Download the latest CBSE Class 12 Accountancy Accounting For Companies Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital

To secure a higher rank, students should use these Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 2 Chapter 1 Accounting for Share Capital Revision Notes for Class 12 Accountancy

Company Accounts - Accounting for Share Capital Meaning of company: A company is an organization formed by an association of persons through a process of law for undertaking (usually) a business venture.

Definition –“Company means a company incorporated under this Act or any previous company -Section 2(20) of the Companies Act, 2013

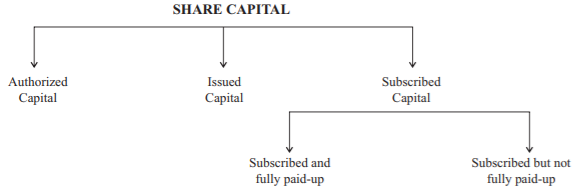

Share Capital - Schedule III of the Companies Act, 2013 classified Share Capital as:

i. Authorised Share Capital is the maximum amount up to which a company can issue shares.

ii. Issued share capital is a part of authorized share capital that is issued by a company for subscription.

iii. Subscribed share capital is a part of issued share capital that is subscribed. Subscribed share capital is shown as (i) Subscribed and fully paid – up (ii) Subscribed but not fully paid – up Called – up amount is the amount of nominal value of shares that has been called up for payment.

Paid – up amount is the amount that is received by the company.

Reserve capital is a part of subscribed share capital that a company resolves, by a special resolution, not to call except in the event and for the purpose of company being wound up.

PREFERENCE SHARES - These are the shares that carry preferential right as to dividend at fixed rate and preferential right as to repayment of capital.

EQUITY SHARES – These shares are the shares that are not preference shares. Shares can be issued

(i) for cash and

(ii) for consideration other than cash. Further, the shares can be issued (i) at par, or (ii) at premium.

OVER SUBSCRIPTION OF SHARES – It means shares applied for are more than the shares offered for subscription.

UNDER SUBSCRIPTION OF SHARES –It means shares applied for are less than the shares offered for subscription.

PRO RATA ALLOTMENT – It means allotment of shares in a fixed proportion. Pro rata allotment takes place only when the shares are oversubscribed

SECURITIES PREMIUM RESERVE – It can be utilized for the purpose prescribed in section 52(2) of the Companies Act, 2013, which are:

(i ) writing off preliminary expenses;

(ii) Writing off expenses such as share such as share issue expenses, commission ,discount allowed on issue of Securities ;

(iii) Providing for the premium payable on redemption of debentures or Preference Shares; or

(iv) in buying-back its own shares.

(v) Issuing fully paid bonus shares;

CALL – It is a demand by a company from the holders of partly paid shares to pay a further installment towards full nominal value.

CALLS-IN-ARREARS-It is the amount not yet received by the company against the call or calls demanded.

CALLS-IN –ADVANCE- It is the amount received by the company from its allottees against the calls not yet made. Calls- In- Advance is shown as 'Other Current Liability' under 'Current Liabilities'.

FORFEITURE OF SHARES- It means cancellation of shares and forfeiting the amount received against these shares. Forfeiture of shares takes place when a shareholder fails to pay the calls made.

Securities premium-How dealt when shares are forfeited. In case where Securities Premium Reserve Account has been credited and also it has been received-Securities Premium Reserve Account is not debited because of the restrictions imposed by Section52(2) of the Companies Act ,2013 as to utilization. In case Securities Premium Reserve Account has been credited but the amount has not been received –Securities Premium Reserve Account is debited because the amount has not been received and therefore Section 52(2) of the Companies Act ,2013 does not apply .

REISSUE OF FORFEITED SHARES-Forfeited Shares can be reissued and they may be reissued at a value lower than its face value. But the discount on reissue of a share cannot be more than the forfeited amount of that share credited to Forfeited Share account at the time of forfeiture .

Regarding Reissue of Forfeited Shares, always keep in mind that:

1. Discount on reissue cannot exceed the forfeited amount.

2. If the discount on reissue is less than the amount forfeited, the surplus (i.e., gain on reissue of shares) is transferred to Capital Reserve.

3. When only a part of the forfeited share is reissued then the gain on reissue of such share is such transferred to Capital Reserve.

4. The forfeited amount on shares not yet reissued is shown in the Balance Sheet as an addition to the paid-up share capital.

5. When the shares are reissued at discount, such discount is debited to Forfeited Shares Account.

6. If the shares are reissued at a price which is more than the nominal (face) value of the shares, the excess amount is credited to Securities Premium Reserve Account.

7. In case of the Forfeited Shares are reissued at a price higher than the paid- up value ,the excess of issue price over paid up value is credited to 'Securities Premium Reserve

PRIVATE PLACEMENT OF SHARES- It refers to issue and allotment of shares to a selected group of persons. In other words, an issue, which is not a public issue but offered to a selected group of persons , is called Private Placement Of Shares.

EMPLOYEES STOCK OPTION PLAN (ESOP) - It is the plan for granting options to subscribe shares by employees and employee directors. A company may issue stock (shares) options fulfilling the following conditions:

(a) These shares are of the same class of shares already issued;

(b) It is authorized by a special resolution passed by the company;

(c) The resolution specifies the number of shares, the current market price, consideration, if any, and the class or classes of directors or employees to whom such equity shares are to be issued;

(d) Not less than one year has, at the date of issue, elapsed since the date on which the company had commenced business and

(e) These shares are issued in accordance with SEBI regulations, if the shares are listed.

Presentation of Share Capital in Company's Balance Sheet As per Schedule III of Companies Act 2013, Share Capital is to be disclosed in a Company's Balance Sheet in the following manner :

EXTRACT OF BALANCE SHEET OF …………… as at……………………..

Journal Entries Regarding Issue of Shares Capital

1. ISSUE OF SHARES FOR CASH

(i) Shares Payable in Lump Sum :

For Receiving Share Application Money:

Bank a/c ….Dr. To Share Application and Allotment a/c

(Being the application money received) For Allotment of Shares:

Share Application and Allotment a/c …….Dr

To Share Capital a/c [With Nominal (face) Value] To Securities Premium Reserves a/c [With Premium Amt]

(Being the shares against share application and allotment money received)

(ii) Shares Payable in Installments :

Accounting Entries in Case of Over subscription

1. For Application Money Received

Bank A/c ……Dr

To Share Application A/c

Application Money For Allotted Shares

Share Application A/c ……Dr

To Share Application A/c

2 Excess Application Money

a) Refund

Share Application A/c ……Dr

To Bank A/C

b) Adjustment

Share Application A/c ……Dr

To Share Allotment A/c

To Calls – in- Advances A/c

Combined Entry

Share Application A/c ……Dr

To share Capital A/c

To Bank A/c

To Share Allotment A/c

To Calls- in – Advance A/c

SHARE ISSUED FOR CONSIDERATION OTHER THAN CASH

The journal entries passed are:

(a) On Purchased of Assets

Sundry Assets A/cs (Individually) …Dr

[With the amount of purchase price] To Vendor’s A/c [With purchase consideration]

(b) On Purchase of Business

Sundry Assets A/cs …Dr [Agreed value of assets] Goodwill A/c* ….Dr

To Sundry Liabilities A/c [Agreed value of liabilities]

To Vendor’s A/c ** [With purchased consideration] To Capital Reserve A/c***

Note: Purchasing consideration is an amount paid by purchasing company in consideration for purchase of assets /business from other enterprise. It may be given in the question otherwise it will be equal to net assets, i.e, sundry assets minus sundry liabilities.

*If purchase consideration given is more than net assets, then the difference is debited in Goodwill Account.

Please click the link below to download CBSE Class 12 Accountancy Accounting for Companies

Free study material for Accountancy

CBSE Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital Notes

Students can use these Revision Notes for Part 2 Chapter 1 Accounting for Share Capital to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 2 Chapter 1 Accounting for Share Capital Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 2 Chapter 1 Accounting for Share Capital Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 2 Chapter 1 Accounting for Share Capital. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Accounting For Companies Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Accounting For Companies Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Accounting For Companies Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Accounting For Companies Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Accounting For Companies Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.