Download the latest CBSE Class 12 Accountancy Analysis Of Financial Statements Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 2 Chapter 4 Analysis of Financial Statements

To secure a higher rank, students should use these Class 12 Accountancy Part 2 Chapter 4 Analysis of Financial Statements notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 2 Chapter 4 Analysis of Financial Statements Revision Notes for Class 12 Accountancy

Financial Statements: Financial statements are the end products of accounting process, which reveal the financial results of a specified period and financial position as on a particular date. These statements include income statement and balance sheet. The basic objective of these statements is to provide information required for decision making by the management as well as other outsiders who are interested in the affairs of the undertaking. Section 129 of as per

Schedule III to the Companies Act, 2013 every year.

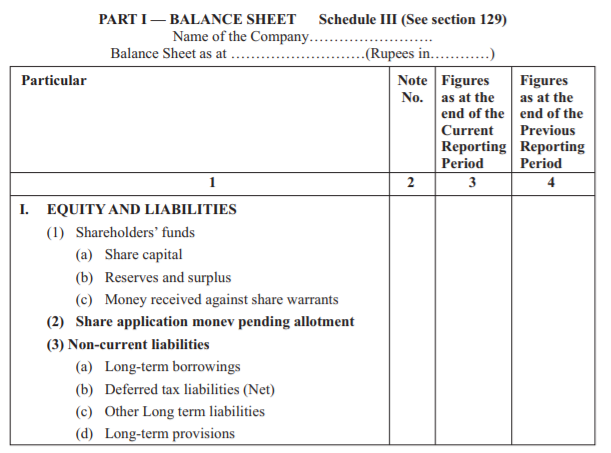

1. Balance Sheet: The balance sheet shows all the assets owned by the concerned, all the obligations or liabilities payable to outsiders or creditors and claims of the owners on a particular date.

2. Income statement or Statement of Profit and Loss : The Income Statement or Profit and Loss is prepared for theperiod (12 months) to determine the operational results of an undertaking. It is a statement of revenue earned and the expenses incurred for earning the revenue.

3. Notes to Accounts. (Balance Sheet & Statement of Profit and Loss) supported by the notes in which details of items is given

4. Cash Flow Statement. Cash flow statement provides information changes in cash and cash equivalents of an enterprise by classifying cash flows into operating, investing and financingactivities for a particular period of time i.e financial year as per AS-3.

ØEmployee Benefit Expenses- Expenses payment made to and for the benefits of the employees. Example- Wages, Salaries, Bonus, Leave encashment, Staff welfare expenses, ESOP expenses are shown in the notes to Accounts on Employee Benefit Expenses and total of these is shown on the face of the statement of Profit and Loss against Employee Benefit Expenses.

ØFinance Cost-Means cost incurred by the company on the borrowings i.e loan processing fee, discount if issues of debenture written off, premium payable of redemption of debenture, interest paid on bank overdraft.

ØBank charges are not a finance cost they come under other expenses as they are expenses on service availed from bank.

Q.1. List any three items that can be shown as contingent Liabilities in a company's Balance sheet.

Ans: (i) Claims against the Company not acknowledged as debts. (ii) Uncalled Liability on partly paid shares.

(iii) Arrears of Dividend on Cumulative preference shares.

Q.2. How is a Company's balance sheet different from that of a Partnership firm? Give two point only?

Ans. (i) For company's Balance Sheet there is a standard forms prescribed under the companies Act.2013 .Whereas, there is no standard form prescribed under the Indian partnership Act, 1932 for a partnership Firms balance sheet.

(ii) In case of a company's Balance sheet previous year's figures are required to be given whereas it is not so in the case of a partnership firms balance sheet.

Q.3. How does analysis of financial statements suffer from the limitation of window dressing?

Ans. Analysis of financial statements is affected from the limitation of window dressing as companies hide some vital information or show items at incorrect value to portray better

profitability and financial Position of the business, for example the company may overvalue closing stock to show higher profits.

Q.4. Operating Cycle and The period when payment is made given below, how will you classify the liabilities.

Introduction To Financial Statements Analysis

1. Financial Statement Analysis

Financial statement analysis is the systematic numerical representation of the relationship of one financial fact with the other to measure the profitability, operational efficiency, solvency and the growth potential of the business.

2. Types Of Financial Statement Analysis

- External analysis

- Internal analysis

- Horizontal analysis

- Vertical analysis

- Long-term analysis

- Short-term analysis

3. Process Of Financial Statement Analysis

- Rearrangement of data

- Comparison

- Analysis

- Interpretation

4. Importance Or Objectives Of Financial Statement Analysis

- Judging the operational efficiency of the business.

- Measuring the profitability.

- Measuring short-term and long-term financial position.

- Indicating the trend of achievements.

- Assessing the growth potential of the business.

- Inter-firm comparison

5. Uses Or Advantages Of Financial Statement Analysis

- Security analysis

- Credit analysis

- Debt analysis

- Dividend decision

- General business analysis

6. Limitations Of Financial Statement Analysis

- Financial statement analysis ignores qualitative aspects like quality of management, labour force and public relations.

- Suffering from the limitations of financial statements, which are as follows:

- Financial statements are historical in nature.

- Financial statements do not show price level changes hence, affect the analysis also.

- The results obtained by analysis of financial statements may be misleading due to window dressing.

- Financial statements are affected by the personal ability and bias of the analyst.

7. Parties Interested In Financial Statement Analysis And Their Areas Of Interest

The analysis of financial figures contained in the company's profit and loss account and balance sheet by employing appropriate techniques is known as a financial statement analysis. Financial statement analysis is useful to different parties to obtain the required information about the organization. Following are the parties interested in financial statement analysis.

- Shareholders: Shareholders are interested in financial statement analysis to know the profitability of the organization. Profitability shows the growth potentiality of an organization and safety of investment of shareholders.

- Investors And Lenders: Investors and lenders are interested to know the solvency position of an organization. They analyze the financial statement position to know about the safety of their investment and ability to pay interest and repayment of principal amount on the due date.

- Creditors: Creditors are interested in analyzing the financial statements in order to know the short term liquidity position of an organization. Creditors analyse the financial statement to know whether the organization is enabled to pay the amount of short term liabilities on the due date.

- Management: Management is interested in analyzing the financial statement for measuring the effectiveness of its policies and decisions. It analyzes the financial statements to know short term and long term solvency position, profitability, liquidity position and return on investment from the business.

- Government: Government is interested in analyzing the financial position in determining the amount of tax liability. It also helps for formulating effective plans and policies for economic growth.

Tools Of Financial Statements Analysis

There are different tools of financial statements analysis available to the analyst. The following tools are used to measure the operational efficiency and financial soundness of an enterprise.

The most common used techniques of financial analysis are:

- Comparative financial statements

- Common size statements

- Ratio analysis

- Cash flow statements

1. Comparative Financial Statements

Statements used to compare the items of income statement i.e. profit and loss account and position statement i.e. balance sheet for ascertaining the trend of the performance and profitability of an enterprise are known as comparative financial statements.

Comparative Income Statement

Income statements provide the details about the results of the operations of the business, and comparative income statements provide the progress made by the business over a period of a few years. This statement also helps in ascertaining the changes that occur in each line item of the income statement over different periods.

The comparative income statement not only shows the operational efficiency of the business but also helps in comparing the results with the competitors, over different time periods. This is possible by comparing the operational data spanning multiple periods of accounting.

Points To Study When Analysing A Comparative Income Statement

- Compare the increase or decrease in sales with a relative increase in the cost of goods sold

- Studying the operational profits of the business

- Overall profitability of the business can be analysed by an increase or decrease in the net profit

Steps In Preparing A Comparative Income Statement

- Specify absolute figures of all the items related to the accounting period under consideration.

- Determine the absolute change that has occurred in the items of the income statement. It can be achieved by finding the difference between previous year values with the current year values.

- Calculate the percentage change in the items present in the current statement with respect to previous year statements.

Comparative Balance Sheet

Comparative balance sheet analyses the assets and liabilities of business for the current year and also compares the increase or decrease in them in relative as well as absolute parameters. A comparative balance sheet not only provides the state of assets and liabilities in different time periods, but it also provides the changes that have taken place in individual assets and liabilities over different accounting periods.

Points To Study When Analysing A Comparative Balance Sheet

- The present financial and liquidity position (study working capital)

- The financial position of the business in the long term

- The profitability of the business

Steps In Preparing A Comparative Balance Sheet

- Determine the absolute value of assets and liabilities related to the accounting periods.

- Determine absolute changes in the items of the balance sheet relative to the accounting periods in question.

- Calculate the percentage change in assets and liabilities by comparing current year values with values of previous accounting periods.

2. Common Size Statements

Common Size Income Statement

This is one type of common size statement where the sales is taken as the base for all calculations. Therefore, the calculation of each line item will take into account the sales as a base, and each item will be expressed as a percentage of the sales.

Use Of Common Size Income Statement

It helps the business owner in understanding the following points:

- Whether profits are showing an increase or decrease in relation to the sales obtained.

- Percentage change in cost of goods that were sold during the accounting period.

- Variation that might have occurred at expense.

- If the increase in retained earnings is in proportion to the increase in profit of the business.

- Helps to compare income statements of two or more periods.

- Recognises the changes happening in the financial statements of the organisation, which will help investors in making decisions about investing in the business.

Common Size Balance Sheet

A common size balance sheet is a balance sheet that displays both the numeric value and relative percentage for total assets, total liabilities, and equity accounts. Common size balance sheets are used by internal and external analysts and are not a reporting requirement of generally accepted accounting principles (GAAP).

Please click the link below to download CBSE Class 12 Accountancy Analysis of Financial Statements

Free study material for Accountancy

CBSE Class 12 Accountancy Part 2 Chapter 4 Analysis of Financial Statements Notes

Students can use these Revision Notes for Part 2 Chapter 4 Analysis of Financial Statements to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 2 Chapter 4 Analysis of Financial Statements Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 2 Chapter 4 Analysis of Financial Statements Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 2 Chapter 4 Analysis of Financial Statements. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Analysis Of Financial Statements Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Analysis Of Financial Statements Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Analysis Of Financial Statements Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Analysis Of Financial Statements Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Analysis Of Financial Statements Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.