Access free DK Goel Solutions Class 11 Accountancy Chapter 13 Ledger 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 13 Ledger DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 13 Ledger Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 13 Ledger DK Goel Class 11 Solved Exercises

Short Answer Question

Question 1.

Solution 1:

Question 2.

Solution 2:

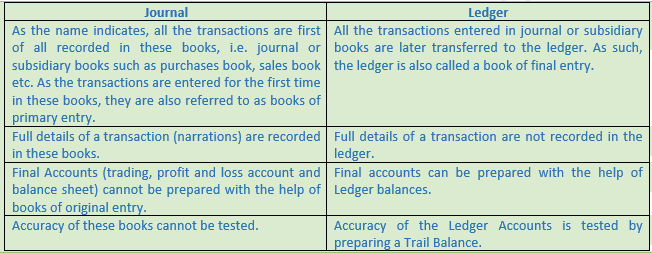

Below are the advantages of ledger:-

(1) All accounts are opened on separate pages in this book. Hence, all the transactions pertaining to an account are collected at one place in the ledger.

(2) A trail balance can be prepared with the help of ledger balances which helps in ascertaining the arithmetical accuracy of the accounts.

(3) A trading and profit and loss account can only be prepared with the help of ledger balances.

(4) A balance sheet can also be prepared with the help of ledger balances which depicts the financial position of the business.

Question 3.

Solution 3:

Below are the rules of posting in the ledger:-

(i) All transactions relating to an account should be entered at one place. Two separate accounts should no the opened for posting transactions relating the same account.

(ii) The word ‘To’ is used before the accounts which appear on the debit side of a account. Similarly, the word ‘By’ is used before the accounts which appear on the credit side of an account.

(iii) If an account has been debited in the Journal entry, the posting in the ledger should also be made on the debit side of such account. In the particulars columns, the name of the other account which has been credited in the journal entry should be written for reference.

(iv) If an account has been credited in the Journal entry, the posting in the ledger should also be made on the credit side of such account. In the particulars columns, the name of the other account which has been debited in the journal entry should be written for reference.

(v) Similar amount which has been posted on the debit side of an account should also be posted on the credit side of another account.

Question 4.

Solution 4: Journal Folio (J.F.) Column in the ledger records Page No. of the journal from which the posting to the Ledger has taken place. Purpose of posting J.F. number is that it provides a ready reference for tracing the page of journal from where the entry has been posted.

Question 5.

Solution 5:

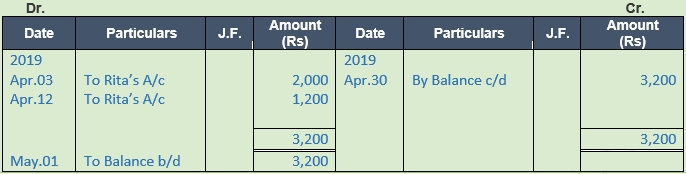

An Account is balanced like we have to add the bigger side either debit or credit whichever may be and write down the bigger one in the parallel column. The debit column if bigger than the credit column. The difference is written on the credit side as 'By Balance c/d'. The totals are then entered in the two columns opposite one another and then on the debit side, the balance is written as 'To Balance b/d' to show the debit balance in hand in the beginning of the next period or vice versa for the credit balance.

Question 6.

Solution 6:

Question 7.

Solution 7:

Question 8.

Solution 8:

Question 9.

Solution 9:

Numerical Questions

Question 1.

Solution 1:

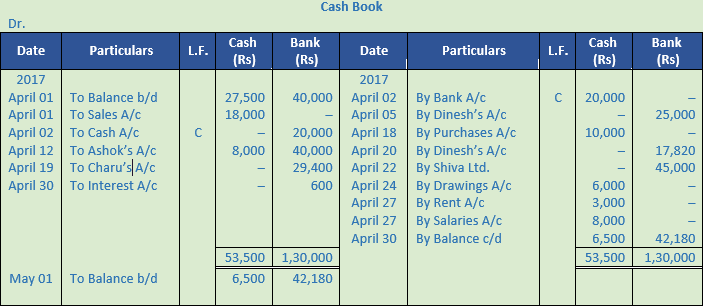

Question 2.

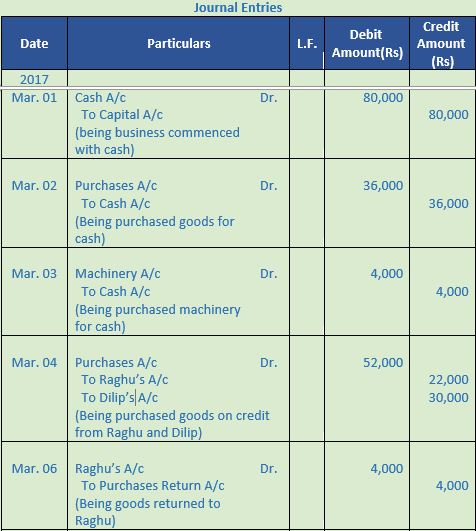

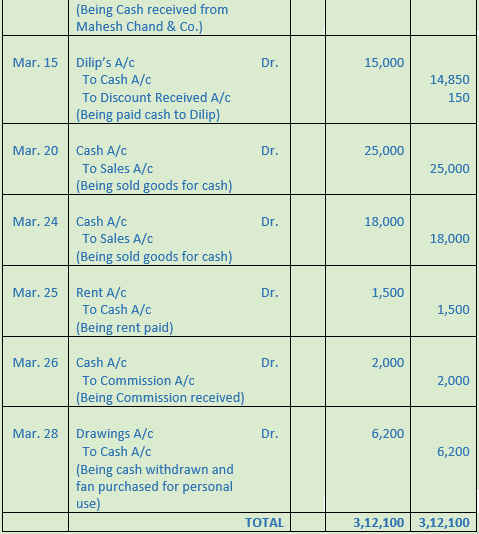

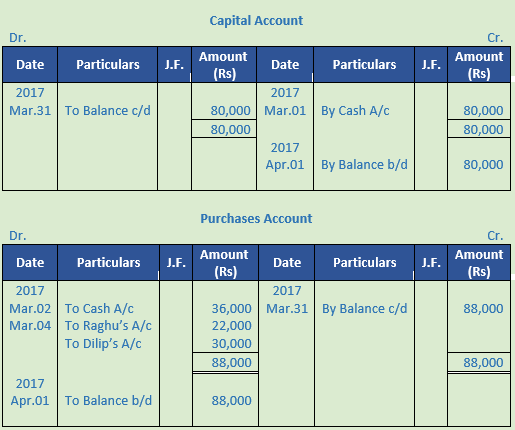

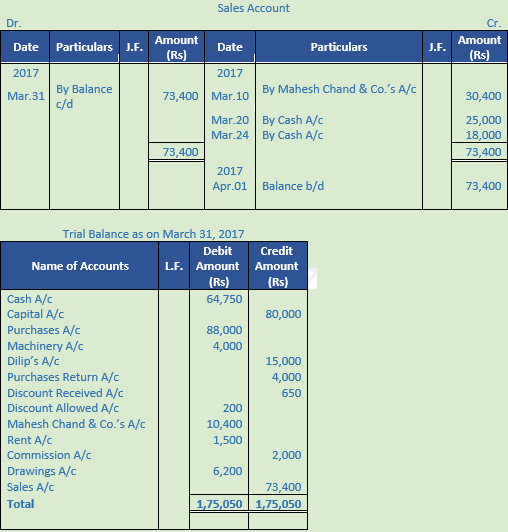

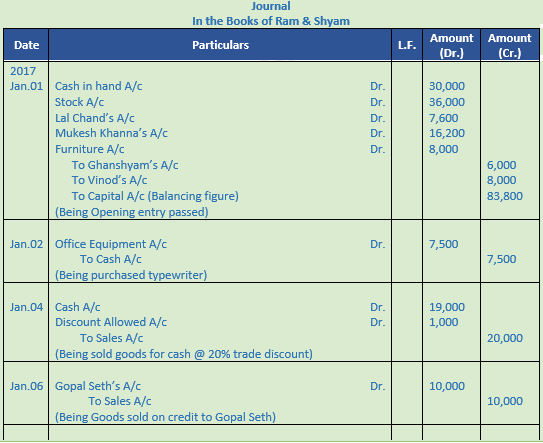

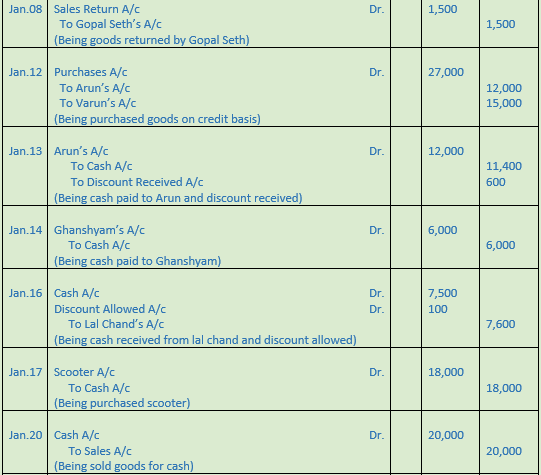

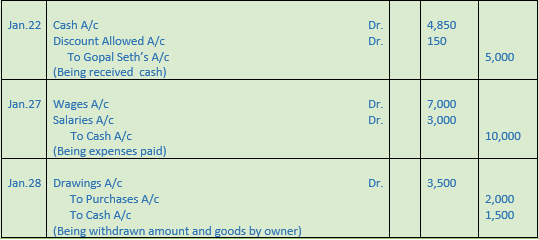

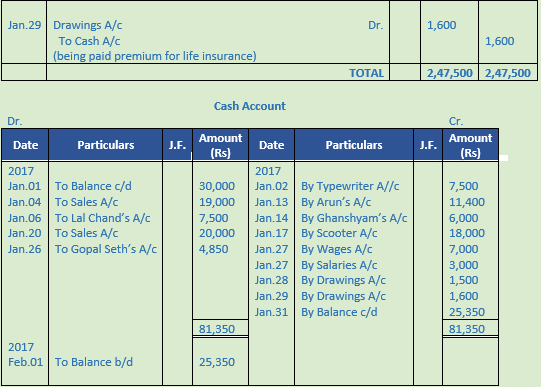

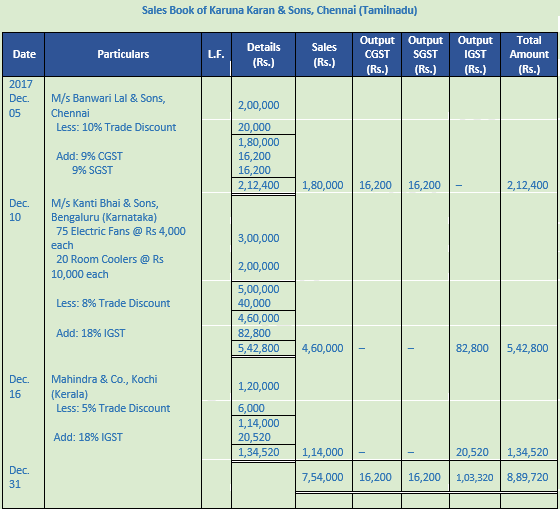

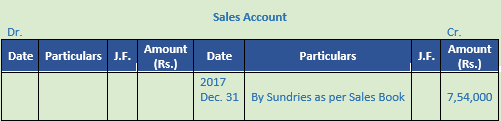

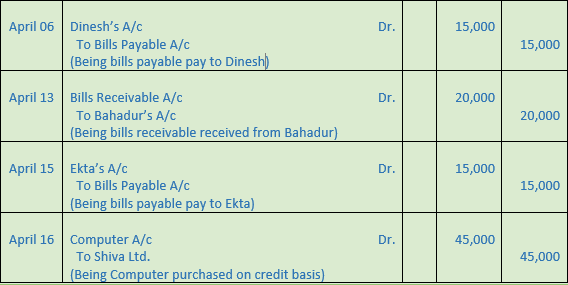

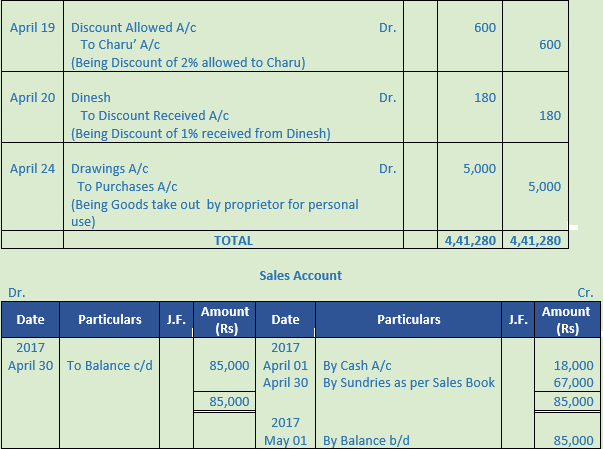

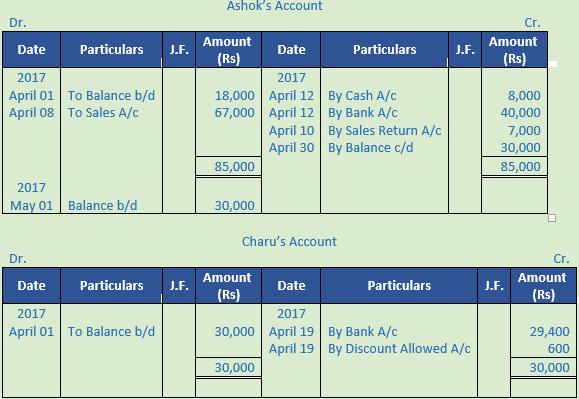

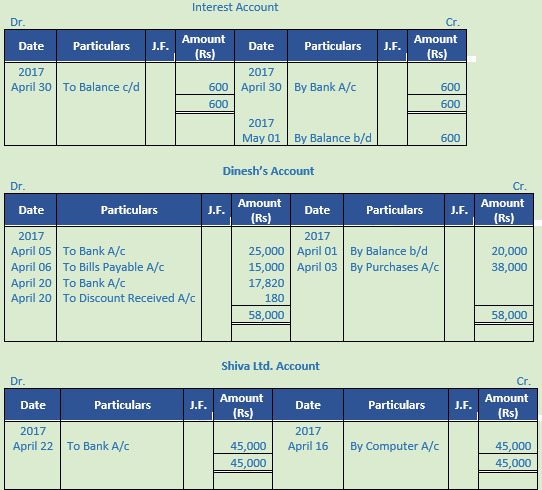

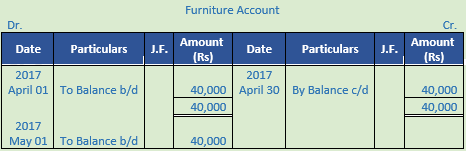

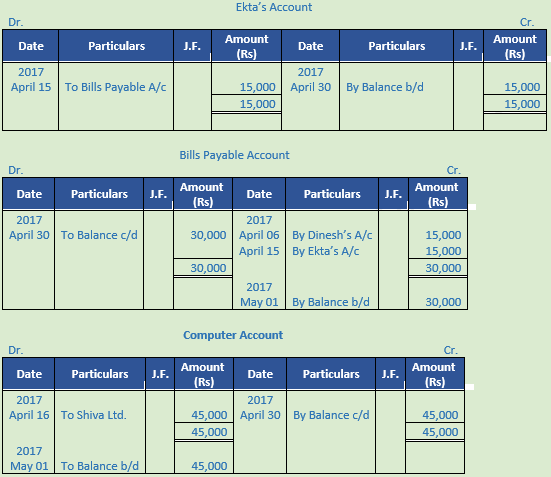

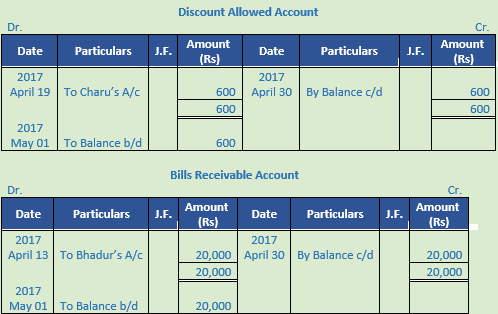

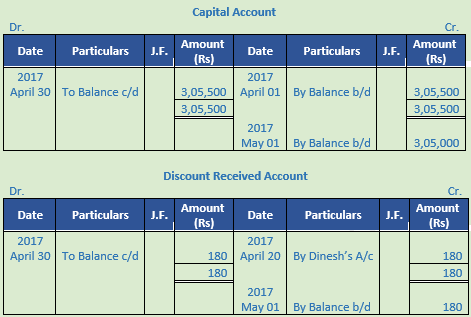

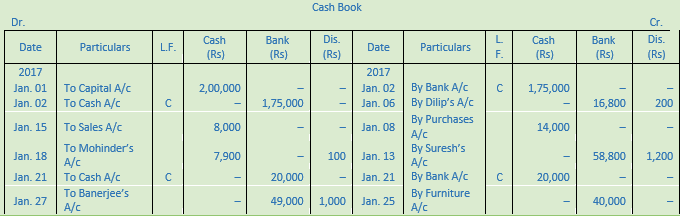

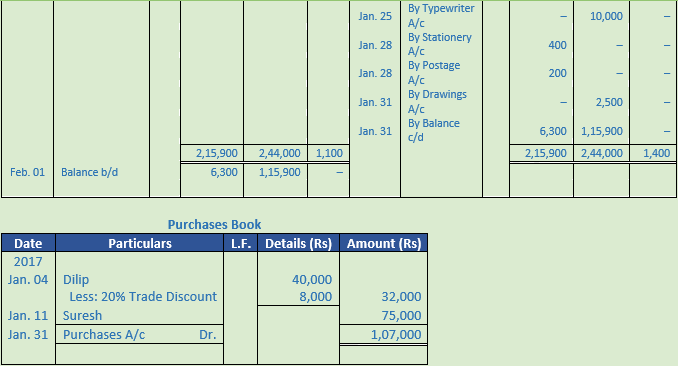

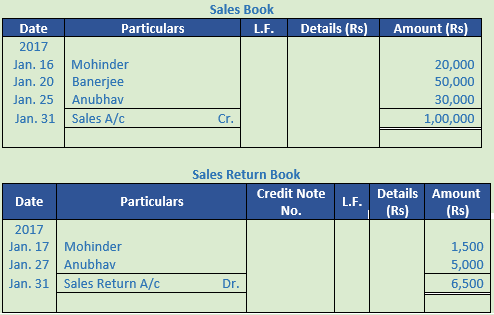

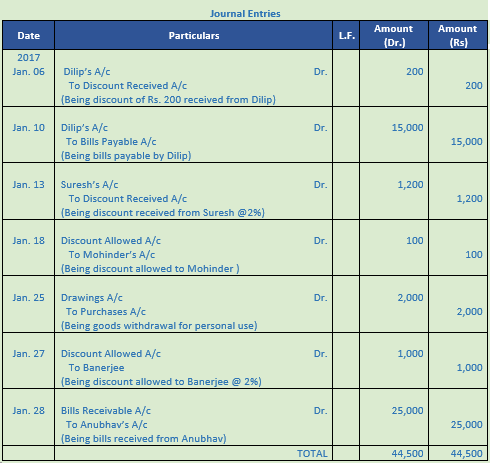

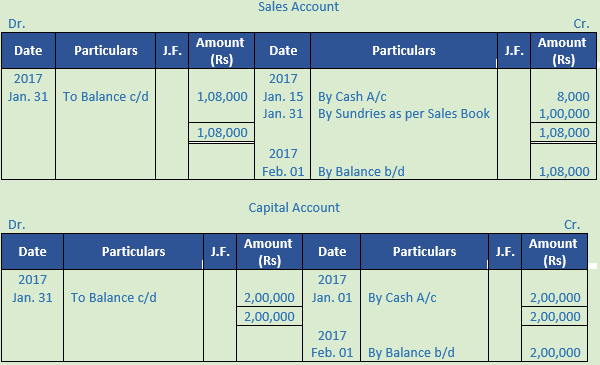

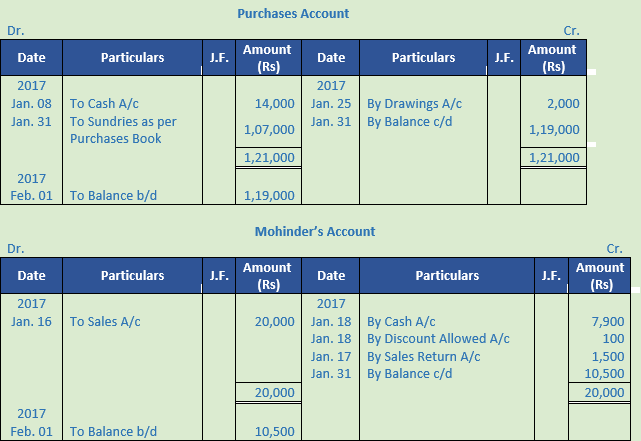

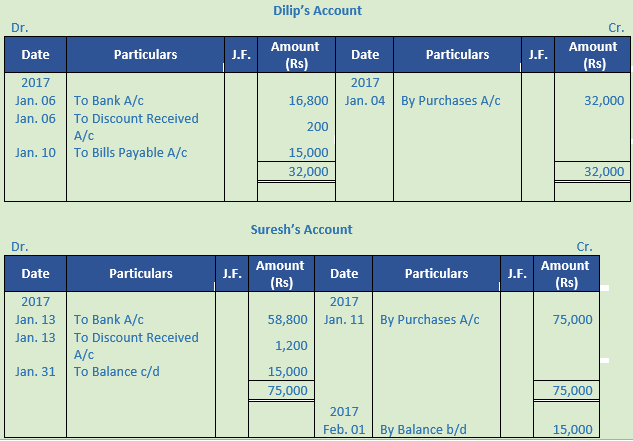

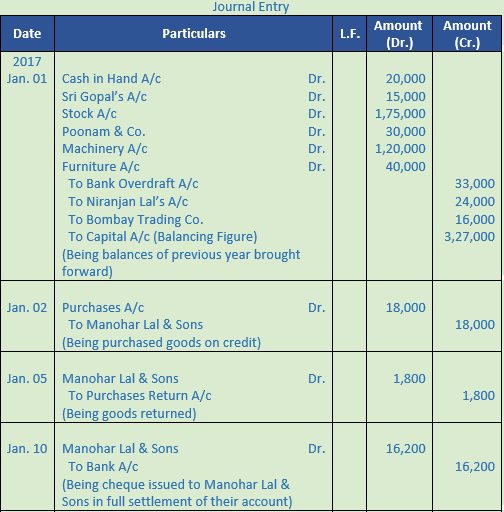

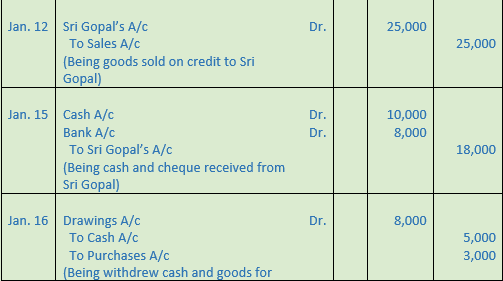

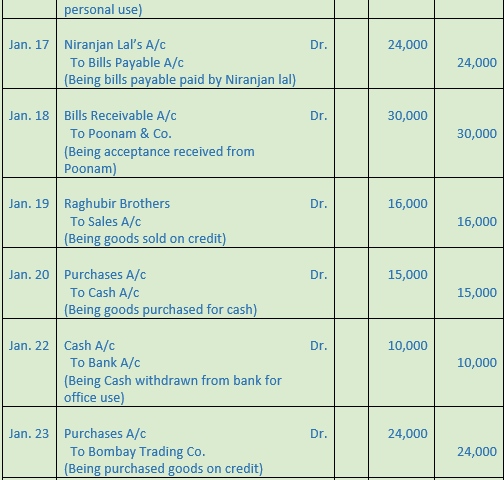

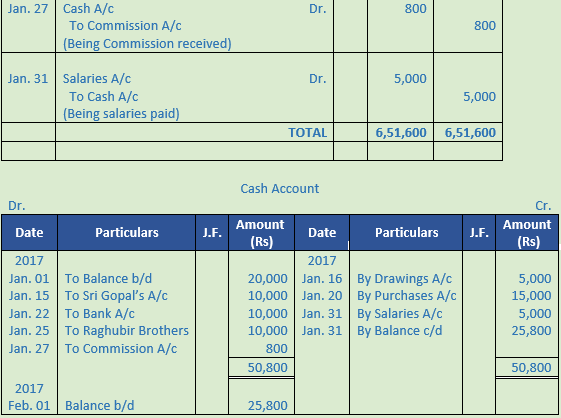

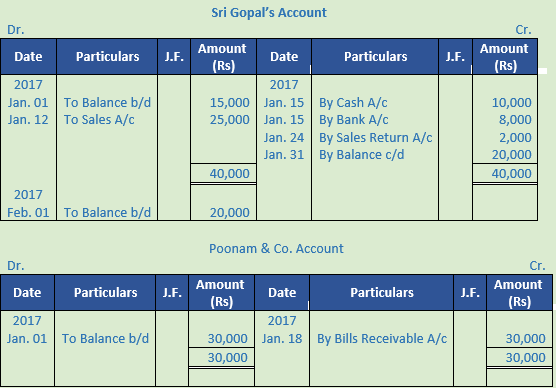

Journalise the above transactions, post them into Ledger, balance them and prepare a Trial Balance.

Solution 2:

Point of Knowledge:-

A Cash Account is balanced like any other account. The debit column is always bigger than the credit column. The difference is written on the credit side as 'By Balance c/d'. The totals are then entered in the two columns opposite one another and then on the debit side, the balance is written as 'To Balance b/d' to show the cash balance in hand in the beginning of the next period.

Question 3.

Solution 3:

Point of Knowledge:-

In an account, transactions of one nature are posted or summarized. All the accounts put together constitute a 'Ledger'. A Ledger may be defined as a "book or register which contains, in a summarized and classified form, a permanent record of all transactions." It is the most important book of accounts, since, the Trial Balance is drawn from it and from the Trial Balance, and Financial Statements are prepared. Hence, the Ledger is called the Principal Book.

Question 4.

Solution 4:

Point of Knowledge:-

1. Identify in the Ledger the account to be debited.

2. Enter the date of the transaction in the 'Date' column on the debit side of the account.

3. Write the name of the account which has been credited in the respective entry in the 'Particulars' column on the debit side of the amount as 'To (name of account credited)'.

4. Record the page number of the Journal where the entry exists in the Journal folio (J,F.) column.

5. Enter the relevant amount in the 'Amount' column on the debit side.

Question 5.

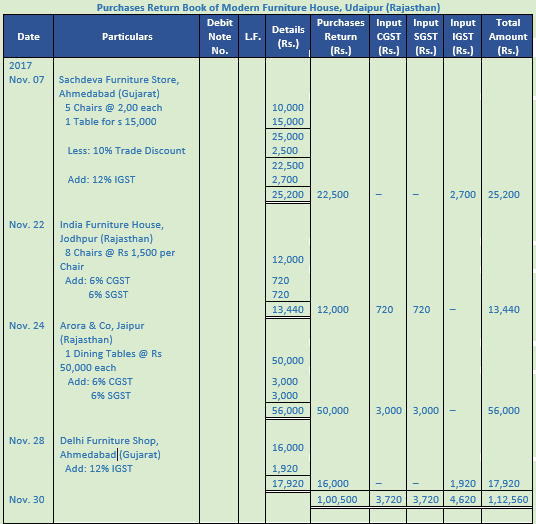

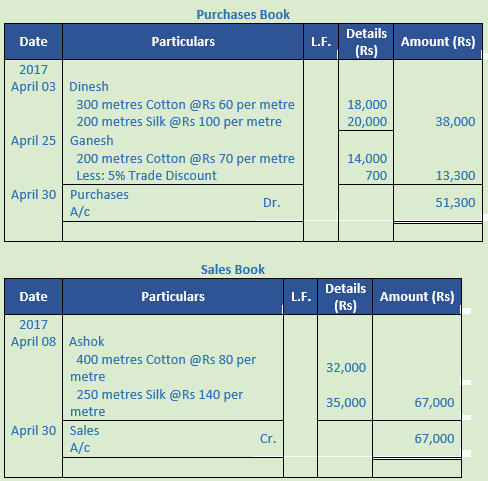

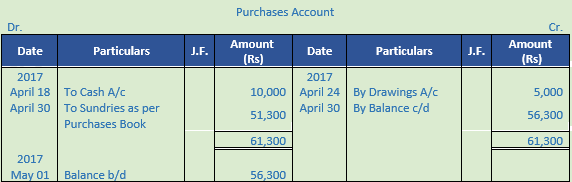

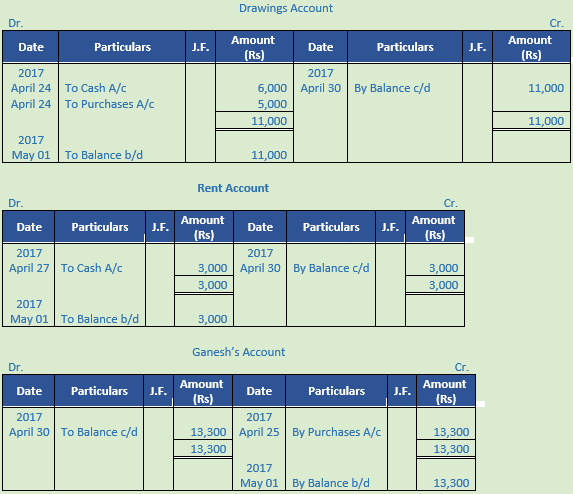

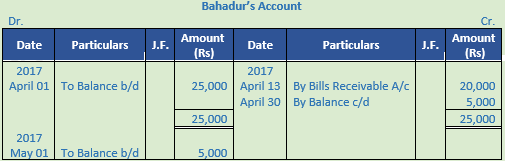

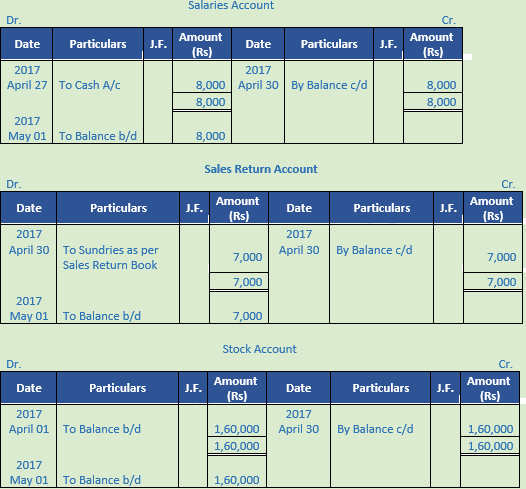

Solution 5: Purchases Book of Modern Furniture House, New Delhi

Point of knowledge:-

- Identify in the Ledger the account to be debited.

- Enter the date of the transaction in the 'Date' column on the debit side of the account.

- Write the name of the account which has been credited in the respective entry in the 'Particulars' column on the debit side of the amount as 'To (name of account credited)'.

- Record the page number of the Journal where the entry exists in the Journal folio (J,F.) column.

- Enter the relevant amount in the 'Amount' column on the debit side.

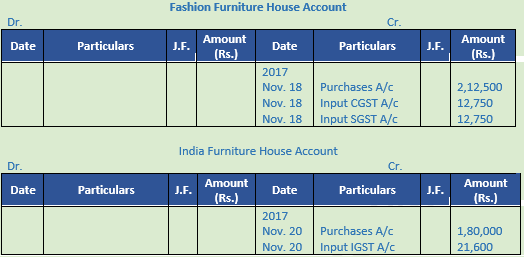

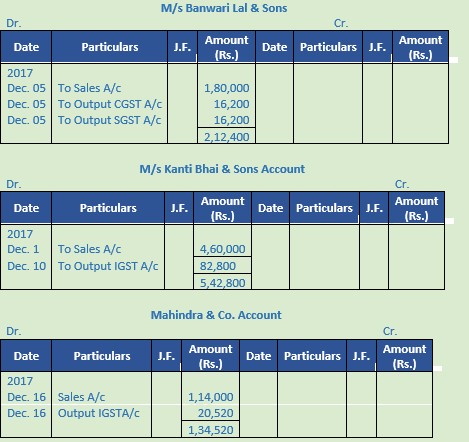

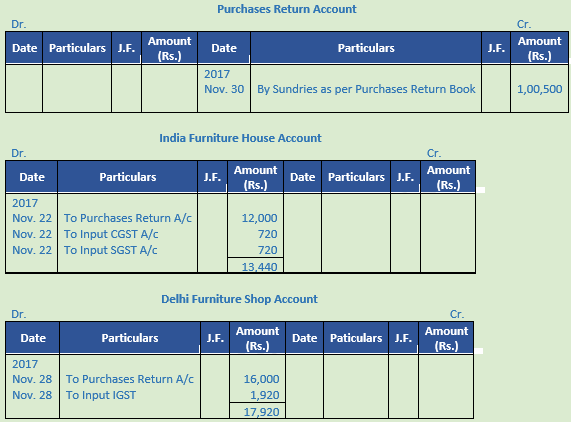

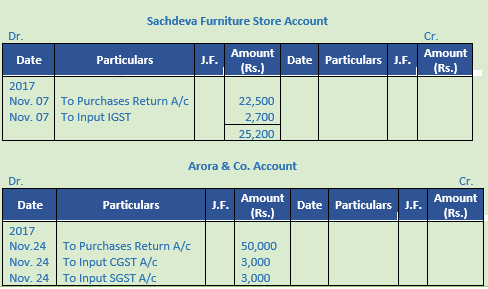

Question 6.

Solution 6:

Point of knowledge:-

- Identify in the Ledger the account to be credited.

- Enter the date of the transaction in the 'Date' column on the credit side of the account.

- Write the name of the account which has been debited in the respective entry in the 'Particulars' column on the credit side of the account as 'By (name of account debited)'.

- Record the page number of the Journal where the entry exists in the Journal folio (J.F.) column.

- Enter the relevant amount in the 'Amount' column on the credit side.

Question 7.

Solution 7:

Question 8.

Solution 8:

Point of knowledge:-

- Identify in the Ledger the account to be credited.

- Enter the date of the transaction in the 'Date' column on the credit side of the account.

- Write the name of the account which has been debited in the respective entry in the 'Particulars' column on the credit side of the account as 'By (name of account debited)'.

- Record the page number of the Journal where the entry exists in the Journal folio (J.F.) column.

- Enter the relevant amount in the 'Amount' column on the credit side.

Question 9.

Solution 9:

Point of knowledge:-

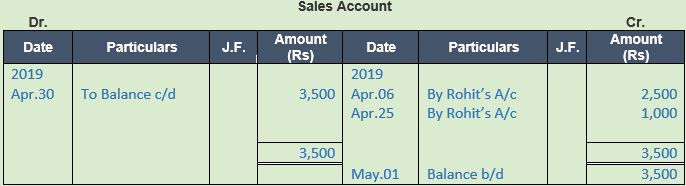

(1) If the debit side total is more than the credit side total write the difference on the credit side as “By Balance c/d”.

(2) If the credit side total is more than the debit side total write the difference on the credit side as “To Balance c/d”.

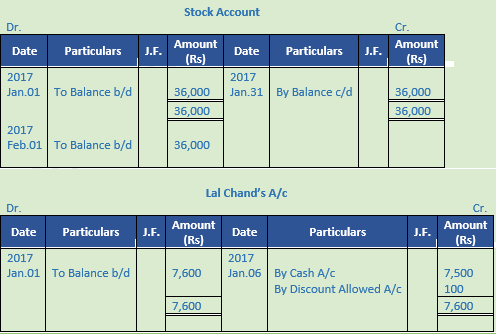

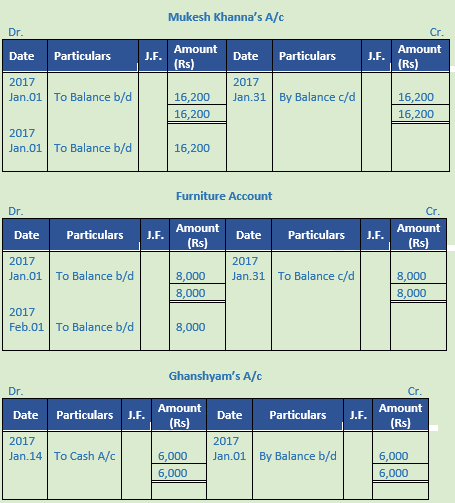

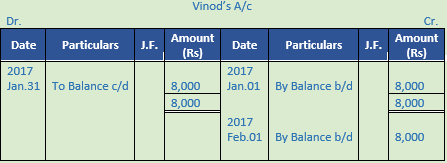

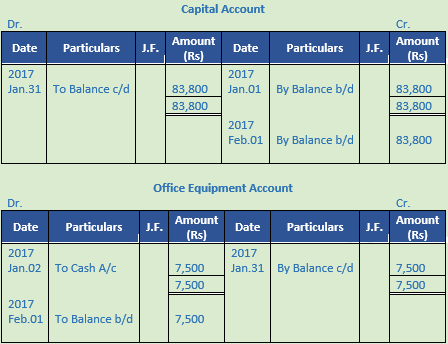

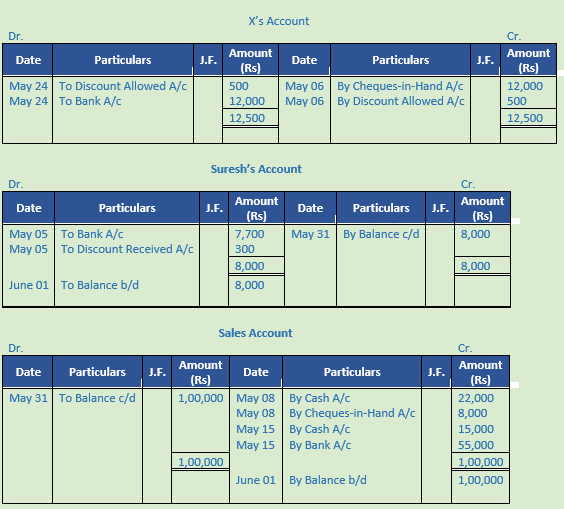

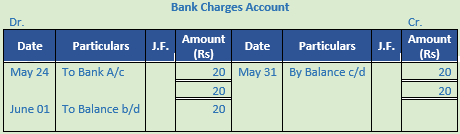

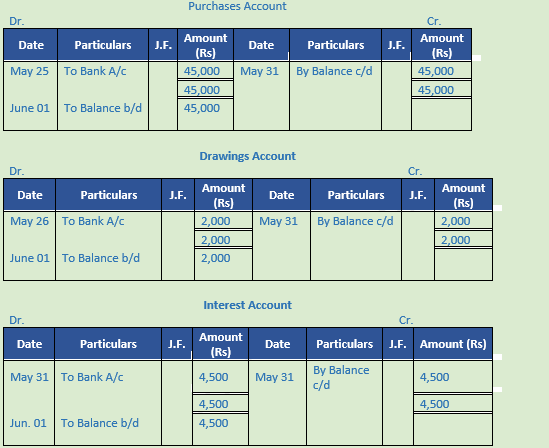

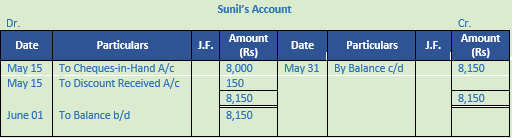

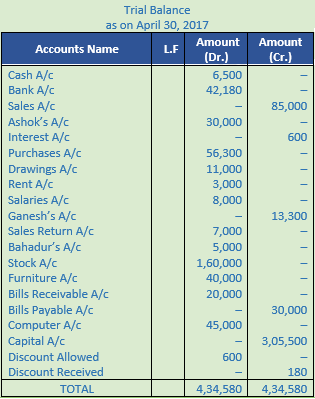

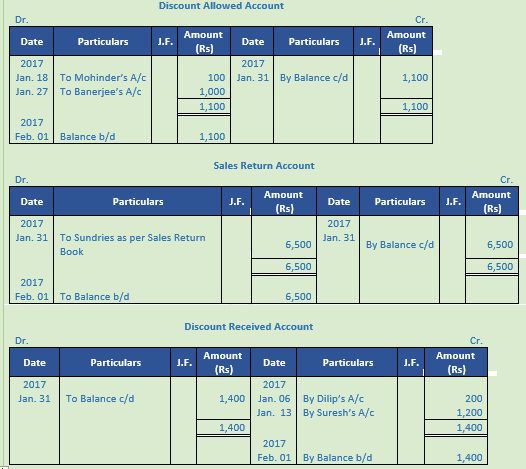

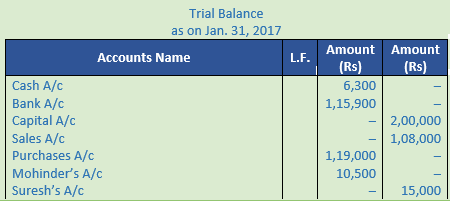

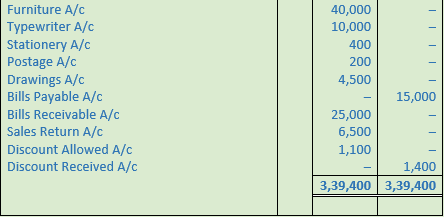

Question 10.

Solution 10:

Point of knowledge:-

(1) If the debit side total is more than the credit side total write the difference on the credit side as “By Balance c/d”.

(2) If the credit side total is more than the debit side total write the difference on the credit side as “To Balance c/d”.

Question 11.

Solution 11:

Point of Knowledge:-

Journal Folio (J.F.) Column in the ledger records Page No. of the journal from which the posting to the Ledger has taken place. Purpose of posting J.F. number is that it provides a ready reference for tracing the page of journal from where the entry has been posted.

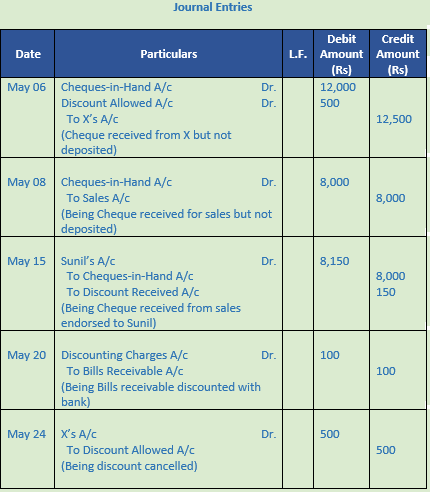

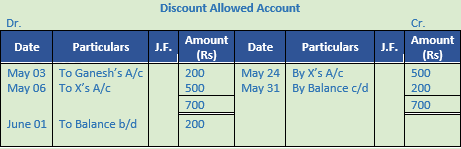

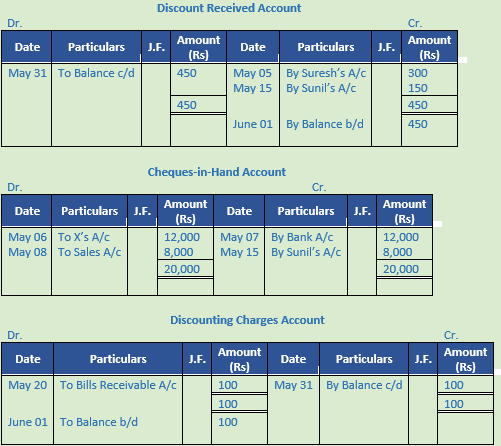

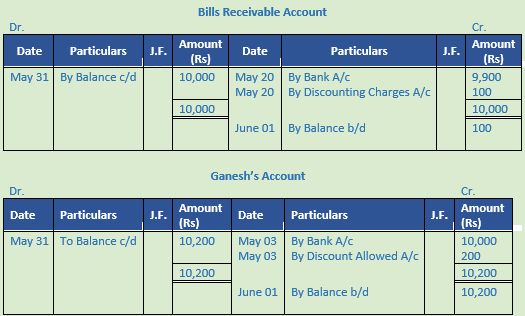

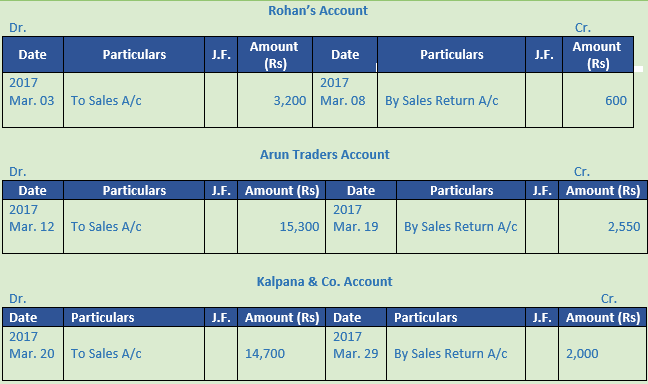

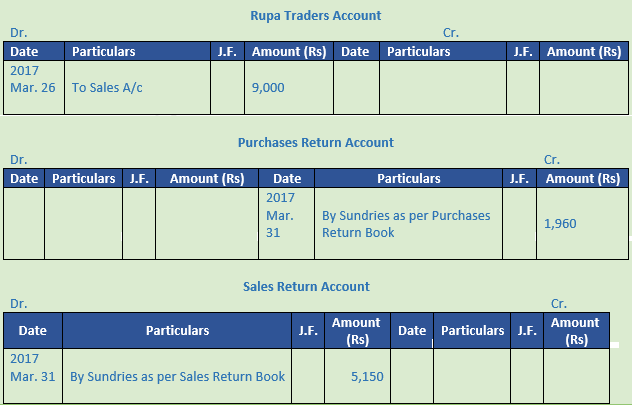

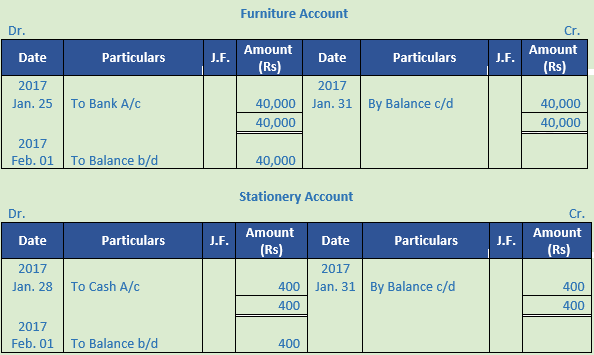

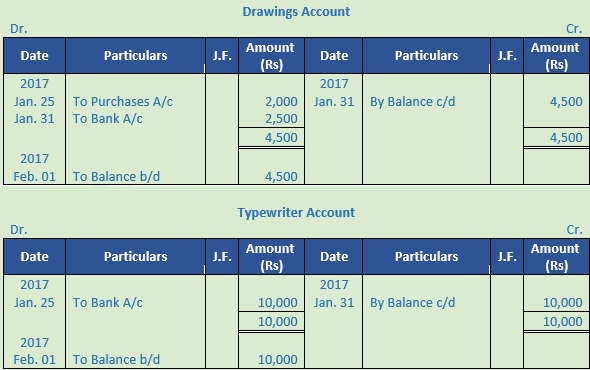

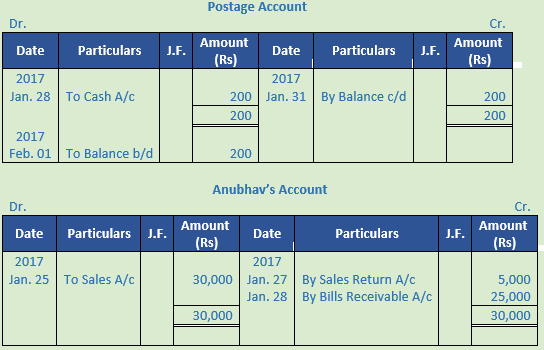

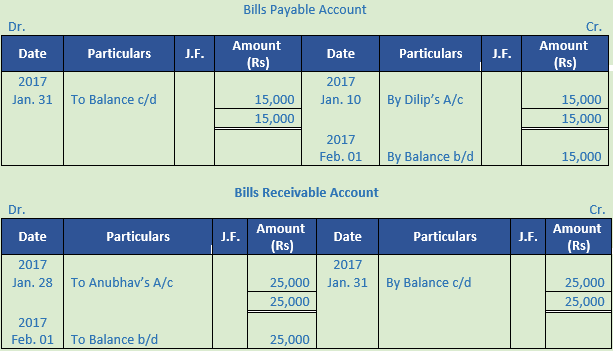

Question 12.

Solution 12:

Point of Knowledge:-

Earlier, we discussed the term Account. In an account, transactions of one nature are posted or summarized. All the accounts put together constitute a 'Ledger'. A Ledger may be defined as a "book or register which contains, in a summarized and classified form, a permanent record of all transactions." It is the most important book of accounts, since, the Trial Balance is drawn from it and from the Trial Balance, and Financial Statements are prepared. Hence, the Ledger is called the Principal Book.