Access free DK Goel Solutions Class 12 Accountancy Chapter 5 Dissolution of a Partnership Firm 2026 below. Students can now access free DK Goel Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 5 Dissolution of a Partnership Firm DK Goel Solutions

Get step-by-step DK Goel Solutions for Chapter 5 Dissolution of a Partnership Firm Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 5 Dissolution of a Partnership Firm DK Goel Class 12 Solved Exercises

Short Answer Questions

Question 1.

Solution 1 Below are the circumstances under which a firm is dissolved:-

1.) When a partner has become of unsound mind.

2.) When a partner, other than the partner filing a suit, has become permanently incapable of performing his duties as a partner.

3.) When a partner, other than the partner filing a suit, is guilty of misconduct that may harm the partnership.

4.) When a partner, other than the partner filing a suit, wilfully or persistently commits breach of partnership agreement.

5.) When a partner, other than the partner filing a suit, has transferred the whole of his interests in the firm to a third party.

Question 2.

Solution 2

Question 3.

Solution 3 A ‘Realisation Account’ is opened for disposing of all the assets of the firm and making payment to all the creditors. Realisation account is a nominal account and the object of such an account is to find out the profit or loss on realisation of assets and payment of liabilities.

Question 4.

Solution 4 Amount realised from the sale of the assets of the firm shall be applied in the following manner and order:

1.) First of all, outside debts of the firm will be paid.

2.) Out of the remaining amount, the loans advanced by partners will be paid off.

3.) Thereafter the balance of Partners Capital Account will be returned.

4.) If some amount remains, it will be divided among the partners in their profit sharing ratio.

Question 5.

Solution 5

(i) When expenses are paid by the firm:

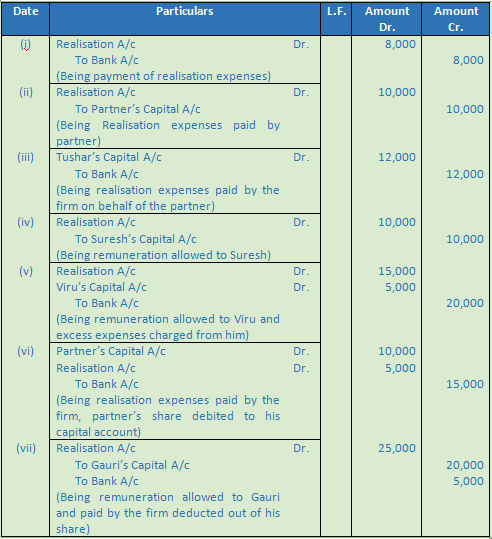

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

(iii) When the firm has agreed to pay a fixed amount to the partner towards realisation expenses and the partner has bear the expenses:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration allowed to the partner)

(iv) When realisation expenses are to be borne by the partner and the expenses are paid by the firm:

Partner’s Capital A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid on behalf of the partner)

(v) No entry will be passed if the expenses are to be borne and paid by the partner out of his pocket.

Question 6.

Solution 6

(i) When assets are sold for cash:

Cash/ Bank A/c Dr.

To Realisation A/c

(Being Assets sold for cash)

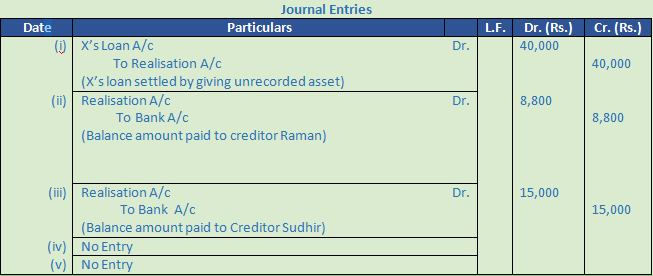

(ii) When assets is taken away by one of the partners:

Partner’s Capital A/c Dr.

To Realisation A/c

(Being Assets taken over by partner)

(iii) If an asset is given away to a Creditor in part or full payment of his dues, the agreed amount of the asset is deducted from the claim of the creditor and the balance is paid to him. No entry is passed for the transfer of assets to the creditor.

Question 7.

Solution 7 The following accounts are opened in the order to dissolution of partnership firm:-

1.) Realisation Account

2.) Partner’s Loan Account

3.) Partner’s Capital Account

4.) Cash or Bank Account

Practical Questions

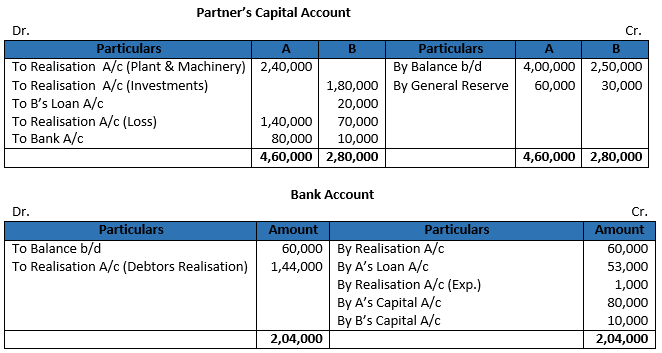

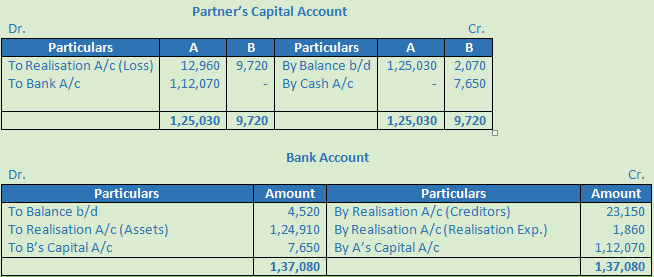

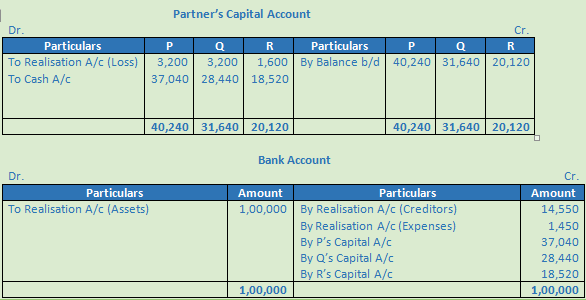

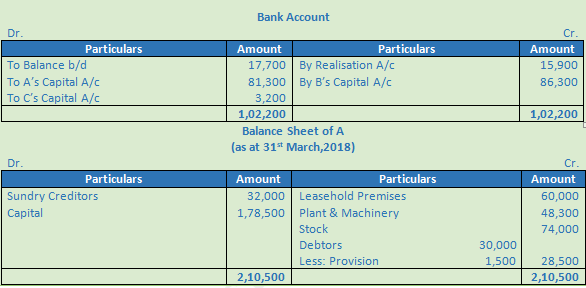

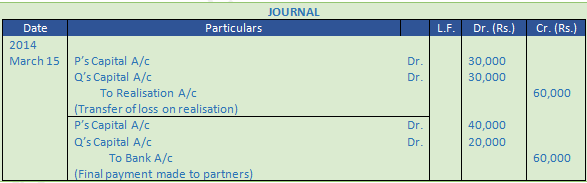

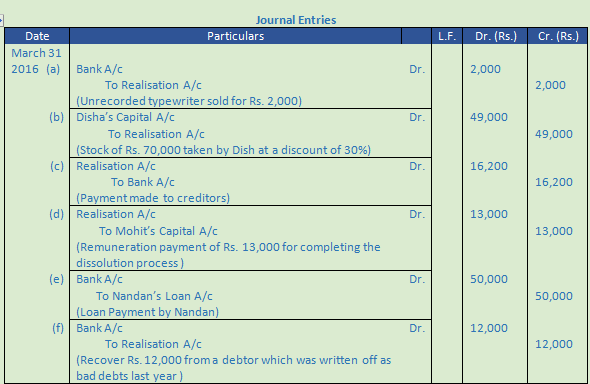

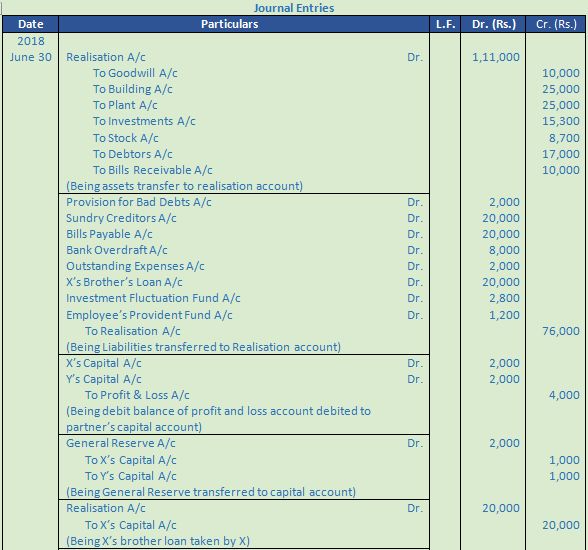

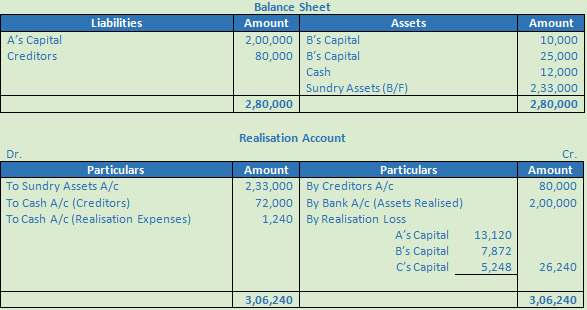

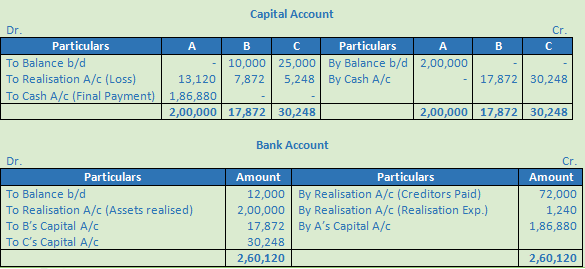

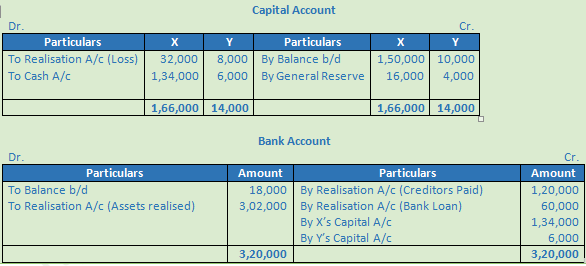

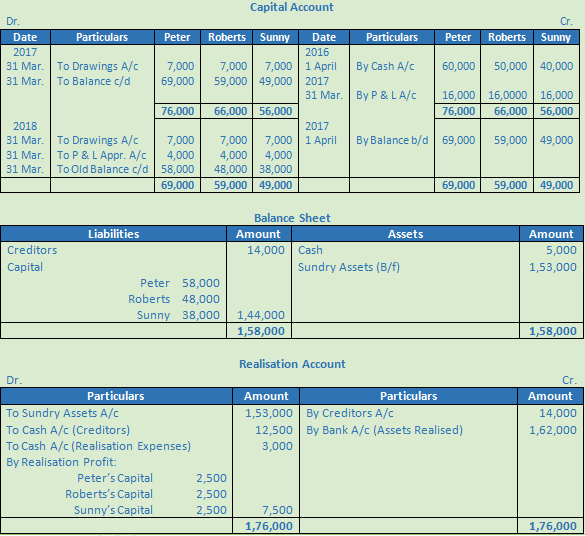

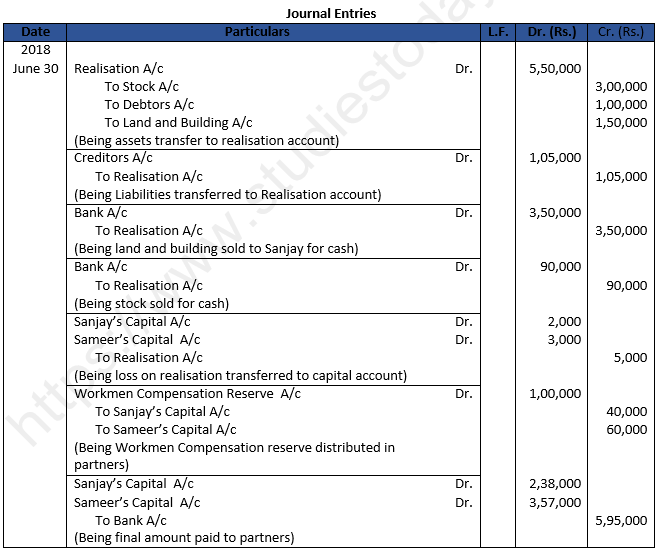

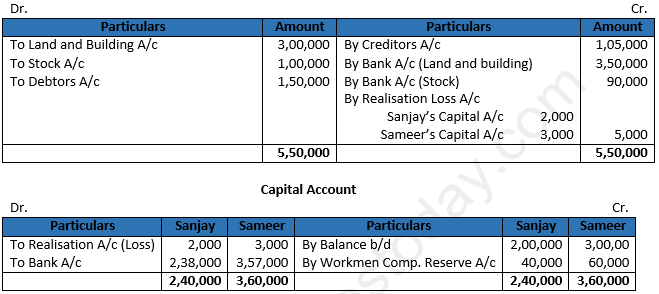

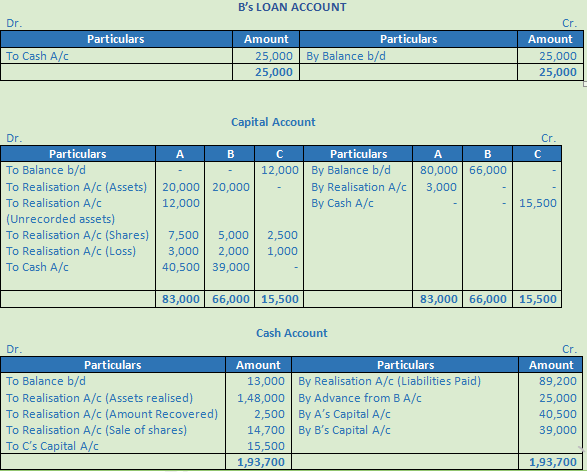

Question 1.

Solution 1

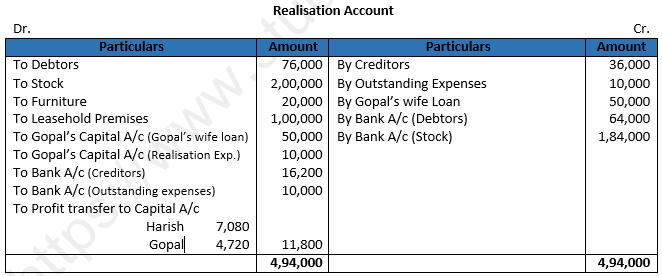

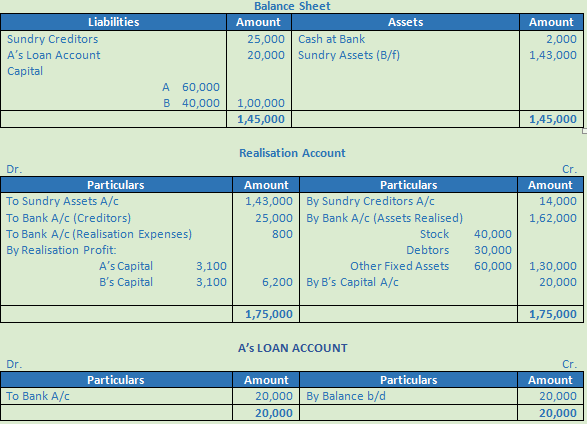

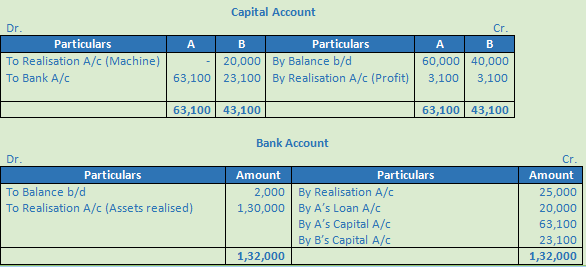

Question 2.

Solution 2

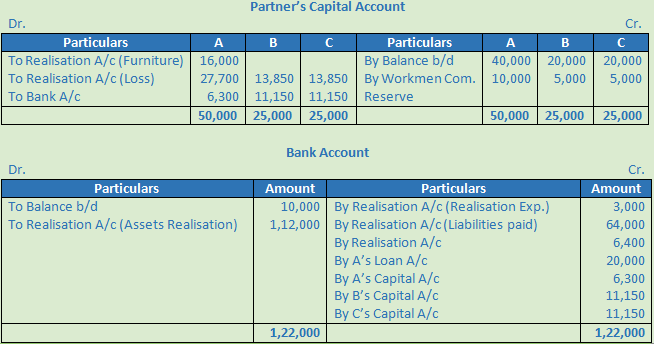

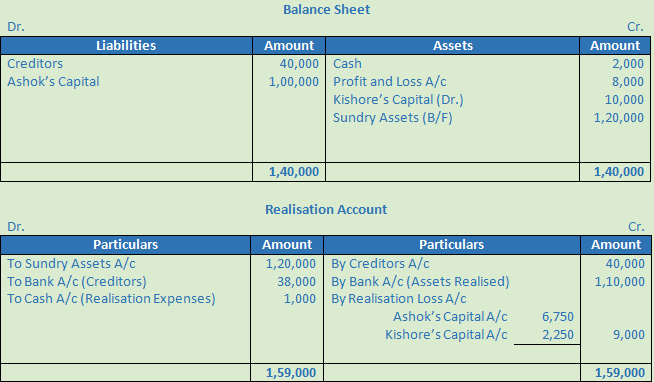

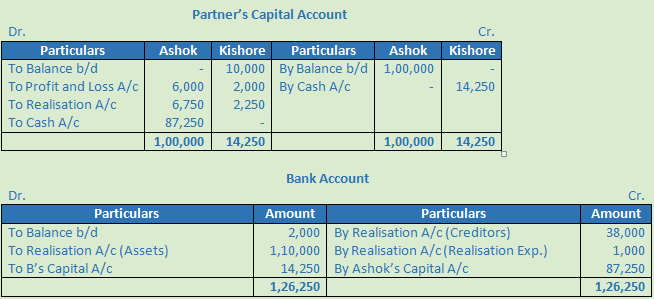

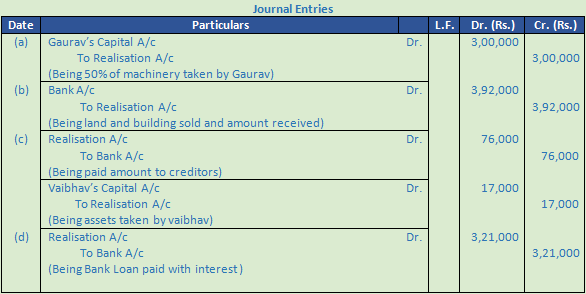

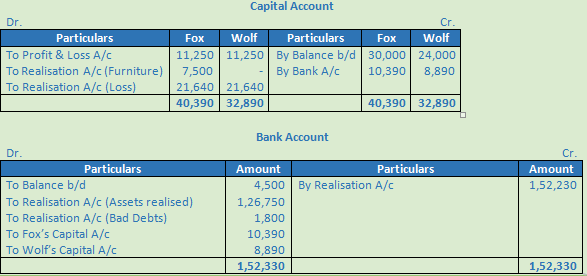

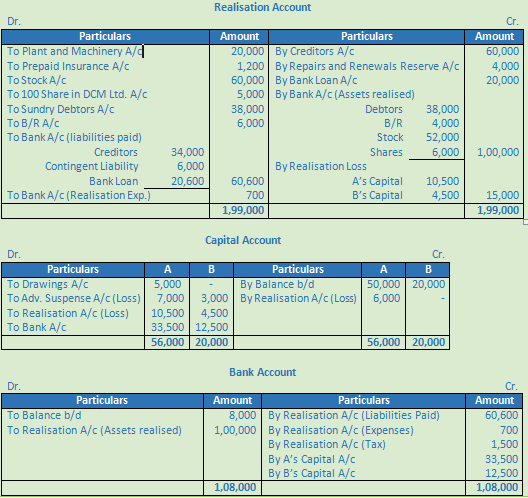

Question 3.

Solution 3

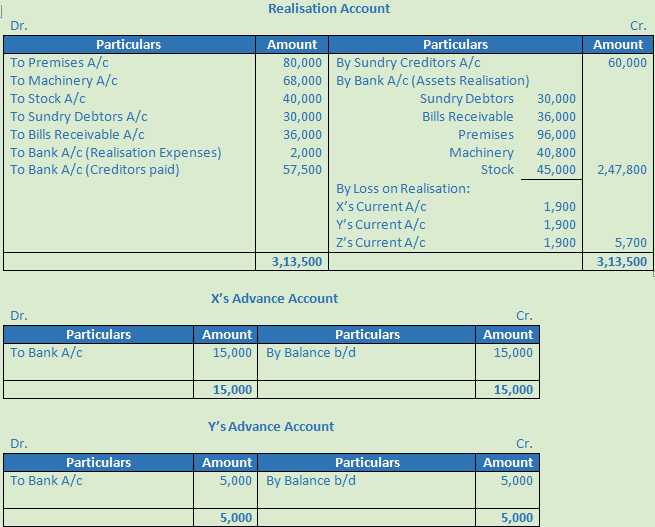

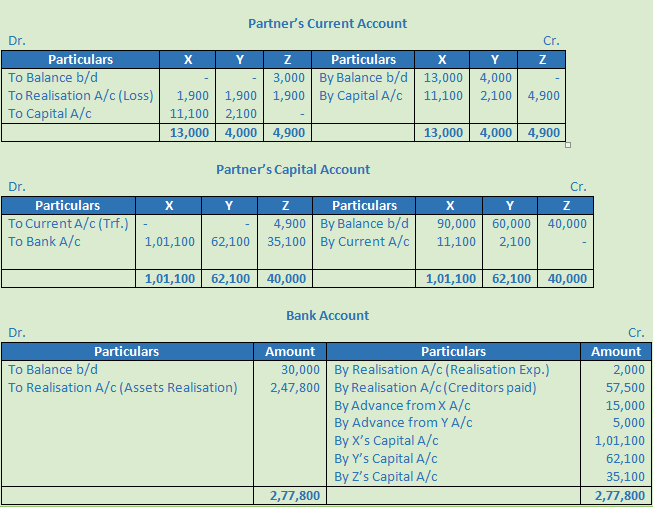

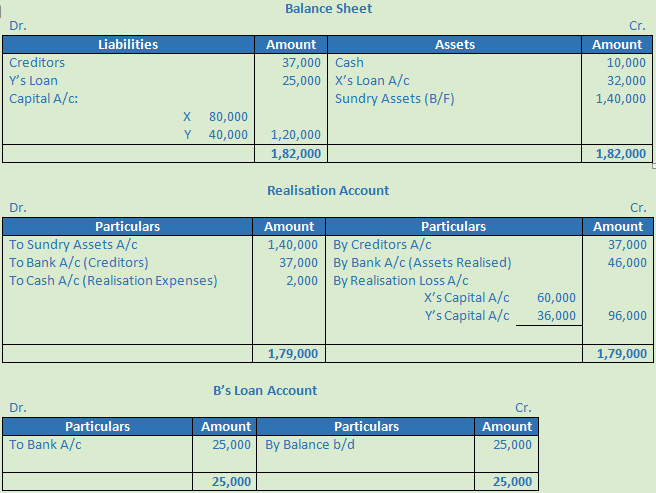

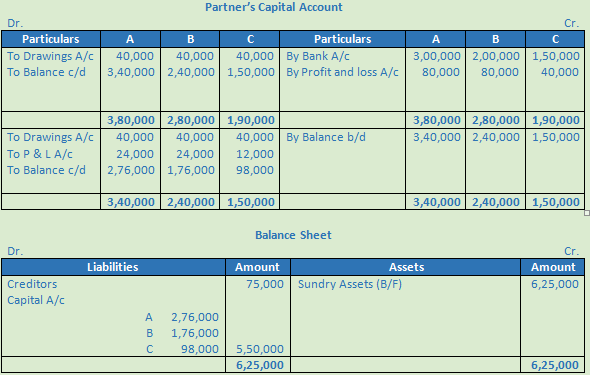

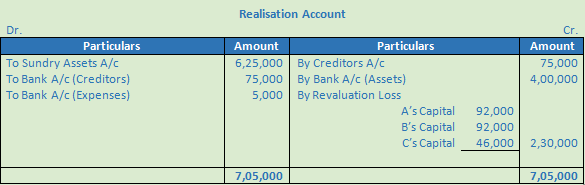

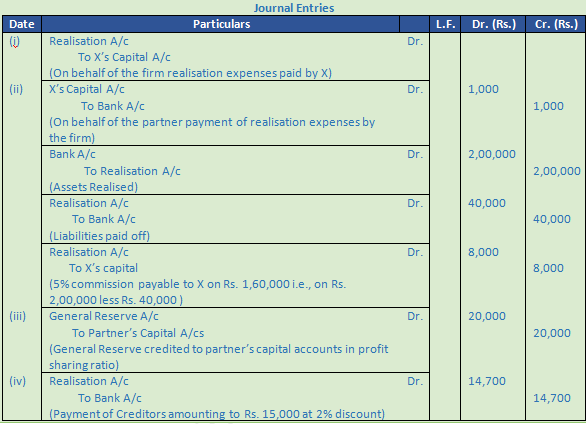

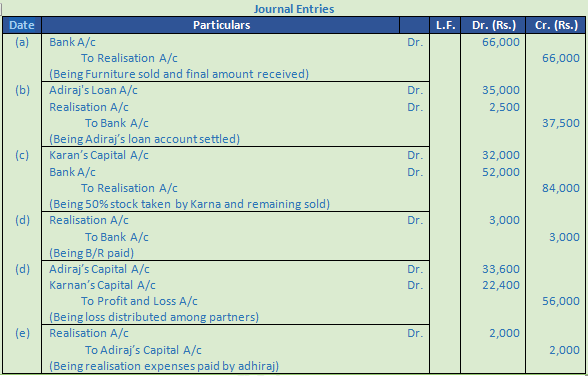

Question 4.

Solution 4

Point of Knowledge:-

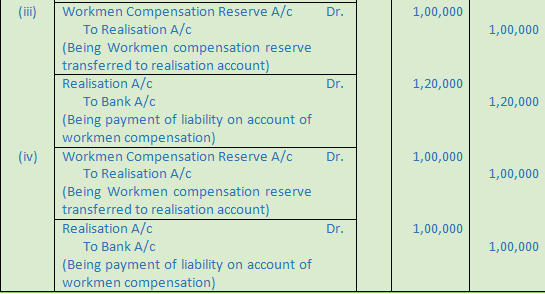

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

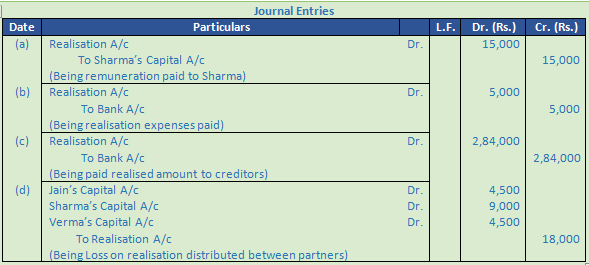

Question 5.

Solution 5

Question 6.

Solution 6.

Question 7.

Solution 7

Question 8.

Solution 8

Question 9.

Solution 9.

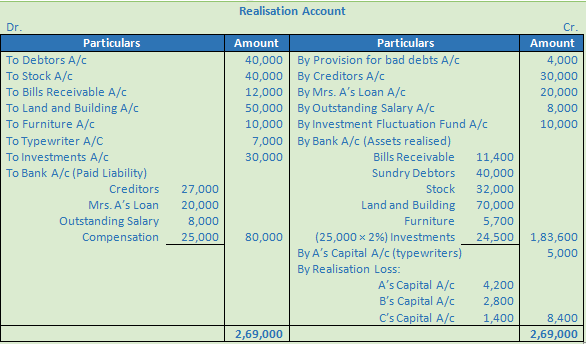

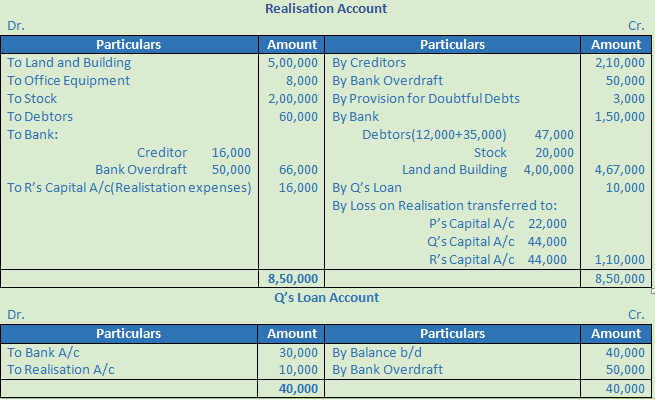

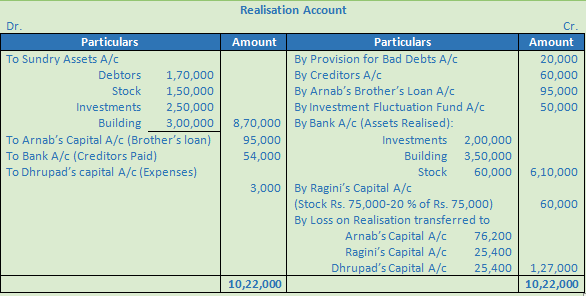

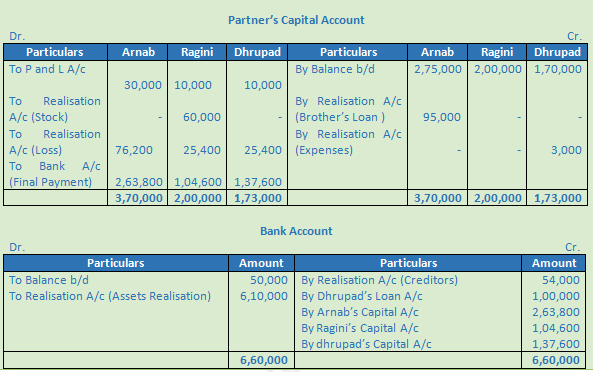

Realisation Account

For the year of 31 March, 2021

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

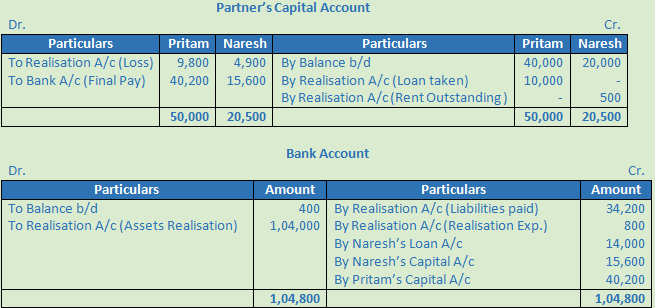

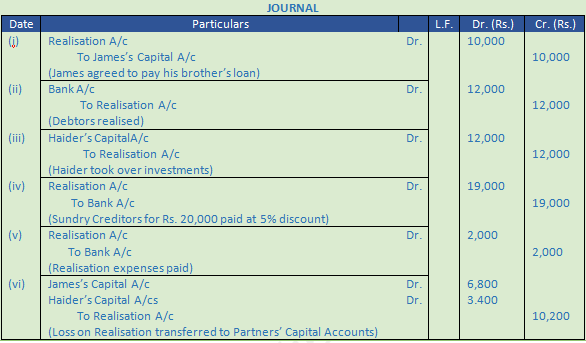

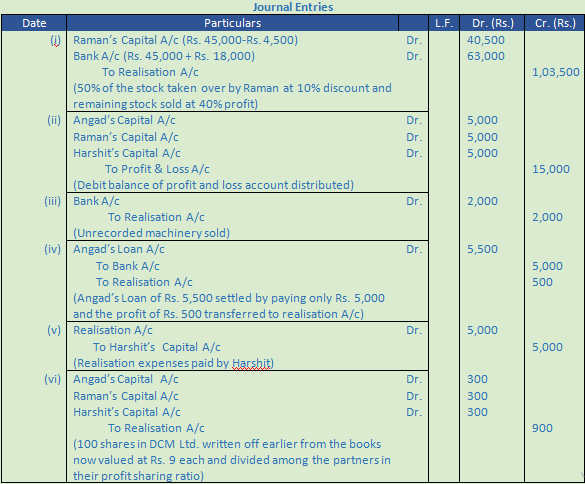

Question 10. (A)

Solution 10 (A)

Question 10. (B)

Solution 10 (B)

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

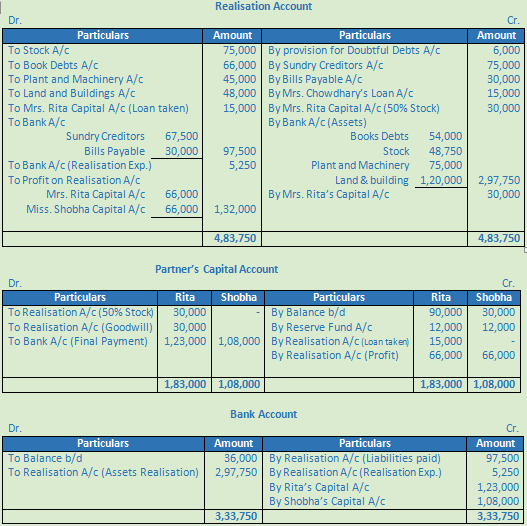

Question 11.

Solution 11

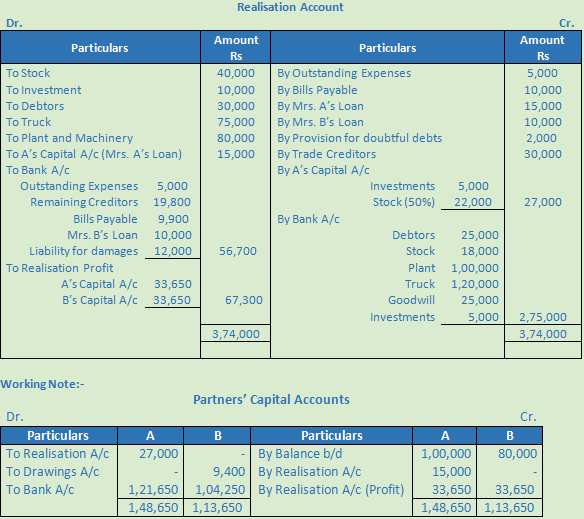

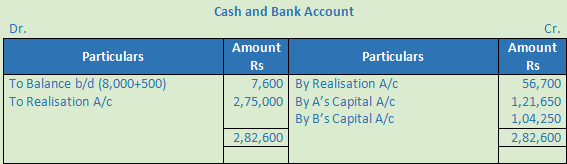

Question 12.

Solution 12

Question 13.

Solution 13

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 14.

Solution 14

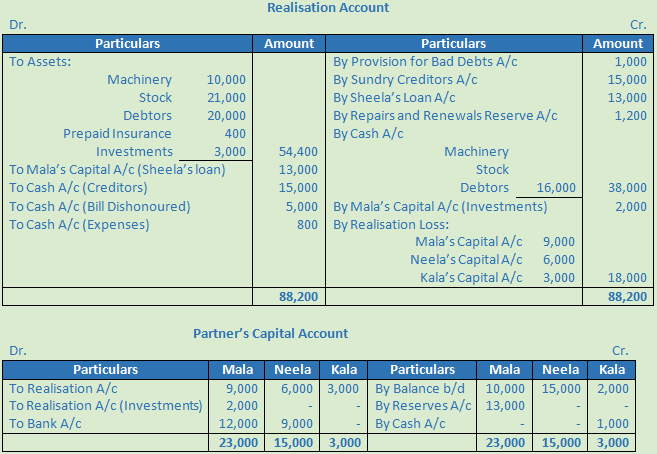

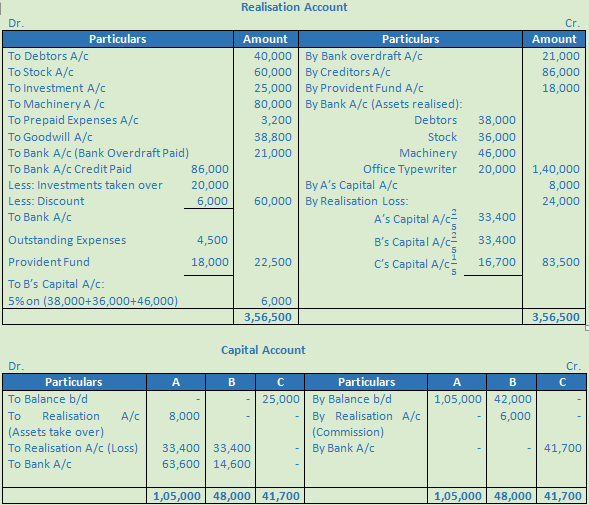

Realisation Account

as at 31 March, 2021

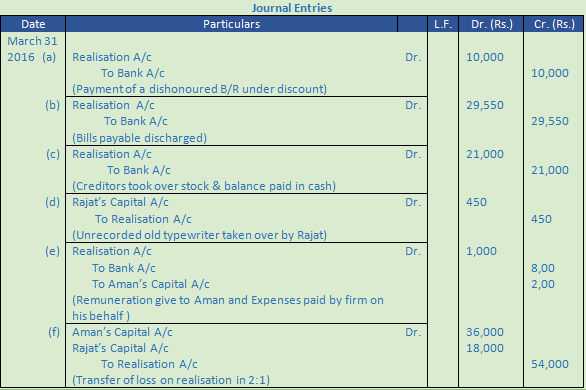

Question 15.

Solution 15

Question 16.

Solution 16

Question 17.

Solution 17

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 18.

Solution 18

Question 19.

Solution 19

Question 20.

Solution 20

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 21.

Solution 21

Question 22.

Solution 22

Question 23.

Solution 23

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 24.

Solution 24

Question 25.

Solution 25

Question 26. (A)

Solution 26 (A)

Question 26. (B)

Solution 26 (B)

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 27.

Solution 27

Question 28. (A)

Solution 28 (A)

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 28. (B)

Solution 28 (B)

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 29.

Solution 29

Question 30.

Solution 30

Question 31.

Solution 31

Question 32.

Solution 32

Question 33.

Solution 33

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 34.

Solution 34

Question 35.

Solution 35

Question 36.

Solution 36

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 37.

Solution 37

Question 38.

Solution 38

Question 39.

Solution 39

Question 40 (new).

Solution 40 (new).

Question 40.

Solution 40

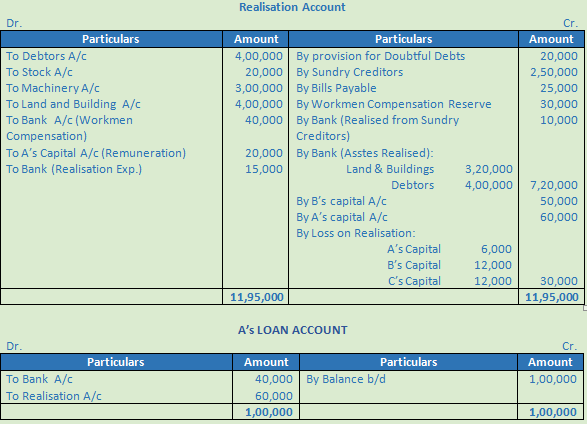

Question 41.

Solution 41

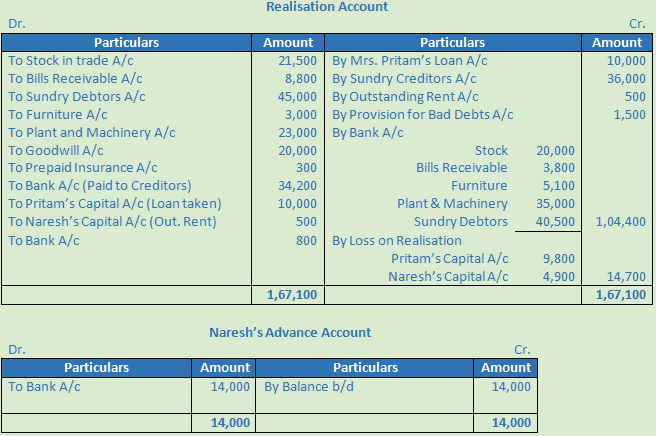

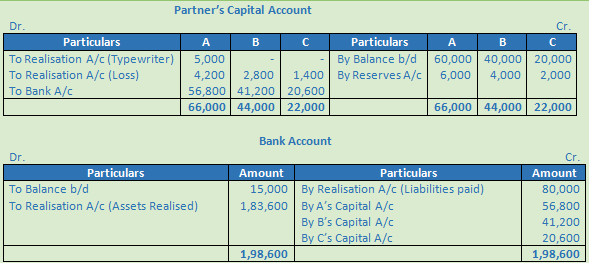

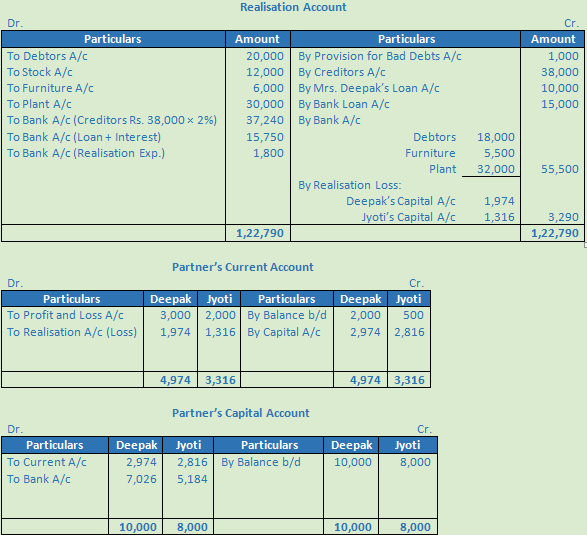

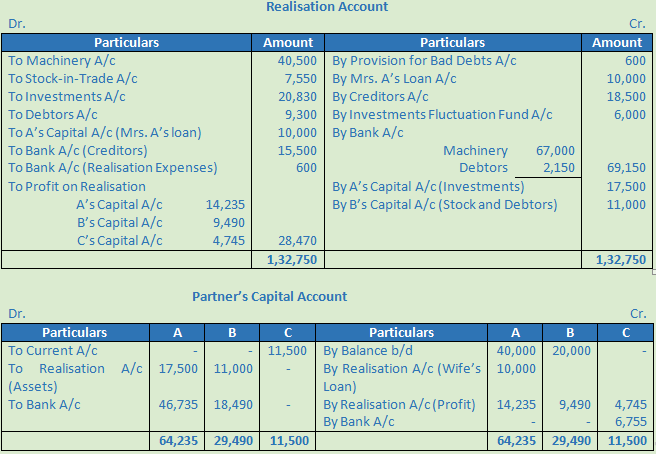

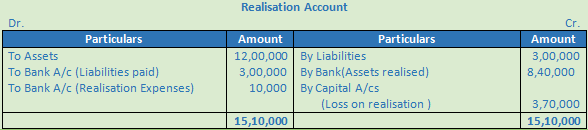

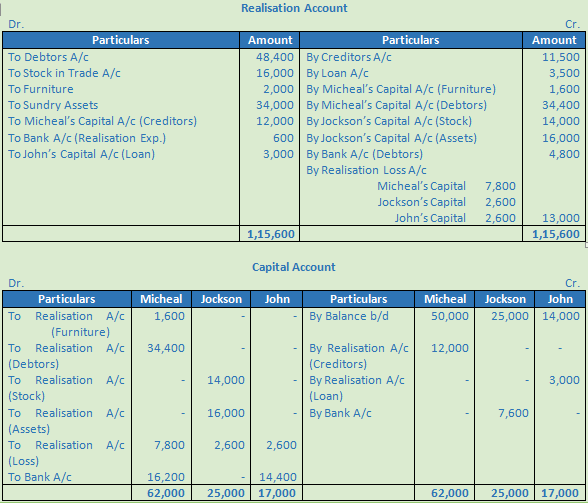

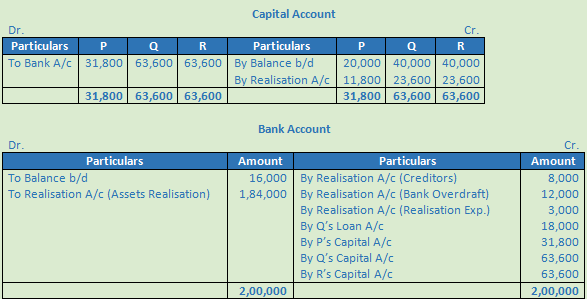

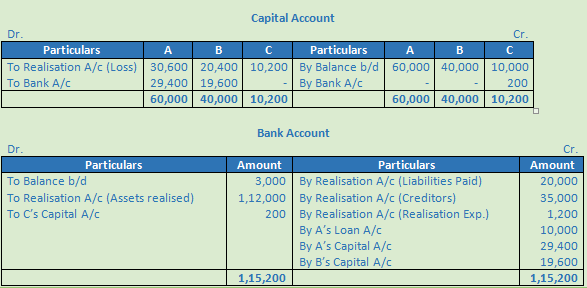

Loss on realisation can be easily calculated by preparing a realisation account:

Question 42.

Solution 42

Question 43.

Solution 43

Question 44.

Solution 44

Question 45.

Solution 45

Question 46.

Solution 46

Question 47.

Solution 47

Question 48.

Solution 48

Question 49.

Solution 49

Question 50.

Solution 50

Question 51.

Solution 51

Question 52.

Solution 52

Question 53.

Solution 53

Question 54.

Solution 54

Question 55.

Solution 55

Question 56.

Solution 56

Question 57.

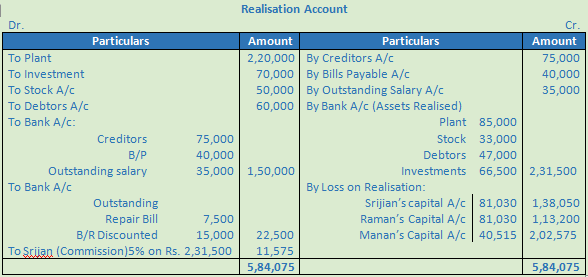

Solution 57.

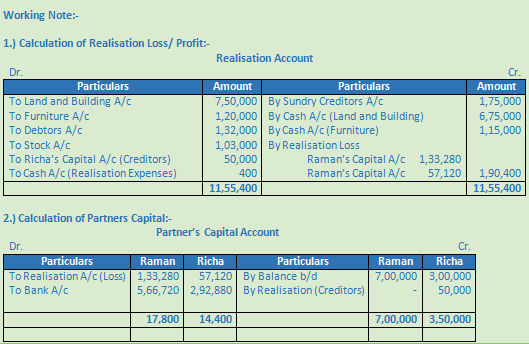

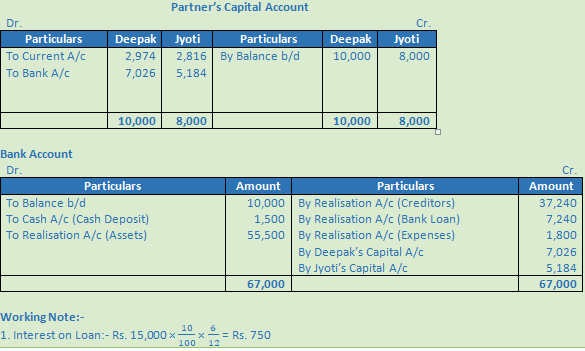

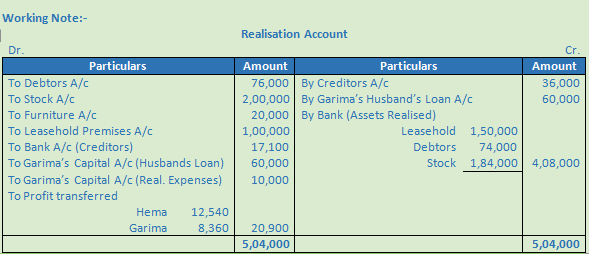

Working Note:-

Realisation Account

as at 31st March, 2021

Question 58.

Solution 58

Question 59.

Solution 59

Question 60.

Solution 60

Question 61 .

Solution ( 61).

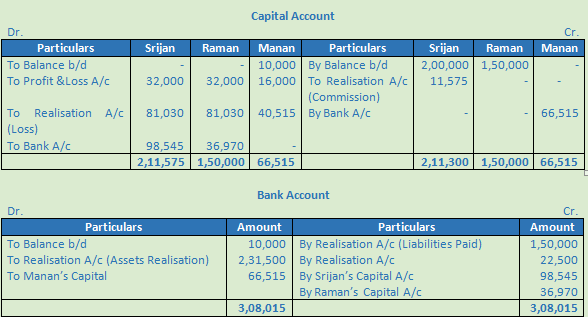

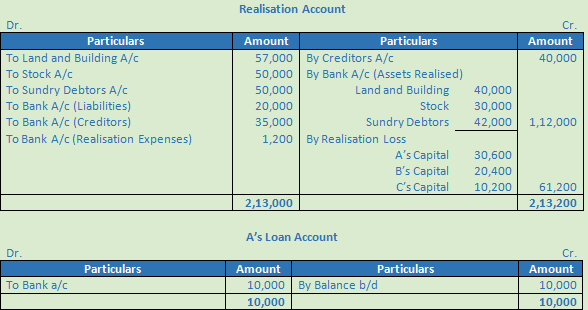

Realisation Account

As at 31st March, 2021

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 62.

Solution 62

Question 63 (new).

Solution 63 (new).

Question 63.

Solution 63

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)

Question 64 (new).

Solution 64 (new).

Question 64.

Solution 64

Question 65 (new).

Solution 65 (new).

Question 65.

Solution 65

Point of Knowledge:-

(i) When expenses are paid by the firm:

Realisation A/c Dr.

To Cash/Bank A/c

(Being Realisation expenses paid in cash)

(ii) When expenses of realisation are paid by a partner on behalf of the firm:

Realisation A/c Dr.

To Partner’s Capital A/c

(Being Remuneration expenses paid by the partner)