Download the latest CBSE Class 12 Accountancy Accounting For Share Capital Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital

To secure a higher rank, students should use these Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 2 Chapter 1 Accounting for Share Capital Revision Notes for Class 12 Accountancy

Accounting for Share Capital

Company: It is

1. A Form of business organization

2. It is an Association of persons who provide capital

3. Is an artificial, invisible and intangible

4. Has separate legal identity

5. Has Perpetual existence

6. Has Common seal

7. is not affected by death , insolvency or insanity of individual

Private company:

According to section 3(1)(iii)

1. Has paid up capital of one lakh

2. Maximum number of members is 50

3. It restricts the right to transfer of shares

4. Prohibits any invitation to public to subscribe for shares and Debentures

5. Prohibits any invitation or acceptance of deposits from persons other than its members , directors or their relatives

PUBLIC COMPANY:

According to section 3(1)(iv)

1. Is not a private company

2. Has minimum paid up capital of 5 lakhs or higher as may be prescribed

3. Is a private company which is subsidiary of a company which is not a private company

GOVERNMENT COMPANY

As per section 617 is a company in which more than 50% of paid up capital is held by Central or State Government or both

FOREIGN COMPANY

Section 591of Act states this type of company is incorporated outside India but has established business in India.

Incorporation of company

There are 4 stages

1. Promotion -conceiving an idea of business

2. Incorporation or registration

3. Capital subscription which means raising capital

4. Commencement of business for which certificate of Commencement of business is to be obtained.

Some important definitions(theory questions)

MINIMUM SUBSCRIPTION : It is number of shares on which amount received is sufficient to commence business .

PROSPECTUS : It is an invitation to public for subscription of shares or debentures.

PRELIMINARY EXPENSES : are expenses incurred for incorporating the company are carried in balance sheet unless these are written off.

CAPITAL : means amount invested in the business for the purpose of earning revenue. In case of company money is contributed by public and people who contribute money are called shareholders.

SHARE CAPITAL: capital raised by issue of shares is called share capital.

AUTHORISED CAPITAL : Also Called as Nominal or registered capital .It is the maximum amount of capital a company can issue . It is stated in Memorandum of Association.

ISSUED CAPITAL : this is part of authorized capital which is offered to public for subscription. It cannot exceed authorized capital .

SUBSCRIBED CAPITAL : It is part of issued capital subscribed or applied by public.

CALLED UP CAPITAL : It is the amount of nominal value of shares that has been called up by the company for payment by the subscriber towards the share.

PAID UP CAPITAL : It is part of called up capital that the members of company or shareholders have paid.

Example : X Ltd. is registered with the following share capital 1,25,000 equity shares of Rs. 10 each, payable in the following manner 10% on application,20% on allotment ,30% on first call the balance on final call .

The company offered for subscription 80,000 equity shares .The public applied for 75,000 share The company duly allotted these shares .It made only first call by 31st March 2010.The first call was received on all shares except 300 equity shares. Prepare Balance Sheet of Company.

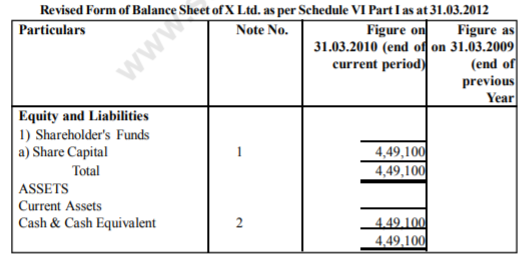

Disclosure of share capital in Company’s Balance Sheet

Note No. :1

Authorised Captial

1,25,000 equity shares @ ` 10 each 12,50,000

Issued Capital

80000 Equity Shares @ ` 10 each 8,00,000

Subscribed & Paid up

75000 eq. shares of @ ` 10 each

issued to public @ ` 6 4,50,000

Less : Unpaid calls 900 4,49,100

4,49,100

Note No. 2 : Amount received on application

75000 @ ` 1(10%) 75,000

Amount received on allotment 1,50,000

75000 sh @ ` 2(20%)

Amount Received on call 2,24,100

74700 Shares @ ` 3(30%)

4,49,100

RESERVE CAPITAL : It is that part of uncalled capital which the company reserve to be called only upon winding up of company. For this a special resolution has to be passed

CAPITAL RESERVE : It is capital profit not available for distribution as dividend.

It is represented in balance sheet of company as Reserves and Surplus under the heading Shareholders' Funds

CLASSES OF SHARES : There are two classes of shares

1. Preference shares

2. Equity shares

Equity shares : The shares which are not preference shares are called equity shares and do not get preference in above respect.

ISSUE OF SHARES

Shares can be issued in two ways

1. for cash

2. for consideration other than cash

Terms of issue of share : shares can be issued in three ways

1. Issue of shares at Par

2. Issue of shares at Premium

3. Issue of shares at Discount

Shares payable in Instalments

1. First instalment paid along with application is called as application money.

2. Second instalment paid on allotment is called as allotment money.

3. Subsequent instalment paid are called as call money calls can be more than one and called First call, second call or as the case may be

ISSUE OF SHARES FOR CASH AT PAR : This means shares are issued at face value Journal entries

NOTE : For each entry narration is compulsory as given in example below and carries marks columns are compulsory table should be made in proper format ( all columns are compulsory) after each entry in column of particulars line must be drawn.

Example : X Ltd. invited application for 10,000 shares of the value of Rs.10 each. The amount is payable as Rs.2 on application and Rs.5 on allotment and balance on First and Final call. Teh whole of the above issue was applied and cash duly recived. Give Journal entries for the above transaction.

In the Books of X Ltd.

Solution

ISSUES OF SHARES AT PREMIUM : It is issue of share at more than face value. (Section 78)

This premium can be utilised for

1. Issue of bonus shares

2. Write off preliminary expenses, discount, commission on issue of shares

3. Buy back of shares

4. Redemption of debentures o preference shares

Please click the link below to download pdf file for CBSE Class 12 Accounting for Share Capital.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital Notes

Students can use these Revision Notes for Part 2 Chapter 1 Accounting for Share Capital to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 2 Chapter 1 Accounting for Share Capital Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 2 Chapter 1 Accounting for Share Capital Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 2 Chapter 1 Accounting for Share Capital. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Accounting For Share Capital Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Accounting For Share Capital Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Accounting For Share Capital Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Accounting For Share Capital Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Accounting For Share Capital Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.