Access free TS Grewal Accountancy Class 11 Solution Chapter 13 Trial Balance 2026 below. Students can now access free TS Grewal Solutions for Class 11 Accountancy. These chapter-wise exercises are designed by expert Accountancy teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Accountancy Chapter 13 Trial Balance TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 13 Trial Balance Class 11 Accountancy below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 13 Trial Balance TS Grewal Class 11 Solved Exercises

TS Grewal Accountancy Class 11 Solution Chapter 13 Trial Balance is an important chapter for students of Class 11 studying accountancy. In this chapter, concepts of Trial Balance have been explained in detail. Students will be able to learn about the trial balance, which is a statement that shows the balances of all the ledger accounts at the end of an accounting period. Companies generate trial balance on a periodic basis to assess the companies financial condition and also to assess that the company books are accurate. There are detailed notes and concepts relating to the purpose of the trial balance, the method of preparing it, how to check and scrutinize the trial balance and the limitations of the trial balance. The chapter also covers topics such as errors of omission, errors of commission, errors of principle, and compensating errors, which may occur during the preparation of the trial balance. By understanding the concepts covered in this chapter, students will be able to prepare a trial balance accurately and identify any errors in the accounting records, which is essential for maintaining the accuracy of financial statements. Along with the concepts there are lot of questions given which the students can practice on daily basis. We have given detailed solutions below which the students can use to compare there answers.

Question.1. What is a Trail Balance? State any four functions of a Trail Balance.

Answer 1. After posting the transactions in the accounts and balancing them, a statement is prepared to show separately the debit and credit balances. Such a statement is known as Trial Balance. The total of the debit side of Trial Balance must be equal to that of its credit side. This is based on the principle that in double entry system, for every debit there must be a corresponding credit. The agreement of Trial Balance indicates arithmetic accuracy of the accounting work. If the two sides do not agree, there is definitely some error or errors. It must be remembered that equalizing the two sides of a Trial Balance is not the sole and conclusive proof of the complete correctness of accounting work.

Four Functions of a Trial Balance are:

(i) Ascertain the Arithmetical Accuracy of Ledger Accounts: The Trial Balance enables one to establish whether posting and other accounting processes have been carried out without committing arithmetical errors.

(ii)To Help Prepare the Final Accounts: Financial Statements are prepared from the Trial Balance. Preparation of Financial Statements, therefore, is the second objective of preparing a Trial Balance.

(iii)Summary of Each Account: The Trial Balance offers a summary of the Ledger. The Ledger may have to be referred to only when more details is required in respect of an account.

(iv)To Help in Locating Errors: The Trial Balances helps in locating errors in Book keeping work. It should, however, be borne in mind that it does not disclose all the errors in Book Keeping but only the arithmetical inaccuracies.

Question.2 Define Trail Balance. Why is it prepared?

Answer 2. Definition of a Trial Balance

According to J.R. Batliboi, "A Trial Balance is a statement, prepared with the debit and credit balances of the Ledger Accounts to test the arithmetical accuracy of the books."

Four Functions of a Trial Balance are:

(i) To Ascertain the Arithmetical Accuracy of Ledger Accounts: The Trial Balance enables one to establish whether posting and other accounting processes have been carried out without committing arithmetical errors.

(ii) To Help Prepare the Final Accounts: Financial Statements are prepared from the Trial Balance. Preparation of Financial Statements, therefore, is the second objective of preparing a Trial Balance.

(iii) Summary of Each Account: The Trial Balance offers a summary of the Ledger. The Ledger may have to be referred to only when more details are required in respect of an account.

(iv) To Help in Locating Errors: The Trial Balances helps in locating errors in Book keeping work. It should, however, be borne in mind that it does not disclose all the errors in Book Keeping but only the arithmetical inaccuracies.

Question.3. What are objectives or functions of a Trail Balance?

Answer 3. The following are the Objective or Functions of a Trial Balance.

(i) To Ascertain the Arithmetical Accuracy of Ledger Accounts: The Trial Balance enables one to establish whether posting and other accounting processes have been carried out without committing arithmetical errors.

(ii) To Help Prepare the Final Accounts: Financial Statements are prepared from the Trial Balance. Preparation of Financial Statements, therefore, is the second objective of preparing a Trial Balance.

(iii) Summary of Each Account: The Trial Balance offers a summary of the Ledger. The Ledger may have to be referred to only when more details is required in respect of an account.

(iv) To Help in Locating Errors: The Trial Balances helps in locating errors in Book keeping work. It should, however, be borne in mind that it does not disclose all the errors in Book Keeping but only the arithmetical inaccuracies.

Question.3. Discuss the methods of preparation of a Trail Balance. (Old Question)

Answer 3. Methods of Preparing a Trial Balance:

A Trial Balance may be prepared by following either the Balance Method or the Totals Method.

(i) Balance Method: In this method, only the debit or credit balances are entered separately in the two columns. This is known as the Net Trial Balance. This is the commonly used method of preparing a Trial Balance because it facilitates the preparation of the final accounts.

(ii) Totals Method: In this method, the total of each side of the account is entered respectively in the debit and credit columns of the Trial Balance. Such a Trial Balance is known as the Gross Trial Balance.

Question.4. Define a Trail Balance. Why is it prepared? (Old Question)

Answer 4. Definition of a Trial Balance

According to J.R. Batliboi, "A Trial Balance is a statement, prepared with the debit and credit balances of the Ledger Accounts to test the arithmetical accuracy of the books."

A Trial Balance is prepared for. A Trial Balance is a list of accounts showing debit balances and credit balances. If the Trial Balance agrees it proves that:

(i) The accounts are arithmetically accurate;

(ii) Both aspects of all the transactions have been recorded and

(iii) Both debit and credit entries are posted in the Ledger.

A Trial Balance facilitates the preparation of final accounts, i.e., the Trading Account, the Profit and Loss Account and the Balance Sheet.

PRACTICAL PROBLEMS :---->

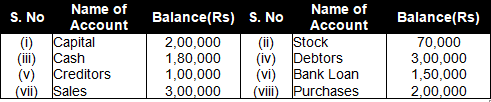

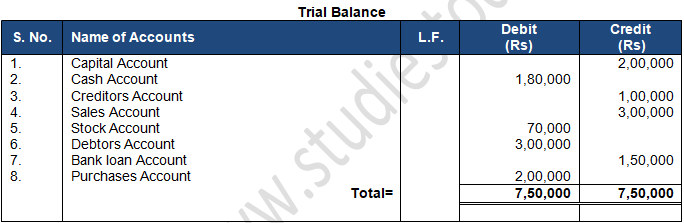

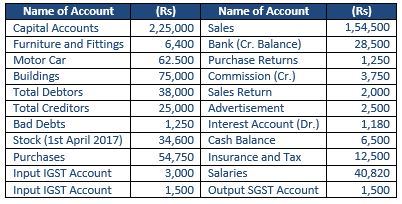

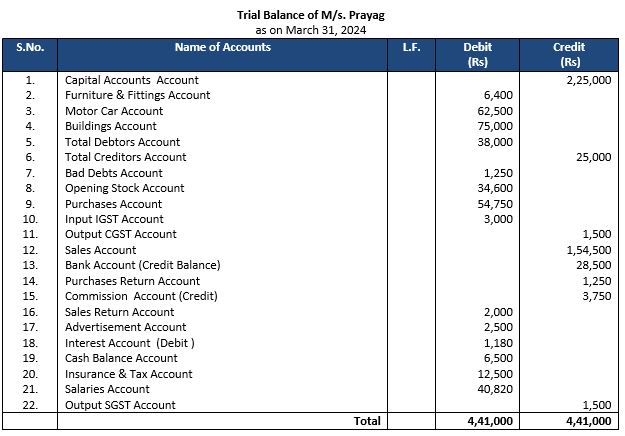

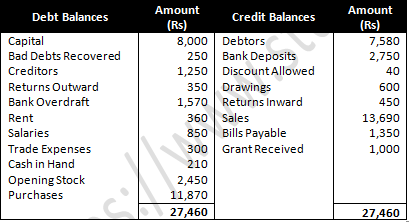

Question 1: Prepare a Trial Balance with the following information:

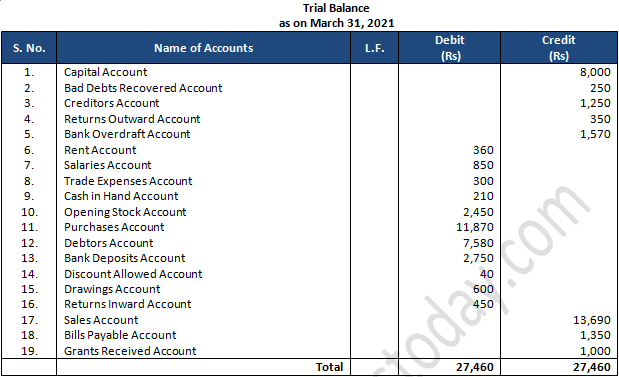

Answer 1:

STATEMENT OF TRIAL BALANCE

Point of Knowledge:

- Trial balance is a list of balances of all Ledger accounts and Cash Book.

- Trial balance verifies the arithmetical accuracy of posting of entries from the Journal to the Ledger.

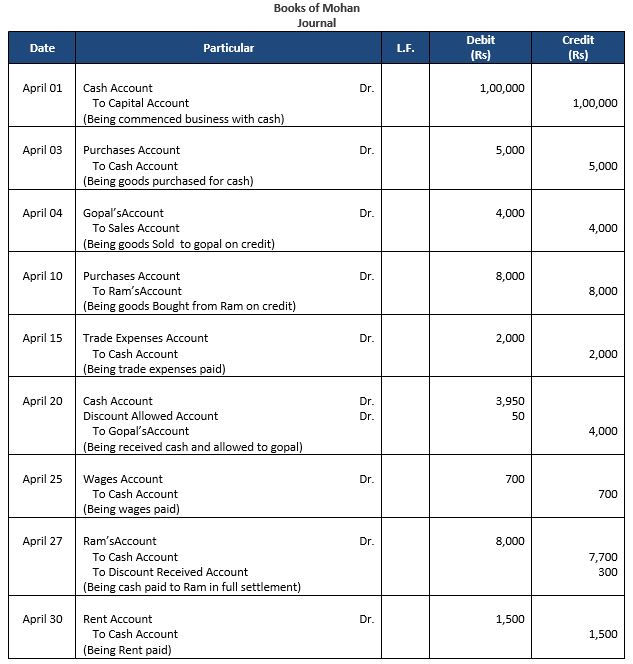

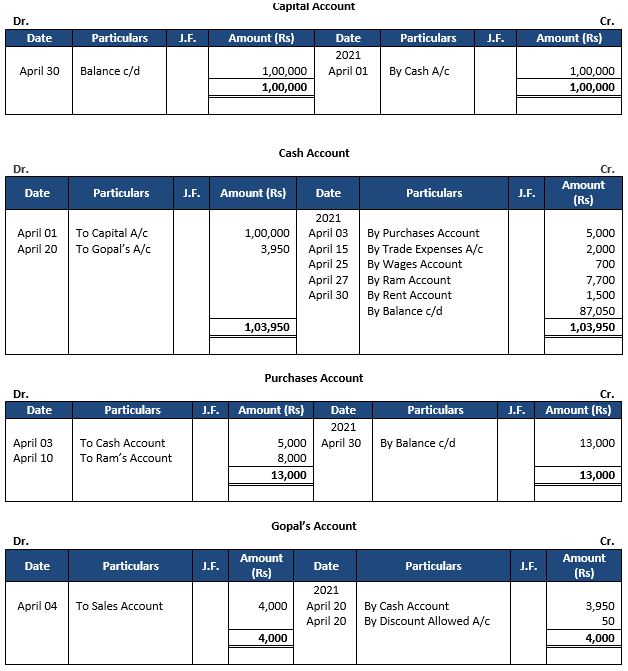

Question 2: Journalize the following transactions, post them into Ledger and prepare a Trial Balance:

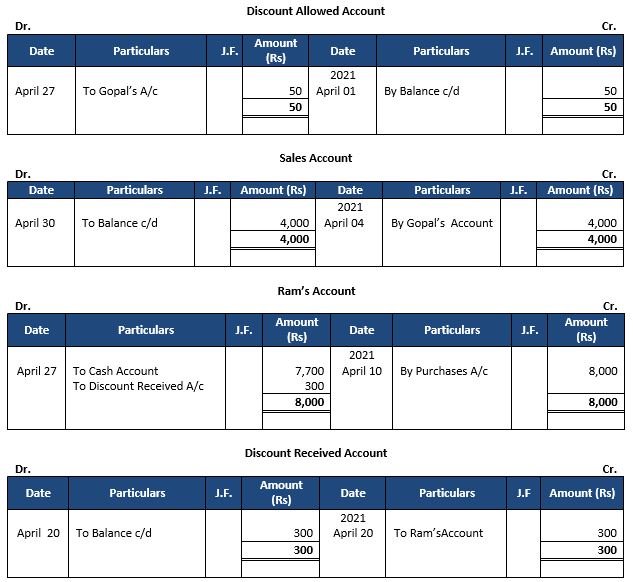

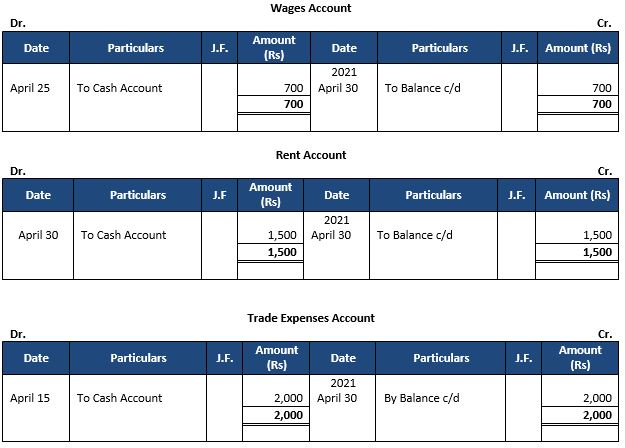

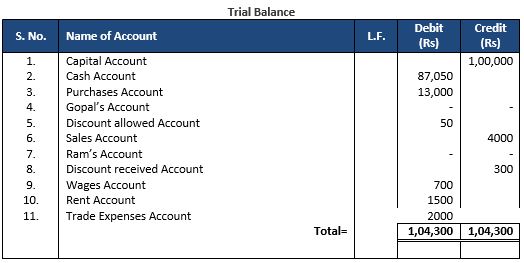

Answer 2:

FOLLOWING ARE THE JOURNAL ENTRIES FOR THE ABOVE TRANSACTIONS

LEDGER ACCOUNTS IN THE BOOKS OF VIJAY

Point of Knowledge:

- Trail Balance is not an account so we can’t use ‘To’ or ‘By’ in this.

- If an Account does not show any balance, it is ignored.

- At the end of the year balance of purchases account will be transferred to the debit of trading account.

- At the end of the year balance of sales account will be transferred to the credit of trading account.

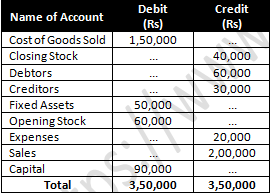

Question 3: Prepare a Trial Balance from the following items:

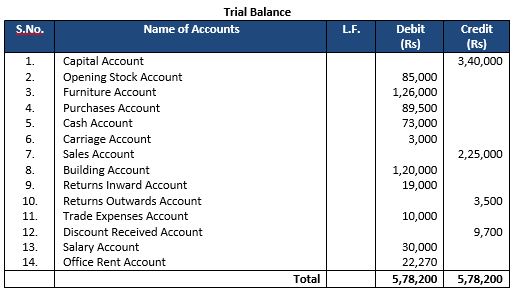

Answer 3:

STATEMENT OF TRIAL BALANCE

Point of Knowledge:-

The opening Stock Account shows a debit balance which is shown on the debit column of a Trial Balance.

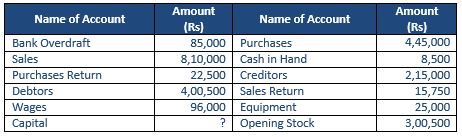

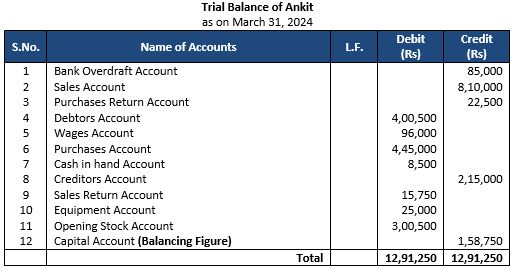

Question 4: Prepare the Trial Balance of Ankit as on 31st March, 2024. He has omitted to open a Capital Account:

Answer 4:

STATEMENT OF TRIAL BALANCE:-

Working Note:-

Amount of Capital Account = Sum of Debit Side – Sum of Credit Side

Amount of Capital Account = 12, 91,250 – 11, 32,500

Amount of Capital Account = 1, 58,750

Point of Knowledge:

- Total Method of Trail Balance:- In this method the total of each side of the account is entered respectively in the debit and credit columns of the Trial Balance.

- This Trail Balance method is known as the gross trail balance.

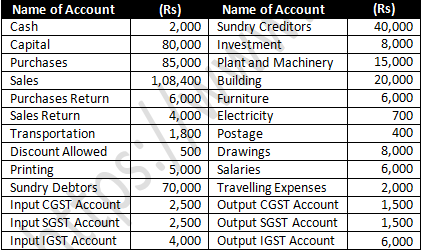

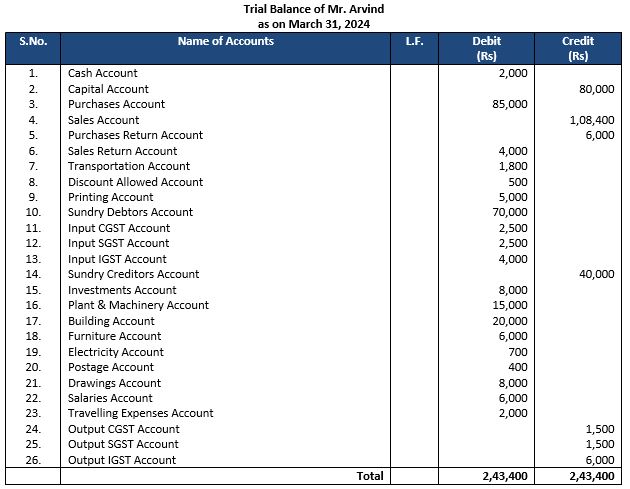

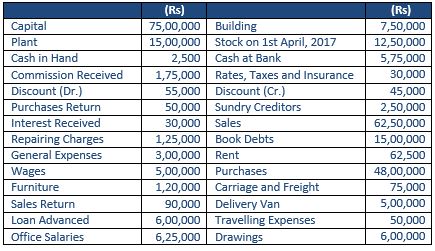

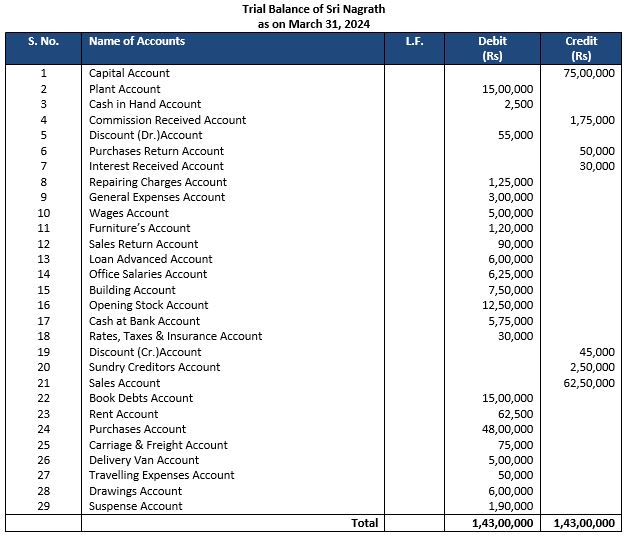

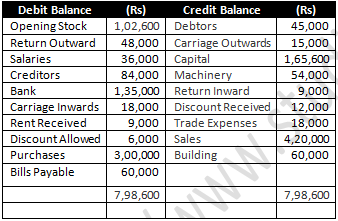

Question 5: The following are the balances extracted from the books of Arvind. Prepare a Trial Balance as on 31st March, 2024:

Answer 5:

STATEMENT OF TRIAL BALANCE

Point of Knowledge:

- It can be prepared immediately after the completion of posting from books of original entry to the ledger.

- It shows the total amounts of the debit and credit side in each ledger account.

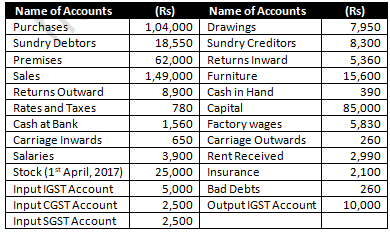

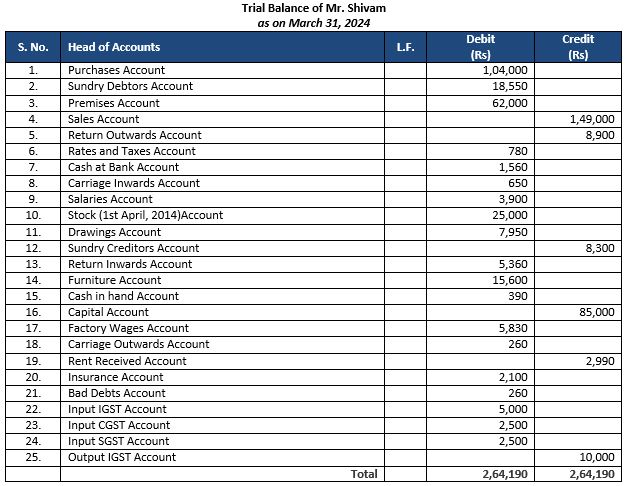

Question 6: From the following information, prepare a Trial Balance of Gurman for the year ended 31st March, 2024:

Answer 6:

STATEMENT OF TRIAL BALANCE:

Point of Knowledge:

- Sales Returns Account always shows a debit balance and hence us shown in the debit column of a trail balance.

- Financial statement are normally prepared on the basis of trial balance, otherwise the work of making financial statement may be difficult or not possible.

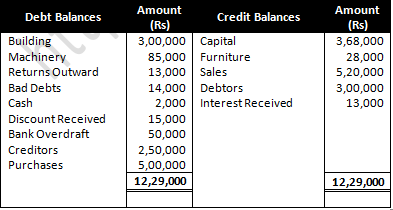

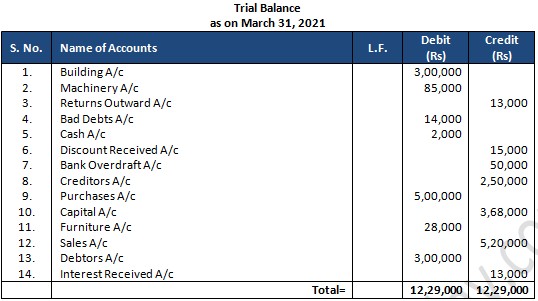

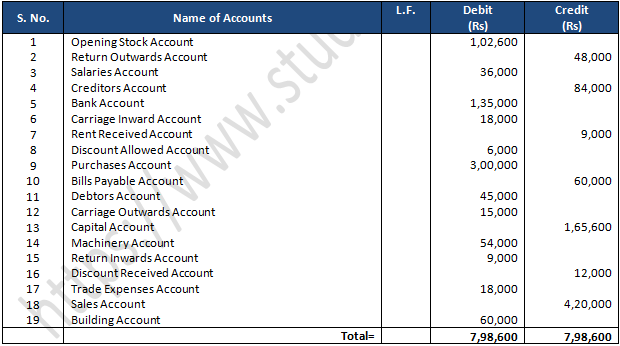

Question 7: From the following balances extracted from the Ledger of Sri Narugopal, prepare Trial Balance as on 31st March, 2024:

Answer 7:

Point of Knowledge:

- Accounts of income and gains shows credit balance and are shown on the credit side of a trial balance.

- Account of expenses and losses show debit balance and are shown on the debit side of a trial balance.

Answer 8:

Point of Knowledge:

- At the end of the year balance of purchases account will be transferred to the debit of trading account.

- Trail Balance helps in locating errors in book keeping work. It should, be noted that it does not disclose all the errors in book keeping work but only the arithmetical inaccuracies.

Question 9: Following Trial Balance is given but it is not correct. Prepare correct Trial Balance.

Answer 9:

STATEMENT OF TRIAL BALANCE

Point of Knowledge:

- Trial balance is a list of balances of all Ledger accounts and Cash Book.

- A Trial balance is only a prime facie evidence of the arithmetical accuracy of the records.

- Trial Balance offers a summary of the Ledgers.

Question 10: Redraft correctly the Trial Balance given below:

Answer 10:

STATEMENT OF TRIAL BALANCE

Point of Knowledge:-

- Opening Stock account shows a debit balance which is shown on the debit column of a trail balance.

- A Trial balance is only a prime facie evidence of the arithmetical accuracy of the records.

Question 11: Prepare a correct Trial Balance from the following Trial Balance in which there are certain mistakes:

Answer 11:

Point of Knowledge:

At the time of correction in trail balance remember below points:-

- Closing Stock will not be taken in the Trail Balance because it has not yet been brought into account.

- All assets and expenses accounts will show a debit balance.

- All liabilities and income account will show a credit balance.

Question 12: Correct the following Trial Balance:

Answer 12:

STATEMENT OF TRIAL BALANCE

Point of Knowledge:

- Accounts of income and gains shows credit balance and are shown on the credit side of a trial balance.

- Account of expenses and losses show debit balance and are shown on the debit side of a trial balance.