Access free DK Goel Solutions Class 11 Accountancy Chapter 21 Financial Statement 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 21 Financial Statement DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 21 Financial Statement Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 21 Financial Statement DK Goel Class 11 Solved Exercises

Short Answer Questions

Question 1.

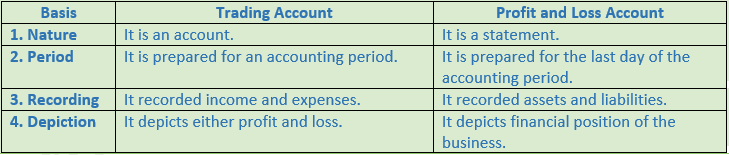

Solution 1: On the basis of financial statement they can judge as to how much bonus and increase in their wages is possible from the profits of the enterprise.

Question 2.

Solution 2: They can assess the short-term and long –term financial soundness and earning capacity of the business with the help of financial statement. They can also study the trend of sales, trend of profit, shortcomings and the prospects of future growth of the enterprise.

Question 3.

Solution 3: Operating profit is the profit earned through normal operating activities of the business. It is arrived at by deducting the operating express from gross profit. Expenses which are related to the main or normal activities of the business are called operating expenses.

Question 4.

Solution 4: Indirect expenses are those expenses which are incurred and are not directly associated with the purchases of goods or manufacture of goods.

The two examples of indirect expenses are:

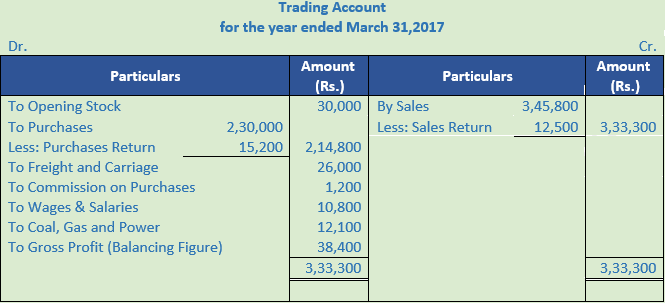

- Office salaries.

- Warehouse expenses.

Question 5.

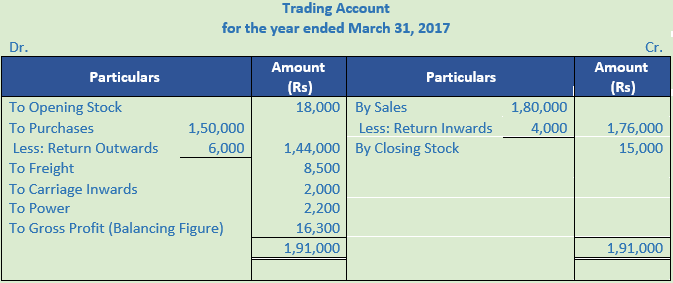

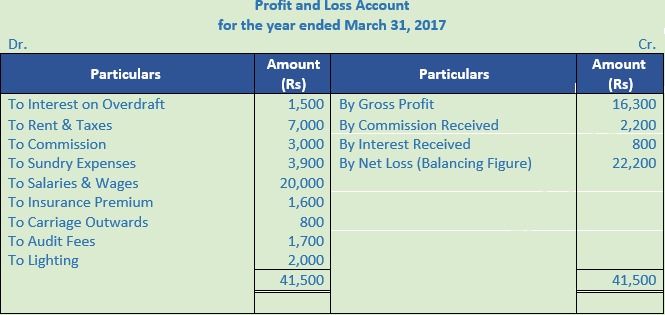

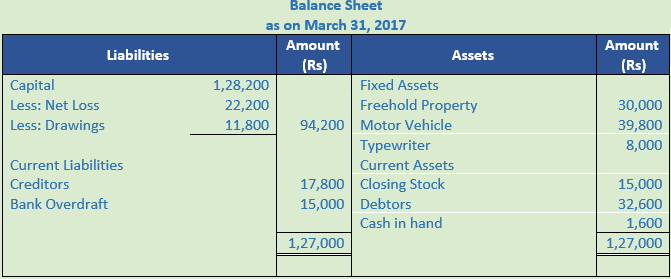

Solution 5:

Question 6.

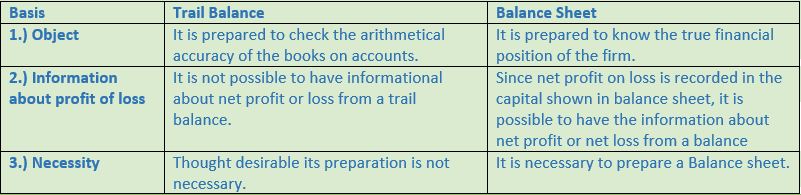

Solution 6: A balance sheet is prepared to ascertain the financial position of an enterprise on a particular date. It shows liabilities on the left hand side and assets on right hand side.

Question 7.

Solution 7: Grouping means showing the assets or liabilities of similar nature common heading and Marshalling means showing the assets and liabilities in a proper order.

Question 8.

Solution 8: According to this method an asset which is most easily convertible into cash such as cash in hand is written first and then will follow those assets which are comparatively less easily convertible so that the least liquid asset such as goodwill is shown last.

Question 9.

Solution 9: An asset which is most easily convertible into cash such as cash in hand is written first and then will follow those assets which are comparatively less easily convertible so that the least liquid asset such as goodwill is shown last.

Question 10.

Solution 10: Current Assets are those assets which are held for resale or for converting into cash. These are the assets which are likely to be realized within a period of one year or during the period of normal operating cycle. A business earns profit by selling these assets but not by keeping them as stock for a longer period. These assets are temporary in nature and may change from time to time. These are sometimes referred to as floating or circulating assets.

Non-Current Assets are those assets are which are acquired for continuous use and last for many years such as Land and Building, Plant and Machinery, Motor Vehicles, Furniture etc.

Question 11.

Solution 11: Example of Fixed Assets:-

1.) Land and Building

2.) Plant and Machinery

Example of Current Assets:-

1.) Cash

2.) Stock

Question 12.

Solution 12: These are the liabilities which will become payable only on the happing of some specific event, otherwise not such as:-

(i) Liabilities for bill discounted

(ii) Liabilities in respect of a suit pending in a court of law

(iii) Liability in respect of a guarantee give for another person.

Question 13.

Solution 13:

Question 14.

Solution 14: Those liabilities which are to be paid at the earliest will be written first. In other words, current liabilities are written first of all, then non-current or long-term liabilities and lastly the proprietor’s capital.

Numerical Questions

Question 1.

Solution 1:

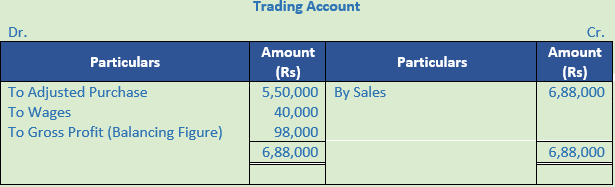

Point of Knowledge:-

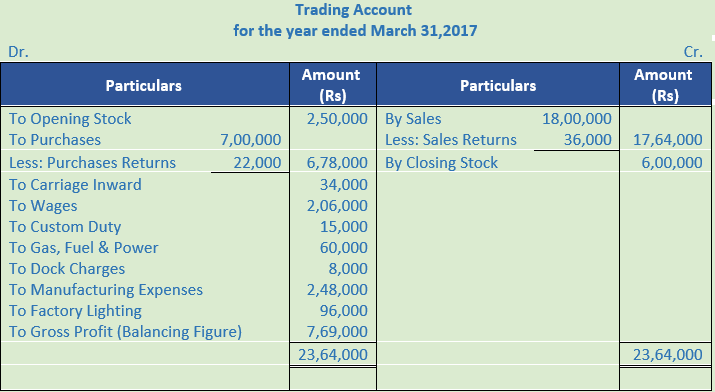

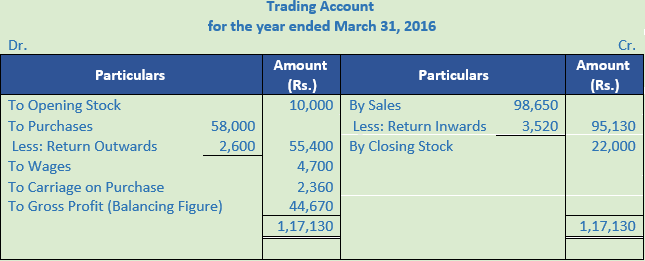

Trading Account is the account that reveals the gross profit or gross loss. It is credited with the amount of sales of goods and debited with the opening stock of goods along with the direct expenses related to the sales made. Trading Account is prepared to know gross profit or gross loss during the accounting period.

Question 2. (A)

Solution 2: (A)

Working Note:-

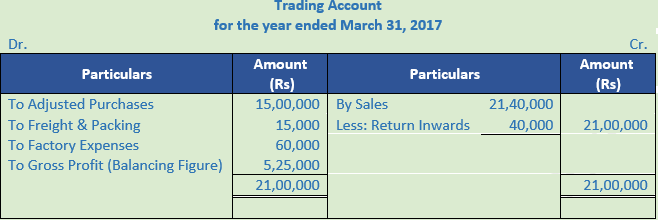

Calculation of Adjusted Purchases = Opening Stock + Net Purchases – Closing Stock

Point of Knowledge:-

Closing stock is not showing separately in trading account as it is already subtracted in adjusted purchases.

Solution 2: (B) Calculate Gross Profit from the following information:

Working Note:-

Calculation of Adjusted Purchases = Opening Stock + Net Purchases – Closing Stock

Point of Knowledge:-

Closing stock is not showing separately in trading account as it is already subtracted in adjusted purchases.

Question 3. (A)

Solution 3: (A) Calculation of Cost of Goods Sold:-

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Cost of Goods Sold = 40,000 + 50,000 + 10,000 – 15,000

Cost of Goods Sold = Rs. 85,000

Question 3. (B)

Solution 3 (B):

Calculation of Gross Profit:-

Gross Profit = Net Sales – COGS (Cost of goods sold)

Gross Profit = Rs. 3,92,000 – Rs. 3,92,000

Gross Profit = Rs. 1,10,000

Calculation of Cost of Goods Sold:-

Cost of goods sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Cost of goods sold = Rs. 32,000 + Rs. 2,80,000 + Rs. 20,000 – Rs. 50,000

Cost of goods sold = Rs. 2,82,000

Calculation of Net Sales:-

Net Sales = Sales – Sales Return

Net Sales = Rs. 4,00,000 – Rs. 8,000

Net Sales = Rs. 3,92,000

Question 4.

Solution 4 :

Calculation of Gross Profit:-

Gross Profit = Net Sales – COGS (Cost of goods sold)

Gross Profit = Rs. 6,00,000 – Rs. 5,40,000

Gross Profit = Rs. 60,000

Calculation of Cost of Goods Sold:-

Cost of goods sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Cost of goods sold = Rs. 0 + Rs. 6,50,000 + Rs. 70,000 – Rs. 0

Cost of goods sold = Rs. 7,20,000

Cost of goods sold = ¾ × 7,20,000

Cost of goods sold = Rs. 5,40,000

Calculation of Net Purchases:-

Net Purchases = Purchases – Purchases Return

Net Purchases = Rs. 6,80,000 – Rs. 30,000

Net Purchases = Rs. 6,50,000

Calculation of Direct Expenses:-

Direct Expenses = Carriage Inwards + Wages

Direct Expenses = Rs. 20,000 + Rs. 50,000

Direct Expenses = Rs. 70,000

Question 5. (A)

Solution 5: (A)

Calculation of Closing Stock:-

Cost of goods sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Closing Stock = Opening Stock + Purchases + Direct Expenses – COGS

Closing Stock = Rs. 5,000 + Rs. 9,100 + Rs. 1,000 – Rs. 9,000

Closing Stock = Rs. 6,100

Calculation of Cost of Goods Sold:-

Cost of goods sold = Net Sales – Gross Profit

Cost of goods sold = Rs. 15,000 – Rs. 6,000

Cost of goods sold = Rs. 9,000

Calculation of Net Purchases:-

Net Purchases = Purchases - Purchases Return

Net Purchases = Rs. 10,000 - Rs. 900

Net Purchases = Rs. 9,100

Question 5. (B)

Solution 5 (B):

Calculation of Closing Stock:-

Cost of goods sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Closing Stock = Opening Stock + Purchases + Direct Expenses – COGS

Closing Stock = Rs. 38,000 + Rs. 3,36,000 + Rs. 26,000 – Rs. 3,75,000

Closing Stock = Rs. 25,000

Calculation of Cost of Goods Sold:-

Cost of goods sold = Net Sales + Gross Loss

Cost of goods sold = Rs. 3,60,000 – Rs. 5,000 + Rs. 20,000

Cost of goods sold = Rs. 3,75,000

Calculation of Net Purchases:-

Net Purchases = Purchases - Purchases Return

Net Purchases = Rs. 3,40,000 - Rs. 4,000

Net Purchases = Rs. 3,36,000

Question 6. (A)

Solution 6: (A) Net Sales = Rs. 8,00,000

Gross Profit = Sales × 40%

Gross Profit = Rs. 8,00,000 × 40%

Gross Profit = Rs. 3,20,000

Cost of Goods Sold = Sales – Gross Profit

Cost of Goods Sold = Rs. 8,00,000 – Rs. 3,20,000

Cost of Goods Sold = Rs. 4,80,000

Question 6. (B)

Solution 6: (B)

Cost of Goods Sold = Sales – Gross Profit

Cost of Goods Sold = Rs. 12,00,000 – Rs. 4,00,000

Cost of Goods Sold = Rs. 8,00,000

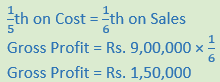

Question 7.

Solution 7:

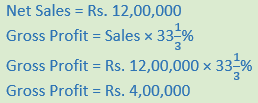

Net Sales = Rs. 9,00,000

Gross Profit = Sales × 20%

We know,

Cost of Goods Sold = Sales – Gross Profit

Cost of Goods Sold = Rs. 9,00,000 – Rs. 1,50,000

Cost of Goods Sold = Rs. 7,50,000

Question 8.

Solution 8:

Calculation of Closing Stock:-

Cost of goods sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Closing Stock = Opening Stock + Purchases + Direct Expenses – COGS

Closing Stock = Rs. 1,20,000 + Rs. 9,30,000 + Rs. 0 – Rs. 9,36,000

Closing Stock = Rs. 10,50,000 – Rs. 9,36,000

Closing Stock = Rs. 1,14,000

Calculation of Cost of Goods Sold:-

Cost of Goods sold = Net Sales – Gross Profit

Cost of Goods sold = Rs. 15,60,000 – Rs. 6,24,000

Cost of Goods sold = Rs. 9,36,000

Calculation of Gross Profit:-

Gross Profit = 40% of Sales

Gross Profit = Rs. 15,60,000 × 40%

Gross Profit = Rs. 6,24,000

Question 9.

Solution 9:

Calculation of Closing Stock:-

Cost of goods sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Closing Stock = Opening Stock + Purchases + Direct Expenses – COGS

Closing Stock = Rs. 4,80,000 + Rs. 13,60,000 + Rs. 0 – Rs. 15,00,000

Closing Stock = Rs. 18,40,000 – Rs. 15,00,000

Closing Stock = Rs. 3,40,000

Calculation of Cost of Goods Sold:-

Cost of Goods Sold = Sales – Gross Profit

Question 10.

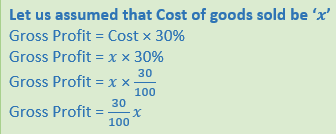

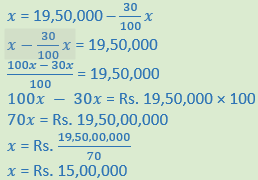

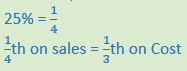

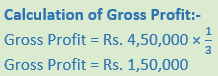

Solution 10 : Gross Profit = 25% on sales

We know,

Calculation of Sales:-

Cost of goods sold = Sales + Gross Profit

Sales = Cost of goods sold + Gross Profit

Sales = Rs. 4,50,000 + Rs. 1,50,000

Sales = Rs. 6,00,000

Question 11.

Solution 11:

Question 12.

Solution 12:

Working Note:-

Calculation of Operating Profit:-

Operating Profit = Net Profit – Non-Operating Income + Non-Operating Expenses

Operating Profit = Rs. 3,30,000 – Rs. 0 + Rs. 20,000

Operating Profit = Rs. 3,50,000

Point of Knowledge:-

Trading Account is the account that reveals the gross profit or gross loss. It is credited with the amount of sales of goods and debited with the opening stock of goods along with the direct expenses related to the sales made. Trading Account is prepared to know gross profit or gross loss during the accounting period.

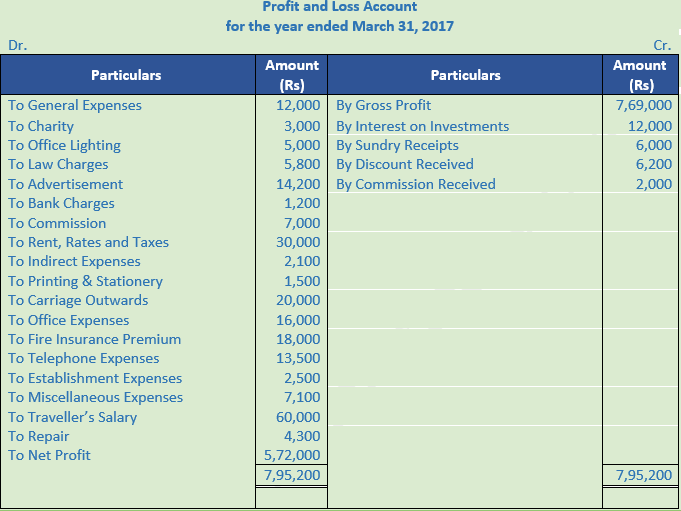

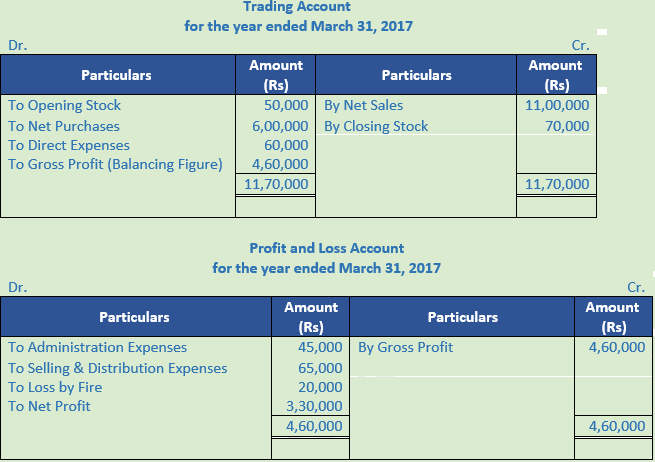

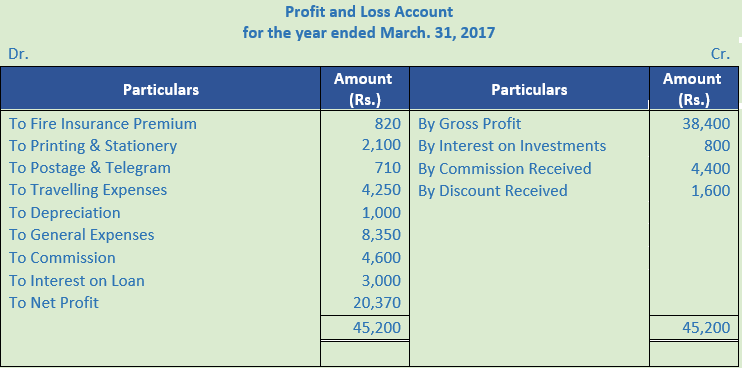

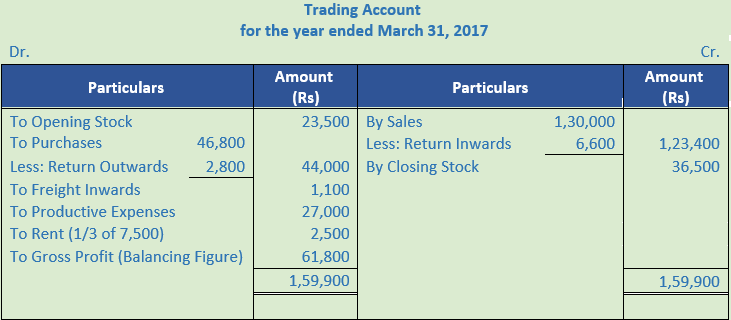

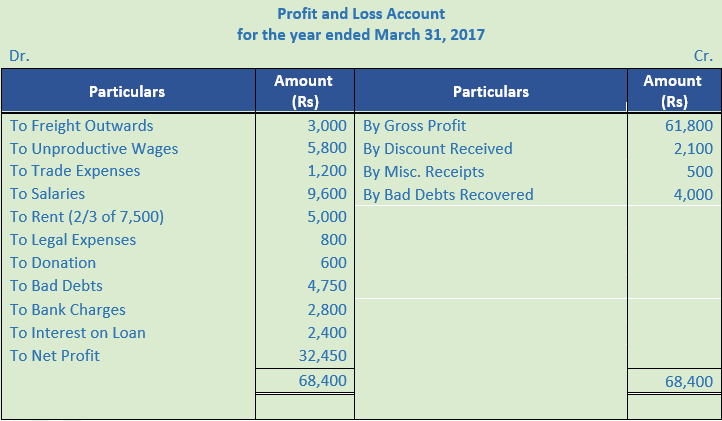

Question 13.

Solution 13:

Calculation of Operating Profit:-

Operating Profit = Net Profit − Non-Operating Income + Non-Operating Expenses

Operating Profit = 5,00,000 − 30,000 + 77,100

Operating Profit = Rs 5,47,100

Non-Operating Income = Dividend Received + Rent Received

Non-Operating Income = 6,000 + 24,000

Non-Operating Income = 30,000

Non-Operating Expenses = Loss on Sale of Furniture + Loss by Fire + Interest on Loan + Donation

Non-Operating Expenses = 12,000 + 50,000 + 10,000 + 5,100

Non-Operating Expenses = Rs 77,100

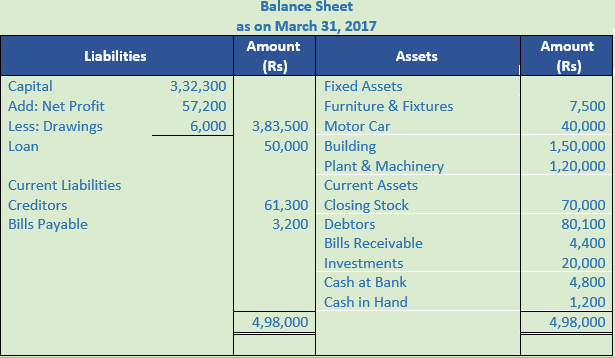

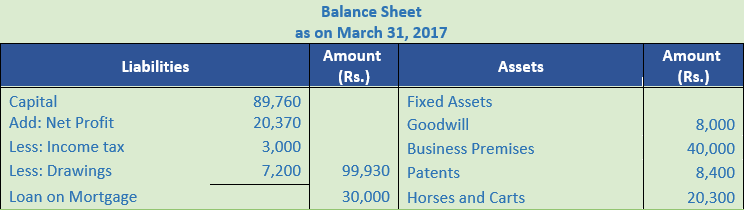

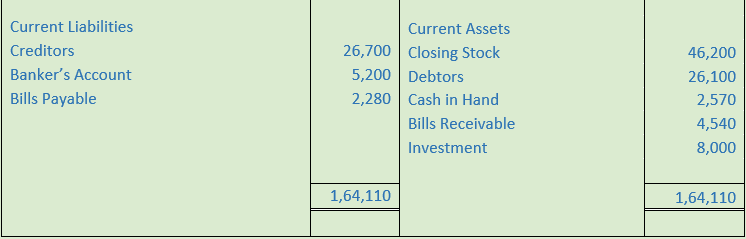

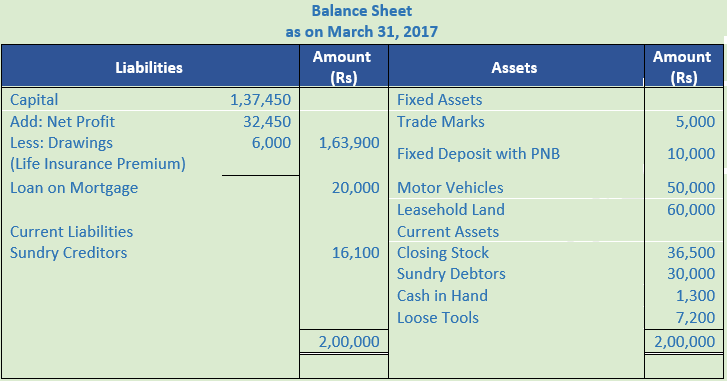

Question 14.

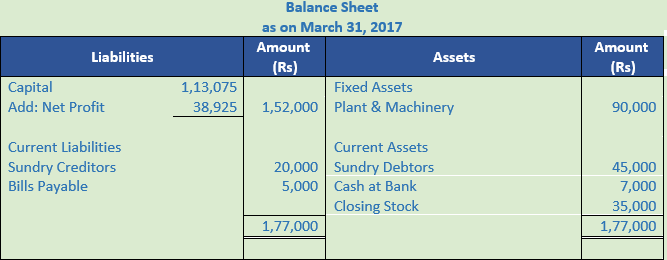

Solution 14:

Working Note:-

Balance Sheet is prepared with a view to measure true financial position of a business at a particular point of time. It is a method to show the financial position of a business in a systematic and standard form. The financial position of the business can be understood at a glance. The debit and credit balances of related accounts are shown on the assets and liabilities side of the Balance Sheet.

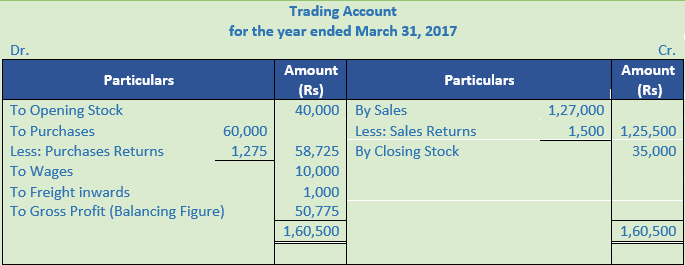

Question 15.

Solution 15:

Working Note:-

Indirect expenses are those expenses which are incurred and are not directly associated with the purchases of goods or manufacture of goods.

The two examples of indirect expenses are:

- Office salaries.

- Warehouse expenses

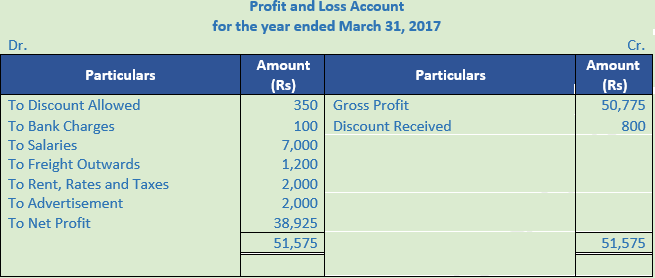

Question 16.

Solution 16

Point of Knowledge:-

Current Assets are those assets which are held for resale or for converting into cash. These are the assets which are likely to be realized within a period of one year or during the period of normal operating cycle. A business earns profit by selling these assets but not by keeping them as stock for a longer period. These assets are temporary in nature and may change from time to time. These are sometimes referred to as floating or circulating assets.

Question 17.

Solution 17:

Working Note:-

Calculation of Drawings:-

Drawings = Household Expenses + Life Insurance Premium

Drawings = Rs. 10,000 + Rs. 1,800

Drawings = Rs. 11,800

Question 18.

Solution 18:

Point of Knowledge:-

Current Assets are those assets which are held for resale or for converting into cash. These are the assets which are likely to be realized within a period of one year or during the period of normal operating cycle. A business earns profit by selling these assets but not by keeping them as stock for a longer period. These assets are temporary in nature and may change from time to time. These are sometimes referred to as floating or circulating assets.

Question 19.

Solution 19:

Point of Knowledge:-

Direct expenses are those expenses which are incurred on purchases of goods up to the point of bringing them to the place of business. In the case of manufacturing business, they are the expenses incurred to make then ready for sale.

The two examples of direct expenses are:

- Octroi paid on purchases.

- Power Expenses

Question 20.

Solution 20: Below is the Presentation of assets in the order of Permanence:

- Goodwill

- Land and Building

- Plant and Machinery

- Motor Vehicle

- Loose Tools

- Furniture

- Investment (Long-term)

- Stock

- Sundry Debtors

- Marketable Securities (Short-term)

- Cash at Bank

- Cash in Hand

Point of Knowledge:-

Current Assets are those assets which are held for resale or for converting into cash. These are the assets which are likely to be realized within a period of one year or during the period of normal operating cycle. A business earns profit by selling these assets but not by keeping them as stock for a longer period. These assets are temporary in nature and may change from time to time. These are sometimes referred to as floating or circulating assets.