Access free TS Grewal Solution Class 12 Chapter 4 Accounting Ratios 2026 below. Students can now access free TS Grewal Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 4 Accounting Ratios TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 4 Accounting Ratios Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 4 Accounting Ratios TS Grewal Class 12 Solved Exercises

About this chapter: TS Grewal Solution Class 12 Chapter 4 Accounting Ratios is a very important topic in class 12 accountancy as it explains about various types of ratios which can be used to understand the financial position of an organisation. In this chapter, various formulas for calculating ratios and the meaning of each ratio has been explained in an easy to understand manner. After explanation of each ratio lot of solved questions have been provided so that the students are able to understand the meaning of the ratios as well as the process of solving the questions relating to ratios in their exams. This is a very scoring topic as once you are able to understand the meaning of the ratios and the process to derive the ratios then you will be able to solve all types of questions and get full marks. Ratio analysis is also been done by financial consultants to understand the financial performance of company. At the end of the chapter there are lot of practical and numerical questions which have been given by the author. We have provided answers to all the questions in this chapter which will help you to understand the concepts and also understand how the ratios have to be derived in a step by step manner.

Solutions for T.S. Grewal's Analysis of Financial Statements

Textbook for CBSE Class 12 TS Grewal Solutions Class 12 Accountancy

TS Grewal Solutions Class 12 Accountancy

Chapter 4 Accounting Ratios

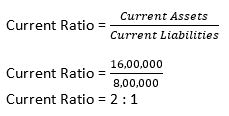

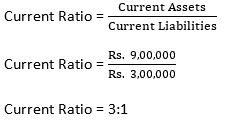

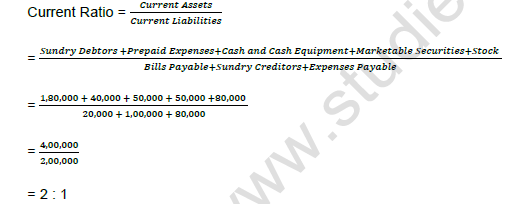

Q1. From the following compute Current Ratio:

Answer:

Current Assets = Trade Receivables + Prepaid Expenses + Cash and Cash Equivalents + Marketable Securities + Inventories

Current Assets = Rs. 7,20,000 + Rs. 1,60,000 +Rs. 2,00,000 + Rs. 2,00,000 + Rs. 3,20,000

Current Assets = Rs. 16,00,000

Current Liabilities = Bills Payables + Sundry Creditors + Expenses Payable

Current Liabilities = Rs. 80,000 + Rs. 4,00,000 + Rs. 3,20,000

Current Liabilities = Rs. 8,00,000

About Solution:

Current Ratio = (Current Assets)/(Current Liabilities)

Things to Remember:

Meaning of Accounting Ratio:

1. It is a ratio which is calculated on the basis of accounting information.

2. It can be expressed as an arithmetical relationship between two accounting variables.

3. It is a relationship that exists between figures shown in a Balance Sheet, Statement of Profit and Loss or any other statements or reports prepared by the organisation.

Important Notes:

Meaning Of Ratio Analysis:

1. It is a study of relationship among various financial factors in a business.

2. It is a technique of analysing the financial statements with the help of accounting ratio.

3. It is a process of determining and interpreting relationships between items of financial statements to provide a meaningful understanding of the financial performance and position of an enterprise.

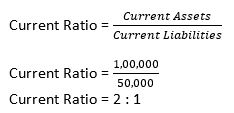

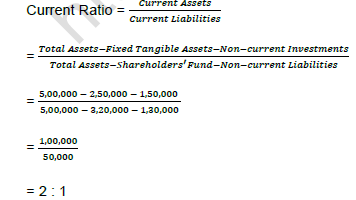

Q2. Calculate Current Ratio from the following information:

Answer:

Calculation of Current Assets:-

Current Assets = Total Assets – Fixed Tangible Assets – Non Current Investment

Current Assets = Rs. 20,00,000 – Rs. 10,00,000 – Rs. 6,00,000

Current Assets = Rs. 4,00,000

Calculation of Current liabilities:-

Current Liabilities = Total Assets – Shareholders Fund – Non-Current Liabilities

Current Liabilities = Rs. 20,00,000 – Rs. 12,80,000 – Rs. 5,20,000

Current Liabilities = Rs. 2,00,000

About Solution:

Current Ratio = (Current Assets)/(Current Liabilities)

Things to Remember:

Objectives of Ratio Analysis:

i. It simplifies understanding of financial information presented in the financial statement.

ii. It helps in determining short-term and long-term solvency of the business.

iii. t helps in assessing the operating efficiency of the business.

iv. It analyses profitability of the business.

v. It helps in comparative analysis which can be either intra-firm or inter firm comparisons.

Important Notes:

Advantages Of Ratio Analysis:

i. Tool for analysis of Financial Statements: It helps the users of financial statements to analyze the financial position of an enterprise. Such users can be bankers, investors, creditors, etc. who are concerned about the performance of an enterprise.

ii. Simplifies Accounting Data: It simplifies understanding of accounting information presented in the financial statement. Calculation of ratios summarizes briefly the results of detailed and complicated information.

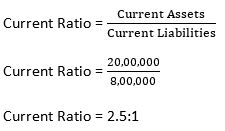

Q3. Current Assets ₹ 20,00,00, Inventories ₹ 10,00,000, Working Capital ₹ 12,00,000. Calculate Current Ratio.

Answer:

Calculation of Current Ratio:-

Calculation of Current Liabilities:-

Working Capital = Current Assets – Current Liabilities

Rs. 12,00,000 = Rs. 20,00,000 – Current Liabilities

Current Liabilities = Rs. 20,00,000 – Rs. 12,00,000

Current Liabilities = Rs. 8,00,000

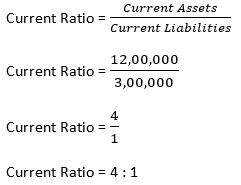

Question 4. Trade Payable Rs. 50,000, Working Capital Rs. 9,00,000, Current Liabilities Rs. 3,00,000. Calculate Current Ratio.

Answer:

About Solution:

Calculation of Working Capital:-

Working Capital = Current Assets – Current Liabilities

Rs. 9,00,000 = Current Assets – Rs. 3,00,000

Current Assets = Rs. 9,00,000 + Rs. 3,00,000

Current Assets = Rs. 12,00,000

Things to Remember:

Credit Analysis: It is useful when a firm or bank offers credit to a new customer or a dealer. Management is always interested to know credit worthiness of client so as to take decisions regarding whether to allow or extend credit to them or not.

Important Notes:

Debt Analysis: It is useful when a firm wants to know its borrowing capacity.

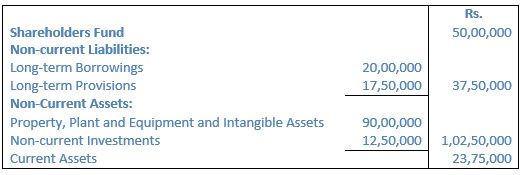

Question 5. Working Capital ₹ 6,00,000, Total Debt ₹ 27,00,000, Non-Current Liabilities ₹ 24,00,000. Calculate Current Ratio

Answer:

Calculation of Current Assets:-

Working Capital = Current Assets – Current Liabilities

Rs. 6,00,000 = Current Assets – Rs. 3,00,000

Current Assets = Rs. 3,00,000 + Rs. 6,00,000

Current Assets = Rs. 9,00,000

Calculation of Current Liabilities:-

Total Debt = Non-Current Liabilities + Current Liabilities

Rs. 27,00,000 = Rs. 24,00,000 + Current Liabilities

Current Liabilities = Rs. 27,00,000 - Rs. 24,00,000

Current Liabilities = Rs. 3,00,000

About Solution:

Working Capital = Current Assets – Current Liabilities

Things to Remember:

Since, ratios are calculated based on the financial information, if the information available is not correct ratios calculated using such information will also be incorrect. Therefore, such ratios are not completely reliable to make any future decisions for an enterprise.Only Quantitative Factors considered: Calculation of ratios takes into consideration only quantitative factors and all the related qualitative factors are ignored, which may be important for future decision making of an enterprise.

Important Notes:

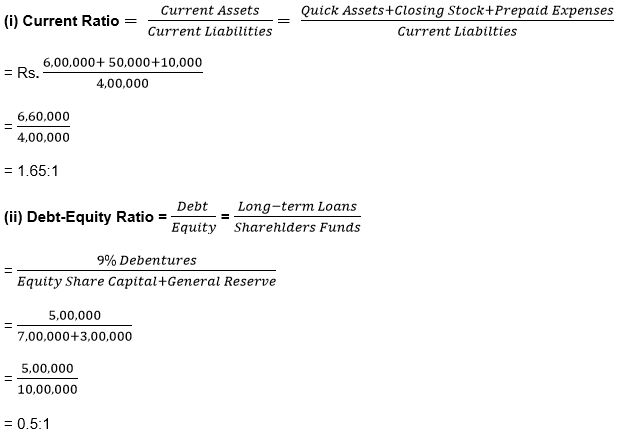

Liquidity (short-term solvency): These are the ratios which show the ability of the enterprise to meet its short-term financial obligations. It includes:

1. Current Ratio

2. Quick Ratio

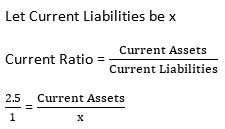

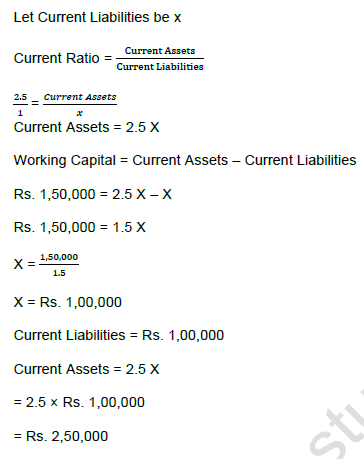

Question 6. Current Ratio is 2.5, Working Capital is Rs. 1,50,000. Calculate the amount of Current Assets and Current Liabilities.

Answer:

Current Assets = 2.5x

Working Capital = Current Assets – Current Liabilities

Rs. 1,50,000 = 2.5x – x

Rs. 1,50,000 = 1.5x

x = 1,50,000/1.5

x = Rs. 1,00,000

Current Liabilities = Rs. 1,00,000

Current Assets = 2.5x

Current Assets = 2.5 × Rs. 1,00,000

Current Assets = Rs. 2,50,000

Things to Remember:

To Assess the Short-term and Long-term Solvency Of the Enterprise: This assessment is possible by analysis the financial statements minutely. Creditors or suppliers are interested to know the ability of the entity to meet the short-term liabilities and Debenture holders and lenders are interested to know the long term and short term solvency of the enterprise to assess the ability of the company to repay the principal and interest thereon.

Important Notes:

To facilitate Inter-firm Comparison: Inter-firm Comparison helps an enterprise to assess its own performance as well as that of others if mergers and acquisitions are to be considered.

Question 7. Working Capital is Rs. 18,00,000; Trade Payable Rs. 1,80,000; and Other Current Liabilities are Rs. 4,20,000. Calculate Current Ratio.

Answer:

Calculation of Current Assets:-

Working Capital = Current Assets – Current Liabilities

Rs. 18,00,000 = Current Assets – Rs. 6,00,000

Current Assets = Rs. 18,00,000 + Rs. 6,00,000

Current Assets = Rs. 24,00,000

Calculation of Current Liabilities:-

Current Liabilities = Trade Payable + Other Current Liabilities

Current Liabilities = Rs. 1,80,000 + Rs. 4,20,000

Current Liabilities = Rs. 6,00,000

Things to Remember:

Financial Statement Analysis is largely a study of relationships among the various financial factors in a business, as disclosed by a single set of statements, and a study of trends of these factors, as shown in a series of statements.

Important Notes:

To Assess the Earning Capacity or Profitability: Earning Capacity and Profitability of the enterprise can be accessed from the financial statement analysis. It also facilitates forecasting of the same for the future years. External users are interested in earnings and hence, this is their prime objective of analyzing financial statement. ii. To Assess the Managerial Efficiency: This assessment is possible because financial statement analysis identifies the areas where managers have been efficient and where not. Favorable and unfavorable variations can be identified to pinpoint the managerial inefficiency.

Q8. Working Capital ₹ 9,00,000; Total Debts (Liabilities) ₹ 19,50,000; Long Term Debts ₹ 15,00,000. Calculate Current Ratio

Answer:

Calculation of Current Assets:-

Working Capital = Current Assets – Current Liabilities

Rs. 9,00,000 = Current Assets – Rs. 4,50,000

Current Assets = Rs. 9,00,000 + Rs. 4,50,000

Current Assets = Rs. 13,50,000

Calculation of Current Liabilities:-

Total debts = Non-Current Liabilities + Current Liabilities

Rs. 19,50,000 = Rs. 15,00,000 + Current Liabilities

Current Liabilities = Rs. 19,50,000 – Rs. 15,00,000

Current Liabilities = Rs. 4,50,000

Q9. Current Assets are Rs. 7,50,000 and Working Capital is Rs. 2,50,000. Calculate Current Ratio.

About Solution:

Calculation of Working Capital:-

Working Capital = Current Assets – Current Liabilities

Rs. 2,50,000 = Rs. 7,50,000 – Current Liabilities

Current Liabilities = Rs. 7,50,000 – Rs. 2,50,000

Current Liabilities = Rs. 5,00,000

Things to Remember:

To Forecast and Prepare Budgets: Analysis of historical data in the financial statements helps in assessing developments in future. It facilitates forecasting and preparing budgets for the future years.

Important Notes:

Security Analysis: It is a process used by the investor to identify whether the firm is fulfilling his expectations with regard to dividends, capital appreciation, etc. Such analysis is done by a security analyst who is interested in cash generating ability, dividend pay-out policy and the behavior of share prices.

Q10. A company had Current Assets of Rs. 4,50,000 and Current Liabilities of Rs. 2,00,000. Afterwards it purchased goods for Rs. 30,000 on credit. Calculate Current Ratio after the purchase.

Answer:

About Solution:

Current Assets after Purchase = Existing Current Assets + Purchased Goods

Current Assets after Purchase = Rs. 4,50,000 + Rs. 30,000

Current Assets after Purchase = Rs. 4,80,000

Current Liabilities after purchase = Existing Current liabilities + Creditors for Purchased Goods

Current Liabilities after purchase = Rs. 2,00,000 + Rs. 30,000

Current Liabilities after purchase = Rs. 2,30,000

Things to Remember:

Dividend Decision: It is useful in determining the rate of dividend in order to decide how much of the earnings are to be distributed in the form of dividends and how much is to be retained. Dividend decisions have a direct impact on profitability of the firm and behavior of its share prices so are to be taken wisely using Financial Statement Analysis.

Important Notes:

General Business Analysis: It is useful in identifying the key profit drivers and business risks in order to assess the profit potential of the firm and also assist in future growth scenarios.

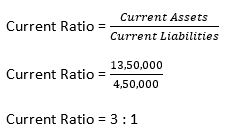

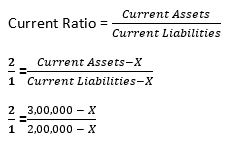

Q11. Current Liabilities of a company were Rs. 1,75,000 and its Current Ratio was 2:1. It paid Rs. 30,000 to a Creditor. Calculate Current Ratio after payment.

Answer:

Current Assets = Rs. 1,75,000 × 2

Current Assets = Rs. 3,50,000

Current Assets after Payment = Existing Current Assets – Amount Paid

Current Assets after Payment = Rs. 3,50,000 – Rs. 30,000

Current Assets after Payment = Rs. 3,20,000

Calculation of Current Liabilities:-

Current Liabilities after payment = Existing Current Liabilities – Amount paid

Current Liabilities after payment = Rs. 1,75,000 – Rs. 30,000

Current Liabilities after payment = Rs. 1,45,000

Things to Remember:

Management: Financial analysis helps the management to ascertain overall as well as segment- wise efficiency of the business. It also helps in decision making, controlling and self-evaluation.

Important Notes:

Employees and Trade Unions: Financial Analysis is considered helpful for employees to get a clear idea of the emoluments, bonus, working conditions and security of their jobs by analysis profitability, sustainability and financial position of the enterprise from its financial statements. In order to take proper decisions and enter into beneficial wage agreements, trade unions also analysis financial statements to determine the degree of profitability of the enterprise based on which they can further negotiate.

Answer:

Let the amount of Current Liabilities to be paid or the amount of current Assets to be given = X

2(2,00,000 – X) = 3,00,000 – X

4,00,000 – 2X = 3,00,000 – X

X - 2X = 3,00,000 – 4,00,000

-X = - 1,00,000

X = 1,00,000

About Solution:

We have calculated or computed as above the amount of the Current liabilities that should be paid, so that Current Ratio at the Level of 2:1 may be maintained.

Things to Remember:

Shareholder or Owners or Investors: These are the investors who invest or contribute their savings in the form of capital. Therefore, they are interested in the returns of the business which can be ascertained from the profitability of the business. Also, growth potential helps in investment appreciation.

Important Notes:

Potential Investors: These are those who are interested to know the present profitability and the financial position a well as future prospects to make their mind on investment into business concern.

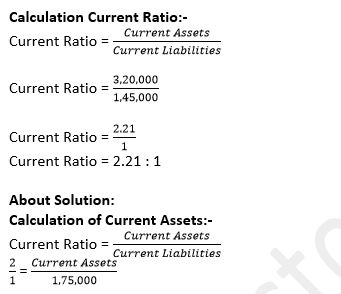

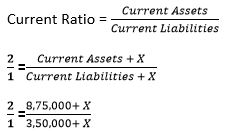

Q13. Ratio of Current Assets Rs. 8,75,000 to Current Liabilities Rs. 3,50,000 is 2:5:1. The firm wants to maintain Current Ratio of 2:1 by purchasing goods on credit. Compute amount of goods that should be purchased on Credit.

Answer:

2(3,50,000 + X) = 8,75,000 + X

7,00,000 + 2X = 8,75,000 + X

2X - X = 8,75,000 – 7,00,000

X = 1,75,000

We have calculated or computed as above the amount of the Current Assets that should be purchased, so that Current Ratio at the Level of 2:1 may be maintained.

About Solution:

The main objective of this ratio is measure the ability of firm to issue short term liability.

Things to Remember:

Suppliers or Creditors: This set of interested users are concerned whether the enterprise can make timely payments of the amounts due on account of credit transactions done with them and also whether to extend further credit to such enterprise. Such decision is based on the short term solvency of the enterprise which can be determined by analysing the financial statements of the enterprise.

Important Notes:

Bankers and Lenders: These are those parties to an enterprise who provide funds in the form of loans which is repayable at the end of a pre-determined term. In order to identify the repaying capacity of the enterprise, such parties should have a clear idea of the long-term solvency of the enterprise. Such information is obtained by analyzing financial statements of respective enterprise.

Q14. A firm had Current Assets of Rs. 5,00,000. It paid Current Liabilities of Rs. 1,00,000 and the Current Ratio became 2:1. Determine Current Liabilities and Working Capital before and after the payment was made.

Answer:

Calculation of Current Liabilities:-

Current Liabilities before payment = Rs. 3,00,000

Current Liabilities after payment = Rs. 3,00,000 – Rs. 1,00,000 = Rs. 2,00,000

Calculation of Working Capital:-

Working Capital before payment = Rs. 5,00,000 – Rs. 3,00,000 = Rs. 2,00,000

Working Capital after payment = Rs. 4,00,000 – Rs. 2,00,000 = Rs. 2,00,000

About Solution:

Formula for current ratio:

Current Ratio = Current Assets/Current Liabilities

Things to Remember:

Researchers: Parties engaged into research activity and wish to perform the same over the business entities so as to analyze the profitability, growth and financial position of an enterprise. To gather information on such areas, they are interested in analyzing respective aspects of such areas which includes data related to business operations, finance, human resource, etc.

Important Notes:

Tax Authorities: Tax Authorities are interested in ensuring proper assessment of tax liabilities of the enterprise as per the tax laws in force from time to time.

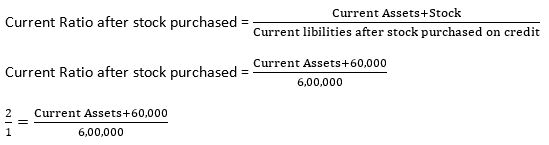

Q15. A firm had current Liabilities of ₹ 5,40,000. It purchased stock of ₹ 60,000 on credit. After the purchase of stock, Current Ratio was 2:1. Calculate Current Assets and Working Capital after and before the stock was purchased.

Answer:

Given that, Current Liabilities = Rs. 5,40,000 and stock Purchased = Rs. 60,000

Current Assets before Stock purchased = Rs. 12,00,000 – Rs. 60,000

Current Assets before Stock purchased = Rs. 11,40,000

Current Liabilities after stock purchased on credit = Rs. 5,40,000 + Creditors of stock

Current Liabilities after stock purchased on credit = Rs. 5,40,000 + Rs. 60,000

Current Liabilities after stock purchased on credit = Rs. 6,00,000

Current Assets after stock purchased = Current Assets before stock purchased + Stock

Current Assets after stock purchased = Rs. 11,40,000 + Rs. 60,000

Current Assets after stock purchased = Rs. 12,00,000

Working Capital before purchased = Current Assets before purchased – Current liabilities before purchased

Working Capital before purchased = Rs. 11,40,000 – Rs. 5,40,000

Working Capital before purchased = Rs. 6,00,000

Working Capital before purchased = Current Assets after purchased – Current liabilities after purchased

Working Capital before purchased = Rs. 12,00,000 – Rs. 6,00,000

Working Capital before purchased = Rs. 6,00,000

About Solution:

Current ratio is a part of Liquidity ratio. Liquidity Ratio has two parts:

a) Current Ratio

b) Quick Ratio / Liquidity Ratio

Things to Remember:

Internal Analysis: This is a detailed and accurate type of analysis done by the management of the enterprise to determine the financial position and operational efficiency of the organisation. Since, management has access of complete information, they perform an extensive type of analysis which is more detailed and accurate.

Important Notes:

Horizontal Analysis: It is also known as Dynamic Analysis. It is done to review and analyse financial statement for a number of years and hence, is also known as time series analysis. It facilitates comparison of financial data for several years against a chosen base year.

Q16. State giving reason, whether the Current Ratio will improve or decline or will have no effect in each of the following transactions if Current Ratio is 2:1:

(a) Cash paid to Trade Payables.

(b) Bills Payable discharged.

(c) Bills Receivable endorsed to a creditor.

(d) Payment of final Dividend already declared.

(e) Purchase of Stock-in-Trade on credit.

(f) Bills Receivable endorsed to a Creditor dishonoured.

(g) Purchases of Stock-in-Trade for cash.

(h) Sale of Fixed Assets (Book Value of Rs. 50,000) for Rs. 45,000.

(i) Sale of Fixed Assets (Book Value of Rs. 50,000) for Rs. 60,000.

Answer:

About Solution:

Idol ratio for current ratio is 2:1. If current asset is more than current liability it’s used to find solvency of a company.

Things to Remember:

Customers: Customers have an interest in information about the continuance of an enterprise. This is particularly when they are either dependent on the enterprise or they have a long term involvement with the enterprise.

Important Notes:

External Analysis: This type of analysis is done by investors, credit agencies, researchers, etc. who do not have access to the confidential and complete records of an enterprise and therefore, have to depend on information published in various statements or reports which shall comprise of Statement of Profit and Loss, Balance Sheet, Auditor's Reports etc.

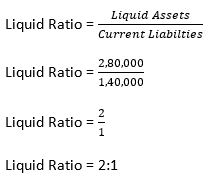

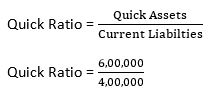

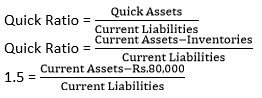

Q17. From the following information, calculate Liquid Ratio:

Answer:

Calculation of Liquid Ratio:-

Calculation of Liquid Assets:-

Liquid Assets = Current Assets – Inventories – Prepaid Expenses

Liquid Assets = Rs. 4,00,000 – Rs. 1,00,000 – Rs. 20,000

Liquid Assets = Rs. 2,80,000

Things to Remember:

Vertical Analysis: It is also known as Static Analysis. It is done to review and analyse the financial statements of one year only. It is useful in comparing the performance of several companies of the same type or divisions or departments in one enterprise.

Important Notes:

Inter-firm Analysis: It facilitates a comparison of two or more firms based on the various financial factors or variables that will help decide the competitiveness of the respective firms. A comparison of a single set of statements of two or more firms is termed as Cross-sectional Analysis.

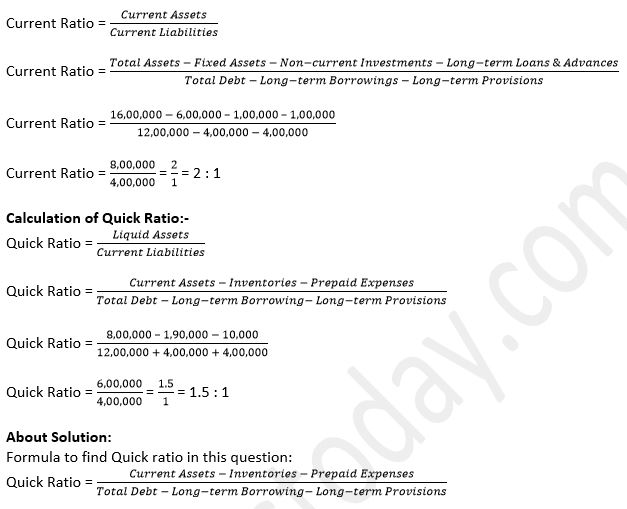

Answer:

Calculation of Quick Ratio:-

Quick Ratio = 1.5:1

Current Liabilities = Total Debt – Long term Borrowings – Long term Provisions

Current Liabilities = Rs. 12,00,000 – Rs. 4,00,000 – Rs. 4,00,000

Current Liabilities = Rs. 4,00,000

Current Assets = Total Assets – Property, Plant and Equipment – Non-Current Investments – long term Loans and Advances

Current Assets = Rs. 16,00,000 – Rs. 6,00,000 – Rs. 1,00,000 – Rs. 1,00,000

Current Assets = Rs. 8,00,000

Quick Assets = Current Assets – Prepaid Expenses – Inventories

Quick Assets = Rs. 8,00,000 – Rs. 10,000 – Rs. 1,90,000

Quick Assets = Rs. 6,00,000

Things to Remember:

Interpretation: This is the concluding part of the financial statement analysis. The interpretation should be precise and directed towards indicating the movement if various financial characteristics.

Important Notes:

Comparative Statements:

i.) It means a comparative study of individual components or elements or items of Balance Sheet and Statement of Profit or Loss for two or more years.

ii.) At first, the value of each component or element or item of two or more financial years is placed alongside each other.

iii.) After this, differences between the two amounts are determined.

iv.) Lastly percentage change in the amount from the base year is ascertained. Such comparative statements can be Intra-Firm or Inter-Firm Comparisons.

Q19. Quick Assets Rs. 3,00,000; Inventory (Stock) Rs. 80,000; Prepaid Expenses Rs. 20,000; Working Capital Rs. 2,40,000. Calculate Current Ratio.

Answer:

Calculation of Current Assets:-

Current Ratio = (Current Assets)/(Current Liabilties)

Current Ratio = 4,00,000/1,60,000

Current Ratio = 2.5:1

Calculation of Current Assets:-

Current Assets = Quick Assets + Stock + Prepaid Expenses

Current Assets = Rs. 3,00,000 + Rs. 80,000 + Rs. 20,000

Current Assets = Rs. 4,00,000

Calculation of Current Liabilities:-

Current Liabilities = Current Assets – Working Capital

Current Liabilities = Rs. 4,00,000 – Rs. 2,40,000

Current Liabilities = Rs. 1,60,000

Things to Remember:

Intra-firm Analysis: It facilitates a comparison of the various financial variables of an enterprise over a period of time and therefore, it is also known as Time Series Analysis or Trend Analysis. It helps analyzing performance of an enterprise over a period of time.

Important Notes:

Rearrangement of Financial Statements: It is necessary to reclassify the complex data contained in the financial statement into purposive classes so that maximum desired information from every data for analysis can be obtained.

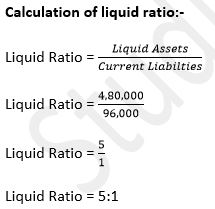

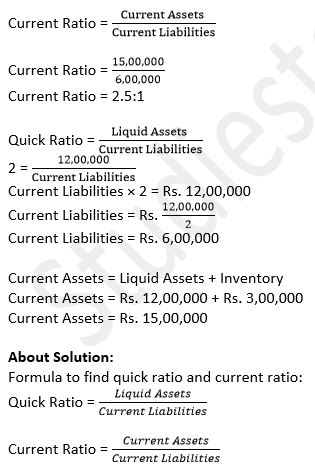

Q20. Current Assets Rs. 6,00,000; Inventories Rs. 1,20,000; Working Capital Rs. 5,04,000. Calculate Quick Ratio.

Answer:

Calculation of Liquid Assets:-

Liquid Assets = Current Assets – Inventories

Liquid Assets = Rs. 6,00,000 – Rs. 1,20,000

Liquid Assets = Rs. 4,80,000

Calculation of Current Assets:-

Current Liabilities = Current Assets – Working Capital

Current Liabilities = Rs. 6,00,000 – Rs. 5,04,000

Current Liabilities = Rs. 96,000

Things to Remember:

Comparison: Once the classification of the complex data is done, it is necessary to obtain comparative data of the same enterprise of the past periods if it is a time series analysis. If it is a cross sectional analysis, it is necessary to obtain comparative data of the same accounting period of similar or comparable enterprises.

Important Notes:

Analysis: The comparative financial data is then analyzed with reference to financial characteristics like profitability, solvency and liquidity.

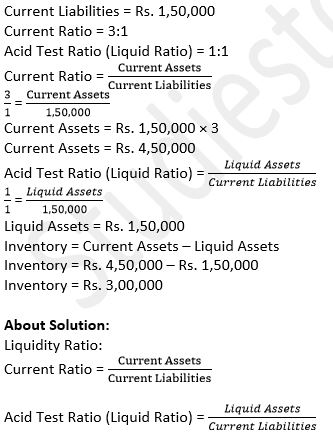

Question 21. Current Liabilities of a company are Rs. 6,00,000. Its Current Ratio is 3 : 1 and Liquid Ratio is 1 : 1. Calculate value of Inventory.

Answer:

About Solution:

Formula for calculating Liquid Ratio:

Liquid Ratio = (Liquid Assets)/(Current Liabilties)

Things to Remember:

Common Size Financial Statements:

i.) It is a vertical analysis of Financial Statements in which amounts of individual items of Balance Sheet or Statement of Profit or Loss are written. These amounts are further converted into percentages to a common base.

ii.) These percentages can be compared with the corresponding percentages in other periods and meaningful conclusions can be drawn.

iii.) Such statements may be prepared for intra-firm and inter-firm comparison.

iv.) Such statements may be prepared for Balance Sheet as well as Income Statement.

Important Notes:

Ratio Analysis:

1. It is a study of relationship among various financial factors in a business.

2. It is a technique of analyzing the financial statements with the help of accounting ratio.

3. It is a process of determining and interpreting relationships between items of financial statements to provide a meaningful understanding of the financial performance and position of an enterprise.

Question 22. Moon Ltd. has a Current Ratio of 3.5:1 and Quick Ratio of 2:1. If the Inventories is Rs. 24,000; Calculate total Current Liabilities and Current Assets.

Answer:

About Solution:

Formula to find inventory:

Inventory = Current Assets – Liquid Assets

Things to Remember:

Historical Analysis: Financial Statements are prepared using the historical information of the financial transactions that have already taken place. As a result financial statements are correctly termed as a historical record of financial transactions. Analysis of such transactions is therefore, a historical analysis. Therefore, the statement is incorrect as it makes reference to use of future data.

Important Notes:

Price Level Changes are not considered: If there is a change in the price level, analysis of financial statements of different accounting years become invalid as accounting records ignore change in value of money.

Q23. Umesh Ltd. has Current Ratio of 4.5:1 and a Quick Ratio of 3:1. If its inventory is Rs. 36,000, find out its total Current Assets and total Current Liabilities.

Answer

Inventory = Current Assets – Liquid Assets

Rs. 36,000 = 4.5 X – 3 X

Rs. 36,000 = 1.5 X

X = (36,000)/(1.5)

X = 24,000

Current Liabilities = Rs. 24,000

Current Assets = 4.5 × X

Current Assets = 4.5 × Rs. 24,000 = Rs. 1,08,000

About Solution:

Current Assets are those which can be converted into cash within short period of time.

Things to Remember:

Qualitative Aspect Ignored: Financial Statements record only monetary transactions which are quantitative in nature. Other important qualitative elements which affect the financial statements are not considered.

Important Notes:

Financial Statements Limitations: Financial Statements are not always accurate and are subject to some limitations. Since, analysis is based on the information provided by financial statements, such limitations will therefore, have an impact on the decisions taken based on the analysis of information provided by such financial statement.

Q24. Current Ratio 4; Liquid Ratio 2.5; Inventory Rs. 6,00,000. Calculate Current Liabilities, Current Assets and Liquid Assets.

Answer:

About Solution:

Current Liabilities are those which has expected too paid within one year.

Things to Remember:

Not free from bias: Financial statements are the outcome of accounting concepts and conventions combined with estimates. Estimates cannot be relied upon completely as there are chances that the amounts may fluctuate and hence, are not free from bias. Therefore, the financial statements are not completely reliable.

Important Notes:

Accounting Practices: In order to compare the profitability and the financial position of different firms, it is necessary that these firms follow same accounting practices. If different accounting practices are followed, inter-firm comparison is not possible.

Q25. Current Liabilities of a company are Rs. 1,50,000. Its Current Ratio is 3:1 and Acid Test Ratio (Liquid Ratio) is 1 : 1. Calculate values of Current Assets, Liquid Assets and Inventory.

Answer:

Things to Remember:

Window Dressing: It refers to the presentation of a better financial position than what it actually is by way of manipulating the books of accounts. Such false representation will provide misleading information for analysis which will result in wrong decision making.

Important Notes:

Symptoms: Financial statements analysis facilitates identifying symptoms or problems but it fails to provide solution or remedy for the same. Rectification of the error or problem has to be taken care of by the management based on their respective analysis.

Q26. Xolo Ltd. Liquidity Ratio is 2.5:1. Inventory is Rs. 6,00,000. Current Ratio is 4:1. Find out the Current Liabilities.

Answer:

Calculation of Inventory:-

Inventory = Current Assets – Liquid Assets

Rs. 6,00,000 = 4X – 2.5X

Rs. 6,00,000 = 1.5X

X = 6,00,000/1.5

X = Rs. 4,00,000

About Solution:

If ratio is given you need to use reverse approach for ex-

Current Asset = Liquid Assets – Inventory

Liquid Assets=Current Assets - Inventory

Things to Remember:

Comparative Financial Statements is a tool of financial analysis that shows change in each item from the base year in absolute amount and in percentage, taking the amounts for the preceding or previous accounting period as the base. Therefore, preparation of such statement is important because for the following different reasons:

1. Shareholders

2. Lenders

3. Investment Decision

Important Notes:

Aggregate Information: Financial Statements show aggregate information and not detailed information and hence, it is not that useful for the users in decision making.

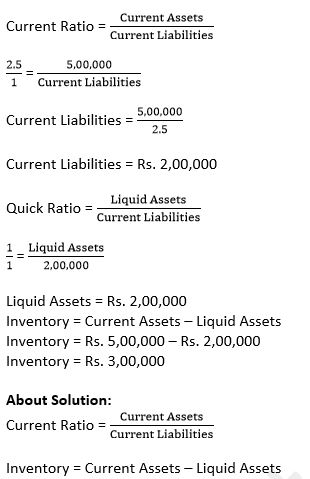

Q27. Current Assets of a company is are Rs. 5,00,000. Its Current Ratio is 2.5:1 and Quick Ratio is 1:1. Calculate value of Current Liabilities, Liquid Assets and Inventory.

Answer:

Current Assets = Rs. 5,00,000

Current Ratio = 2:5:1

Quick Ratio = 1:1

Things to Remember:

It is a statement which is used for comparing the assets, liabilities and capital and ascertaining increase or decrease in those items It is horizontal analysis of Balance Sheet in which each item of assets, equity and liabilities is analyzed horizontally for two or more accounting periods.

Important Notes:

Meaning: It is a horizontal analysis of Income Statement which shows the operating results for more than one accounting period so that changes in absolute amounts and percentages from one period to another are known. It will consist of all the items that are present in the normal Income statement like revenue from operations, cost of materials consumed, employee benefit expenses, etc. The methodology or formulae used to compute all these amounts also remain the same.

Q28. Working Capital of a company is ₹ 3,60,000; Total Debts ₹ 7,80,000; Long term debts ₹ 6,00,000; Inventories ₹ 1,80,000. Calculate Liquid Ratio.

Answer:

Liquid Ratio = (Quick Assets)/(Current Liabilities)

Liquid Ratio = 3,60,000/1,80,000

Liquid Ratio = 2:1

Calculation of Current Assets:-

Working Capital = Current Assets – Current Liabilities

Rs. 3,60,000 = Current Assets – Rs. 1,80,000

Current Assets = Rs. 3,60,000 + Rs. 1,80,000

Current Assets = Rs. 5,40,000

Total Debts = Non-Current Liabilities + Current Liabilities

Rs. 7,80,000 = Rs. 6,00,000 + Current Liabilities

Current Liabilities = Rs. 7,80,000 - Rs. 6,00,000

Current Liabilities = Rs. 1,80,000

Q29. Working Capital ₹ 4,00,000; Total Debts ₹ 18,00,000; Non-Current Liabilities ₹ 16,00,000; Inventories ₹ 1,90,000; Prepaid Expenses ₹ 10,000.

Answer:

Quick Ratio = (Quick Assets)/(Current Liabilities)

Quick Ratio = 4,00,000/2,00,000

Quick Ratio = 2:1

Total Debts = Non-Current liabilities + Current Liabilities

Rs. 18,00,000 = Rs. 16,00,000 + Current Liabilities

Rs. 18,00,000 = Rs. 16,00,000 + Current Liabilities

Current Liabilities = Rs. 18,00,000 - Rs. 16,00,000

Current Liabilities = Rs. 2,00,000

Working Capital = Current Assets – Current Liabilities

Rs. 4,00,000 = Current Assets – Rs. 2,00,000

Current Assets = Rs. 4,00,000 + Rs. 2,00,000

Current Assets = Rs. 6,00,000

Quick Assets = Current Assets – Inventories – Prepaid Expenses

Quick Assets = Rs. 6,00,000 – Rs. 1,90,000 – Rs. 10,000

Quick Assets = Rs. 4,00,000

Q30. Quick Ratio of a company is 2:1. State giving reasons, which of the following transactions would (i) improve, (ii) reduce, (iii) Not change the Quick Ratio:

(a) Purchase of goods for cash;

(b) Purchase of goods on credit;

(c) Sale of goods (costing Rs.10,000) for Rs.10,000;

(d) Sale of goods (costing Rs.10,000) for Rs.11,000;

(e) Cash received from Trade Receivables.

Answer:

The Quick Ratio of a Company is 2:1. The following are given reasons for the answers.

Quick Ratio = (Liquid Assets)/(Current Liabilities)

Quick Ratio = (Rs. 40,000)/(Rs. 20,000) = 2/1 = 2:1 (Let the expected figures be)

(a) Purchases of goods for cash will decreased cash or quick assets but will increase current assets for increase in stock. Therefore numerator of the fraction will decrease which alternatively reduce the ratio.

(b) Purchase of goods on credit will increase stock i.e., current assets but not the Liquid Assets. The creditors i.e., Current Liabilities will increase due to credit purchases. When numerator remains constant and denominator increases then quick ratio will reduce.

(c) Sale of Goods (Costing Rs. 10,000) for Rs. 10,000 will increase cash and quick assets by Rs. 10,000. The increase in numerator will improve the ratio.

(d) Sale of goods (Costing Rs. 10,000) for Rs. 11,000 will increase quick assets and cash. When only numerator of the fraction is increased the ratio will improve.

(e) Cash received from debtors will no way change quick assets. So the quick ratio will not change.

About Solution:

Formula to find quick ratio:

Quick Ratio = (Liquid Assets)/(Current Liabilities)

Things to Remember:

Meaning of Common Size Statement of Profit and Loss: A Common-size Statement of Profit and Loss may be prepared for different periods of the firm or for the same period of two firms. It shows the relative efficiency in operating the business.

Important Notes:

Objectives: Following are the Objectives of Common-size Statement of Profit and Loss:

i.) To analyze change in individual items of Income Statement.

ii.) To study the trend in different items of Incomes and Expenses. To assess the efficiency.

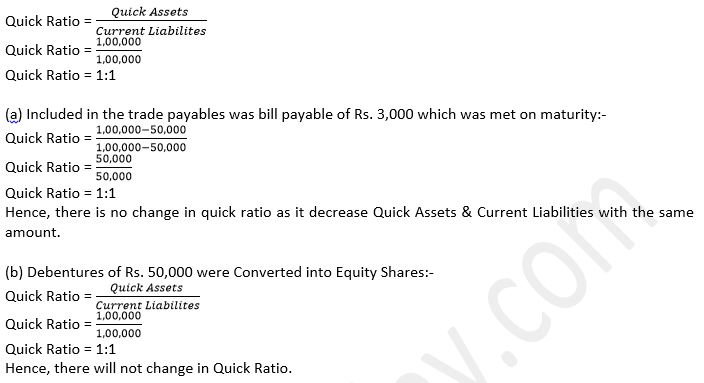

Q31: Quick Ratio of Z Ltd. is 1 : 1. State, with reason, which of the following transactions would (i) Increase (ii) Decrease or (iii) Not Change the ratio:

(a) Included in the trade payables was bill payable of ₹ 3,000 which was met on maturity;

(b) Debentures of ₹ 50,000 were converted into equity shares.

Answer:

Let’s assume Quick Assets be Rs. 1,00,000 and Current Liabilities be Rs. 1,00,000

Q32. The Quick Ratio of a company is 0.8:1. State with reason, whether the following transactions will increase, decrease or not change the Quick Ratio:

(i) Purchase of loose tools for Rs.2,000; (ii) Insurance premium paid in advance Rs.500; (iii) Sale of goods on credit Rs.3,000; (iv) Honoured a bills payable of Rs.5,000 on maturity.

Answer:

The Quick Ratio of a Company is 0.8:1. The following are given reasons for the answers.

Quick Ratio = (Liquid Assets)/(Current Liabilities)

Quick Ratio = (Rs. 8,000)/(Rs. 10,000)

Quick Ratio = 0.8/1

Quick Ratio = 0.8:1 (Let the expected figures be)

(i) Purchase of loose tools for Rs. 2,000 for cash will decrease cash or quick assets but will increase current assets for increase in loose tools. Therefore numerator of the fraction will decrease which alternatively reduce the ratio.

(ii) Insurance premium paid in advance Rs. 500 in cash will decreased cash or quick assets but will increase current assets for increase in prepaid expenses. Therefore numerator of the fraction will decrease which alternatively reduce the ratio.

(iii) Sale of goods on credit Rs. 3,000 will increase debtors and reduce stock Rs. 3,000 which alternatively increase liquid assets and reduce current assets. Therefore numerator of the fraction will increase which alternatively increase the ratio.

(iv) Honoured bill payable of Rs. 5,000 on maturity in cash will decreased cash or quick assets and decrease current liabilities. Therefore numerator and denominator of the fraction will increase which alternatively reduce the ratio.

About Solution:

Formula to find quick ratio:

Quick Ratio = (Liquid Assets)/(Current Liabilities)

Things to Remember:

Solvency (long-term solvency): These are the ratios which assess the long-term financial position of the enterprise. They assess the ability to meet the long-term financial obligations of the enterprise. It includes:

1. Debt to Equity Ratio

2. Total Assets to Debt Ratio

3. Proprietary Ratio

4. Interest Coverage Ratio

Important Notes:

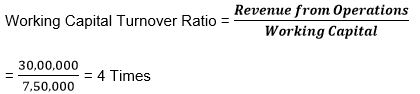

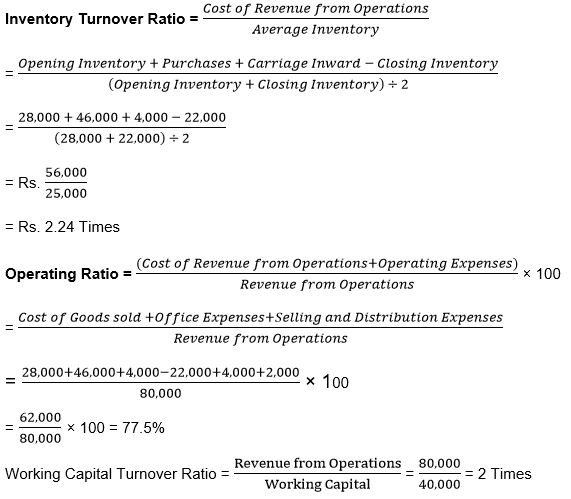

Activity/Turnover: These are the ratios which show how efficiently the enterprise resources are being used for the business operations. It includes:

1. Inventory Turnover Ratio

2. Trade Receivables Turnover Ratio

3. Trade Payables Turnover Ratio

4. Working Capital Turnover Ratio

Q33. Venus. Ltd’s Inventory is ₹ 3,00,000. Total Liquid Assets are ₹ 12,00,000 and Quick Ratio is 2 : 1. Work out Current Ratio.

Answer:

Things to Remember:

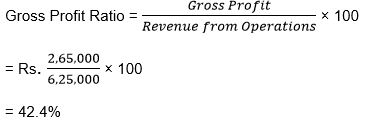

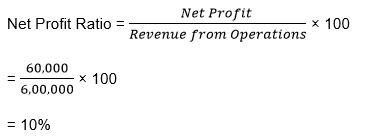

Profitability: These ratios show the profitability of the enterprise. It includes:

1. Gross Profit Ratio

2. Operating Ratio

3. Operating Profit Ratio

4. Net Profit Ratio

5. Return on Investment

Important Notes:

A liquidity ratio that measures the ability of the enterprise to pay its short-term financial obligations i.e., current liabilities.

Q34. Total Assets Rs. 11,00,000; Fixed Assets Rs. 5,00,000; Capital Employed Rs.10,00,000. There were no Long-term Investments. Calculate Current Ratio.

Answer:

Current Assets = Total Assets – Fixed Assets

Current Assets = Rs. 11,00,000 – Rs. 5,00,000

Current Assets = Rs. 6,00,000

Current Liabilities = Total Assets – Capital Employed

Current Liabilities = Rs. 11,00,000 – Rs. 10,00,000

Current Liabilities = Rs. 1,00,000

Current Ratio = (Current Assets)/(Current Liabilities)

Current Ratio = 6,00,000/1,00,000

Current Ratio = 6/1

Current Ratio = 6 : 1

About Solution:

To find current assets and current liability in this question:

Current Assets = Total Assets – Fixed Assets

Current Liabilities = Total Assets – Capital Employed

Things to Remember:

Liquidity Ratio helps to identify whether the enterprise will be able to meet its short-term financial obligations when they become due for payment.

Important Notes:

Ideal Ratio for liquidity ratio is 2 : 1. High Current Ratio means better liquidity but too high current ratio means poor operational efficiency.

Q35. Capital Employed Rs. 20,00,000; Fixed Assets Rs. 14,00,000; Current Liabilities Rs. 2,00,000. There are no Long-term Investments. Calculate Current Ratio.

Answer:

Current Ratio = Current Assets/Current Liabilities

Current Ratio = 8,00,000/2,00,000

Current Ratio = 4/1

Current Ratio = 4 : 1

Total Assets = Capital Employed + Current Liabilities

Total Assets = Rs. 20,00,000 + Rs. 2,00,000

Total Assets = Rs. 22,00,000

Total Assets = Fixed Assets + Current Assets

Rs. 22,00,000 = Rs. 14,00,000 + Current Assets

Current Assets = Rs. 22,00,000 – Rs. 14,00,000

Current Assets = Rs. 8,00,000

Things to Remember:

Current Assets: These are the assets that are either In the form of Cash and Cash Equivalents or can be converted into Cash and Cash Equivalents within 12 months from the date of Balance Sheet or within the period of operating cycle.

Important Note:

Current Assets include:

1. Short-term loans and advances,

2. Current Investments,

3. Inventories (excluding Loose Tools and Stores and Spares),

4. Trade Receivables (bills receivable and sundry debtors less provision for doubtful debts),

5. Cash and Cash Equivalents (cash in hand, cash at bank, cheques/drafts in hand, etc.)

Other Current Assets (prepaid expenses, interest receivable, etc.)

Q36. From the following Calculate: (i) Current Ratio; and (ii) Quick Ratio:

Answer:

Things to Remember:

Operating Cycle: It is the time between the acquisition of assets for processing and their realisation into Cash and Cash Equivalents. In case the normal operating cycle cannot be identified, it is assumed to be a period of 12 months.

Important Notes:

Working Capital: Where working capital is given, value of current assets and current liabilities can be ascertained using the given current ratio. Working Capital is the excess of Current Assets over Current Liabilities which is expressed as follows:

Working Capital= Current Assets - Current Liabilities; Or

Current Assets = Working Capital + Current Liabilities; Or

Current Liabilities = Current Assets - Working Capital

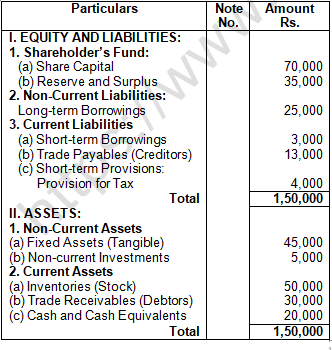

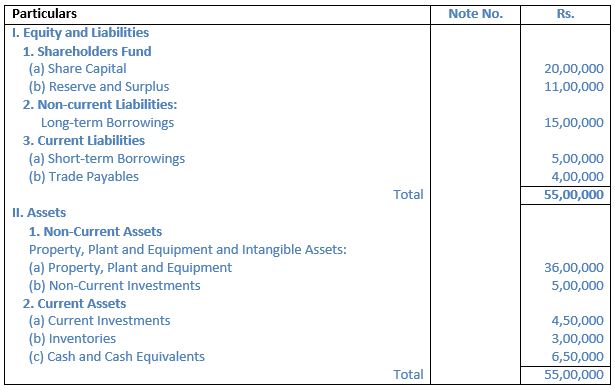

Q37. Following is the Balance Sheet of Crescent Chemical Works Limited as at 31st March, 2023:

Answer:

Calculation of Current Ratio:-

Current Ratio = Current Assets/Current Liabilities

Current Ratio = 1,00,000/20,000

Current Ratio = 5:1

Current Assets = Inventories + Debtors + Cash and Cash Equivalents

Current Assets = Rs. 50,000 + Rs. 30,000 + Rs. 20,000

Current Assets = Rs. 1,00,000

Current Liabilities = Short term borrowings + Trade Payables + Short term Provision

Current Liabilities = Rs. 3,000 + Rs. 13,000 + Rs. 4,000

Current Liabilities = Rs. 20,000

Calculation of Liquid Ratio:-

Liquid Ratio = (Liquid Assets)/(Current Liabilities)

Liquid Ratio = 50,000/20,000

Liquid Ratio = 2.5:1

Liquid Assets = Current Assets – Inventories

Liquid Assets = Rs. 1,00,000 – Rs. 50,000

Liquid Assets = Rs. 50,000

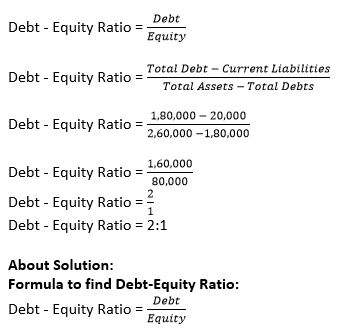

Q38. Total Assets Rs. 2,60,000; Total Debts Rs. 1,80,000; Current Liabilities Rs. 20,000. Calculate Debt to Equity Ratio.

Answer:

Things to Remember:

Such assets are shown under the head 'Current Assets' in the Balance Sheet and therefore includes:

1. Short-term Loans and Advances,

2. Current Investment,

3. Trade Receivables,

4. Cash and Cash Equivalents

5. Other Current Assets except Prepaid Expenses.

6. Inventories and Prepaid expenses are not included in Liquid assets because inventories takes time to convert in cash and cash equivalents and prepaid expenses are something that has already been paid in advance and cannot be converted into cash.

Important Notes:

Current Liabilities: These are the liabilities that are repayable within 12 months from the date of Balance Sheet or within the period of operating cycle.

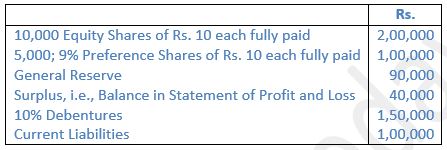

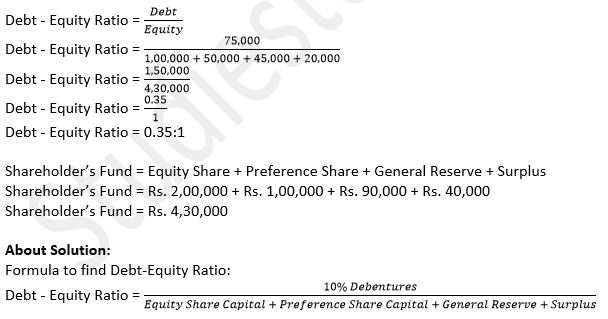

Q39. Calculate Debt to Equity Ratio: Equity Share Capital Rs. 5,00,000; General Reserve Rs. 90,000; Accumulated Profits Rs. 50,000; 10% Debentures Rs. 1,30,000; Current Liabilities Rs. 1,00,000.

Answer:

About Solution:

Working Capital= Current Assets - Current Liabilities

Current Assets = Working Capital + Current Liabilities

Current Liabilities = Current Assets - Working Capital

Things to Remember:

Understanding Liquid or Quick or Acid Test Ratio:

It is a liquidity ratio which measures the ability of the enterprise to meet its short-term financial obligations, i.e., Current Liabilities.

Important Notes:

Understanding Liquid Assets and Current Liabilities for Quick Ratio:

Liquid Assets: These are those assets that are either in the form of Cash and Cash Equivalents or can be converted into Cash and Cash Equivalent in a very short time. These are considered as the most liquid assets.

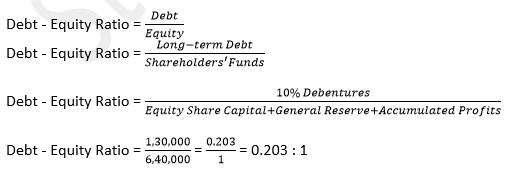

Q40. From the following information, calculate Debt to Equity Ratio:

Answer:

Things to Remember:

Current Liabilities includes the following items:

1. Short-term borrowings,

2. Short-term provision

3. Trade Payables (bills payable and sundry creditors),

4. Other Current Liabilities (current maturities of long term debts, interest accrued but not due, interest accrued and due, outstanding expenses, unclaimed dividend, calls-in advance, etc.)

Important Notes:

Debt–to–Equity Ratio is a relationship between long-term external equities, i.e., external debts (includes long term borrowings and long-term provisions) and internal equities (Shareholders' Funds) of the enterprise.

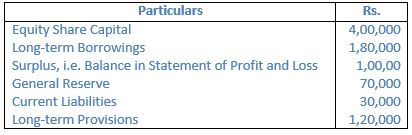

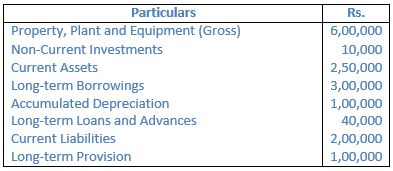

Calculate ratios indicating the long-term and the Short-term financial position of the company.

Answer:

Proprietors' Funds and Total Assets for computing Proprietary ratio:

Proprietors' Funds: This can be computed using either of the 2 approaches available as follows:

Liabilities Approach: In this approach,

Proprietors' funds = Share Capital (Equity + Preference) + Reserves and Surplus.

Assets Approach: In this approach,

Proprietors' funds = Non-current Assets + Working Capital (i.e. Current Assets - Current Liabilities) - Non-current Liabilities.

Answer:

Things to Remember:

Interest Coverage Ratio:

1. It is a relationship between Net Profit before Interest and Tax and Interest on Long Term Debts.

2. It is calculated to ascertain the amount of profit available to cover interest on long term debts.

3. For lenders a higher Interest Coverage Ratio is considered better as it signifies a higher margin to meet interest cost.

Important Notes:

Interest Coverage Ratio = Profit before interest and tax/Intrest on Long term debt

Q43. From the following information, calculate Debt to Equity Ratio: Total Debts ₹ 6,00,000; Current Liabilities ₹ 2,00,000 and Capital Employed ₹ 6,00,000.

Answer:

Debt to Equity Ratio = Debt/Equity

Debt to Equity Ratio = 4,00,000/2,00,000

Debt to Equity Ratio = 2:1

Total Debts = Non-Current Liabilities + Current Liabilities

Rs. 6,00,000 = Non-Current Liabilities + Rs. 2,00,000

Non-Current Liabilities = Rs. 6,00,000 - Rs. 2,00,000

Non-Current Liabilities = Rs. 4,00,000

Capital Employed = Equity + Non- Current Liabilities

Rs. 6,00,000 = Equity + Rs. 4,00,000

Equity = Rs. 6,00,000 - Rs. 4,00,000

Equity = Rs. 2,00,000

Q44. Calculate Debt to Equity Ratio: Total Assets ₹ 14,00,000; Total Debt ₹ 12,00,000; Capital Employed ₹ 10,00,000.

Answer:

Debt to Equity Ratio = Debt / Equity

Debt to Equity Ratio = 8,00,000/2,00,000

Debt to Equity Ratio = 4:1

Equity = Total Assets – Total Debts

Equity = Rs. 14,00,000 – Rs. 12,00,000

Equity = Rs. 2,00,000

Capital Employed = Equity + Debt (Non-Current liabilities)

Rs. 10,00,000 = Rs. 2,00,000 + Debt (Non-Current liabilities)

Debt (Non-Current liabilities) = Rs. 10,00,000 - Rs. 2,00,000

Debt (Non-Current liabilities) = Rs. 8,00,000

Q45. Capital Employed Rs. 8,00,000; Shareholders' Funds Rs. 2,00,000. Calculate Debt to Equity Ratio.

Answer:

Things to Remember:

Understanding Proprietary Ratio:

1. It is a relationship between proprietor's fund and total assets.

2. It shows the financial strength of the entity.

Important Notes:

Proprietary Ratio is an important ratio for the creditors as it helps them identify the portion of shareholders' funds in the total assets employed in the firm and also the safety margin available to them.

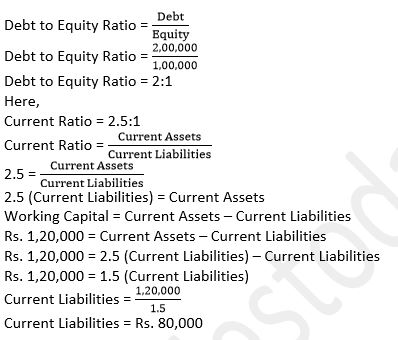

Q46. King Ltd. has Current Ratio of 2.5:1. Its Working Capital is ₹ 1,20,000. Total Assets are of ₹ 3,80,000 and Total Debt of ₹ 2,80,000. Calculate Debt to Equity Ratio.

Answer:

Debt (Non-Current liabilities) = Total Debt - Current Liabilities

Debt (Non-Current liabilities) = Rs. 2,80,000 – Rs. 80,000

Debt (Non-Current liabilities) = Rs. 2,00,000

Equity (Shareholders Fund) = Total Assets – Total Debts

Equity (Shareholders Fund) = Rs. 3,80,000 – Rs. 2,80,000

Equity (Shareholders Fund) = Rs. 1,00,000

Q47. Monica Ltd. has Quick Ratio of 1.5 : 1. Its Working Capital is ₹ 1,20,000 and its inventories are of ₹ 80,000. Total Assets of ₹ 3,80,000 and Total Debts of ₹ 2,80,000. Calculate Debt to Equity Ratio.

Answer:

1.5 (Current Liabilities) = Current Assets – Rs. 80,000

Current Assets = 1.5 (Current Liabilities) + Rs. 80,000

Working Capital = Current Assets – Current Liabilities

Rs. 1,20,000 = Current Assets – Current Liabilities

Rs. 1,20,000 = 1.5 (Current Liabilities) + Rs. 80,000 – Current Liabilities

Rs. 1,20,000 - Rs. 80,000 = 0.5 (Current Liabilities)

Rs. 40,000 = 0.5 (Current Liabilities)

0.5 (Current Liabilities) = Rs. 40,000

Current Liabilities = 40,000/0.5

Current Liabilities = Rs. 80,000

Debt to Equity Ratio = Debt/Equity

Debt to Equity Ratio = 2,00,000/1,00,000

Debt to Equity Ratio = 2:1

Debt (Non Current Liabilities) = Total Debts – Current Liabilities

Debt (Non Current Liabilities) = Rs. 2,80,000 – Rs. 80,000

Debt (Non Current Liabilities) = Rs. 2,00,000

Shareholder Fund = Total Assets – Total Debts

Shareholder Fund = Rs. 3,80,000 – Rs. 2,80,000

Shareholder Fund = Rs. 1,00,000

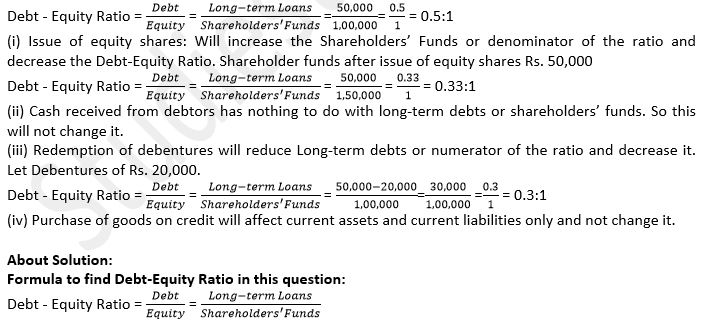

Q48. When Debt to Equity Ratio is 2, state giving reason, whether this ratio will increase or decrease or will have no change in each of the following cases:

(i) Sale of Land (Book value Rs. 4,00,000) for Rs. 5,00,000; (ii) Issue of Equity Shares for the purchase of Plant and Machinery worth Rs. 10,00,000; (iii) Issue of Preference Shares for redemption of 13% Debentures, worth Rs. 10,00,000.

Answer:

Debt - Equity Ratio = Debt/Equity = Long-term Loans/Shareholders^' Funds

(i) Sale of land (Book Value Rs. 4,00,000 for Rs. 5,00,000: Sale of Land at a Profit of Rs. 1,00,000 will increase Shareholders’ Funds. Hence Debt- Equity Ratio will decrease.

(ii) Issue of Equity Shares for the Purchase of Plant and Machinery worth Rs. 10,00,000: Issue of Equity Shares for the Purchase of Plant and Machinery will increase shareholders’ funds, hence the ratio will decrease.

(iii) Issue of Preference Share for redemption of 13% debentures, worth Rs. 1,00,000: Total Long-term debts are decreased and total Shareholders’ Fund are increased the same amount, hence the ratio will decrease.

About Solution:

Formula to find Debt-Equity Ratio:

Debt - Equity Ratio = Debt/Equity

or

Debt - Equity Ratio = (Long-term Loans)/(Shareholders^' Funds)

Things to Remember:

Debt-to-equity measures the proportion of external funds and shareholder's invested in the company.

Important Notes:

Debt-to-Equity assesses long-term financial soundness of the enterprise and indicates the extent to which the enterprise depends on borrowed funds for its business.

Q49. Debt to Equity Ratio of a company is 0.5:1. Which of the following suggestions would increase, decrease or not change it?

(i) Issue of Equity Shares: (ii) Cash received from debtors:

(iii) Redemption of debentures; (iv) Purchased goods on Credit?

Answer:

Let Long-term Loan be = Rs. 50,000 and Shareholders’ Funds = Rs. 1,00,000

Things to Remember:

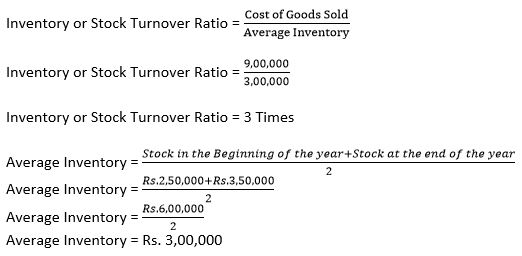

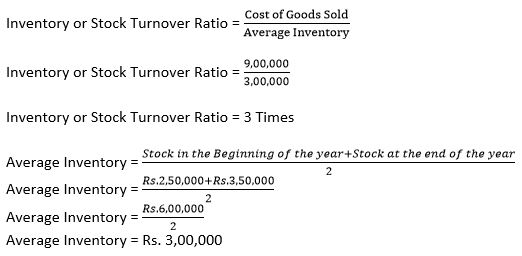

Inventory Turnover Ratio:

A high ratio shows that more sales are being produced by a rupee of investment in the inventories. On the other hand, a low ratio means inefficient use of investment in inventory, over investment in stocks, etc. A very high ratio indicates overtrading which may result in working capital shortage. Only an optimum Inventory Turnover Ratio ensures adequate working capital and helps firm ear a reasonable margin.

Important Note:

Inventory Turnover Ratio: It measures the number of times an enterprise sells and replaces its inventory and therefore, it is an activity as well as efficiency ratio that measures efficiency of inventory management.

Q50. Assuming That the Debt to Equity Ratio is 2:1, state giving reasons, which of the following transactions would: (i) increase; (ii) Decrease; (iii) Not alter Debt to Equity Ratio:

(i) Issue of new shares for cash.

(ii) Conversion of debentures into equity shares

(iii) Sale of a fixed asset at profit.

(iv) Purchase of a fixed asset on long-term deferred payment basis.

(v) Payment to creditors.

Answer:

Debt to Equity Ratio is 2:1. Reasons are given below for which the following transactions would (i) Increase: (ii) Decrease: (iii) Not alter Debt to Equity Ratio.

(i) Issue of new shares for cash - will decrease the ratio.

Reason - If shares are issued then the denominator of the ratio will increase which will decrease the ratio.

(ii) Conversion of debentures into equity shares - will decrease the ratio.

Reason - If debentures into equity shares then the denominator of the ratio will increase and numerator will decrease which will decrease the ratio.

(iii) Sale of fixed assets at profit - will decrease the ratio.

Reason - If fixed assets are sold at a profit then the denominator of the ratio will increase which will decrease the ratio.

(iv) Purchase of a fixed asset on long-term deferred payment basis - will increase the ratio.

Reason - If fixed asset is purchased on long-term deferred payment basis then the numerator of the ratio will increase which will increase the ratio.

(v) Payment to creditors - will not alter the ratio.

Reason - If payment to creditors is made then it will not affect the debt or equity, hence it will not change the ratio.

About Solution:

Formula to find Debt-Equity Ratio in this question:

Debt - Equity Ratio = Debt/Equity

Things to Remember:

Inventory Turnover Ratio: It ascertains whether the investment in stock is appropriate and that only the required amount is invested in stock.

Important Note:

Direct Expenses: Such an item will be shown separately in the Note to Accounts and may be in form of Employees Benefit Expenses and/or Other Expenses. In case if no direct expenses are given, it is assumed that direct expenses are in

Average Inventory: It is calculated as follows:

Average Inventory = (Opening Inventory + Closing Inventory) + 2

Q51. From the following Balance Sheet of ABC Ltd. as at 31st March, 2019, Calculate Debt to Equity Ratio:

Answer:

Things to Remember:

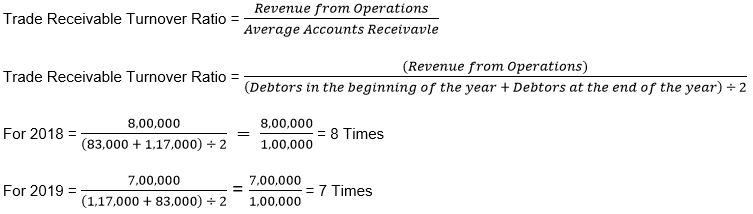

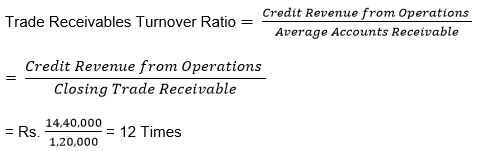

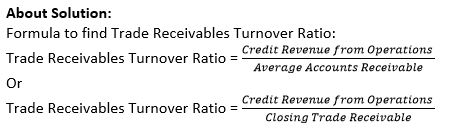

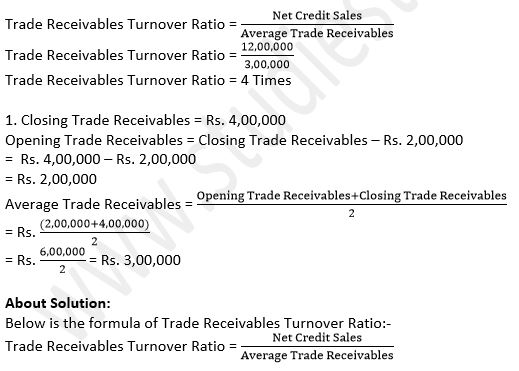

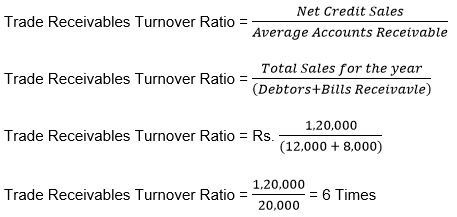

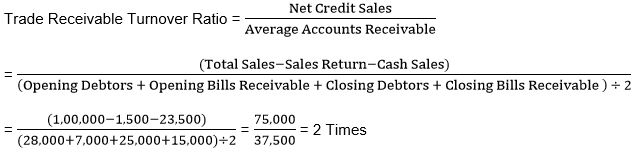

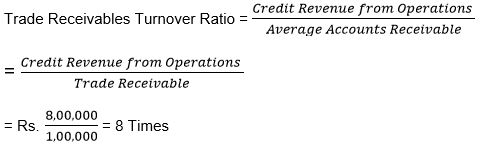

Understanding Trade Receivables Turnover ratio:

1. It is the relationship between Credit Revenue from Operations (i.e., Net Credit Sales) and

2. Average Trade Receivables ( i. e., Average of debtors and bi IIS receivable of the year).

3. It indicates the number of times trade receivables are turned over in a year in relation to credit sales.

Important Note:

Trade Receivables Turnover ratio: It identifies how quickly trade receivables are converted into Cash and Cash Equivalents and therefore, indicates the efficiency in collection of amounts due against trade receivables.

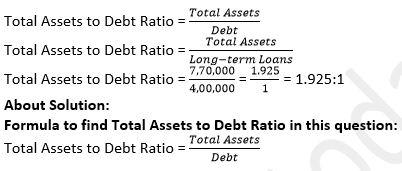

Q52. Calculate Total Assets to Debt Ratio from the following information: Long-term Debts Rs. 4,00,000; Total Assets Rs. 7,70,000.

Answer:

Things to Remember:

Trade Receivables Turnover Ratio:

A higher ratio shows that debts are collected more promptly and a lower ratio shows inefficiency in collection or increased credit period or more investment in debtors.

Important Note:

Trade Receivables Turnover Ratio:

It should be computed keeping in mind that provision for doubtful debts is not deducted from trade receivables since the purpose is to calculate the number of days for which sales are tied up in trade receivables and not to ascertain realizable value of debtors.

Q53. Shareholder’s Funds ₹ 1,60,000; Total Debts ₹ 3,60,000; Current Liabilities ₹ 40,000. Calculate Total Assets to Debt Ratio.

Answer:

Total Assets to Debt Ratio = Total Assets/Debt

Total Assets to Debt Ratio = 5,20,000/3,20,000

Total Assets to Debt Ratio = 1.625:1

Total Assets = Shareholder’s Fund + Total Debts

Total Assets = Rs. 1,60,000 + Rs. 3,60,000

Total Assets = Rs. 5,20,000

Total Debts = Non-Current Liabilities + Current Liabilities

Rs. 3,60,000 = Non-Current Liabilities + Rs. 40,000

Non-Current Liabilities = Rs. 3,60,000 - Rs. 40,000

Non-Current Liabilities = Rs. 3,20,000

Q54. Total Debt Rs. 60,00,000; Shareholder’s Fund Rs. 10,00,000; Reserves and Surplus Rs. 2,50,000; Current Assets Rs. 25,00,000; Working Capital Rs. 5,00,000. Calculate Total Assets to Debt Ratio.

Answer:

Total Assets to Debt Ratio = Total Assets/Debt

Total Assets to Debt Ratio = 70,00,000/40,00,000

Total Assets to Debt Ratio = 1.75:1

Total Assets = Total Debt + Shareholders Fund

Total Assets = Rs. 60,00,000 + Rs. 10,00,000

Total Assets = Rs. 70,00,000

Working Capital = Current Assets – Current Liabilities

Rs. 50,00,000 = Rs. 25,00,000 – Current Liabilities

Current Liabilities = Rs. 50,00,000 - Rs. 25,00,000

Current Liabilities = Rs. 25,00,000

Total Debt = Non-current Liabilities + Current Liabilities

Rs. 60,00,000 = Non-current Liabilities + Rs. 20,00,000

Non-current Liabilities = Rs. 60,00,000 - Rs. 20,00,000

Non-current Liabilities = Rs. 40,00,000

Q55. Total Debt ₹ 15,00,000; Current Liabilities ₹ 5,00,000; Capital Employed ₹ 15,00,000. Calculate Total Assets to Debt Ratio.

Answer:

Total Assets to Debt Ratio = Total Assets/Debt

Total Assets to Debt Ratio = 20,00,000/10,00,000

Total Assets to Debt Ratio = 2:1

Total Assets = Capital Employed + Current Liabilities

Total Assets = Rs. 15,00,000 + Rs. 5,00,000

Total Assets = Rs. 20,00,000

Total Debt = Non-Current Liabilities + Current Liabilities

Rs. 15,00,000 = Non-Current Liabilities + Rs. 5,00,000

Non-Current Liabilities = Rs. 15,00,000 - Rs. 5,00,000

Non-Current Liabilities = Rs. 10,00,000

Q56. Total Debt ₹ 12,00,000; Shareholder’s Funds ₹ 2,00,000; Reserves and Surplus ₹ 50,000; Current Assets ₹ 5,00,000; Working Capital ₹ 1,00,000; Calculate Total Assets to Debt Ratio.

Answer:

Total Assets to Debt Ratio = Total Assets/Debt

Total Assets to Debt Ratio = 14,00,000/8,00,000

Total Assets to Debt Ratio = 1.75:1

Total Assets = Shareholders Fund + Total Debt

Total Assets = Rs. 2,00,000 + Rs. 12,00,000

Total Assets = Rs. 14,00,000

Working Capital = Current Assets – Current Liabilities

Rs. 1,00,000 = Rs. 5,00,000 – Current Liabilities

Current Liabilities = Rs. 5,00,000 - Rs. 1,00,000

Current Liabilities = Rs. 4,00,000

Total Debt = Non-Current Liabilities + Current Liabilities

Rs. 12,00,000 = Non-Current Liabilities + Rs. 4,00,000

Non-Current Liabilities = Rs. 12,00,000 - Rs. 4,00,000

Non-Current Liabilities = Rs. 8,00,000

Q57. Calculate Total Assets to Debt Ratio from the following information:

Find Total Assets to Debt Ratio from the following information:

Answer:

Calculation of Total Assets to Debt Ratio:-

Total Assets to Debt Ratio = Total Assets/Debt

Total Assets to Debt Ratio = 15,00,000/9,80,000

Total Assets to Debt Ratio = 1.53:1

Current Liabilities = Creditors + Bills Payable + Bank overdraft + Outstanding Expenses

Current Liabilities = Rs. 90,000 + Rs. 60,000 + Rs. 50,000 + Rs. 20,000

Current Liabilities = Rs. 2,20,000

Total Debt = Non Current Liabilities + Current Liabilities

Rs. 12,00,000 = Non Current Liabilities + Rs. 2,20,000

Non Current Liabilities = Rs. 12,00,000 - Rs. 2,20,000

Non Current Liabilities = Rs. 9,80,000

Q58. From the following information, calculate Total Assets to Debt Ratio:

Answer:

Total Assets to Debt Ratio = (Total Assets)/Debt

Total Assets to Debt Ratio = 9,00,000/3,00,000

Total Assets to Debt Ratio = 3:1

Debt = Long-term Borrowings + Long term Provisions

Debt = Rs. 1,80,000 + Rs. 1,20,000

Debt = Rs. 3,00,000

Shareholders Fund = Equity Share Capital + Surplus + General Reserve

Shareholders Fund = Rs. 4,00,000 + Rs. 1,00,000 + Rs. 70,000

Shareholders Fund = Rs. 5,70,000

Total Assets = Shareholders Fund + Non Current Liabilities (Debt) + Current Liabilities

Total Assets = Rs. 5,70,000 + Rs. 3,00,000 + Rs. 30,000

Total Assets = Rs. 9,00,000

Q59. From the following information, calculate Total Assets to Debt Ratio:

Answer:

Total Assets to Debt Ratio = Total Assets/Debt

Total Assets to Debt Ratio = 8,00,000/4,00,000

Total Assets to Debt Ratio = 4:1

Debt = Long-term Borrowings + Long term Provisions

Debt = Rs. 3,00,000 + Rs. 1,00,000

Debt = Rs. 4,00,000

Total Assets = [Fixed Assets (Gross)- Depreciation] + Non-Current Investments + Long term Loan and Advances + Current Assets

Total Assets = [Rs. 6,00,000- Rs. 1,00,000] + Rs. 10,000 + Rs. 40,000 + Rs. 2,50,000

Total Assets = Rs. 5,00,000 + Rs. 10,000 + Rs. 40,000 + Rs. 2,50,000

Total Assets = Rs. 8,00,000

Q60. From the following information, calculate Proprietary Ratio:

Answer:

Things to Remember:

The ratio is an arithmetical expression i.e. relationship of one number to another. It may be defined as an indicated quotient of the mathematical expression. It is expressed as a proportion or a fraction or in percentage or in terms of number of times. A financial ratio is the relationship between two accounting figures expressed mathematically.

Important Notes:

Ratios provide clues to the financial position of a concern. These are the indicators of financial strength, soundness, position or weakness of an enterprise. One can draw conclusions about the financial position of a concern with the help of accounting ratios.

Answer:

Things to Remember:

Broadly accounting ratios can be grouped into the following categories:

(a) Liquidity ratios

(b) Activity ratios

(c) Solvency ratios

(c) profitability ratios

(e) Leverage ratio

Important Notes:

Liquidity Ratios the term liquidity refers to the ability of the company to meet its current liabilities. Liquidity ratios assess capacity of the firm to repay its short term liabilities. Thus, liquidity ratios measure the firms’ ability to fulfill short term commitments out of its liquid assets. The important liquidity ratios are:

(i) Current ratio

(ii) Quick ratio

Q62. Calculate Proprietary Ratio from the following:

Answer:

Things to Remember:

Current ratio Current ratio is a ratio between current assets and current liabilities of a firm for a particular period. This ratio establishes a relationship between current assets and current liabilities. The objective of computing this ratio is to measure the ability of the firm to meet its short term liability. It compares the current assets and current liabilities of the firm.

Important Notes:

Current Assets are those assets which can be converted into cash within a short period i.e. not exceeding one year.

It includes the following: Cash in hand, Cash at Bank, Bill receivables, Short term investment, Sundry debtors, Stock, Prepaid expenses

Current liabilities are those liabilities which are expected to be paid within a year. It includes the following: Bill payables, Sundry creditors, Bank overdraft, Provision for tax, outstanding expenses.

Q63. Calculate Proprietary Ratio, if Total Assets to Debt Ratio is 2 : 1. Debt is ₹ 5,00,000. Equity Shares Capital is 0.5 times of debt. Preference Shares Capital is 25% of equity share capital. Net Profit before tax is ₹ 10,00,000 and rate of tax is 40%.

Answer:

Total Assets to Debt Ratio = 2:1

Debt = Rs. 5,00,000

Total Assets to Debt Ratio = Total Assets/Debt

2 = (Total Assets)/5,00,000

Total Assets = 2 × Rs. 5,00,000

Total Assets = Rs. 10,00,000

Equity share Capital = 0.5 × Rs. 5,00,000

Equity share Capital = Rs. 2,50,000

Preference Share Capital = Equity Share Capital × 25%

Preference Share Capital = Rs. 2,50,000 × 25%

Preference Share Capital = Rs. 62,500

Proprietary Ratio = (Shareholders Fund)/(Total Assets )

Proprietary Ratio = 9,12,500/10,00,000

Proprietary Ratio = 0.9125:1

Net Profit Before tax = Rs. 10,00,000

Tax Rate = 40%

Profit After tax = Rs. 10,00,000 – (10,00,000 × 40%)

Profit After tax = Rs. 10,00,000 – Rs. 4,00,000

Profit After tax = Rs. 6,00,000

Shareholders’ Funds = Equity Share Capital + Preference Share Capital + Profit

Shareholders’ Funds = Rs. 2,50,000 + Rs. 62,500 + Rs. 6,00,000

Shareholders’ Funds = Rs. 9,12,500

Q64. State with reason, whether the Proprietary Ratio will improve, decline or will not change because of the following transactions if Proprietary Ratio is 0.8 : 1:

(i) Obtained a loan of Rs. 5,00,000 from State Bank of India payable after five years.

(ii) Purchased machinery of Rs. 2,00,000 by cheque.

(iii) Redeemed 7% Redeemable Preference Shares Rs. 3,00,000.

(iv) Issued equity shares to the vendor of building purchased for Rs. 7,00,000.

(v) Redeemed 10% redeemable debentures of Rs. 6,00,000.

Answer:

The Proprietary Ratio of a Company is 0.8:1. The following are given reasons for the answers.

Proprietary Ratio = Shareholders' Funds/TotalAssets

Proprietary Ratio = 8,00,000/10,00,000

Proprietary Ratio = 0.8/1

Proprietary Ratio = 0.8:1 (Let the expected figures be)

(i) Obtained a loan of Z 5,00,000 from State Bank of India payable after five years. Rising of long term loan will not affect Shareholders Funds but due to rising of loan the cash or bank balance will increase for which, the amount of total assets will increase. Therefore denominator of the fraction will increase which alternatively decrease the ratio.

(ii) Purchase of machinery of Z 2,00,000 by cheque. The bank balance will reduce and fixed assets increase by same amount. There will be no effect in the total assets as well as the Shareholders Funds. Therefore no change in the ratio.

(iii) Redeemed 7% Redeemable Preference Shares Z 3,00,000 will reduce Shareholders Funds as well as Total Assets due to payment through bank. Therefore reduction of Z 3,00,000 from both the numerator and denominator will decrease the ratio.

(iv) Issued equity shares to the vendor of building purchased for Rs. 7,00,000 will increase Shareholders Funds as well as Total Assets due to increase in Fixed Assets. Therefore numerator and denominator of the fraction will increase which alternatively increase the ratio.

(v) Redeemed 10% redeemable debentures of Rs. 6,00,000 will not affect Shareholders Funds but the amount of Total Assets decrease due to payment through bank. Therefore denominator of the fraction will decrease which alternatively increase the ratio.

About Solution:

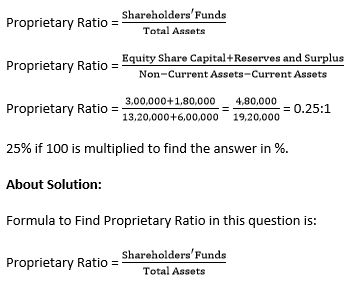

Formula to Find Proprietary Ratio in this question is:

Proprietary Ratio = (Shareholders^' Funds)/TotalAssets

Things to Remember:

Liquid ratio = Liquid or quick assets /Current liabilities

Important Notes:

Liquid assets = current assets – (stock + prepaid expenses)

Q65. From the following information, calculate:

(a) Proprietary Ratio;

(b) Debt to Equity Ratio; and

(c) Total Assets to Debt Ratio.

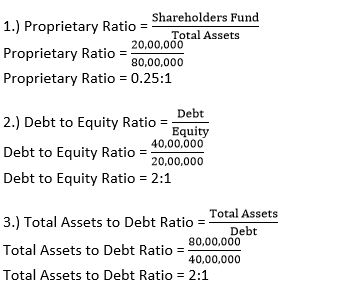

Answer:

Total Assets = Non-Current Assets + Current Assets

Total Assets = Rs. 40,00,000 + Rs. 40,00,000

Total Assets = Rs. 80,00,000

Debt = Long term Borrowings + Long term Provision

Debt = Rs. 15,00,000 + Rs. 25,00,000

Debt = Rs. 40,00,000

Total Assets = Equity + Non-Current Liabilities + Current Liabilities

Rs. 80,00,000 = Equity + Rs. 40,00,000 + Rs. 20,00,000

Rs. 80,00,000 = Equity + Rs. 60,00,000

Equity = Rs. 80,00,000 - Rs. 60,00,000

Equity = Rs. 20,00,000

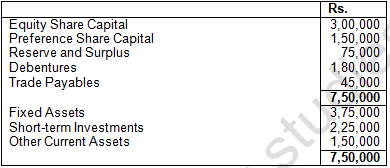

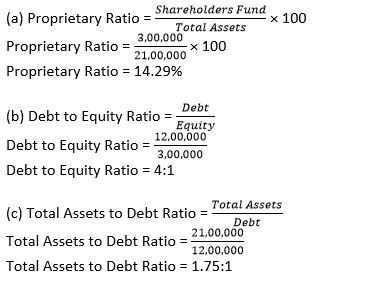

Q66. From the following information, calculate:

(a) Proprietary Ratio;

(b) Debt to Equity Ratio; and

(c) Total Assets to Debt Ratio.

Answer:

Working Note:-

Working Capita = Current Assets – Current Liabilities

Rs. 1,50,000 = Rs. 7,50,000 – Current Liabilities

Current Liabilities = Rs. 7,50,000 – Rs. 1,50,000

Current Liabilities = Rs. 6,00,000

Total Debt = Non-current Liabilities (Debt) + Current Liabilities

Rs. 18,00,000 = Non-current Liabilities (Debt) + Rs. 6,00,0000

Non-current Liabilities (Debt) = Rs. 18,00,000 - Rs. 6,00,0000

Non-current Liabilities (Debt) = Rs. 12,00,000

Shareholders Fund = Capital Employed – Non-Current Liabilities

Shareholders Fund = Rs. 15,00,000 – Rs. 12,00,000

Shareholders Fund = Rs. 3,00,000

Total Assets = Capital Employed + Current Liabilities

Total Assets = Rs. 15,00,000 + Rs. 6,00,000

Total Assets = Rs. 21,00,000

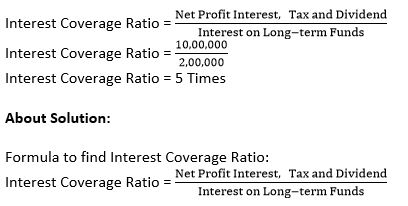

Q67. If Net Profit before Interest and Tax is Rs. 10,00,000 and interest on Long-term Funds is Rs. 2,00,000, find Interest Coverage Ratio.

Answer:

Things to Remember:

Quick ratio is a measure of the instant debt paying capacity of the business enterprise. It is a measure of the extent to which liquid resources are immediately available to meet current obligations. A quick ratio of 1 : 1 is considered good/favorable for a company.

Important Notes:

Activity ratios measure the efficiency or effectiveness with which a firm manages its resources. These ratios are also called turnover ratios because they indicate the speed at which assets are converted or turned over in sales.

Q68. From the following information, calculate Interest Coverage Ratio: Profit after Tax Rs. 4,25,000; Tax Rs. 75,000; Interest on Long-term Funds Rs. 1,25,000.

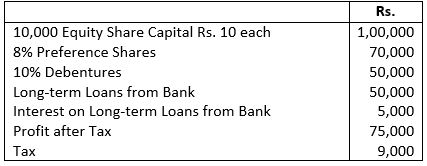

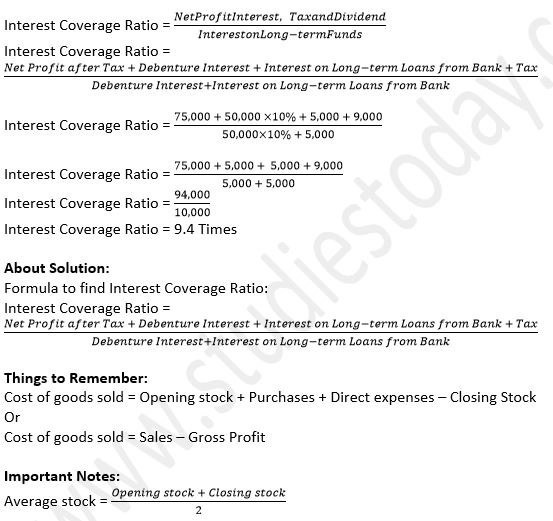

Answer:

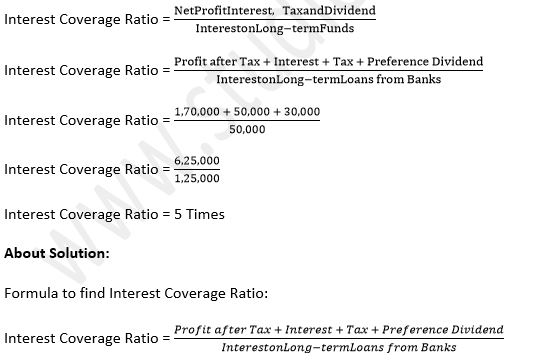

Things to Remember:

These ratios are expressed as ‘times’ and should always be more than one. Some of the important activity ratios are:

(i) Stock turnover ratio

(ii) Debtors turnover ratio

(iii) Creditors turnover ratio

(iv) Working capital turnover ratio

Important Notes:

Stock turnover ratio is a ratio between cost of goods sold and the average stock or inventory. Every firm has to maintain a certain level of inventory of finished goods. But the level of inventory should neither be too high nor too low. It evaluates the efficiency with which a firm is able to manage its inventory. This ratio establishes relationship between cost of goods sold and average stock.

Q69. From the following details, calculate Interest Coverage Ratio:

Net Profit after Tax Rs. 7,00,000

6% Debentures Rs. 20,00,000

Tax Rate 30%

Answer:

Interest on Debenture = 6% × Debenture

Interest on Debenture = 6% × Rs. 20,00,000

Interest on Debenture = Rs. 1,20,000

Profit before Interest and tax = Profit before tax + Interest

Profit before Interest and tax = Rs. 10,00,000 + Rs. 1,20,000

Profit before Interest and tax = Rs. 11,20,000

Q70. From the following information, Calculate Interest Coverage Ratio:

Net Profit after interest and tax ₹ 1,20,000; Rate of Income tax; 40%; 15% Debentures ₹ 1,00,000; 12% Mortgage Loan ₹ 1,00,000.

Answer:

Interest Coverage Ratio = Profit Before Interets and Tax/Interest on Long term loans

Interest Coverage Ratio = 2,2,7,000/27,000

Interest Coverage Ratio = 8.41 times

Let profit before tax be x

Profit after tax = Profit Before tax – Interest

Rs.1,20,000 = x – (40% of x)

Rs.1,20,000 = x – 0.40x

Rs.1,20,000 = 0.60x

0.60x = Rs.1,20,000

x = (Rs.1,20,000)/0.60

x = Rs. 2,00,000

Profit Before tax = Rs. 2,00,000

Interest = 15% Debentures + 12% Mortgage Loan

Interest = 15% × 1,00,000 + 12% × 1,00,000

Interest = 15,000 + 12,000

Interest = 27,000

Profit before interest and tax = Profit Before tax + Interest

Profit before interest and tax = Rs. 2,00,000 + Rs. 27,000

Profit before interest and tax = Rs. 2,27,000

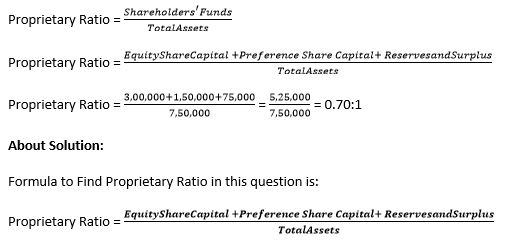

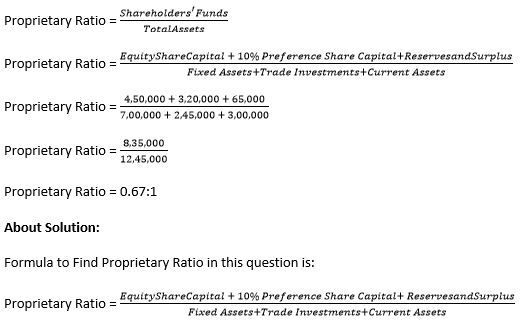

About Solution:

Formula to Find Proprietary Ratio in this question is:

Proprietary Ratio = (EquityShareCapital + ReservesandSurplus)/(Total Assets)

Things to Remember:

Current Ratio indicates the amount of current assets available for repayment of current liabilities. Higher the ratio, the greater is the short term solvency of a firm and vice a versa. However, a very high ratio or very low ratio is a matter of concern. If the ratio is very high it means the current assets are lying idle. Very low ratio means the short term solvency of the firm is not good. Thus, the ideal current ratio of a company is 2 : 1 i.e. to repay current liabilities, there should be twice current assets.

Important Notes:

Quick ratio is also known as Acid test or Liquid ratio. It is another ratio to test the liability of the concern. This ratio establishes a relationship between quick assets and current liabilities. This ratio measures the ability of the firm to pay its current liabilities. The main purpose of this ratio is to measure the ability of the firm to pay its current liabilities. For the purpose of calculating this ratio, stock and prepaid expenses are not taken into account as these may not be converted into cash in a very short period.

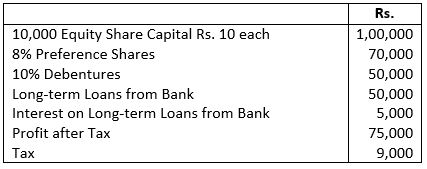

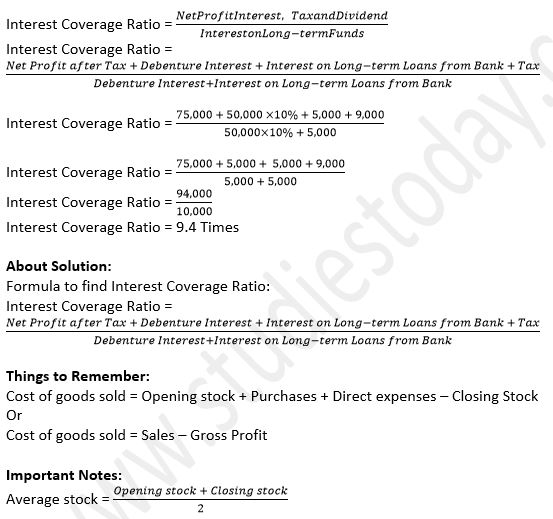

Q71. From the following information, calculate Interest Coverage Ratio:

Answer:

Q71. From the following information, calculate Interest Coverage Ratio:

Answer:

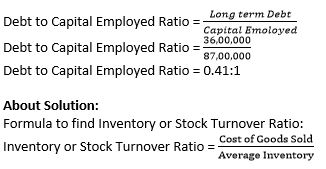

Q72. From the following information, Calculate Debt to Capital Employed Ratio:

Rs.

Shareholder’s Funds 24,00,000

Long-term Borrowings (9% Debentures) 12,00,000

Current Liabilities 2,00,000

Non-Current Assets 28,00,000

Current Assets 10,00,000

Answer:

Debt to Capital Employed Ratio = Long term debt / Capital Employed

Debt to Capital Employed Ratio = 12,00,000/36,00,000

Debt to Capital Employed Ratio = 0.33:1

Long term Debt (9% Debentures) = Rs. 12,00,000

Capital Employed = Shareholders Fund + Long term Borrowings

Capital Employed = Rs. 24,00,000 + Rs. 12,00,000

Capital Employed = Rs. 36,00,000

Q73. From the following information, Calculate Debt to Capital Employed Ratio:

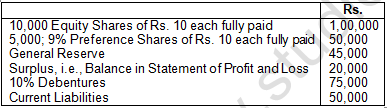

Surplus i.e., Balance in Statement of Profit & Loss: (Rs. 1,00,000)

Answer:

Things to Remember:

Inventory/stock conversion period: It may also be of interest to see average time taken for clearing the stocks. This can be possible by calculating inventory conversion period. This period is calculated by dividing the number of days by inventory turnover

Important Notes:

Stock Turnover Ratio:

i.) If cost of goods sold is not given, the ratio is calculated from the sales.

ii.) If only closing stock is given, then that may be treated as average stock.

Q74. From the following, calculate ‘Debt to Capital Employed Ratio’:

Rs.

9% Debenture 2,00,000

8% Public Deposits 5,00,000

Long-term Provisions 2,00,000