Read TS Grewal Accountancy Class 11 Solution Chapter 8 Journal 2025. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 11 Accounts Chapter 8 Journal TS Grewal Solutions

TS Grewal Solutions for Chapter 8 Journal Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2025 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11.

Chapter 8 Journal TS Grewal Class 11 Solutions

Question 1. What is an Account?

Answer 1. An account is a record of transaction, both cash and credit under a particular head of account like wages, rent, sales, etc., or a particular head like assets, liability, etc. It only shows the amount of transactions but also shows their effect and direction.

Question 2. What is a Personal Account? Is Capital Account a Personal Account? If yes, why?

Answer 2. Account which relate to a person or individuals, firms, companies, debtors or creditors etc., are Personal Accounts.

Yes, Capital Account is a personal Account.

The Natural Personal Accounts like Shyam, Kishan etc., Artifical Personal Account like Hair ltd., Radha Co-operative Society, etc. and Representative Personal Accounts like prepaid rent, outstanding expenses, etc. belongs to persons directly or indirectly. Hence Capital Account belong to persons and is a Personal Account.

Question 3. What is a Real Account?

Answer 3. Real Accounts are those accounts which relate to tangible or intangible assets of the firm excluding debtors. Examples of tangible assets are land, plant, computer, cash, investments, stock etc. Examples of intangible assets are goodwill, patents, copyrights, trademarks, computer software, etc. The golden rule of debit and credit tells debit what comes in, credit what goes out.

Question 4. What is a Nominal Account?

Answer 4. Nominal or Revenue or Expense Accounts are the accounts which relate to losses, expenses, profit, revenue, etc. are termed as Nominal Accounts. The examples of Nominal Accounts are Rent Paid Account, Rent Received Accounts, Sales Account, Purchases Return Account, etc. the net result of all the Nominal Accounts is profit or loss which is transferred to the Capital Account. The golden rule of accounts tells Debit all Expenses and Losses, Credit all Incomes and Gains.

Question 5. What are the two sides of an account called?

Answer 5. The two sides of accounts are called debit side and credit side.

Question 6. What is the object of preparing an account?

Answer 6. The objects of preparing an account are:

1.) To record transactions of a particular head.

2.) To record the amount of a particular transaction.

3.) The record the effect of a transaction.

4.) To record the direction of a transaction.

Question 7. Give a specimen of an account.

Answer 7.

Question 8. Give two examples of Nominal Accounts.

Answer 8.

The two examples of Nominal Account are:

1.) Purchases Account

2.) Commission Received Account

Question 9. State the rule of debiting and crediting of accounts.

Answer 9. The rules ' of' debiting and crediting of accounts are to be classified in the following two ways:

A. Traditional Approach or English Approach:

1. Personal Accounts: Debit the receiver, Credit the giver.

2. Impersonal Accounts or Tangible Accounts or Intangible Accounts: Debit what comes in, Credit what goes out.

3. Nominal Accounts or Revenue Accounts or Expenses Accounts: Debit all expenses and losses, Credit all incomes and gains.

B. Modem Approach or Accounting Equation Approach or American Approach:

1. Asset Accounts: Debit the increases, Credit the decreases.

2. Liability Accounts: Debit the decreases, Credit the increases.

3. Capital Accounts: Debit the decreases, Credit the increases.

4. Expenses Account: Debit the increases, Credit the decreases.

Question 10. State with reasons that Capital and Drawings Accounts look like impersonal accounts but they are always used like personal accounts.

Answer 10. Capital and Drawings Accounts look like impersonal accounts but they are always used like Personal Accounts.

Capital and drawings Accounts look like Representative Personal Accounts like the Outstanding Salary Account represents the amount of salary payable to the employees. Here in the question cash invested and withdrawn by the proprietor of the business is credited and debited to the Capital and Drawings Accounts respectively. Hence Capital and Drawings Accounts look like impersonal accounts but they are always used like personal accounts.

Question 11. What do you understand by ‘debit’ and ‘credit’? Do you think ‘debit’ always stands for decrease in amount and credit for increase?

Answer 11. Debit and Credit means:

Debit means: Debit refers to the left side of an account. Dr. stands for debit in the abbreviated form. An item recorded in the debit side of an account is said to be debited to the account. Debit may represent either increase or decrease depending upon the nature of an account. The rule of debit depends on the nature of account.

Credit means: Credit refers to the right side of an account. Cr. stands for credit in the abbreviated form. An item recorded in the credit side of an account is said to be credited to the account. Credit may represent either increase or decrease depending upon the nature of an account. The rule of credit depends on the nature of account. No. We don't think 'debit' always stands for decrease in amount and 'credit' for increase.

Question 12. When is a Capital Account debited? When is it credited?

Answer 12.

Capital Account is debited when there is a decrease in capital.

Capital Account is credited when there is a increase in capital.

Question 13. When do you credit a liability account? What will you do to reduce the balance of any liability account? Explain with an example.

Answer 13. A Liability Account is credited when there is an increase in liability. We will debit the liability account to reduce the balance.

The example to reduce a liability account is paid outstanding rent Rs. 1000. The Outstanding Rent Account will be debited by Rs. 1000.

Question 14. Briefly state the rules of debiting and crediting accounts classified on the basis of Accounting Equation.

Answer 14. Modem Approach or Accounting Equation Approach or American Approach of the stated rules of debiting and crediting accounts are:

1. Asset Accounts: Debit the increases, Credit the decreases.

2. Liability Accounts: Debit the decreases, Credit the increases.

3. Capital Accounts: Debit the decreases, Credit the increases.

4. Expense Accounts: Debit the increases, Credit the decreases.

Question 15. What type of account is a Capital Account and why?

Answer 15. Capital Account is a personal Account.

Accounts which relate to a person or individuals, firms, companies, debtors or creditors, etc., are Personal Accounts. The Natural Personal Accounts like Rakesh, Harish, etc., Artificial Personal Accounts like Rakesh Ltd., Harish Co-operative Society, etc. and Representative Personal Accounts like prepaid rent, outstanding expenses, etc. belongs to persons directly or indirectly. Hence Capital Account belongs to persons and is a Personal Account.

Question 16. Give transaction that: (Old Question)

(i) Increase an asset and increase a liability

(ii) Increase an asset and decrease another asset.

(iii) Decrease an asset and decrease capital.

Answer 16. The following are the transactions that:

(i) Increase an asset and increase a liability.

Example: Machinery purchased on credit.

(ii) Increase an asset and decrease another asset.

Example: Machinery purchased by giving old furniture in exchange.

(iii) Decrease an asset and decrease capital.

Example: Cash withdrawn by the proprietor for personal use.

Question 17. What is meant by a Journal?

Answer 17. Journal is a book of prime entry or a book of original entry in which transaction are first recorded in a chronological order or sequence they are entered. Journal is called the Book of Original Entry since all transactions are initially recorded in it.

Question 18. Give two advantages of a Journal.

Answer 18. The following are the two advantages of Journal.

1. Recording of accounting data in chronological order.

2. Narration of journal explains the transactions very well.

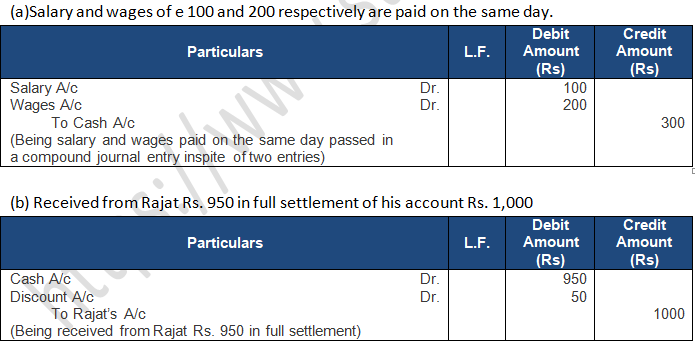

Question 19. What are Compound Journal Entries? Give an example.

Answer 19. Compound Journal Entry is an entry in which two or more accounts are debited and one or more accounts are credited or vice versa. The following are two examples for compound Journal Entries:

Question 20. Is Journal a book of original entry?

Answer 20. Yes. Journal is a book of original entry.

The need for sub-division of Journal is to conveniently maintain a separate book for each class of transaction for recording. Book of this type is called a book of original entry or prime entry - it is a special form of Journal, a sub-division of it. Journal entry is not passed for the transactions recorded in such books. They are posted to the ledger accounts. The system is called the practical system of accounting. The Journal is sub-divided into Cash Book, Purchases Book, Sales Book, Purchases Return Book, Sales Return Book, and Journal Proper.

Question 21. What is an Opening Entry? Give an example.

Answer 21. Firms close their books at the end of the year. The nominal accounts are closed by transferring them to Profit and Loss Account. The balances of personal and real accounts under traditional classification of accounts and assets, liabilities and capital accounts under modern classification of accounts are carried forward to the next year. These balances become the opening balances of the next year. The first entry in the Journal is passed to record closing balances of the previous year. It is called the opening entry. The Balance Sheet prepared at the end of the year shows the closing balances of each asset and liability and forms the basis for this opening entry. While passing opening entry, all assets are debited individually, where as Capital and Liabilities are individually credited. If capital is not given in the information, it is calculated by applying the following accounting equation, that is Capital = Assets — Liabilities.

Question 22. What is Trade Discount?

Answer 22. Trade Discount is allowed by the seller on purchase of goods in large quantity. It is usually by the wholesalers to the retail shop owners who further sell the goods to the consumer. Trade Discount is deducted in the invoice from sale price and is not recorded in the books of account. Sales are recorded at net sales price or sale price less trade discount. GST or CGST, SGST and IGST are levied on the net sale price. Trade discount is allowed on sales, hence it is allowed on both cash and credit sales.

Question 23. What is Cash Discount?

Answer 23. Cash Discount is allowed by the seller to the customers to encourage prompt or early payment. It is allowed as a per cent of invoice value or payment made say @ 5% of invoice value to the buyer. Cash discount is calculated after deducting trade discount from the invoice price. Cash discount is calculated always on net amount. It is allowed at the time of receipt of amount in cash or by cheque. It is an expense for business allowing it and gain for the business availing it. It is recorded in the books of both seller and buyer. Cash discount allowed is debited to ' Discount Allowed Account' by the party receiving the amount and cash discount received is credited to 'Discount Received Account' by the party making the payment. Discount allowed or received is related to payment and thus, they are recorded in the books of account along with the entry recorded for payment and receipt of the amount, in cash or cheque. When cash discount is allowed or received GST or CGST, SGST, IGST is not levied since it is for early payment and not on sale or purchase of goods.

Question 24. What are the advantages of allowing Trade Discount? (Two points) (Old Question)

Answer 24. The following are the two advantages of allowing Trade Discount:

1.) Increased sales due to high quantity involved in sales.

2.) Increased customer base due to low prices and discount offers.

Question 25. What are the advantages of allowing Cash Discount? (Two points) (Old Question)

Answer 25. The following are the two advantages of allowing Cash Discount:

1.) Prompt collection of payment due to discount offer on time period basis.

2.) Increase customer base due to low price and discount offers.

Question 26. Distinguish Trade Discount from Cash Discount. (Two Points) (Old Question)

Answer 26.

Question 27. How is Trade Discount recorded in the books of account?

Answer 27. Trade Discount is deducted in the invoice from sale price and is not recorded in the books of account. Sales are recorded at net sales price or sale price less trade discount. GST or CGST, SGST and IGST are levied on the net sale price. Trade discount is allowed on sales, hence it is allowed on both cash and credit sales. It is only recorded in the work sheets but not in the amount columns in the books like Journal and other principle books.

Question 28. How is Cash Discount recorded in the books of account?

Answer 28. Cash Discount allowed is debited to 'Discount Allowed Account' by the party receiving the amount and cash discount received is credited to 'Discount Received Account' by the party making the payment. Discount allowed or received is related to payment and thus, they are recorded in the books of account along with the entry recorded for payment and receipt of the amount, in cash or cheque. When cash discount is allowed or received GST or CGST, SGST, IGST is not levied since it is for early payment and not on sale or purchase of goods.

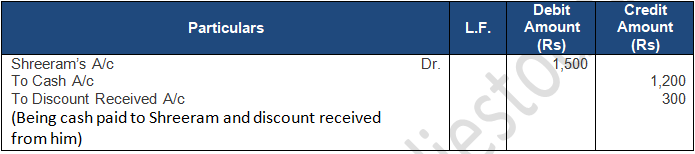

Example of Cash Discount allowed:

Cash Paid to Shreeram Rs. 1200 in full settlement of his account of Rs. 1,500.

Question 29. Which GST is levied on inter-state purchase of goods? (Old Question)

Answer 29. Input IGST is levied on inter-state purchase of goods.

Question 30. Which GST is levied on inter-state sale of goods? (Old Question)

Answer 30. Output IGST is levied on inter-state sale of goods.

Practical Problems ::----->

Simple journal Entries.................

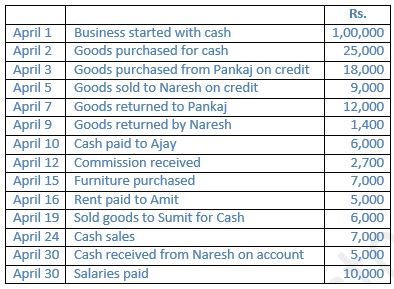

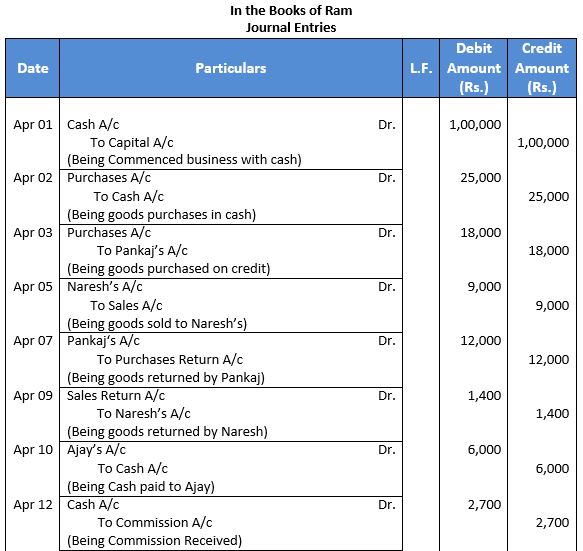

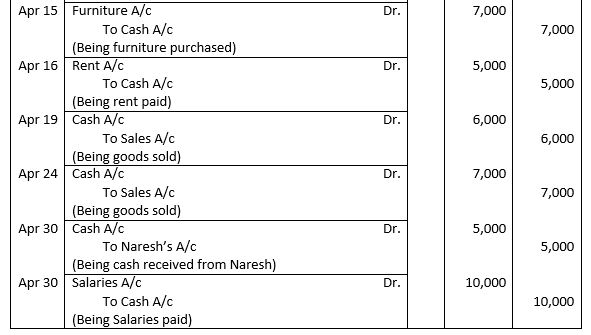

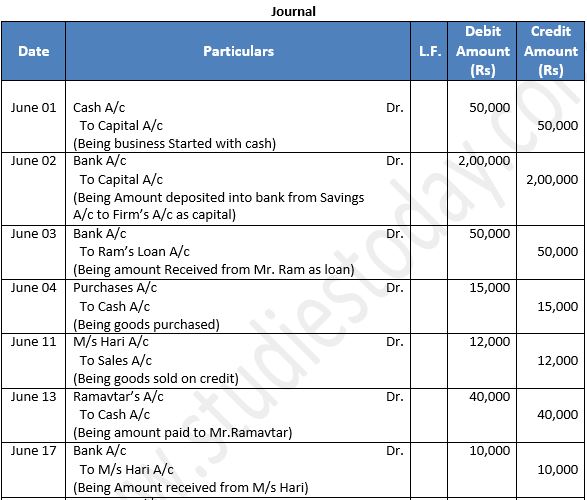

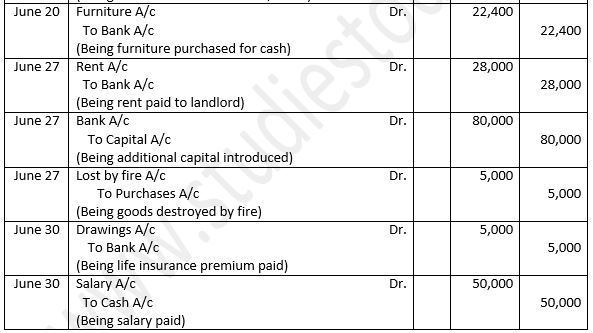

Question.1: Journalise the following transactions in the books of Ram:

Answer 1:

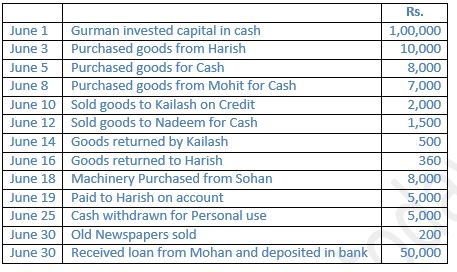

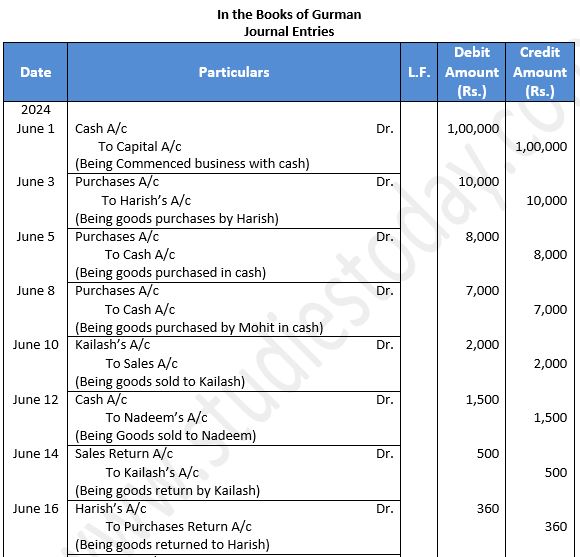

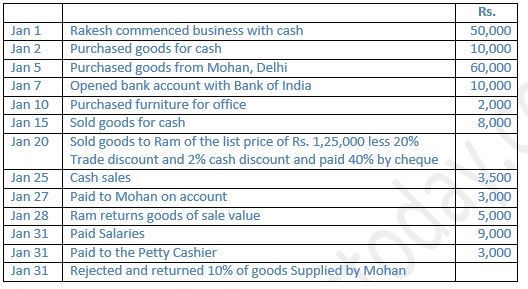

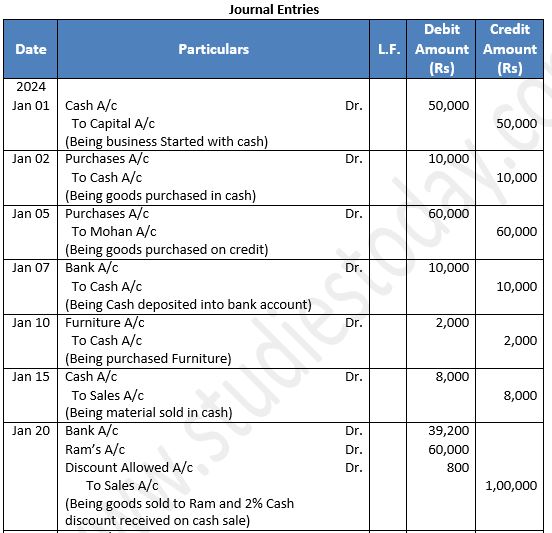

Question 2. Enter the following transactions in the Journal of Gurman:

Answer 2:

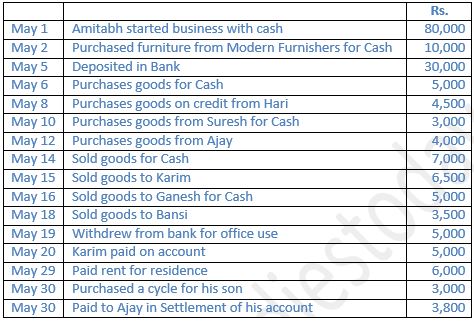

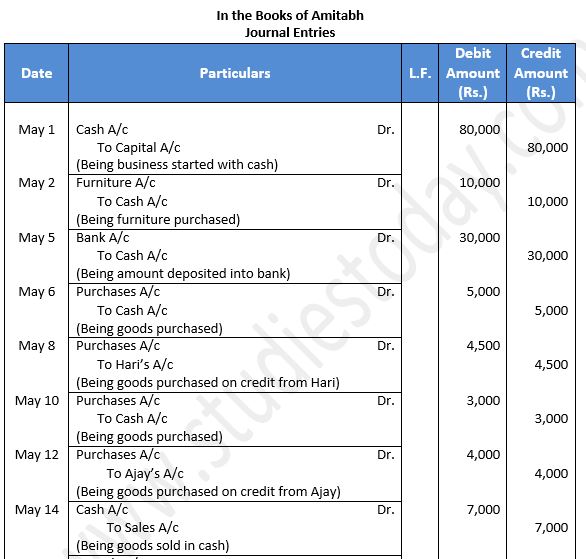

Question.3. Enter the following transactions in the Journal of Amitabh

Answer 3:

Compound Journal Entries...................

Question.4. Pass necessary Journal entries for the following transaction::

Answer 4:

Bad Debts and Bad Debts Recovered

Question.5. Enter the following transactions in the Journal of Ram:

Pass Journal entries for the following transactions:

Answer 5:

Banking Transactions

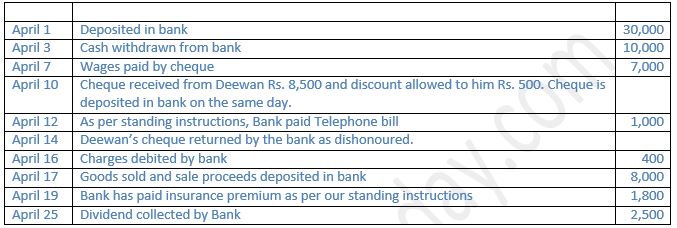

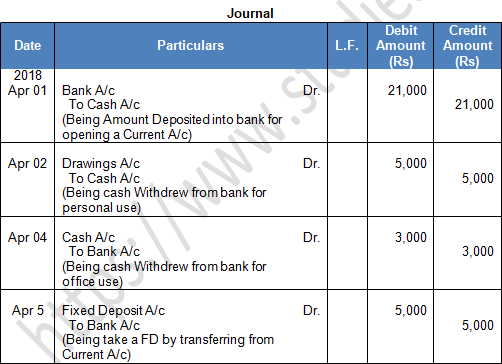

Question.6. Pass necessary Journal entries for the following transactions:

Answer 6:

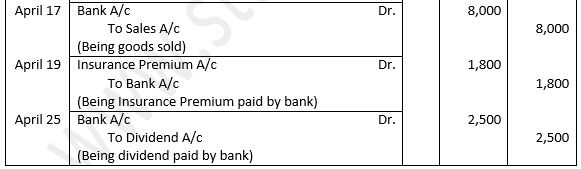

Question.7. Pass necessary Journal entries for the following transactions:

Answer 7:

Transactions Relating to Goods

Question.8. Pass necessary Journal entries for the following transactions:

Answer 8:

Transactions Relating to Goods

Question.9. Pass necessary Journal entries for the following transactions:

Answer 9:

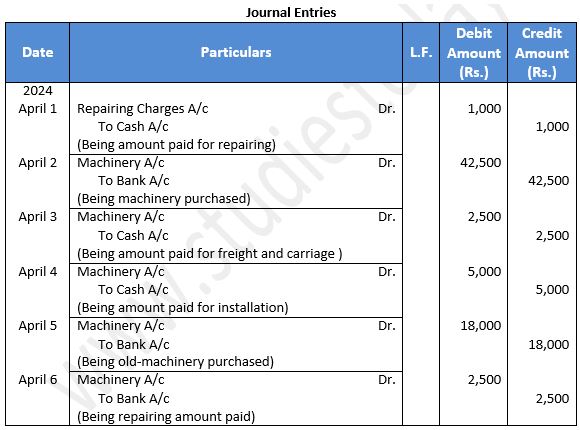

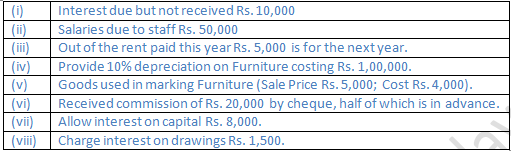

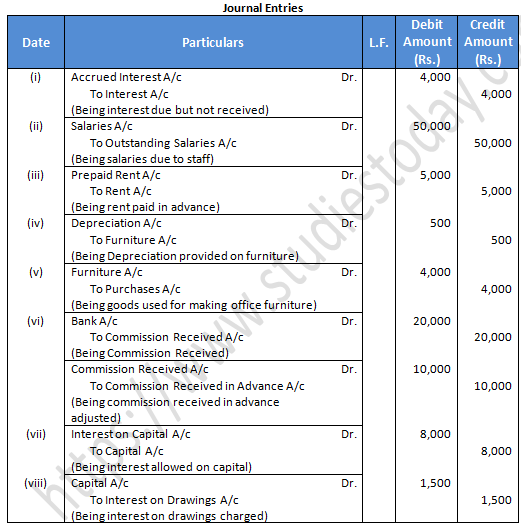

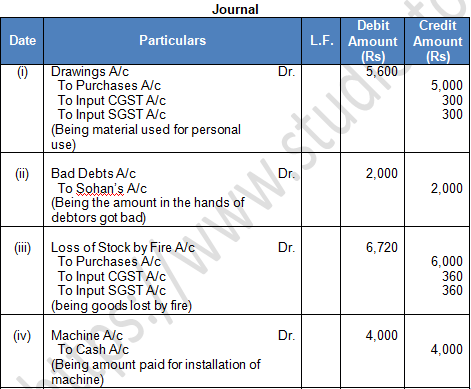

Adjustment Entries

Question.10. Pass necessary Journal entries for the following transactions:

Answer 10:

Opening Capital

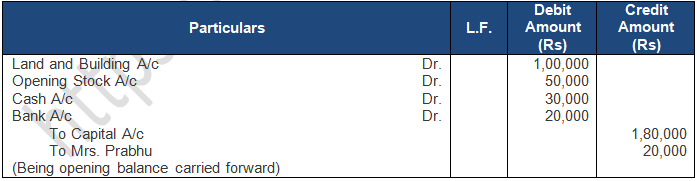

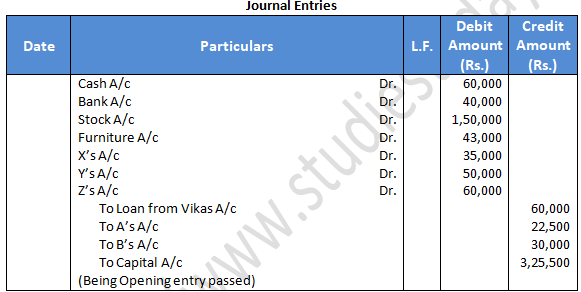

Question.11. Following balance existed in the books of M/s. Anand Store as on 1st April, 2021:

Assets: Capital Rs. 60,000; Bank Rs. 40,000; Stock Rs. 1,50,000; Furniture Rs. 43,000; Debtors Rs. 1,45,000 (X Rs. 35,000; Y Rs. 50,000; Z Rs. 60,000).

Liabilities: Loan from Vikas Rs. 60,000; Creditors Rs. 52,500 (A Rs. 22,500; B Rs. 30,000).

Pass necessary Journal entry to record the above balance.

Answer 11:

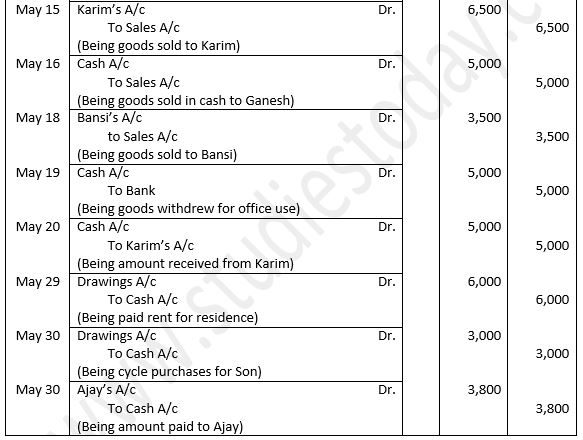

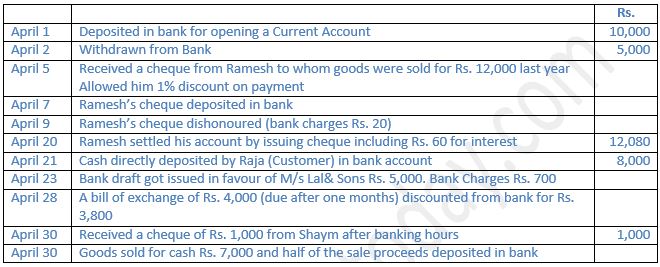

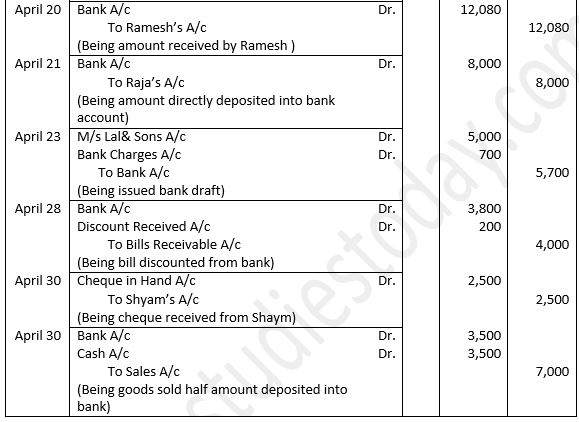

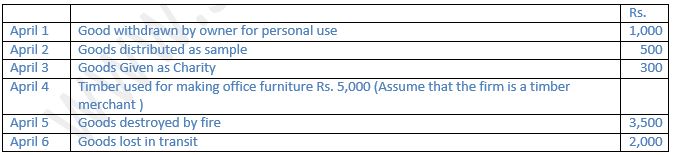

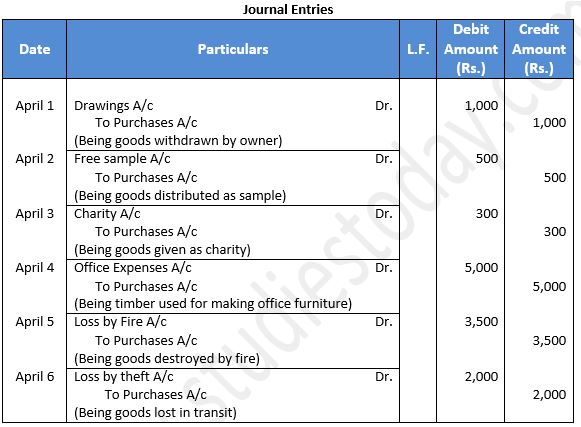

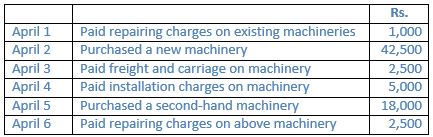

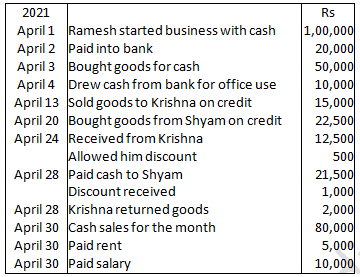

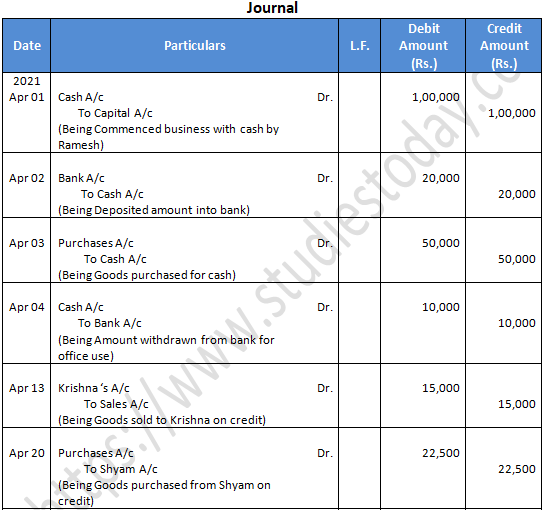

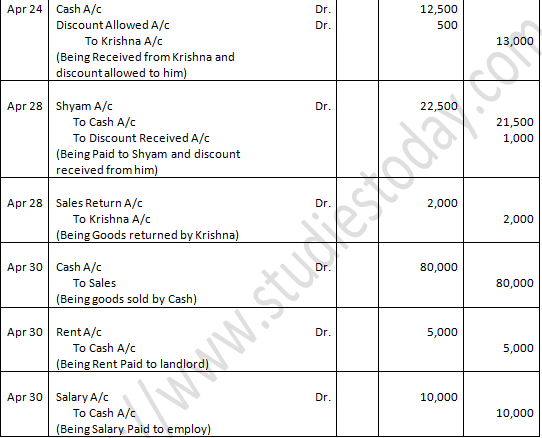

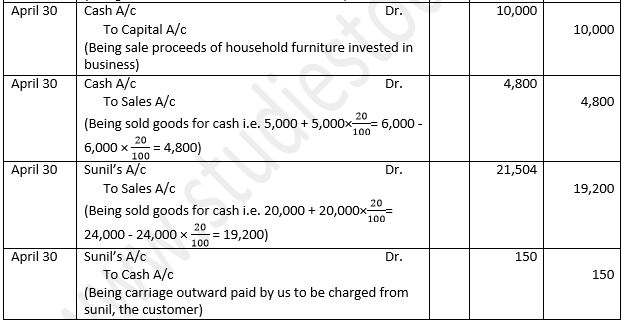

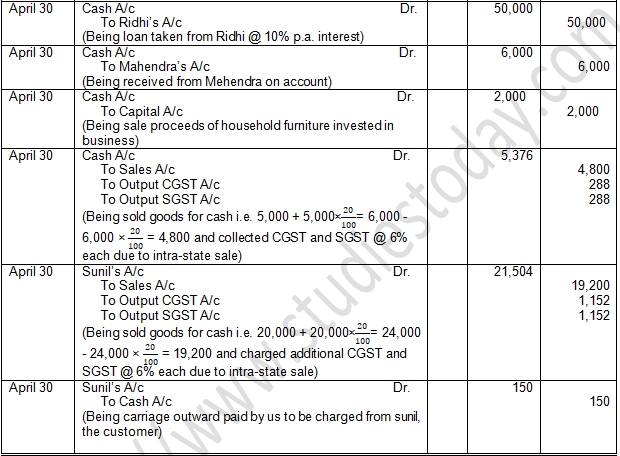

Question 12: Following transactions of Ramesh for April, 2021 are given below. Journalise them.

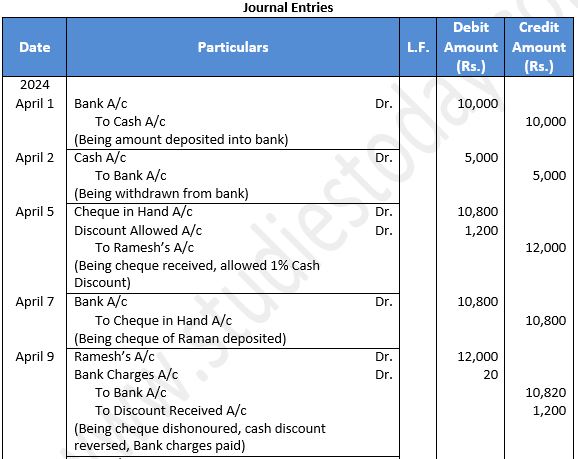

Answer 12:

Statement showing Journal Entries

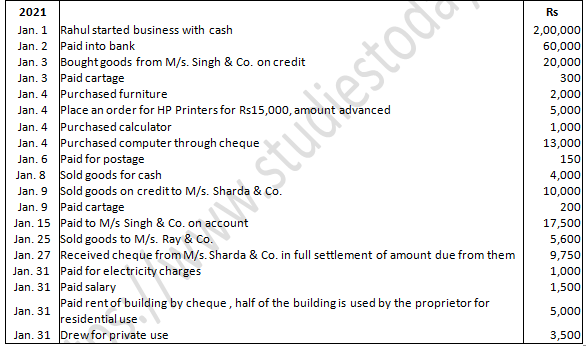

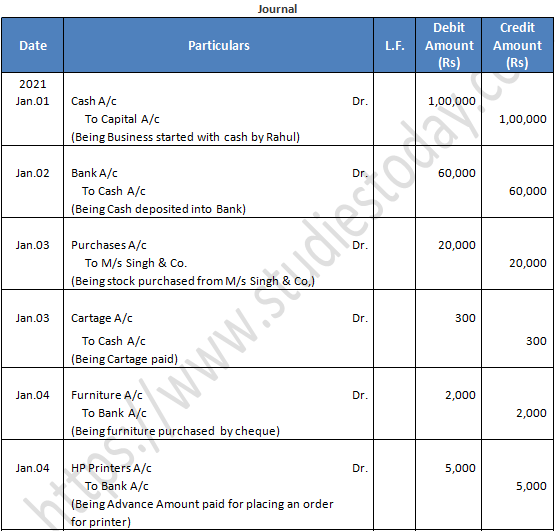

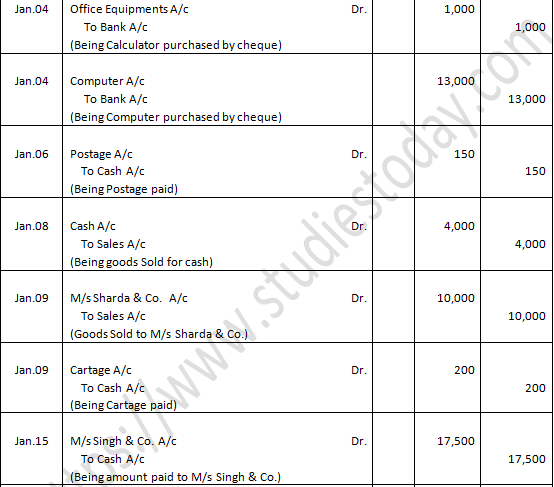

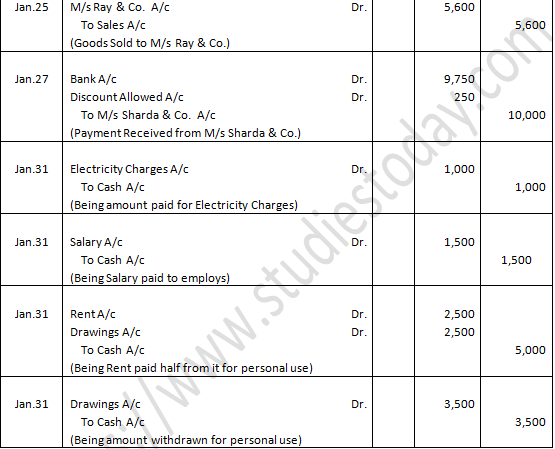

Question 13: Journalise the following transactions of Mr. Rahul:

Answer 13:

Statement showing Journal Entries of Mr.Rahul’s

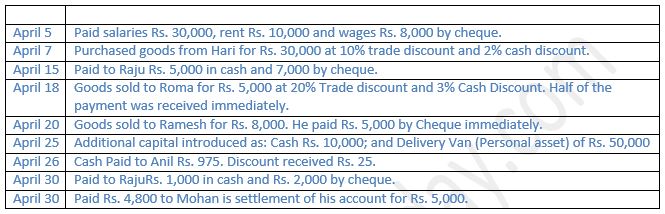

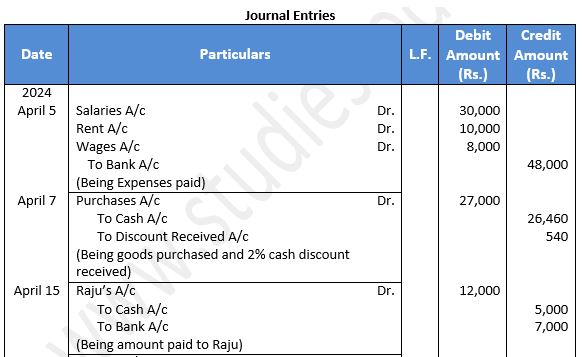

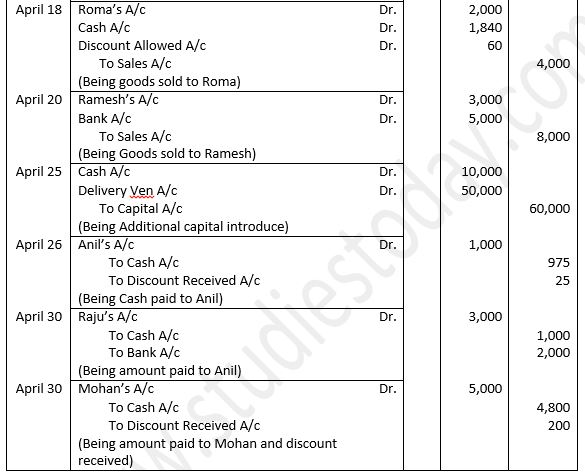

Question 14: Journalise the following transactions of Singh Enterprises, Delhi:

Answer 14:

Statement showing Journal Entries of Singh Enterprises, Delhi

Question 15: Journalise the following transactions of Rakesh Agencies, Delhi (Proprietor Shri Rakesh):

Answer 15:

Statement showing Journal Entries of Rakesh Agencies Delhi

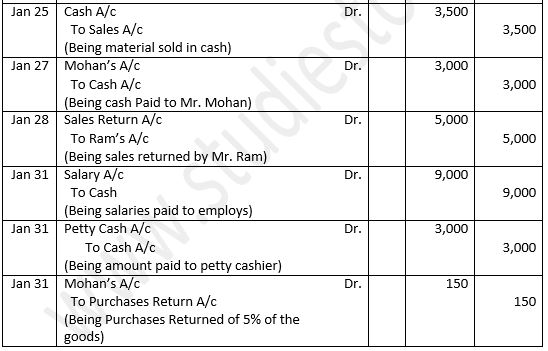

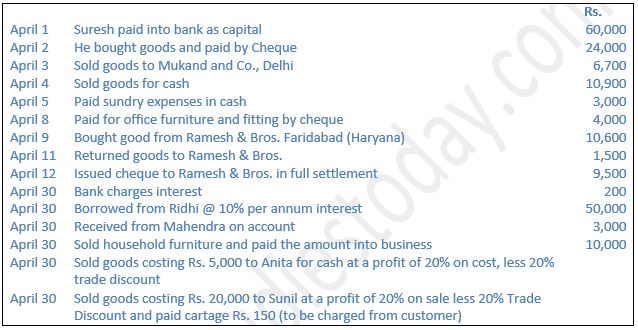

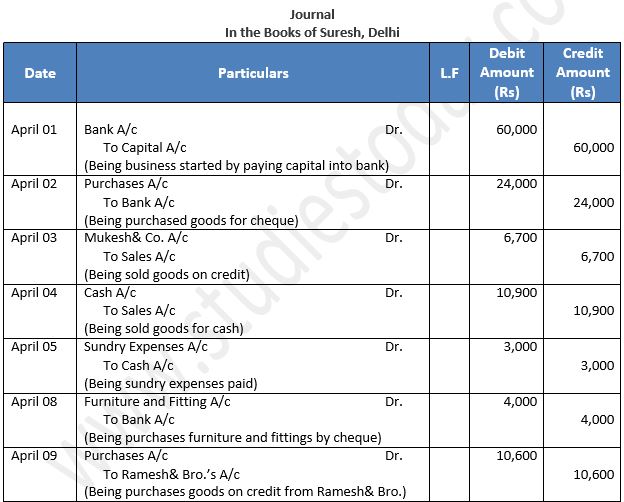

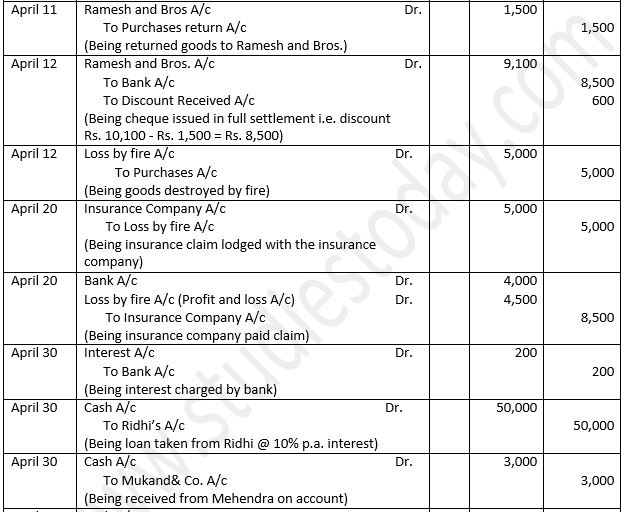

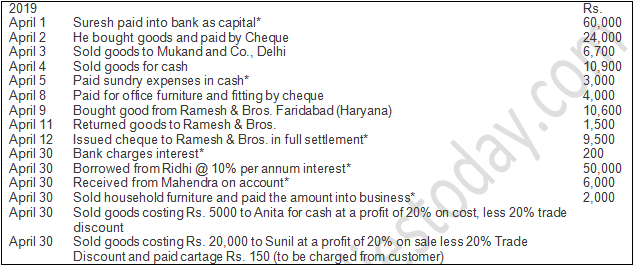

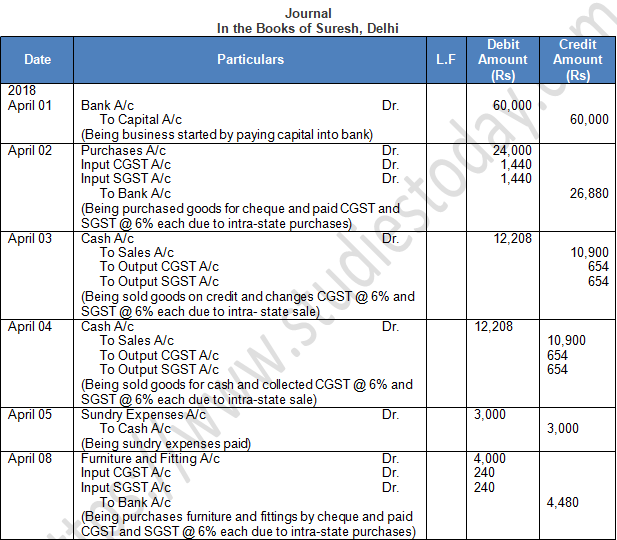

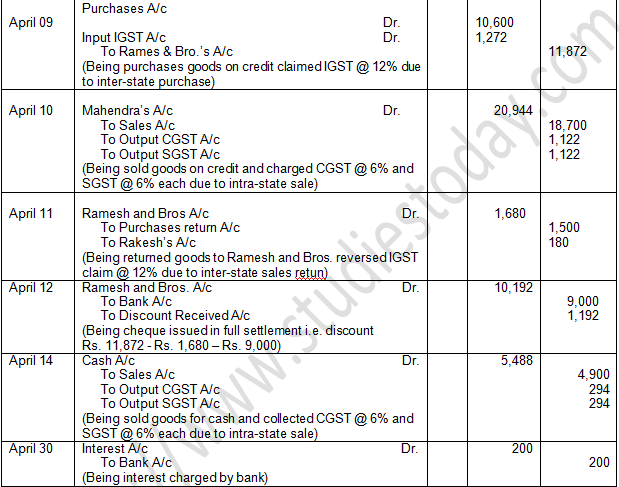

Question 16: Enter the following transaction in the Journal of Suresh, Delhi who trades in readymade garments:

Answer 16:

Statement showing Journal Entries of Suresh, Delhi

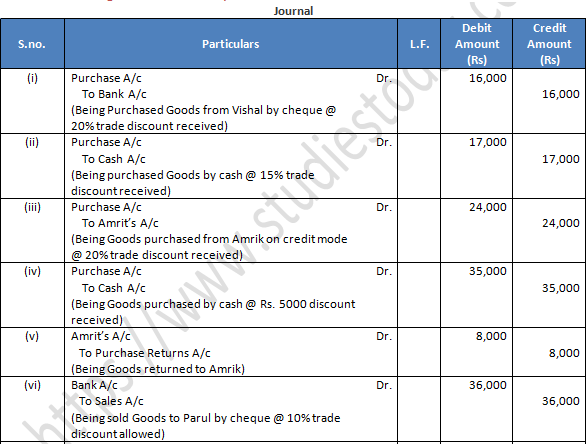

Question 17: Journalise the following transactions in the books of M/s. R.K. & Co.:

(i) Purchased goods at list price of Rs 20,000 from Vishal at 20% trade discount against cheque payment.

(ii) Purchased goods at list price of Rs 20,000 from Naman at 15% trade discount against cash.

(iii) Purchased goods at list price of Rs 30,000 from Amrit at 20% trade discount.

(iv) Purchased goods at list price of Rs 40,000 for Rs 35,000 for cash.

(v) Goods returned of list price Rs 10,000 purchased from Amrit.

(vi) Sold goods to Parul at list price of Rs 40,000 at 10% trade discount against cheque payment.

(vii) Sold goods to Aman at list price of Rs 30,000 at 10% trade discount against cash.

(viii) Sold goods to Pawan at list price of Rs 20,000 at 10% trade discount.

(ix) Sold goods to Yamini at list price of Rs 25,000 for Rs 23,000.

(x) Sold goods costing Rs 10,000 at cost plus 20% less 10% trade discount to Bhupesh.

(xi) Sold goods purchased at list price of Rs 50,000 less 15% trade discount sold at a profit of 25% less 10% trade discount against cheque.

(xii) Aman returned goods of list price of Rs 10,000 sold to him at 10% trade discount.

Answer 17:

Statement showing Journal Entries of M/s R.K. & Co.

Points of Knowledge:-

Working Notes:

Working Note 1: Calculation of Selling price

Selling Price = Cost Price + Profit- Trade Discount

= 10,000 + 2,000 – 1200 =10,800

Profit = 10,000(cost price) × 20%= 2,000

Calculation of Trade Discount =12000 × 10%=Rs 1,200

Working Note 2: Calculation of Purchase price and selling price

Purchase Price = List Price – Trade Discount

= 50,000 – 7,500 = 42,500

Trade Discount = 50,000 × 15% = Rs. 7,500

Sales Price = Purchase Price + Profit – Trade Discount

= 42,500 + 10,625 – 5312.5 = 47,812.5

Calculation of profit = 42,500 × 25% = Rs. 10,625

Calculation of Trade Discount = 53,125 × 10% =5,312.5

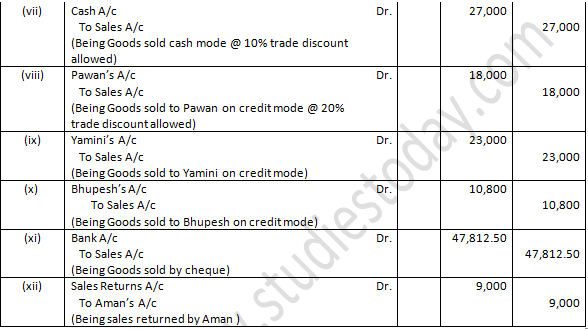

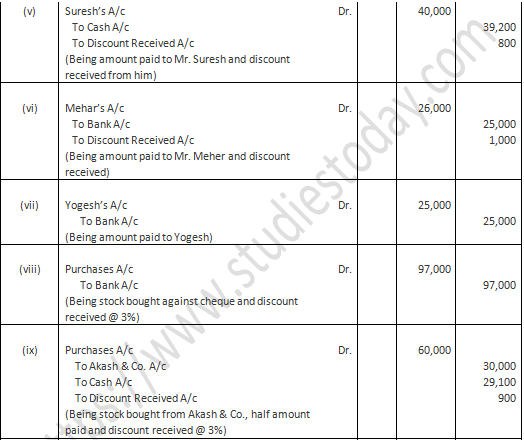

Question 18: Journalise the following transactions in the books of Bhushan Agencies:

(i) Received from Bharat cash Rs 20,000, allowed him discount of Rs 500.

(ii) Received from Vikas Rs 35,000 by cheque, allowed him discount of Rs 750.

(iii) Received from Akhil Rs 38,000 in settlement of his dues of Rs 40,000 in cash.

(iv) Received from Amrit Rs 50,000 by cheque on account against dues of Rs 60,000.

(v) Paid cash Rs 40,000 to suresh, availed discount of 2%.

(vi) Paid by cheque Rs 25,000 to Mehar and settled her dues of Rs 26,000.

(vii) Paid Rs 25,000 to Yogesh by cheque on account.

(viii) Purchased goods costing Rs 1,00,000 against cheque and availed discount of 3%.

(ix) Purchased goods costing Rs 60,000 from Akash & Co., paid 50% immediately availing 3% discount.

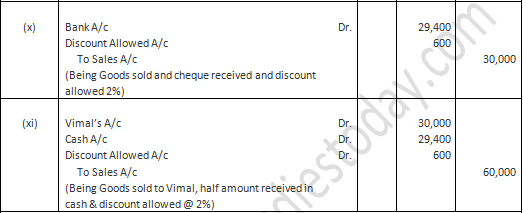

(x) Sold goods of Rs 30,000 against cheque allowing 2% discount.

(xi) Sold goods of Rs 60,000 to Vimal received 50% of due amount allowing 2% discount.

Answer 18:

Statement showing Journal Entries of Bhushan Agenchies

Points of Knowledge:-

- In 4th transection amount received from amrita Rs. 50,000; amount due with her now Rs 10,000.

- Goods Purchased of Rs. 60,000. Half of it Rs. 60,000 × ½ = 30,000.

Discount received on cash payment = Rs. 30,000 × 3% = 900

Cash Amount Paid = 30,000 – 900 = Rs. 29,100

- Goods Sold of Rs. 60,000. Half of it Rs. 60,000 × ½ = 30,000.

Discount allowed on cash payment = Rs. 30,000 × 2% = 600

Cash Amount Paid = 30,000 – 600 = Rs. 29,400

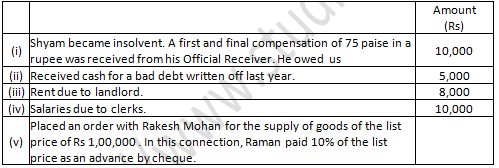

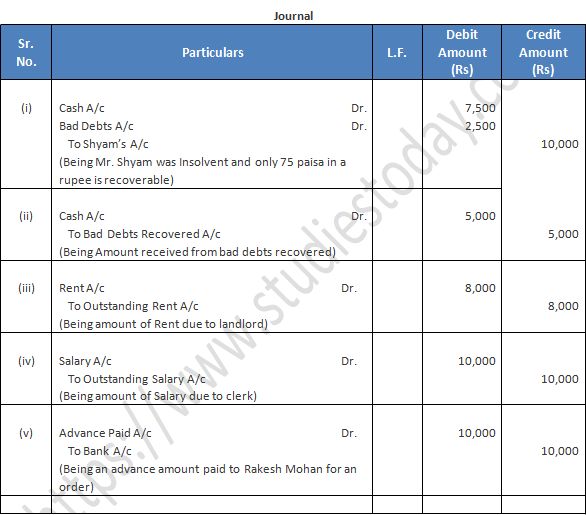

Question 19: Journalise the following transactions:

Answer 19:

Statement showing Journal Entries

Point of knowledge:-

- 1 rupee = 100 paisa

Amount recoverable = 10,000 × 75/100 = Rs. 7,500

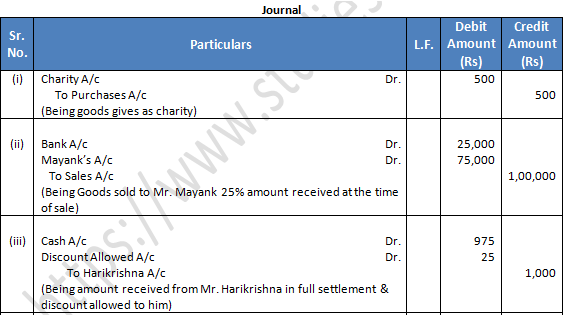

Question 20: Journalise the following entries:

(i) Goods worth Rs 500 given as charity.

(ii) Sold goods to Mayank of Rs 1,00,000, payable 25% by cheque at the time of sale and balance after 30 days of sale.

(iii) Received Rs 975 from Harikrishna in full settlement of his account for 1,000.

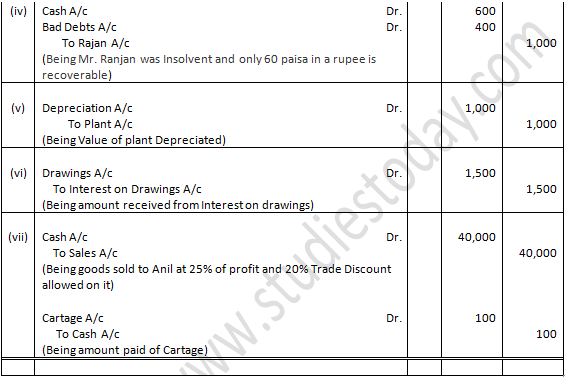

(iv) Received a first and final dividend of 60 paise in a rupee from the Official Receiver of Rajan, who owed us Rs 1,000.

(v) Charged depreciation on plant Rs 1,000.

(vi) Charge interest on Drawings Rs 1,500.

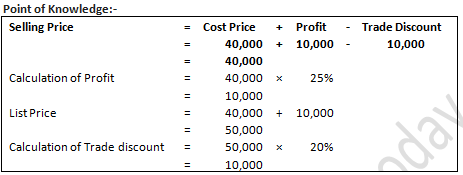

(vii) Sold goods costing Rs 40,000 to Anil for cash at a profit of 25% on cost less 20% trade discount and charged 8% Value Added Tax and paid cartage Rs 100, which is not to be charged from customer.

Answer 20:

Statement showing Journal Entries

Point of Knowledge:-

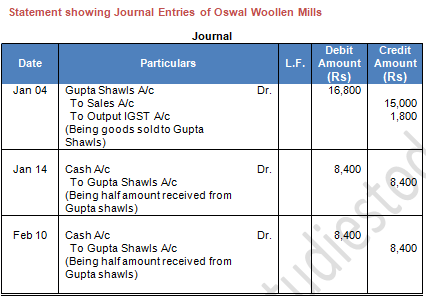

Question 21: Oswal Woollen Mills, Amritsar (Punjab) sold shawls to Gupta Shawls, Jaipur as per details: Sold 100 shawls @ Rs 200 per shawl on 4th January, 2019, IGST is levied @ 12%. Trade Discount 25% and Cash Discount 5% if full payment is made within 14 days. Gupta Shawls sent 50% of the payment on 14th January, 2018 and balance payment on 14th January,2019. Pass Journal entries.

Answer 21:

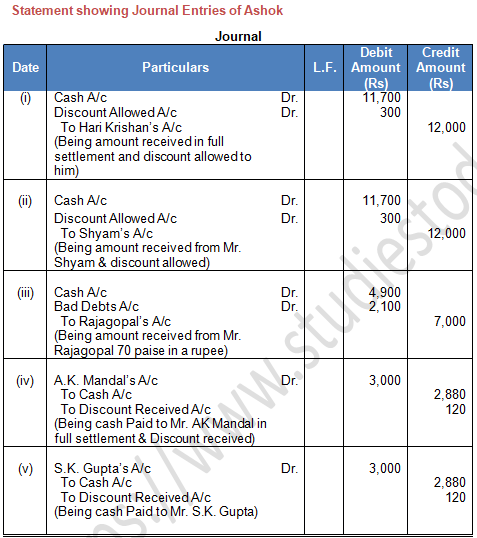

Question 22: Journalise the following transactions in the books of Ashok:

(i) Received Rs 11,700 from Hari Krishan in full settlement of his account for Rs 12,000.

(ii) Received Rs 11,700 from Shyam on his account fro Rs 12,000.

(iii) Received a first and final divident of 70 paise in the rupee from the official receiver of Rajagopal who owed us Rs 7,000.

(iv) Paid Rs 2,880 to A.K. Mandal in full settlement of his account for Rs 3,000.

(v) Paid Rs 2,880 to S.K. Gupta on his account for Rs 3,000.

Answer 22:

Question 23: Enter the following transaction in the Journal of Suresh, Delhi who trades in readymade garments:

CGST and SGST is levied @ 6% each on intra-state and purchase. IGST is levied @ 12% on inter-state sale and purchase. Out of the above, transactions marked with (*) are not subject to levy of GST.

Answer 23:

Statement showing Journal Entries of Suresh, Delhi

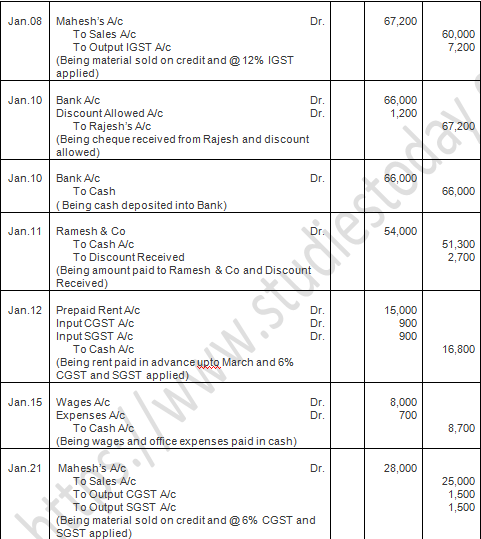

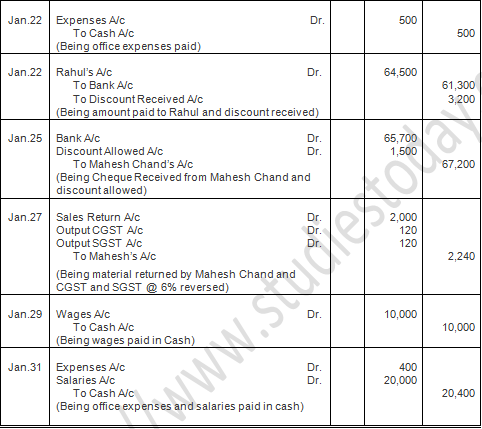

Question 24: Journalise the following transactions:

Answer 24:

Statement showing Journal Entries

Statement showing Journal Entries of Amit Saini

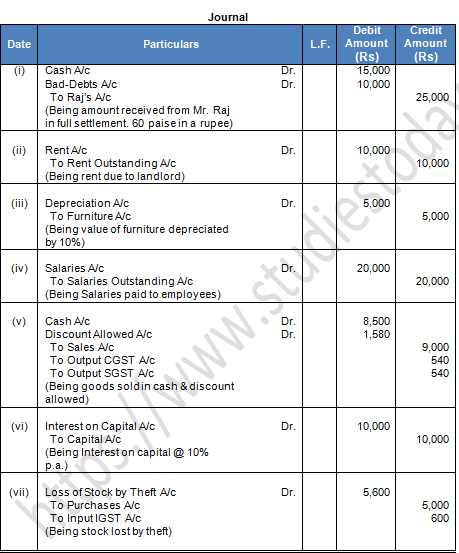

Question 26: Journalise the following transactions in the books of Mohan Singh, Delhi:

(i) Raj of Alwar, Rajasthan who owed Mohan Singh Rs 25,000 became insolvent and received 60 paise in a rupee as full and final settlement.

(ii) Mohan Singh owes to his landlord Rs 10,000 as rent.

(iii) Charge depreciation of 10% on furniture costing Rs 50,000.

(iv) Salaries due to employees Rs 20,000.

(v) Sold to Sunil goods in cash of Rs 10,000 less 10% trade discount plus CGST and SGST @ 6% each and received a net of Rs 8,500.

(vi) Provided interest on capital of Rs 1,00,000 @ 10% per annum.

(vii) Goods lost in theft−-Rs 5,000, which were purchased paying IGST @ 12% from Alwar, Rajasthan.

Answer 26:

Statement showing Journal Entries of Mohan Singh

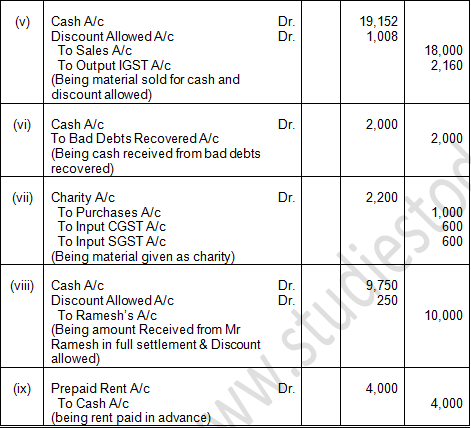

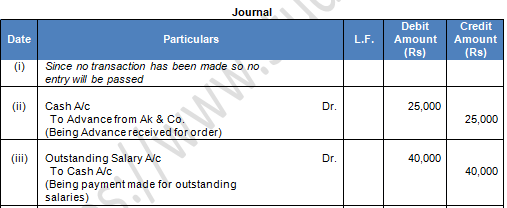

Question 27: Pass Journal entries in the books of Puneet, Delhi for the following:

(i) Received an order from Karan & Co. for supply of goods of Rs 50,000.

(ii) Received an order from AK & Co. for goods of Rs 1,00,000 along with a cheque for Rs 25,000 as advance.

(iii) Paid to staff Rs 40,000 against outstanding salary of Rs 60,000.

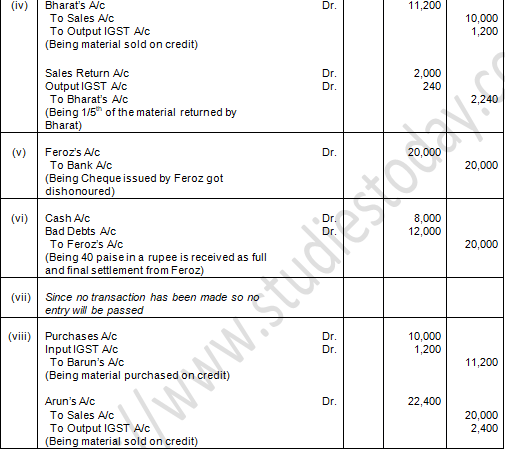

(iv) Sold goods to Bharat, Kaithal (Haryana) of Rs 10,000 plus IGST @ 12% out of which 1/5th were returned being defective.

(v) Cheque of Rs 20,000 issued by Feroz was dishonoured.

(vi) Received 40 paise in a rupee from Feroz against the above dues.

(vii) Received a cheque of Rs 25,000 from Mohan after banking hours.

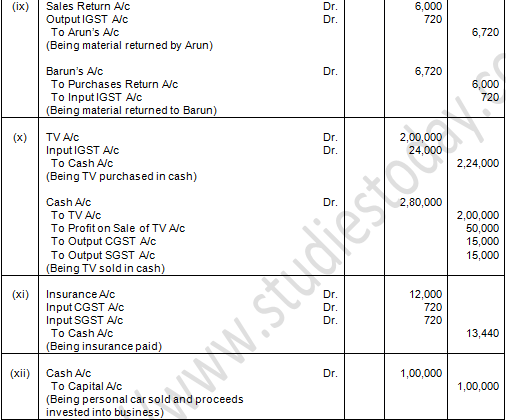

(viii) Purchased goods from Barun of Chandigarh of Rs 10,000 plus IGST @ 12% and sold them to Arun of Shimla (HP) at Rs 22,400, including IGST @ 12%.

(ix) Arun returned goods of Rs 6,720, including IGST which were returned to Barun.

(x) ABC & Co. purchased 10 TV sets @ 20,000 per set and paid IGST @ 12%. It sold all the sets @ 25,000 per set plus CGST and SGST @ 6% each.

(xi) Paid insurance of Rs 12,000 plus CGST and SGST @ 6% each for a period of one year.

(xii) Sold personal car for Rs 1,00,000 and invested the amount in the firm.

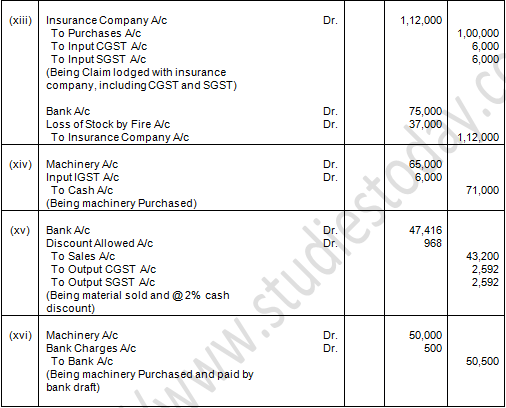

(xiii) Goods costing Rs 1,00,000 were destroyed in fire. Insurance company admitted the claim gor Rs 75,000. These goods were purchased within Delhi.

(xiv) Purchased machinery for Rs 56,000 including IGST of Rs 6,000 and paid cartage thereon Rs 5,000 and installation charges Rs10,000.

(xv) Goods costing Rs 40,000 sold to Mr. X at a profit of 20% on sales less 10% Trade Discount plus CGST and SGST @ 6% each and received a cheque under 2% cash discount.

(xvi) Purchased machinery from New Machinery House for Rs 50,000 and paid it by means of a bank draft purchased from bank. Paid charges Rs 500.

Answer 27:

Statement showing Journal Entries of Puneet

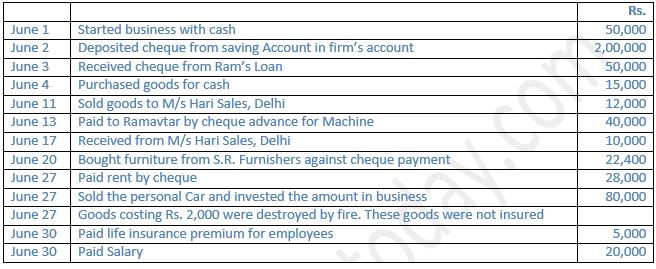

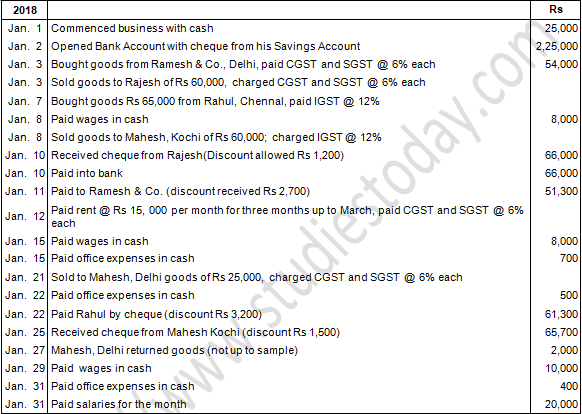

Question 28: D.Chadha commenced business on 1st January, 2017. His transactions for the month are given below. Journalise them.

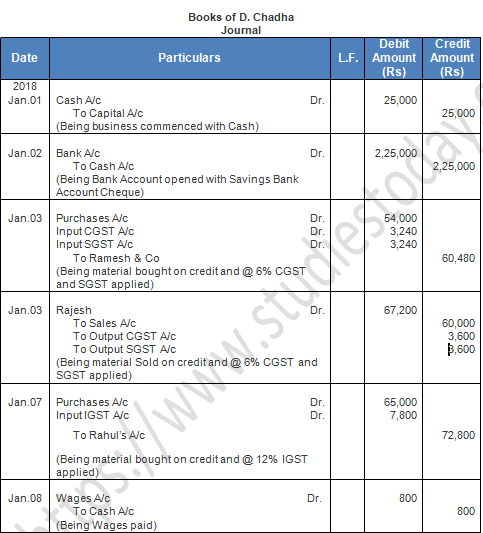

Answer 28:

Statement showing Journal Entries of D. Chadha

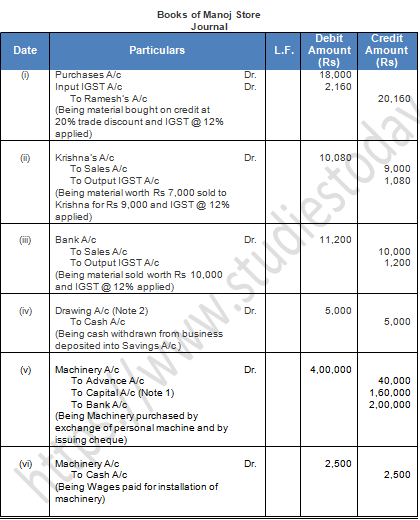

Question 29: Journalise the following transactions in the books of Manoj Store:

(i) Purchased goods from Ramesh Rs 20,000 less Trade Discount at 20% plus IGST @ 12% .

(ii) Sold goods costing Rs 7,000 to Krishna for Rs 9,000 plus IGST @ 12%.

(iii) Sold goods for Rs 10,000 and charged IGST @ 12% against cheque.

(iv) Rs 5,000 were deposited into Saving Account.

(v) Machinery costing Rs 4,00,000 for which order was placed earlier paying advance of Rs 40,000. The balance payment was paid as follows:

(a) An old machine (personal) valued at Rs 30,000 was given in exchange ;

(b) Issued a cheque from his savings account for Rs 1,30,000; and

(c) Balance by issue cheque from firm's bank account.

(vi) Paid in cash wages Rs 2,500 for installation of machine.

Answer 29:

Statement showing Journal Entries of Manoj Store

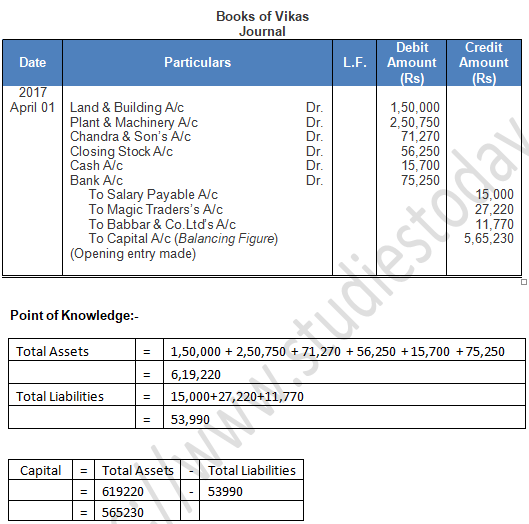

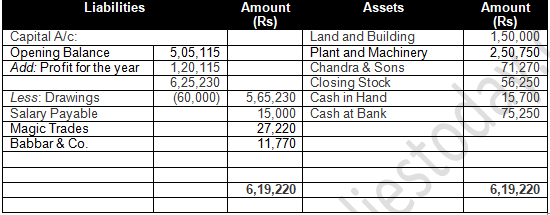

Question 30: Pass the Opening Entry from the following Balance Sheet as at 31st March, 2018 of Vikas:

Answer 30: