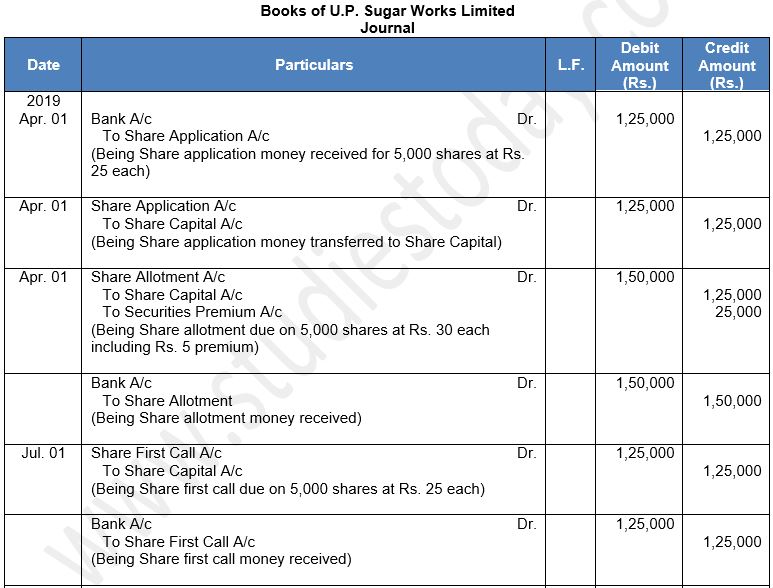

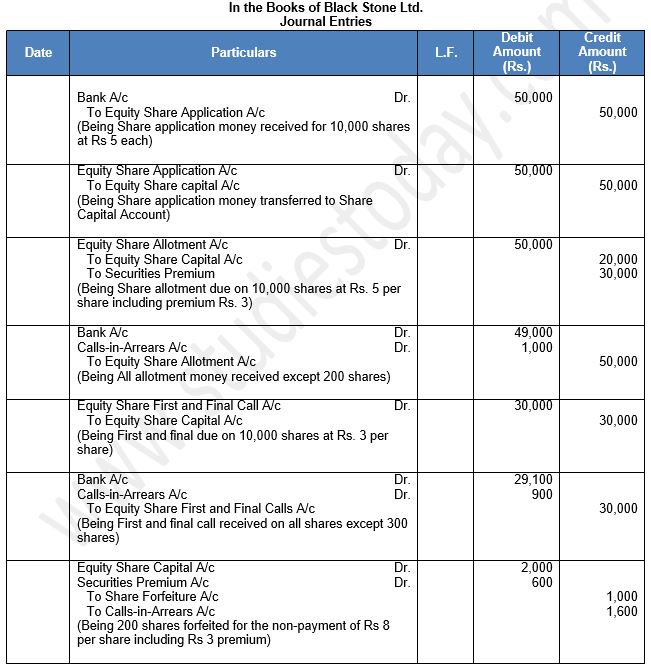

Access free TS Grewal Solution Class 12 Chapter 8 Company Accounts Accounting for Share Capital 2026 below. Students can now access free TS Grewal Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 8 Company Accounts Accounting for Share Capital TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 8 Company Accounts Accounting for Share Capital Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 8 Company Accounts Accounting for Share Capital TS Grewal Class 12 Solved Exercises

About the chapter: TS Grewal Class 12 Chapter 8 Company Accounts Accounting for Share Capital is an important chapter for students studying in Class 12 commerce stream. It covers concepts and practical questions relating to various topics such as types of share capital, issue and allotment of shares, forfeiture and reissue of shares, and redemption of preference shares. There are detailed notes relating to equity share capital and preference share capital, process of issuing and allotting shares, which includes topics such as the minimum subscription, over-subscription, and the issue of shares at a premium or at a discount. There is also information relating to forfeiture and reissue of shares, reasons for the forfeiture of shares and the process of reissuing them, bonus shares and rights issue of shares, redemption of preference shares, repurchasing the preference shares issued by a company.

As this is a very important chapter it should be studied thoroughly by students. We have solved all the practical questions given in this chapter below. We have also provided useful notes after each question. Students should go through the solved TS Grewal questions provided below and get good marks in exams.

TS Grewal Class 12 Accounting for Companies

Textbook for CBSE Class 12

TS Grewal Solutions Class 12 Accountancy

Chapter 8 Company Accounts- Accounting for Share Capital

Question 10. Differentiate between 'Issued Share Capital and 'Subscribed Share Capital.

Question 11. Differentiate between 'Called-up Share Capital' and 'Paid-up Share Capital.

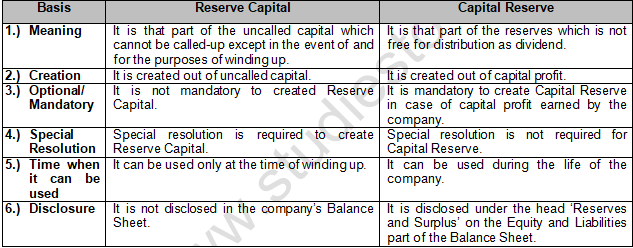

Question 12. What is meant by Reserve Capital?

Reserve Capital is that part of the uncalled capital which the company, by passing a special resolution, may reserve to be called upon only on winding up of the company.

Question 13. Is 'Reserve Capital' a part of 'Unsubscribed Capital' or 'Uncalled Capital’?

Reserve Capital is included in uncalled Capital.

Question 14. What is meant by Capital Reserve?

Capital Reserve is a reserve created out of the profits of capital nature which are not available for distribution as dividend.

Question 15. What are Preliminary Expenses?

Preliminary expenses are those expenses which are incurred for incorporation of a company.

Question 16. What is the name given to the "part of capital" of a company which is called-up only on winding up?

"Part of capital" of a company which is called-up only on winding up of the company is known as “Reserve Capital”.

Question 17. What is meant by Allotment?

Share allotment is the creation and issuing of new shares, by a company. New shares can be issued to either new or existing shareholders. Share allotment can have implications for any existing shareholders share proportion. Typically, new shares are allotted to bring on new business partners.

Question 18. What is meant by pro rata allotment of shares?

Pro rata allotment of shares means allotment of shares in a fixed proportion. Pro rata allotment takes place only when the public issue of shares is oversubscribed.

Question 19. When does the need for a pro rata allotment arise?

Pro rata allotment of share means allotment of shares in a fixed proportion. Pro rata allotment takes place only when the public issue of share is oversubscribed.

Question 20. What is meant by Public subscription of shares?

Public issue of shares means an invitation by a company to public to subscribe the shares offered through a prospectus.

Question 21. What is meant by Private Placement of Shares?

Private Placement of Shares implies issue and allotment of shares to a select group of persons privately and not to public in general through public issue. In order to place the shares privately, a company must pass a special resolution to this effect.

Question 22. What is meant by Minimum Subscription?

Minimum Subscription (Section 39(1) of the Companies Act, 2013) means the amount which in the opinion of the Board of Directors of a company, must be received towards subscription of the issued share capital. As per the Guidelines of the Securities and Exchange Board of India (SEBI), a company must receive a minimum of 90% subscription of the Issued Share Capital before making, any allotment of shares or debentures to the public.

Question 23. What is meant by Securities Premium Reserve?

The excess of issue price over the nominal (face) value of a Share/Debenture is ‘Securities Premium’.

Question 24. State any one purpose for which Securities Premium Reserve Account can be utilised.

Purpose for Securities Premium Reserve Account can be utilised for issuing fully paid bonus shares to the members of the company.

Question 25. Name the head under which the Securities Premium Reserve Account will appear in the Balance Sheet.

Securities Premium Reserve Account and is shown in the Equity and Liabilities part of Balance Sheet under the head ‘Shareholders Funds’ and sub-head ‘Reserves and Surplus’ as Securities Premium Reserve.

Question 26. State the name of capital which refers to that amount which is stated in the Memorandum of Association as the share capital of the company.

‘Authorised Capital’ or ‘Nominal Capital’ is stated in the Memorandum of Association and is the maximum amount that a company can raise as share capital.

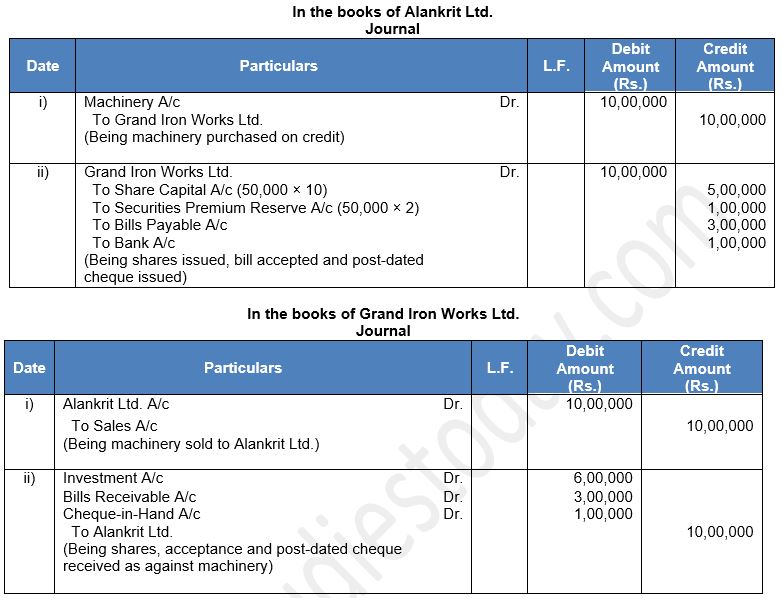

Question 27. What is meant by issue of shares for consideration other than cash?

When the company purchases some assets (including services) or purchases a running business, instead of making the payment to the vendor in cash, it issues its shares. Such issue of shares is termed as Issue of Shares of consideration other than cash.

Question 28. Give the meaning of oversubscription of shares.

Oversubscription of Shares means the number of shares applied for is more than the number of shares offered for subscription.

Question 29. Give any two alternatives available to a company for the allotment of shares in case of oversubscription.

(i) To Make Pro-rata allotment to all the applicants.

(ii) (a) Accepting some applications in full. (b) Allotting the remaining on pro rata basis.

Question 30. What is meant by under subscription of shares?

Under subscription of Shares means the number of shares applied for is less than the number of shares offered for subscription.

Question 31. What is meant by Call money?

After allotment of shares remaining part of share money, when called-up is called Call money. Call money may be called by the company to be paid by the shareholders in one or more instalments.

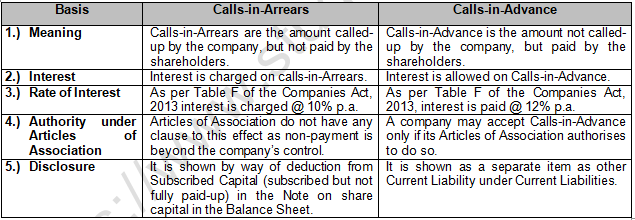

Question 32. Give the meaning of Calls-in-Arrears.

Calls-in-Arrears are that part of capital which has been called-up but has not yet been paid by the shareholders.

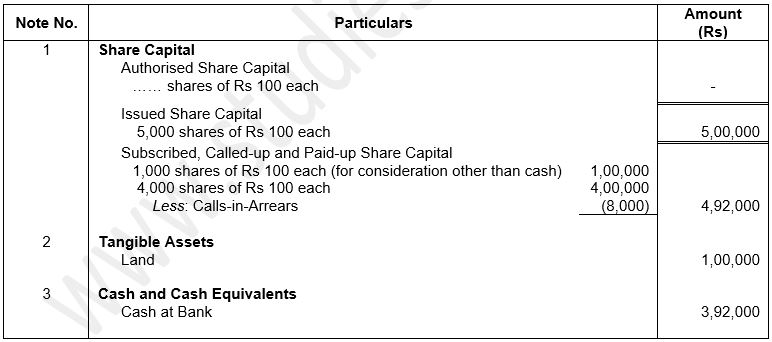

Question 33. How is Calls-in-Arrears shown in the Balance Sheet?

It is shown in the Note to Accounts on Share Capital under Subscribed Capital as follows:

Subscribed and fully paid-up: Amount

1,40,000 Equity Shares of Rs. 10 each 14,00,000

Subscribed but not fully paid-up:

10,000 Equity Shares of Rs. 10 each 1,00,000

Less: Calls-in-Arrears (10,000 × Rs. 2) 20,000 80,000

_____________________

Total 14,80,000

___________

Question 34. What is Calls-in-Advance?

Calls-in-Advance refers to the amount paid by shareholders in excess of the amount due from them.

Question 35. On 28th February, 2016 the first call of Rs. 2 per share became due on 50,000 Equity Shares allotted by Kumar Ltd. Komal, a holder of 1,000 shares, did not pay the first call money. Kovil, a holder of 750 shares, paid the second and final call of 4 per share along with the first call.

Pass the necessary Journal entry for the amount received by opening Calls-in-Arrears and Calls–in-Advance account in the books of the company.

Question 36. Y Ltd. forfeited 100 equity shares of 10 each for non-payment of first call of 2 per share. The final call of Rs. 2 per share was yet to be made. Calculate the maximum amount of discount at which these shares can be reissued.

The maximum discount at which these shares can be re-issued is the credit balance in the Share Forfeiture A/c i.e. Rs. 600.

Question 37. Where is Calls-in- Advance shown in the Balance Sheet?

Call-in- Advance shown in Balance Sheet as ‘Other Current Liabilities’ under the main head ‘Current Liabilities’.

Question 38. Give the meaning of Forfeiture of Shares.

If a shareholder fails to pay any call made on him, which is due on shares, the company may cancel his shares. This cancellation of shares for non-payment of non-payment of amount due on shares is known as Forfeiture of Shares.

Question 39. When does a company forfeit its shares?

Share can be forfeited for the non-payment of call money.

Question 40. At the time of forfeiture of shares, with what amount the Forfeited Share Account is credited?

Forfeited Shares become the property of the company and the company can reissue them at par, at premium or at discount. However, discount cannot exceed the amount forfeited.

Question 41. How the balance in Forfeited Shares Account shown in the Balance Sheet of a company?

The time forfeited shares are reissued, balance of the Forfeited Shares Account is added to paid-up capital under Subscribed Capital in the Note to Accounts on ‘Share Capital’, being part of Shareholders’ Funds shown under Equity and Liabilities part of the Balance Sheet.

Question 42. At the time of forfeiture Shares, with what amount the Share Capital Account is debited?

Share Capital Account is debited with the amount called-up to the date of forfeiture on share forfeited.

Question 43. Can the forfeited shares be reissued at a discount?

Yes, they can be reissued at a discount. And the discount limit is limited. This is different in different cases.

1.) Originally issued at par or premium. But now re issued at a discount. Condition for discount is; the amount of discount should be less than or equal to the amount standing to the credit of forfeited shares account.

2.) When the shares were originally issued at a discount and now are reissued at discount; maximum amount of discount should be less than or equal to the amount credited to Forfeited shares account and the original discount together.

Question 44. How is the gain (profit) on reissue of forfeited shares dealt with?

If forfeited shares are reissued at par or premium, the total amount forfeited on the shares is a gain of capital nature and is transferred to Capital Reserved Account.

Question 45. What is meant by Employees Stock Option Plan (ESOP)?

Employees Stock Option Plan (ESOP) means option granted by the company to its employees and employee directors to subscribe the share at a price that is lower than the market price (Fair Value). It is an option or a right granted by the company but it is not an obligation on the employee to subscribe it. The employees may or may not exercise the option.

Question 46. How is value of option determined?

It is the difference between the market price and the issue price of the security.

Question 47. What is meant by Grant Date?

It is the date at which the enterprise and its employees agree to the terms of employees Stock Option Plan (ESOP).

Question 48. What is meant by Vesting Period?

It is the period between the grant date and the date on which all the specified vesting conditions of an Employees Stock Option Plan (ESOP) are to be satisfied.

Short Answer Type Questions:-

Question 1. What is Reserve Capital? Does it differ from Capital Reserve?

Answer:

Reserve Capital is that part of the uncalled capital which the company, by passing a special resolution, may reserve to be called upon only on winding up of the company.

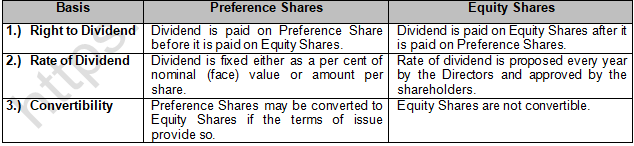

Question 2. Distinguish between Equity Share and Preference Share.

Answer:

Question 3. Distinguish between Oversubscription and under subscription of shares issued by a company. How is Oversubscription dealt with?

Answer:

Question 4. What is securities premium reserve? State any three purposes for which securities premium reserve can be used.

Answer:

The Companies Act, 2013 (Section 52 (1)) prescribes that the amount of the premium received on securities be credited to Securities Premium Account, i.e., Securities Premium Reserve Account. Section 52(1) of the Companies Act, 2013 requires that the amount of premium received on securities to be credited to ‘Securities Premium Account’. Schedule III (Form of Balance Sheet) of the Companies Act, 2013 has given the head ‘Securities Premium Reserve’.

The use of the amount received as premium on securities for the following purposes:

1.) Issuing fully paid bonus shares to the members.

2.) Writing off Preliminary expenses of the company.

3.) Writing off the expenses of, or the commission paid or discount allowed on any issue of securities or debentures of the company.

Question 5. State any three purposes other than 'Issue of bonus Shares' for which securities premium can be utilised.

Answer:

According to Section 52(2) of the Companies Act, 2013, Securities Premium can be applied for the following purposes:

(1) Writing off preliminary expenses of the company,

(2) Writing off the expenses or the commission paid on any issue of shares or debentures or discount allowed on issue of debentures of the company,

(3) Providing for the premium payable on the redemption of redeemable preference shares or of debentures.

Question 6. State any three purposes other than 'buy back of shares' for which securities premium can be utilised.

Answer:

According to Section 52(2) of the Companies Act, 2013, Securities Premium can be applied for the following purposes:

(1) Issuing fully paid bonus to the shareholders.

(2) Writing off preliminary expenses of the company.

(3) Writing off the expenses or the commission paid on any issue of shares or debentures or discount allowed on issue of debentures of the company.

Question 7. Securities Premium can be utilised for three purposes besides (i) issuing fully paid bonus shares' and (ii) Buy back of shares! State those purposes.

Answer:

When shares are issued at a price higher than the nominal (face) value, it is called issue of shares at premium. Excess of issue price over the nominal (face) value is the amount of premium (Securities Premium). It is a capital profit for the company and the amount so received is credited to a separate account called Securities Premium Reserve Account.

According to Section 52(2) of the Companies Act, 2013, Securities Premium can be applied for the following purposes:

(1) Writing off preliminary expenses of the company.

(2) Writing off the expenses or the commission paid on any issue of shares or debentures or discount allowed on issue of debentures of the company.

(3) Providing for the premium payable on the redemption of redeemable preference shares or of debentures.

Question 8. Can Securities Premium Reserve be utilised for the purchase of fixed assets? Give reasons.

Answer:

No, According to Section 52(2) of the Companies Act, 2013, Securities Premium can be applied for the following purposes:

(1) Writing off preliminary expenses of the company.

(2) Writing off the expenses or the commission paid on any issue of shares or debentures or discount allowed on issue of debentures of the company.

(3) Providing for the premium payable on the redemption of redeemable preference shares or of debentures.

(4) Issuing fully paid bonus shares to the members.

(5) Purchasing its own shares.

Question 9. How is Share Capital shown in the Balance Sheet of a Company?

Answer:

Balance Sheet of a company is prepared in the form prescribed in Part I of Schedule III of the Companies Act, 2013. It required a Company to show

(i) Authorised Capital

(ii) Issued Capital

(iii) Subscribed Capital

(i) Authorised Capital or Nominal Capital:- ‘Authorised Capital’ or ‘Nominal Capital’ means such capital as is authorised by the Memorandum of a company to be maximum amount of share capital of a company.

‘Authorised Capital’ or ‘Nominal Capital’ is stated in the Memorandum of Association and is the maximum amount that a company can raise as share capital.

It is stated separately for each class or kind of shares, i.e., Preference Shares and Equity Shares and is the maximum amount of shares capital under each class or kind of shares which a company can issue for subscription. Authorised Share Capital under each class or kind (Equity or Preference) may be more or equal to the issued share capital, but cannot be less than the issued capital.

(ii) Issued Capital:- ‘Issued Capital’ means such capital as the company issues from time to time for subscription. Issued Capital is a part of Authorised Capital that is issued for subscription. It includes besides shares issued for subscription, shares allotted for consideration other than cash, shares subscribed by signatories to the Memorandum of Association and shares taken by directors as qualifying shares. It should be kept in mind that issued capital cannot exceed the company’s Authorised Share Capital.

(iii) Subscribed Capital:- ‘Subscribed Capital’ means such part of the capital which is for the time being subscribed by the members of a company. Subscribed Capital is a part of issued capital which the company has issued for cash or for consideration other than cash. It includes shares issued for subscription and subscribed, shares subscribed by signatories to the Memorandum of Association, shares subscribed by the directors as qualifying shares and shares allotted for consideration other than cash.

Question 10. Can forfeited shares be reissued? If so, at what terms?

Answer:

Yes, forfeited shares are reissued. Reissue of forfeited shares means selling the shares that were cancelled by the company. These shares may be reissued or sold by the company on the terms as it may decide. Thus, forfeited shares may be reissued by the company at par, at premium or at discount. However, if forfeited shares are reissued at discount, the amount of discount allowed on reissued of forfeited shares should not exceed the amount forfeited on reissued shares.

Maximum Permissible Discount on Reissue of Forfeited Shares:- Maximum discount that can be allowed on reissued of forfeited shares is the amount forfeited, i.e. the amount credited to the forfeited shares. In other words, reissue price cannot be less than the amount unpaid on forfeited shares.

Transfer of Balance in Forfeited Shares Account

When forfeited shares are reissued, one of the following two situations arises:

(1) All forfeited shares are reissued

(2) All forfeited shares are not reissued.

Question 11. Distinguish between Calls-in-Arrears and Calls-in-Advance.

Answer:

Question 12. A company invited applications for 30,000 Equity Shares of Rs. 10 each at a premium of 2 each. The total application money received @ Rs. 2 per share was Rs. 72,000. Name the kind of subscription. List the three alternatives for allotting these shares.

Answer:

1.) Full Allotment – The Company may reject the oversubscribed shares. The company may reject the applications for 6,000 shares and make full allotment to remaining applications.

2.) Partial Allotment – The Company may reject some of the applications and then make proportionate allotment to remaining applicants.

3.) Pro-rata Allotment – All the applicants may be allotted shares in the ratio of 36,000 : 30,000 i.e. 6:5.

Question 13. Guru Ltd. invited applications for issuing 5,00,000 equity shares of 10 each at a premium of 5 per share. Because of favourable conditions, the issue was over-subscribed and applications for 15,00,000 shares were received. Suggest the alternatives available to the Board of Directors for the allotment of shares.

Answer:

The following alternatives are available to the Board of Directors for the allotment of share:

(1) First Alternative- Rejection of excess applications: The Company can make full allotment to some applicants and can reject the excess applications and return their application money.

(2) Second Alternative- Pro Rata Allotment: In this case, all the applicants are allotted shares on proportionate basis.

(3) Third Alternative- Rejection and Pro Rata Allotment: In this case, combination of the above two alternatives is adopted.

Exercise ::------>

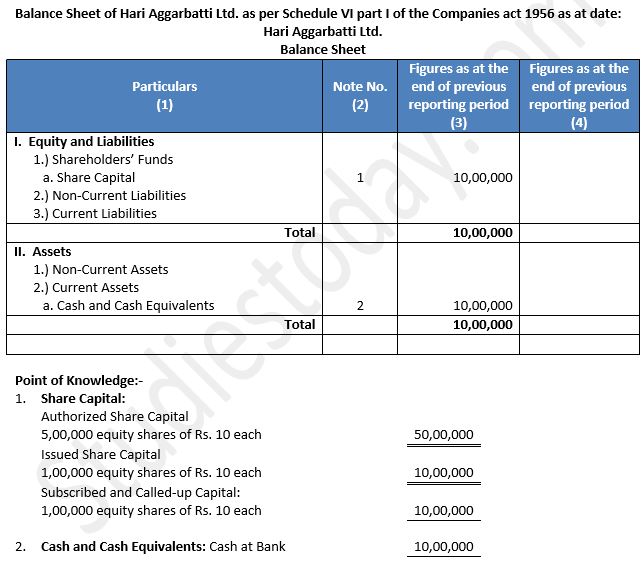

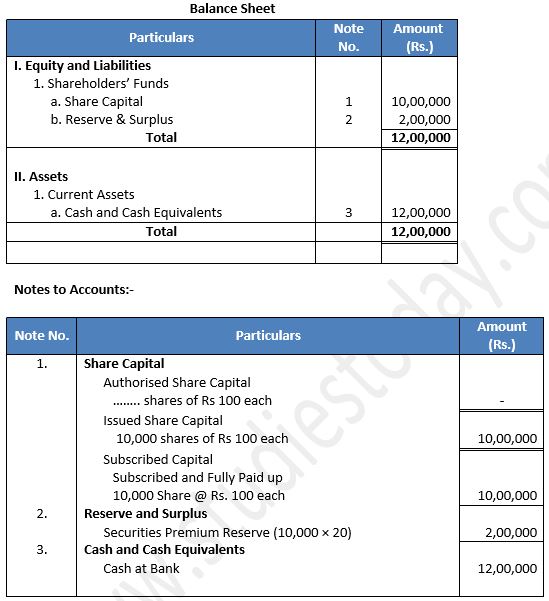

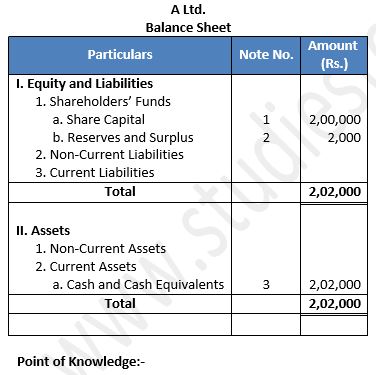

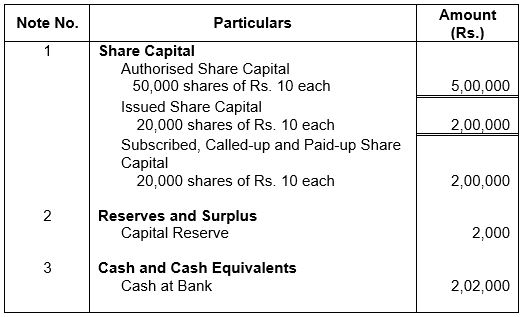

Q1: Hari Aggarbatti was registered with capital of Rs. 50,00,000 divided into 5,00,000 Equity Shares of 10 each. It issued 1,00,000 Equity Shares to public for subscription. The shares were subscribed and calls made were received.

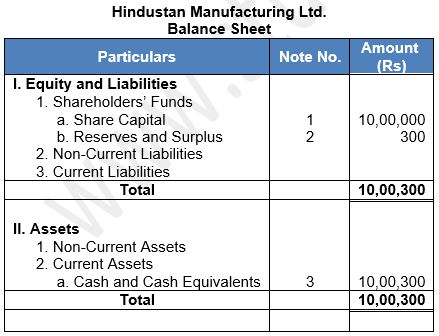

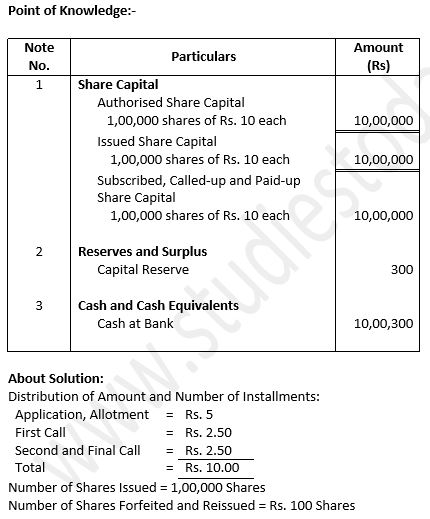

Prepare Balance Sheet of the company showing share capital.

Answer 1:

Balance Sheet of Hari Aggarbatti Ltd. as per Schedule VI part I of the Companies act 1956 as at date:

3. ‘Authorised Capital’ or ‘Nominal Capital’ means such capital as is authorised by the Memorandum of a company to be maximum amount of share capital of a company.

About Solution:-

Unlimited Liability Company: As per Section 2(92) of the Companies Act, 2013, it is a company where the liability of its members is unlimited. Therefore, in the event of winding up of such company, debts of the company shall be met from private property of the members.

Thinks to Remember:-

Company Limited by Guarantee: As per Section 2(21) of the Companies Act, 2013, it is a company having the liability of its members limited by the memorandum to such amount as the members may respectively undertake to contribute to the assets of the company in the event of it being wound up.

Important Notes:-

Promotion: A person or a group of persons who agree to start a business in the form of a company are called Promoters. These promoters undertake the responsibility to bring the company into existence by promoting its objects and activities which is the first stage in incorporation of a company.

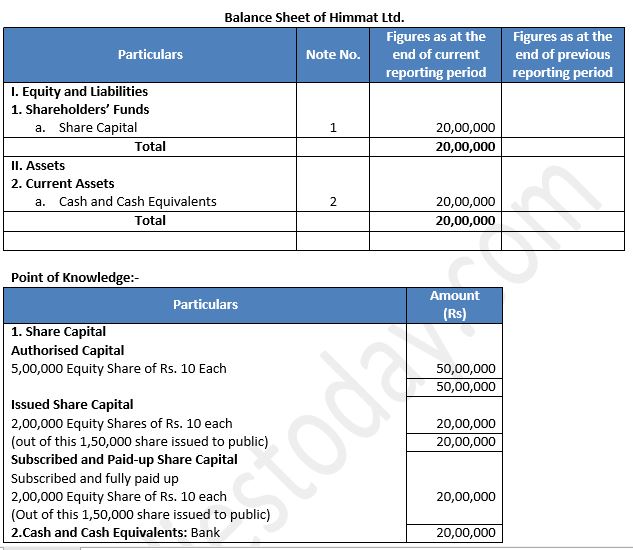

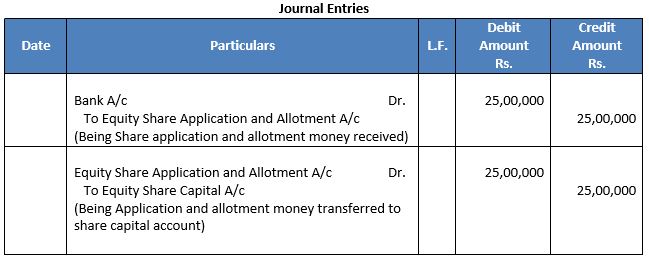

Q2: Farm Products Ltd. has authorised share capital of ₹ 50,00,000 divided into 5,00,000 Equity Shares of ₹ 10 each. It has existing issued and paid up capital of ₹ 5,00,000. It further issued to public 1,50,000 Equity Shares at par for Subscription payable as under:

On Application: Rs. 3

On Allotment: Rs. 4 and

On Call: Balance Amount

The issue was fully subscribed and allotment was made to all the applicants. Call was made during the year and was duly received.

Show share capital of the company in the Balance Sheet of the Company.

Answer 2:

About Solution:

After getting the name of the proposed company approved, the promoters have to submit Memorandum of Association, Articles of Association, consent of first directors to act as directors and a declaration that the requirements of the Companies Act have been complied with.

Things to Remember:

The directors do not file a declaration with the Registrar of Companies to the effect that every subscriber to the Memorandum of Association has paid the value if the shares, if any, agreed to be taken by him.

Important Notes:

It is the amount that a company receives towards Share Capital from issue of both Equity Share and Preference Shares. According to Section 43 of the Companies Act, 2013, Share Capital of the Company can be broadly of two types or classes namely:

1. Equity Shares

2. Preference Shares

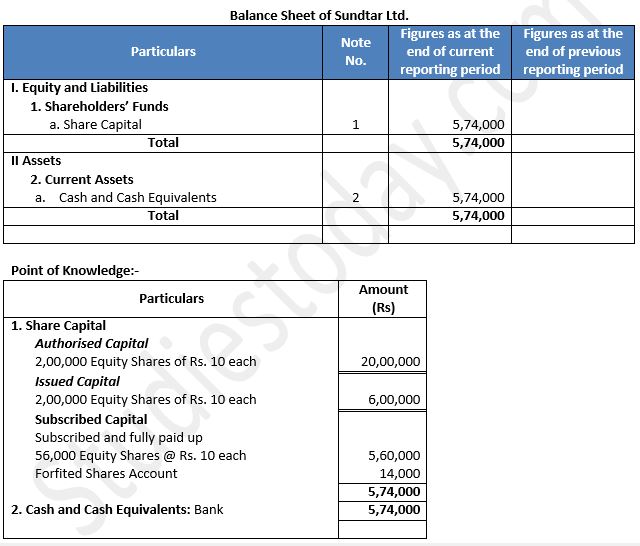

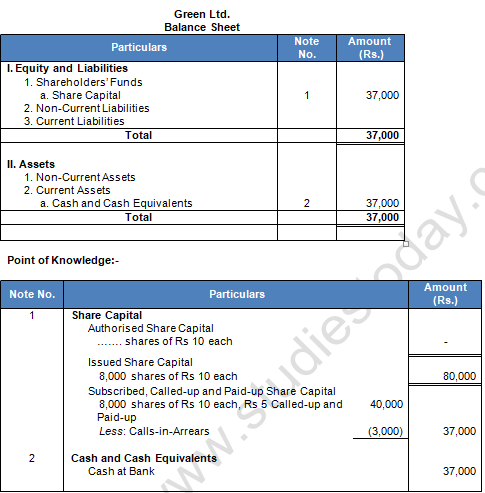

Q3: Sunstar Ltd. has an authorised capital of ₹ 20,00,000 divided into equity shares of ₹ 10 each. The company invited applications for issuing of 60,000 shares. Applications were received for 58,000 shares.

All calls were made and were duly received except the final call of ₹ 3 per share on 2,000 shares. These shares were forfeited.

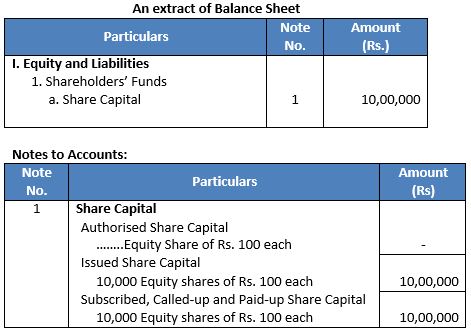

Present the ‘Share Capital’ in the Balance Sheet of the Company as per Schedule III, Part I of the Companies Act, 2013. Also prepare ‘Notes to Accounts’ for the same.

Answer 3:

About Solution:

Right to receive dividend before it is paid to Equity Shareholders. Such dividend is paid as a fixed amount or an amount calculated at a fixed rate which may either be free of or subject to income tax.

Things to Remember:

Right to receive dividend before it is paid to Equity Shareholders. Such dividend is paid as a fixed amount or an amount calculated at a fixed rate which may either be free of or subject to income tax.

Important Notes:

Dividend: With reference to dividend, Preference shares are classified as Cumulative and Non Cumulative Preference Shares.

1. Cumulative: This class carries the right to receive arrears dividend before dividend is paid to the Equity Shareholders.

2. Non-Cumulative: These classes do not carry the right to receive arrears of dividend.

Participation in Surplus Profit: With reference to participation, Preference shares are classified as Participating and Non-Participating Preference Shares.

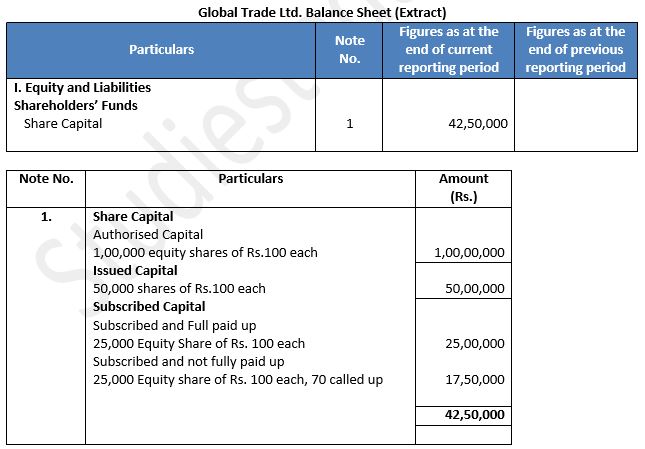

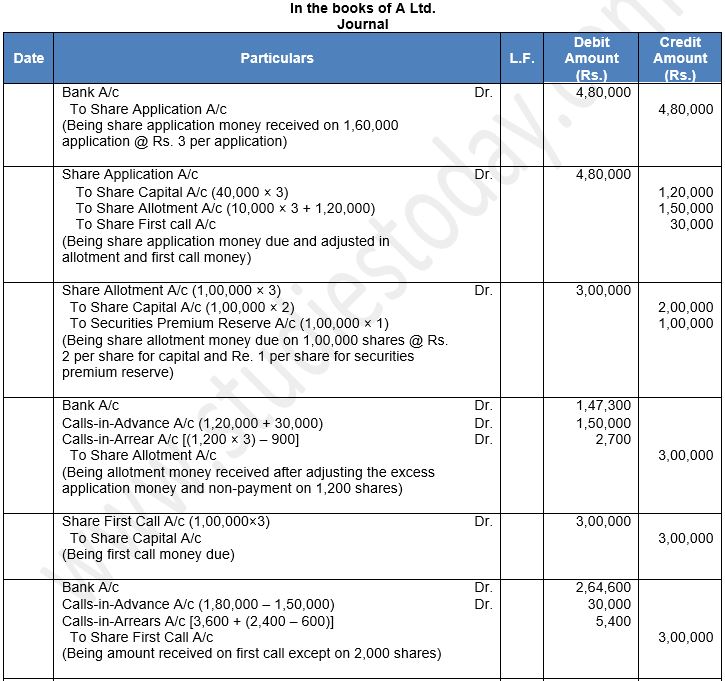

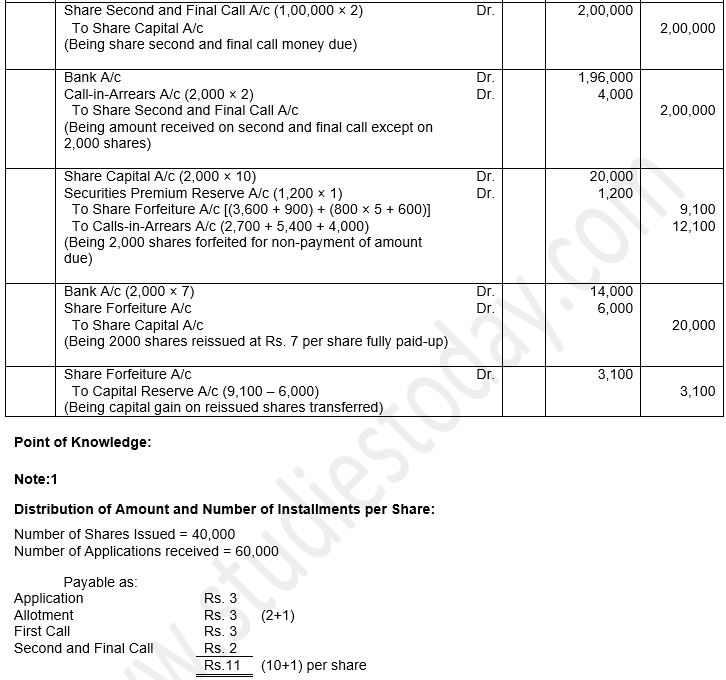

Q 4: Global Trade Ltd. has authorised share capital of ₹ 1,00,00,000 divided into 1,00,000 Equity Shares of ₹ 100 each. It has existing issued and paid up capital of ₹ 25,00,000. It further issued to public 25,000 Equity Shares at a premium of 20% for subscription payable as under:

On Application: Rs. 3

On Allotment: Rs. 4 and

On Call: Balance Amount

The issue was fully subscribed and allotment was made to all the applicants. The company did not make the call during the year.

Show Share Capital in the Balance Sheet of the company.

Answer 4:

About Solution:

Authorised Capital: It is the amount stated in the Memorandum of Association and such amount is the maximum amount that a company can raise as share capital. It is stated separately for each class or kind of shares. As per Section 2 (8) of the Companies Act, 2013, such capital as authorized by the memorandum of a company to be maximum amount of share capital of the company is called as Authorised Capital or Nominal Capital.

Things to Remember:

Issued Capital: It is a part of the nominal value or Authorised Share Capital which is issued from time to time for subscription. Therefore, amount of Issued Capital cannot exceed the company's Authorised Share Capital. As per Section 2 (50) of the Companies Act, 2013,

Important Notes:

Subscribed Capital: It is a part of the capital which is for the time being subscribed by the members of a company. As defined by Section 2 (86) of the Companies Act 2013, such part of the capital which is for time being subscribed by the members of a company. This can further be divided into:

1 - Subscribed and fully paid-up: It is a situation where the company has called-up the total nominal value of the share and has received the same.

2 - Subscribed and not fully paid-up: It is a situation where the company has called-up the total nominal value of the share, but has not receive it or has not called-up the total nominal value of the share.

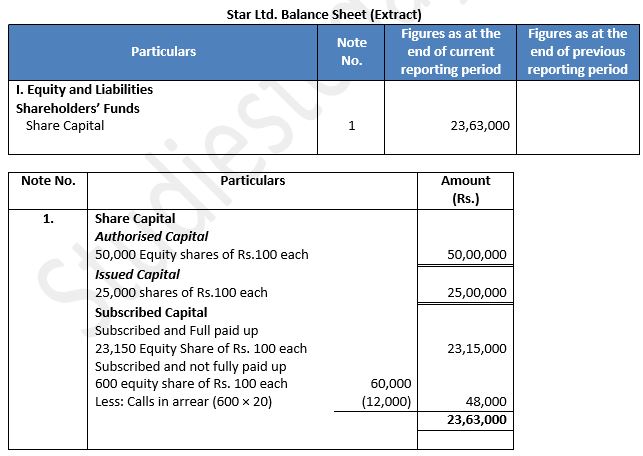

Q5: Star Ltd. is registered with capital of ₹ 50,00,000 divided into 50,000 equity shares of ₹ 100 each. The Company issued 25,000 equity shares for subscription. Subscription was received for 23,750 shares and all the due amount was duly received, except the first and final call of ₹ 20 per share on 600 shares. Show the ‘Share capital’ in the Balance Sheet of the company.

Answer 5:

About Solution:

Understanding the two terms, i.e., Called-up and Paid-up: Called-up Capital: According to section 2(15) of the Companies Act, 2013, Called-up Capital means such part of the capital which has been called for payment.

Paid-up Capital: According to section 2(64) of the Companies Act, 2013, Paid-up Share Capital or Share Capital Paid-up means the amount that the shareholder has paid and the company has received against the amount Called-up in respect of the shares towards share capital or has been credited to it as paid-up.

Things to Remember:

Reserve Capital: It is a part of Subscribed Capital remaining uncalled that a company resolves, by a Special Resolution, not to call except in the event of winding up of the company. Such number of shares are shown as "Subscribed but not fully paid-up".

Important Notes:

The one basic difference between is Reserve Capital is a part of uncalled capital which cannot be called-up except in the event of winding up and capital reserve is a part of reserves which cannot be used for distribution of dividends.

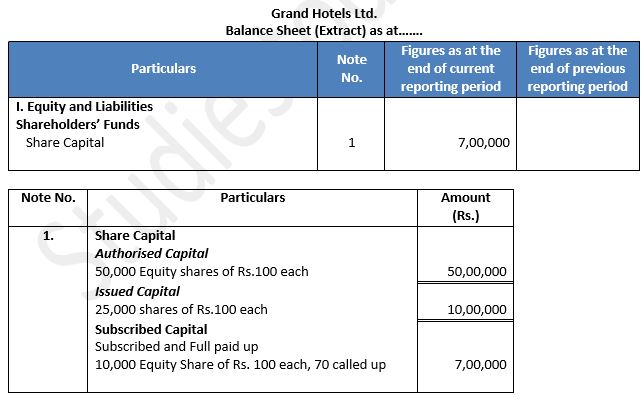

Q6: Grand Hotels Ltd. had authorised capital of ₹ 50,00,000 divided into 50,000 Equity Shares of ₹ 100 each. It issued 10,000 Equity Shares to public for subscription on the following terms:

On Application ₹ 40 per share

On Allotment ₹ 30 per share

Balance on First and Final Call.

Shares were fully subscribed and amounts called were duly received. First and Final call was not yet made.

Prepare Balance Sheet of the company showing Share Capital.

Answer 6:

About Solution:

Meaning of Oversubscription:-Oversubscription means, the number of applications received are more than the number of shares offered.

Things to Remember:

If the shares are allotted against the application, then there is no adjustment required as share capital is credited against the application money received. However, if the applications are rejected, the application money with respect to the rejected applications can be refunded or adjusted (in case of pro-rata allotment) against the allotment or calls on shares.

Important Notes:

Meaning of Pro-rata Allotment of Shares: This is one of the alternative available with the company for allotment of shares when the number of shares applied for are more than the number of shares offered for subscription.

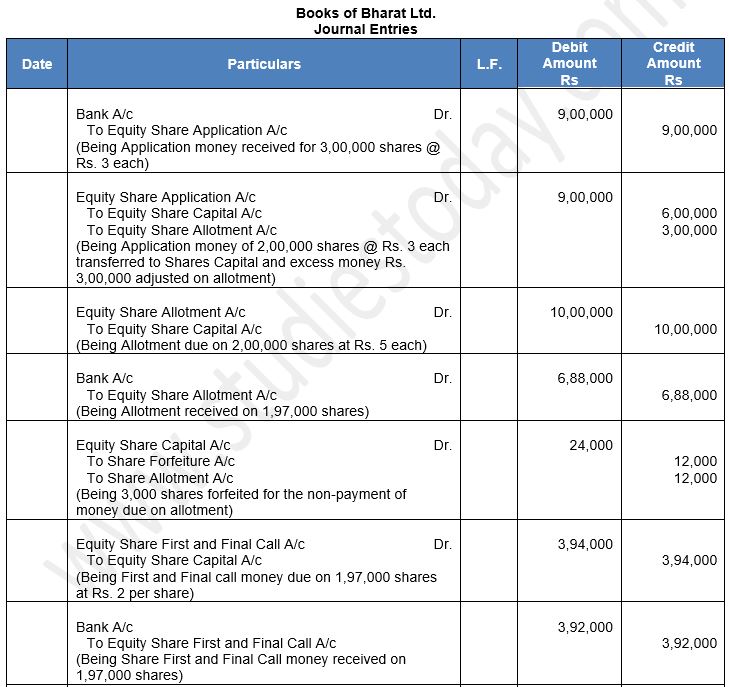

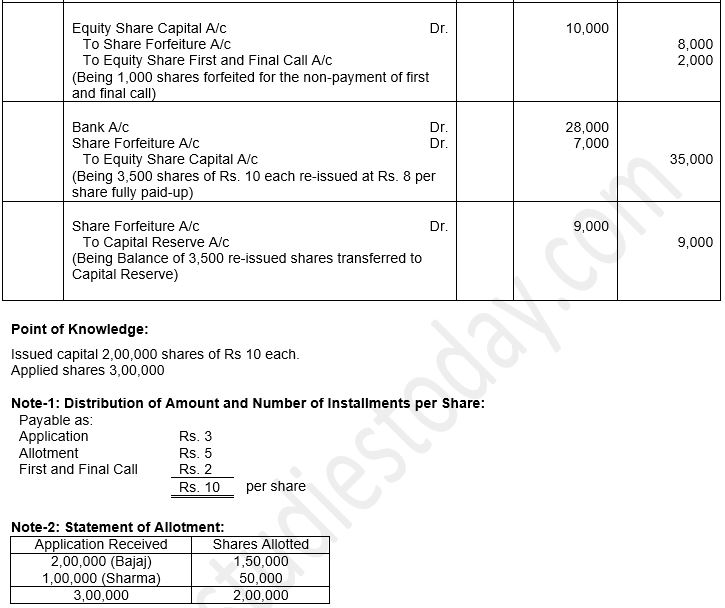

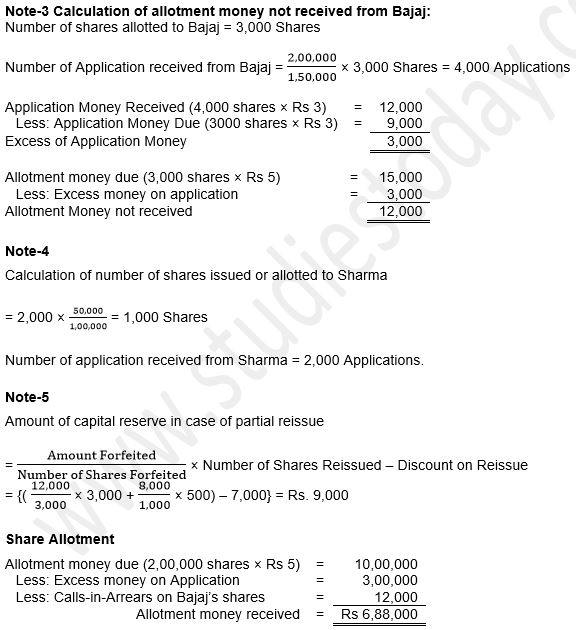

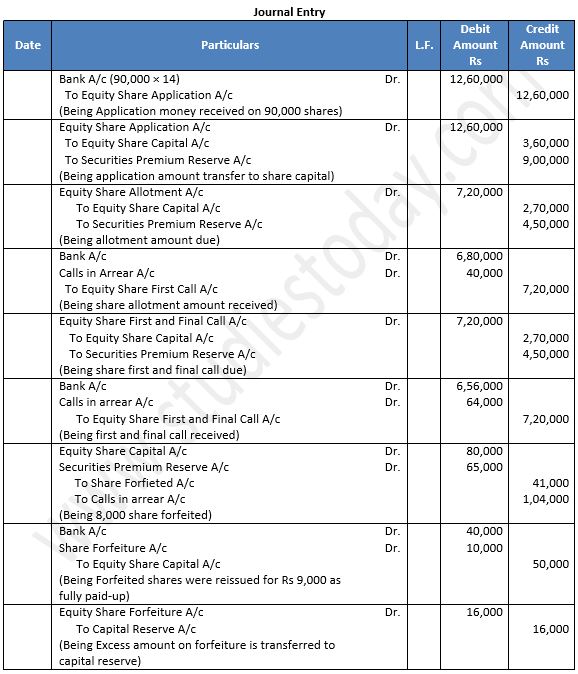

Q7: Altaur Ltd. was registered with an authorised Capital of ₹ 4,00,00,000 divided in 25,00,000 Equity Shares of ₹ 10 each and 1,50,000, 9% Preference Shares of ₹ 100 each. The company issued 8,00,000 Equity Shares for public subscription at 20% premium, payable ₹ 3 on application; ₹ 7 on allotment (including premium) and balance on call. Public had applied for 10,00,000 shares. Excess Applications were sent letters of regret. All the dues on allotment were received except on 15,000 shares held by Sanju. Another shareholder Rocky paid his call dues along with allotment on his holding of 25,000 shares. You are required to prepare the Balance Sheet of the company as per Schedule III of Companies Act, 2013, showing Share Capital balance and also prepare Notes to Accounts.

Answer 7:

About Solution:

Treatment of Surplus Application Money on Pro-rata Allotment:

1 - If the question is silent or states that 'excess application money received is to be adjusted against allotment', surplus application money is adjusted against allotment money due and excess application money, if any is refunded.

2 - If the question requires that surplus application money is to be refunded after adjustment of Allotment Money and Call Money, then the amount is transferred to Shares Allotment Account and Calls-in Advance Account. The balance, if still left, is refunded.

Things to Remember:

Meaning of under subscription of Shares and Difference between Oversubscription and under subscription: Under subscription: It is a situation when the number of shares applied are less than the number of shares issued for subscription

Important Notes:

Meaning of Calls-in-Arrears and Interest on Calls-in-Arrears

Calls-in-Arrears: If the shareholder does not pay the call amount due on allotment or on any subsequent calls according to the terms, the amount not received is called Calls-in Arrears

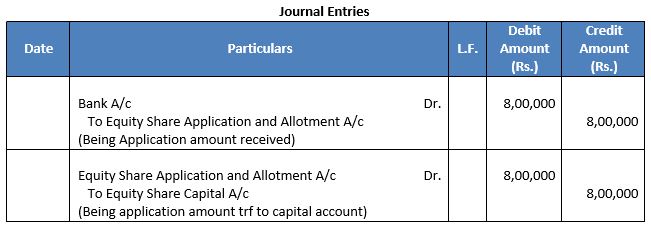

Q8: Fragrances Ltd. was registered with capital of ₹ 5,00,000 divided into 50,000 Equity Shares of ₹ 10 each. It issued 20,000 Equity Shares to public for subscription. The shares were subscribed and calls were made and received except first and final call of ₹ 2 on 500 shares held by Varun.

Prepare Balance Sheet of the company showing Share Capital.

Answer 8:

About Solution:

Interest on Calls-in-Arrears: If the company is authorized by the Articles of Association, it may charge an interest at the specified rate on Calls-in-Arrears from the due date to the date of payment. In case Articles of Association is silent, Table F of the Companies Act, 2013 shall apply which provides for interest on Calls-in-Arrears at the rate of 10% p.a.

Things to Remember:

Accounting treatment without opening Calls-in-Arrears Account: In this method, amount S received from the shareholders is credited to the relevant call account. The respective call accounts (first, second, etc.) will continue showing debit balance equal to the total amount unpaid on those calls. On a subsequent date, when the amount of Calls-in- Arrears is received, Bank Account is debited and relevant call account is credited. Call Money Due.

Important Notes:

Accounting treatment by opening Calls-in-Arrears Account: In this method, unlike the first method, the unpaid amount is transferred to Calls-in-Arrears Account. On account of this, Share Allotment Account and Shares Call Accounts will not show any balance. The Calls-in Arrears Account will show a debit balance equal to the total unpaid amount on allotment or the calls. At a later date, on receipt of arrear amount, it is credited to the Calls- in-Arrears Account and same is closed with a corresponding debit to Bank A/c

Q9: Red Roses Ltd. was registered with capital of ₹ 25,00,000 divided into 25,000 Equity Shares of ₹ 100 each. It issued 15,000 Equity Shares to public for subscription. The shares were subscribed and calls were made and received except allotment money of ₹ 40 on 100 shares held by Parul and first and final call of ₹ 20 on 500 shares, including shares held by Parul. Prepare Balance Sheet of the company showing Share Capital.

Answer 9:

About Solution:

Meaning Of Calls-in-Advance and Interest on Calls-in-Advance:

Calls-in-Advance: An amount which is accepted by the company against the call or calls not yet made is termed as Calls-in-Advance. A company may accept such calls-in-advance amount only if it is allowed by the Articles of Association of the Company.

Interest on Calls-in-Advance: If the Articles of Association provides for any interest on Calls-in-Advance, then interest can be paid by the company. In case when the Articles of Association is silent, Table F of the Companies Act, 2013 shall apply where company is liable to pay interest at the rate of 12% p.a.

Things to Remember:

Journal Entry passed:

To record calls-in-advances:

Bank A/c Dr. [amount of calls money received in advance]

To Calls-in-Advance A/c

Important Notes:

Difference between Calls-in-Arrears and Calls-in-Advance:

Calls-in-Arrears:- Amount which is called-up by the company but not paid by the shareholders.

Calls-in-Advance:- Amount which is not called-up by the company, but paid by the shareholders.

Q10: East India Hotels Ltd. was registered with authorised capital of ₹ 25,00,000 divided into 2,50,000 Equity Shares of ₹ 10 each. It issued 1,50,000 Equity Shares to public for subscription. The shares were subscribed and calls were made and received. First and final call of ₹ 3 was not made. Paresh holder of 5,000 shares paid the call money along with the allotment money.

Prepare Balance Sheet of the company showing Share Capital.

Answer 10:

Question 11: Amit Ltd. was registered with a capital of ₹ 5,00,000 in shares of ₹ 10 each and issued 20,000 such shares at a premium of ₹ 2 per share, payable as ₹ 2 per share on application, ₹ 5 per share on allotment (including premium) and ₹ 2 per share on first call made three months later. All the money payable on application and allotment was duly received but when the first call was made, one shareholder paid the entire balance on his holding of 300 shares and another shareholder holding 1,000 shares failed to pay the first call money. Pass Journal entries to record the above transactions and show how they will appear in the company’s Balance sheet.

Answer 11:

Q12: Global Sales Ltd. issued 2,50,000 Equity Shares of ₹ 10 each to public at par for subscription, amount being payable as application money. Pass necessary Journal entries in the books of the company.

Answer 12:

Things to Remember:

Terms of Issue of Shares: A company may issue shares at par or at premium as explained below:

Shares are issued at Par: It means that the issue price is same as the nominal value (face value) of the shares.

Shares are issued at Premium: It means that the issue price is more than the nominal value (face value) of the shares. Amount in excess of the nominal value of the share is termed as premium and such amount of premium is credited to Securities Premium Account or Securities Premium Reserve Account.

Important Notes:

In such case, allotment can be done by any of the 2 alternatives available.

First Alternative: Under this alternative, some applications are accepted and excess applications are rejected.

Second Alternative: Under this alternative, all applicants are allotted shares in proportion which is known as Partial or Pro-rata Allotment.

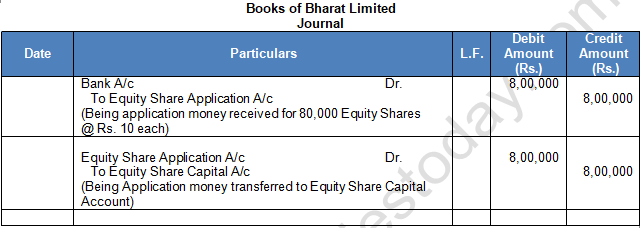

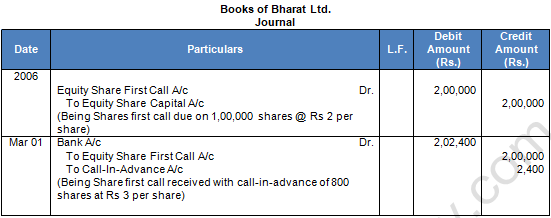

Q13: Authorised Capital of ₹ 16,00,000 of Bharat Ltd. is divided into 1,60,000 Equity Shares of ₹ 10 each. Out of these shares, 80,000 Equity Shares were issued at par to public for subscription. The issue price is payable on application. All the shares were subscribed. Pass necessary Journal entries in the books of the company.

Answer 13:

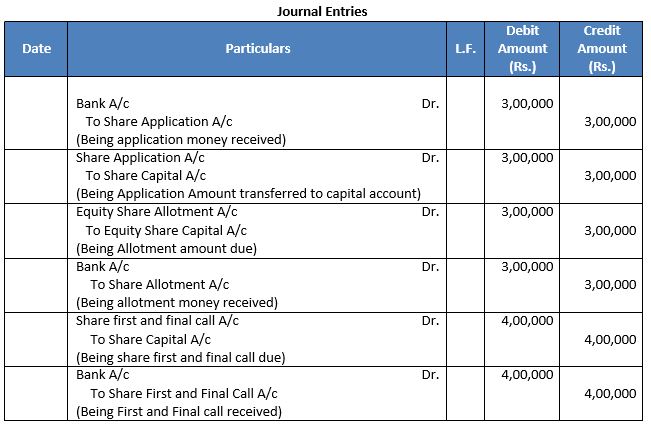

Q14: Alok Leathers Ltd. invited applications for 10,000 shares of ₹ 100 each payable as follows:

₹ 30 on application, ₹ 30 on allotment and balance on first and final call.

All the shares were applied and allotted and the money was duly received.

You are required to Journalise these transactions and show share capital in the Balance Sheet.

Answer 14:

Things to Remember:

Holding Company and Subsidiary Company: A holding company is a company which controls another company (called subsidiary company) either by acquiring more than half of the equity shares of another company or by controlling the composition of Baord of Directors of another company or by controlling a holding company which controls another company.

Important Notes:

Listed Company and Unlisted Company: A company is required to file an application with stock exchange for listing of its securities on a stock exchange. When it qualifies for the admission and continuance of the said securities upon the list of the stock exchange, it is known as listed company. A company whose securities do not appear on the list of the stock exchange is called unlisted company.

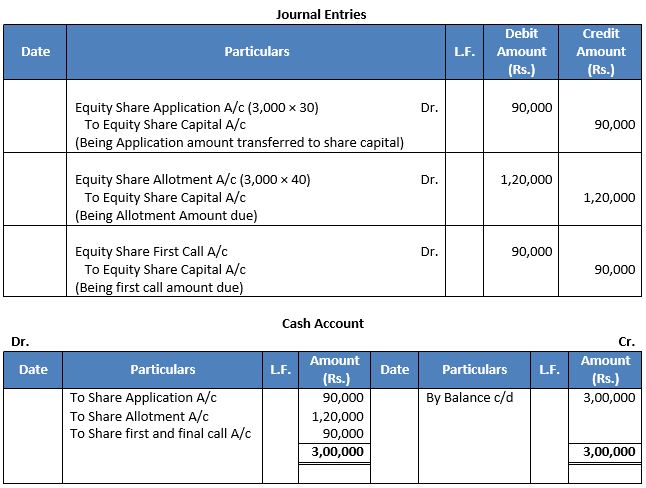

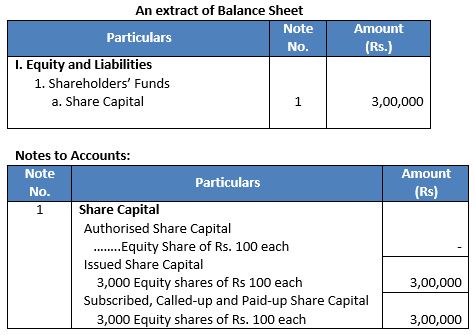

Q15: National Textiles Ltd. was registered with the authorised capital of ₹ 3,00,000 divided into 3,000 shares of ₹ 100 each, which were offered to the public. Amount payable as ₹ 300 per share on application, ₹ 40 per share on allotment and ₹ 30 per share on first and final call. These shares were fully subscribed and all money was duly received.

Prepare Cash Book, Journal and Balance Sheet showing Share Capital.

Answer 15:

Things to Remember:

Shares issued for consideration other than cash are disclosed in the Balance Sheet under 'Subscribed Capital'. This may be further subscribed and fully paid or subscribed but not fully paid as the case may be and shown in Notes to Accounts under Share Capital.

Important Notes:

Meaning and Accounting Entries for Forfeiture of Shares:

i) It means cancellation of shares for non-payment of calls due.

ii) It can be done by the company only if it is allowed by its Articles of Association.

iii) If any of the shareholders of the company does not pay the amount of call, the company may exercise this power to forfeit the shares held by the shareholder on which amount of call is not paid.

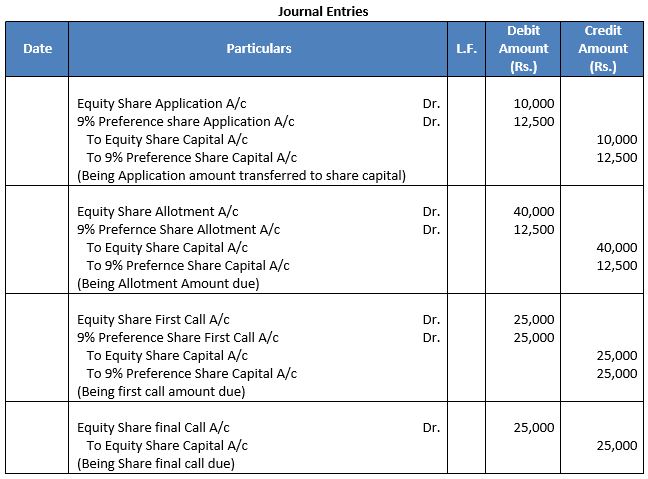

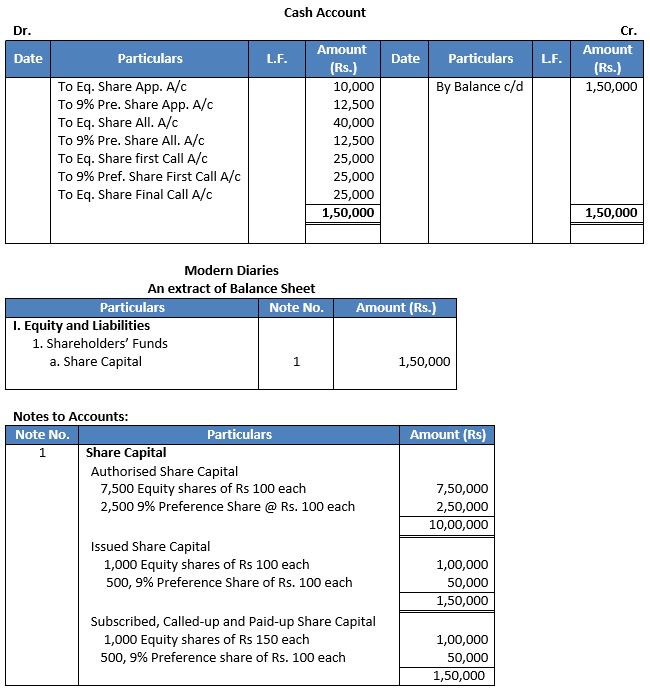

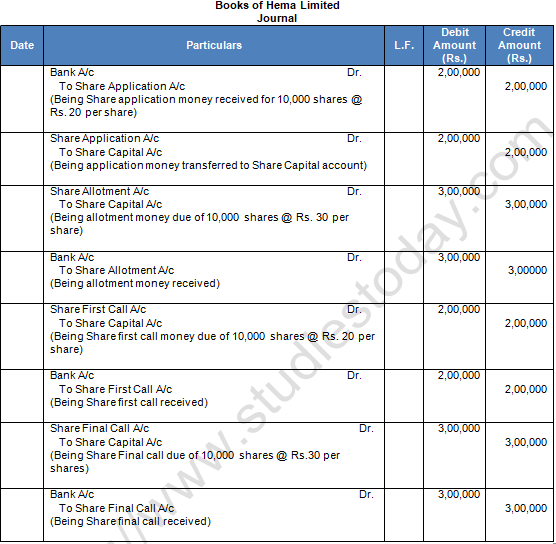

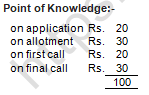

Q16: Modern Diaries Ltd. was registered with an authorised capital of ₹ 10,00,000 divided into 7,500 Equity Shares of ₹ 100 each and 2,500 Preference Shares of ₹ 100 each each. 1,000 Equity Shares and 500; 9% Preference Shares were offered to public on the following terms – Equity Shares payable ₹ 10 on application, ₹ 40 on allotment and the balance in two calls of ₹ 25 each. Preference Shares are payable ₹ 25 on application, ₹ 25 on allotment and ₹ 50 on first and final call. All the shares were applied for and allotted. Amount due was duly received.

You are required to prepare Cash Book, pass necessary Journal entries and show share capital in the Balance Sheet.

Answer 16:

Q17: Premio Ltd. issued 50,000 Equity Shares of ₹ 100 each at a premium of ₹ 50 per share, payable as follows:

₹ 100 per share on Application; and

Balance on Allotment.

The issue was subscribed and shares were issued to the applicants. Pass the necessary Journal entries.

Answer 17:

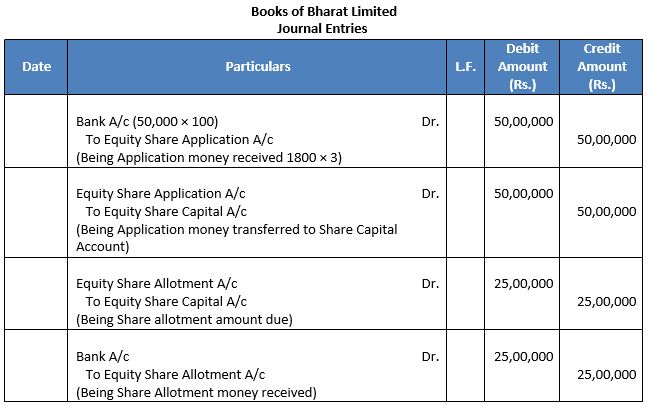

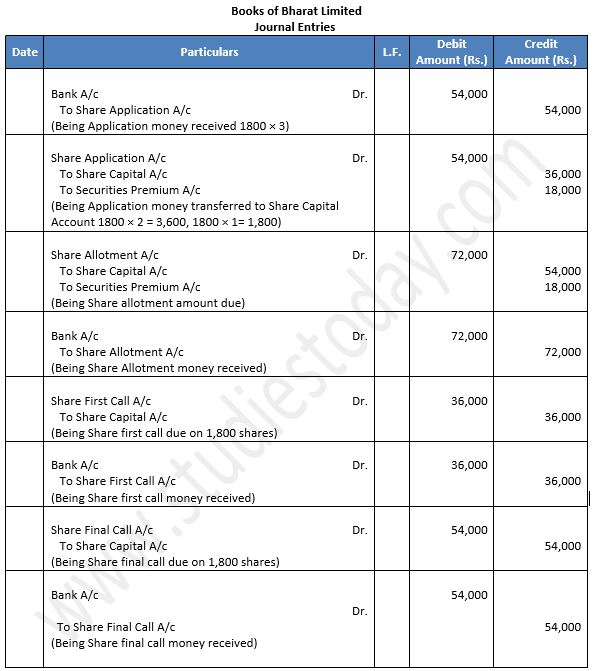

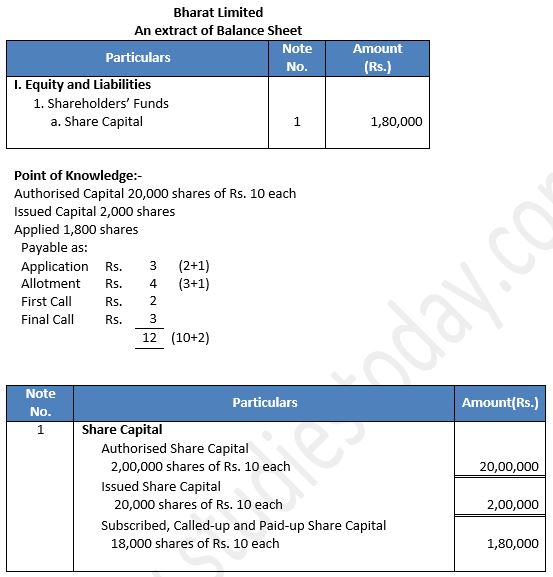

Q18: Bharat Ltd. was incorporated with a capital of Rs. 20,00,000 divided into shares of Rs. 10 each. 20,000 shares were offered for subscription and out of these, 18,000 shares were applied for and allotted. Rs. 3 per share (including Rs. 1 premium) was payable on application, Rs. 4 per share (including Rs. 1 premium) on allotment, Rs. 2 per share on first call and Rs. 3 per share on final call. All the money was received. Give necessary Journal entries and show share capital in the Balance Sheet.

Answer 18:

About Solution:

Securities offered to the selective group of persons by issuing private placement offer is known as the Private Placement of Shares. There are conditions specified by Companies Act, 2013 that are to be fulfilled for offering such private placement of shares.

Things to Remember:

i. Shares issued are of the same class of shares already issued;

ii. Such issue is authorised by a special resolution passed by the company;

iii. Such resolution specifies all possible details of the number of shares, consideration, market price, and class or classed of employees or directors to whom such shares are to be issued;

iv. At the date of issue, not less than 1 year has been elapsed since the date on which the company had commenced business.

Important Notes:

Public companies whose shares are listed in recognised stock exchanges for public trading are called as Listed Company. Such companies are also known as Quota Companies. Once the securities are listed it helps the investors in knowing the value of their investment in a listed company. It provides the potential investors an idea about the goodwill of the company and helps them on taking future investment decisions and evaluate the viability of investing in the company.

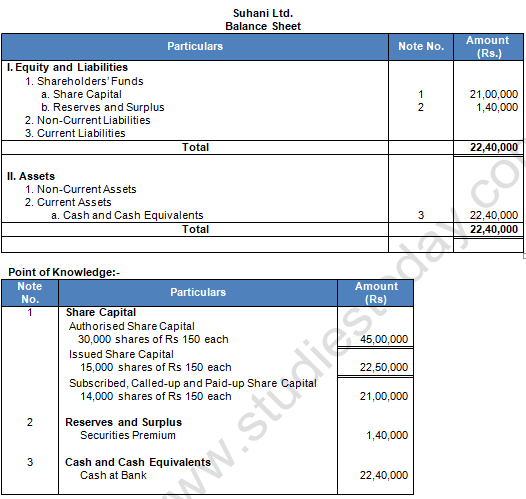

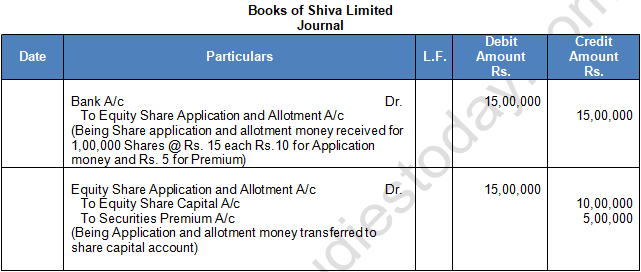

Q19: Authorized capital of Suhani Ltd. is Rs. 45,00,000 divided into 30,000 shares of Rs. 150 each. Out of these company issued 15,000 shares of Rs. 150 each at a premium of Rs. 10 per share. The amount was payable as follows: Rs. 50 per share on application , Rs. 40 per share on allotment (including premium), Rs. 30 per share on first call and balance on final call. Public applied for 14,000 shares. All the money was duly received. Prepare an extract of Balance Sheet of Suhani Ltd. as per Schedule III, Part I of the companies Act, 2013 disclosing the above information. Also prepare 'Notes to Accounts ' for the same.

Answer 19:

About Solution:

The minimum amount of shares that must be subscribed by the public, so that the share allotting company can allot shares to the applicants, is termed as Minimum Subscription. If Minimum Subscription is not attained, the company cannot allot shares to its applicants and it should refund the amount received to the public. Minimum Subscription should not be less than 90% of the amount issued.

Things to Remember:

Two types of shares:

i.) Preference Share: Section 43 of the Company Act, 2013 defines preference shares as which entitles the holder to receive dividend and also the right to receive capital invested in order of preference before equity share holders when the company is wind up.

ii.) Equity Shares: Equity shareholders manage the affairs of the company and also have a voting right. These types of share do not possess any preferential right for dividend payment or capital repayment. The dividend rate is not fixed and varies year on year which is dependent on available profit left after distributing to preference shareholders.

Important Notes:

When the shareholder pays the whole amount before the share payment date becomes due i.e. before the share issuing company makes a call for it. It is known as Calls-in-advance. In case of advance payment the company has provision in their article of association to pay interest to shareholders from date of payment till date of call. If the article of association is silent in this regard, then a default 6% interest is provided.

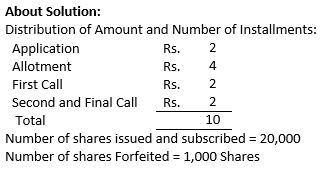

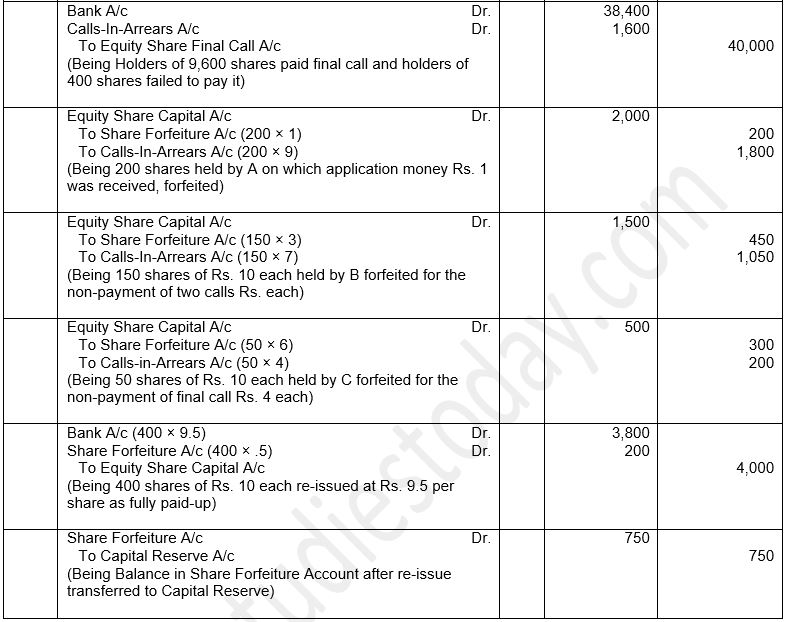

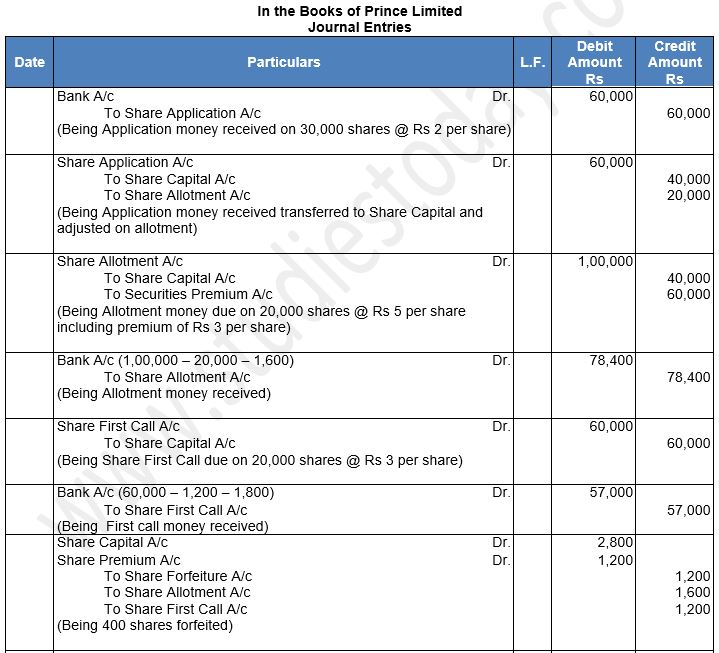

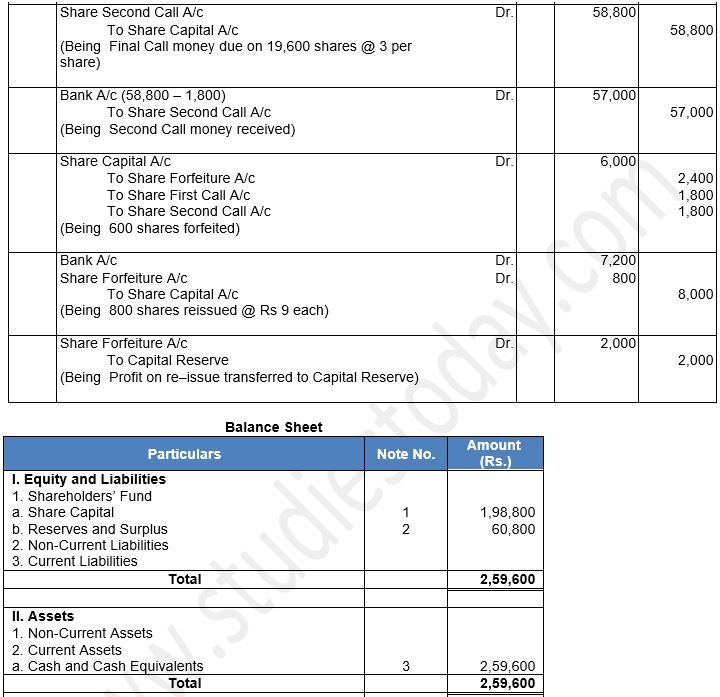

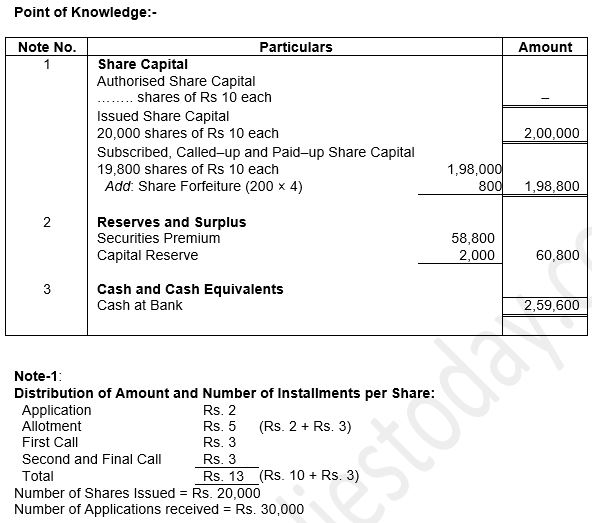

Q20: Super Star Ltd. makes an issue of 10,000 Equity Shares of Rs. 100 each, payable as:

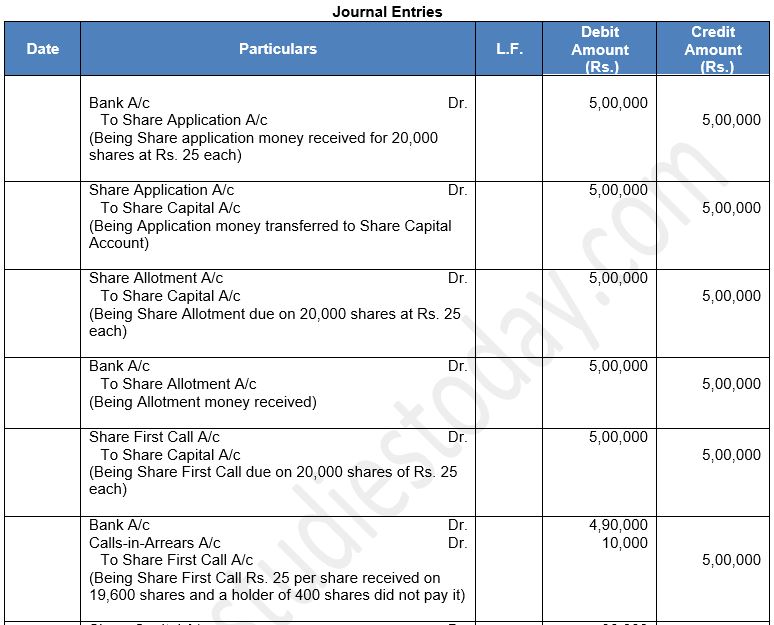

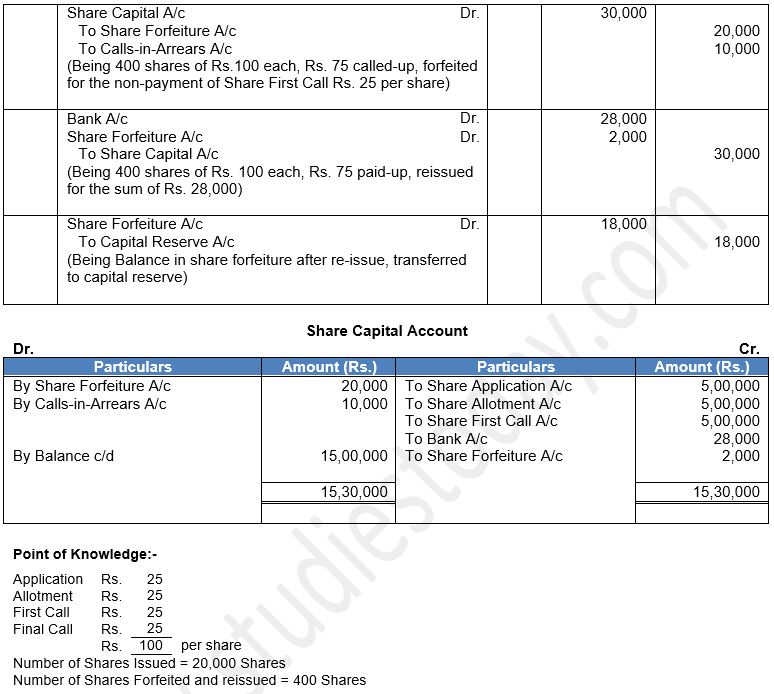

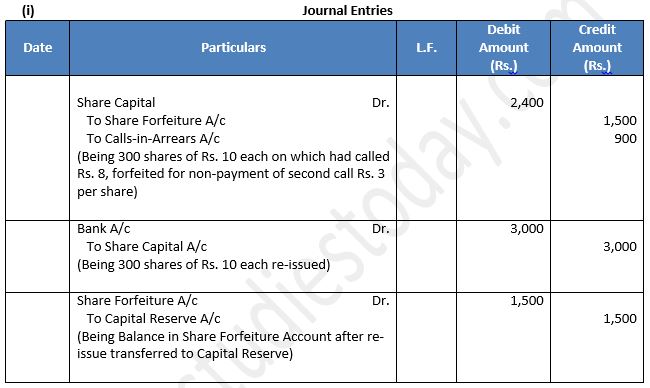

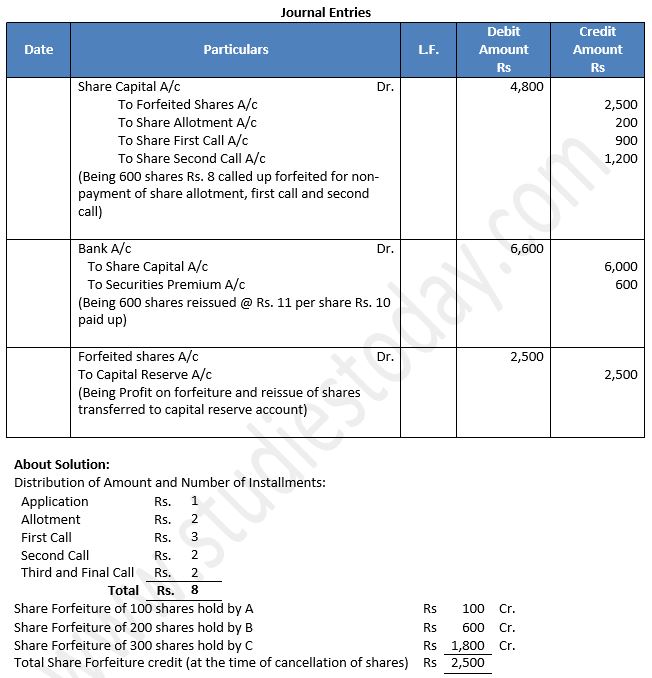

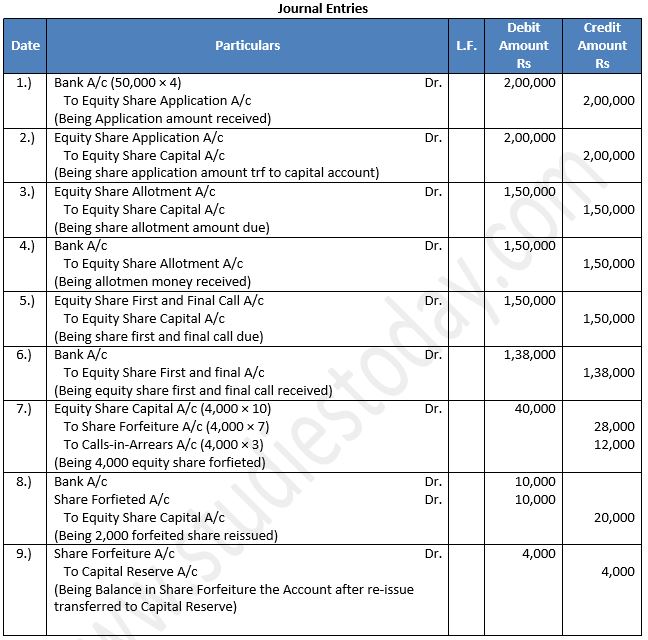

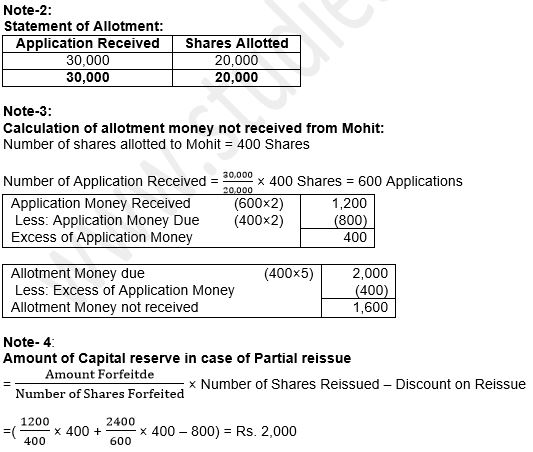

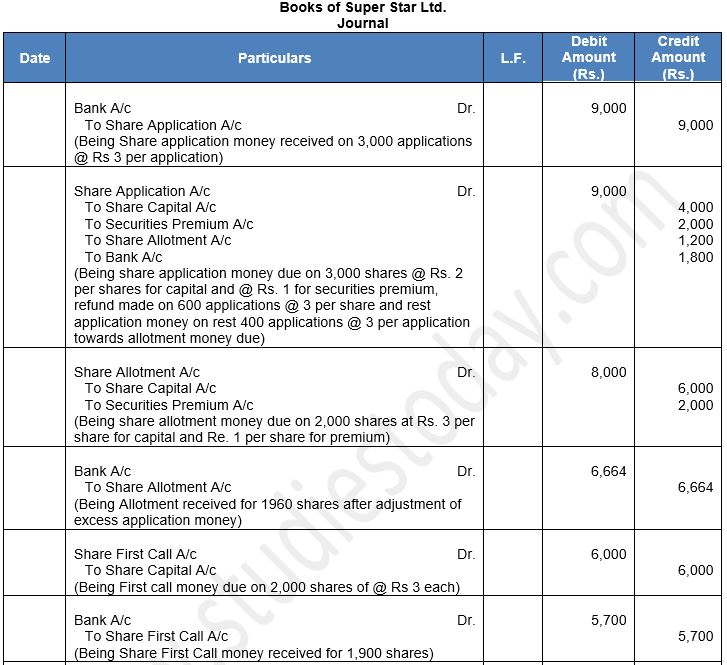

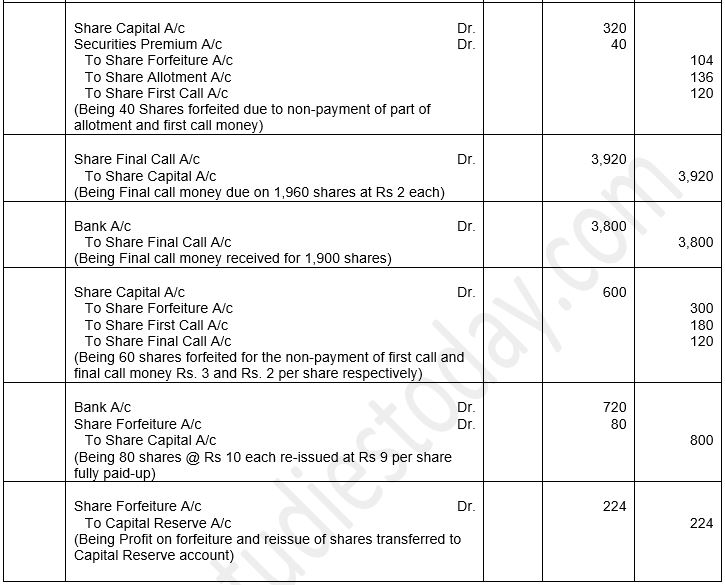

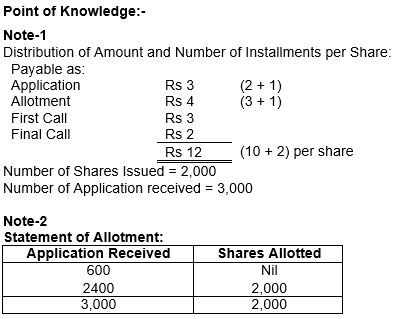

On application and allotment Rs. 50 per share,

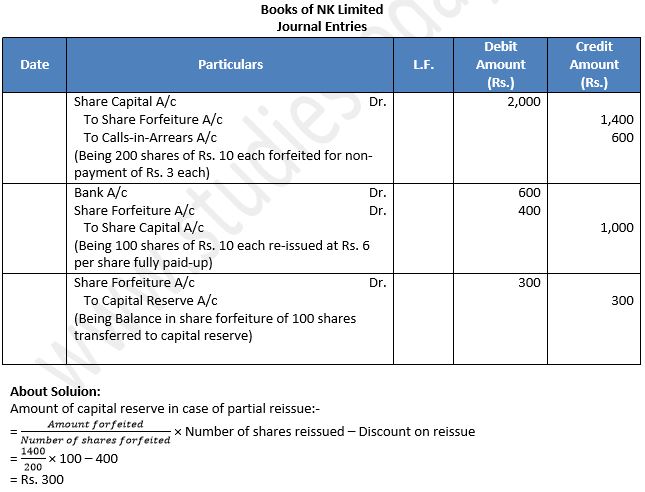

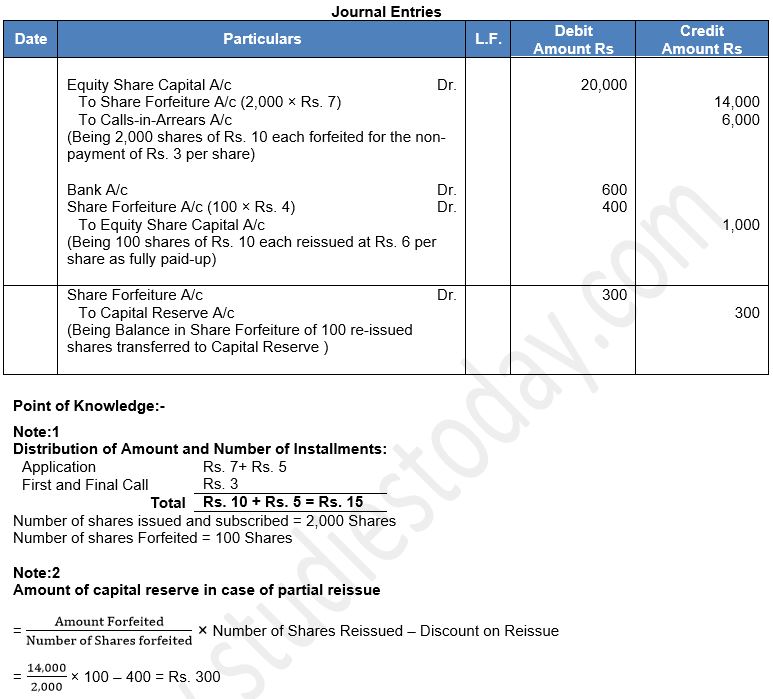

On first call Rs. 25 per share,

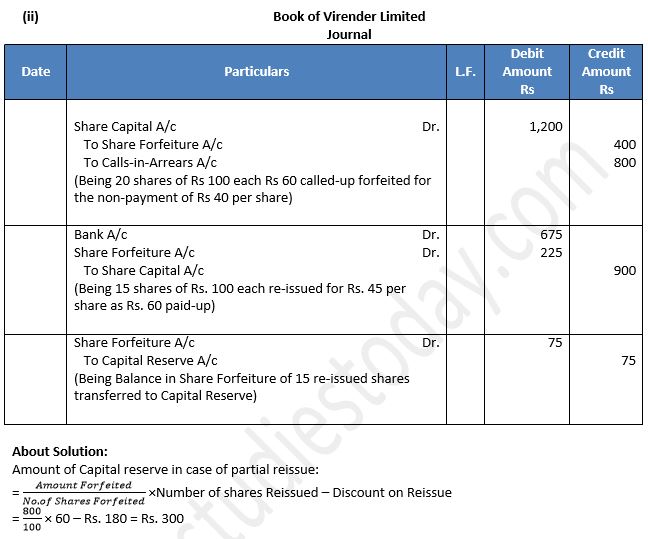

On second and final call Rs. 25 per share.

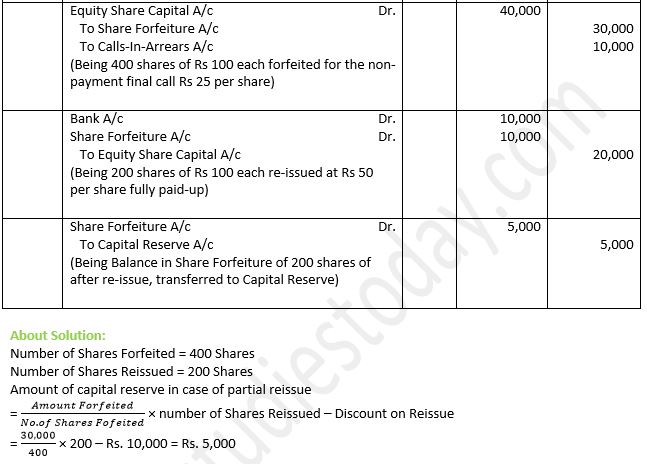

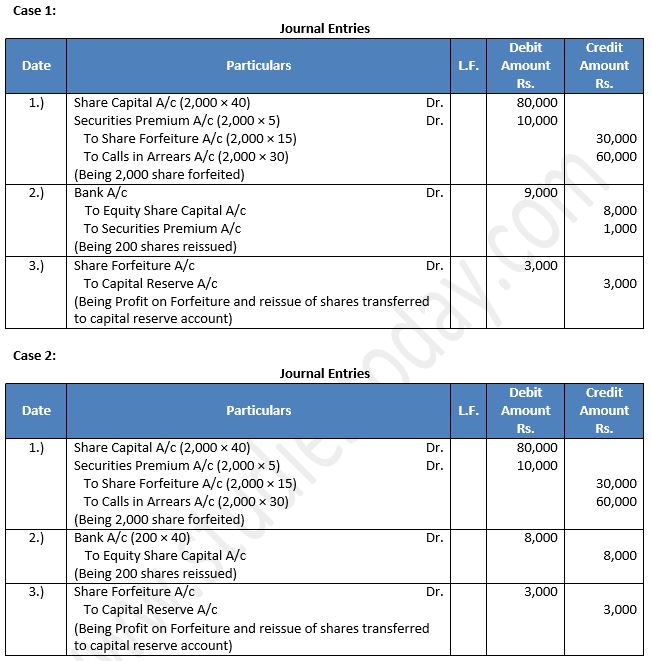

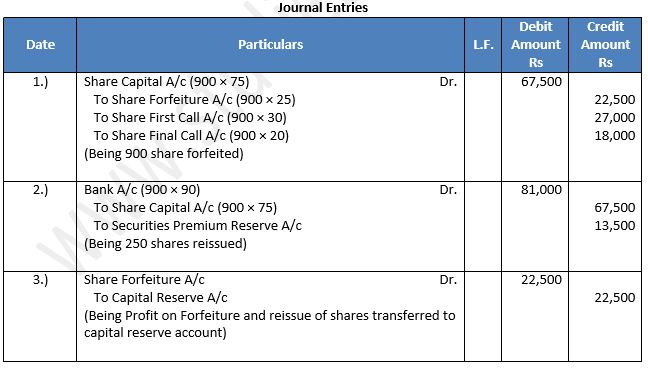

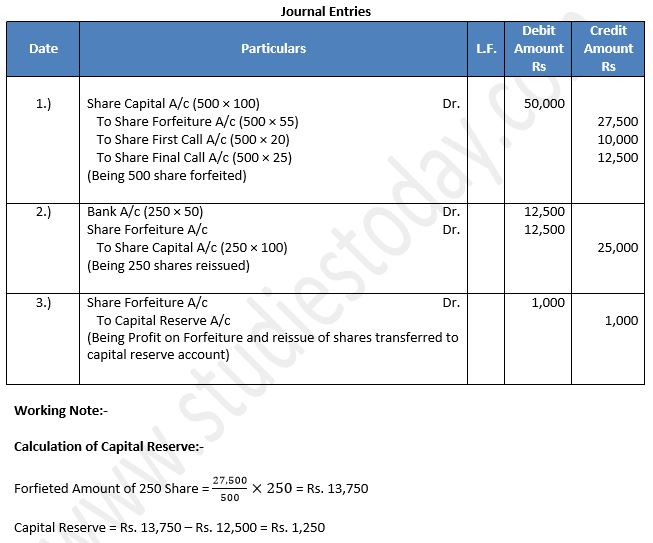

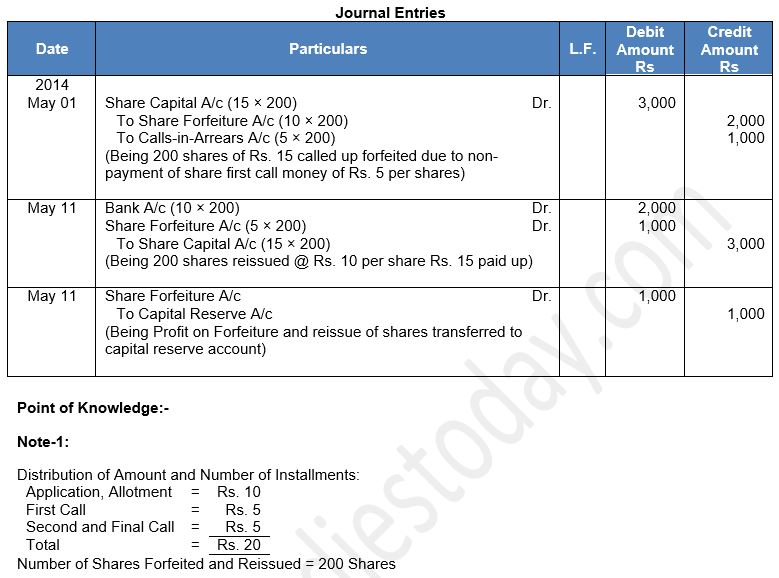

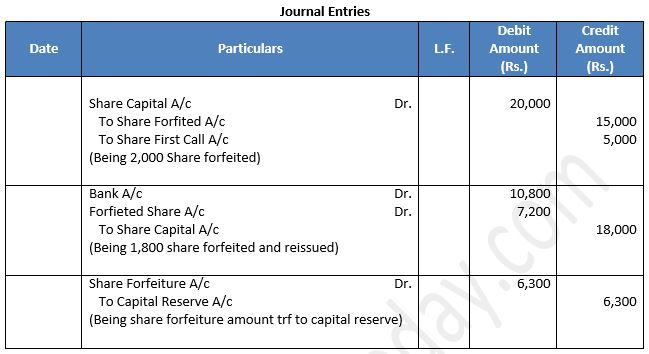

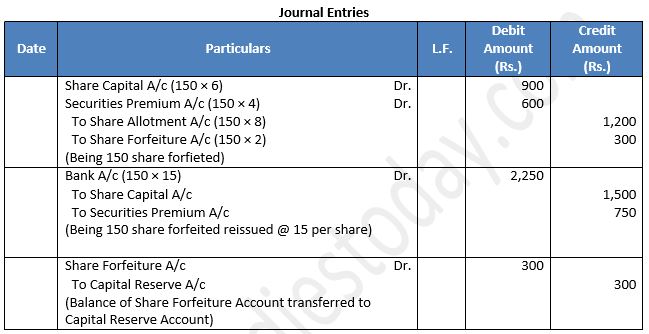

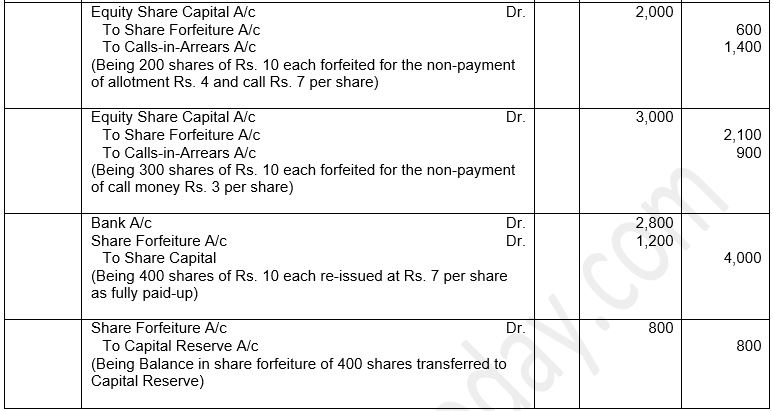

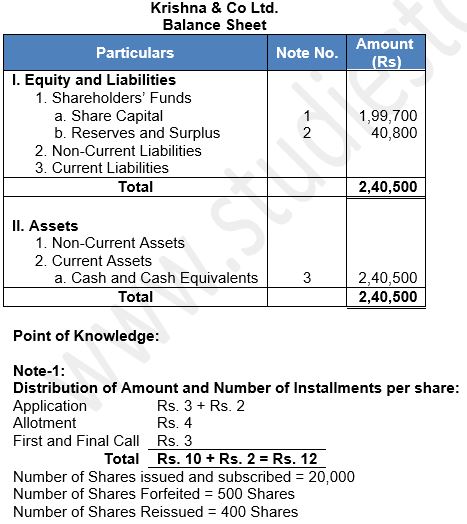

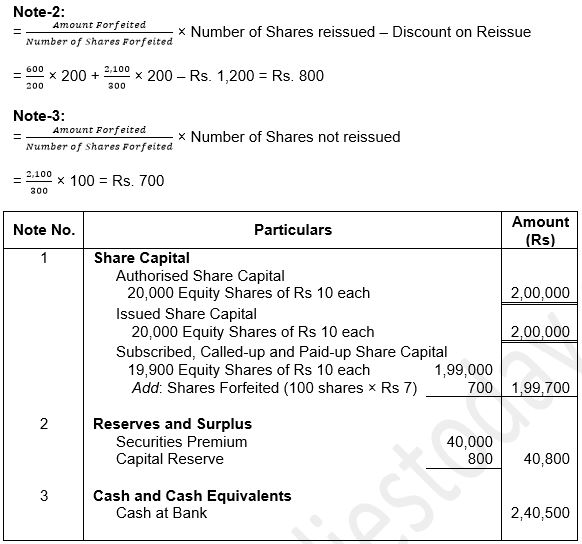

Members holding 400 shares did not pay the second and final call and the shares are duly forfeited, 200 of which are reissued as fully paid-up @Rs. 50 per share. Pass journal entries in the books of the company.

Answer 20:

Things to Remember:

Interest on Calls-in-Advance: If the Articles of Association provides for any interest on Calls-in-Advance, then interest can be paid by the company. In case when the Articles of Association is silent, Table F of the Companies Act, 2013 shall apply where company is liable to pay interest at the rate of 12% p.a.Interest on Calls-in-Advance: If the Articles of Association provides for any interest on Calls-in-Advance, then interest can be paid by the company. In case when the Articles of Association is silent, Table F of the Companies Act, 2013 shall apply where company is liable to pay interest at the rate of 12% p.a.

Important Notes:

If shares are issued for purchase of business: When a business is purchased, both assets and liabilities are taken over for a consideration which can be equal to, more than or less than the difference between values of assets and liabilities.

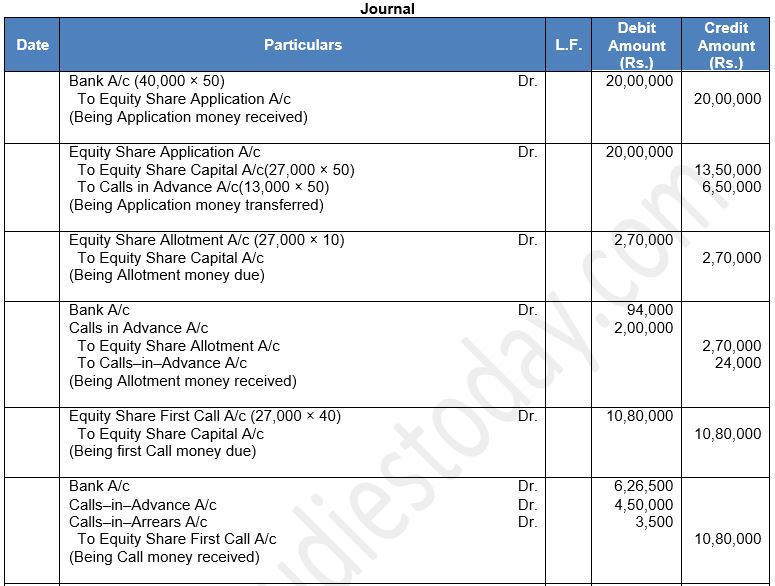

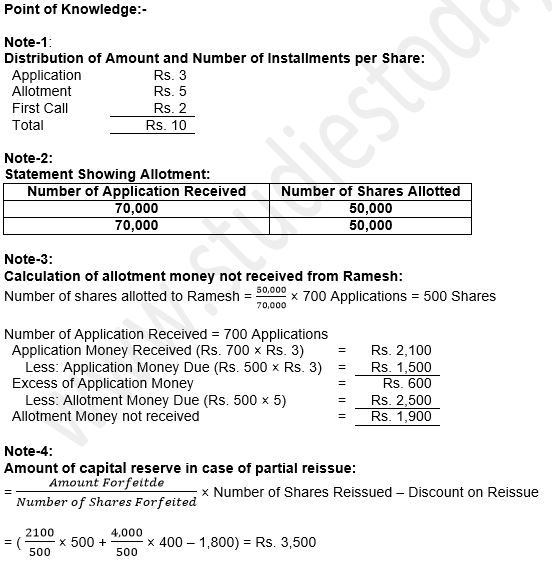

Q21: Faber Ltd. Invited applications for 70,000 equity shares of ₹ 100 each. The application money received @ ₹ 30 per share was ₹ 27,00,000. Name the kind of subscription. List the three alternatives for allotting these shares.

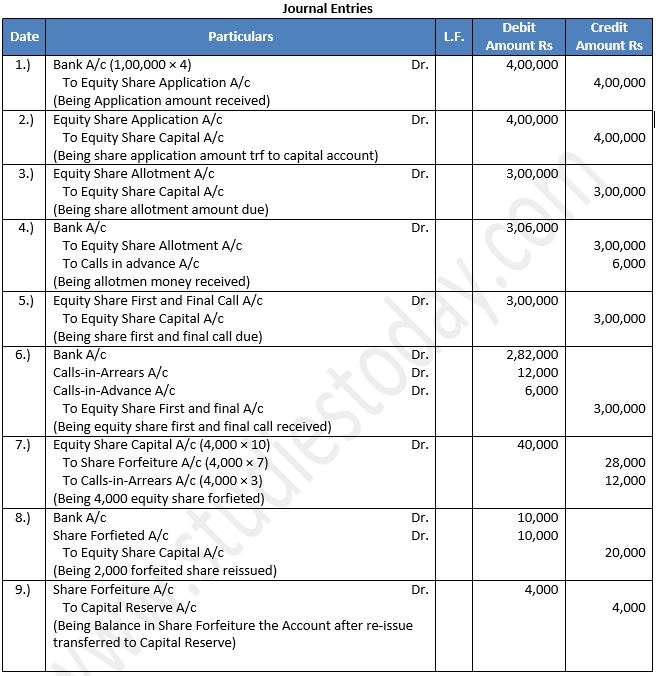

Answer 21:

Application Money is 70,000 × 3 = ₹ 21,00,000

Application Money Received = ₹ 27,00,000

Hence, it is the case of over-subscription.

1. The excess money over application ₹ 6,00,000 can be returned

2. The excess money over application ₹ 6,00,000 can be adjusted on allotment.

3. A part of the excess money over application can be returned and rest can be adjusted in allotment money.

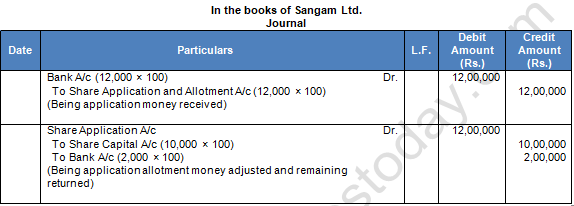

Q22: Sangam Ltd. invited applications for 10,000 Equity Shares of Rs. 100 each issued at par. The amount was payable on application. The issue was oversubscribed by 2,000 shares and allotment was made on pro rata basis. Pass necessary Journal entries.

Answer 22:

About Solution:

Preference Share: Section 43 of the Company Act, 2013 defines preference shares as which entitles the holder to receive dividend and also the right to receive capital invested in order of preference before equity share holders when the company is wind up.

Things to Remember:

Equity Shares: Equity shareholders manage the affairs of the company and also have a voting right. These types of share do not possess any preferential right for dividend payment or capital repayment. The dividend rate is not fixed and varies year on year which is dependent on available profit left after distributing to preference shareholders.

Important Notes:

Registration of a Company: In order to incorporate a company, procedure prescribed in the Companies Act, 2013 should be followed, this includes:

1. Promoters have to get the proposed company name approved from the Registrar of Companies.

2. After getting the name of the proposed company approved, the promoters have to submit Memorandum of Association, Articles of Association, consent of first directors to act as directors and a declaration that the requirements of the Companies Act have been complied with.

Thereafter, if the Registrar is satisfied that the requirements of the Companies Act, 2013 have been complied with, he shall issue the Certificate of Incorporation to the Company.

Q23: Citizen Watches Ltd. invited applications for 50,000 shares of Rs. 10 each payable Rs. 3 on application, Rs. 4 on allotment and balance on first and final call. Applications were received for 60,000 shares. Applications were accepted for 50,000 shares and remaining applications were rejected. All calls were made and received except First and Final call on 500 shares.

Pass the journal entries in the books of Citizen Watches Ltd.

Answer 23:

About Solution:

Minimum subscription: It is the amount stated in the prospectus that must be subscribed and the amount payable on application for the amount stated as minimum subscription have been paid to and received by the company by cheque or other instrument.

Things to Remember:

Minimum amount is not subscribed and the amount payable on application is not received within the specified period, then the application money shall have to be refunded within fifteen days from the closure of the issue.

Important Notes:

Prospectus: It is a document in which terms and conditions of the issue are stated along with the purpose of the proceeds of issue.

Q24: Tiny Toys Ltd. issued ₹ 10,00,000 shares of ₹ 100 each at a premium of ₹ 20 for subscription payable as:

₹ 10 per share on application,

₹ 40 per share and ₹ 10 premium on allotment, and

₹ 50 per share and ₹ 10 premium on final payment.

Issue was oversubscribed receiving applications for 13,000 shares. Applicants for 11,000 shares were allotted 10,000 shares and applicants for 2,000 shares were sent letters of regret. All the money due on allotment and final call was duly received. Pass necessary entries in the company’s books to record the above transactions. Also, prepare company’s Balance Sheet on completion of the above transactions.

Answer 24:

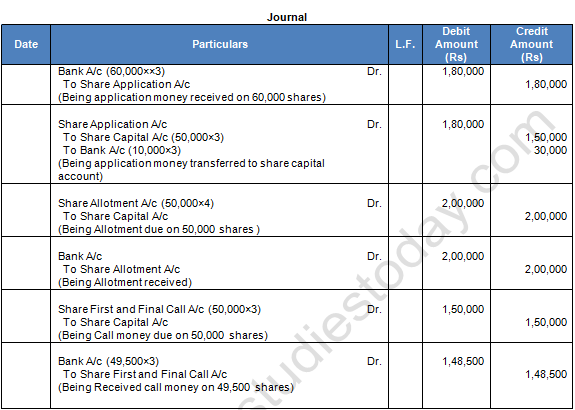

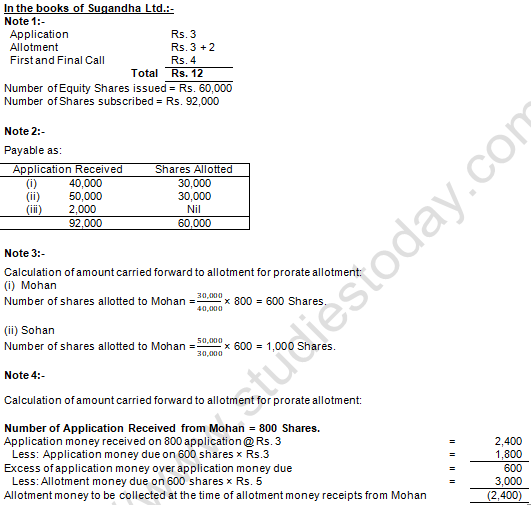

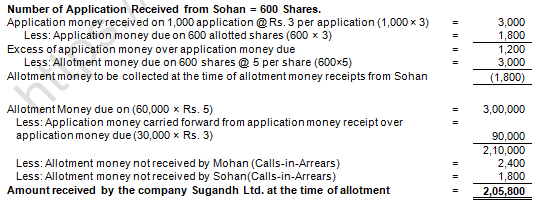

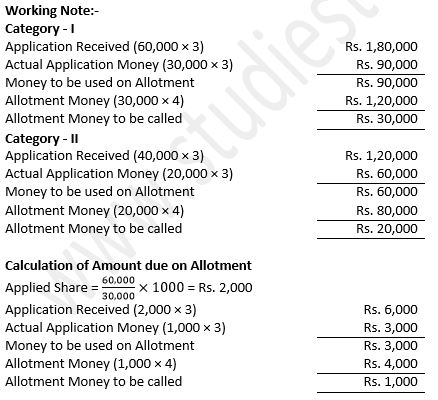

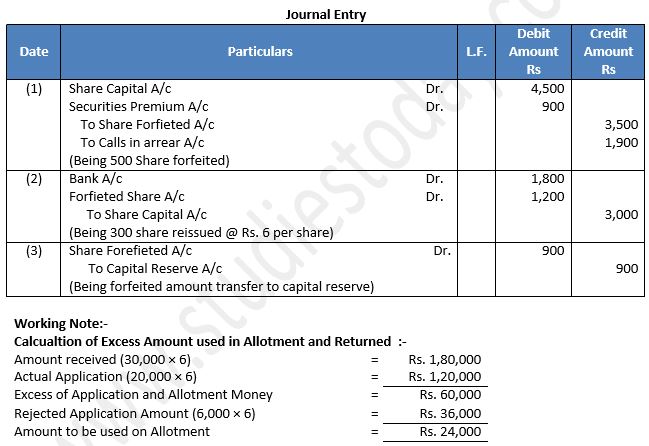

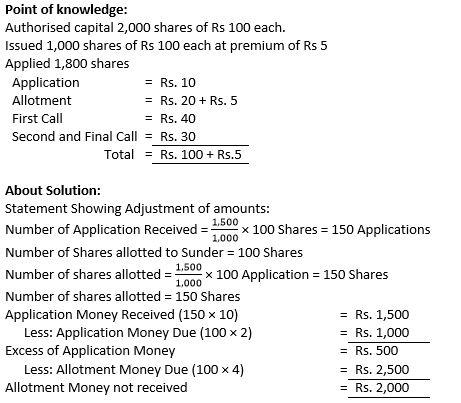

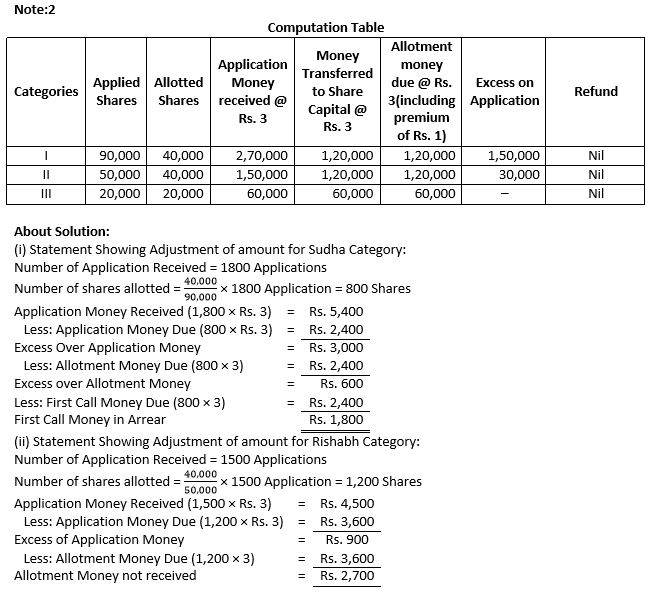

Q25: Sugandh Ltd. issued 60,000 shares of Rs. 10 each at a premium of Rs. 2 per share payable as Rs. 3 on application, Rs. 5 (including premium) on allotment and the balance on first and final call. Applications were received for 92,000 shares. The Directors resolved to allot as:

(i) Applicants of 40,000 shares 30,000 shares,

(ii) Applicants of 50,000 shares 30,000 shares,

(iii) Applicants of 2,000 shares Nil.

Mohan, who had applied for 800 shares in Category

(i) and Sohan, who was allotted 600 shares in Category

(ii) Failed to pay the allotment money. Calculate amount received on allotment.

Answer 25:

About Solution:

In the beginning, the size of business firms was very small. Sole proprietorship was therefore, the usual form of business organisation. Later on partnership become popular when the size of business firms increased. But sole proprietorship and partnership could not meet the growing demand of big size business because of their limitations such as limited capital, limited managerial ability, unlimited liability and other drawbacks. Therefore, in the present days of business world, it is only the Joint stock company form of business organisation which proved to be useful.

Things to Remember:

A company is a voluntary association of persons formed for some common purpose, with capital divisible into parts, known as shares and with a limited liability. It is created by law and is known as an artificial person with a perpetual succession and a common seal. It has a separate legal entity.

Important Notes:

Companies can be classified under the following heads:

1. On the basis of formation

2. On the basis of liability

3. On the basis of ownership

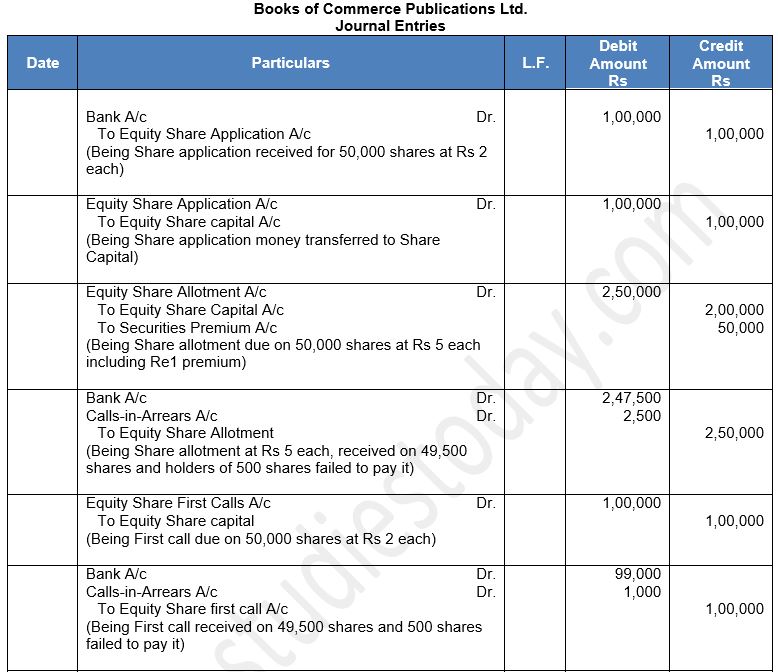

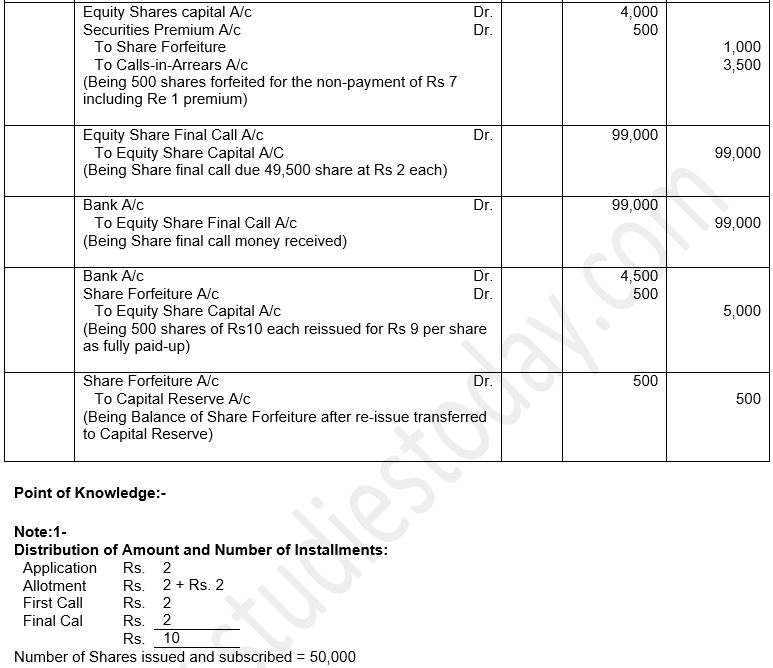

Q26: Sony Media Ltd. issued 50,000 shares of ₹ 10 each payable ₹ 3 on application, ₹ 4 on allotment and balance on first and final call. Applications were received for 1,00,000 shares and allotment was made as follows:

(i) Applicants for 60,000 shares were allotted 30,000 shares.

(ii) Applicants for 40,000 shares were allotted 20,000 shares.

Anupam to whom 1,000 shares were allotted from category (i), failed to pay the allotment money.

Pass Journal entries up to allotment.

Answer 26:

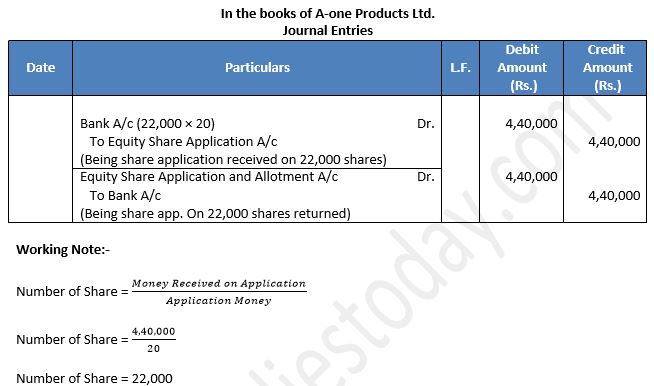

Q27: Quality Stationers Ltd. registered with authorised capital of ₹ 20,00,000 divided into 1,00,000 equity shares of ₹ 20 each. 50,000 Equity Shares were issued for subscription at par, issue price being payable along with application. It received application money of ₹ 4,40,000.

You are requited to pass the necessary Journal entries.

Answer 27:

Things to Remember:

In case of such forfeiture, the company must first give a clear 14days' notice to the defaulting shareholder to pay the amount due on call and interest thereon if any.

Important Notes:

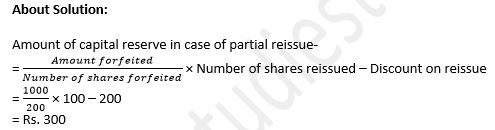

Maximum Permissible Discount: At the time of reissue of the forfeited shares, care has to be taken with respect to the maximum permissible discount on the shares reissued. The maximum permissible discount that can be allowed on reissue of forfeited shares is the amount forfeited, i.e., the amount credited to the forfeited shares. In simple terms, the reissue price cannot be less than the amount unpaid on the forfeited shares.

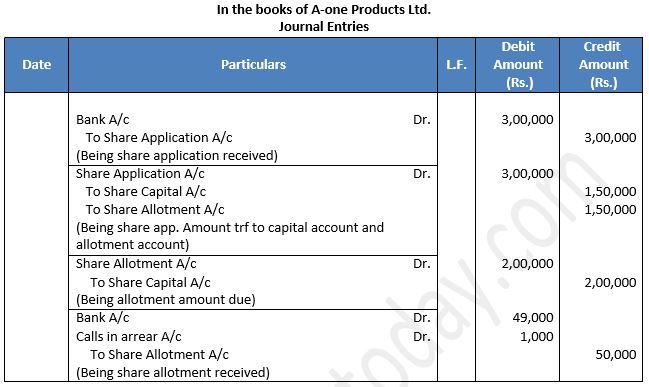

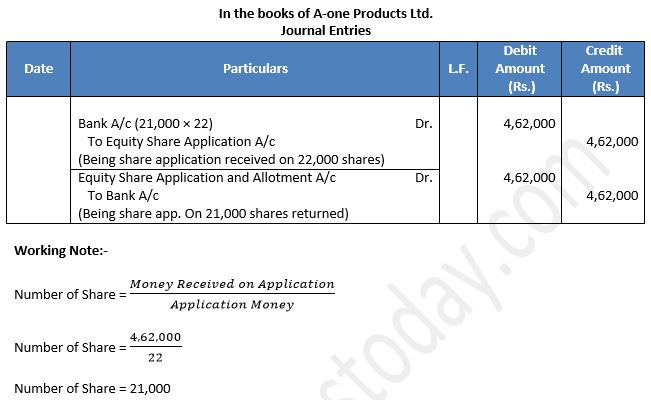

Q28: A-one Product Ltd. is registered with authorised capital of ₹ 10,00,000 divided into 50,000 Equity Shares of ₹ 20 each. It issued 25,000 Equity Shares for Subscription at premium of ₹ 2 per share, issue price being payable along with application. It received ₹ 4,62,000 towards application money.

You are required to pass the necessary Journal entries.

Answer 28:

Things to Remember:

Conditions to issue stock options:

i) Shares issued are of the same class of shares already issued;

ii) Such issue is authorised by a special resolution passed by the company;

iii) Such resolution specifies all possible details of the number of shares, consideration, market price, and class or classed of employees or directors to whom such shares are to be issued;

iv) At the date of issue, not less than 1 year has been elapsed since the date on which the company had commenced business.

Important Notes:

Limited Liability: The members of a company are liable only to the extent of value of shares subscribed by them or amount guaranteed to be paid at the time of winding up in case of companies limited by guarantee. However, the liability of the members is unlimited, in case if the company that is incorporated with unlimited liabilities, liability of members is unlimited.

Q29: Home Products Ltd. is registered with authorised capital of ₹ 10,00,000 divided into 1,00,000 Equity Shares of ₹ 10 each. it issued 70,000 Equity Shares for subscription at premium of ₹ 2 per share, payable ₹ 3 on application, ₹ 5 on allotment and balance on first and final call. It received subscription for 62,500 shares.

You are required to pass the necessary Journal entries.

Answer 29:

Things to Remember:

Limited Liability: The members of a company are liable only to the extent of value of shares subscribed by them or amount guaranteed to be paid at the time of winding up in case of companies limited by guarantee. However, the liability of the members is unlimited, in case if the company that is incorporated with unlimited liabilities, liability of members is unlimited.

Important Notes:

Common Seal: A cannot sign or enter into any contract on its own by signing the documents. Therefore, a common seal is maintained by many companies to affix it on all important documents of the company.

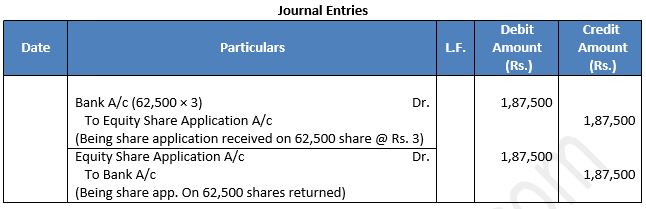

Q30: Pure Products Ltd. is registered with authorised capital of ₹ 10,00,000 divided into 1,00,000 equity shares of ₹ 10 each. It issued 70,000 Equity Shares for subscription of ₹ 2 per share, payable ₹ 3 on application, ₹ 5 on allotment and balance on first and final call. It received application money amounting to ₹ 1,89,000.

You are required to:

(i) Determine whether the company should allot shares; and

(ii) If yes, pass the necessary Journal entries assuming that the company has received due amount on allotment and call.

Answer 30:

(i) Minimum subcription is 70,000 × 90% = 63,000 shares.

Total Application Amount received = Rs. 1,89,000

Number of Share = 1,89,000/3

Number of Share = 63,000

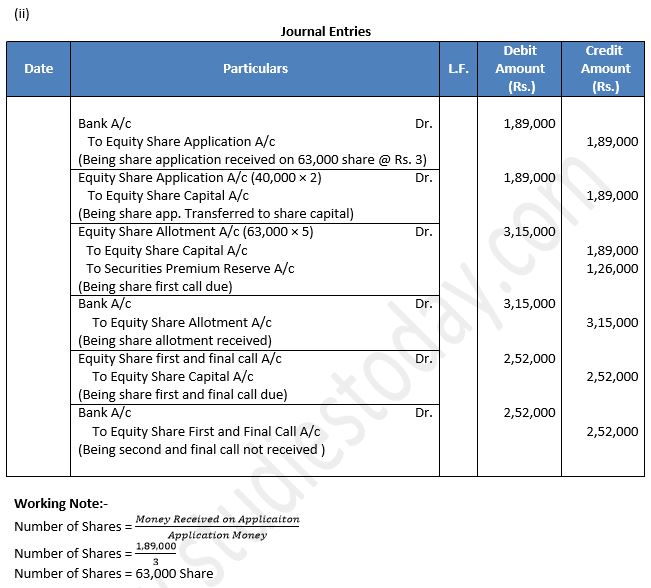

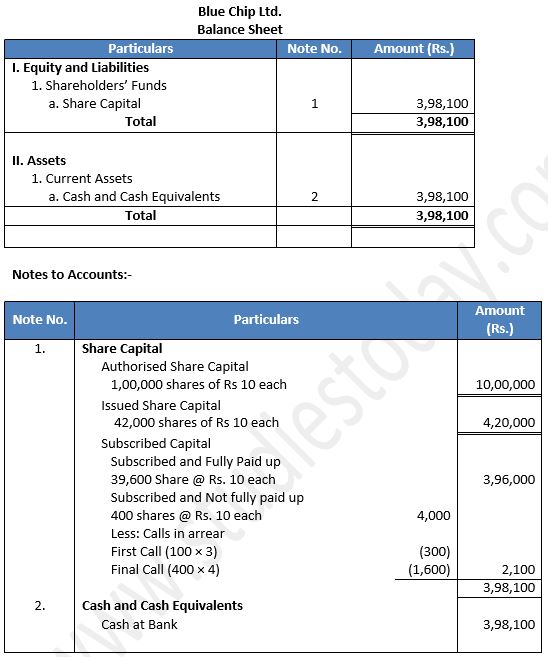

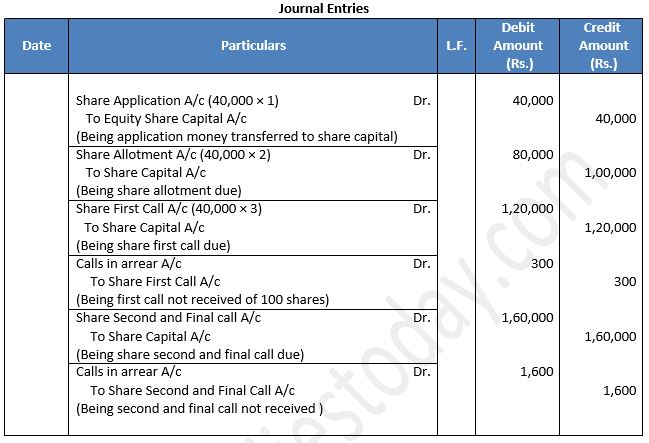

Q31: Blue Chip Ltd. was registered on 1st January, 2023 with a capital of ₹ 10,00,000 divided into 1,00,000 shares of ₹ 10 each. The company issued 42,000 shares of which 40,000 shares were taken up by the public and ₹ 1 per share was received with application. on 1st February, 2023, these shares were allotted and ₹ 2 per share was duly received on 28th February, 2023 as allotment money. First call of ₹ 3 per share was made on 1st March, 2023 and the call money on all shares with the exception of 100 shares was received. The final call of ₹ 4 per share was made on 1st June, 2023 and the amount due, with the exception of 400 shares, was received by 30th June, 2023.

Pass necessary Journal and Cash Book entries and prepare the Balance Sheet as at 30th June, 2024.

Answer 31:

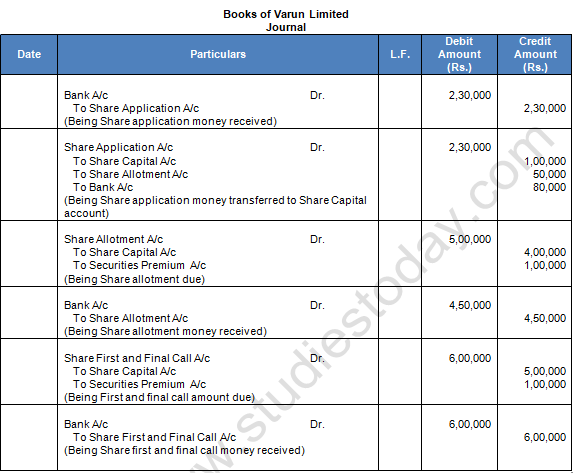

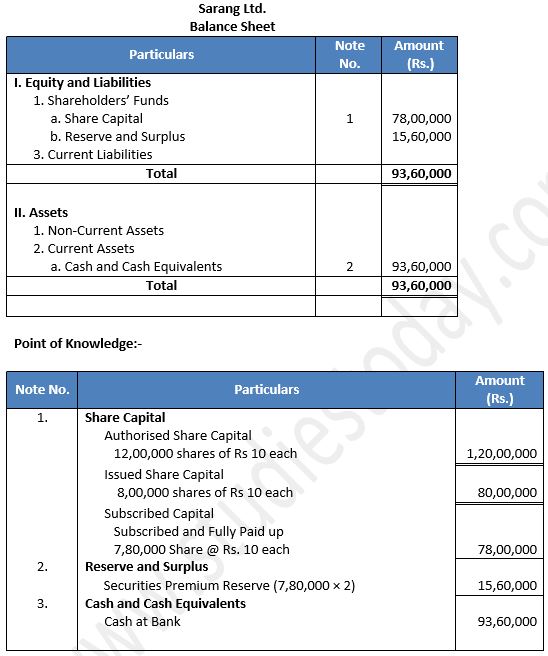

Q32: The authorised capital of Sarang Ltd. is ₹ 1,20,00,000 divided into 12,00,000 shares of ₹ 10 each. Out of these, company issued 8,00,000 shares of ₹ 10 each at a premium of 20%. The amount per share was payable as follows:

Public applied for 7,80,000 shares. All the money was duly received. Prepare an extract of Balance Sheet of Sarang Ltd. as per Schedule III, Part I of the Companies Act, 2013, disclosing the above information. Also prepare ‘Notes to Accounts’ for the same.

Answer 32:

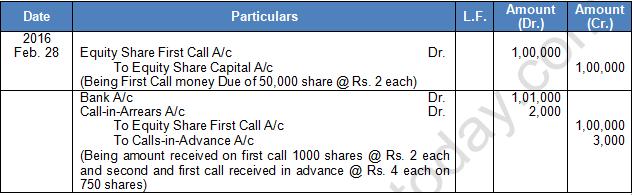

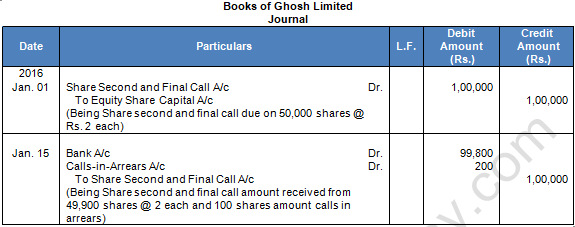

Q33: Ghosh Ltd. made the second and final call on its 50,000 Equity Shares @ Rs. 2 per share on 1st January, 2016. The entire amount was received on 15th January, 2016 except on 100 shares allotted to Venkat. Pass necessary journal entries for the call money due and received by opening Calls-in-Arrears Account.

Answer 33

Things to Remember:

Company Under Section 25: A company created under section-25 is to promote art, culture and societal aims. Such companies need not use the term limited at the end of their name. Punjab, Haryana, Delhi chambers of commerce, etc. are the examples of such companies.

Important Notes:

Unlimited Company: The company not having any limit on the liability of its members, is called an unlimited company. Liability in such a case extends to the personal property of its shareholders. Such companies do not use the word ‘limited’ at the end of their name.

Q34: Avon Ltd. issued for subscription 10,000 shares of ₹ 25 each, payable ₹ 5 per share on application, ₹ 10 per share on allotment (including ₹ 5 per share as premium), ₹ 5 per share as first call on the shares and the balance in two equal amounts at intervals of three months. All the shares were applied for and allotted. Due amount was received except the second call and final call on 200 and 400 shares respectively.

Pass the entries in the company’s Journal, Cash Book and the Ledger. Also show the company’s Balance Sheet on Completion of the above transactions.

Answer 34:

Q35: Usha Ltd. was formed with a capital of ₹ 10,00,000 divided into shres of ₹ 100 each. It offered 90% shares to public for subscription. The amount per share was payable as 40% on application, 20% on allotment and the balance on first and final call. The applicants paid ₹ 3,60,000 on application and ₹ 1,69,000 on allotment.

The call has not yet been made. Calculate:

(a) Authorised Capital, (b) Issued Capital, (c) Subscribed Capital, (d) Called Up Capital, (e) Paid-up Capital, and (f) Calls-in-arrears.

Answer 35:

Authorised Capital = Rs. 10,00,000 (10,000 share @ Rs. 100 each)

Issued Capital = Rs. 10,00,000 × 90%

Issued Capital = Rs. 9,00,000

Subscribed Capital = Rs. 9,00,000

Called up Capital = 9,000 Shares @ Rs. 60 per share

Called up Capital = Rs. 5,40,000

Paid up Capital = Rs. 3,60,000 + Rs. 1,69,000

Paid up Capital = Rs. 5,29,000

Calls in arrear:-

Allotment Amount (900 × 20) = Rs. 1,80,000

Amount Received on Allotment = Rs. 1,69,000

= Rs. 11,000

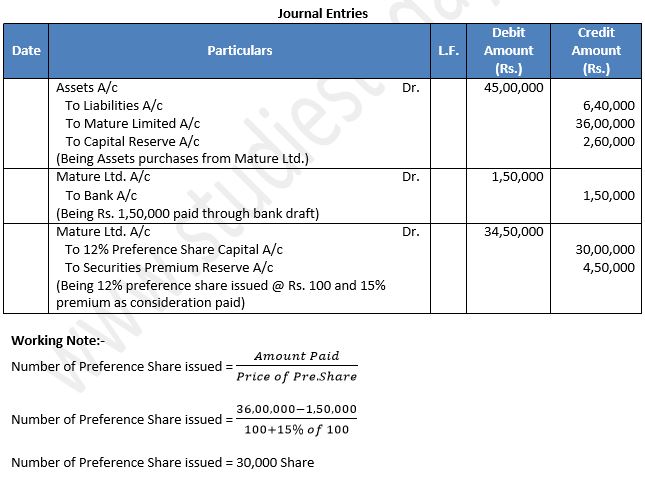

Q36: Random Ltd. took over running business of Mature Ltd. comprising of Assets of ₹ 45,00,000 and Liabilities of ₹ 6,40,000 for a purchase consideration of ₹ 36,00,000. The amount was settled by bank draft of ₹ 1,50,000 and balance by issuing 12% Preference Shares of ₹ 100 each at 15% premium. Pass entries in the books of Random Ltd.

Answer 36:

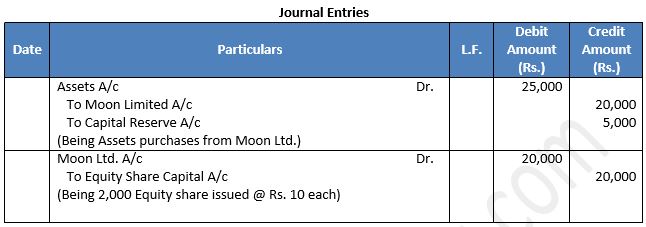

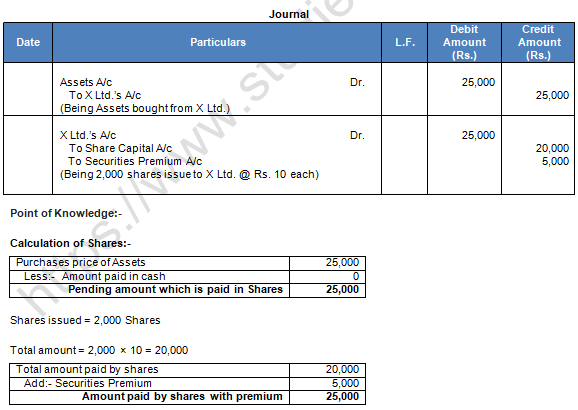

Q37: 2,000 Equity Shares of ₹ 10 each were issued to Moon Limited from whom assets of ₹ 25,000 were acquired Pass Journal entry.

Answer 37:

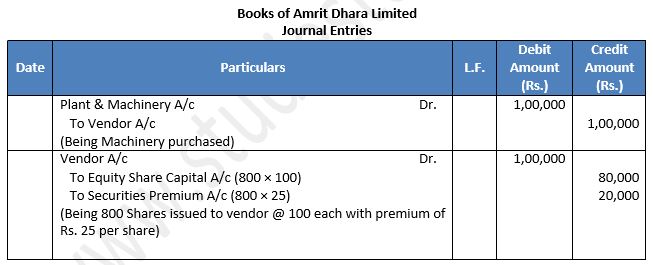

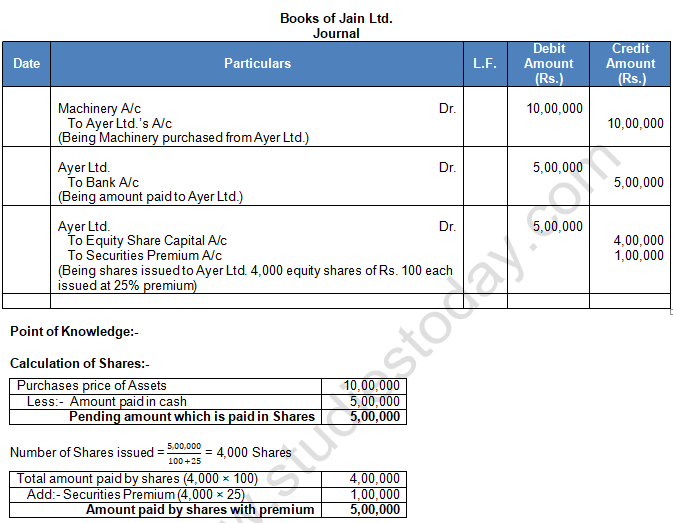

Q38: 'Amrit Dhara Ltd.' issued 800 Equity Shares of Rs. 100 each at a premium of 25% as fully paid-up in consideration of the purchase of plant and machinery of Rs. 1,00,000.

Pass entries in company's Journal.

Answer 38:

About Solution:

Calculation of Shares:-

Pending amount which is paid in Shares = Rs. 1,00,000

Number of Shares issued = 1,00,000/(100+25) = 800 Shares

Things to Remember:

A joint stock company divides its capital into units of equal denomination. Each unit is called a share. These units i.e. shares are offered for sale to raise capital. This is termed as issuing shares. A person who buys share/shares of the company is called a shareholder and by acquiring share or shares in the company he/she becomes one of the members of the company.

Important Notes:

A share is an indivisible unit of capital. It expresses the proprietory relationship between the company and the shareholder. The denominated value of a share is its face value. The total capital of a company is divided into number of shares.

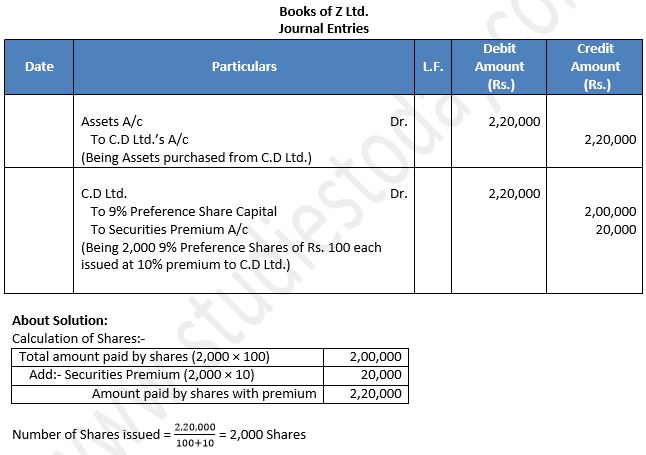

Q39: Z Ltd. purchased furniture costing Rs. 2,20,000 from C.D Ltd. The payment was to be made by issue of 9% Preference Shares of Rs. 100 each at premium of Rs. 10 per share. Pass necessary Journal entries in the books of Z Ltd.

Answer 39:

Things to Remember:

Characteristics of Preference Shares

1. Such type of shareholders has priority in the payment of dividend before any other class of shareholders gets their payment of dividend.

2. The rate of dividend of such shares is pre-determined.

Important Notes:

Equity Shares which are not preference shares are equity shares. Holders of these shares receive dividend out of the profits of the company after the payment of dividend has been made to the preference shareholders.

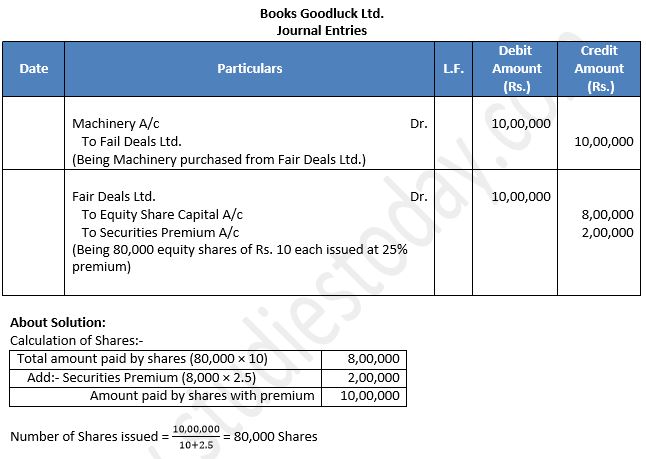

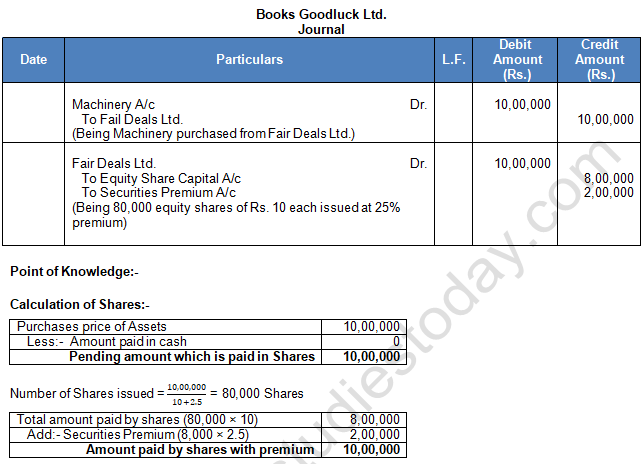

Q40: Goodluck Ltd purchased machinery costing Rs. 10,00,000 from Fair Deals Ltd. The company paid the price by issue of Equity Shares of Rs. 10 each at a premium of 25%. Pass necessary Journal entries for the above transactions in the books of Goodluck Ltd.

Answer 40:

Things to Remember:

Characteristics of Equity Shares

i. Its dividend rate can change from year to year.

ii. Dividend on Equity shares is paid after the payment of dividend to preference shareholders.

iii. In the event of winding up of company the repayment of capital to equity shareholder is made at last. iv. They are real owners of the company. Equity shareholders have the right to elect directors of the company. Equity shares are the permanent source of capital.

Important Notes:

A joint stock company estimates its future capital requirements. The amount of the capital is mentioned in the capital clause of the Memorandum of Association registered with the Registrar of the Companies. Total capital is divided into a number of small indivisible units of fixed amount and each such unit is called a share. A share is nothing but a part in the share capital of the company. As the total capital of the company is divided into shares, the capital of the company is called share capital.

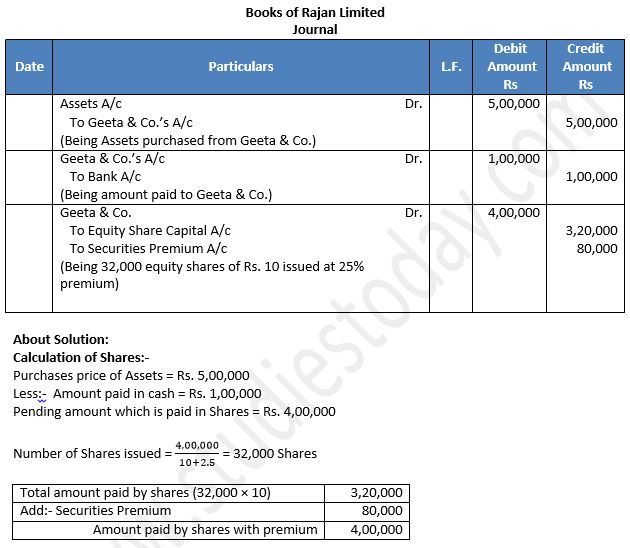

Q41: Rajan Ltd. purchased assets from Geeta & Co. for Rs. 5,00,000. A sum of Rs. 1,00,000 was paid by means of a bank draft and for the balance due Rajan Ltd. issued equity Shares of Rs. 10 each at a premium of 25%. Journalize the above transactions in the books of the company.

Answer 41:

Things to Remember:

According to the Companies Act, a company can issue the following types of Shares:

(i) Preference Shares

(ii) Equity Shares

Important Notes:

Preference Shares: A preference share is one which carries following preferential rights over other type of shares called equity shares in regard to the following:

1. Payment of dividend

2. Repayment of capital at the time of winding up of the company.

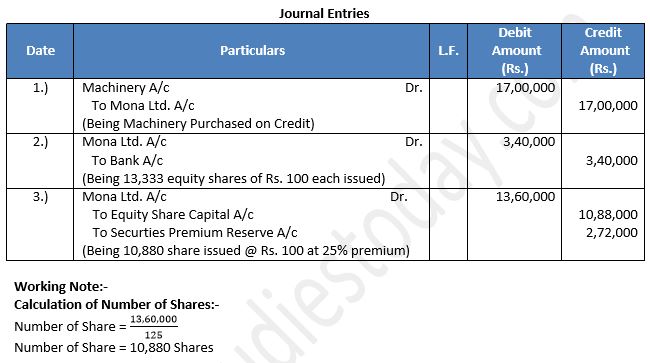

Q42: Sona Ltd purchased machinery costing ₹ 17,00,000 from Mona Ltd. Sona Ltd. paid 20% of the amount by cheque and for the balance amount issued Equity Shares of ₹ 100 each at a premium of 25%.

Pass necessary Journal entries for the above transactions in the books of Sonal Ltd. Show your working notes clearly.

Answer 42:

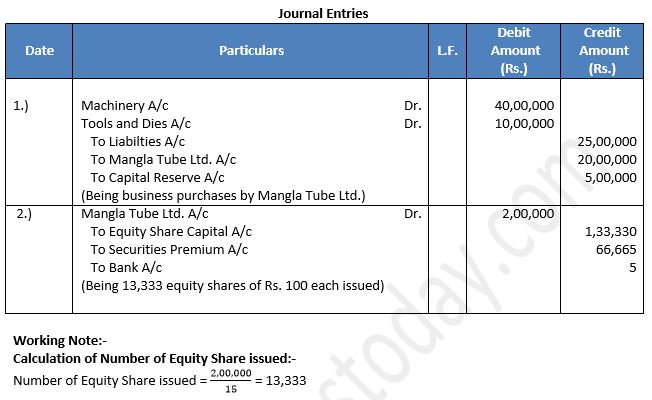

Q43: Mangla Cortubi Ltd. took over a unit of Mangla Tubes Ltd. consisting of Machinery – ₹ 4,00,000, Tools and Dies – ₹ 10,00,000 and Liabilities of ₹ 25,00,000 for a consideration of ₹ 20,00,000. The consideration was paid by issuing Equity Shares of ₹ 10 each at a premium of ₹ 5.

You are required to pass the journal entries in the books of Mangla Cortubi Ltd.

Answer 43:

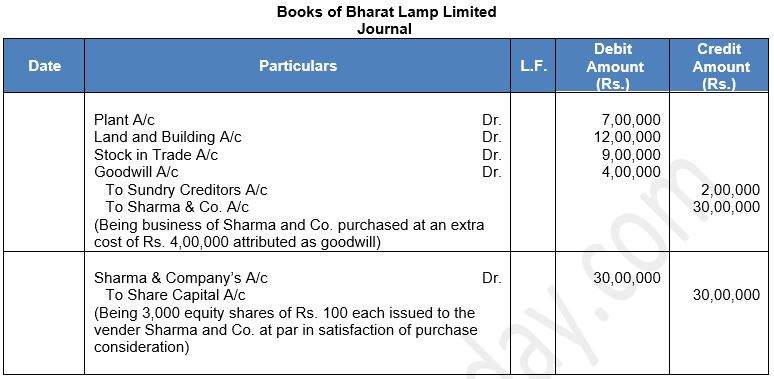

Q44: Bhushan Lamp Ltd. issued 30,000 fully paid-up shares of Rs. 100 each for purchase of the following assets and liabilities from Sharma & Co:

Plant Rs. 7,00,000 Stock-in-Trade Rs. 9,00,000

Land and Building Rs. 12,00,000 Sundry Creditors Rs. 2,00,000

You are required to pass necessary Journal entries.

Answer 44:

Things to Remember:

Paid up Capital is the portion of called up capital which has been paid by the shareholders, to calculate the paid up capital, the amount of instalments in arrears is deducted from the called up capital.

Important Notes:

Reserve Capital: Company may keep some part of its share capital uncalled and keep in reserve to be called only in case of need at the time of its winding up. This is known as Reserve capital. For this, a special resolution will have to be passed by the company. Thus, it is that portion of the uncalled capital which a company has decided to call only in case of liquidation of the company.

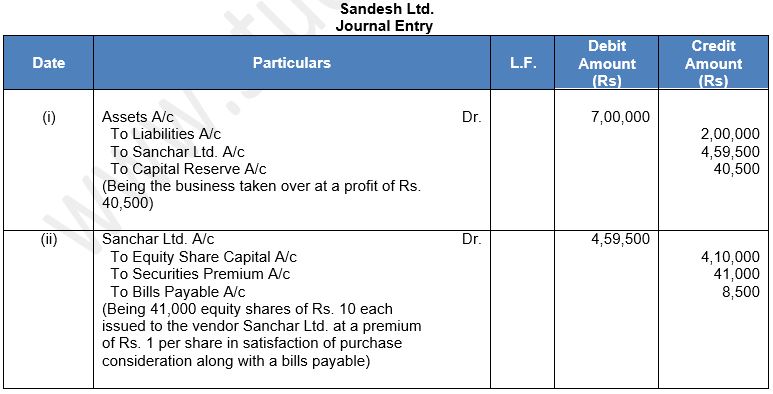

Q45: Sandesh Ltd. took over the assets of Rs. 7,00,000 and liabilities of Rs. 2,00,000 from Sanchar Ltd. for a purchase consideration of Rs. 4,59,500. Rs. 8,500 were paid by accepting a draft in favour of Sanchar Ltd. payable after three months and the balance was paid by issue of equity shares of Rs. 10 each at a premium of 10% in favour of Sanchar Ltd.

Pass necessary journal entries for the above transactions in the books of Sandesh Ltd.

Answer 45:

About Solution:

Number of Equity Shares to be issued Sandesh Ltd. = Rs.4,51,000/10+1

Number of Equity Shares = 41,000 Equity Shares

Things to Remember:

The company purchases certain assets from vendors (sellers or suppliers) on credit. Instead of making payment to vendors in cash, the company issues them certain agreed number of shares at the agreed rate as a consideration (payment in exchange) of assets purchased. Shares may be issued to vendors at par, at premium or at discount.

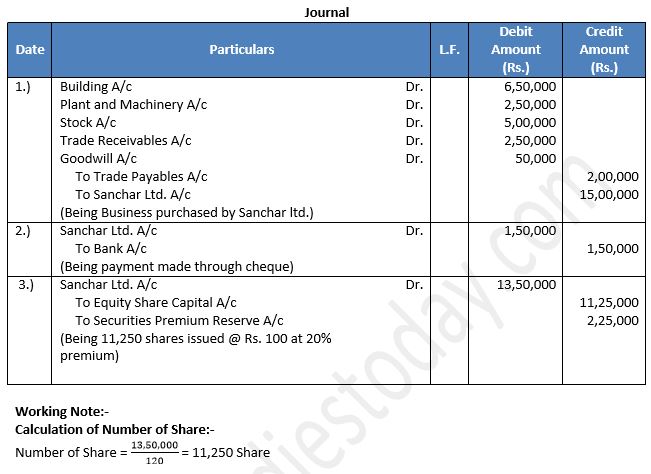

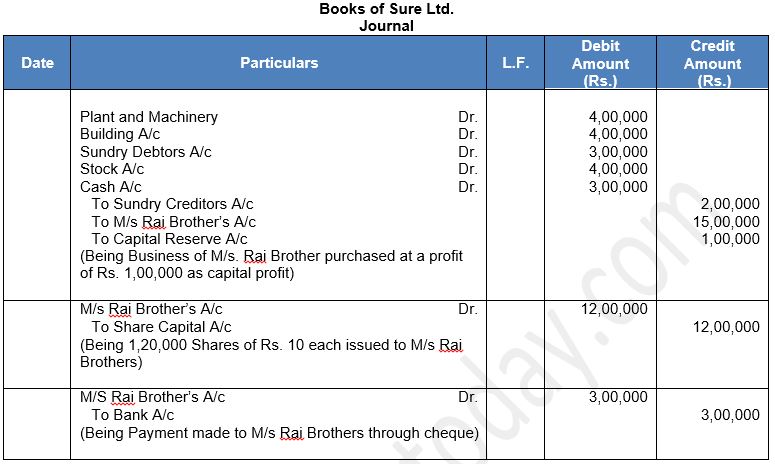

Important Notes:

Promoters are those persons, firms or companies, who promote the company. They are entrusted with the work of the formation of the company. Promoters are paid remuneration for their services. This remuneration can be paid in the form of shares also. In such cases companies issue shares to their promoters without payment

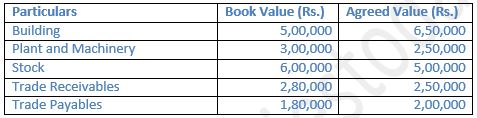

Q46: Sandesh Ltd. purchased a running business from Sanchar Ltd for ₹ 15,00,000 payable 10% by cheque and the balance by the issue of fully paid Equity Shares of ₹ 100 each at a premium of 20%. The assets and liabilities consisted of the following:

Pass the necessary Journal Entries in the books of Sandesh Ltd.

Answer 46:

Things to Remember:

Limited Liability: The members of a company are liable only to the extent of value of shares subscribed by them or amount guaranteed to be paid at the time of winding up in case of companies limited by guarantee. However, the liability of the members is unlimited, in case if the company that is incorporated with unlimited liabilities, liability of members is unlimited.

Important Notes:

Common Seal: A cannot sign or enter into any contract on its own by signing the documents. Therefore, a common seal is maintained by many companies to affix it on all important documents of the company.

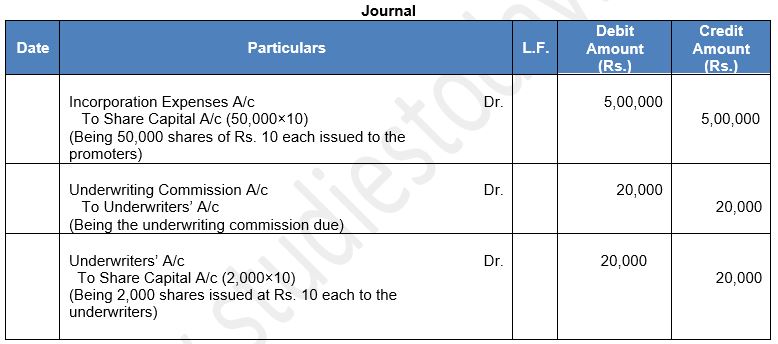

Q47: Light Lamps Ltd. issued 50,000 shares of Rs. 10 each as fully paid-up to the promoters for their services to set-up the company. It also issued 2,000 shares of Rs. 10 each credited as fully paid-up to the underwriters of shares for their services. Journalize these transactions.

Answer 47:

Things to Remember:

Uncalled Capital: Uncalled Capital is that portion of the issued/subscribed capital that is not called up by the company on the shares allotted.

Important Notes:

Paid up Capital is the portion of called up capital which has been paid by the shareholders, to calculate the paid up capital, the amount of instalments in arrears is deducted from the called up capital.

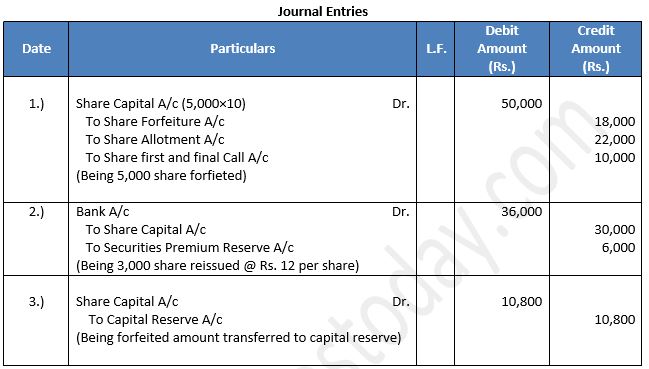

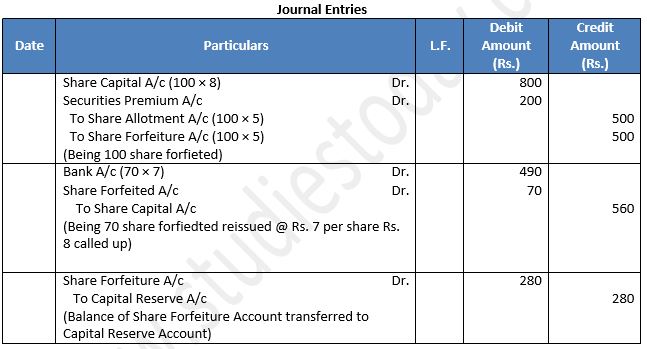

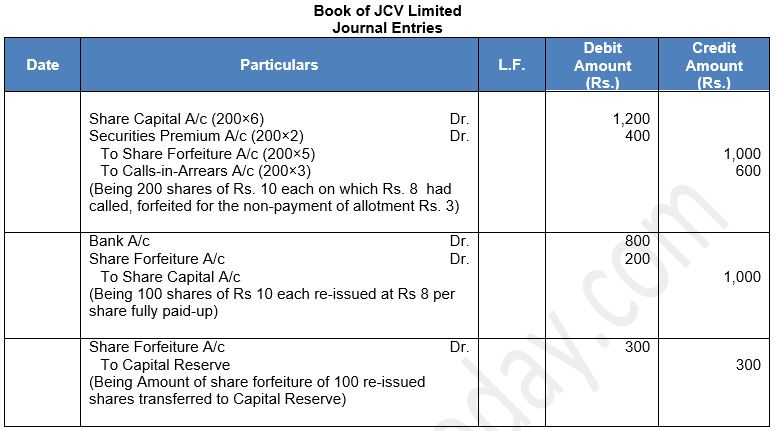

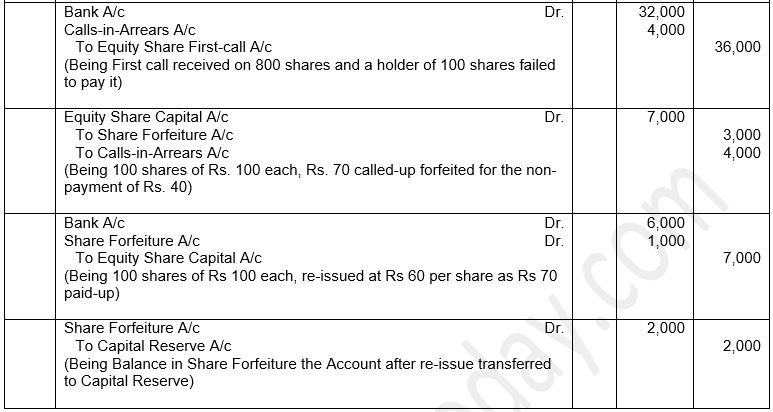

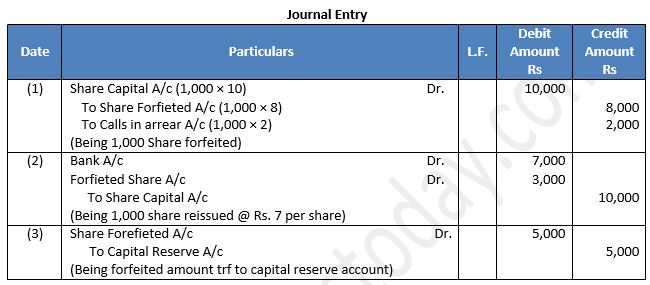

Q48: Vikram Ltd. forfeited 5,000 shares of Rahul, who had applied for 6,000 shares for non-payment of allotment money of ₹ 5 per share and first and final call of ₹ 2 per share. Only application money of ₹ 3 was paid by him. Out of these, 3,000 shares were re-issued @ ₹ 12 per share as fully paid.

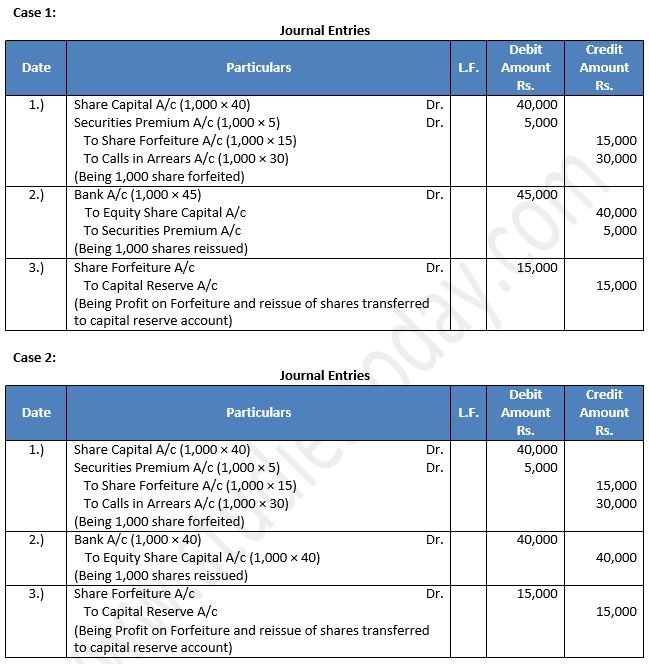

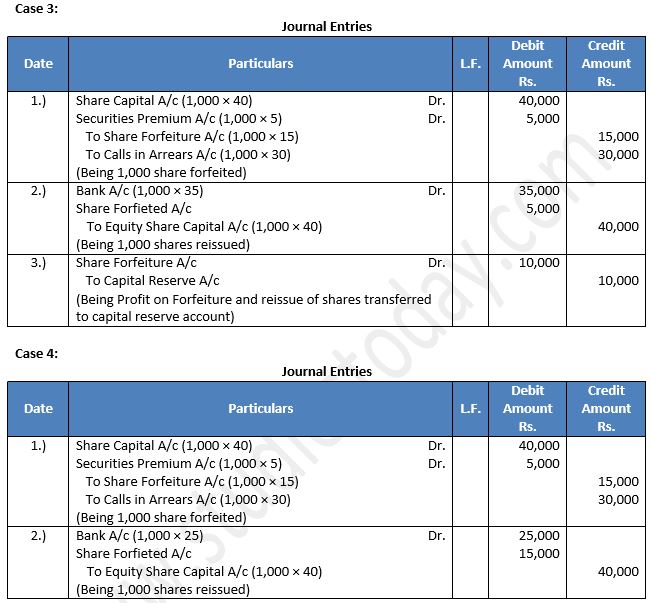

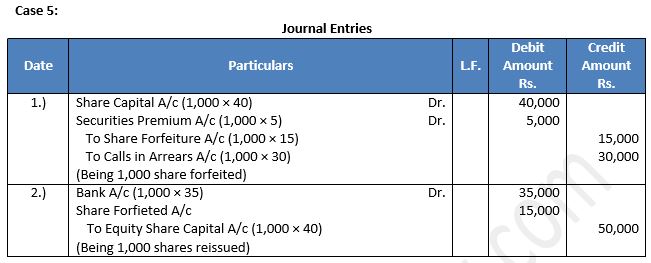

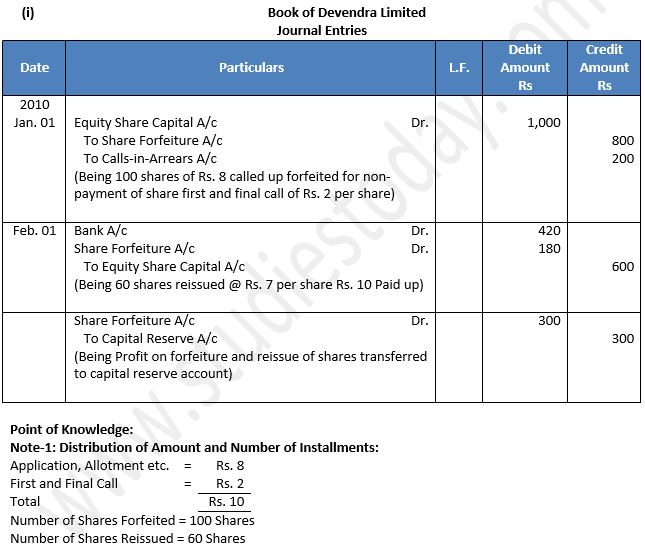

Pass entries for forfeiture and reissue of shares.

Answer 48:

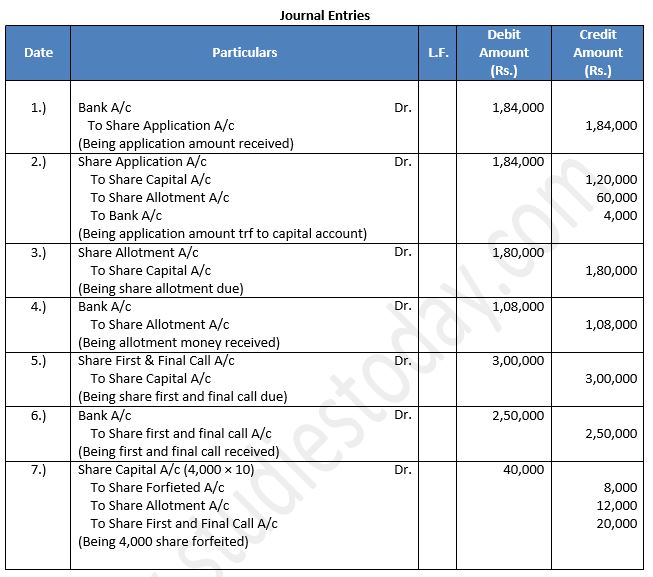

Q49: Sangita Limited invited applications for issuing 60,000 shares of ₹ 10 each at par. The amount was payable as follows: on application ₹ 2 per share; on allotment ₹ 3 per share; on first and final call ₹ 5 per share. Applications were received for 92,000 shares.

Allotment was made on the following basis: (a) to applicants for 40,000 shares; full, (b) to applicants for 50,000 shares: 40%; (c) to applicants for 2,000 shares; nil. ₹ 1,08,000 was realised on account of allotment (excluding the amount carried from application money) and ₹ 2,50,000 on account of call. The directors decided to forfeit shares of those applicants to whom full allotment was made and on which allotment money was overdue.

Pass Journal entries in the books of Sangita Limited to record the above transactions.

Answer 49:

Things to Remember:

In case of such forfeiture, the company must first give a clear 14days' notice to the defaulting shareholder to pay the amount due on call and interest thereon if any.

Important Notes:

Maximum Permissible Discount: At the time of reissue of the forfeited shares, care has to be taken with respect to the maximum permissible discount on the shares reissued. The maximum permissible discount that can be allowed on reissue of forfeited shares is the amount forfeited, i.e., the amount credited to the forfeited shares. In simple terms, the reissue price cannot be less than the amount unpaid on the forfeited shares.

Q50: Alpha Ltd. issued 20,000 Equity Shares of Rs. 10 each at par payable: On application Rs. 2 per share; on allotment Rs. 3 per share; on first call Rs. 3 per share; on second and final call Rs. 2 per share. Mr. Gupta was allotted 100 shares. Pass necessary Journal entry relating to the forfeiture of shares in each of the following alternative cases:

Case I If Mr. Gupta failed to pay the allotment money and his shares were immediately forfeited.

Case II If Mr. Gupta failed to pay allotment money and on his subsequent failure to pay the first call, his shares were forfeited.

Case III If Mr. Gupta failed to pay the first call and on his subsequent failure to pay the second and final call, his shares were forfeited.

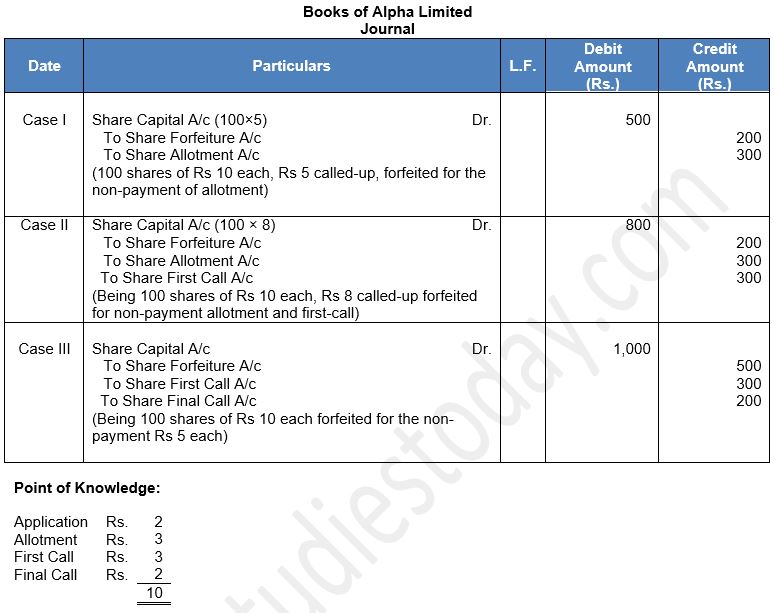

Answer 50:

Things to Remember:

Minimum Subscription: As per SEBI Guidelines, minimum subscription is to receive subscription for at least 90% of the shares issued. If the company does not receive minimum subscription, it cannot allot the shares and therefore, it will have to refund the application money to the subscribers.

Important Notes:

Calls-in-Arrears: If the shareholder does not pay the call amount due on allotment or on any subsequent calls according to the terms, the amount not received is called Calls-inArrears.Interest on Calls-in-Arrears: If the company is authorized by the Articles of Association, it may charge an interest at the specified rate on Calls-in-Arrears from the due date to the date of payment. In case Articles of Association is silent, Table F of the Companies Act, 2013 shall apply which provides for interest on Calls-in-Arrears at the rate of 10% p.a. However, directors have the right to waive such interest.

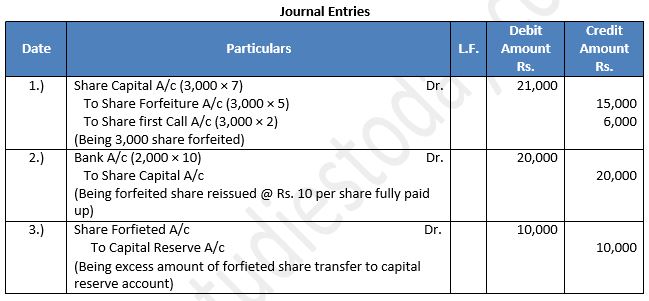

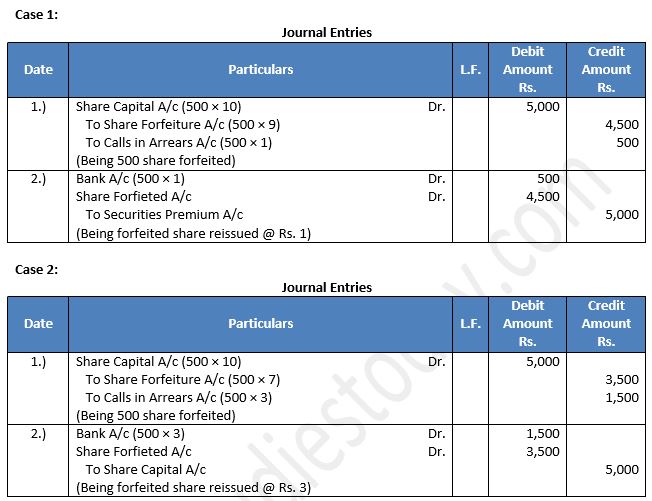

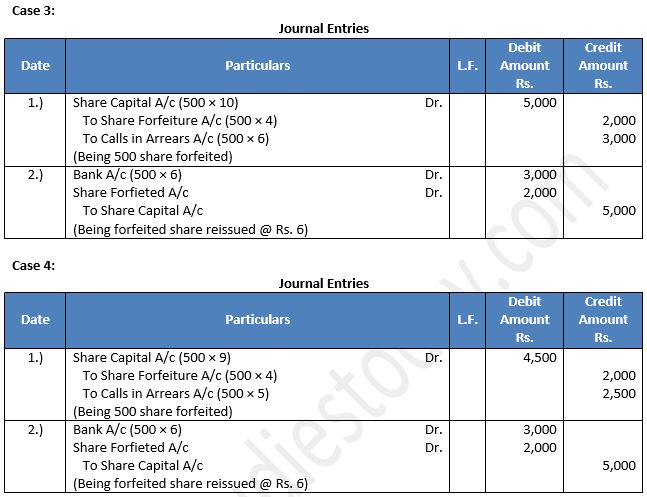

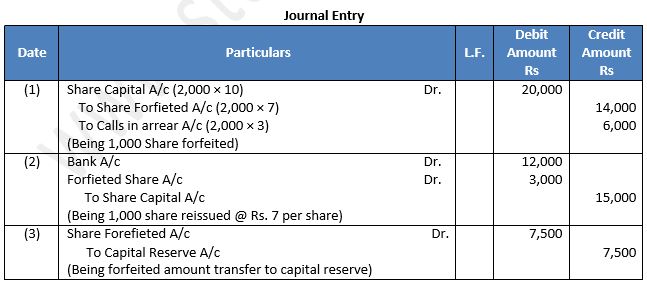

Q51: Ratan Ltd forfeited 3,000 shares of ₹ 10 each (issued at ₹ 2 premium) for non-payament of first call of ₹ 2 per share. Final call of ₹ 3 per share was not yet made. Out of thse, 2,000 shares were re-issued at ₹ 10 per share as fully paid. Pass entries for forfeiture and reissue of shares.

Answer 51:

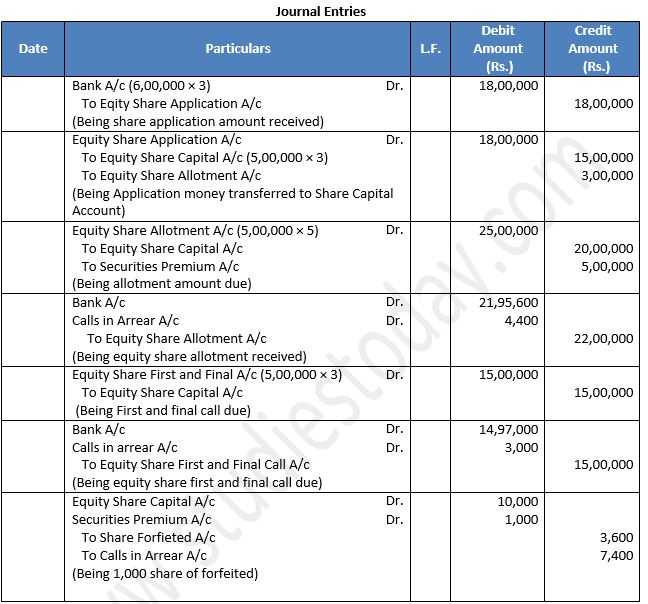

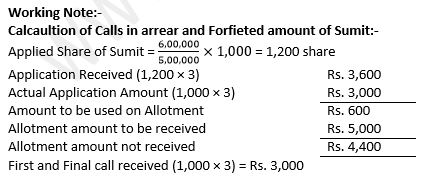

Q51: Ajanta Ltd. issued a prospectus inviting applications for issuing 5,00,000 equity shares of ₹ 10 each issued at a premium of 10%. The amount was payable as follows:

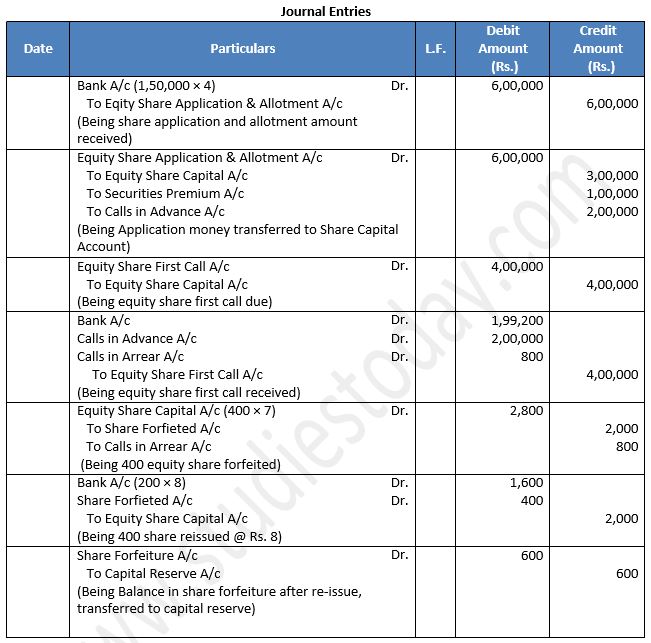

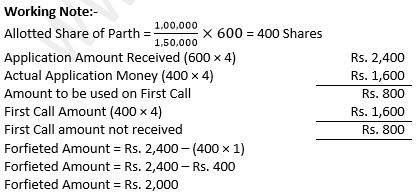

Applications were received for 6,00,000 shares and pro rata allotment was made to all applicants. Excess money received on application was adjusted towards sums due on allotment. All amounts were duly received except from Sumit, who was the holder of 1,000 shares, and failed to pay the allotment and first and final call. His shares were forfeited.

Pass Journal entries for the above transactions in the books of Ajanta Ltd. Open Calls-in-Arrears Account wherever necessary.

Answer 51:

Question 52: Ankit Ltd. issued 20,000 equity shares of 10 each at a premium of Rs. 2 per share, payable as:

On Application : Rs. 3

On Allotment : Rs. 5 (including premium)

On First Call : Rs. 2

On Second and Final Call : Rs. 2

Vijay was allotted 500 shares. Pass the necessary Journal entries relating to the forfeiture of shares in following cases.

Case I Vijay did not pay allotment money and his shares were immediately forfeited.

Case II Vijay did not pay allotment and first call, his shares were forfeited after first call.

Case III Vijay failed to pay first call and his shares were forfeited immediately.

Case IV Vijay failed to pay both the calls and his shares were forfeited.

Answer 52:

About Solution:

Section 43 of the Companies Act, 2013 prescribes that Shares Capital of a company broadly can be of two types or classes-

1.) Preference Share

2.) Equity Shares

Things to Remember:

Accounting treatment without opening Calls-in-Arrears Account: In this method, amount S received from the shareholders is credited to the relevant call account. The respective call accounts (first, second, etc.) will continue showing debit balance equal to the total amount unpaid on those calls. On a subsequent date, when the amount of Calls-in- Arrears is received, Bank Account is debited and relevant call account is credited.

Important Notes:

Call Money Due:

Share First Call A/c . .Dr. [with actual amount due on say, 100 shares @ 3 each]

To ShareCapital A/c

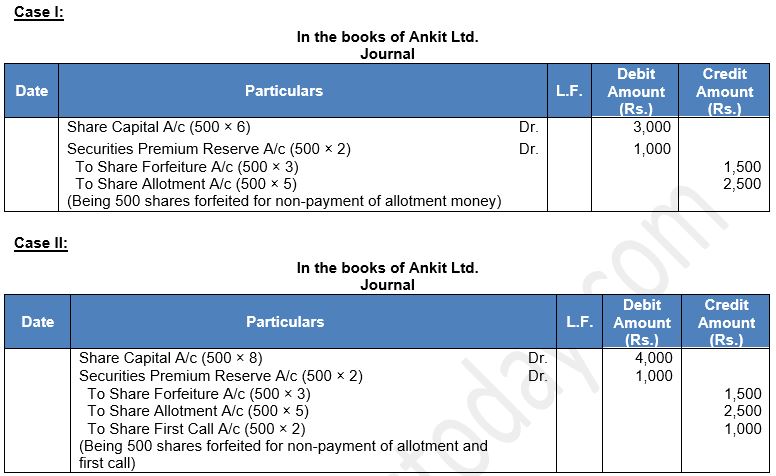

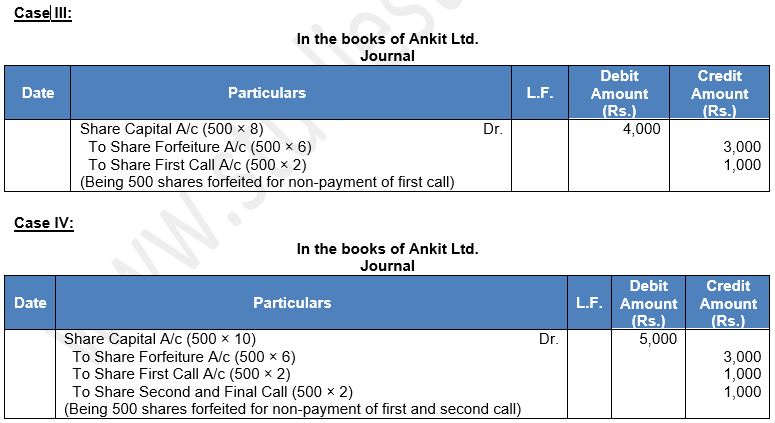

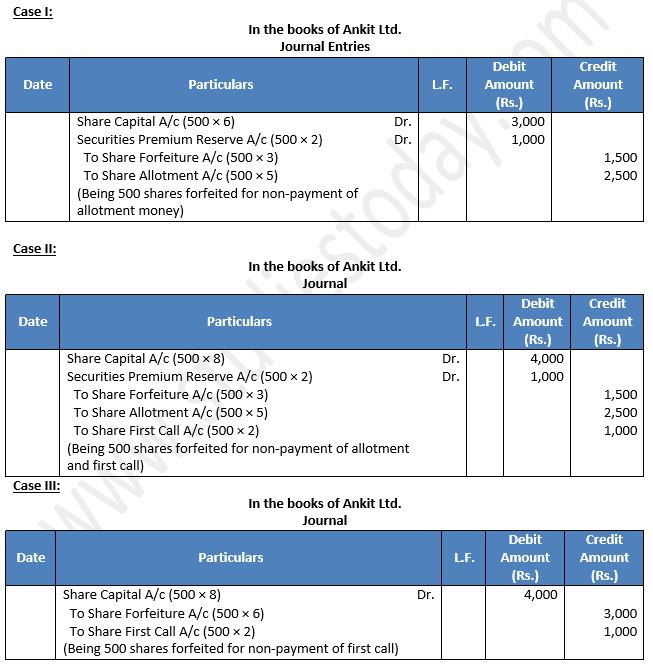

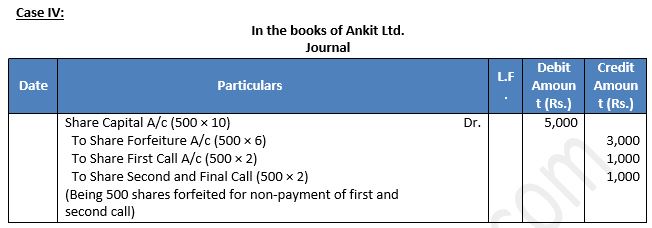

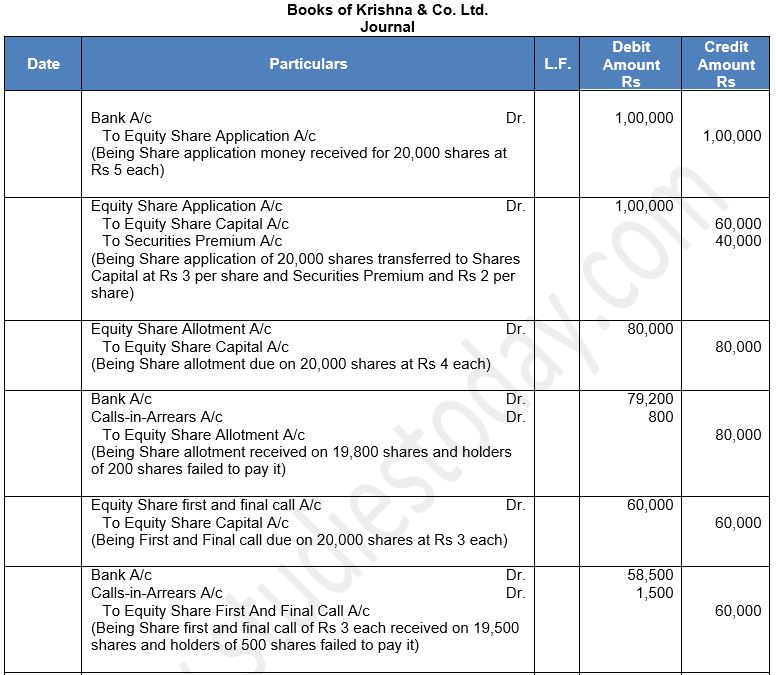

Q53: Ankit Ltd. issued 20,000 equity shares of 10 each at a premium of Rs. 2 per share, payable as:

On Application : Rs. 3

On Allotment : Rs. 5 (including premium)

On First Call : Rs. 2

On Second and Final Call : Rs. 2

Vijay was allotted 500 shares. Pass the necessary Journal entries relating to the forfeiture of shares in following cases.

Case I Vijay did not pay allotment money and his shares were immediately forfeited.

Case II Vijay did not pay allotment and first call, his shares were forfeited after first call.

Case III Vijay failed to pay first call and his shares were forfeited immediately.

Case IV Vijay failed to pay both the calls and his shares were forfeited.

Answer 53:

About Solution:

Section 43 of the Companies Act, 2013 prescribes that Shares Capital of a company broadly can be of two types or classes-

1) Preference Share

2) Equity Shares

Things to Remember:

Accounting treatment without opening Calls-in-Arrears Account: In this method, amount S received from the shareholders is credited to the relevant call account. The respective call accounts (first, second, etc.) will continue showing debit balance equal to the total amount unpaid on those calls. On a subsequent date, when the amount of Calls-in- Arrears is received, Bank Account is debited and relevant call account is credited.

Important Notes:

Call Money Due:

Share First Call A/c . .Dr. [with actual amount due on say, 100 shares @ 3 each]

To ShareCapital A/c

Q54: Vani Limited invited applications for issuing 1,00,000 equity shares of ₹ 10 each at a premium of 10%. The amounts were payable as under: