Access free TS Grewal Accountancy Class 11 Solution Chapter 16 Accounting for Bills of Exchange 2026 below. Students can now access free TS Grewal Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 16 Accounting for Bills of Exchange TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 16 Accounting for Bills of Exchange Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 16 Accounting for Bills of Exchange TS Grewal Class 11 Solved Exercises

Question.1. Define bill of exchange. What are the features of a Bill of Exchange?

Answer .1 Definition of Bill of Exchange: As per Section 5 of the Negotiable Instruments Act, 1881, "A Bill of Exchange is an instrument in writing containing an unconditional order signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument."

Features or Characteristics of Bill of Exchange are:

- Bill of exchange is a written order.

- Bill of exchange is drawn and signed by the maker or drawer of the bill.

- Bill of exchange is an unconditional order to a person or drawee, to pay the specified amount. The drawee must accept it to make it a valuable document.

- The specified amount is payable to the person named in the bill or to his order or to the bearer.

- It specifies the date by which the amount should be paid.

- It is accepted by the drawee.

Question.2. Define Bill of Exchange. What are the parties to a Bill of Exchange?

Answer .2 Definition of Bill of Exchange: As per Section 5 of the Negotiable Instruments Act, 1881, "A Bill of Exchange is an instrument in writing containing an unconditional order signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument."

Parties to a Bill of Exchange

There are three parties in Bill of Exchange:

- Drawer: Drawer is the person who makes or writes the Bill of Exchange. He is a person who granted credit to the person on whom the Bill of Exchange is drawn.

- Drawee: Drawee is the person on whom the Bill of Exchange is drawn, for his acceptance. He is a person to whom credit has been granted by the Drawer of the Bill of Exchange.

- Payee: Payee is the person named in the Bill of Exchange to whom the amount is to be paid. Payee may be the Drawer himself or a third person.

Question.3. Give a definition of Bill of Exchange and its two characteristics.

Answer .3 Definition of Bill of Exchange: As per Section 5 of the Negotiable Instruments Act, 1881, "A Bill of Exchange is an instrument in writing containing an unconditional order signed by the maker, directing a certain person to pay a certain sum of money only to , or to the order of, a certain person or to the bearer of the instrument."

Two Features or Characteristics of Bill of Exchange are:

1.) Bill of Exchange is a written order.

2.) Bill of Exchange is drawn and signed by the maker or drawer of the bill.

Question.4. Define a Promissory Note. What are the features of Promissory Note?

Answer .4 Definition of Promissory Note: Definition of Promissory Note as per Section 4 of the Negotiable Instruments Act, 1881 is," A Promissory Note is an instrument is writing (not being a bank note or a currency note) containing an unconditional undertaking signed by the maker to pay a certain sum of money only to or to the order of a certain person or to the bearer of the instrument."

Features of a Promissory Note:

The following are the features or characteristics of a Promissory Note:

- Promissory Note is an unconditional written undertaking to pay the specified amount.

- Promissory Note is drawn and signed by the maker.

- It specifies the name of the payee or the person to whom payment is to be made.

- Specified amount is payable to the specified person or to his order or to the bearer.

- Date of payment is specified.

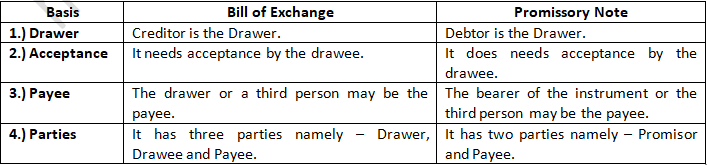

Question.5. Distinguish between Bills of Exchange and Promissory Note on the basis of:

(i) Drawer

(ii) Acceptance

(iii) Payee

(iv) Number of Parties.

Answer.5

Question.5. Who are the parties to a Promissory Note? (Old Question)

Answer .5 Parties to a Promissory Note:

A Promissory Note has two parties as given below:

- Maker: Maker is the person who makes the promise to pay the amount. It is a person who has availed the credit.

- Payee: Payee is the person to whom payment is to be made. It is the person who has given the credit.

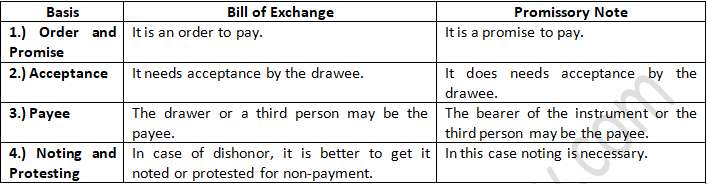

Question.6. Distinguish between Bills of Exchange and Promissory Note on the following basis.

(i) Order or Promise and Parties

(ii) Acceptance

(iii) Payee

(iv) Noting.

Answer.6

Question.7. Explain any three of the following:

(i) Retiring of Bills of Exchange

(ii) Holder in due course

(iii) Bills sent to bank for collection

(iv) Noting charges.

Answer.7

(i) Retiring of Bills of Exchange: When the Drawee pays the bill before its due date, it is called Retirement of a Bill. The holders allow him a rebate of certain amount calculated at a certain rate per cent per annum, from the date of retirement to the date of maturity.

(ii) Holder in due course: Holder in due course of a Bill of Exchange or Promissory Note or Cheque or Negotiable Instrument, is a person entitled in his own name to the possession thereof and to receive or recover the amount due thereon from the parties to it.

(iii) Bills sent to bank for collection: A bill received may be retained till the date of maturity. But, it may be deposited with the bank, with instructions that the bill be retained till maturity and realised on its due date. It is known as Bill Sent for Collection. It means bank will retain the bill in safe custody and present it for payment on the due date. The bank will credit the amount of the customer on realisation of the amount. If the bill is sent to the bank with such instructions, is known as bill for collection. The balance in the Bills Sent for Collection Account is shown in the Balance Sheet as an asset.

When the bill is sent to the bank for collection the entry will be:

Bills Sent for Collection A/c Dr.

To Bills Receivable A/c

(Being the acceptance sent to the bank for collection)

When the bill is sent to the bank for collection is collected by bank:

Bank A/c Dr.

To Bills Sent for Collection A/c

(Being the acceptance sent to the bank for collection collected)

(iv) Noting Charges: Noting Charges is the fee paid to the Notary Public for noting and protesting the Bills of Exchange of its dishonor.

Question.8 Write a note on the following:

(i) Dishonor of Bill (ii) Endorsement of Bill.

Answer.8

(i) Dishonor of a Bill: Dishonor means that the bill is not paid by the drawee on its due date. It arises when the acceptor is unable to pay the amount of the bill, i.e., Bill of Exchange or Promissory Note or Cheque due to insolvency or any other reason.

(ii) Endorsement of Bill: Endorsement means transfer of Bill of Exchange or Promissory Note to another person. The person receiving the Bill of Exchange or Promissory Note becomes authorised to receive the payment. The person who transfers the Bill of Exchange or Promissory Note in favour of other person is called endorser. The person to whom the Bill of Exchange or Promissory Note is endorsed is called endorsee.

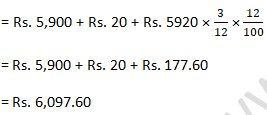

Question.9. A Bill of Exchange drawn on 1st July, 2018 for Rs. 5,900 for 3 months was dishonored on due date and a sum of Rs. 20 was incurred as nothing charges. The bill was renewed for another 3 months with 12% interest per annum. Find out the amount of the renewed bill.

Answer.9

Amount of the renewed bill = Bill Value + Noting Charges + Interest for the Dishonored Period

Question.10. Ashok drew on Rakesh three Bills of Exchange respectively on 29th, 30th and 31st January, 2019. The term in each case is 1 month. What will be the due date in each case?

Answer .10 The due date in each of the three bills = 3rd March of the same year.

Question.11. A Bill of Exchange was drawn on 12th July, 2018. Its term was 1 month. What will be the date of maturity?

Answer .11 If the Bill of Exchange was drawn on 12th July, 2018 its term 1 month. The date of maturity will be 14th August as 15th August is a national holiday.

Question.11. A Bill of Exchange for Rs 3,000 drawn on 1st June, 2018 and payable after 3 months was discounted with a bank at 10% p.a. but was dishonored on due date and Rs. 8 were paid as noting charges. What was the amount claimed by the bank from the Drawer? (Old Question)

Answer.11 Amount claimed by the bank from the Drawer = Bill Value + Noting Charges

= Rs. 3,000 + Rs. 8

= Rs. 3,008

Practical Problems...........:->

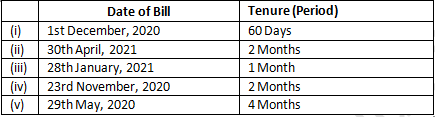

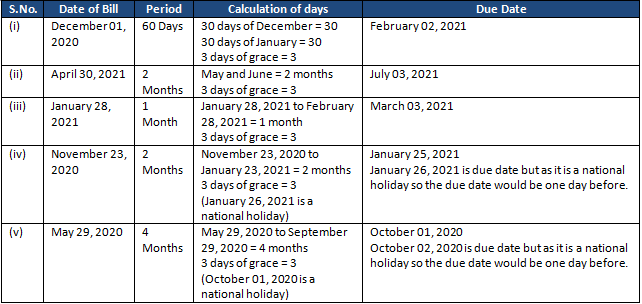

Question 1: Calculate the due dates of the bills in the following cases:

Answer 1:

CALCULATION OF DUE DATES OF THE BILLS

Points for knowledge:

- Although in point (iv) and (v) January 26, 2021 and October 02, 2020 are national holidays so the due date in both the cases would be one day before that holiday.

- In the process of calculation of due dates of bill, 3 days of grace would be considered.

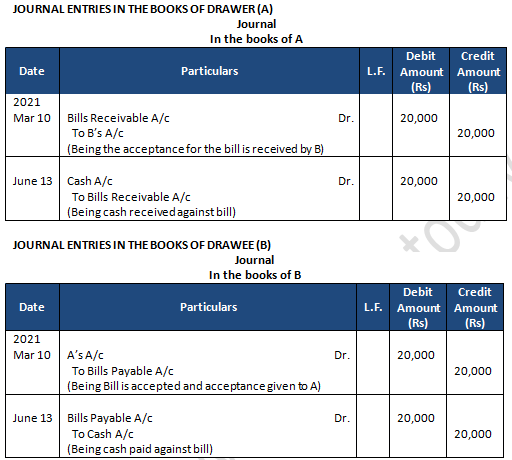

Question 2: On 10th March, 2021, A draws on B a bill at 3 months for Rs 20,000 which B accepts immediately and returns to A. The bill is honoured due date. Pass necessary Journal entries in the books of both the parties.

Answer 2:

JOURNAL ENTRIES IN THE BOOKS OF DRAWER (A)

Points for knowledge:

- Drawer is the person who makes or writes the bill of exchange. He is the person who has granted credit to the person on whom the bill of exchange is drawn.

- Drawee is the person on whom the bill of exchange is drawn for his acceptance. He is the person to whom credit has been granted by the drawer of the bill of exchange.

- In the above question, a being the person who draws the bill will be treated as drawer and B will be considered as drawee.

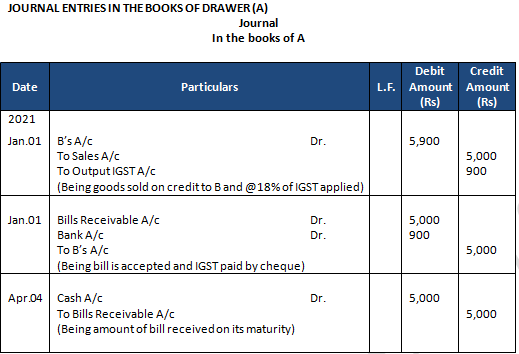

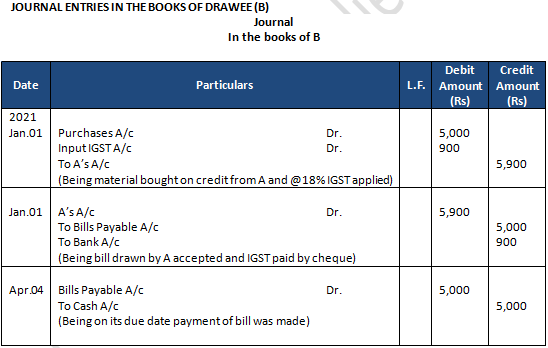

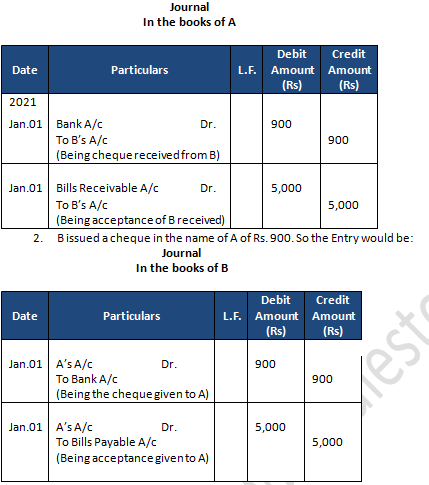

Question 3: On 1st January, 2021, A sold goods to B for Rs 5,000 plus IGST @ 18% A received Rs. 900 by cheque from B and drew on him a bill for the balance amount payable 3 months after date. The bill was duly accepted by B. A retained the bill till due date. On due date, the bill was paid. Pass Journal entries in the books of A and B. Also, show necessary accounts in the books of both the parties.

Answer 3:

Points for knowledge:

- A received a cheque of Rs 900 from B. So the Entry would be:

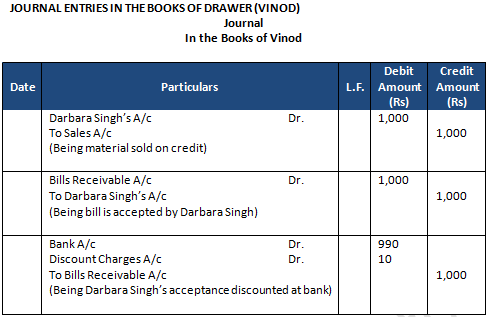

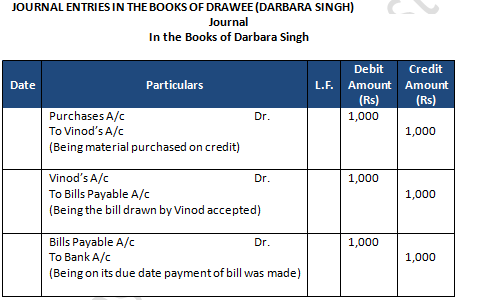

Question 4: Vinod sold goods to Darbara Singh for Rs 1,000. He drew on the latter a bill for the amount payable 3 months after date. He discounted the bill with his bankers for Rs 990. On maturity, the bill is duly met. Make the Journal entries in the books of Vinod and Darbara Singh.

Answer 4:

Points for knowledge:

- The bills of exchange can be discounted at the bank so that the enterprise allowing the creditor can receive the amount immediately without the debtor having to pay before time.

- Computation of amount of discount charges:

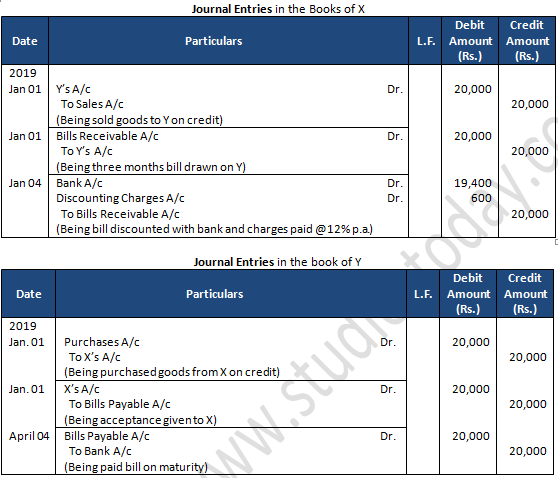

Question 5: On 1st January, 2021, X sold goods of Rs. 20,000 to Y and drew a bill on Y at three months for the amount. Y accepted the bill. The bill is met on maturity. Pass the necessary Journal entries in the books of X and Y, if X discounted the bill @ 12% p.a. from bank on 4th January.

Answer 5:

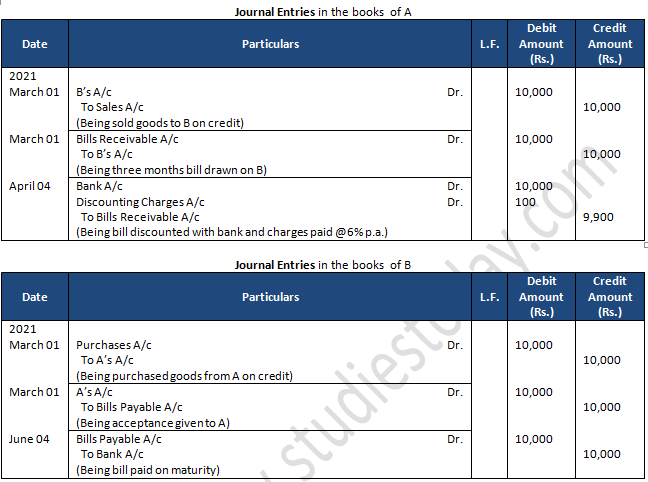

Question 6: A sells goods of Rs. 10,000 on 1st March, 2021 to B on credit. B accepts a bill on the same date for the amount payable three months after date. A discounts the bill at 6% p.a. from bank on 4th April. On maturity, the bill is met by B. Pass the necessary Journal entries in the books of both the parties.

Answer 6:

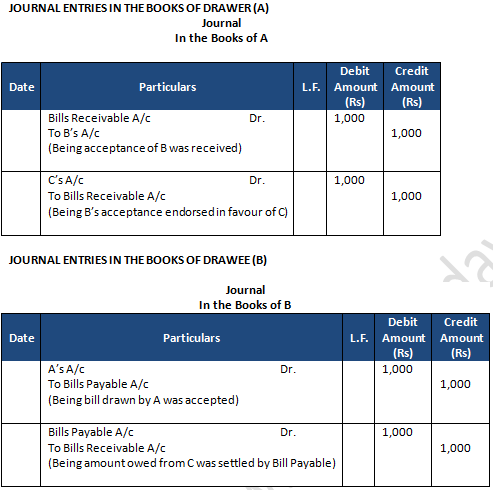

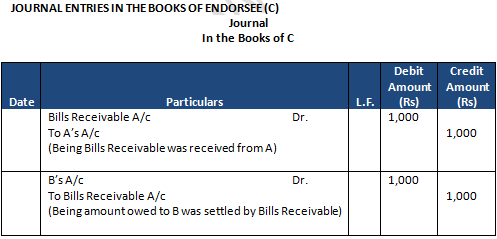

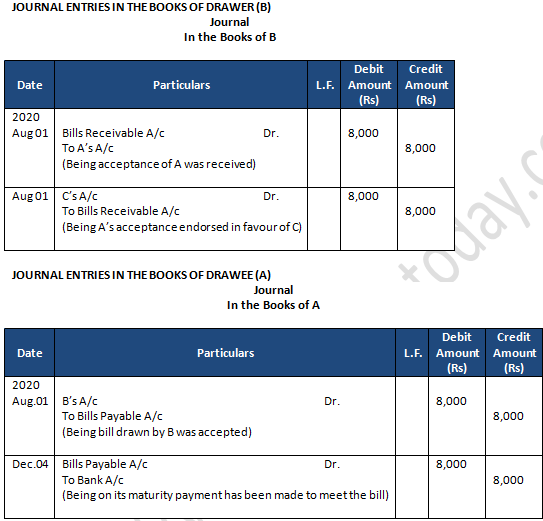

Question 7: A drew a bill of Rs 1,000 on B for 3 months which was duly accepted by the latter. A endorsed the bill to C in full payment of his own acceptance to C for a like amount. C endorsed the bill to B.

Answer 7:

Points for knowledge:

- The bills of exchange can be endorsed to other parties, thus they serve the almost same purpose as cash.

- The recovery of the debt is possible without having to remind the debtor.

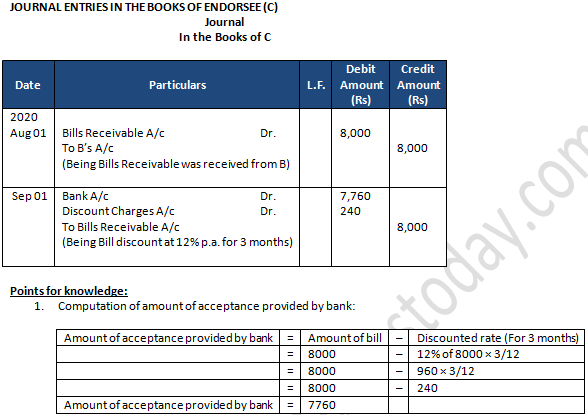

Question 8: A owed B Rs 8,000. He gave a bill for the same on 1st August, 2020 payable after 4 months at the Bank of India. Chandni Chowk, Delhi. Immediately after receiving the bill, B endorsed it to C in payment of his debt. On 1st September, C discounted the bill at 12% p.a. The bill is met on due date. Pass the necessary Journal entries in the books of A, B and C.

Answer 8:

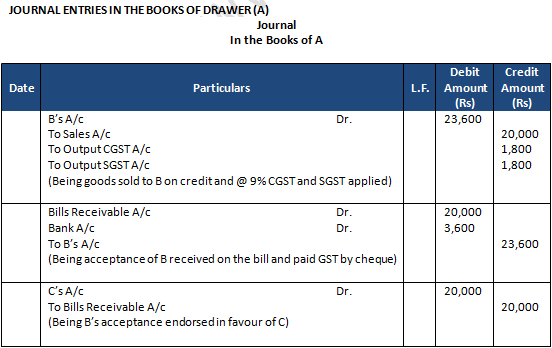

Question 9: A sold goods to B for Rs 20,000 plus CGST and SGST @ 9% each on credit 3 months. B paid A Rs 3,600 by cheque and accepted a draft for the balance amount. The draft was endorsed in favour of C, who got the payment on maturity.

Give Journal entries in the books of A.

Answer 9:

Points for knowledge:

- B has paid Rs. 3,600 to A through cheque at the time of purchasing goods. So bill will be drawn for Rs. 20,000 only and not for the whole amount of Rs. 23,600.

- Meanwhile, A endorsed the bill in favour of C so at the end of said 3 months (on the date of maturity) the amount will be received by C.

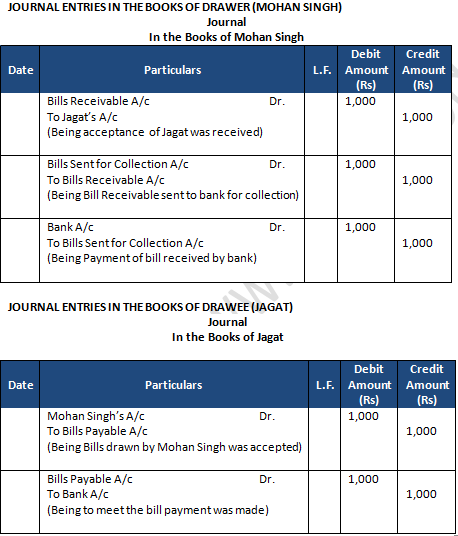

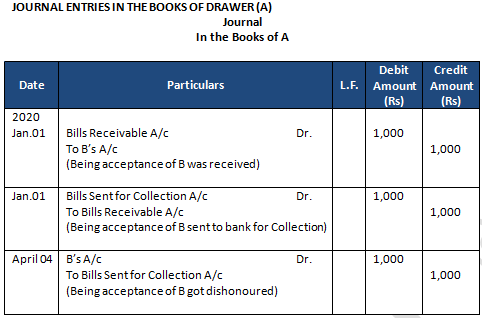

Question 10: Mohan Singh draws a bill on Jagat for Rs 1,000 payable 2 months after date. Immediately after its acceptance, Mohan Singh sends the bill to his bank for collection. On due date, bank gets the payment. Make the entries in the books of all the parties.

Answer 10:

Points for knowledge:

Mohan Singh draws a bill on Jagat for Rs 1,000 and Jagat gives his acceptance on the same. After getting acceptance, Mohan Singh sends the bill to his bank for collection. On the date of the maturity of the bill payment of bill received by bank.

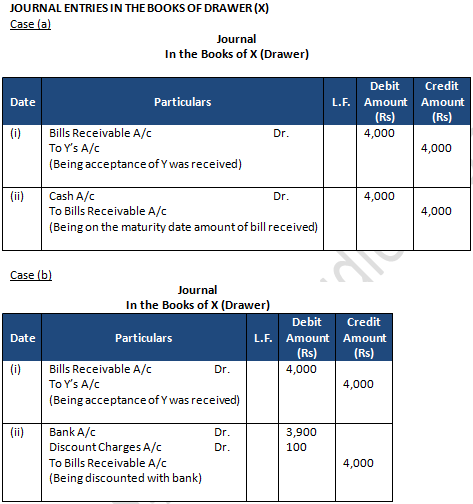

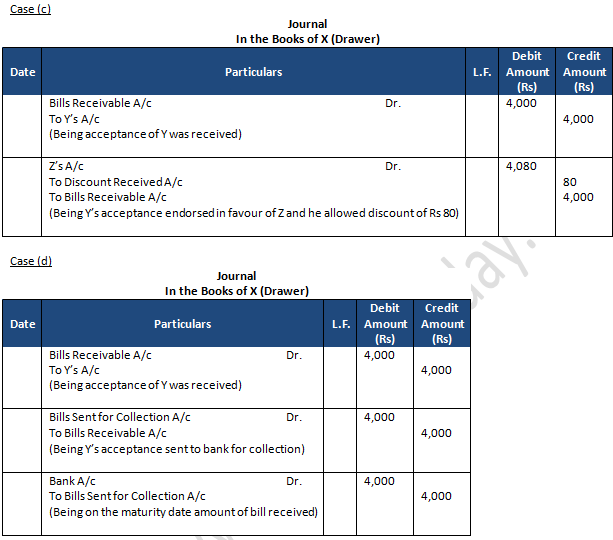

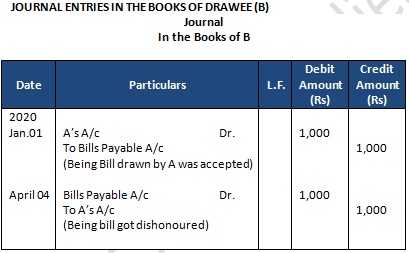

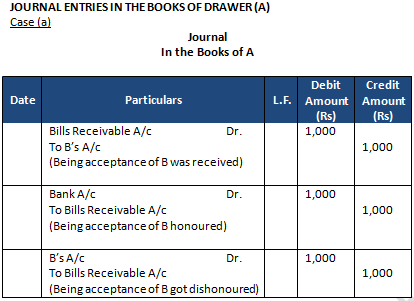

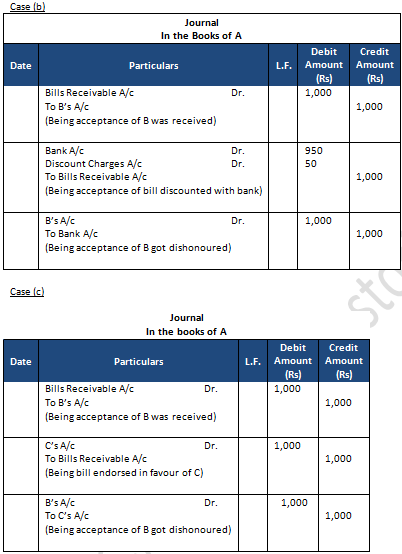

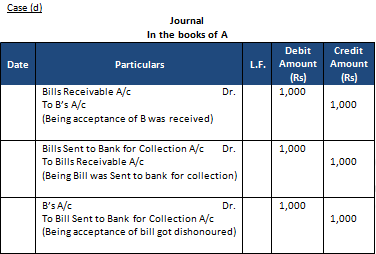

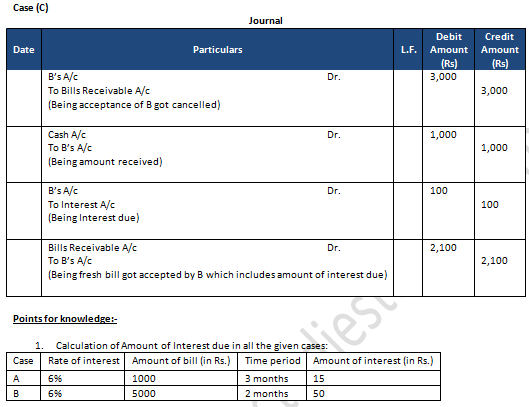

Question 11: X draws on Y a bill for Rs 4,000 which was duly accepted by Y. Y meets the bill on its due date. Show what entries would be passed in the books of X under each of the following circumstances:

(a) If X retains the bill till due date.

(b) If X discounts the same with his banker paying Rs 100 for discount.

(c) If X endorses the same to his creditor Z in full settlement of his debt of Rs 4,080.

(d) If X sends the bill to his banker for collection the next day.

Answer 11:

Points for knowledge:

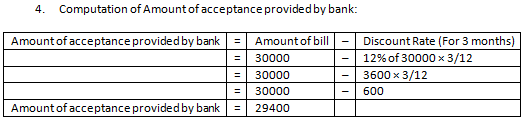

- In Case B, Computation of amount of acceptance provided by bank:

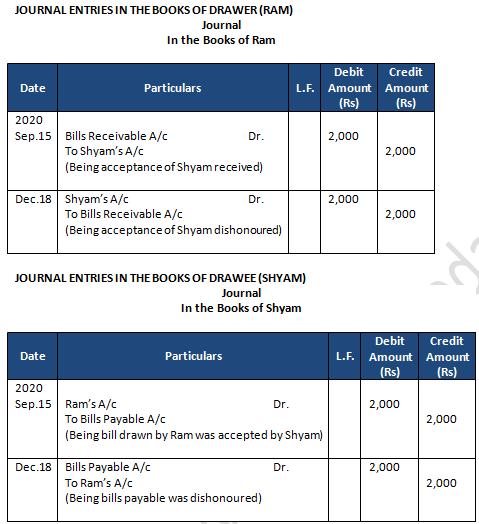

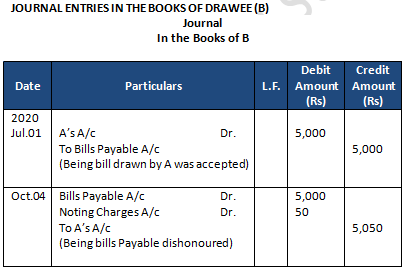

Question 12: Ram draws a bill for Rs 2,000 on Shyam on 15th September, 2020 for 3 months. On maturity, Shyam failed to honour the bill.

Pass the necessary Journal entries in the books of Ram and Shyam.

Answer 12:

Points for knowledge:

Ram draws a bill on Shyam, but on the maturity date the bill got dishonoured so in case on non-payment of bill, reverse Journal entry will be passed in the books of Ram and Shyam both.

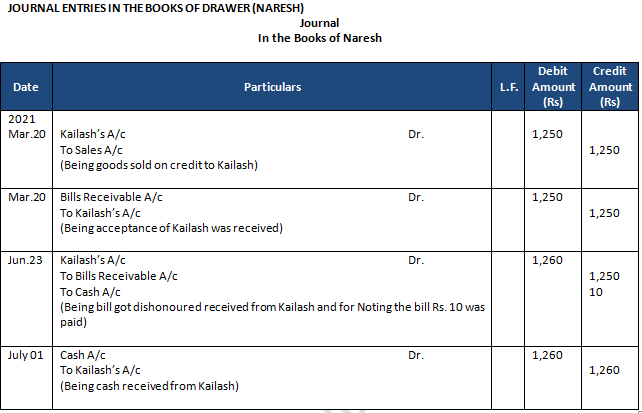

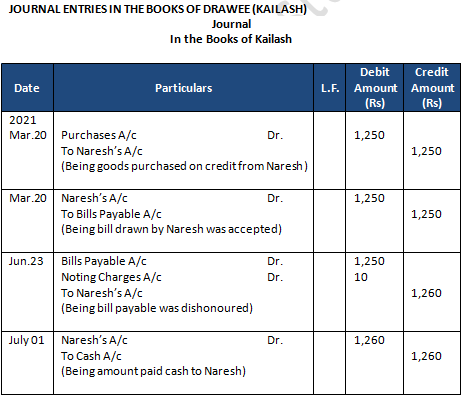

Question 13: On 20th March, 2021, Naresh sold goods to Kailash to the value of Rs 1,250, taking a bill at 3 months for the amount. On maturity, the bill was dishonoured. Naresh paid Rs 10 as noting charges. On 1st July, Kailash cleared his account by paying Rs 1,260.

Make the entries in the books of both the parties to record the above transactions.

Answer 13:

Points for knowledge:

- The bill drawn by Naresh to Kailash for Rs.1250 got dishonoured and Naresh has to pay Rs. 10 as noting charges to the bank. Now at the time of receiving the amount due from Kailash, Naresh will also charge the amount which is being paid to bank.

Total amount due on Kailash will be = Amount of bill + Noting charges

= Rs. 1250 + Rs. 10

= Rs. 1260

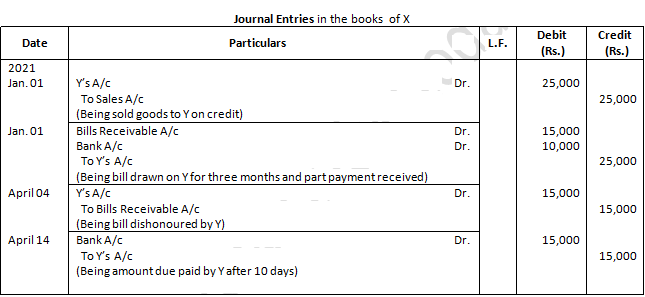

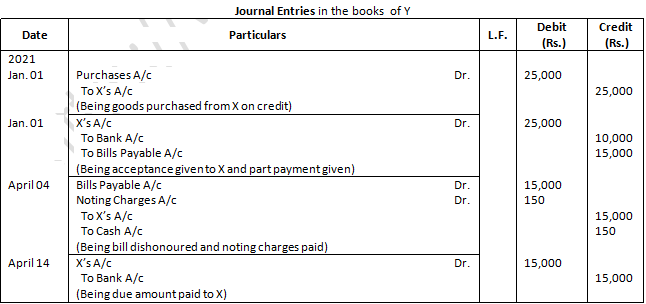

Question 14: On 1st January, 2021, X sold goods to Y for Rs. 25,000 and immediately received from Y Rs. 10,000 by cheque and drew a bill on Y at three months for the balance amount. Bill is accepted by Y. Bill was dishonored on the due date and Y paid Rs. 150 as noting charges. Ten days later, Y pays the due amount to X. Pass the Journal entries in the books of both the parties.

Answer 14:

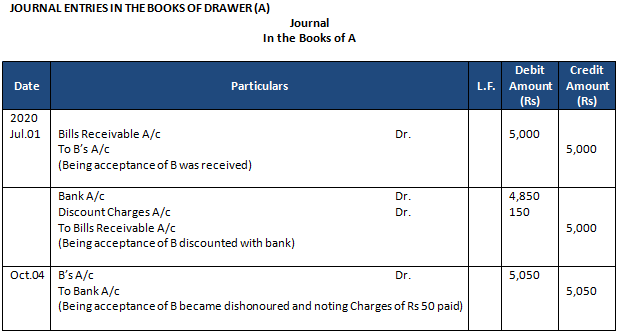

Question 15: On 1st July, 2020, A drew a bill for Rs 5,000 on B payable after 3 months. A discounted it with the Bank for Rs 4,850. On maturity B failed to pay the amount of his acceptance and the bank had to pay Rs 50 as noting charges. Draw up the necessary Journal entries in the books of A and B.

Answer 15:

Points for knowledge:

- The bill had drawn by A to B for Rs.5000 and A discounted the bill with the banker for Rs. 4850. After expiration of 3 months bill got dishonoured and Bank has to pay Rs. 50 as noting charges. Now at the time of receiving the amount due from B, amount of bill as well as noting charges will be received.

Total amount due on B will be = Amount of bill + Noting charges

= Rs. 5000 + Rs. 50

= Rs. 5050

2. Computation of Amount of Discount Charges:

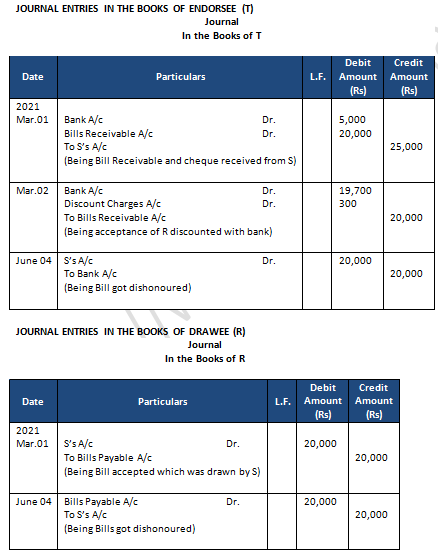

Question 16: On 1st March, 2021, R accepted a Bill of Exchange of Rs 20,000 from S payable 3 months after date in full settlement of his dues. On the same day S endorsed the Bill of Exchanges to T together with a cheque for Rs 5,000 in settlement of his debt to the latter. On 2nd March, 2021, T discounted the Bill of Exchange @ 6% p.a. with his bankers. On maturity the Bill of Exchange was dishonoured.

Journalise the transactions in the books of R and T.

Answer 16:

Points for knowledge:-

- Computation of Amount of acceptance provided by bank:

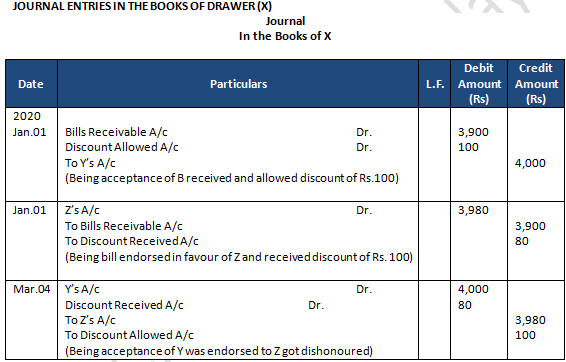

Question 17: Y owes X Rs 4,000. On 1st January, 2020, Y accepts a 3 months bill for Rs 3,900 in satisfaction of his full claim. On the same date, it was endorsed by X to Z in satisfaction of his claim of Rs 3,980. The bill is dishonoured on the due date. Give the Journal entries in the books of X.

Answer 17:

Points for knowledge:-

- Y owes X a Sum of Rs. 4000. X issues a bill of exchange and Y gives his consent on that and agrees to pay a sum of Rs. 3900 in full settlement, discount allowed of Rs. 100.

- X endorsed the same bill to Z in full settlement of his claim of Rs. 3980 and received discount of Rs. 80 from him.

- Acceptance of Y which was endorsed to Z regarded as dishonoured and now in the books of X all the previous entries will be reversed.

Question 18: On 1st January, 2020, A draws a bill on B for Rs 1,000 payable after 3 months. Immediately after its acceptance, A sends the bill to his bank for collection. On the due date, the bill was dishonoured. Record the transactions in the Journals of A and B.

Answer 18:

Points for knowledge:-

- As in the above problem, the bill got dishonoured by the bank now the journal entries would be reversed in the books of the both the parties.

Question 19: A bill for Rs 1,000 is drawn by A on B and accepted by the latter payable at the New Bank of India. Show what entries should be passed in the books of A under each of the following circumstances:

(a) If A retained the bill till the due date and then realized it on maturity.

(b) If A discounted it with his bankers for Rs 950.

(c) If A endorsed it to his creditor C in full settlement of his debt.

(d) If A sent it to his bankers for collection.

Also, give the necessary entries in each of the cases if the bill is dishonoured.

Answer 19:

Points for knowledge:-

- In case A, if the Bill got honoured with the bank then receivable A/c will be credited and Bank A/c will be debited. In contrary to this, if the bill got dishonoured with the bank then reverse entry of the previously entered entry will be passed in the books of the party.

- In case B, Computation of amount of discount charges:

- In case C, A endorsed the bill to his creditor C in full settlement and if in case the bill got dishonoured then B’s A/c will be debited and C’s A/c will be credited.

- In case D, the bill has send to bank for collection on the date of acceptance of bill but if on the due date the bill gone dishonoured then B’s A/c will be debited and Bill sent for collection A/c will be credited

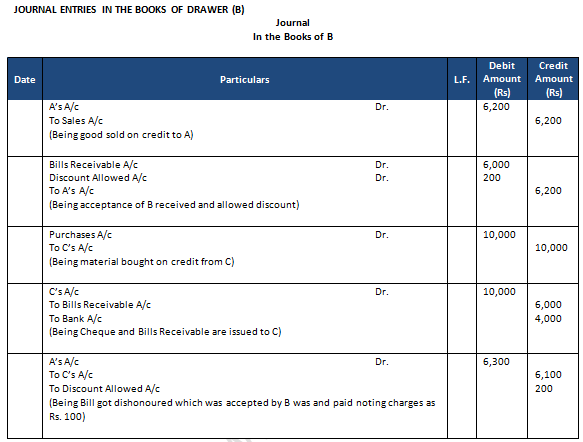

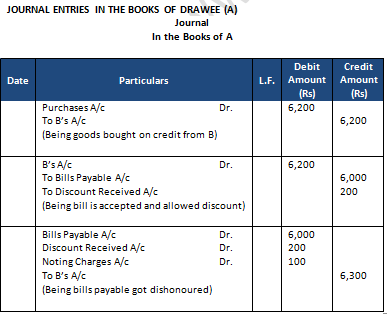

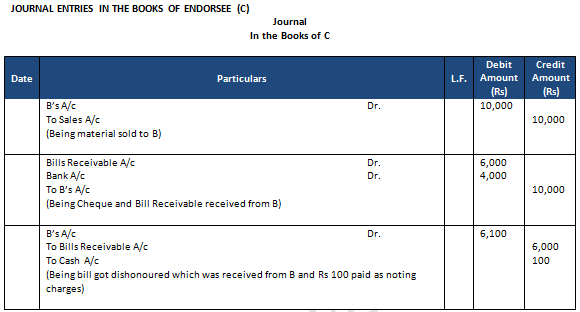

Question 20: A purchases goods worth Rs 6,200 from B and gives him his acceptance for Rs 6,000 in full satisfaction. B purchases goods worth Rs 10,000 from C and endorses the bill to him, paying the balance by cheque. On maturity the bill is dishonoured, noting charges amounted to Rs 100.

Give the Journal entries in the books of A, B and C.

Answer 20:

Points for knowledge:-

- The bill had drawn by B to A for Rs.6000 and the same bill was endorsed to C by B. The bill got dishonoured and A has to pay Rs. 100 as noting charges to the bank.

Total amount due on A will be = Amount of bill + Noting charges

= Rs. 6000 + Rs. 100

= Rs. 6100

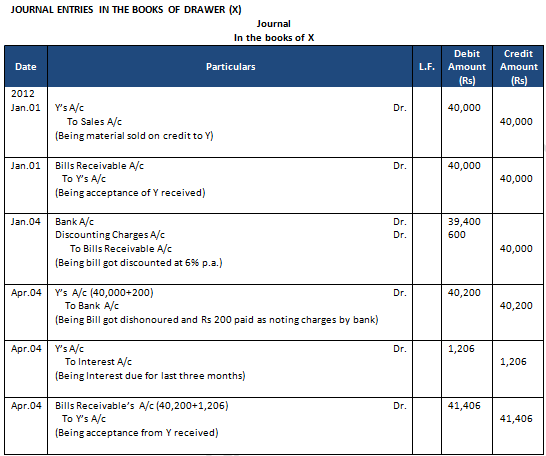

Question 21: X sells goods for Rs 40,000 to Y on 1st January, 2019 and on the same day draws a bill on Y at three months for the amount. Y accepts it and returns it to X, who discounted it on 4th January, 2019 with his bank at 6% p.a. The acceptance is dishonoured on the due date and the noting charges were paid by bank being Rs 200.

On 4th April, 2019, Y accepts a new bill at three months for the amount then due to X together with interest at 12% p.a.

Make Journal entries to record these transactions in the books of X.

Answer 21:

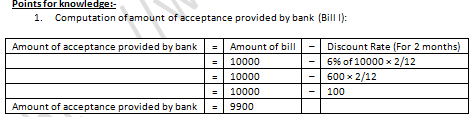

Question 22: On 15th June, 2020, X sold to Y goods to the value of Rs 15,000 drawing upon the latter two bills, one for Rs 10,000 payable 2 months after date and other for Rs 5,000 payable 3 months after date, X discounted the first bill with his bankers at 6% p.a. and endorsed the second bill in favour of his creditor, Z. The first bill was met on maturity but the second was dishonoured. Z paid Rs 50 as noting charges. On 1st October, Y cleared his account to X by paying Rs 5,100 which included Rs 50 as interest.

Answer 22:

2. The bill had drawn by X to Y for Rs.5000 (Bill II). The bill got dishonoured. Calculation of amount due on Y are as follows:

Total amount due on Y will be = Amount of bill + Noting charges

= Rs. 5000 + Rs. 50

= Rs. 5050

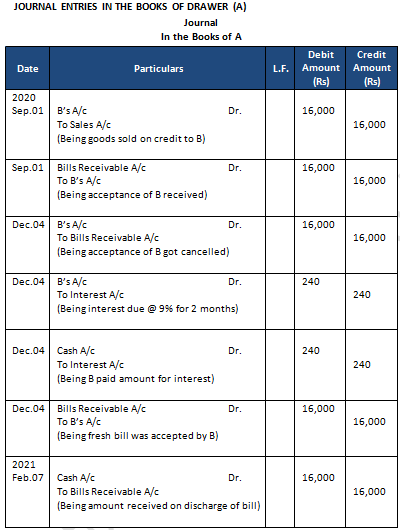

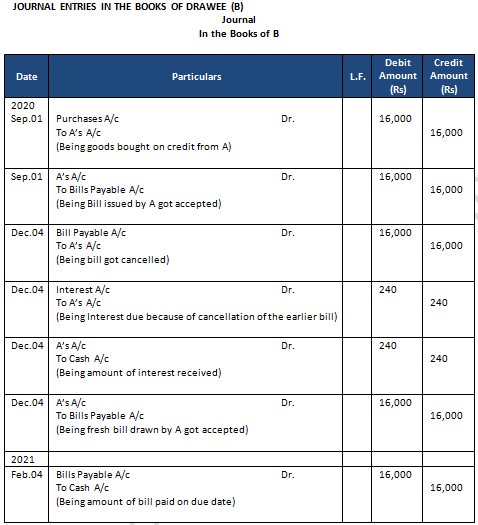

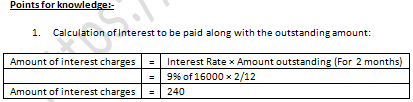

Question 23: A sold goods to B on 1st September, 2020 for Rs 16,000. B immediately accepted a 3 months bill. On the due date, B requested that the bill be renewed for a further period of 2 months. A agreed provided interest at 9% p.a. was paid immediately in cash. To this B was agreeable. The second bill was met on the due date. Give the Journal entries in the books of A.

Answer 23:

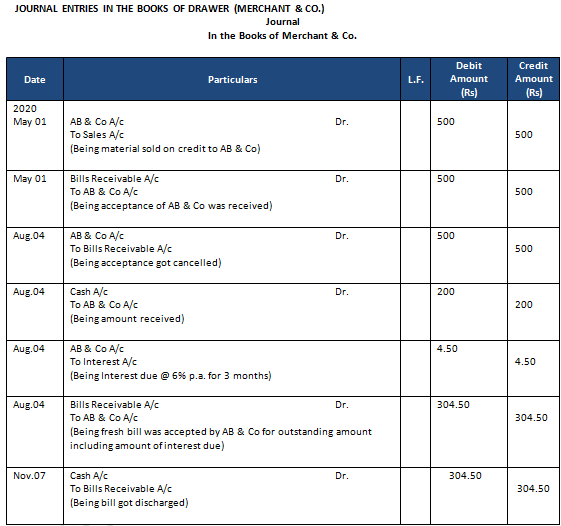

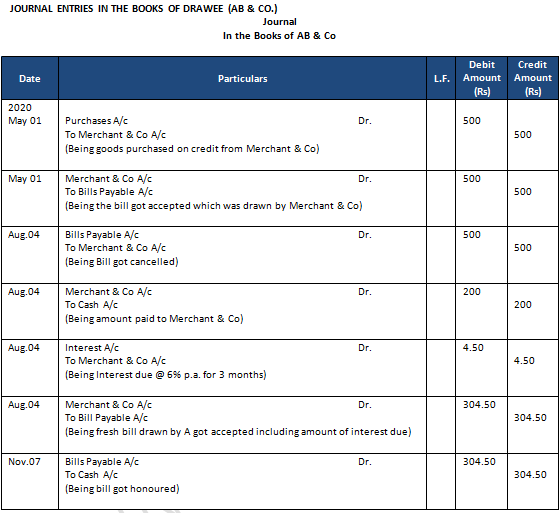

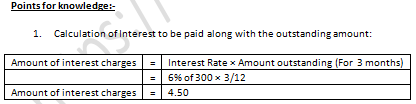

Question 24: On 1st May, 2020 Merchant & Co. sold goods to AB & Co. valued at Rs 500 and drew upon them a bill at 3 months for the amount. AB & Co. accepted the draft on presentation. When the bill was about to mature. AB & Co. expressed their inability to meet it, and offered to pay Merchant & Co. Rs 200 in cash and to accept a fresh bill for the balance plus interest at 6% p.a. for 3 months Merchant & Co. agreed to the proposal and bill was renewed. On maturity, the bill was duly met.

Make the entries in the books of both the parties to record the above transactions.

Answer 24:

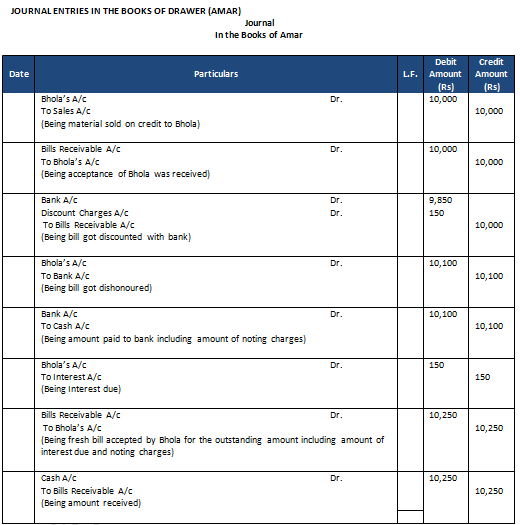

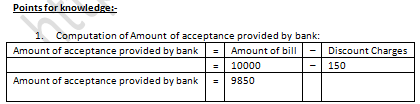

Question 25: Amar sells goods to Bhola for Rs 10,000 and draws upon him a bill for the amount payable 3 months after date. The bill is accepted by Bhola. Amar discounts the bill with his bankers at a discount of Rs 150 inclusive of all charges. Bhola fails to meet this bill on maturity. Amar pays off his banker and his expenses amounting to Rs 100. Bhola gives a fresh bill, 2 months' date to Amar for Rs 10,250, which he met at maturity.

Show the necessary Journal entries in Amar's books.

Answer 25:

Question 26: A owed B Rs 400. A accepted a Bill of Exchange at 3 months date for this amount which B discounted for Rs. 380.

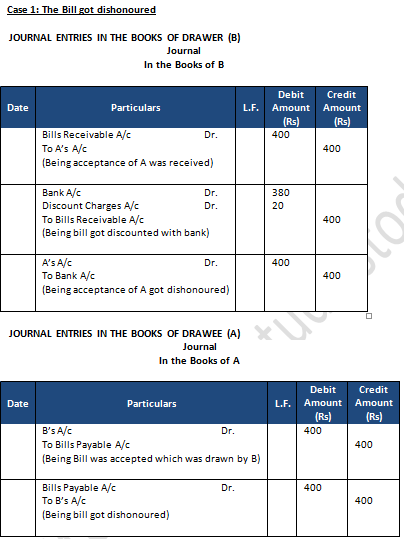

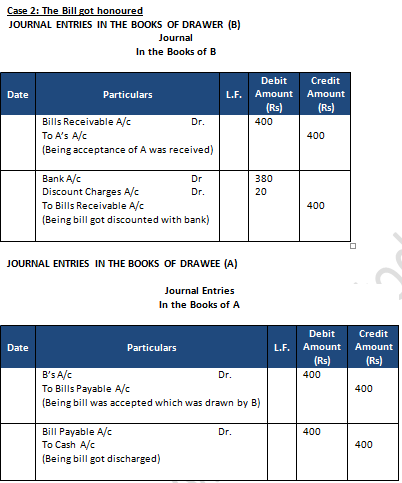

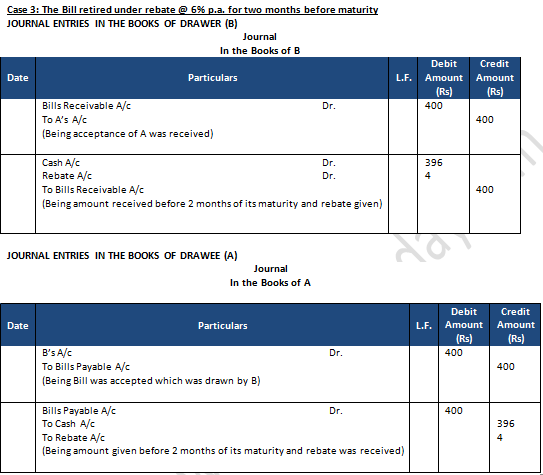

Give the necessary Journal entries in the books of A and B if this bill is:

(a) dishonoured on the due date;

(b) met at maturity and

(c) retired under rebate at 6% p.a. 2 months before its maturity.

Answer 26:

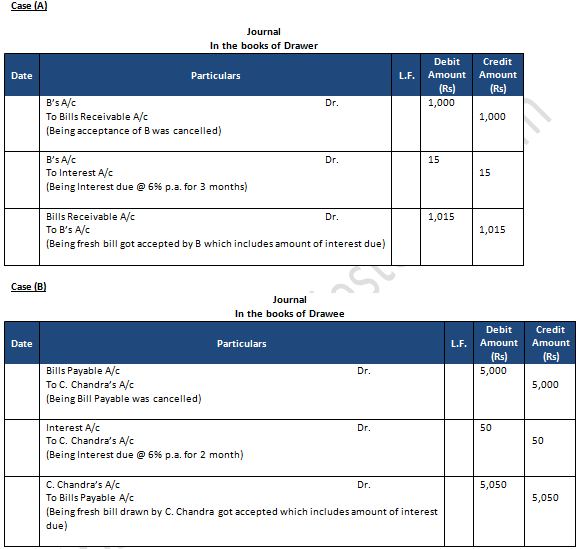

Question 27: Give the Journal entries for the following:

(a) B's acceptance to us for Rs 1,000 due this day, renewed at his request for 3 months with interest @ 6% p.a.

(b) Our bill to C. Chandra for Rs 5,000 renewed for 2 months with interest @ 6% p.a.

(c) B's acceptance of Rs 3,000 is discharged on his paying us cash Rs 1,000 and accepting a fresh bill for the balance with interest Rs 100.

Answer 27:

JOURNAL ENTRIES

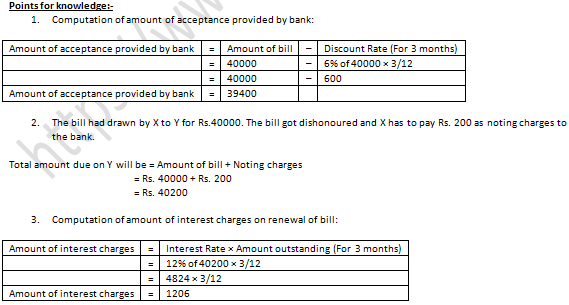

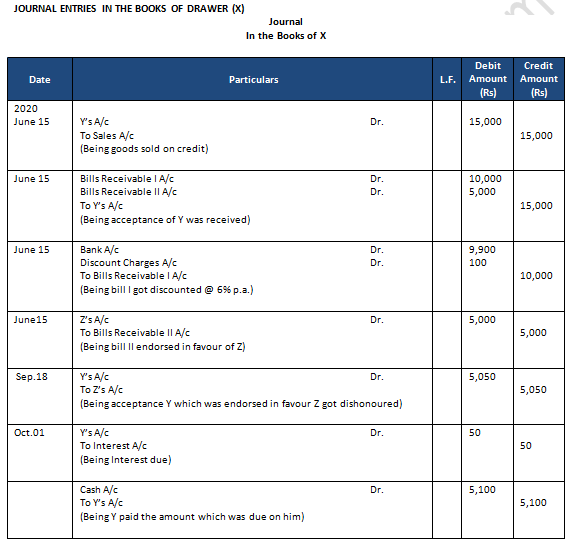

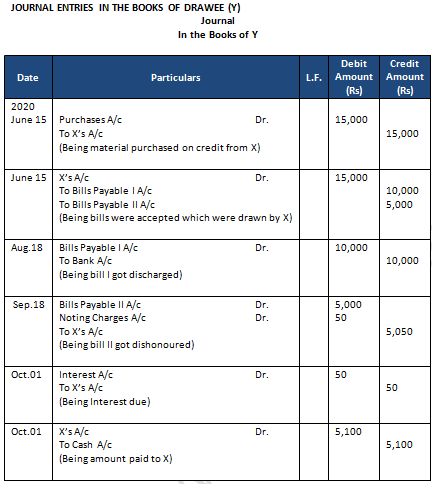

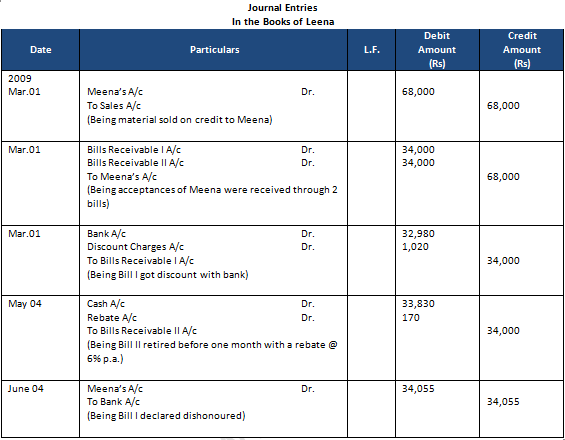

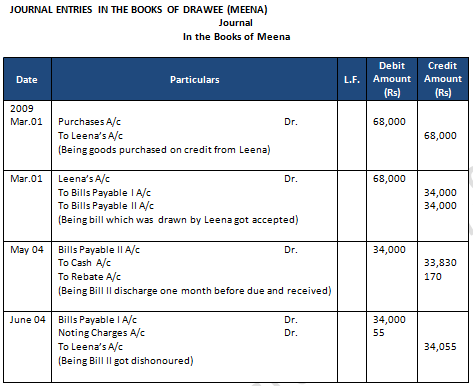

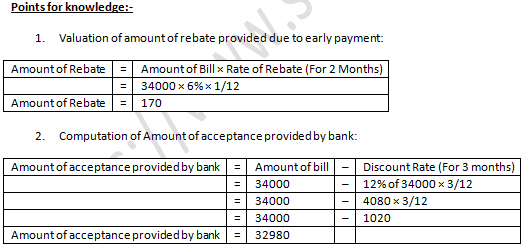

Question 28: Leena sold goods to Meena on 1st March, 2009 for Rs 68,000 and drew two Bills of Exchange of the equal amount upon Meena payable after three months. Leena immediately discounted the first bill with her bank at 12% p.a. The bill was dishonoured by Meena and Bank paid Rs. 55 as noting charges. The second bill was retired on 4th May, 2009 under a rebate of 6% p.a. with mutual agreement. Journalise the above in the books of Leena and Meena.

Answer 28:

JOURNAL ENTRIES IN THE BOOKS OF DRAWER (LEENA)

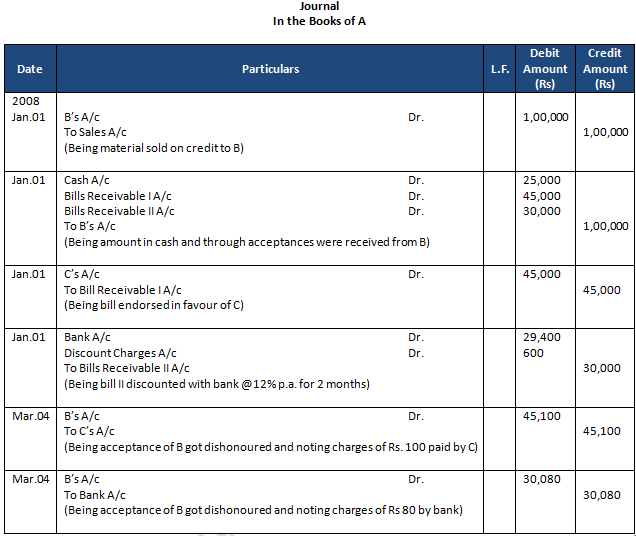

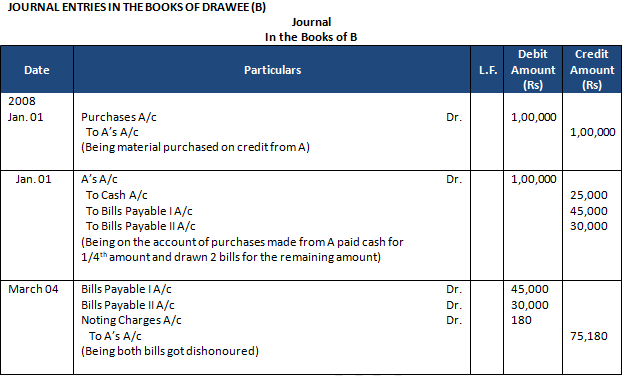

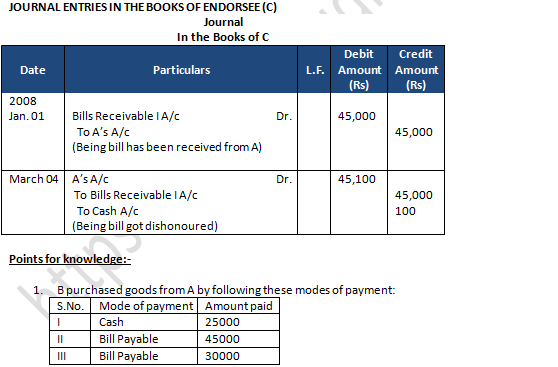

Question 29: On 1st January, 2008, A sold goods to B for Rs. 1,00,000 received Rs. 25,000 in cash and drew two bills, first Rs. 45,000 and second for Rs. 30,000 of two months each. Both bills were duly accepted by B. First bill was endorsed to C in settlement of his account of Rs. 45,000 and second bill was discounted from the bank at the rate of 12% p.a. On the due date of these bills, both bills were dishonoured, C has paid Rs. 100 and bank has paid Rs. 80 as noting charges.

Pass Journal entries in the books of A, B and C.

Answer 29:

JOURNAL ENTRIES IN THE BOOKS OF DRAWER (A)

2. A endorsed the Bill I of amounting Rs. 45000 to his creditor C and on the date of maturity the bill got dishonoured on account of that C has to pay Rs. 100 as noting charges.

3. Bill II got dishonoured on account of that bank has to pay noting charges of Rs. 80

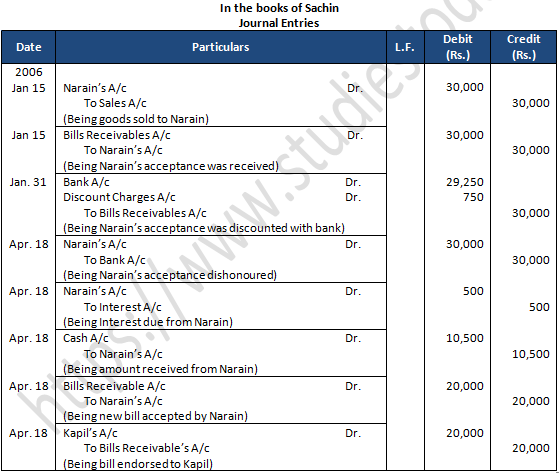

Question 30: On 15th January, 2016 Sachin sold goods for Rs. 30,000 to Narain and drew upon later a bill for the same amount payable after 3 months. The bill was accepted by Narain. The bill was discounted by Sachin from his bank for Rs.29,250 on 31th January, 2016, on maturity the bill was dishonored . He further agreed to pay Rs. 10,500 in cash including Rs. 500 interest and accept a new bill for two months for the remaining Rs. 20,000. The new bill was endorsed by Sachin in favour of his creditor Kapil for debt of Rs. 20,000. The new bill was duly met by Narain on maturity. Record the necessary Journal entries in the books of Sachin.

Answer 30:

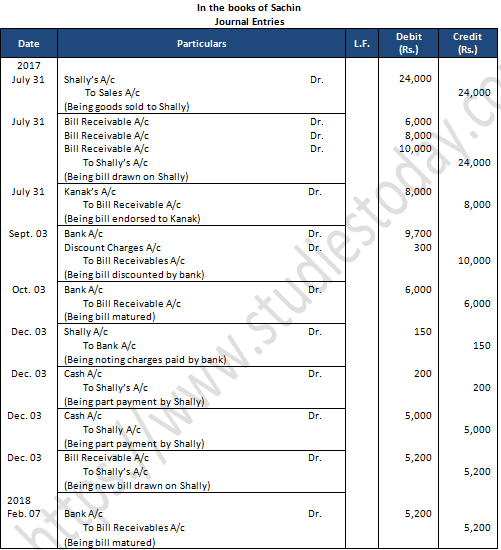

Question 31: Mehak sold goods for Rs. 24,000 to Shally on 31st July, 2017 and drew three bills for Rs. 6,000, Rs. 8,000 and Rs. 10,000 payable after two, three and four months respectively. The first bill was kept by Mehak with her till maturity date. She endorsed the second bill in favour of her creditor Kanak. The third bill was discounted on 3rd September, 2017 @ 12% p.a. from bank. The first and second bill were duly were duly met on maturity but the third bill was dishonored and the bank paid Rs. 150 as noting charges. On 3rd December, 2017 Shally paid Rs. 5,000 and noting charges in cash and accepted a new bill at two months after date for the balance amount plus interest Rs. 200. The new bill was met on maturity by Shally. You are required to give the Journal entries in the books on Mehak.

Answer 31: