Access free TS Grewal Accountancy Class 11 Solution Chapter 12 Bank Reconciliation Statement 2026 below. Students can now access free TS Grewal Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 12 Bank Reconciliation Statement TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 12 Bank Reconciliation Statement Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 12 Bank Reconciliation Statement TS Grewal Class 11 Solved Exercises

TS Grewal Accountancy Class 11 Chapter 12 on Bank Reconciliation Statement is an important topic in Class 11. In this chapter there are concepts relating to the importance and process of reconciling bank book and bank statement and ensure all variances are identified and reasons are captured properly. Preparing bank reconciliation statement is very important for any business as it helps business or individual to make sure that their financial statements are accurate.

In this chapter of TS Grewal Class 11 Accountancy book, the meaning of a bank reconciliation statement and its importance, different reasons for the differences between the bank balance and bank book balance, such as outstanding checks, deposits in transit, and bank charges have been explained. Students will be able to learn step by step process of preparation of a bank reconciliation statement, which involves comparing the bank statement and bankbook, and noting down reasons for the differences.

There are lot of important questions given in this chapter which are really crucial for students to practice. Our accountancy teachers have given detailed solutions below which will help you to understand how the questions are solved and also can be a guide during exams.

Question.1. What is a Bank Reconciliation Statement? Explain briefly any four points regarding need and importance of preparing a Bank Reconciliation Statement.

Answer 1. Meaning of Bank Reconciliation Statement is a statement prepared by the account holder on a particular date to reconcile the bank balance as per cash book with the balance as per bank statement or bank pass book if the two balances differs showing entries causing differences between the two balances.

Preparation of Bank Reconciliation Statement is not a part of Double Entry System of Book Keeping. It is a method or technique to reconcile bank balance in Cash Book with the balance as per Bank Statement or Bank Pass Book to ensure that errors if any, are corrected and transactions if omitted, are recorded.

The following are the purposes of preparing Bank Reconciliation Statement:

Bank Reconciliation Statement is prepared for the following reasons:

1. It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

2. Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

3. Regular reconciliation discourages embezzlements. Reconciliation helps the management to verify the accuracy of entries recorded in the Cash Book.

4. It shows actual bank balance.

Question.2. What is a Bank Reconciliation Statement? Explain the purpose of preparing such a statement.

Answer 2. Meaning of Bank Reconciliation Statement is a statement prepared by the account holder on a particular date to reconcile the bank balance as per cash book with the balance as per bank statement or bank pass book if the two balances differs showing entries causing differences between the two balances.

Bank Reconciliation Statement is prepared for the following purposes:

1. It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

2. Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

3. Regular reconciliation discourages embezzlements. Reconciliation helps the management to verify the accuracy of entries recorded in the Cash Book.

4. It shows actual bank balance.

Question.3. Explain any two reasons on account of which the balance as shown by the Pass Book does not agree with the balance as shown by the bank column of the Cash Book.

Answer 3. The two Reasons of difference between balances as per Cash Book and Bank Statement or Bank Pass Book are given below:

Balances as per Cash Book and Bank Statement or Bank Pass Book may differ under some situations shown as follows:

Difference due to Timing:

(a) Cheques issued or Drawn but not yet presented for payment: Cheques issued or drawn but not yet presented for payment is recorded immediately in Cash Book at the time of issue but bank records it when it is presented for payment. Thus, there is a gap of few days between entry in the Cash Book and in the Bank Statement or Bank Pass Book. If Bank Reconciliation Statement is prepared on a date between the date of issue of cheque and its presentation to the bank for payment, the difference will arise and balance as per Cash Book will be less by the amount of issued cheques than that of Pass Book Balance.

(b) Cheques Deposited or paid into the Bank but yet cleared: Cheques deposited or paid into the bank are recorded in the receipts or debit side of the Cash Book on the date of deposit. But bank credits the accountholder’s account when it has received the payment from the other bank or when cheques have been cleared. Hence, there is gap of few days between the deposit of cheques and credit given by the bank. If Bank Reconciliation Statement is prepared in between the two dates, differences will exist. The Cash Book balance will be more than the Pass Book balance.

Question.4. How is a Bank Reconciliation Statement prepared?

Answer 4. Bank Reconciliation Statement is prepared in the following manner:

1.) Date: The date on which Bank Reconciliation Statement is prepared.

2.) Balance: It should be kept mind from where to start the Bank Reconciliation Statement.

3.) Preparing Bank Reconciliation Statement: After deciding which entries are to be added to the balance of the concerned book and which entries are to be subtracted. Bank Reconciliation Statement is prepared in a statement form.

4.) Starting With: Bank Reconciliation Statement is prepared by starting with either Cash Book balance or Pass Book balance. Thereafter, entries that cause the difference are determined. Starting balance is then adjusted by noting how the balance would have changed if same entries were recorded in the two books.

Question.5. List any two items which increase the balance in Cash Book and two items which decrease the balance.

Answer 5: Below are the items which increase the balance in Cash Book:-

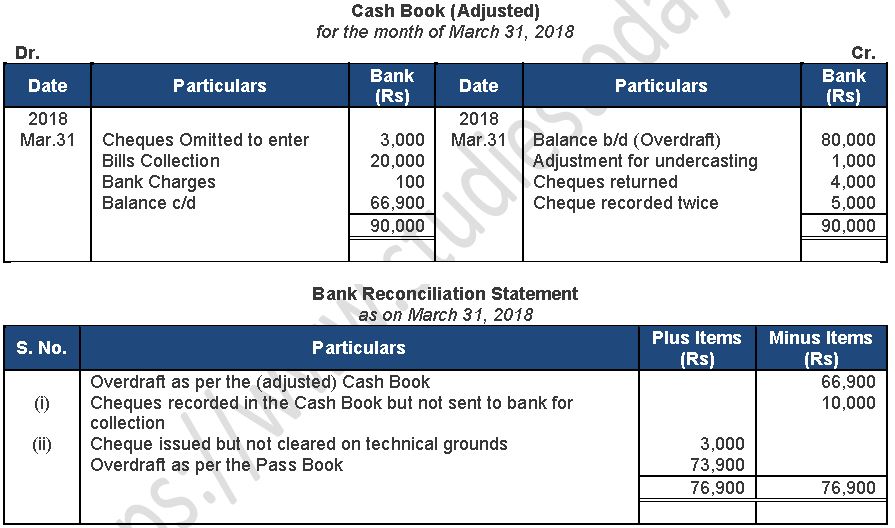

1. Cheques deposited but not credited by the bank.

2. Bank charges not recorded in the cash book.

Below are the items which decrease the balance in Cash Book:-

1. Cheque issued but not presented.

2. Interest credited by the bank.

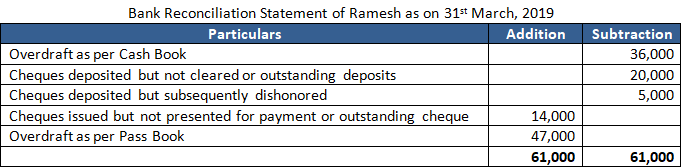

Question.5. On 31st March, 2019 Bank Account in the books of Ramesh shows a credit balance of Rs. 36,000. On the same date, outstanding cheques amounted to Rs. 14,000 and outstanding deposits amounted to Rs. 20,000. A Cheque for Rs. 5,000 received from a debtor, was subsequently dishonored. The receipt had been correctly recorded but no entry has yet been made in the books for the dishonor. On the basis of the above information, determine the balance as per the Bank Statement. (Old Question)

Answer 5.

Question.6. Explain the process of preparing Bank Reconciliation Statement with Adjusted Cash Balance.

Answer 6: At the end of the financial year, the cash book must be adjusted for the entries that should be incorporated but have not been incorporated, before preparing the Bank Reconciliation Statement.

Following procedure is to be followed for ascertaining the adjusted Cash Balance:

Step 1- Draw up Cash Book having only bank column. If favorable balance as per Cash book is given, write it on debit side and if unfavorable balance is given write down the balance on the credit side of the Cash Book.

Step 2- Pass entries in the Cash book in respect of following items:

(a) Amount recorded in the pass book but not yet recorded in the Cash book.

(b) Rectifying entries in respect of errors committed in the cash book.

Step 3- The adjusted balance of the cash book is taken as starting point. The bank reconciliation statement with amended and adjusted Cash book is prepared.

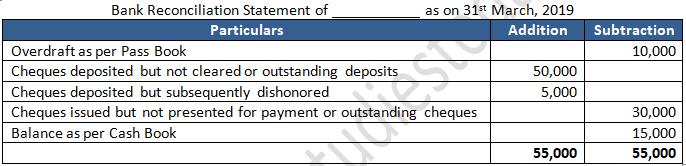

Question.6 On 31st March, 2019, the balance as per the Bank Statement was Rs.10,000 debit. IN the sane date, outstanding cheques amounted to Rs.30,000 and outstanding deposits amounted to Rs. 50,000. Also, there was a dishonored cheque from a customer of Rs. 5,000 recorded in the Bank Statement but not in the Cash Book. On the basis of the above information, determine the balance as per the Cash Book. (Old Question)

Answer 6.

Bank Reconciliation Statement Practical Questions Class 11

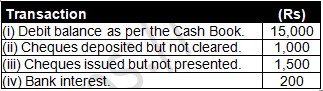

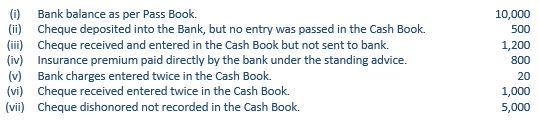

Question 1: Prepare Bank Reconciliation Statement from the following:

Answer 1:

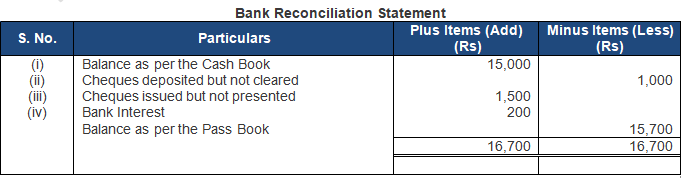

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance as per the Pass Book is Rs.15,700

Point of Knowledge:

- Cheque deposited but not cleared deducted from the Cash Book Balance as it stands increased but the bank has not given credit.

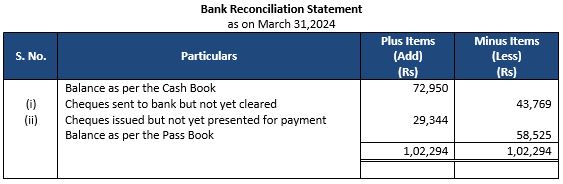

Question 2: Ramesh has his account at Punjab National Bank, Delhi, According to his Cash Book, his bank balance on 31st March, 2024 was Rs. 72,950. He sent cheque for Rs. 90,075 to his bank for collection but cheque amounted to Rs. 43,769 was not collected by that date. Out of the cheques issued by him in payment of his debts, cheque for Rs. 29,344 were not presented for payment.

Prepare Bank Reconciliation Statement and determine the balance as shown by his Pass Book.

Answer 2:

Statement of Bank Reconciliation on the basis of the given transactions:-

Point of Knowledge:

- The amount of Cheque issued but not presented for payment is added to the balance because it has not been deducted by the bank as they have not been presented for payment.

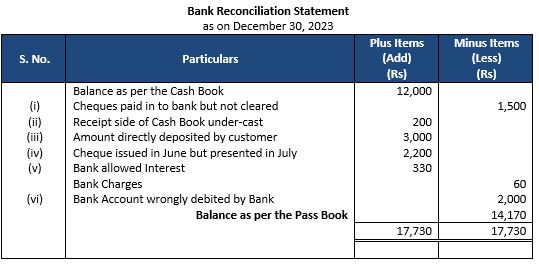

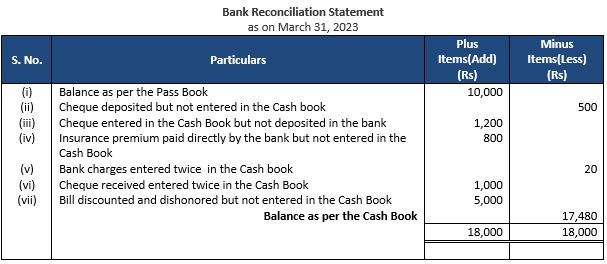

Question 3: On 30th December, 2023, bank column of the Cash Book of Gurman showed balance of Rs. 12,000 but the Pass Book showed a different balance due to the following reasons:

(i) Cheques paid into the bank Rs. 8,000 but out of these only cheques of Rs. 6,500 credited by bankers.

(ii) The receipt column of the Cash Book under-cast by Rs. 200.

(iii) On 29th December, a customer deposited Rs 3,000 directly in the Bank Account but it was entered in the Pass Book only.

(iv) Cheques of Rs. 9,200 were issued of which Rs. 2,200 were presented for payment on 15th January, 2024.

(v) Pass Book shows a credit of Rs. 330 as interest and a debit of Rs. 60 as bank charges.

(vi) The Bank had wrongly debited the account of Gurman by Rs. 2,000, which was rectified after 31st December, 2023.

Prepare Bank Reconciliation Statement as on 31st December, 2023.

Answer 3:

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance as per the Pass Book is Rs.14,170

Point of Knowledge:

- The receipt column of cash book is undercasted with Rs. 200. So the same amount would be added to the cash book, to rectify the error.

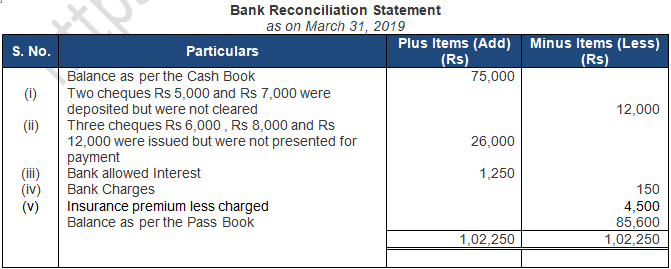

Question 3: On 31st March, 2019, Cash Book of Mahesh showed debit bank balance of Rs 75,000. When compared with the Bank Statement, following facts were discovered. On 30th March, two cheques of Rs 5,000 and Rs 7,000 were deposited in the bank but were not realised till date. On 28th March, three cheques of ₹ 6,000, Rs 8,000 and Rs 12,000 were issued but none of these were presented to the bank for payment. On 31st March, bank credited Rs 1,250 as interest but this was not recorded in the Cash Book. Similarly, the bank had charged Rs 150 as bank charges but this was not recorded in the Cash Book. Bank paid insurance premium of Rs 5,000 but it was recorded as Rs 500 in Cash Book. Prepare Bank Reconciliation Statement on 31st March, 2019. (Old Question)

Answer 3:

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance as per the Pass Book is Rs.85,600

Point of Knowledge:

1. The amount of insurance premium of Rs. 5,000, recorded as Rs. 500 in Cash Book. Remaining Rs. 4,500 will be deducted from Cash Book.

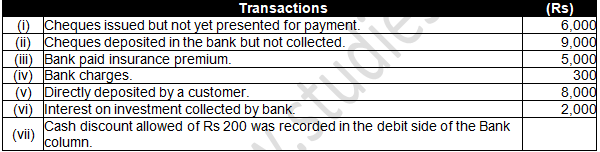

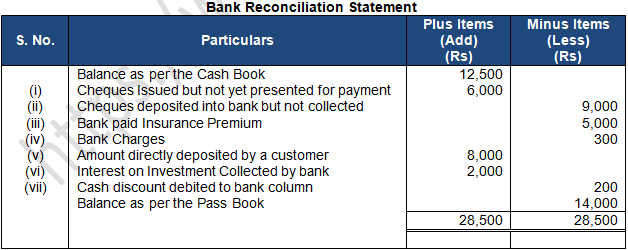

Question 4: Cash Book shows a balance of Rs 12,500. On comparing the Cash Book with the Pass Book, following discrepancies were noted:

Prepare Bank Reconciliation Statement.

Answer 4:

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance as per the Pass Book is Rs.14,000

Point of Knowledge:

- Interest on investment amounting Rs. 2000 collected by bank would increases the balance of Cash Book. So the same amount will be added in the cash book.

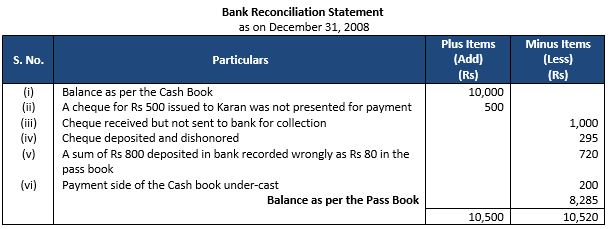

Question 5: From the following particulars, prepare Bank Reconciliation Statement as on 31st December, 2023:

(i) Debit balance as per Cash Book Rs. 10,000.

(ii) A cheque for Rs. 500 issued in favour of Karan has not been presented for payment.

(iii) A post-dated cheque of Rs. 1000 debited in the bank column of the Cash Book but not sent to bank.

(iv) A cheque for Rs. 295 deposited in the bank has been dishonored.

(v) A sum of Rs. 800 deposited in the bank has been credited as Rs. 80 in the Pass Book.

(vi) Payment side of the Cash Book has been under-cast by Rs. 200.

Answer 5:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:-

- The payment column of cash book is undercasted with Rs. 200. So the same amount would be deducted from the cash book, to rectify the error.

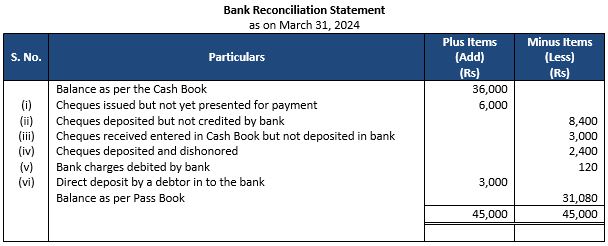

Question 6: Prepare a Bank Reconciliation Statement as on 31st March, 2024 from the following:

(i) On 31st March, 2024, Cash Book of a firm showed bank Balance of Rs. 36,000 (Dr.).

(ii) Cheque had been issued for Rs. 30,000, out of which cheque of Rs. 24,000 were presented for payment.

(iii) Cheque of Rs. 8,400 were deposited in the bank on 28th March, 2024 but had not been credited by the bank. Also, a cheque of Rs. 3,000 entered in the Cash Book on 30th March, 2024 was banked on 3rd April.

(iv) A cheque from Suresh for Rs. 2,400 was deposited in the bank on 26th March, 2024 was dishonored, advice was received on 2nd April, 2024.

(v) Pass Book showed bank charges of Rs. 120 debited by the bank.

(vi) One of the Debtors deposited Rs. 3,000 in the bank account of the firm on 26th March, 2024, but the intimation in this respect was received from the bank on 2nd April, 2024

Answer 6:

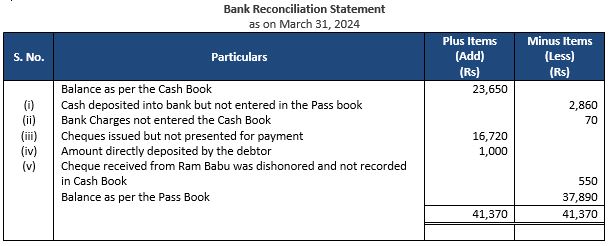

Question 7: On examining the Bank Statement of Mukesh Bros., it is found that the balance shown on 31st March, 2024, differs from the bank balance of Rs. 23,650 shown by the Cash Book on that date. From a detailed comparison of the entries it is found that:

(i) Rs. 2,860 is entered in the Cash Book as paid into the bank on 31st March, 2024 but not credited by the bank until the following day.

(ii) Bank charges of Rs. 70 on 31st March, 2024 are not entered in the Cash Book.

(iii) Cheques totaling Rs. 16,720 were issued by the company and duly recorded in the Cash Book before 31st March, 2024 but had not been presented at the Bank for payment until after that date.

(iv) On 25th March, 2024, a debtor paid Rs. 1,000 into the Company's Bank in settlement of his account but no entry was made in the Cash Book of the company in respect of this.

(v) No entry has been made in the Cash Book to record the dishonor on 15th March, 2024, of a cheque for Rs. 550 received from Ram Babu.

Prepare a Bank Reconciliation Statement as on 31st March, 2024.

Answer 7:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

- Rs. 1000 directly deposited by the debtors, so the same amount would be added to the receipt column of the cash book.

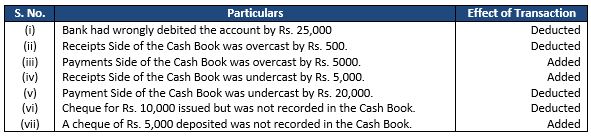

Question 8: A Bank Reconciliation Statement is prepared as on 31st March, 2024 starting with debt balance as per Cash book. State whether the following transactions will be shown in the Bank Reconciliation Statement by adding or deducting these from the given balance giving reasons:

(i) Bank had wrongly debited the account by Rs. 25,000 on 1st March, 2024 and reversed on 3rd April, 2024.

(ii) Receipts Side of the Cash Book was overcast by Rs. 500.

(iii) Payments Side of the Cash Book was overcast by Rs. 5000.

(iv) Receipts Side of the Cash Book was undercast by Rs. 5,000.

(v) Payment Side of the Cash Book was undercast by Rs. 20,000.

(vi) Cheque for Rs. 10,000 issued but was not recorded in the Cash Book.

(vii) A cheque of Rs. 5,000 deposited was not recorded in the Cash Book.

Answer 8:

Statement of Bank Reconciliation on the basis of the given transactions

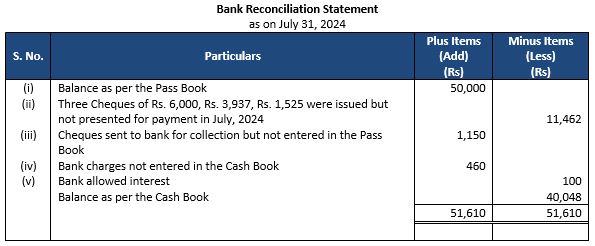

Question 9: Prepare Bank Reconciliation Statement from the following particulars on 31st July, 2024:

(i) Balance as per the Pass Book Rs. 50,000.

(ii) Three cheques for Rs 6,000, Rs 3,937 and Rs 1,525 issued in last week of July, 2024 were presented for payment to the bank in August, 2024.

(iii) Two cheques of Rs 500 and Rs 650 sent to the bank for collection were not entered in the Pass Book by 31st July, 2024.

(iv) The bank charged Rs 460 for its commission and allowed interest of Rs 100 which were not mentioned in the Bank Column of the Cash Book

Answer 9:

Statement of Bank Reconciliation on the basis of the given transactions

Debit Balance as per the Cash Book is Rs.40,048

Point of Knowledge:

1. As three cheques of Rs. 6000, Rs 3937 and Rs. 1525 were only issued but not yet presented for payment, so the total amount would be deducted from the Pass book.

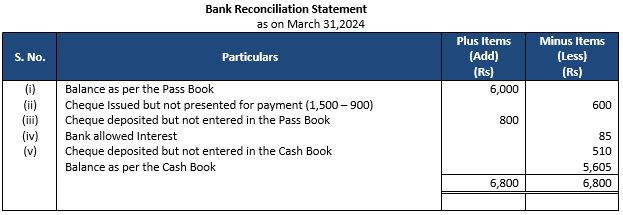

Question 10: Draw Bank Reconciliation Statement showing adjustment between your cash book and pass book as on 31st March, 2011.

(i) On 31st March, 2011 your pass book showed a balance of Rs. 6,000 to your credit.

(ii) Before that date, you had issued cheques amounting to Rs. 1,500 of which cheques of Rs. 900 have been presented for payment.

(iii) A cheque of Rs. 800 paid by you into the bank on 29th March, 2011 is not yet credited in pass book.

(iv) There was a credit of Rs. 85 for interest on Current Account in the pass book.

(v) On 31st March, 2011 a cheque for Rs. 510 received by you and was paid into bank but the same was omitted to be entered in cash book.

Answer 10:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

- Cheques of Rs. 1500 issuedbut cheques of Rs. 900 have been presented for payment, remaining Rs. 600 will be deducted from the Pass book.

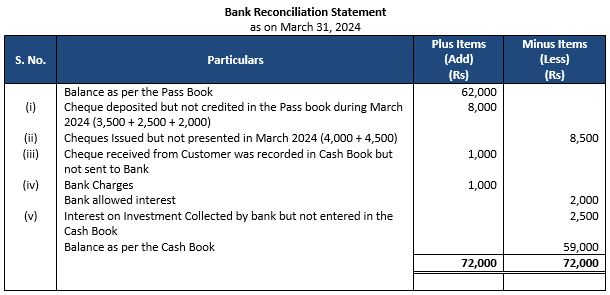

Question 11: Bank Statement of a customer shows bank balance of Rs. 62,000 on 31st March, 2024. On Comparing it with the Cash Book the following discrepancies were noted:

(i) Cheques were paid into the bank in March but were credited in April: P–Rs. 3,500; Q–Rs. 2,500; R–Rs. 2,000.

(ii) Cheques issued in March were presented in April: X–Rs. 4.000; Q–Rs. 4,500.

(iii) Cheque for Rs. 1,000 received from a customer entered in the Cash Book but was not banked.

(iv) Pass Book shows a debit of Rs. 1,000 for bank charges and credit of Rs. 2,000 as interest.

(v) Interest on investment Rs. 2,500 collected by the bank appeared in the Pass Book.

Prepare Bank Reconciliation Statement showing the balance as per Cash Book on 31st March, 2024.

Answer 11:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

Cheque deposited but not credited is added because the cash book balance already stands increased. By adding the amount the balance will come at par with the cash book balance.

Question 12: Prepare Bank Reconciliation Statement as on 30th September, 2023 from the following particulars

Answer 12:

Statement of Bank Reconciliation on the basis of the given transactions

Question 13: Prepare Bank Reconciliation Statement as on 31st March, 2024 from the following particulars:

Answer 13:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

1. The credit column of cash book is under-casted with Rs. 200. So the same amount would be added in the pass book, to rectify the error.

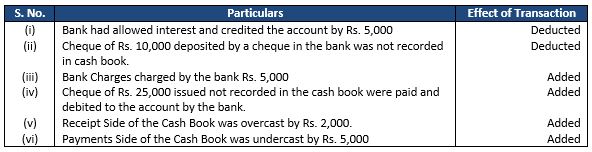

Question 14: Bank Reconciliation Statement is prepared as on 31st March, 2024 starting with credit balance as per Bank Pass Book. State whether the following transactions will be shown in the Bank Reconciliation Statement by adding or deducting these from the given balance giving reason:

(i) Bank had allowed interest and credited the account by Rs. 5,000

(ii) Cheque of Rs. 10,000 deposited by a cheque in the bank was not recorded in cash book.

(iii) Bank Charges charged by the bank Rs. 5,000

(iv) Cheque of Rs. 25,000 issued not recorded in the cash book were paid and debited to the account by the bank.

(v) Receipt Side of the Cash Book was overcast by Rs. 2,000.

(vi) Payments Side of the Cash Book was undercast by Rs. 5,000

Answer 14:

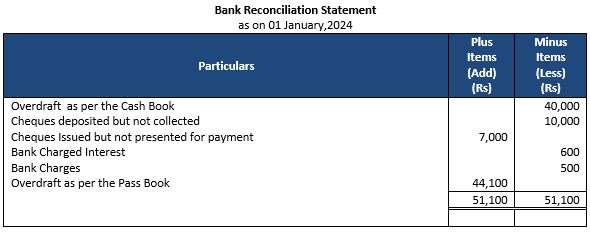

Question 15: On 1st January, 2024, Naresh had an overdraft of Rs. 40,000 as shown by his Cash Book in the bank column. Cheques amounting to Rs. 10,000 had been deposited by him but were not collected by the bank by 1st January, 2024. He issued cheques of Rs 7,000 which were not presented to the bank for payment up to that day. There was also a debit in his Pass Book of Rs. 600 for interest and Rs. 500 for bank charges. Prepare a Bank Reconciliation Statement.

Answer 15:

Point of Knowledge:

The interest charged by the bank is deducted from the Overdraft balance of the cash book. So, Rs. 600 would be deducted from the cash book.

Question 16: A Bank Reconciliation Statement is prepared as on 31st March, 2024 starting with Credit balance as per Cash Bank. State whether the following transactions will be shown in the Bank Reconciliation Statement by adding or deducting these from the given balance giving reason:

(i) Cheque of Rs. 10,000 deposited was dishonored.

(ii) Cheque of Rs. 20,000 was recorded in Cash Book but was deposited.

(iii) Post-dated cheque of Rs. 20,000 discounted from Bank was dishonored.

(iv) A cheque issued to Ramesh for Rs. 5,500 was not recorded in Cash Book.

(v) Payment Side of the Cash Book was undercast by Rs. 4,000.

Answer 16:

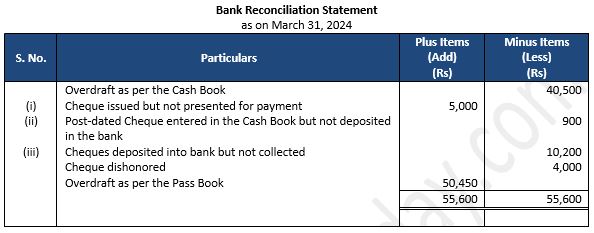

Question 17: Tiwari and Sons find that the bank balance shown by their Cash Book on 31st March, 2024 is Rs. 40,500 (credit) but the Pass Book shows a difference due to the following reasons:

(i) A cheque for Rs. 5,000 drawn in favor of Manohar has not yet been presented for payment.

(ii) A post-dated cheque for Rs. 900 has been debited in the bank column of the Cash Book but it could not have been presented in any case.

(iii) Cheques totaling Rs. 10,200 deposited with the bank have not yet been collected and a cheque for Rs. 4,000 has been dishonored.

Prepare Bank Reconciliation Statement and find out the balance as per Pass Book.

Answer 17:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

The bill of Rs. 10,000 got retired by the bank and under a rebate of Rs. 150 but full amount was credited in the cash book, so it would be added to the cash book to reconcile the transaction.

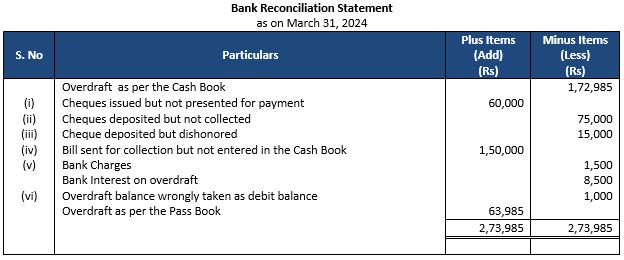

Question 18: On 31st March, 2024, Cash Book of a merchant showed bank overdraft of Rs 1,72,985. On comparing the Cash Book with Bank Statement, following discrepancies were noted:

(i) Cheques issued for Rs 60.000 were not presented in the bank till 7th April, 2024.

(ii) Cheques amounting to Rs 75.000 were deposited in the bank but were not collected.

(iii) A Cheque of Rs 15,000 received from Mahesh Chand and deposited in the bank was dishonored but the non-payment advice was not received from the bank till 1st April, 2024.

(iv) Rs 1,50,000 being the proceeds of a bill receivable collected appeared in the Pass Book but not in the Cash Book.

(v) Bank charges Rs 1,500 and interest on overdraft Rs 8,500 appeared in the Pass Book but not in the Cash Book.

(vi) Overdraft balance as per Cash Book of Rs 500 on 28th February, 2024 was wrongly carried forward as debit balance. The error was noted at the time of preparing the Bank Reconciliation Statement as on 31st March, 2024.

Prepare Bank Reconciliation Statement

Answer 18:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

In the entry dated 28th February, 2024 there is an overdraft balance of Rs. 500 which was wrongly carried forward as debit balance. Therefore, to rectify the error double amount (Rs. 1,000) would be deducted.

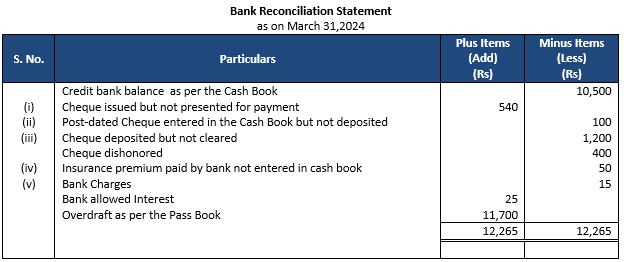

Question 19: Prepare Bank Reconciliation Statement from the following:

On 31st March, 2024, a merchant's Cash Book showed a credit bank balance of Rs 10,500 but due to the following reasons the Pass Book showed a difference.

(i) A cheque of Rs. 540 issued to Mohan has not been presented for payment.

(ii) A post-dated cheque for Rs. 100 has been debited in the bank column of the Cash Book but under no circumstances was it possible to prove it.

(iii) Four cheque for Rs. 1,200 sent to the bank have not been collected so far. A cheque of Rs. 400 deposited in the bank has been dishonored.

(iv) As per instructions, the bank paid Rs. 50 as Fire Insurance premium but the entry has not been made in the Cash Book.

(v) There was a debit in the Pass Book of Rs. 15 in respect of bank charges and a credit of Rs. 25 for interest on Current Account but no record exists in the Cash Book.

(vi) Cheque of Rs. 5,000 dated 15th April, 2024 issued to M & Co. was dishonored being post-dated. It was also not recorded in the books of account yet.

Answer 19:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

- As the cheque amounted Rs. 5,000 dated 15th April, 2024 got dishonoured but after 31st March, 2024. So it will not create any impact on Bank Reconciliation Statement as on 31st March, 2024.

Question 20: Overdraft balance show by the bank column in the Cash Book of Vivek is Rs. 45,000. Prepare Bank Reconciliation Statement as on 31st December, 2017:

(i) A bill recevable for Rs.5,000 previously discounted with the dark had been dishonored and debited in the pass book.

(ii) Interset on investment collected by the bank and credited in the pass book Rs.1,500.

(iii) Cheques deposited into bank but not yet collected Rs.7,500.

(iv) Interset charged by the bank on overdraft balance Rs.1,850.

(v) Cheques issued but not yet presented for payment Rs.11,350.

(vi) Received a payment derectly from a customer into bank account Rs.12,500.

(vii) Cheques recorded in the cash book not sent to the bank for collection was Rs.17,500.

(viii) Bank charges debited as per pass book Rs.500.

Answer 20:

Question 21: From the following particulars, ascertain the Pass Book balance of M/s Deepak & Co. as on 31st March, 2024:

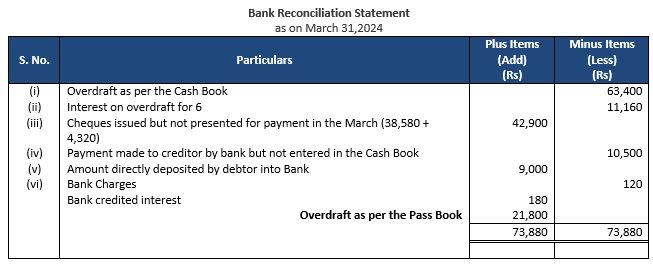

(i) Bank overdraft as per Cash Book on 31st March, 2024 Rs. 63,400.

(ii) Interest on overdraft for 6 month ending 31st March, 2024 Rs. 1,600 is entered in the Pass book.

(iii) Bank charges for Rs. 300 for the above period are debited in the Pass book.

(iv) Cheque issued but not presented for payment before 31st March, 2024 amounted to Rs. 11,600.

(v) Cheque deposited into bank but not cleared before 31st march, 2024 were for Rs. 21,700.

(vi) Interest on Investments collected by the bank in the Pass Book Rs. 12,000.

Answer 21:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

Point (vii) will have no effect on the statement as error in recording cash deposit entry is already rectified by the bank before 31st March, 2018

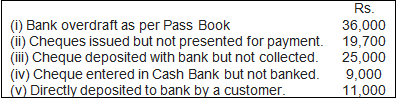

Question 22: From the following information, prepare Bank Reconciliation Statement as on 31st March, 2024:

Answer 22:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

1. The Amount directly deposited by the customer in the bank, So the same amount would be deducted from the overdraft balance as per the pass book.

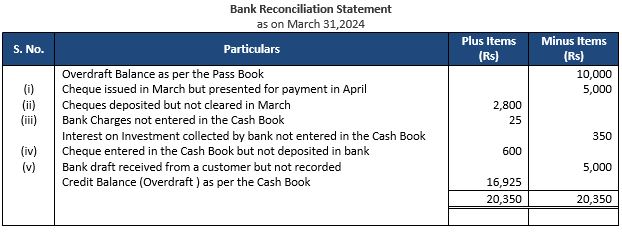

Question 23: On 31st March, 2024, Pass Book of Sapna shows debit balance of Rs. 10,000. From the following particulars, prepare Bank Reconciliation Statement.

(i) Cheques amounting to Rs. 8,000 drawn on 25th March 2024 of which cheques of Rs. 5,000 cashed in April, 2024.

(ii) Cheques paid into bank for collection of Rs. 5,000 but cheques of Rs. 2,200 could only be collected in March 2024.

(iii) Bank charges Rs. 25 and dividend of Rs. 350 on investment collected by bank could not be shown in the Cash Book.

(iv) A cheque of Rs. 600 debited in the Cash Book omitted to be banked.

(v) Bank draft of Rs. 5,000 received from a customer was deposited but not recorded in the Cash Book.

Answer 23:

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance (Overdraft) as per the Cash Book is Rs.16,925

Point of Knowledge:

Bill discounted with bank Rs. 5000 not recorded in the cash book, will be deducted from the overdraft balance of pass book.

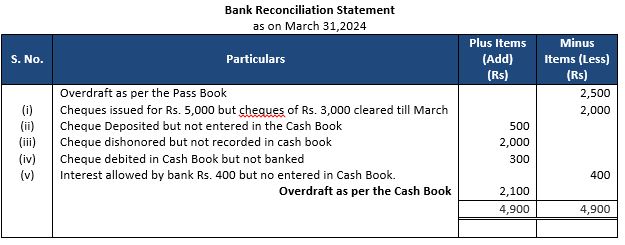

Question 24: Prepare Bank Reconciliation Statement from the following particulars as on 31st March, 2024, when Pass Book shows a debit balance of Rs. 2,500:

(i) Cheque issued for Rs. 5,000 but up to 31st March, 2024 only Rs. 3,000 could be cleared.

(ii) Cheques deposited for Rs. 5,500 but cheques for Rs 500 were collected on 10th April 2024.

(iii) cheque for Rs. 2,000 was dishonored but was not recorded in cash book.

(iv) A cheque of Rs. 300 debited in Cash Book but omitted to be banked.

(v) Interest allowed by bank Rs. 400 but no entry was passed in the Cash Book.

Answer 24:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

Interest allowed by the bank of Rs. 400 not recorded in the Cash Book, so it would be deducted from the overdraft balance of pass book.

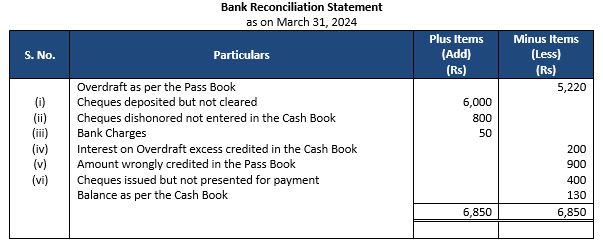

Question 25: On checking the Bank Pass Book it was found that it showed an overdraft of Rs. 5,220 as on 31st March, 2024, while as per Ledger it was different. The following differences were noted:

(i) Cheques deposited but not yet credited by the bank Rs. 6,000.

(ii) Cheques dishonored and debited by the bank but not given effect to it in the Ledger Rs. 800.

(iii) Bank charges debited by the bank but Debit Memo not received from the bank Rs. 50.

(iv) Interest on overdraft excess credited in the Ledger Rs. 200.

(v) Wrongly credited by the bank to account, deposit of some other party Rs. 900.

(vi) Cheques issued but not presented for payment Rs. 400.

Answer 25:

Statement of Bank Reconciliation on the basis of the given transactions:

Point of Knowledge:

Interest on overdraft of excess amount has been credited in the cash book, so the same amount will be deducted from the overdraft as per pass book.

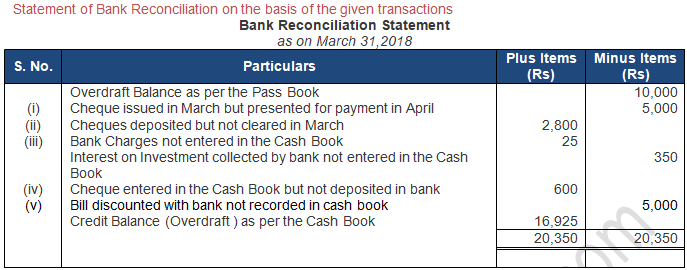

Question 26: On 31st March, 2018, Pass Book of Shri Bhama Shah shows debit balance of Rs 10,000. From the following particulars, prepare Bank Reconciliation Statement.

(i) Cheques amounting to Rs 8,000 drawn on 25th March of which cheques of Rs 5,000 cashed in April, 2018.

(ii) Cheques paid into bank for collection of Rs 5,000 but cheques of Rs 2,200 could only be collected in March 2018.

(iii) Bank charges Rs 25 and dividend of Rs 350 on investment collected by bank could not be shown in the Cash Book.

(iv) A cheque of Rs 600 debited in the Cash Book omitted to be banked.

(v) Bill of Rs 5,000 discounted with Bank but was not recorded in the Cash Book.

Answer 26:

Point of Knowledge:

1. Bill discounted with bank Rs. 5000 not recorded in the cash book, will be deducted from the overdraft balance of pass book.

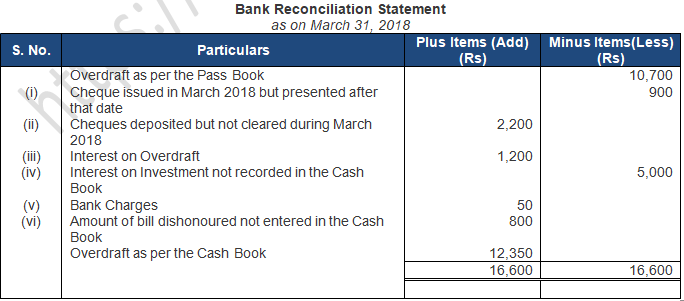

Question 27: On 31st March, 2018, Bank Pass Book of Naresh & Co. showed an overdraft of Rs 10,700. From the following particulars, prepare Bank Reconciliation Statement: (Old Question)

(i) Cheques issued before 31st March, 2018 but presented for payment after that date amounted to Rs 900.

(ii) Cheques paid into the bank but not collected and credited unitl 31st March, 2018 amounted to Rs 2,200.

(iii) Interest on overdraft amounting to Rs 1,200 did not appear in the Cash Book.

(iii) Rs 5,000 being interest on investments collected by the bank and credited in the Pass Book were not shown in the Cash Book.

(iv) Bank charges of Rs 50 were not entered in the Cash Book.

(v) Rs 800 in respect of dishonoured cheque were intered in the Pass Book but not in the Cash Book.

Answer 27:

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance (Overdraft) as per the Cash Book is Rs.12,350

Point of Knowledge:

1. Interest on overdraft Rs. 1200 would be added in the overdraft amount of Pass book because adding the amount will increase the overdraft balance as per the bank.

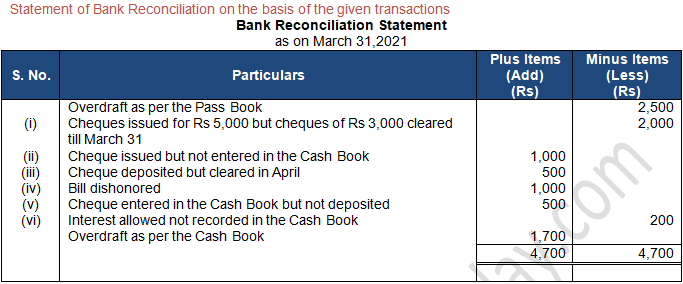

Question 28: Prepare Bank Reconciliation Statement from the following particulars as on 31st March, 2021, when Pass Book shows a debit balance of Rs. 2,500:

(i) Cheque issued for Rs. 5,000 but up to 31st March, 2021 only Rs. 3,000 could be cleared.

(ii) Cheques issued for Rs. 1,000 but omitted to be recorded in the Cash Book.

(iii) Cheques deposited for Rs. 5,500 but Cheques for Rs. 500 were collected on 4th April 2021.

(iv) A discounted Bill of exchange dishonored Rs. 1,000.

(v) A cheque of Rs 500 debited in Cash Book but omitted to be banked.

(vi) Interest allowed by bank Rs 200 but no entry was passed in the Cash Book.

Answer 28:

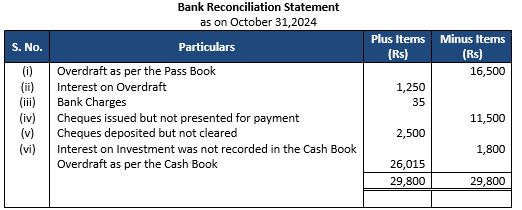

Question 29: From the following particulars, you are required to ascertain the bank balance as would appear in the Cash Book of Ramesh as on 31st October, 2023:

(i) Bank Pass Book showed an overdraft of Rs. 16,500 on 31st October.

(ii) Interest of Rs. 1,250 on overdraft up to 31st October, 2023 has been debited in the Bank Pass Book but it has not been entered in the Cash Book.

(iii) Bank charges debited in the Bank Pass Book amounted to Rs. 35.

(iv) Cheques issued prior to 31st October, 2023 but not presented till that date, amounted of Rs. 11,500.

(v) Cheques paid into bank before 31st October, but not collected and credited up to that date, were for Rs. 2,500.

(vi) Interest on investment collected by the bankers and credited in the Bank Pass Book amounted to Rs. 1,800.

Answer 29:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

Interest on overdraft Rs. 1250 would be added in the overdraft amount of Pass book because adding the amount will increase the overdraft balance as per the bank.

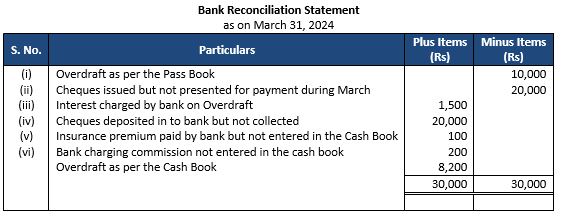

Question 30: From the following particulars of Gurpeet, prepare Bank Reconciliation statement showing the balance as per Cash Book on 31st March, 2024.

(i) Balance as per Pass Book on 31st March, 2024 overdrawn Rs. 10,000.

(ii) Cheques drawn in the last week of March, 2024 but not cleared till 3rd April, 2024 Rs. 20,000.

(iii) Interest on bank overdraft not entered in the Cash Book Rs. 1,500.

(iv) Cheques of Rs. 20,000 deposited in the bank in March, 2024 but not collected and credited till 3rd April, 2024.

(v) Rs. 100 Insurance premium paid by the bank under a standing order has not been entered in the Cash Book.

(iv) A draft of Rs. 10,000 favoring Atul & Co. was issued by the bank charging commission of Rs. 200. However, in the Cash Book entry was passed by Rs. 10,000.

Answer 30:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

Interest charges by bank on overdraft Rs. 1500 would be added in the overdraft amount of Pass book because adding the amount will increase the overdraft balance as per the bank.

Question 31: Prepare Bank Reconciliation Statement as on 31st March, 2024 from the following particulars:

(i) Raj's overdraft as per Pass Book Rs. 12,000 as on 31st March 2024.

(ii) On 30th March, cheques had been issued for Rs. 70,000 of which Cheques amounting to Rs. 3,000 only had been encashed up to 31st March.

(iii) Cheques amounting to Rs. 3,500 had been paid into the bank for collection but of these only Rs. 500 had been credited in the Pass Book.

(iv) Bank has charged Rs. 500 as interest on overdraft and the intimation of which has been received on 2nd April, 2024.

(v) Bank Pass Book shows credit for Rs. 1,000 representing Rs. 400 paid by debtor of R direct into the bank and Rs. 600 collected directly by the bank in respect of interest on Raj's investment. Raj had no knowledge of these items.

(vi) A cheque for Rs. 200 has been debited in the bank column of Cash Book by Raj but it was not sent to the bank at all.

Answer 31:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

A Cheque amounting Rs. 200 recorded in the Cash Book but not sent to the bank for collection, added back to the overdraft balance as per the pass book.

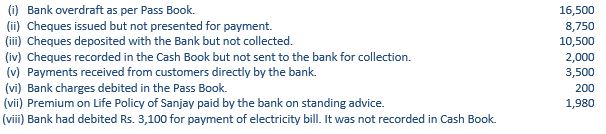

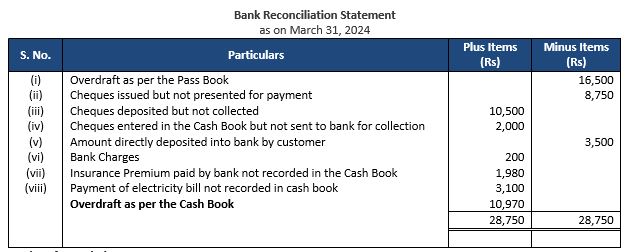

Question 32: From the following information supplied by Sanjay, prepare his Bank Reconciliation Statement as on 31st March, 2024

Answer 32:

Statement of Bank Reconciliation on the basis of the given transactions

Point of Knowledge:

The insurance premium paid by the bank is Rs. 1980 but the same amount has not been recorded in the cash book, so at the time of reconciliation the amount will be added in the overdraft balance of the pass book.

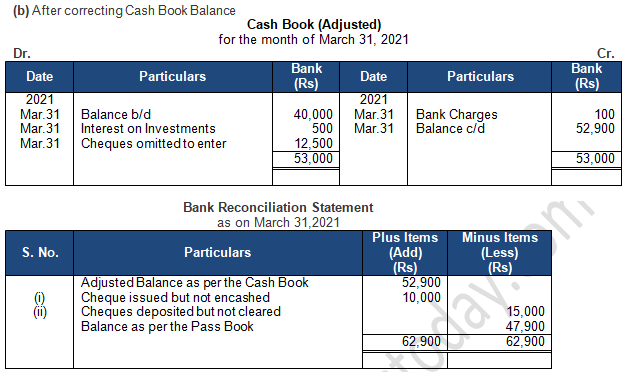

Question 33: From the following particulars, ascertain the bank balance as per Pass Book as on 31st March, 2021 (a) without correcting the Cash Book balance and (b) after correcting the Cash Book balance:

(i) The bank balance as per Cash Book on 31st March, 2021 Rs 40,000.

(ii) Cheques issued but not encashed up to 31st March, 2021 amounted to Rs 10,000.

(iii) Cheques paid into the bank, but not cleared up to 31st March, 2021 amounted to Rs 15,000.

(iv) Interest on investments collected by the bank but not entered in the Cash Book Rs 500.

(v) Cheques deposited in the bank but not entered in the Cash Book Rs 12,500.

(vi) Bank charges debited in the Pass Book but not entered in the Cash Book Rs 100.

Answer 33:

Point of Knowledge:

At the end of the financial year, the cash book must be adjusted for the entries that should be incorporated but have not been incorporated, before preparing the Bank Reconciliation Statement.

Following procedure is to be followed for ascertaining the adjusted Cash Balance:

Step 1- Draw up Cash Book having only bank column. If favourable balance as per Cash book is given, write it on debit side and if unfavourable balance is given write down the balance on the credit side of the Cash Book.

Step 2- Pass entries in the Cash book in respect of following items:

- Amount recorded in the pass book but not yet recorded in the Cash book.

- Rectifying entries in respect of errors committed in the cash book.

Step 3- The adjusted balance of the cash book is taken as starting point. The bank reconciliation statement with amended and adjusted Cash book is prepared.

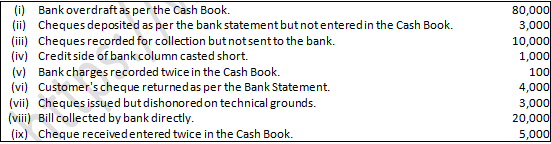

Question 34: From the following particulars, find out corrected bank balance as per Cash Book and thereafter prepare a Bank Reconciliation Statement as on 31st March, 2021 of a sole proprietor:

Answer 34:

Point of Knowledge:

At the end of the financial year, the cash book must be adjusted for the entries that should be incorporated but have not been incorporated, before preparing the Bank Reconciliation Statement.

Following procedure is to be followed for ascertaining the adjusted Cash Balance:

Step 1- Draw up Cash Book having only bank column. If favourable balance as per Cash book is given, write it on debit side and if unfavourable balance is given write down the balance on the credit side of the Cash Book.

Step 2- Pass entries in the Cash book in respect of following items:

(a) Amount recorded in the pass book but not yet recorded in the Cash book.

(b) Rectifying entries in respect of errors committed in the cash book.

Step 3- The adjusted balance of the cash book is taken as starting point. The bank reconciliation statement with amended and adjusted Cash book is prepared.

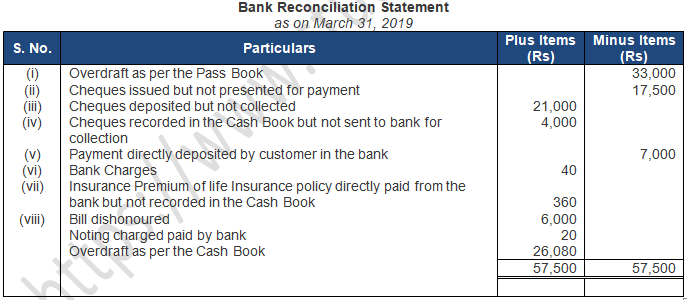

Question 35: From the following information supplied by Mr. D.H., prepare his Bank Reconciliation Statement as on 31st March, 2019: (Old Question)

Answer 35:

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance (Overdraft) as per the Cash Book is Rs.26,080

Point of Knowledge:

1. Cheques amounted Rs. 4000 recorded in the Cash Book but not sent to the bank for collection, added back to the overdraft balance as per the pass book.

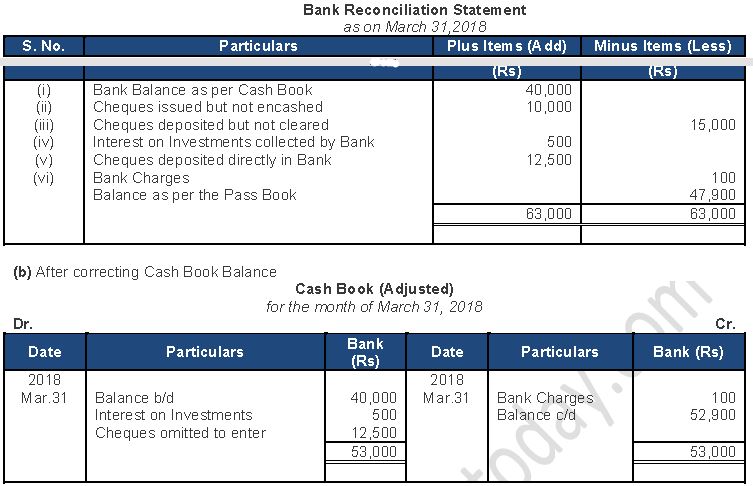

Question 36: From the following particulars, ascertain the bank balance as per Pass Book as on 31st March, 2018 (a) without correcting the Cash Book balance and (b) after correcting the Cash Book balance:

(i) The bank balance as per Cash Book on 31st March, 2018 Rs 40,000.

(ii) Cheques issued but not encashed up to 31st March, 2018 amounted to Rs 10,000.

(iii) Cheques paid into the bank, but not cleared up to 31st March, 2018 amounted to Rs 15,000.

(iv) Interest on investments collected by the bank but not entered in the Cash Book Rs 500.

(v) Cheques deposited in the bank but not entered in the Cash Book Rs 12,500.

(vi) Bank charges debited in the Pass Book but not entered in the Cash Book Rs 100.

Answer 36:

Statement of Bank Reconciliation on the basis of the given transactions

(a) Without correcting Cash Book Balance

Credit Balance as per the Pass Book is Rs.47,900

Point of Knowledge:

1. At the end of the financial year, the cash book must be adjusted for the entries that should be incorporated but have not been incorporated, before preparing the Bank Reconciliation Statement.

Following procedure is to be followed for ascertaining the adjusted Cash Balance:

Step 1- Draw up Cash Book having only bank column. If favourable balance as per Cash book is

given, write it on debit side and if unfavourable balance is given write down the balance on the

credit side of the Cash Book.

Step 2- Pass entries in the Cash book in respect of following items:

A. Amount recorded in the pass book but not yet recorded in the Cash book.

B. Rectifying entries in respect of errors committed in the cash book.

Step 3- The adjusted balance of the cash book is taken as starting point. The bank reconciliation statement with amended and adjusted Cash book is prepared.

Question 37: From the following particulars, find out corrected bank balance as per Cash Book and thereafter prepare a Bank Reconciliation Statement as on 31st March, 2018 of a sole proprietor:

Answer 37:

Statement of Bank Reconciliation on the basis of the given transactions

Debit Balance (Overdraft) as per the Pass Book is Rs.73,900

Point of Knowledge:

1. At the end of the financial year, the cash book must be adjusted for the entries that should be incorporated but have not been incorporated, before preparing the Bank Reconciliation Statement.

Following procedure is to be followed for ascertaining the adjusted Cash Balance:

Step 1- Draw up Cash Book having only bank column. If favourable balance as per Cash book is given, write it on debit side and if unfavourable balance is given write down the balance on the credit side of the Cash Book.

Step 2- Pass entries in the Cash book in respect of following items:

(A) Amount recorded in the pass book but not yet recorded in the Cash book.

(B) Rectifying entries in respect of errors committed in the cash book.

Step 3- The adjusted balance of the cash book is taken as starting point. The bank reconciliation statement with amended and adjusted Cash book is prepared.

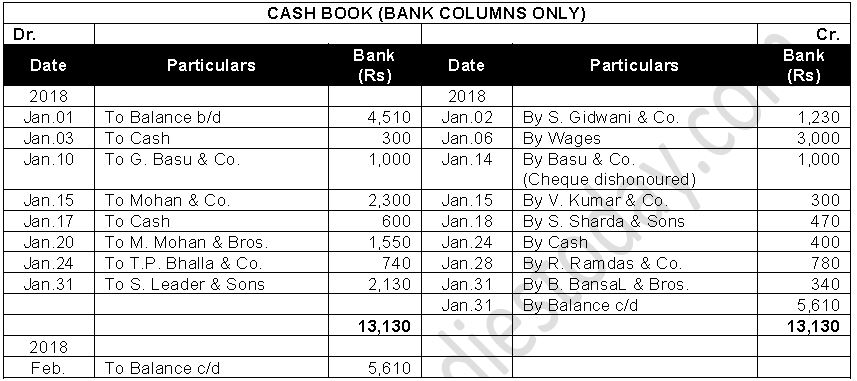

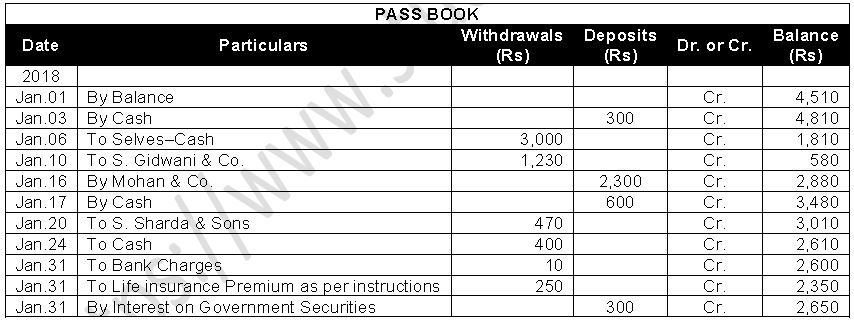

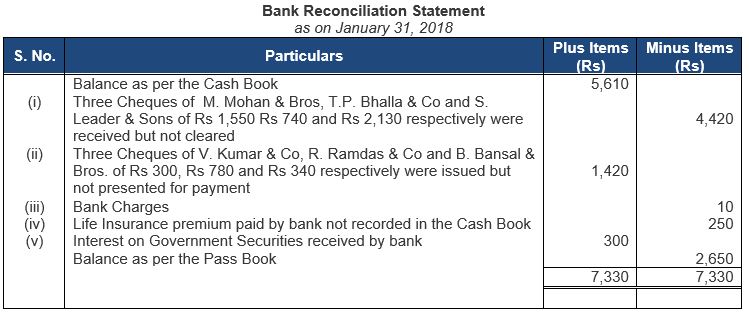

Question 38: From the following extracts from the Cash Book and the Pass Book for the month of January, 2018,

prepare Bank Reconciliation Statement:

Answer 38:

Statement of Bank Reconciliation on the basis of the given transactions

Credit Balance as per the Pass Book is Rs.2,650

Point of Knowledge:

1. At the end of the financial year, the cash book must be adjusted for the entries that should be incorporated but have not been incorporated, before preparing the Bank Reconciliation Statement.

Following procedure is to be followed for ascertaining the adjusted Cash Balance:

Step 1- Draw up Cash Book having only bank column. If favourable balance as per Cash book is given, write it on debit side and if unfavourable balance is given write down the balance on the credit side of the Cash Book.

Step 2- Pass entries in the Cash book in respect of following items:

(A) Amount recorded in the pass book but not yet recorded in the Cash book.

(B) Rectifying entries in respect of errors committed in the cash book.

Step 3- The adjusted balance of the cash book is taken as starting point. The bank reconciliation statement with amended and adjusted Cash book is prepared.

2. Cheque received from G. Basu & Co of Rs. 1000 is debited in the Cash book, thereafter at the time of dishonour entry is reversed by crediting G. Basu & Co with Rs. 1000. Therefore its effect is NIL in Cash book