Access free TS Grewal Solution Class 12 Chapter 9 Company Accounts Issue of Debentures 2026 below. Students can now access free TS Grewal Solutions for Class 12 Accountancy. These chapter-wise exercises are designed by expert Accountancy teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Accountancy Chapter 9 Company Accounts Issue of Debentures TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 9 Company Accounts Issue of Debentures Class 12 Accountancy below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 9 Company Accounts Issue of Debentures TS Grewal Class 12 Solved Exercises

About the chapter: TS Grewal Class 12 Chapter 9 explains concepts and provides questions relating to the Company Accounts Issue of Debentures. This chapter is very important as a lot of questions are asked in exams from here. There are detailed notes relating to the process of issuing debentures, types of debentures, advantages, and disadvantages, and accounting entries associated with the issuance of debentures. It also has concepts relating to redeemable, irredeemable, convertible, and non-convertible debentures. Other topics such as the benefits and drawbacks of issuing debentures, advantages of acquiring long-term capital for the company etc have been also explained. There are a lot of solved practical questions relating to different methods of issuing debentures such as at par, premium, and discount, and how the interest on debentures is calculated. Students should also learn the accounting treatment for the issue of debentures, including the preparation of journal entries, ledger accounts, and balance sheets.

Students will be able to get a detailed understanding of the issue of debentures and the accounting procedures associated with them. Please refer to the solutions for the practical questions provided in this chapter below. They have been prepared by expert accountancy teachers.

TS Grewal Class 12 Accounting for Companies

Textbook for CBSE Class 12

TS Grewal Solutions Class 12 Accountancy

Chapter 9 Company Accounts - Issue of Debentures

Question 12. Discount or Loss on issue of Debentures may be written off from Securities Premium Reserve. Why?

Discount or Loss on issue of Debentures is written off at the earliest but within the life, i.e., tenure of the debentures. It is a capital loss for the company and hence, is written off from Capital Reserve, if it has a balance. If Capital Reserve does not exist, it is written off from Securities Premium Reserve (Section 52(2)).

The Journal entry for writing off discount or loss is:

Securities Premium Reserve A/c ……….Dr.

To Discount or Loss on Issue of Debentures A/c

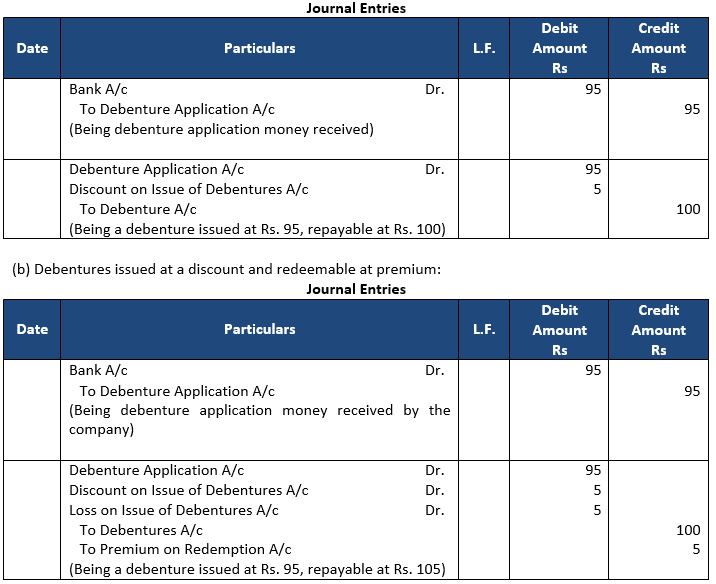

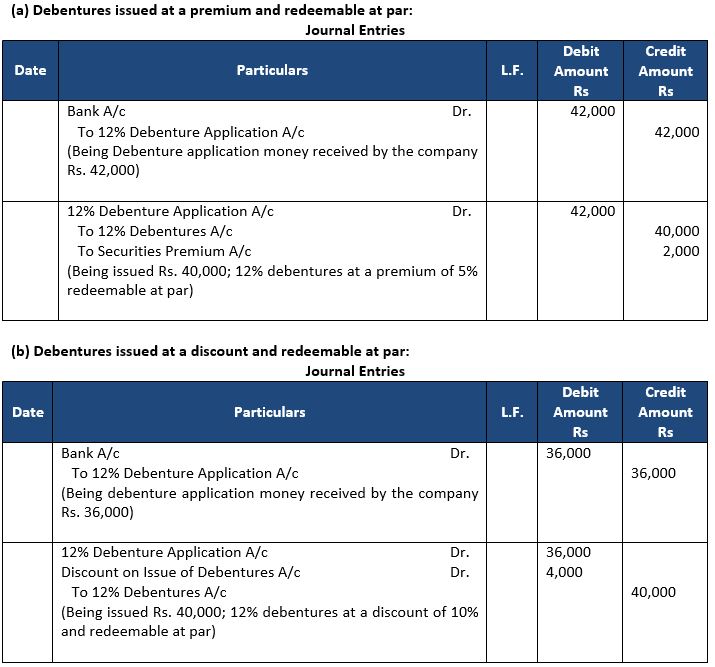

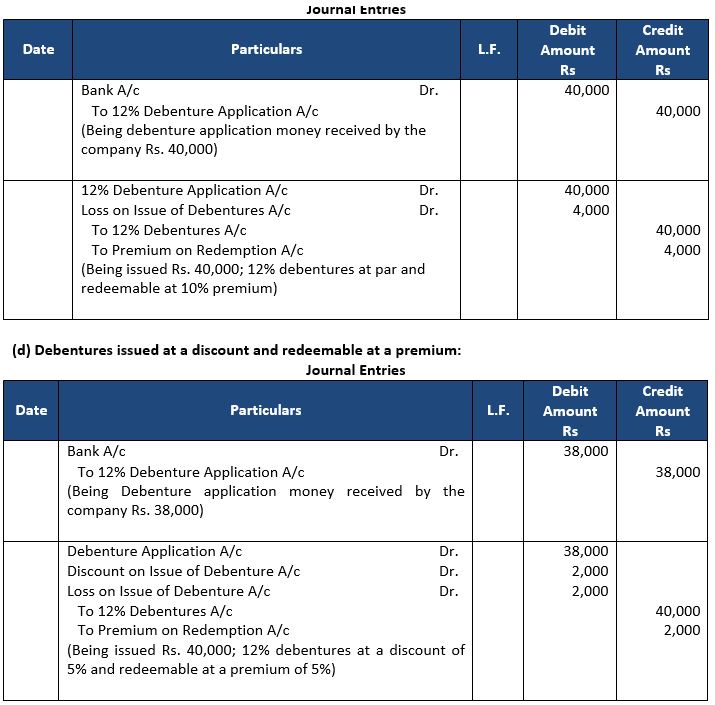

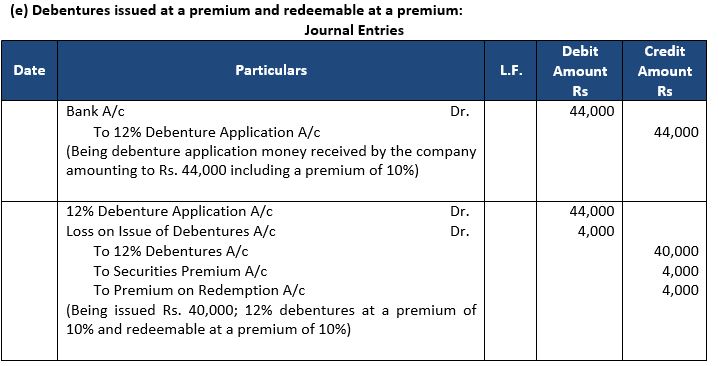

Question 13. What is meant by ‘Debentures issued at Discount and Redeemable at Premium’?

The company incurs loss on two counts, i.e., discount allowed at the time of issue of debentures and premium payable at the time of its redemption.Both these losses are accounted at the time of issue of debentures following the principle of prudence. The entries are:

Bank A/c ……….Dr.

To Debentures Application A/c

Debentures Application A/c ……….Dr.

Discount on issue of Debentures A/c ……….Dr.

Loss on issue of Debentures A/c ..………Dr.

To Discount or Loss on Issue of Debentures A/c

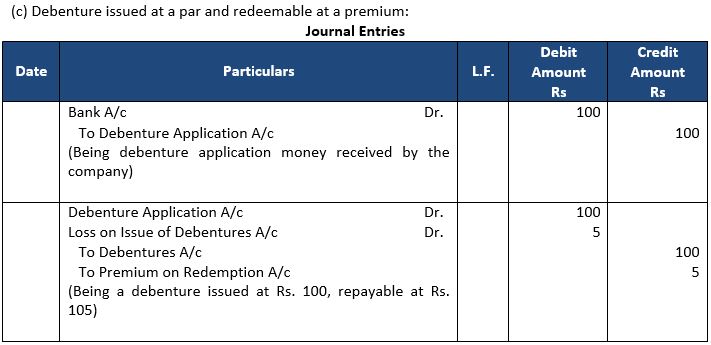

Question 14. What is meant by ‘Premium of Redemption of Debentures Account’?

When Debentures are redeemable at premium the difference between redeemable value and the issue price is a loss for the company, which is debited to loss on issue of debentures account at the time of allotment of debentures following the principal of ‘prudence’. The entries are:

(a) Bank A/c ……………..Dr.

To Debentures Application A/c

(b) Debentures Application A/c ……………..Dr.

Loss on issue of debentures A/c ………………Dr.

To ….% Debentures A/c

To Premium on Redemption of Debentures A/c

Question 15. What is meant by ‘Debentures issued at Discount and Redeemable at premium’?

The company incurs loss on two counts, i.e., discount allowed at the time of issue of debentures and premium payable at the time of its redemption. Both these losses are accounted at the time of issue of debentures following the principle of prudence. The entries are:

(a) Bank A/c ……………..Dr.

To Debentures Application A/c

(b) Debentures Application A/c ……………..Dr.

Discount on issue of debentures A/c ……………Dr.

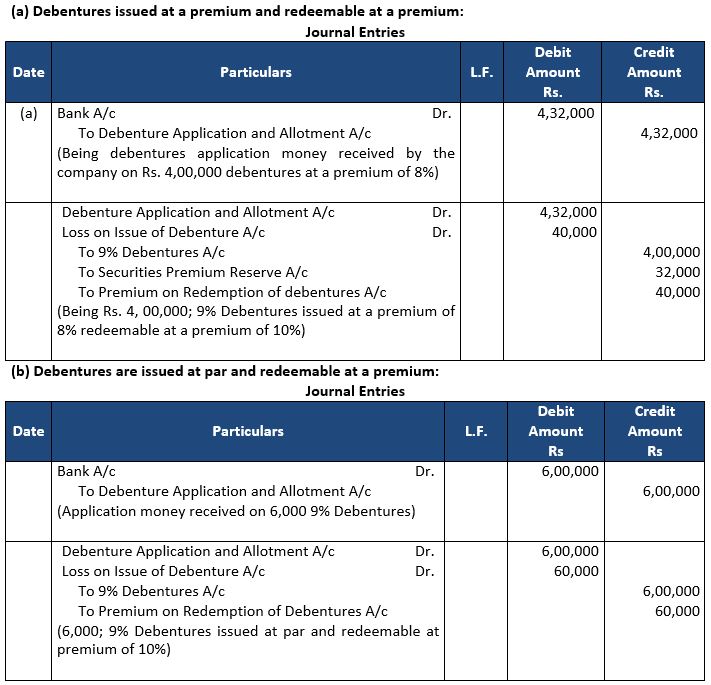

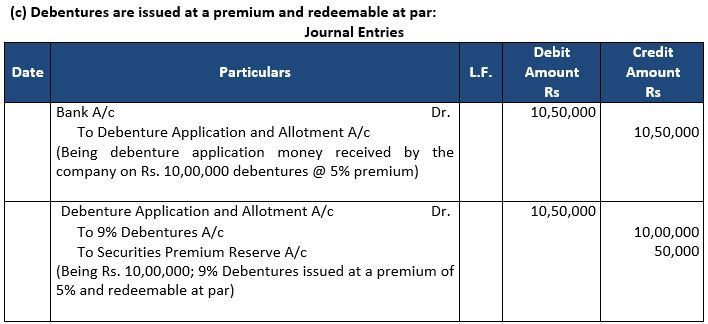

Loss on issue of debentures A/c ……………Dr.

To ….% Debentures A/c

To Premium on Redemption of Debentures A/c

Question 16. How is Discount or Loss on issue of Debentures written off?

Discount or Loss on Issue of Debentures is a capital loss for the company, which should be written off at the earliest but within the tenure of the debentures, i.e., it should be written off within the period the debenture are to be redeemed. The company thus, may write off discount or loss on issue of debentures at any time before the debentures are due for redemption.

Discount or Loss on Issue of Debentures written off is a part of Finance Cost in Statement of Profit and loss. Discount or Loss on Issue of Debentures may be written off following any of the following options:

(i) It may be written off in the first year itself; or

(ii) It may be written off over the tenure (life) of the debentures.

Question 17. Can Discount or Loss on Issue of Debentures be written off from Securities Premium Reserve? Explain.

Discount or Loss may be written off from Capital Reserve or from Securities Premium Reserve or from Statement of Profit and Loss. Accounting entry will be as follows:

Securities Premium Reserve A/c ……………Dr.

To Discount or Loss on Issue of Debentures A/c

Question 18. What is meant by ‘Issue of debentures for consideration other than cash’?

Issue of Debentures for consideration other than cash means that the company has not received amount (in cash or by cheque) against the debentures issued. Debentures may be issued for consideration other than cash under the following circumstances:

(i) Issue of Debentures to Promoters

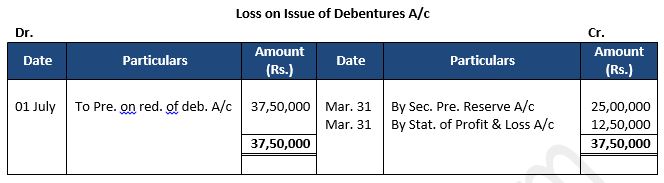

(ii) Issue of Debentures to Venders

Question 19. What is meant by issue of debentures as purchase consideration?

Purchases Consideration is the amount agreed to be paid for taking over the business from another enterprise. Purchases consideration may be given in the question; otherwise it will be equal to Net Assets (i.e., Agreed value of Assets taken- Agreed amount of Liabilities assumed).

Question 20. Name the type debentures which are payable only to the person who is holding the debentures.

Bearer Debentures are payable only to the person who is holding the debentures.

Question 21. Is the interest on debentures calculated at the fixed percentage on the issue price?

Interest on debentures calculated at a fixed rate and always on the face value and not on the issue price.

Question 22. Name the head under which ‘interest accrued and due on debentures’ appears in the Balance Sheet of a company.

Interest Accrued (whether due or not) on Debentures is shown under the head ‘Current Liabilities’ and sub-head ‘Other Current Liabilities’.

Question 23. Name the head under which ‘interest accrued but not due on debentures’ appears in the Balance Sheet of a company.

Interest Accrued (whether due or not) on Debentures is shown under the head ‘Current Liabilities’ and sub-head ‘Other Current Liabilities’.

Question 24. What is meant by issue of debentures as Collateral Security?

Security given in addition to the prime or principal security is termed or known as Collateral Security.

Question 25. How are Debenture issued as Collateral Security shown in the Balance sheet?

Debentures issued as Collateral Security are shown separately from other debentures in the Balance sheet.

Question 26. What is the nature of Interest on Debentures?

Interest on debentures is a Charge against profit. It is, therefore, provided even if the company does not have profit or has inadequate profit.

Question 27. Why does a company pay interest on debentures before payment of dividend?

Interest on debentures is calculated at fixed rate on its nominal (face) value payable quarterly, half yearly or yearly as per the terms of issue. Rate of interest is prefixed to the debentures, say 9% Debentures and, therefore, is payable even if the company incurs loss.

Question 28. Why would an investor prefer to invest in the debentures of a company rather than in its shares?

Debentures provide a fixed return even in case of loss, so there is no risk to investor therefore an investor prefers to invest in the debentures of a company rather than in its shares.

Question 29. Why would an investor prefer to invest partly in share and partly in the debentures of a company?

Shares provide higher return than debentures but Debentures provide a fixed return even in case of loss. So by investing in both an investor gets higher return with lower risk.

Question 30. Why would an investor prefer to invest in the shares of a company rather than in the Debentures?

Shares provide higher return in short time so, investor prefer to invest in the shares of a company rather than in the Debentures.

Question 31. Pass Journal entry when 10,000 debentures of Rs. 100 each are issued as collateral security against a Bank Loan of Rs. 8,00,000.

Short Answer Type Questions:-

Question 1. What are debentures? What are the kinds of debentures?

Answer:

Debenture is a written instrument or document issued by the company acknowledging a debt. It contain terms of repayment of principal and also payment of interest (usually paid half-yearly) at a rate specified at time of its issue.

“Debenture includes debenture stock, bonds and any other instrument of the company evidencing a debt, whether constituting a charge on the assets of the company or not.”

A company may issue different kinds of debentures which can be classified as under:

1. From Security Point of View

(i) Secured Debentures: Secured Debentures are those debentures which are secured by either a fixed charge or a floating charge on the assets of the company. A charge on the assets of the company is registered with the Registrar of Companies.

(ii) Unsecured Debentures: Unsecured Debentures are those debentures which are not secured by any charge on assets of the company.

2. From Redemption Point of View

(i) Redeemable Debentures: Redeemable Debentures are those debentures that are repayable by the company at the end of a specified period or by instalments during the existence of the company.

(ii) Irredeemable Debentures: Irredeemable Debentures are those debentures that are not repayable during the lifetime of the company and hence are repaid only when the company is liquidated.

3. From Records Point of View

(i) Registered Debentures: Registered Debentures are the debentures that are registered in the company’s records in the name of the holder. Principal and interest of such debentures is payable to the registered debenture holder.

(ii) Bearer Debentures: Bearer debentures are the debentures that are not registered in the records of the company in the name of the holder.

4. From Priority Point of View

(i) First Debentures: The debentures which have to be repaid before the other debentures are known as first debentures.

(ii) Second Debentures: The debentures, which will be repaid after the first debentures are redeemed, are known as second debentures.

5. From the Point of View of Coupon Rate

(i) Specific Coupon Rate Debentures: These debentures are issued with a specified rate of interest, called the coupon rate.

(ii) Zero Coupon Rate Debentures (Bonds): These debentures do not carry a specific rate of interest. In order to compensate the investors such debentures are issued at a substantial discount.

6. From Convertibility Point of View

(i) Convertible Debentures: Convertible Debentures are the debentures that are convertible into shares. If a part of the debenture amount is convertible into Equity Shares, they are known as Partly Convertible Debentures. If full amount of debentures is convertible into Equity shares, they are known as Fully Convertible Debentures.

(ii) Non-Convertible Debentures: Non-convertible debentures are the debentures that are not convertible into shares.

Question 2. Give any three characteristics of a debenture.

Answer:

Below are the characteristics of debenture:-

- Debenture is a written document or certificate acknowledging debt by the company.

- Mode and period of repayment of principal and interest is fixed.

- Rate of interest on the debenture is specified. It is practice to prefix ‘Debentures’ with the rate of interest. For example, if the rate of interest is 9%, the title of the debentures will be ‘9% Debentures’.

Question 3. Can a company issue debentures for ‘consideration other than cash’? If so, what accounting Journal entries such a company must pass?

Answer:

Yes, a company issue debentures for ‘consideration other than cash’. Issue of Debentures for consideration other than cash means that company has not received amount (in cash or by cheque) against the debentures issued. Debentures may be issued for consideration other than cash under the following circumstances:

(i) Issued of Debentures to Promoters: A company may allot debentures to the promoters for rendering their services for incorporating the company. The entry is:

(a) When assets are purchased and debentures are issued:

Question 4. Explain the meaning and accounting treatment of debentures issued as collateral security.

Answer:

Issue of debentures as Collateral Security means issue of debentures as additional security, i.e., in addition to the principal security. It is only to be realised when the principle security fails to pay the amount of loan. For example, when a company takes a loan of Rs. 10,00,000 from the bank, it may have to issue debentures as collateral security in addition to the principal security.

Accounting Treatment: Debentures issued as a collateral security can be dealt with in two ways:

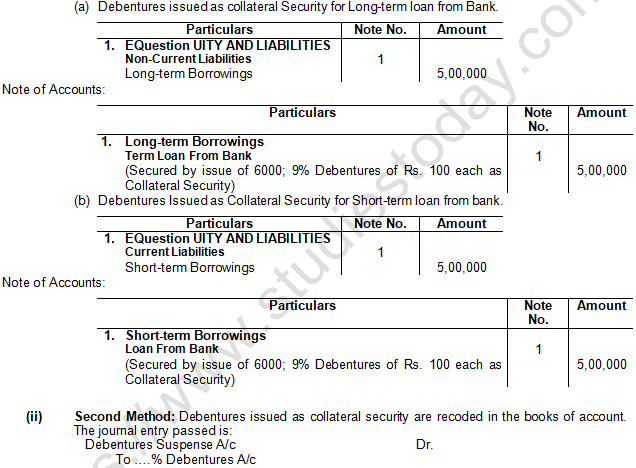

(i) First Method: Entry for issue of debentures as collateral security is not passed in the books of account at the issuing such debentures. It is disclosed under the head. Secured Method in the Equity and Liabilities part of the Balance Sheet that debentures have issued as collateral security as follows:

(a) Debentures issued as collateral Security for Long-term loan from Bank.

Question 4. Explain the meaning and accounting treatment of debentures issued as collateral security.

Answer:

Issue of debentures as Collateral Security means issue of debentures as additional security, i.e., in addition to the principal security. It is only to be realised when the principle security fails to pay the amount of loan. For example, when a company takes a loan of Rs. 10,00,000 from the bank, it may have to issue debentures as collateral security in addition to the principal security.

Accounting Treatment: Debentures issued as a collateral security can be dealt with in two ways:

(i) First Method: Entry for issue of debentures as collateral security is not passed in the books of account at the issuing such debentures. It is disclosed under the head. Secured Method in the Equity and Liabilities part of the Balance Sheet that debentures have issued as collateral security as follows:

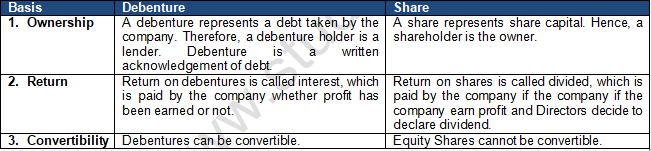

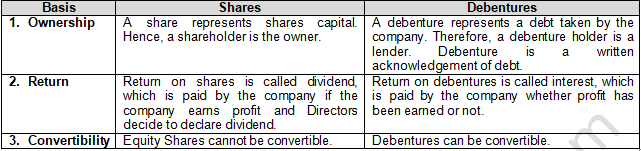

Question 5. Write any three points of difference between equity shares and debentures.

Answer:

Question 6. What are the alternatives available to a company for the allotment of debentures when there is oversubscription of Debentures?

Answer:

Oversubscription of Debentures means that the company has received applications for more number of debentures than it has issued. In such a situation, the company may make allotment, by any of the following three options or combination:

First Alternative- Rejecting Excess Application.

Second Alternative- Partial or Pro rata Allotment.

Third Alternative- A Combination of the Above Two Alternatives.

Excess application money received on oversubscription may be retained for adjustment towards allotment and the respective calls, in case of pro rata allotment, if so provided in the terms of issue. However, application money is refunded to those applicants to whom debentures are not allotted.

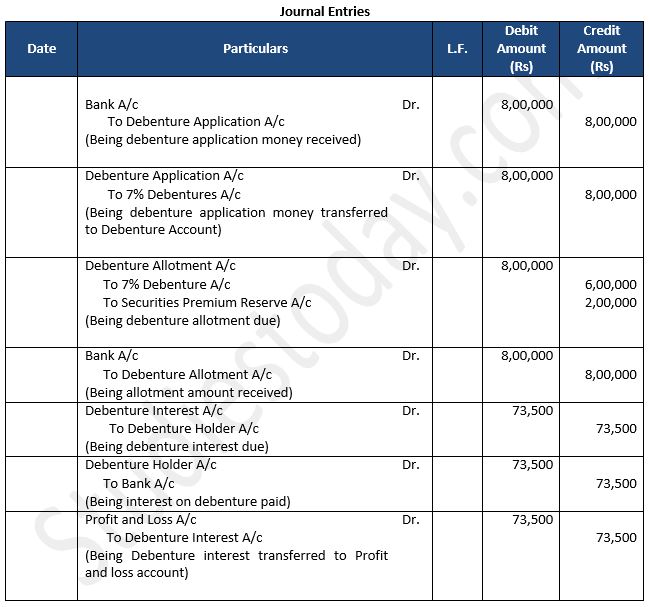

Question 7. What is the nature of ‘interest on debentures’? Give Journal entries: (a) when the interest is due and (b) when the interest is paid (ignore tax).

Answer:

Exercise ::--->

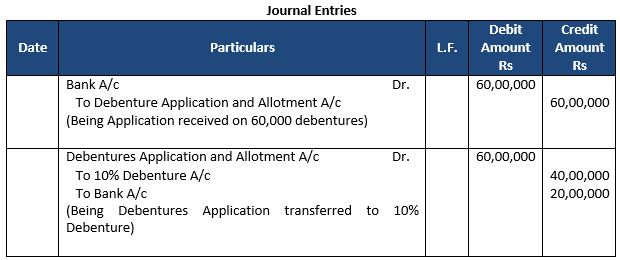

Question 1: Epson Ltd. issued 40,000; 10% Debentures of ₹ 100 each at par for cash payable in full along with the application. Applications were received for 60,000 debentures. Debentures were allotted and excess application money was refunded. Pass Journal entries in the books of the company.

Answer 1:

Things to remember:

A unit of loan amount is a debenture. A firm offers debentures when it wants to borrow money from the general public. A debenture holder is a person who holds a debenture or debentures.

Important note:

A document carrying the business seal is called a debenture. It serves as an acknowledgement of the company's receipt of a loan with a notional value equivalent to the debenture. It displays the redemption date, interest rate, and method of payment. The company's creditor is a holder of debentures.

Debentures comprise debenture stock, bonds, and any other instruments of the company, whether or not they represent a charge on the firm's assets, according to section 2(12) of the Companies Act of 1956.

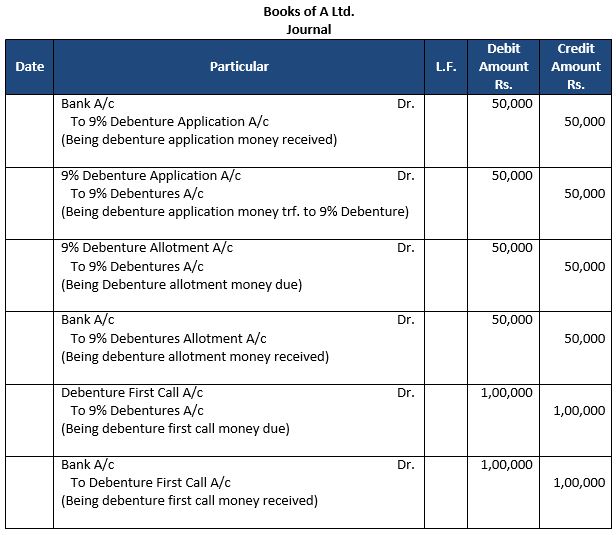

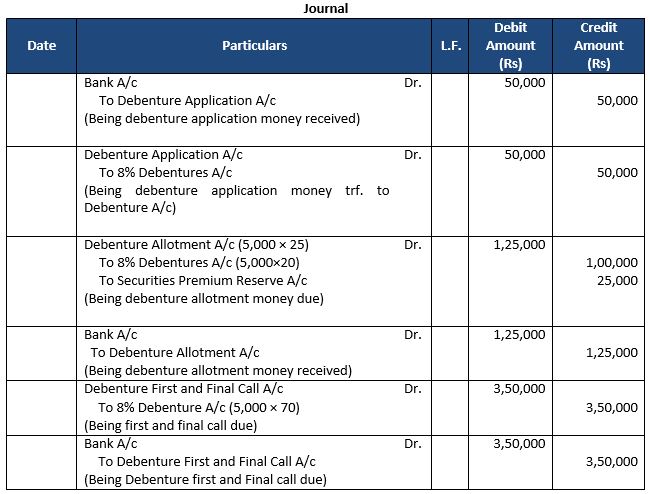

Question 2: Saurab Ltd. issued 2,000; 9% Debentures of ₹ 100 each payable as follows:

₹ 25 on application; ₹ 25 on allotment and ₹ 50 on first and final call.

Applications were received for all the debentures along with the application money and allotment was made. Call money was also received on the due date. Pass necessary Journal entries in the books of the company.

Answer 2:

Things to remember:

A debenture is a document bearing the company's common seal and admitting a debt. It contains a contract for the payment of interest at a given rate payable typically either half-yearly or yearly on fixed dates, and for the repayment of principal after a specified period or at intervals or at the company's option.

Important note:

In contrast to a debenture, which just acknowledges debt, a share indicates ownership of the corporation. A debenture is a portion of borrowed capital, whereas shares are a portion of owned capital.

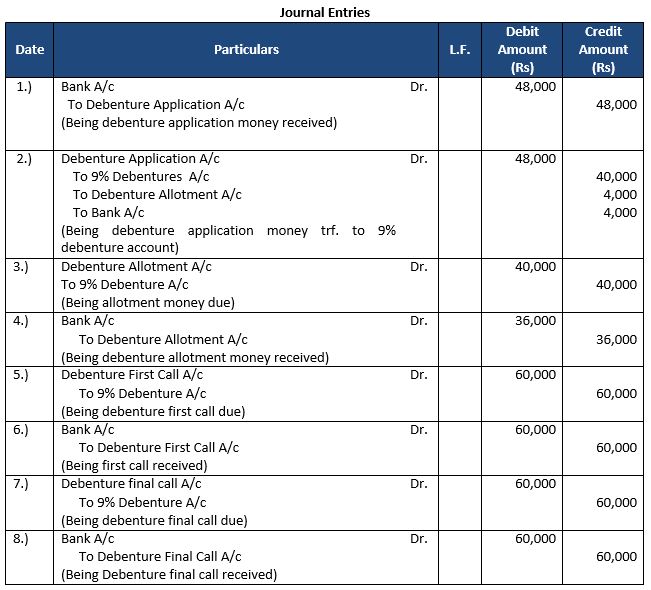

Question 3: Dogra Ltd. issued 2,000; 9% Debentures of Rs. 100 each on the following terms: Rs. 20 on application; Rs. 20 on allotment; Rs. 30 on First Call; Rs. 30 on second and final call. Applications were received for 2,400 debentures. Application for 1,800 debentures were accepted in full. Applications for 400 debentures were allotted 200 debentures and applications for 200 debentures were rejected. Pass necessary Journal entries.

Answer 3:

Things to remember:

Debentures that have a charge placed on the company's assets for the purpose of payment in the event of default are referred to as secured debentures. Either a fixed or floating charge may apply. A floating charge is formed on the company's overall assets, whereas a fixed charge is created on a specific item. Whereas a floating charge applies to all assets excluding those allocated to secured creditors, a fixed charge is made against assets kept by a corporation for use in operations not intended for sale.

Important note:

Debenture could be Partially Convertible Debentures (PCD): At the issuer's discretion, a portion of these securities may be converted into equity shares in the future. The conversion ratio is chosen by the issuer. Typically, this is chosen at the time of subscription.

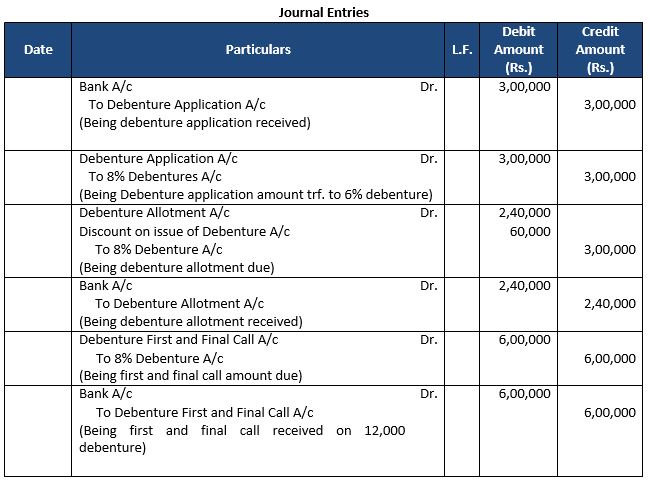

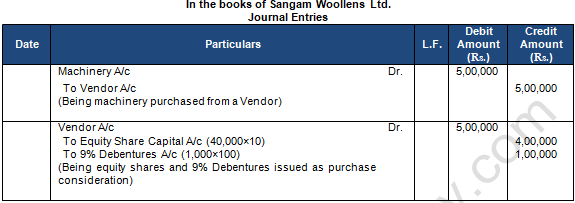

Question 4: Super Seals Ltd. issued 10,000, 8% Debentures of ₹ 100 each at par for subscription payable ₹ 40 on application, ₹ 30 on allotment and balance as first and final call. Debentures issued were applied and allotment was made. First and Final Call is yet to be made.

You are required to pass the necessary Journal entries.

Answer 4:

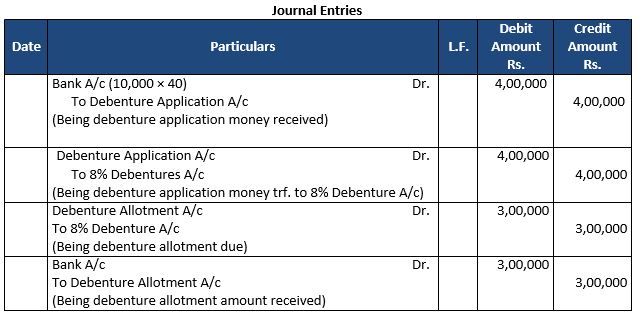

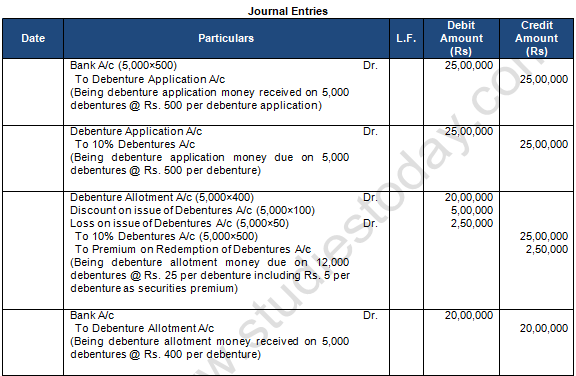

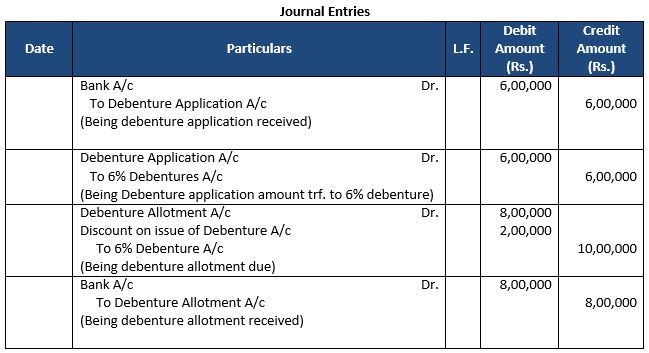

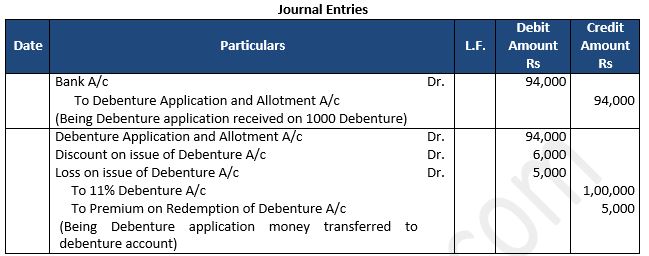

Question 5: Narain Laxmi Ltd. invited applications for issuing 7,500; 12% Debentures of Rs. 100 each at a premium of Rs.35 per debenture. The full amount was payable on application. Applications were received for 10,000 Debentures. Allotment was made to all the applications on pro rata. Pass necessary Journal entries for the above transactions in the books of Narain Laxmi Ltd.

Answer 5:

About solution:

Distribution of Debenture face value into installments:-

Application = Rs. 100 + Rs. 35 = Rs. 135

Number of Debentures issued = 7,500

Number of Application received = 10,000

Things to remember:

When debenture obligations are issued at a price higher than their nominal value, this is referred to as being issued at premium.

Important note:

Unsecured debentures are those that have no security attached to the principle amount or unpaid interest. Simple debentures are what they are known as. Such debentures carry no charge on the company's assets. It serves as an acknowledgment of the loan the company got in the amount of the debenture's nominal value. It displays the redemption date, interest rate, and method of payment. The company's creditor is a holder of debentures.

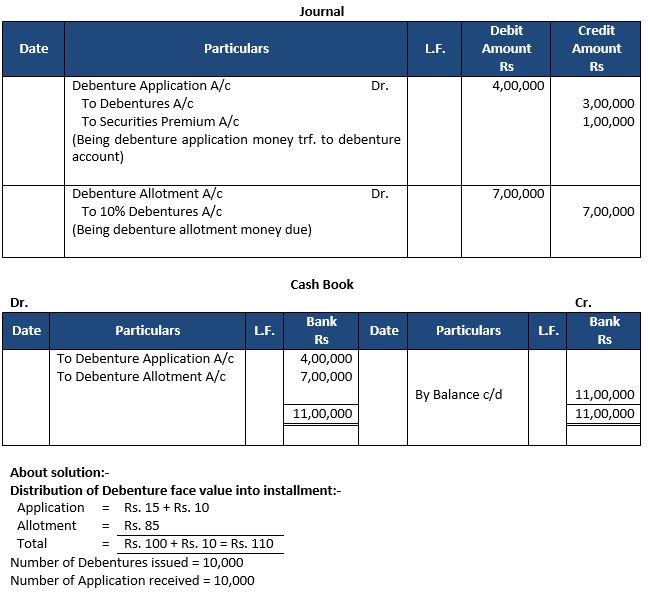

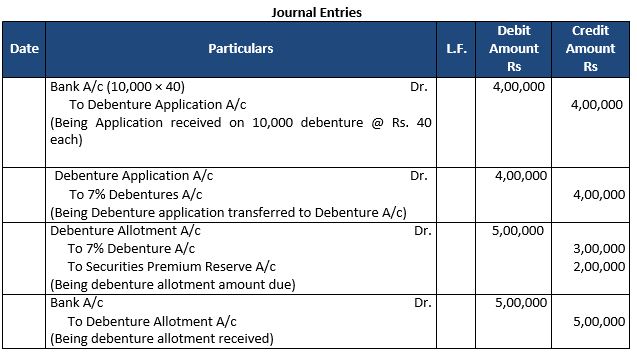

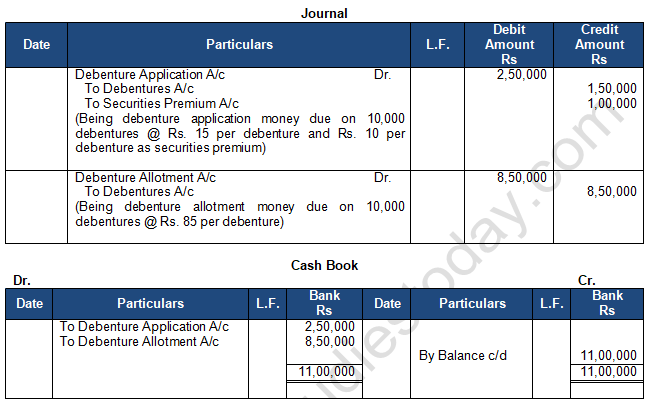

Question 6: Nipa Limited issued 10,000 Debentures of Rs. 100 each at a premium of 10%, payable 30% of nominal (face) value on application (including premium) and the balance on allotment. The debentures were applied for and the amount was dully received.

You are required to give Journal entries and prepare Cash Book.

Answer 6:

Things to remember:

By issuing debentures, the corporation signifies that it will publish a certificate bearing its stamp as an acknowledgement of the debt that it has incurred. The process for a firm to issue debentures is comparable to that of issuing shares. Letters of allocation are issued, a prospectus is released, and applications are requested. Application fees are returned when applications are declined. In the event of partial allocation, any remaining application funds may be applied to upcoming calls.

Important note:

A bond is a debt acknowledgment tool as well. In the past, only the government issued bonds, but today, semi-government and non-governmental organizations also issue bonds. Now, the phrases "debentures" and "bonds" are interchangeable.

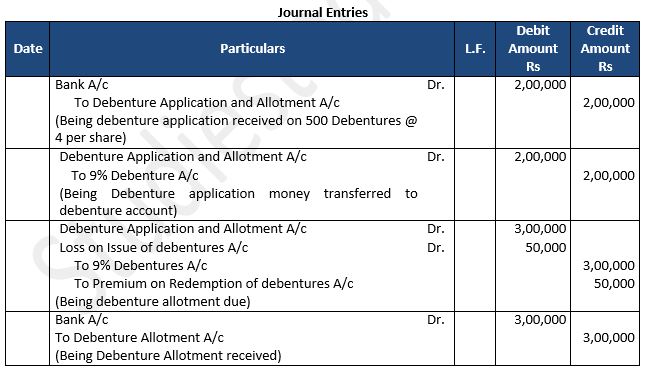

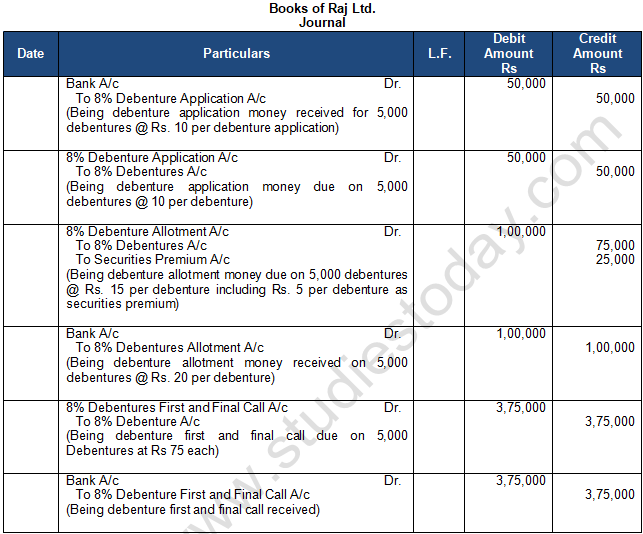

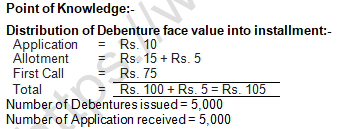

Question 7: Raj Ltd. issued 5,000; 8% Debentures of Rs. 100 each at a premium of 5% payable as follows:

Rs. 10 on Application; Rs. 20 plus premium on Allotment and balance on first and final call. Pass necessary Journal entries.

Answer 7:

Things to remember:

Whereas the return on debentures is known as interest, the return on shares is known as a dividend. Depending on the company's profits, the rate of return on shares may change from year to year, whereas the rate of interest on debentures is fixed. Dividend payments are an appropriation of profits, whereas interest payments are charges against profits that must be made even in the absence of a profit.

Important note:

The quantity of shares is typically not refunded over the course of the company's existence, but the debentures are typically issued for a set length of time and are repayable at the end of that time.

Question 8: Grand Hospitality Ltd. issued 10,000, 7% Debentures of Rs. 100 each at premium of Rs. 20 per debenture. Issue price was payable as follows: Rs. 40 on application, Rs. 50 (including premium) on allotment and balance on first and final call. It received Rs. 4,00,000 as application money. On Allotment due amount was received. First and Final call is yet to be made.

You are required to pass the necessary Journal entries.

Answer 8:

Things to remember:

Debentures can be converted into shares if the terms of the issue permit it; in such case, they are referred to as convertible debentures. Shares cannot be converted into debentures.

Important note:

The quantity of shares is typically not refunded over the course of the company's existence, but the debentures are typically issued for a set length of time and are repayable at the end of that time.The business may request payment in full at the time of application or through installments at the time of application, at the time of allocation, and at various calls. Debentures can be sold for a discount, at a premium, or at par. They may also be issued as a collateral security or for a consideration other than cash.

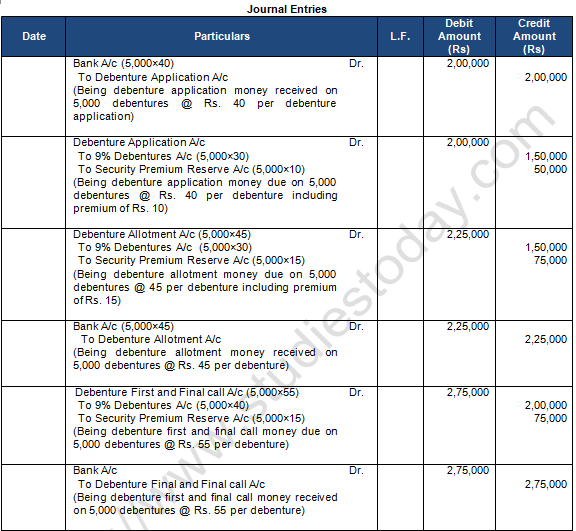

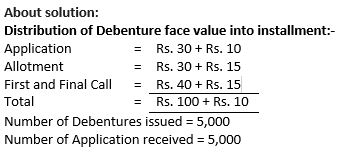

Question 9: Iron Products Ltd. issued 5,000; 9% Debentures of Rs. 100 each at a premium of Rs. 40 payable as follows;

(i) Rs. 40 , including premium of Rs. 10 on applications;

(ii) Rs. 45, including premium of Rs. 15 on allotment; and

(iii) Balance as first and final call.

The issue was subscribed and allotment made. Calls were made and due amount was received. Pass Journal entries.

Answer 9:

Things to remember:

Bearer debentures are those that can be delivered and can be transferred, and the firm keeps no record of them. A person who provides the interest coupon affixed to such debentures will be paid interest on the debt.

Question 10: Pure Products Ltd. issued 30,000, 8% Debentures of Rs. 100 each at 10% premium for subscription. The issue price was payable Rs.40 on application, Rs. 40 (including premium) on allotment and balance on first and final call. It received application money amounting to Rs. 10,80,000. Allotment was made and allotment money was received. First and final call is yet to be made.

Answer 10

Things to remember:

Occasionally a business buys assets from suppliers and instead of paying with cash, issues debentures as payment. Debentures issued for consideration other than cash are the type of issuance that fall under this category. The entries made in that situation are identical to those of the shares issued for consideration other than cash, and the debentures may likewise be issued at par, at a premium, or at a discount.

Important note:

A unit of loan amount is a debenture. A firm offers debentures when it wants to borrow money from the general public. A debenture holder is a person who holds a debenture or debentures. A document bearing the business seal is called a debenture. It serves as a confirmation of the loan that the company obtained in an amount equivalent to the nominal value of the debenture.

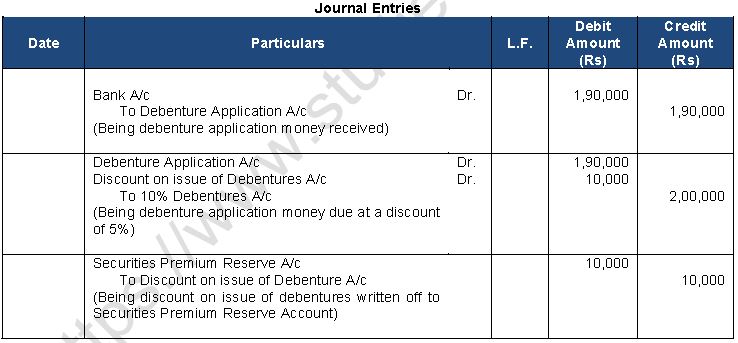

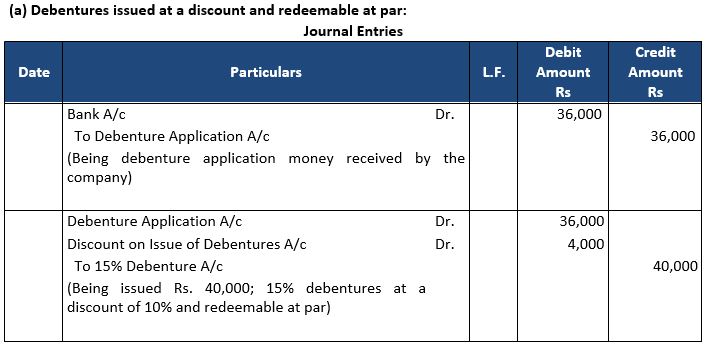

Question 11: Kati Ltd. issued 8,000, 9% Debentures of Rs. 100 each at a discount of 10%. The full amount was payable on application. Applications were received for 9,000 debentures and allotment was made on pro rata basis.

Pass the necessary Journal entries for the above transactions in the books of Kati Ltd.

Answer 11:

Things to remember:

Yet debentures can occasionally be granted for reasons other than cash. When a firm buys another company or purchases assets from a vendor, it may decide to settle the payment by issuing debentures to the vendors rather than paying with cash.

Important note:

Letters of allocation are issued, a prospectus is released, and applications are requested. Application fees are returned when applications are declined. In the event of partial allocation, any remaining application funds may be applied to upcoming calls.

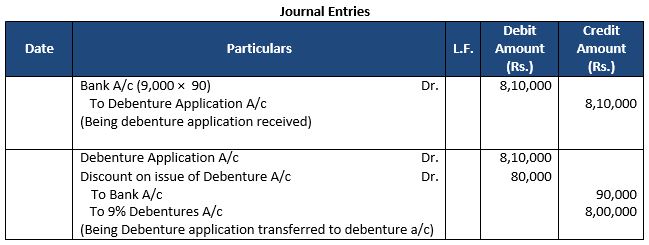

Question 12: Linux Ltd. issued 12,000; 8% Debentures of Rs. 100 each at a discount of 5% payable as 25% on application; 20% on allotment and balance after three months.

Pass Journal entries.

Answer 12:

Things to remember:

Debentures are typically issued with clauses stipulating how they will be redeemed when they reach maturity. Debenture redemption is the process of repaying the holders of the debt to satisfy the debt's obligation. Debentures have two redemption options: par and premium.

Important note:

When a firm redeems debentures provided to debenture holders, it means that the company pays the debenture holders their money when the debentures mature. The debentures could be repaid by the corporation before they mature, though. Corporation issuing debentures must open a debenture redemption reserve account under the law. The debenture holders are paid from deposits made to the reserve account. Reserve funds cannot be used for any other purpose by businesses.

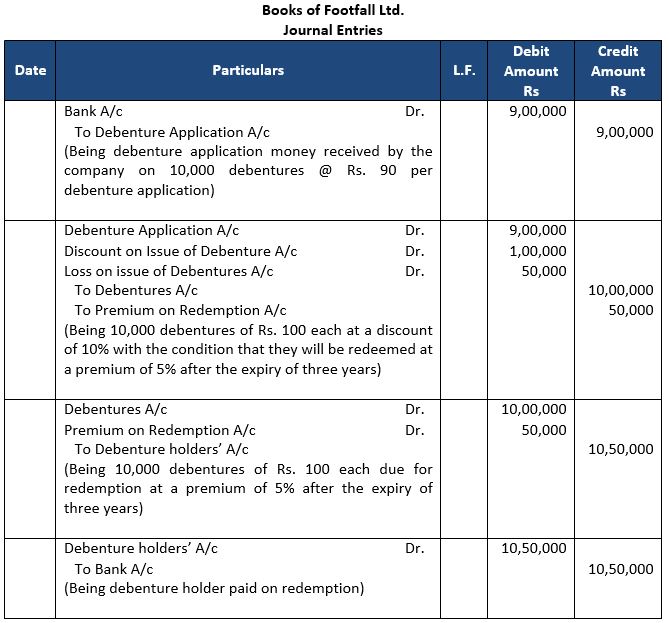

Question 13: Alka Ltd. issued 5,000, 10% Debentures of Rs. 1,000 each at a discount of 10% redeemable at a premium of 5% after 5 years. According to the terms of issue Rs. 500 was payable on application and the balance amount on allotment of debentures. Record necessary entries regarding issue of 10% Debentures.

Answer 13:

Things to remember:

Redeemable debentures are those that are redeemable at the end of the specified period for a lump sum or for periodic payments for the duration of the business. Debentures have two redemption options: par and premium.

Important note:

If firm issues discounted debentures, the full amount of the discount is not recorded in the company's profit and loss statement for the accounting year in which the discount is permitted. The corporation benefits from the borrowing by issuing debentures over a number of years, although the amount of such a discount is fairly substantial. Hence, a portion of the discount amount is written off each year.

Question 14: The Décor Ltd. issued 20,000, 6% Debentures of Rs. 100 each at 10% discount payable Rs. 30 on application, Rs. 40 (after discount) and balance as first and final call. Debentures were subscribed and allotment was made. Amount due on allotment was made and received. First and Final call is yet to be made.

You are required to pass the necessary Journal entries.

Answer 14:

About solution:

The procedure by which the corporation repays the debenture holders for the debentures they issued refers to the process by which the debenture holders receive payment following the maturity of the debenture. The debentures could be repaid by the business, nevertheless, before they mature. A corporation issuing debentures is required by law to establish a debenture redemption reserve account. The reserve account receives deposits that are used to pay the debenture holders. Funds set aside for reserves cannot be used for any other reason.

Things to remember:

The corporation offers fixed maturity date debentures. The corporation reimburses the holders of debentures for their investment at the time of maturity. The amount that the corporation repays may be greater than, less than, or equal to the face value of the debentures. As a result, the corporation must abide by all the terms and conditions in the prospectus while issuing debentures.

Important note:

Section 39(1) of the Companies Act of 2013 states that a firm cannot distribute securities unless the minimum subscription amount specified in the prospectus is met. Determining such a minimal subscription will therefore be up to the corporation.

Question 15: Joy Ltd. company bought a Building for Rs. 9,00,000 and the consideration was paid by issuing 10% Debentures of the normal (face) value of Rs. 100 each at a discount of 10%. Give Journal entries.

Answer 15:

About solution:

Amount of Face Value of Debentures to be Issued = Rs. 9,00,000 ×100/90 = Rs. 10,00,000

Things to remember:

Sometimes a business buys assets from suppliers and instead of paying with cash, issues debentures as payment. Debentures issued for consideration other than cash are the type of issuance that fall under this category. The entries made in that situation are identical to those of the shares issued for consideration other than cash, and the debentures may likewise be issued at par, at a premium, or at a discount.

Important note:

Registered debentures are registered with the business. Only those debenture holders whose names are listed in the company registry are eligible to receive the amount of such debentures.

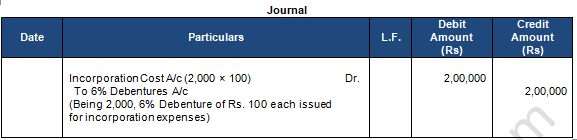

Question 16: Amrit Ltd. issued 1,000, 6% Debenture of Rs. 100 each to Amit and Bhaskar (Promoters) each for their services in incorporating the company.

Pass Journal entry.

Answer 16:

About solution:

Debenture issuance by a firm follows a similar process to share issuance. Letters of allotment are issued together with a prospectus and an invitation to apply. Money paid for applications is reimbursed in the event of rejection. Excess application funds may be applied to following calls in the event of partial allocation.

Things to remember:

Dividends are the name given to returns on shares, whereas interest is the name given to returns on debentures. The return on shares may change from year to year depending on the company's profits, whereas the interest rate on debentures is fixed. The payment of interest is a charge on earnings and must be made even if there are no profits, in contrast to the payment of dividends, which is an appropriation of profits.

Important note:

Due to the fact that the corporation does not guarantee the repayment of any funds acquired through the issuance of irredeemable debentures, they are sometimes referred to as perpetual debentures. When a corporation is dissolved or after a considerable period of time has passed, these debentures must be repaid.

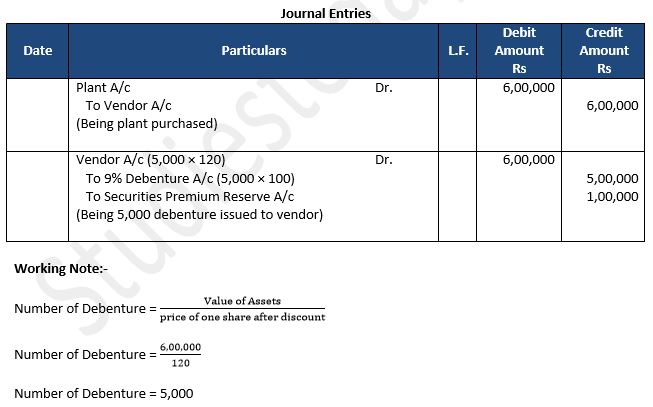

Question 17: B Ltd. issued 9% Debentures of Rs. 100 each at a premium of 20% to Vendors for purchase of Plant costing Rs. 6,00,000. Pass the necessary Journal entry for the payment made to vendors.

Answer 17:

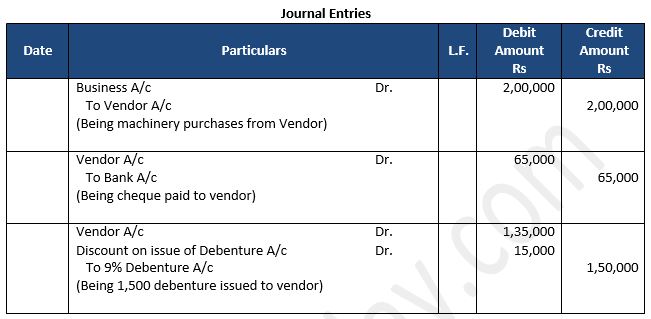

Question 18: Wye Ltd. purchased an established business for Rs. 2,00,000 payable as Rs. 65,000 by cheque and the balance by issuing 9% Debentures of Rs. 100 each at a discount of 10%. Give journal entries in the books of Wye Ltd.

Answer 18:

Working Note:-

Number of Debenture = 1,35,000/90

Number of Debenture = 1,500

Question 19: Reliance Ltd. purchased machinery costing Rs. 1,35,000. It was agreed that the purchase consideration be paid by issuing 9% Debentures of Rs. 100 each. Assume debentures have been issued.

(i) at par and

(ii) at a discount of 10%.

Give necessary journal entries.

Answer 19:

Things to remember:

It is supplied with the company's common seal. Debentures are redeemable after a predetermined time throughout the company's existence. In most cases, it places a charge on the company's assets. Whether the company is making a profit or not, interest is paid to the holder of the debenture at a fixed rate.

Important note:

Debenture issuance follows the same process as share issuance. Prospectuses are released, and interested parties apply for debentures. The business may demand payment in full at the time of application or by installments at the time of application, allocation, and on different calls.

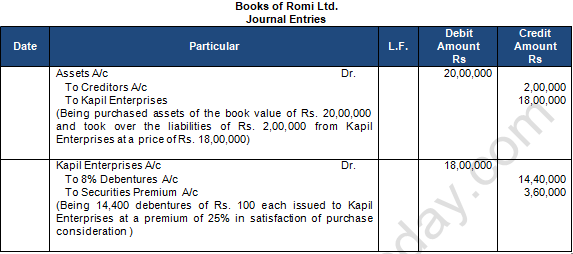

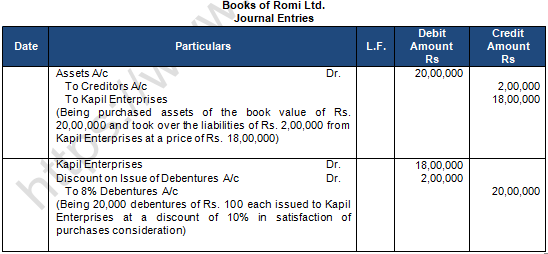

Question 20: Romi Ltd. acquired assets of Rs. 20 lakhs and took over creditors of Rs. 2 lakhs from Kapil Enterprises. Romi Ltd. issued 8% Debentures of Rs. 100 each at a discount of 25% as purchase consideration. Record necessary journal entries in the books of Romi Ltd.

Answer 20:

About solution:

Number of Debentures to be issued = 1,80,000 / 100 + 25

Number of Debentures to be issued = 14,400 Debentures

Things to remember:

1. Voting rights are absent from financial obligations;

2. Debentures serve as the company's debt representation;

3. Whether secured or unsecured, debentures

4. Debentures can be either convertible or not;

5. Debentures may be redeemed or may not;

6. Debentures have a fixed rate of interest;

Important note:

Typically, businesses use this approach when dealing with their vendors or sellers. In this scenario, a corporation issues its debentures as payment for the assets it purchases from the seller in lieu of paying cash. A business can also issue debentures at par, premium, or discount, and they are likewise recorded similarly.

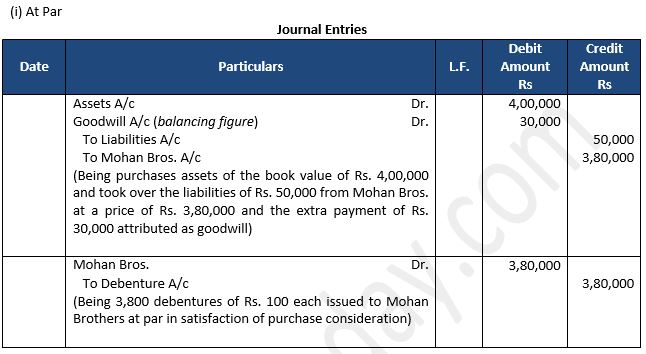

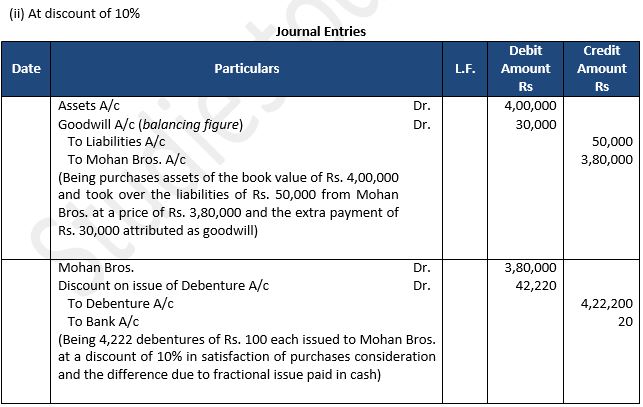

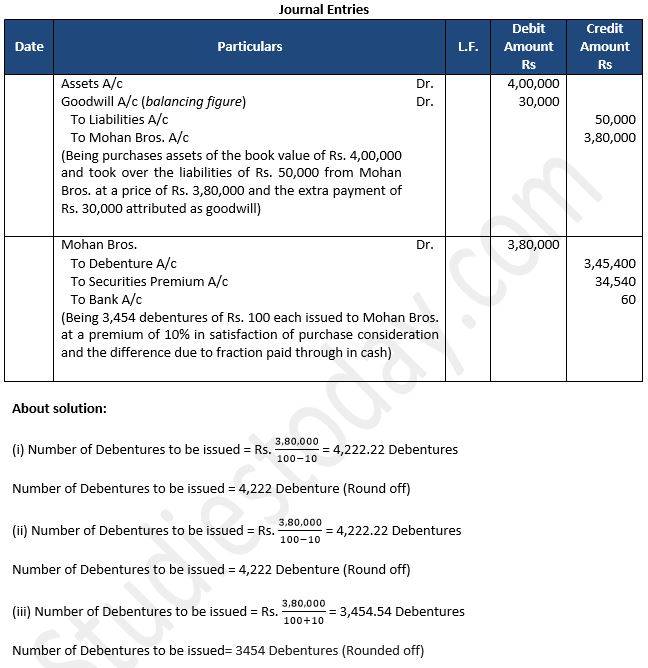

Question 21: Exe Ltd. purchased the assets of the book value Rs. 4,00,000 and took over the liabilities of Rs. 50,000 from Mohan Bros. It was agreed that the purchase consideration, settled at Rs. 3,80,000 be paid by issuing debentures of Rs. 100 each. Pass journal entries if debentures are issued:

(a) at par

(b) at a discount of 10% and

(c) at a premium of 10%.

It was agreed that any fraction of debentures be paid in cash.

Answer 21:

Things to remember:

Unsecured debentures are those that have no security attached to the principle amount or unpaid interest. Simple debentures are what they are known as. Such debentures carry no charge on the company's assets.

Important note:

Whereas the return on debentures is known as interest, the return on shares is known as a dividend. Depending on the company's profits, the rate of return on shares may change from year to year, whereas the rate of interest on debentures is fixed. Dividend payments are an appropriation of profits, whereas interest payments are charges against profits that must be made even in the absence of a profit.

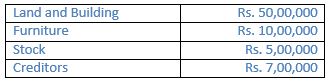

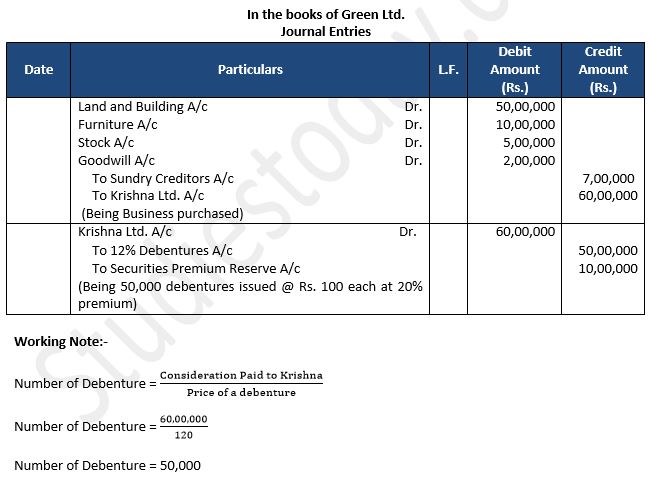

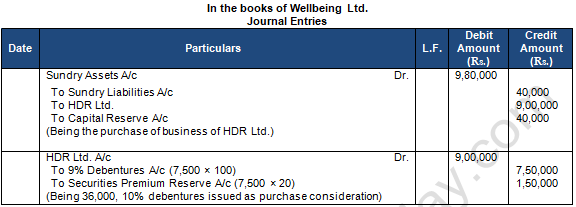

Question 22: Rama Ltd. took over following assets and liabilities of Krishna Ltd. on 1st April, 2019:

The purchase consideration of Rs. 60,00,000 was paid by issuing 12% Debentures of Rs. 100 each at a premium of 20%.

Pass the necessary Journal Entries for the above in the books of Rama Ltd.

Answer 22:

About solution:

Debenture refers to any instrument of the corporation that evidences a debt, whether or not it places a charge on the company's assets. This includes debenture stock, bonds, and other similar instruments.

Things to remember:

The corporation is released from its obligations upon redemption of its debentures, and it is also removed from the balance sheet. Also, the fact that a sizable sum of money is involved makes this a big transaction for the organization. This is the rationale behind the establishment of the DRR account by the corporation. It only makes use of this reserve to redeem bonds.

Important note:

If a firm issues debentures at a discount, the entire discount is not recorded in the company's profit and loss statement during the accounting year in which the discount is permitted. The corporation benefits from the borrowing by issuing debentures over a number of years, although the amount of such a discount is fairly substantial. Hence, a portion of the discount amount is written off each year. Usually, it is written off before these debentures are redeemed.

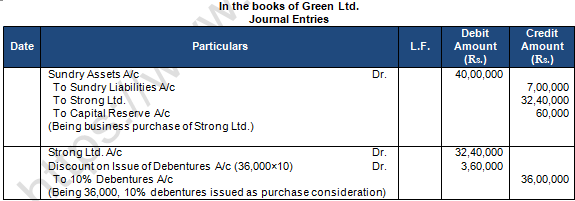

Question 23: Green Ltd. purchased the assets of Strong Ltd. for Rs. 40,00,000 and took over liabilities of 7,00,000 at an agreed value of Rs. 32,40,000. Payment was made by issuing 10% Debentures of 100 each at a discount of 10%. Pass the necessary Journal entries in the books of Green Ltd.

Answer 23:

About solution:

Debenture: The Latin word "debere" (which means to borrow) is the root of the English term "debenture."

A debenture is a document bearing the company's common seal and admitting a debt. It includes a contract for the payment of interest at a given rate due often either half-yearly or yearly on fixed dates, as well as for the repayment of principal after a set period of time, at intervals, or at the company's discretion. According to section 2(30) of The Companies Act, 2013, a "Debenture" is any security issued by a company, including bonds, debenture inventory, and other securities, whether or not they represent a charge on the company's assets.

Things to remember:

Bonds are also a kind of debt acknowledgment. Bonds were historically only issued by the government, but today semi-government and non-governmental organisations are also issuing bonds. Now, the phrases "debentures" and "bonds" are interchangeable.

Important note:

In contrast to a debenture, which just acknowledges debt, a share indicates ownership of the corporation. A debenture is a portion of borrowed capital, whereas shares are a portion of owned capital.

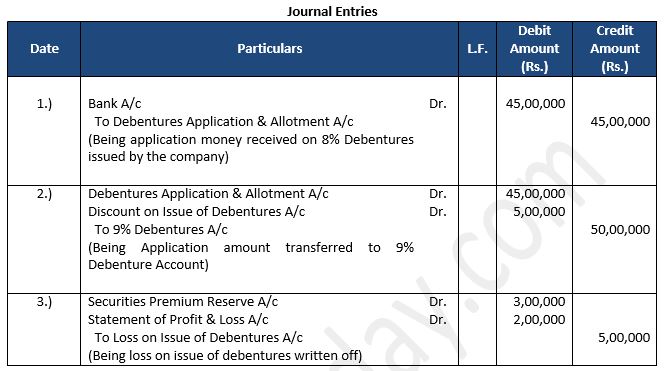

Question 24: Anthony Ltd. issued 20,000, 9% Debentures of Rs. 100 each at 10% discount to Mithoo Ltd. from whom Assets of Rs. 23,50,000 and Liabilities of Rs. 6,00,000 were taken over. Pass entries in the books of Anthony Ltd. if these debentures were to be redeemed at 5% premium.

Answer 24:

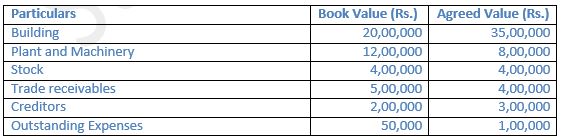

Question 25: Neeraj Ltd. took over business of Ajay Enterprises on 01 April, 2020. The details of the agreement regarding the assets and liabilities to be taken over are:

It was decided to pay for purchase consideration as Rs. 7,00,000 through Cheque and Balance by issue of 2,00,000, 9% debentures of Rs. 20 each at a premium of 25%. Journalize.

Answer 25:

Working Note:-

Number of Debenture = 57,00,000 - 7,00,000 / 25

Number of Debenture = 50,00,000/25

Number of Debenture = 2,00,000

About solution:

The company incurs loss on two counts, i.e., discount allowed at the time of issue of debentures and premium payable at the time of its redemption. Both these losses are accounted at the time of issue of debentures following the principle of prudence. The entries are:

(a) Bank A/c ……………..Dr.

To Debentures Application A/c

(b) Debentures Application A/c ……………..Dr.

Discount on issue of debentures A/c ……………Dr.

Loss on issue of debentures A/c ……………Dr.

To ….% Debentures A/c

To Premium on Redemption of Debentures A/c

Thing to remember:

In the form of a dividend that the business pays as a distribution of earnings. As a result, such a dividend is only paid when the business is profitable. Except for preference shares, which are redeemed on the due date, the amount of the share is not returned during the company's existence.

Important note:

If issued to obtain long-term loans or below short-term loans, debentures issued as collateral security are disclosed via information in Note to Accounts below Long-term Borrowings under Non-Current Liabilities.

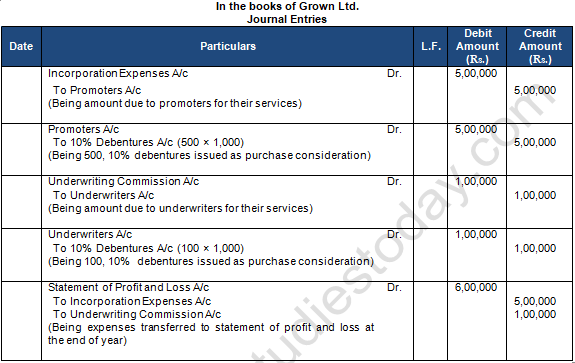

Question 26: Grown Ltd. issued 500, 10% Debentures of Rs. 1,000 each credited as fully paid-up to the promoters for their services to incorporate the company. It also issued 100, 10% Debentures of Rs. 1,000 each credited as fully paid-up to the underwriters towards their commission. Pass the Journal entries.

Answer 26:

About solution:

Discount or Loss on issue of Debentures is written off at the earliest but within the life, i.e., tenure of the debentures. It is a capital loss for the company and hence, is written off from Capital Reserve, if it has a balance. If Capital Reserve does not exist, it is written off from Securities Premium Reserve (Section 52(2)).

The Journal entry for writing off discount or loss is:

Securities Premium Reserve A/c Dr.

To Discount or Loss on Issue of Debentures A/c

Things to remember:

The whole value of the discount is not charged to the firm's profit and loss account in the accounting year in which the discount is permitted if the company issues debentures at a discount. By issuing debentures over a period of years, the corporation benefits from the borrowing despite the very large amount of the discount. Because of this, a portion of the discount is written off each year. Before these debentures are redeemed, it is often written off.

Important note:

Due to the fact that the discount on debenture issuance is recognised as a capital loss, it is recorded on the asset side of the company's balance sheet under the heading "Miscellaneous Expense" up until and to the extent that it is not wiped off.

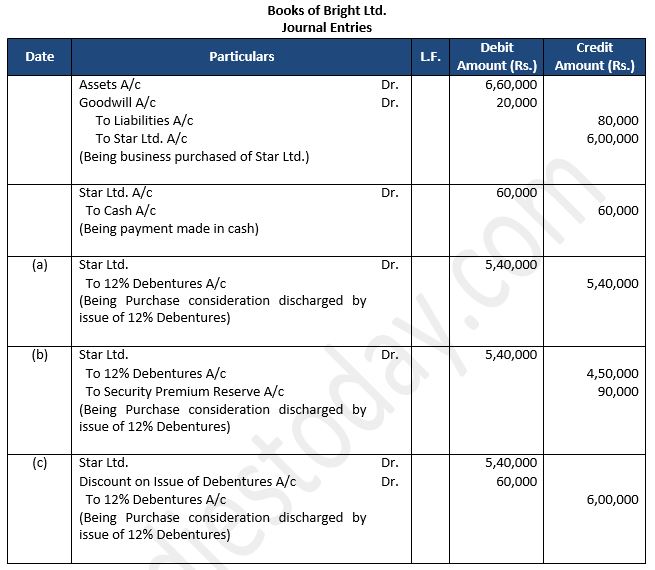

Question 27: Bright Ltd. took over the assets of Rs. 6,60,000 and liabilities of Rs. 80,000 of Star Ltd. for an agreed purchase consideration of Rs. 6,00,000 payable 10% in cash and the balance by the issue of 12% Debentures of Rs. 100 each. Give necessary Journal entries in the books of Bright Ltd., assuming that:

Case (a): The debentures are issued at par.

Case (b): The debentures are issued at 20% premium.

Case (c): The debentures are issued at 10% discount.

Answer 27:

About solution:

1. Number of Debentures to be issued = 5,40,000/(100+20)

Number of Debentures to be issued = 4,500 Debentures

2. Number of Debentures to be issued = 5,40,000/(100-10)

Number of Debentures to be issued = 6,000 Debentures

Things to remember:

Zero coupon rate debentures: There is no set interest rate on these debentures. Such debentures are issued at a significant discount in order to compensate the investors, and the difference between the nominal value and the issue price is recognised as the amount of interest pertaining to the tenure of the debentures.

Important note:

If a firm issue discounted debentures, the full amount of the discount is not recorded in the company's profit and loss statement for the accounting year in which the discount is permitted. The corporation benefits from the borrowing by issuing debentures over a number of years, although the amount of such a discount is fairly substantial. Hence some part of the amount of discount is written off every year. Usually, it is written off before these debentures are redeemed.

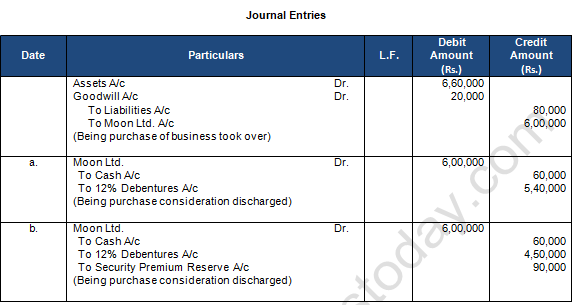

Question 28: Star Ltd. took over the assets of Rs. 6,60,000 and liabilities of Rs. 80,000 of Moon Ltd. for Rs. 6,00,000. Give necessary Journal entries in the books of Star Ltd. assuming that:

Case (a): The purchase consideration was payable 10% in cash and the balance in 5,400; 12% Debentures of Rs. 100 each.

Case (b): The purchase consideration was payable 10% in cash and the balance in 4,500; 12% Debentures of Rs.100 each issued at 20% premium.

Answer 28:

About solution:

1. Number of Debentures to be issued = (6,00,000-60,000)/100

Number of Debentures to be issued = 5,400; 12% Debentures

2. Number of Debentures to be issued = 5,40,000/(100+20)

Number of Debentures to be issued = 4,500; 12% Debentures

Things to remember:

When a firm issues debentures, it is acknowledging the debt it has taken on by issuing a certificate withits stamp. Debenture issuance by a firm follows a similar process to share issuance. Letters of allotment are issued together with a prospectus and an invitation to apply. Money paid for applications is reimbursed in the event of rejection. Excess application funds may be applied to following calls in the event of partial allocation.

Important note:

Debentures are redeemable after a predetermined time throughout the company's existence. In most cases, it places a charge on the company's assets. Regardless of the company's financial performance, a predetermined rate of interest is paid to debenture holders.

Question 29: A company took a loan of Rs. 4,00,000 from Bandhan Bank Ltd. and issued 8% Debentures of Rs. 4,00,000 as a collateral security.

Answer 29:

About solution:

When a business takes a loan or overdraft from a bank or another financial institution, a collateral security may be described as a subsidiary, secondary, or supplementary security in addition to the primary security. As a secured loan for the aforementioned loan, it may pledge or mortgage certain assets.

Things to remember:

Nonetheless, lending Institutions may demand on extra assets as collateral security so that, in the event that the proceeds from the sale of the principal security fall short of the loan amount, the loan amount can be recovered in full with the help of collateral security. In this case, in addition to some other assets that have already been pledged, the corporation may also issue its own debentures to the lenders. Debentures issued as Collateral Security are referred to as such a debenture issue.

Important note:

In the event that the company defaults on the loan and interest payments, the lender is free to collect his money from the sale of the primary security. If the realizable value of the primary security is insufficient to cover the entire amount, the lender has the option of using the benefit of collateral security, which allows the lender to redeem or sell the debentures on the open market.

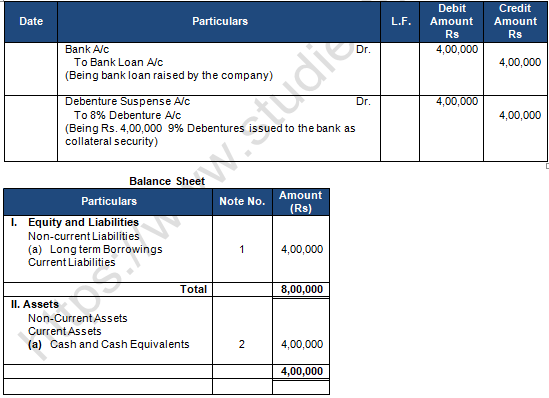

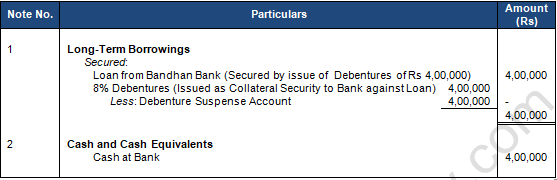

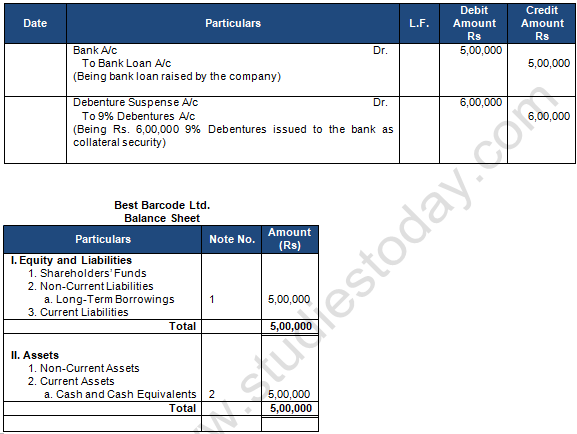

Question 30: Best Barcode Ltd. took a loan of Rs. 5,00,000 from a bank giving Rs. 6,00,000; 9% Debentures as collateral security. Pass journal entries regarding issue of debentures, if any, and show this loan in the Balance Sheet of the company.

Answer 30:

About solution:

Balance Sheet and Statement of Profit and Loss of a company is prepared in the form prescribed in Schedule III of the Companies Act, 2013. It prescribes that liabilities and assets be classified into non- current and current.

Current Liabilities are those liabilities which are:

1. Expected to be settled in company’s normal operating cycle.

2. Held primarily for the purposes of being traded.

3. Due to be settled in which 12 months after the reporting date

4. There is no unconditional right to defer the settlement of liability for a period of a least 12 moneths after the reporting date.

Current Assets are those assets which are:

1. Expected to be realized in or intended for sale or consumption in the company’s normal operating cycle;

2. Held primarily for the purpose of being traded

3. Expected to be realized within 12 months from the reporting date.

4. Cash and Cash Equivalents unless they are restricted from being exchange or used to settle a liability for at least 12 months after the Balance Sheet.

Things to remember:

Security provided in addition to the principal security is known as collateral security. It is a supplementary security or subsidiary security. Debentures may be issued by a firm as secondary security in addition to the primary security whenever it obtains a loan from a bank or other financial institution. Such a bond issue is referred to as a "issue of bonds as collateral security."

Important note:

Only in the event that the company defaults on the loan balance and the principle security is depleted would the lender have a claim over such debentures. If the need to exercise this right doesn't materialize, the corporation will receive the debentures back. Because the corporation pays interest on the loan, no interest is paid on the debentures issued as collateral security.

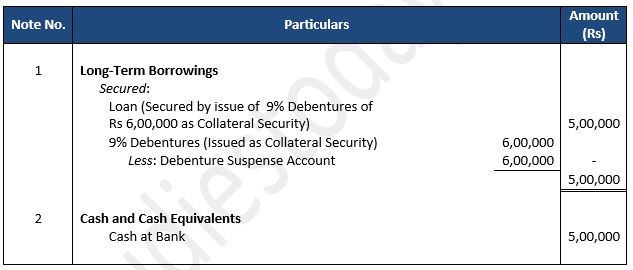

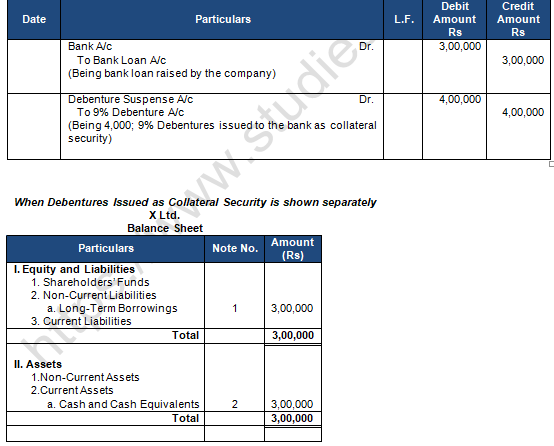

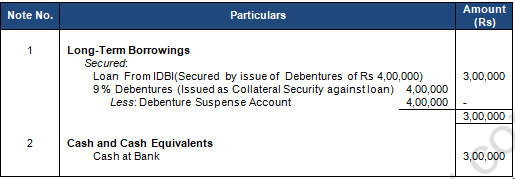

Question 31: X Ltd. took a loan of Rs. 3,00,000 from IDBI Bank. The company issued 4,000; 9% Debentures of Rs. 100 each as a collateral security for the same. Show how these items will be presented in the Balance Sheet of the company.

Answer 31:

About solution:

Prefixing "Debentures" with the interest rate is a frequent practise; for example, if the interest rate is 10%, the title of the debentures will be "10% Debentures." The corporation treats it as long-term borrowings or external equity. Often, a charge on the company's assets is used to secure it. Interest paid on debentures is deducted from profits.

Things to remember:

Security provided in addition to the principal security is known as collateral security. It is a supplementary security or subsidiary security. Debentures may be issued by a firm as secondary security in addition to the primary security whenever it obtains a loan from a bank or other financial institution. Such a bond issue is referred to as a "issue of bonds as collateral security.

Important note:

Only in the event that the company defaults on the loan balance and the principle security is depleted would the lender have a claim over such debentures. If the need to exercise this right doesn't materialize, the corporation will receive the debentures back. Because the corporation pays interest on the loan, no interest is paid on the debentures issued as collateral security.

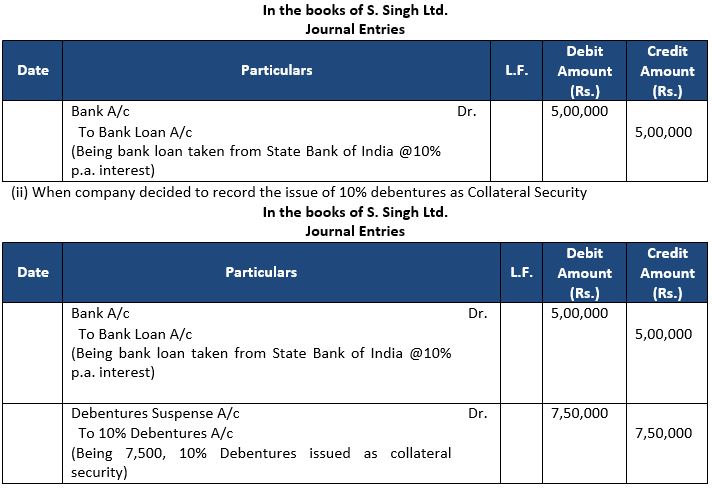

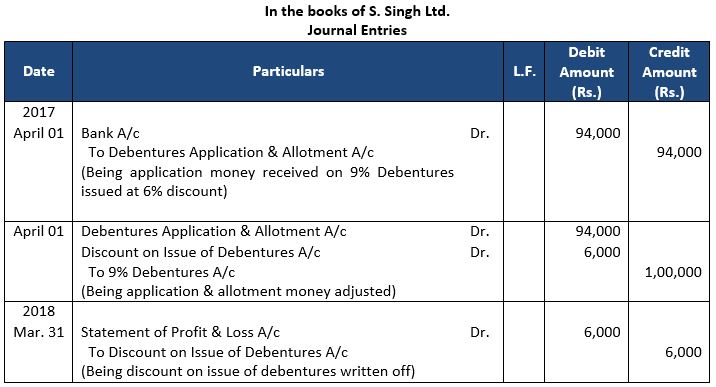

Question 32: S. Singh Limited obtained a loan of Rs. 5,00,000 from State Bank of India @ 10% p.a. interest. The company issued Rs. 7,50,000, 10% Debentures of Rs. 100 each in favors of State Bank of India as Collateral Security. Pass necessary Journal entries for the above transactions:

(i) When company decided not to record the issue of 10% Debentures as Collateral Security.

(ii) When company decided to record the issue of 10% Debentures as Collateral Security.

Answer 32:

(i) When company decided not to record the issue of 10% debentures as Collateral Security

About solution:

A unit of loan amount is a debenture. A firm offers debentures when it wants to borrow money from the general public. A debenture holder is a person who holds a debenture or debentures. A document bearing the business seal is called a debenture. It serves as an acknowledgement of the company's receipt of a loan with a notional value equivalent to the debenture. It displays the redemption date, interest rate, and method of payment. The company's creditor is one of its debenture holders.

Things to remember:

Dividends are the name given to returns on shares, whereas interest is the name given to returns on debentures. The return on shares may change from year to year depending on the company's profits, whereas the interest rate on debentures is fixed. The payment of interest is a charge on earnings and must be made even if there are no profits, in contrast to the payment of dividends, which is an appropriation of profits.

Important note:

Collateral security is defined as security provided for loans in addition to the primary or principle security. When the borrower is unable to provide any other asset as a collateral security, debentures may be issued as a substitute.

Question 33: On 1st April, 2021, Bingo Ltd. issued Rs. 20,00,000, 9% Debentures of Rs. 100 each at a premium of 10%, redeemable at a premium of 5%.

Pass the necessary Journal entries for issue of debentures in the books of Bingo Ltd.

Answer 33:

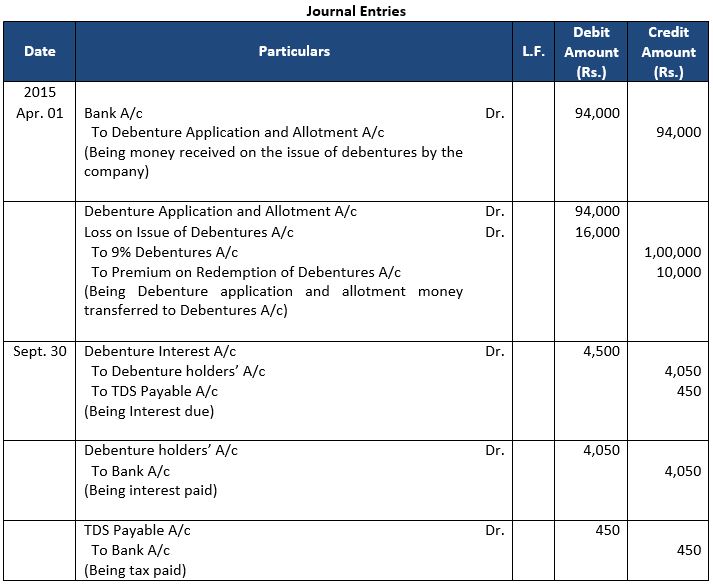

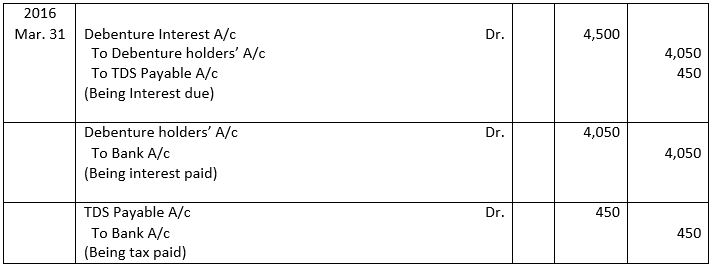

Question 34: ZK Ltd. issued Rs. 4,00,000, 9% Debenture of Rs. 100 each at a discount of 5% redeemable at a premium of 10%. Pass necessary Journal entries for the above transactions in the Books of ZK Ltd.

Answer 34:

Question 35: On 1st April, 2018, Sakshi Ltd. issued 1,000, 11% Debenture of Rs. 100 each at a discount of 6%, redeemable at a premium of 5% after three years.

Pass the necessary Journal entries for the issue of debenture in the books of Sakshi Ltd.

Answer 35:

Question 36: Care Cosmetics Ltd. issued 50,000; 9% Debentures of Rs. 10 each on 1st April, 2021 redeemable at a premium of 10% after 10 years. According to the terms of issue, Rs. 4 is payable on application and balance on allotment of debentures. Record necessary Journal entries regarding issue of debentures.

Answer 36:

Things to remember:

When a business issues debentures, it is required to make periodic fixed percentage (half-yearly) interest payments until the debentures are redeemed. The interest payable is computed using the nominal value of the debentures, and this percentage is typically included in the name of the debentures,

Important note:

Debenture interest is a charge against the company's profit and is due whether or not the company has made any money. If the interest payment on debentures exceeds the allowed maximum, a firm is required by the Income Tax Act of 1961 to deduct income tax at a stipulated rate. To be deposited with the tax authorities, it is known as Tax Deducted at Source (TDS). Of course, the debenture holders are free to offset this sum with the tax owed by them.

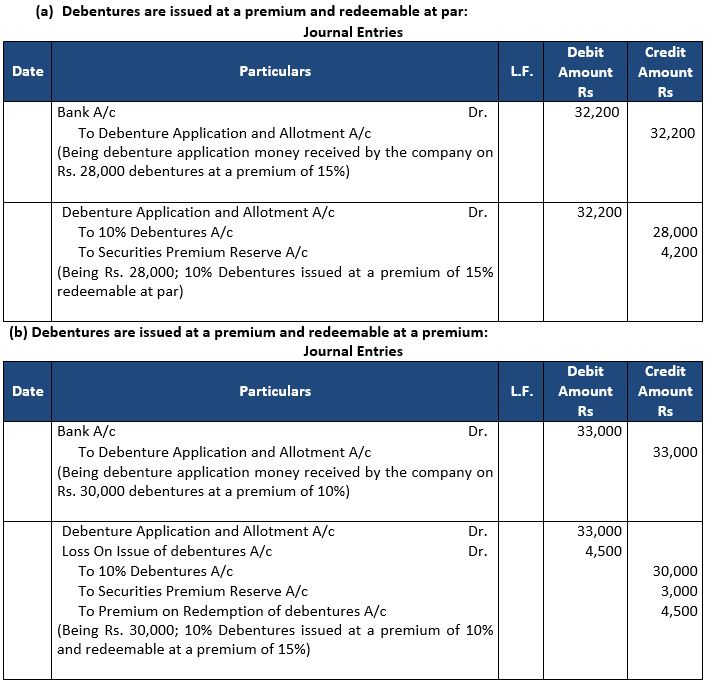

Question 37: Pass necessary Journal entries relating to the issue of debentures for the following:

(a) Issued Rs. 28,000; 10% Debentures of Rs. 100 each at a premium of 15% redeemable at par.

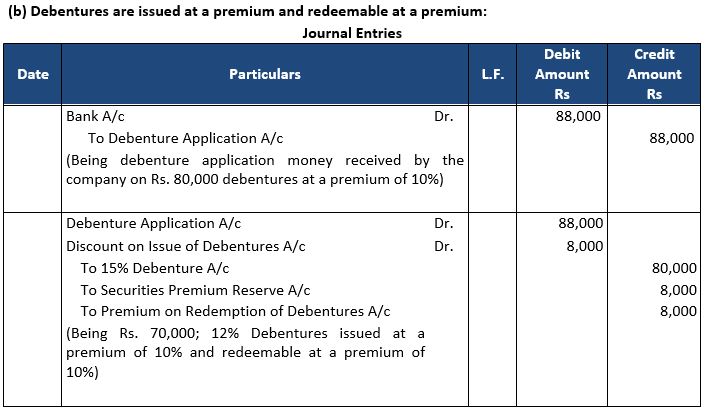

(b) Issued Rs. 30,000; 10% Debentures of Rs. 100 each at a premium of 10% and redeemable at a premium of 15%.

(c) Issued Rs. 80,000; 10% Debentures of Rs. 100 each at par repayable at a premium of 10%.

Answer 37:

About solution:

It is an agreement between the company and the holders of its debentures for the repayment of the principle amount on a specific date and the payment of interest at a set rate until the principal is repaid.

It serves as proof of an obligation owed to the holder, typically in the form of a loan that is secured by a charge.

Things to remember:

Another name for the debenture redemption reserve is sinking fund. This fund is established by the company by designating a portion of its revenues to redeem debentures at maturity and then designating this sum to suitable investments.

Important note:

Debentures are sold to the general public by the companies to raise money for growth and expansion. The main benefit of this strategy is that it has a lower cost of capital because issuing equity carries a greater price tag than issuing debt. The business also redeems its stock after a long time. As a result, the business has enough time to fulfill its obligations.

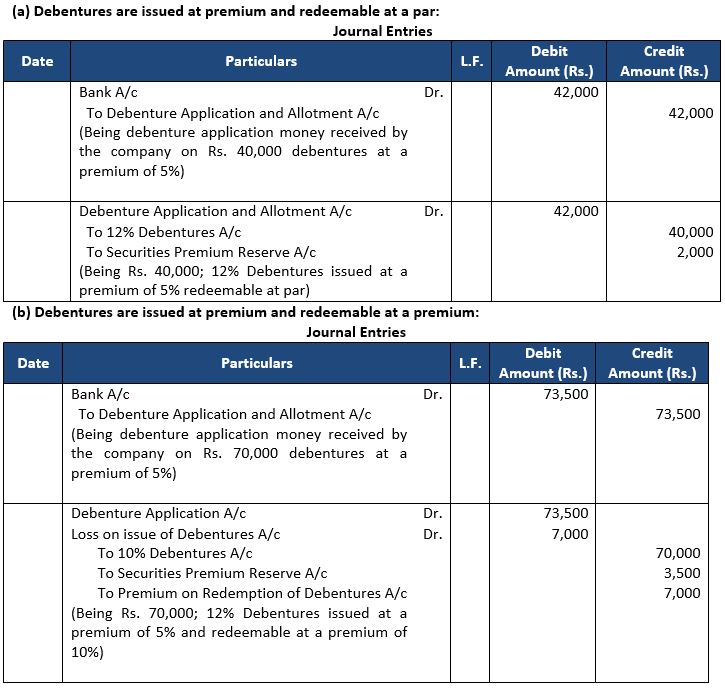

Question 38: Pass necessary Journal entries for the issue of debentures in the following cases:

(a) Rs. 40,000; 12% Debentures of Rs. 100 each issued at a premium of 5% redeemable at par.

(b) Rs. 70,000; 12% Debentures of Rs. 100 each issued at a premium of 5% redeemable at Rs. 110.

Answer 38:

About solution:

Interest on debentures is calculated at fixed rate on its nominal (face) value payable quarterly, half yearly or yearly as per the terms of issue. Rate of interest is prefixed to the debentures, say 9% Debentures and, therefore, is payable even if the company incurs loss. Interest on debentures is a charge against profit. Interest may be subject to tax deduction at source (TDS).

(a) When the interest is due:-

Debentures Interest or Interest on Debentures A/c …Dr.

To Debenture holders’ A/c

To Income Tax Payable A/c

(b) When the interest is paid (ignore tax):-

Debentures holders’ A/c …Dr.

To Bank A/c

Thing to remember:

In terms of both content and texture, a bond is comparable to a debenture. It is an acknowledgment of debt that the business has issued and has been signed by a designated signatory. Bonds were traditionally issued by the government. Today, however, non-governmental and semi-governmental organizations are also issuing bonds as a means of acknowledging debt.

Important note:

Whereas the return on debentures is known as interest, the return on shares is known as a dividend. Depending on the company's profits, the rate of return on shares may change from year to year, whereas the rate of interest on debentures is fixed. Dividend payments are an appropriation of profits, whereas interest payments are charges against profits that must be made even in the absence of a profit.

Question 39: Chiranjeevi Limited issued 2,000, 10% Debentures of Rs. 100 each. Pass the necessary Journal entries for the issue of debentures in the following cases:

(a) When debenture were issued at 10% premium, redeemable at% premium.

(b) When debenture were issued at 5% discount, redeemable at 10% premium.

(c) When debenture were issued at par, redeemable at a premium of 10%.

Answer 39:

Question 40: Pass necessary Journal entries for the issue of debentures in the following cases:

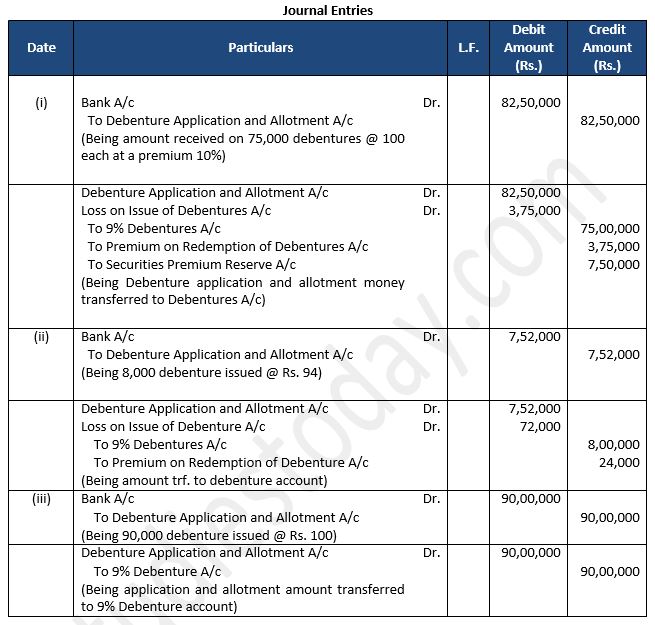

(i) Issued Rs. 75,00,000, 9% Debentures of Rs. 100 each at a premium of 10% redeemable at a premium of 5% after 3 years.

(ii) Issued 8,000, 9% Debentures of Rs. 100 each at a discount of 6% redeemable at a premium of 3% after 5 years.

(iii) Issued 90,000, 9% Debentures of Rs. 100 each at par, redeemable at par after 4 years.

Answer 40:

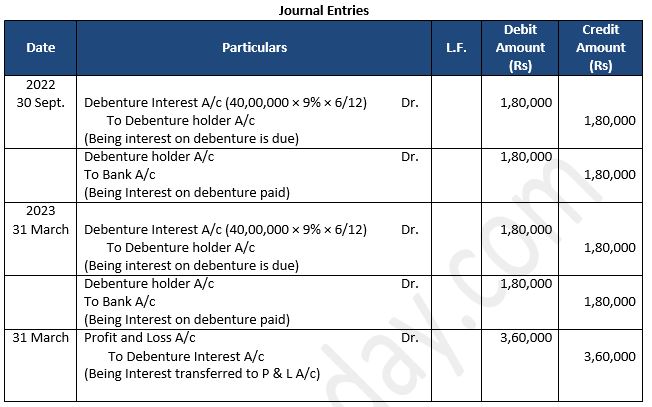

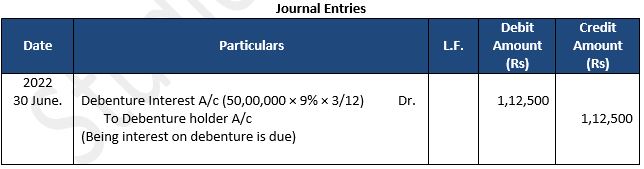

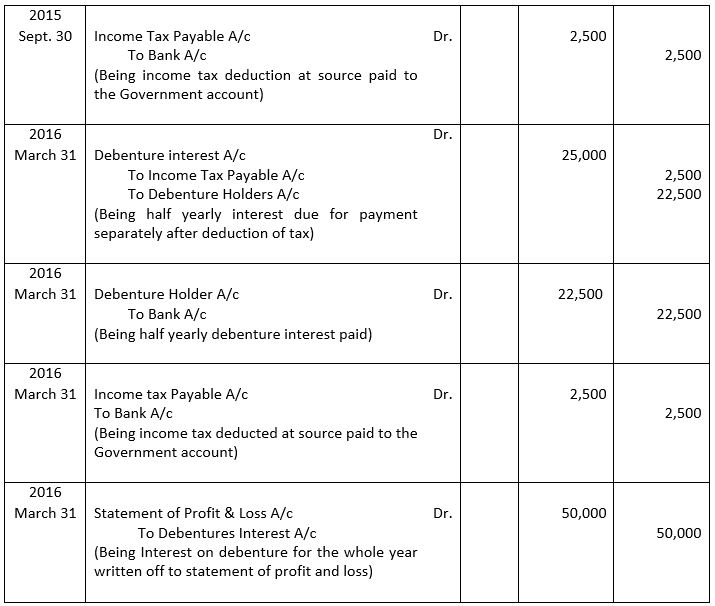

Question 41: Assuming that the interest was paid half yearly on 30th September and 31st March, give Journal entries relating to debenture interest for the half year ended 31st March, 2023.

Answer 41:

Question 42: Pratham Ltd. issued 50,000, 9% Debentures of ₹ 100 each on 1st April, 2022 at 10% discount, redeemable at 10 premium. Interest is payable quarterly on 30th June, 20th September, 31st December and 31st March. Pass the Journal entries for interest for the period ended 30th June, 2022.

Answer 42:

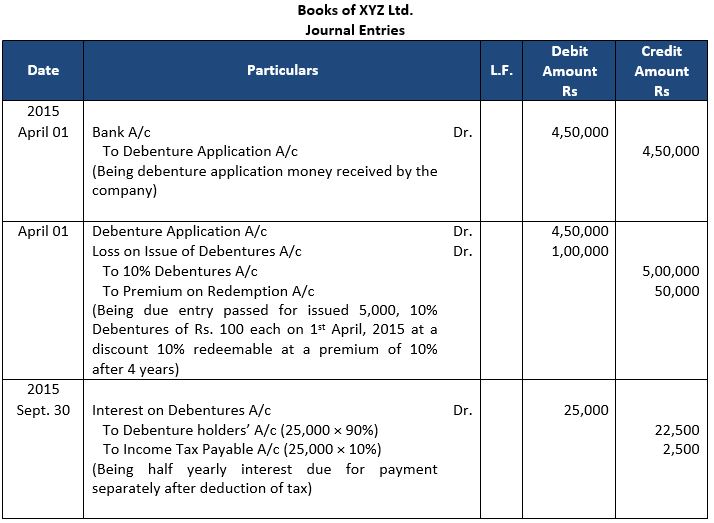

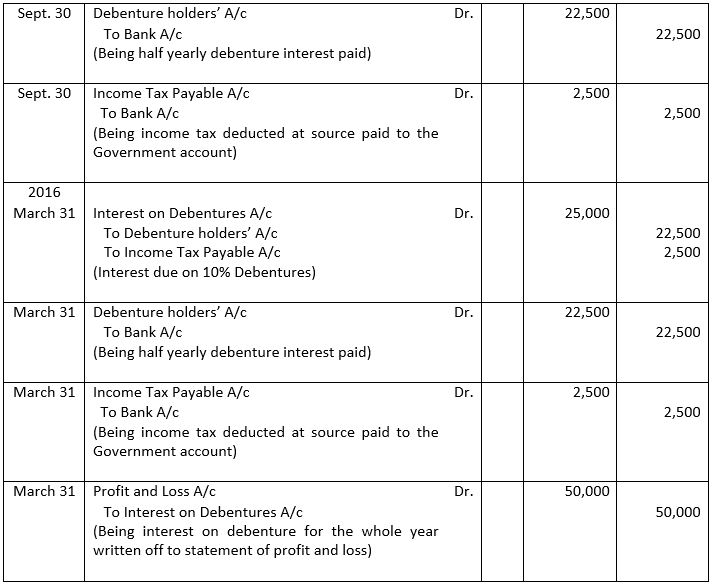

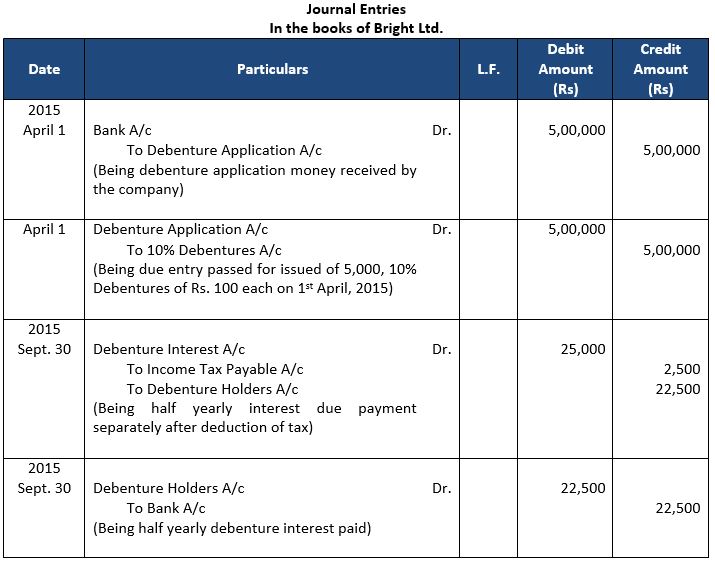

Question 43: Bright Ltd. issued 5,000; 10% Debentures of ₹ 100 each on 1st April, 2022. The issue was fully subscribed As per the terms of issue, interest on the debentures is payable half-yearly on 30th September and 31st March.

Pass necessary Journal entries related to the debentures interest for the year ending 31st March, 2023 and transfer of interest on debentures of the year to the Statement of Profit & Loss.

Answer 43:

Things to remember:

An interest payment is a reward given to all holders of debentures for their investment in the company's debentures. Typically, interest is charged against profits and paid on the face value of the debentures in a periodic, methodical manner at a defined rate of interest.

Important note:

Have you ever considered the connotation this prefix has. It is the annual interest rate that will be paid to the holders of debentures. In general, businesses pay interest on their debentures every six months. The corporation deducts income tax on such interest at the source.

Question 44: On 1st April, 2022, V.V.L. Ltd. issued 1,000, 9% Debentures of Rs. 100 each at a discount of 6%, redeemable at a premium of 10% after three years. Pass necessary journal entries for the issue of debentures and debenture interest for the year ended 31st March, 2023, assuming that interest is payable on 30th September and 31st March. The company closed its books on 31st march, every year.

Answer 44:

About solution:

Discount or Loss may be written off from Capital Reserve or from Securities Premium Reserve or from Statement of Profit and Loss. Accounting entry will be as follows:

Securities Premium Reserve A/c ……………Dr.

To Discount or Loss on Issue of Debentures A/c

Things to remember:

When a business issues debentures, it is required to pay interest on those securities at a predetermined percentage (once every six months) until the debentures are repaid. The nominal value of the debentures is used to compute interest payable, and this percentage is typically included in the name of the debentures (e.g., 8% debentures, 10% debentures, etc.).

Important note:

Debentures' interest is routinely paid at a predetermined rate on their face value. It should be highlighted that regardless of the company's revenue position, this interest must be paid to the holders as a charge against the company's profit.

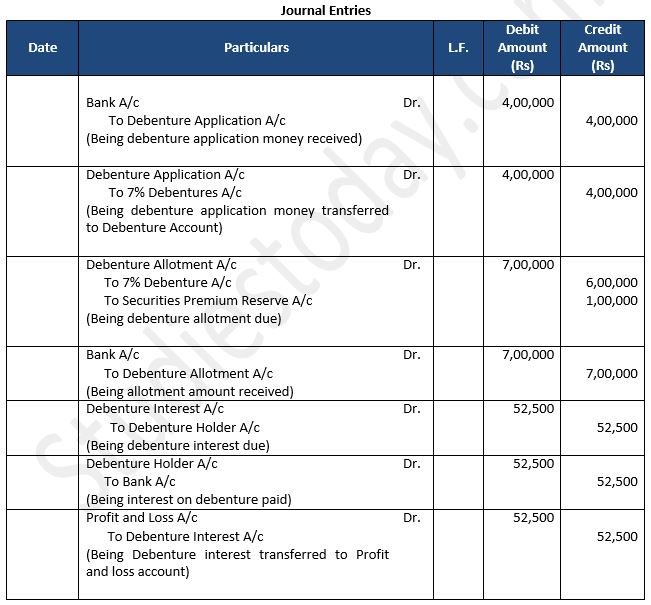

Question 45: Pawan Hans Ltd. issued on 1st July, 2022, 10,000, 7% Debentures of ₹ 100 each for subscription at 10% premium payable ₹ 40 on application and balance on allotment. The debentures were subscribed and due amounts were received. Interest was payable on 31st March each year.

Pass the Journal entry for issue of debentures and interest for the year ended 31st March, 2023 and transfer the interest to Statement of Profit & Loss.

Answer 45:

Question 46: Suzlon Ltd. issued on 1st July, 2022, 20,000, 7% Debentures of ₹ 100 each for subscription at 10% premium payable ₹ 40 on application; ₹ 40 (including premium) on allotment and balance on first and final call. The debentures were subscribed and allotted. The company has not made first and final call during the year ended 31st March, 2023. Interest was payable on 31st March each year.

Pass the Journal entry for issue of debentures and interest for the year ended 31st March, 2023 and transfer the interest to Statement of Profit & Loss.

Answer 46:

Question 47: Kitply Ltd. issued Rs. 2,00,000, 10% Debentures at a discount of 5% .The terms of issue provide the repayment at the end of 4 years. Kitply Ltd.has a balance of Rs. 5,00,000 in Securities Premium Reserve. The company decided to write off discount on issue of debentures from Securities Premium Reserve in the first year. Pass the journal entry.

Answer 47:

About solution:

The amount of discount to be written off from Securities Premium Reserve Account in the First Year

Securities Premium Reserve = Rs. 2,00,000 × 5%

Securities Premium Reserve = Rs. 10,000

Things to remember:

If firm issues discounted debentures, the full amount of the discount is not recorded in the company's profit and loss statement for the accounting year in which the discount is permitted. The corporation benefits from the borrowing by issuing debentures over a number of years, although the amount of such a discount is very substantial. Hence, a portion of the discount amount is written off each year. Usually, it is written off before these debentures are redeemed.

Important note:

Due to the fact that the discount on debenture issuance is recognized as a capital loss, it is recorded on the asset side of the company's balance sheet under the heading "Miscellaneous Expense" up until and to the extent that it is not wiped off.

Question 48: Mercury Ltd. issued ₹ 10,00,000; 9% Debentures of ₹ 100 each at a discount of 6% on 1st April, 2022. These debentures are to be redeemed equally. Spread over 5 annual installments. It had balance in Capital Reserve of ₹ 75,000.

Pass the Journal entries for issue of debentures and writing off the discount.

Answer 48:

About solution:

It is a piece of paper called a debenture certificate. Debenture is an evidence of a debt to the holder typically arising out of a loan and mostly secured by a charge. It is an acknowledgement of debt by the company.

Things to remember:

The amount of discount will be dispersed equally throughout the number of years between the issuance of the debentures and their redemption when they are to be redeemed after a set time.

Important note:

The corporation benefits from the borrowing by issuing debentures over a number of years, although the amount of such a discount is fairly substantial. Hence, a portion of the discount amount is written off each year. Usually, it is written off before these debentures are redeemed.

Question 49: Gladiators Ltd. issued 10,000; 8% Debentures of ₹ 100 each at a discount of 5%, redeemable at a premium of 5% payable along with application. It had balance of ₹ 70,000 in Securities Premium and ₹ 50,000 in Capital Reserve. The debentures were fully subscribed and amounts were duly received.

Pass the necessary Journal entries for issue of debentures and writing off Loss on issue of Debentures.

Answer 49:

Question 50: Sujata Ltd. invited applications for issuing 50,000, 9% Debentures of ₹ 100 each at a discount of 10% redeemable at par after 5 years. The debentures were fully subscribed and all money was duly received. The company had a balance of ₹ 3,00,000 in Securities Premium which it decided to use for writing off the discount/loss on issue of debentures. It also decided to write off the remaining discount/loss on issue of debentures in the first year.

Pass the Journal entries for issue of debentures and for writing off discount/loss on issue of debentures.

Answer 50:

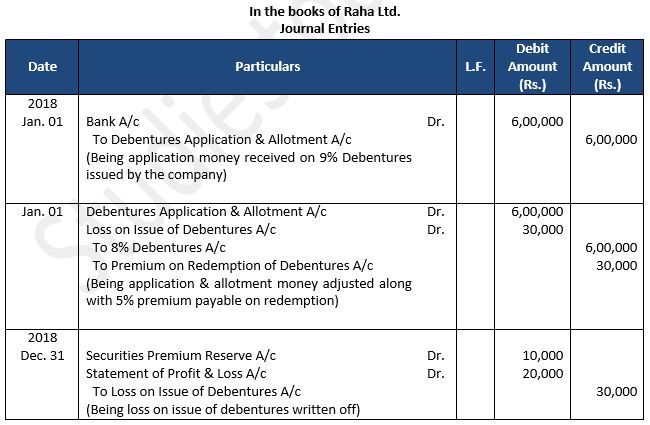

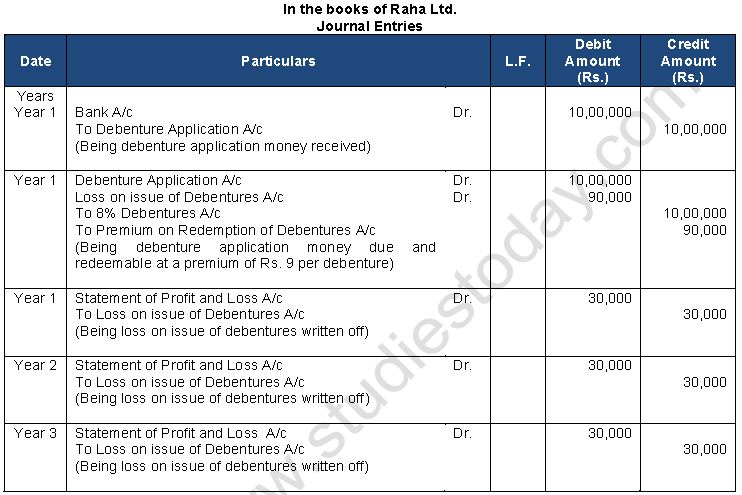

Question 51: On 1st January, 2018, Raha Ltd. issued 6,000, 8% Debentures of nominal (face) value of Rs. 100 each redeemable at 5% premium in equal proportions at the end of 5, 10 and 15 years. It has a balance of Rs.10,000 in Securities Premium Reserve. Pass Journal entries. Also give Journal entries for writing off Loss on Issue of Debentures.

Answer 51:

About solution:

Debentures' discount or loss on issuance is written off as a capital loss in the year they are issued. The securities premium reserve may be used to write off a discount or loss [section 52(2)]. If capital earnings are absent or insufficient, the amount should be deducted from the year's revenue profits.

Things to remember:

It is an agreement between the company and its debenture holders for repayment of the principal amount on a specified date along with interest at a pre-determined rate charged on the principal amount until the principal is repaid.

Important note:

In contrast to a debenture, which just acknowledges debt, a share indicates ownership of the corporation. A debenture is a portion of borrowed capital, whereas shares are a portion of owned capital.

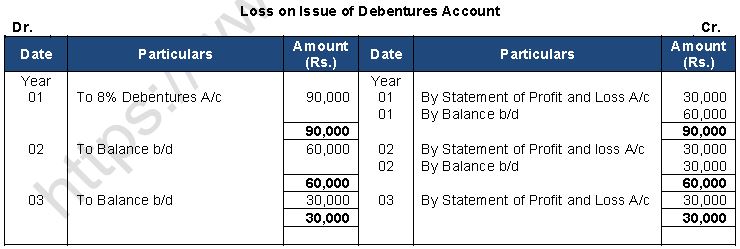

Question 52: Global Ltd. issued 10,000, 8% Debentures of Rs. 100 each redeemable in four equal installments by draw of lots from the end of 3 years at a premium of Rs. 9. Pass the Journal entries for writing off the Loss on Issue of Debentures. Also prepare Loss on issue of Debentures Account.

Answer 52:

About solution:

Loss on Issue of Debentures: Loss on issue of Debentures, whether consisting of only premium payable on redemption or discount on issue of debentures plus premium payable or redemption is a capital loss and should be dealt with in the same manner as discount on the issue of debentures have discount and illustrated above. The Journal entry for writing off the Loss on issue of Debentures is:

Capital Reserve A/c ……………..Dr.

Securities Premium Reserve A/c……………Dr.

Statement of Profit and loss A/c ……………. Dr.

To Loss on issue of Debentures A/c (with the amount of loss written off)

Things to remember:

In the event that the firm issues debentures at a discount, the entire discount is not applied to the company's profit and loss account during the accounting year in which the discount is permitted. By issuing debentures over a period of years, the corporation benefits from the loan while paying a very steep discount. As a result, an annual write-off of a portion of the discount amount occurs.

Important note:

The corporation is released from its obligations upon redemption of its debentures, and it is also removed from the balance sheet. Also, the fact that a sizable sum of money is involved makes this a big transaction for the organizations. This is the rationale behind the establishment of the DRR account by the corporation. It only makes use of this reserve to redeem bonds.

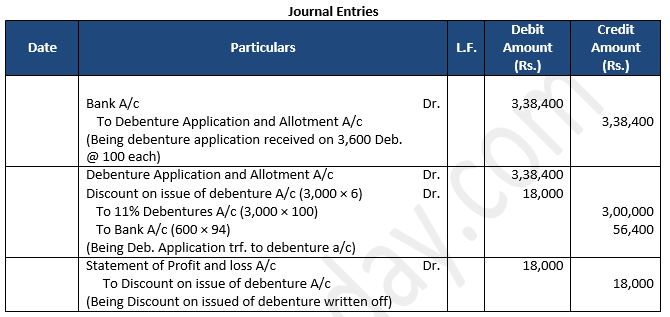

Question 53: Garvit Ltd. invited applications for issuing 3,000, 11% Debentures of ₹ 100 each at a discount of 6%. The full amount was payable on application. Applications were received for 3,600 debentures. Applications for 600 debentures were rejected and the application money was refunded. Debentures were allotted to the remaining applicants.

Pass the necessary Journal entries for the above transactions, including writing off the Discount on Issue of Debentures, in the books of Garvit. Ltd.

Answer 53:

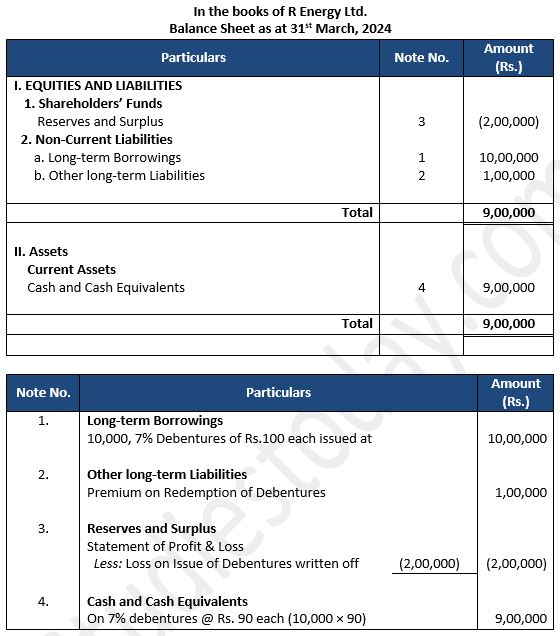

Question 54: On 1st June, 2020, R Energy Ltd. issued 10,000, 7% Debentures of Rs. 100 each at a discount of 10% redeemable at a premium of 10% at the end of five years. All the debentures were subscribed and allotment was made. Prepare the Balance Sheet (extract) as at 31st March, 2024.

Answer 54:

About solution:

When a business takes a loan or overdraft from a bank or another financial Institution, a collateral security may be described as a subsidiary, secondary, or supplementary security in addition to the primary security. As a secured loan against the said loan, it may pledge or mortgage some assets.

Things to remember:

They are the company's borrowings, thus they are viewed as liabilities and are consequently listed in the Equity and Liabilities section of the balance sheet. Depending on the duration of such debentures, they may be stated as either a Non-Current Liability or a Current Liability. It's crucial to keep in mind that debentures are displayed under Non-current Liabilities as Long-term Borrowings unless the question specifically specifies otherwise.

Important note:

In order to ensure that the loan amount may be recovered in full with the help of collateral security in the event that the proceeds from the sale of the principal security fall short of the loan amount, institutions may insist on additional assets as collateral security. When this occurs, the business may provide its own debentures to the lenders in addition to some other assets that have previously been pledged. Debentures issued as Collateral Security are what this type of debenture issue is known as.

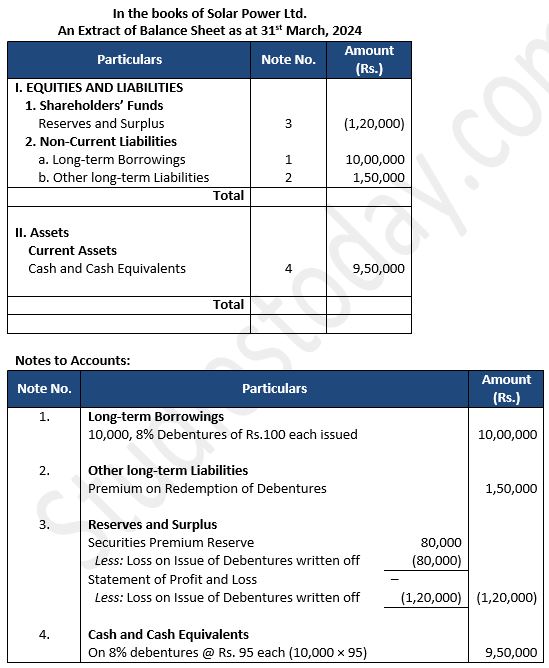

Question 55: On 1st April, 2022, Solar Power Ltd. issued 10,000, 8% Debentures of Rs. 100 each at a discount of 5% redeemable at a premium of 15% at the end of five years. All the debentures were subscribed and allotment was made. The company had balance in Securities Premium Reserve of Rs. 80,000.

Prepare the Balance Sheet (extract) as at 31st March, 2024.

Answer 55:

About solution:

The lender is free to collect his money from the sale of the primary security in the event that the company defaults on the loan and interest. If the realizable value of the primary security is insufficient to cover the entire amount, the lender has the option to use the benefit of collateral security, which allows debentures to be either presented for redemption or sold on the open market.

Things to remember:

According to the Income Tax Act of 1961, corporations that issue debentures must deduct TDS at a specific rate of interest from debenture interest payments. But only if the payable interest amount exceeds the specified threshold is such a tax applied. The denture issuing company deposits the tax that was thusly obtained with the appropriate income tax authorities.

Important note:

Security provided in addition to the principal security is known as collateral security. It is a supplementary security or subsidiary security. A firm may issue its debentures as secondary security, in addition to the primary security, if it obtains a loan from a bank or other financial institution.

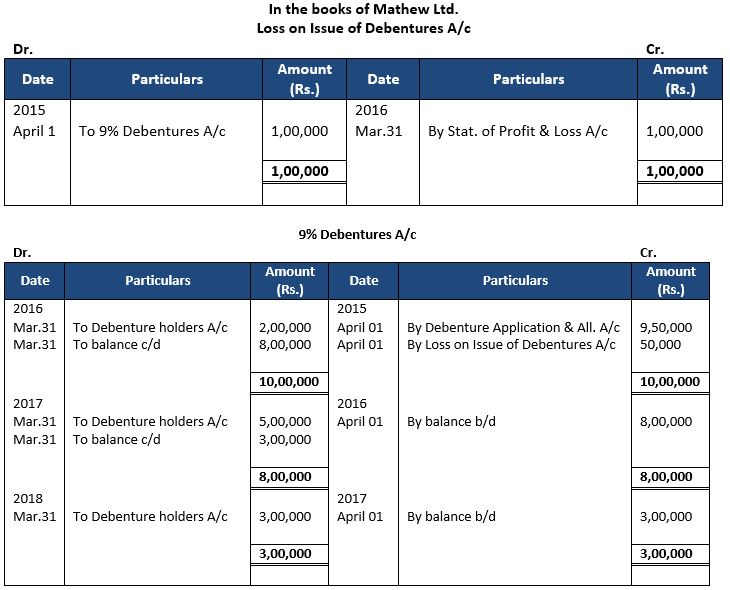

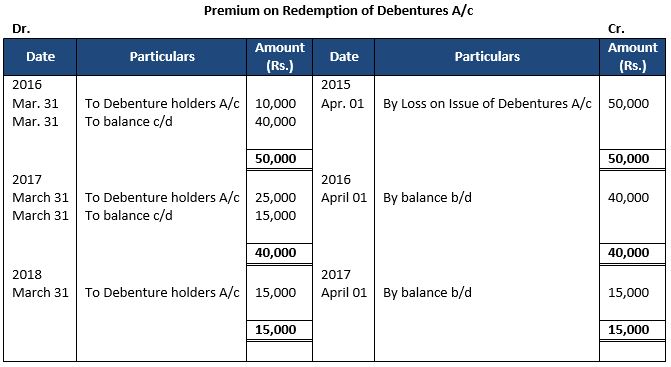

Question 56: On 1st April, 2015, Mathew Ltd. issued 10,000, 9% Debentures of Rs. 100 each at a discount of 5%, redeemable at a premium of 5%. These debentures were redeemable as follows:

On 31st March, 20162,000 Debentures;

On 31st March, 20175,000 Debentures;

On 31st March, 20183,000 Debentures.

Prepare the Loss on Issue of Debentures Account, Debentures Account and Premium on Redemption of Debentures Account for three years.

Answer 56:

About solution:

If firm issues discounted debentures, the full amount of the discount is not recorded in the company's profit and loss account during the accounting year in which the discount is permitted.

Things to remember:

This discount is fairly substantial, and the corporation benefits from the loan by issuing debentures over a period of time. Because of this, a portion of the discount is written off each year. Before these debentures are redeemed, it is often written off.

Important note:

Collateral security is provided for loans in addition to the prime or principle security. When the borrower is unable to provide any other asset as a collateral security, debentures may be issued as a substitute.

Question 57: Dev Ltd. acquired running business of Amrit Ltd. having assets of ₹ 10,00,000 and liabilities of ₹ 2,50,000. 9% Debentures of ₹ 100 each were issued for the acquisition of business at a premium of ₹ 20 per debenture. The company issued 10,000, 8% Debentures of ₹ 100 each redeemable at premium of ₹ 20 per debenture after 5 years.

You are required to pass the Journal entries for the above transactions.

Answer 57:

Things to remember:

Debt that the company raised in the form of debentures is repaid in the process of "redemption of debentures." Debentures with a set maturity date are issued by the company. The corporation pays the holders of debentures back for their investment at maturity. The cost of repayment by the corporation can be higher, lower, or even the same as the face value of the debentures. The corporation must therefore abide by all of the criteria in the prospectus when issuing debentures.

Important note:

The corporation is released from its obligation and is taken off the balance sheet upon redemption of its debentures. Also, because a substantial sum of money is involved, this transaction is important for the organisation. Due to this, the business also establishes a Debenture Redemption Reserve (DRR) account. This reserve is solely applied to the redemption of debentures.

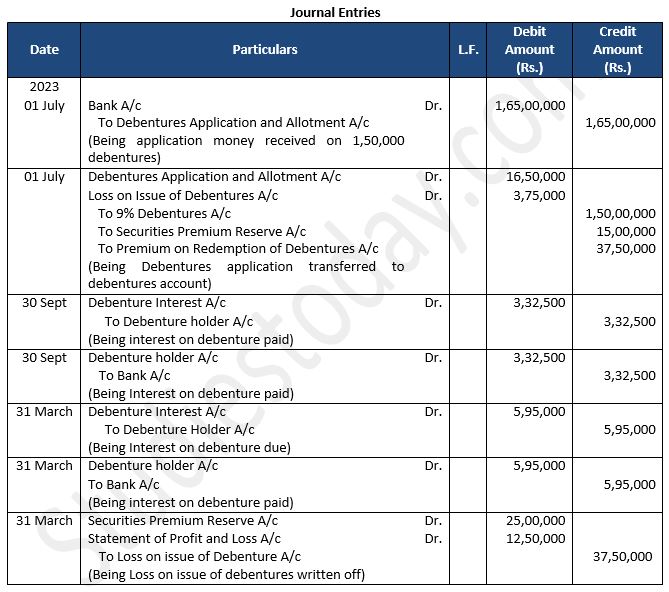

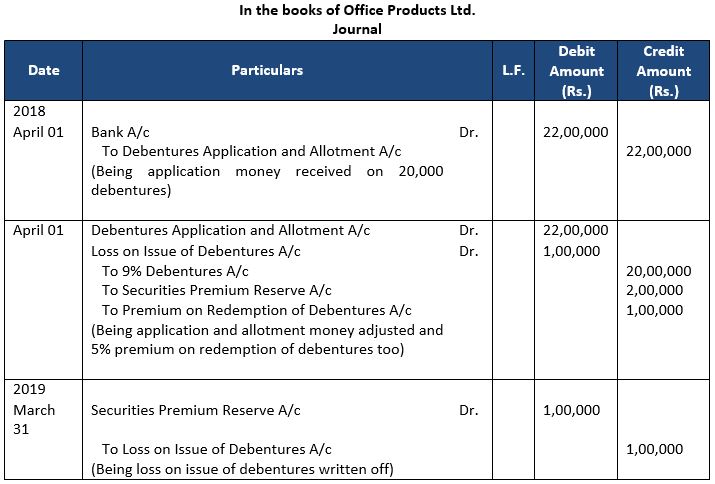

Question 58: Fit India Ltd. has paid-up share capital of ₹ 1,00,00,000 (divided into 5,00,000 Equity Shares of ₹ 20 each) and 10,000, 7% Debentures of ₹ 200 each. On 1st July, 2021, it further issued 7% Debentures at a premium of 10% redeemable at 25% premium to meet the long-term funds requirement of ₹ 1,65,00,000. The issue price was payable along with application. Balance in Securities Premium Account after the issue of debentures of ₹ 25,00,000. Loss for the year ended 31st March, 2022 is ₹ 10,00,000.

You are required to:

(i) Pass Journal entries for issue of Debentures.

(ii) Prepare Loss on Issue of Debentures Account.

(iii) Pass Journal entries for interest on debentures, If interest is payable on 30th September and 31st March each year.

Answer 58:

Old Questions

Question: Raj Ltd. issued 5,000; 8% Debentures of Rs. 100 each at a premium of 5% payable as follows: Rs. 10 on application; Rs. 20 along with premium on allotment and balance on first and final call. Pass necessary Journal entries.

Answer:

Question: Nipa Limited issued Rs. 10,00,000 Debentures of Rs. 100 each at a premium of 10% , payable 25% on application (including premium) and the balance on allotment . The debentures were applied for and the amount was dully received. You are required to give Journal entries and prepare Cash Book.

Answer:

Point of Knowledge:-

Question: Alok Ltd. issued 7,000, 10% Debentures of Rs. 500 each at a premium of Rs. 50 per debenture redeemable at a premium of 10% after 5 years. According to the terms of issue, Rs. 200 was payable on application and balance on allotment. Record necessary Journal entries at the time of issue of 10% Debentures.

Answer:

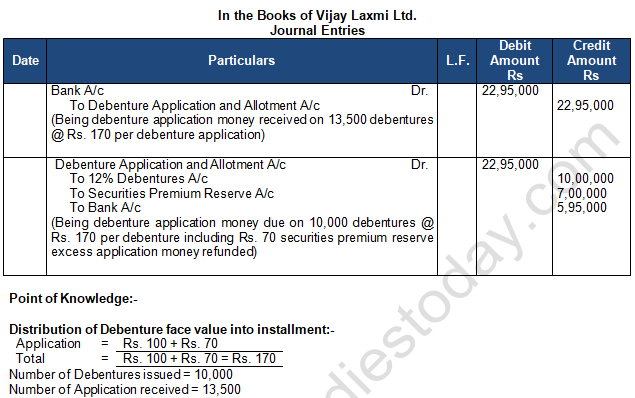

Question: Vijay Laxmi Ltd. invited applications for 10,000; 12% Debentures of Rs. 100 each at a premium of Rs. 70 per debenture .The full amount was payable on application. Applications were received for 13,500 debentures. Applications for 3,500 debentures were rejected and application money was refunded. Debentures were allotted to the remaining applications.

Answer: