c

To Debenture Redemption Reserve A/c

Debenture Redemption Reserve A/c appears on the liability side of the Balance Sheet, under the head "Reserves and Surplus". The balance in Debenture Redemption Reserve A/c increases with each redemption. When all the debentures are redeemed, the Debenture Redemption Reserve A/c is closed by transferring its balance to General Reserve A/c.

Redemption by Purchase in the Open Market

A company, if authorized by its Articles of Association, can redeem its own debenture by purchasing them in the open market.

If a company purchases its own debenture for the purpose of immediate cancellation, the purchase and cancellation of such debenture are called, redemption by purchase in the open market.

Advantages:

1. A company can redeem the debentures at its convenience whenever it has surplus funds.

2. A company can save money by purchasing its own debenture when they are available in the market at discount.

Accounting Treatment:

(In Case of Profits)

(a) On purchase of own debentures for immediate cancellation

Debenture A/c Dr.

To Bank A/c

To Profit on Cancellation of Debenture A/c

(b) On transfer of Profit on Redemption

Profit on Cancellation of Debenture A/c Dr.

To Capital Reserve A/c

(In Case of Loss)

(a) On purchase of own debenture for immediate cancellation.

Debenture A/c Dr.

Loss on Cancellation of Debenture A/c Dr.

To Bank A/c

(b) On transfer of Loss on Redemption

Profit and Loss A/c Dr.

To Loss on Cancellation of Debenture A/c

Redemption by Conversion

Sometimes, at the time of issue of debentures, a company gives the convertible debenture holders the privilege that they can get their debentures changed into shares or new debentures after the expiry of a specified period. Whenever debenture is redeemed by conversion, the debenture holders have to apply for the same. The new shares or debentures may be issued at par, discount, or a premium.

No Debenture Redemption Reserve is required in case of convertible debentures because no funds are required for redemption.

If debentures to be changed were issued at discount, the issue price of the share must be equal to the amount actually received from debentures. If this rule is not followed, it would be a violation of section 79 of the Companies Act, 1956.

Accounting Treatment:

(i) For the amount due to debenture holders

(a) If Redemption at par

Debentures A/c Dr.

To Debentureholder A/c

Or If Redemption at a premium

Debentures A/c Dr.

Securities Premium A/c Dr.

To Debentureholder A/c

(b) For discharging obligation by issuing shares or debentures

Debenture Holder A/c Dr.

To Equity Share Capital

Or

To Debentures A/c (New)

If the new shares/debentures are issued at a premium, the Securities Premium A/c is credited or new shares/debentures are issued at a discount, the Discount on Issue of Shares/Debentures A/c is debited in the above-mentioned entry (b).

Sinking Fund Method

The amount required for the redemption of debentures is generally large and the date of redemption is known to the company. Thus, it is prudent for a company to make arrangements to ensure the availability of adequate funds for the redemption of debenture at the end of the stipulated period for which debentures are issued. Hence, it is better for the company to set aside every year a part of divisible profits and to invest the same outside the business in marketable securities.

This is done by creating a Sinking Fund. The company adopts the method of Debenture Redemption Sinking Fund. An appropriate amount calculated by referring to Sinking Fund Factors, depending upon the interest rate on investments and the number of years for which investments are made, is set aside.

Basic Concepts

Meaning of Redemption of Debentures: Redemption of debentures means repayment of debentures to the debentureholders. Debenture is a liability on the part of a company, so the redemption of debentures means the discharge of liability. Hence, redemption of debentures means discharge of an obligation arising out of the contractual obligations created through the Debenture Trust Deed.

Methods of Redemption of Debentures: Following are the methods for redemption of debentures:

- Lump sum payment.

- Draw of lots or annual drawings.

- Purchase of own debentures from open market.

- Conversion.

Note: Purchase of own Debentures from open market and conversion of Debentures are not discussed as they have been excluded from the syllabus.

Sources of Redemption: Sources available for redemption of debentures are:

- Redemption out of capital (No DRR is created)

- Redemption out of profits (100% DRR is created)

- Redemption out of profits and Capital (25% DRR is created)

Note: Redemption only out of capital is not possible as companies other than exceptions need to transfer amount to DRR.

Debenture Redemption Reserve (DRR): According to Section 71(4) of the Companies Act, 2013, along with the Rule 18(7) of the Companies (Share Capital and Debentures) Rules, 2014, the companies are required to set aside an amount out of profit (Surplus, i.e., Balance in Statement of Profit and Loss) for redemption of debentures to a separate account. This account is known as Debenture Redemption Reserve (DRR).

DRR is shown on the Equity and Liabilities part of the Balance Sheet under the head 'Shareholders' Funds' and Sub-head 'Reserves and Surplus'. DRR can be transferred to General Reserve either after every redemption is over or after all the debentures have been redeemed.

As per rule 18(7) of the Companies Rules, 2014, the following companies would now be required to create DRR of an amount equal to 25% of the total nominal (face) value of debentures:

- Non-Banking Financial Companies (NBFCs) registered with RBI.

- Financial Institutions except All India Financial Institutions regulated by RBI.

- Housing Finance Companies those registered with National Housing Bank. In case of privately placed debentures, issued by the above mentioned companies, DRR is not required.

- For other companies it is required to create DRR for both public and privately placed debentures.

Debenture Redemption Investment (DRI)

As per Companies Act, 2013 in Rule 18(7) of the Companies (Share Capital and Debentures) Rules, 2014, Debentures Redemption Investment is described as follows:

"The Company shall invest an amount at least equal to 15% of the nominal (face) value of debentures that shall be redeemed by the company by 31st March of the next year and the amount should be invested on or before 30th April of the Current year."

It means the amount invested or deposited should not at any time fall below 15% of the nominal (face) value of debentures maturing by 31st March of the financial year.

Securities specified for Investment:

- In deposits with any Scheduled Bank, free from any charge.

- In unencumbered securities of the Central Government or any State Government.

- In unencumbered securities mentioned in Sub-clauses (a) to (d) and (ee) of Section 20 of Indian Trust Act, 1882.

- In unencumbered bonds issued by any other company which is notified under Sub-clause (f) of Section 20 of Indian Trust Act, 1882.

Exceptions: According to Rule 18(7) (b) of the Companies (Share Capital and Debentures) Rules, 2014 the following type of companies are not required to create DRR:

- All India Financial Institutions regulated by Reserve Bank of India (RBI)

- Banking Companies.

Lump Sum Payment at Maturity: Under this method, the total amount of debentures is paid to debentureholders in lump-sum at the expiry of a specified period, i.e., at maturity date of the debentures. The company can pay the amount even before maturity if the debenture deed so provides. Such redemption can be made at par or at premium according to the terms of issue.

Journal Entries:

(A) When debentures become due for payment.

(i) At Par:

Debentures A/c Dr. (with nominal value)

To Debentureholders' A/c

(ii) At Premium:

Debentures A/c Dr. (with nominal value)

Premium on Redemption of Debentures A/c Dr. (with amount of Premium)

To Debentureholders' A/c (with total amount)

(B) When debentures are redeemed

Debentureholders' A/c Dr. (with the amount paid)

To Bank A/c

Redemption of Debentures out of capital: When sufficient profits are not transferred to DRR from Surplus, i.e., Balance in Statement of Profit and Loss before the redemption of debentures, then it is known as redemption out of capital. It should be noted that as per Section 71(4) of the Companies Act, 2013, along with the Rule 18(7) of the Companies (Share Capital and Debentures) Rules, 2014 all companies except exempted Companies except exempted companies are required to create DRR. The following journal entries are passed in case of redemption out of capital:

(i) When Debentures become due for payment:

- Debentures A/c Dr. (with nominal value)

- Premium on Redemption of Debentures A/c Dr. (if premium is payable on redemption)

- To Debentureholders' A/c (with total amount due)

Free study material for Accountancy

CBSE Class 12 Accountancy Part 2 Chapter 2 Issue and Redemption of Debentures Notes

Students can use these Revision Notes for Part 2 Chapter 2 Issue and Redemption of Debentures to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 2 Chapter 2 Issue and Redemption of Debentures Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 2 Chapter 2 Issue and Redemption of Debentures Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 2 Chapter 2 Issue and Redemption of Debentures. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Accounting For Debentures Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Accounting For Debentures Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Accounting For Debentures Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Accounting For Debentures Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Accounting For Debentures Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.