Access free DK Goel Solutions Class 11 Accountancy Chapter 20 Capital and Revenue 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 20 Capital and Revenue DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 20 Capital and Revenue Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 20 Capital and Revenue DK Goel Class 11 Solved Exercises

Very Short Answer Questions

Question 1.

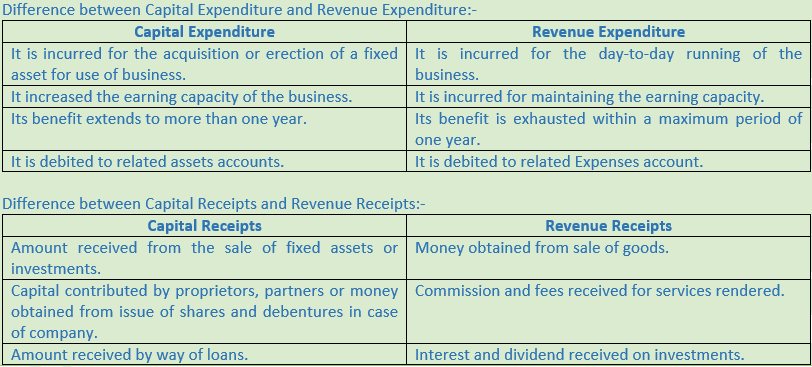

Solution 1: Any expenditure which is incurred in acquiring or increasing the value of a fixed asset is treated as capital expenditure.

Question 2.

Solution 2: Below are the examples of capital expenditure:-

1.) Purchases of Land and Building

2.) Purchases of Plant and Machinery

Question 3.

Solution 3: Any expenditure the benefit of which is received during the current year itself is termed a as revenue expenditure. For example:- Expenses incurred for the purpose of day to day running of business such as manufacturing expenses, office expenses, selling expenses etc.

Question 4.

Solution 4:

Question 5.

Solution 5:

Question 6.

Solution 6: Wages paid on installation of a machine is a capital expenditure because it will be treated as a cost of machine.

Long Answer Questions

Question 1.

Solution 1: Any expenditure which is incurred in acquiring or increasing the value of a fixed asset is treated as capital expenditure. For example:- Purchases of Land and Building, Purchases of Plant and Machinery. Whereas Any expenditure the benefit of which is received during the current year itself is termed a as revenue expenditure. For example:- Expenses incurred for the purpose of day to day running of business such as manufacturing expenses, office expenses, selling expenses etc.

Question 2.

Solution 2: Any expenditure which is incurred in acquiring or increasing the value of a fixed asset is treated as capital expenditure. As such, the amount spent on the purchases of land and building, plant and machinery, furniture hence is written in assets.

Examples are:-

1.) Expenditure which results in the acquisition of a fixed asset such as land, building, plant, motor vehicles, trademarks etc. Such asset would be used in the business for a number of years.

2.) Expenditure in connection with the purchase or erection of a fixed asset such as wages paid to workers for erecting machines, cartages paid on acquiring plant and machinery, over-hauling of second-hand machines etc.

Any expenditure the benefit of which is received during the current year itself is termed a as revenue expenditure. As such, all the revenue expenditures are debited to trading and profit and loss account. Such expenditure does not result in an increase in the earning of the business but only helps in maintaining the existing earning capacity.

Examples are:-

1.) Expenses incurred for the purpose of day to day running of business such as manufacturing expenses, office expenses, selling expenses etc.

2.) Expenses incurred on the ordinary repairs and maintenance of fixed assets, white-washing of building etc.

Question 3.

Solution 3:

Question 4.

Solution 4:

(a) Preliminary Expenses : Deferred Revenue Expenditure

(b) Purchases of Furniture : Capital Expenditure

(c) Payment of Salary : Revenue Expenditure

(d) Expenses paid for construction of building : Capital Expenditure

Practical Questions

Question 1.

Solution 1:

(i) Capital Expenditure cost of installation is also a capital expenditure and include in machinery account. This expense will increase the earning capacity of the firm.

(ii) Capital Expenditure as the company has been painted at first time it will included in the assets. It will be treated as a capital expenditure.

(iii) Capital Expenditure all expenses related to new machine will be capital expenditure.

(iv) Capital Expenditure as repairs are done before the generator is use.

(v) Revenue Expenditure as repairs is done on regular basis.

(vi) Capital Expenditures as raising the capital will be treated as capital expenditure.

Question 2.

Solution 2:

(i) Revenue expenditure Book value = Rs. 10,000 – Rs. Sale price = Rs. 2,500 = Loss on sale of furniture of Rs. 7,500. Purchase of New furniture + cartage Rs. 6,050 will be Capital expenses.

(ii) Capital expenditure purchases of property and other related expense are capital expenditure.

(iii) Capital expenditure, as new machinery is purchased.

(iv) Capital expenditure, as damages paid on accident does not result in increasing the earning capacity of the firm.

(v) Capital expenditure, as new construction is done in increasing the earning capacity of the firm.

Question 3.

Solution 3:

(a) Here Rs. 20,000 is capital expenditure as it will increase the output of the firm. Rs. 5,000 is revenue expenditure Repairs as it is done on regular basis.

(b) Revenue Expenditure repairs of Rs. 40,000 is done on regular basis and Rs. 1,60,000 is done on improvements which will give future benefits, therefore its capital expenditure.

(c) Revenue expenditure, Compensation and remuneration to employees are done in normal course of business.

(d) Capital expenditure, Any expenses incurred on bringing the asset into operation will be capitalized.

(e) Revenue expenditure, Compensation and remuneration to employees are done in normal course of business.

(f) Deferred revenue expenditure benefit will be derived over a number of years.

Question 4.

Solution 4:

(a) Revenue receipt as this transaction belongs to normal business transaction.

(b) Capital receipt as it is a capital gain which arose by selling of machinery.

(c) Revenue receipt as it is received in normal course of business over exchange of goods.

(d) Capital receipt as it will improve the financial position of the company of the company.

(e) Capital receipt as it will enhance the productivity of the company.

(f) Revenue receipt as it is received regularly from the government.

(g) Capital receipt as it is received for construction and will it will result in increasing the earning capacity of the firm.