Download the latest CBSE Class 12 Accountancy Dissolution Of A Partnership Firm Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 1 Chapter 4 Dissolution of Partnership Firm

To secure a higher rank, students should use these Class 12 Accountancy Part 1 Chapter 4 Dissolution of Partnership Firm notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 1 Chapter 4 Dissolution of Partnership Firm Revision Notes for Class 12 Accountancy

CBSE Class 12 Dissolution Of A Partnership Firm. Learning the important concepts is very important for every student to get better marks in examinations. The concepts should be clear which will help in faster learning. The attached concepts made as per NCERT and CBSE pattern will help the student to understand the chapter and score better marks in the examinations.

CHAPTER 6

DISSOLUTION OF A PARTNERSHIP FIRM

Dissolution of a firm: As per Indian Partnership Act, 1932: “Dissolution of firm means termination of partnership among all the partners of the firm”. When a firm is dissolved, the business of the firm terminates. All the assets of the firm are disposed off and all outsiders’ liabilities and partners’ loan and partners capitals are paid.

Dissolution of Partnership: Dissolution of Partnership refers to termination of old partnership agreement (i.e., Partnership Deed) and a reconstruction of the firm. It may take place on

- Change in profit sharing ratio among the existing partner;

– Admission of a partner; and

– Retirement or Death of a partner.

It may or may not result into closing down of the business as the remaining partners may decide to carry on the business under a new agreement. Types of dissolution of firms : A partnership firm can be dissolved in any of the

following ways :

(A) Without the intervention of the court :

(1) When all partners agree to dissolve the firm (Sec. 40);

(2) Compulsory Dissolution (Sec. 41)

(i) When all or all but one partner of the firm become insolvent.

(ii) when business of the firm become unlawful.

(3) On the happening of any of the following events : (Sec. 42)

(i) On the insolvency of a partner.

(ii) On the fulfilment of the objective of the firm for which the firm was formed.

(iii) On the expiry of the term (period) for which the firm was formed.

(4) By Notice (Sec. 43) : When the duration of the partnership firm is not fixed and it is at will of the partners. Any partner by giving notice to other partners can dissolve the firm.

(B) Dissolution by order of the court (Sec 44) : A court on application by a partner may order the dissolution of the firm under the following circumstances :

(1) When a partner has become of unsound mind.

(2) When a partner has become permanently incapable of performing his duties as a partner.

(3) When a partner is found guilty of misconduct that may harm the partnership.

(4) When a partner consistently and deliberately commits breach of partnership agreement.

(5) When a partner transfer whole of his interest in the business firm to a third party, without the consent of existing partners.

(6) When the court is satisfied that the partnership firm cannot be carried on except at a loss.

(7) When the court find is that the dissolution of firm is justified and equitable.

ACCOUNTING TREATMENT ON DISSOLUTION

On dissolution of a firm, the following accounts are opened to close the books of the firm:

– Realisation Account;

– Partner’s Loan Account;

– Partners’ Capital Accounts; and

– Cash or Bank Account.

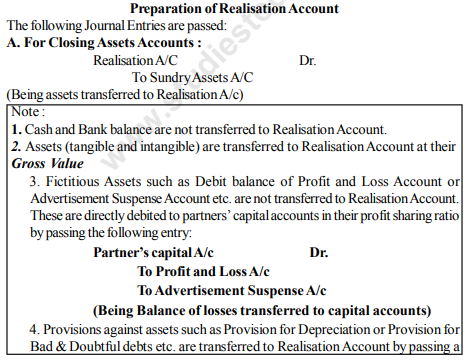

Realisation Account: It is nominal account opened on the dissolution of a firm to ascertain the profit or loss on realisation of assets and payments of outsiders’ liabilities. This account is closed by transferring the balance (i.e., profit or loss on realisation) to partner’s capital accounts.

Dissolution of a Partnership Firm

1. Dissolution

Dissolution means stopping an existing relationship among the partners. According to Indian Partnership Act, 1932, dissolution can be either of partnership or of a firm.

2. Dissolution of Partnership

It changes the existing relationship between partners but the firm may carry on its business as before.

3. Dissolution of Partnership Firm

Dissolution of a firm means stopping of partnership among all the partners in the firm. In this case, the business of the firm also comes to an end.

4. Modes of Dissolution of Partnership Firm

(i) Dissolution by mutual agreement

(ii) Compulsory dissolution

(iii) Dissolution on the happening of an event

(iv) Dissolution by notice

(v) Dissolution by court

5. Settlement of Accounts in Case of Dissolution of Firm

(i) Treatment of Losses

Losses shall be paid, first out of profits, then out of partner's capital and lastly, by the partners individually in their profit sharing ratio, if necessary.

(ii) Application of Assets

(a) Payment to outsiders/creditors

(b) Loans and advances of partners

(c) Payment of capital of partners

(d) The balance shall be divided among the partners in their profit sharing ratio

6. Treatment of Firm's Debt and Private Debts

Where both the debts of the firm and private debts of a partner exist together. The following rules, as stated in Section 49 of the Act, shall apply:

(i) Firm's property is used first in payment of firm's debts and if there is any surplus, then the share of each partner is used in the payment of his private debts or paid to him.

(ii) Partner's private property is used first in payment of his private debts and the surplus (if any) in payment of firm's debts if the firm's liabilities go beyond the firm's assets.

7. Accounting Treatment on Dissolution of Firm

On dissolution, the books of the firm are closed. The process is completed by opening the following accounts:

(i) Realisation account

(ii) Partners' capital account

(iii) Partners' loan account

(iv) Cash/bank account

Realisation Account

It is a nominal account set up at the time of dissolution of partnership firm to show profit or loss on realisation of assets and payment of liabilities.

Note:

(i) Goodwill appearing in the balance sheet is treated as any other asset. In case, question is silent about the realisation of goodwill, it is assumed the goodwill does not have any value and no amount is realised for it.

(ii) When an asset is transferred to a realisation account, its corresponding reserve or provision appearing on the liabilities side of the balance sheet is also transferred to the realisation account.

(iii) In the absence of any information regarding realisation of assets (tangible or intangible) and settlement of any outside liabilities, it should be assumed that no amount has been realised from such assets and an amount equal to the book value of such liability has been paid off.

| Dr. | Realisation A/c | Cr. | ||

|---|---|---|---|---|

| Particulars | Amount (Rs.) | Particulars | Amount (Rs.) | |

| To Land and Building | XXX | By Sundry Creditors | XXX | |

| To Plant and machinery | XXX | By Bills payables | XXX | |

| To Furniture and Fittings | XXX | By Bank overdraft | XXX | |

| To Bills Receivable | XXX | By Outstanding expenses | XXX | |

| To Sundry Debtors | XXX | By Provision for doubtful debts | XXX | |

| To Cash/Bank (payment of liabilities) | XXX | Cash/Bank (sale of assets) | XXX | |

| To Cash/Bank (payment of unrecorded liabilities) | XXX | By Partner's capital account (assets taken by partner) | XXX | |

| To Partner's capital account (liabilities assumed by partners) | XXX | By Loss (transferred to partner's capital account) | XXX | |

| To Profit (transferred to partner's capital account in their profit sharing ratio) | XXX | |||

| Total | XXX | Total | XXX | |

Partners' Capital Account

Balance of partner's capital and current account are recorded in this account. Any asset of the firm taken over by the partner is recorded on the debit side and liability taken over is recorded on the credit side.

Undistributed profits and reserves are recorded on the credit side and undistributed losses or fictitious assets are recorded on the debit side. When capital accounts are maintained following a fixed capital account method, partners have current accounts also. These current accounts may have credit or debit balance. Current accounts are closed by transferring them to the concerned partner's fixed capital accounts.

The entries are as follows:

(a) In case of debit balance in a current account of a partner

Concerned Partners' Capital A/c Dr

To Concerned Partners' Current A/c

(b) In case of credit balance in a current account of a partner

Concerned Partners' Current A/c Dr

To Concerned Partners' Capital A/c

The balance of partner's capital account are closed in the following manner

(a) For making final payment to a partner (In case of credit balance)

Partner's Capital A/c Dr

To Cash/Bank A/c

(b) When a partner is required to bring in cash (In case of a debit balance)

Cash/Bank A/c Dr

To Partner's Capital A/c

Format of Partner's Capital Account

| Dr. | Partners' current account | Cr. | |||||

|---|---|---|---|---|---|---|---|

| Date | Particulars | A Rs. | B Rs. | Date | Particulars | A Rs. | B Rs. |

| To Balance b/d* | xxx | xxx | By Balance b/d* | xxx | xxx | ||

| To Drawings A/c | xxx | xxx | By Interest on capital A/c | xxx | xxx | ||

| To Interest on drawings A/c | xxx | xxx | By Salary A/c | xxx | xxx | ||

| To Profit and loss appropriation A/c (share of loss) | xxx | xxx | By Commission A/c | xxx | xxx | ||

| By Profit and loss appropriation A/c (share of profit) | xxx | xxx | |||||

| To Balance c/d** | xxx | xxx | By Balance c/d** | xxx | xxx | ||

| xxx | xxx | xxx | xxx |

Note: * The opening balance may be either credit balance or debit balance for a partner. ** The closing balance may be either credit balance or debit balance for a partner.

Partner's Loan Account

Partner's loan will be paid after all outside liabilities are paid.

Partner's Loan A/c Dr

To Cash/Bank A/c

Bank or Cash Account

It is a real account. On the debit side, opening balance, amount realised through sale of assets and any amount paid in by the partners are shown. On the credit side, all the payments for liabilities, realisation expenses and final settlement made to partners are shown. In case both cash and bank balances appear in the balance sheet, it is always better to open a single account. It is a self-balancing account.

Preparation of Memorandum Balance Sheet for Ascertaining Sundry Assets

Memorandum balance sheet is prepared for calculating the missing figures of sundry assets. Sometimes, the total value of sundry assets is not given. However, the value realised from the assets is given, also the partners capitals and other liabilities are also given. In that case, sundry assets have to be worked out by preparing the old balance sheet. The amount of capitals and other liabilities are added. The sum total is the total amount of assets.

Dissolution Of A Partnership Firm

Basic Concepts

Meaning Of Dissolution Of Partnership Firm: According to Section 39 of the Indian Partnership Act, 1932, "Dissolution of the firm means dissolution of partnership among all the partners in the firm". In such an event, all assets of the firm are realised i.e., sold and liabilities are paid. The surplus balance is paid to the partners in settlement of their accounts and short fall is met from their private estates.

Unlike dissolution of partnership which means only change in existing relationship between the partners and the firm continues. Dissolution of firm means the firm is dissolved i.e. wind up.

Types Of Dissolution Of A Firm: The Indian Partnership Act, 1932 states ways of dissolution of a partnership firm. A partnership firm stands dissolved in the following ways:

1. Dissolution By Agreement (Section 40)

(i) Voluntary dissolution through mutual agreement amongst partners.

(ii) Consensual dissolution according to the partnership agreement or a contract.

2. Compulsory Dissolution (Section 41)

(i) When the business of the firm is declared illegal.

(ii) When all the partners except one decide to retire from the firm.

(iii) When all the partners or all except one partner die.

(iv) When all the partners or all except one partner are declared insolvent.

3. Dissolution Upon Contingency, If The Partnership Deed So Provides (Section 42)

(i) When the firm is constituted for a fixed term, on the expiry of that term.

(ii) When the firm is constituted to carry out one or more projects/ventures, on the completion thereof.

(iii) When a partner of the firm dies.

(iv) When a partner of the firm is declared insolvent.

4. Dissolution By Notice (Section 43)

In case of partnership at will, the firm may be dissolved if any one partner gives a notice in writing to the other partners.

5. Dissolution By Order Of Court (Section 44)

(i) When a partner has become mentally disturbed or has unsound mind.

(ii) When a partner has become permanently incapable of performing his duties.

(iii) When a partner has transferred whole of his interest in the firm to a third party.

(iv) When a partner deliberately commits breach of agreements relating to the management of the firm.

(v) When the court is satisfied that the firm cannot be carried on except at a loss.

(vi) When the court is satisfied that the dissolution of the firm is just and equitable.

Settlement Of Accounts: Section 48 of the Indian Partnership Act, 1932 provides the following rules for the settlement of accounts between the partners:

(a) Payment Of Losses: [Section 48 (a)] Losses shall be paid first out of profits, next out of capital and lastly, if necessary, by the partners individually in their profit-sharing ratio.

(b) Distribution Of Assets: [Section 48 (b)] Assets of the firm are first to be applied in paying the debts of the firm to the third parties; next in paying to each partner rateably what is due to him from the firm for advances as distinguished from capital; in paying to each partner rateably what is due to him on account of capital, and the residue to be divided among the partners in the proportion in which they were entitled to share profits.

Distinction Between Dissolution Of Partnership And Dissolution Of Firm

| S.No. | Basis Of Difference | Dissolution Of Partnership | Dissolution Of Firm |

|---|---|---|---|

| 1. | Change in economic relation | The economic relations of partnership among different partners are changed. | The economic relations among all the partners come to end. |

| 2. | Termination of business | The business of the firm is not terminated. | The business of the firm is closed. |

| 3. | Assets and Liabilities | Assets and liabilities are revalued and new balance sheet is drawn. | Assets are sold and realised and liabilities are paid off. |

| 4. | Closure of books of accounts | It does not require the closing of books because the business is not terminated. | All books of accounts are closed. |

| 5. | Implication | It does not imply dissolution of the firm. | It implies dissolution of the partnership and the firm. |

Settlement Of Firm's Debts And Private Debts: (Section 49) Firm's debts are the debts incurred by the firm whereas private debts are incurred by partners under their individual capacity.

- Firm's assets are first utilized for settlement of firm's debt and the surplus (if any) is applied towards payment of partner's private debts to the extent of his share in profits of the firm.

- Private debts of the partners are first paid out of private property of the partners and the surplus if any thereafter, is used to pay off the firm's debts.

Realisation Account: Realisation Account is opened on dissolution of firm to close down the books of accounts of the firm. This account is a nominal account. The purpose of this account is to show the profit or loss on realisation of assets and payment of liabilities.

Format Of Realisation Account

| Dr. | Realisation Account | Cr. | |

|---|---|---|---|

| Particulars | (?) | Particulars | (?) |

| To Assets (excluding Cash/Bank balance, fictitious assets, debit balance of P&L A/c, debit balance of Partners' Capital/Current Accounts, Loan to Partner) | By Liabilities excluding credit balance of P&L A/c, Reserves (not representing assets), Partners' Capital/Current Accounts, Loan from Partner Provision on any asset (such as Provision for Doubtful Debts, Provision for Depreciation etc.) | ||

| To Bank/Cash A/c (i) (amount paid for discharging liabilities) (ii) (amount paid for unrecorded liabilities) (iii) (expenses on realisation) | By Bank/Cash A/c (i) (amount received on realisation of assets) (ii) (amount received from unrecorded assets) |

| Dr. | Realisation Account | Cr. | |

|---|---|---|---|

| To Partner's Capital A/c (for liability taken over by a partner or any expenses paid by him or remuneration/commission payable to him) | By Partner's Capital A/c (asset taken over by a partner) | ||

| To Partners' Capital A/cs (for transferring profit on realisation) | By Partners' Capital A/cs (for transferring loss on realisation) |

Distinction Between Realisation Account And Revaluation Account

| S.No. | Basis Of Difference | Realisation Account | Revaluation Account |

|---|---|---|---|

| 1. | Time of preparation | This account is prepared at the time of dissolution of firm. | This account is prepared at the time of admission, retirement or death of a partner. |

| 2. | Object | This account is prepared to find out the profit or loss on realisation of assets and payment of liabilities. | This account is prepared to find out the profit or loss on revaluation of assets and liabilities. |

| 3. | Amount | Assets and liabilities are shown in this account at their book value. | The amount of increase or decrease in the value of assets and liabilities are shown in this account. |

| 4. | Expenses | Usually dissolution expenses are shown in this account. | No expenses are shown in this account. |

Unrecorded Assets And Liabilities: These refer to those assets and liabilities that do not appear in the books of accounts at all but they do exist otherwise because they being written off or omitted to have been recorded. At the time of dissolution, for unrecorded assets and liabilities, the accounting entries passed will be as follows:

Unrecorded Assets

When the assets are sold for cash:

Cash/Bank A/c Dr.

To Realisation A/c

When an asset is taken over by a partner:

Concerned Partner's Capital A/c Dr.

To Realisation A/c

Unrecorded Liabilities

When the liabilities are settled:

Realisation A/c Dr.

To Cash/Bank A/c

When a partner agrees to pay off a liability:

Realisation A/c Dr.

To Concerned Partner's Capital A/c

Treatment Of Reserves And Accumulated Profits: The undistributed profits and losses and reserves are always transferred to partners' capital accounts in their profit sharing ratio and not to the realisation account.

For Distribution Of Reserves Or Accumulated Profits

General Reserve Dr.

Reserve Fund Dr.

Profit and Loss A/c Dr.

To Partners' Capital A/cs (in profit-sharing ratio)

(Being undistributed profits and reserves transferred to partners' capital accounts)

For Distribution Of Accumulated Losses

Partners' Capital A/cs Dr.

To Profit and Loss A/c

(Being undistributed losses transferred to partners' capital accounts)

Partner's Loan Account: If a partner has given any loan to the firm, first of all, it will be shown on the credit side of partner's loan account. When all the outside liabilities are paid in full, afterwards this loan will be paid. Thus, partner's loan account is prepared separately and paid off by passing the following entry:

Partner's Loan A/c Dr.

To Cash/Bank A/c

(Being partner's loan paid off)

Notes:

(1) Partner's loan account is prepared before partners' capital accounts because at the time of dissolution, capitals are paid off only if any balance is left after payment of partner's loan.

(2) Loan from a relative of a partner is an external liability and is paid through Realisation Account.

(3) Partner's loan is transferred to Capital Account and not paid directly through Cash/Bank A/c of that partner having a debit capital balance.

Treatment Of Goodwill: In case of dissolution of a firm, goodwill should be treated just like other assets. If nothing is mentioned about the realisation of goodwill, it can be assumed that the goodwill is valueless and as such, nothing is received or realised from it.

Cash Or Bank Account: All the receipts are recorded on the debit side and all the payments are recorded on the credit side of cash account. At the time of dissolution, this account is closed at last and total of both the sides (Dr. and Cr.) must be equal. It means all accounts are closed. Thus, this account also helps in the verification of the arithmetical accuracy of the accounts at the time of dissolution. If both cash and bank balance are given in the balance sheet, only one account, either a cash account or a bank account is prepared. If cash account is prepared, an entry is made for withdrawing the bank balance and if a bank account is prepared, an entry is passed for depositing the cash balance into bank which are as follows:

(i) For cash deposited into bank:

Bank A/c Dr.

To Cash A/c

(ii) For cash withdrawn from bank:

Cash A/c Dr.

To Bank A/c

Treatment Of Realisation Expenses: Process of dissolution of a firm incur some expenses which are known as realisation or dissolution or liquidation expenses. Normally it is paid by the firm, but a partner may bear these expenses in lieu of commission/remuneration. Journal Entries for various situations are as follows:

1. Realisation Expenses Are Borne And Paid By The Firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being realisation expenses paid)

2. When Realisation Expenses Are Borne By The Firm But Paid By A Partner On Firm's Behalf:

Realisation A/c Dr.

To Concerned Partner's Capital A/c

(Being realisation expenses paid by partner on behalf of the firm)

3. When A Partner Receives A Specific Amount Or Commission/Remuneration For Undertaking Dissolution Work And The Partner Is To Bear The Dissolution Expenses:

(i) For payment of a fixed amount to the partner

Realisation A/c Dr.

To Concerned Partner's Capital A/c

(Being remuneration due to the partner)

Please click the link below to download pdf file for CBSE Class 12 Dissolution Of A Partnership Firm.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 4 Dissolution of Partnership Firm Notes

Students can use these Revision Notes for Part 1 Chapter 4 Dissolution of Partnership Firm to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 1 Chapter 4 Dissolution of Partnership Firm Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 1 Chapter 4 Dissolution of Partnership Firm Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 1 Chapter 4 Dissolution of Partnership Firm. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Dissolution Of A Partnership Firm Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Dissolution Of A Partnership Firm Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Dissolution Of A Partnership Firm Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Dissolution Of A Partnership Firm Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Dissolution Of A Partnership Firm Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.