Access free TS Grewal Accountancy Class 11 Solution Chapter 4 Bases of Accounting 2026 below. Students can now access free TS Grewal Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 4 Bases of Accounting TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 4 Bases of Accounting Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 4 Bases of Accounting TS Grewal Class 11 Solved Exercises

About this chapter: TS Grewal Accountancy Class 11 Chapter 4 Bases of Accounting is an important chapter which explains various basis of accounting such as accrual basis, hybrid bases and cash basis accounting. Every organisation has to select one of the basis of accounting based on which day decide to keep their day to day books of accounts. For example cash basis for accounting only records cash transactions which have been received and paid whereas under accrual basis of accounting all transactions which are due to be received or paid are recorded on accrual basis. These transactions are recorded irrespective of actual cash transaction. Mr TS Grewal has explained about the advantages and disadvantages of both the different types of accounting. Students should understand this chapter carefully as this will help them in future if they want to have a career in accountancy. As this is an important topic which forms basis of accounting for students and helps them to build a strong foundation you should also refer to the answers which have been provided below to all the questions given at the end of this chapter.

Question.1 Discuss the Cash and Accrual Basis of Accounting?

Answer.1.

Cash Basis of Accounting: Cash basis of accounting is a system in which transactions arerecorded when cash is received or paid. Revenue is recognised on receipt of cash. Expenses are recorded as incurred when they have been paid. The difference between the totalincomes and total expenses represents profit or loss of a business for the accounting period. Thus, when Cash Basis of Accounting is followed, outstanding and prepaid expenses andincome received in advance or accrued incomes are not considered.

Accrual Basis of Accounting: Under accrual basis of accounting income is recorded as incomewhen it is earned or accrued. Similarly, if an expense has been incurred but payment hasnot been made, it will be recorded as an expense. Accrual Basis of Accounting is based onthe concept of realisation and expiration and follows two basic accounting principles, i.e., revenue recognition and matching principle. Under this method net income for the period isthe result of matching revenue realised in the period and cost incurred, whether paid or not.The difference between total income and total expense incurred is the profit or loss for theperiod.

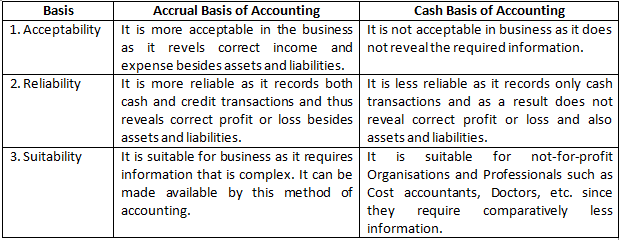

Question.2. Write any three difference between Cash Basis and Accrual Basis of Accounting.

Answer.2.

The following are three differences between Cash Basis and Accrual Basis of Accounting:

Question.3. What is meant by accrual basis of accounting? Give two advantages of accrual basis accounting.

Answer.3.

Accrual Basis of Accounting: Under accrual basis of accounting income is recorded asincome when it is earned or accrued. Similarly, if an expense has been incurred butpayment has not been made, it will be recorded as an expense. Accrual Basis of accounting is based on the concept of realisation and expiration and follows two basic accountingprinciples, i.e., revenue recognition and matching principle. Under this method net incomefor the period is the result of matching revenue realised in the period and cost incurred,whether paid or not. The difference between total income and total expense incurred is theprofit or loss for the period.

The following three advantages of Accrual Basis of Accounting are:

(i) It is more scientific compared to cash Basis of Accounting and hence is preferred byaccountants

(ii)This basis discloses correct profit or loss for a particular period and also exhibits truefinancial position of the business on a particular day.

(iii) It reflects true profit or loss during the accounting period and, therefore, has wideacceptability. This system is followed by most of the industrial and commercial firms.

Question.4 What is meant by Cash basis of accounting? Give two disadvantages of cash basis of accounting.

Answer.4.

Cash Basis of Accounting: Cash basis of accounting is a system in which transactions are recorded when cash is received or paid. Revenue is recognised on receipt of cash. Expenses are recorded as incurred when they have been paid. The difference between the total incomes and total expenses represents profit or loss of a business for the accounting period. Thus, when Cash Basis of Accounting is followed, outstanding and prepaid expenses and income received in advance or accrued incomes are not considered.

The following two disadvantages of cash basis of Accounting are:

(i) It does not follow the matching principle of accounting.

(ii) This system does not distinguish between capital and revenue items and, as a result, there is no consistency in the profit of the two years.

Question.5. ‘Cash Basis of Accounting’ is not a better basis for depicting the correct financial position of an enterprise. Do you agree? Give reason in support of your answer.

Answer.5.

‘Cash Basis of Accounting’ is not a better basis for depicting the correct financial position of an enterprise because it does not give a true and fair view of the profit or loss and the financial position of an enterprise because it ignores outstanding and prepaid expense and accrued income and income received in advance.

Question.6. During the financial year 2020-21, Mohan had cash sales of Rs. 90,000 and credit sales of Rs. 60,000. His expenses for the year were Rs. 70,000 out of which Rs. 30,000 is still to be paid. Find out Mohan’s income for 2020-21 following the Cash Basis of Accounting.

Answer.6.

Mohan’s income for First Year – Second Year following Cash Basis of Accounting

= Cash Sales – Expenses paid in Cash

= Rs. 90,000 – (Rs. 70,000 – Rs. 30,000)

= Rs. 90,000 – Rs.40,000

= Rs. 50,000

Question.7. Taking the figures given in Questionuestion.6, find out the net income according to Accrual Basis of Accounting.

Answer.7.

Mohan’s income for First Year – Second Year following Accrual Basis of Accounting

= Total Sales – Total Expenses

= Cash Sales + Credit Sales – Total Expenses

= Rs. 90,000 + Rs. 60,000 – Rs. 70,000

= Rs. 1,50,000 – Rs. 70,000

= Rs. 80,000

Question.8. Vijay, a consultant, during the financial year 2020-21 earned Rs. 4,00,000. Out of which he received Rs. 3,50,000. He incurred an expense of Rs. 1,70,000, out of which Rs. 40,000 are outstanding. He also received consultancy fee relating to previous year Rs. 45,000 and also paid Rs. 20,000 expenses of last year.

You are required to determine his income for the year if

(i) He follows Cash Basis of Accounting and

(ii) He follows Accrual Basis of Accounting.

Answer.8.

Vijay’s income for the year First Year – Second Year if:

(i) He follows Cash Basis of Accounting = Current Year’s Consultancy Received + Last Year’s Consultancy Received – Current Year’s Expenses Paid – Last Year’s Expenses Paid

= Rs. 3,50,000 + Rs. 45,000 – (Rs. 1,70,000 – Rs. 40,000) – Rs. 20,000

= Rs. 2,45,000

(ii) He follows Accrual Basis of Accounting = Current Year’s Consultancy Due – Current Year’s Expenses Due

= Rs. 4,00,000 – Rs. 1,70,000

= Rs. 2,30,000