Download the latest CBSE Class 12 Accountancy Accounting For Partnership Firms Fundamentals Notes in PDF format. These Class 12 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 12 students.

Revision Notes for Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner

To secure a higher rank, students should use these Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Revision Notes for Class 12 Accountancy

Accounting for Partnership Firms

Fundamentals

According to Section4 of the Indian Partnership Act, 1932 :

"Partnership is the relationship between persons who have agreed to the share the profits of a business carried on by all or any one of them acting for all"

Features of Partnership

1. There must be at least two persons to form a valid partnership. Section 11 of the Indian Partnership Act, 1932 restrict the (maximum) number of partners to 10 for carrying on banking business and 20 for other kind of business.

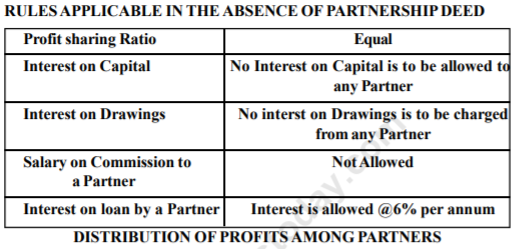

2. Partnership comes into existence by an agreement (either written or oral) among the partners. The written agreement among teh partners is called Partnership Deed.

3. A Partnership can formed for the purpose of carrying at sharing the profits or losses of the business

4. An agreement between the partners must be aimed at sharing the profits or losses of the business.

5. A partnership can be carried on by all or any one of them acting for all. PARTNERSHIP DEED

The partnership deed is a written agreement among the partners which contains the terms of agreement. A partnership deed should contain the following points:

1. Name and address of the firm.

2. Name and addresses of the partners.

3. Nature of the business

4. Terms of Partnership

5. Capital contribution by each partner.

6. Interest on capital

7. Drawings and interest on drawings.

8. Profit sharing ratio

9. Interest on loan.

10. Partner's Salary/commission etc.

11. Method for valuation of goodwill

6 Accountancy&XII

12. Accounting period of the firm

13. Rights and duties of partners.

Benefits of Partnership deed

(1) Helps to avoid dispute in future

(2) It is an evidence in the court

(3) Facilitates functioning of business by avoiding misunderstanding

A Profit and Loss Appropriation Account is prepared to show the distribution of profits among partners as per the provision of Partnership Deed (or as per the provision of Indian Partnership Act, 1932 in the absesnce of Partnership Deed). It is an extension of Profit and Loss Acccount. It is nominal account.

The Journal Entries regarding Profit and Loss Appropriation Account are as follows:

1. For transfer of balance of Profit and Loss Account

Profit and Loss A/c Dr.

To Profit and Loss Appropriation A/c

(Being net profit transferred to P & L Appropriation A/c)

2. For Interest on Capital

1. For allowing Interest on capital

Interest on Capital A/c

To Partners' Capital/Current A/cs

(Being interest on capital allwoed @ ___ % p.a)

2. For transferring Interest on Capital to Profit and Loss Appropriation

Profit and Loss Appropriation A/c Dr.

To Interest on Capital A/c

(Being interest on capital transferre to P & L Appropriation A/c)

3. For Salary of Commission payable to a partner

i. For allowing Salary or Commission to a partner :

Partner's Salary/Commission A/c Dr.

To Partner's Capital /Current A/cs

(Being salary/commission payable to a partner)

ii. For transferring Partner's Salary/Commission A/c to Profit and Loss Appropriation A/c :

Profit and Loss appropriation A/c Dr.

To Partner's Salary/ Commission A/c

4. For transfer of Reserves :

Profit and Loss Appropriation A/c Dr.

To Reserve A/c

(Being reserve created)

5. For Interest on Drawings :

1. For charging interest on a partner's drawings :

Partner's Capital/Current A/c Dr.

To Interest on Drawings A/c

( Being interest on drawings charged @ ____%p.a.)

2. For transferring Interest on drawings to Profit and Loss Appropriation A/c : Dr.

Interest on Drawings A/c

To Profit and Loss Appropriation A/c

(Being interest on drawings transferred to P & L Apprpriation A/c)

6. For transfer to Profit (i.e. Credit Balance of Profit and Loss Appropriation Account

Profit and Loss Appropriation A/c Dr.

To Partners Capital A/cs

(Being profits distributed among partners)

SPECIMEN OF PROFIT AND LOSS APPROPRIATION ACCOUNT

Profit and Loss Appropriation Account

For the year ending on ________________

Partner's Capital Accounts : It is an account which represents the partner's interst in the business.

In case of partnership business, a separate capital account is maintained for each partner. The capital accounts of partners may be maintained by following any of the following two methods:

(1) Fixed Capital Accounts

(2) Fluctuating Capital Accounts

1. Fixed Capital Accounts

Under this method the following two accounts are maintained:

1. Capital Account

This account will always show a credit balance. Balance of Capital account remains fixed and only the following two transactions are recorded in the Fixed Capital Accounts:

* Additional Capital Introduced

* Capital Withdrawn or Drawings out of Capital

2. Current Account

The Current account may show a debit or credit balance. All the usual adjustments such as Interest on Capital, partner's salary/commission, drawings (out of profits), interest on drawings and share in profits or losses etc. are recorded in this account

Reconstruction Of Partnership: Admission Of A Partner

Basic Concepts

Meaning of Admission of a Partner: Admission of a partner is one of the modes of reconstitution of a partnership firm under which existing agreement comes to an end and a new one comes into existence by admitting a new partner. According to Section 31(1) of the Indian Partnership Act, 1932, a new partner can be admitted only with the consent of all the existing partners.

Rights acquired by the New Partner

(i) Right to share in assets: For this right, the new partner brings an agreed amount of capital either in cash or kind.

(ii) Right to share in profits: For acquiring this right, the new partner brings some amount which is known as a premium (or share of goodwill).

Accounting Adjustments required at the time of Admission of a New Partner: When a new partner is admitted into partnership firm, following adjustments have to be made in the books of the firm:

(i) New Profit-Sharing Ratio of all the Partners.

(ii) Sacrificing Ratio of the Old Partners.

(iii) Goodwill and its Treatment.

(iv) Treatment of Undistributed or Accumulated Profits/Losses and Reserves.

(v) Revaluation of Assets and Reassessment of Liabilities.

(vi) Adjustment of Partners' Capitals.

New Profit-sharing Ratio: The ratio in which all partners including new partner, share the future profits or losses of the business is called new profit-sharing ratio.

Calculation of New Profit-Sharing Ratio

Case I: Only New Partner's Share being Given: If the share of new partner is given in the question, then in the absence of any other agreement, it is presumed that the old partners will continue to share the remaining profit in the old profit-sharing ratio.

In this situation after deducting the share of the new partner, the balance of the share is divided among old partners in their old ratio. This gives us new shares of the old partners.

Case II: Fixed Proportionate Contribution by Old Partners for New Partner: When new partner obtains his share from the old partners in a certain ratio, the new profit-sharing ratio of the old partners will be calculated after deducting the sacrifice made by the old partners from their existing share of profits.

Case III: Equal Proportionate contribution by Old Partners for New Partner: In this case, the new profit-sharing ratio of the old partners will be ascertained by deducting the sacrifice made by the old partners from their existing share of profit.

Case IV: New Partner's Share being Determined by Old Partners' Sacrifice: In this situation, the sacrifice of old partners in favour of new partner is given. Thus, the old partners' new share is determined by deducting the sacrificed share from their old share. The new partner's share is the total of sacrifices made by the old partners.

Sacrificing Ratio: Sacrificing Ratio is the ratio in which old partners sacrifice their share of profit in favour of incoming partner. It is calculated as:

Calculation of Sacrificing Ratio

Case I: Old and New Profit-Sharing Ratios Given: The new share of the old partner is deducted from his old share. This difference is known as sacrifice. The ratio in which the new partner is given the share by old partners is called the sacrificing ratio.

Case II: Old Profit-Sharing Ratio and New Partner's Share Given: When there is no information about sacrifices of old partners, in such condition the sacrificing ratio would be the old ratio.

Case III: Sacrifices of Old Partners' Given: In this case the relative sacrifice made by each partner in favour of the new partner is given. Thus, the ratio between given sacrifices will be the sacrificing ratio.

Case IV: Acquisition of Share by New Partner in a Given Proportion: In this case sacrifice is ascertained by distributing the share of the new partner in the agreed sacrificing ratio. Afterwards sacrifice of old partners is deducted from their old share to calculate new share.

Case V: Change in Relative Ratio between Old Partners in the New Firm: When old partners agree to share in different relative ratio in the new firm after the admission of the new partner, the combined share of the old partners in the new firm will be shared between them in new agreed relative ratio.

Accounting Treatment of Goodwill

At the time of admission of a new partner who is going to acquire the right to share in future profits must compensate the existing partners by making payment to them. This payment is called as premium or share of goodwill.

According to Accounting Standard 26 (AS-26), goodwill should be recorded in the books of accounts only when consideration in money or money's worth has been paid for it or for purchased goodwill. At the time of reconstitution of firm, i.e., admission, death or retirement of a partner or change in profit sharing ratio among partners, valuation of goodwill is made, so it should not be brought in books because it is inherent goodwill. The amount of goodwill should be adjusted through partners' capital/current accounts in their sacrificing ratio. Goodwill may be brought in cash or in any other kind.

Hidden (Inferred) Goodwill: Sometimes the amount of goodwill being brought in by the new partner is not clearly mentioned. The profits of current year and previous year are also not given. In such a case goodwill is calculated on the basis of profit-sharing ratio and capitalisation (Net worth) method.

Following steps will be taken for calculating hidden goodwill:

Step1: Ascertain the total/combined capital of old and new partners:

If different items of assets and liabilities are given, then total capital of the old partners will be the difference between assets and liabilities.

Capital = Assets (revalued) - Outside Liabilities (revalued)

Step 2: Find out the total capital of the new firm: For finding out the total capital of the new firm, new partner's capital is taken as the basis. For example, if new partner's capital for his 1/5th share is Rs.50,000, then total capital of the new firm will be 5 times of new partner's capital i.e., Rs.50,000 × 5 = Rs.2,50,000.

Step 3: Determination of goodwill: Excess of the capital of the new firm over the combined capital of old and new partners is assumed to be goodwill.

| Total capital of new firm on the basis of capital brought in by incoming partner (Incoming partner's capital × Reciprocal of share of incoming partner) | Rs. |

| Less: Net worth (excluding goodwill) of new firm | - |

| Value of goodwill | - |

Here, Net worth = Total Assets - Outside Liabilities

Or

Capital of partners + Net Accumulated Profit and Reserves (if any)

Note: Hidden goodwill never comes in the form of cash. It is always recorded by debiting new partner's current account.

Revaluation of Assets and Reassessment of Liabilities: Admission of a new partner involves revaluation of assets and liabilities as they are reassessed and their true values are arrived at. Over a period of time, values of assets and liabilities tend to increase or decrease because of several internal and external factors. Quite often it is observed that actual values of such items differ from those given in the Balance Sheet. Thus, in order to avoid a new partner from reaping benefits of increase in assets or decrease in value of liabilities and vice versa, a revaluation is undertaken. The profits or losses arising from this process are distributed amongst the old partners in their old profit-sharing ratio.

Accounting Entries on Revaluation

| 1. For increase in the value of assets | Assets A/c Dr. To Revaluation A/c (Being value of assets (by name) increased) |

| 2. For decrease in the value of assets | Revaluation A/c Dr. To Assets A/c (Being value of assets (by name) decreased) |

| 3. For increase in the value of liabilities | Revaluation A/c Dr. To Liabilities A/c (Being value of liabilities (by name) increased) |

| 4. For decrease in the value of liabilities | Liabilities A/c Dr. To Revaluation A/c (Being value of liabilities (by name) decreased) |

| 5. For unrecorded assets | Assets A/c Dr. To Revaluation A/c (Being unrecorded assets taken into account) |

| 6. For unrecorded liabilities | Revaluation A/c Dr. To Liabilities A/c (Being unrecorded liabilities brought into account) |

| 7. For profit on revaluation | Revaluation A/c Dr. To Old Partners' Capital A/cs (Being profit on revaluation credited to old partners' capital accounts in their old profit-sharing ratio) |

| 8. For loss on revaluation | Old Partners' Capital A/cs Dr. To Revaluation A/c (Being loss on revaluation debited to old partners' capital accounts in their old profit-sharing ratio) |

Please click the link below to download pdf file for CBSE Class 12 Accounting for Partnership Firms Fundamentals.

Free study material for Accountancy

CBSE Class 12 Accountancy Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Notes

Students can use these Revision Notes for Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 12. Our teachers always suggest that Class 12 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Summary

Our expert team has used the official NCERT book for Class 12 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 12. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Part 1 Chapter 2 Reconstitution of a Partnership Firm Admission of a Partner. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 12 Accountancy Accounting For Partnership Firms Fundamentals Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 12 students get the best study material for Accountancy.

Yes, our CBSE Class 12 Accountancy Accounting For Partnership Firms Fundamentals Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 12 Accountancy Accounting For Partnership Firms Fundamentals Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 12 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 12 Accountancy Accounting For Partnership Firms Fundamentals Notes, Class 12 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 12 Accountancy Accounting For Partnership Firms Fundamentals Notes, are available for immediate free download. Class 12 Accountancy study material is available in PDF and can be downloaded on mobile.