Access free DK Goel Solutions Class 11 Accountancy Chapter 15 Bank Reconciliation Statement 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 15 Bank Reconciliation Statement DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 15 Bank Reconciliation Statement Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 15 Bank Reconciliation Statement DK Goel Class 11 Solved Exercises

Long Answer Question

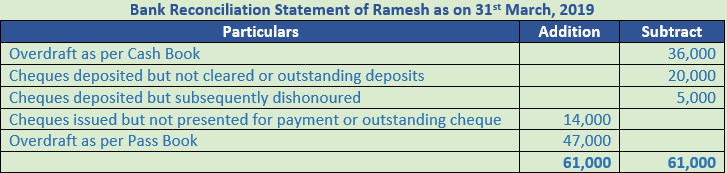

Question 1.

Solution 1: Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Need and Importance of Bank Reconciliation Statement:-

(1) A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

(2) By Preparing a bank reconciliation statement, the customer becomes sure of the correctness of the bank balance shown by the cash book. It helps him in making further transactions with the bank.

(3) A reconciliation statement facilitates the preparation of a revised cash book.

(4) Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

(5) A reconciliation statement helps in revealing the unnecessary delay in the collection of cheque by the bank.

(6) It also help in keeping a track of cheque which have been sent to the bank for collection.

Short Answer Question

Question 1.

Solution 1:

Bank Reconciliation Statement is prepared for the following reasons:

- It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

- Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

- Regular reconciliation discourages embezzlements. Reconciliation helps the management to verify the accuracy of entries recorded in the Cash Book.

- It shows actual bank balance.

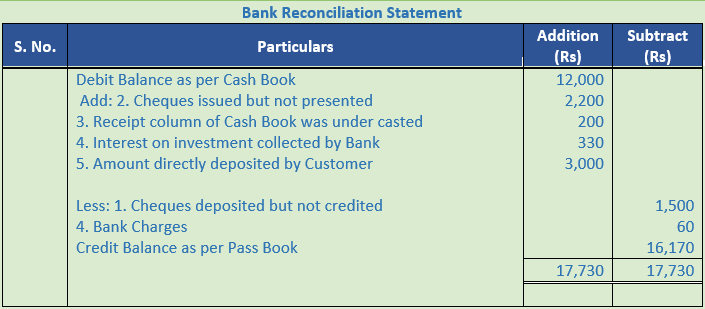

Question 2.

Solution 2:

(i) Cheques drawn but not cleared.

(ii) Interest on bank overdraft.

(iii) Cheques paid into the bank but not collected.

(iv) Interest on investment collected by the bank.

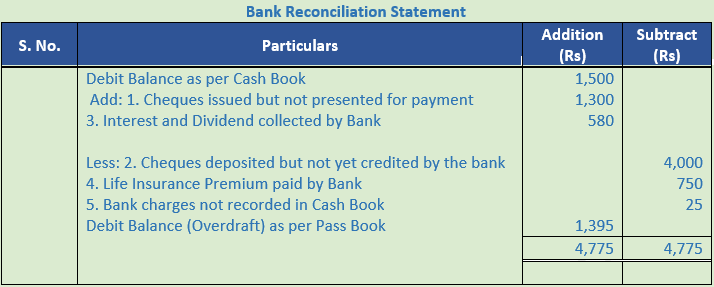

Question 3.

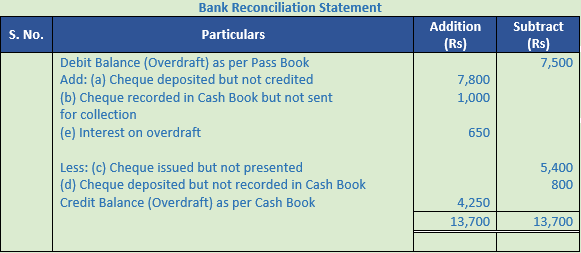

Solution 3:

Question 4.

Solution 4: Cheque issued but not yet presented for payment in the bank.

- Bank charges and commission charged by the bank.

- Direct deposit by customer into the bank.

- Direct payment made by the bank on behalf of customers.

- Transaction wrongly debited in cash book.

- Transaction wrongly credited in pass book.

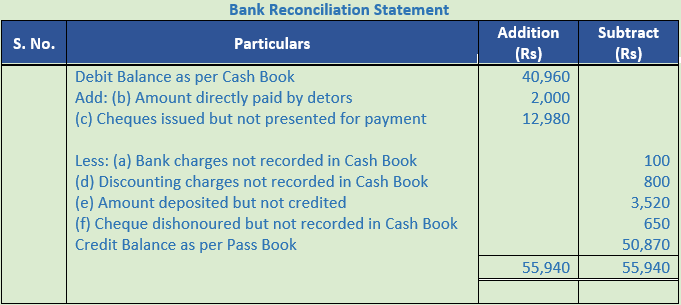

Question 5.

Solution 5:

(i) Plus

(ii) Minus

(iii) Minus

(iv) Plus

Question 6.

Solution 6:

(i) Minus

(ii) Minus

(iii) Minus

(iv) Plus

Question 7.

Solution 7:

Question 8.

Solution 8:

Bank Reconciliation Statement Practical Questions Class 11 BRS

Numerical Questions

Question 1.

Solution 1.

Point of Knowledge:-

- Regular reconciliation discourages embezzlements. Reconciliation helps the management to verify the accuracy of entries recorded in the Cash Book.

- Bank reconciliation statement shows actual bank balance.

Question 2.

Solution 2:

Working Note:-

- Cheque issued but not presented for payment = Rs. 600 + Rs. 800 + Rs. 1,200 = Rs. 2,600

- Cheque deposited but not credited by the bank = Rs. 500 + Rs. 700 = Rs. 1,200

Point of Knowledge:-

- It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

- Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

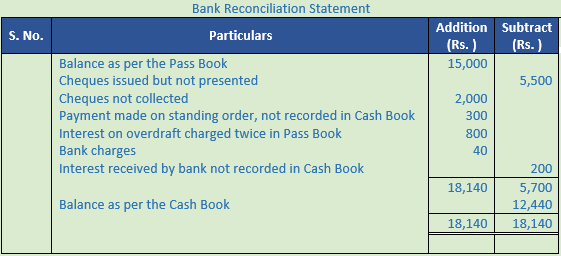

Question 3.

Solution 3:

Working Note:-

1.) Cheques issued but not presented = 9,200 – 7,000 = 2,200

2.) Cheques deposited but not credited = 8,000 – 6,500 = 1,500

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 4.

Solution 4:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 5.

Solution 5 :

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 6.

Solution 6 :

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 7.

Solution 7:

Point of knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 8.

Solution 8:

Working Note:-

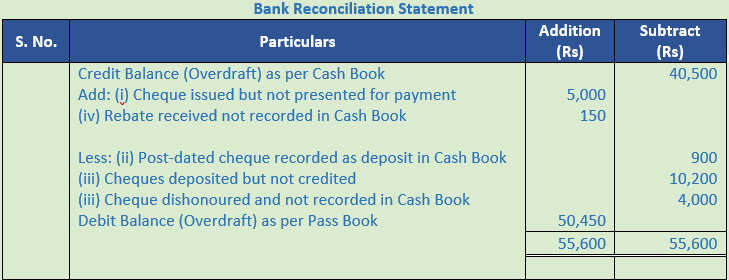

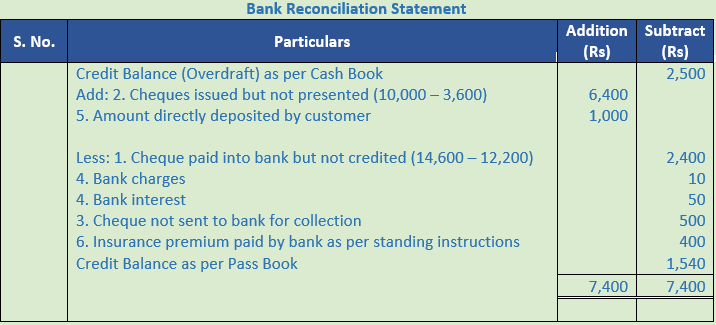

Cheques issued but not presented = Rs. 10,000 – Rs. 3,600 = Rs. 6,400

Cheque paid into bank but not credited Rs. 14,600 – Rs. 12,200 = Rs. 2,400

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 9.

Solution 9:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 10.

Solution 10:

Point of knowledge:-

- It detects the errors that may have been committed either in the Cash Book or Bank Statement or Bank Pass Book.

- Undue delay in clearance of cheque deposited or issued is known from the reconciliation.

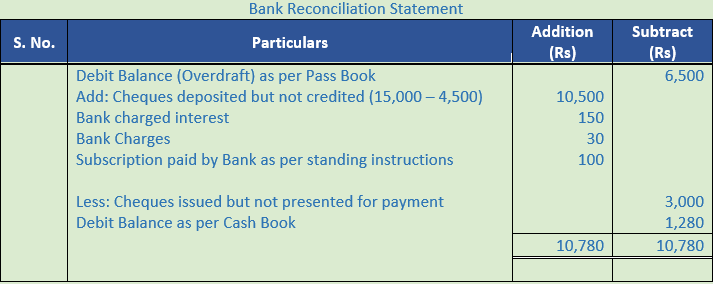

Question 11.

Solution 11:

Working Note:-

Cheques deposited but not credited = Rs. 15,000 – Rs. 4,500 = Rs. 10,500

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 12.

Solution 12:

Point of knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 13.

Solution 13:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 14.

Solution 14:

Working Note:-

Cheque issued but not presented = Rs. 15,600 – Rs. 11,000 = Rs. 4,600

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

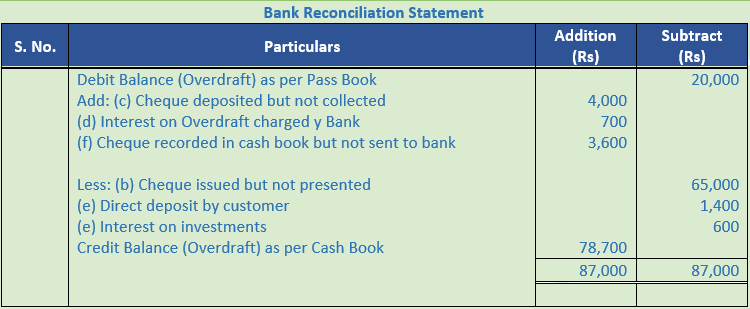

Question 15.

Solution 15:

Working Note:-

1. Cheque deposited but not collected = Rs. 6,500 – Rs. 2,500 = Rs. 4,000

2. Cheque issued but not presented = Rs. 80,000 – Rs. 15,000 = Rs. 65,000

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 16.

Solution 16:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 17.

Solution 17:

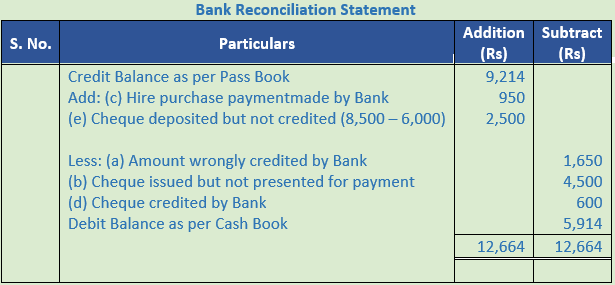

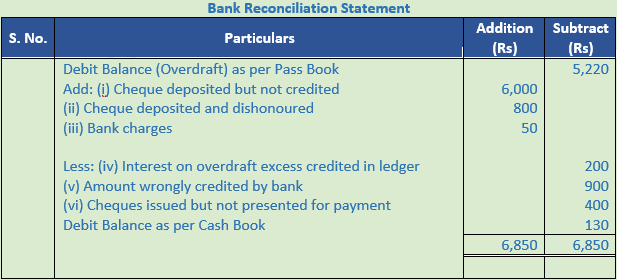

Question 18.

Solution 18:

Working Note:-

Cheque deposited but not credited = Rs. 8,500 – Rs. 6,000 = Rs. 2,500

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

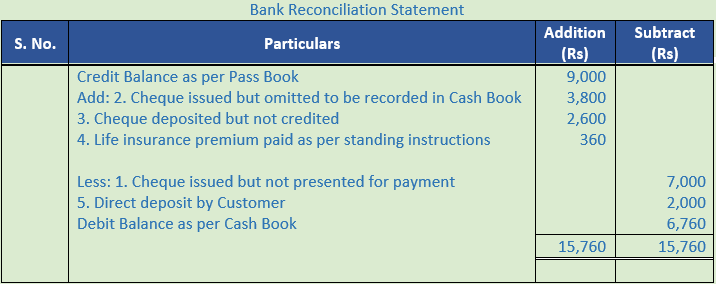

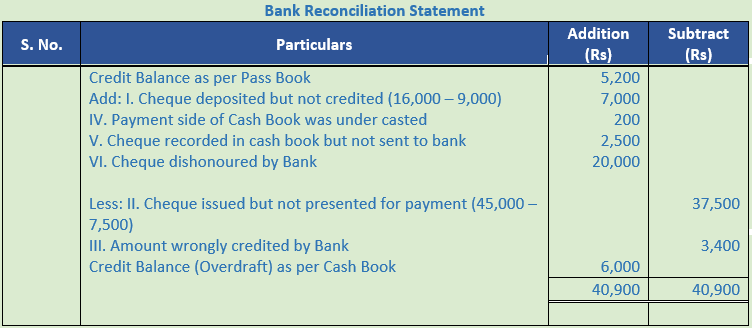

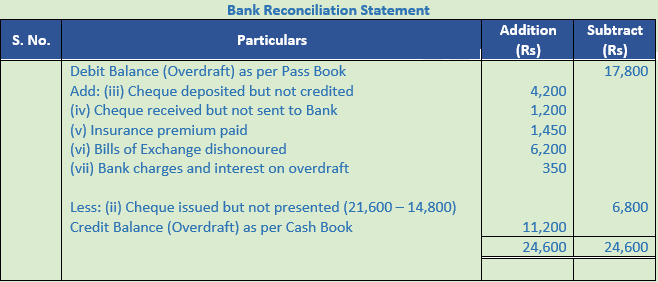

Question 19.

Solution 19:

Working Note:-

Cheque deposited but not credited Rs. 16,000 – Rs. 9,000 = Rs. 7,000

Cheque issued but not presented for payment = Rs.45,000 – Rs. 7,500 = Rs. 37,500

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 20.

Solution 20:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 21.

Solution 21:

Working Note:-

Cheque issued but not presented for payment Rs. 15,000 – Rs. 3,000 = Rs. 12,000

Point of knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

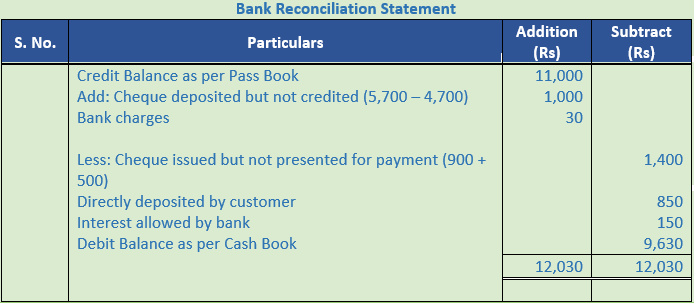

Question 22.

Solution 22:

Working Note:-

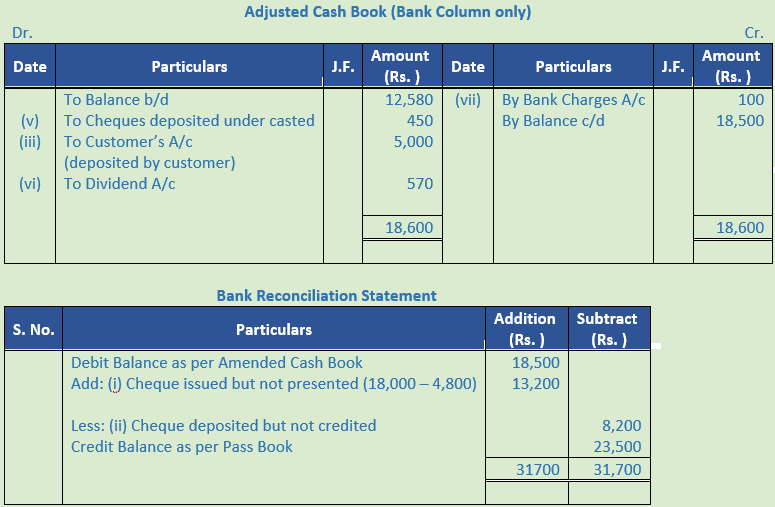

Cheques deposited under casted = Rs. 12,720 – Rs. 12,270 = Rs. 450

Cheque issued but not presented = Rs. 18,000 – Rs. 4,800 = Rs. 13,200

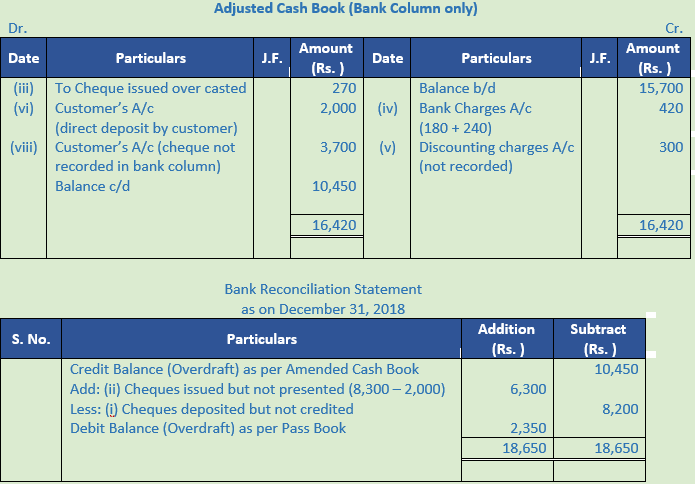

Question 23.

Solution 23:

Working Note:-

Cheque issued over casted Rs. 4,520 – Rs. 4,250 = Rs. 270

Bank Charges = Rs. 180 + Rs. 240 = Rs. 420

Cheques issued but not presented = Rs. 8,300 – Rs. 2,000 = Rs. 6,300

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 24.

Solution 24:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 25.

Solution 25:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 26.

Solution 26:

Working Note:-

Amount wrongly credited by bank Rs. 530 – Rs. 350 = Rs. 180

Overcasting of Payment side of Cash Book Rs. 5,420 – Rs. 4,520 = Rs. 900

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 27.

Solution 27:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 28.

Solution 28:

Point of Knowledge:-

Bank reconciliation statement is a statement prepared mainly to reconcile the difference between the ‘Bank Balance’ shown by the Cash Book and Bank Pass Book.”

Question 29.

Solution 29:

Working Note:-

Cheque deposited but not credited Rs. 4,800 – Rs. 3,800 = Rs. 1,000

Cheque issued but not presented Rs. 1,200 + Rs. 200 = Rs. 1,400

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 30.

Solution 30:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 31.

Solution 31:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

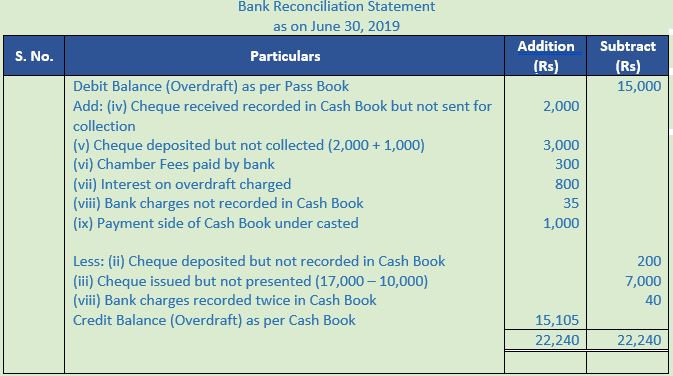

Question 32.

Solution 32:

Working Note:-

Cheque deposited but not collected = Rs. 2,000 + Rs. 1,000 = Rs. 1,000

Cheque issued but not presented = Rs. 17,000 – Rs. 10,000 = Rs. 7,000

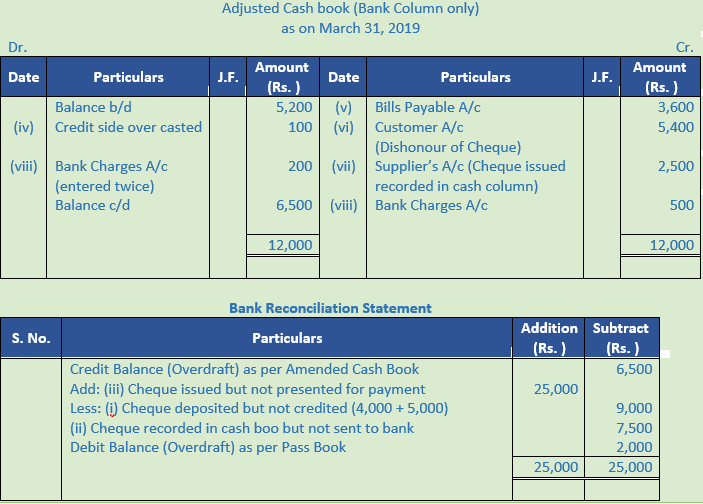

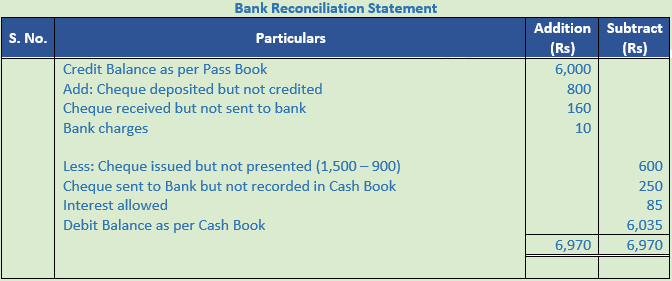

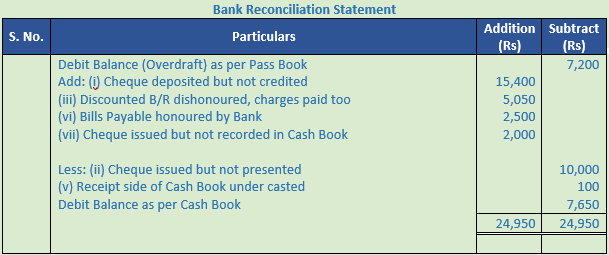

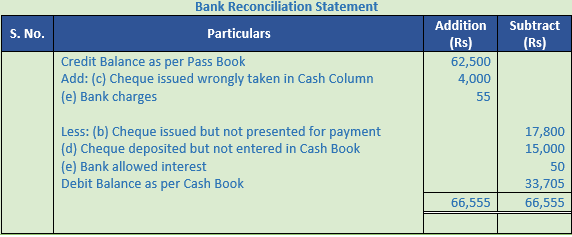

Question 33.

Solution 33:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

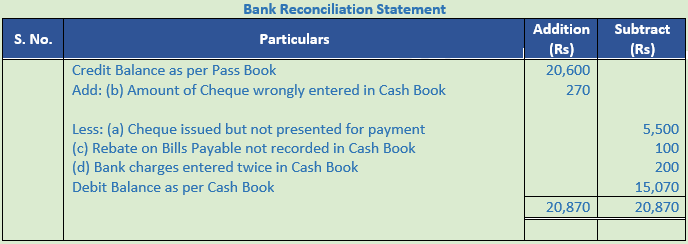

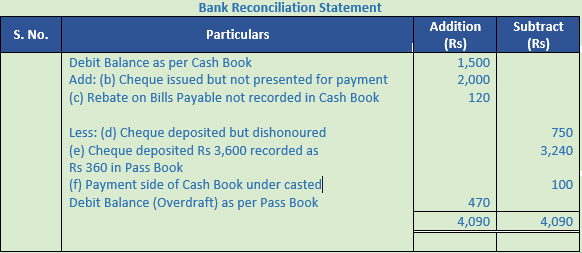

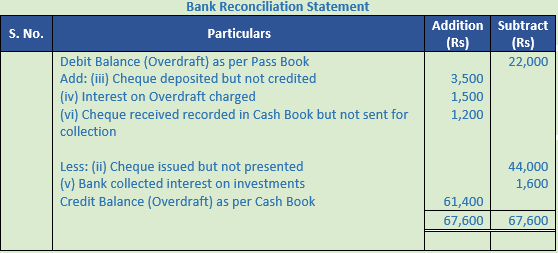

Question 34.

Solution 34:

Working Note:-

Amount of Cheque wrongly entered in Cash Book = Rs. 5,745 – Rs. 5,475 = Rs. 270

Point of Knowledge:-

The third transaction in above question will not effect on the balance of bank as the cheque is not represented into bank.

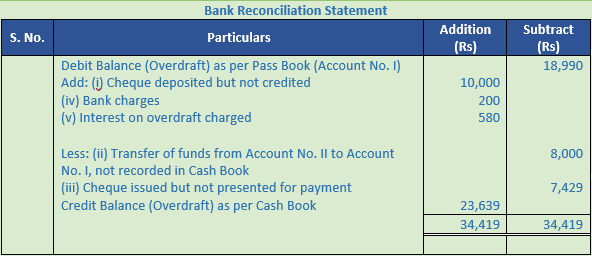

Question 35.

Solution 35:

Working Note:-

Cheque deposited but not credited Rs. 8,000 + Rs. 6,000 + Rs. 1,400 = Rs. 15,400

Cheque issued but not presented Rs. 12,000 – Rs. 2,000 = Rs. 10,000

Point of Knowledge:-

The fourth transaction in above question will not effect on the balance of bank as the cheque is not represented into bank.

Question 36.

Solution 36:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 37.

Solution 37:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

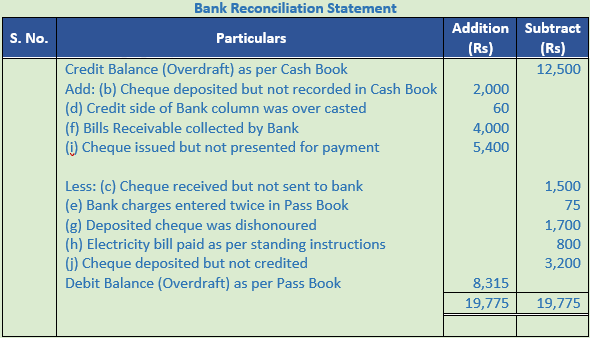

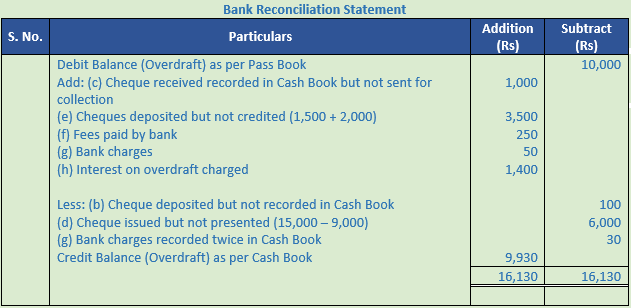

Question 38. .

Solution 38:

Working Note:-

Cheques deposited but not credited = Rs. 1,500 + Rs. 2,000 = Rs. 3,500

Cheque issued but not presented = Rs. 15,000 – Rs. 9,000 = Rs. 6,000

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 39.

Solution 39:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

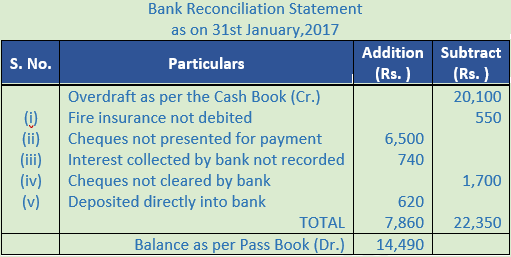

Question 40. :

Prepare a Bank Reconciliation Statement of Mr. James Flint as on 31-12-2019.

Solution 40:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 41.

Solution 41:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

Question 42.

Solution 42:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 43.

Solution 43:

Working Note:-

Cheque deposited but not credited Rs. 4,500 – Rs. 1,000 = Rs. 3,500

Cheque issued but not presented Rs. 50,000 – Rs. 6,000 = Rs. 44,000

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.

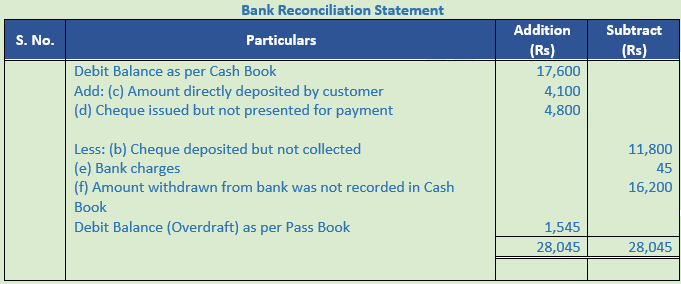

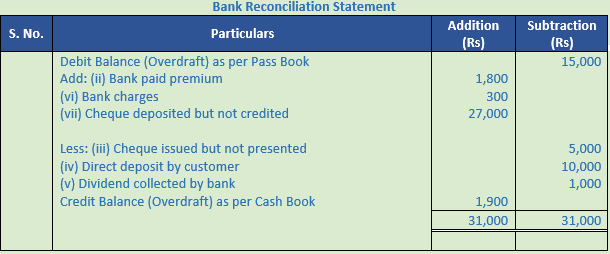

Question 44.

Solution 44:

Working Note:-

Bank paid premium = Rs. 2,000 – Rs. 200 = Rs. 1,800

Cheque deposited but not credited = Rs. 78,000 – Rs. 51,000 = Rs. 27,000

Cheque issued but not presented = Rs. 55,000 – Rs. 50,000 = Rs. 5,000

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 45.

Solution 45:

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

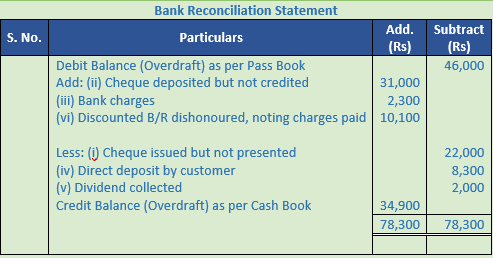

Question 46.

Solution 46:

Working Note:-

Cheque issued but not presented Rs. 7,800 – Rs. 2,400 = Rs. 5,400

Point of Knowledge:-

A bank reconciliation statement locates the error or omissions that may have been committed either on the part of the bank. The error so detected can be rectified accordingly.

Question 47.

Solution 47:

Point of Knowledge:-

Periodic preparation of this statement reduce the chances of embezzlement by the staff of this firm or even that of the bank. For example, if a cashier makes an entry in the cash book but does not deposited the cash and cheques into the bank, it will be disclosed by preparing a bank reconciliation statement.