Access free DK Goel Solutions Class 11 Accountancy Chapter 9 Books of Original Entry Journal 2026 below. Students can now access free DK Goel Solutions for Class 11 Accountancy. These chapter-wise exercises are designed by expert Accountancy teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Accountancy Chapter 9 Books of Original Entry Journal DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 9 Books of Original Entry Journal Class 11 Accountancy below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 9 Books of Original Entry Journal DK Goel Class 11 Solved Exercises

Very Short Questions

Question 1.

Solution 1: Journal is a book of prime entry or a book of original entry in which transaction are first recorded in a chronological order or sequence they are entered. Journal is called the Book of Original Entry since all transactions are initially recorded in it.

Question 2.

Solution 2: All the transactions are recorded firstly in the journal so it is called book of original entry.

Question 3.

Solution 3: The method of recording the transaction in the journal is called journalising.

Question 4. .

Solution 4: Recording of accounting data in chronological order is the advantage of journal.

Question 5.

Solution 5: It is impossible to record all the heavy and bulky transactions are the only limitation of journal.

Question 6.

Solution 6: All the transaction has a brief description after each entry is known as narrative.

Question 7.

Solution 7: Ledger folio or L.F. is the page number where the journal is posing made. The page number is recorded in the journal.

Question 8.

Solution 8: When two or more transactions related to one particular account take place on the same date. In this situation, instead of recording separate entries only one entry is passed. This type of journal entry is known as compound journal entry.

Question 9.

Solution 9: The first entry in the Journal is passed to record closing balances of the previous year. It is called the opening entry. The Balance Sheet prepared at the end of the year shows the closing balances of each asset and liability and forms the basis for this opening entry.

Question 10.

Solution 10: Drawings A/c Dr.

To Purchase A/c

Question 11.

Solution 11: Machine account.

Practical Questions

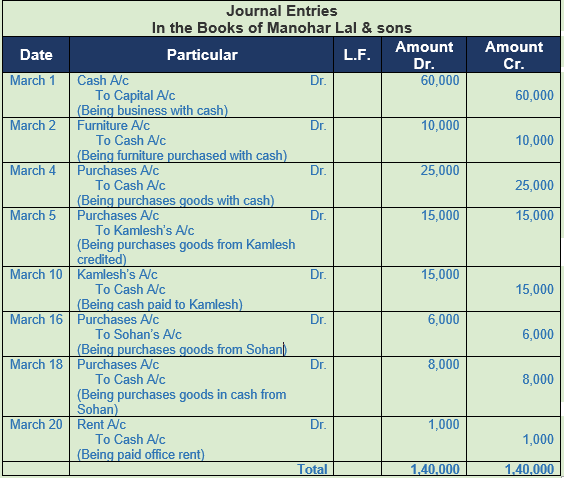

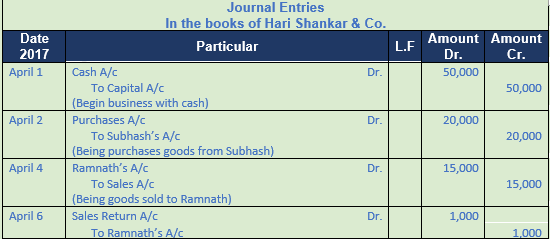

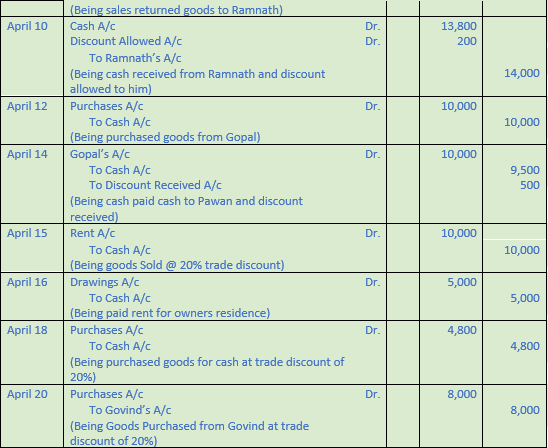

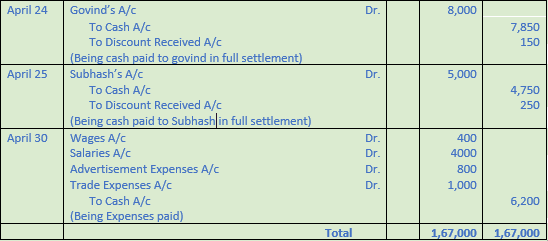

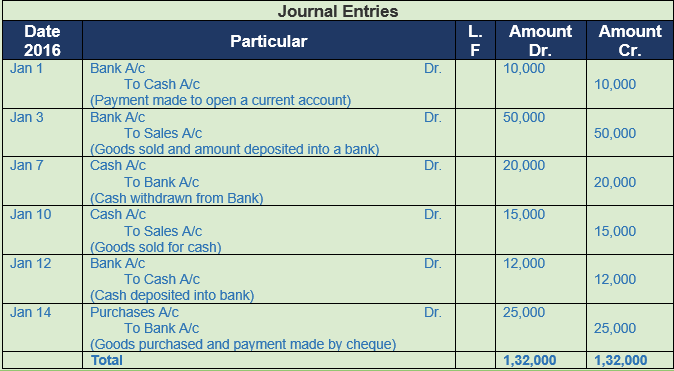

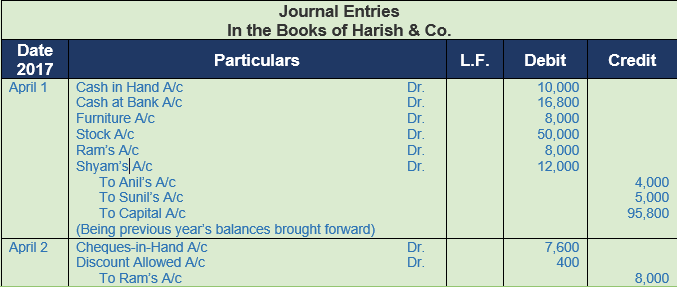

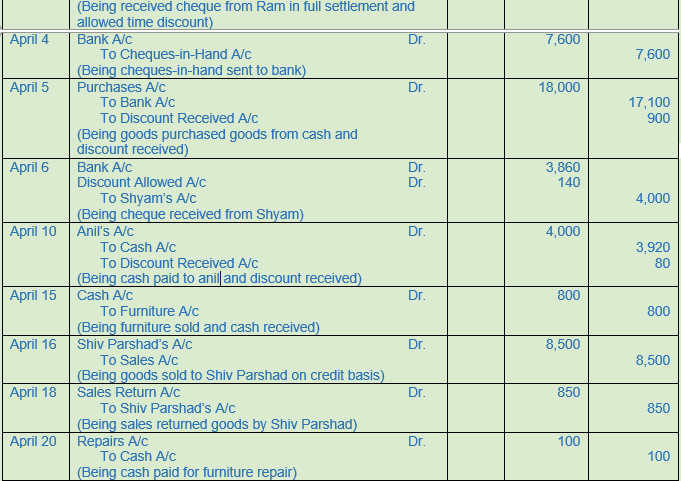

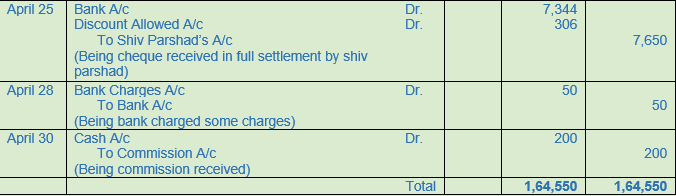

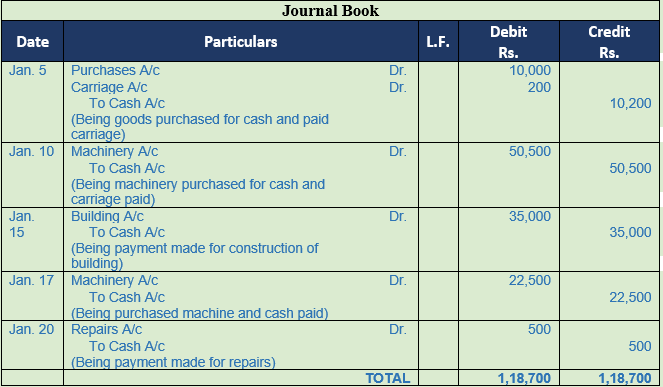

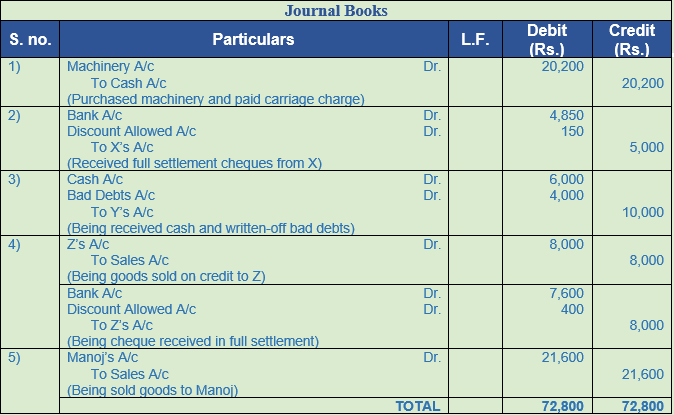

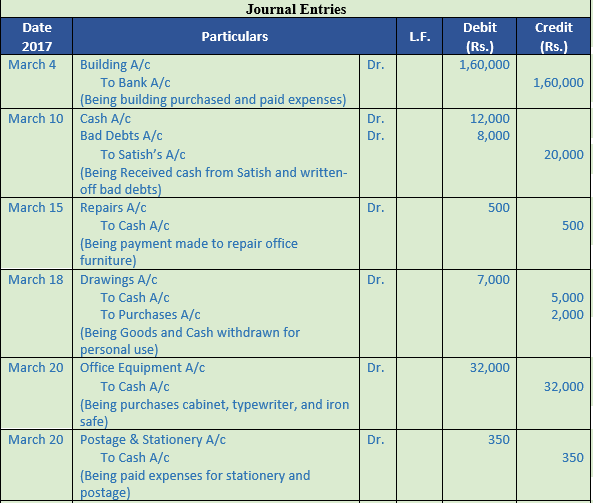

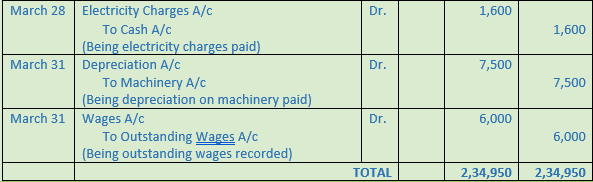

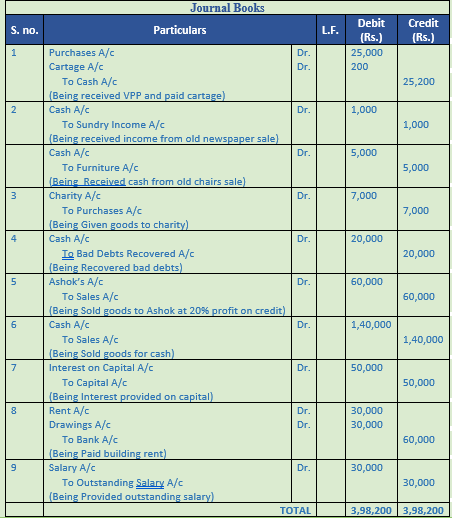

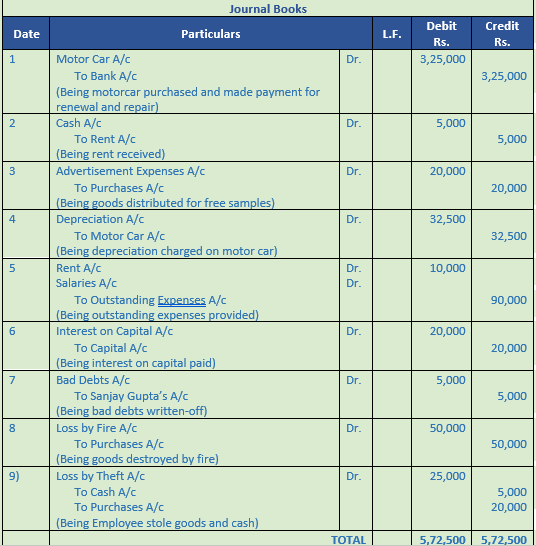

Question 1.

Solution 1:

Point of Knowledge:-

Journal is a book of prime entry or a book of original entry in which transaction are first recorded in a chronological order or sequence they are entered. Journal is called the Book of Original Entry since all transactions are initially recorded in it.

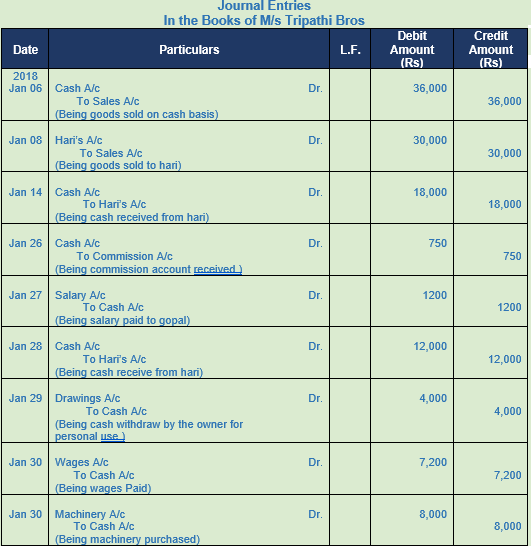

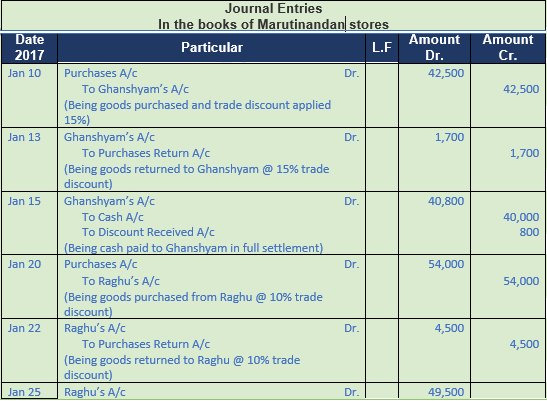

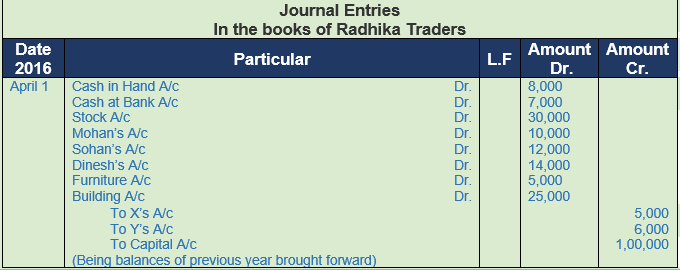

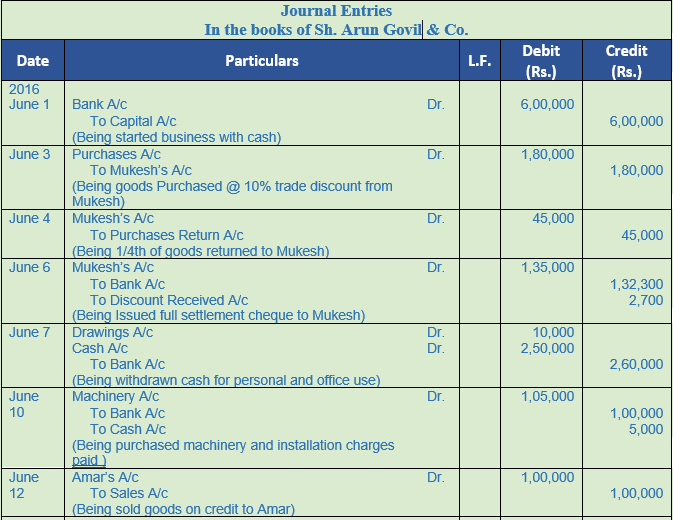

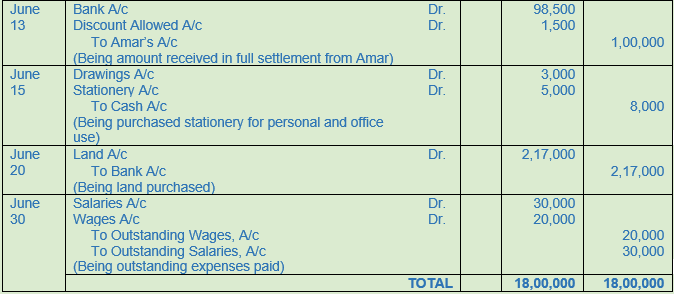

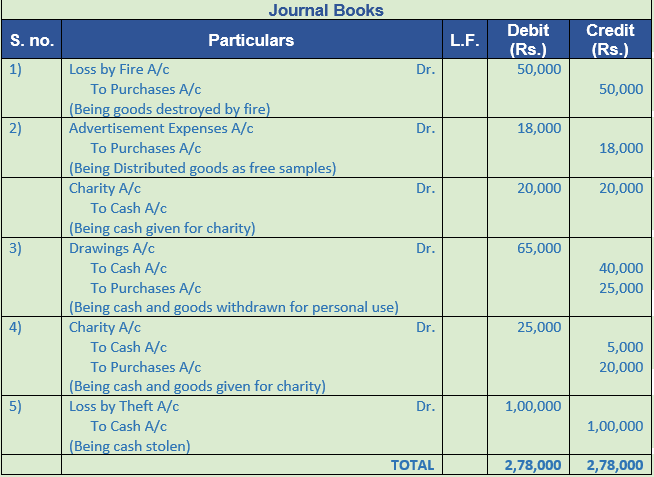

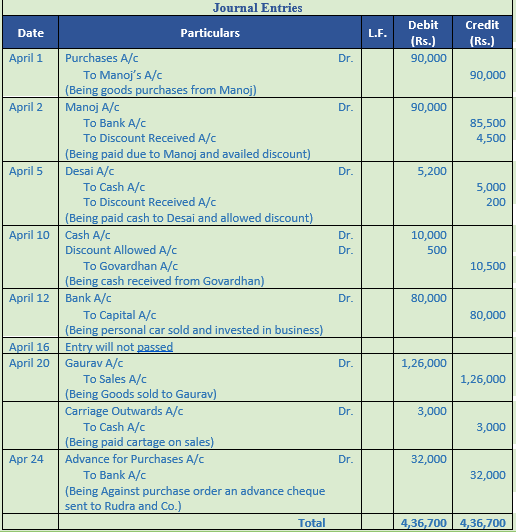

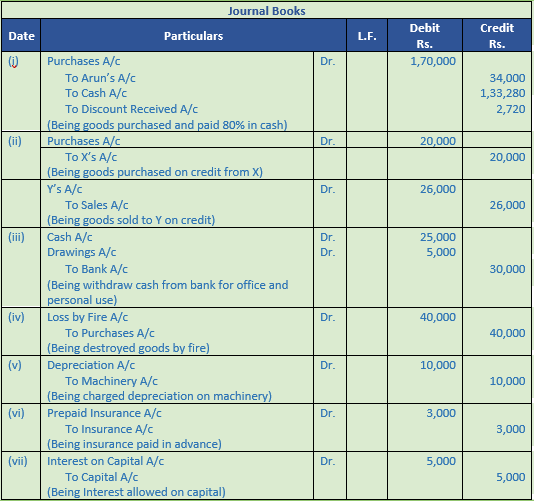

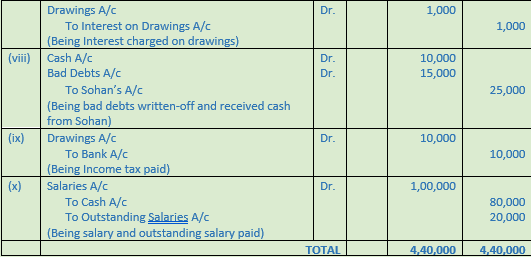

Question 2.

Solution 2:

Working Note:-

The first entry in the Journal is passed to record closing balances of the previous year. It is called the opening entry. The Balance Sheet prepared at the end of the year shows the closing balances of each asset and liability and forms the basis for this opening entry.

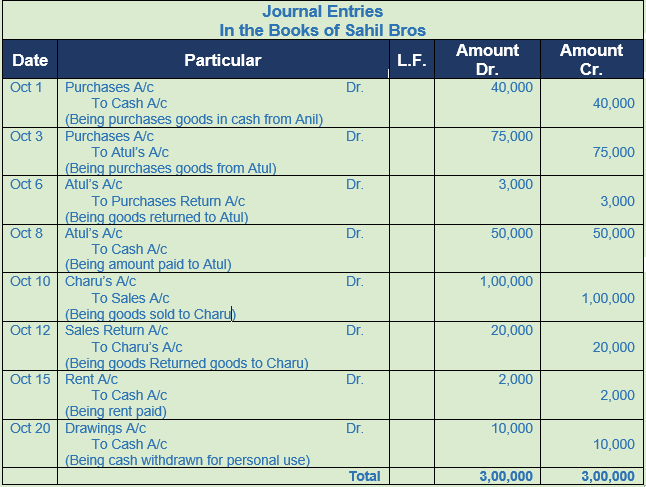

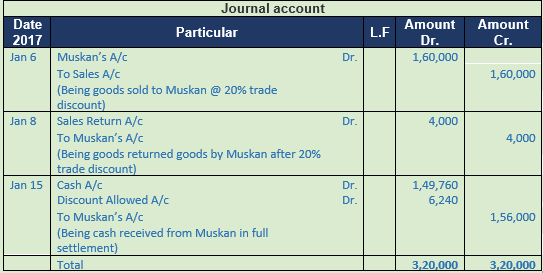

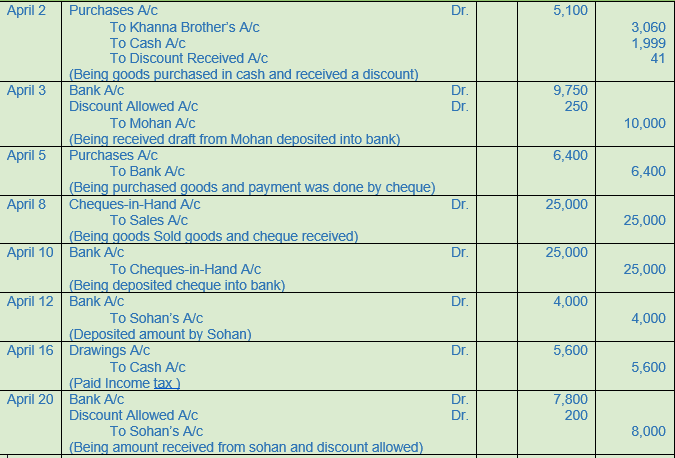

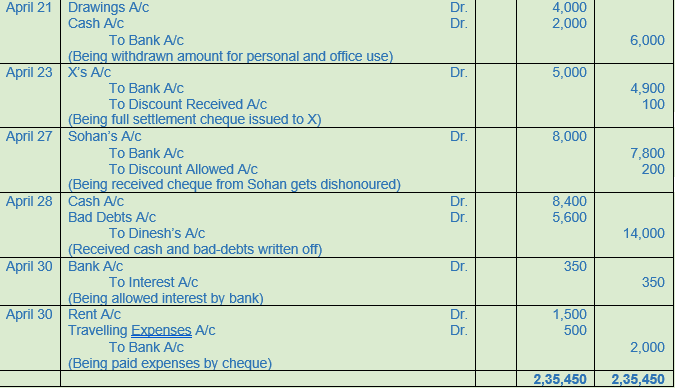

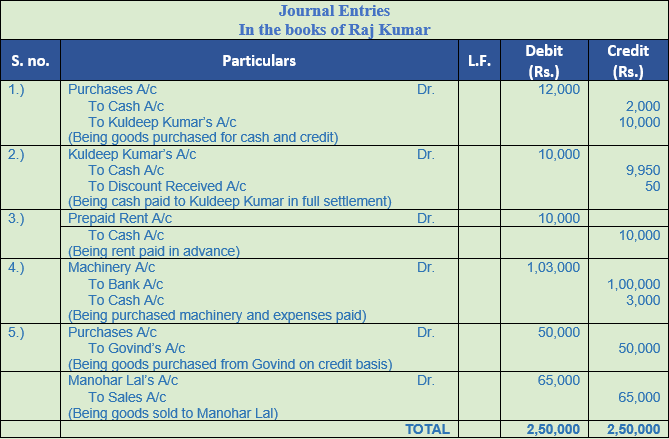

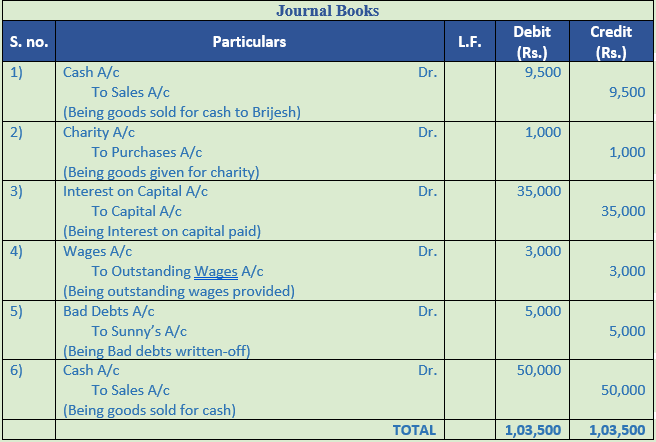

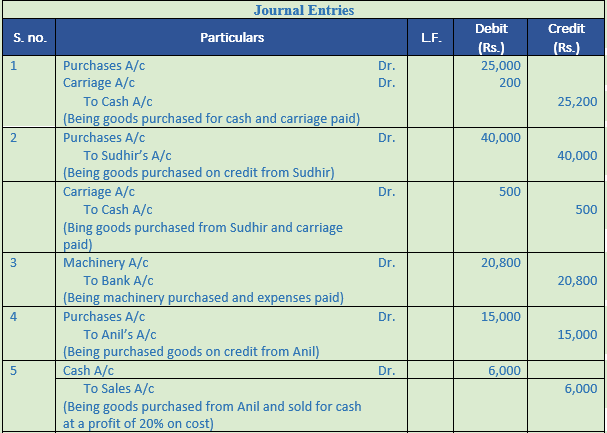

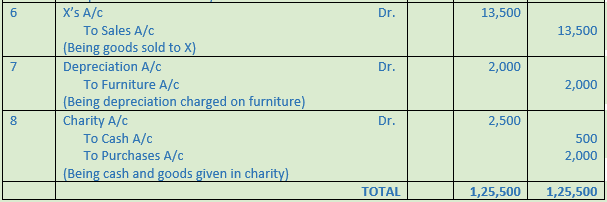

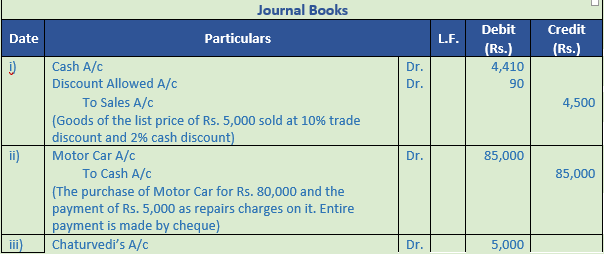

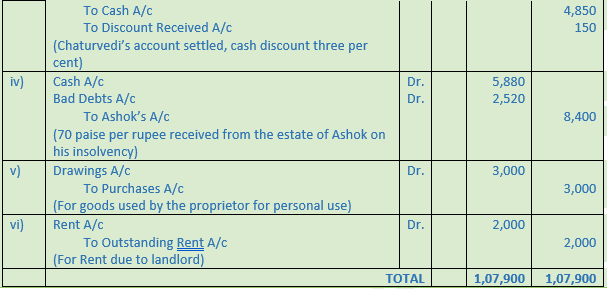

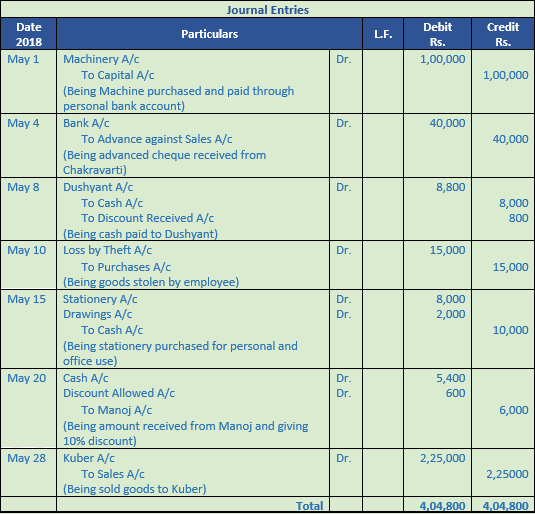

Question 3.

Solution 3:

Working Note:-

1.) Total Sales to Charu = 1,00,000

Sales Return = Rs. 1,00,000 × 20% = Rs. 20,000

Point of the Knowledge:-

- Capital Account is debited when there is a decrease in capital.

- Capital Account is credited when there is a increase in capital.

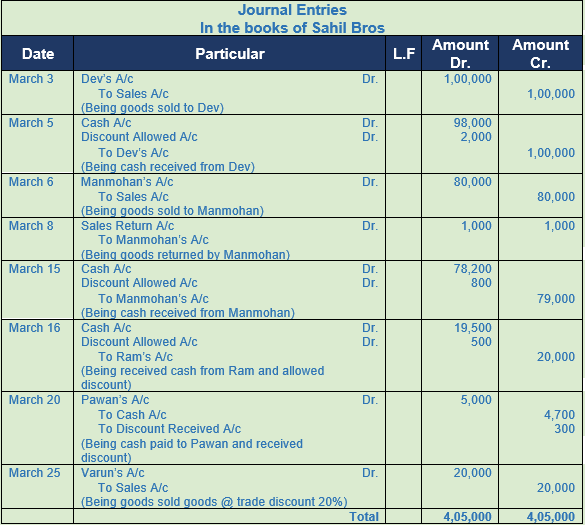

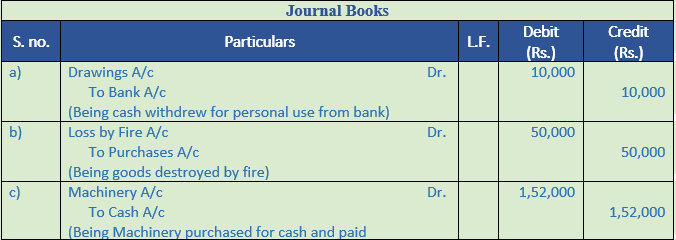

Question 4.

Solution 4:

Working Note:-

1.) Calculation of selling price

List price = Rs. 25,000

Trade discount = 20%

Trade Discount = Rs. 25,000 × 20% = Rs. 5,000

Sales = Rs. 25,000 – Rs. 5,000

Sales = Rs. 20,000

Point of Knowledge:-

The following are the two advantages of Journal.

- Recording of accounting data in chronological order.

- Narration of journal explains the transactions very well.

Solution 5:

Working Note:-

1.) Calculation of discount

Discount Amount = Rs. 10,000 × 5% = Rs. 500

Amount paid to Gopal = Rs. 10,000 – Rs. 500

= Rs. 9,500

Point of knowledge:-

Trade Discount is allowed by the seller on purchase of goods in large quantity. It is usually by the wholesalers to the retail shop owners who further sell the goods to the consumer. Trade Discount is deducted in the invoice from sale price and is not recorded in the books of account. Sales are recorded at net sales price or sale price less trade discount. GST or CGST, SGST and IGST are levied on the net sale price. Trade discount is allowed on sales, hence it is allowed on both cash and credit sales.

Question 6.

Solution 6:

Working Note:-

1.) Calculation of selling price

List price = Rs. 50,000

Trade discount = 15%

Trade Discount = Rs. 50,000 × 15% = Rs. 7,500

Sales = Rs. 50,000 – Rs. 7,500

Sales = Rs. 42,500

2.) Calculation of selling price

List price = Rs. 60,000

Trade discount = 10%

Trade Discount = Rs. 60,000 × 10% = Rs. 6,000

Sales = Rs. 60,000 – Rs. 6,000

Sales = Rs. 54,000

Point of knowledge:-

The following are the two advantages of allowing Trade Discount:

1.) Increased sales due to high quantity involved in sales.

2.) Increased customer base due to low prices and discount offers.

Question 7.

Solution 7:

Working Note:-

1.) Calculation of selling price

List price = Rs. 2,00,000

Trade discount = 20%

Trade Discount = Rs. 2,00,000 × 20% = Rs. 40,000

Sales = Rs. 2,00,000 – Rs. 40,000

Sales = Rs. 1,60,000

Point of Knowledge:-

Cash Discount is allowed by the seller to the customers to encourage prompt or early payment. It is allowed as a per cent of invoice value or payment made say @ 5% of invoice value to the buyer. Cash discount is calculated after deducting trade discount from the invoice price. Cash discount is calculated always on net amount. It is allowed at the time of receipt of amount in cash or by cheque.

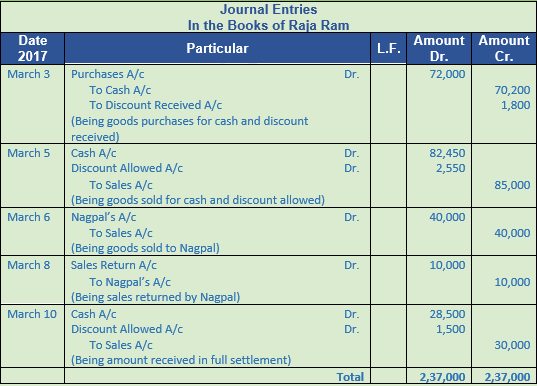

Question 8.

Solution 8:

Working Note:-

1.) Calculation of selling price

List price = Rs. 80,000

Trade Discount = 10%

Trade Discount = Rs. 80,000 × 10% = Rs. 8,000

Sales = Rs. 80,000 – Rs. 8,000

Sales = Rs. 72,000

Cash discount = 2.5%

Discount amount = Rs. 72,000 × 2.5%

= Rs. 1,800

Amount Received = Rs. 72,000 – Rs. 1,800

= Rs. 70,200

Point of knowledge:-

- Recording of accounting data in chronological order.

- Narration of journal explains the transactions very well.

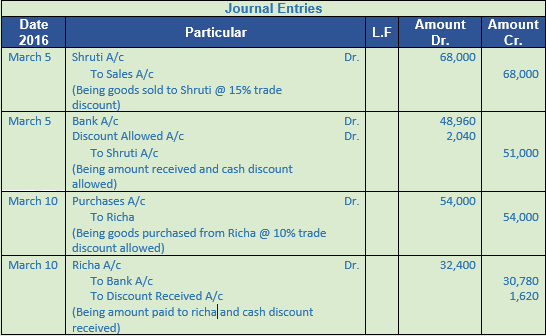

Question 9.

Solution 9:

Working Note:-

1.) Calculation of selling price

List price = Rs. 80,000

Trade Discount = 15%

Trade Discount = Rs. 80,000 × 15% = Rs. 12,000

Sales = Rs. 80,000 – Rs. 12,000

Sales = Rs. 68,000

Amount received in cash = Rs. 68000 × 75%

= Rs. 51,000

Cash discount = 4%

Discount amount = Rs. 51,000 × 4%

= Rs. 2,040

Amount Received = Rs. 51,000 – Rs. 2,020

= Rs. 48,960

2.) Calculation of purchases price

List price = Rs. 60,000

Trade Discount = 10%

Trade Discount = Rs. 60,000 × 10% = Rs. 6,000

Sales = Rs. 60,000 – Rs. 6,000

Sales = Rs. 54,000

Amount received in cash = Rs. 54,000 × 60%

= Rs. 32,400

Cash discount = 5%

Discount amount = Rs. 32,400 × 5%

= Rs. 1,620

Amount Received = Rs. 32,400 – Rs. 1,620

= Rs. 30,780

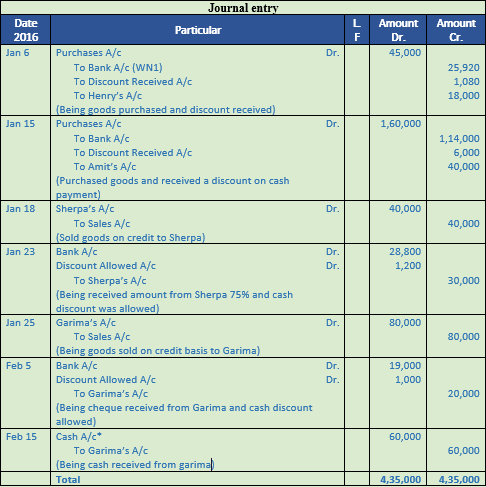

Question 10.

Solution 10:

Working Note:-

1.) Calculation of amount paid to hanry:-

List price = Rs. 50,000

Trade Discount = 10%

Trade Discount = Rs. 50,000 × 10% = Rs. 5,000

Sales = Rs. 50,000 – Rs. 5,000

Sales = Rs. 45,000

Amount received in cash = Rs. 45,000 × 60%

= Rs. 27,000

Cash discount = 4%

Discount amount = Rs. 27,000 × 4%

= Rs. 1,080

Amount Received = Rs. 27,000 – Rs. 1,080

= Rs. 25,920

Question 11.

Solution 11:

Working Note:-

List price = Rs. 2,50,000

Trade Discount = 20%

Trade Discount = Rs. 2,50,000 × 20% = Rs. 50,000

Sales = Rs. 2,50,000 – Rs. 50,000

Sales = Rs. 2,00,000

Amount received in cash = Rs. 1,20,000

Cash discount = 10%

Discount amount = Rs. 1,20,000 × 10%

= Rs. 12,000

Amount Received = Rs. 1,20,000 – Rs. 12,000

= Rs. 1,08,000

Point of Knowledge:-

Trade Discount is allowed by the seller on purchase of goods in large quantity. It is usually by the wholesalers to the retail shop owners who further sell the goods to the consumer. Trade Discount is deducted in the invoice from sale price and is not recorded in the books of account.

Question 12.

Solution 12:

Working Note:-

1.) Calculation of amount paid by bhushan:-

List price = Rs. 10,000

Trade Discount = 10%

Trade Discount = Rs. 1,00,000 × 10% = Rs. 1,000

Sales = Rs. 10,000 – Rs. 1,000

Sales = Rs. 9,000

Point of Knowledge:-

Trade Discount is allowed by the seller on purchase of goods in large quantity. It is usually by the wholesalers to the retail shop owners who further sell the goods to the consumer. Trade Discount is deducted in the invoice from sale price and is not recorded in the books of account.

Cash Discount is allowed by the seller to the customers to encourage prompt or early payment. It is allowed as a per cent of invoice value or payment made say @ 5% of invoice value to the buyer. Cash discount is calculated after deducting trade discount from the invoice price.

Question 13.

Solution 13:

Point of knowledge:-

1. Asset Accounts: Debit the increases, Credit the decreases.

2. Liability Accounts: Debit the decreases, Credit the increases.

3. Capital Accounts: Debit the decreases, Credit the increases.

4. Expense Accounts: Debit the increases, Credit the decreases.

Question 14.

Solution 14: (A)

Working Note:-

1.) Calculation of amount paid by bhushan:-

List price = Rs. 8,000

Trade Discount = 20%

Trade Discount = Rs. 8,000 × 20% = Rs. 1,600

Sales = Rs. 8,000 – Rs. 1,600

Sales = Rs. 6,400

Point of Knowledge:-

1.) Increased sales due to high quantity involved in sales.

2.) Increased customer base due to low prices and discount offers.

Question 14.

Solution 14: (B)

Working Note:-

List price = Rs. 20,000

Trade Discount = 10%

Trade Discount = Rs. 20,000 × 10% = Rs. 2,000

Sales = Rs. 20,000 – Rs. 2,000

Sales = Rs. 18,000

Cash discount = 5%

Discount amount = Rs. 18,000 × 5%

= Rs. 900

Amount Received = Rs. 18,000 – Rs. 900

= Rs. 17,100

Point of Knowledge:-

Trade Discount is allowed by the seller on purchase of goods in large quantity. It is usually by the wholesalers to the retail shop owners who further sell the goods to the consumer. Trade Discount is deducted in the invoice from sale price and is not recorded in the books of account.

Cash Discount is allowed by the seller to the customers to encourage prompt or early payment. It is allowed as a per cent of invoice value or payment made say @ 5% of invoice value to the buyer. Cash discount is calculated after deducting trade discount from the invoice price.

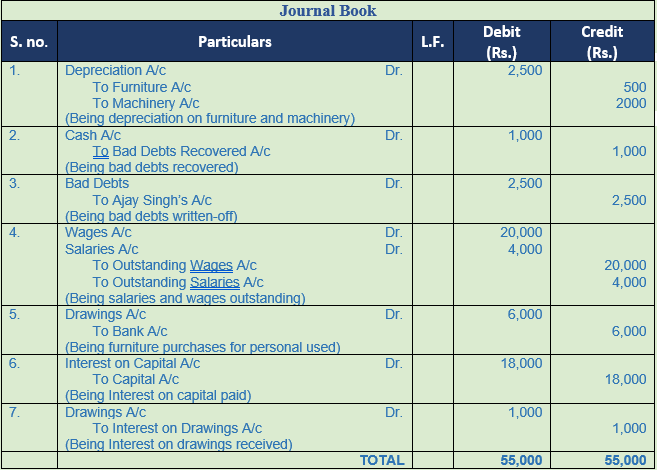

Question 15.

Solution 15:

Point of knowledge:-

- Asset Accounts: Debit the increases, Credit the decreases.

- Liability Accounts: Debit the decreases, Credit the increases.

- Capital Accounts: Debit the decreases, Credit the increases.

- Expense Accounts: Debit the increases, Credit the decreases.

Question 16.

Solution 16:

Question 17.

Solution 17:

Question 18.

Solution 18:

Point of Knowledge:-

Cash Discount allowed is debited to 'Discount Allowed Account' by the party receiving the amount and cash discount received is credited to 'Discount Received Account' by the party making the payment. Discount allowed or received is related to payment and thus, they are recorded in the books of account along with the entry recorded for payment and receipt of the amount, in cash or cheque. When cash discount is allowed or received GST or CGST, SGST, IGST is not levied since it is for early payment and not on sale or purchase of goods.

Question 19.

Solution 19:

Working Note:-

List price = Rs. 10,000

Trade Discount = 20%

Trade Discount = Rs. 10,000 × 20% = Rs. 2,000

Sales = Rs. 10,000 – Rs. 2,000

Sales = Rs. 8,000

Cash discount = 5%

Discount amount = Rs. 8,000 × 5%

= Rs. 400

Amount Received = Rs. 8,000 – Rs. 400

= Rs. 7,600

Point of Knowledge:-

Discount allowed or received is related to payment and thus, they are recorded in the books of account along with the entry recorded for payment and receipt of the amount, in cash or cheque. When cash discount is allowed or received GST or CGST, SGST, IGST is not levied since it is for early payment and not on sale or purchase of goods.

Question 20.

Solution 20:

Point of Knowledge:-

1. Asset Accounts: Debit the increases, Credit the decreases.

2. Liability Accounts: Debit the decreases, Credit the increases.

3. Capital Accounts: Debit the decreases, Credit the increases.

4. Expense Accounts: Debit the increases, Credit the decreases.

Question 21:

Solution 21:

Question 22.

Solution 22:

Point of Knowledge:-

1.) To record transactions of a particular head.

2.) To record the amount of a particular transaction.

3.) The record the effect of a transaction.

4.) To record the direction of a transaction.

Question 23.

Solution 23:

Question 24.

Solution 24:

Question 25.

Solution 25:

Question 26.

Solution 26:

Question 27.

Solution 27:

Question 28.

Solution 28:

Question 29.

Solution 29:

Question 30.

Solution 30:

Question 31.

Solution 31:

Working Note:-

Calculation Selling price of the goods sold to M/s Kalu & Sons

Cost = Rs. 60,000

Profit = Rs. 60,000 × 10%

= Rs. 6,000

List Price = Cost price + Profit

= Rs. 60,000 + Rs. 6,000

= 66,000

Trade discount = 5%

Trade discount = List Price × % of trade discount

= Rs. 66,000 × 5%

= Rs. 3,300

Sale price = List Price – Trade discount

= 66,000 - 3,300

= 62,700

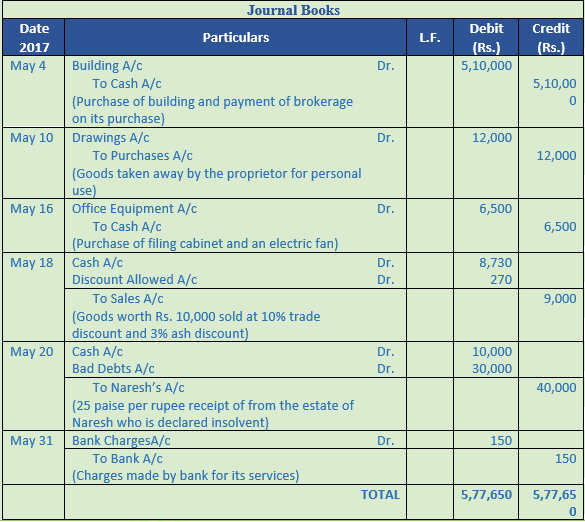

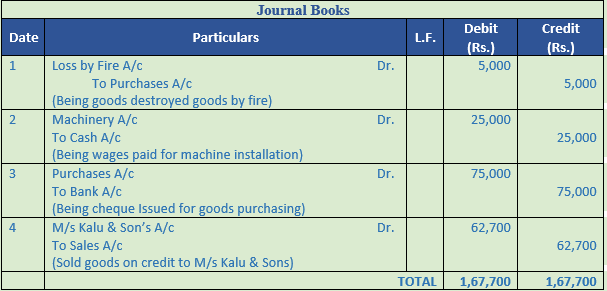

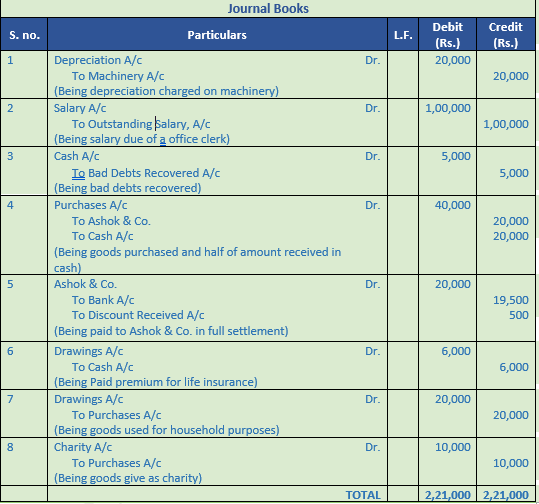

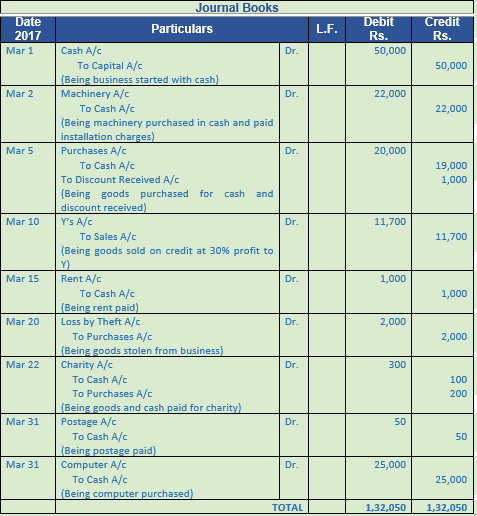

Question 32.

Solution 32:

Question 33.

Solution 33:

Working Note:-

List price = Rs. 25,000

Trade Discount = 20%

Trade Discount = Rs. 25,000 × 20% = Rs. 5,000

Sales = Rs. 25,000 – Rs. 5,000

Sales = Rs. 20,000

Cash discount = 5%

Discount amount = Rs. 20,000 × 5%

= Rs. 1,000

Amount Received = Rs. 20,000 – Rs. 1,000

= Rs. 19,000

Question 34.

Solution 34:

Question 35.

Solution 35:

Working Note:-

List price = Rs. 2,00,000

Trade Discount = 15%

Trade Discount = Rs. 2,00,000 × 15% = Rs. 30,000

Sales = Rs. 2,00,000 – Rs. 30,000

Sales = Rs. 1,70,000

Cash Received = 1,70,000 × 80%

= Rs. 1,36,000

Cash discount = 2%

Discount amount = Rs. 1,36,000 × 2%

= Rs. 2,720

Amount Received = Rs. 1,36,000 – Rs. 2,720

= Rs. 1,33,280

Question 36.

Solution 36:

Point of Knowledge:-

1. Asset Accounts: Debit the increases, Credit the decreases.

2. Liability Accounts: Debit the decreases, Credit the increases.

3. Capital Accounts: Debit the decreases, Credit the increases.

4. Expense Accounts: Debit the increases, Credit the decreases.

Question 37.

Solution 37:

Working Note:-

List price = Rs. 5,000

Trade Discount = 10%

Trade Discount = Rs. 5,000 × 10% = Rs. 500

Sales = Rs. 5,000 – Rs. 500

Sales = Rs. 4,500

Cash discount = 5%

Discount amount = Rs. 4,500 × 5%

= Rs. 225

Amount Received = Rs. 4,500 – Rs. 225

= Rs. 4,275

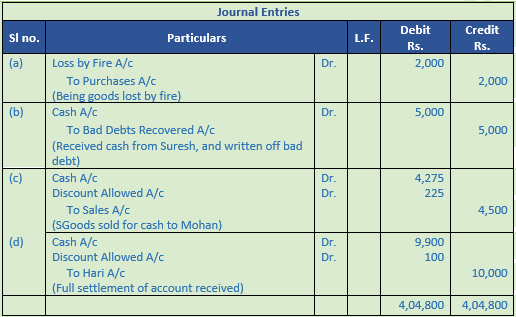

Point of Knowledge:-

- Recording of accounting data in chronological order.

- Narration of journal explains the transactions very well.

Question 38.

Solution 38:

Point of knowledge:-

A Liability Account is credited when there is an increase in liability. We will debit the liability account to reduce the balance.

The example to reduce a liability account is paid outstanding rent Rs. 1000. The Outstanding Rent Account will be debited by Rs. 1000.

Question 39.

Solution 39:

Point of Knowledge:-

- Asset Accounts: Debit the increases, Credit the decreases.

- Liability Accounts: Debit the decreases, Credit the increases.

- Capital Accounts: Debit the decreases, Credit the increases.

- Expense Accounts: Debit the increases, Credit the decreases.