Access free TS Grewal Accountancy Class 11 Solution Chapter 19 Adjustments in Preparation of Financial Statements 2026 below. Students can now access free TS Grewal Solutions for Class 11 Accountancy. These chapter-wise exercises are designed by expert Accountancy teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Accountancy Chapter 19 Adjustments in Preparation of Financial Statements TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 19 Adjustments in Preparation of Financial Statements Class 11 Accountancy below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 19 Adjustments in Preparation of Financial Statements TS Grewal Class 11 Solved Exercises

About this chapter: While maintaining books of accounts there are various types of adjustments that the Accountants have to do on regular basis to make sure the books are complete and accurate. In Chapter 19 of TS Grewal these concepts of passing adjustment entries have been explained in an easy to understand manner. there are very types of adjustments such as bad debts, provision for doubtful debts, accrued income, and prepaid expenses etc which have to be passed at the month end or end of the year to correctly adjust the books accounts. it is very important for class 11 students to clearly understand the topics which have been explained in the chapter as a lot of questions come in the exams relating to these topics. There are a lot of concepts followed by the article and numerical questions which have been given in this chapter which the students should practice on a regular basis. we have provided the solutions to all the questions in the final accounts with adjustments questions with solutions chapter and you can refer to the answers provided below, these have been prepared by the accountancy teachers of class 11th.

Question.1 What is meant by Adjusting Entries?

Answer 1.

Adjusting Entries are the entries passed to record expenses and incomes that relate to the accounting period but yet to be paid or recovered.

Question.2 Why is it necessary to pass adjusting entries when final accounts are prepared?

Answer 2.

It necessary to pass adjusting entries when final accounts are prepared, because Accrual Concept is the fundamental accounting concept and requires that all expenses, whether paid or not, should be accounted to ascertain correct profit or loss, assets and liabilities. They are recorded through the adjustment entries.

Question.3 What are Outstanding Expenses? What is its adjusting entry?

Answer 3.

Outstanding Expenses mean the expenses incurred but not yet paid. At the end of the accounting year such expenses is accounted in the books, otherwise profit will be overstated and liabilities will be understated. Its adjusting entry is:

Expenses A/c Dr.

To Outstanding Expenses A/c

(Being particular expenses provided)

Question.4 What is meant by Prepaid Expenses? How are they adjusted in the Final Accounts?

Answer 4.

Prepaid Expenses are those expenses which we pay in this year, the benefit of which expenses relates to next accounting year. Such part of the expenses is known as prepaid expenses or unexpired expenses. The unexpired part such expenses is deducted from the total expenses in the Profit and Loss Account and prepaid expenses are shown as an asset in the Balance Sheet under the head current assets.

Question.5 Define Accrued Income. What is its adjusting entry?

Answer 5.

Accrued Incomes or Outstanding Incomes are those incomes which have been earned during the accounting period but have not been received till the end of accounting period. As per the Accrual Concept of Accounting, total income of the period, both received and yet to be received, are shown in the Final Accounts otherwise the profit and assets will remain under stated.

The adjusting entry for this purpose is:

Accrued Income A/c

To Income A/c (Amount of Particular Income)

To Output CGST A/c (Amount of CGST)

To Output SGST A/c (Amount of SGST)

(Being the particular accrued income accounted in the books)

Question.6 What is Unearned Income? How is it adjusted in the Final Accounts?

Answer 6.

Unearned Income or Income Received in Advance means an income that has not been earned but is received in advance. At times an amount is received during a year in respect of an income that relates partially or fully to the next year.

It is adjusted in the Final Accounts as given below:

1. In the credit side of Profit and Loss Account by deducting from the amount under that head of income.

2. In the liabilities side of the Balance Sheet under the head current liabilities.

3. If income received in advance is shown in the trial Balance, it means that the adjusting entry is already passed. It such a case, Income Received in Advance is shown in the Balance Sheet under the head current liabilities.

Question.7 What is meant by Provision for Discount on Debtors?

Answer 7.

Customers are entitled to cash discount if they pay the due amount on time. The payment may be received in next year, therefore the discount should also be allowed only in the next year. But, since the book debts have arisen during the current year, discount to be allowed should be treated as an expense of the current year. The process is the same as for the Provision for Doubtful Debts. The expect amount of the discount to be allowed is debited to the Profit and Loss Account and credited to the Provision for Discount on Debtors Account. The balance in the letter account is deducted from book debts in the Balance Sheet and is carried forward to the next year. Actual discount allowed next year is debited to Provision for Discount on Debtors Account and not to the Profit and Loss Account. The amount debited reduces balance in the Provision for Discount on Debtors Account, it is made up to the required amount by a debit to Profit and Loss Account and credit to the Provision for Discount on Debtors Account just like Provision for Doubtful Debts Account.

Question.8 Show the treatment of the following in final accounts when given inside the Trial Balance:

(i) Provision for Discount on debtors

(ii) Closing stock

(iii) Commission Received in Advance.

Answer 8.

(i) If provision for discount on debtors is given in the Trial Balance, then it is shown in the credit side of Profit and Loss Account. If new provision fordiscount on debtors is made in the current year, then it is shown in thedebit side of the Profit and Loss Account and provision for discount ondebtors if given in the Trial Balance at lesser value than the new provisionfor discount amount then it is deducted in the debit side from newprovision and vice versa.

(ii) If closing stock is given in the Trial Balance, then it is shown in the assets side of Balance Sheet under the head current assets.

(iii) If Commission received in Advance Account is given in the Trial Balance, then it is shown in the liabilities side of Balance side under the head current liabilities.

Question.9 Ravi’s Trail Balance as on 31st March,2019 has the following information:

What is the amount of outstanding interest to be provided?

Answer 9.

The amount of outstanding interest to be provided

=Total Interest – Interest paid during the year

= Rs. 1,00,000 × 10/100 × 6/12 – Rs. 4,000

= Rs. 5,000 – Rs. 4,000

= Rs. 1,000

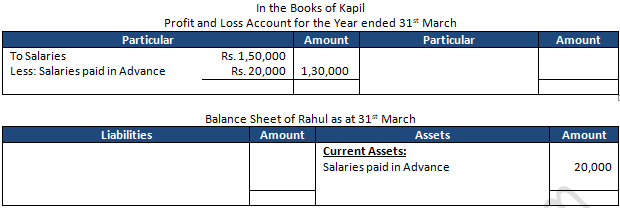

Question.10 Manish has paid salaries of Rs. 1,50,000 for the year ended 31st March, 2019. Salaries include Rs. 20,000 paid in advance for the year ending 31st March. 2020. Show how it will be shown in the Profit and Loss Account and the Balance Sheet.

Answer 10.

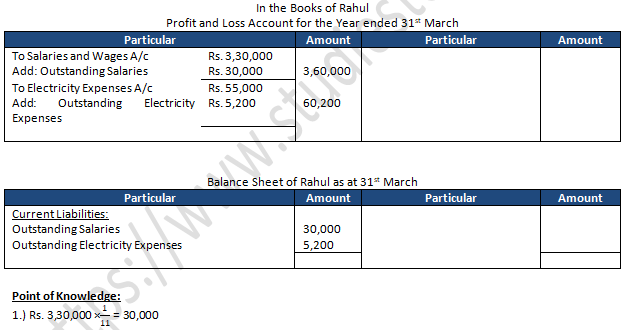

Question.11 Rahul’s Trial Balance as on 31st March,2019 has the following information:

Additional information: (i) Salary for the month of March, 2019 is yet to be paid. (ii) Electricity Bill for March,2019 amounted to Rs.5,200 was received on 2nd April,2019.

Answer 11.

Question.12 Ramesh’s Trail Balance as on 31st March, 2019 given the following information:

Show how the above items would appear in the Profit and Loss Account and Balance Sheet.

Answer 12.

Question.13 Ramesh’s Trail Balance given the following information:

Depreciation is provided @ 10% p.a. on the fixed assets. Show how this will be shown in the Profit and Loss Account.

Answer 13.

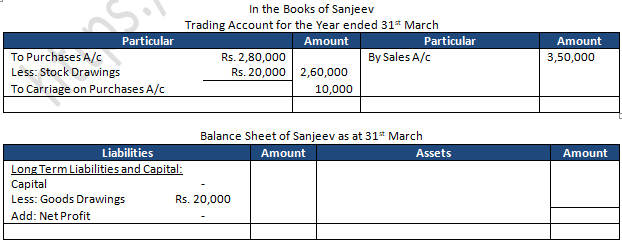

Question.14 Sanjiv’s Trial Balance as on 31st March, 2019 shows the following information:

Sanjiv took goods costing Rs.20,000 for his personal use but entry was not passed in the books of account. Show the treatment in the Final Accounts.

Answer 14.

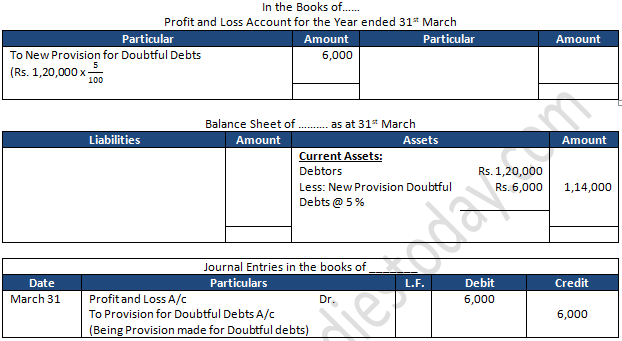

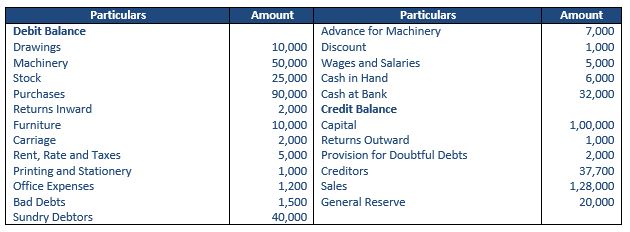

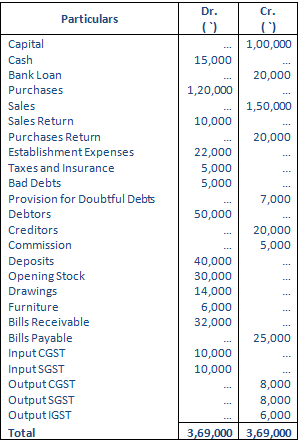

Question.15 Following is the extract of Trail Balance as on 31st March,2019:

![]()

Adjustment: Create a Provision for Doubtful Debts @ 5% on Debtors. Pass necessary entry and show these items in the Profit and Loss account and the Balance Sheet.

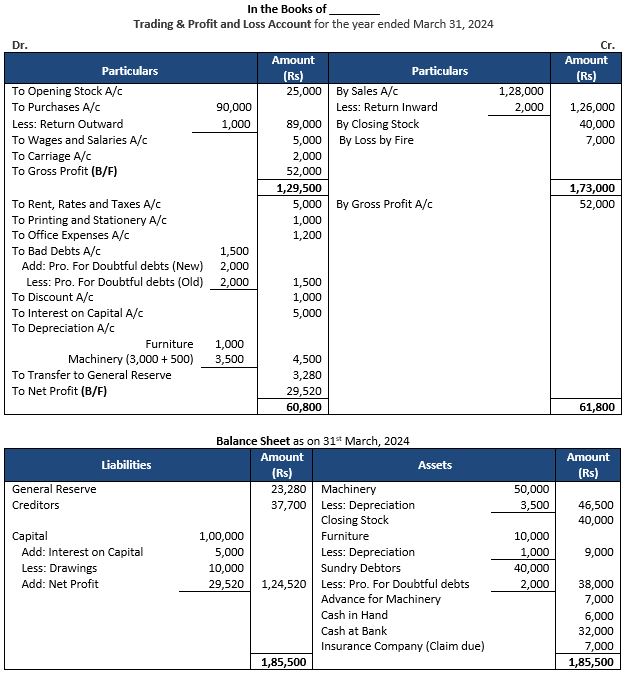

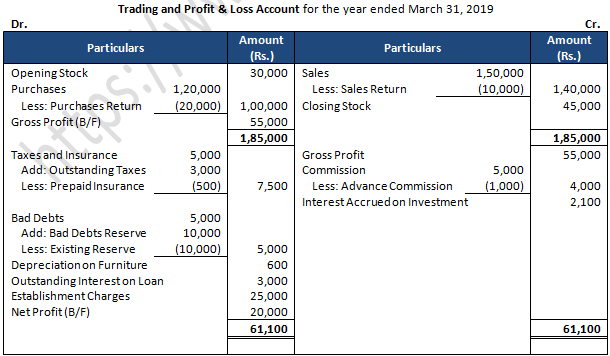

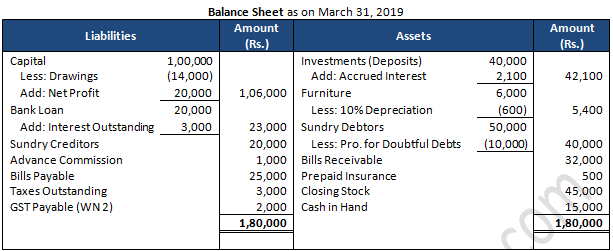

Answer 15.

Question.16 Sundry debtors in a Trail Balance are Rs. 90,000. Write off Rs. 5,000 as bad debts and make a Provision for Doubtful Debts @ 10% on sundry debtors.

Pass necessary Journal entries.

Answer 16.

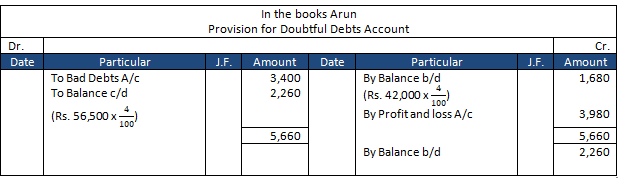

Question.17 Arun is a trader. While preparing his final accounts on 31st March, 2018, he made a provision for doubtful debts @ 4% of the sundry debtors amounting to Rs.42,000. During the year ended 31st March,2019 doubtful debts amounted to Rs. 3,400. On 31st March,2019, Sundry debtors were Rs. 56,500 and the provision for doubtful debts was maintained at the same rate.

Show the entries to record the above matters in Arun’s Ledger Accounts.

Answer 17.

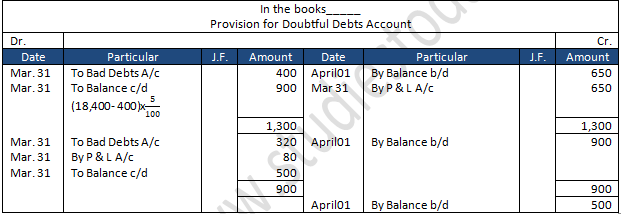

Question.18 On 1st April, 2007, Shiv had a Provision for Doubtful Debts of Rs. 650. On 31st March,2018, total debtors amounted to Rs. 18,400 out of which Rs. 400 were bad and had to be written off. It was decided to maintain a Provision for Doubtful Debts at 5% of the debtors.

On 31st March,2019, debtors were Rs. 10,320 out of which Rs.320 had to be written off as bad debts. Provision for Doubtful Debts is to be maintained at 5% of the Debtors.

Show the Bad Debts Account and Provision for Doubtful Debts Account for the years ended on 31st March, 2018 and 2019.

Answer 18.

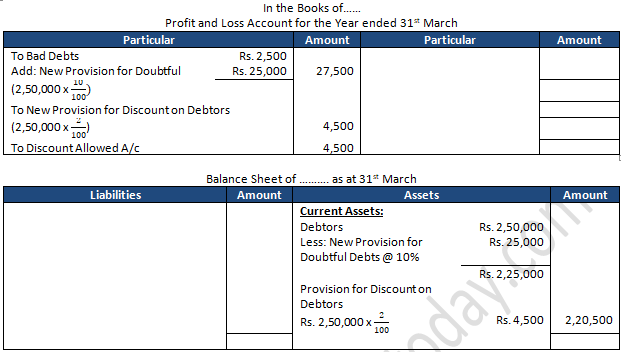

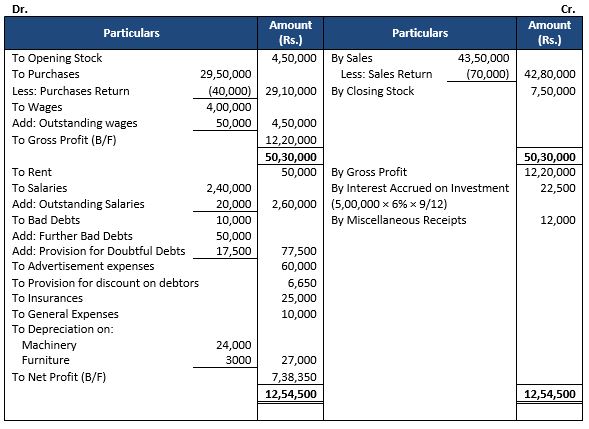

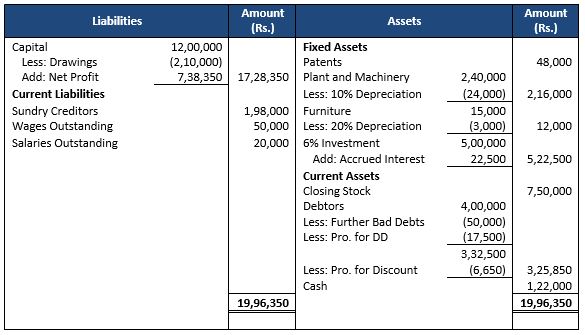

Question.19 The Trail Balance of Manish gives the following information:

It is decided to create a Provision for Doubtful Debts @ 10% on debtors and a Provision for Discount @ 2% on debtors. Show how the adjustment will appear in the Final Accounts.

Answer 19.

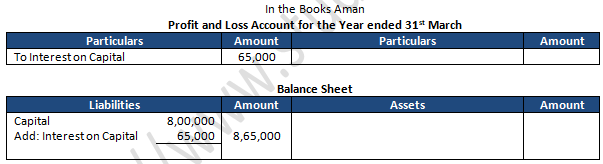

Question 20. Aman started business with capital of Rs. 5,00,000 on 1st April, 2020. He introduced additional capital of Rs. 3,00,000 on 1st October, 2020. He charged interest on capital @ 10% p.a. Calculate the amount of interest on capital and shows it in final accounts.

Answer 20:

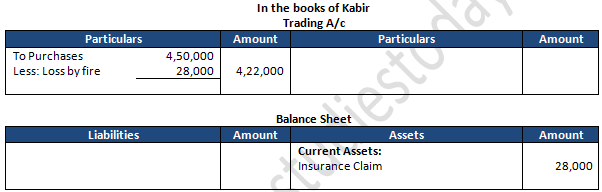

Question 23. Following extract is taken from the Trial Balance of Kabir as on 31st March, 2021:

A fire broke out on 31st March, 2021 and stock of value of Rs. 28,000 was destroyed. It was fully insured and the insurance company admitted the claim in full. Show the treatment in final accounts.

Answer 23:

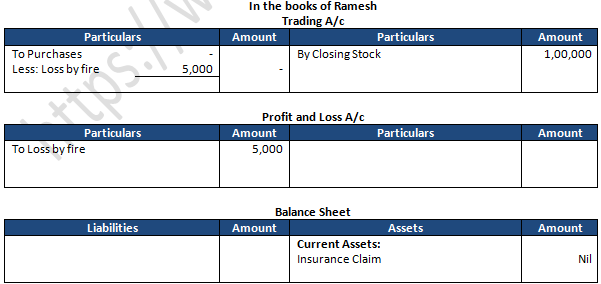

Question 24. Ramesh valued stock at the end of the year at Rs. 1,00,000. Goods costing Rs. 5,000 were destroyed by fire during the accounting period. Show the treatment if the goods are not insured.

Answer 24:

Question 25. Following is the extract of Trial Balance as on 31st March, 2021:

Additional Information:

One installment of Loan from SBI of Rs. 40,000 was received on 1st January, 2021. Calculate the amount of outstanding interest to be provided.

Answer 25:

Calculation of Interest on Loan:-

Interest on Loan = Rs. 1,20,000 × 8/100 × 6/12

Interest on Loan = Rs. 4,800

Interest on Loan = Rs. 1,60,000 × 8/100 × 3/12

Interest on Loan = Rs. 3,200

Outstanding Interest on Loan = Rs. 8,000 – Rs. 6,000 = Rs. 2,000

Question.26 Give Journal entries for the following adjustments in final accounts:

(i) Salaries Rs. 5,000 are outstanding.

(ii) Insurance amounting to Rs.2,000 is paid in advance.

(iii) Rs. 4,000 for rent have been received in advance.

(iv) Commission earned but not received Rs. 1000.

(v) Interest on Capital Rs. 1,500.

(vi) Interest on Drawings Rs. 300.

(vii) Write off Rs. 2,000 as further debts.

(viii) Closing Stock Rs. 3,000.

Answer 26.

(i) Salaries Rs. 5,000 are outstanding.

Practical Problems:-

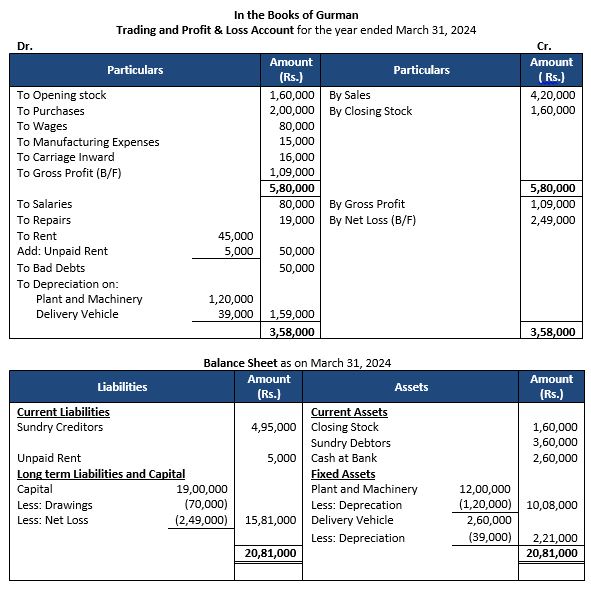

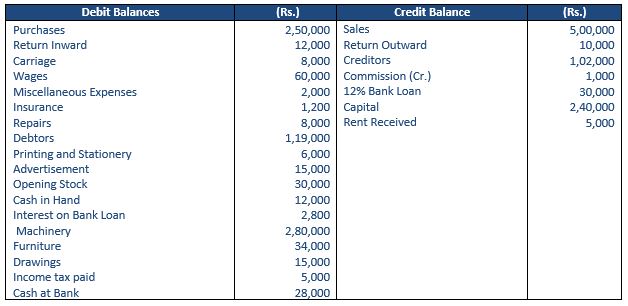

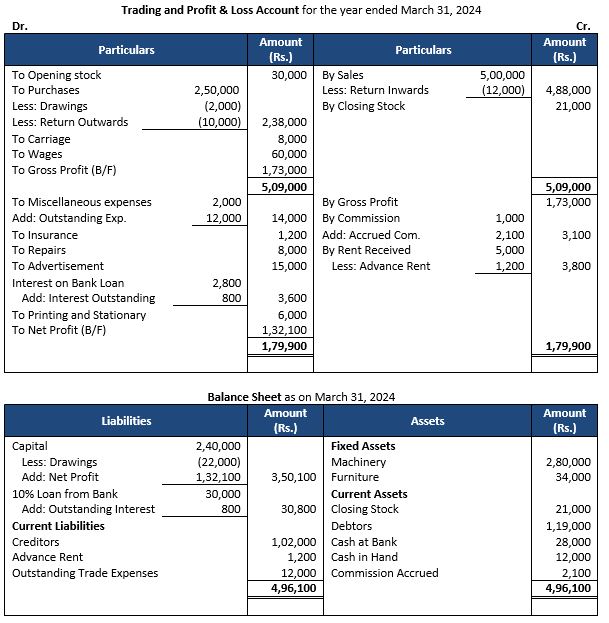

Question 1. Following are the balances extracted from the books of Gurman on 31st March, 2024:

Prepare Trading and Profit and Loss Account and Balance Sheet as at 31st March, 2019 after following adjustments are made:

(i) Closing Stock was Rs. 16,000.

(ii) Depreciate Plant and Machinery @ 10% and Delivery Vehicle @ 15%.

(iii) Unpaid Rent amounted to Rs. 500.

Answer 1:

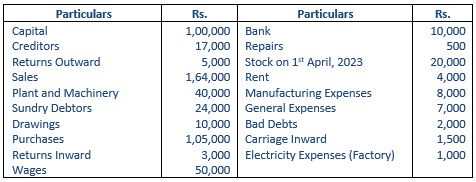

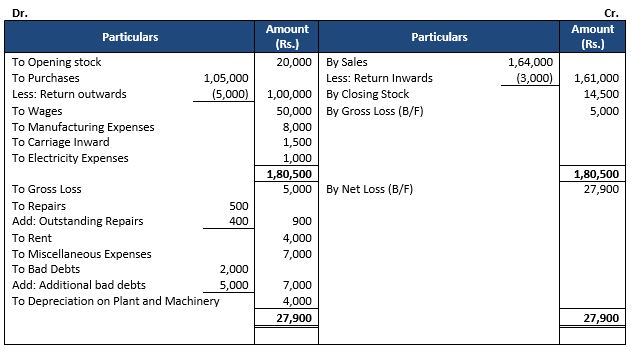

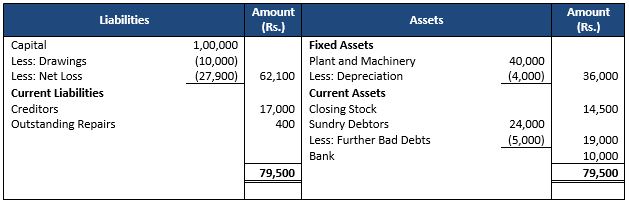

Question 2: Prepare Trading and Profit and Loss Account and Balance Sheet from the following balances, relating to the year ended 31st March, 2024:

Additional Information:

(i) Closing Stock was valued at Rs. 14,500.

(ii) Depreciate Plant and Machinery by Rs. 4,000.

(iii) Write off Bad Debts Rs. 5,000.

(iv) Rs. 400 is due for repairs.

Answer 2:

Trading and Profit & Loss Account for the year ended March 31, 2024

Balance Sheet as on March 31, 2024

Question 3: Following Trial Balance has been extracted from the books of Pawan as on 31st March, 2024:

Additional Information:

(i) Outstanding salaries were Rs. 45,000.

(ii) Depreciate Machinery at 10%.

(iii) Wages outstanding were Rs. 5,000.

(iv) Rent prepaid Rs. 10,000.

(v) Provide for interest on capital @ 5% per annum.

(vi) Stock on 31st March, 2024 Rs. 8,00,000.

Prepare Trading and Profit and Loss Account for the year ended 31st March, 2024 and Balance Sheet as at that date.

Answer 3:

In the Books of M/s. Ram Prasad & Sons

Trading Account Profit & Loss for the year ended March 31, 2024

Balance Sheet as on March 31, 2024

Question 4: Trial Balance of a business as at 31st March, 2024 is given below:

Prepare Trading and Profit and Loss Account for the year ended 31st March, 2024 and Balance Sheet as at that date after taking into account the following adjustments:

(i) Closing Stock was valued at Rs. 70,000.

(ii) Outstanding liabilities for wages were Rs. 6,000 and salaries Rs. 14,000.

(iii) Depreciation is to be provided @ 5% p.a. on fixed assets.

(iv) Included in Plant and Machinery is a machine purchased for Rs. 1,00,000 on 1st October, 2023.

(v) Insurance premium paid in advance Rs. 2,000.

Answer 4:

Trading and Profit & Loss Account for the year ended March 31, 2024

Balance Sheet as on March 31, 2024

Question 5: From the following Trial Balance of Sunil as 31st March, 2024, prepare Trading and Profit & Loss Account for the year ended 31st March, 2024 and Balance Sheet as at that date:

Adjustments:-

(i) Closing Stock Rs. 6,40,000.

(ii) Wages outstanding Rs. 24,000.

(iii) Interest rate of Bank Loan is 18% p.a.

(iv) Bad Debts Rs. 6,000.

(v) Provision for Doubtful debts to be 5%.

(vi) Rent is paid for 11months.

(vii) Insurance premium is paid per annum, ended 31st May, 2024.

(viii) Loan from the bank was taken on 1st October, 2023.

(ix) Provide Depreciation on Machinery @ 10% and on Furniture @ 5%.

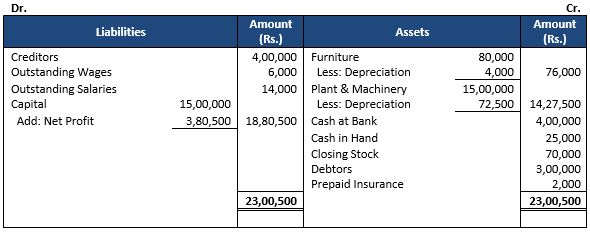

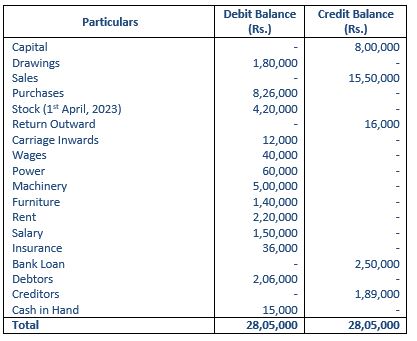

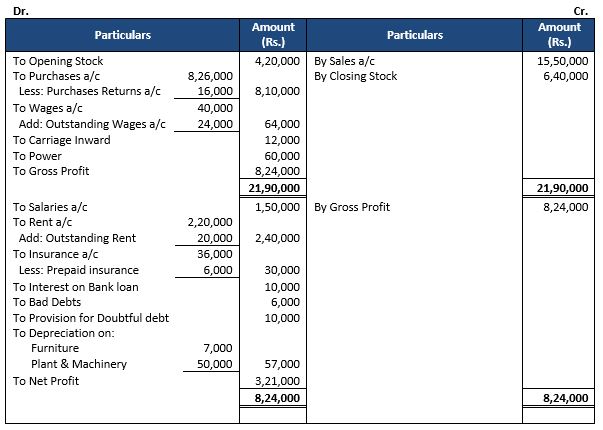

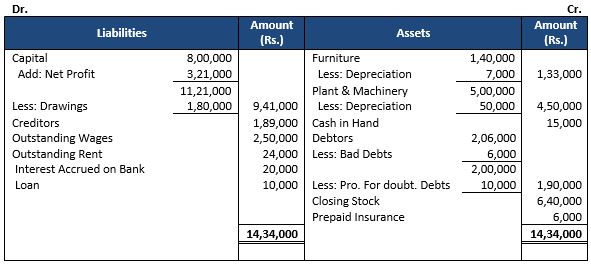

Answer 5:

Trading and Profit & Loss Account for the year ended March 31, 2024

Balance Sheet as on March 31, 2024

Question 6: Prepare Trading and Profit & Loss Account for the year ended 31st March, 2024 and Balance Sheet as at that date from the following balance taken from the books of Vijay on 31st March, 2024 after giving effect to the following adjustments:

(i) Stock as on 31st March, 2024 was valued at Rs. 2,30,000.

(ii) Write off Further Rs. 1,800 as Bad Debts and maintain the Provision for Doubtful Debts at 5%.

(iii) Depreciate Machinery at 10%.

(iv) Provide Rs. 7,000 as outstanding interest as loan.

Answer 6:

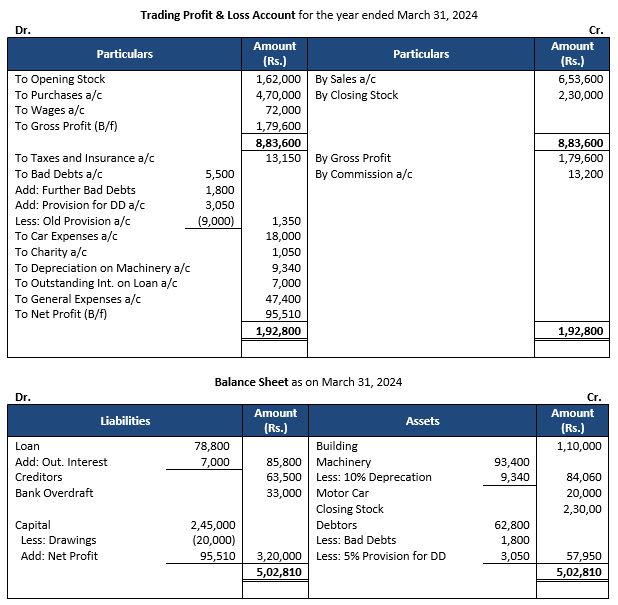

Question 7: Following are the balances extracted from the books of Narain on 31st March, 2024:

Additional Information:

(i) Closing Stock as on 31st March, 2024 was Rs. 2,00,600, whereas its Net Realisable Value (Market Value) was Rs. 2,05,000.

(ii) Depreciate: Business Premises by Rs.3,000 and Furniture and Fittings by Rs. 2,500.

(iii) Make a provision of 5% on debtors for doubtful debts.

(iv) Carry forward Rs. 2,000 for unexpired insurance.

(v) Outstanding salary was Rs. 15,000.

Prepare Trading and Profit and Loss Account for the year and Balance Sheet as at that date.

Answer 7:

Question 8: Following balances are taken from the books of Ramesh. Prepare Trading and Profit & Loss Account for the year ended 31st March, 2024 and Balance Sheet as on that date:

Adjustments:

(i) Closing Stock Rs. 7,50,000.

(ii) Depreciate Machinery by 10% and Furniture by 20%.

(iii) Wages Rs. 50,000 and salaries Rs. 20,000 are outstanding.

(iv) Write off Rs. 50,000 as further Bad Debts and create 5% Provision for Doubtful Debts. Also, create a reserve for discount on Debtors @ 2%.

(v) Investments were made on 1st July, 2023 and no interest has been received so far.

Answer 8:

Trading and Profit & Loss Account for the year ended March 31, 2024

Balance Sheet as on March 31, 2024

Question 9: From the following information of Menal, prepare his Final Accounts for the year ended 31st March, 2024:

Additional Information:

(i) Closing Stock on 31st March, 2024 was Rs. 21,000.

(ii) Rent of Rs. 1,200 has been received in advance.

(iii) Outstanding liability for Miscellaneous expenses Rs. 12,000.

(iv) Commission earned during the year but not received was Rs. 2,100.

(v) Goods costing Rs. 2,000 were taken by the proprietor for his personal use but entry was not passed in the books of account.

Answer 9:

Point of Knowledge:-

Calculation of Outstanding Interest on Loan

Interest on loan (30,000 × 12%) 3,600

Less: Interest (2,800)

Interest Outstanding on Loan 800

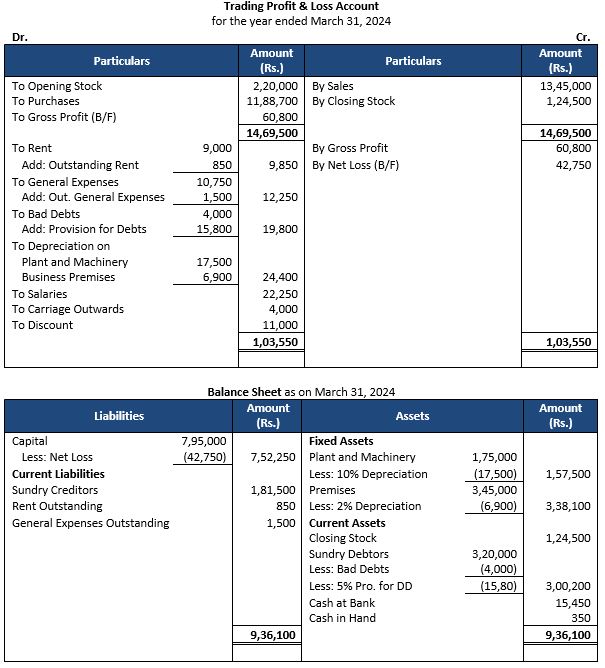

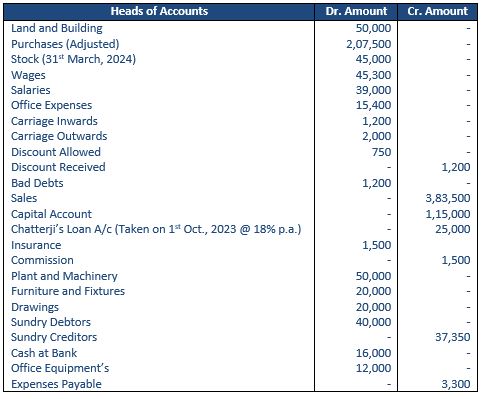

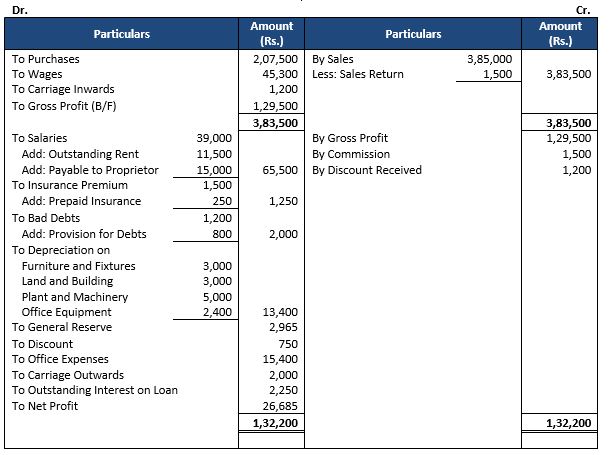

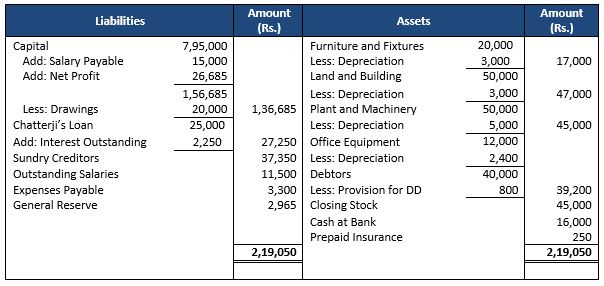

Question 10: From the following Trial Balance and other information, prepare Trading and Profit and Loss Account for the year ended 31st March, 2024 and Balance Sheet as at that date:

Additional Information:

(i) Stock on 31st March, 2024 was Rs.1,24,500.

(ii) Rent was unpaid to the extent of Rs.850 and Rs.1,500 were outstanding for General Expenses.

(iii) Rs.4,000 are to be written off as bad debts out of the above debtors and 5% is to be provided for doubtful debts. (iv) Depreciate Plant and Machinery by 10% and Premises by 2%.

(v) Manager is entitled to a commission of 5% on net profit after charging his commission.

(vi) A fire broke out on 1st April, 2024 destroying goods costing Rs. 20,000.

Answer 10:

Question 11. From the following Trial balance of Shubho, Prepare Trading and Profit and Loss Accounts for the year ended 31st March, 2024 and Balance Sheet as at that date:

The following adjustments be made:

(i) Depreciate Land and Building @ 6%, Plant and Machinery @ 10%, Office equipment’s @ 20% and Furniture and Fixtures @ 15%.

(ii) Create Provision for Doubtful Debts at 2% on Sundry Debtors.

(iii) Insurance includes Rs. 250 Insurance Premium paid in advance.

(iv) Provide salary to Shubho Rs. 15,000 p.a.

(v) Outstanding Salaries Rs. 11,500.

(vi) 10% of the final profit is to be transferred to General Reserve.

Answer 11:

Trading Profit & Loss Account

for the year ended March 31, 2024

Balance Sheet as on March 31, 2024

Question 12. Prepare Trading and Profit and Loss Account for the year ending on 31st March, 2024 and Balance Sheet as on that date from the following balances of Trail Balance:

Adjustments:

1.) The value of stock on 31st March, 2024 Rs. 40,000.

2.) Provision for Doubtful Debts is to be maintained at 5% on Sundry Debtors.

3.) Change depreciation on both Furniture and Machinery @ 10% p.a.

4.) Machinery costing Rs. 20,000 was purchased on 1st January, 2024.

5.) Allow interest on capital @5% p.a.

6.) A fire occurred on 20th March, 2024 and stock of the value of Rs. 7,000 was destroyed. It was fully insured and the insurance company admitted the claim in full.

7.) 10% of net profit to be carried to General Reserve.

Answer 12:

Question 13. Following is the Trail Balance of M/s Indramani as on 31st March, 2024:

Prepare Trading and Profit and Loss Account for the year ending 31st March, 2021 and Balance Sheet as on that date after making the following adjustments:-

(i) Value of Closing Stock Rs. 6,100.

(ii) Depreciate Machinery @ 10% p.a.

(iii) Create provision for doubtful debts at 5% on debtors.

(iv) Commission payable to manager at 10% on net profit.

(v) On 25th March, 2021, goods costing Rs. 1500 and furniture costing Rs. 3000 where destroyed by fire, insurance company has accepted claims of Rs. 1000 for goods and Rs. 2000 for furniture.

Answer 13:

In the Books of ________

Trading & Profit and Loss Account for the year ended March 31, 2024

Question 14. On 31st March, 2024 the following Trail Balance was prepared from the books of Manpreet:

Prepare Trading and Profit and Loss Account for the year ended 31st March, 2024 and also the Balance Sheet as at that date after making the following adjustments:

(i) Closing Stock at cost was Rs. 35,000 whereas its net realizable value (market value) was Rs. 30,000.

(ii) A new machine was purchased for Rs. 3,000 on 1st April, 2020 but it was not paid for and no entry was passed in the books.

(iii) Wages included Rs. 500 paid for the installation of machinery.

(iv) Provision for Doubtful Debts was raised to Rs. 1,400 and further bad debts of Rs. 300 were written off.

(v) Fire Broke out on 20th March, 2024 and destroyed stock to the value of Rs. 8,000. The insurance company admitted claim for loss of stock of Rs. 5,000 only and the amount was paid in 15th April, 2024.

(vi) Outstanding wages were Rs. 700 while outstanding salaries were Rs. 500.

(vii) Prepaid insurance was Rs. 250 and prepaid advertisement Rs. 500.

(viii) Machinery was depreciated by 10% and furniture by 15%.

Answer 14:

In the Books of ________

Trading & Profit and Loss Account for the year ended March 31, 2024

Question 15: Prepare Trading and Profit and Loss Account for the year ended 31st March, 2019 and Balance Sheet as at that date from the following Trial Balance: (Old Question)

Adjustments:

(i) Taxes Rs. 3,000 are outstanding but Insurance Rs.500 is prepaid.

(ii) Commission Rs. 1,000 received in advance for the next year.

(iii) Interest Rs. 2,100 is to be received on Deposits and Interest on Bank Loan Rs. 3,000 is to be paid.

(iv) Provision for Doubtful Debts to be maintained at Rs. 10,000.

(v) Depreciate Furniture by 10%.

(vi) Stock on 31st March, 2019 is Rs. 45,000.

(vii) A fire occurred on 1st April, 2019 destroying goods costing Rs. 10,000. These goods were purchased paying CGST and SGST @ 6% each.

Answer 15:

Question 15. From the following Trial Balance and information, prepare Trading and Profit & Loss Account of Gurman for the year ended 31st March, 2024 and Balance Sheet as on that date

Additional Information:

(i) Value of Closing Stock on 31st March, 2024 at cost was Rs. 27,300 and its net realisable value (market value) was Rs. 30,000.

(ii) Fire occurred on 23rd March, 2024 and goods costing Rs. 10,000 were destroyed. Insurance company accepted claim of Rs. 6,000 only and paid the claim money on 10th April, 2024.

(iii) Bad Debts amounting to Rs. 400 are to be written off. Provision for Doubtful Debts is to be maintained at 5% and Provision for Discount on Debtors at 2%.

(iv) Received goods costing Rs. 6,000 on 27th March, 2024 but the purchases were not recorded.

(v) Gurman took goods of Rs. 2,000 for his personal use but was not recorded

(vi) Charge depreciation @ 2% on Loan and Building @ 20% on Plant and Machinery and @ 5% on Furniture.

Answer 15

Trading and Profit & Loss Account

for the year ended March 31, 2024

Balance Sheet as on March 31, 2024

Question 16. The following is the Trial Balance of Ashok as on 31st March, 2024:

Prepare Trading and Profit and Loss Account for the year ended 31st March, 2024 and Balance Sheet as on that date after making the following adjustments:

(i) Salaries for the month of March, 2024 of Rs. 1,000 were unpaid which are to be provided. Balance in the account included Rs. 800 paid in advance.

(ii) Insurance is prepaid to the extent of Rs. 2,000.

(iii) Depreciate Furniture by 10% on original cost and Building by 5%.

(iv) Stock of Rs. 1,500 was taken by Ashok for his personal use.

(v) Make a Provision for Doubtful Debts equal to 10% of Sundry Debtors.

Answer 16:

In the Books of ________

Trading & Profit and Loss Account for the year ended March 31, 2024

Point of Knowledge:-

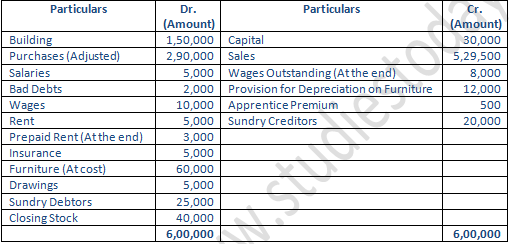

1. Purchases (Adjusted) means opening stock and closing stock are already adjusted in purchases and as such these two items are not shown in Trading Account. As closing stock appears in Trail Balance, it is shown in the assets side of Balance Sheet Alone.

2. As prepaid rent and wages outstanding exist in the trial balance, adjustment entry for these items are already passed. Therefore, these items will be shown in Balance Sheet only.

Question 17. From the following Trial Balance and additional information of Bharat, a proprietor, prepare Trading and Profit and Loss Account for the year ending 31st March, 2024 and the Balance Sheet as at that date:

Additional Information:-

(i) Salaries outstanding for the month of March, 2024 is Rs. 7,000.

(ii) Prepaid Insurance is Rs. 900.

(iii) Depreciate Machinery @ 15% p.a.

(iv) Value of Closing Stock is Rs. 1,11,000.

(v) Bharat took goods of Rs. 2,000 for personal use which was not recorded (Ignore GST).

Answer 17:

In the Books of Bharat

Trading & Profit and Loss Account for the year ended March 31, 2024

Question 18. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2024 and Balance Sheet as at that date from the following Trail Balance:

Additional Information:-

(i) Taxes Rs. 3,000 are outstanding but Insurance Rs. 500 is prepaid.

(ii) Commission Rs. 1,000 received in advance for the year.

(iii) Interest Rs. 2,100 is to Received on Deposits and Interest on Bank Loan Rs. 3,000 is to be paid.

(iv) Provision for Doubtful Debts to be maintained at Rs. 10,000.

(v) Depreciate Furniture by 10%.

(vi) The cost of Closing Stock as on 31st March, 2021 was Rs. 45,000 but its Net Realizable Value (Market Value) was Rs. 50,000.

(vii) A fire occurred on 1st April, 2021 destroying goods costing Rs. 10,000. The Stock was fully insured (Ignore GST).

Answer 18:

In the Books of ________

Trading & Profit and Loss Account for the year ended March 31, 2024

Question 19. From the following Trial Balance of Ramesh, prepare Trading, Profit and Loss Account for the year ending 31st March, 2024 and a Balance Sheet as on that date:

Adjustments:

(i) Cost of stock on 31st March, 2024 was Rs. 37,000. However, its market value was Rs. 35,000.

(ii) Wages outstanding were Rs. 6,000 and salaries outstanding were Rs.5,000 on 31st March, 2024.

(iii) Depreciate Land and Building @ 21/2%, Plant and Machinery @ 10% p.a. and Furniture @ 15% p.a.

(iv) Purchase includes purchase of machinery for Rs.10,000 on 1st October, 2023.

(v) Debtors include bad debts of Rs.2,000. Maintain a provision for doubtful debts @ 10% on Debtors.

Answer 19:

Trading Profit & Loss Account for the year ended March 31, 2024

Balance Sheetas on March 31, 2024