Access free DK Goel Solutions Class 11 Accountancy Chapter 22 Financial Statements With Adjustments 2026 below. Students can now access free DK Goel Solutions for Class 11 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 11 Math Chapter 22 Financial Statements With Adjustments DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 22 Financial Statements With Adjustments Class 11 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 22 Financial Statements With Adjustments DK Goel Class 11 Solved Exercises

Short Answer Questions

Question 1.

Solution 1: Necessity of doing adjustments:

- To ascertain the true net Profit or loss of the business.

- To ascertain the true financial position of the business.

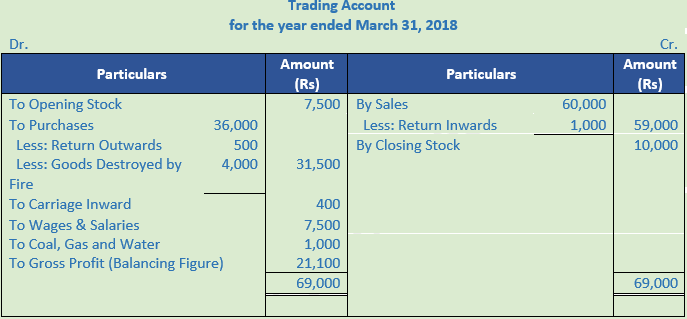

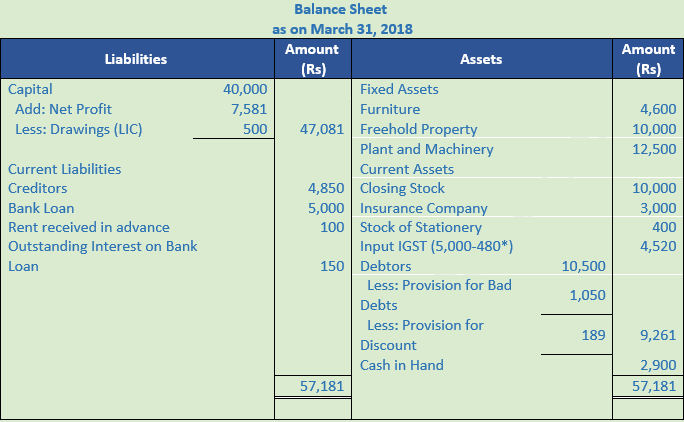

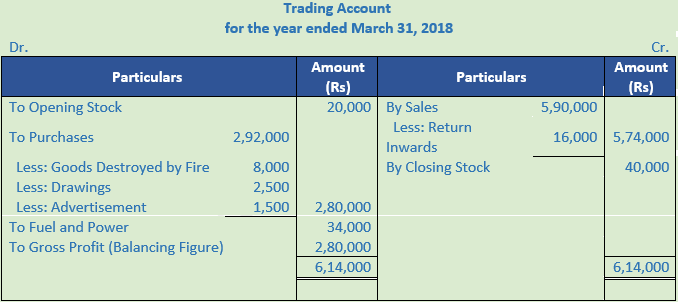

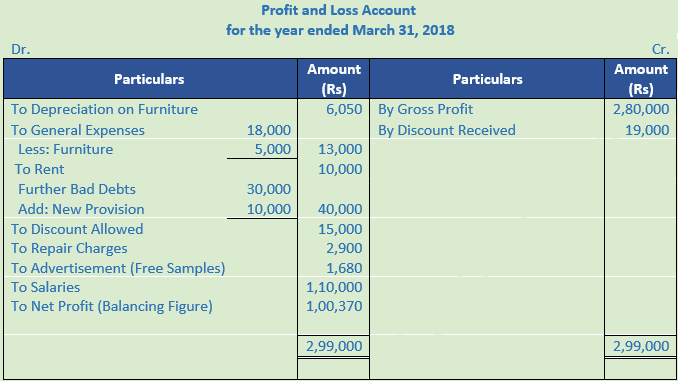

- To make a record of the transaction omitted from the books.

Question 2.

Solution 2: The term provision should be used instead of reserve because the aim is not to strengthen the financial position of the business but to cover an expected future loss.

Question 3.

Solution 3:

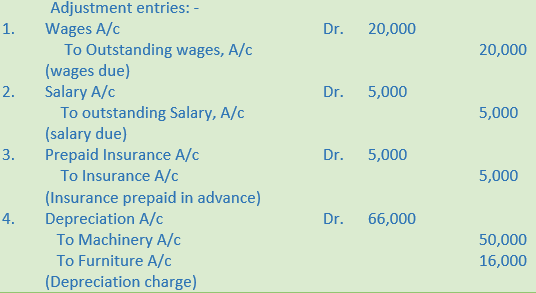

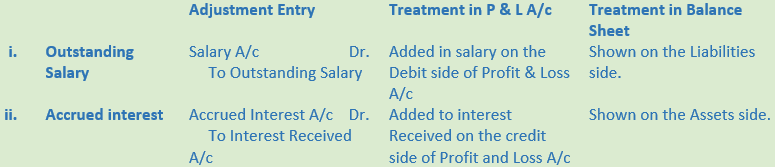

These are the expenses which have been incurred during the year but have been left unpaid on the date of preparation of final accounts.

Question 4.

Solution 4:

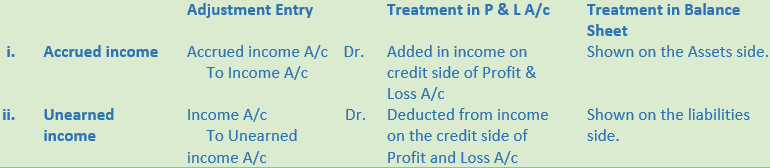

- Accrued Income: It is quite common that certain items of income such as interest on securities, commission, rent etc., are earned during the current year but have not been actually received by the end of the current year. Such incomes are known as accrued income.

- Unearned Income: Certain income is received in the current year but the whole amount of it does not belong to the current year. Such portion of this income which belongs to the next year is known as unearned income.

- Provision for doubtful debts: such a provision is created at a fixed percentage on debtors every year and is called ‘provision for bad and doubtful debts’.

Question 5.

Solution 5:

1) Capital Expenditure: If benefit of expenditure is received for more than one year, it is called capital expenditure. Example: Purchase of Machinery.

2) Revenue Expenditure: It is the amount spent to purchase goods and services that are used during an accounting period is called revenue expenditure. For Example: Rent, interest, etc.

3) Deferred Revenue Expenditure: There are certain expenditures which are revenue in nature but benefit of which is derived over number of years. For Example: Huge Advertisement Expenditure.

Question 6.

Solution 6:

- Purchase of machinery.

- Expenditure on installation of machinery.

Question 7.

Solution 7:

1) Capital Expenditure: If benefit of expenditure is received for more than one year, it is called capital expenditure. Example: Purchase of Machinery.

2) Revenue Expenditure: It is the amount spent to purchase goods and services that are used during an accounting period is called revenue expenditure. For Example: Rent, interest, etc.

Question 8.

Solution 8:

- Assets

- of P & L A/c

- Assets

- of P & L A/c

Question 9.

Solution 9:

Question 10.

Solution 10:

Practical Questions

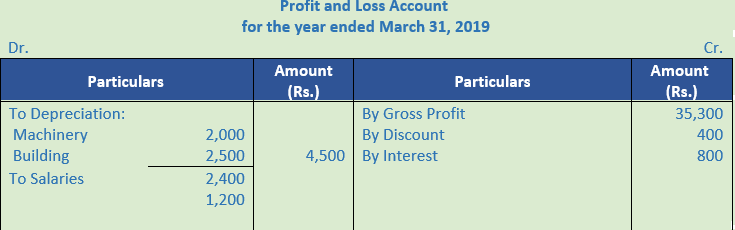

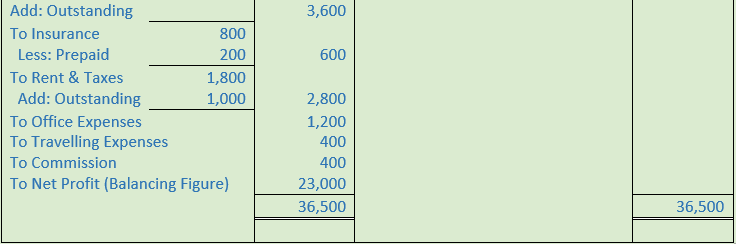

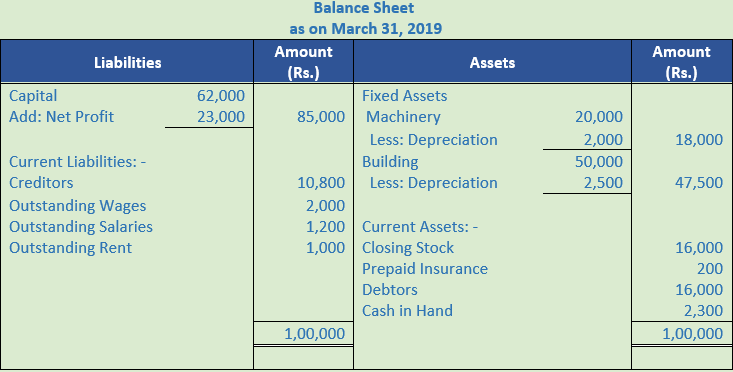

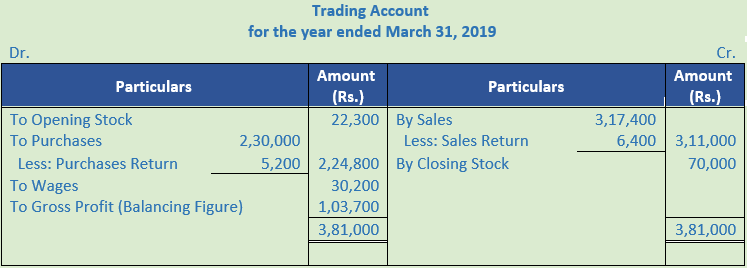

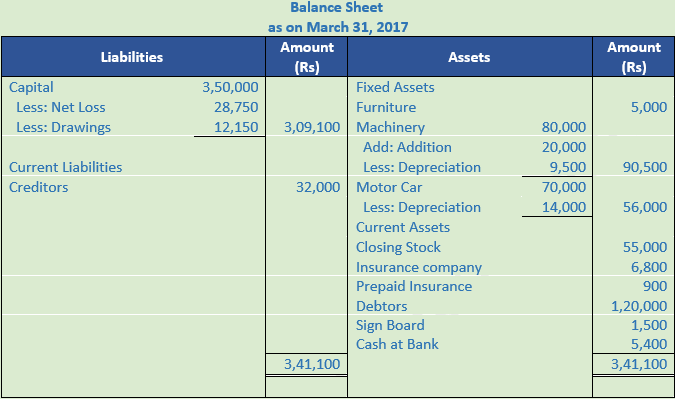

Question 1.

Solution 1:

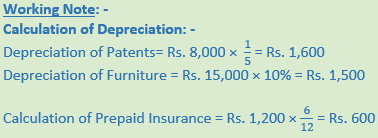

Working Note:-

Calculation of Depreciation:-

Depreciation on Building = Rs. 50,000 × 5%

Depreciation on Building = Rs. 2,500

Depreciation on Machinery = Rs. 20,000 × 10%

Depreciation on Machinery = Rs. 2,000

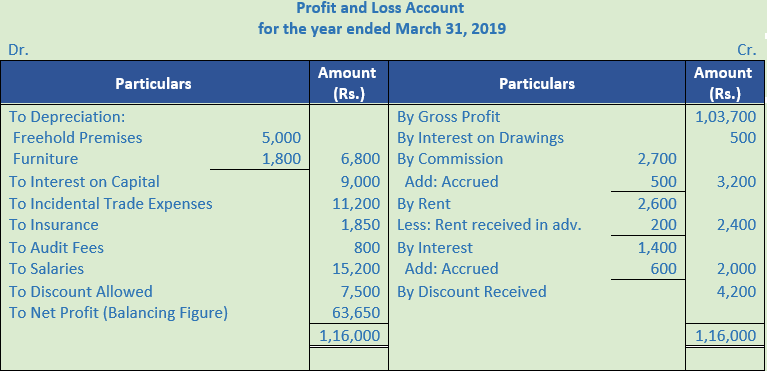

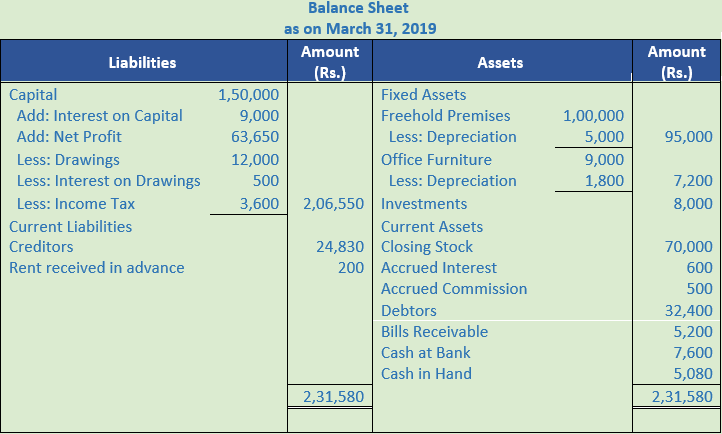

Question 2.

Solution 2:

Working Note:-

Calculation of Depreciation:-

Depreciation on Freehold Premises = Rs. 1,00,000 × 5%

Depreciation on Freehold Premises = Rs. 5,000

Depreciation on Office Furniture = Rs. 9,000 × 20%

Depreciation on Office Furniture = Rs. 1,800

Calculation of Interest on Capital:-

1,50,000 × 6% = Rs. 9,000

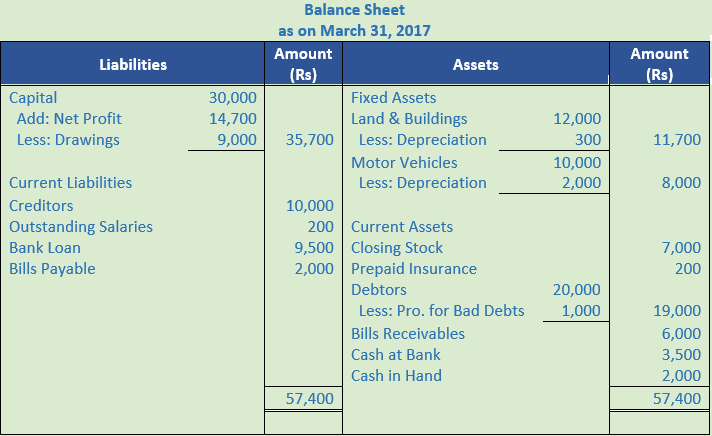

Question 3.

Solution 3:

Working Note:-

Calculation of Depreciation:-

Depreciation on Land & Building = Rs. 12,000 × 2.5%

Depreciation on Land & Building = Rs. 300

Depreciation on Motor Vehicles = Rs. 10,000 × 20%

Depreciation on Motor Vehicles = Rs. 2,000

Calculation of Interest on Capital:-

20,000 × 5% = Rs. 1,000

Calculation of Drawings:-

Rs. 5,000 + Rs. 4,000 = Rs. 9,000

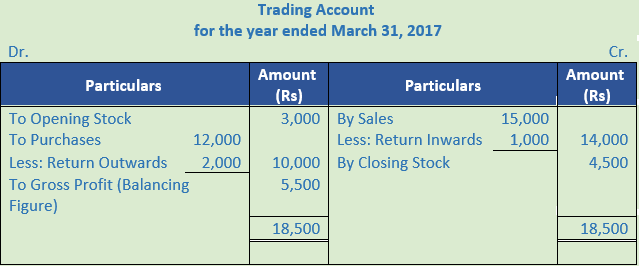

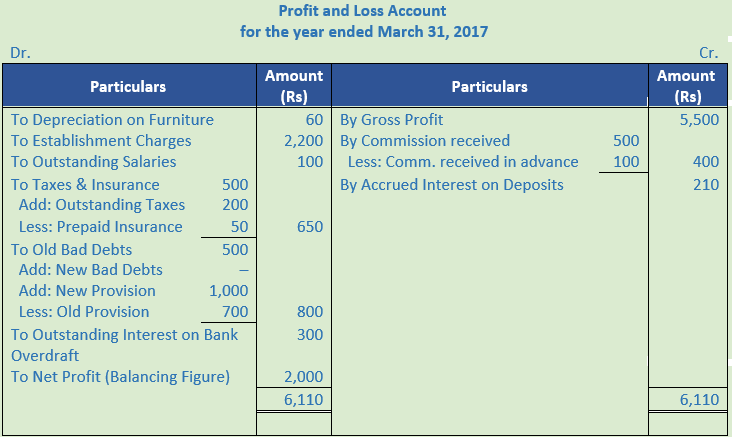

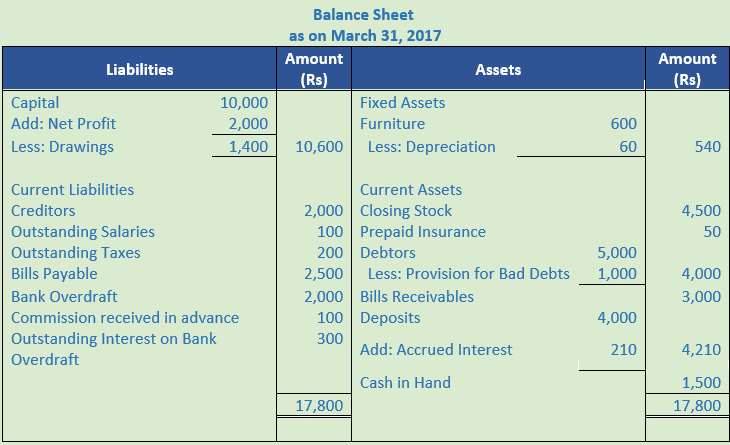

Question 4.

Solution 4:

Working Note:-

Calculation of Depreciation:-

Depreciation on Furniture = Rs. 600 × 10%

Depreciation on Furniture = Rs. 60

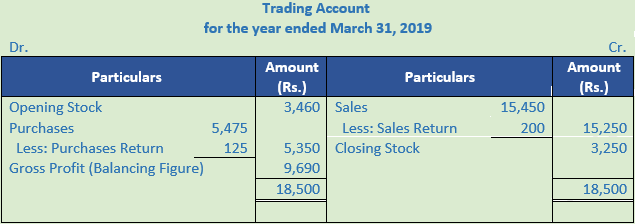

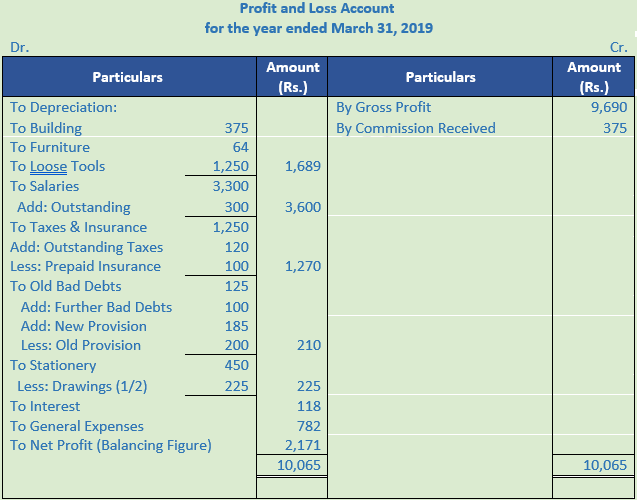

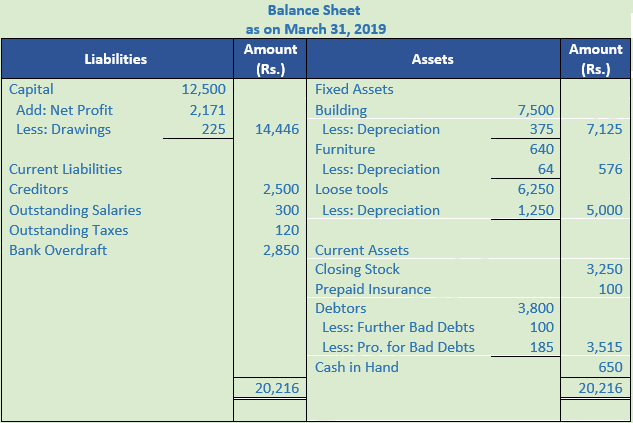

Question 5.

Solution 5:

Working Note:-

Calculation of Depreciation:-

Depreciation on Building = 7,500 × 5% = Rs. 375

Depreciation on Furniture = 640 × 10% = Rs. 64

Depreciation on Patents = Rs. 6,250 – Rs. 5,000 = Rs. 1,250

Calculation of Doubtful Debts:-

Provision for Doubtful Debts = Sundry Debtors – Bad Debts on Furniture × Rate of Provision

Provision for Doubtful Debts = (3,800 – 100) × 5%

Provision for Doubtful Debts = 3,700 × 5%

Provision for Doubtful Debts = Rs. 185

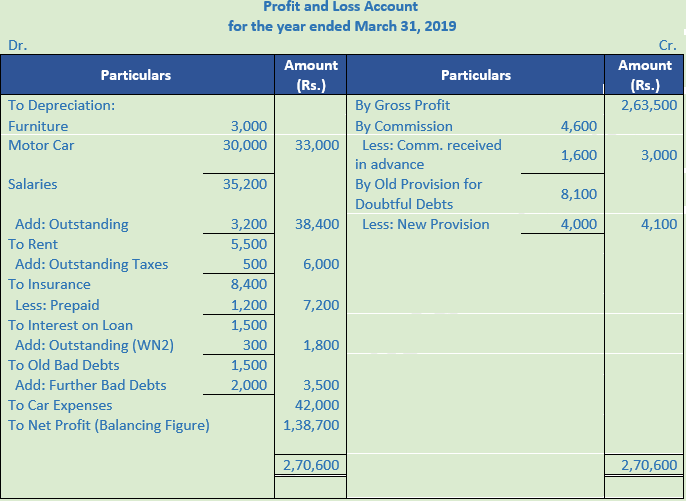

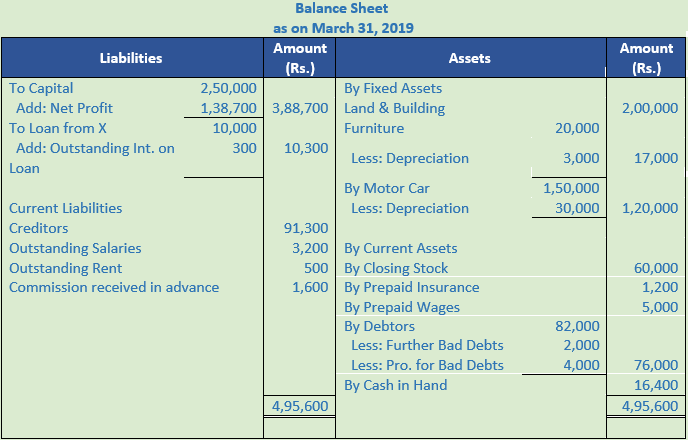

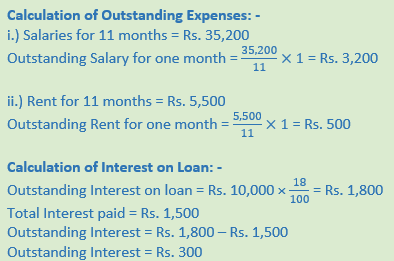

Question 6.

Solution 6:

Working Note:-

Calculation of Depreciation:-

Depreciation on Furniture = 20,000 × 15% = Rs. 3,000

Depreciation on Motor Car = 1,50,000 × 20% = Rs. 30,000

Calculation of Provision for Doubtful Debts:-

Provision Doubtful Debts = Sundry Debtors – Further Bad Debts × Rate

Provision Doubtful Debts = 82,000 – 2,000 × 5%

Provision Doubtful Debts = Rs. 4,000

Question 7.

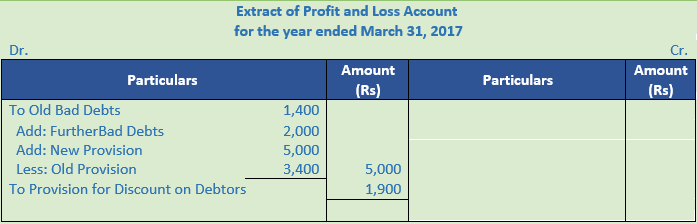

Solution 7:

Working Note:-

Calculation of Provision for Doubtful Debts:-

Provision Doubtful Debts = Sundry Debtors – Further Bad Debts × Rate

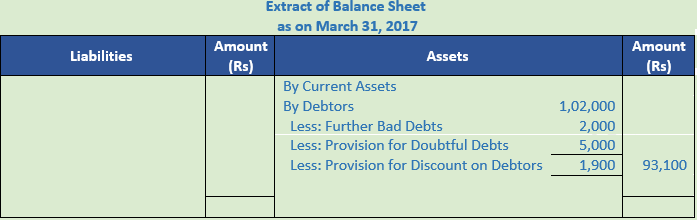

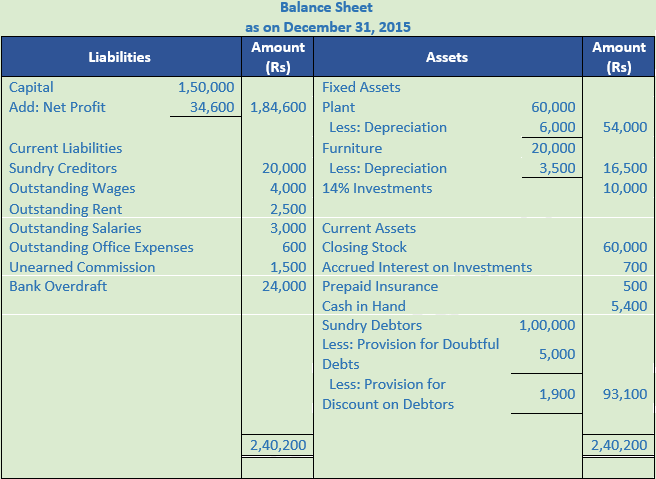

Provision Doubtful Debts = 1,02,000 – 2,000 × 5%

Provision Doubtful Debts = Rs. 5,000

Calculation of Provision for Discount on Debtors:-

Provision for Discount on Debtors = Debtors – Further Bad Debts – Provision for Doubtful Debts × Rate

Provision for Discount on Debtors = 1,02,000 – 2,000 – 5,000 × 2%

Provision for Discount on Debtors = Rs. 1,900

Question 8.

Solution 8:

Working Note:-

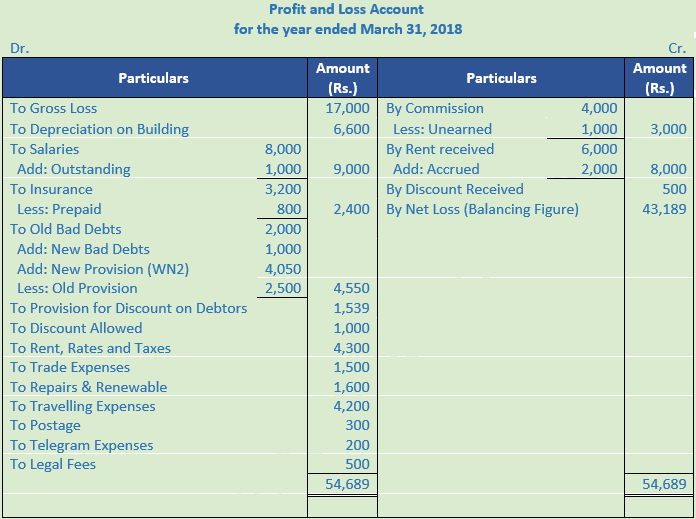

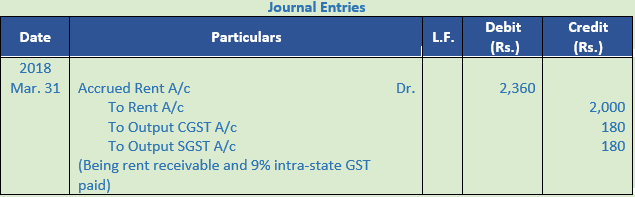

Adjustment Entry of Accrued Rent:-

Calculation of Depreciation:-

Depreciation on Building = Rs. 1,10,000 × 6% = Rs. 6,600

Calculation of Provision for Doubtful debts:-

Provision for doubtful debts = Debtors – Further Bad debts × Rate

Provision for doubtful debts = Rs. 82,000 – Rs. 1,000 × 5%

Provision for doubtful debts = Rs. 81,000 × 5%

Provision for doubtful debts = Rs. 4,050

Calculation of Provision for Discount on Debtors:-

Provision for Discount on Debtors = Debtors – Further Bad Debts – Provision for Doubtful Debts × Rate

Provision for Discount on Debtors = 82,000 – 1,000 – 4,050 × 2%

Provision for Discount on Debtors = Rs. 1,539

Question 9.

Solution 9:

Working Note:-

Calculation of Outstanding Interest On bank loan:-

Interest on Bank Loan = Rs. 5,000 × 12% = Rs. 600

Interest charged by bank = Rs. 450

Outstanding Interest = Rs. 600 – Rs. 450 = Rs. 150

Calculation of Provision for Doubtful debts:-

Provision for doubtful debts = Sundry Debtors × Rate

Provision for doubtful debts = Rs. 10,500 × 10%

Provision for doubtful debts = Rs. 1,050

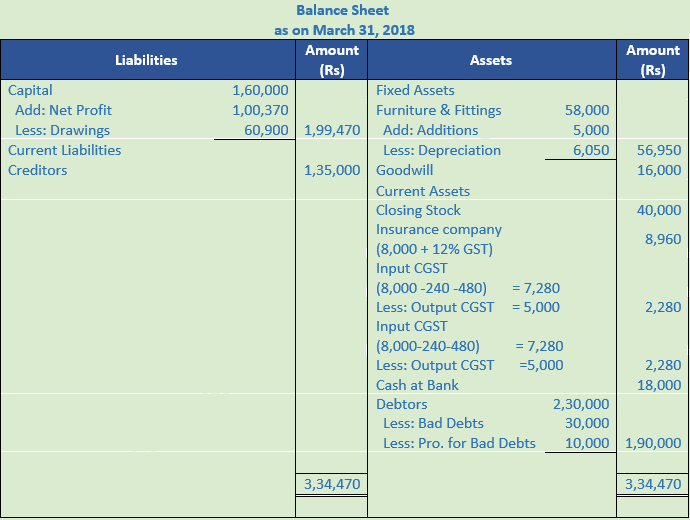

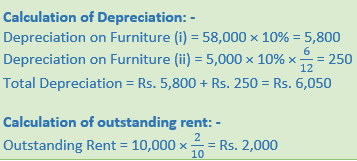

Question 10. (A)

Solution 10 (A)

Working Note:-

Calculation of Drawings = Rs. 58,100 + Rs. 2,800 = Rs. 60,900

Calculation of Provision for Doubtful debts:-

Provision for doubtful debts = Sundry Debtors – further Bad debts × Rate

Provision for doubtful debts = (Rs. 2,30,000 – Rs. 30,000) × 5%

Provision for doubtful debts = Rs. 10,000

Question 10. (B)

Solution 10 (B):

Question 11.

Solution 11:

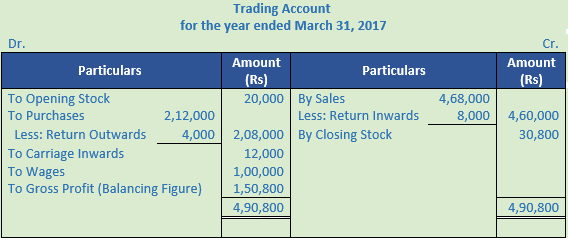

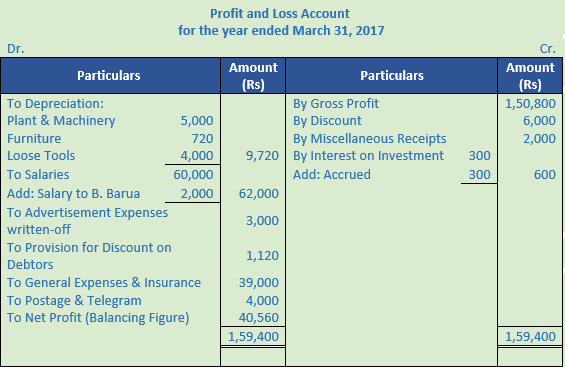

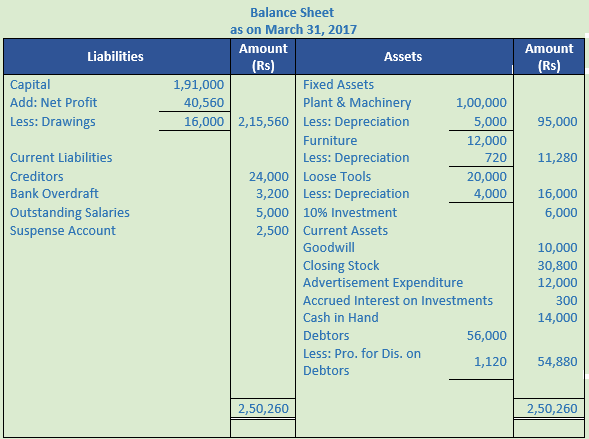

Question 12.

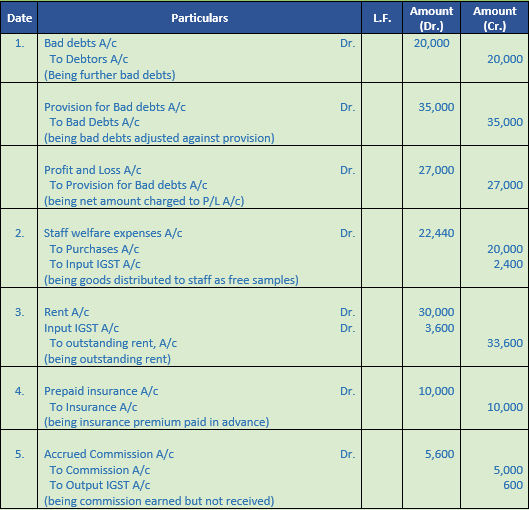

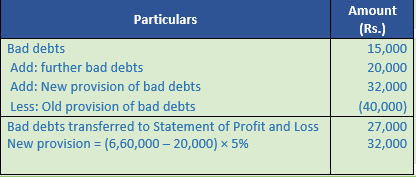

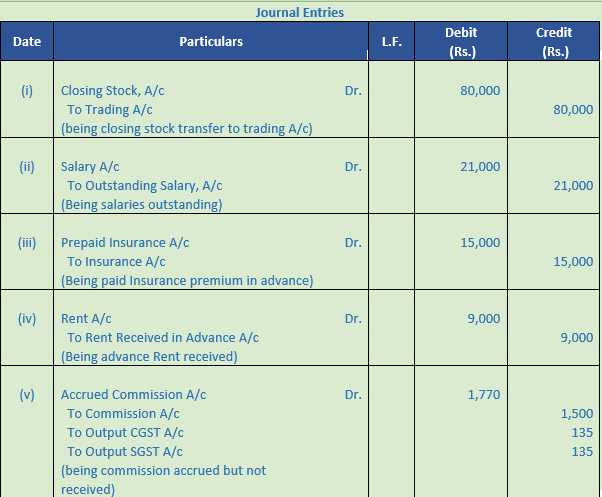

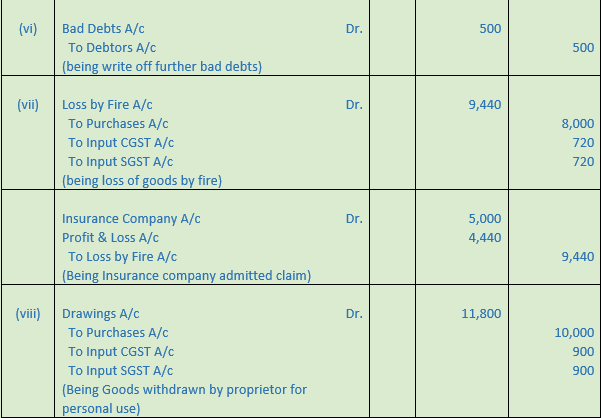

Solution 12:

Working Note:-

Calculation of bad debts

Question 13.

Solution 13:

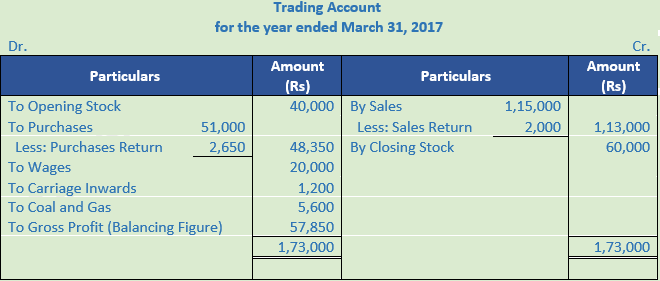

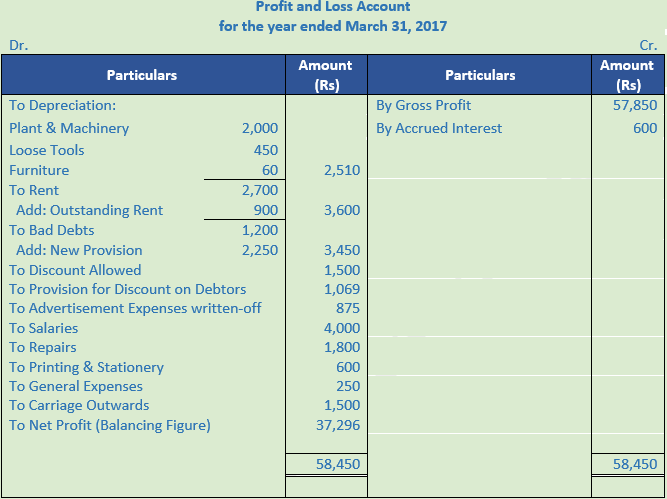

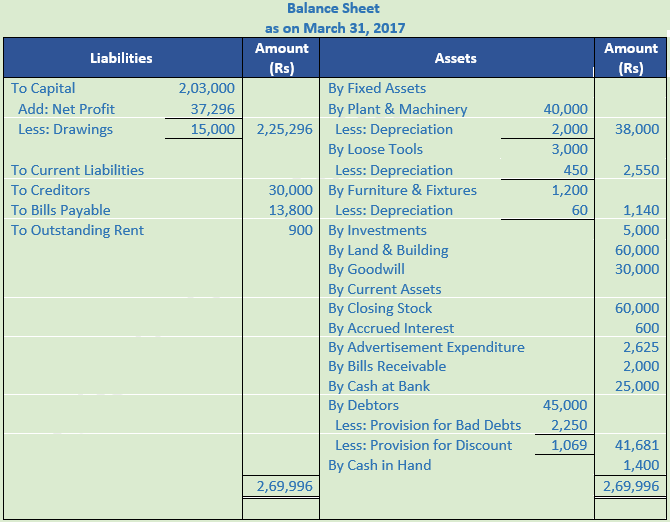

Question 14.

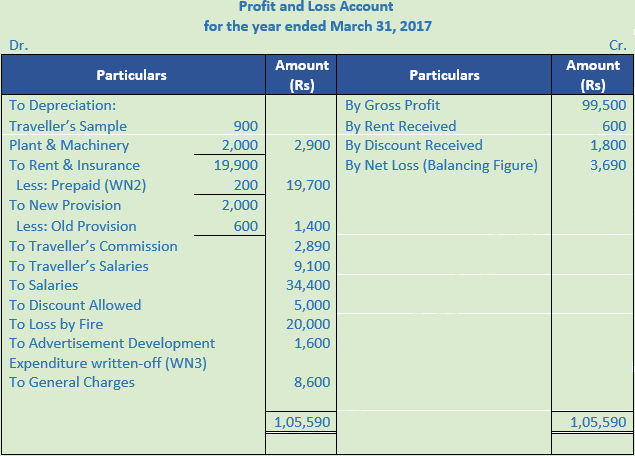

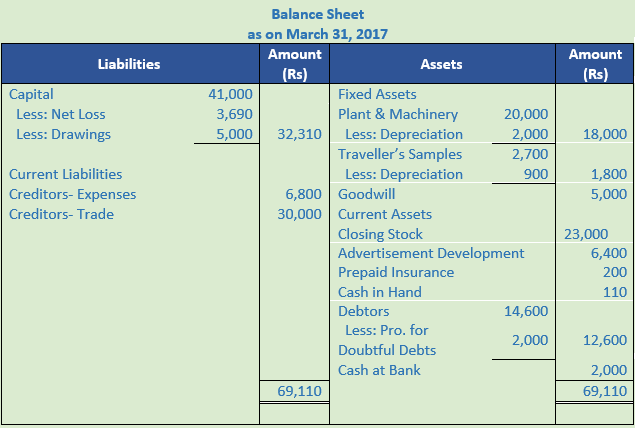

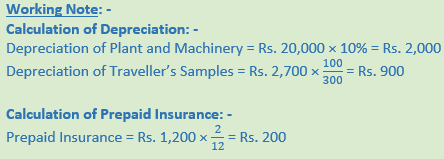

Solution 14:

Working Note:-

Calculation of Depreciation:-

Depreciation of Plant and Machinery = Rs. 40,000 × 5% = Rs. 2,000

Depreciation of Furniture and Fixtures = Rs. 1,200 × 5% = Rs. 60

Depreciation on Loose tools = Rs. 3,000 × 15% = Rs. 450

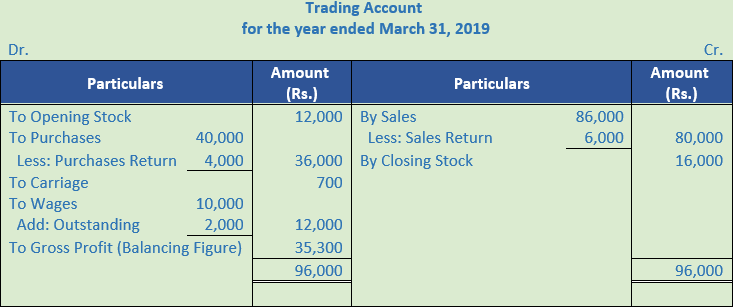

Calculation of Outstanding Rent:-

Rent paid for 3 quarters = Rs. 2,700

Rent for a quarter = 2700/3 = Rs. 900

Calculation of Provision for Doubtful debts:-

Provision for doubtful debts = Sundry Debtors × Rate

Provision for doubtful debts = Rs. 45,000 × 5%

Provision for doubtful debts = Rs. 2,250

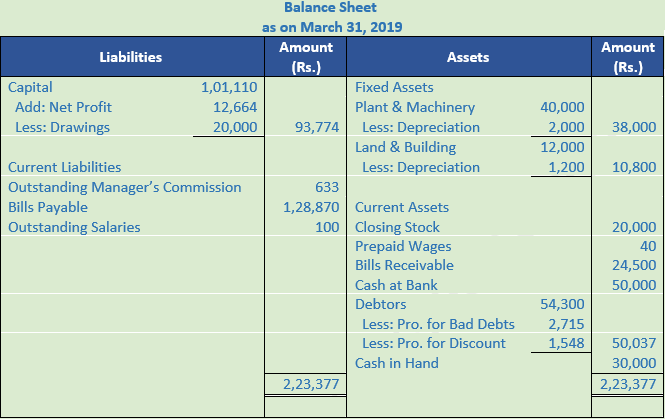

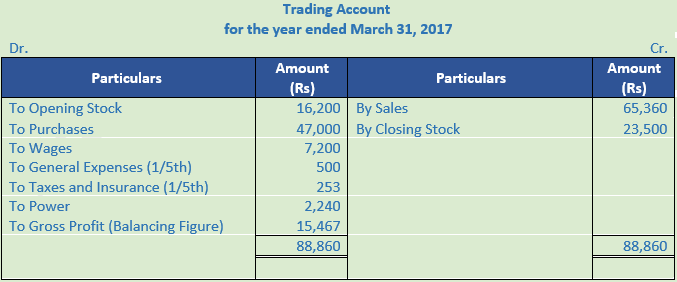

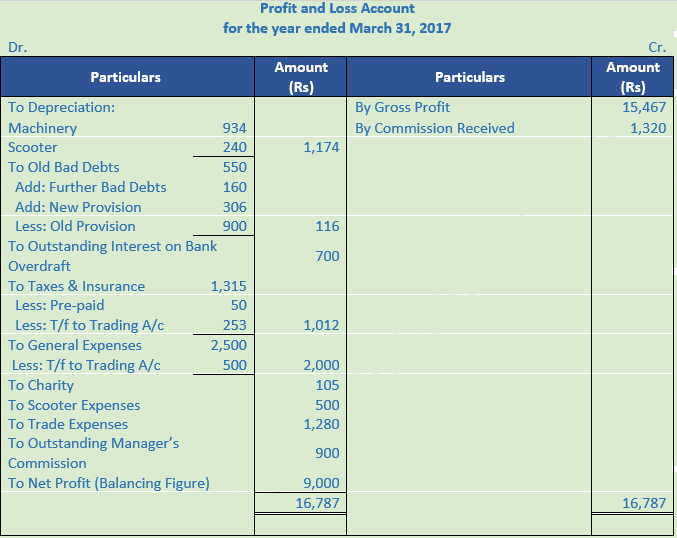

Question 15.

Solution 15:

Working Note:-

Calculation of Depreciation:-

Depreciation of Plant and Machinery = Rs. 40,000 × 5% = Rs. 2,000

Depreciation of Building = Rs. 12,000 × 10% = Rs. 1,200

Calculation of Provision for Doubtful debts:-

Provision for doubtful debts = Sundry Debtors × Rate

Provision for doubtful debts = Rs. 54,300 × 5%

Provision for doubtful debts = Rs. 2,715

Calculation of Provision for Discount on Debtors:-

Provision for doubtful debts = Sundry Debtors – Provision for bad debts × Rate

Provision for doubtful debts = (Rs. 54,300 – Rs. 2,715) × 3%

Provision for doubtful debts = Rs. 1,548

Question 16.

Solution 16:

Working Note:-

Calculation of Depreciation:-

Depreciation of Machinery = Rs. 9,340 × 10% = Rs. 934

Calculation of Provision for Doubtful debts:-:-

Provision for doubtful debts = Sundry Debtors – Provision for bad debts × Rate

Provision for doubtful debts = (Rs. 6,280 – Rs. 160) × 5%

Provision for doubtful debts = Rs. 306

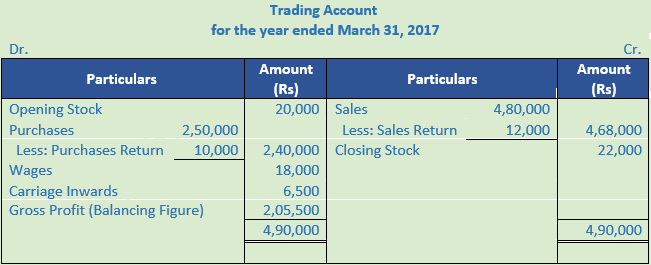

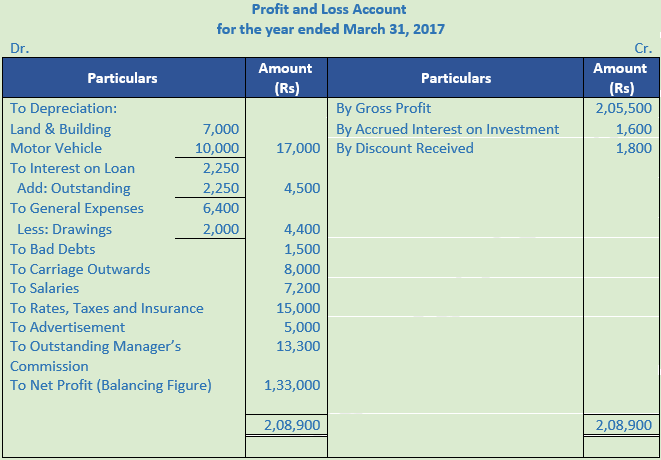

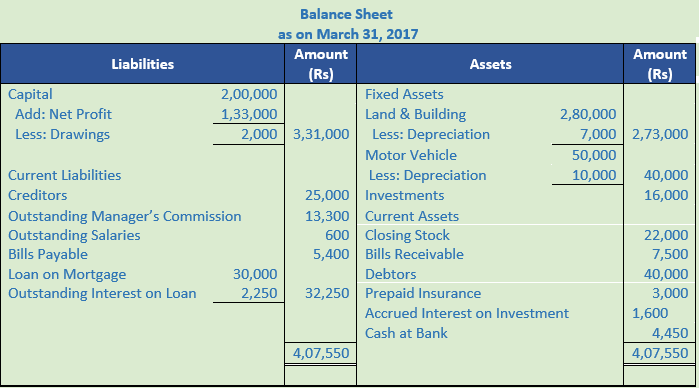

Question 17. (A)

Solution 17 (A):

Working Note:-

Calculation of Depreciation:-

Depreciation of Land and Building = Rs. 2,80,000 × 2.5% = Rs. 7,000

Depreciation of Motor Vehicle = Rs. 50,000 × 20% = Rs. 10,000

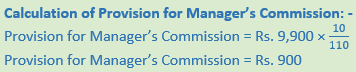

Calculation of Provision for Manager’s Commission:-

Provision for Manager’s Commission = Rs. 2,08,900 – Rs. 62,600

Provision for Manager’s Commission = Rs. 1,46,300

Provision for Manager’s Commission = Rs. 1,46,300 × 10% = Rs. 13,300

Question 17. (B)

Solution 17 (B):

Point of knowledge:-

In the event of loss managers are not entitled to get and commission.

Question 18.

Solution 18:

- Capital Expenditure

Reason: Purchases of machinery is a capital expenditure all expenses related to machinery on the purchasing date is treated as capital expenditure.

- Capital Expenditure

Reason: Whitewashing on the new building will increase the revenue generating capacity of the building, thus, it will be capitalised and treated as capital expenditure.

- Revenue Expenditure

Reason: Annual insurance premium is a recurring expenditure to carry on day-to-day business activities. Thus, it is a revenue expense.

- Capital Expenditure

Reason: To enhance the working capacity of the assets if any expenditure is incurred once in a while, then it will be treated as capital expenditure. So, the expenses made on repairing of second hand machinery will be capitalised and treated as capital expenditure.

- Revenue Expenditure

Reason: The expenditure on repairing of machinery will help to raise the working capacity of the machinery, so it is revenue expenditure.

- Capital Expenditure

Reason:

To enhance the working capacity of the assets if any expenditure is incurred once in a while, then it will be treated as capital expenditure. So, the expenses made on air conditioner will be treated as capital expenditure.

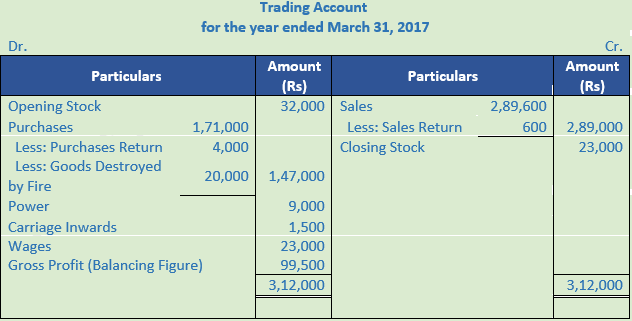

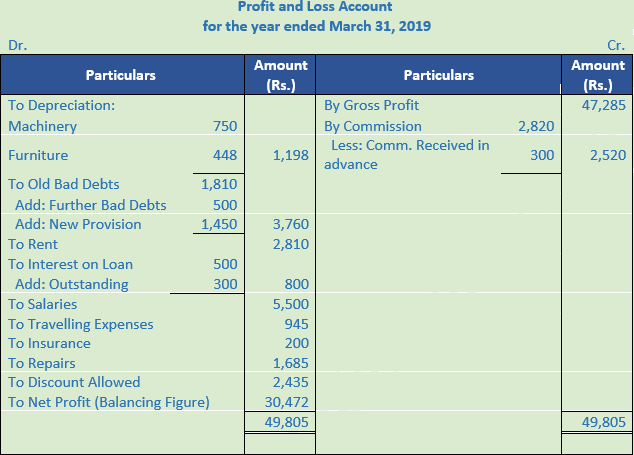

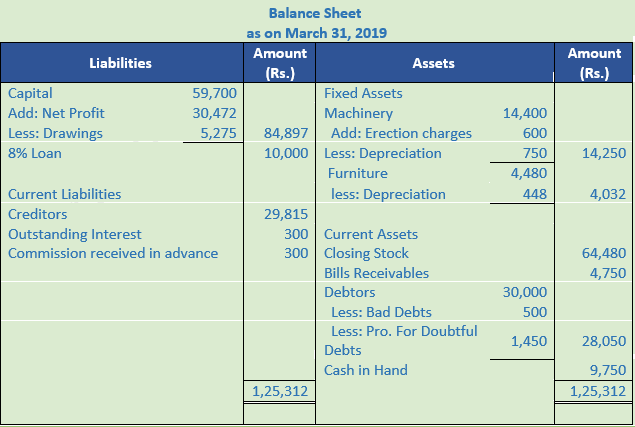

Question 19.

Solution 19:

Working Note:-

Calculation of Depreciation:-

Depreciation of Machinery = Rs. 14,400 + Rs. 600 × 5% = Rs. 750

Calculation of Provision for Doubtful debts:-:-

Provision for doubtful debts = Sundry Debtors – Further Bad debts – Amount recovered × Rate

Provision for doubtful debts = (Rs. 30,000 – Rs. 500 - Rs. 500) × 5%

Provision for doubtful debts = Rs. 1,450

Question 20.

Solution 20:

Working Note:-

Calculation of Provision for Doubtful debts:-:-

Provision for doubtful debts = Sundry Debtors – Further Bad debts – Amount recovered × Rate

Provision for doubtful debts = (Rs. 4,80,000 – Rs. 15,000 - Rs. 5,000) × 6%

Provision for doubtful debts = Rs. 27,600

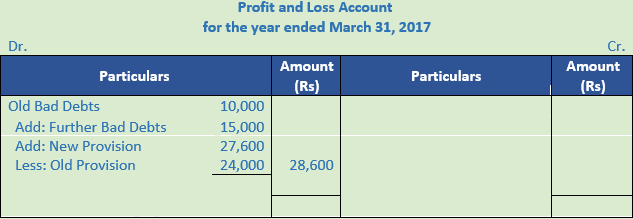

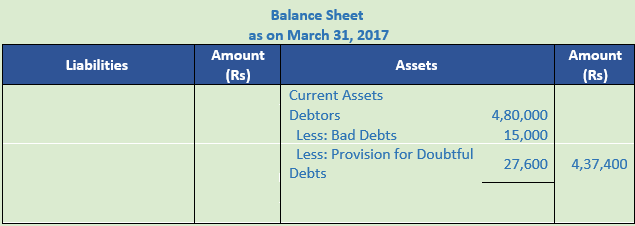

Question 21.

Solution 21:

Working Note:-

Land and Building = Rs. 25,000 + Rs. 3,000 + Rs. 2,000 = Rs. 30,000

Calculation of Depreciation:-

Depreciation of Land and Building = Rs. 30,000 × 2.5% = Rs. 750

Depreciation of Plant and Machinery = Rs. 14,470 × 10% = Rs. 1,427

Calculation of Provision for Doubtful debts:-:-

Provision for doubtful debts = Sundry Debtors – Further Bad debts × Rate

Provision for doubtful debts = Rs. 30,000 × 5%

Provision for doubtful debts = Rs. 1,890

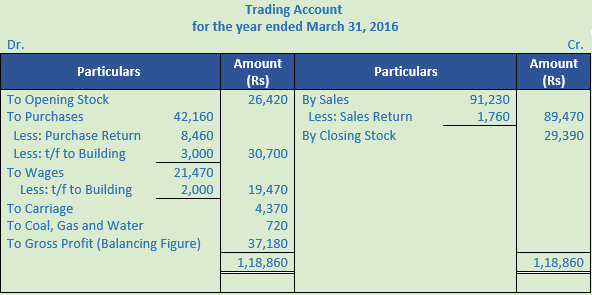

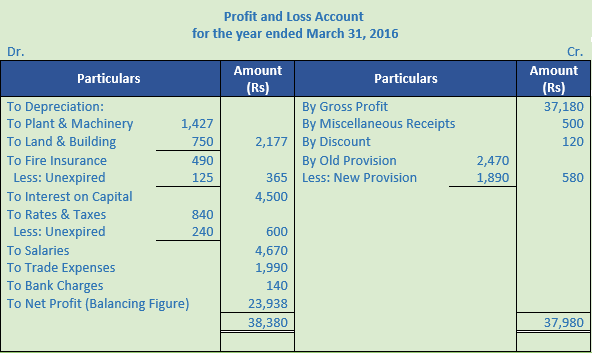

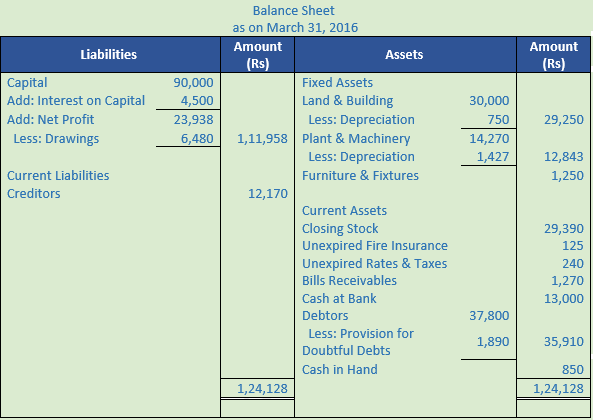

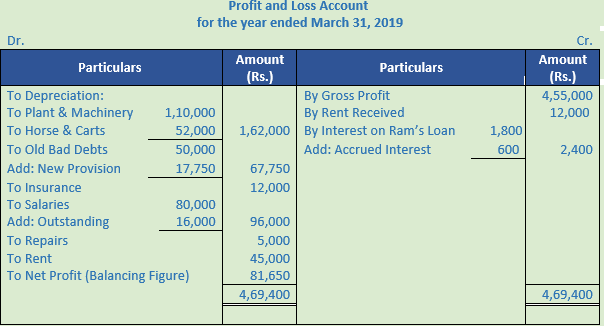

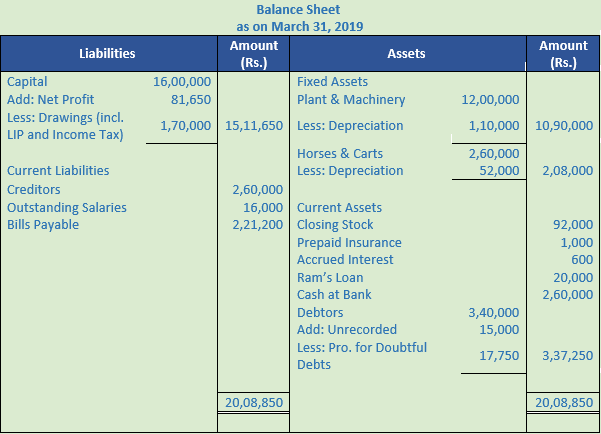

Question 22.

Solution 22:

Working Note:-

Calculation of Depreciation:-

Depreciation of Land and Building = Rs. 30,000 × 2.5% = Rs. 750

Depreciation of Plant and Machinery = Rs. 14,470 × 10% = Rs. 1,427

Calculation of Provision for Doubtful debts:-

Provision for doubtful debts = Sundry Debtors + Unrecorded sales × Rate

Provision for doubtful debts = (Rs. 3,40,000 + Rs. 15,000) × 5%

Provision for doubtful debts = Rs. 17,750

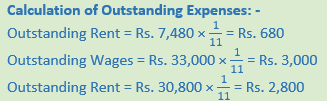

Calculation of Outstanding Expenses:-

Salaries for 10 months = Rs. 80,000

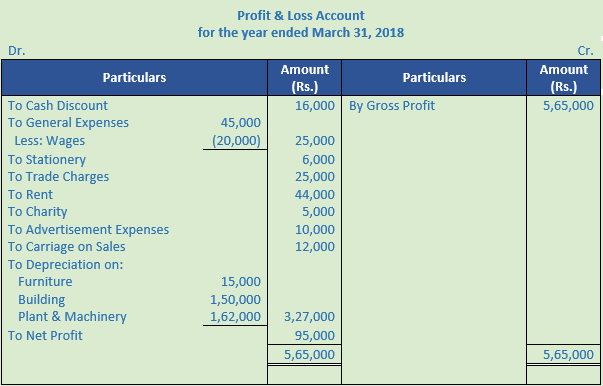

![]()

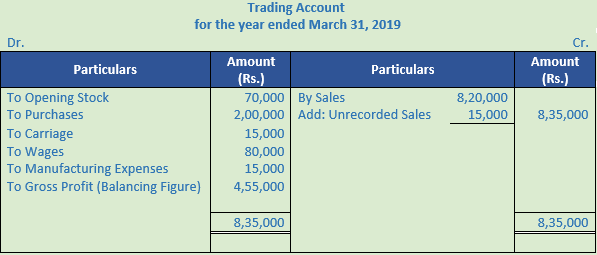

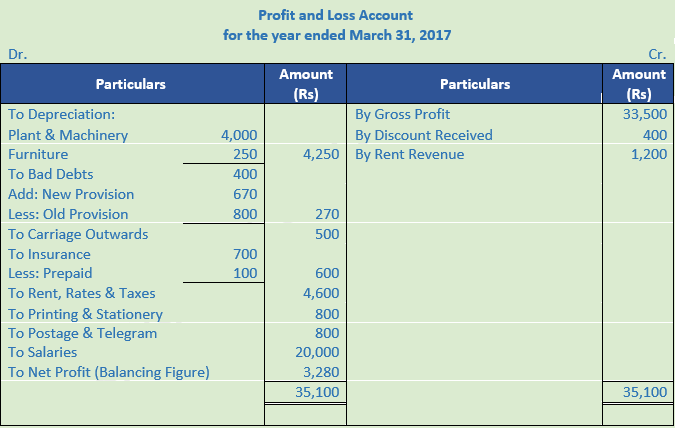

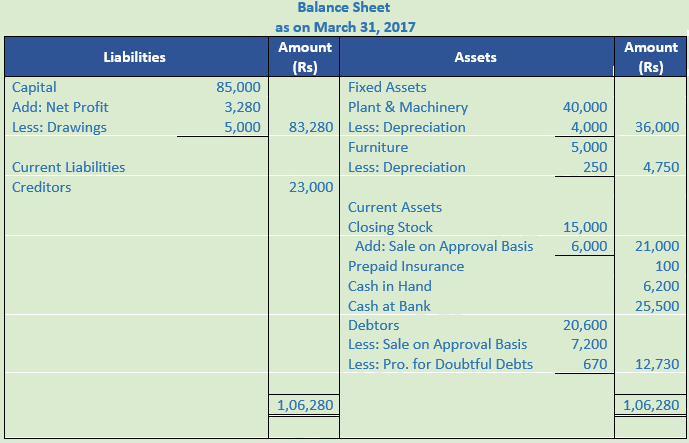

Question 23.

Solution 23:

Working Note:-

Calculation of Depreciation:-

Depreciation of Land and Building = Rs. 40,000 × 10% = Rs. 4,000

Depreciation of Plant and Machinery = Rs. 5,000 × 5% = Rs. 250

Calculation of Provision for Doubtful debts:-

Provision for doubtful debts = Sundry Debtors – Sales on Approval × Rate

Provision for doubtful debts = (Rs. 20,600 - Rs. 7,200) × 5%

Provision for doubtful debts = Rs. 670

Question 24.

Solution 24:

Working Note:-

Calculation of Depreciation:-

Depreciation of Machinery = Rs. 1,00,000 × 5% = Rs. 5,000

Depreciation of Furniture = Rs. 12,000 × 6% = Rs. 720

Depreciation of Furniture = Rs. 20,000 – Rs. 16,000 = Rs. 4,000

Calculation of Provision for Discount on Debtors:-

Provision for doubtful debts = Sundry Debtors × Rate

Provision for doubtful debts = Rs. 56,000 × 2%

Provision for doubtful debts = Rs. 1,120

Question 25.

Solution 25:

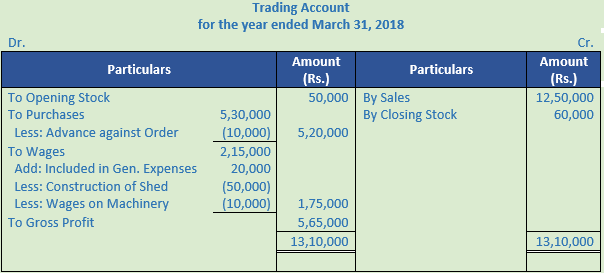

Question 26.

Solution 26:

Question 27.

Solution 27:

Question 28.

Solution 28:

Question 29.

Solution 29:

Working Note:-

Calculation of Depreciation:-

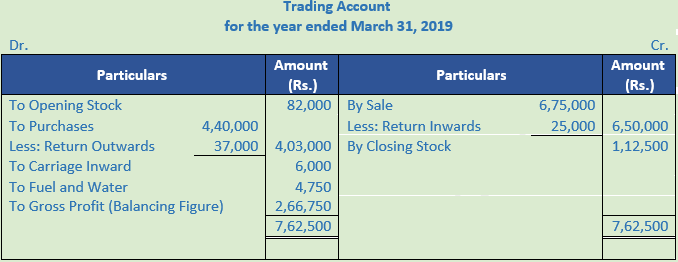

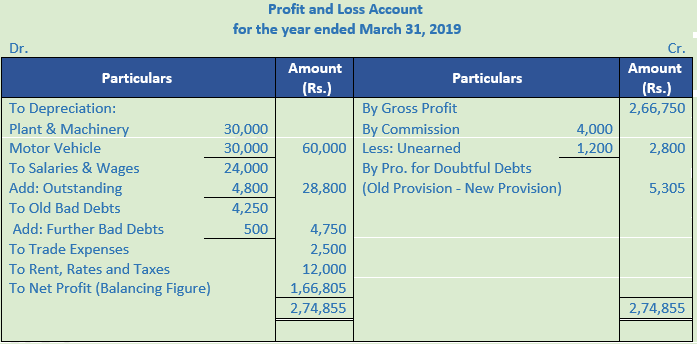

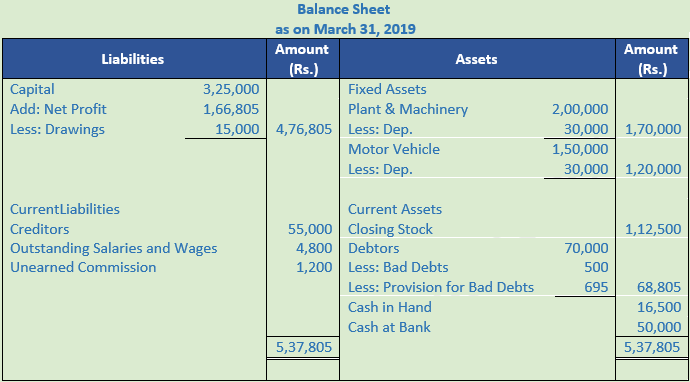

Depreciation of Machinery = Rs. 2,00,000 × 15% = Rs. 30,000

Depreciation of Motor Vehicle = Rs. 1,50,000 × 20% = Rs. 30,000

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors – future Bad debts × Rate

Provision for doubtful debts = (Rs. 70,000 – Rs. 500) × 1%

Provision for doubtful debts = Rs. 695

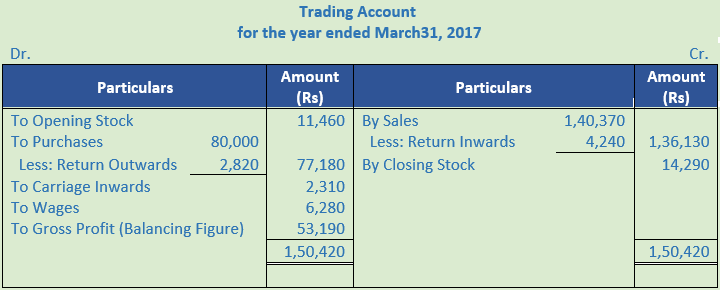

Question 30.

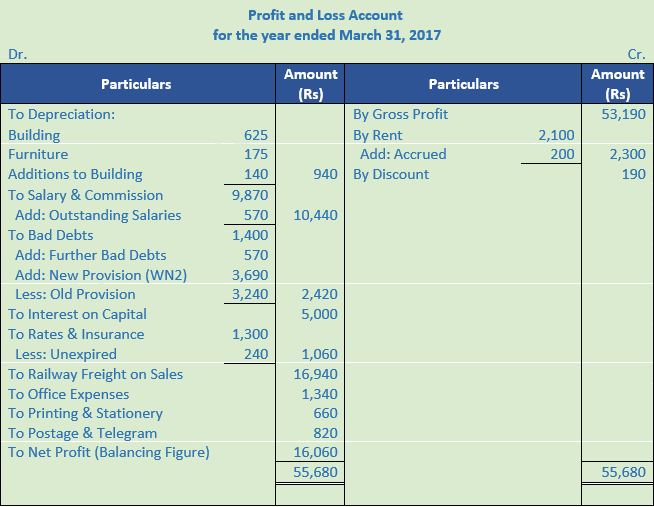

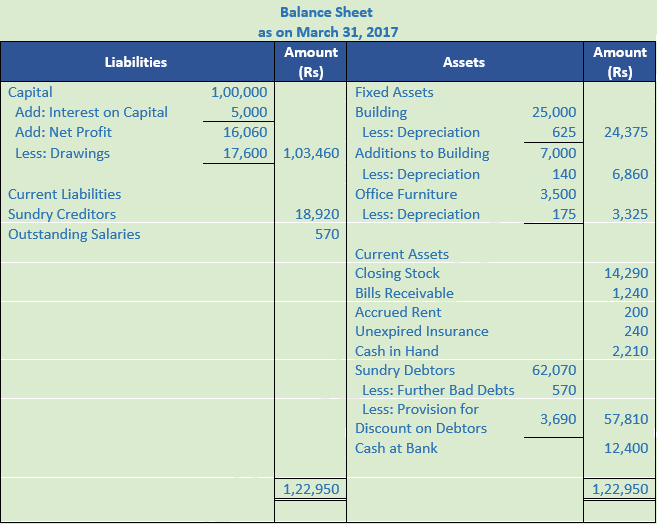

Solution 30:

Working Note:-

Calculation of Depreciation:-

Depreciation of Building = Rs. 25,000 × 2.5% = Rs. 625

Depreciation of Building2 = Rs. 7,000 × 2% = Rs. 140

Depreciation of office furniture = Rs. 3,500 × 5% = Rs. 175

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors – future Bad debts × Rate

Provision for doubtful debts = (Rs. 62,070 – Rs. 570) × 6%

Provision for doubtful debts = Rs. 3,690

Question 31.

Solution 31:

Working Note:-

Calculation of drawings = Rs. 45,000 + Rs. 5,000 = Rs. 50,000

Calculation of Depreciation:-

Depreciation of Building = Rs. 3,00,000 × 5% = Rs. 15,000

Depreciation of Furniture = Rs. 80,000 × 10% = Rs. 8,000

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors – future Bad debts × Rate

Provision for doubtful debts = Rs. 2,50,000 × 5%

Provision for doubtful debts = Rs. 12,500

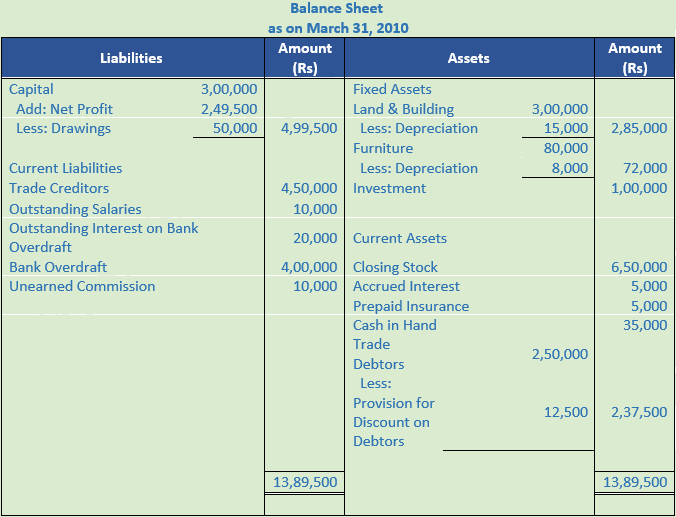

Question 32.

Solution 32:

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors – future Bad debts × Rate

Provision for doubtful debts = (Rs. 80,000 – Rs. 2,000) × 5%

Provision for doubtful debts = Rs. 3,900

Question 33.

Solution 33:

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors – future Bad debts × Rate

Provision for doubtful debts = (Rs. 18,200 – Rs. 200) × 5%

Provision for doubtful debts = Rs. 900

Question 34.

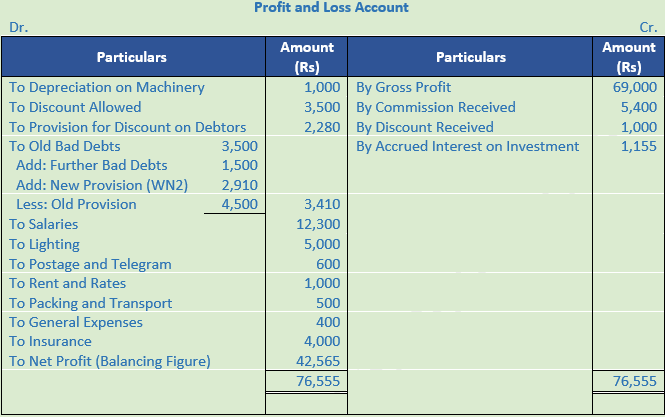

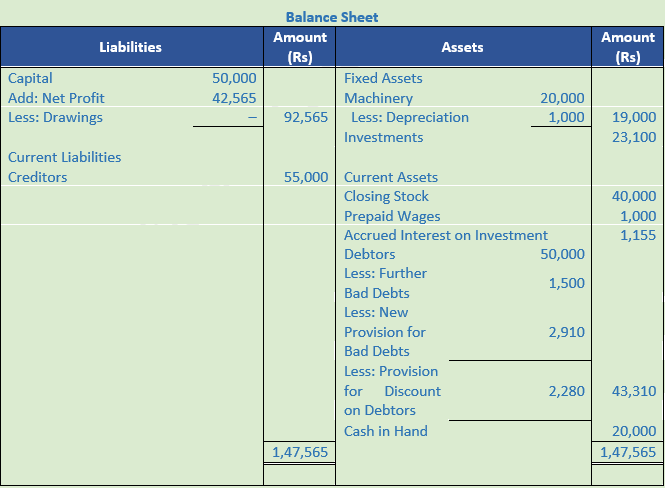

Solution 34:

Working Note:-

Calculation of Depreciation:-

Depreciation of Machinery = Rs. 20,000 × 5% = Rs. 1,000

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors – future Bad debts × Rate

Provision for doubtful debts = (Rs. 50,000 – Rs. 1,000) × 6%

Provision for doubtful debts = Rs. 2,910

Calculation of Provision for Discount on Debtors:-

Provision for doubtful debts = Sundry Debtors – future Bad debts – Pro. For Bad debts × Rate

Provision for doubtful debts = (Rs. 50,000 – Rs. 1,500 - Rs. 2,910) × 5%

Provision for doubtful debts = Rs. 2,280

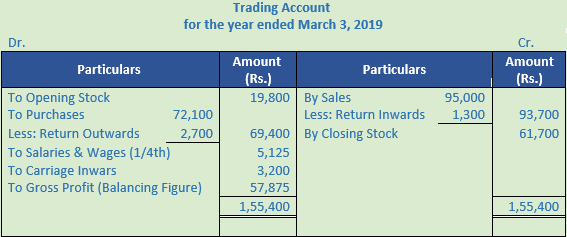

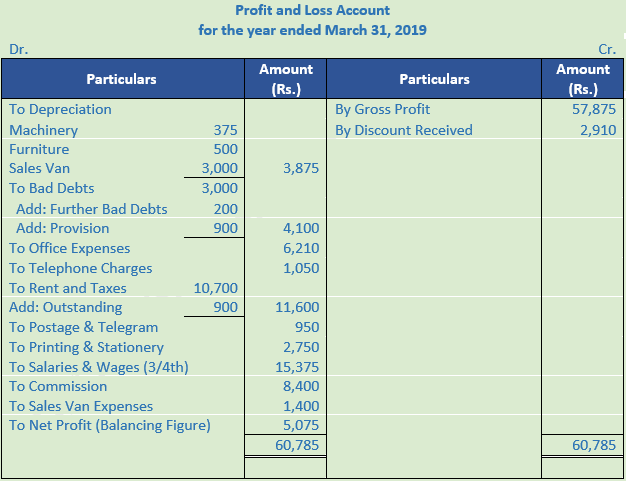

Question 35.

Solution 35:

Working Note:-

Calculation of Depreciation:-

Depreciation of Plant = Rs. 60,000 × 10% = Rs. 6,000

Depreciation of Furniture = Rs. 15,000 × 20% = Rs. 3,000

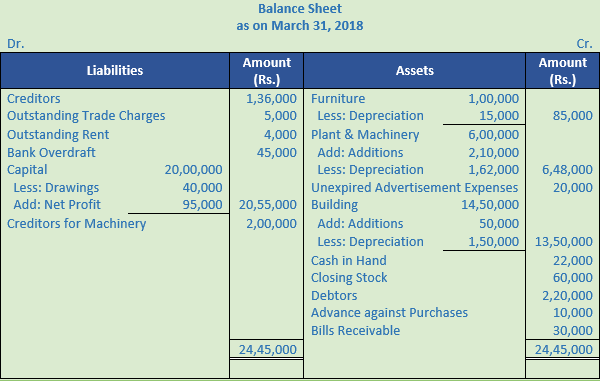

![]()

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors × Rate

Provision for doubtful debts = Rs. 1,00,000 × 5%

Provision for doubtful debts = Rs. 5,000

Calculation of Provision for Discount on Debtors:-

Provision for doubtful debts = Sundry Debtors – Pro. For Bad debts × Rate

Provision for doubtful debts = (Rs. 1,00,000 – Rs. 5,000) × 2%

Provision for doubtful debts = Rs. 1,900

Question 36.

Solution 36:

Working Note:-

Calculation of Salaries & Wages = 1/4th × 40,000 = Rs. 10,000

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = Sundry Debtors – Further Bad Debts × Rate

Provision for doubtful debts = (Rs. 73,800 – Rs. 800) × 5%

Provision for doubtful debts = Rs. 7,300

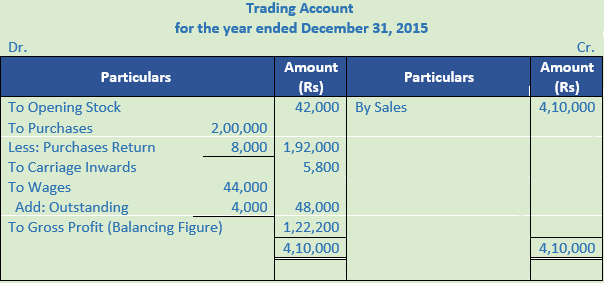

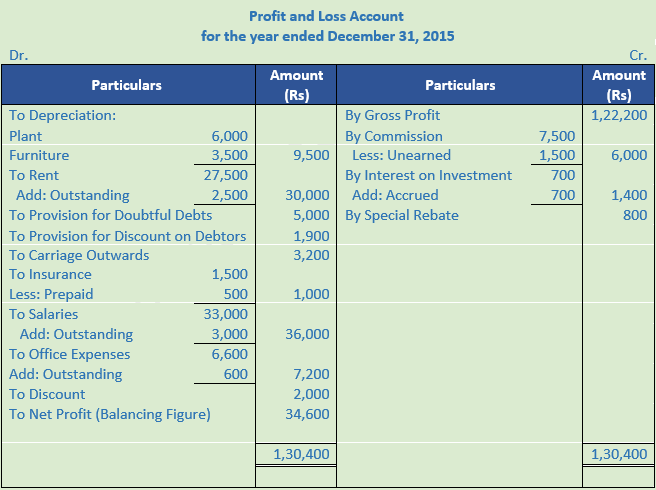

Question 37.

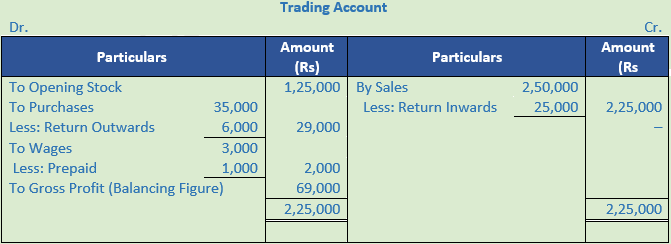

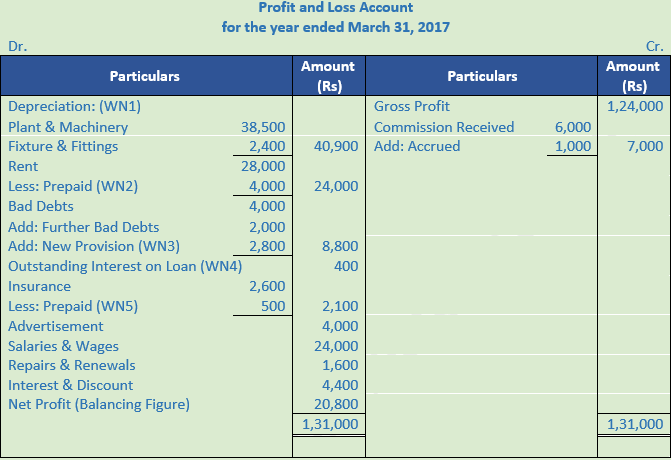

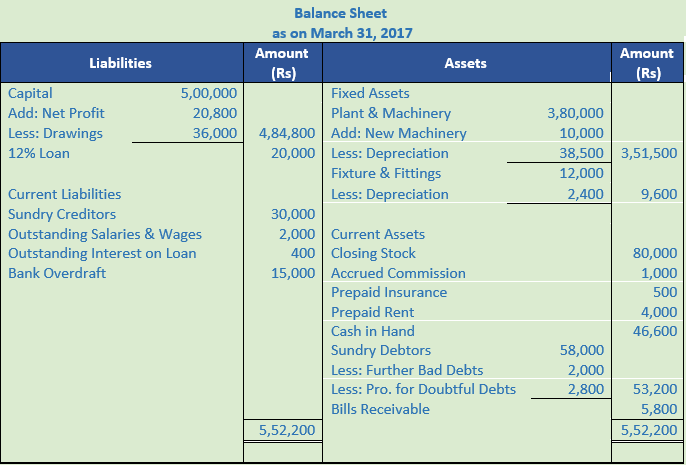

Solution 37:

Working Note:-

Calculation of Depreciation:-

Depreciation of Plant and Machinery = Rs. 3,80,000 × 10% = Rs. 38,000

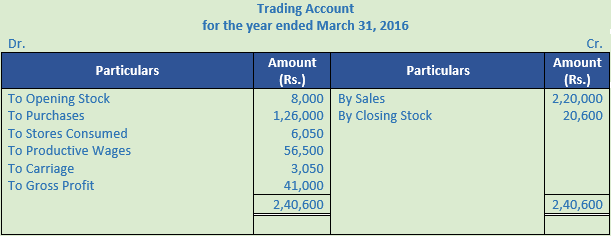

![]()

Depreciation of Fixtures and Furniture = Rs. 12,000 × 20% = Rs. 2,400

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = (Sundry Debtors – Further Bad Debts) × Rate

Provision for doubtful debts = (Rs. 58,000 – Rs. 2,000) × 5%

Provision for doubtful debts = Rs. 2,800

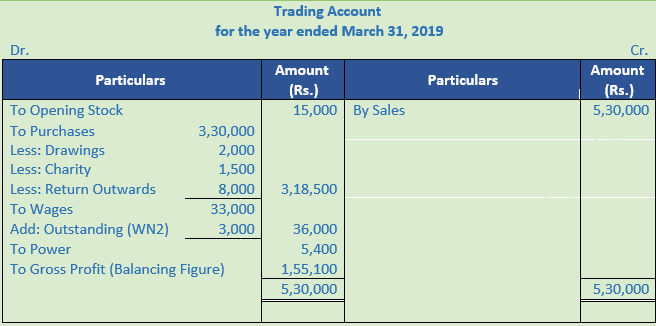

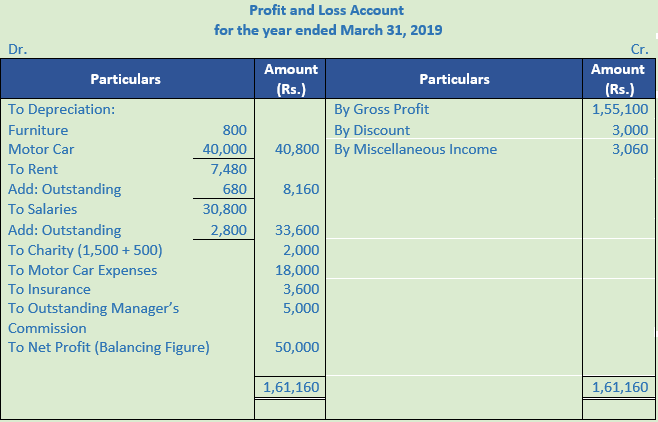

Question 38.

Solution 38:

Working Note:-

Calculation of Depreciation:-

Depreciation of Motor car = Rs. 2,00,000 × 20% = Rs. 40,000

Depreciation of Fixtures and Furniture = Rs. 8,000 × 10% = Rs. 800

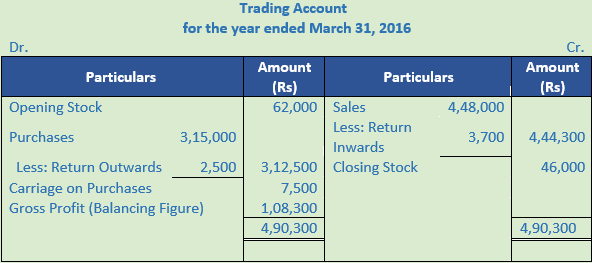

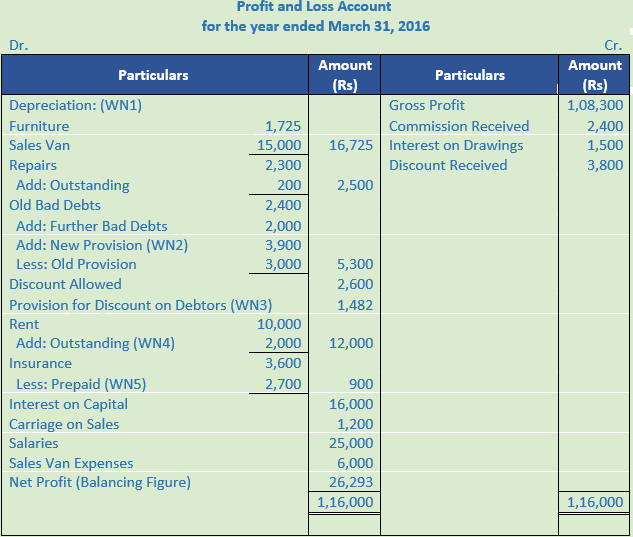

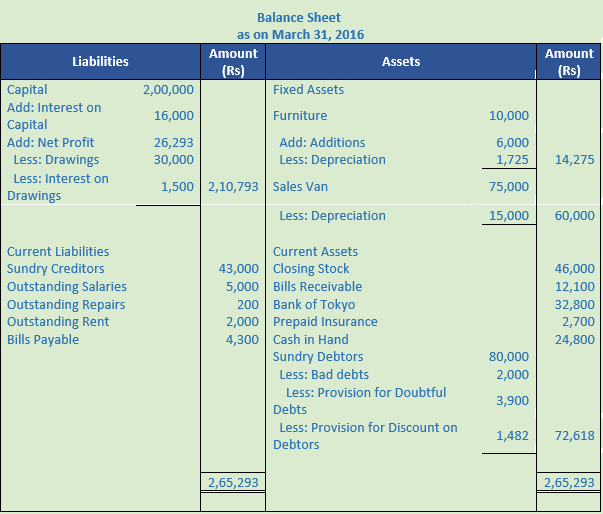

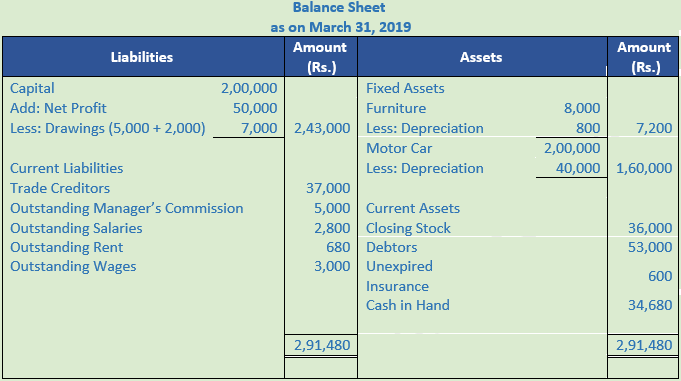

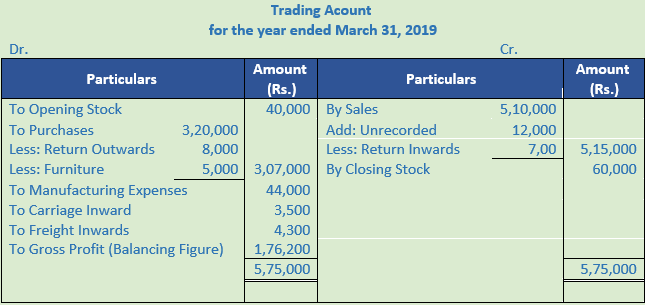

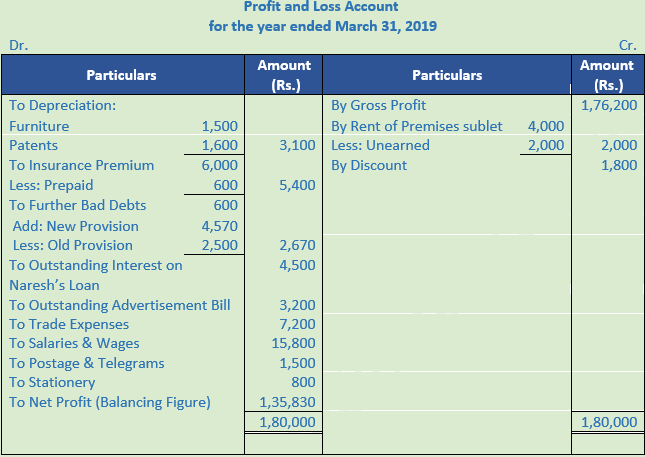

Question 39.

Solution 39:

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = (Sundry Debtors + Unrecorded – Further Bad Debts) × Rate

Provision for doubtful debts = (Rs. 80,000 + Rs. 12,000 – Rs. 2,000) × 5%

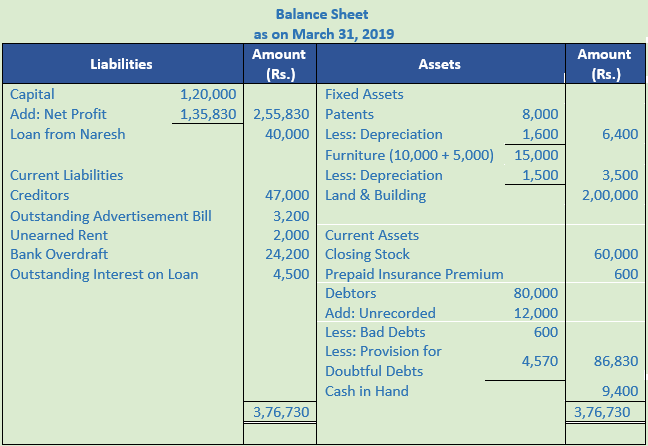

Provision for doubtful debts = Rs. 4,570

Question 40.

Solution 40:

Calculation of Provision for Doubtful Debts:-

Provision for doubtful debts = (Sundry Debtors – Further Bad Debts) × Rate

Provision for doubtful debts = (Rs. 1,42,000 – Rs. 2,000) × 5%

Provision for doubtful debts = Rs. 7,000

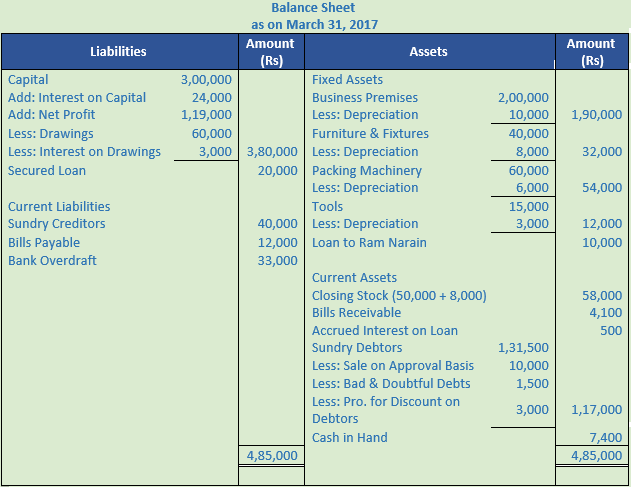

Question 41.

Solution 41:

Working Note:-

Calculation of Depreciation:-

Depreciation of Premise = Rs. 2,00,000 × 5% = Rs. 10,000

Depreciation of Furniture = Rs. 40,000 × 20% = Rs. 8,000

Depreciation of Packing Machinery = Rs. 60,000 × 10% = Rs. 6,000

Depreciation of Tools = Rs. 15,000 –Rs. 12,000 = Rs. 3,000

Calculation of Provision for Discount on Debtors:-

Provision for Discount on Debtors = (Sundry Debtors – Further Bad Debts) × Rate

Provision for Discount on Debtors = (Rs. 80,000 + Rs. 1,500) × 2.5%

Provision for Discount on Debtors = Rs. 3,250

Question 42.

Solution 42:

Working Note:-

Calculation of Provision for Doubtful Debts:-

Provision for Doubtful Debts = Sundry Debtors × Rate

Provision for Doubtful Debts = Rs. 40,000 × 5% = Rs. 2,000

Calculation of Manager’s Commission:-

Manager’s Commission = Rs. 1,06,000 - Rs. 46,900

Manager’s Commission = Rs. 60,000 × 10% = Rs. 6,000

Question 43.

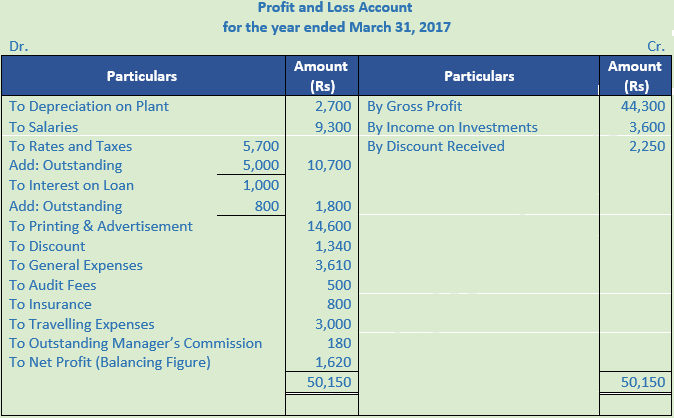

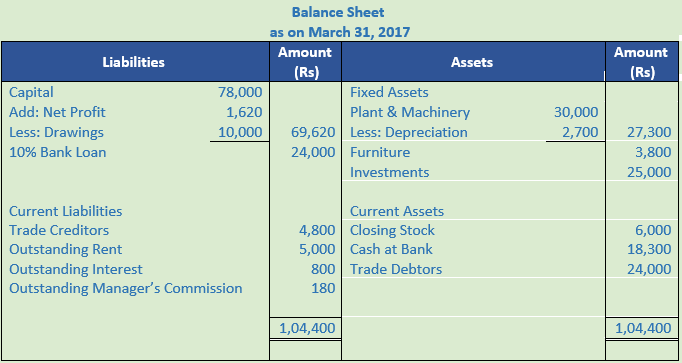

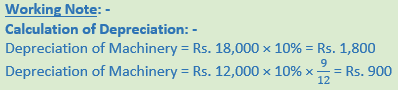

Solution 43:

Calculation of Manager’s Commission:-

Manager’s Commission = Rs. 50,150 - Rs. 48,350

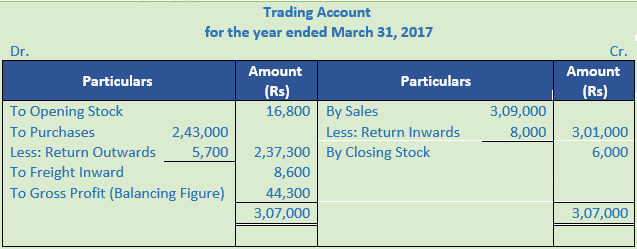

Manager’s Commission = Rs. 1,800 × 10% = Rs. 180