Access free DK Goel Solutions Class 11 Accountancy Chapter 12 Books of Original Entry Special Purpose Subsidiary Books 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 12 Books of Original Entry Special Purpose Subsidiary Books DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 12 Books of Original Entry Special Purpose Subsidiary Books Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 12 Books of Original Entry Special Purpose Subsidiary Books DK Goel Class 11 Solved Exercises

Question 1.

Solution 1: Purchases Book:- All the credit purchases of goods are recorded in the purchases book. This is a subsidiary book which records credit purchase of goods. Purchases Book also known as invoice book or purchases day book.

Purchases Return Book:- This book is used to recorded the return of such goods as work purchases on credit basis. This book is also known as return onward book.

Question 2.

Solution 2: Debit note:- A debit note is prepared by the purchaser when goods are returned by him is called a debit note because the party’s account is debited with the amount written in it.

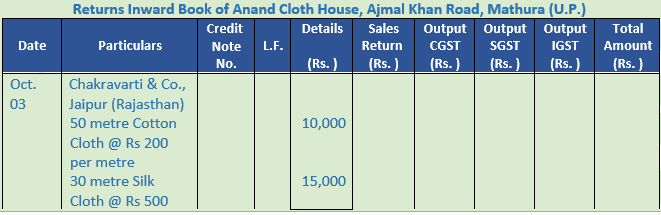

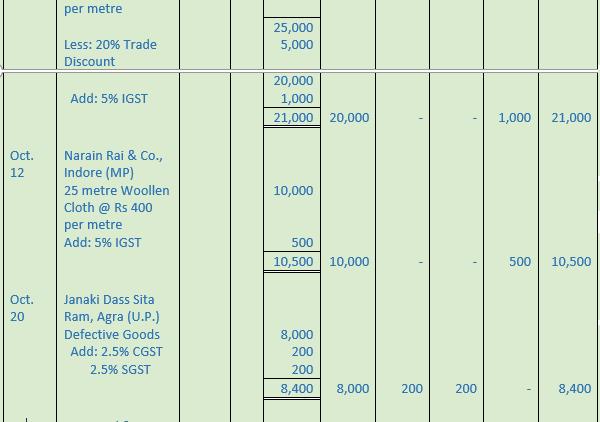

Credit note:- A credit note is prepared by the seller when the goods sold are received back. It is called a credit note because the party’s account, from whom goods are received back, is credited with the amount written in the note.

Question 3.

Solution 3: Below are the entries which have to be passed through a journal through we might have kept all the subsidiary books in the business:-

1.) Purchases of Fixed Assets on Credit i.e. Purchases of Machinery on credit basis.

2.) Making provisions for doubtful debts.

3.) Providing depreciation on assets.

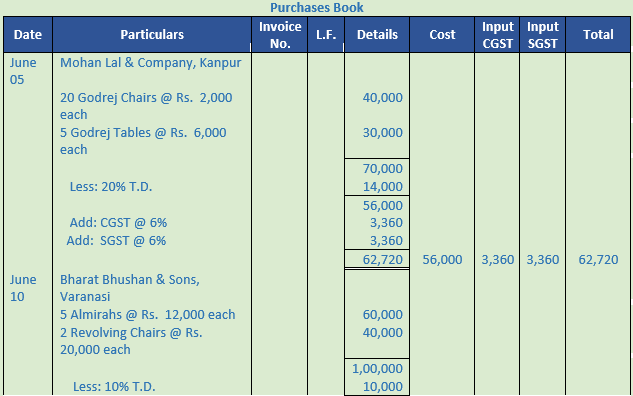

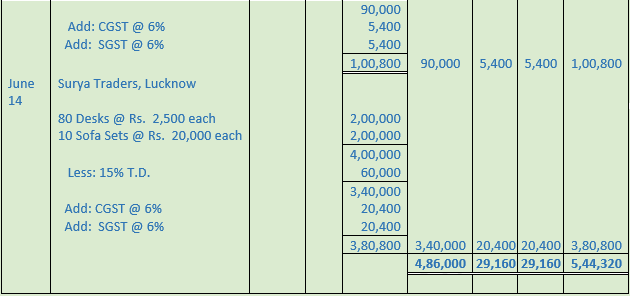

Question 1.

Solution 1:

Working Note:-

- Price of a chair = Rs. 2,000

Price of 20 such chairs = Rs. 2,000 × 20 = Rs. 40,000

Price of a table = Rs. 6,000

Price of 5 such tables = Rs. 6,000 × 5 = Rs. 30,000

- Price of a Almirah = Rs. 12,000

Price of 5 such chairs = Rs. 12,000 × 5 = Rs. 60,000

Price of a Revolving chairs = Rs. 20,000

Price of 2 such tables = Rs. 20,000 × 2 = Rs. 40,000

Point of Knowledge:-

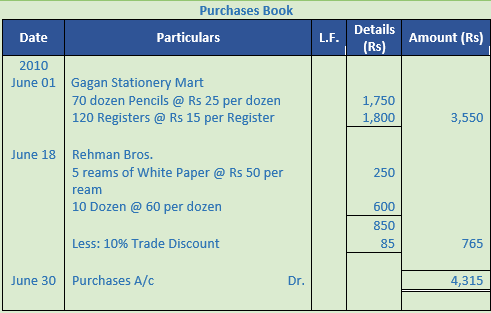

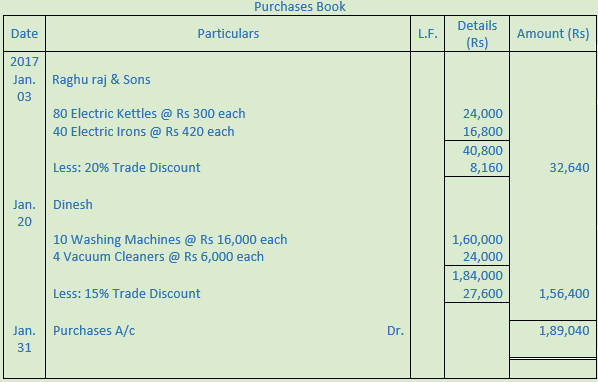

In Purchases Book, we record only the credit purchase of goods, so transaction dated June 20 (being cash purchase of goods) and June 25 (being credit purchase of Fixed Asset) will not be recorded.

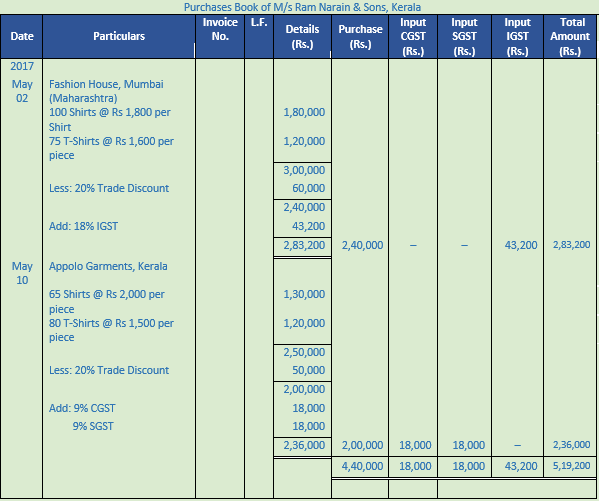

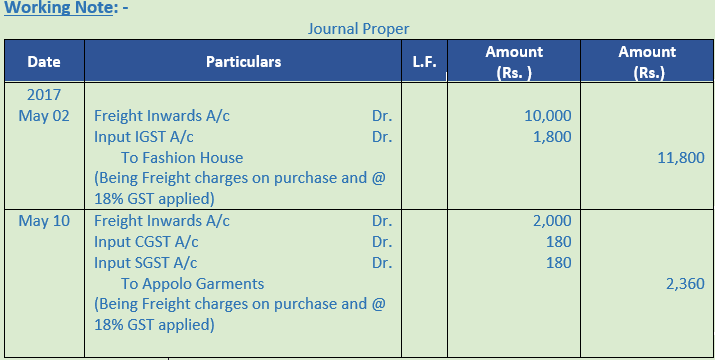

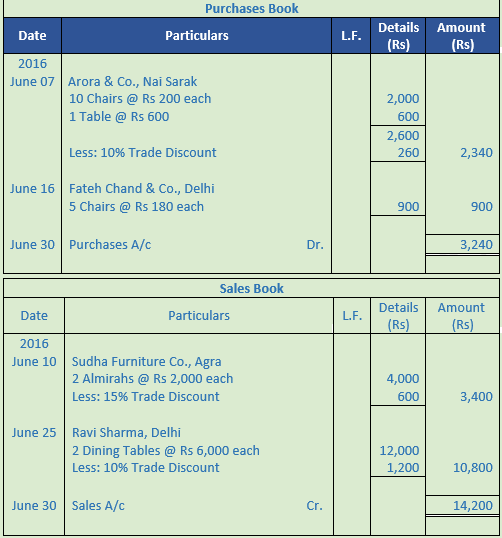

Question 2.

Solution 2:

Point of Knowledge:-

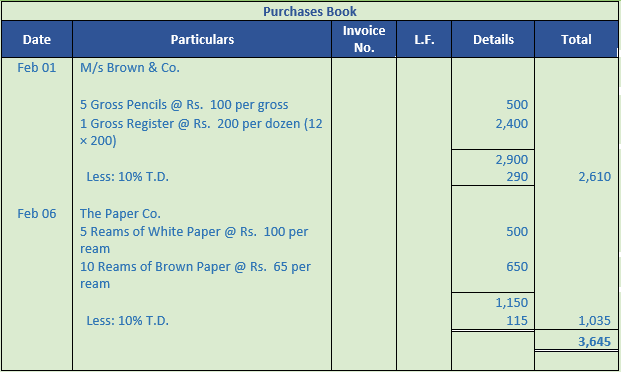

In Purchases Book, we record only the credit purchase of goods, so transaction dated May 15 (being purchase of Furniture on credit) and May 25 (being purchase of goods for cash) will not be recorded.

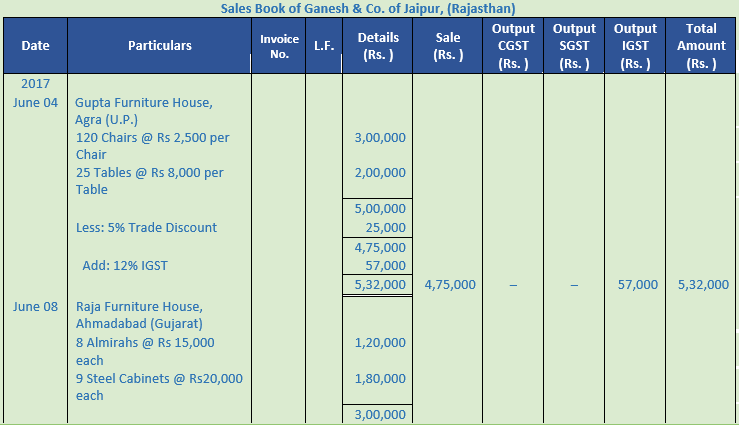

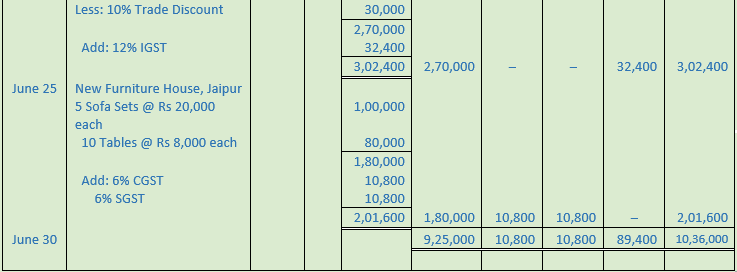

Question 3.

Solution 3:

Working Note:-

- Price of a chair = Rs. 2,500

Price of 120 such chairs = Rs. 2,500 × 120 = Rs. 3,00,000

Price of a table = Rs. 8,000

Price of 25 such tables = Rs. 8,000 × 25 = Rs. 2,00,000

- Price of a Almirah = Rs. 15,000

Price of 8 such chairs = Rs. 15,000 × 8 = Rs. 1,20,000

Price of a Steel cabinet = Rs. 20,000

Price of 9 such tables = Rs. 20,000 × 9 = Rs. 1,80,000

Point of Knowledge:-

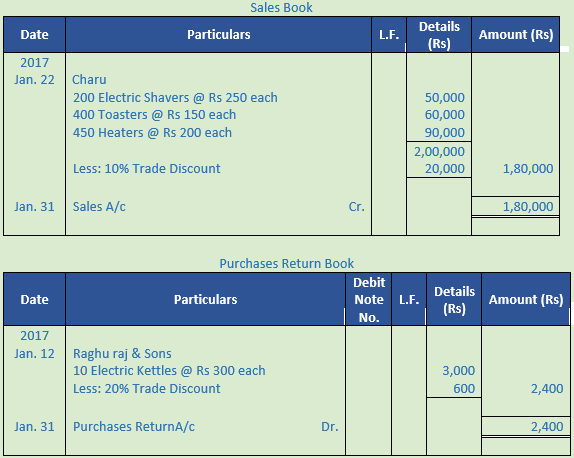

In Sales Book, we record only the credit sale of goods, so transaction dated June 12 (being Computer sold on credit) and June 20 (being Sofa Sets sold for cash) will not be recorded.

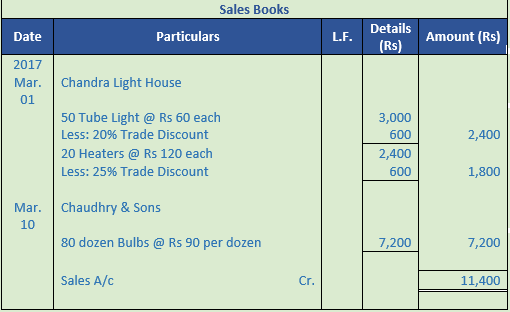

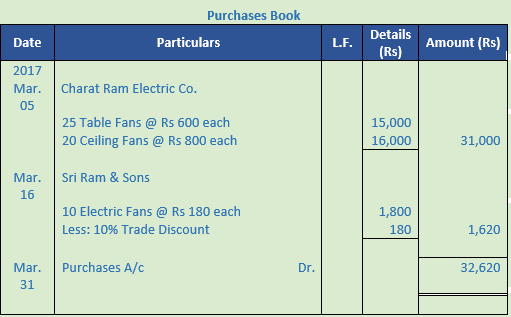

Question 4.

Solution 4:

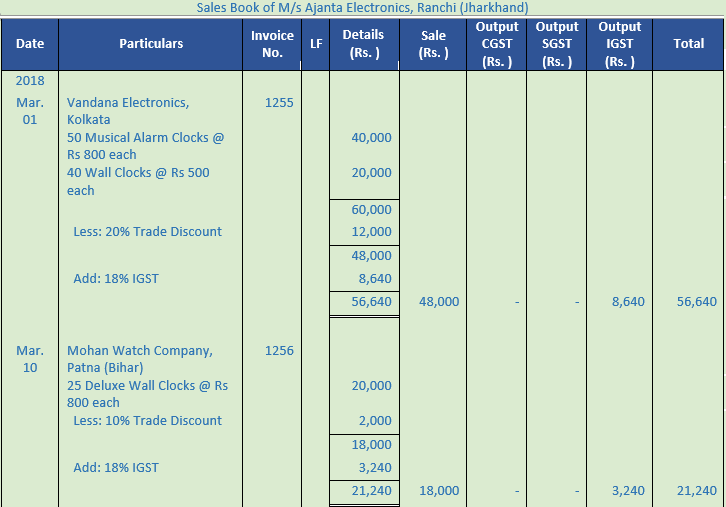

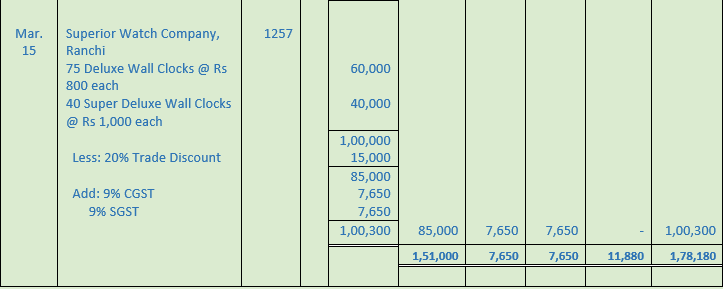

Working Note:-

- Price of a Musical Alarm Clock = Rs. 800

Price of 50 such Musical Alarm Clock = Rs. 800 × 50 = Rs. 40,000

Price of a Wallclock = Rs. 500

Price of 40 such Wallclock = Rs. 500 × 40 = Rs. 20,000

- Price of a Deluxe Wall Clocks = Rs. 800

Price of 75 such Deluxe Wall Clocks = Rs. 800 × 75 = Rs. 60,000

Price of a Super Deluxe Wall Clocks = Rs. 1,000

Price of 40 such tables = Rs. 1,000 × 40 = Rs. 40,000

Point of Knowledge:-

In the Sales Book we record only credit transactions related to goods, so transaction dated March 20 (being sale of electronics for cash) will not be recorded.

Question 5.

Solution 5:

Point of Knowledge:-

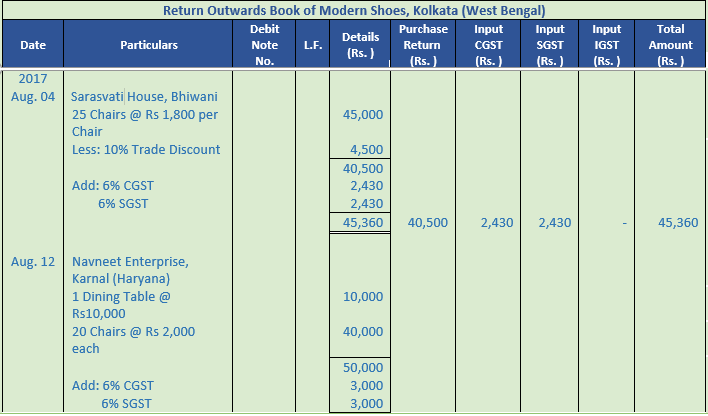

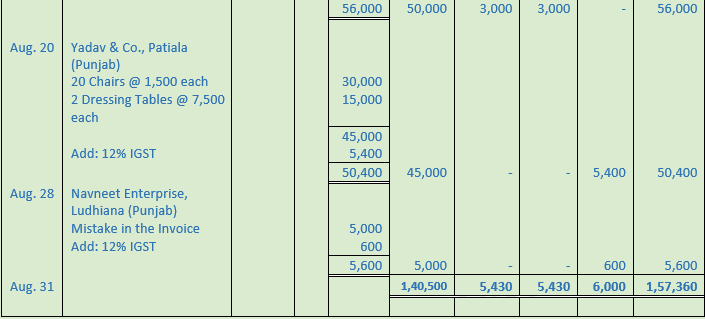

The purchaser prepares a 'Debit Note' and sends it to the supplier. A Debit Note is prepared w en goods are returned by the purchaser due to some reason. It is called a Debit Note because the party's account is debited with the amount written in this note. The 'Debit Note' is the basis for writing in the Purchases Return or Return Outward Book.

Question 6.

Solution 6:

Point of Knowledge:-

The reason for maintaining separate accounts for CGST, SGST and IGST are to setoff the GST Paid against the GST Collected in the prescribed order. GST paid or Input GST individually (Input CGST, SGST and IGST) is set off against GST Collected (Output GST) individually (Output CGST, SGST and IGST) in the prescribed order. Hence, it is necessary that separate accounts for Input GST and Output GST for each category of GST be maintained. It will enable the taxpayer to follow prescribed order of setting off the each category of GST.

Question 7.

Solution 7:

Point of Knowledge:-

Debit note:- A debit note is prepared by the purchaser when goods are returned by him is called a debit note because the party’s account is debited with the amount written in it.

Credit note:- A credit note is prepared by the seller when the goods sold are received back. It is called a credit note because the party’s account, from whom goods are received back, is credited with the amount written in the note.

Question 8.

Solution 8:

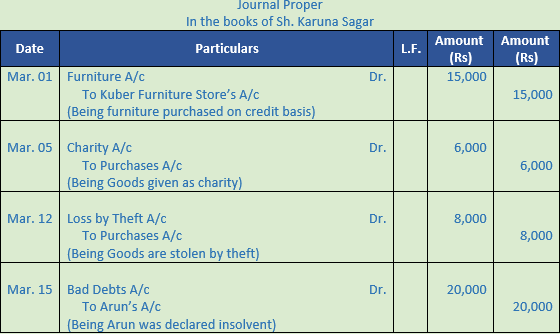

Point of Knowledge:-

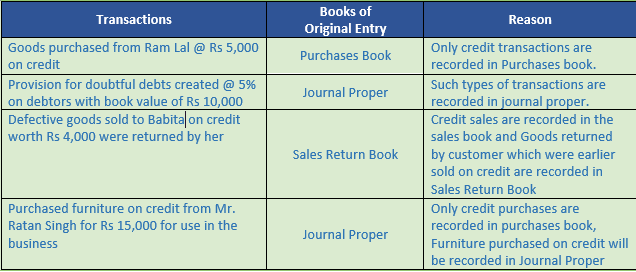

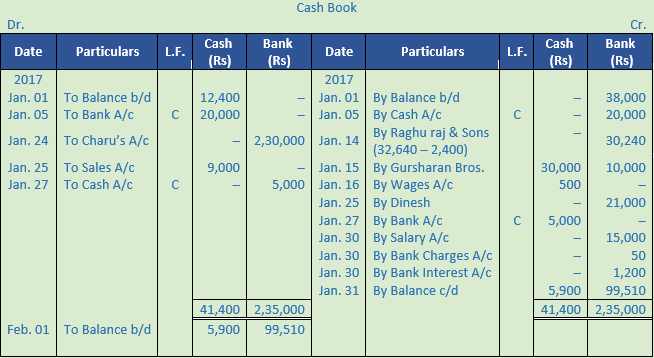

Only credit transactions are recorded in the Journal Proper.

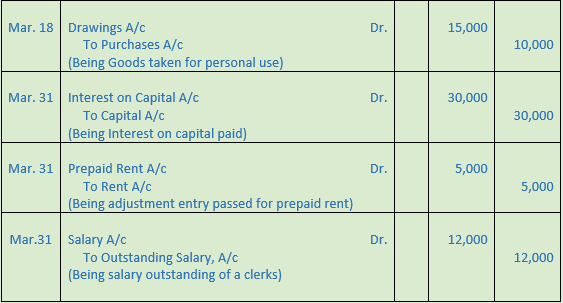

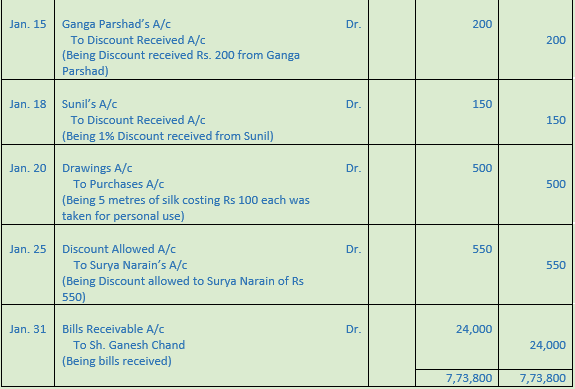

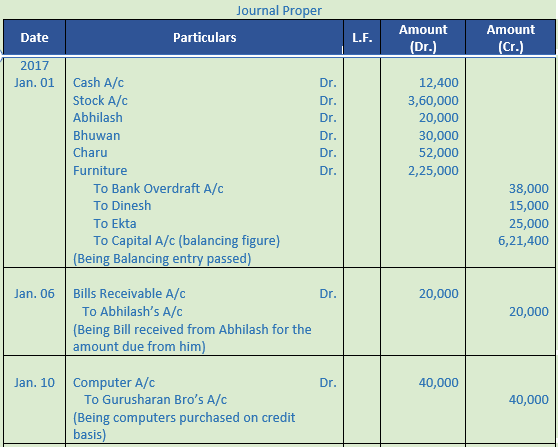

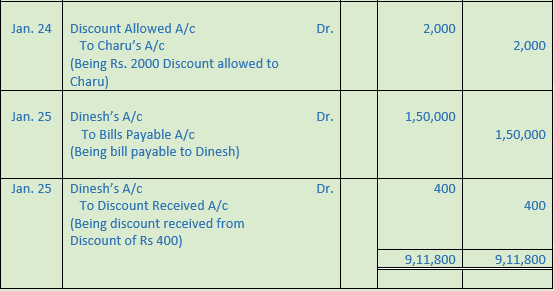

Question 9.

Solution 9:

7,73,800

Point of Knowledge:-

Adjustment Entries are passed at the end of the year to adjust the amounts paid or received in advance or for amounts not yet settled in cash. Such an adjustment is also made through Journal entries. Usually the adjustment entries are made for outstanding expenses, prepaid expenses, interest on capital, depreciation, etc.

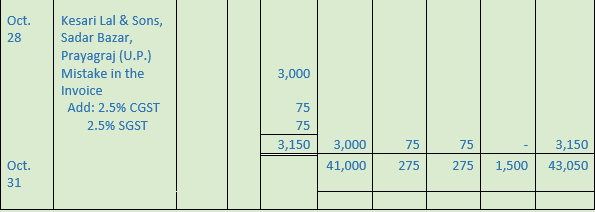

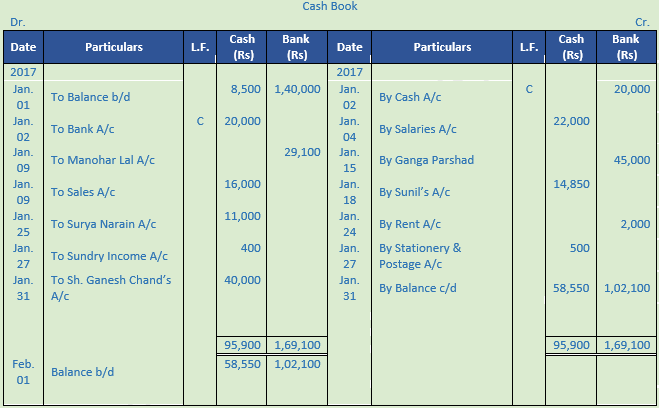

Question 10.

Solution 10:

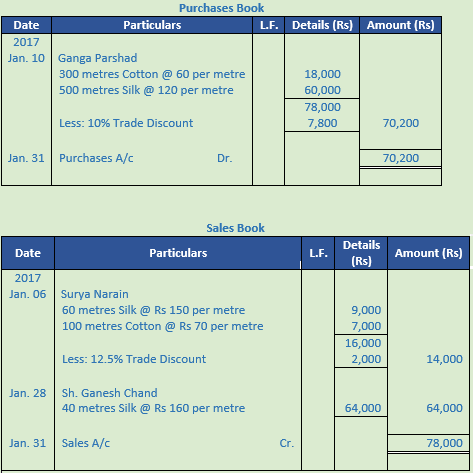

Question 11.

Solution 11:

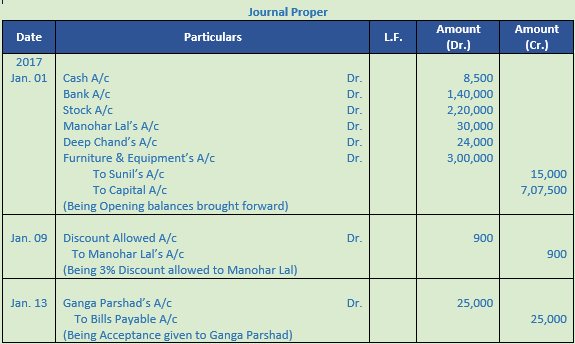

Working Note:-

1dozen = 12units

120 pen will be = = 10 dozen

Price of 1 dozen pen = Rs. 60

Price of 10 dozen pen = Rs. 60 × 10 = Rs. 600

Point of Knowledge:-

Purchases book records only the credit purchase of goods, so transaction dated June 10 (being purchase of furniture) and June 15 (being purchase of goods for cash) will not be recorded.

Question 12.

Solution 12:

Point of knowledge:-

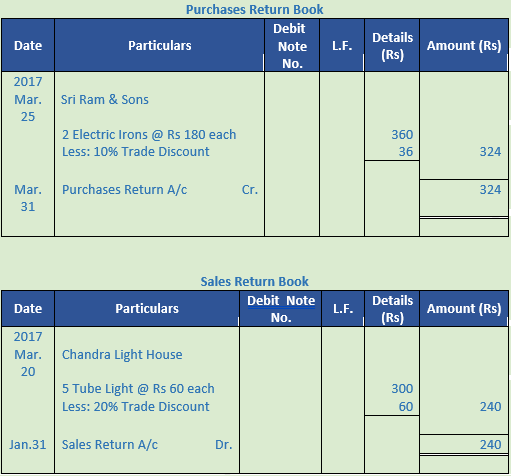

Debit note:- A debit note is prepared by the purchaser when goods are returned by him is called a debit note because the party’s account is debited with the amount written in it.

Credit note:- A credit note is prepared by the seller when the goods sold are received back. It is called a credit note because the party’s account, from whom goods are received back, is credited with the amount written in the note.

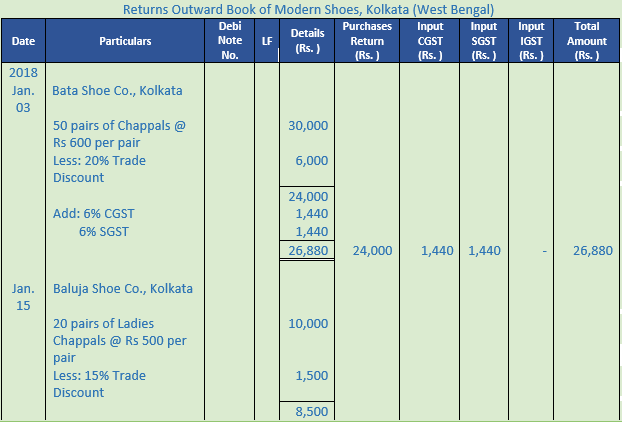

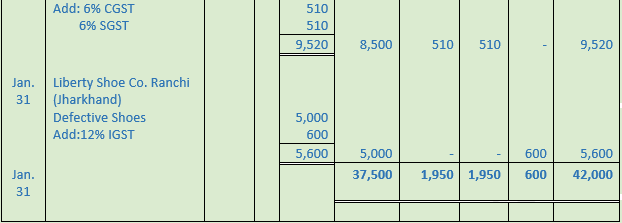

Question 13.

Solution 13:

Point of Knowledge:-

Sales book records only the credit sale of goods, so transaction dated Jan. 20, Jan. 24 and Jan. 31 will not be recorded.

Question 14.

Solution 14:

Point of Knowledge:-

Debit note:- A debit note is prepared by the purchaser when goods are returned by him is called a debit note because the party’s account is debited with the amount written in it.

Credit note:- A credit note is prepared by the seller when the goods sold are received back. It is called a credit note because the party’s account, from whom goods are received back, is credited with the amount written in the note.

Question 15.

Solution 15:

Point of Knowledge:-

Purchases Book is a subsidiary book in which credit purchases of goods dealt in or stores and raw material used for production are recorded.

Sales Book is a subsidiary book in which credit sales of goods dealt in are recorded.

Journal Proper is a book of account in which those transactions and events are recorded which are not recorded in the subsidiary books.

Question 16.

Solution 16:

Point of knowledge:-

Purchases Book is a subsidiary book in which credit purchases of goods dealt in or stores and raw material used for production are recorded.

Sales Book is a subsidiary book in which credit sales of goods dealt in are recorded.

Journal Proper is a book of account in which those transactions and events are recorded which are not recorded in the subsidiary books.