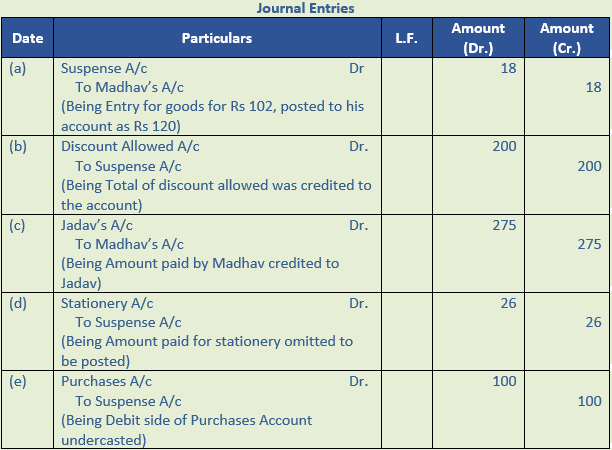

Access free DK Goel Solutions Class 11 Accountancy Chapter 19 Rectification of Errors 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 19 Rectification of Errors DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 19 Rectification of Errors Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 19 Rectification of Errors DK Goel Class 11 Solved Exercises

Numerical Questions

Question 1.

Solution 1:

Point of Knowledge:-

- Maintaining correct accounting records.

- Redrafting the Trial Balance with the rectified ledger balances.

- Preparation of correct Profit and Loss Account by using the rectified figures to find out the correct profit/loss as the case may be.

- Preparation of Balance Sheet with the rectified figures to depict the correct value of the assets and liabilities of the business.

Question 2.

Solution 2:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

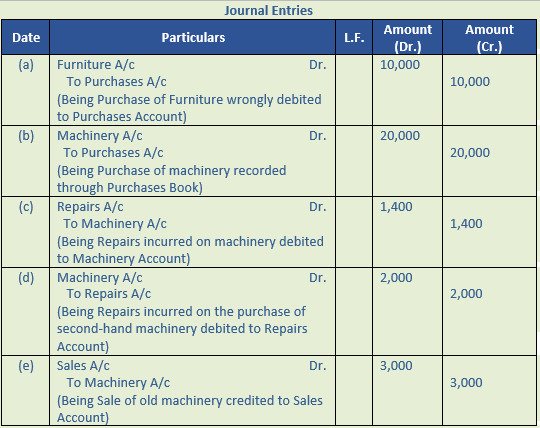

Question 3.

Solution 3:

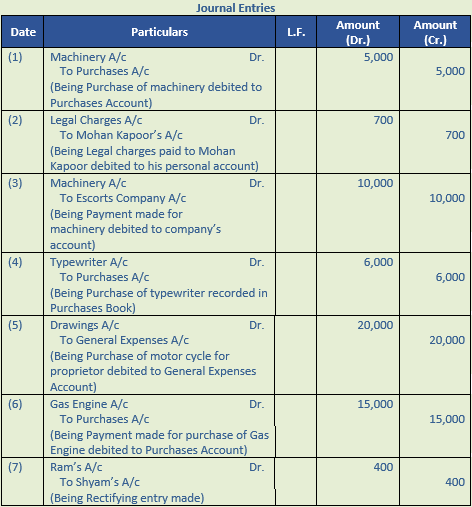

Question 4.

Solution 4:

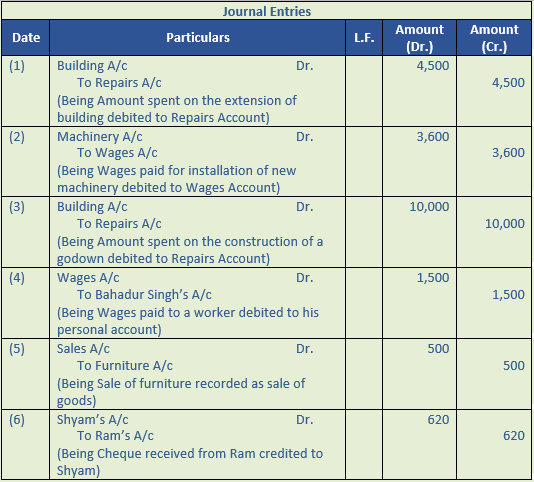

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

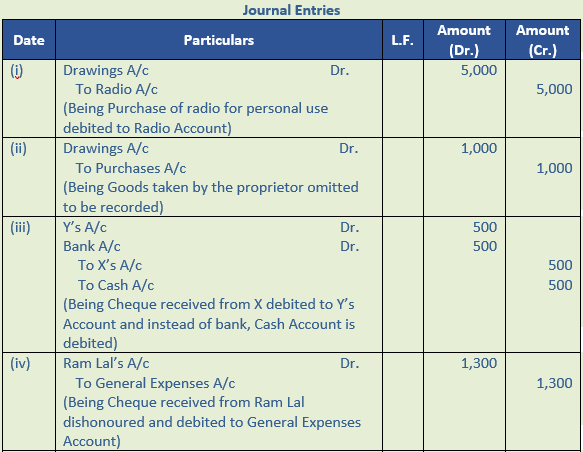

Question 5.

Solution 5:

Question 6.

Solution 6:

Question 7.

Solution 7:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 8.

Solution 8:

Question 9.

Solution 9:

Question 10.

Solution 10:

Question 11.

Solution 11:

Question 12.

Solution 12:

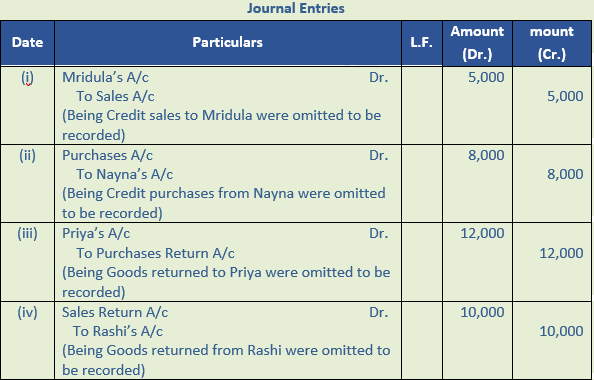

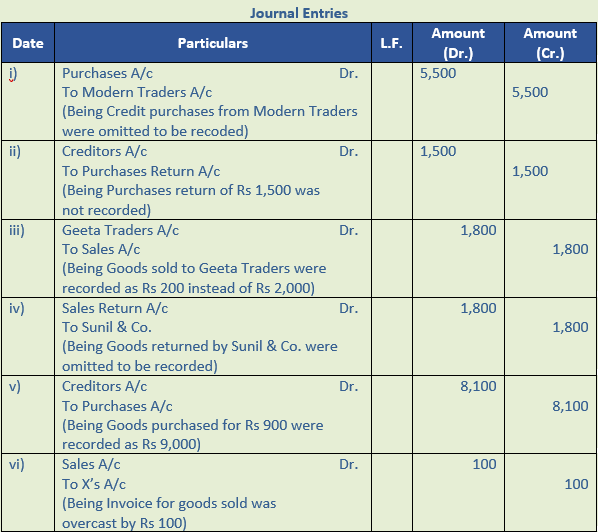

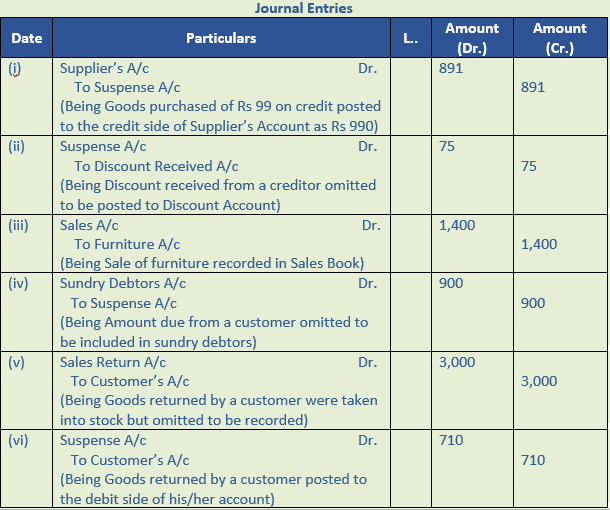

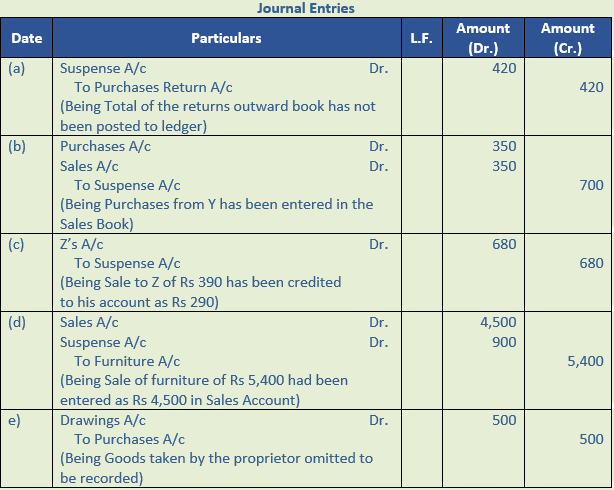

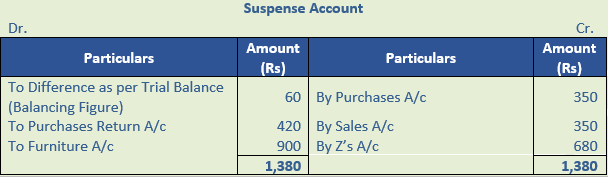

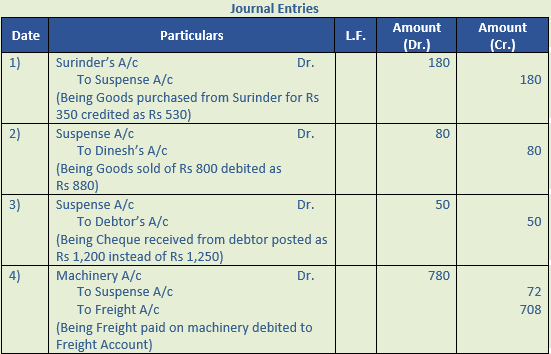

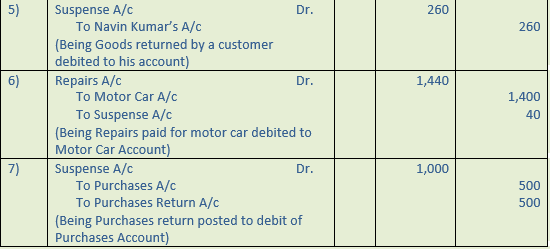

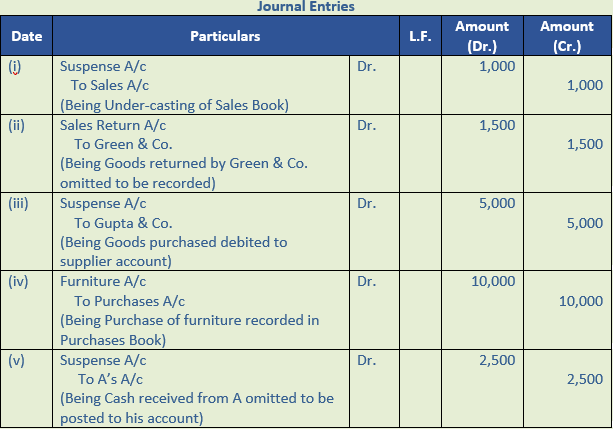

Question 13.

Solution 13:

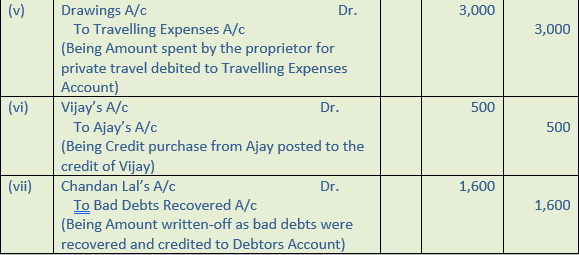

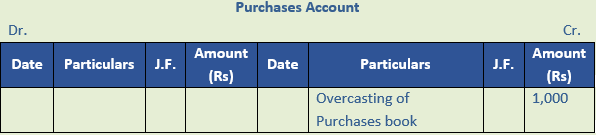

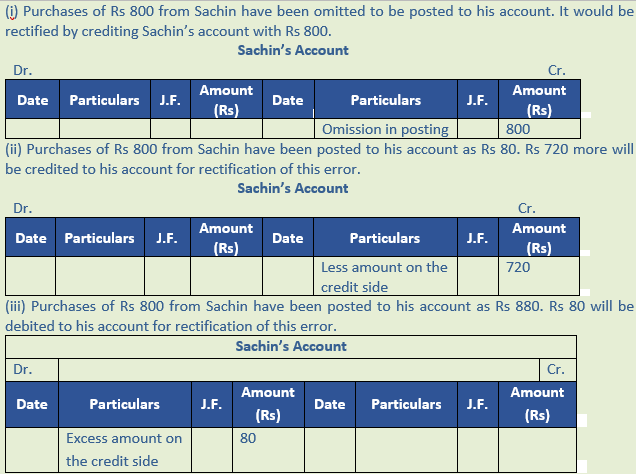

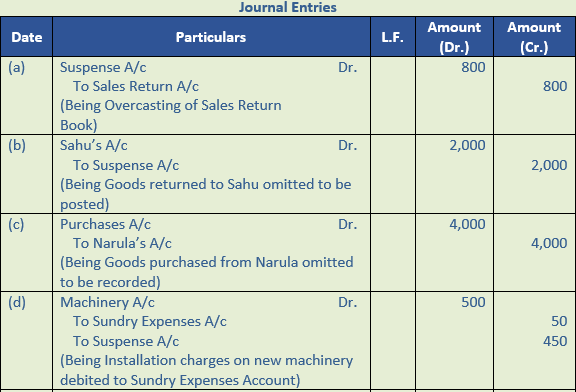

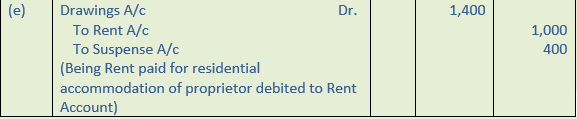

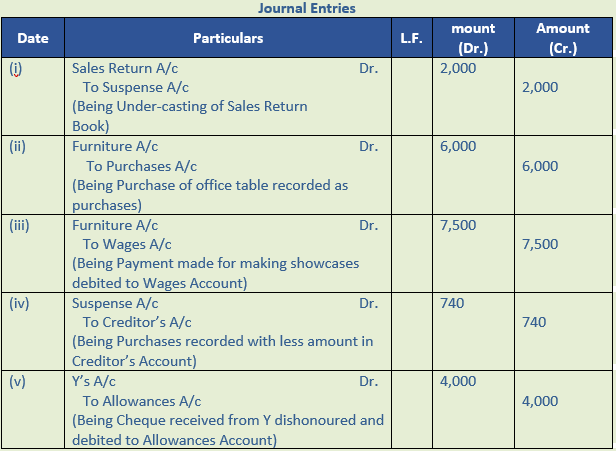

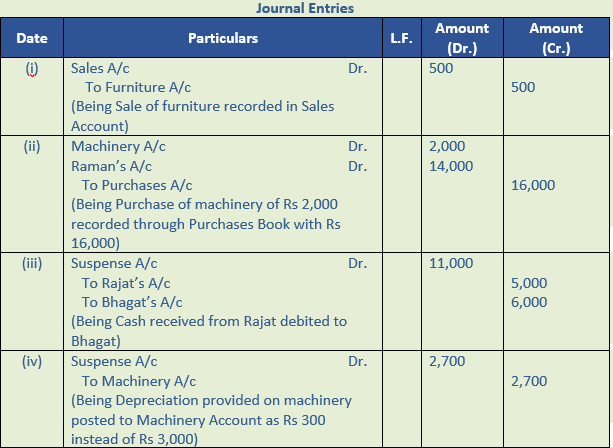

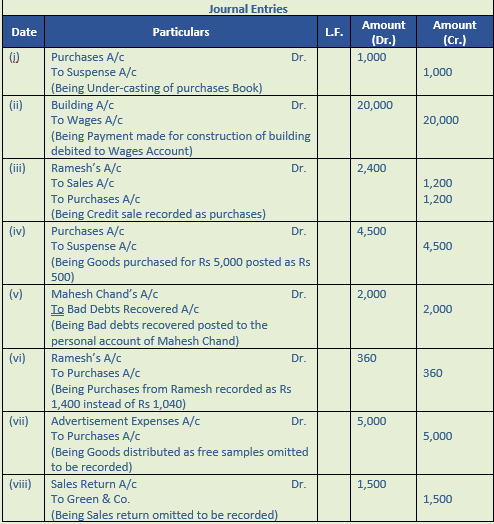

(i) Purchases Book has been over-casted by Rs 1,000. Purchases Account will be rectified by recording Rs 1,000 on the credit side of Purchases Account.

(ii) Purchases from Ram Rs 20,000 has been omitted to be posted to his account. To rectify this error Rs 20,000 should be posted on the credit side of Ram’s Account.

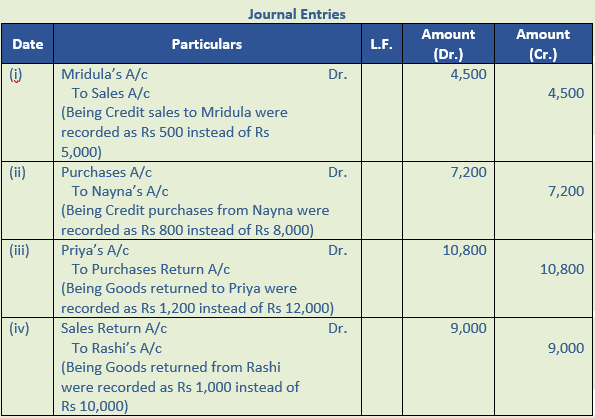

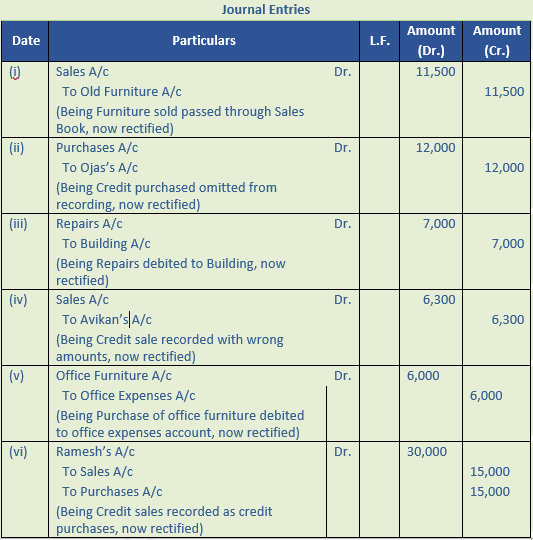

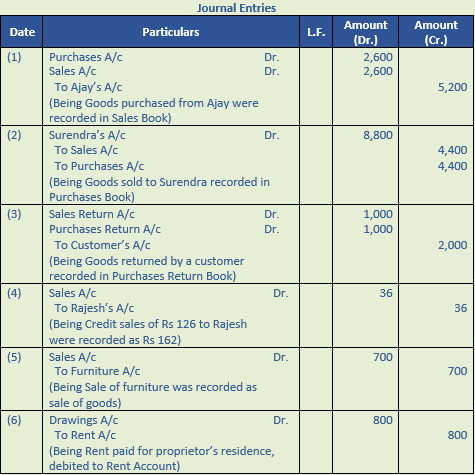

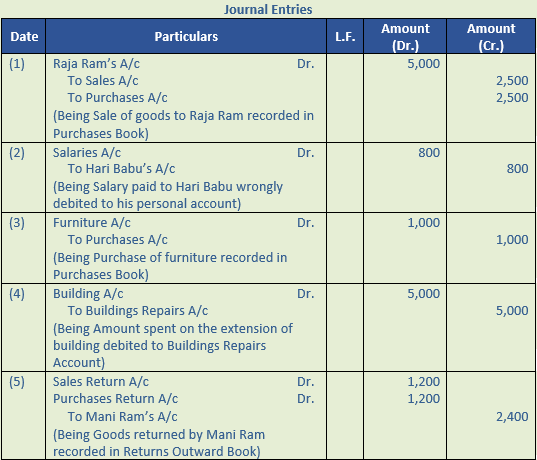

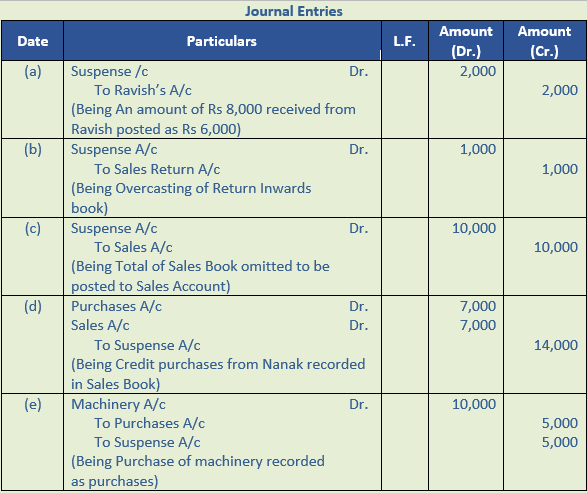

Question 14.

Solution 14:

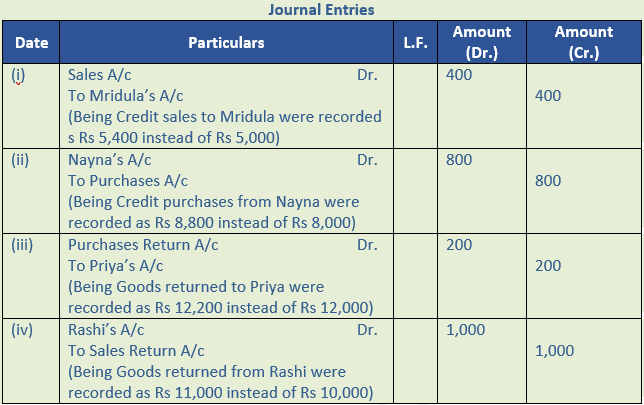

Question 15 (A).

Solution 15 (A):

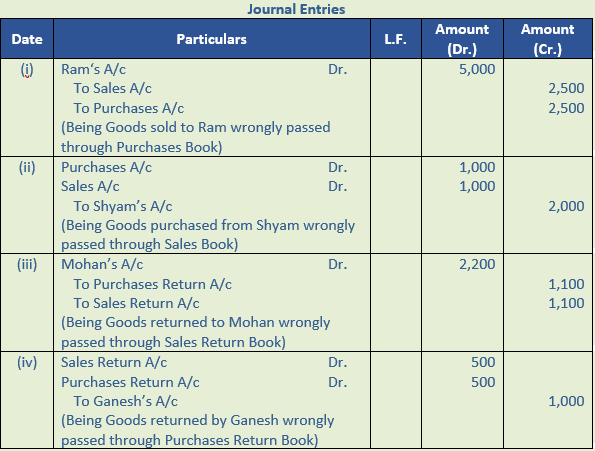

Question 15 (B).

Solution 15 (B):

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 16.

Solution 16:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 17.

Solution 17:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 18.

Solution 18:

Question 19.

Solution 19:

Question 20.

Solution 20:

Question 21.

Solution 21:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 22.

Solution 22:

Question 23.

Solution 23:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 24.

Solution 24:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 25.

Solution 25:

Question 26.

Solution 26:

Question 27.

Solution 27:

Question 28.

Solution 28:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 29.

Solution 29:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

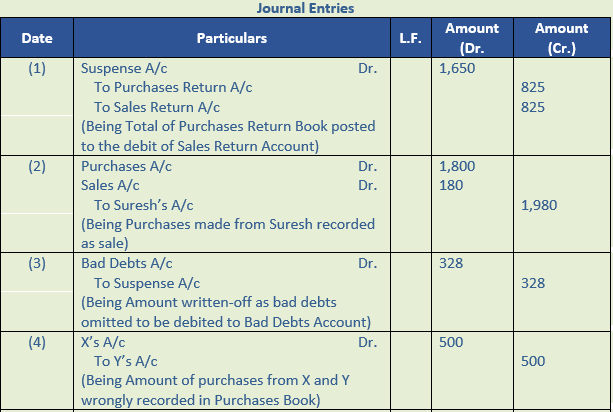

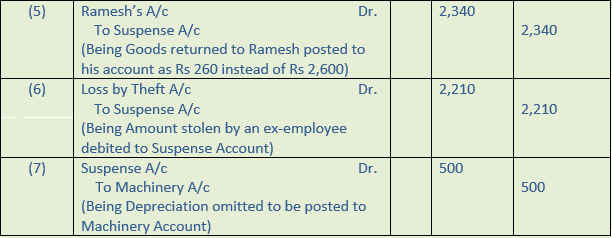

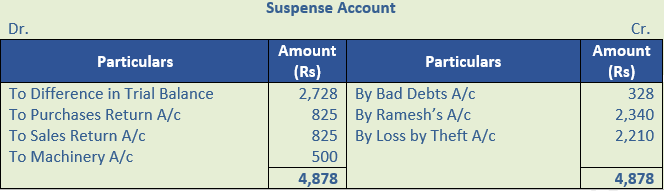

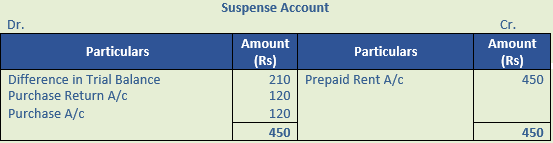

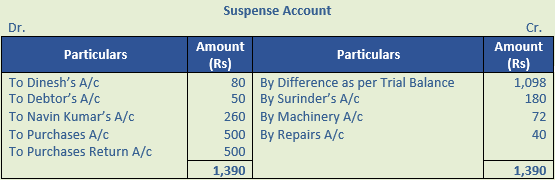

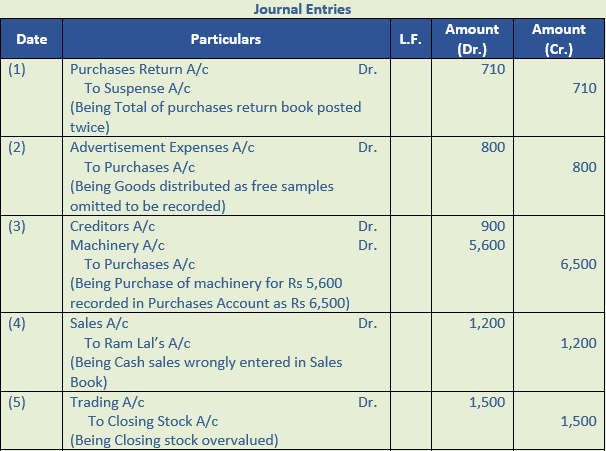

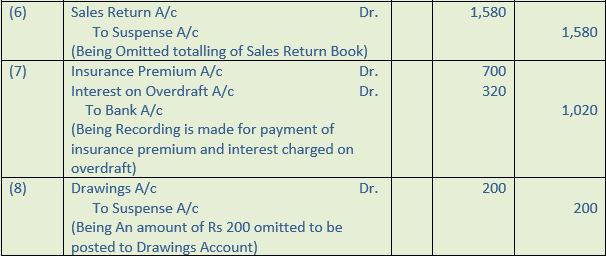

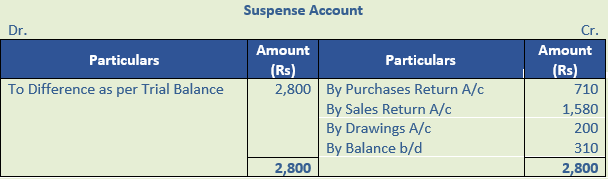

Question 30.

Solution 30:

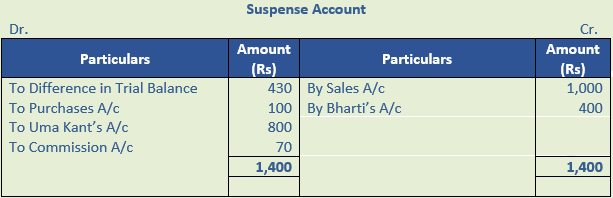

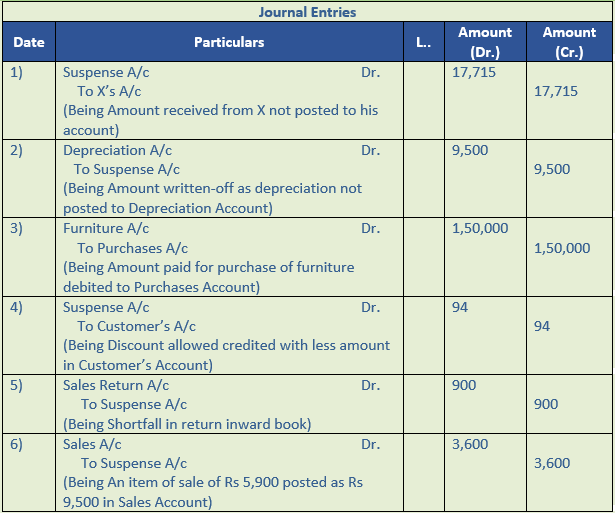

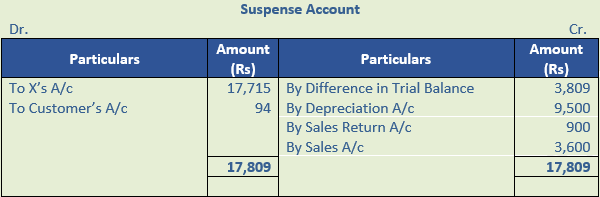

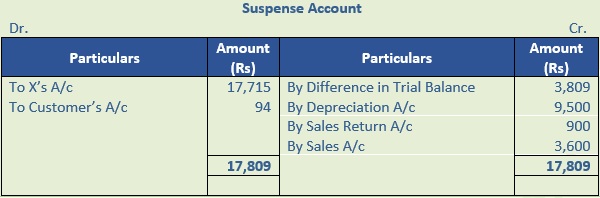

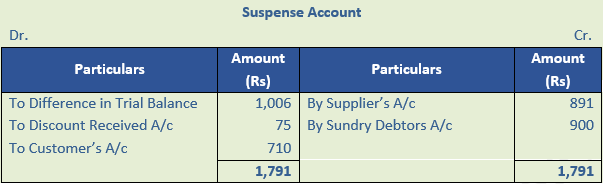

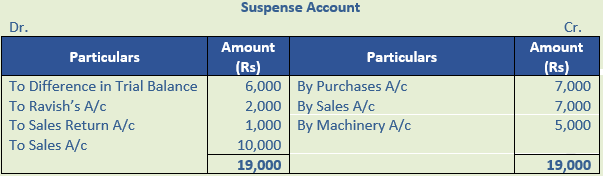

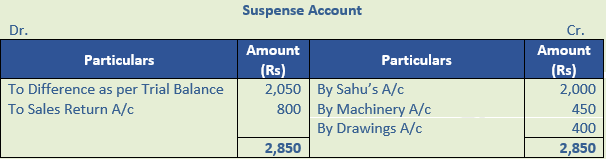

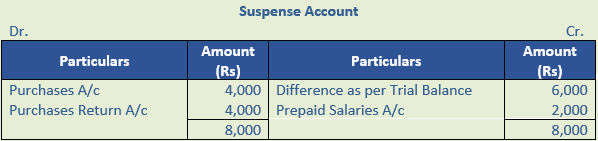

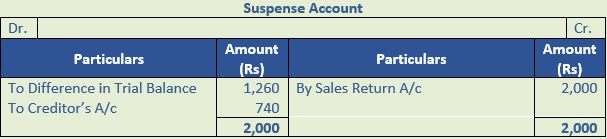

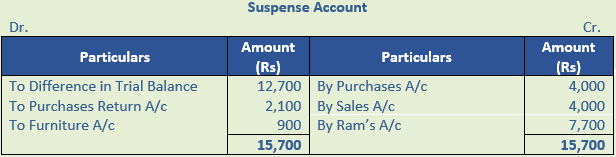

Point of Knowledge:-

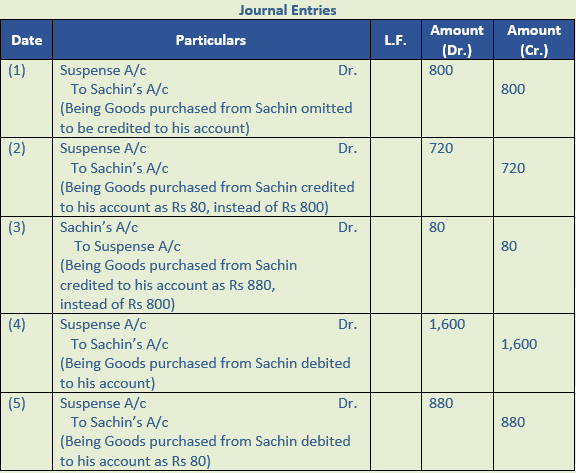

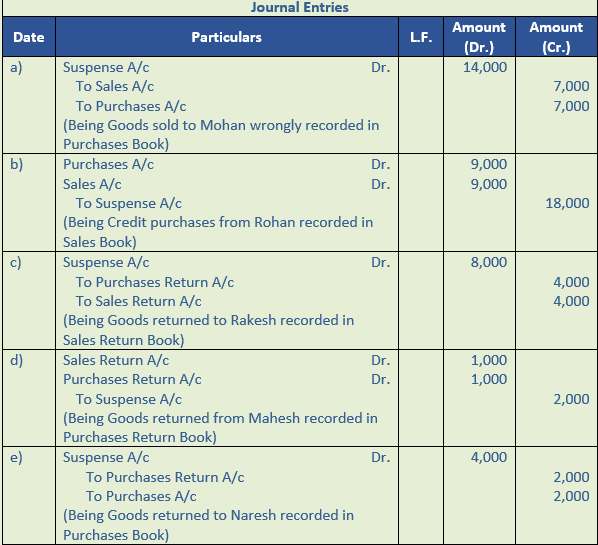

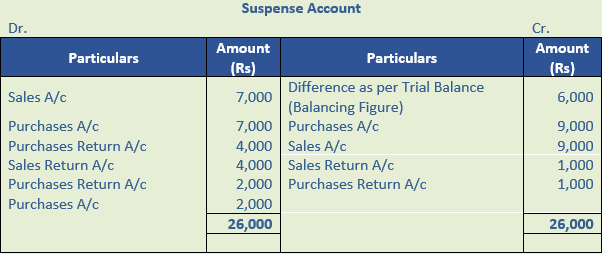

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

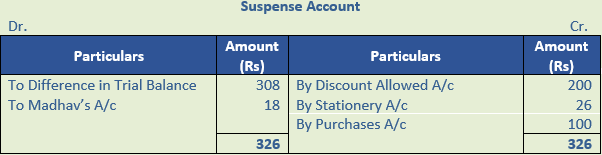

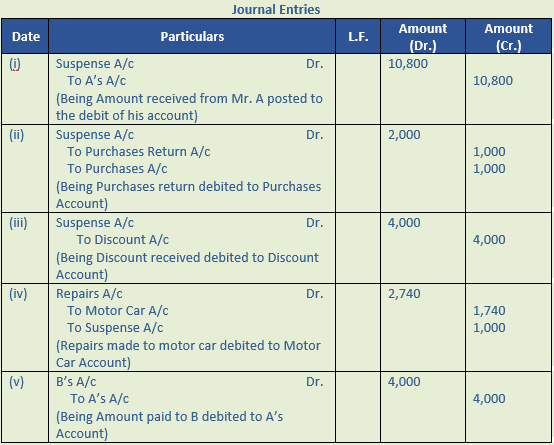

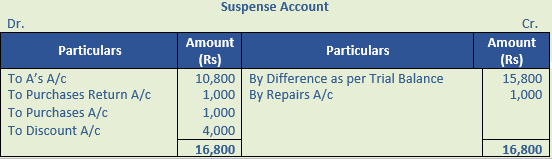

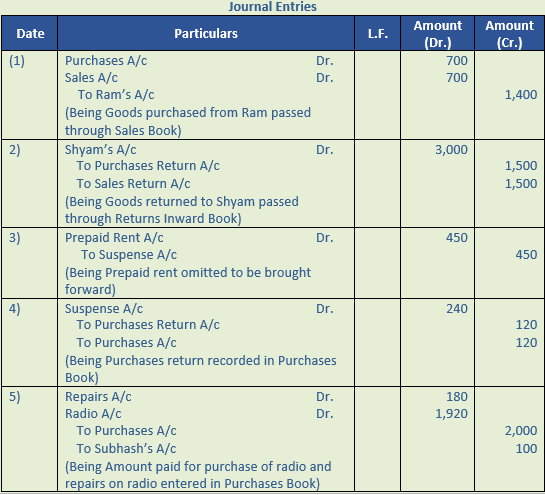

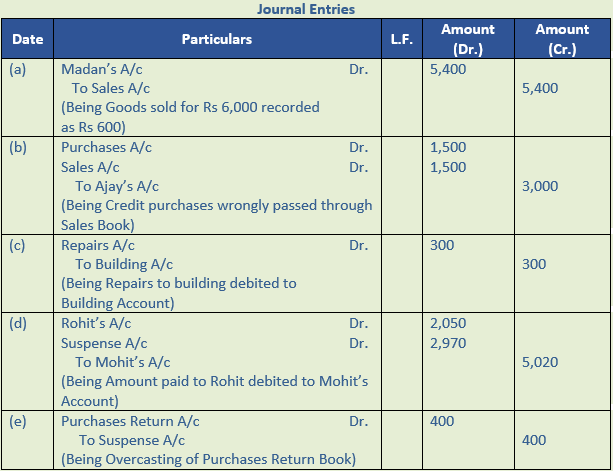

Question 31.

Solution 31:

Point of Knowledge:-

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

Question 32.

Solution 32:

Point of Knowledge:-

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

Question 33.

Solution 33:

Point of Knowledge:-

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

Question 34.

Solution 34:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 35.

Solution 35:

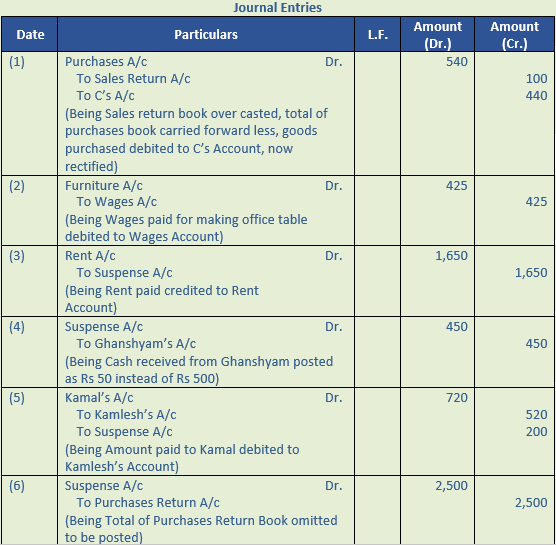

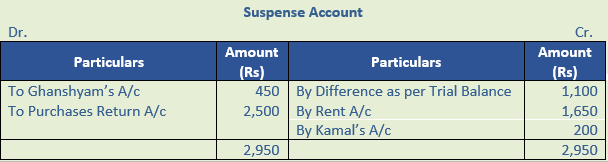

Point of Knowledge:-

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

Question 36.

Solution 36:

Point of Knowledge:-

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

Question 37.

Solution 37:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 38.

Solution 38:

Point of Knowledge:-

Errors may or may not affect the Trial Balance but it must be detected and rectified. The process of detecting errors and the procedure to correct the accounting records is called the rectification of errors.

Question 39.

Solution 39:

Point of Knowledge:-

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

Question 40.

Solution 40:

Point of Knowledge:-

- Errors of Omission

- Errors of Commission

- Errors of Principle

- Compensating Errors of omission and compensating errors do not affect the agreement of a Trial Balance.

Question 41.

Solution 41:

Point of Knowledge:-

Suspense Account is the account to which the difference in the Trial Balance is placed and it is opened when the Trial Balance doesn't match. The Suspense Account is placed in the debit side if the total debit amount is less than the total credit amount and vice versa. The Suspense Account is transferred to the asset side of the Balance sheet in case of a debit balance of a Suspense Account, otherwise transferred to the liabilities side of the in case of a credit balance. Suspense Account is used to rectify all one sided errors which affect the Trial Balance. Suspense Account is the net effect of one sided errors. Errors are rectified by entering the amount to the debit of the correct account and then credit is placed in the Suspense Account.

Question 42.

Solution 42:

Point of Knowledge:-

- Errors of Omission

- Errors of Commission

- Errors of Principle

- Compensating Errors of omission and compensating errors do not affect the agreement of a Trial Balance.

Question 43.

Solution 43:

Point of Knowledge:-

- Errors of Omission

- Errors of Commission

- Errors of Principle

- Compensating Errors of omission and compensating errors do not affect the agreement of a Trial Balance.

Question 44.

Solution 44:

Point of Knowledge:-

- Errors of Omission

- Errors of Commission

- Errors of Principle

- Compensating Errors of omission and compensating errors do not affect the agreement of a Trial Balance.