Read TS Grewal Accountancy Class 11 Solution Chapter 7 Origin of Transactions Source Documents and Preparation of Voucher 2026. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 11 Accounts Chapter 7 Origin of Transactions Source Documents and Preparation of Voucher TS Grewal Solutions

TS Grewal Solutions for Chapter 7 Origin of Transactions Source Documents and Preparation of Voucher Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11.

Chapter 7 Origin of Transactions Source Documents and Preparation of Voucher TS Grewal Class 11 Solutions

Question.1. What is a Source Document?

Answer 1. The source documents are the information about the transaction based on which account are debited or credited with the transacted amount. A source Document is a written document containing details of the transaction. A source document is of prime importance in accounting because accounting is based on factual financial information that is evidence. The source documents are also known as supporting documents.

Question.2. Explain any two Source Documents.

Answer 2.

(a) Cash Memo: Cash Memo is prepared by the seller when goods are sold against cash. It has details of goods sold, quantity, rate of each item and the total amount received, besides the date of transaction and other terms and conditions, if any. It is an evidence for the purchaser for, goods purchased against cash, and for the enterprise, it is an evidence of sales for cash.

(b) Cheque: A cheque is a document in writing, drawn upon the bank with which the account is held and is payable on demand. The bank supplies the cheque forms. The name of the party to whom payment is to be made is written after the words ‘Pay to’. Then the amount is written- both in words and figures. A cheque must be dated and signed by the drawer. Each cheque has a counterfoil. The same details are entered on the counterfoil which remains with the account holder for future reference and is the source voucher recording the transaction in the books of account.

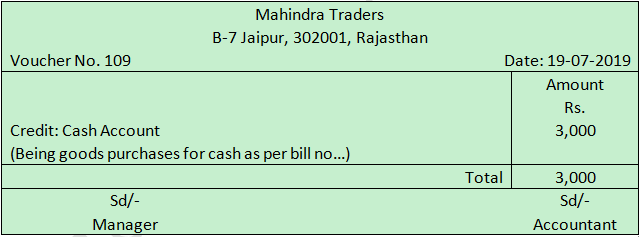

Question.3 What is a Voucher? Prepare an imaginary Specimen of Voucher.

Answer 3. A voucher is a document evidencing a business transaction. It flows from the above definition that when a transaction is entered into, evidence to that effect is also established. Such evidences are Source Documents. Examples of Source Documents are Cash Memo, Invoice or Bill, Receipt, Cheque, Debit Notes and Credit Notes. On the basis of Source Documents, a voucher detailing the accounts that are debited and credited is prepared.

The Specimen of a Credit Voucher is given below:

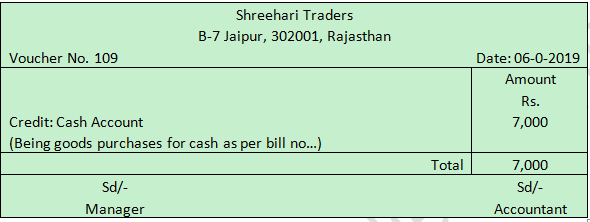

Question.4. Give an example of a ‘Voucher’.

Answer 4. Given an example for purchased goods worth Rs. 7,000 by Shreehari Traders for cash on 06-06-2019 for a Voucher:

The Specimen of a Credit Voucher is given below:

Question.5. What are Accounting Vouchers?

Answer 5. Accounting Voucher is a written document containing an analysis of business transaction for accounting and reporting purposes, prepared by the accountant on the basis of supporting voucher and signed by another authorised person. Before recording in the books of account, these source vouchers are analysed to determine which account or accounts are to be debited or credited. The decision is recorded on a document termed ‘Accounting Voucher’.

Question.6. Differentiate between Source Documents and Vouchers.

Answer 6:

1.) Source Documents:- Source Documents are documents which come into existence when a transaction is entered into.

Features of Source Voucher:

1. It is a written document.

2. It contains complete details of the transaction.

3. It is a proof of a transaction having taken place.

4. It is generally for a business transaction.

5. It is signed by the maker.

2.) Accounting Vouchers:- An Accountant has with him source or supporting vouchers for cash payments, cash receipts, invoices for credit purchases and sales. Yet, before recording in the books of account, these source vouchers are analysed to determine which account or accounts are to be debited and credited. The decision is recoded on a document termed ‘Accounting Vouchers’.

Features of Source Voucher:

1. It is written document.

2. It is prepared on the basis of evidence of the transaction, i.e., Source Document.

3. It is an analysis of a transaction.

4. It is prepared and signed usually by an Accountant and countersigned by the authorised signatory.

5. In the case of cash/bank voucher, it is receipt.

Question.7. What are the types of Accounting Vouchers?

or

Name the two type of voucher?

Answer7.

The following are the types of Accounting Vouchers:

(a) Cash Vouchers

(b) Non-Cash Vouchers or Transfer Vouchers.

Practical Problems :-->

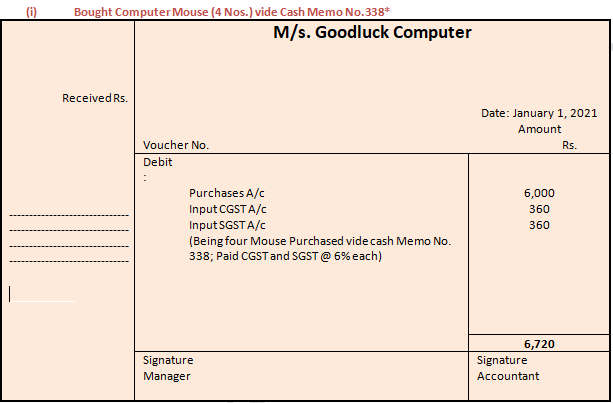

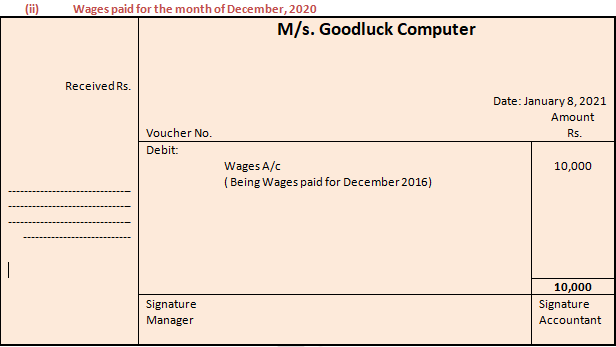

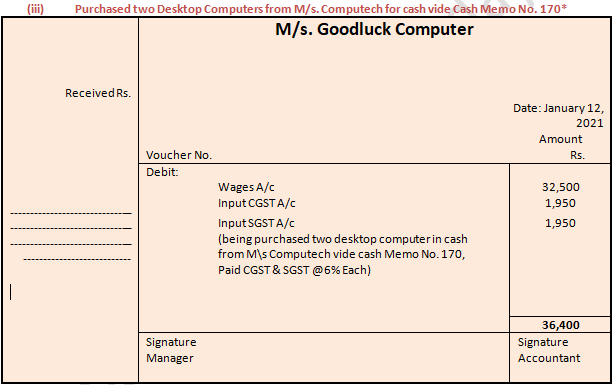

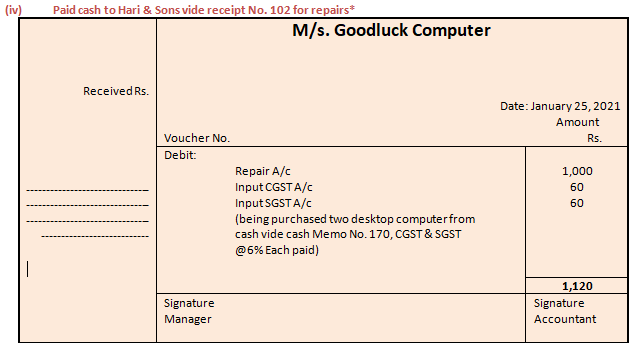

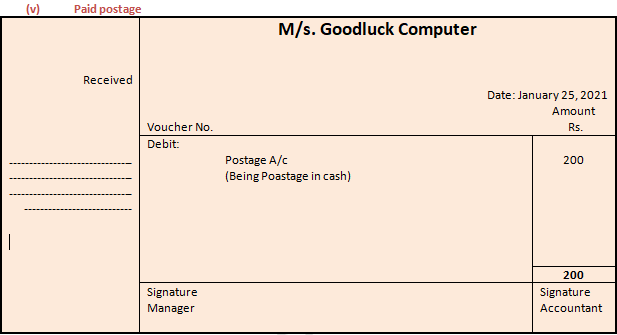

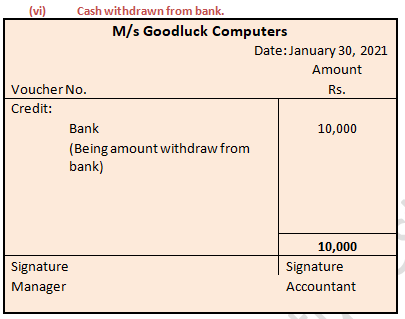

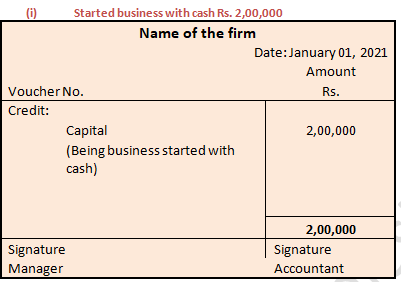

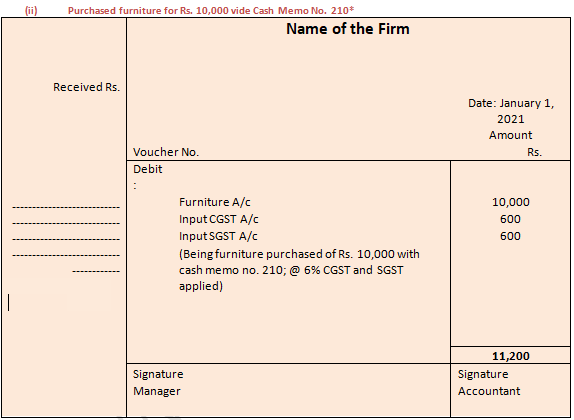

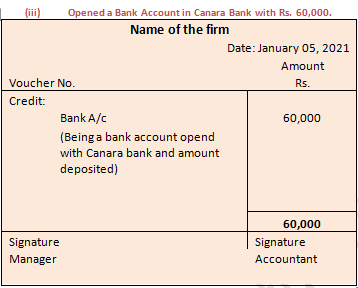

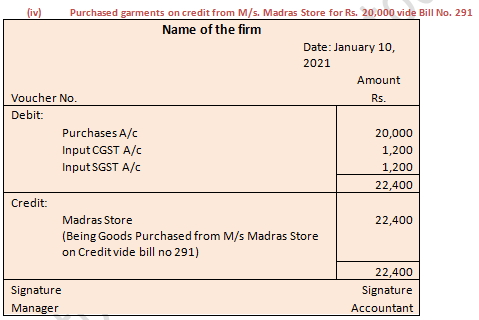

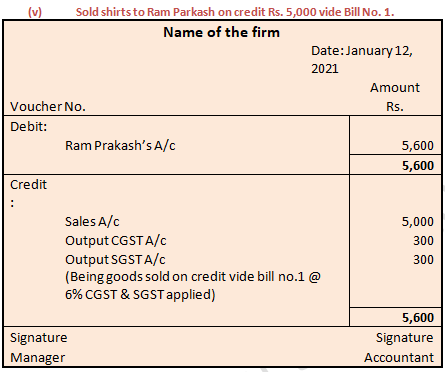

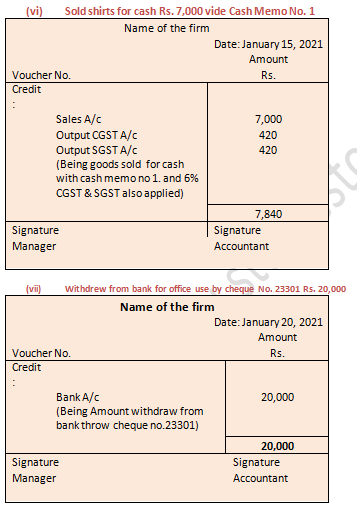

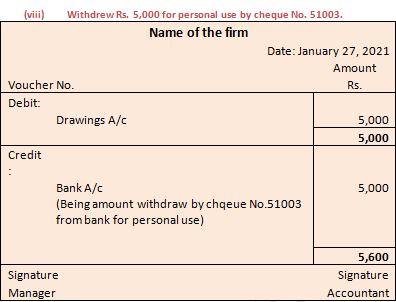

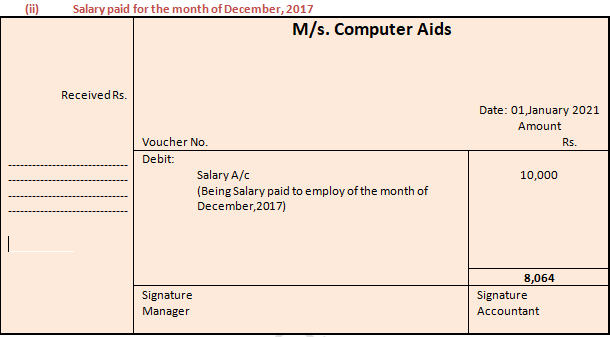

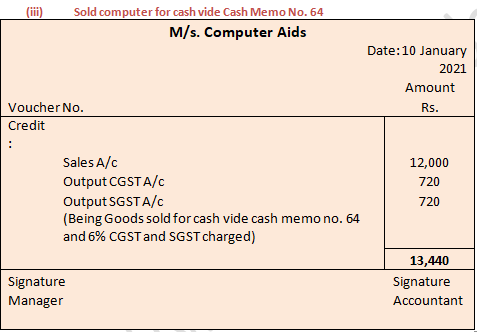

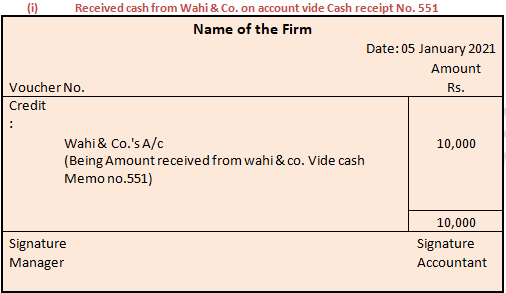

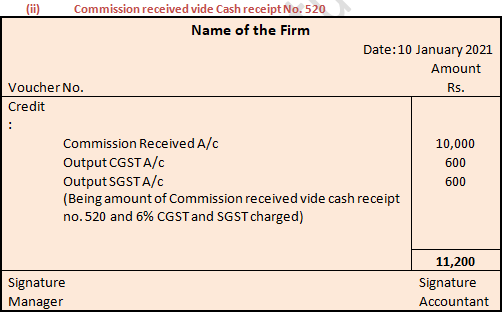

Question 1: The following transactions took place in M/s. Goodluck Computers. Prepare the Accounting Vouchers:

Transactions marked with * are subject to levy of CGST and SGST @ 6% each.

Answer 1:

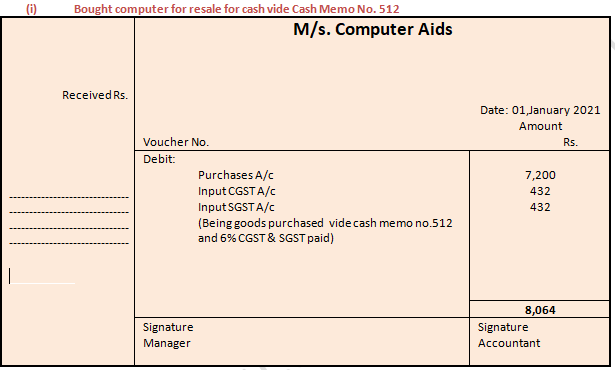

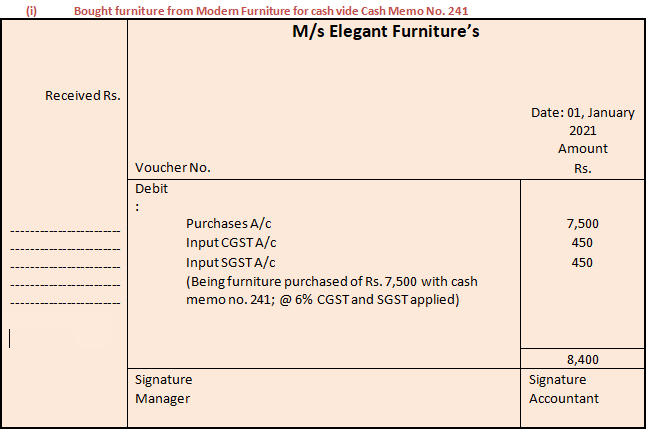

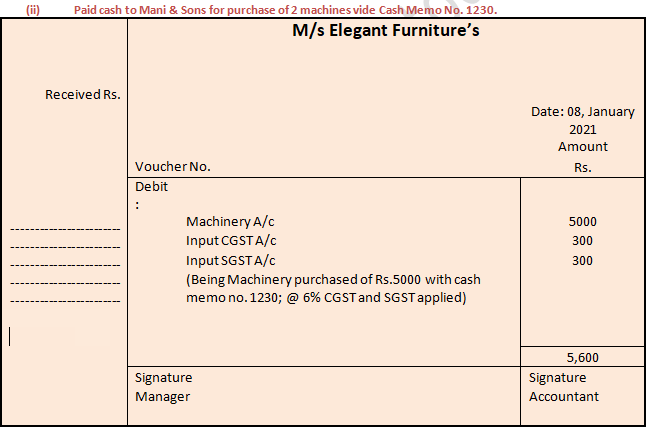

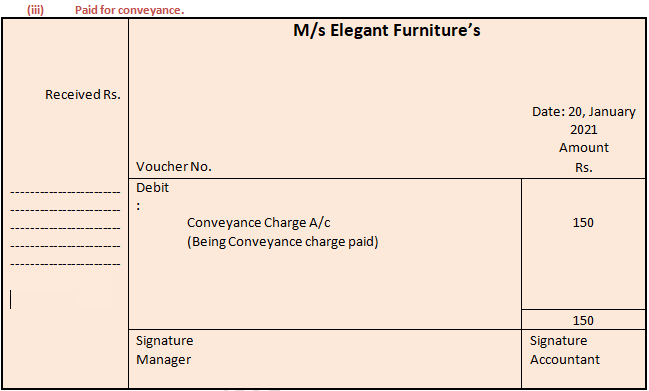

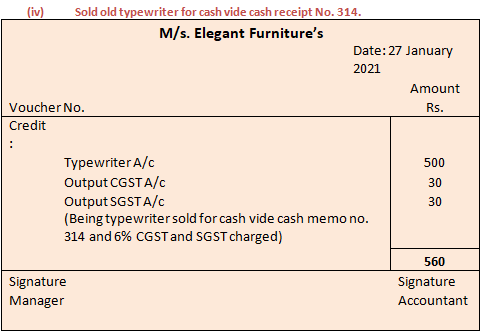

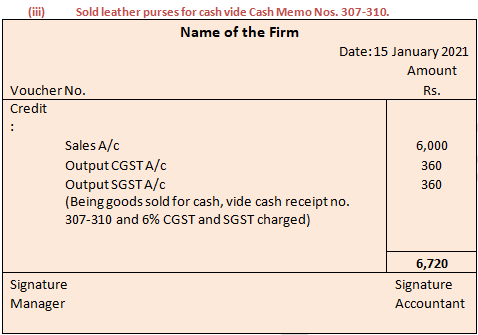

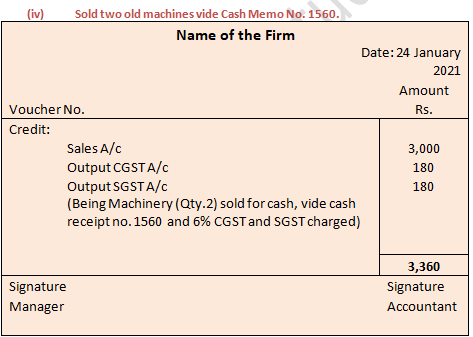

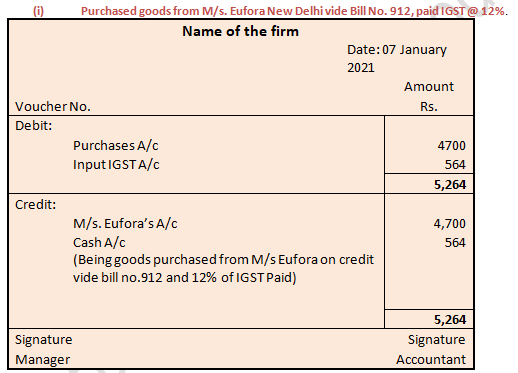

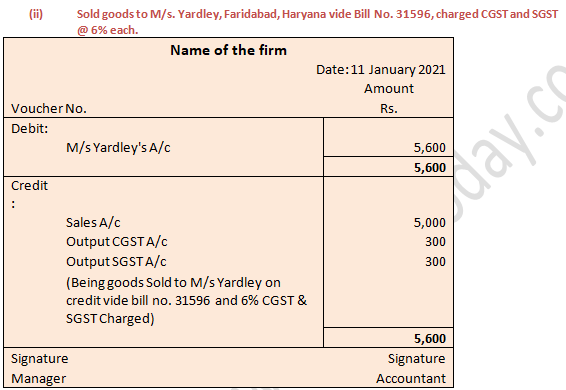

Question 2: Prepare the Accounting Vouchers for the following transactions:

Transactions marked with * are subject to levy of CGST and SGST @ 6% each.

Answer 2:

Transactions marked with * are subject to levy of CGST and SGST @ 6% each.

Answer 3:

Transactions marked with * are subject to levy of CGST and SGST @ 6% each.

Answer 4:

Transactions marked with * are subject to levy of CGST and SGST @ 6% each.

Answer 5:

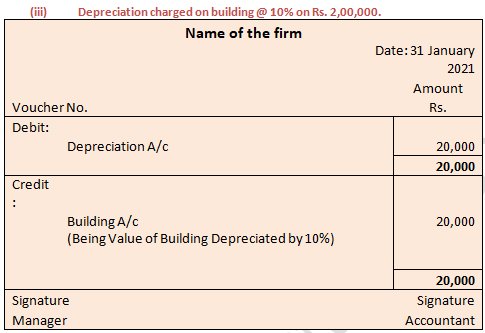

Solution 6:

Point of Knowledge:-

- Depreciation = Value of Assets × % of Depreciation

= Rs. 2,00,000 × 10%

= Rs. 20,000