Access free TS Grewal Solution Class 12 Chapter 8 Dissolution of a Partnership Firm 2026 below. Students can now access free TS Grewal Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 8 Dissolution of a Partnership Firm TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 8 Dissolution of a Partnership Firm Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 8 Dissolution of a Partnership Firm TS Grewal Class 12 Solved Exercises

About this chapter: TS Grewal Class 12 Chapter 8 Dissolution of a Partnership Firm explains the accounting concepts relating to selling of assets, paying off liabilities, distribution of remaining amount among the partners in their profit sharing ratio, payment to creditors and finally closing the books. Students will also understand that the dissolution can take place in different ways, such as by mutual consent, by insolvency, by court order, and by the expiration of a partnership. You will be able to understand all concepts relating to accounting treatment of these different types of dissolution of a partnership firm.

You will be able to learn the accounting entries to be posted in the books of accounts while going through the process of dissolution of partnership firm. As there are lot of numerical problems also given in the chapter. The students will be able to solve the questions and practice for the Class 12 Board Exams. We have also provided detailed step by step solutions for all questions given in the chapter which will help you in upcoming exams

Solutions for TS Grewal's Double Entry Book Keeping:

Accounting for Not for Profit Organizations and Partnership Firms (Vol.1)

Textbook for CBSE Class 12

TS Grewal Solutions Class 12 Accountancy

Chapter 8

Dissolution of a Partnership Firm

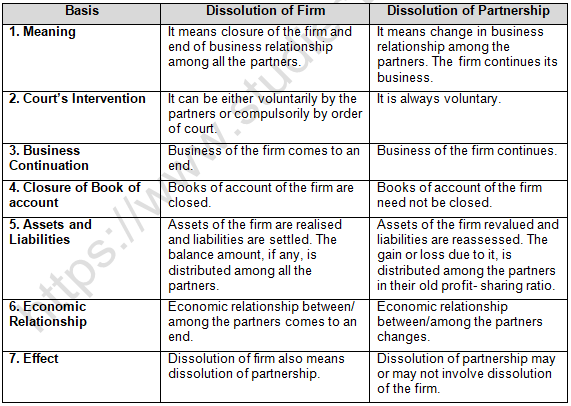

Question 3. Distinguish between Dissolution of Partnership and Dissolution of Partnership Firm on the basis of closure of books.

Question 4. Distinguish between 'Dissolution of Partnership' and 'Dissolution of Partnership Firm' on the basis of Court’s intervention.

Question 5. Distinguish between 'Dissolution of Partnership' and 'Dissolution of Partnership Firm' on the basis of Economic Relationship’.

Question 6. Differentiate between 'Dissolution of Partnership and Dissolution of the Partnership Firm' on the basis of 'Continuity of Business’.

Question 7. Distinguish between 'Dissolution of Partnership' and 'Dissolution of Partnership Firm' on the basis of settlement of assets and liabilities.

Question 8. Give any one difference between reconstitution of a firm and dissolution of a firm.

Question 10. All the partners want to dissolve the firm. Y, a partner, demands that his loan of 2,00,000 be paid before payment of capitals of the partners. But X, another partner, demands that capitals be paid before payment of Y’s loan. Who is correct?

X is correct. According to Section 48 of the Indian Partnership Act, 1932, outside party’s debts are paid before payment of partner’s loan.

Question 11. A and B are partners in a firm sharing profits in the ratio of 3:2. Mrs. A has given a loan of 20,000 to the firm and the firm also obtained a loan of 10,000 from B. The firm was dissolved and its assets were red J. State the order of payment of Mrs. A's loan and B's loan with reason, if there were no creditors of the firm.

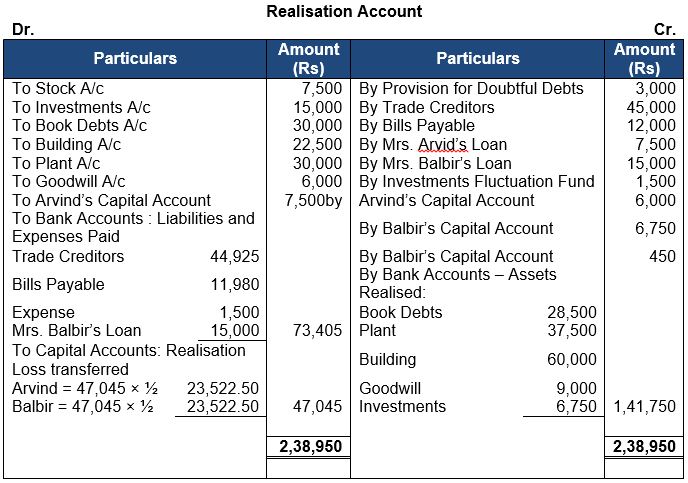

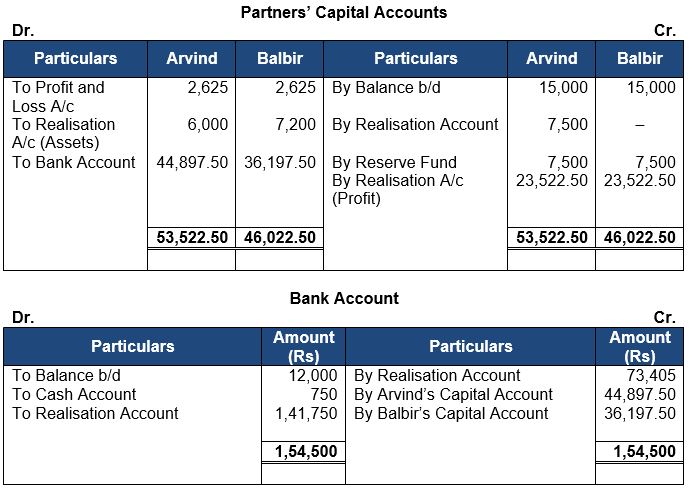

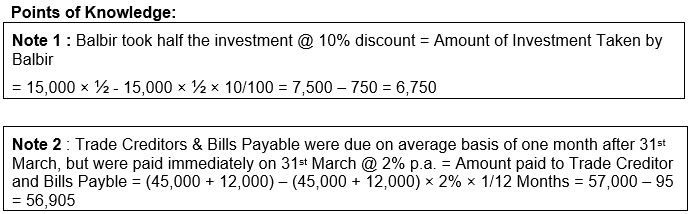

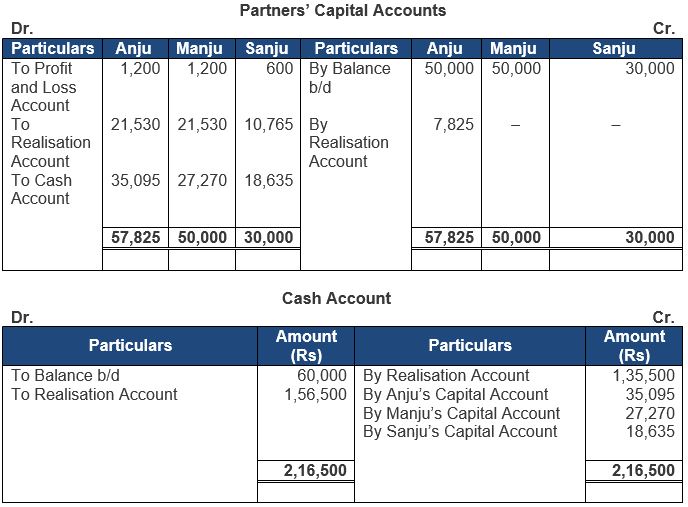

According to the Section 48 of the Indian Partnership Act, 1932, Mrs. A’s loan of Rs. 20,000, being outside party’s debt will be paid before payment of B’s loan. B will be paid up to the available cash, i.e. Rs. 5,000.

Question 12. Give the Journal entry for the treatment of partner’s loan appearing on the asset side of the Balance Sheet, on dissolution of partnership firm.

Partner’s loan is paid after outside liabilities have been paid bit before payment of capital.

Partner’s Loan A/c………………………. Dr.

To Bank/ Cash A/c

Question 13. What is Realisation Account?

Realisation Account is opened on the dissolution of a firm. The object of preparing this account is to close the books of account of the dissolved firm and to determine gain (profit) or loss on the realisation of assets and payment of liabilities.

Question 14. Give any two objects of preparing Realisation Account in the dissolution of a firm.

(I) transferring all assets except Cash or Bank Account to the debit side of the account

(ii) transferring all liabilities except Partner’s Loan Account and Partners’ Capital Accounts to the credit of the account.

Question 15. State the ratio in which the partners share gain (profit) or loss on realisation of various assets and payment of various liabilities.

Balance in the Realisation account is either gain or loss, which is transferred to the Capital Accounts of the Partners in their profit-sharing ratio.

Question 16. State any one occasion for the dissolution of the firm on court’s orders.

Court may pass order for the dissolution of the firm when a partner becomes a person of unsound mind.

Question 17. List any two grounds on which a court may dissolve a firm.

Court may pass order for the dissolution of the firm when:

(a) A partner becomes permanently incapable of preforming his duties as a partner.

(b) A partner is found guilty of misconduct, which is likely to adversely affect the business of the firm.

Question 18. What Journal entry is passed when an asset is given to any of the firm’s creditors towards partial payment of dues?

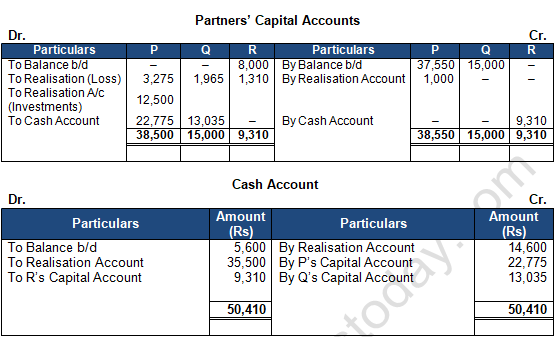

No entry is passed.

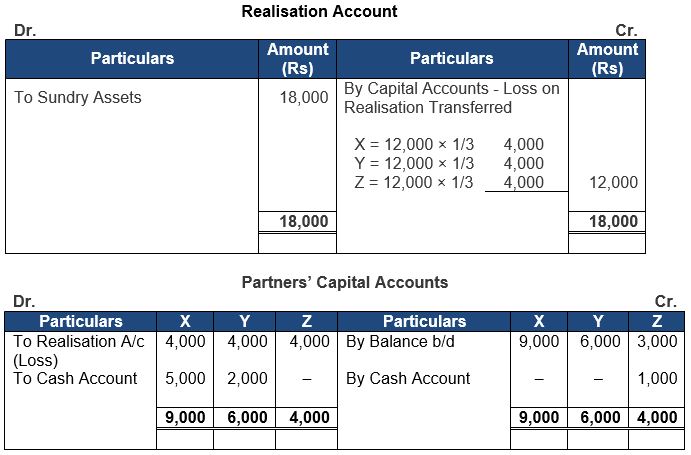

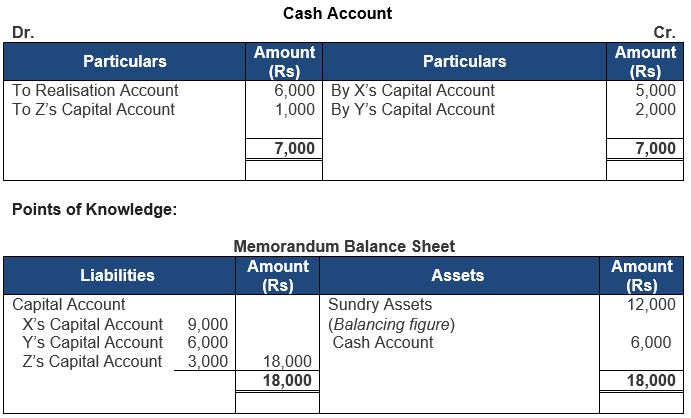

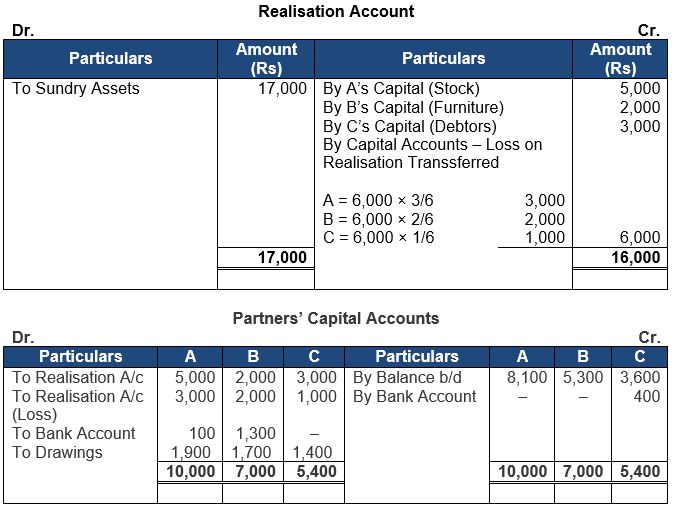

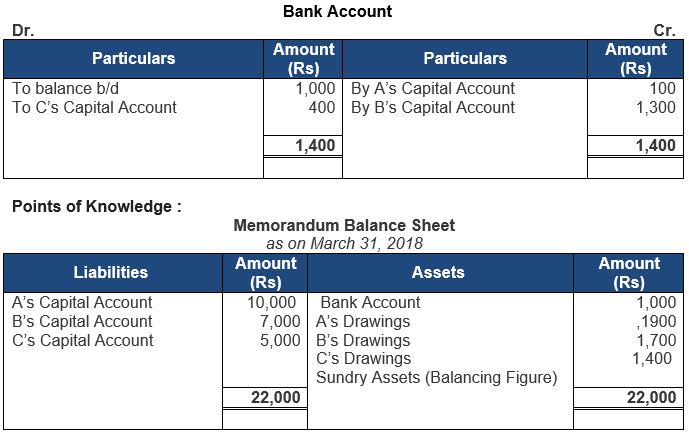

Question 19. What Journal entry is passed when a partner agrees to pay the realisation expenses on behalf of the firm?

Realisation A/c ……………………….. Dr.

To Partner’s Capital A/c

(Being the remuneration due to partner)

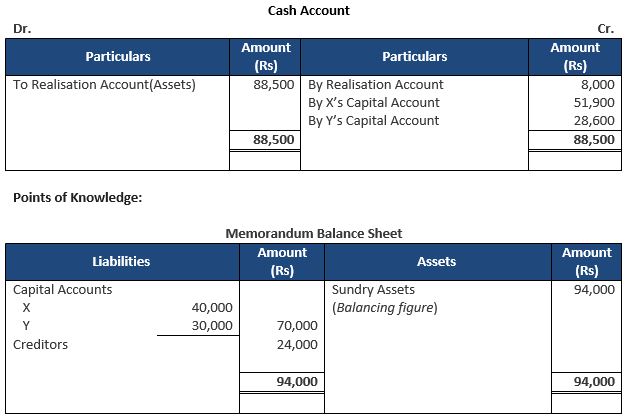

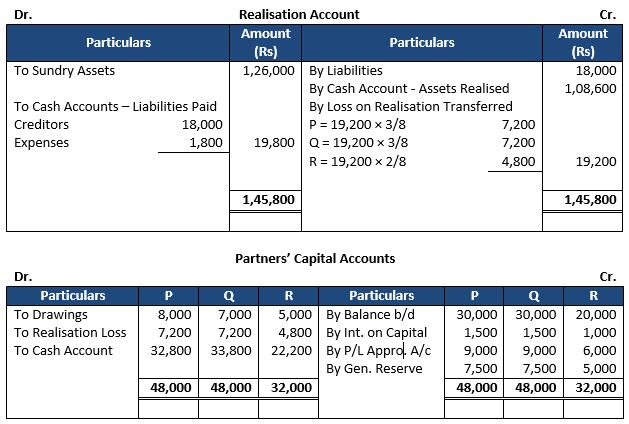

Question 20. What Journal entry is passed when the firm pays realisation expenses on behalf of a partner who has to bear the expenses?

Concerned Partner’s Capital A/c ………………………. Dr.

To Cash/Bank A/c

(Being realisation expenses paid on behalf of the partner)

Question 21. If a loan from a partner appears on the liabilities side of the Balance Sheet of the firm and the Capital Account of such partner shows a debit balance, how is loan dealt with?

Debit Balance in Partner’s Capital Account is less than the loan given by him. Hence, the amount of capital is transferred from his loan account to his capita account.

Question 22. Does the loan from an outside have priority over the loan from a partner as to repayment?

Yes, the loan from an outside have priority over the loan from a partner as to repayment.

Short Answer Type Questions........................

Question 1. Explain the provisions of Section 48 of Partnership Act, 1932 dealing with the settlement of accounts at the time of dissolution of firm.

Answer:

Section 48 of the Indian Partnership Act, 1932 deals with the settlement of accounts when the firm is dissolved. It is discussed below:

Treatment of losses: Loss, including deficiencies of capital, is paid first out of profit, then out of capital and lastly, if necessary, by the partners individually in the proportion in which they share profits.

Application of Assets: Assets of the firm, including amount contributed by the partners to make up deficiencies of capital, are applied in the following order:

(a) In paying firm’s debts to the third parties,

(b) In paying to each partner rateably what is due to him an account of loans or advances;

(c) In paying to each other rateably what is due to him on account of capital;

(d) The residue, if any, is distributed among the partners in their profit- sharing ratio.

Question 2. Distinguish between dissolution of Partnership and dissolution of partnership firm.

Answer:

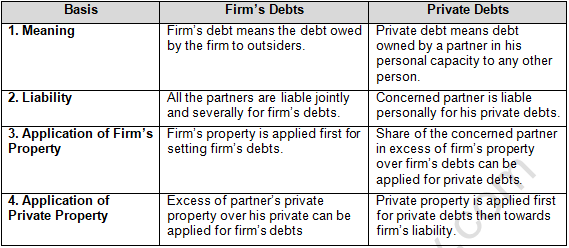

Question 3. Distinguish between firm’s debts and private debts.

Answer:

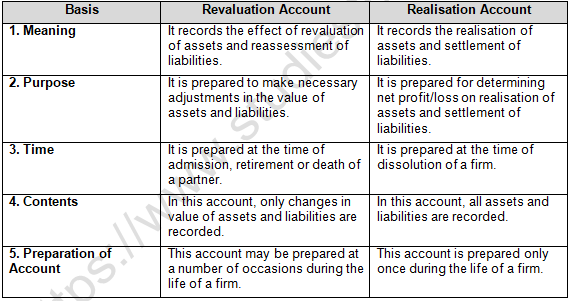

Question 4. Give two points of distinction between Revaluation Account and Realisation Account.

Answer:

Question 5. State any six situations in which the court may order to dissolve a partnership firm.

Answer:

Court may pass order for the dissolution of the firm when:

(a) A partner becomes a person of unsound mind;

(b) A partner becomes permanently incapable of preforming his duties as a partner.

(c) A partner is found guilty of misconduct, which is likely to adversely affect the business of the firm.

(d) Partnership agreement is breached persistently by a partner or partners;

(e) Court finds dissolution of the firm justified;

(f) When the business of the firm cannot be carried on except at a loss.

Question 6. Explain dissolution of a firm by (i) Agreement and (ii) Notice.

Answer:

The modes by which a firm may be dissolved are:

1.) Agreement:- a firm may be dissolved when all the partners agree for its dissolution. A partnership firm is set up by an agreement, similarly, it can be dissolved by an agreement.

2.) Notice:- In case partnership is at will, the firm may be dissolved by any partner giving notice in writing to all the other partners of his intention to dissolve the firm.

EXERCISE ::------->

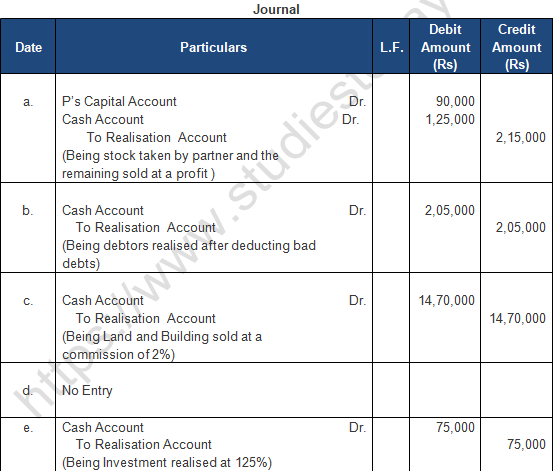

Question 1: Land and Building (book value) Rs. 1,60,000 sold for Rs. 3,00,000 through a broker who charged 2% commission on the deal. Journalise the transaction, at the time of dissolution of the firm.

Answer 1:

Working Note:-

Calculation of Commission:- 3,00,000 × 2 % = 6,000

Value of Land and Building = 3,00,000 – 6,000 = 2,94,000

About Solution:-

To close the asset accounts, all recorded assets (including goodwill) are moved to the realisation account at their book value, with the exception of fictitious assets, cash on hand, and the partner's capital account or bank current account (Dr. Balance). The Asset Account will be ended by crediting the assets because they have a debit Balance.

Realisation A/c ………………………………………Dr.

To Various Assets A/c

Things to Remember:

Dissolution of partnership firm is a process in which relationship between partners of firm is dissolved or terminated. If a relationship between all the partners of firm is dissolved then it is known as dissolution of firm. In case of dissolution of partnership firm, the firm ceases to exist.

Important Notes:

According to Section 39 of the Indian Partnership Act, 1932, the dissolution of partnership between all the partners of a firm is called "Dissolution of the Firm". A firm may be dissolved with the consent of all the partners or in accordance with a contract between the partners.

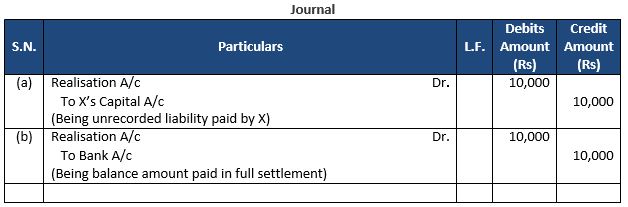

Question 2: (a) Pass the Journal entry when an unrecorded liability of ₹ 15,000 is settled at ₹ 10,000 and paid by X, a partner on the dissolution of a firm?

(b) What Journal entry will be passed when a machine having a book value of ₹ 15,000 is given to Rakesh, a creditor of ₹ 22,000 at an agreed value of ₹ 12,000 towards part payment of his dues?

Answer 2:

About Solution:-

i) Moving all assets—aside from cash and bank accounts—to the account's debit side.

ii) The account is credited with the amount realized from the selling of assets.

Things to Remember:

Modes of Dissolution of a Firm:

1. A firm can be dissolved either voluntarily or by an order from the Court.

2. Voluntary Dissolution of a Firm (without the order of the Court)

Important Notes:

According to Section 40 of the Indian Partnership Act, 1932, partners can dissolve the partnership by agreement and with the consent of all the partners. Partners can also dissolve the partnership based on a contract that has already been made.

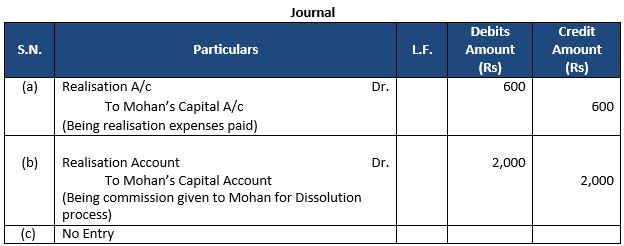

Question 3: Pass journal entries for the following:

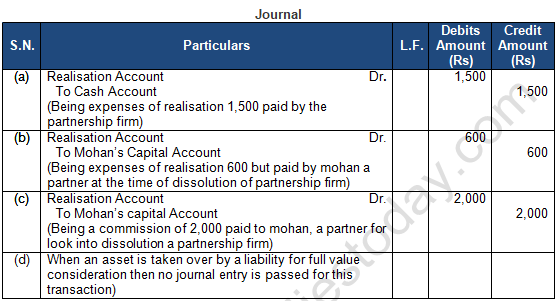

(a) Expenses of realisation Rs. 600 to be borne by the firm and are paid by Mohan, a partner.

(b) Mohan, one of the partners of the firm, was asked to carry out dissolution of the firm for which he was allowed a salary of Rs. 20,000. Expenses for dissolution were Rs. 5,000.

(c) Motor car of book value Rs. 50,000 taken by a creditor for Rs. 40,000 in settlement.

Answer 3:

About Solution:-

An event can make it unlawful for the firm to carry on its business. In such cases, it is compulsory for the firm to dissolve. However, if a firm carries on more than one undertakings and one of them becomes illegal, then it is not compulsory for the firm to dissolve. It can continue carrying out the legal undertakings. Section 41 of the Indian Partnership Act, 1932, specifies this type of voluntary dissolution.

Things to Remember:

On the happening of certain contingencies (Section 42):

According to Section 42 of the Indian Partnership Act, 1932, the happening of any of the following contingencies can lead to the dissolution of the firm:

1. Some firms are constituted for a fixed term. Such firms will dissolve on the expiry of that term.

2. Some firms are constituted to carry out one or more undertaking. Such firms are dissolved when the undertaking is completed.

3. Death of a partner.

4. Insolvency of a partner.

Important Notes:

By notice of partnership at will (Section 43): According to Section 43 of the Indian Partnership Act, 1932, if the partnership is at will, then any partner can give notice in writing to all other partners informing them about his intention to dissolve the firm. In such cases, the firm is dissolved on the date mentioned in the notice. lf no date is mentioned, then the date of dissolution of the firm is the date of communication of the notice.

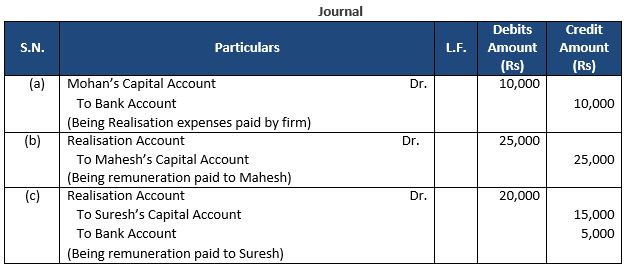

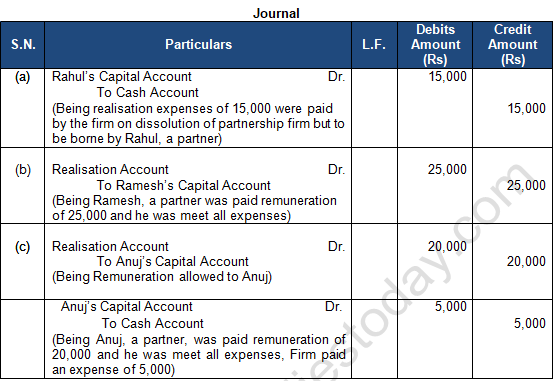

Question 4: Pass journal entries for the following:

(a) Realisation expenses Rs. 10,000 were to be borne by Raman, a partner, but were paid by the firm.

(b) Mahesh, a partner, was paid Rs. 25,000 and he was to bear the expenses.

(c) Suresh, a partner, was paid Rs. 20,000 and he was to bear the expenses. Firm paid an expenses of Rs. 5,000.

Answer 4:

About Solution:-

Dissolution of the Firm by the Court (Section 44):According to Section 44 of the Indian Partnership Act, 1932, the Court may dissolve a firm on the suit of a partner on any of the following grounds: Insanity/Unsound mind: If an active partner becomes insane or of an unsound mind, and other partners files a suit in the court, then the court may dissolve the firm.

Things to Remember:

Permanent Incapability: If a partner becomes permanently incapable of performing his duties as a partner, and other partners file a suit in the court, then the court may dissolve the firm. Also, the incapacity may arise from a physical disability, illness etc.

Important Notes:

Misconduct: When a partner is guilty of conduct which is likely to affect prejudicially the carrying on of the business and the other partners file a suit in the court, then the court may dissolve the firm. Further, it is not important that the misconduct is related to the conduct of the business. The court looks at the effect of the misconduct on the business along with the nature of the business.

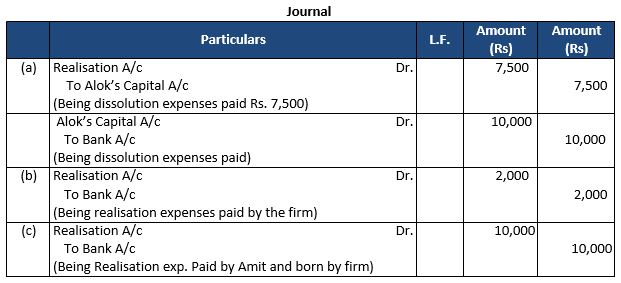

Question 5: Pass Journal entries for the following:

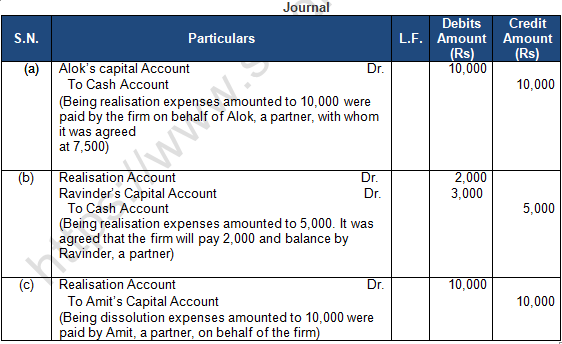

(a) Firm agreed to pay Alok Rs. 7,500 towards dissolution expenses. Dissolution expenses were Rs. 10,000 which were paid by the firm.

(b) Realisation expenses were Rs. 5,000. It was agreed that the firm will bear Rs. 2,000 and balance by Ravi, a partner.

(c) Dissolution expenses of Rs. 10,000 were paid by Amit, a partner, on behalf of the firm.

(d) Realisation expenses of Rs. 6,000 was agreed by the firm to reimburse Ajay. Dissolution expenses were Rs. 7,000.

Answer 5:

About Solution:-

Persistent Breach of the Agreement: A partner may fully or persistently commit a breach of the agreement relating to:

1. The management of the affairs of the firm, or

2. A reasonable conduct of its business,

3. Conduct himself in matters relating to business that is not reasonably practicable for other partners to carry on the business in partnership with him.

Things to Remember:

The term dissolution means coming to an end or discontinuation. The dissolution of the firm implies a complete breakdown of the partnership relation among all the partners. Dissolution of the partnership (owing to retirement, death or insolvency of a partner), merely involves change in the relation of the partners but it does not end the firm; the partnership would certainly come to an end but the firm, the reconstituted one might continue under the same name.

Important Notes:

The dissolution of the partnership may or may not include the dissolution of the firm but the dissolution of the firm necessarily means the dissolution of the partnership. On dissolution of the firm, the business of the firm ceases to exist since its affairs are wound up by selling the assets and by paying the liabilities and discharging the claims of the partners. The dissolution of partnership among all partners of a firm is called dissolution of the firm.

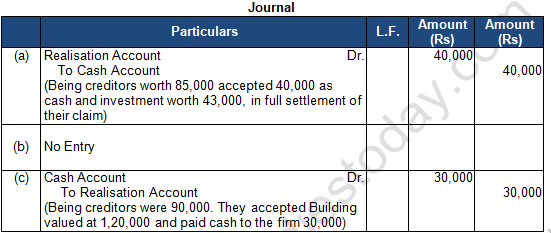

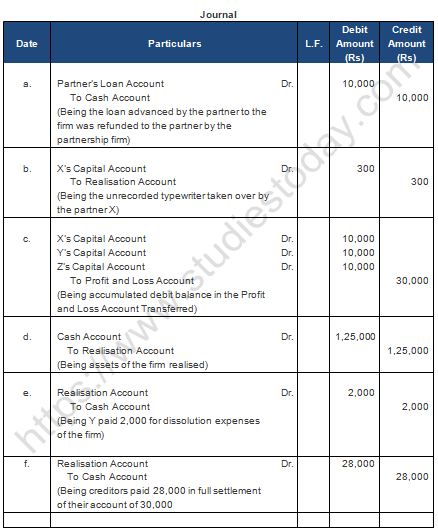

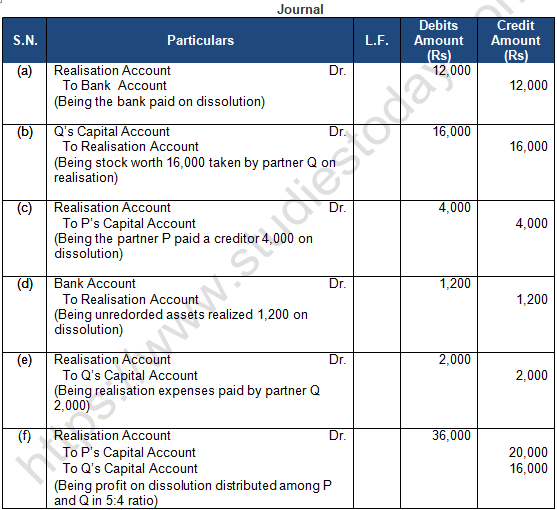

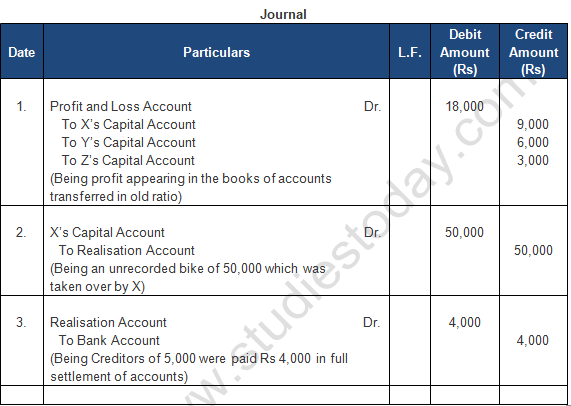

Question 6: Pass necessary Journal entries in the following cases:

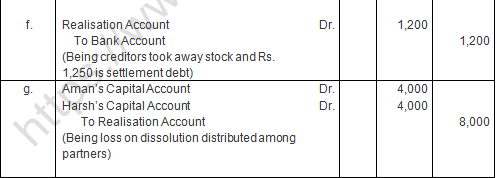

(a) Creditors of ₹ 85,000 accepted ₹ 40,000 as cash and investment of ₹ 43,000, in full settlement of their claim.

(b) Creditors were ₹ 16,000. They accepted Machinery valued at ₹ 18,000 in settlement of their claim.

(c) Creditors were ₹ 90,000. They accepted Building valued at ₹ 1,20,000 and paid cash to the firm ₹ 30,000.

Answer 6:

About Solution:-

1. Transferring all assets except Cash and Bank Account to the debit side of the account.

2. Amount realised on sale of assets is credited to the account.

Things to Remember:

Dissolution by Agreement: A firm is dissolved in case

1. All the partners give consent or

2. As per the terms partnership agreement.

Important Notes:

A firm is dissolved compulsorily in the following cases, when all the partners or all excepting one partner becomes insolvent or of unsound

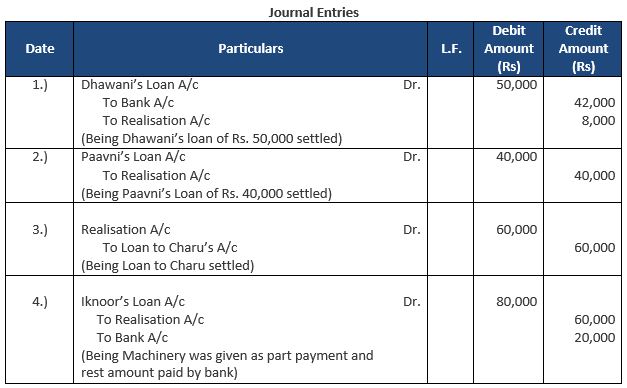

Question 7: Charu, Dhwani, Iknoor and Paavni were partners in a firm. They had entered into partnership firm last year only, through a verbal agreement. They contributed Capitals in the firm and to meet other financial requirement, few partners also provided loan to the firm. Within a year, their conflicts arisen due to certain disagreements and they decided to dissolve the firm. The firm had appointed Mr. Kavya, who is a financial advisor and legal consultant, to carry on the dissolution process. In the firm instance, Mr. kavya had transferred various assets and external liabilities to Realisation Account. Due to her busy schedule; Ms. Kavya has delegated this assignment to you, being an intern in her firm. On the date of dissolution, you have observed the following transactions:

(i) Dhwani’s Loan of ₹ 50,000 to the firm was settled by paying ₹ 42,000.

(ii) Paavni’s Loan of ₹ 40,000 was settled by giving an unrecorded asset of ₹ 45,000.

(iii) Loan to Charu of ₹ 60,000 was settled by payment to Charu’s brother loan of the same amount.

(iv) Iknoor’s Loan of ₹ 80,000 to the firm and she took over Machinery of ₹ 60,000 as part payment.

You are required to pass necessary entries for all the above-mentioned transactions.

Answer 7:

About Solution:-

You have already studied that on the occasion of admission, retirement and death existing partnership comes to an end, but the business of the firm continues under a new agreement. When a firm decides to wind up its business operations under any of the circumstances mentioned, it stands dissolved. Dissolution of a partnership firm is different from the dissolution of a partnership.

Things to Remember:

Dissolution of a firm means that the firm closes its business and comes to an end. While dissolution of a partnership means termination of old partnership agreement and a reconstitution of firm due to admission, retirement and death of a partner. In dissolution of a partnership the remaining partners may agree to carry on the business under a new agreement.

Important Notes:

When the partners decide to discontinue the business of the firm, it becomes necessary to settle its accounts. For this purpose, it disposes off all its assets (except cash and bank balances) for satisfying all the claims against it. For this purpose a separate account called ‘Realisation Account’ is opened. Realisation Account is an account in which assets excluding cash in hand and bank are transferred at their book value and all external liabilities are transferred at their book value.

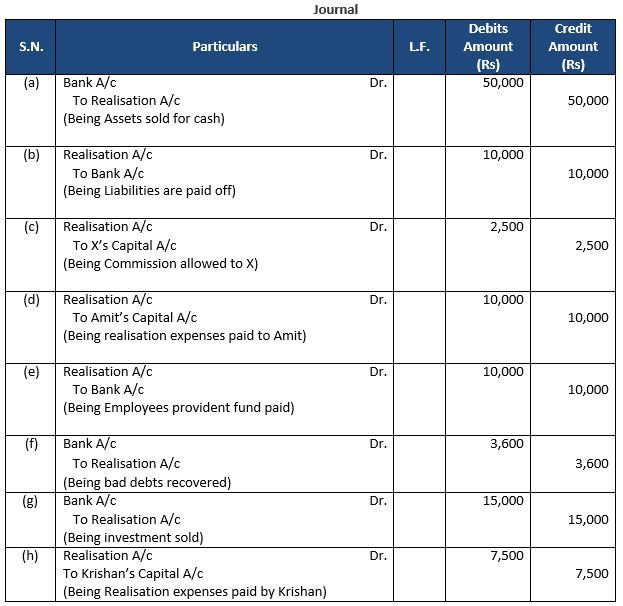

Question 8: Pass, Journal entries for the following at the time of dissolution of the firm of X and Y after the various assets (other than cash) and outside liabilities have been transferred to Realisation Account:

(a) Sale of Assets – ₹ 50,000.

(b) Payment of Liabilities – ₹ 10,000.

(c) A commission of 5% allowed to X, a partner, on sale of assets.

(d) Realisation expenses were ₹ 15,000. The firm had agreed with Amrit, to reimburse him ₹ 10,000.

(e) Employees Provident Fund ₹ 10,000.

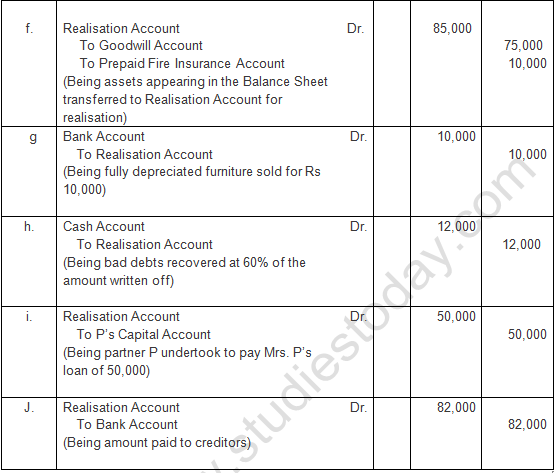

(f) Z, a debtor, whose account of ₹ 6,000 was written off as bad earlier, paid 60% of the amount.

(g) Investment (Book Value ₹ 10,000) realised at 150%.

(h) Realisation expenses were ₹ 10,000. The firm had agreed with Krishan, a partner, to reimburse him up to ₹ 7,500.

Answer 8:

About Solution:-

Assets account is closed by transferring it to the Realisation Account at its Book Value.

Realisation A/c Dr.

To Assets A/c

(Transfer of assets)

Things to Remember:

It is to be noted that the following items on the assets side of the Balance Sheet are not transferred to the Realisation Account:

(i) Undistributed loss (i.e. Debit Balance of Profits and Loss account).

(ii) Fictitious assets or deferred revenue expenditures such as preliminary expenses.

Important Notes:

All the above items are closed by transferring them to the partners’ Capital Account in their profit sharing ratio. The Journal entry is made:

Partner’s capital A/c Dr. (Individually)

To Profit & Loss A/c

To Fictitious Assets A/c

(Transfer of loss and fictitious Assets)

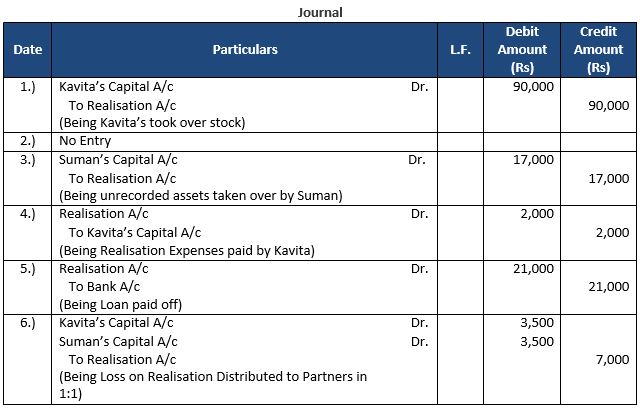

Question 9: Pass necessary Journal entries for the following transactions, on the dissolution of a partnership firm of Kavita and Suman on 31st March, 2022, after the various assets (other than cash) and third party liabilities have been transferred to Realisation Account.

(a) Kavita took over stock amounting to ₹ 1,00,000 at ₹ 90,000.

(b) Creditors of ₹ 2,00,000 took over Plant and Machinery of ₹ 3,00,000 in full settlement of their claim.

(c) There was an unrecorded asset of ₹ 23,000 which was taken over by Suman at ₹ 17,000.

(d) Realisation expenses ₹ 2,000 were paid by Kavita.

(e) Bank Loan of ₹ 21,000 was paid off.

(f) Loss on dissolution amounted to ₹ 7,000.

Answer 9:

About Solution:-

Provisions and reserves against assets should be closed by crediting the Realisation Account. The Journal entry is made:

Provision for Doubtful Debts A/c Dr.

Provision for Depreciation A/c Dr.

Any other Provision A/c Dr.

To Realisation A/c

(Transfer of provision on assets)

Things to Remember:

The accounts of various external liabilities are closed by transferring them to the Realisation Account. The loan given to the firm by a partner’s wife is treated as an external liability and is transferred to the credit of Realisation Account.

Important Notes:

The relevant Journal entry is as under:

External Liabilities A/c Dr. (Individually)

To Realisation A/c (Transfer of external liability)

Capital and Loan account of the partners’ are treated separately and so are not transferred to the Realisation Account.

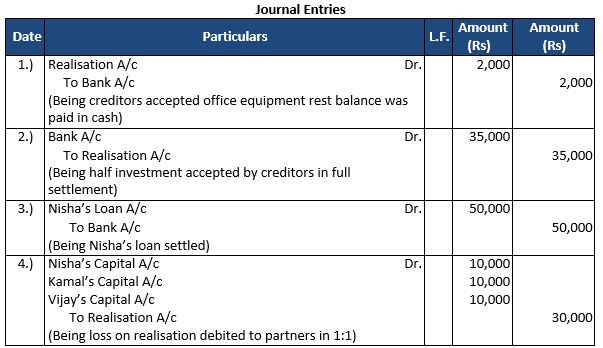

Question 10: Nisha, Kamal and Vijay has an automobile spare parts business. Due to strained relationship among the partners, they were unable to take collective decisions for the growth of business. As a result, firm has been in losses for the last 3 years. The partners decided to dissolve the firm.

Following transactions took place at the time of dissolution:

(i) Shiv, a creditor, to whom ₹ 6,000 were due, accepted office equipment at ₹ 4,000 and the balance was paid to him.

(ii) Investment, which appeared in the book at ₹ 1,00,000, half of it is taken by Mohan, a creditor, at 10% above the book value in settlement of his claim and the remaining half was sold in the market at a loss of 30%.

(iii) Loan of ₹ 50,000 advanced by Nisha to the firm was returned.

(iv) Loss on realisation ₹ 30,000 was distributed among the partners equally.

Journalise the above transaction at the time of dissolution of the firm.

Answer 10:

About Solution:-

Any balance of accumulated reserves (e.g. general reserves), Profit and Loss Account (Cr.), Reserve Fund and other reserves on the date of dissolution will be credited to the Partners’ Capital accounts on the basis of profit sharing ratio.

Things to Remember:

Journal entry will be recorded:

Profit and Loss A/c Dr.

General Reserve A/c Dr.

Any Other Fund Dr.

To Partners’ Capital A/c (Individually)

(Transfer of profit and reserve)

Important Notes:

For Sale of Assets (for cash) journal entry will be:-

Bank/ Cash A/c Dr. (Realised Value)

To Realisation A/c (Sale of assets)

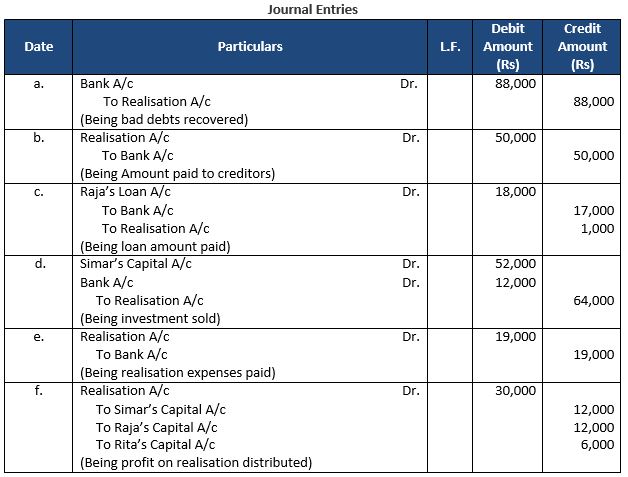

Question 11: Simar, Raja and Rita were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. The firm was dissolved on 31st March, 2019. After the transfer of assets (other than cash) and external liabilities to the Realization Account, the following transactions took place:

(a) A debtor whose debt of ₹ 90,000 had been written off as bad, paid ₹ 88,000 in full settlement.

(b) Creditors to whom ₹ 1,21,000 were due to be paid, accepted stock at ₹ 71,000 and the balance was paid to them by a cheque.

(c) Raja had given a loan to the firm of ₹ 18,000. He was paid ₹ 17,000 in full settlement of his loan.

(d) Investments were ₹ 53,000 out of which investments of ₹ 43,000 were taken by Simar at ₹ 52,000 and the balance of the investments were sold for ₹ 12,000.

(e) Expenses on dissolution amounted to ₹ 19,000 and the same were paid by the firm.

(f) Profit on dissolution amounted to ₹ 30,000.

Pass the necessary Journal entries for the above transactions in the books of the firm.

Answer 11:

About Solution:-

Treatment of Accumulated Reserves and Profit/Loss: Any balance of accumulated reserves (e.g. general reserves), Profit and Loss Account (Cr.), Reserve Fund and other reserves on the date of dissolution will be credited to the Partners’ Capital accounts on the basis of profit sharing ratio. The following journal entry will be recorded:

Profit and Loss A/c Dr.

General Reserve A/c Dr.

Any Other Fund Dr.

To Partners’ Capital A/c (Individually)

(Transfer of profit and reserve)

Things to Remember:

For Sale of Assets (for cash)

Bank/ Cash A/c Dr. (Realised Value)

To Realisation A/c

(Sale of assets)

Important Notes:

For Assets taken Over by the Partner:-

(a) Partners’ Capital A/c Dr.

To Realisation A/c (Agreed Price)

(Assets taken over by partner)

(b) Bank/Cash/Partners capital A/c Dr.

To Partner’s Loan A/c

(Settlement of loan to a partner)

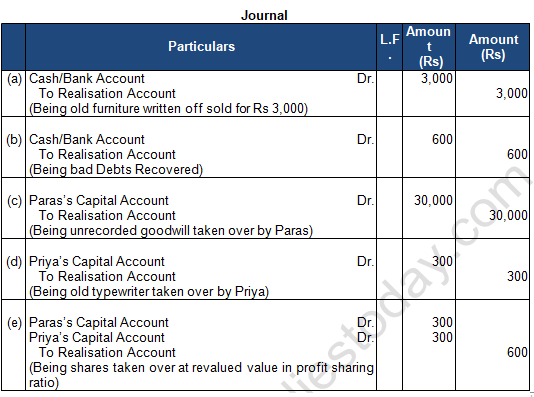

Question 12: Pass necessary Journal entries to record the following unrecorded assets and liabilities in the books of Paras and Priya.

(a) There was old furniture in the firm which had been written off completely in the books. This was sold for ₹ 3,000.

(b) Ashish, an old customer whose account for ₹ 1,000 was written off as bad in the previous year, paid 60% of the amount.

(c) Paras agreed to take over the firm’s goodwill (not recorded in the books of the firm), at a valuation of ₹ 30,000.

(d) There was an old typewriter which had been written off completely from the books. It was estimated to realise ₹ 400. It was taken by Priya at an estimated price less 25%.

(e) There was 100 shares of ₹ 100 each in Star Limited acquired at a cost of ₹ 2,000 which has been written off completely from the books. These share are valued @ ₹ 6 each and divided among the partners in their profit sharing ratio.

Answer 12:

About Solution:-

Settlement of loans given by the Partner

Partners’ Loan A/c Dr.

To Bank/Cash/Partners’ capital A/c

(Settlement of loan given by the partner)

Things to Remember:

Payment of Liabilities by the Partner(s)

Realisation A/c Dr.

To Partner Capital A/c

(Liabilities taken over by partner)

Important Notes:

For Transfer of Liabilities: The accounts of various external liabilities are closed by transferring them to the Realisation Account. The loan given to the firm by a partner’s wife is treated as an external liability and is transferred to the credit of Realisation Account. The relevant Journal entry is as under:

External Liabilities A/c Dr. (Individually)

To Realisation A/c

(Transfer of external liability)

Capital and Loan account of the partners’ are treated separately and so are not transferred to the Realisation Account.

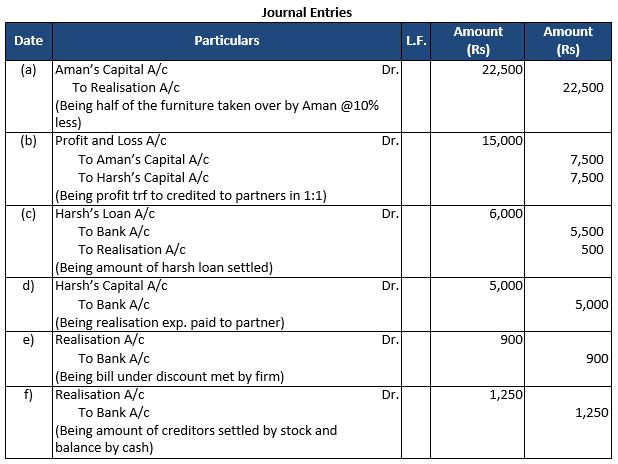

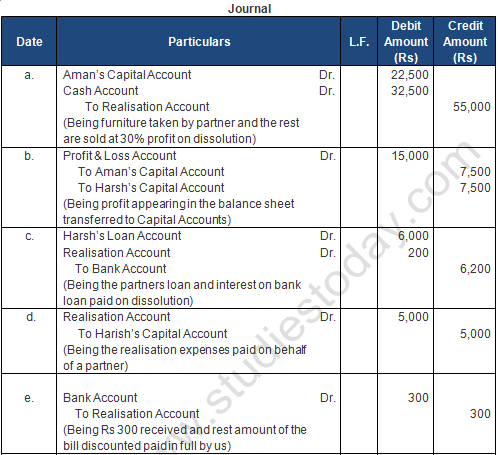

Question 13: Aman and Harsh were partners in a firm. They decided to dissolve their firm. Pass necessary Journal entries for the following after assets (other than Cash and Bank) and outside liabilities have been transferred to Realisation Account.

(a) There was furniture of ₹ 50,000. Aman took over 50% of the furniture at 10% discount.

(b) Profit & Loss Account was showing a credit balance of ₹ 15,000 on the date of dissolution.

(c) Harsh’s loan of ₹ 6,000 was settled by paying ₹ 5,500.

(d) The firm paid realisation expenses of ₹ 5,000 on behalf of Harsh, a partner.

(e) There was a bill for ₹ 1,200 under discount. The bill was received from Soham who became insolvent and a first and final dividend of 25% was received from his estate.

(f) Creditors, to whom the firm owed ₹ 6,000, accepted stock of ₹ 5,000 at a discount of 5% and the balance in cash.

Answer 13:

About Solution:-

Sometimes, there may be some assets that have already been written off completely in previous years and thus, do not appear in the Balance Sheet but physically they still exist for operational purposes. For example, there is an old computer, which is still in working condition though its book value is zero. Similarly, there may be some liabilities, which do not appear in the Balance Sheet, but actually they are still there. For example, a bill discounted with bank, on dissolution it was dishonoured and had to be taken up by the firm for payment purposes.

Things to Remember:

It is to be kept in mind that an unrecorded asset would never be transferred to the debit of the Realisation Account, because the amount realised from its sale is in nature of a gain and the Realization Account is only credited accordingly. Similarly, an unrecorded liability need not be transferred to Realisation.

Important Notes:

When the amount realised from the sale of an unrecorded asset.

Cash/Bank A/c Dr.

To Realisation A/c

(Sale of unrecorded assets)

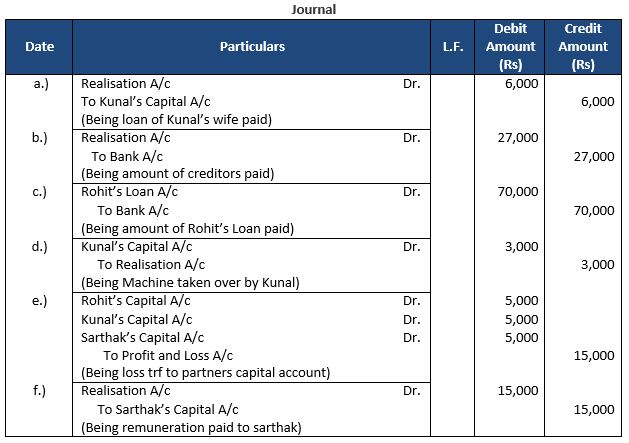

Question 14: Rohit, Kunal and Sarthak are partners in a firm. They decided to dissolve their firm. Pass necessary Journal entries for the following after various assets (other than Cash and Bank) and the third-party liability have been transferred to Realisation Account:

(a) kanal agreed to pay his wife’s loan of ₹ 6,000.

(b) Total Creditors of the firm were ₹ 40,000. Creditors of ₹ 10,000 were given a piece of furniture of book value ₹ 8,000 out of total furniture of book value ₹ 28,000 in settlement. Remaining Creditors allowed a discount of 1%.

(c) Rohit had given a loan of ₹ 70,000 to the firm which was duly paid.

(d) A machine which was not recorded in the books was taken by Kunal at ₹ 3,000, whereas its expected value was ₹ 5,000.

(e) The firm had a debit balance of ₹ 15,000 in the Profit & Loss Account on the date of dissolution.

(f) Sarthak paid the realisation expenses of ₹ 16,000 out of his private funds, who was to get a remuneration of ₹ 15,000 for completing dissolution process.

Answer 14:

About Solution:-

When realisation expenses are paid by the firm (i.e. borne by the firm). The following journal entry will be recorded:

Realisation A/c Dr.

To Bank/ Cash A/c

(Payment of realisation expenses)

Things to Remember:

When realisation expenses are paid by the firm (i.e. borne by the firm). The following journal entry will be recorded:

Realisation A/c Dr.

To Bank/ Cash A/c

(Payment of realisation expenses)

Important Notes:

Realisation expenses were agreed to be paid by the partner and were paid by the firm:-

Partner’s Capital A/c Dr.

To Cash/Bank A/c

(Realisation expenses paid and borne by partner)

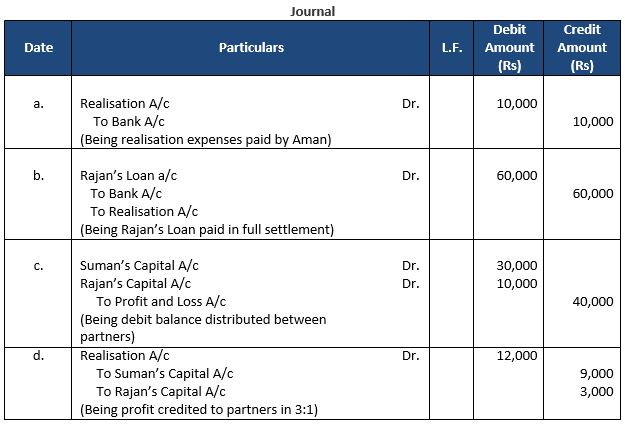

Question 15: Suman and Rajan were partners in a firm sharing profits and losses in the ratio of 3 : 1. The firm was dissolved on 31st March 2019. Pass the necessary Journal entries for the following transactions after various assets (other than cash in hand and a bank) and third-party liabilities have been transferred to Realisation Account.

(a) Dissolution expenses ₹ 10,000 were paid by the firm.

(b) Rajan had given a loan of ₹ 60,000 to the firm for which he accepted ₹ 58,000 in full settlement.

(c) The firm had a debit balance of ₹ 40,000 in the Profit & Loss Account on the date of dissolution.

(d) Profit on realisation was ₹ 12,000.

Answer 15:

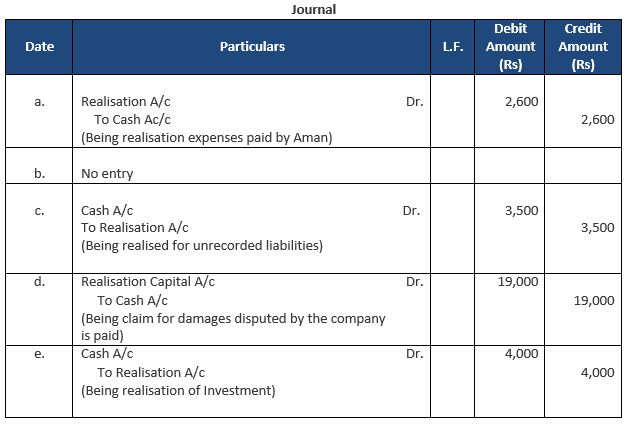

Question 16: Pass necessary Journal Entries for the following transactions on the dissolution of a firm after various assets (other than cash) and outside liabilities have been transferred to Realisation Account:

(i) Realisation expenses of the firm amounting to Rs. 2,600 were paid by partner, Aman.

(ii) A creditor of Rs. 4,500 took over stock valued at Rs. 5,200 in full settlement.

(iii) An unrecorded assets realised Rs. 3,500.

(iv) Remaining creditors amounting to Rs. 20,000 were paid at a discount of 5%.

(v) Remaining stock of Rs. 30,000 was taken over by Bimal, a partner, at a discount of 20%.

(vi) Investment whose face value was Rs. 10,000 was realised at 40%.

Answer 16:

About Solution:-

An unrecorded asset would never be transferred to Realisation Account, because the amount realised from its sale is in the form of a gain and the Realization Account is only credited accordingly.

Things to Remember:

After all the adjustments related to partners’ capital accounts and transfer of profit or loss on realisation to the partner’s capital accounts, the capital accounts are closed.

Important Notes:

Partner’s capital accounts are closed through making payment from the bank account and thereby bank account stands closed by making/ receiving payment.

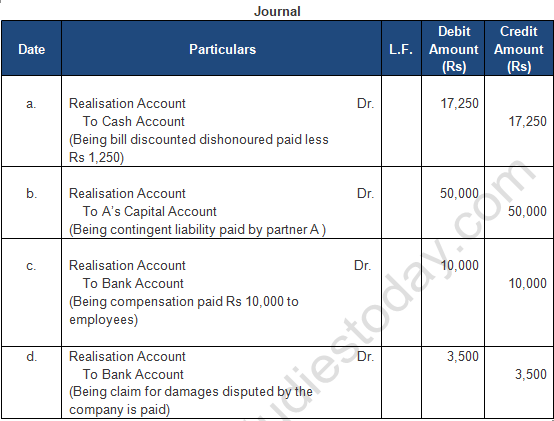

Question 17: What journal entries would be passed for discharge of following unrecorded liabilities on the dissolution of a firm of partners A and B:

(a) There was a contingent liability in respect of bills discounted but not matured of Rs 18,500. An acceptor of one bill of Rs 2,500 became insolvent and fifty paisa in a rupee was recovered. The liability of the firm on account of this bill discounted and dishonoured has not so far been recorded.

(b) There was a contingent liability in respect of a claim from damages for Rs75,000, such liability was settled for Rs 50,000 and paid by the partner A.

(c) Firm will have to pay Rs 10,000 as compensation to an injured employee, which was a contingent liability not accepted by the firm.

(d) Rs 5,000 for damages claimed by a customer has been disputed by the firm. It was settled at 70% by a compromise between the customer and the firm.

Answer 17:

About Solution:-

The balance in the realisation account would show either profit or loss on dissolution. If the total of the credit side is more than the debit side, then there is a profit and following journal entry is made: Realisation A/c Dr. (Individually)

To Partner’s Capital/ Current A/c (Individually)

(Profit on realisation transferred to capital accounts)

Things to Remember:

The debit side is more than credit side, then there is a loss on dissolution and following journal entry is made:

Partner’s Capital/Current A/c Dr. (Individually)

To Realisation A/c

(Loss on realisation transferred to capital account)

Important Notes:

After all the adjustments related to partners’ capital accounts and transfer of profit or loss on realisation to the partners’ capital accounts, the capital accounts are closed in the following manner: (a) If the Partner’s Capital Account shows a debit balance, the partner has to bring the necessary amount of cash. The following journal entry is made:

Bank/Cash A/c Dr.

To Partner’s Capital A/c

(Cash brought by the partner)

Question 18: Pass necessary journal entries on the dissolution of a firm in the following cases:

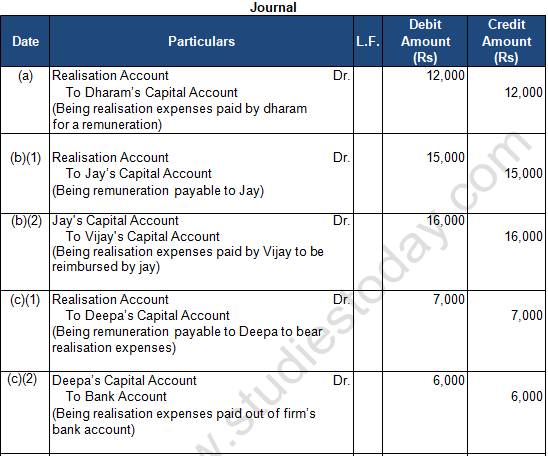

(a) Dharam, a partner, was appointed to look after the process of dissolution at a remuneration of Rs 12,000 and he had to bear the dissolution expenses. Dissolution expenses Rs 11,000 were paid by Dharam.

(b) Jay, a partner, was appointed to look after the process of dissolution and was allowed a remuneration of Rs 15,000. Jay agreed to bear dissolution expenses. Actual dissolution expenses Rs 16,000 were paid by Vijay, another partner on behalf of Jay.

(c) Deepa, a partner, was to look after the process of dissolution and for this work she was allowed a remuneration of Rs 7,000. Deepa agreed to bear dissolution expenses. Actual dissolution expenses Rs 6,000 were paid from the firm's bank account.

(d) Dev, a partner, agreed to do the work of dissolution for Rs 7,5000. He took away stock of the same amount as his commission. The stock had already been transferred to Realisation Account.

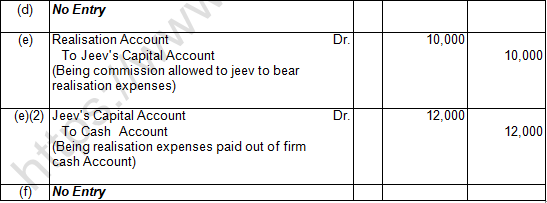

(e) Jeev, a partner, agreed to do the work of dissolution for which he was allowed a commission of Rs 10,000. He agreed to bear the dissolution expenses. Actual dissolution expenses paid by Jeev were Rs 12,000. These expenses were paid by Jeev by drawing cash from the firm.

(f) A debtor of Rs 8,000 already transferred to Realisation Account agreed to pay the realisation expenses of Rs 7,800 in full settlement of his account.

Answer 18:

About Solution:-

If the Partner’s Capital Account shows a credit balance, he/she is to be paid off the necessary amount of cash. The following journal entry will be made:

Partner’s Capital A/c Dr.

To Bank/Cash A/c

(Cash paid to partner)

Things to Remember:

After closing the partners’ capital accounts, bank account is prepared and all entries pertaining to the bank/cash are posted in it including any cash brought in by the partner on the dissolution of firm. Partners’ capital accounts are closed by making payment from the bank account and thereby bank account stands closed by making/receiving payment. In this way all the accounts stand closed. If cash/bank account does not show any balance, it implies that all the accounts of the dissolved firm have been closed properly

Important Notes:

When a firm decides to close its business and no business activity is carried out by the firm, it is said to be dissolved.

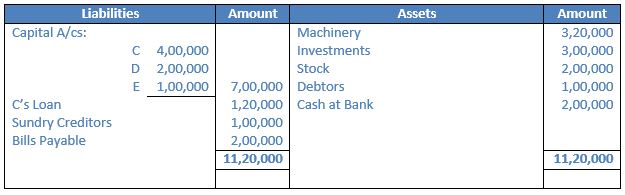

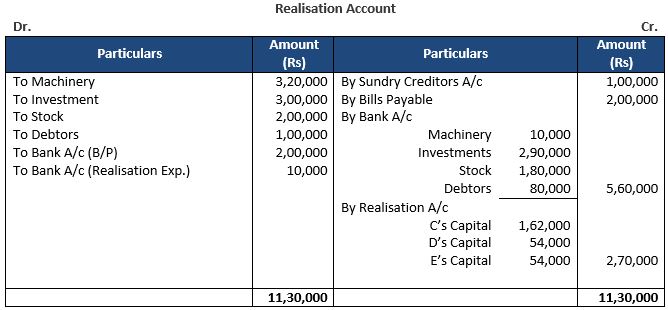

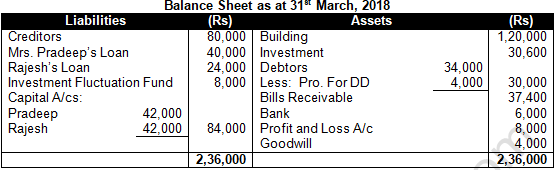

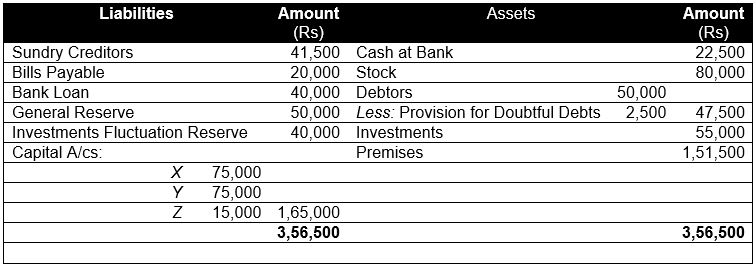

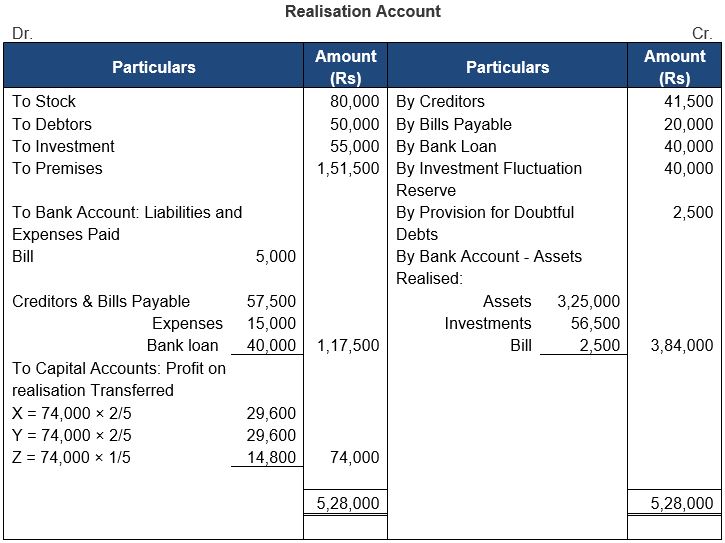

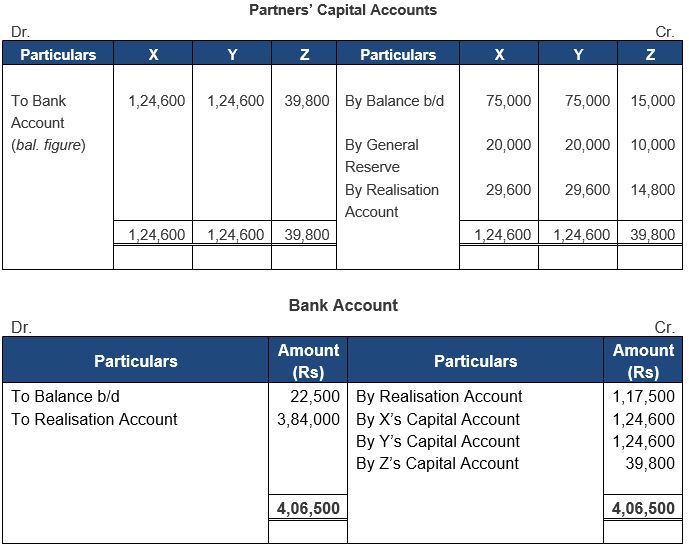

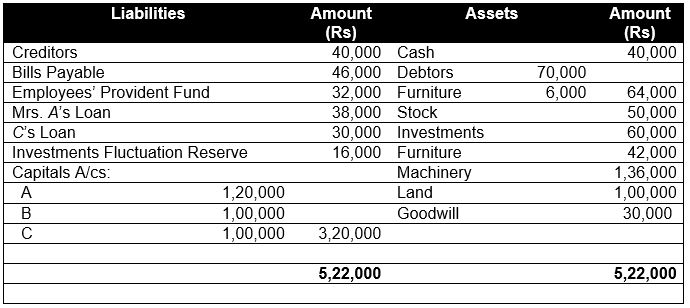

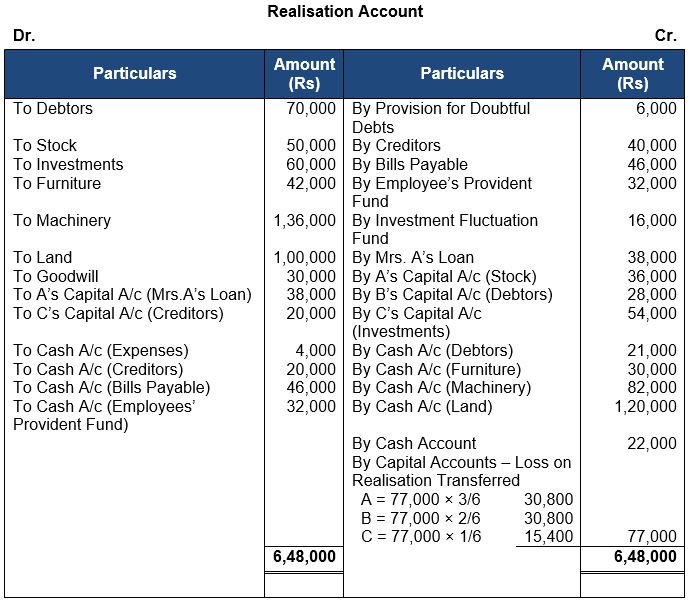

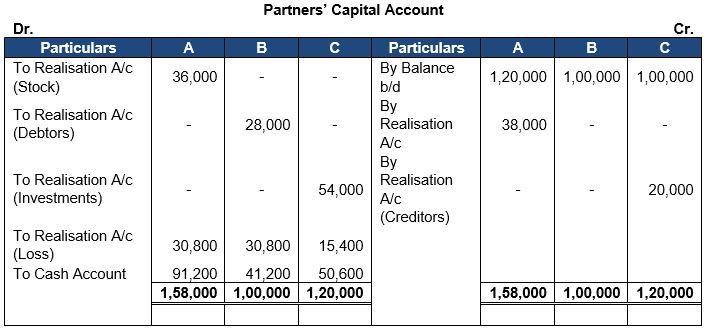

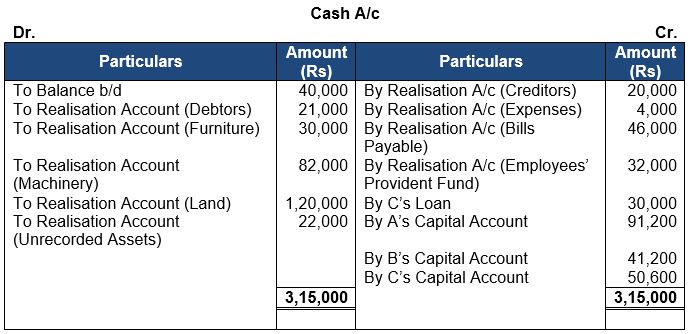

Question 19: C, D and E were partners in a firm sharing profits in the ratio of 3:1:1. Their Balance Sheet as at 31st March, 2022 was as follows:

On the above date, the firm was dissolved due to certain disagreement among the partners.

(i) Machinery of ₹ 3,00,000 were given to creditors in full settlement of their account and remaining machinery was sold for ₹ 10,000.

(ii) Investments realised ₹ 2,90,000.

(iii) Stock was sold for ₹ 1,80,000.

(iv) Debtors for ₹ 20,000 proved bad.

(v) Realisation expenses amounted to ₹ 10,000.

Prepare Realisation Account.

Answer 19:

About Solution:-

An unrecorded asset would never be transferred to Realisation Account, because the amount realised from its sale is in the form of a gain and the Realization Account is only credited accordingly.

Things to Remember:

After all the adjustments related to partners’ capital accounts and transfer of profit or loss on realisation to the partner’s capital accounts, the capital accounts are closed.

Important Notes:

Partner’s capital accounts are closed through making payment from the bank account and thereby bank account stands closed by making/ receiving payment.

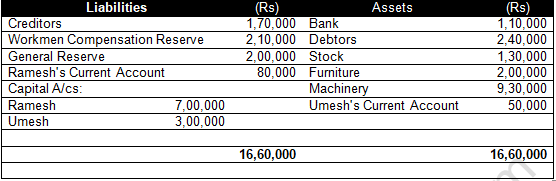

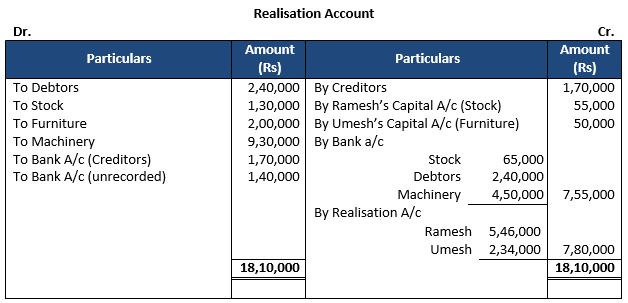

Question 20: Ramesh and Umesh were partners in a firm sharing profits in the ratio of their capitals. On 31st March, 2023, their Balance Sheet was as follows:

On the above date the firm was dissolved.

(a) Ramesh took 50% of stock at Rs. 10,000 less than book value.

(b) Furniture was taken by Umesh for Rs. 50,000 and machinery was sold for Rs. 4,50,000.

(c) Creditors were paid in full.

(d) There was an unrecorded bill for repairs for Rs. 1,60,000 which was settled and paid at Rs. 1,40,000.

Prepare Realisation Account.

Answer 20:

About Solution:-

Dissolution of a firm is different from the dissolution of a partnership. Dissolution of a firm means that the firm closes its business and comes to an end. While dissolution of a partnership means termination of old partnership agreement and a reconstitution of firm due to admission, retirement and death of a partner.

Things to Remember:

On dissolution of the firm the books of accounts are closed. All assets and liabilities are transferred to an account called “Realisation Account”. This account records the realisation of assets and the payment of liabilities.

Important Notes:

When the partners decide to discontinue the business of the firm, it becomes necessary for it to settle its accounts. For this purpose, it disposes off all its assets (except cash and bank balances) for satisfying all the claims against it.

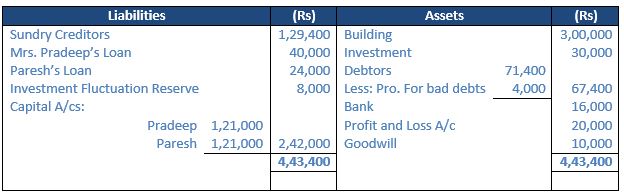

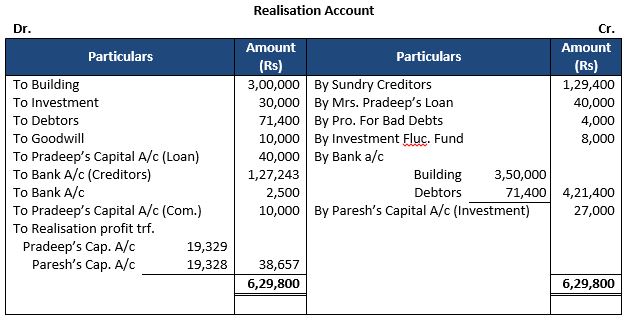

Question 21: Pradeep and Paresh partners in a firm decided to decided to dissolve their partnership firm on 1st April, 2024. Pradeep was deputed to realised the assets and to pay off the liabilities. He was paid Rs. 10,000 as commission for his services. Balance Sheet of the firm on 31st March, 2024 was as follows:

Following terms and conditions were agreed upon:

(a) Pradeep agreed to pay his wife’s loan.

(b) Investment was given to Paresh for Rs. 27,000.

(c) Building realised Rs. 3,50,000.

(d) Creditors were to be paid after two months, they were paid immediately at 10% p.a. discount.

(e) Realisation expenses were Rs. 2,500.

Prepare Realisation Account.

Answer 21:

About Solution:-

i) Moving all assets—aside from cash and bank accounts—to the account's debit side.

ii) The account is credited with the amount realized from the selling of assets.

Things to Remember:

Modes of Dissolution of a Firm:

1. A firm can be dissolved either voluntarily or by an order from the Court.

2. Voluntary Dissolution of a Firm (without the order of the Court)

Important Notes:

According to Section 40 of the Indian Partnership Act, 1932, partners can dissolve the partnership by agreement and with the consent of all the partners. Partners can also dissolve the partnership based on a contract that has already been made.

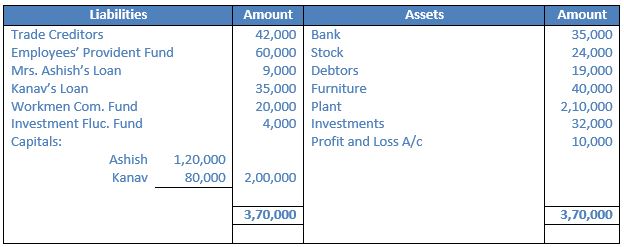

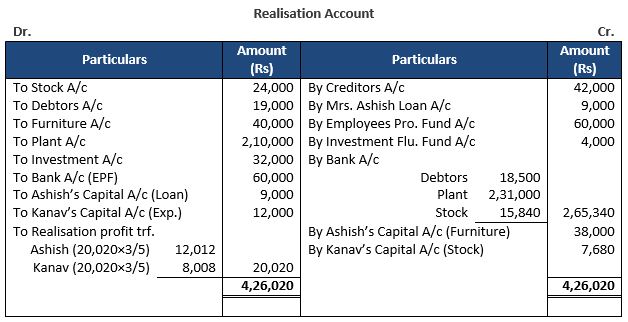

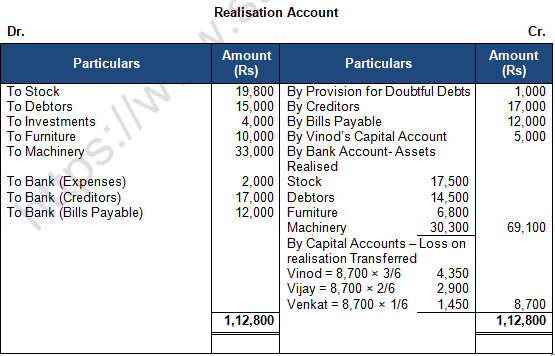

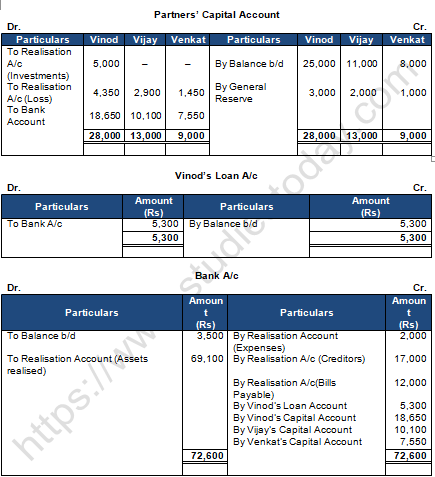

Question 22: Ashish and Kanav were partners in a firm sharing profits and losses in the ratio of 3 : 2. On 31st March, 2018 their Balance Sheet was as follows:

On the above date they decided to dissolve the firm.

(a) Ashish agreed to take over furniture at Rs. 38,000 and pay Mrs. Ashish’s Loan.

(b) Debtors realised Rs. 18,500 and Plant realised 10% more.

(c) Kanav took over 40% of the stock at 20% less than the book value. Remaining stock was sold at a gain of 10%.

(d) Trade creditors took over investments in full settlement.

(e) Kanav agreed to take over the responsibility of completing dissolution at an agreed remuneration of Rs. 12,000 and to bear realisation expenses. Actual expenses of realisation amounted to Rs. 8,000.

Prepare Realisation Account.

Answer 22:

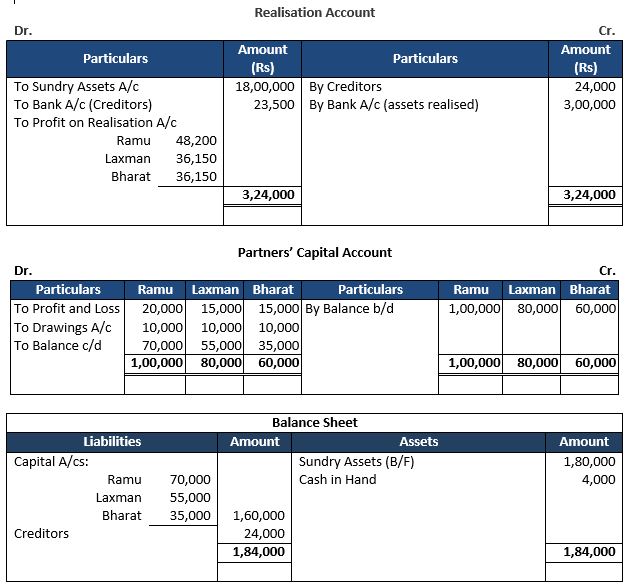

Question 23: Ramu, Laxman and Bharat started business on 1st April, 2021 with capitals of ₹ 1,00,000, ₹ 80,000 and ₹ 60,000 respectively sharing profits and losses in the ratio of 4:3:3. For the year ending 31st March, 2022, the firm incurred loss of ₹ 50,000. Each of the partners withdrew ₹ 10,000 during the year.

On 31st March, 2022 the firm was dissolved. The creditors of the firm stood at ₹ 24,000 on that date and cash in hand was ₹ 4,000. Assets realised ₹ 3,00,000 and creditors were paid ₹ 23,500 in settlement of their claims. Prepare Realisation Account and show your workings clearly.

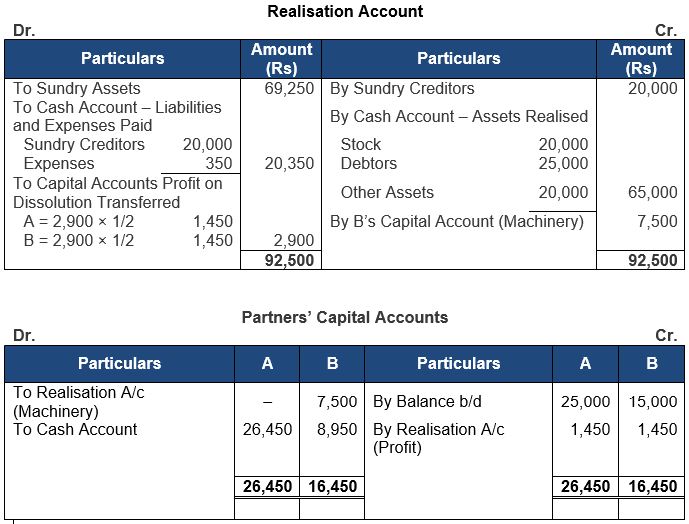

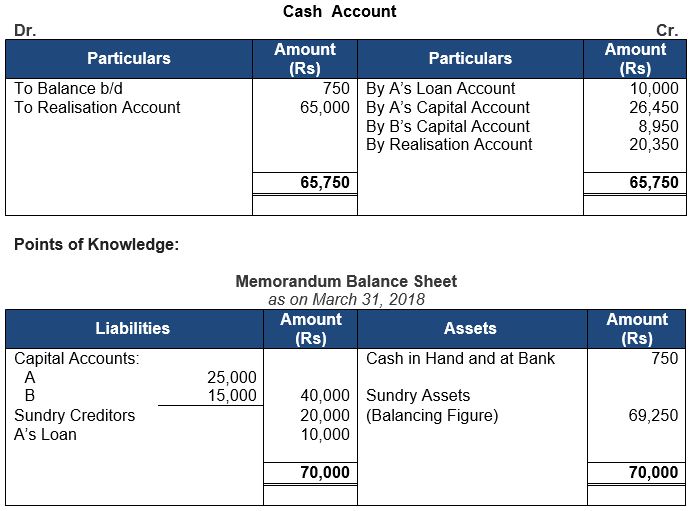

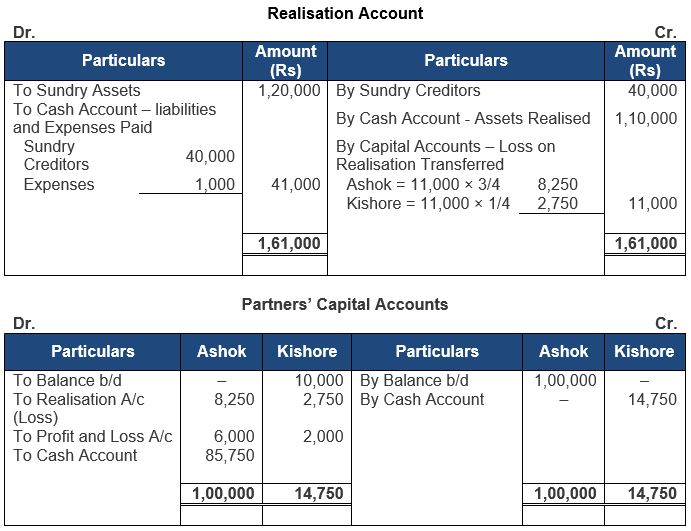

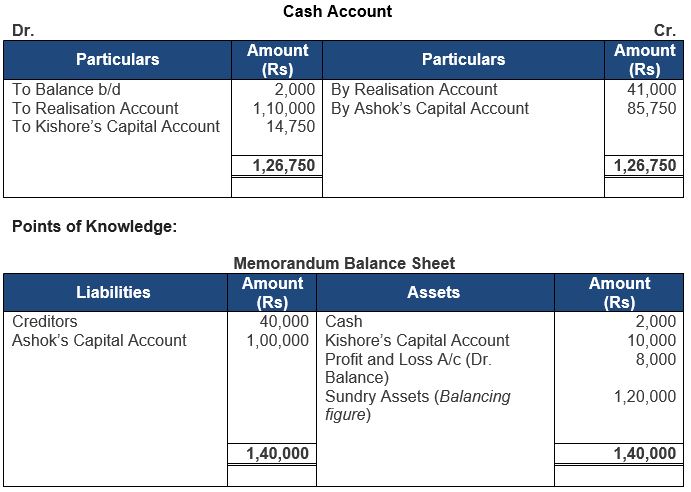

Answer 23:

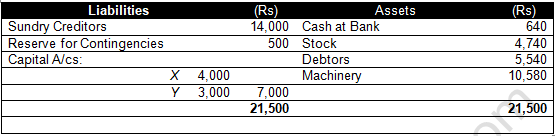

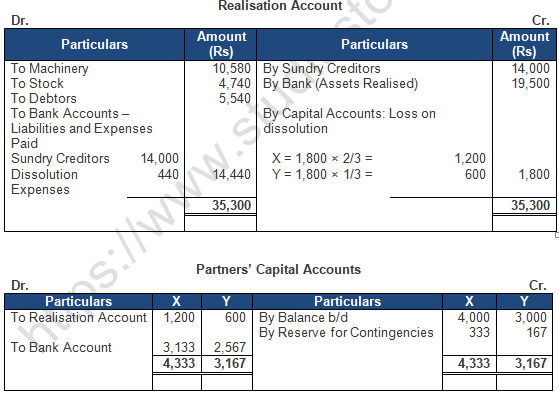

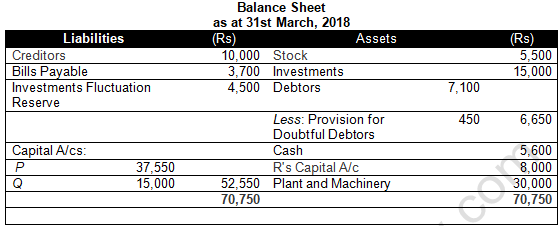

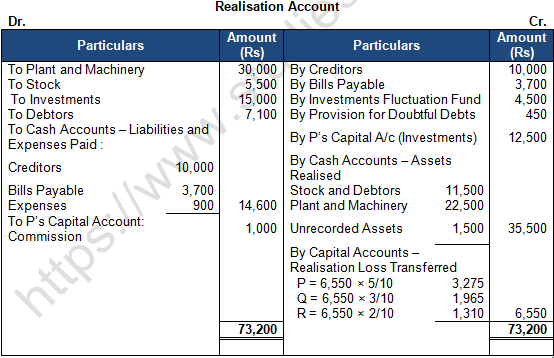

Question 24: A, B and C were partners sharing profits and losses in the ratio of 2:2:1. Their Balance Sheet as at 31st March, 2018 was as follows:

On the above date they dissolved the firm and following amounts were realised:

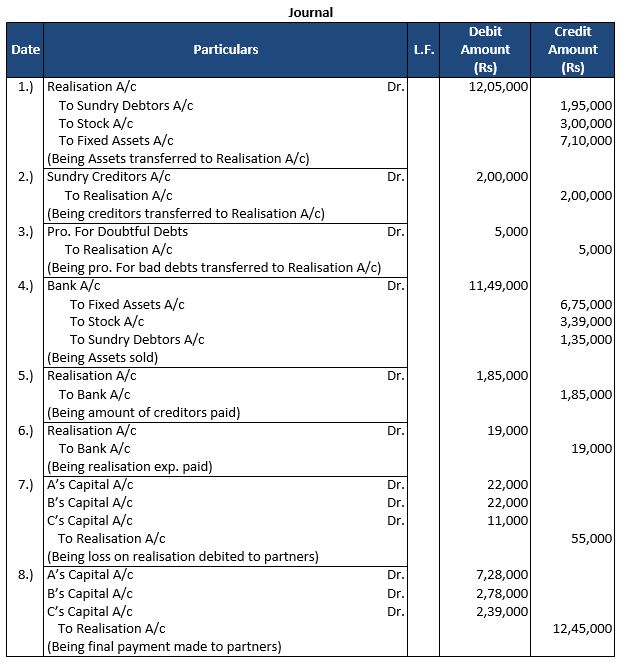

Fixed Assets Rs. 6,75,000; Stock Rs. 3,39,000; Debtors Rs. 1,35,000; Creditors were paid Rs. 1,85,000 in full settlement of their claim. Expenses on realisation amounted to Rs. 19,000.

Pass the necessary Journal entries on the dissolution of the firm.

Answer 24:

About Solution:-

When an unrecorded asset is taken over by a partner at an agreed value.

Partner’s Capital A/c Dr.

To Realisation A/c

(Unrecorded assets taken by partner)

Things to Remember:

When unrecorded liability has been discharged by the firm.

Realisation A/c Dr.

To Bank/Cash A/c

(Payment of unrecorded liabilities)

Important Notes:

When an unrecorded liability is discharged by a partner on behalf of the firm.

Realisation A/c Dr.

To Partner’s Capital A/c

(Unrecorded Liabilities payment by partner)

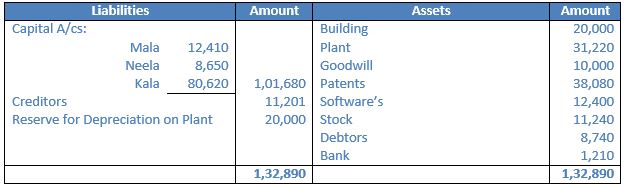

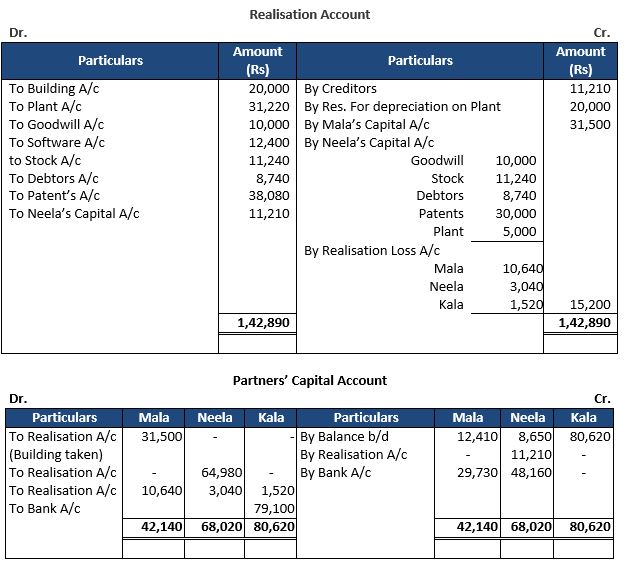

Question 25: Mala, Neela and Kala were in partnership sharing profits in the ratio of 7:2:1 and the Balance Sheet of the firm as at 31st March, 2024 was:

It was agreed to dissolve the partnership as on 31st March, 2024 and the terms of dissolution were-

(a) Mala to take over the Building at an agreed amount of Rs. 31,500.

(b) Neela, who was to carry on the business, to take over the Goodwill, Stock and Debtors at the book value, the partners at Rs. 30,000 and Plant at Rs. 5,000. He was also to pay the Creditors.

Show Ledger Accounts recording the dissolution in the books of the firm.

Answer 25:

About Solution:-

You have already studied that on the occasion of admission, retirement and death existing partnership comes to an end, but the business of the firm continues under a new agreement. When a firm decides to wind up its business operations under any of the circumstances mentioned, it stands dissolved. Dissolution of a partnership firm is different from the dissolution of a partnership.

Things to Remember:

Dissolution of a firm means that the firm closes its business and comes to an end. While dissolution of a partnership means termination of old partnership agreement and a reconstitution of firm due to admission, retirement and death of a partner. In dissolution of a partnership the remaining partners may agree to carry on the business under a new agreement.

Important Notes:

When the partners decide to discontinue the business of the firm, it becomes necessary to settle its accounts. For this purpose, it disposes off all its assets (except cash and bank balances) for satisfying all the claims against it. For this purpose a separate account called ‘Realisation Account’ is opened. Realisation Account is an account in which assets excluding cash in hand and bank are transferred at their book value and all external liabilities are transferred at their book value.

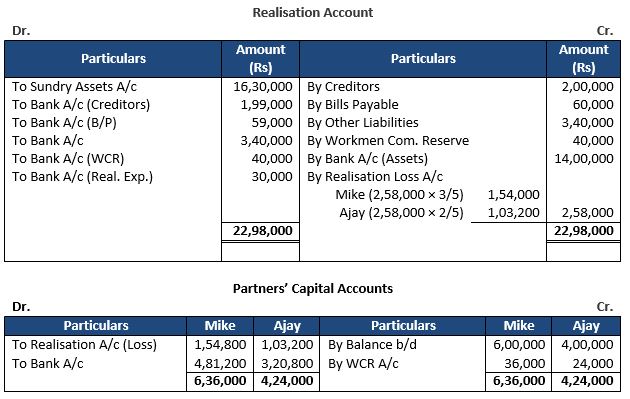

Question 26: Mike and Ajay are partners sharing profit and losses in ratio of the capitals. They decide to dissolve their firm on 31st March, 2024 the date on which the Balance Sheet stood as under:

Following additional information is given:

Sundry assets realised Rs. 14,00,000 and the liabilities were discharged as follows:

(i) Creditors due on 31st May, 2024 were paid at a discount of 3% per annum.

(ii) Bills Payable were discharged at a rebate of Rs. 1,000.

(iii) Workmen Compensation Claim of Rs. 40,000 was met.

(iv) Expenses of dissolution amounting to Rs. 30,000 were paid.

You are required to prepare:

(a) Realisation Account.

(b) Partners’ Capital Accounts.

Answer 26:

About Solution:-

1. Transferring all assets except Cash and Bank Account to the debit side of the account.

2. Amount realised on sale of assets is credited to the account.

Things to Remember:

Dissolution by Agreement: A firm is dissolved in case

1. All the partners give consent or

2. As per the terms partnership agreement.

Important Notes:

A firm is dissolved compulsorily in the following cases, when all the partners or all excepting one partner becomes insolvent or of unsound.

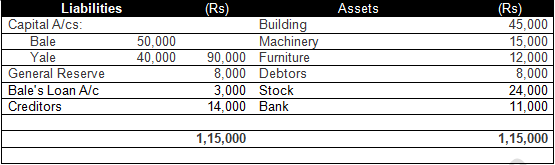

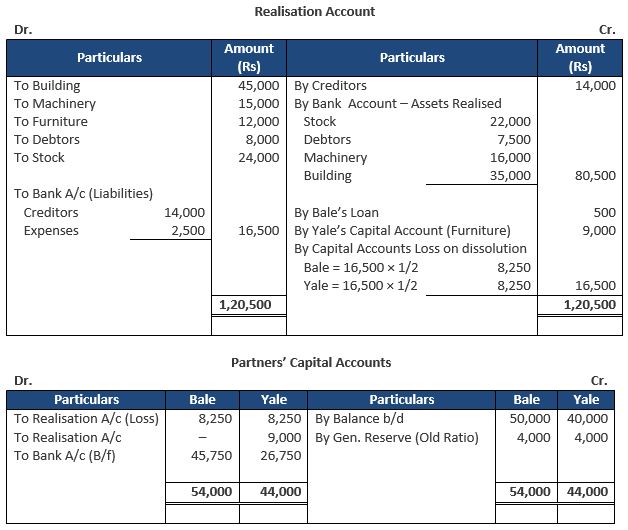

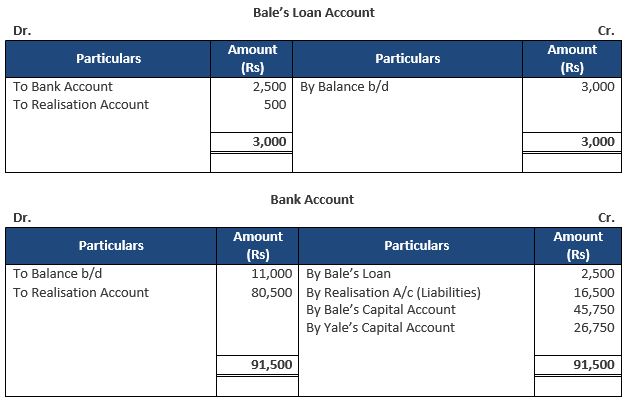

Question 27: Bale and Yale are equal partners of a firm. They decide to dissolve their partnership on 31st March, 2024 at which date their Balance Sheet stood as:

(a) The assets realised were:

Stock Rs 22,000; Debtors Rs 7,500; Machinery Rs 16,000; Building Rs 35,000.

(b) Yale took over the Furniture at Rs 9,000.

(c) Bale agreed to accept Rs 2,500 in full settlement of his Loan Account .

(d) Dissolution Expenses amounted to Rs 2,500.

Prepare the:

(i) Realisation Account; (ii) Capital Accounts of Partners;

(iii) Bale's Loan Account; (iv) Bank Account.

Answer 27:

About Solution:-

An event can make it unlawful for the firm to carry on its business. In such cases, it is compulsory for the firm to dissolve. However, if a firm carries on more than one undertakings and one of them becomes illegal, then it is not compulsory for the firm to dissolve. It can continue carrying out the legal undertakings. Section 41 of the Indian Partnership Act, 1932, specifies this type of voluntary dissolution.

Things to Remember:

On the happening of certain contingencies (Section 42):

According to Section 42 of the Indian Partnership Act, 1932, the happening of any of the following contingencies can lead to the dissolution of the firm:

1. Some firms are constituted for a fixed term. Such firms will dissolve on the expiry of that term.

2. Some firms are constituted to carry out one or more undertaking. Such firms are dissolved when the undertaking is completed.

3. Death of a partner.

4. Insolvency of a partner.

Important Notes:

By notice of partnership at will (Section 43):

According to Section 43 of the Indian Partnership Act, 1932, if the partnership is at will, then any partner can give notice in writing to all other partners informing them about his intention to dissolve the firm. In such cases, the firm is dissolved on the date mentioned in the notice. lf no date is mentioned, then the date of dissolution of the firm is the date of communication of the notice.

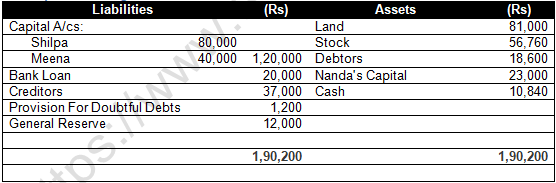

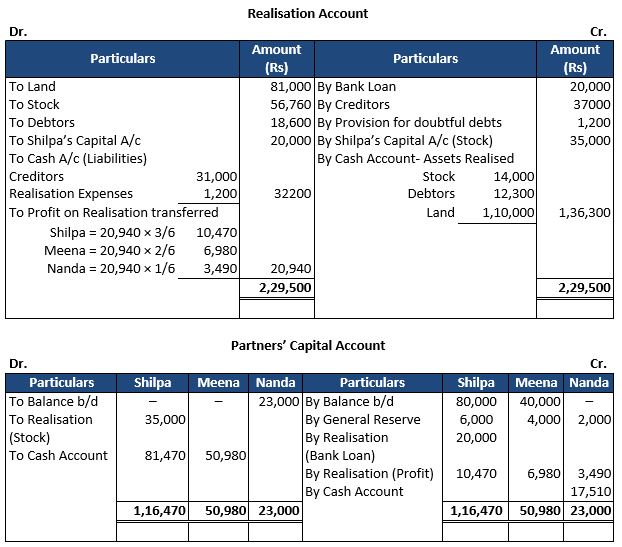

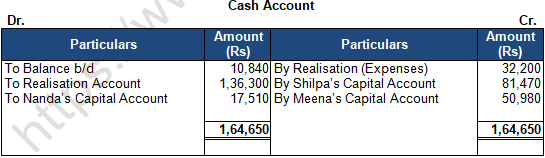

Question 28: Shilpa, Meena and Nanda decided to dissolve their partnership on 31st March, 2023. Their profit-sharing ratio was 3 : 2 : 1 and their Balance Sheet was as under:

It is agreed as follows:

The stock of value of Rs. 41,660 are taken over by Shilpa for Rs 35,000 and she agreed to discharge bank loan. The remaining stock was sold at Rs 14,000 and debtors amounting to Rs 10,000 realised Rs 8,000. Land is sold for Rs 1,10,000. The remaining debtors realised 50% at their book value. Cost of realisation amounted to Rs 1,200. There was a typewriter not recorded in the books worth of Rs 6,000 which were taken over by one of the Creditors at this value. Prepare Realisation Account, Partners' Capital Accounts, and Cash Account to close the books of the firm.

Answer 28:

About Solution:-

Dissolution of the Firm by the Court (Section 44):According to Section 44 of the Indian Partnership Act, 1932, the Court may dissolve a firm on the suit of a partner on any of the following grounds: Insanity/Unsound mind: If an active partner becomes insane or of an unsound mind, and other partners files a suit in the court, then the court may dissolve the firm.

Things to Remember:

Permanent Incapability: If a partner becomes permanently incapable of performing his duties as a partner, and other partners file a suit in the court, then the court may dissolve the firm. Also, the incapacity may arise from a physical disability, illness etc.

Important Notes:

Misconduct: When a partner is guilty of conduct which is likely to affect prejudicially the carrying on of the business and the other partners file a suit in the court, then the court may dissolve the firm. Further, it is not important that the misconduct is related to the conduct of the business. The court looks at the effect of the misconduct on the business along with the nature of the business.

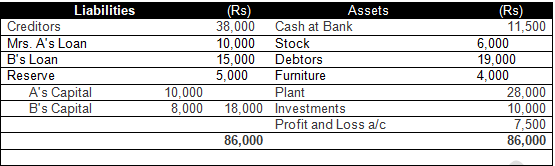

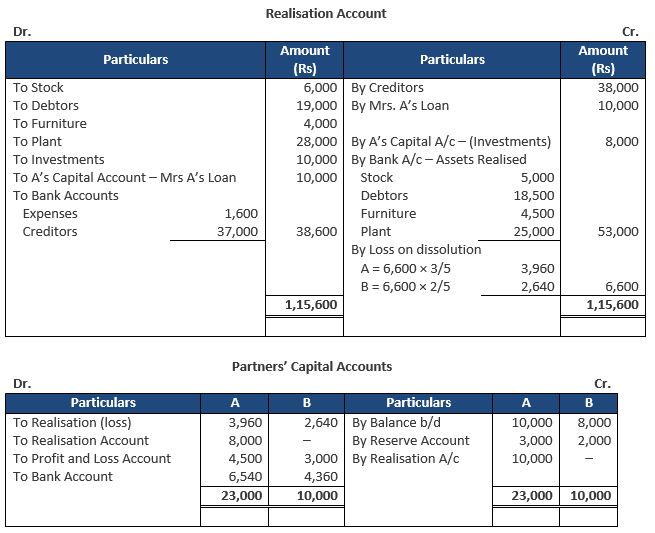

Question 29: A and B are partners in a firm sharing profits and losses in the ratio of 3:2. On 31st March, 2023, their Balance Sheet was as follows:

The firm was dissolved on 31st March, 2023 and both the partners agreed to the following:

(a) A took Investments at an agreed value of Rs 8,000. He also agreed to settle Mrs. A's Loan.

(b) Other assets realised as: Stock——Rs 5,000; Debtors——Rs 18,500; Furniture——Rs 4,500; Plant——Rs 25,000.

(c) Expenses of realisation came to Rs 1,600.

(d) Creditors agreed to accept Rs 37,000 in full settlement of their claims.

Prepare Realisation Account, Partners' Capital Accounts and Bank Account.

Answer 29:

About Solution:-

Persistent Breach of the Agreement: A partner may fully or persistently commit a breach of the agreement relating to:

1. The management of the affairs of the firm, or

2. A reasonable conduct of its business,

3. Conduct himself in matters relating to business that is not reasonably practicable for other partners to carry on the business in partnership with him.

Things to Remember:

The term dissolution means coming to an end or discontinuation. The dissolution of the firm implies a complete breakdown of the partnership relation among all the partners. Dissolution of the partnership (owing to retirement, death or insolvency of a partner), merely involves change in the relation of the partners but it does not end the firm; the partnership would certainly come to an end but the firm, the reconstituted one might continue under the same name.

Important Notes:

The dissolution of the partnership may or may not include the dissolution of the firm but the dissolution of the firm necessarily means the dissolution of the partnership. On dissolution of the firm, the business of the firm ceases to exist since its affairs are wound up by selling the assets and by paying the liabilities and discharging the claims of the partners. The dissolution of partnership among all partners of a firm is called dissolution of the firm.

Question 30: Balance Sheet of P, Q and R as at 31st March, 2024, who were sharing profits in the ratio 5:3:1, was:

The partners dissolved the firm. Assets realised – Stock Rs. 23,400; Debtors 50%; Building and Plant and Machinery 10% less than book value. Creditors were settled for Rs. 32,000. There was an Outstanding Bill of electricity Rs. 800 which was paid. Realisation expenses Rs. 1,250 were also paid.

Prepare Realisation Account, Partners Capital Account and Bank Account.

Answer 30:

About Solution:-

Assets account is closed by transferring it to the Realisation Account at its Book Value.

Realisation A/c Dr.

To Assets A/c

(Transfer of assets)

Things to Remember:

It is to be noted that the following items on the assets side of the Balance Sheet are not transferred to the Realisation Account:

(i) Undistributed loss (i.e. Debit Balance of Profits and Loss account).

(ii) Fictitious assets or deferred revenue expenditures such as preliminary expenses.

Important Notes:

All the above items are closed by transferring them to the partners’ Capital Account in their profit sharing ratio. The Journal entry is made:

Partner’s capital A/c Dr. (Individually)

To Profit & Loss A/c

To Fictitious Assets A/c

(Transfer of loss and fictitious Assets)

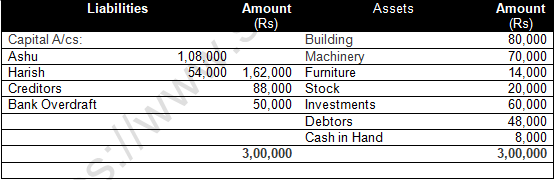

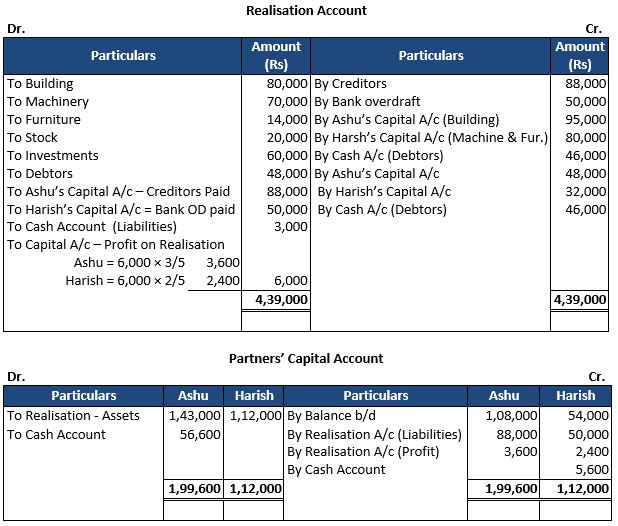

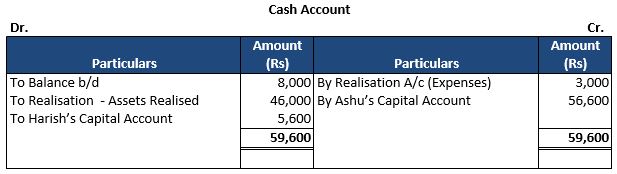

Question 31: Ashu and Harish are partners sharing profits and losses as 3 : 2 . They decided to dissolve the firm on 31st March, 2023. Their Balance Sheet on the above date was:

Ashu is to take over the building at Rs. 95,000 and Machinery and Furniture is taken over by Harish at value of Rs. 80,000. Ashu agreed to pay Creditor and Harish agreed to meet Bank overdraft. Stock and Investments are taken by both Partners in profit-sharing ratio. Debtors realised for Rs. 46,000, expenses of realisation amounted to Rs. 3,000. Prepare necessary Ledger Accounts.

Answer 31:

About Solution:-

Provisions and reserves against assets should be closed by crediting the Realisation Account. The Journal entry is made:

Provision for Doubtful Debts A/c Dr.

Provision for Depreciation A/c Dr.

Any other Provision A/c Dr.

To Realisation A/c

(Transfer of provision on assets)

Things to Remember:

The accounts of various external liabilities are closed by transferring them to the Realisation Account. The loan given to the firm by a partner’s wife is treated as an external liability and is transferred to the credit of Realisation Account.

Important Notes:

The relevant Journal entry is as under:

External Liabilities A/c Dr. (Individually)

To Realisation A/c (Transfer of external liability)

Capital and Loan account of the partners’ are treated separately and so are not transferred to the Realisation Account.

Question 32: A, B and C were equal partners. On 31st March, 2023, their Balance Sheet stood as:

The firm was dissolved on the above date on the following terms:

(a) For the purpose of dissolution, Investments were valued at Rs 18,000 and A took over the Investments at this value.

(b) Fixed Assets realised Rs 29,700 whereas Stock and Debtors realised Rs 80,000.

(c) Expenses of realisation amounted to Rs 1,300.

(d) Creditors allowed a discount of Rs 800.

(e) One Bill receivable for Rs 1,500 under discount was dishonoured as the acceptor had become insolvent and was unable to pay anything and hence the bill had to be met by the firm.

Prepare Realisation Account, Partner's Capital Accounts and Cash Account showing how the accounts would finally be settled among the partners.

Answer 32:

About Solution:-

Any balance of accumulated reserves (e.g. general reserves), Profit and Loss Account (Cr.), Reserve Fund and other reserves on the date of dissolution will be credited to the Partners’ Capital accounts on the basis of profit sharing ratio.

Things to Remember:

Journal entry will be recorded:

Profit and Loss A/c Dr.

General Reserve A/c Dr.

Any Other Fund Dr.

To Partners’ Capital A/c (Individually)

(Transfer of profit and reserve)

Important Notes:

For Sale of Assets (for cash) journal entry will be:-

Bank/ Cash A/c Dr. (Realised Value)

To Realisation A/c (Sale of assets)

Question 33: A, B and C are in partnership sharing profits and losses in the proportions of 1/2, 1/3 and 1/6 respectively. On 31st March, 2024, they decided to dissolve the partnership and the position of the firm on this date is represented by the following Balance Sheet:

During the realisation process, a liability under a suit for damages is settled at Rs 20,000 as against Rs 5,000 only provided for in the books of the firm. Land and Building were sold for Rs 40,000 and the Stock and Sundry Debtors realised Rs 30,000 and Rs 42,000 respectively. The expenses of realisation amounted to Rs 1,200.

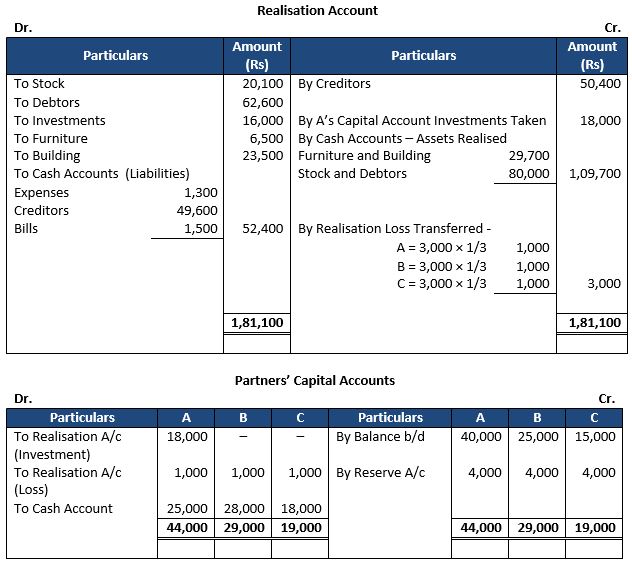

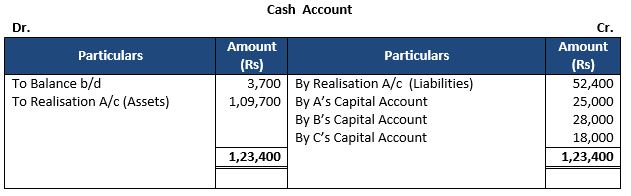

There was a car in the firm, which was completely written off from the books. It was taken over by A for Rs 20,000. He also agreed to pay Outstanding Salary of Rs 20,000 not provided in books. Prepare Realisation Account, Partners' Capital Accounts and Bank Account in the books of the firm.

Answer 33:

About Solution:-

Settlement of loans given by the Partner

Partners’ Loan A/c Dr.

To Bank/Cash/Partners’ capital A/c

(Settlement of loan given by the partner)

Things to Remember:

Payment of Liabilities by the Partner(s)

Realisation A/c Dr.

To Partner Capital A/c

(Liabilities taken over by partner)

Important Notes:

For Transfer of Liabilities: The accounts of various external liabilities are closed by transferring them to the Realisation Account. The loan given to the firm by a partner’s wife is treated as an external liability and is transferred to the credit of Realisation Account. The relevant Journal entry is as under:

External Liabilities A/c Dr. (Individually)

To Realisation A/c

(Transfer of external liability)

Capital and Loan account of the partners’ are treated separately and so are not transferred to the Realisation Account.

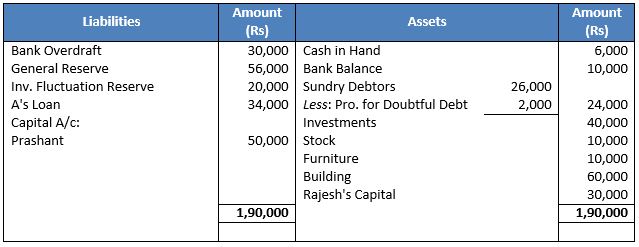

Question 34: Prashant and Rajesh are partners in a firm sharing profits and losses in the ratio of 3:2. On 31st March, 2024, their Balance Sheet was:

On that date, the partners decide to dissolve the firm. A took over Investments at an agreed value of Rs. 35,000. Other assets were realised as follows:

Sundry Debtors: Full amount. The firm could realise Stock at 15% less and Building was sold at Rs. 1,00,000.

Compensation to employees paid by the firm was Rs. 10,000. This liability was not provided for in the above Balance Sheet.

You are required to close the books of the firm by preparing Realisation Account, Partners' Capital Accounts and Bank Account.

Answer 34:

About Solution:-

Sometimes, there may be some assets that have already been written off completely in previous years and thus, do not appear in the Balance Sheet but physically they still exist for operational purposes. For example, there is an old computer, which is still in working condition though its book value is zero. Similarly, there may be some liabilities, which do not appear in the Balance Sheet, but actually they are still there. For example, a bill discounted with bank, on dissolution it was dishonoured and had to be taken up by the firm for payment purposes.

Things to Remember:

It is to be kept in mind that an unrecorded asset would never be transferred to the debit of the Realisation Account, because the amount realised from its sale is in nature of a gain and the Realization Account is only credited accordingly. Similarly, an unrecorded liability need not be transferred to Realisation.

Important Notes:

When the amount realised from the sale of an unrecorded asset.

Cash/Bank A/c Dr.

To Realisation A/c

(Sale of unrecorded assets)

Question 35: Yogesh and Naresh were partners sharing profit equally. They dissolved the firm on 1st April, 2019. Naresh was assigned the responsibility to realise the assets and pay the liabilities at a remuneration of Rs. 10,000 including expenses. Balance Sheet of the firm as on that date was as follows:

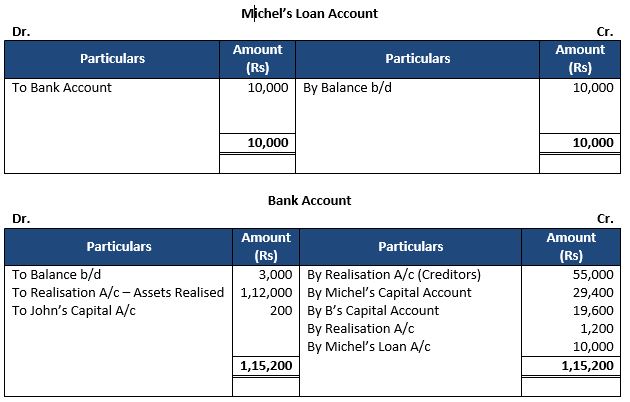

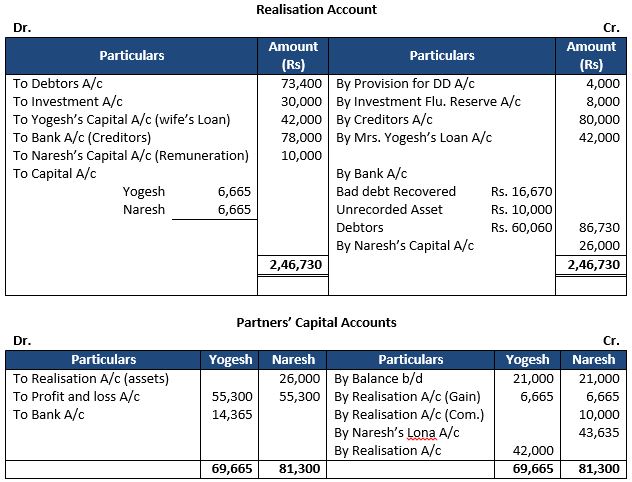

The firm was dissolved on following terms:

(a) Yogesh was to pay his wife’s loan.

(b) Debtors realised Rs. 60,060.

(c) Naresh was to take investment at an agreed value of Rs. 26,000.

(d) Creditors were payable after two months but were paid immediately at a discount of 15% p.a.

(e) A Debtors previously written off as Bad Debts paid Rs. 16,670.

(f) An unrecorded asset realised Rs. 10,000.

Prepare Realisation Account, Partner’s Capital Account, Partner’s Loan Account and Cash/ Bank Account.

Answer 35:

Working Note:-

Payment of Creditors:-

Discount = Rs. 80,000 × 15% × 2/12

Discount = Rs. 2,000

Final Payment = Rs. 80,000 – Rs. 2,000

Final Payment = Rs. 78,000

About Solution:-

Treatment of Accumulated Reserves and Profit/Loss: Any balance of accumulated reserves (e.g. general reserves), Profit and Loss Account (Cr.), Reserve Fund and other reserves on the date of dissolution will be credited to the Partners’ Capital accounts on the basis of profit sharing ratio. The following journal entry will be recorded:

Profit and Loss A/c Dr.

General Reserve A/c Dr.

Any Other Fund Dr.

To Partners’ Capital A/c (Individually)

(Transfer of profit and reserve)

Things to Remember:

For Sale of Assets (for cash)

Bank/ Cash A/c Dr. (Realised Value)

To Realisation A/c

(Sale of assets)

Important Notes:

For Assets taken Over by the Partner:-

(a) Partners’ Capital A/c Dr.

To Realisation A/c (Agreed Price)

(Assets taken over by partner)

(b) Bank/Cash/Partners capital A/c Dr.

To Partner’s Loan A/c

(Settlement of loan to a partner)

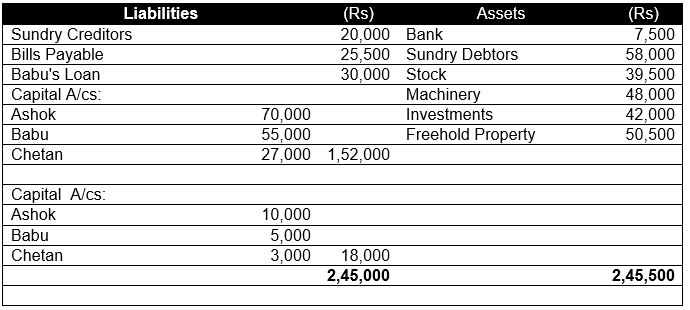

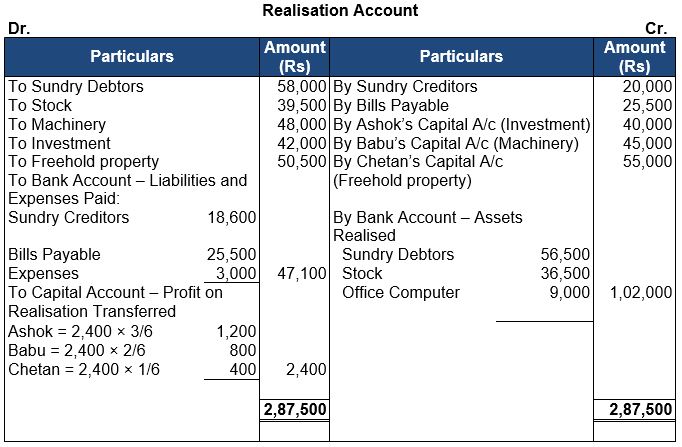

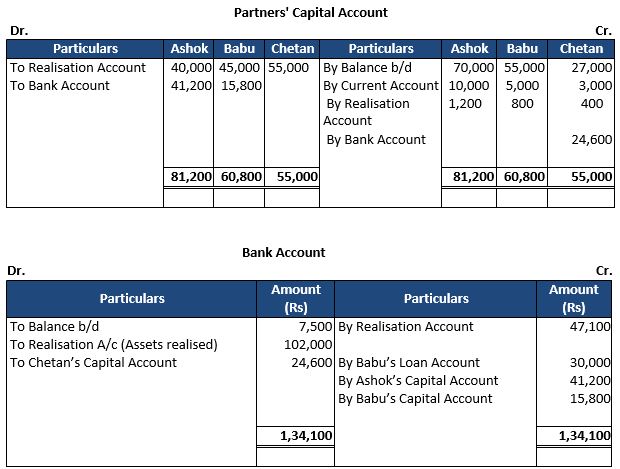

Question 36: Ashok, Babu and Chetan are in partnership sharing profit in the proportion of 1/2, 1/3, 1/6 respectively. They dissolve the partnership of the 31st March, 2024 when the Balance Sheet of the firm as under:

The Machinery was taken over by Babu for Rs 45,000, Ashok took over the Investments for Rs 40,000 and Freehold property took over by Chetan at Rs 55,000. The remaining Assets realised as follows:

Sundry Debtors Rs 56,500 and Stock Rs 36,500. Sundry Creditors were settled at discount of 7%. A office computer, not shown in the books of accounts realised Rs 9,000. Realisation expenses amounted to Rs 3,000.

Prepare Realisation Account, Partners' Capital Accounts and Bank Account.

Answer 36:

About Solution:-

When an unrecorded asset is taken over by a partner at an agreed value.

Partner’s Capital A/c Dr.

To Realisation A/c

(Unrecorded assets taken by partner)

Things to Remember:

When unrecorded liability has been discharged by the firm.

Realisation A/c Dr.

To Bank/Cash A/c

(Payment of unrecorded liabilities)

Important Notes:

When an unrecorded liability is discharged by a partner on behalf of the firm.

Realisation A/c Dr.

To Partner’s Capital A/c

(Unrecorded Liabilities payment by partner)

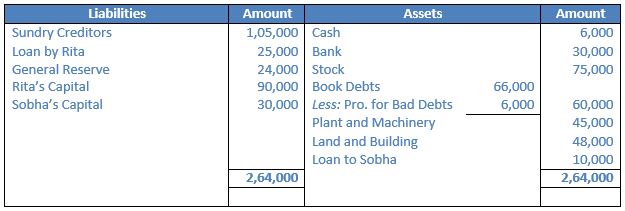

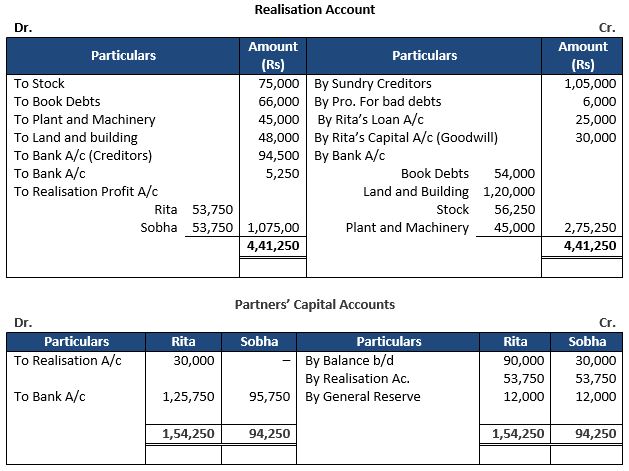

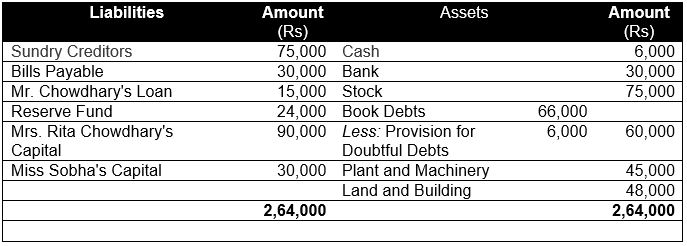

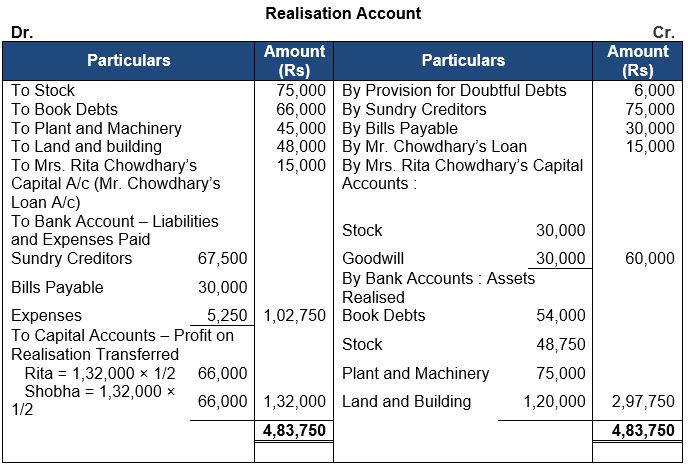

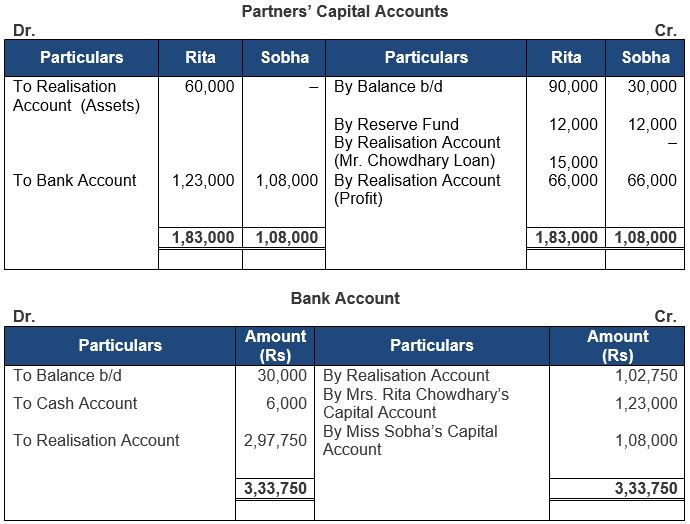

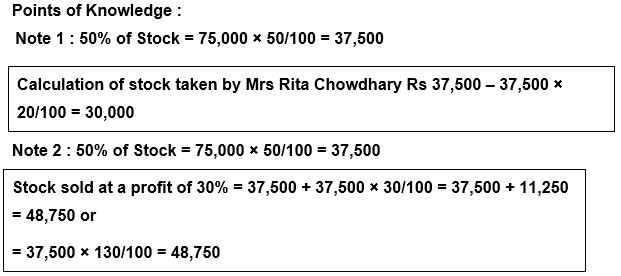

Question 37: Rita and Sobha are partners in a firm, Fancy Garments Exports, sharing profits and losses equally. On 1st April, 2024, the Balance Sheet of the firm was:

The firm was dissolved on the date given above. The following transactions took place:

(a) Rita took 25% of the Stock at a discount of 20% in settlement of her loan.

(b) Sundry Debtors realised Rs. 54,000.

(c) Sundry Creditors were paid at a discount of 10%.

(d) Land and Building realised Rs. 1,20,000.

(e) Rita took over the goodwill of the firm at a value of Rs 30,000.

(f) An unrecorded asset of Rs 6,900 was handed over to an unrecorded liability of Rs 6,000 in full settlement.

(g) Realisation expenses were Rs 5,250.

Show Realisation Account, Partners' Capital Accounts and Bank Account in the books of the firm.

Answer 37:

About Solution:-

You have already studied that on the occasion of admission, retirement and death existing partnership comes to an end, but the business of the firm continues under a new agreement. When a firm decides to wind up its business operations under any of the circumstances mentioned, it stands dissolved. Dissolution of a partnership firm is different from the dissolution of a partnership.

Things to Remember:

Dissolution of a firm means that the firm closes its business and comes to an end. While dissolution of a partnership means termination of old partnership agreement and a reconstitution of firm due to admission, retirement and death of a partner. In dissolution of a partnership the remaining partners may agree to carry on the business under a new agreement.

Important Notes:

When the partners decide to discontinue the business of the firm, it becomes necessary to settle its accounts. For this purpose, it disposes off all its assets (except cash and bank balances) for satisfying all the claims against it. For this purpose a separate account called ‘Realisation Account’ is opened. Realisation Account is an account in which assets excluding cash in hand and bank are transferred at their book value and all external liabilities are transferred at their book value

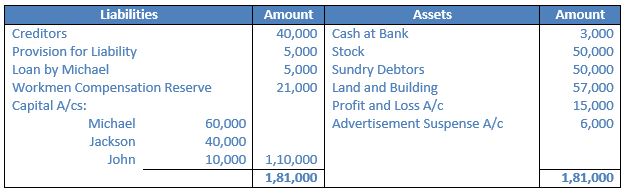

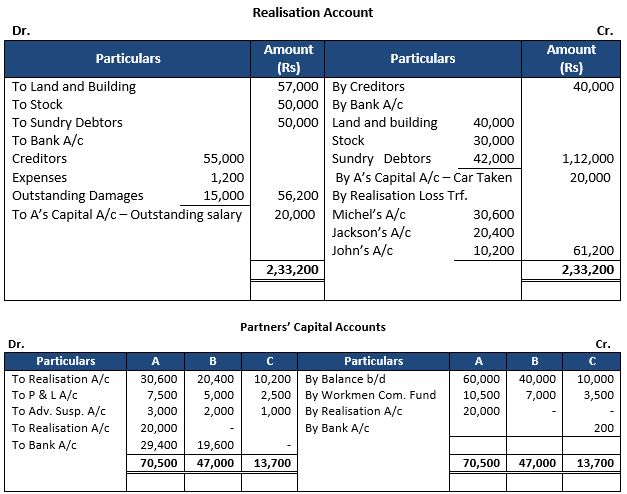

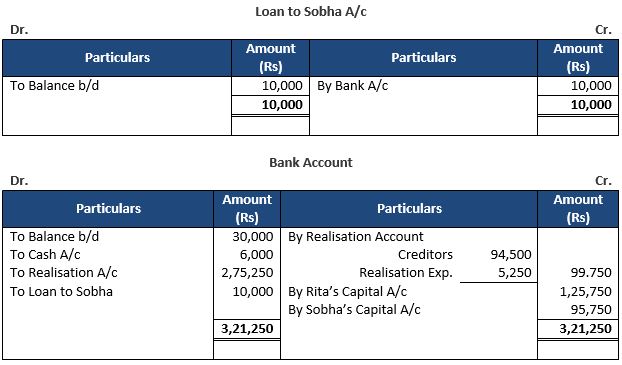

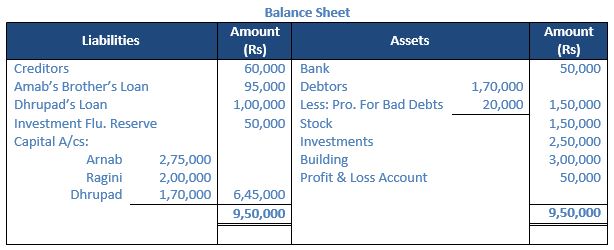

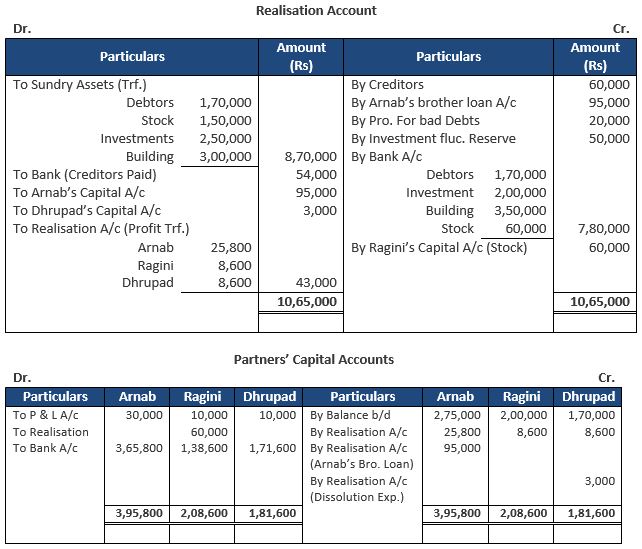

Question 38: Arnab, Ragini and Dhrupad are partners sharing profits in the ratio of 3:1:1. Last year, conflicts arose due to certain issues of disagreements and on 31st March, 2023, they decided to dissolved the firm. On that date their Balance sheet was as under:

The assets were realised and the liabilities were paid as under:

(i) Arnab agreed to pay his brother’s Loan.

(ii) Investments realised 20% less.

(iii) Creditors were paid at 10% less.

(iv) Building was auctioned for Rs. 3,55,000. Commission on auction was Rs. 5,000.

(v) 50% of the stock was taken over by Ragini at market price which was 20% less than the book value and the remaining was sold at market price.

(vi) Dissolution expenses were Rs. 8,000. Rs. 3,000 were to borne by the firm and the balance by Dhrupad. The expenses were paid by him.

Prepare Realisation Account and Partners’ Capital Accounts

Answer 38:

About Solution:-

Tangible Assets will be assumed to have realised at the book value i.e. the value stated in the Balance Sheet. Examples of tangible assets are: Cash, Bank, Land and Building, Plant and Machinery, Vehicles, Furniture and Fixtures, Computer, tools, Sundry Assets, Investments, Stock, Debtors etc.

Things to Remember:

Intangible Assets will have assumed to have realised at no value. Intangible Assets include the following assets: Goodwill, Patents, Trade Marks, Computer Software, Prepaid Expenses, Deferred Revenue Expenditure such as Advertisement Suspense A/c

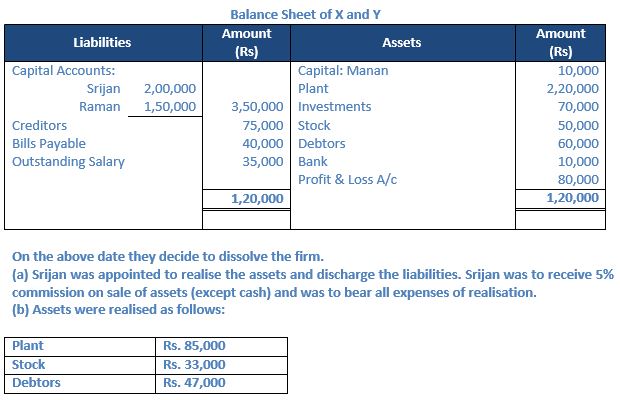

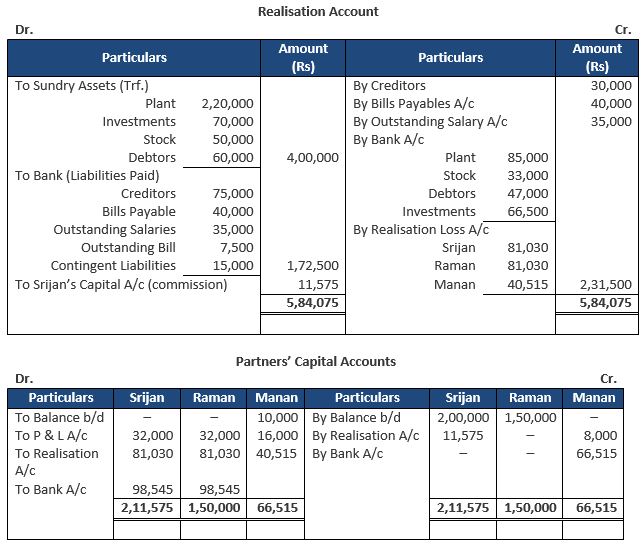

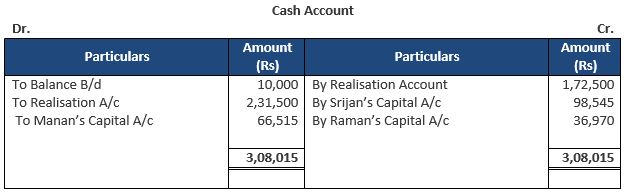

Question 39: Srijan, Raman and Manan were partners in a firm sharing profits and losses in the ratio of 2:2:1. On 31st March, 2017 their Balance sheet was as follows

(c) Investments were realised at 95% of the book value.

(d) The firm had pay Rs. 7,500 for an outstanding repair bill not provided for earlier.

(e) A contingent liability in respect of bills receivable discounted with the bank had also materialised and had to be discharged for Rs. 15,000.

(f) Expenses of realisation amounting to Rs. 3,000 were paid by Srijan.

Prepare Realisation Account, Partners’ Capital Accounts and Bank Account.

Answer 39:

About Solution:-

The balance in the realisation account would show either profit or loss on dissolution. If the total of the credit side is more than the debit side, then there is a profit and following journal entry is made: Realisation A/c Dr. (Individually)

To Partner’s Capital/ Current A/c (Individually)

(Profit on realisation transferred to capital accounts)

Things to Remember:

The debit side is more than credit side, then there is a loss on dissolution and following journal entry is made:

Partner’s Capital/Current A/c Dr. (Individually)

To Realisation A/c

(Loss on realisation transferred to capital account)

Important Notes:

After all the adjustments related to partners’ capital accounts and transfer of profit or loss on realisation to the partners’ capital accounts, the capital accounts are closed in the following manner: (a) If the Partner’s Capital Account shows a debit balance, the partner has to bring the necessary amount of cash. The following journal entry is made:

Bank/Cash A/c Dr.

To Partner’s Capital A/c

(Cash brought by the partner)

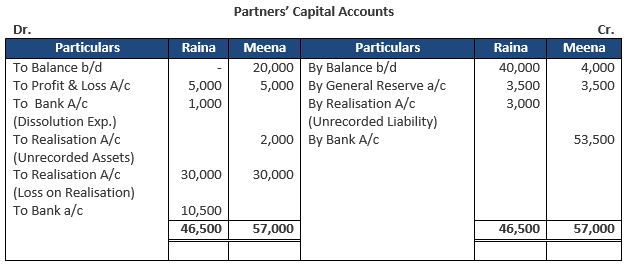

Question 40: Raina and Meenu were partners in a firm which they dissolved on 31st March, 2023. On this date, Balance Sheet of the firm, apart from realisable assets and outside liabilities showed the following:

On the date of dissolution of the firm:

(a) Raina’s loan was repaid by the firm along with interest of ₹ 500.

(b) Dissolution expenses of ₹ 1,000 were paid by the firm on behalf of Raina.

(c) An unrecorded asset of ₹ 2,000 was taken by Meena while Raina paid an unrecorded liability of ₹ 3,000.

(d) Dissolution resulted in a loss of ₹ 60,000 from the realisation of assets and settlement of liabilities.

You are required to prepare Partner’s Capital Accounts.

Answer 40:

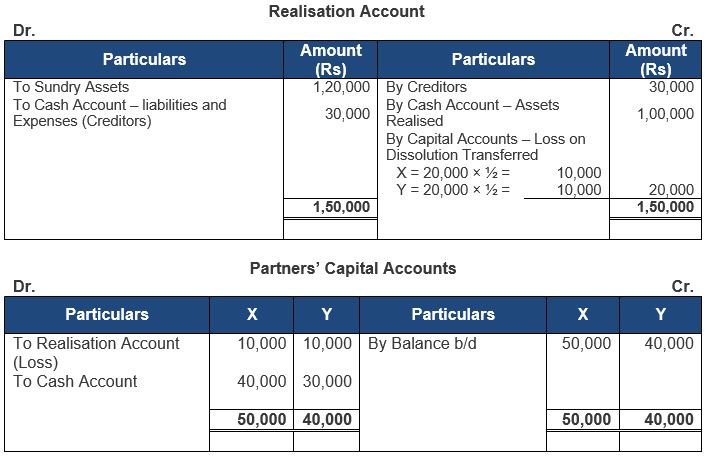

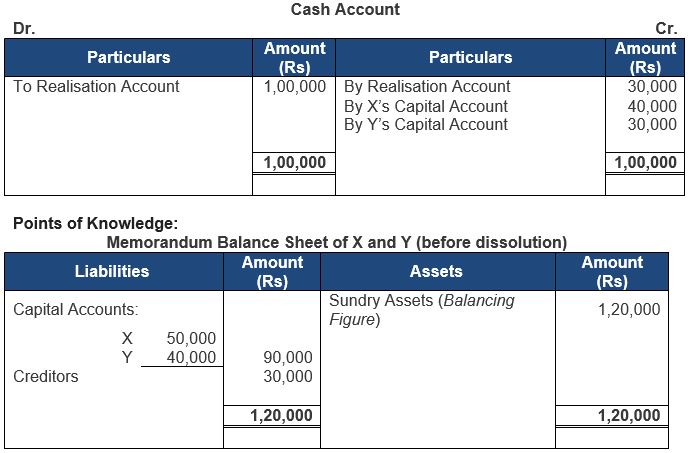

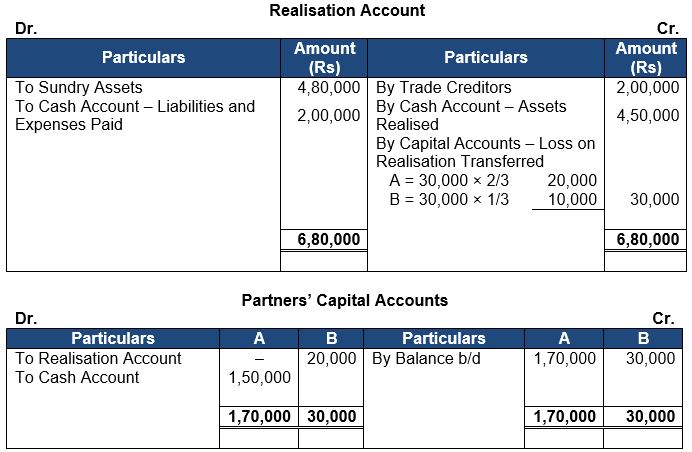

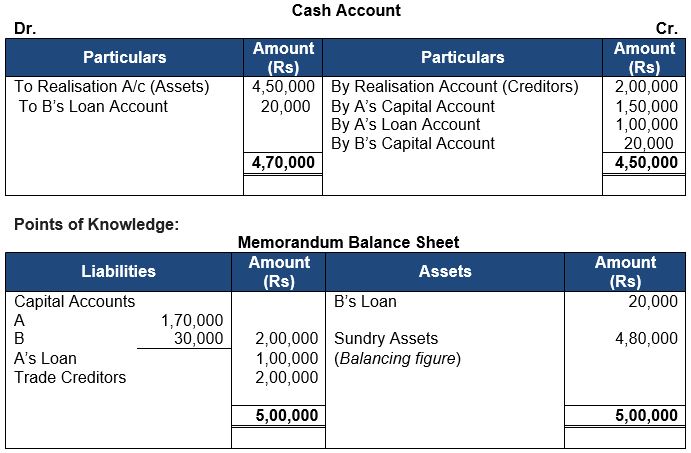

Question 41: There are two partners X and Y in a firm and their capitals are Rs. 50,000 and Rs. 40,000. The creditors are Rs. 30,000. The assets of the firm realise Rs. 1,00,000. How much will X and Y received?

Answer 41:

About Solution:-

When an unrecorded asset is taken over by a partner at an agreed value.

Partner’s Capital A/c Dr.

To Realisation A/c

(Unrecorded assets taken by partner)

Things to Remember:

When unrecorded liability has been discharged by the firm.

Realisation A/c Dr.

To Bank/Cash A/c

(Payment of unrecorded liabilities)

Important Notes:

When an unrecorded liability is discharged by a partner on behalf of the firm.

Realisation A/c Dr.

To Partner’s Capital A/c

(Unrecorded Liabilities payment by partner)

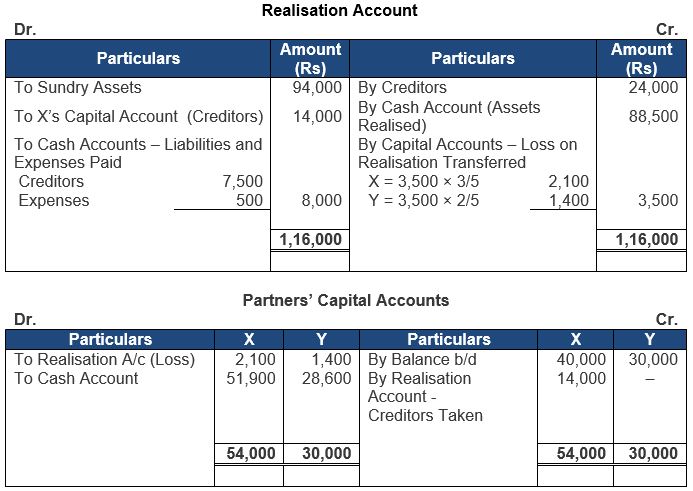

Question 42: A, B and C were partners sharing profits in the ratio of 5:3:2. On 31st March, 2023, A's Capital and B's Capital were Rs. 30,000 and Rs. 20,000 respectively but C owed Rs. 5,000 to the firm. The liabilities were Rs. 20,000.The assets of the firm realised Rs. 50,000.

Prepare Realisation Account, Partner's Capital Accounts and Bank Account.

Answer 42:

About Solution:-

An event can make it unlawful for the firm to carry on its business. In such cases, it is compulsory for the firm to dissolve. However, if a firm carries on more than one undertakings and one of them becomes illegal, then it is not compulsory for the firm to dissolve. It can continue carrying out the legal undertakings. Section 41 of the Indian Partnership Act, 1932, specifies this type of voluntary dissolution.

Things to Remember:

On the happening of certain contingencies (Section 42):

According to Section 42 of the Indian Partnership Act, 1932, the happening of any of the following contingencies can lead to the dissolution of the firm:

1. Some firms are constituted for a fixed term. Such firms will dissolve on the expiry of that term.

2. Some firms are constituted to carry out one or more undertaking. Such firms are dissolved when the undertaking is completed.

3. Death of a partner.

4. Insolvency of a partner.

Important Notes:

By notice of partnership at will (Section 43):

According to Section 43 of the Indian Partnership Act, 1932, if the partnership is at will, then any partner can give notice in writing to all other partners informing them about his intention to dissolve the firm. In such cases, the firm is dissolved on the date mentioned in the notice. lf no date is mentioned, then the date of dissolution of the firm is the date of communication of the notice.

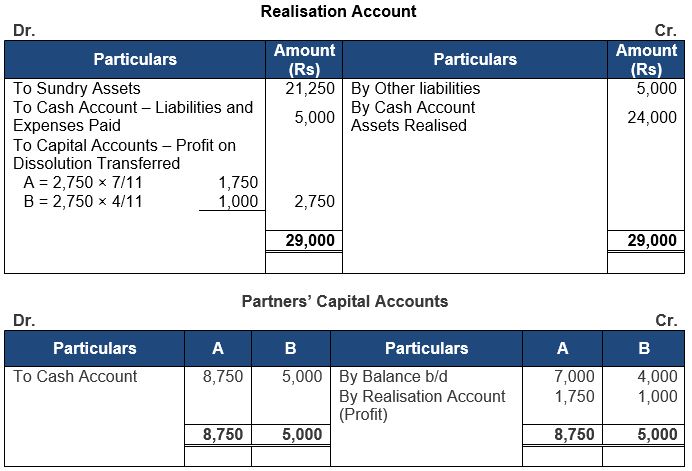

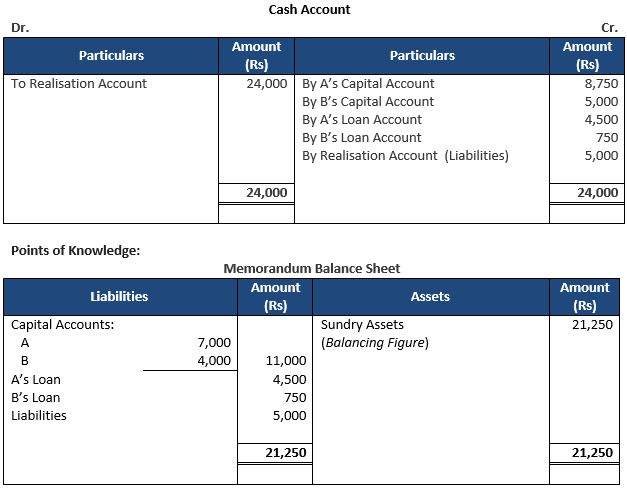

Question 43: A and B were partners sharing profits and losses as to 7/11th to A and 4/11th to B. They dissolved the partnership on 30th May, 2023. As on that date their capitals were: A Rs. 7,000 and B Rs. 4,000. There were also due on Loan A/c to A Rs. 4,500 and to B Rs. 750. The other liabilities amounted to Rs 5,000. The assets proved to have been undervalued in the last Balance Sheet and actually realised Rs. 24,000.

Prepare necessary accounts showing the final settlement between partners.

Answer 43:

About Solution:-

When Realization Exp. are paid by the firm on its own behalf Realization Account Dr.

To Bank/Cash Account

Things to Remember:

When Realization Exp. are paid by the partner On Firm's behalf Realization Account Dr.

To Partner's Capital/Current A/c

(Concerned Partner's Capital/Current Account)

Important Notes:

When Realization Exp. are paid by the firm on behalf of a partner who has to bear such Exp.

Partner's Capital/Current Account Dr.

To Bank/Cash Account

Question 44: A, B and C started business on 1st April, 2022 with capitals of Rs. 1,00,000; Rs. 80,000 and Rs. 60,000 respectively sharing profits (losses) in the ratio of 4:3:3. For the year ended 31st March, 2023, the firm suffered a loss of Rs. 50,000. Each of the partners withdrew Rs 10,000 during the year.

On 31st March, 2023, the firm was dissolved, the creditors of the firm stood at Rs. 24,000 on that date and Cash in Hand was Rs. 4,000. The assets realised Rs. 3,00,000 and Creditors were paid Rs 23,500 in full settlement of their claims.

Prepare Realisation Account and show your workings clearly.

Answer 44:

About Solution:-

All outside liabilities are transferred to Realization Account.

Things to Remember:

Items on the liability side of Balance Sheet i.e. Accumulated Profits and Reserves are transferred to Partner’s Capital Account.

Important Notes:

Loan from a relative or spouse of a partner is an external liability and will be transferred to Realization Account.

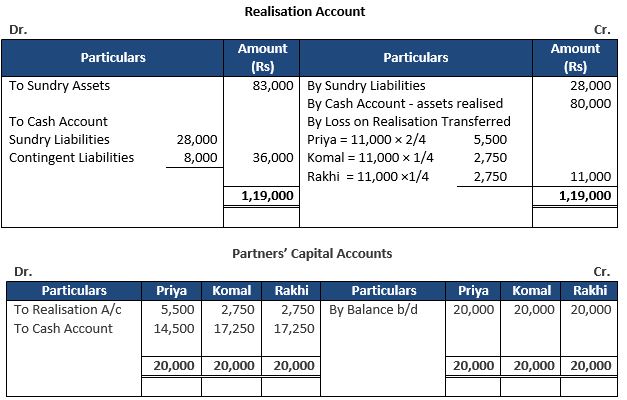

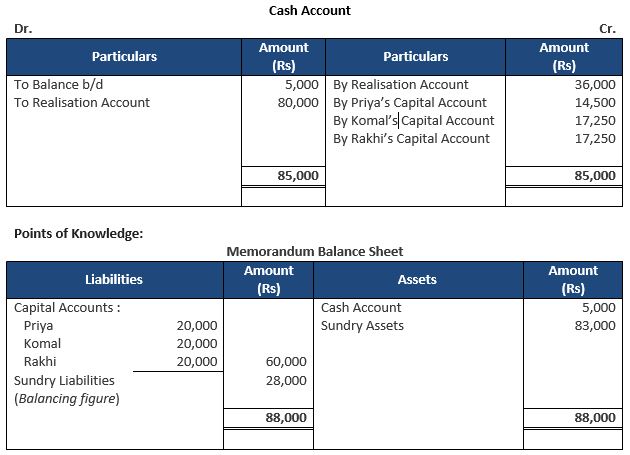

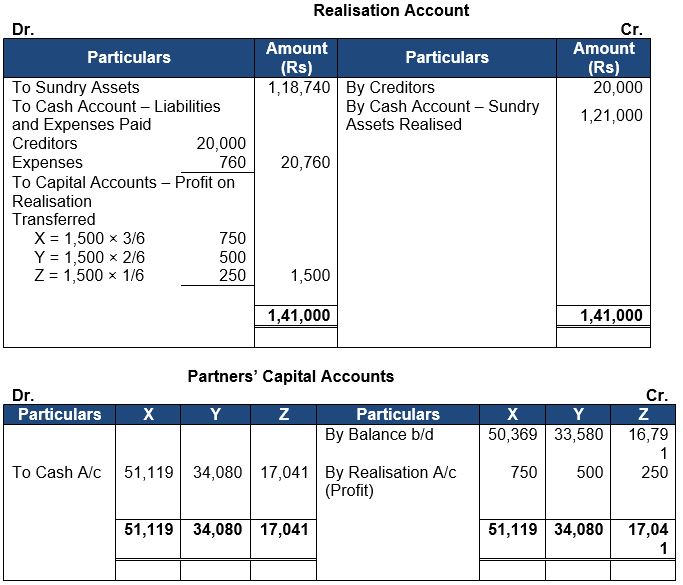

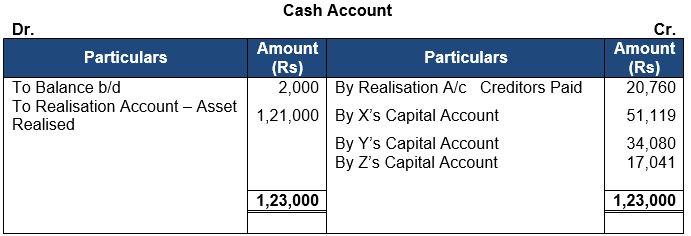

Question 45: Priya, Komal and Rakhi were in partnership sharing profits and losses in the ratio of 2:1:1. They decided to dissolve the partnership. On that date of dissolution, Sundry Assets (including cash Rs 5,000) amounted to Rs. 88,000, assets realised Rs. 80,000 (including an unrecorded asset which realised Rs 4,000). A contingent liability on account of bills discounted Rs. 8,000 was paid by the firm. The Capital Accounts of Priya, Komal and Rakhi showed a balance of Rs 20,000 each.

Prepare Realisation Account, Partners' Capital Accounts and Cash Account.

Answer 45:

About Solution:-

If, Amount of claim < Amount of WC Reserve:- WCR equal to the amount of claim will be transferred to Realization Account.

Things to Remember:

If, Amount of claim = Amount of WC Reserve:- WCR equal to the amount of claim will be transferred to Realization Account.

Important Notes: