Access free DK Goel Solutions Class 11 Accountancy Chapter 23 Accounts from Incomplete Records 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 23 Accounts from Incomplete Records DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 23 Accounts from Incomplete Records Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 23 Accounts from Incomplete Records DK Goel Class 11 Solved Exercises

Short Answer Questions

Question 1.

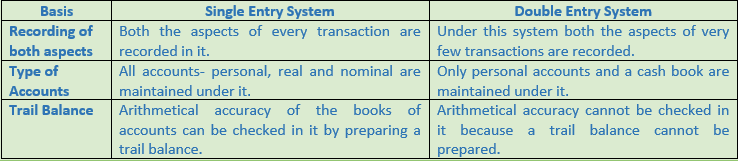

Solution 1: Below are the characteristics of Single Entry System:-

1.) Maintenance of Personal Accounts only:- Usually under this system, only personal accounts are prepared in the books and the real and nominal accounts are ignored.

2.) Maintenance of Cash Book:- A Cash Book is maintained under this system, which usually mixes up business as well as private transactions of the proprietor.

3.) Dependence on Original Vouchers:- In order to collect the required information one has to depend on original vouchers.

Question 2.

Solution 2: Below are the reasons for keeping records under single entry system:-

1.) Simple Method:- It is an easy and simple method of recording business transactions because it does not require any special knowledge of the principles of double entry system.

2.) Less Expensive:- Only the cash book and some of the ledger accounts are maintained under this system. As such the staff required for maintaining the accounts is also less in comparison to double entry system.

3.) Suitable for small concerns:- This method is most suitable to small business concerns which have mostly cash transactions and very few assets and liabilities.

Question 3.

Solution 3: Below are the defects of Incomplete records:-

1.) Preparation of Trail Balance not Possible:- The method does not record both the aspects of transaction. As such, a trail balance cannot be prepared to check the arithmetical accuracy of the books of accounts. This increases the possibility of frauds and misappropriations.

2.) Incomplete and Unscientific System:- The system is incomplete and unscientific due to the fact that both the aspects, debit and credit of a transaction are not recorded.

3.) True Profit or Loss cannot be ascertained:- Because nominal accounts are not maintained, a Trading and profit and loss account cannot be prepared and hence, the profit earned or loss suffered during a particular period cannot be ascertained with reasonable accuracy.

Question 4.

Solution 4:

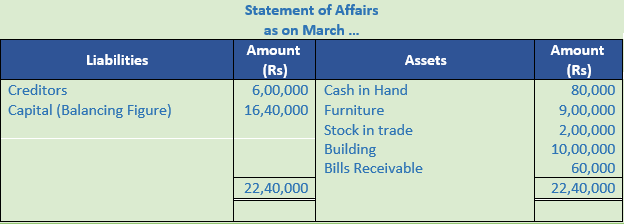

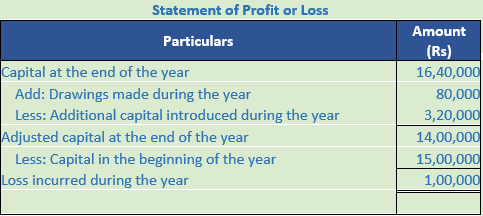

Question 5.

Solution 5:

Despite the records being incomplete, the businessman would like to know the trading results also the financial position of his business at the end of a particular period. This is done by adopting one of the two methods mentioned below:-

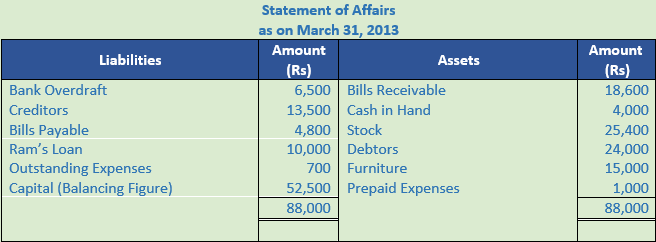

1.) Statement of affairs method or capital comparison method or Net worth method.

2.) Conversion into double entry method.

Question 6.

Solution 6: According to this method, the profits are ascertained by comparing the capital at the end and capital at the beginning of the accounting period. If the capital at the end of an accounting period is more than that at the beginning (with the necessary adjustments), the difference is treated as profit.

Question 7.

Solution 7:

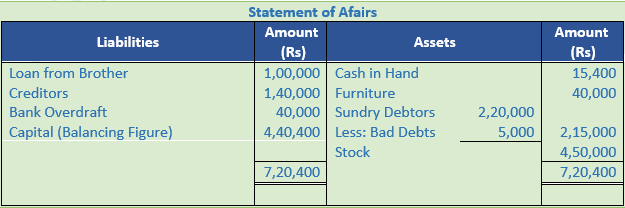

Question 8.

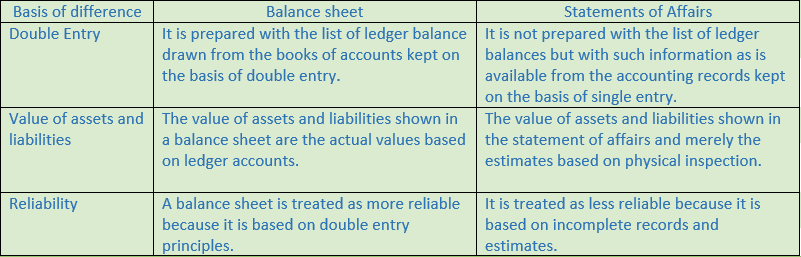

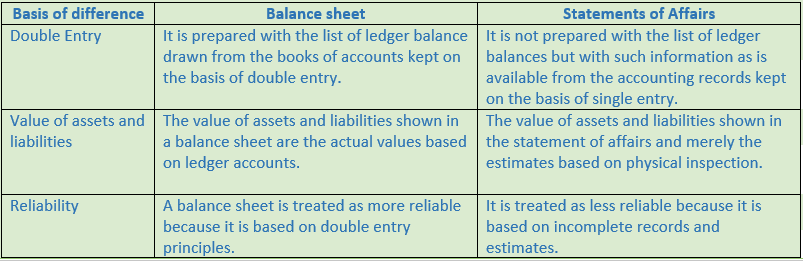

Solution 8: Statement of Affairs not called a balance sheet because;-

Question 9.

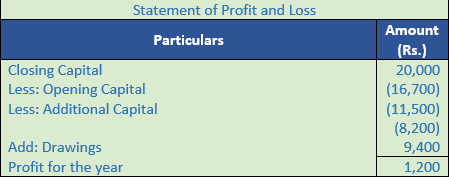

Solution 9: Drawings are added to the closing capital on the logic that if the drawings had not been made, closing capital would have higher by this amount. Similarly additional capital is deducted from the closing capital on the logic that if the amount.

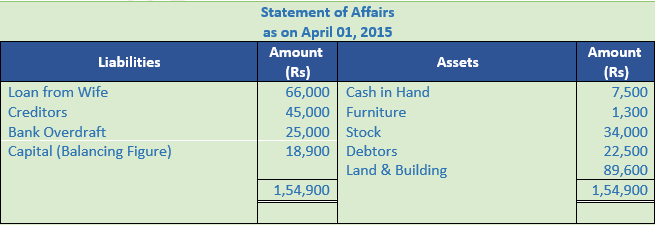

Question 10.

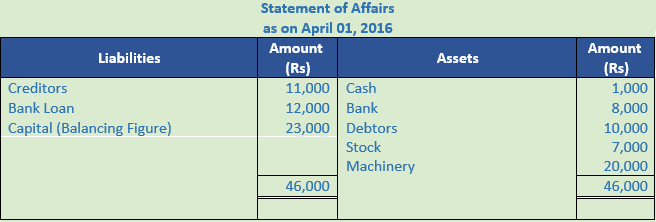

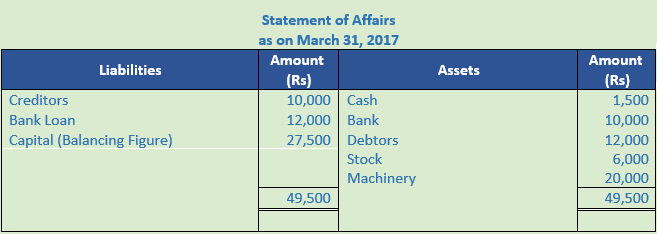

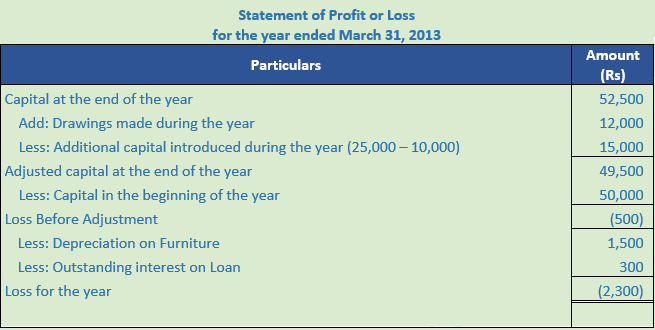

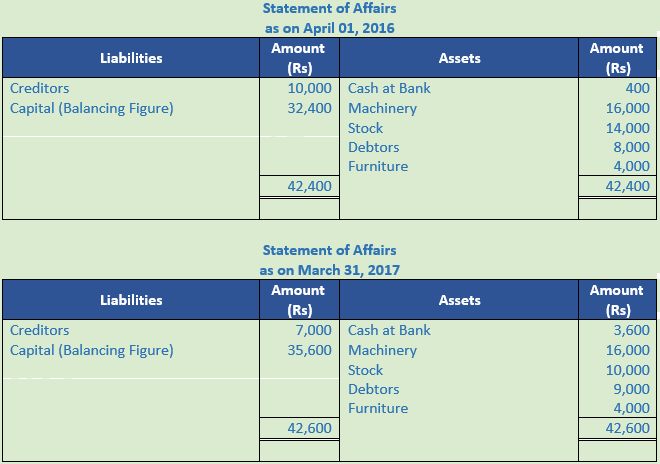

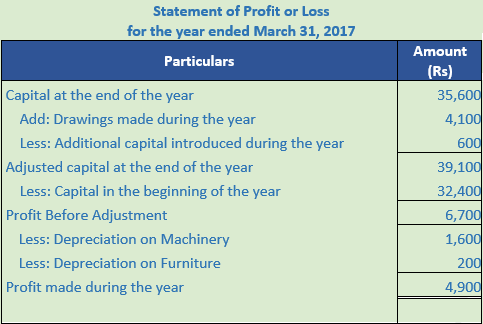

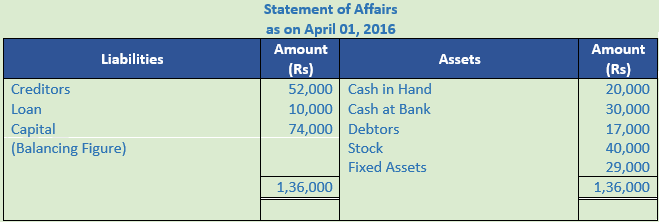

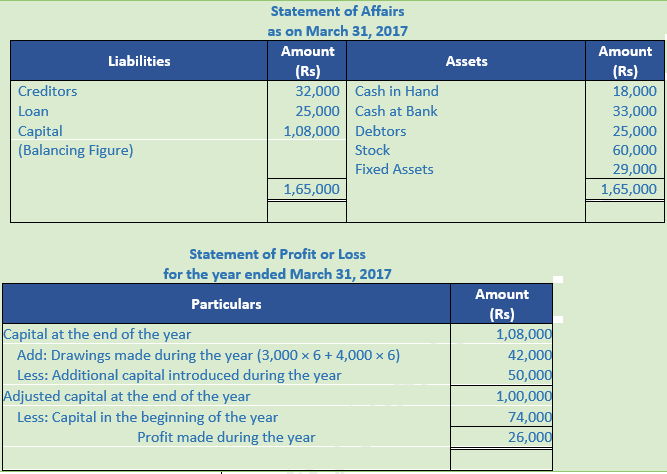

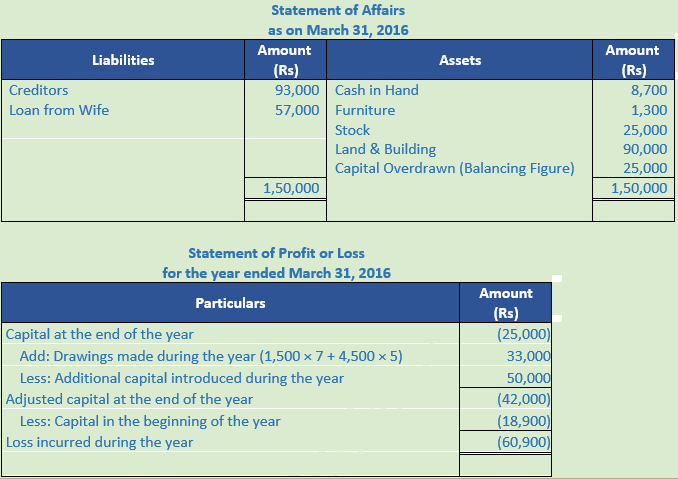

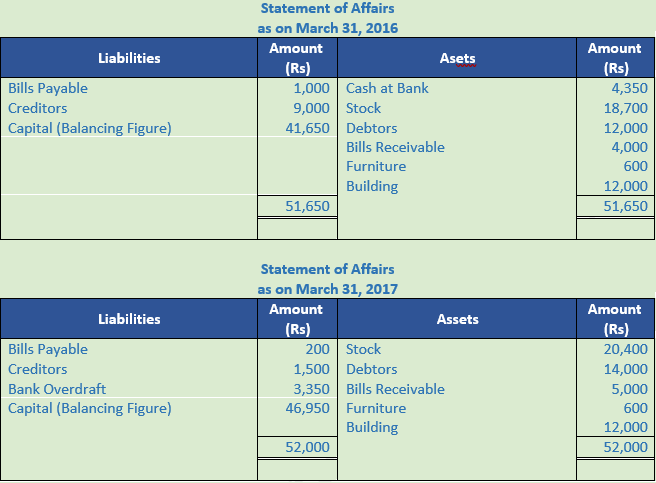

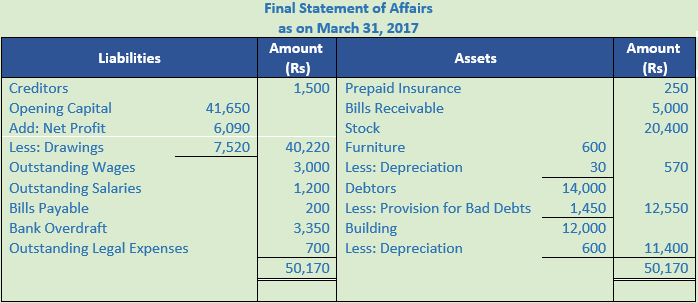

Solution 10: In order to ascertain profit according to this method, it is necessary to calculate the capital at the beginning of the year and also at the end of the year. Capital at the beginning is calculated by preparing an ‘opening statement of Affairs’ and similarly, capital at the end is calculated by preparing a ‘Closing Statement of Affairs’.

Question 11.

Solution 11:

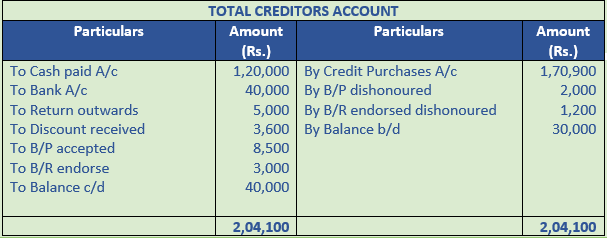

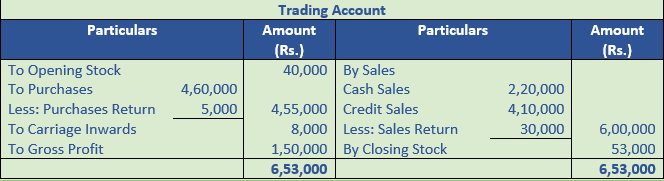

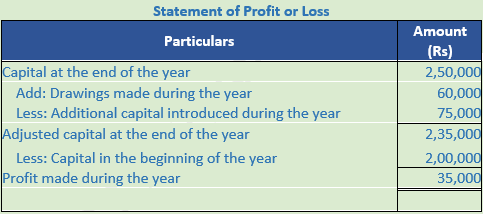

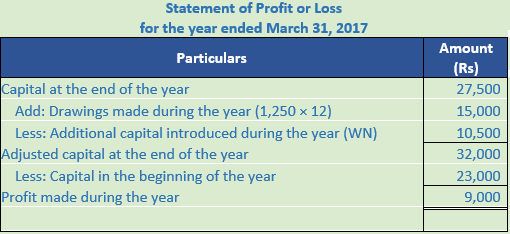

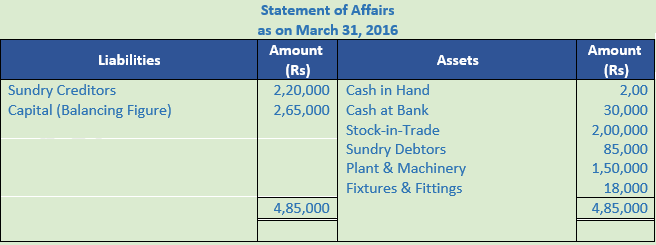

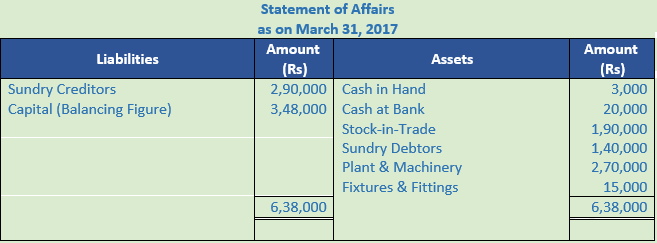

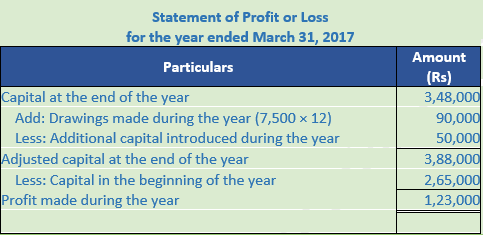

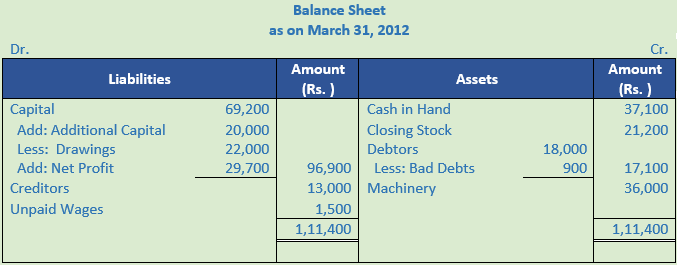

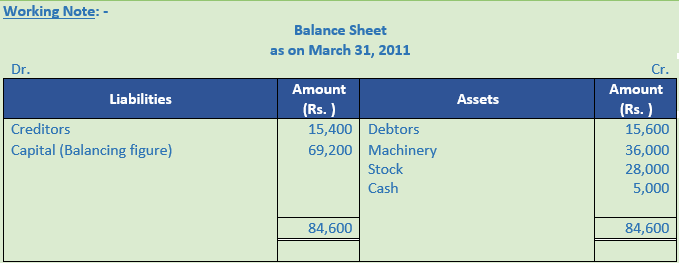

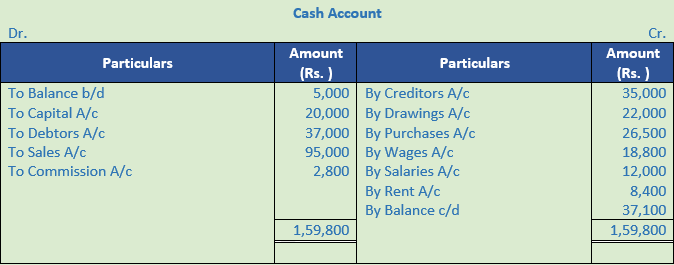

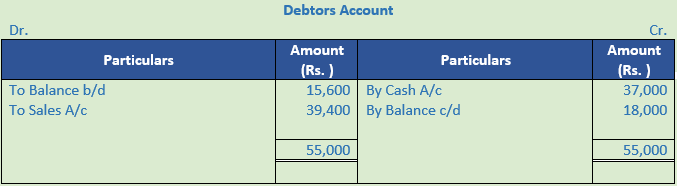

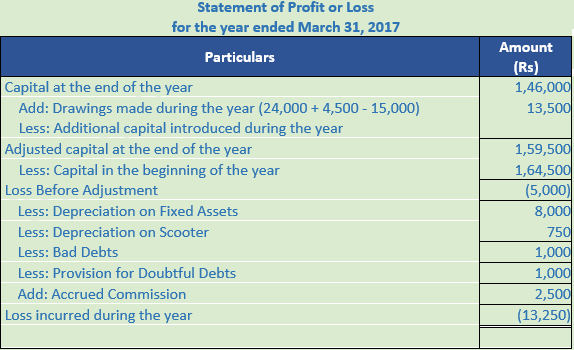

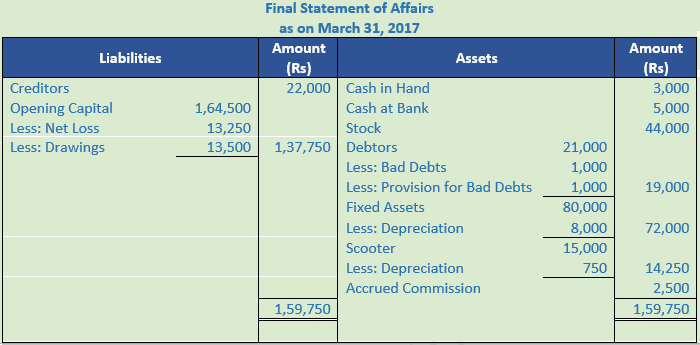

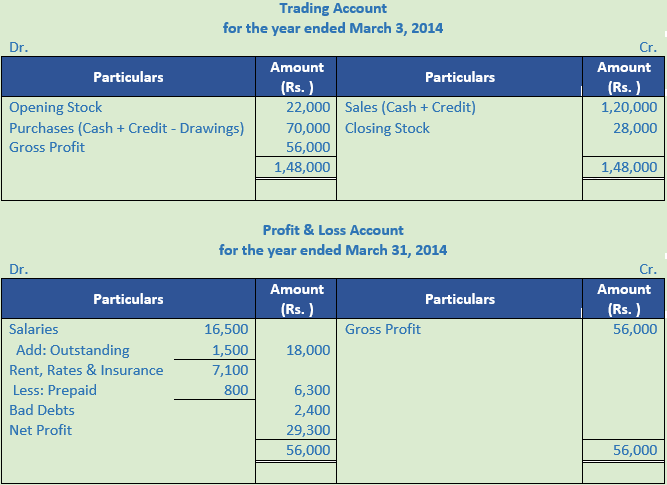

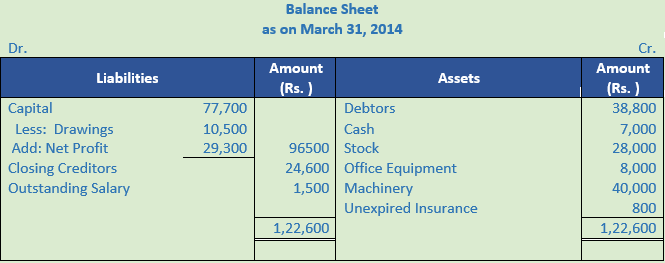

Question 12.

Solution 12:

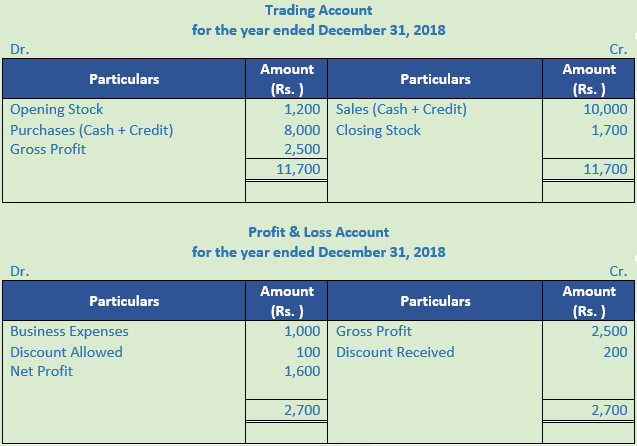

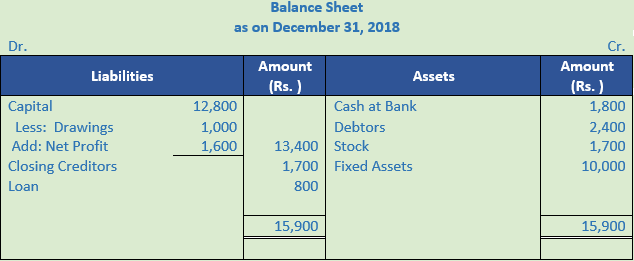

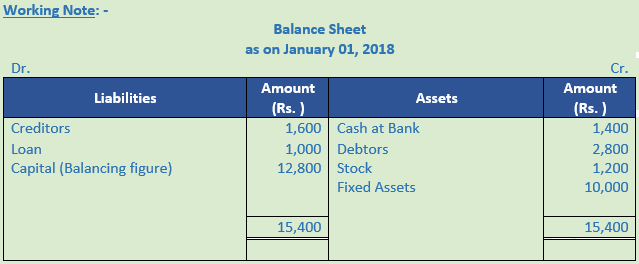

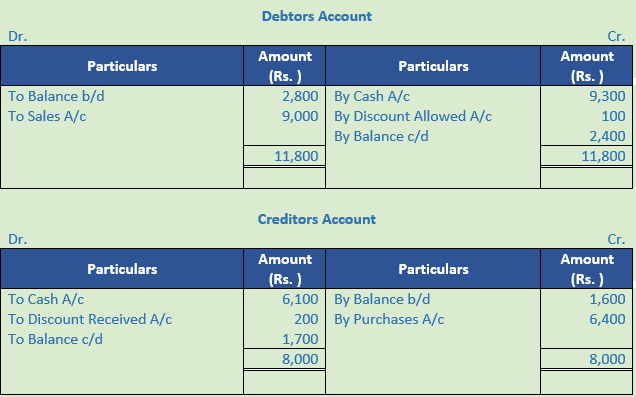

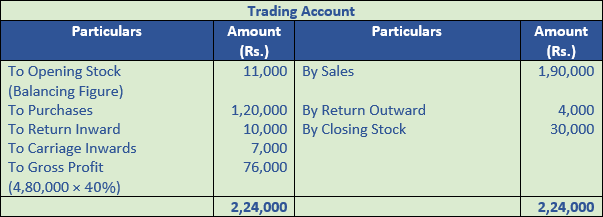

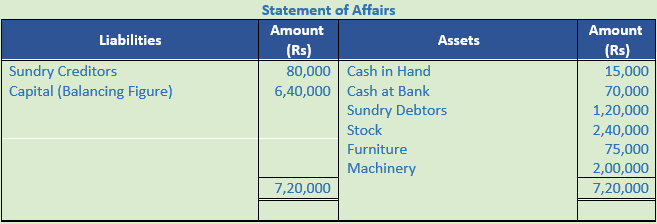

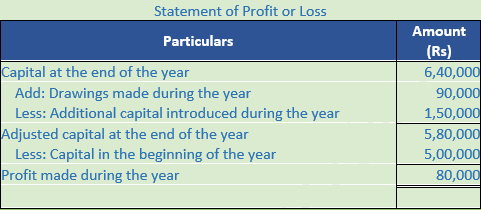

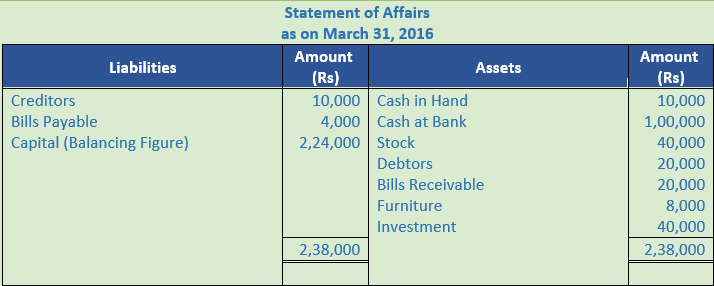

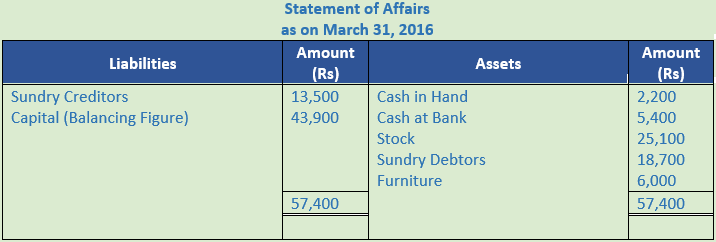

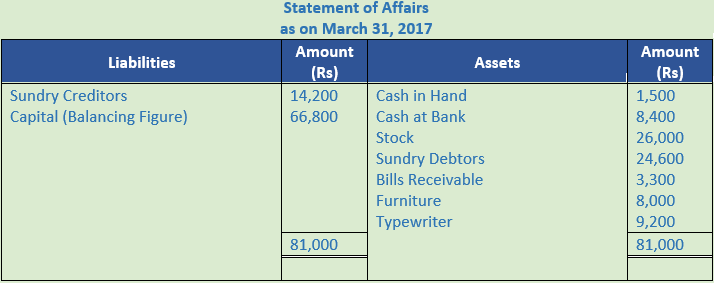

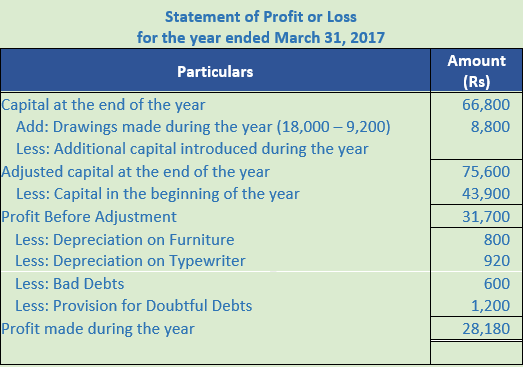

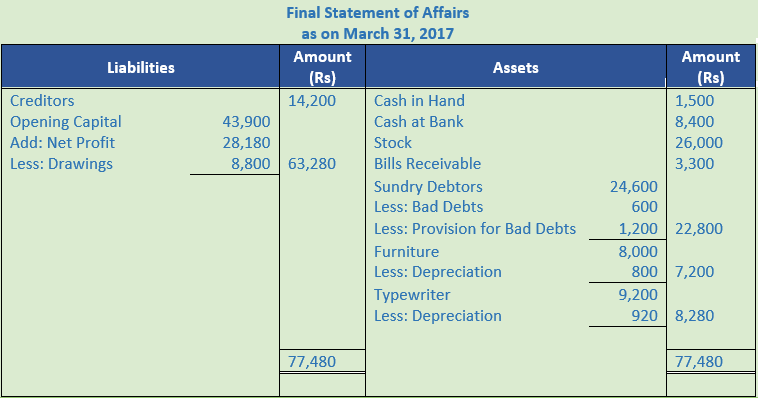

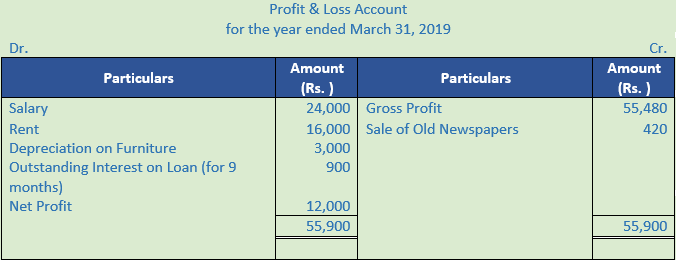

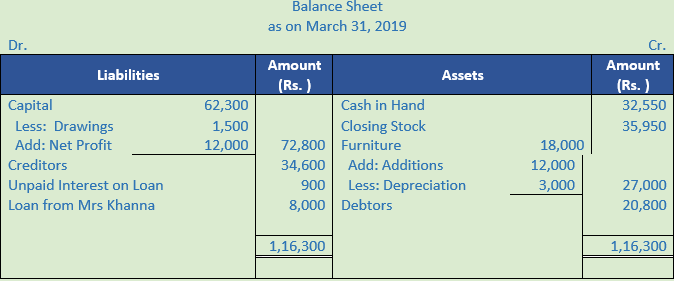

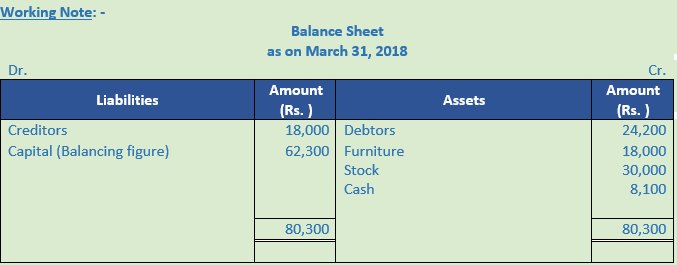

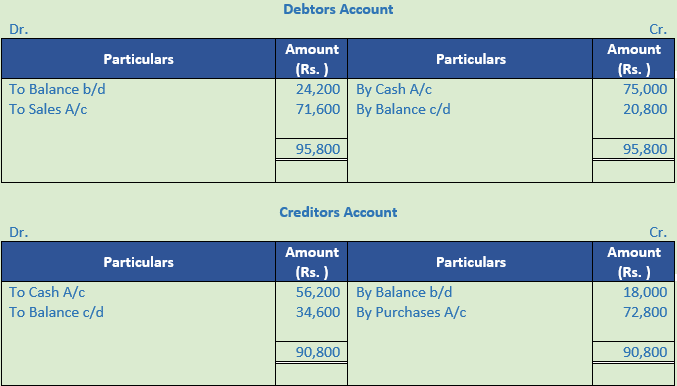

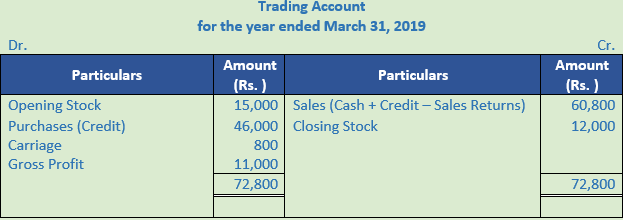

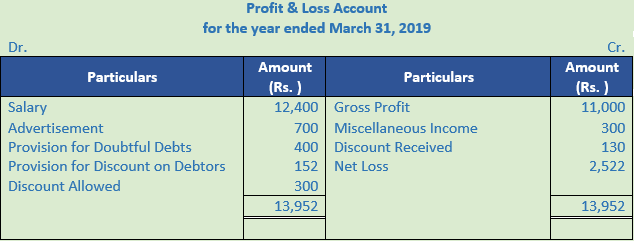

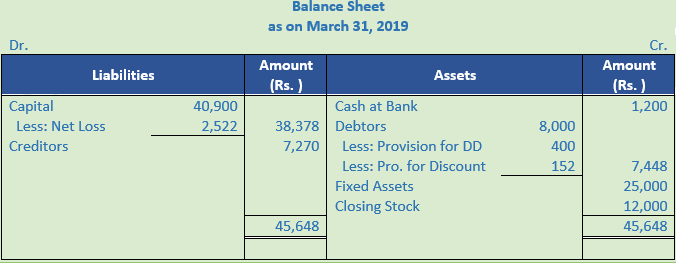

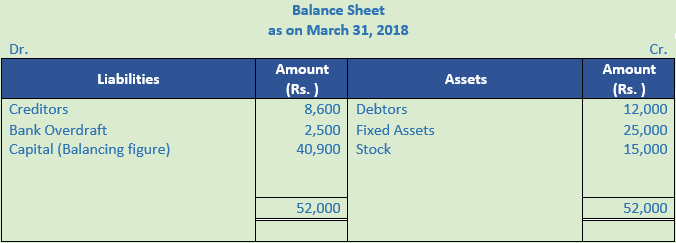

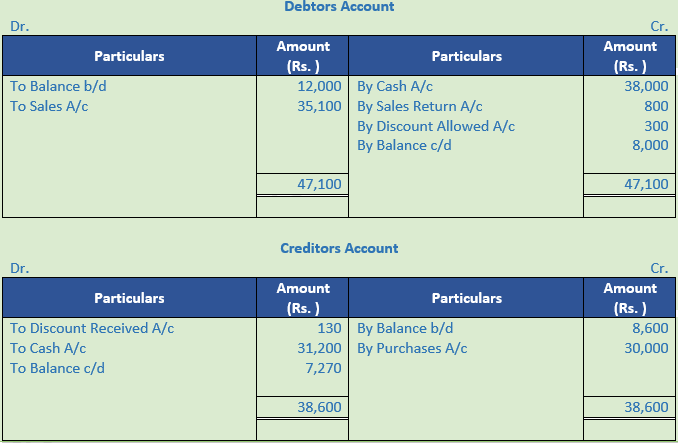

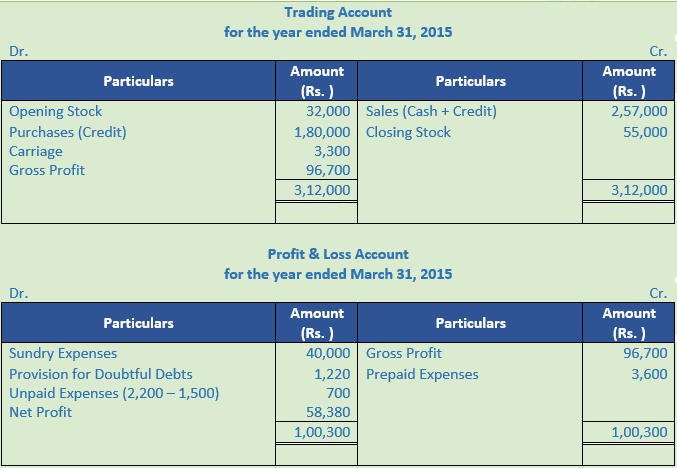

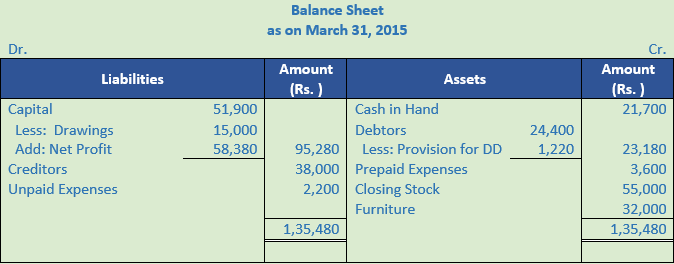

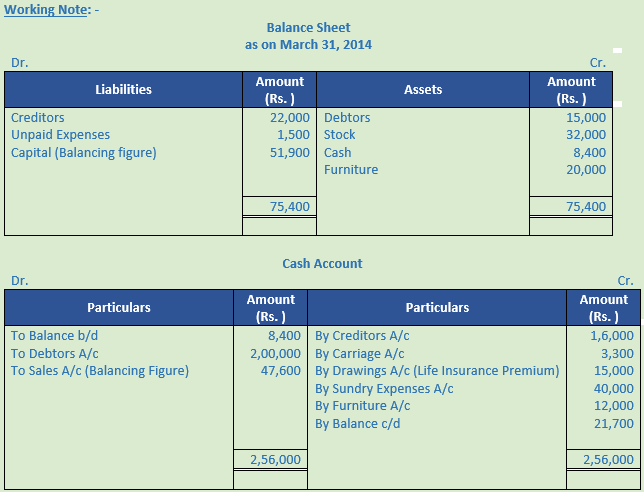

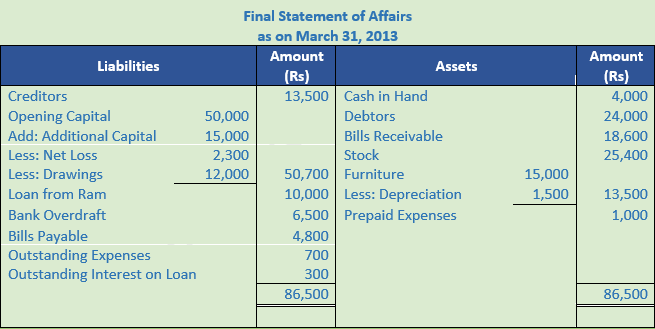

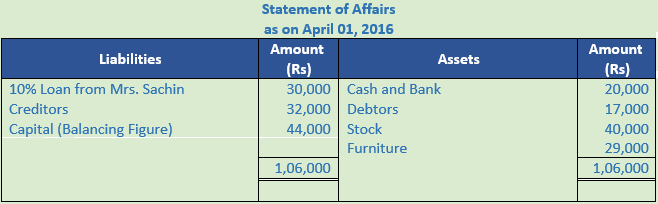

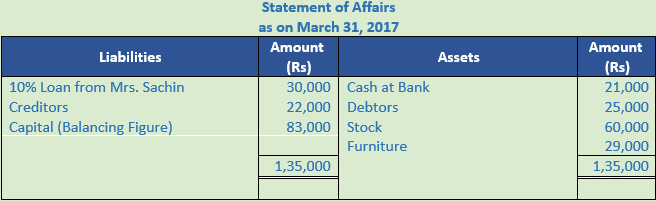

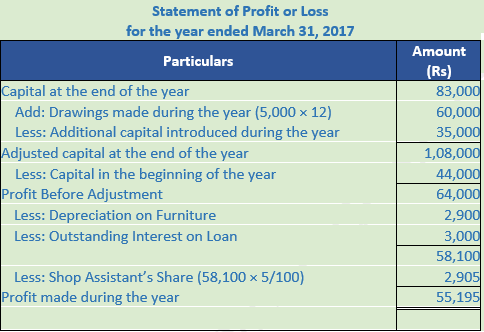

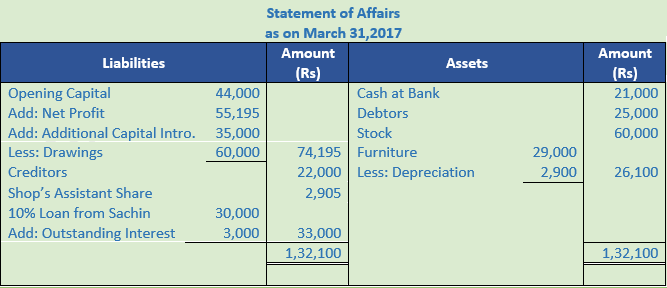

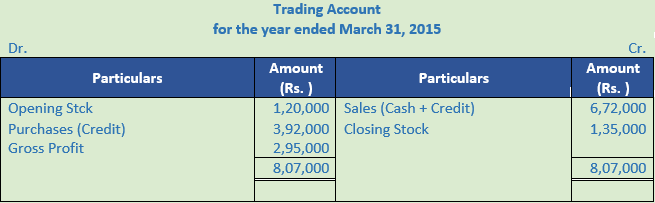

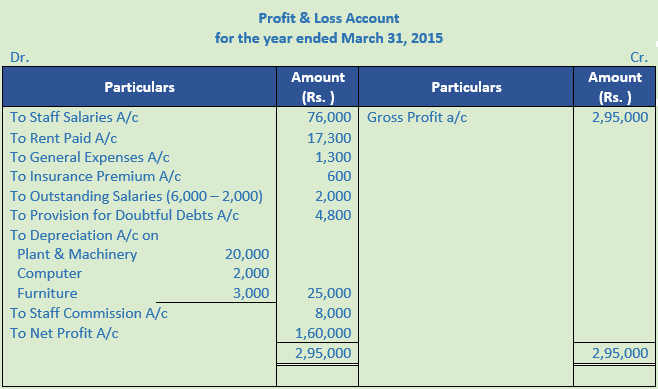

Question 13.

Solution 13:

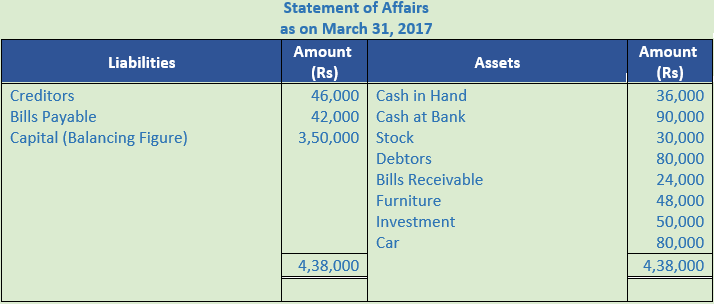

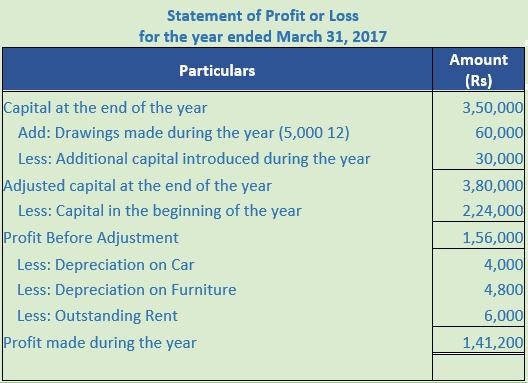

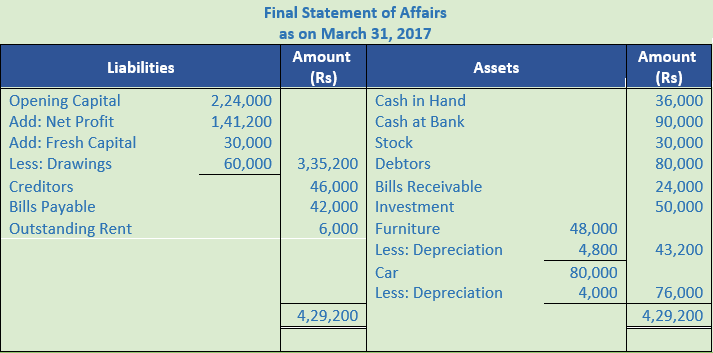

Question 14.

Solution 14:

Question 15.

Solution 15:

Question 16.

Solution 16:

Practical Questions

Question 1.

Solution 1:

Point of Knowledge:-

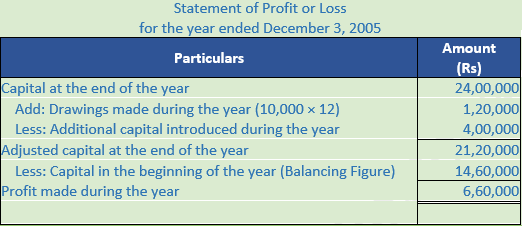

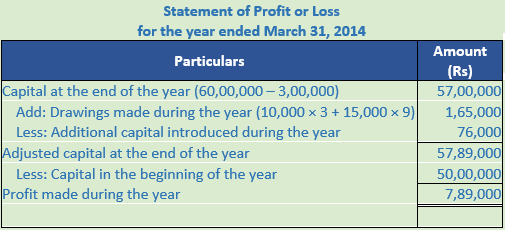

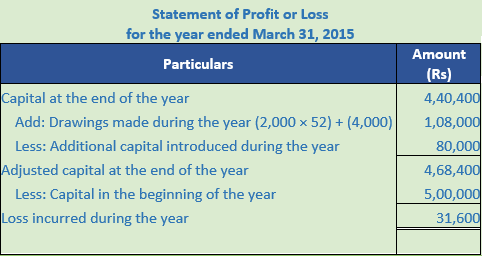

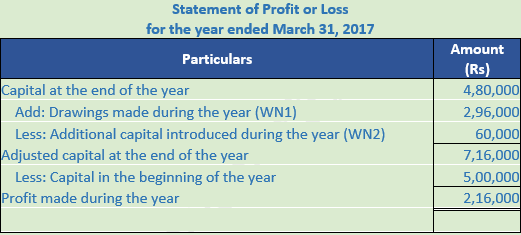

Profit = Closing Capital + Drawings – Additional Capital – Opening Capital

Question 2.

Solution 2:

Question 3.

Solution 3:

Question 4.

Solution 4:

Question 5. (A)

Solution 5 (A):

Question 5. (B)

Solution 5 (B):

Profit = Closing Capital + Drawings – Additional Capital – Opening Capital

Closing Capital = Opening Capital + Additional Capital + Profits - Drawings

Closing Capital = 90,000 + 40,000 + 25,000 - 17,000

Closing Capital = Rs 1,38,000

Question 6.

Solution 6:

Working Note:-

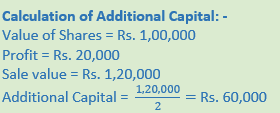

Investment value = Rs. 80,000

Loss on investment = Rs. 80,000 × 5% = Rs. 4,000

Selling value of investment = Rs. 80,000 – Rs. 4,000 = Rs. 76,000

Question 7.

Solution 7:

Working Note:-

Investment value = Rs. 10,000

Profit on investment = Rs. 10,000 × 5% = Rs. 500

Selling value of investment = Rs. 10,000 + Rs. 500 = Rs. 10,500

Question 8.

Solution 8:

Question 9.

Solution 9:

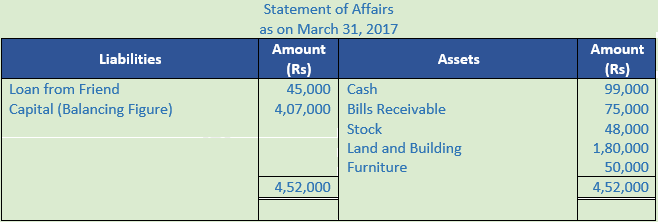

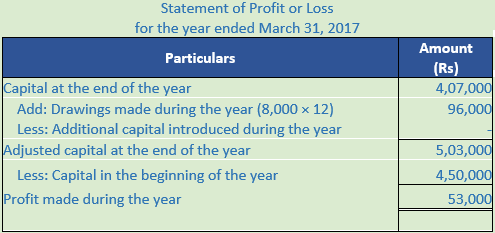

Question 10.

Solution 10:

Calculation of Drawings:-

Cash withdrawn = Rs. 8,000 × 12 = Rs. 96,000

Income tax paid = Rs. 20,000

Personal Loan instalment = Rs. 15,000 × 12 = Rs. 1,80,000

Total Drawings = Rs. 96,000 + Rs. 20,000 + Rs. 1,80,000 = Rs. 2,96,000

Question 11.

Solution 11:

Question 12.

Solution 12:

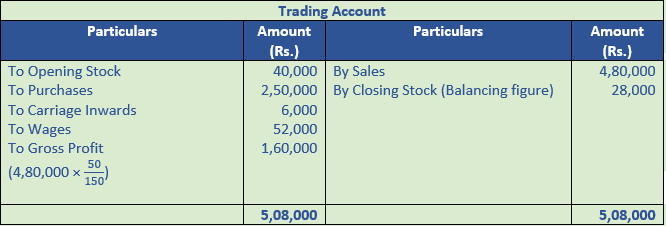

Question 13.

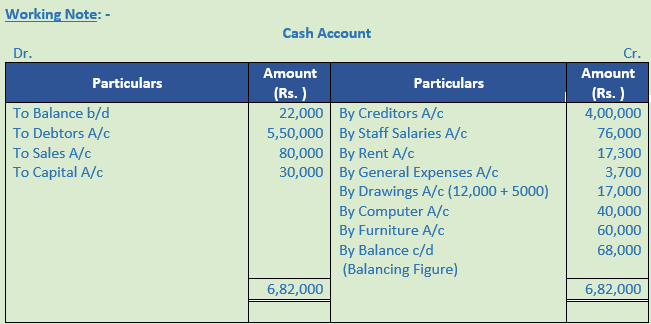

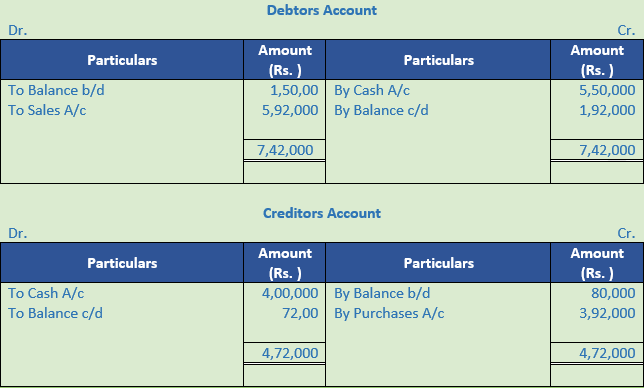

Solution 13:

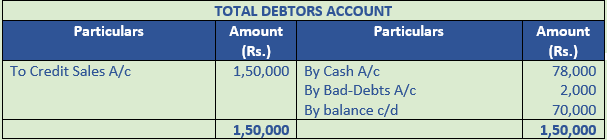

Working Note:-

Calculation of Total Sales:-

Total Cash = Cash Sales + Credit Sales

Total Cash = Rs. 1,05,000 + Rs. 3,80,00

Total Cash = Rs. 4,85,000

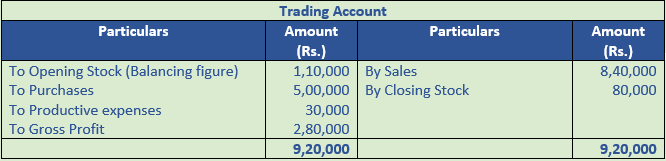

Question 14.

Solution 14:

Question 15.

Solution 15:

Question 16.

Solution 16:

Question 17.

Solution 17:

Question 18.

Solution 18:

Question 19.

Solution 19:

Question 20.

Solution 20:

Rate of Gross Profit (on cost) = 25%

Rate of Gross Profit (on sales) = 20%

Gross Profit = Rs. 1,20,000 × 20%

Gross Profit = Rs .24,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = Rs. 1,20,000 – Rs. 24,000

Cost of Goods Sold = Rs. 96,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

Closing Stock = Opening Stock + Purchases + Direct Expenses – Cost of Goods Sold

Closing Stock = Rs. 16,000 + Rs. 93,000 + Rs. 20,000 – Rs. 96,000

Closing Stock = Rs. 33,000

Question 21.

Solution 21:

Rate of Gross Profit (on sales) = 40%

Gross Profit = 40% × (2,05,000 – 5,000)

Gross Profit = 80,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales –Gross Profit

Cost of Goods Sold = Rs. 2,00,000 – Rs. 80,000

Cost of Goods Sold = Rs. 1,20,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

1,20,000 = Opening Stock + (Rs. 1,24,000 – Rs. 4,000) + Rs. 8,000 – Rs. 36,000

Opening Stock = Rs. 1,20,000 – Rs. 1,20,000 – Rs. 8,000 + Rs. 36,000

Opening Stock = Rs. 28,000

Question 22.

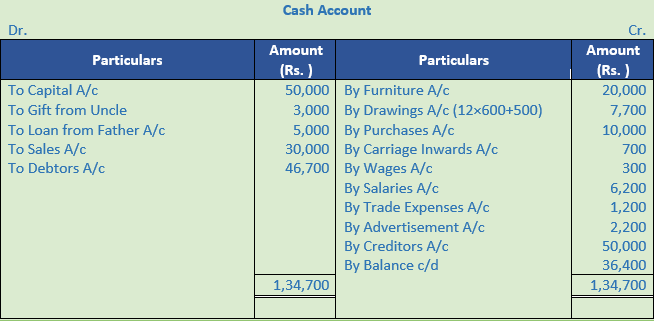

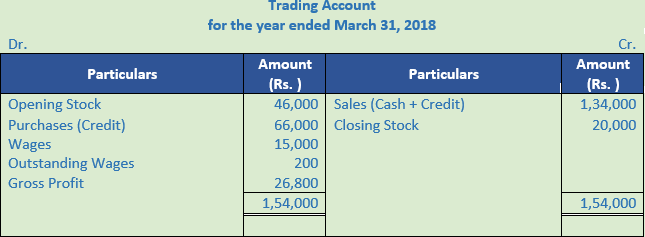

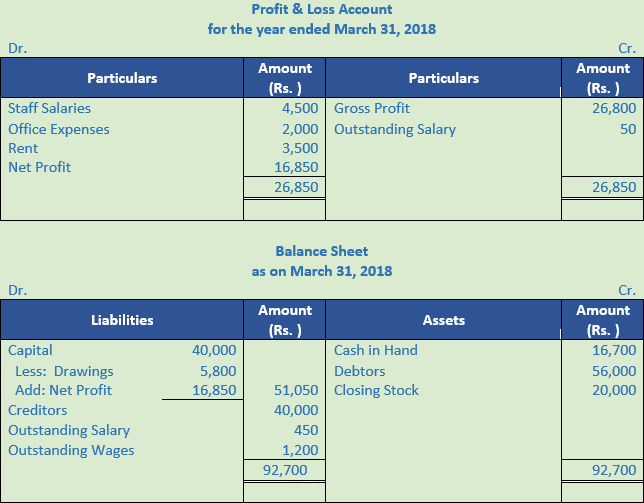

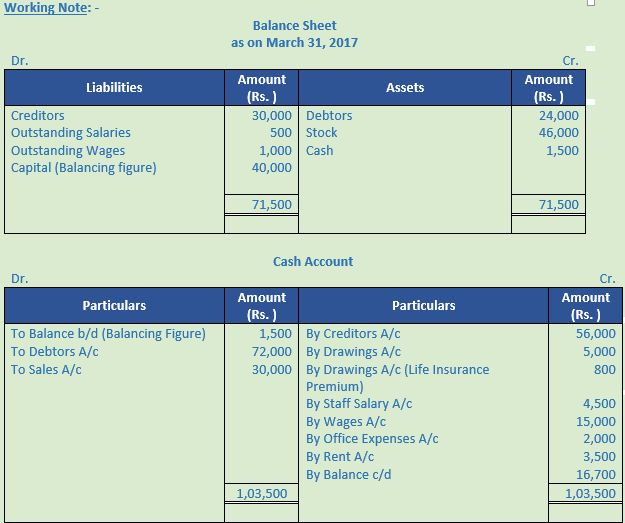

Solution 22:

Rate of Gross Profit (on cost) = 25%

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% of (30,000 + 1,04,000)

Gross Profit = 26,800

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = 1,34,000 – 26,800

Cost of Goods Sold = Rs. 1,07,200

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

1,07,200 = Opening Stock + 66,000 + (15,000 + 200) – 20,000

Opening Stock = 1,07,200 – 66,000 – 15,200 + 20,000

Opening Stock = Rs. 46,000

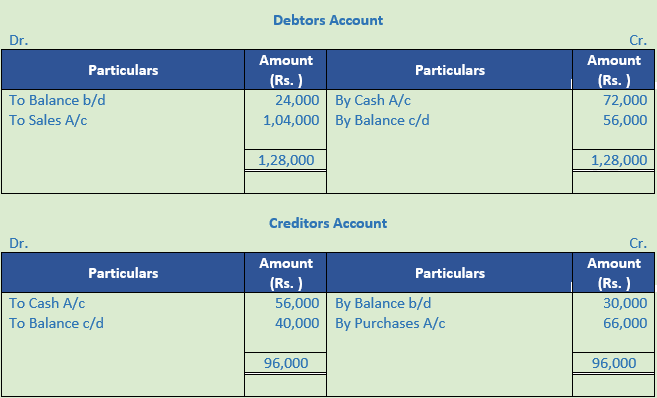

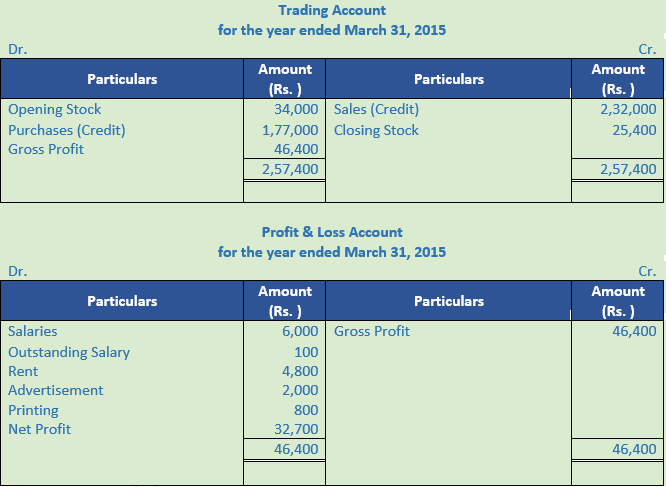

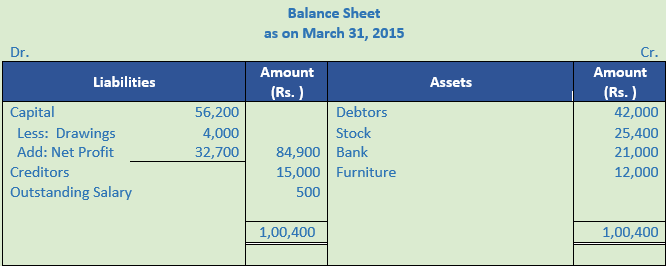

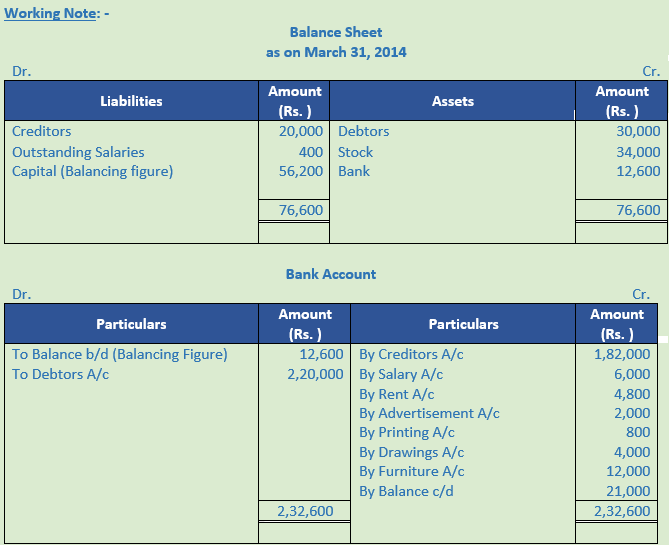

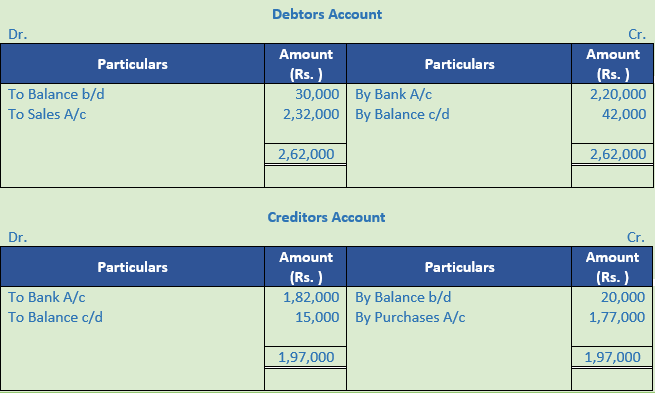

Question 23.

Solution 23:

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% × Rs. 2,32,000

Gross Profit = Rs. 46,400

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Gross Profit - Net Sales

Cost of Goods Sold = Rs. 2,32,000 – Rs. 46,400

Cost of Goods Sold = Rs. 1,85,600

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

1,85,600 = 34,000 + 1,77,000 – Closing Stock

Closing Stock = 34,000 + 1,77,000 – 1,85,600 = Rs. 25,400

Question 24.

Solution 24:

Question 25.

Solution 25:

Question 26.

Solution 26:

Question 27.

Solution 27:

Question 28.

Solution 28:

Question 29.

Solution 29:

Question 30.

Solution 30:

Question 31.

Solution 31:

Question 32.

Solution 32:

Working Note:-

Calculation of Amount of Drawings:-

Cash Withdrawn = Rs 18,000

Loan to Brother = Rs 8,000

Rent = Rs 10,800

Electricity Charges = Rs 3,000

Total Drawings = Rs 39,800

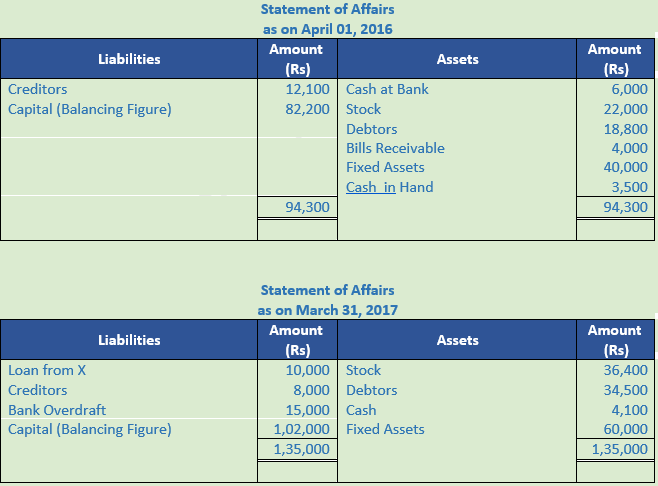

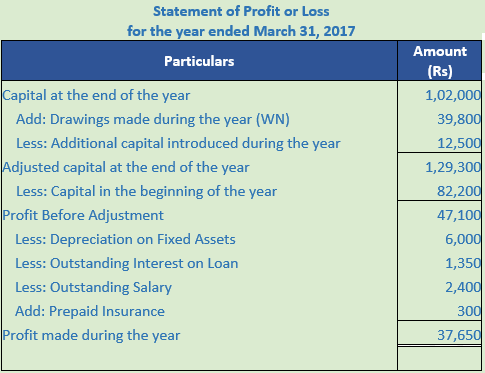

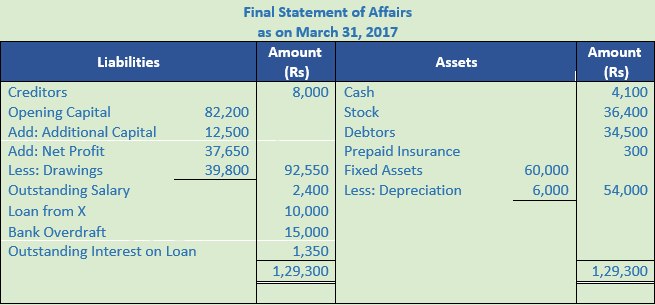

Question 33.

Solution 33:

Question 34.

Solution 34:

Question 35.

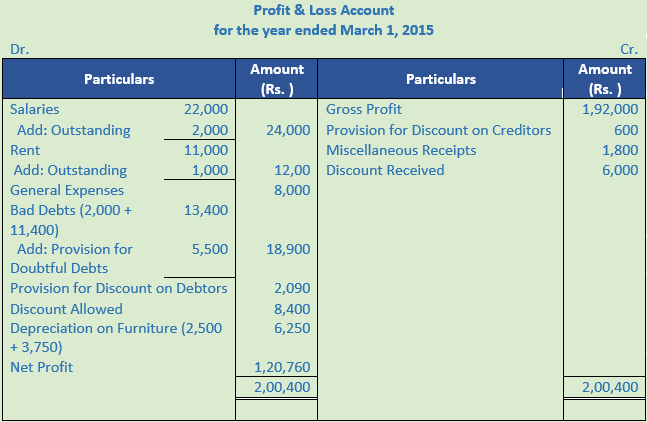

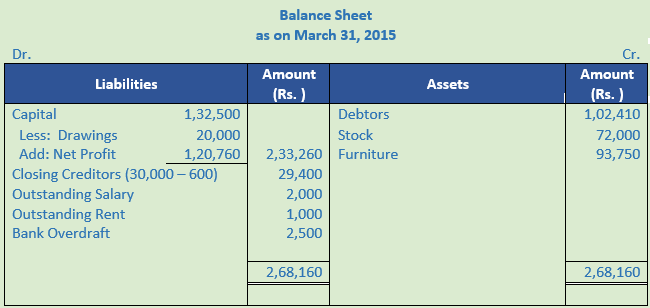

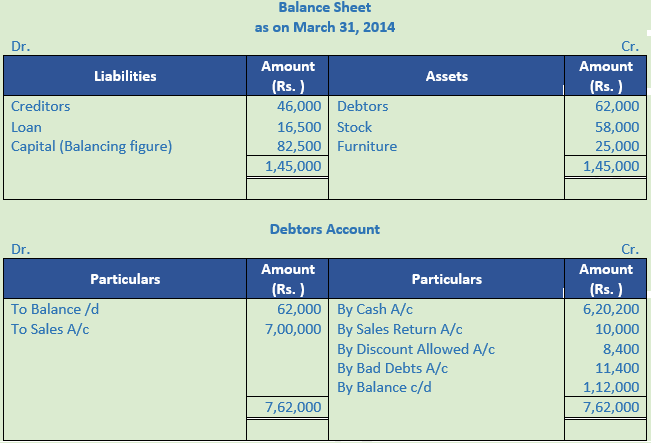

Solution 35:

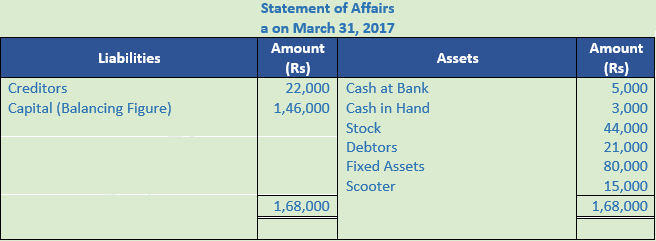

Working Note:-

Calculation of Capital = 82,500 + 50,000 – 20,000 + 1,20,760 = 2,33,260

Calculation of Debtors = 1,12,000 – 2,000 –5,500 – 2,090 = 1,02,410

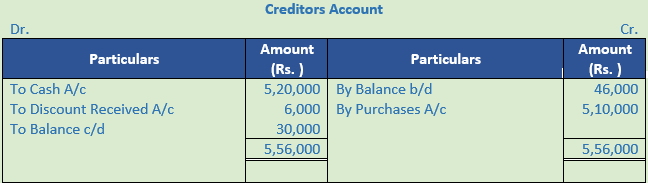

Calculation of Closing Creditors = 30,000 – 600 = 29,400

Calculation of Furniture = 25,000 + 75,000 – 6,250 = 93,750

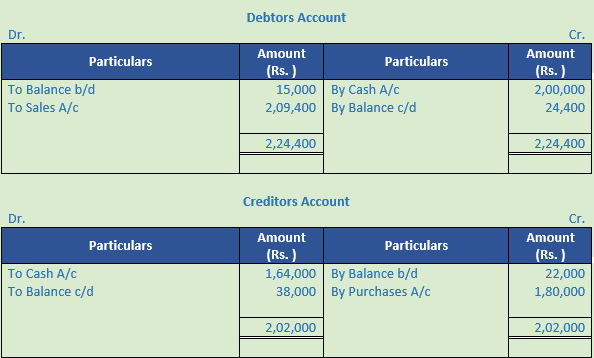

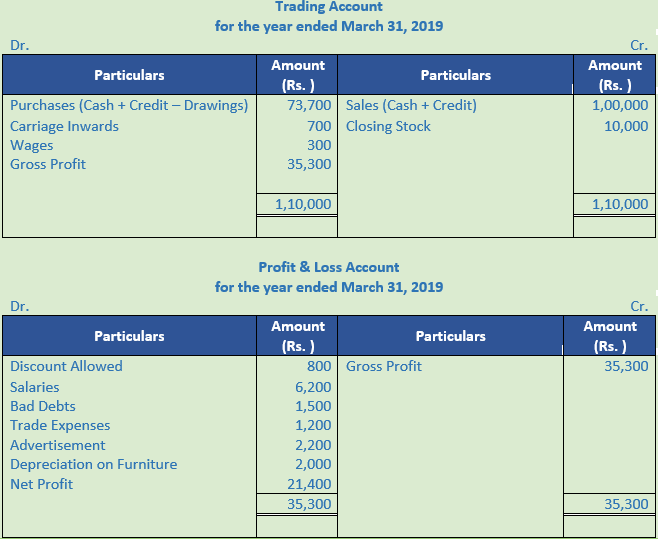

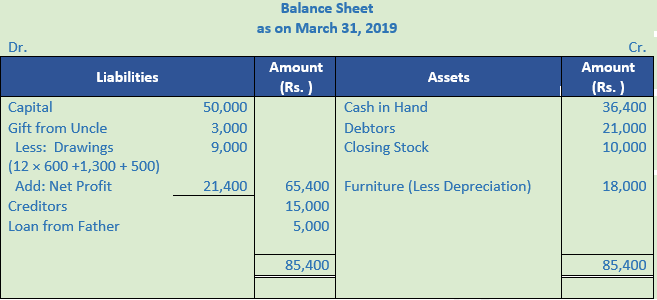

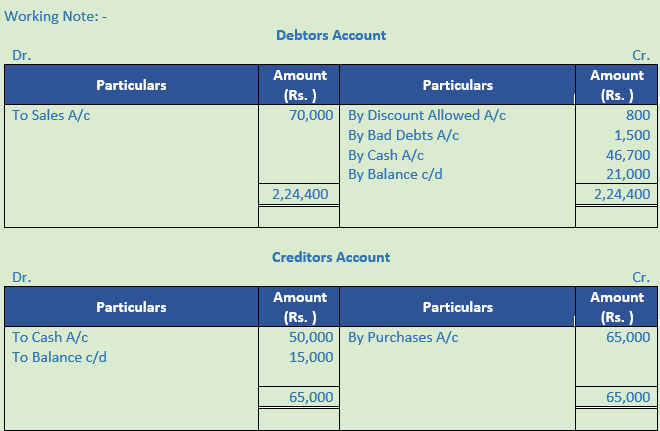

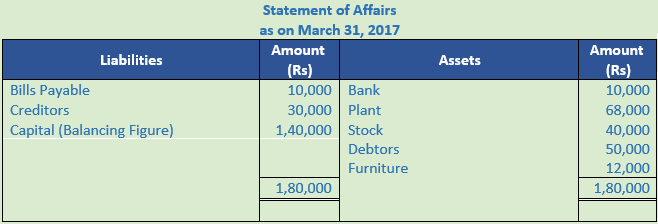

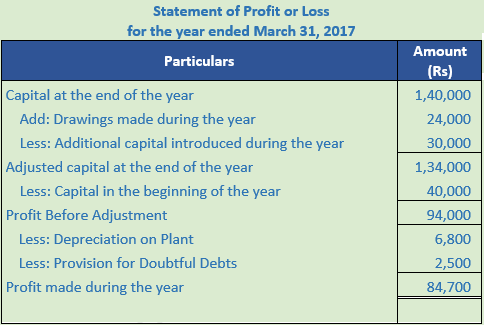

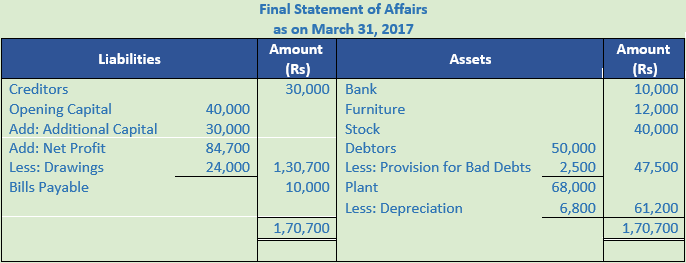

Question 36.

Solution 36:

Question 37.

Solution 37:

Question 38.

Solution 38:

Rate of Gross Profit (on cost) = 25%

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% × 1,00,000 = 20,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales - Gross Profit

Cost of Goods Sold = 1,00,000 – 20,000

Cost of Goods Sold = Rs. 80,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

80,000 = 18,000 + 69,000 + 10,000 – Closing Stock

Closing Stock = 18,000 + 69,000 + 10,000 – 80,000 = Rs. 17,000

Question 39.

Solution 39:

Rate of Gross Profit (on cost) = 50%

Rate of Gross Profit (on sales) = 33.33%

Gross Profit = 33.33% × 1,05,000 = 35,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales - Gross Profit

Cost of Goods Sold = 1,05,000 – 35,000

Cost of Goods Sold = Rs. 70,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

70,000 = Opening Stock + 60,000 + 3,000 – 20,000

Opening Stock = 70,000 – 60,000 – 3,000 + 20,000 = Rs. 27,000

Question 40.

Solution 40:

Rate of Gross Profit (on sales) = 20%

Gross Profit = 20% × 90,000

Gross Profit = 18,000

Gross Profit = Net Sales – Cost of Goods Sold

Cost of Goods Sold = Net Sales – Gross Profit

Cost of Goods Sold = 90,000 – 18,000

Cost of Goods Sold = Rs. 72,000

Cost of Goods Sold = Opening Stock + Purchases + Direct Expenses – Closing Stock

72,000 = 20,000 + 69,500 + 2,000 – Closing Stock

Closing Stock = 20,000 + 69,500 + 2,000 – 72,000 = Rs. 19,500

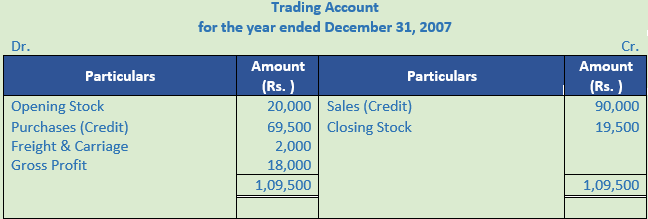

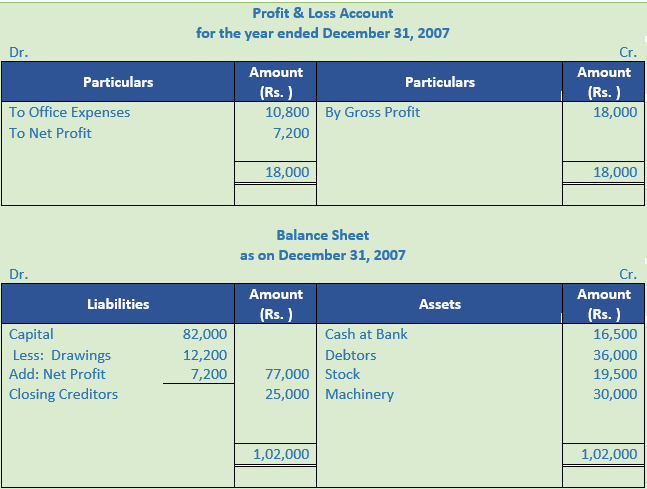

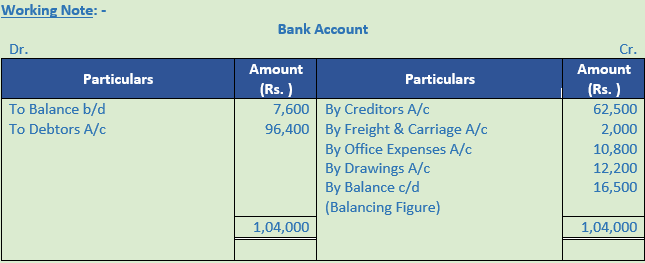

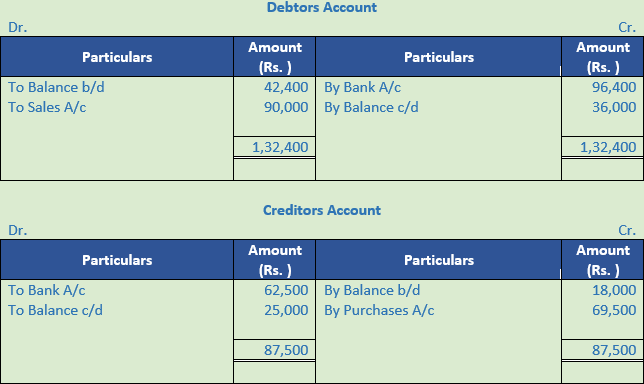

Question 41.

Solution 41: