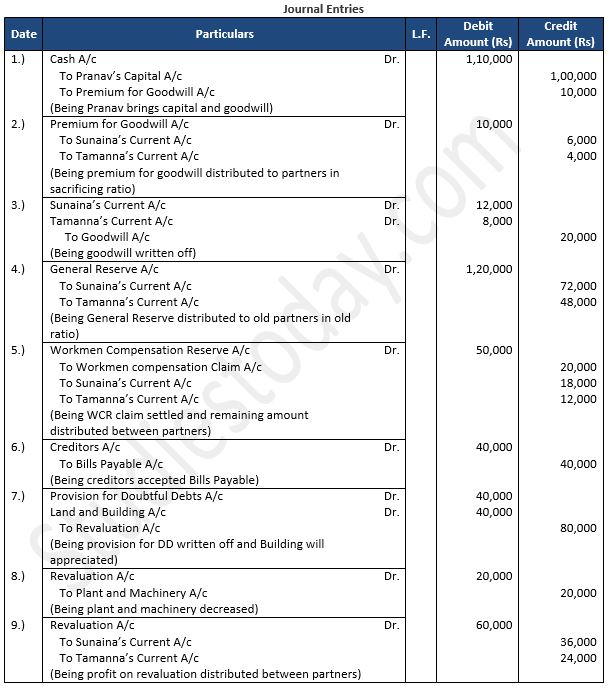

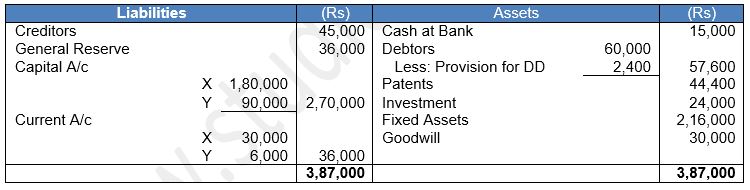

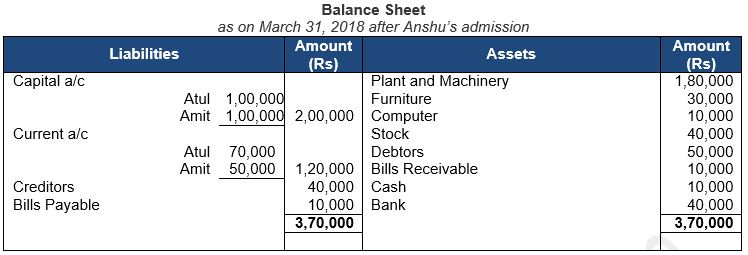

Read TS Grewal Solution Class 12 Chapter 5 Admission of a Partner 2026. Students should study TS Grewal Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These TS Grewal Class 12 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 5 Admission of a Partner TS Grewal Solutions

TS Grewal Solutions for Chapter 5 Admission of a Partner Class 12 Accounts have been provided below based on the latest TS Grewal Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 5 Admission of a Partner TS Grewal Class 12 Solutions

About this chapter: TS Grewal Class 12 Chapter 5 Admission of a Partner is an important chapter for Class 12 students. Lot of questions are asked in the exams from this chapter. This chapter explains the process of admitting a new partner into an existing partnership. There are detailed explanation regarding reasons why a partnership might admit a new partner, which is sometimes due to need for additional capital, skills or expertise. It explains that a partnership agreement should be defined, which outlines the terms and conditions of the partnership. Students will be able to understand different methods of admitting a new partner, including the payment of premium and goodwill, and the adjustment of the capital accounts of existing partners. Various accounting entries have to be passed during the admission of a partner. By going through the concepts explained here students will be able to understand the accounting treatment for admission of a partner, including the preparation of a new balance sheet and the revaluation of assets and liabilities. We have provided solutions to all questions given in this chapter which will be easy for students to learn and even use for their Class 12 exams.

Very Short Answer Type Questions

Question 1. What do you understand by admission of a partner?

Answer:

When a new partner is admitted into the firm, it is known as admission of a new partner. On admission of a new partner, old partnership comes to an end new partnership comes into existence.

Question 2. How is new partner admitted to the firm?

Answer:

A person can be admitted as a new partner:

1.) If it is so agreed in the Partnership Deed, or

2.) In the absence of the Partnership Deed, if all the partners agree for the admission.

Question 3. State any one purpose of admitting a new partner in a firm.

Answer:

The purpose of admitting a new partner in a firm new or incoming partner becomes entitled to share future profit of the firm and the combined share of the old partners gets reduced.

Question 4. List any two matters that need adjustments at the time of admission of a partner.

Answer:

(i) Adjustment of Accumulated Profit, Reserves and Losses.

(ii) Adjustment of Goodwill.

Question 5. State one right acquired by a newly admitted partner.

Answer:

Rights of a newly admitted partner:-

1.) Right to share future profit of the firm.

Question 6. State the other right which a newly admitted partner acquires besides the right to share the profit of the firm.

Answer:

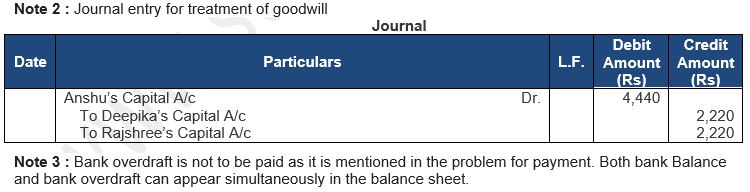

Rights of a newly admitted partner:-

1.) Right to share in the assets of the firm.

Question 7. State the two main rights that a newly admitted partner acquires in the firm.

or

State the rights acquired by a newly admitted partner.

Answer:

Rights of a newly admitted partner:-

1.) Right to share future profit of the firm.

2.) Right to share in the assets of the firm.

Question 8. State the need for treatment of goodwill on admission of a partner.

Answer:

Goodwill is an intangible asset which enables a firm to earn higher profit than the normal profit earned by other firms in the industry. It arises due to efforts made by the existing partners in the past. The goodwill so generated is known as internally, i.e., self-generated goodwill.

Question 9. State the reason of contributing for goodwill by a new partner at the time of his admission.

or

Why should a new partner contribute towards goodwill on his admission?

Answer:

At the time of admission, new partner who acquires the share in future profit from the existing partners should compensate sacrificing partners by paying them an amount, termed as goodwill or premium of goodwill.

Question 10. If the new partner brings in his share of goodwill in cash and if goodwill also appears in books, how is existing amount of goodwill dealt with?

Answer:

When the new or incoming partner brings goodwill in cash or by cheque for his share of goodwill, it is transferred to Capital Accounts of the sacrificing partners in their sacrificing ratio.

Question 11. What is meant by "Sacrificing Ratio"?

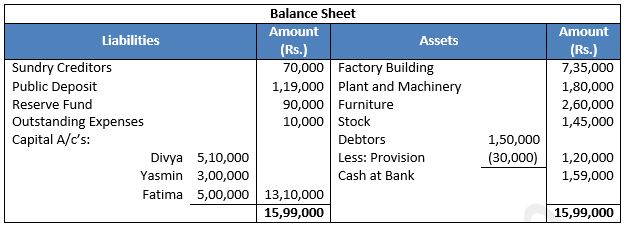

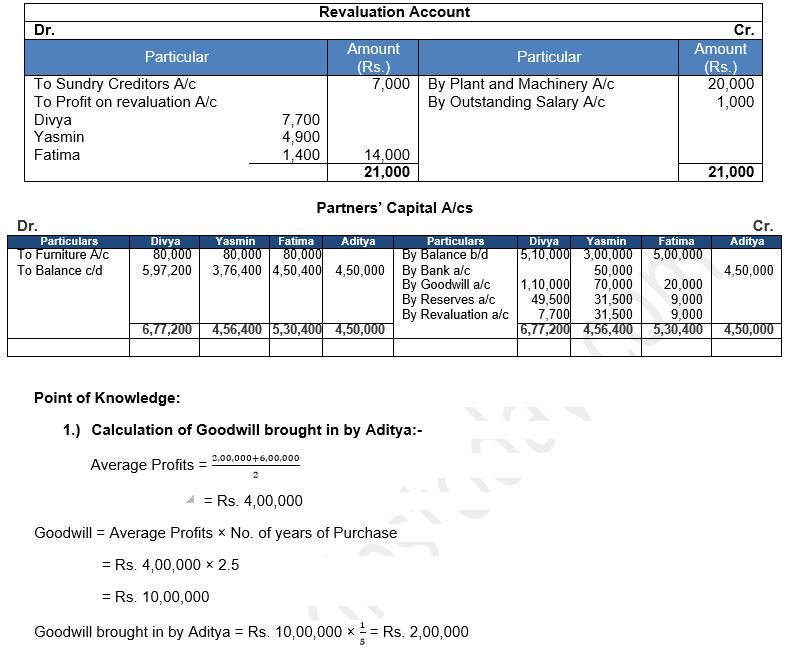

Answer:

Sacrificing Ratio is sacrificed share in profit of two or more partners in term of ratio. Sacrificed share of each partner is calculated as follows:

Sacrificed Share = Old Profit Share – New Profit Share.

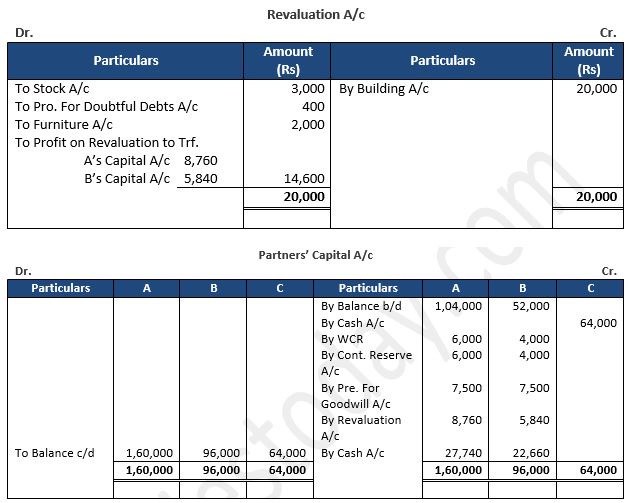

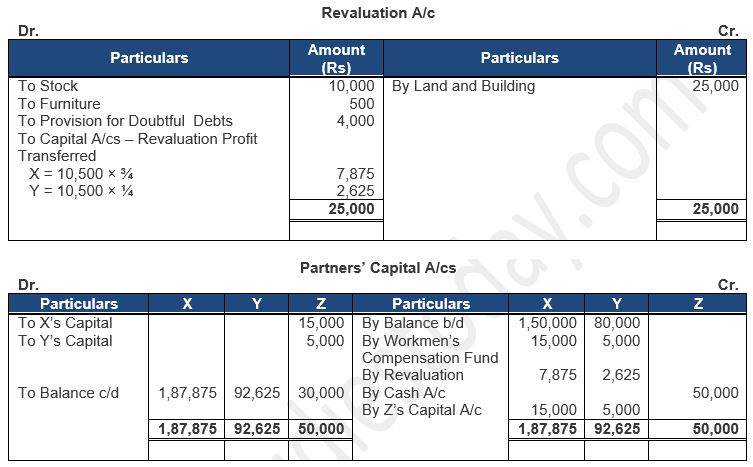

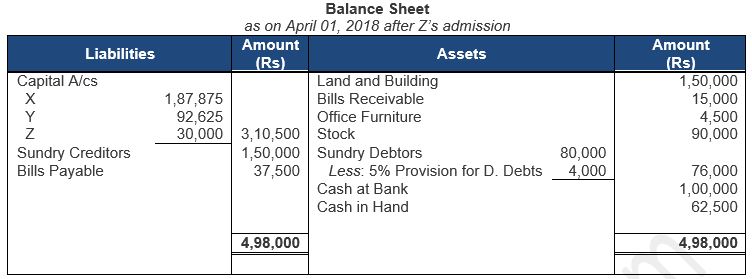

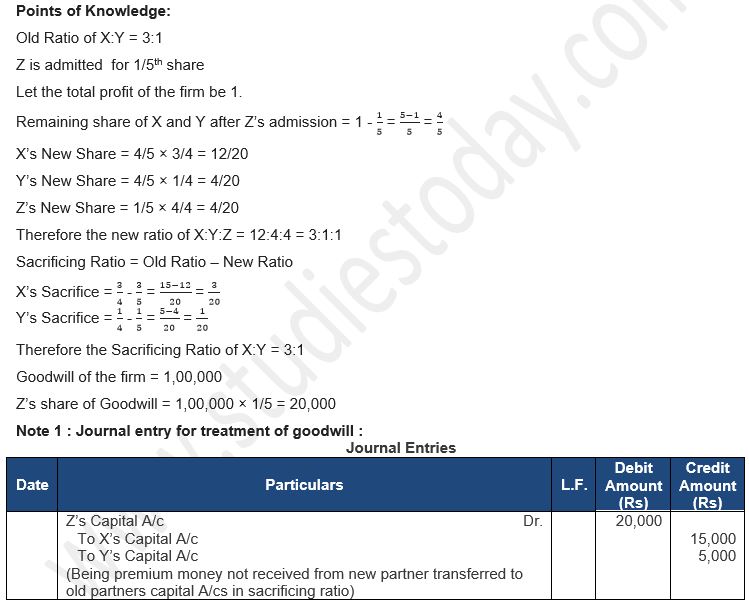

Question 12. At the time of admission of a partner, who decides what will be the out of the firm's profit?

Answer:

Partnership is a result of mutual agreement between partners who agree to share profit in some ratio. The share of profit to be taken by new partner is dependent upon the agreement with other partners.

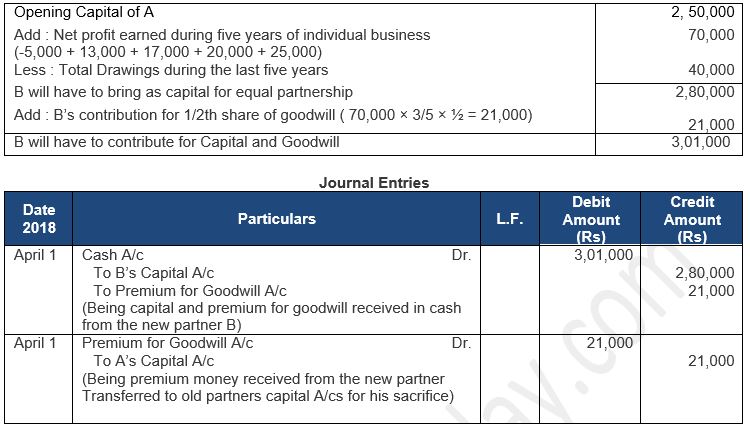

Question 13. Unless given otherwise, what will be the ratio of sacrifice of the old a new partner?

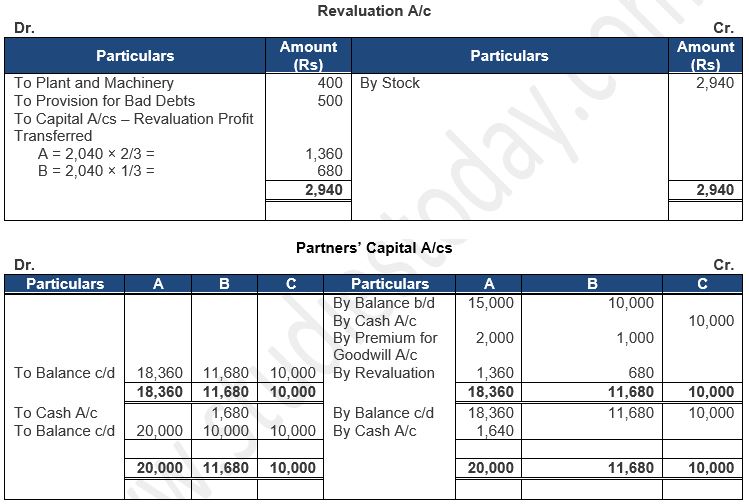

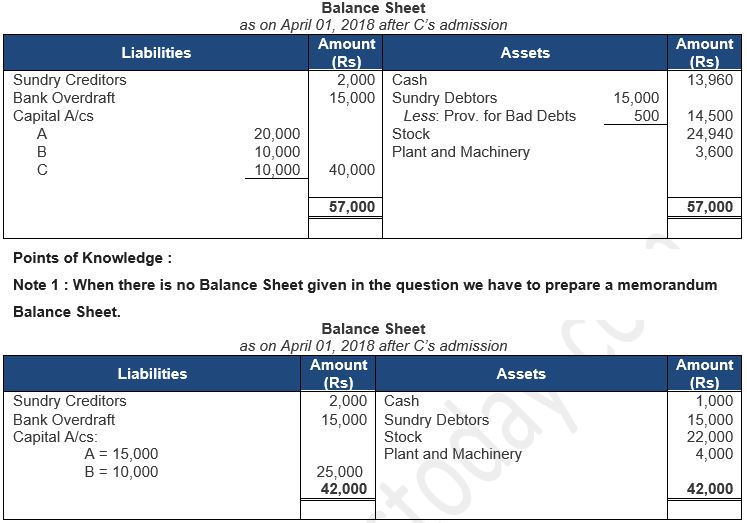

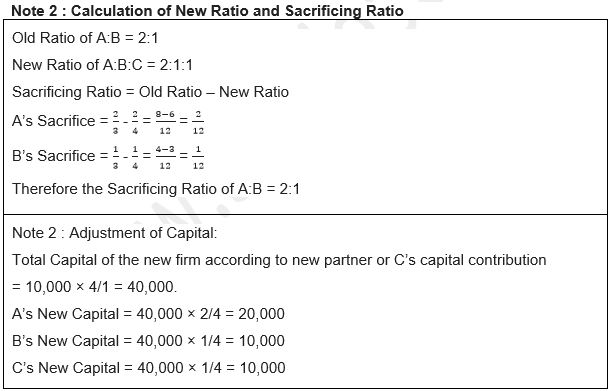

Answer:

Sacrificing ratio may be given to the new or incoming partner by all the old partners equally or by all or some of the partners in agreed ratio.

Question 14. State the ratio in which the old partners share accumulated profit, reserve and losses.

Answer:

The old partners share accumulated profit, reserve and losses in their old ratio.

Question 15. Give two circumstances in which the sacrificing ratio is applied.

[Hints: (i) At the time of admission of a new partner for distributing goodwill brought in by him.

(ii) For adjusting goodwill in the case of change in the profit-sharing ratio of the existing partners.)

Answer:

(i) At the time of admission of a new partner for distributing goodwill brought in by him.

(ii) For adjusting goodwill in the case of change in the profit-sharing ratio of the existing partners.

Question 16. Define New Profit-Sharing Ratio in the case of admission of a partner?

Answer:

The ratio in which all partners, including the incoming partner, will share the profit and losses in future is known as New Profit-sharing Ratio.

Question 17. Why do we distribute reserves, accumulated profits and losses among the old partners?

Answer:

At the time of admission of a new partner, reserves or accumulated profits in the books of the firm should be transferred to the old partners' capital or current accounts in the old ratio, because these items belong to the old partners only.

Question 18. What is meant by Revaluation Account?

Answer:

The change in value of assets and liabilities is adjusted through an account titled Revaluation Account or Profit and loss Adjustment Account. Increase in the value of assets and decrease in the amount of liabilities is credited to Revaluation Account, it being a gain. On the other hand, decrease in value of assets and increase in amount of liabilities is debited to the account, it belong loss.

Question 19. Why is it necessary to revalue assets and liabilities of a firm in case of admission of a partner?

Answer:

When a new partner is admitted, assets are revalued and liabilities are reassessed so that the gain or loss arising on account of such revaluation up to the date of admission of a new partner may be ascertained and adjusted in the Old partners’ Capital Account in their old profit-sharing ratio and the new partner should neither gain nor suffer because of change in the value of assets or amount of liabilities.

Question 20. In which account increase in the value of asset is credited on the admission of a new partner?

Answer:

In Revaluation Account increase in the value of assets is credited on the admission of a new partner.

Question 21. State whether Revaluation Account is debited or credited to record the increase in the value of Plant and Machinery.

Answer:

If the value of Plant and Machinery is increased Revaluation Account is credited.

Question 22. State whether Revaluation Account is debited or credited to record the decrease in the value of Plant and Machinery.

Answer:

If the value of Plant and Machinery is increased Revaluation Account is debited.

Question 23. State whether Revaluation Account is debited or credited to record the decrease in the amount of creditors.

Answer:

Revaluation Account is credited to record the decrease in the amount of creditors.

Question 24. State whether Revaluation Account is debited or credited to record the increase in the amount of creditors.

Answer:

Revaluation Account is debited to record the increase in the amount of creditors.

Question 25. State whether Revaluation Account is debited or credited to record an unrecorded asset.

Answer:

Revaluation Account is credited to record an unrecorded asset.

Question 26. State whether Revaluation Account is debited or credited to record the increase in Provision for Doubtful Debts.

Answer:

Revaluation Account is debited to record the increase in Provision for Doubtful Debts.

Question 27. State any two reasons for the preparation of Revaluation Account on the admission of a new partner.

Answer:

Reasons for the preparation of Revaluation Account on the admission of a new partner:-

(i) Assets and Liabilities may appear in the books at revised (new) values.

(ii) Assets and Liabilities may appear in the books at old values.

Question 28. State whether the Partner's Capital Account is debited or credited to record the gain of Revaluation Account.

Answer:

If the gain in Revaluation Account profit will be transferred to the Old partners’ Capital Account (in the old profit sharing ratio) and same will be credited in the Partners’ Capital Account.

Question 29. State whether the Partner's Capital Account is debited or credited to record the loss of Revaluation Account.

Answer:

If the loss in Revaluation Account loss will be transferred to the Old partners’ Capital Account (in the old profit sharing ratio) and same will be debited in the Partners’ Capital Account.

Question 30. State the ratio in which the partners share the gain or loss on revaluation of assets and liabilities.

Answer:

In the Old Profit sharing ratio the partners share the gain or loss on revaluation of assets and liabilities.

Question 31. When the General Reserve is distributed, are the Partners' Capital Accounts debited or credited?

Answer:

At the time of distribution of General Reserve Partner’s Capital Account is credited.

Question 32. Under what circumstances will the premium for goodwill paid by the incoming partner not be recorded in the books of account?

Answer:

Premium for Goodwill is not recorded in the books of account when the incoming partner pays it privately to the sacrificing partners.

Question 33. State with reason whether at the time of admission of a partner, partnership is dissolved or partnership firm is dissolved.

Answer:

At the time of admission of a partner only partnership is dissolved and not the partnership firm as there is change in the existing agreement and a new agreement comes into existence.

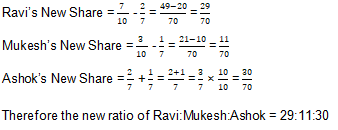

Question 34. Amit and Beena were partners in a firm sharing profits and losses in the ratio of 3:1. Chaman was admitted as a new partner for 1/6th share in the profits. Chaman acquires 2/5th of his share from Amit. How much share did Chaman acquire from Beena?

Answer:

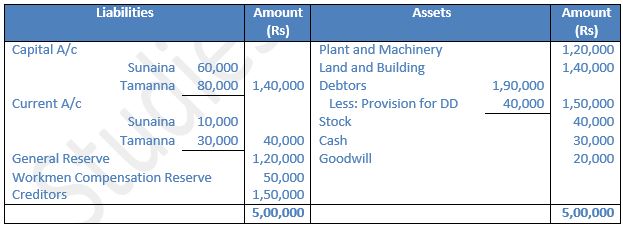

Question 35. A, B and C are partners having capitals of Rs. 3,00,000, Rs. 2,00,000 and Rs. 1,00,000. They admit D as a partner for 1/5th share on 1st April, 2019. On this day, the firm has reserve of Rs. 60,000. A and B demand that reserve should be shared in proportion of capital whereas C is of the opinion that it should be shared equally as they do not have partnership deed. A and B agree to C’s viewpoint.

What argument must have been put by C that convinced both A and B?

Answer:

In the absence of partnership deed reserves should be divided equally between the partners. Hence C’s point of view is correct.

Question 37. X and Y are partners sharing profits and losses equally. They admit Z as partner for 1/3rd share which he takes from Y. Z bring Rs. 50,000 as his share of goodwill. X is of the opinion that goodwill brought by Z should be shared whereas Y is of the opinion that Rs. 50,000 should be credited to his capital. X finally agrees to Y’s view.

What argument must have been given by Y that made X agree?

Answer:

No, entry will be passed in the books as Z has paid his share of goodwill to Y for credited to his capital account. By this only Y’s Capital is increased.

Question 38. Geeta, Sunita and Anita were partners in a firm sharing profit in the ratio 5:3:2. On 1st January, 2015, they admitted Yogita as a new partner for 1/10th share in the profit. On Yogita’s admission, the Profit and Loss Account of the firm was showing a debit balance of Rs. 20,000 which was credited by the accountant of the firm to the Capital Accounts of Geeta, Sunita and Anita in their profit-sharing ratio. Did the accountant give correct treatment? Give reason in support of your answer.

Answer:

No, the accountant did not give correct treatment as the debit balance of Profit and Loss Account shows loss, it should be debited to the Partner’s Capital Account.

Question 39. Karan, Nakul and Asha were partners in a firm sharing profit and losses in the ratio 3:2:1. At the time of admission of a partner, the goodwill of the firm was valued at Rs. 2,00,000. The accountant of the firm passed the entry in the books of account and thereafter showed goodwill at Rs. 2,00,000 as an asset in the Balance Sheet. Was he correct in doing so? Why?

Answer:

No, the accountant’s decision is not correct because according to AS-26, goodwill should be recorded in the books only when consideration in money or money’s worth has been paid for it.

Question 40. A, B, C and D were partners in a firm sharing profit in the ratio of 4:3:2:1. On 1st January, 2015, they admitted E as a new partner for 1/10 share in the profits. E brought Rs. 10,000 for his share of goodwill premium which was correctly recorded in the books by the accountant. The accountant showed goodwill at Rs. 1,00,000 in the books. Was the accountant correct in doing so? Give reason in support of your answer.

Answer:

No, the accountant was not correct in doing so.

Reason: Since the new partner has brought his share of goodwill in cash against self-generated goodwill, it cannot be recorded in the books of account. Only purchased goodwill can be recorded in the books of accounts as per AS-26.

EXERCISE ::->

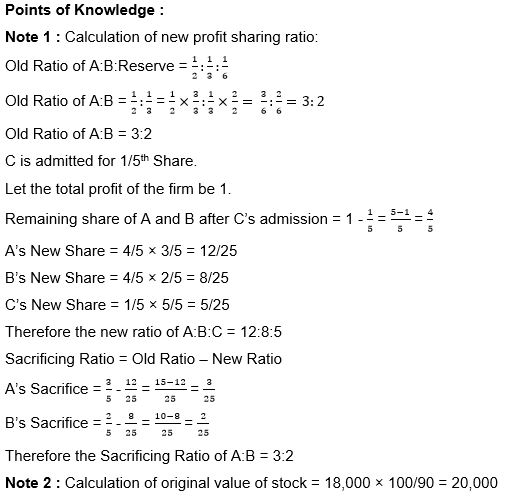

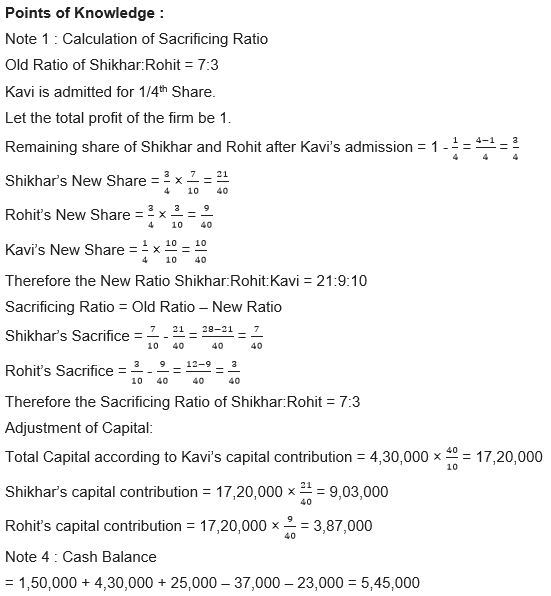

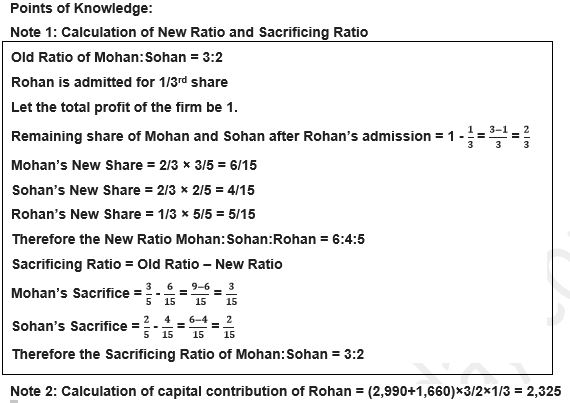

Calculation of New Profit-Sharing Ratio and Sacrificing Ratio

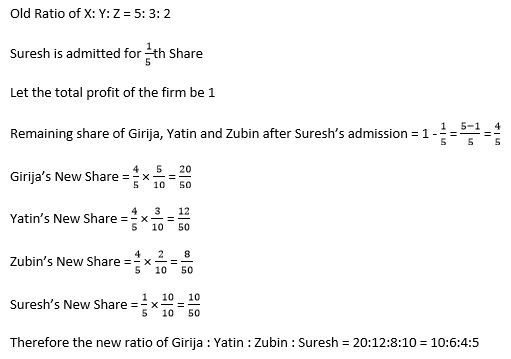

Question 1: Girija, Yatin and Zubin are partners sharing profits and losses in the ratio of 5:3:2. They admit Suresh into partnership and give him 1/5th share of profits. Find the new profit-sharing ratio.

Answer:

About Solution:-

As existing partnership firm may take up expansion/diversification of the business in that case it may need managerial help on additional capital and option before the partnership firm is to admit partner/ and partners when a partner is admitted to the existence partnership firm it is called admission of partner.

Things to Remember:

According to the partnership Act 1932 a person can be admitted into partnership only with the consent of the entire existing partner unless otherwise agreed upon.

Important Notes:

When a new partner is admitted he/she she acquire his/her share in profit from the existing partners and result the profit sharing ratio in the new firm is decided mutually between the existing partner and new partner the incoming partner acquires his/her share of future profit either from no or more existing partner the existing partner sacrifice a share of their profit in the favour of new partner hence the calculation of new profit sharing ratio becomes necessary.

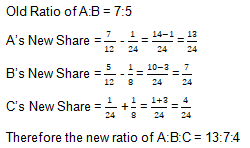

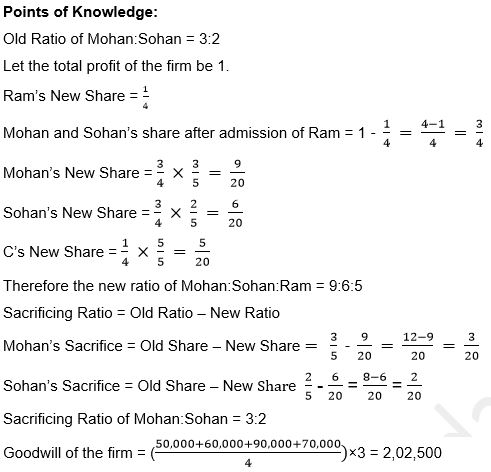

Question 2: A and B are partners sharing profits and losses in the proportion of 7 : 5. They agree to admit C, their manager, into partnership who is to get 1/6th share in the profits. He acquires this share as 1/24th from A and 1/8th from B. Calculate new profit-sharing ratio.

Answer:

About Solution:-

Sometimes a new partner is needed into the business due to the following reasons:

1. When more capital is needed for the expansion of the business.

2. When a competent and experience person is needed for the efficient running of the business.

3. To increase the goodwill and reputation of the business by taking a reputed and renowned person into the partnership.

Things to Remember:

A new partner gets the following two rights:-

1. Right to share future profits of the firm.

2. Right to share in the assets of the firm.

Important Notes:

Following adjustments are needed at the time of the admission of a new partner:-

1. Calculation of new profit sharing ratio.

2. Accounting treatment of goodwill.

3. Accounting treatment for revaluation of assets and liabilities.

4. Accounting treatment of reserves and accumulated profit.

5. Adjustment of capital on the basis of new profit sharing ratio.

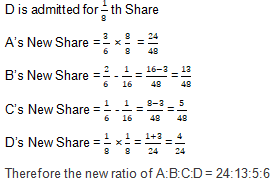

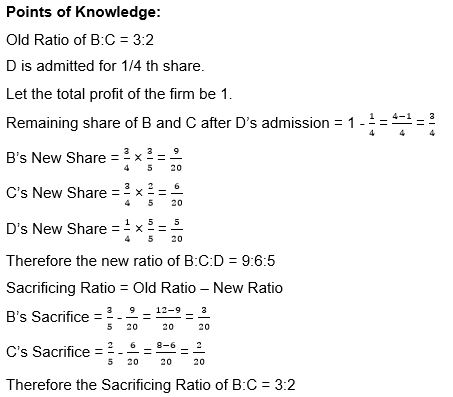

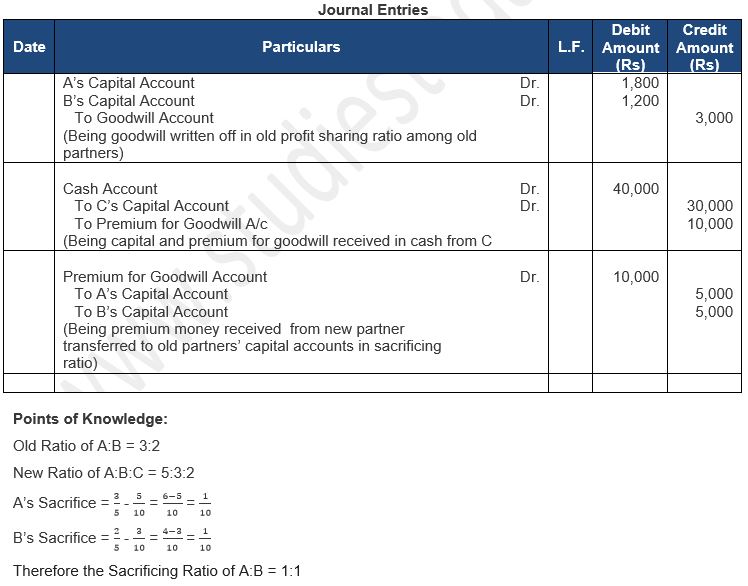

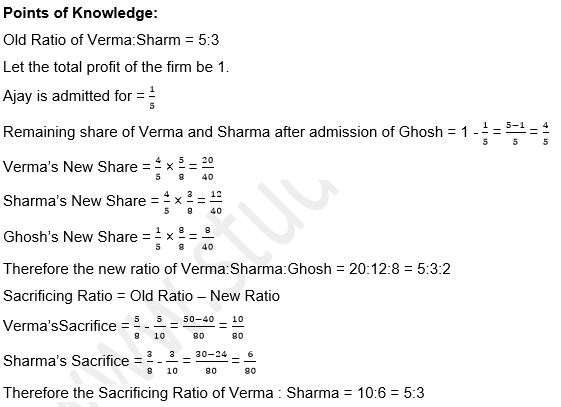

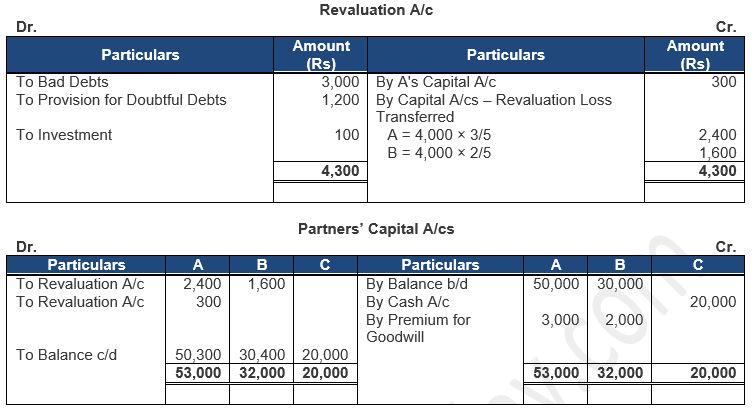

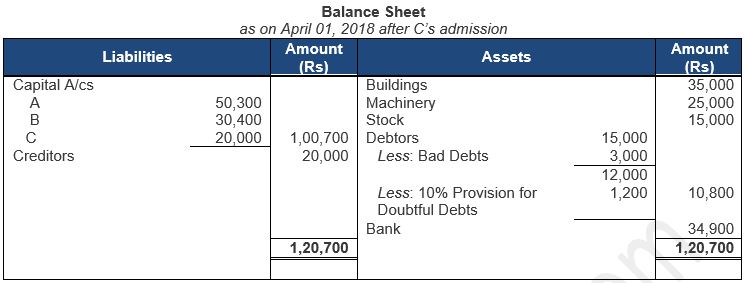

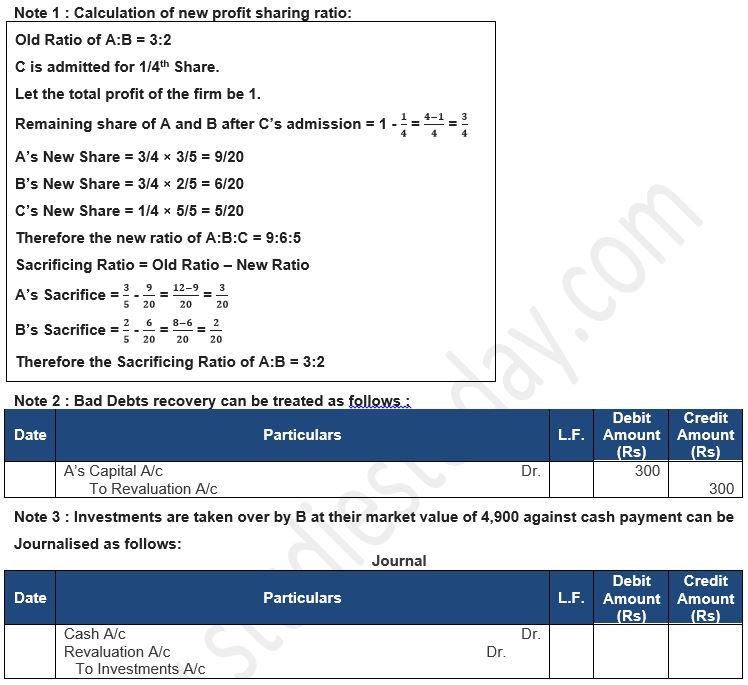

Question 3: A, B and C were partners in a firm sharing profits in the ratio of 3 : 2 : 1. They admitted D as a new partner for 1/8th share in the profits, which he acquired 1/16th from C . Calculate the new profit-sharing ratio of A, B , C and D.

Answer:

Old Ratio of A:B:C = 3:2:1

About Solution:-

Section 31 of the Indian Partnership Act, 1932: Accounting to section 31 of the Indian Partnership Act, 1932, a person can be admitted as a new partner:

1. If it is agreed in the Partnership Deed

2. In the absence of the above, if all partners agree for the admission.

Things to Remember:

When a partner is newly admitted into the partnership, the new partner gets the following rights:

1. Right to share the future profit of the firm.

2. Right to share in the assets of the firm.

Important Notes:

Revolution of assets and reassessment of liabilities is to be done. The net increase or decrease is then adjusted in the existing partner’s capital account in their old profit sharing ratio.

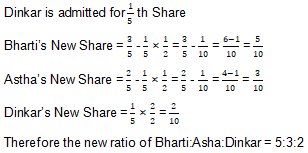

Question 4: Bharati and Astha were partners sharing profits in the ratio of 3 : 2 . They admitted Dinkar as a new partner for 1/5th share in the future profits of the firm which he got equally from Bharati and Astha. Calculate the new profit-sharing ratio of Bharati , Astha and Dinkar.

Answer:

Old Ratio of Bharti:Astha = 3:2:1

About Solution:-

Right and liabilities of the newly admitted partner at the same time the newly admitted partner becomes liable for any liability of the business incurred after his admission and any loss incurred by the firm.

Things to Remember:

Calculation of sacrificing ration when old ratio of existing partners and new ratio of all partners is given:

1. When old ratio and new ratio of the old and existing partners is available, sacrificing ratio is to be calculated by deducting the new share from the old share.

2. Formula used is as follows:

Sacrificing Share = Old Share – New Share

Important Notes:

Calculation of sacrificing ratio when new or incoming partner acquires the share by surrender of a particular fraction of share by old partners:

1. In such a case, the share surrendered by the partner is deducted from his old share of profit to determine his share in the reconstituted firm.

2. Total of shares surrendered by all the partners in favour of new or incoming partner is considered as the share of new or incoming partner.

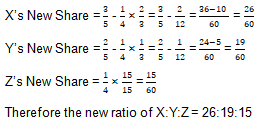

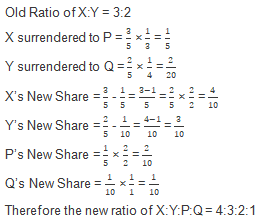

Question 5: Mohan and Mahesh are partners in a firm sharing profits and losses in the ratio of 3 : 2. Z is admitted as partner with 1/4 share in profit. Nusrat takes his share from Mohan and Mahesh in the ratio of 2 : 1. Calculate new profit-sharing ratio.

Answer:

Old Ratio of X:Y = 3:2

About Solution:-

Sacrificing Ratio in which the old partners agree to sacrifice their share in profit in favour of a new partner.

Things to Remember:

New Ratio in which all the partners of the firm including the incoming partner share the future profit and losses.

Important Notes:

Sacrificing Ratio is using following formula:

Sacrificing Ratio = Old Ratio – New Ratio

New Ratio is using following formula:

New Profit Sharing Ratio = Old Ratio – Sacrificing Ratio

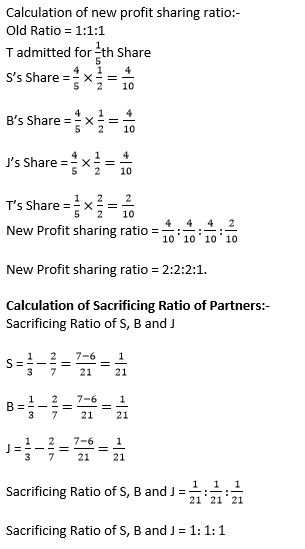

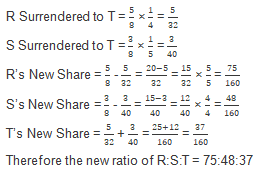

Question 6: S, B and J were partners in a firm. T was admitted as a partner in the partnership firm for 1/5th share of profits. Calculate the sacrificing ratio of S, B and J.

Answer:

Question 7: P and Q were partners in a firm sharing profits in a ratio of 5:3. R was admitted for 1/4th share in the profits, of which he took 75% from P and the remaining from Q. Calculate, the sacrificing ratio of P and Q.

Answer:

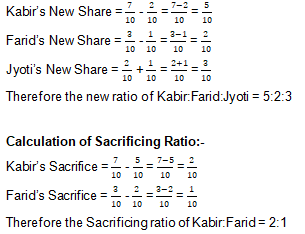

Question 8: Kabir and Farid are partners in a firm sharing profits and losses in the ratio of 7 : 3 . Kabir surrenders 2/10th from his share and Farid surrenders 1/10th from his share in favour of Jyoti; the new partner. Calculate new profit-sharing ratio and sacrificing ratio.

Answer:

Old Ratio of Kabir:Farid = 7:3

About Solution:-

Calculation of new profit sharing ratio when profit share of new or incoming partner is given but sacrifice made by old partners is not given:

i) In such a case, it is assumed that the new partner has acquired his share from old partners in their old profit-sharing ratio.

ii) Therefore, old partners will continue to share balance profits or losses in their old profit sharing ratio. It means that, in the absence of any information, profit sharing ratio among the existing partners remains unchanged.

Things to Remember:

Calculation of new profit sharing ratio for each partner will be as follows:

• Deduct new or incoming partners’ share of profit from 1; and

• Divide the remaining share of profit among old partners in their old profit sharing ratio.

Important Notes:

Calculation of new profit sharing ratio when share of new or incoming partner is given and also new profit sharing of old partner is given:

1. In such a case, new partner’s share of profit is deducted from 1 and balance share of profit is divided among old partners in their new profit sharing ratio.

2. Such arrangement gives the new profit share of each of the partners in the new firm.

Question 9: Find New Profit-sharing Ratio:

(i) R and T are partners in a firm sharing profits in the ratio of 3:2. S joins the firm. R surrenders 1/4th of his share and T 1/5th of his share in favour of S.

(ii) A and B are partners. They admit C for 1/4th share. In future, the ratio between A and B would be 2 : 1 .

(iii) A and B are partners sharing profits and losses in the ratio of 3:2. They admit C for 1/5th share in the profit. C acquires 1/5th of his share from A and 4/5th share from B.

(iv) X, Y and Z are partners in the ratio of 3 : 2 : 1. W joins the firm as a new partner for 1/6th share in profits. Z would retain his original share.

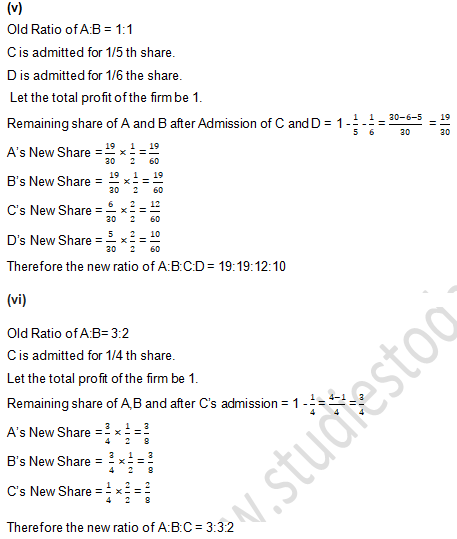

(v) A and B are equal partners. They admit C and D as partners with 1/5th and 1/6th share respectively.

(vi) A and B are partners sharing profits/losses in the ratio of 3:2. C is admitted for 1/4th share. A and B decide to share equally in future.

Answer:

About Solution:-

Calculation of new profit sharing ratio when new or incoming partner acquires his share from the old or existing partners equally:

1. In such case, new share of each old partner is to be determined by calculating the new profit sharing ratio among all the partners.

2. The sacrifice made in favour of the new or incoming partner is deducted from the existing share of profit of each old partner.

Things to Remember:

Calculation of new profit sharing ratio when new or incoming partner acquires his share from the old existing partners in a particular ratio:

1. In such situation, share of existing or old partners will change to the extent of share sacrifice on admission of the new or incoming partner.

2. New share of profit of the existing partners in the reconstituted firm is determined by deducting the sacrifice made by them from their existing share of profit.

Important Notes:

Sacrificing ratio in which the old partners agree to sacrifice their in profit in favour of new profit.

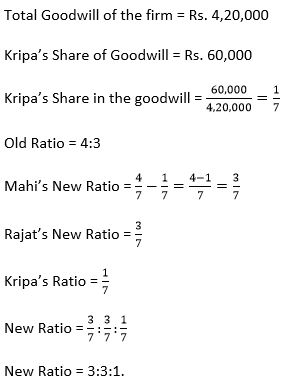

Question 10: Mahi and Rajat were in partnership sharing profits and losses in the ratio of 4:3. They admitted Kripa as a new partner. Kripa brought ₹ 60,000 as her share of goodwill premium which was entirely credited to Mahi’s Capital Account. On the date of admission, goodwill of the firm was valued at ₹ 4,20,000. Calculate the new profit-sharing ratio of Mahi, Rajat, and Kripa.

Answer:

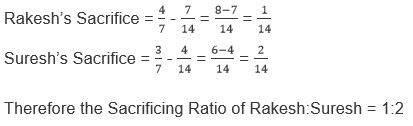

Question 11: Rakesh and Suresh are sharing profits in the ratio of 4:3. Zaheer joins and the new ratio among Rakesh, Suresh and Zaheer is 7:4:3. Find out the sacrificing ratio.

Answer:

Old Ratio of Rakesh:Suresh = 4:3

New Ratio of Rakesh:Suresh:Zaheer = 7:4:3

Sacrificing Ratio = Old Ratio – New Ratio

About Solution:-

Calculation of sacrificing ratio when old ratio of existing partners and new ratio of all partners is given:

1.) When old ratio and new ratio of the old and existing partners is available, sacrificing ratio is to be calculated by deducting the new share from the old share.

2.) Formula used is as follows:

Sacrificing Share = Old Share – New Share

Things to Remember:

Calculation of sacrificing ratio when new or incoming partner acquires the share by surrender of a particular fraction of shares by old partners:

1.) In such a case, the share surrendered by the partner is deducted from his old share of profit to determine his share in the reconstituted firm.

2.) Total of shares surrendered by all the partner in favour of new or incoming partner is considered as the share of new or incoming partner.

Important Notes:

Gain in profit share of existing or old partner or partners:

1. In the event of admission of a partner in a partnership firm, some partner sacrifice while some partners gain.

2. Sacrifice made by one or more old partners is the total of share acquired by new or incoming partner and share gained by existing or old partner or partners.

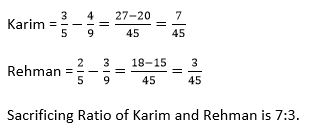

Question 12: Karim and Rehman are partners profits in the ratio of 3:2. Naval is admitted as a partner. New profit sharing ratio among karim, Rehman and Naval is 4:3:2. Find the sacrificing ratio.

Answer:

Calculation of Sacrificing Ratio of Karim and Rehman:-

Old Ratio = 3:2

New Ratio = 4:3:2

Sacrificing Ratio of Karim and Rehman:-

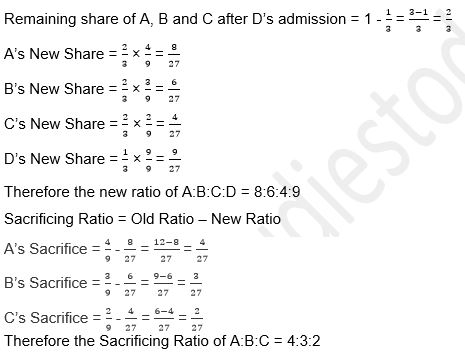

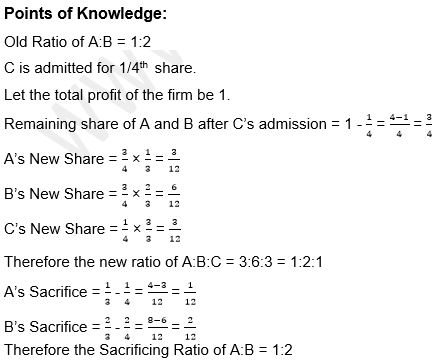

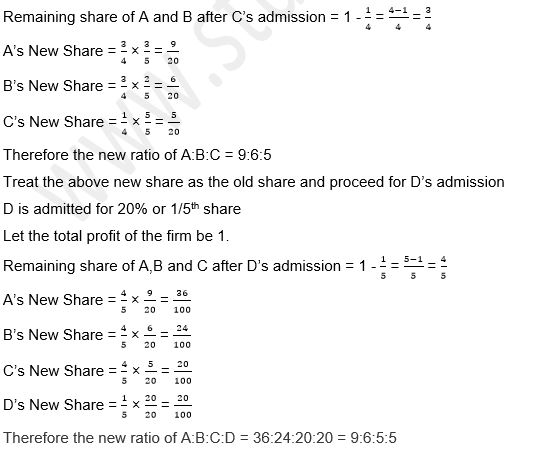

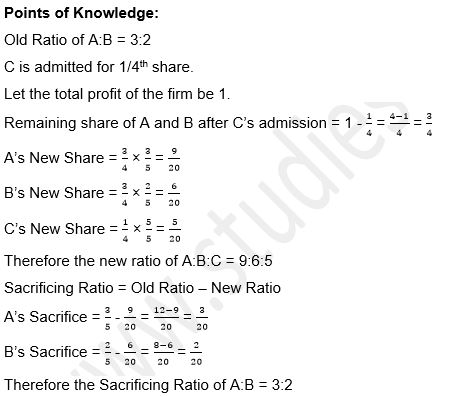

Question 13: A, B and C are partners sharing profits in the ratio of 4 : 3 : 2. D is admitted for 1/3rd share in future profits . What is the sacrificing ratio?

Answer:

Old Ratio of A:B:C = 4:3:2

D is admitted for 1/3rd Share.

Let the total profit of the firm be 1.

About Solution:-

As per AS-26 on Intangible Assets self-generated goodwill is not recognised as an asset in the books of account. It means that the goodwill which is internally generated by the company over past few years, cannot be recognised as it is self-generated by the business.

Things to Remember:

Goodwill should be recorded in the books only when consideration in money or money's worth is paid for it, i.e., when goodwill is purchased.

Important Notes:

In case of change in profit sharing ratio among the partners or admission or retirement/death of a partner, goodwill is not to be raised in the books of the firm as no consideration in money or money's worth is paid for it. If goodwill is raised, it should be immediately written off.

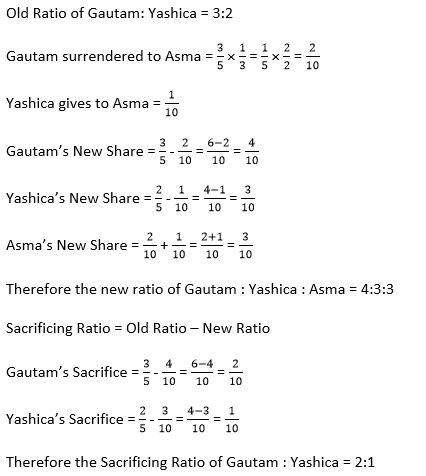

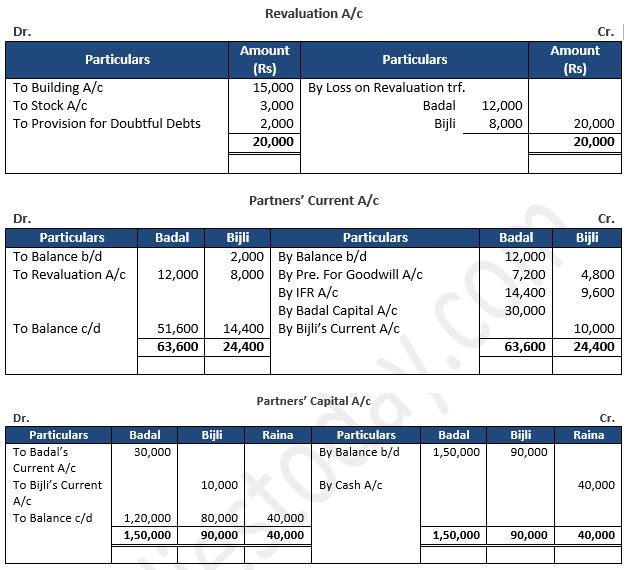

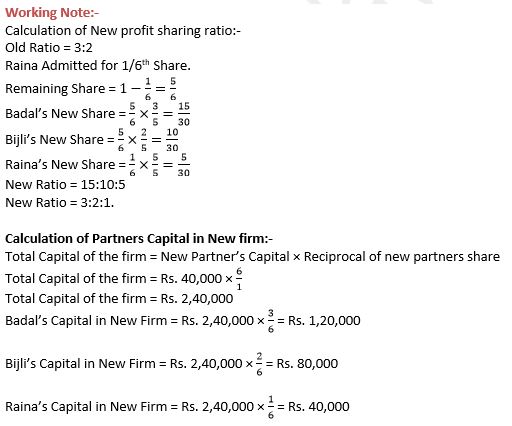

Question 14: Gautam and Yashica are partners sharing profits and losses in the ratio of 3:2. They admit Asma into partnership. Gautam gives 1/3rd of his share while Y gives 1/10th from his share to Asma. Calculate new profit-sharing ratio and sacrificing ratio.

Answer:

About Solution:-

A combined single entry can be passed as follows:

Cash/Bank A/c . Dr. [With Share of Capital and Goodwill]

To New Partner's Capital A/c [With Capital]

To Premium for Goodwill A/c [With Share of Goodwill]

Things to Remember:

The concept of goodwill is also useful outside of accounting for valuation purposes. It's used to refer to any value built up within the company due to intangible factors like customer service and teamwork.

Important Notes:

Amount of Goodwill is credited to the New Partner's Capital Account and thereafter, adjusted in favour of Old or existing partners in their sacrificing ratio for which following entries are passed:

i.) Cash/Bank A/c

To New Partner's Capital

Question 15: A, B and C are partners sharing profits in the ratio of 2 : 2 : 1. D is admitted as a new partner for 1/6th share. C will retain his original share . Calculate the new profit-sharing ratio and sacrificing ratio.

Answer:

Old Ratio of A:B:C = 2:2:1

D is admitted for 1/6th share.

Let the total profit of the firm be 1.

About Solution:-

In the event of admission of a partner, new partner who acquires the share in future profits from the existing partners should compensate sacrificing partners by paying them an amount. This amount paid by the incoming partner is termed as Goodwill or Premium for Goodwill.

Things to Remember:

In such situation, the assets brought in are debited individually with their values and Premium for Goodwill Account is credited with his share of goodwill and also new Partner's Capital Account with his capital.

Important Notes:

Ratio in which the old partners agree to sacrifice their share in profits in favour of a new partner.

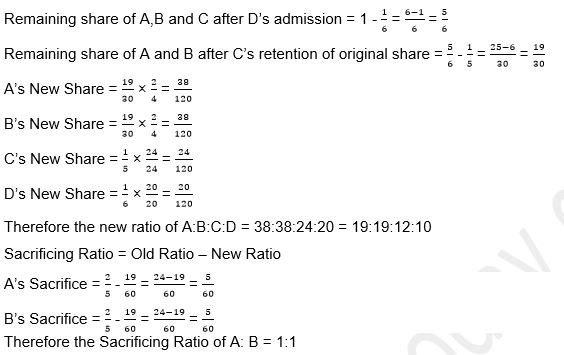

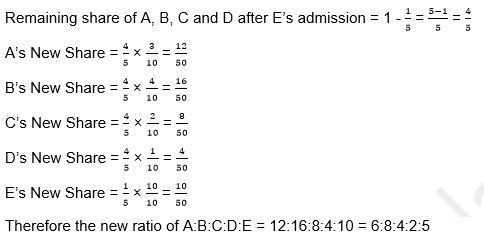

Question 16: A, B, C and D are in partnership sharing profits and losses in the ratio of 36:24:20:20 respectively. E joins the partnership for 20% share and A , B , C and D in future would share profits among themselves as 3/10 : 4/10 : 2/10 : 1/10. Calculate new profit-sharing ratio after E's admission.

Answer:

Old Ratio of A:B:C:D = 36:24:20:20 = 9:6:5:5

E is admitted for 20% = 20/100 = 1/5th Share

Let the total profit of the firm be 1.

About Solution:-

Accounting Treatment of Goodwill Existing in Books of Account:-

Goodwill existing in the books of the firm is written off by debiting Old Partners' Capital Account/Current Account in their Old Profit Sharing Ratio and crediting Goodwill Account.

Old Partners' Capital/Current A/c Dr. (in Old Ratio)

To Goodwill A/c

Things to Remember:

Accounting Treatment when Goodwill (Premium on Goodwill) is paid privately: In this situation, Goodwill (Premium on Goodwill) is paid by the new or Incoming Partner privately to the sacrificing partners. In such situation, journal entry is not passed in the books of account of the firm.

Important Notes:

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is retained in business: In this situation, Amount brought in by the new or Incoming Partner is transferred to Capital Accounts Of the sacrificing partners in their sacrificing ratio. Following entries are to be passed:

Brought in cash by the new or incoming partner:

Cash/Bank A/c . Dr. [With share of Goodwill]

To Premium for Goodwill A/c

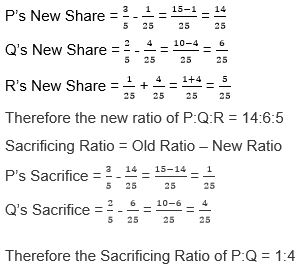

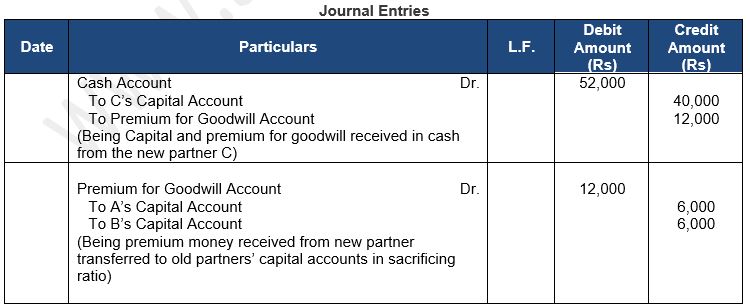

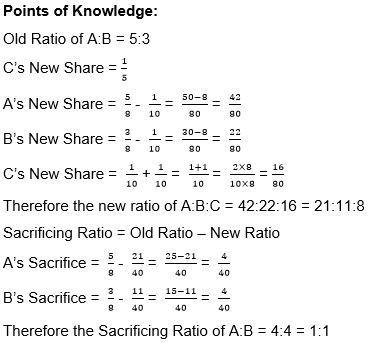

Question 17: P and Q are partners sharing profits in the ratio of 3 : 2. They admit R, a new partner who acquires 1/5th of his share from P and 4/25th share from Q. Calculate New Profit-sharing Ratio and sacrificing ratio.

Answer:

Old Ratio of P:Q = 3:2

About Solution:-

Old partners will continue to share balance profits or losses in their old profit sharing ratio. It means that, in the absence of any information, profit sharing ratio among the existing partners remains unchanged.

Things to Remember:

At the time of change in profit sharing ratio, it is important to determine the Sacrificing ratio and gaining ratio of partners. Explanation: This may result in some partners gaining and others losing

Important Notes:

At the time of the admission of a new partner, there is a change in the profit sharing ratio of the old partners also. The new profit sharing ratio is calculated after considering the new partner's share in profit and the sacrifice made by the old partners.

Goodwill/Premium for Goodwill is brought in Cash by the New Partner and Retained in the Business.

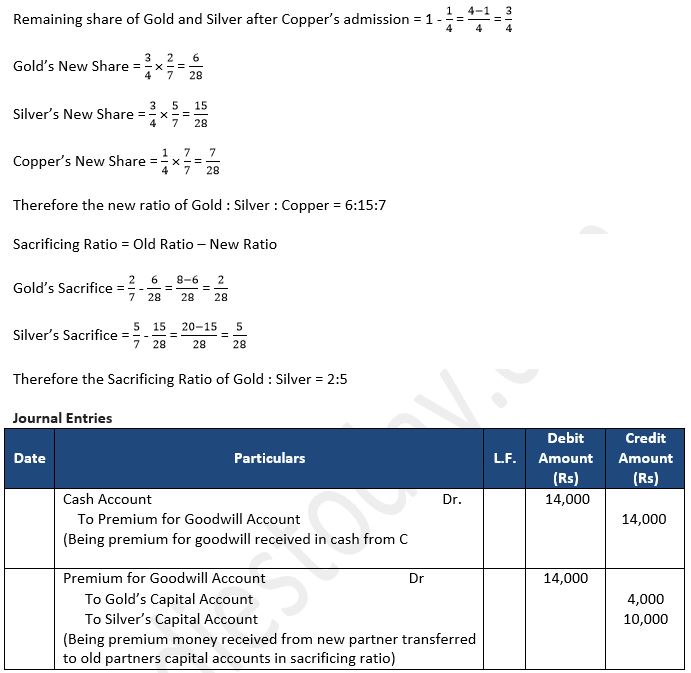

Question 18: Gold and Silver are partners sharing profits and losses in the ratio of 2:5. They admit Copper on the condition that he will bring in Rs. 14,000 as his share of goodwill in cash to be distributed between Gold and Silver. Copper's share in the future profits or losses will be 1/4th. What will be the new profit-sharing ratio and what amount of goodwill brought in by Copper will be received by Gold and Silver?

Answer:

Old Ratio of A:B = 2:5

C is admitted for 1/4 th share.

Let the total profit of the firm be 1.

About Solution:-

When premium of goodwill is withdrawn by the partners (Sacrificing partners) Treatment:

(1) Cash/ Bank A/c Dr.

To New Partners’ Capital A/c

To Premium for goodwill A/c

(Being Capital and goodwill is brought by new partner)

(2) Premium for Goodwill A/c Dr.

To Sacrificing Partners’ Capital/Current A/c

(Being premium brought by the new partner is transferred to Sacrificing partners)

(3) Sacrificing Partners’ Capital/Current A/c Dr.

To Cash/ Bank A/c

(Being amount of premium withdrawn by the sacrificing partners)

Things to Remember:

When new partner is unable to bring his share of goodwill: Treatment:

New Partners’ Current/Capital A/c Dr.

To Sacrificing Partners’ Capital/Current A/c

(Being new partners’ current A/c or Capital A/c is debited for the unpaid amount of premium)

Important Notes:

When goodwill appearing in the balance sheet (It is to be written off)

Old Partners’ Capital/Current A/c Dr.

To Goodwill A/c

(Being old goodwill written off by the old partners in their old ratio)

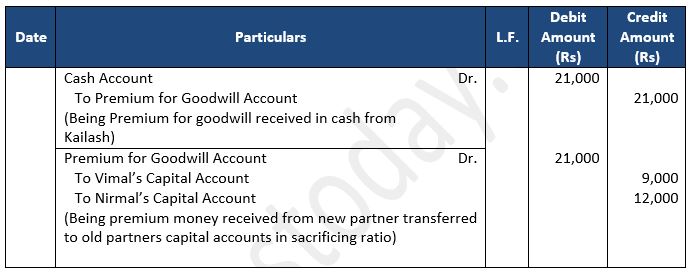

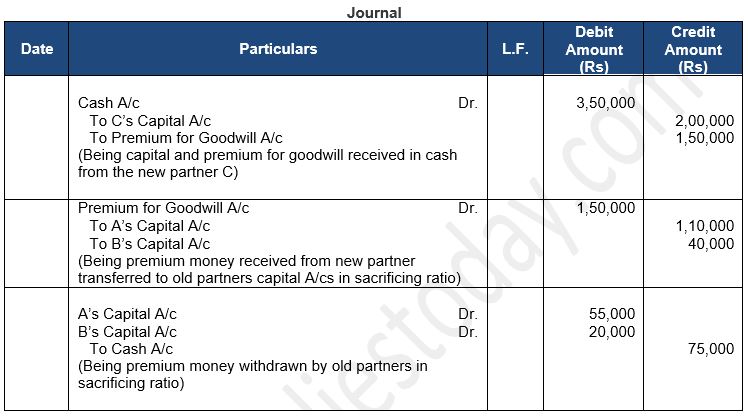

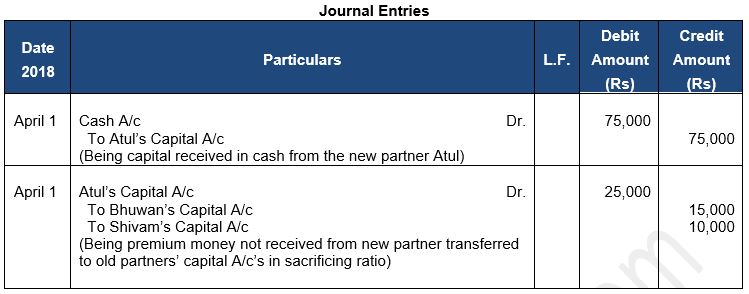

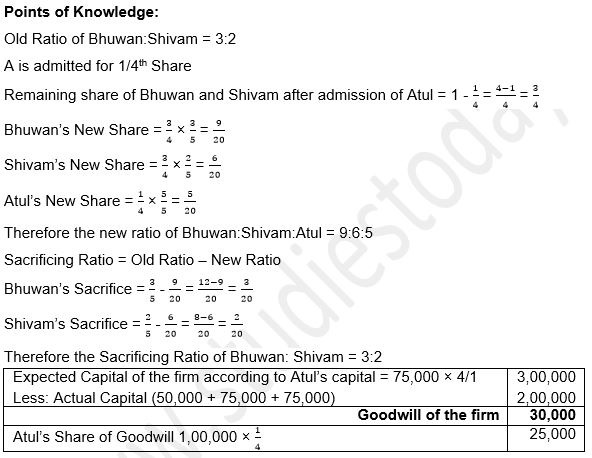

Question 19: Vimal and Nirmal are partners in a firm sharing profits and losses in the ratio of 3 : 2 . A new partner Kailash is admitted. Vimal surrenders 1/5th of his share and Nirmal surrenders 2/5th of his share in favour of Kailash . For this purpose of Kailash's admission, goodwill of the firm is valued at Rs. 75,000 and Kailash brings in his share of goodwill in cash which is retained in the business. Journalise the above transactions.

Answer:

About Solution:-

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in kind: In such situation, the assets brought in are debited individually with their values and Premium for Goodwill Account is credited with his share of goodwill and also new Partner's Capital Account with his capital. Such Premium for Goodwill is transferred to the Capital Accounts of the sacrificing partners in their sacrificing ratio.

Things to Remember:

When old ratio and new ratio of the old and existing partners is available, sacrificing ratio is be calculated by deducting the new share from the old share.

Important Notes:

Sacrificing ratio is nothing but the proportion in which old partners sacrifices their share in favour of new partner. Therefore, the surrender of share by old partner in certain ration is nothing but the sacrificing ratio. It is calculated by subtracting new ratio from the old ratio.

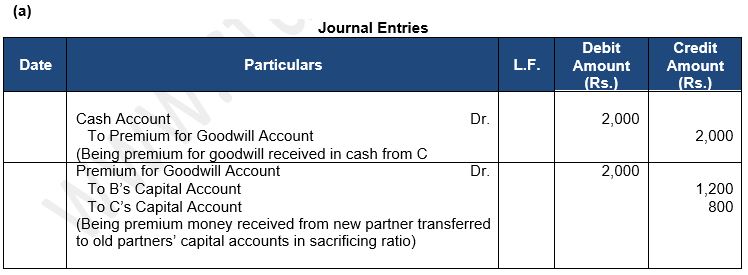

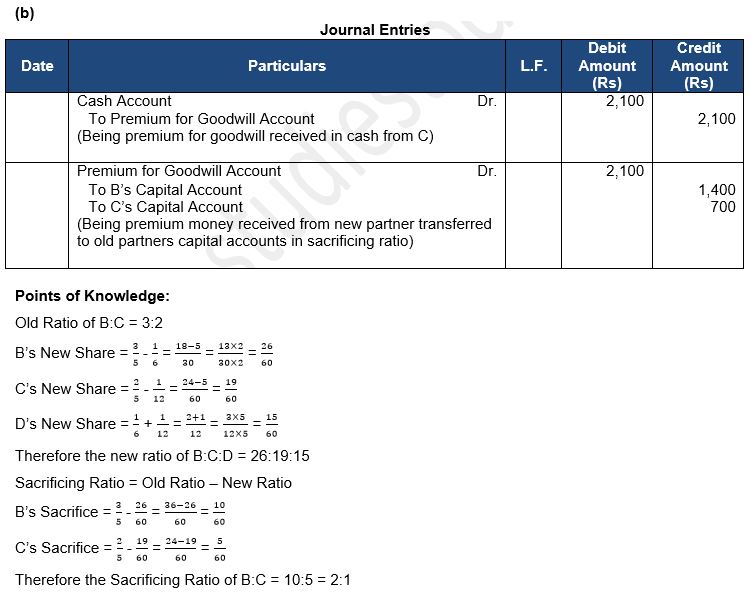

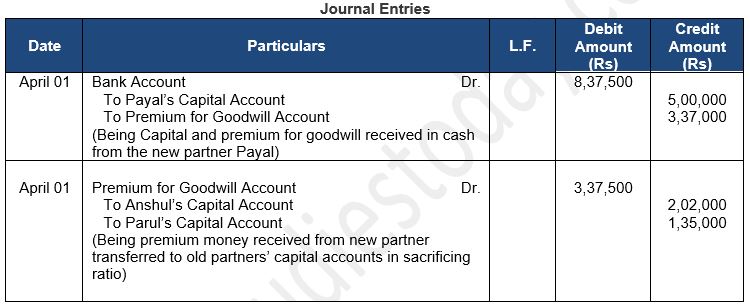

Question 20: Give Journal entries to record the following arrangements in the books of the firm:

(a) B and C are partners sharing profits in the ratio of 3:2. D is admitted paying a premium (goodwill) of Rs. 2,000 for 1/4th share of the profits, shares of B and C remain as before.

(b) B and C are partners sharing profits in the ratio of 3 : 2. D is admitted paying a premium of Rs. 2,100 for 1/4th share of profits which he acquires 1/6th from B and 1/12th from C.

Answer:

About Solution:-

Assets brought in by New Partner:

Assets A/c . Dr. [Individually]

To New Partners' Capital A/c [With amount of Capital]

To Premium for Goodwill A/c[With share of Goodwill brought in]

Things to Remember:

Total of shares surrendered by all the partners in favour of new or incoming partner is considered as the share of new or incoming partner.

Important Notes:

Sacrifice made by one or more old partner(s) is the total of share acquired by new or incoming partner and share gained by existing or old partner or partners.

Question 21: B and C are in Partnership sharing profits and losses as 3:1. They admit D into the firm, D paying a premium of Rs. 15,000 for 1/3rd share of the profits. As between themselves, B and C agree to share the future profits and losses equally. Draft journal entries showing appropriations of the premium money.

Answer:

About Solution:-

1. Credit to Sacrificing Partners by Incoming Partner's full share of Goodwill:

Incoming Partner's Capital/Current A/c . Dr. [With unpaid Share of Goodwill]

To Sacrificing Partners' Capital A/c [ln sacrificing ratio]

Things to Remember:

Amount paid by the incoming partner is termed as Goodwill or Premium for Goodwill. Accounting treatment of such Goodwill has been explained with respect to some situations which may arise in the event of partner's admission

Important Notes:

Accounting Treatment of Goodwill at the time Of Admission Of a Partner: In the event of admission of a partner, new partner who acquires the share in future profits from the existing partners should compensate sacrificing partners by paying them an amount.

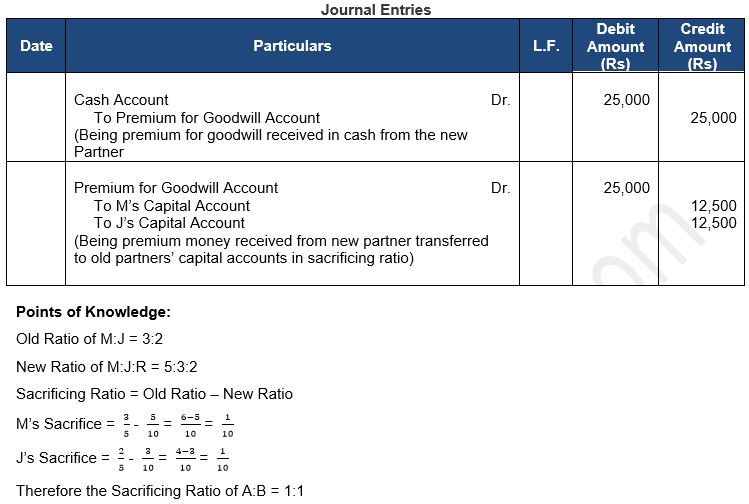

Question 22: Geeta and Sunita are partners in a firm sharing profits in the ratio of 3 : 2. They admit R as a new partner. The new profit-sharing ratio between M, J and R will be 5 : 3 : 2. R brought in Rs. 25,000 for his share of premium for goodwill. Pass necessary journal entries for the treatment of goodwill.

Answer:

About Solution:-

Goodwill Account is raised for the amount not brought by the incoming partner and is also written off by passing the following entries:

(i) Premium for Goodwill A/c Dr. [With Premium for Goodwill brought in]

Goodwill A/c . Dr. [With Unpaid Amount]

To Sacrificing Partners' Capital/Current A/c [ln sacrificing ratio]

(ii) Incoming Partner's Capital/Current A/c Dr. [Unpaid Amount]

To Goodwill A/c

Things to Remember:

Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is retained in business.

Important Notes:

Accounting Treatment when Goodwill (Premium on Goodwill) is paid privately: In this situation, Goodwill (Premium on Goodwill) is paid by the new or Incoming Partner privately to the sacrificing partners. In such situation, journal entry is not passed in the books of account of the firm.

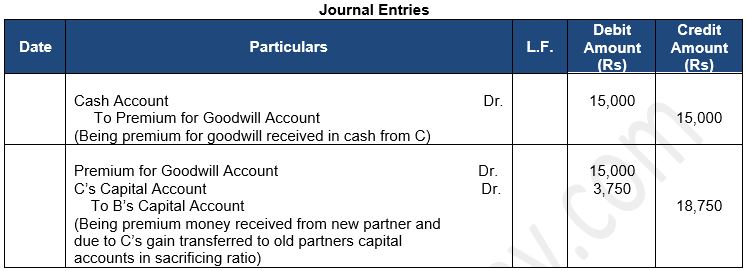

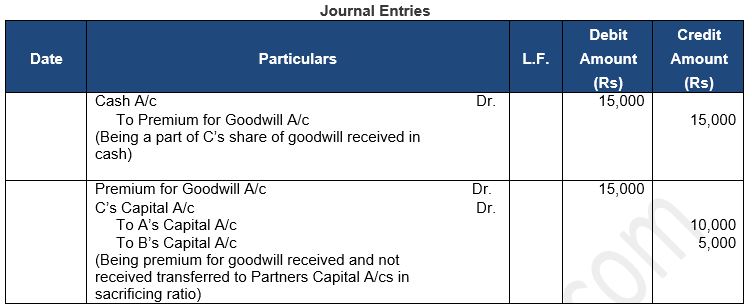

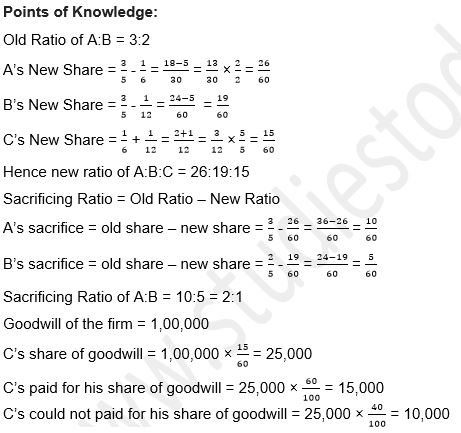

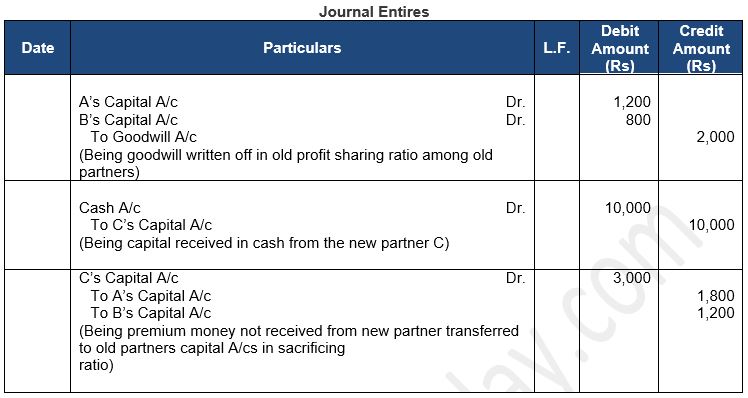

Question 23: A and B are in partnership sharing profits and losses in the ratio of 5:3. C is admitted as a partner who pays Rs. 40,000 as capital and the necessary amount of goodwill which is valued at Rs. 60,000 for the firm. His share of profits will be 1/5th which he takes 1/10th from A and 1/10th from B.

Pass journal entries and also calculate future profit-sharing ratio of the partners.

Answer:

About Solution:-

It is possible that the value of Goodwill of the firm is not given and such value of goodwill is to be inferred based on the net worth (capital of the firm). Such inferred value of Goodwill is termed as Hidden or Inferred Goodwill.

Things to Remember:

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is retained in business: In this situation, either of the 2 options is to be followed to record the accounting treatment of Goodwill.

Important Notes:

Amount brought in by the new or Incoming Partner is transferred to Capital Accounts Of the sacrificing partners in their sacrificing ratio. Following entries are to be passed:

Brought in cash by the new or incoming partner:

Cash/Bank A/c . Dr. [With share of Goodwill]

To Premium for Goodwill A/c

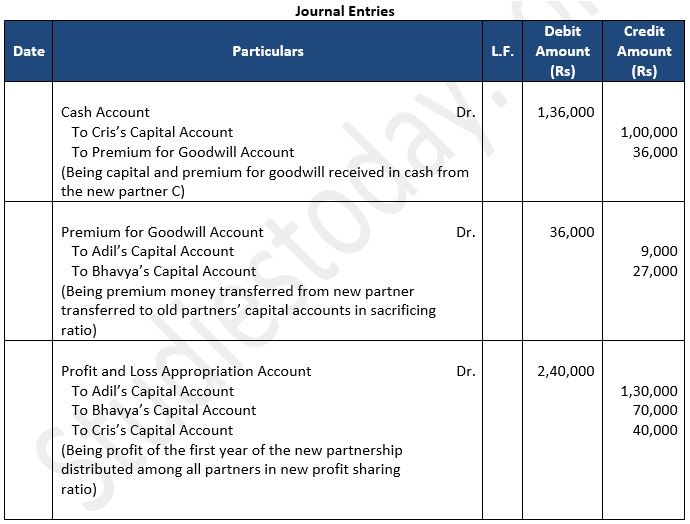

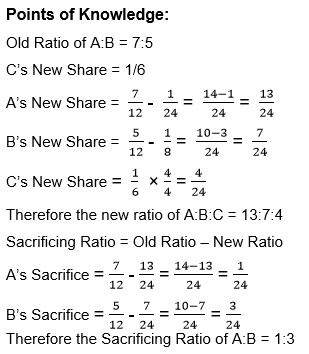

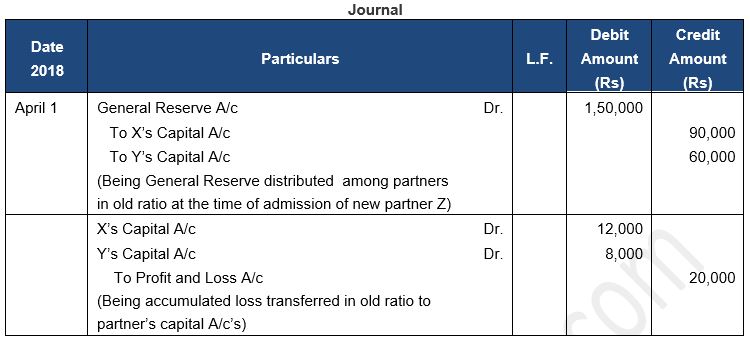

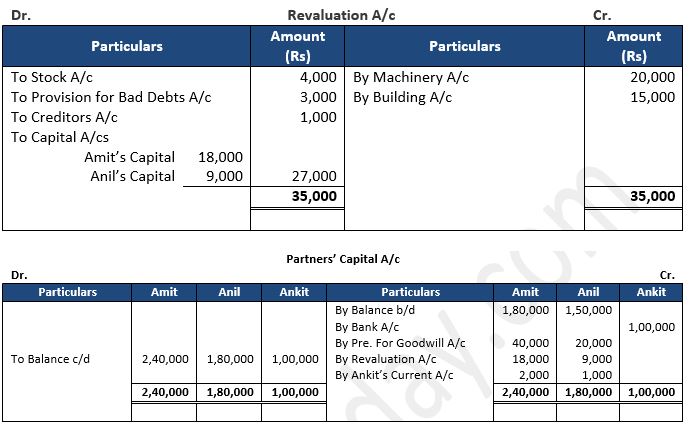

Question 24: Adil and Bhavya are partners sharing profits and losses in the proportion of 7 : 5 . They admit Cris, their Manager, into partnership who is to get 1/6th share in the business. Cris brings in Rs. 1,00,000 for his capital and Rs. 36,000 for the 1/6th share of goodwill which he acquires 1/24th from Adil and 1/8th from Bhavya. Profits for the first year of the new partnership amount to Rs. 2,40,000. Pass necessary journal entries in connection with C's admission and apportion the profits between the partners.

Answer:

About Solution:-

Old partners will continue to share balance profits or losses in their old profit sharing ratio. It means that, in the absence of any information, profit sharing ratio among the existing partners remains unchanged.

Things to Remember:

Old partners will continue to share balance profits or losses in their old profit sharing ratio. It means that, in the absence of any information, profit sharing ratio among the existing partners remains unchanged.

Important Notes:

Sacrifice made by one or more old partner(s) is the total of share acquired by new or incoming partner and share gained by existing or old partner or partners.

Question 25: Aayush and Aarushi are partners sharing profits and losses in the ratio of 3:2. They admitted Naveen into partnership for 1/4th share. Goodwill of the firm was to be valued at three year’s purchase of super profits. Average net profit of the firm was ₹ 20,000. Capital investment in the business was ₹ 50,000 and Normal Rate of Return was 10%. Calculate the amount of Goodwill premium brought by Naveen.

Answer:

Calculation of Goodwill of the firm:-

Normal Profit = Capital Employed × Normal Rate of Return

Normal Profit = Rs. 50,000 × 10%

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 20,000 – Rs. 5,000

Super Profit = Rs. 15,000

Goodwill = Super Profit × 3 year of Purchase

Goodwill = Rs. 15,000 × 3

Goodwill = Rs. 45,000

Calculation of Premium of Goodwill:-

Premium of Goodwill = 45,000 × 1/4

Premium of Goodwill = Rs. 11,250

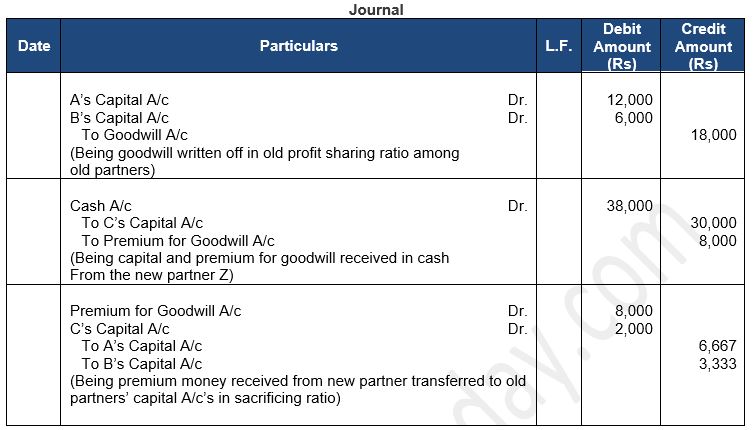

Question 26: A and B are partners in a firm sharing profits and losses in the ratio of 3:2. They admit C into partnership for 1/5th share. C brings in Rs. 30,000 as capital and Rs. 10,000 as goodwill. At the time of admission of C, goodwill appears in the Balance Sheet of A and B at Rs. 3,000. The new profit-sharing ratio of the partners will be 5:3:2. Pass necessary journal entries.

Answer:

About Solution:-

In the event of admission of a partner, new partner who acquires the share in future profits from the existing partners should compensate sacrificing partners by paying them an amount. This amount paid by the incoming partner is termed as Goodwill or Premium for Goodwill.

Things to Remember:

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is withdrawn by Sacrificing Partners fully or partly: Such amount of premium brought in by the new or incoming partner is shared by the sacrificing partners in the sacrificing ratio. These sacrificing partners may withdraw the premium amount fully or partly.

Important Notes:

Following entries are to be passed:

Premium for goodwill brought in cash by the new partner:

Cash/Bank A/c Dr. [Amount of premium]

To Premium for Goodwill A/c

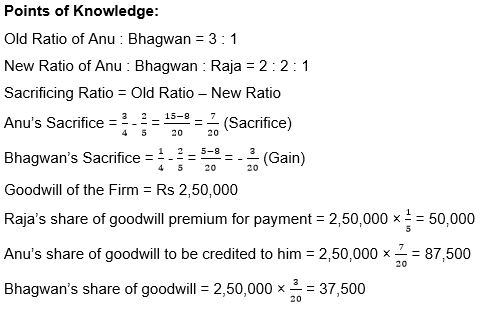

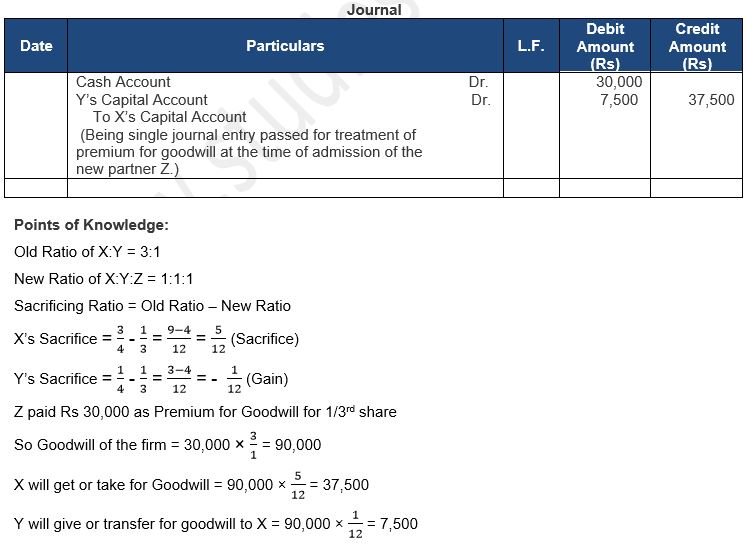

Question 27: Anu and Bhagwan were partners in a firm sharing profits in the ratio of 3:1. Goodwill appeared in the books at Rs 4,40,000. Raja was admitted to the partnership. The new profit-sharing ratio among Anu, Bhagwan and Raja was 2:2:1.

Raja brought Rs 1,00,000 for his capital and necessary cash for his goodwill premium. The goodwill of the firm was valued at Rs 2,50,000.

Record necessary journal entries in the books of the firm for the above transactions

Answer:

About Solution:-

It is possible that the value of Goodwill of the firm is not given and such value of goodwill is to be inferred based on the net worth (capital of the firm). Such inferred value of Goodwill is termed as Hidden or Inferred Goodwill.

Things to Remember:

Accounting Treatment when Goodwill (Premium on Goodwill) is brought in kind: In such situation, the assets brought in are debited individually with their values and Premium for Goodwill Account is credited with his share of goodwill and also new Partner's Capital Account with his capital. Such Premium for Goodwill is transferred to the Capital Accounts of the sacrificing partners in their sacrificing ratio.

Important Notes:

Accounting Treatment when Goodwill (Premium on Goodwill) is not brought in full or a part by the new or Incoming Partner: In such case, premium for goodwill account is credited with the amount of premium for goodwill brought by the new or incoming partner.

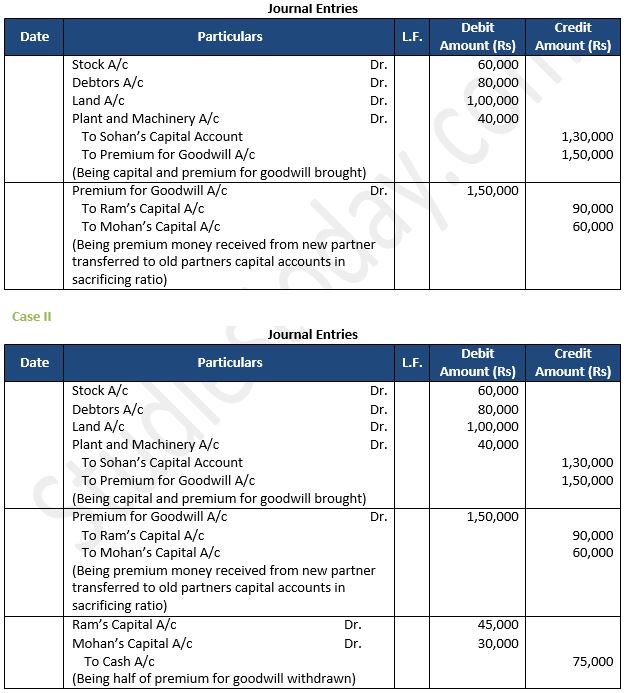

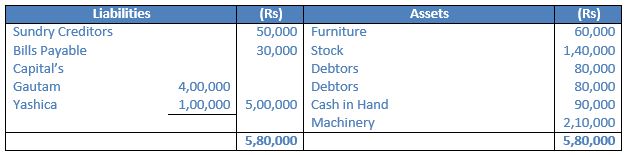

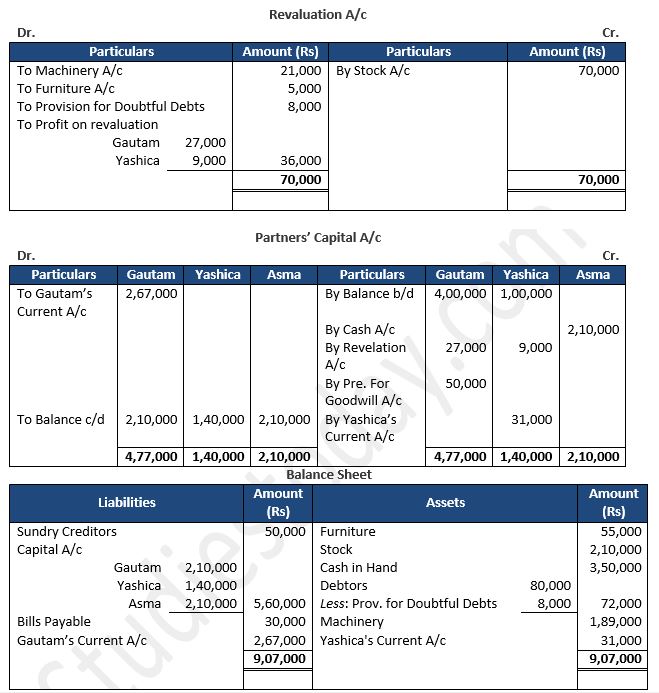

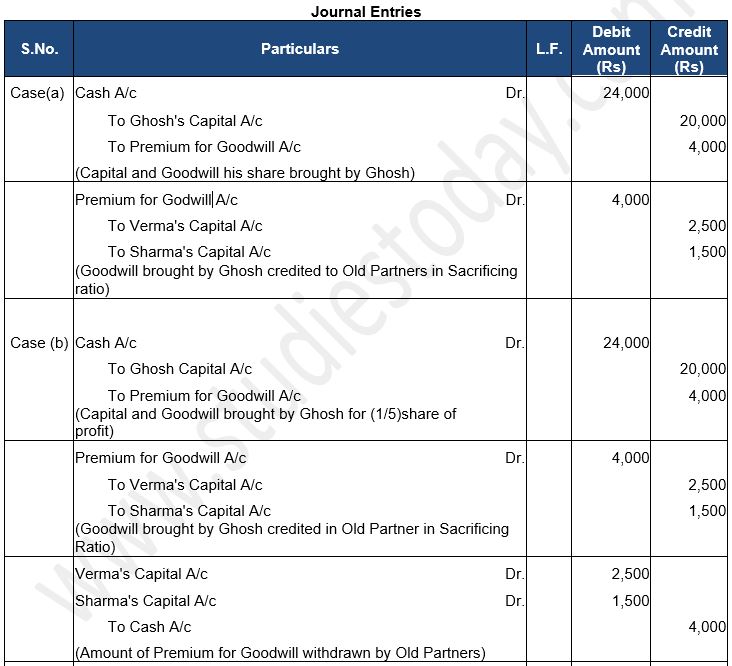

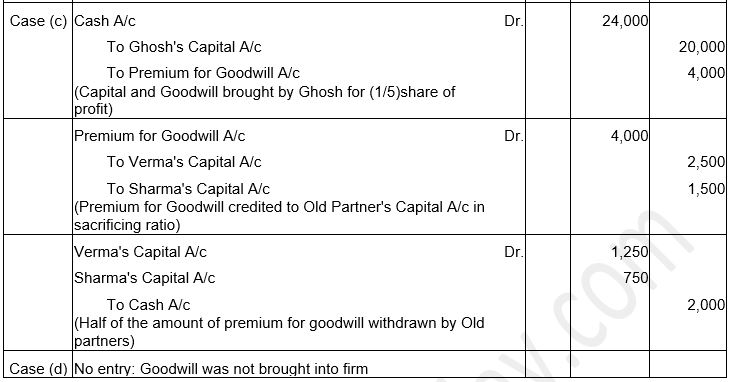

Question 28: Ram and Mohan are partners in a firm sharing profits in the ratio of 3:2. On 1st April, they admit Sohan as a partner for 1/4th share in the profits. Sohan contributed following assets towards his capital and for his share of goodwill.

Stock ₹ 60,000; Debtors ₹ 80,000; Land ₹ 1,00,000, Plant and Machinery ₹ 40,000.

On the date of admission of Sohan, the goodwill of the firm was valued at ₹ 6,00,000.

Pass necessary Journal entries in the books of the firm on Sohan’s admission if:

i) Partners do not withdraw the share of goodwill.

ii) Partners withdraw half of their share of goodwill.

Answer:

Calculation of Treatment of Goodwill:-

Sohan’s Premium of Goodwill = Rs. 6,00,000 × 1/4

Sohan’s Premium of Goodwill = Rs. 1,50,000

Sacrificing Ratio of Ram and Mohan = 3:2.

Ram’s share on Goodwill = 1,50,000 × 3/5 = Rs. 90,000

Mohan’s share on Goodwill = 1,50,000 × 2/5 = Rs. 60,000

Case I

When Premium for Goodwill is brought in by New or Incoming Partner and is withdrawn by Old Partners Fully or Partly

Question 29: A and B are partners in a business sharing profits and losses in the ratio of 1/3rd and 2/3rd. On 1st April, 2024, their capitals are Rs. 8,000 and Rs. 10,000 respectively. On that date, they admit C in partnership and give him 1/4th share in the future profits. C brings in Rs. 8,000 as his capital and Rs. 6,000 as goodwill. The amount of goodwill is immediately withdrawn by the old partners in cash. Draft the journal entries and show the Capital Accounts of all the Partners. Calculate proportion in which partners would share profits and losses in future.

Answer:

About Solution:-

5 situations which may arise in the event of partner's admission which are as follows:

(i) Goodwill (Premium on Goodwill) is paid privately;

(ii) Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is retained in business;

(iii) Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is withdrawn by Sacrificing Partners fully or partly;

(iv) Goodwill (Premium on Goodwill) is brought in kind;

(v) Goodwill (Premium on Goodwill) is not brought in full or a part by the new or Incoming Partner.

Things to Remember:

Calculation of sacrificing ratio when new or incoming partner acquires the share by surrender of a particular fraction Of shares by Old partners: In such a case, the share surrendered by the partner is deducted from his old share of profit to determine his share in the reconstituted firm.

Important notes:

Total of shares surrendered by all the partners in favour of new or incoming partner is considered as the share of new or incoming partner.

Question 30: A and B were partners in a firm sharing profits and losses in the ratio of 3 : 2 . They admitted C as a new partner for 3/7th share in the profit and the new profit-sharing ratio will be 2:2:3. C brought Rs. 2,00,000 as his capital and Rs. 1,50,000 as premium for goodwill. Half of their share of premium was withdrawn by A and B from the firm. Calculate sacrificing ratio and pass necessary journal entries for the above transactions in the books of the firm.

Answer:

About Solution:-

Revaluation of assets and reassessment of liabilities is to be done. The net increase or decrease is then adjusted in the existing partner's capital account in their old profit sharing ratio.

Things to Remember:

Sacrifice made by one or more old partner(s) is the total of share acquired by new or incoming partner and share gained by existing or old partner or partners.

Important notes:

Gain in profit share can be calculated from such shares sacrificed by the partners or where old and new share is given, by using the below mentioned formula.

Gaining Share = New Share - Old Share

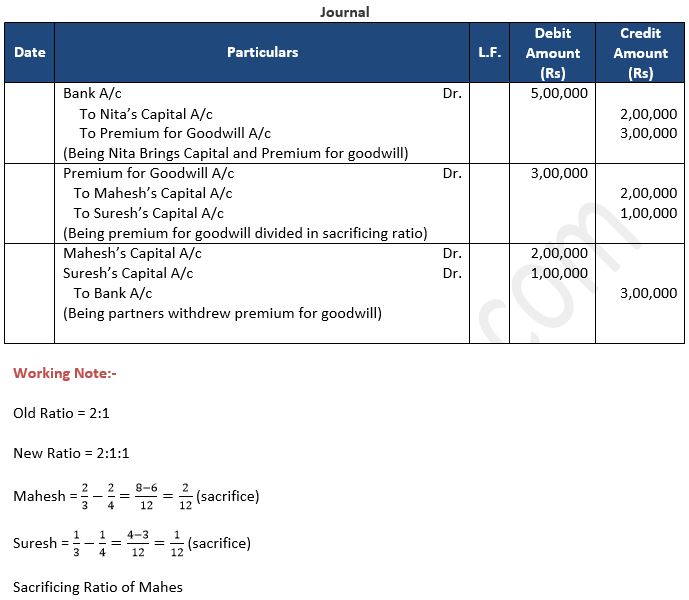

Question 31: Mahesh and Suresh were partners in a firm sharing profits and losses in the ratio of 2:1. They decided to admit Nita into partnership with 1/4th share in the profits. Nita brought ₹ 2,00,000 for her capital and the requisite amount of goodwill premium in cash. The goodwill of the firm is valued at ₹ 12,00,000. The new profit sharing ratio of the partners is 2:1:1. Mahesh and Suresh withdraw their share of goodwill. Pass necessary Journal entries in the books of the firm for the above transactions.

Answer:

When Only Part of Premium for Goodwill is brought by New Partner in Cash

Question 32: A and B are partners sharing profits in the ratio of 2 : 1 . They admit C for 1/4th share in profits. C brings in Rs. 30,000 for his capital and Rs. 8,000 out of his share Rs. 10,000 for goodwill. Before admission, goodwill appeared in books at Rs. 18,000 .Give journal entries to give effect to the above arrangements.

Answer:

About Solution:-

Old partners will continue to share balance profits or losses in their old profit sharing ratio. It means that, in the absence of any information, profit sharing ratio among the existing partners remains unchanged.

Things to Remember:

At the time of change in profit sharing ratio, it is important to determine the Sacrificing ratio and gaining ratio of partners. Explanation: This may result in some partners gaining and others losing

Important Notes:

At the time of the admission of a new partner, there is a change in the profit sharing ratio of the old partners also. The new profit sharing ratio is calculated after considering the new partner's share in profit and the sacrifice made by the old partners.

When New Partner is not able to bring his Share of Premium for Goodwill

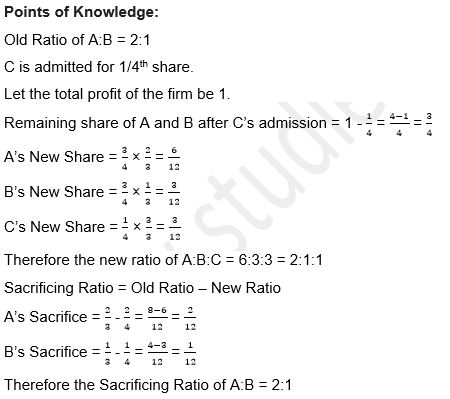

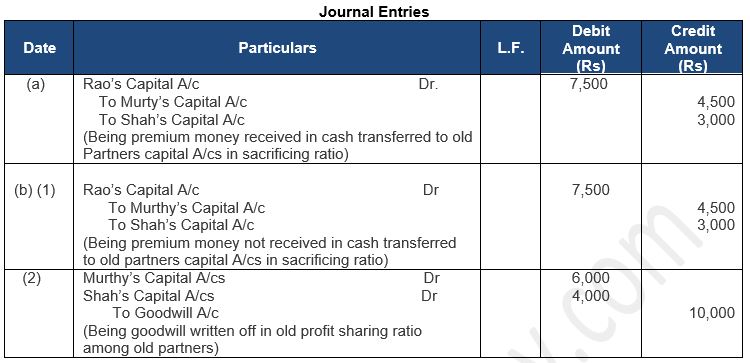

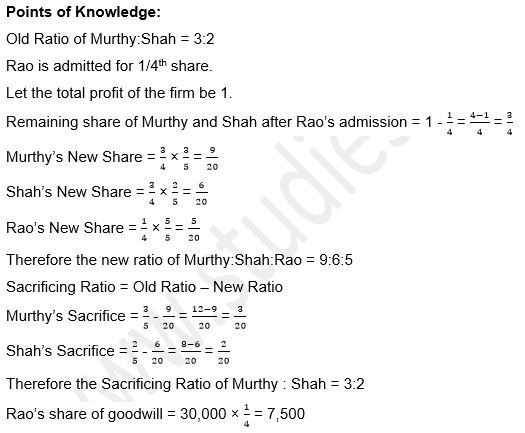

Question 33: On the admission of Rao, goodwill of Murty and Shah is valued at Rs 30,000. Rao is to get 1/4th share of profits. Previously Murty and Shah shared profits in the ratio of 3:2. Rao cannot bring in any cash. Give journal entries in the books of Murty and Shah when:

(a) Goodwill does not exist in the books.

(b) Goodwill exists in the books at Rs 10,000.

Answer:

About Solution:-

Hidden or Inferred Goodwill: It is possible that the value of Goodwill of the firm is not given and such value of goodwill is to be inferred based on the net worth (capital of the firm). Such inferred value of Goodwill is termed as Hidden or Inferred Goodwill.

Things to Remember:

Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is retained in business.

Important Notes:

Goodwill (Premium on Goodwill) is brought in cash or by cheque by the new or Incoming Partner and is withdrawn by Sacrificing Partners fully or partly.

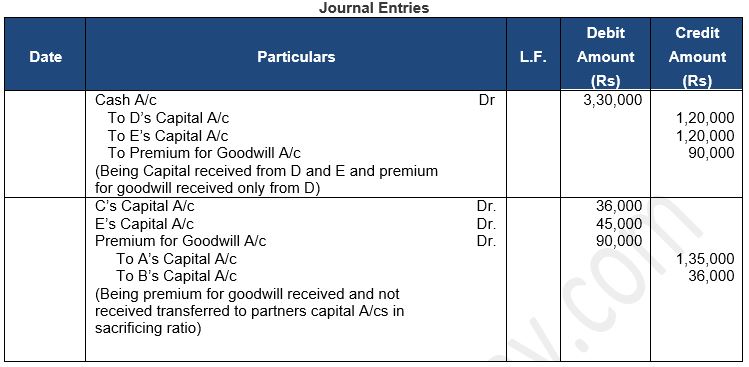

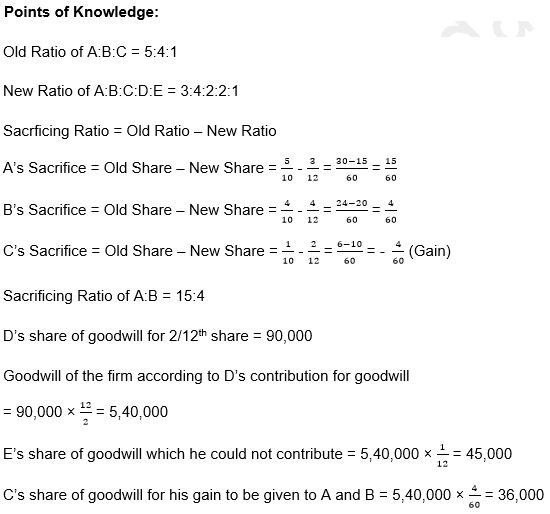

Question 34: A, B and C are in partnership sharing profits and losses in the ratio of 5:4:1 respectively. Two new partners D and E are admitted. The profits are now to be shared in the ratio of 3:4:2:2:1 respectively. D is to pay Rs. 90,000 for his share of Goodwill but E has insufficient cash to pay for Goodwill. Both the new partners introduced Rs. 1,20,000 each as their capital. You are required to pass necessary journal entries.

Answer:

About Solution:-

The partners are not necessarily required to record the revised values in the books of the firm. The partners may decide to:

i) Record revised values of assets and liabilities; or

ii) Not to record the revised values of assets and liabilities.

Things to Remember:

Accounting Treatment when revised values of assets and liabilities are to be recorded: In such situation, revaluation of assets and reassessment of liabilities are to be recorded in an account known as 'Revaluation Account' or 'Profit and Loss Adjustment Account'.

Important Notes:

Any gain or loss from the revaluation of assets and liabilities is to be distributed among the partners in their old profit sharing ratio and is adjusted in their Capital or Current Accounts.

Question 35: A and B are partners in a firm with capital of Rs. 60,000 and Rs. 1,20,000 respectively. They decide to admit C into the partnership for 1/4th share in the future profits. C is to bring in a sum of Rs. 70,000 as his capital. Calculate amount of goodwill.

Answer:

About Solution:-

Accounting Treatment when Goodwill (Premium on Goodwill) is paid privately: In this situation, Goodwill (Premium on Goodwill) is paid by the new or Incoming Partner privately to the sacrificing partners. In such situation, journal entry is not passed in the books of account of the firm.

Things to Remember:

Treatment: All free reserves and profits given in the liabilities side should be credited to Partner's Capital Accounts or Current Account (If Capitals are fixed) and all fictitious assets/ accumulated losses should be debited to the Partner's Capital Account or Current Account (If Capitals are fixed) in their old ratios.

Important Notes:

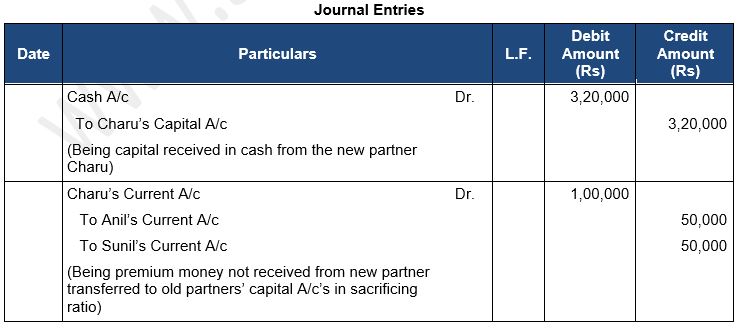

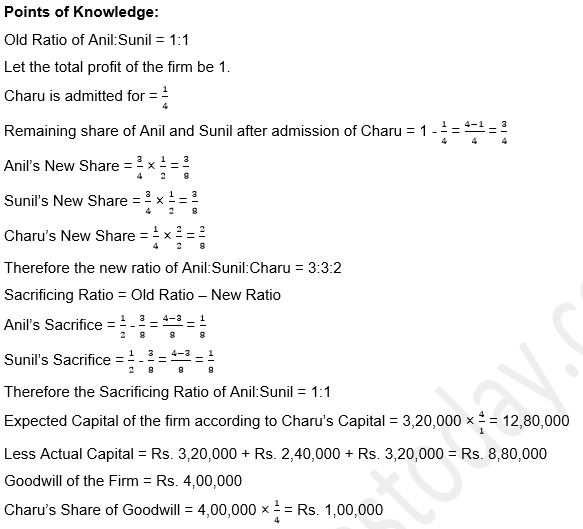

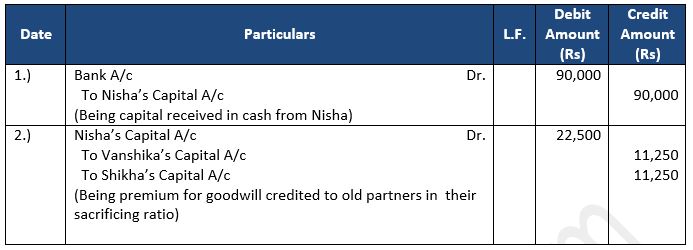

Treatment of Revaluation of Assets and Re-assessment of liabilities and Preparation of Revaluation Account is same as we have done in case of Admission of a partner.

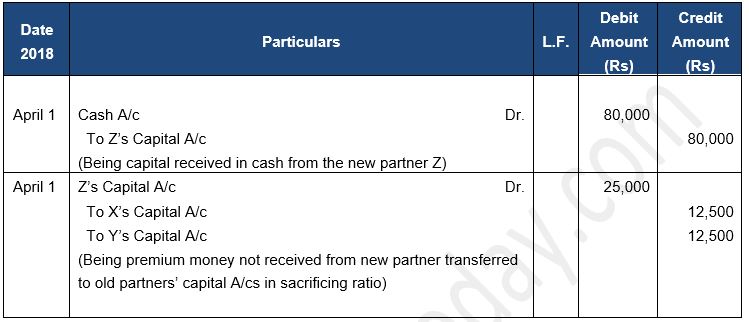

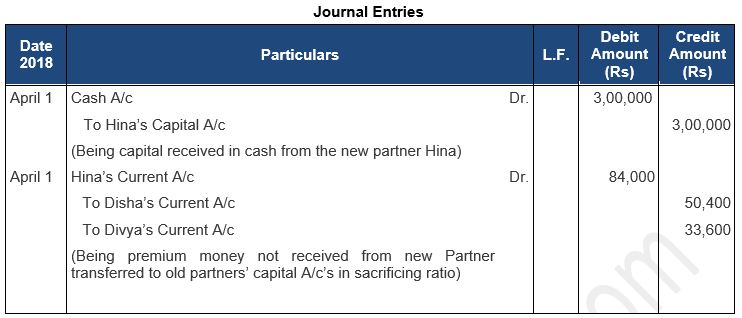

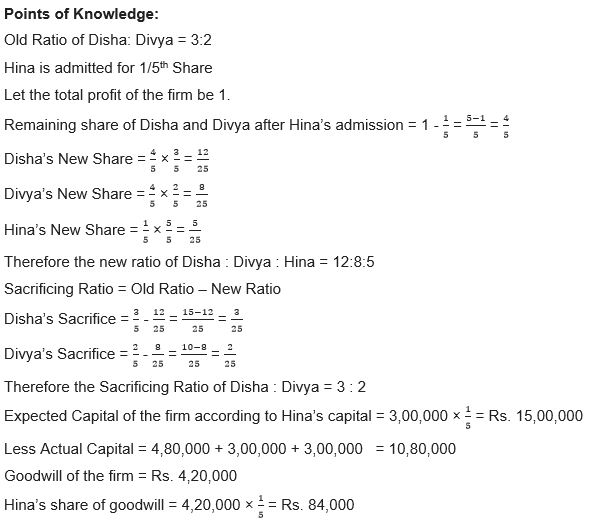

Question 36: Anil and Sunil are partners in a firm with fixed capitals of Rs 3,20,000 and Rs 2,40,000 respectively. They admitted Charu as a new partner for 1/4th share in the profits of the firm on 1st April, 2012. Charu brought Rs 3,20,000 as her share of capital.

Calculate value of goodwill and record necessary journal entries.

Answer:

About Solution:-

Understanding Revaluation Account: It is an account which is used to record change in value of assets and liabilities. Following are the items which are to be recorded in the Revaluation Account: Credited to Revaluation Account:

i) Increase in assets,

ii) Unrecorded assets,

iii) Decrease in liabilities,

iv) Writing back excess provision.

Things to Remember:

At the time of retirement of a partner, all the accumulated profits/Losses and Reserves are to be distributed to the old partners in their old profit-sharing Ratio.

Important Notes:

Goodwill given in the Balance Sheet of the firm should be debited all old partners in their old ratio.

Question 37: Vanshika and Shikha were partners in a firm with capitals of ₹ 1,00,000 and ₹ 80,000 respectively. They admitted Nisha on 1st April, 2022 as a new partner for 1/4th share in the future profits of the firm. Nisha brought ₹ 90,000 as her capital. Nisha acquired her share equally from Vanshika and Shikha. Calculate the value of goodwill of the firm and pass necessary Journal entries on Nisha’s admission, assuming that Nisha did not bring her share of goodwill premium in cash. Show the working clearly.

Answer:

Working note:-

Calculation of Hidden Goodwill of the firm:-

Total capital of the Firm according to new partner share = New partners Capital × reciprocal of new partners share

Total capital of the Firm = Rs. 90,000 × 4/1

Total capital of the Firm = Rs. 3,60,000

Total capital of the Firm = Rs. 1,00,000 + Rs. 80,000 + Rs. 90,000

Total capital of the Firm = Rs. 2,70,000

Goodwill of the Firm = Rs. 3,60,000 – Rs. 2,70,000

Goodwill of the Firm = Rs. 90,000

Question 38: X and Y are partners with capitals of Rs. 50,000 each. They admit Z as a partner with 1/4th share in the profits of the firm. Z brings in Rs. 80,000 as his share of capital. The Profit and Loss A/c showed a credit balance of Rs. 40,000 as on date of admission of Z.

Give necessary journal entries to record the goodwill.

Answer:

About Solution:-

Accounting Treatment when Goodwill (Premium on Goodwill) is paid privately: In this situation, Goodwill (Premium on Goodwill) is paid by the new or Incoming Partner privately to the sacrificing partners. In such situation, journal entry is not passed in the books of account of the firm.

Things to Remember:

Profit from the date of last balance sheet to the date of death = (Number of days or month from the date of last balance sheet to the date of death/ 365 or 12) x Previous years' profit or Average profits of given number of past years.

Important Notes:

Average sales of given number of past years) x Previous years' Profits or Average Profits of given number of Past years.

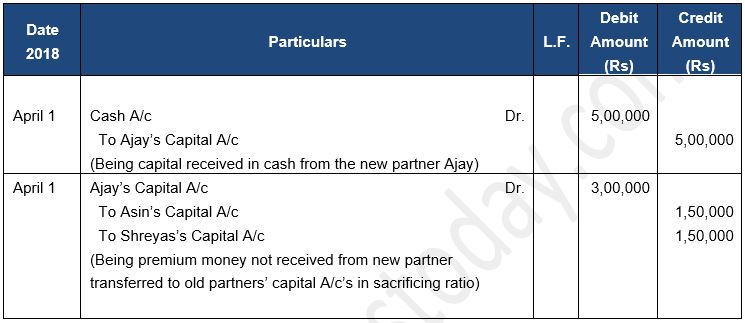

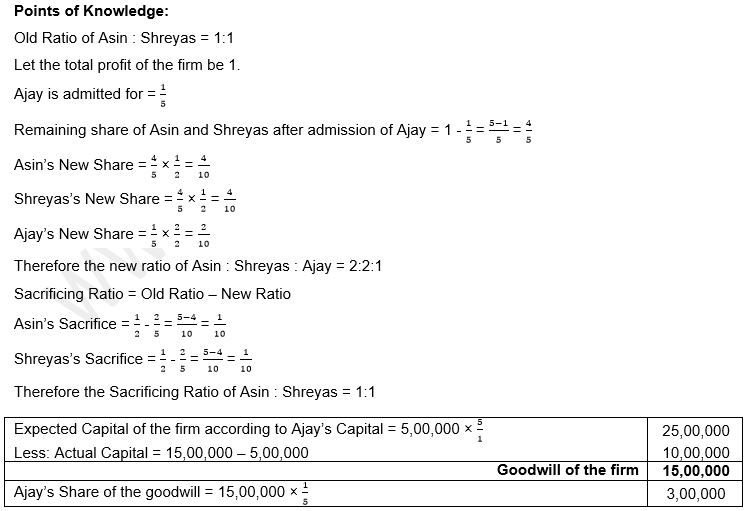

Question 39: Asin and Shreyas are partners in a firm. They admit Ajay as a new partner with 1/5th share in the profits of the firm. Ajay brings Rs. 5,00,000 as his share of capital. The value of the total assets of the firm was Rs. 15,00,000 and outside liabilities were valued at Rs. 5,00,000 on that date . Give necessary journal entry to record goodwill at the time of Ajay's admission. Also show your workings.

Answer:

About Solution:-

Amount of Goodwill is credited to the New Partner's Capital Account and thereafter, adjusted in favour Of Old or existing partners in their sacrificing ratio for which following entries are passed:

(i) Cash/Bank A/c

To New Partner's Capital

(ii) New Partner's Capital A/c

To Sacrificing Partner's Capital/Current A/c (Individually)

(Being the goodwill brought by new partner distributed among the sacrificing partners in their sacrificing ratio)

Things to Remember:

Treatment of Revaluation of Assets and Re-assessment of liabilities and Preparation of Revaluation Account is same as we have done in case of Admission of a partner.

Important Notes:

All free reserves and profits given in the liabilities side should be credited to Partner's Capital Accounts or Current Account (If Capitals are fixed) and all fictitious assets/ accumulated losses should be debited to the Partner's Capital Account or Current Account (If Capitals are fixed) in their old ratios.

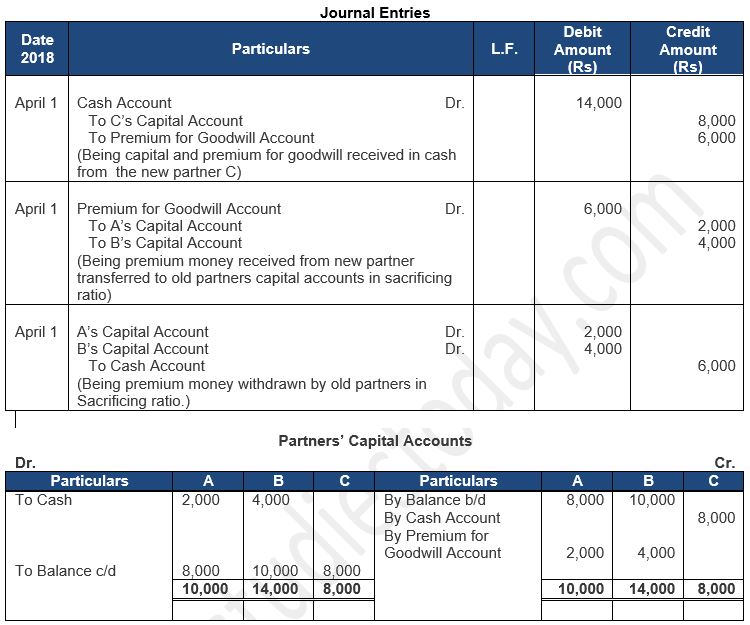

Question 40: Arun and Vijay are partners in a firm sharing profits & loss in the ratio of 3:2.

If the value of machinery in the Balance Sheet is excess by 33 1/3%, find the value of machinery to be shown in the New Balance Sheet.

Answer:

Calculation of Correct Book value of Machinery:-

Let value of the Machinery be x

Now according to the question,

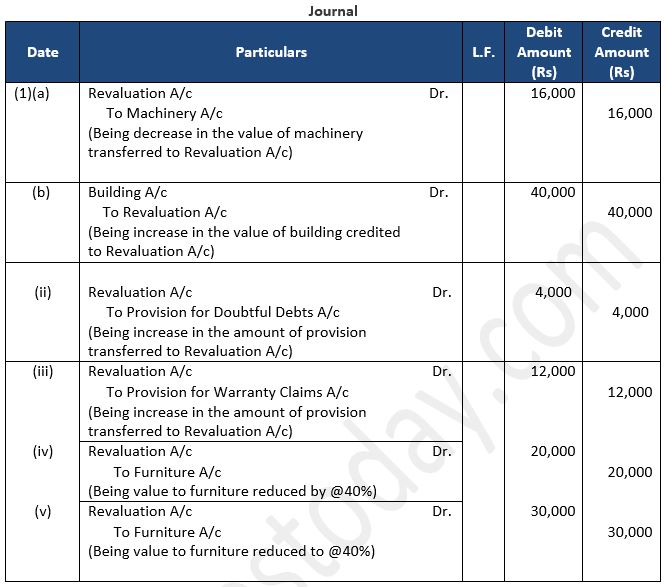

Question 41: Pass entries in the firm's journal for the following on admission of a partner:

(i) Machinery be depreciated by Rs. 16,000 and Building be appreciated by Rs. 40,000.

(ii) A provision be created for Doubtful Debts @ 5% of Debtors amounting to Rs. 80,000.

(iii) Provision for warranty claims be increased by Rs. 12,000.

(iv) Furniture (Book Value Rs. 50,000) is to be reduced by 40%.

(v) Furniture (Book Value Rs. 50,000) is to be reduced to 40%.

Answer:

About Solution:-

Accounting Treatment when revised values of assets and liabilities are to be recorded: In such situation, revaluation of assets and reassessment of liabilities are to be recorded in an account known as 'Revaluation Account' or 'Profit and Loss Adjustment Account'.

Things to Remember:

In case of change in profit sharing ratio among the partners or admission or retirement/death of a partner, goodwill is not to be raised in the books of the firm as no consideration in money or money's worth is paid for it. If goodwill is raised, it should be immediately written off.

Important Notes:

Accounting Treatment of Goodwill at the time of Admission of a Partner: In the event of admission of a partner, new partner who acquires the share in future profits from the existing partners should compensate sacrificing partners by paying them an amount.

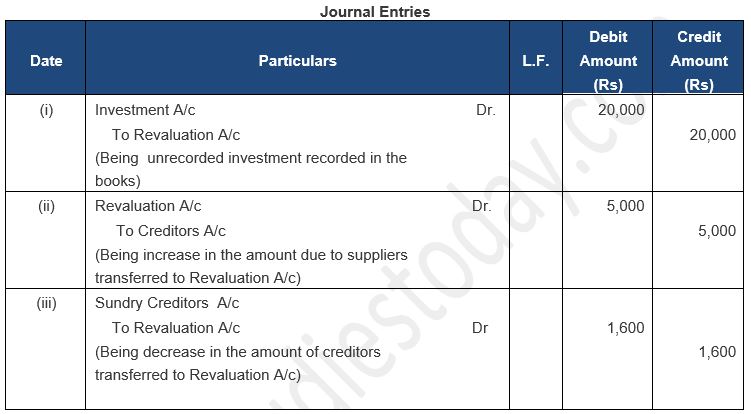

Question 42: Pass entries in the firm's journal for the following on admission of a partner:

(i) Unrecorded Investments of Rs. 20,000 are to be accounted.

(ii) Unrecorded liability towards suppliers for Rs. 5,000 is to be accounted.

(iii) An item of Rs. 1,600 included in Sundry Creditors is not likely to be claimed and hence should be written back.

Answer:

About Solution:-

Accounting Treatment when Goodwill (Premium on Goodwill) is paid privately: In this situation, Goodwill (Premium on Goodwill) is paid by the new or Incoming Partner privately to the sacrificing partners. In such situation, journal entry is not passed in the books of account of the firm.

Things to Remember:

Accounting Treatment of Goodwill Existing in Books of Account Goodwill existing in the books of the firm is written off by debiting Old Partners' Capital Account/Current Account in their Old Profit Sharing Ratio and crediting Goodwill Account.

Old Partners' Capital/Current A/c Dr. (in Old Ratio)

To Goodwill A/c

Important Notes:

Accounting Treatment when Goodwill (Premium on Goodwill) is paid privately: In this situation, Goodwill (Premium on Goodwill) is paid by the new or Incoming Partner privately to the sacrificing partners. In such situation, journal entry is not passed in the books of account of the firm.

Question 43: X and Y are partners in a firm sharing profits in the ratio of 3:2. They admitted Z as a new partner and fixed the new profit-sharing ratio as 3:2:1. At the time of admission of Z, Debtors and Provision for Doubtful Debts appeared at Rs. 50,000 and Rs. 5,000 respectively all debtors are good. Pass the necessary journal entries.

Answer:

About Solution:-

Decrease in the value of an asset:

Revaluation A/c Dr.

To Asset A/c (Individually)

Things to Remember:

Assets and liabilities revalue are to be shown in the books of firm at the revalue figures only.

Important Notes:

Decrease in the amount Of a liability:

Liability A/c (Individually) Dr.

To Revaluation A/c

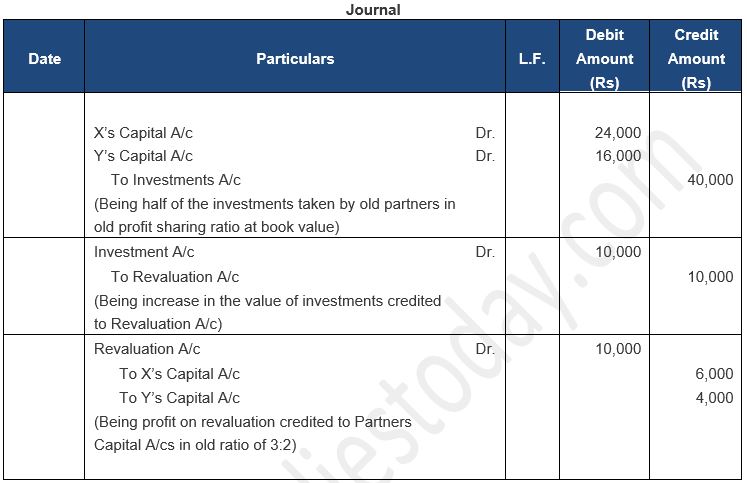

Question 44: X and Y are partners sharing profits in the ratio of 3:2. They admitted Z as a new partner for 1/4th share of profits. At the time of admission of Z, Investments appeared at Rs. 80,000. Half of the investments to be taken over by X and Y in their profit-sharing ratio at book value. Remaining investments were valued at Rs 50,000. Pass the necessary journal entries.

Answer:

About Solution:-

Decrease in the amount Of a liability:

Liability A/c (Individually) Dr.

To Revaluation A/c

Things to Remember:

Recording an unrecorded asset:

Unrecorded Asset A/c Dr.

To Revaluation A/c

Important Notes:

Recording an unrecorded liability:

Revaluation A/c Dr.

To Unrecorded Liability A/c

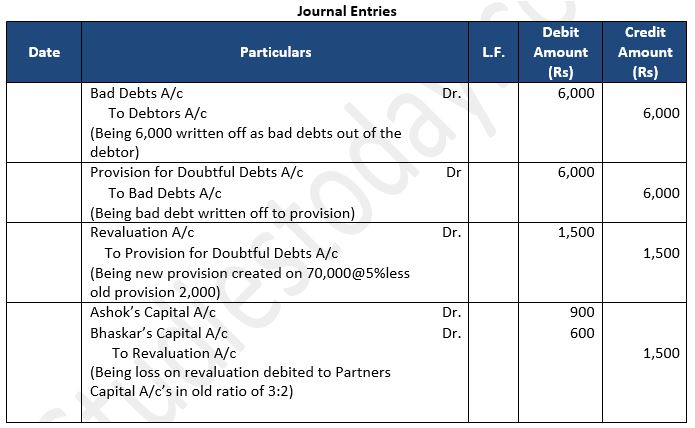

Question 45: Ashok and Bhaskar are partners sharing profits in the ratio of 3:2. They admitted Chaman as a partner for 1/4th share of profits. At the time of admission of Chaman, Sundry Debtors and Provision for Doubtful Debts existed at Rs. 76,000 and Rs. 8,000 respectively. Rs. 6,000 of the debtors proved bad. A provision of 5% is to be created on Sundry Debtors for doubtful debts. Pass the necessary journal entries.

Answer:

About Solution:-

Revaluation Loss:

Old Partners' Capital A/c

To Revaluation A/c

Things to Remember:

Revaluation Gain (profit):

Revaluation A/c Dr.

To Old Partners' Capital A/c [In old profit sharing ratio]

Important Notes:

If Revaluation Account is prepared by an entity, assets and liabilities will appear in the Balance Sheet of the reconstituted firm at their revised (changed) values.

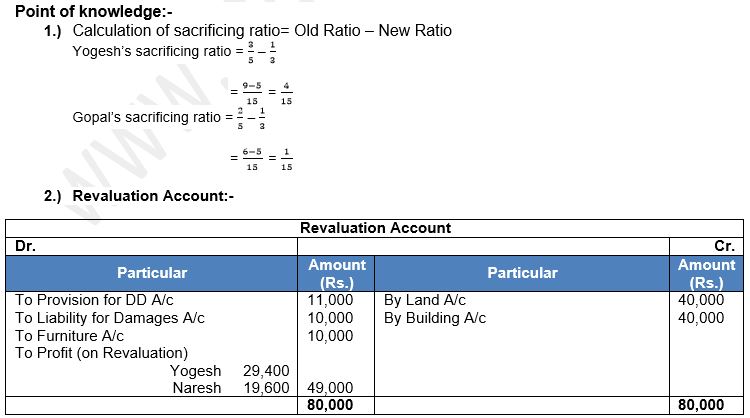

Question 46: At the time of admission of a partner Suresh, assets and liabilities of Ramesh and Naresh were revalue as follows:

(a) A Provision for Doubtful Debts @10% was made on Sundry Debtors (Sundry debtors Rs. 50,000).

(b) Creditors were written back by Rs. 5,000.

(c) Building was appreciated by 20% (Book Value of Building Rs. 2,00,000).

(d) Unrecorded Investments were worth Rs. 15,000.

(e) A Provision of Rs. 2,000 was made for an Outstanding Bill for repairs.

(f) Unrecorded Liability towards suppliers was Rs. 3,000.

Pass necessary journal entries.

Answer:

About Solution:-

Decrease in the value of assets and decrease in the amount Of liabilities:

Memorandum Revaluation A/c Dr.

To Assets A/c (Individually)

To Liabilities A/c (Individually)

Things to Remember:

Transferring the balance of the first part of the Memorandum Revaluation Account:

If credit side exceeds debit side and it is a gain:

Memorandum Revaluation A/c Dr.

To Old Partners' Capital A/c [In old ratio]

Important Notes:

If debit side exceeds credit side and it is a loss:

Old Partner’s Capital A/c Dr.

To Memorandum Revaluation A/c [In old ratio]

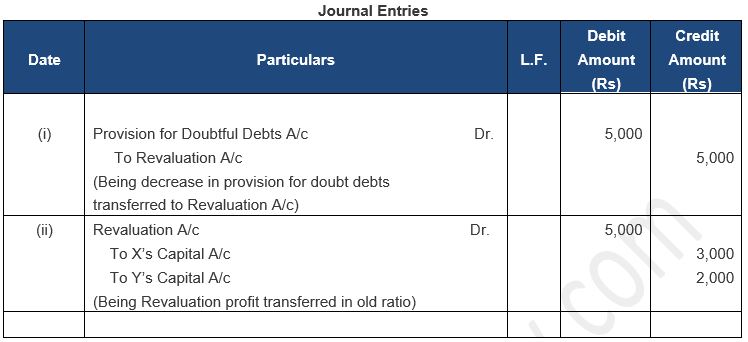

Question 47: Om and Shiv are partners in a firm sharing profits equally.

An amount of ₹ 12,000 due from Mohan, a debtor, is to be written off as no longer receivable, Provision for Doubtful Debts on remaining debtors is to be maintained at the current rate.

What amount of Provision for Doubtful Debts should be credited to maintain its current rate?

Answer:

Current Rate of Provision for Doubtful Debts = 15,000/1,50,000×100

Current Rate of Provision for Doubtful Debts = 10%

New Provision for Doubtful Debts = (Rs. 1,50,000 – Rs. 12,000) × 15% = Rs. 13,800

Provision for doubtful debts = Rs. 15,000 – Rs. 12,000 – Rs. 13,800

Provision for doubtful debts = Rs. 10,800

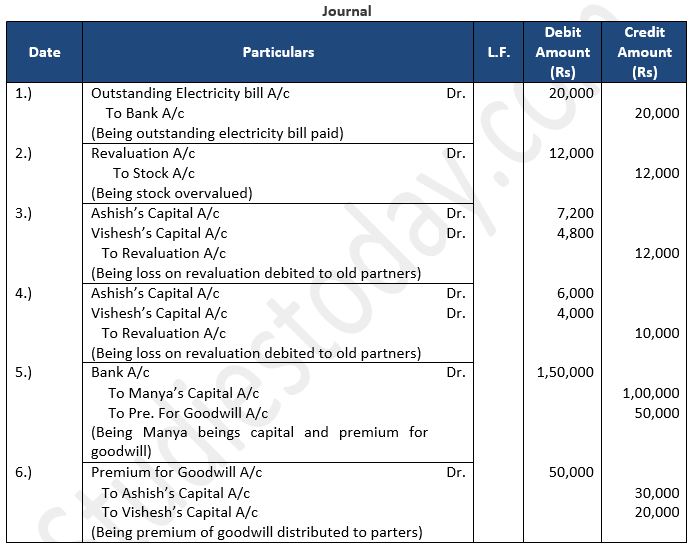

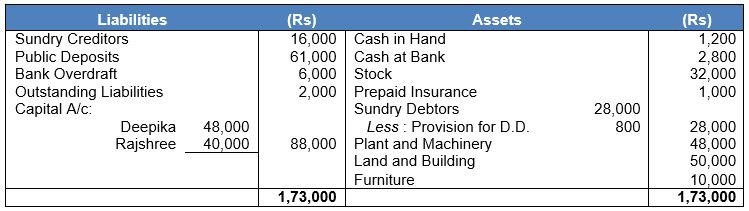

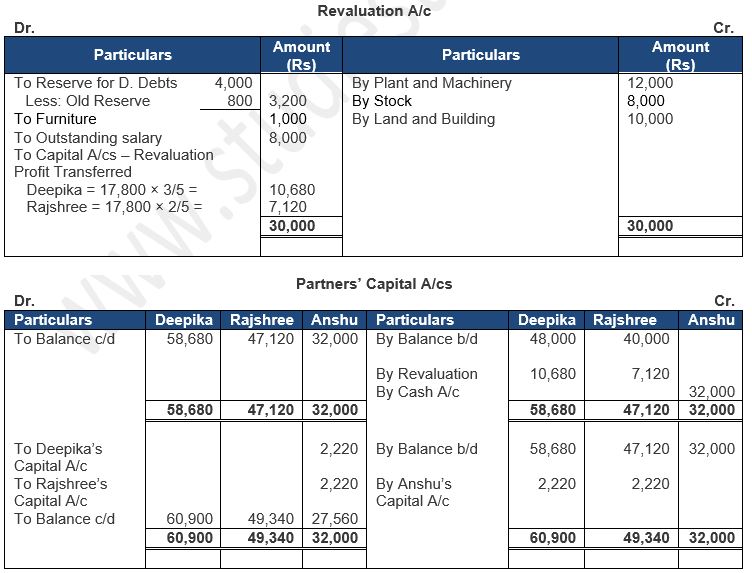

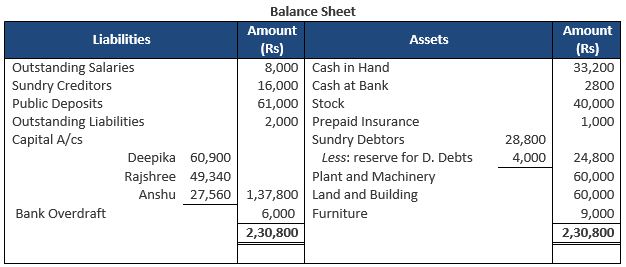

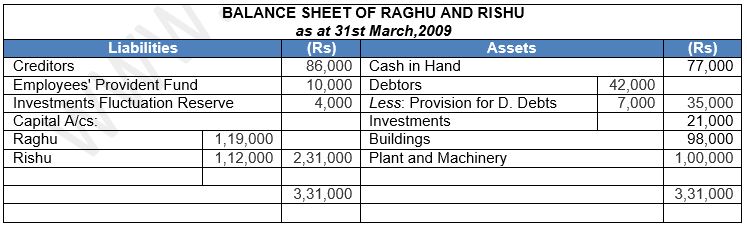

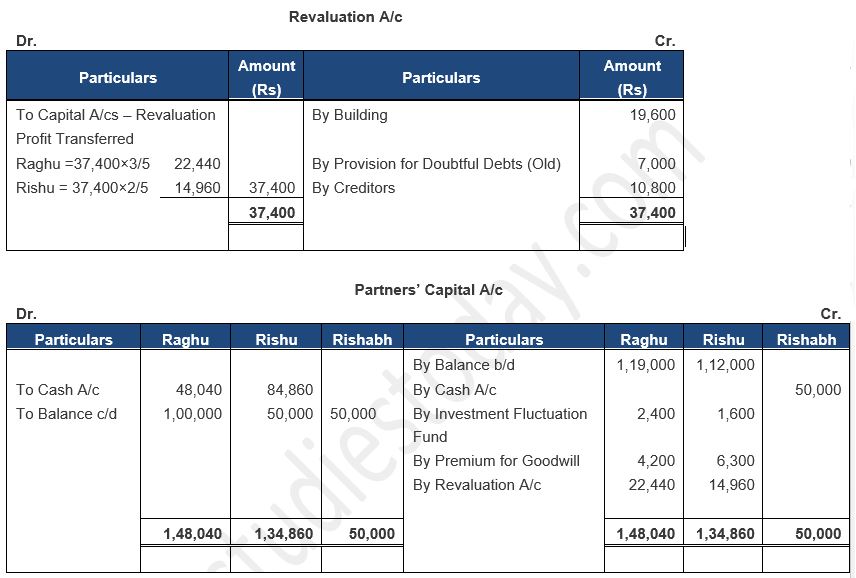

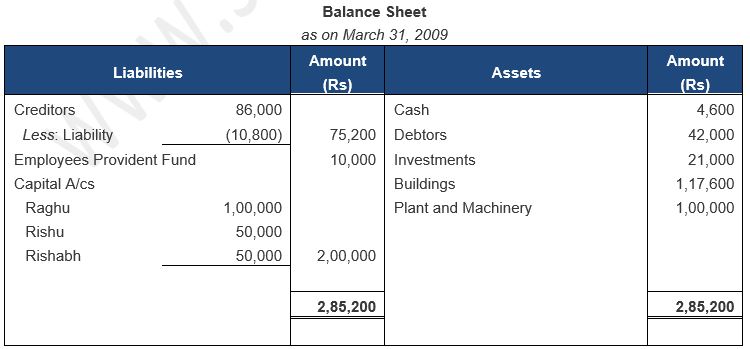

Question 48: Ashish and Vishesh were partners sharing profits and losses in the ratio of 3 : 2. Their Balance Sheet as at 31st March, 2022 was as under:

On 1st April, 2022, Manya was admitted into the firm with 1/4th share in the profits on the following terms:

(i) Manya will bring ₹ 1,00,000 as her capital and ₹ 50,000 as her share of goodwill premium in cash.

(ii) Outstanding electricity bill will be paid off.

(iii) Stock was found over valued by ₹ 12,000.

Pass the necessary Journal entries in the books of the firm on Manya’s admission.

Answer:

About Solution:-

1.) In the absence of any further information, sacrificing ratio is always equal to the old ratio of the partners.

2.) In the absence of any further information, revaluation loss is debited to the old partners in old ratio.

Question 49: Ram and Shyam were partners in a firm sharing profits and losses in the ratio of 2:1. Mohan was admitted for 1/3rd share in the profits. On the date of Mohan's admission, the Balance Sheet of Ram and Shaym showed General Reserve of Rs. 2,50,000 and a credit balance of Rs. 50,000 in Profit and Loss A/c. Pass necessary journal entries on the treatment of these items on Mohan's admission.

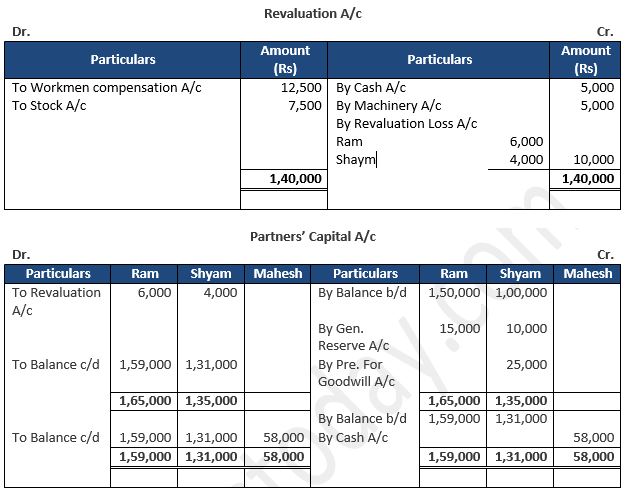

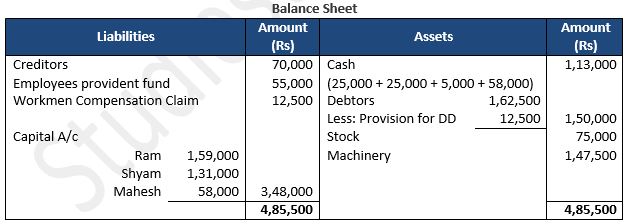

Answer:

About Solution:-

Increase in the value of assets and decrease in the amount of liabilities:

Assets A/c (Individually) Dr.

Liabilities A/c (Individually) Dr.

To Memorandum Revaluation A/c

Things to Remember:

When bad debts and provision for doubtful debts both are specified in the question, first bad debts are to be deducted from Debtors and then Provision for Doubtful Debts is to be calculated on balance bad debts. Any excess of Bad Debts over old Provision for Doubtful Debts should be debited to Revaluation Account. Also, any deficit in Provision for Doubtful Debts should be debited to Revaluation Account.

Important Notes:

Accounting Treatment when revised values of assets and liabilities are not to be recorded: In such case, the partners may decide that the value of assets and liabilities will continue to appear in the books at their existing values and therefore, any increase or decrease in the value of assets and liabilities is recorded in the Memorandum Revaluation Account.

Question 50: X and Y are partners in a firm sharing profits and losses in the ratio of 3:2. On 1st April, 2024, they admit Z as a new partner for 1/5th share in profits. On that date, there was a balance of Rs. 1,50,000 in General Reserve and a debit balance of Rs. 20,000 in the Profit and Loss A/c of the firm. Pass necessary journal entries regarding adjustment of reserve and accumulated profit/loss.

Answer:

About Solution:-

(i) Reversing the first entry:

Memorandum Revaluation A/c Dr.

To Assets A/c (Individually)

To Liabilities A/c (Individually)

(ii) Reversing the second entry:

Assets A/c (Individually) Dr.

Liabilities A/c (Individually) Dr.

To Memorandum Revaluation A/c

Things to Remember:

Accounting Treatment when revised values of assets and liabilities are not to be recorded: In such case, the partners may decide that the value of assets and liabilities will continue to appear in the books at their existing values and therefore, any increase or decrease in the value of assets and liabilities is recorded in the Memorandum Revaluation Account.

Important Notes:

Memorandum Revaluation Account is prepared by the partners of the firm when they mutually decide to give effect to the revaluation of assets and reassessment of liabilities without affecting the existing book values.

Question 51: (a) An extract of the Balance Sheet of Murari and Vohra sharing profits and losses in the ratio of 3:2 was as under:

New Partner Krishna was admitted for 1/5th share of profits. A claim on account of workmen Compensation Reserve is estimated for ₹ 900.

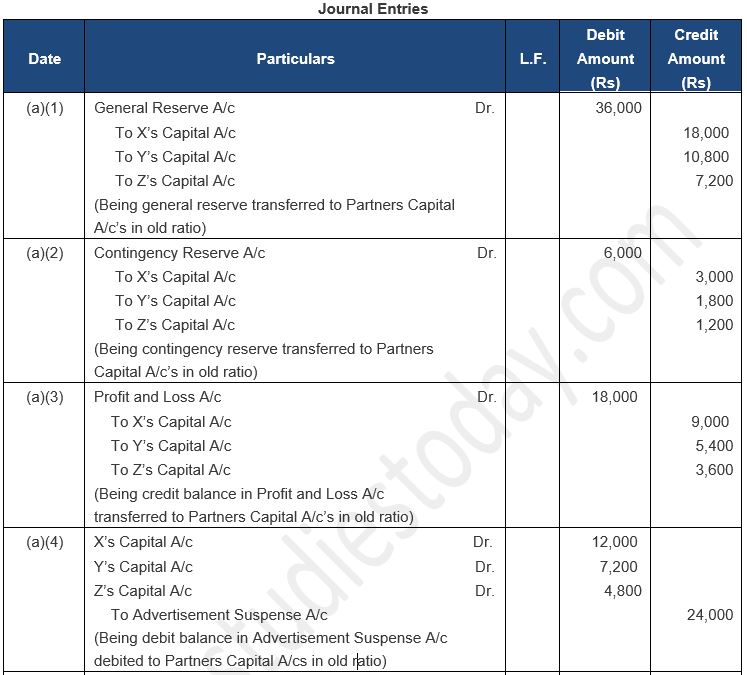

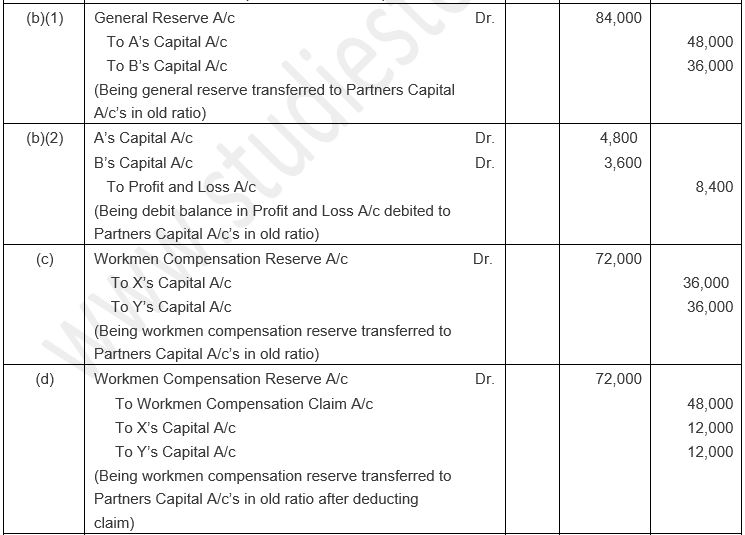

Pass the necessary Journal entries to adjust accumulated profits and losses.

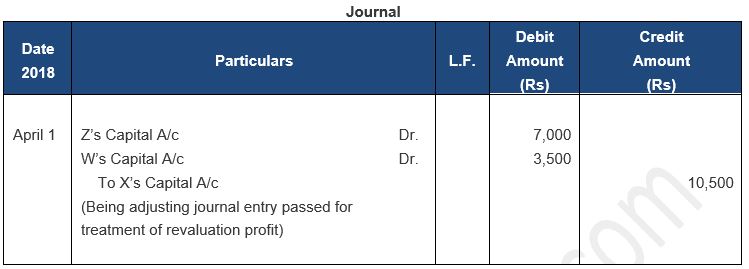

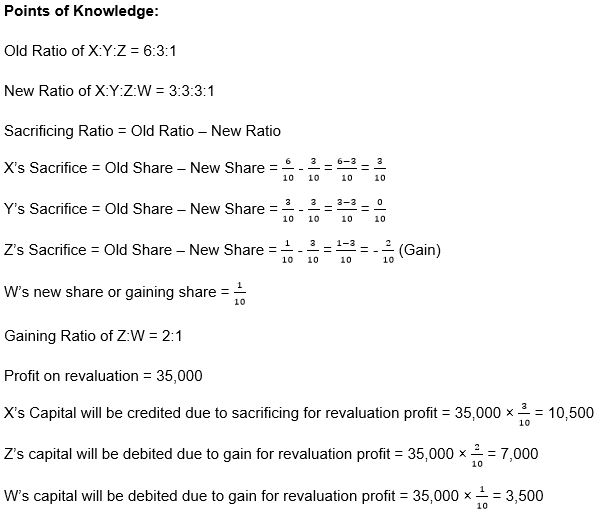

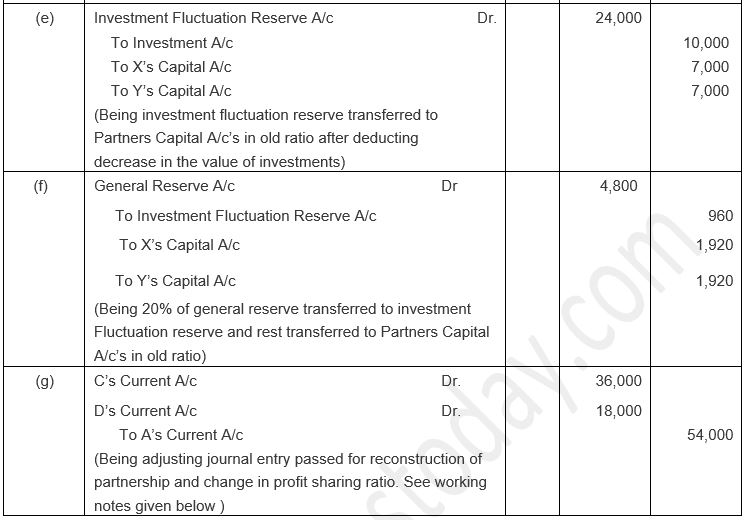

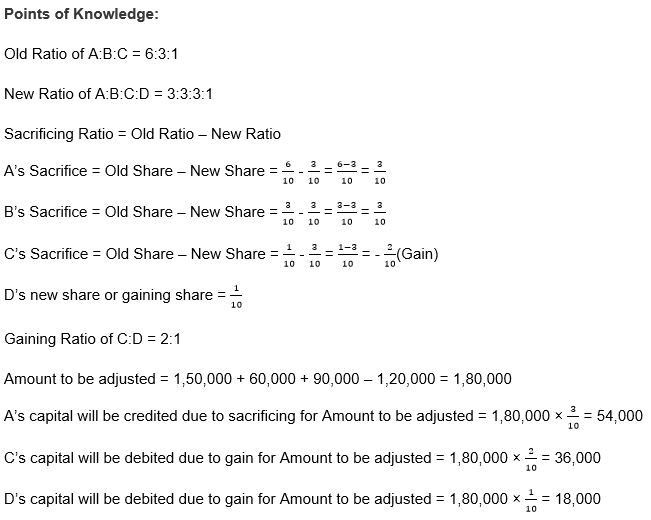

(b) A, B and C were partners sharing profits and losses in the ratio of 6 : 3 : 1. They take D into partnership with effect from 1st April, 2023. The new profit sharing ratio between A, B, C and D will be 3:3:3:1. They also decide to record the effect of the following without affecting their book values by passing an adjusting entry:

Pass the necessary adjustment entry through the Partner’s Current Account.

Answer:

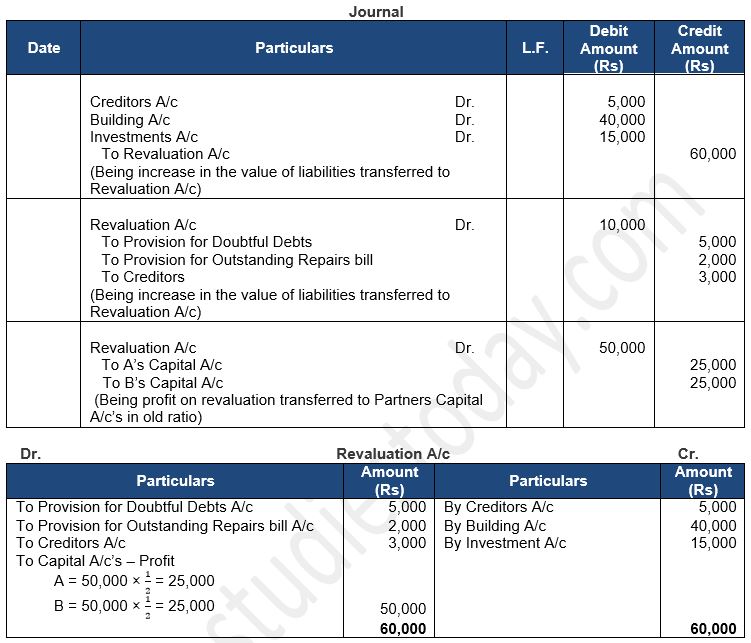

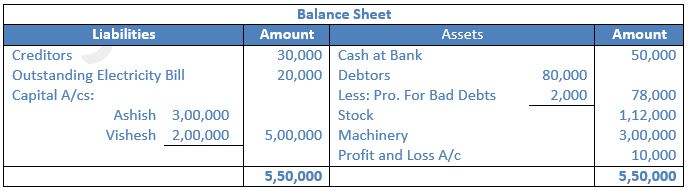

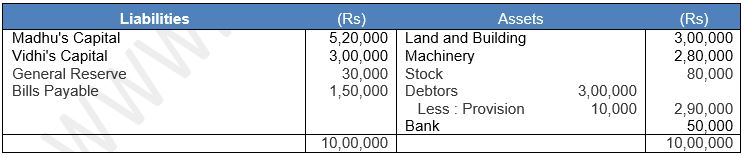

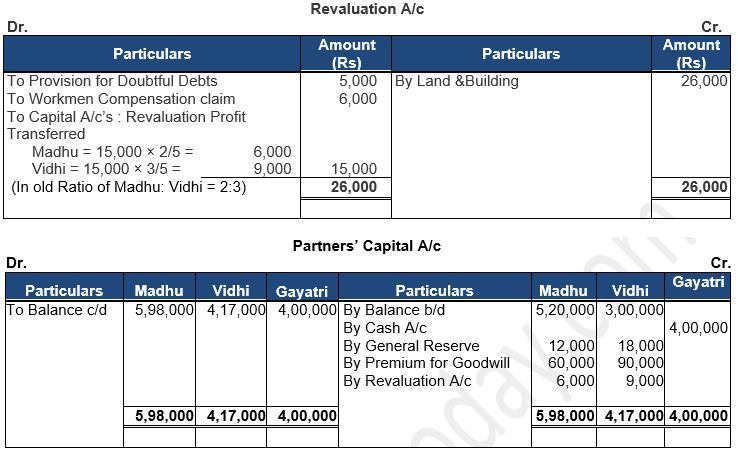

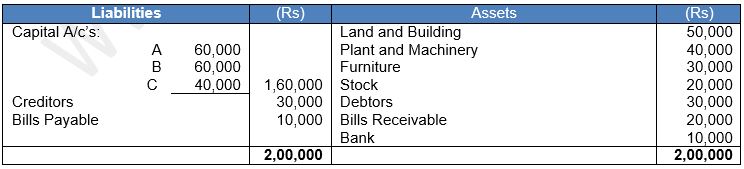

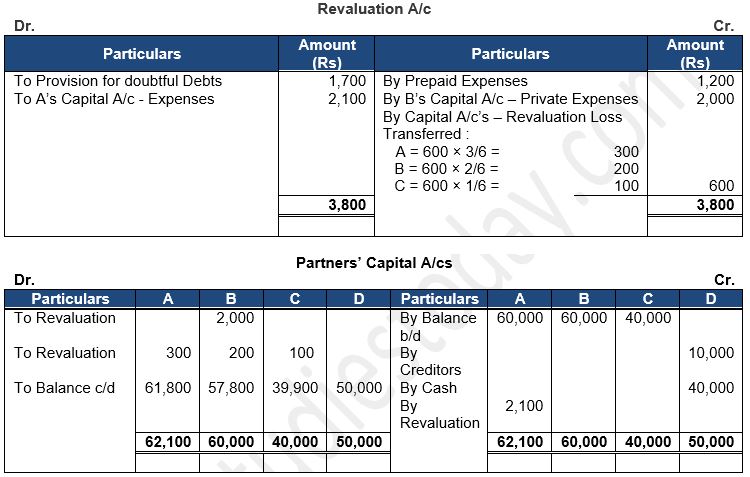

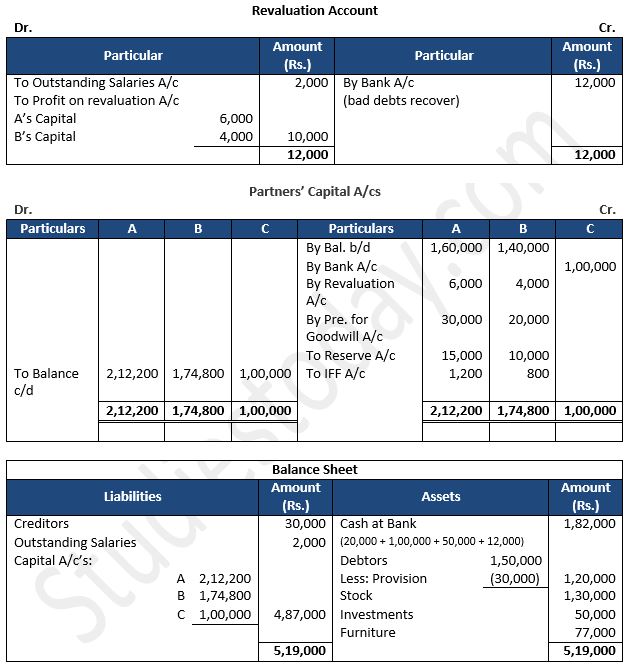

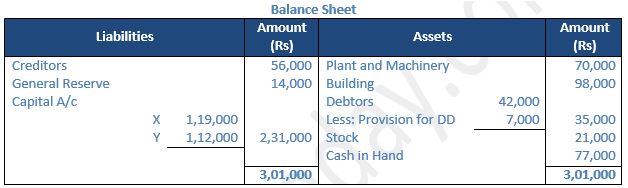

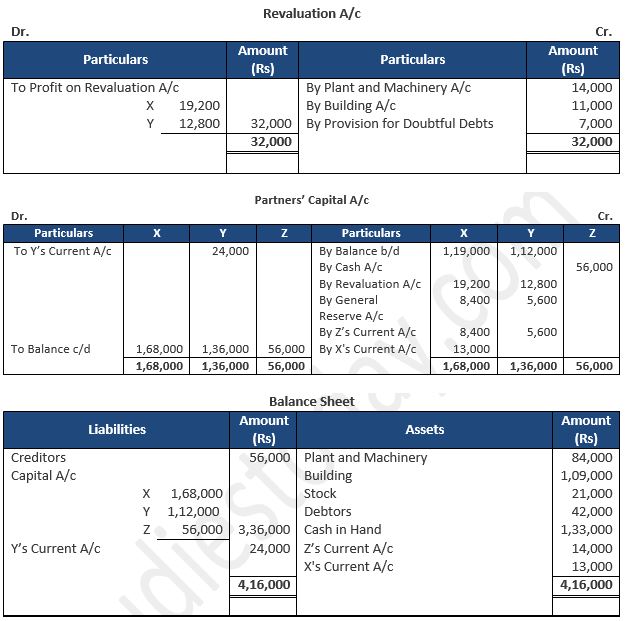

Question 52: Amit and Anil are partners sharing profits and losses in the ratio of 2:1. Their Balance Sheet as on 31st March, 2023 was as follows:

Ankit is admitted as a partner on the date of the Balance Sheet on the following terms:

(a) Ankit will being in ₹ 1,00,000 as his capital and ₹ 60,000 as his share of goodwill for 1/4th share in profits.

(b) Machinery is to be appreciated to ₹ 1,20,000 and the value of building is to be appreciated by 10%.

(c) Stock is found overvalued by ₹ 4,000.

(d) General Reserve will continue to appear in the books of the reconstituted firm at its original value.

(e) A Provision for Doubtful Debts is to be created at 5% of debtors.

(f) Creditors were unrecorded to the extent of ₹ 1,000.

Prepare Revaluation Account and Partner’s Capital Accounts.

Answer:

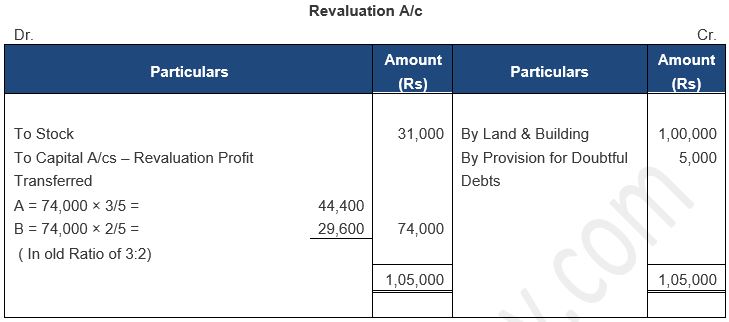

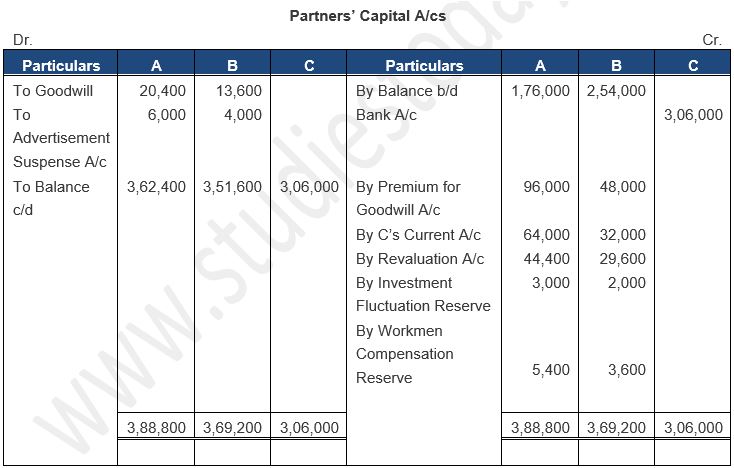

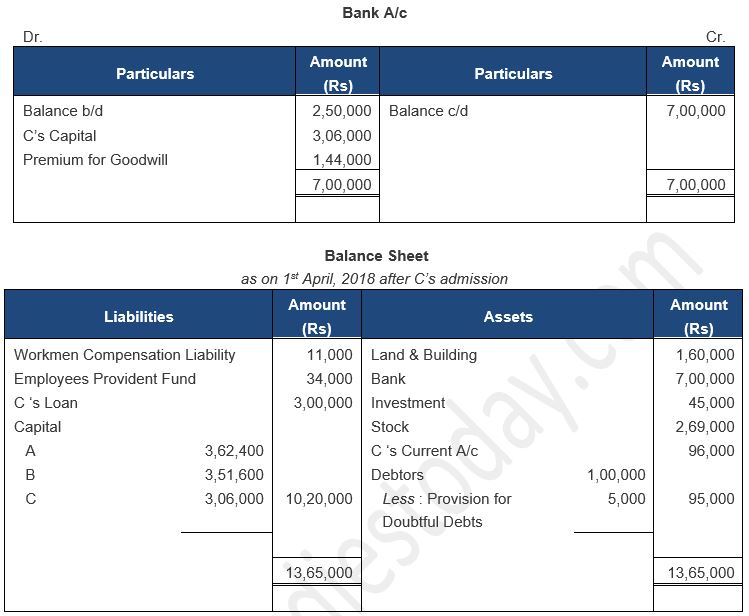

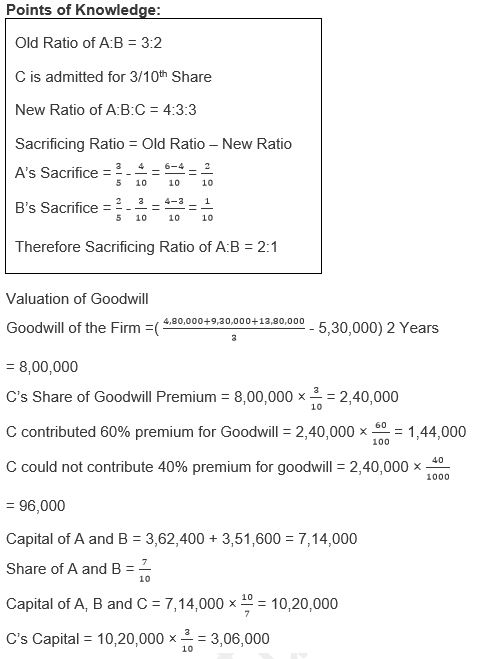

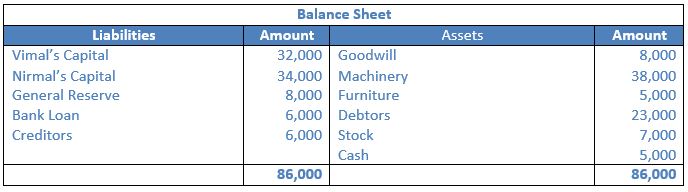

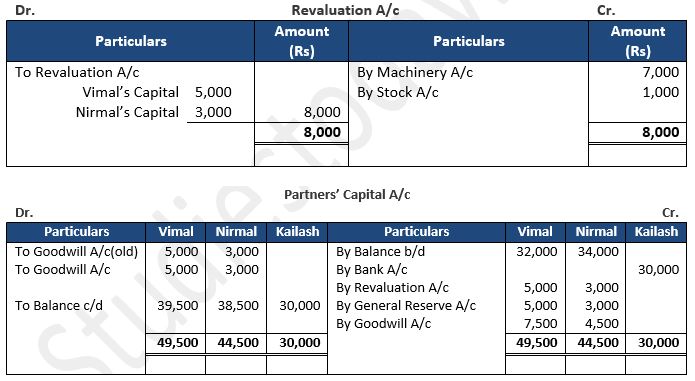

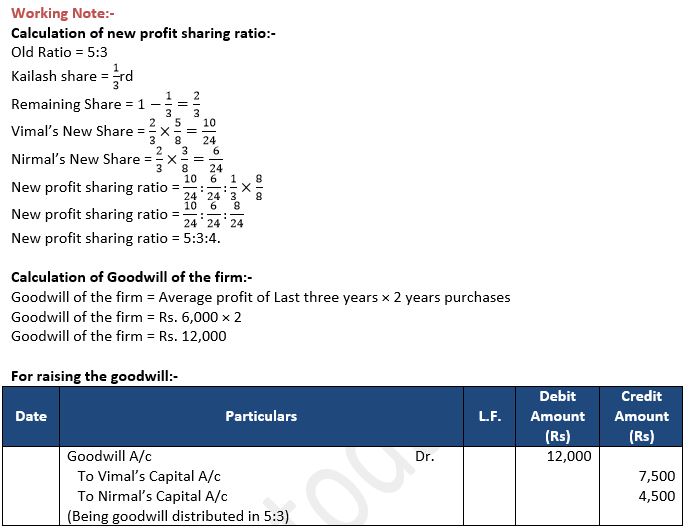

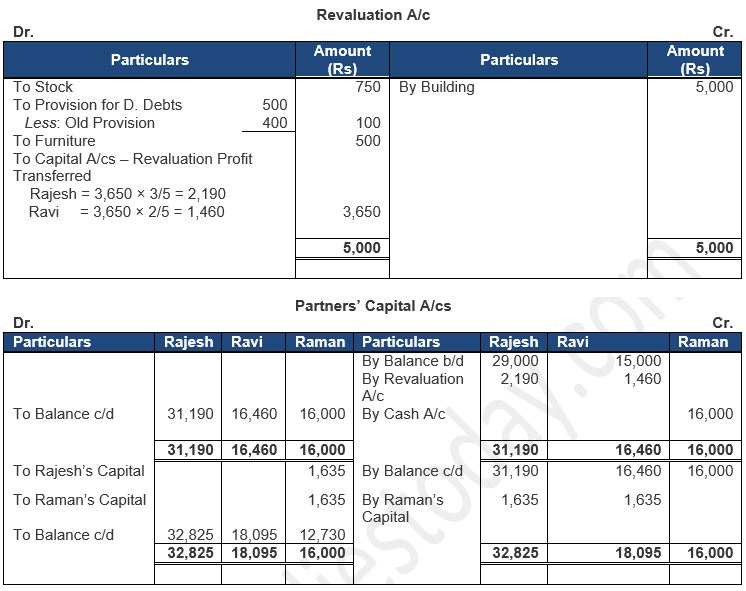

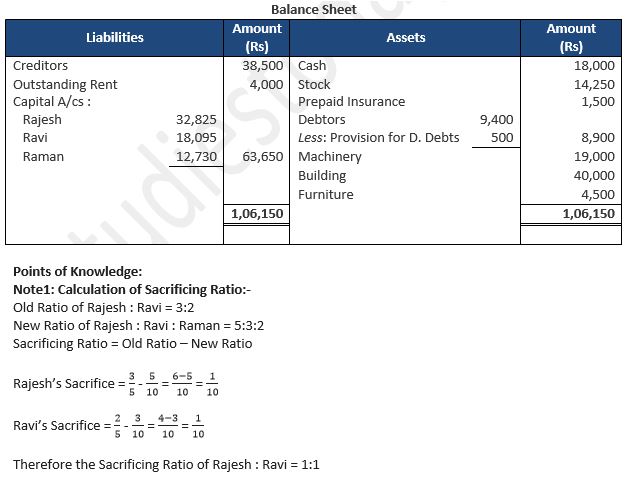

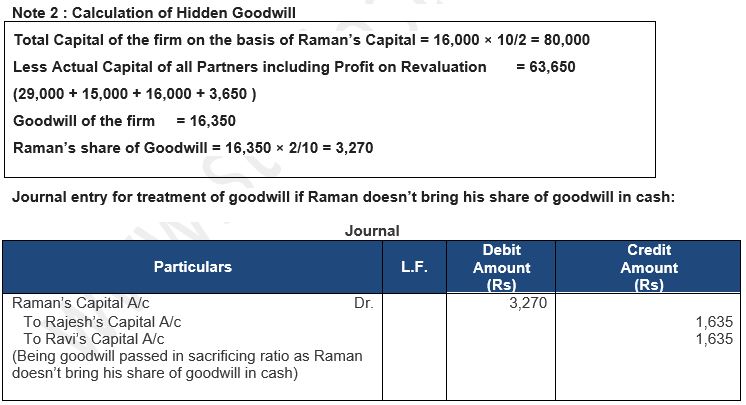

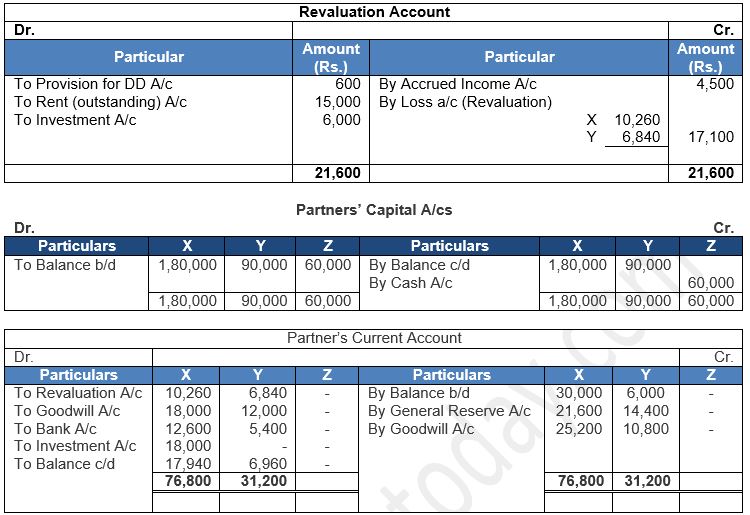

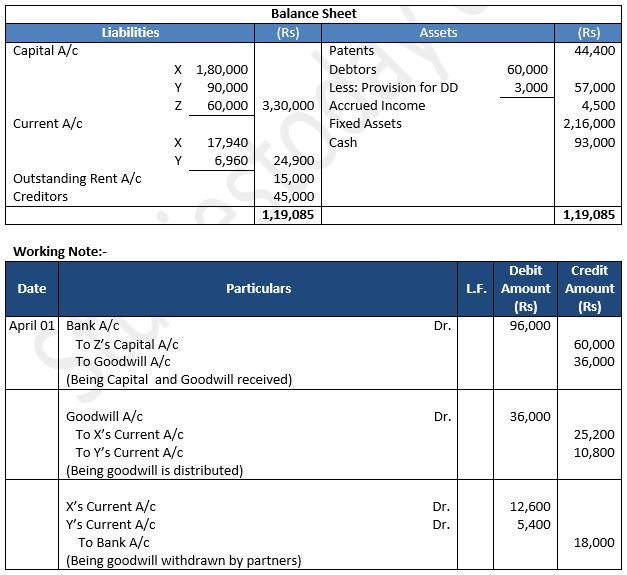

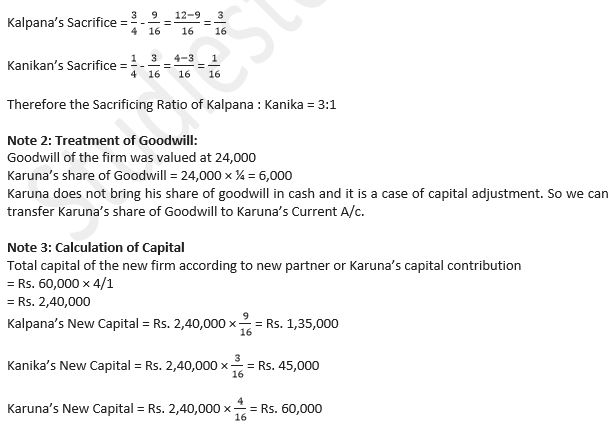

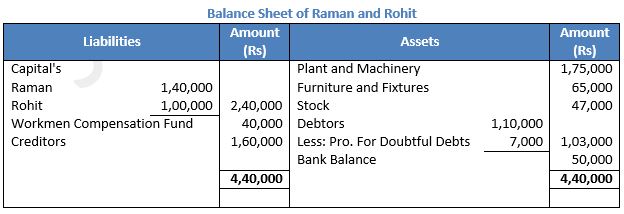

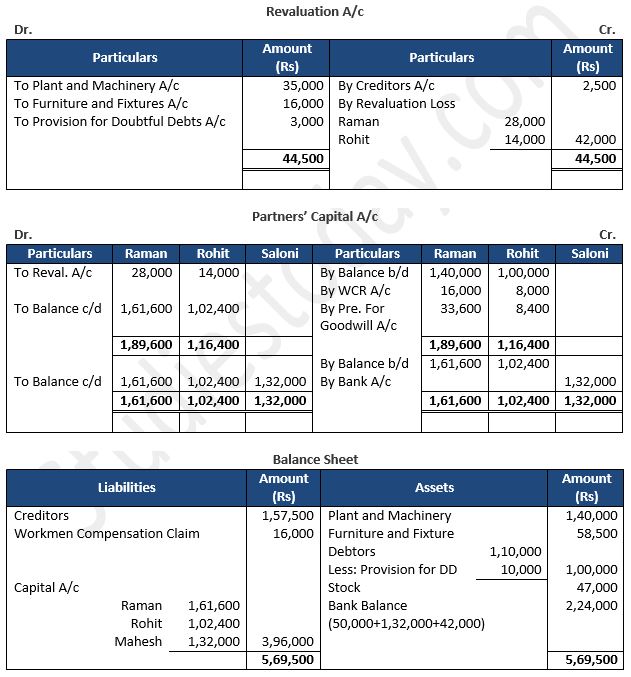

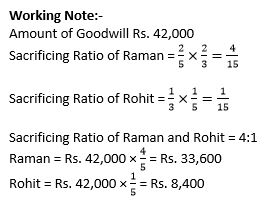

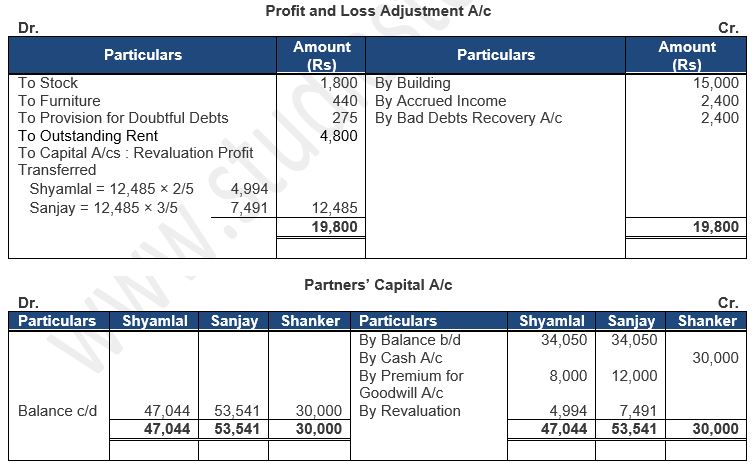

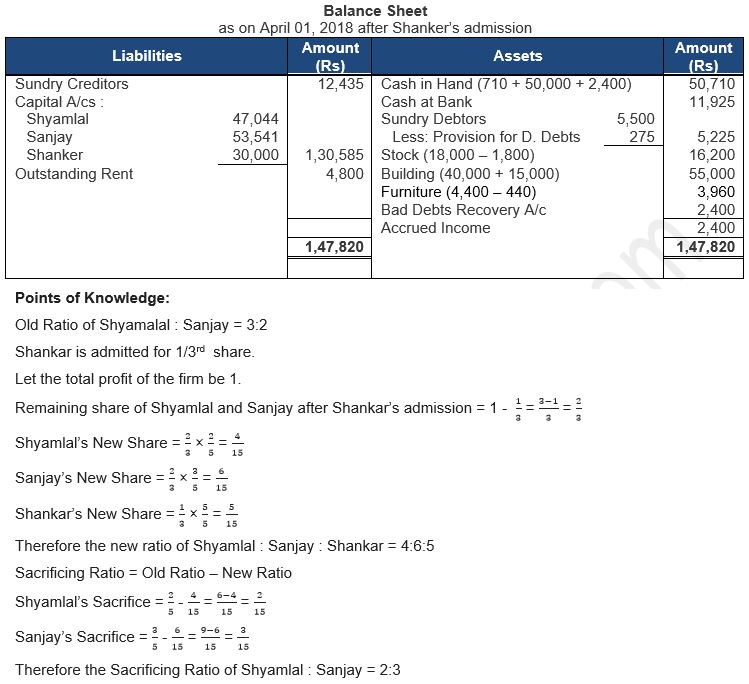

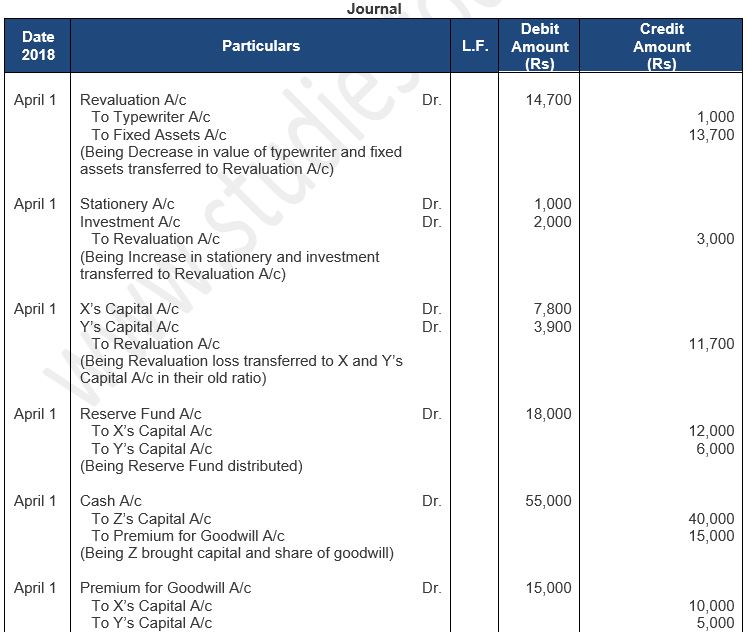

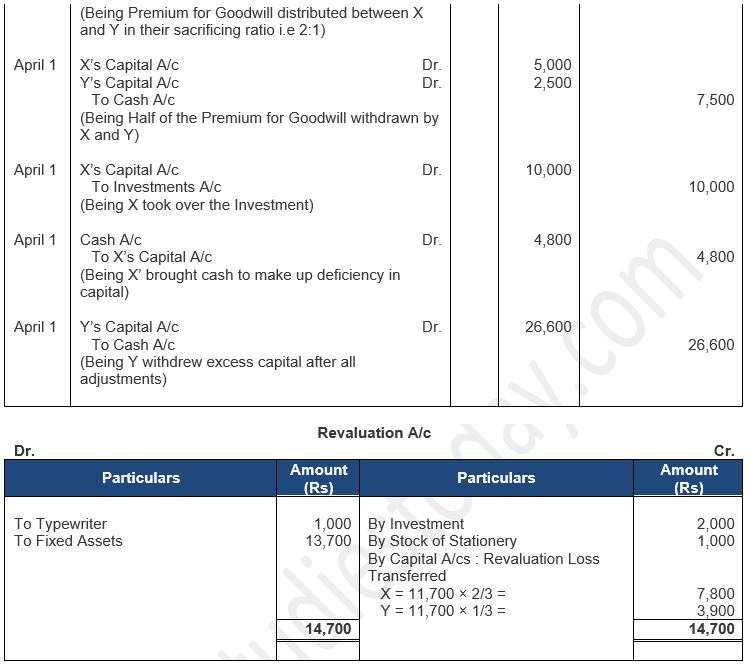

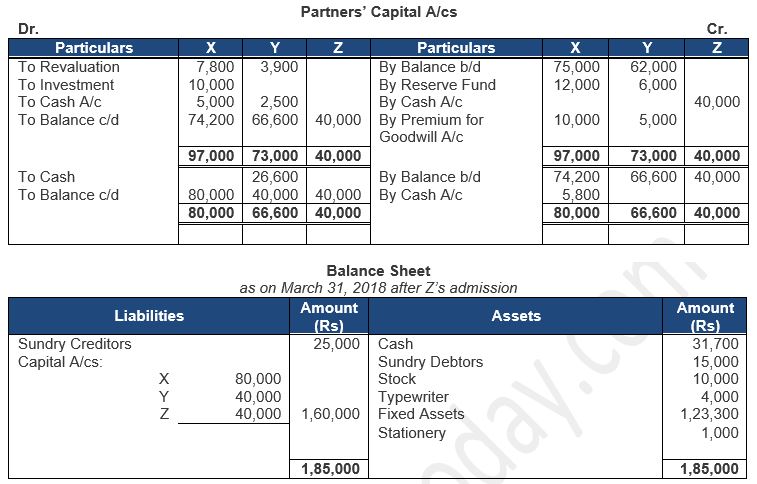

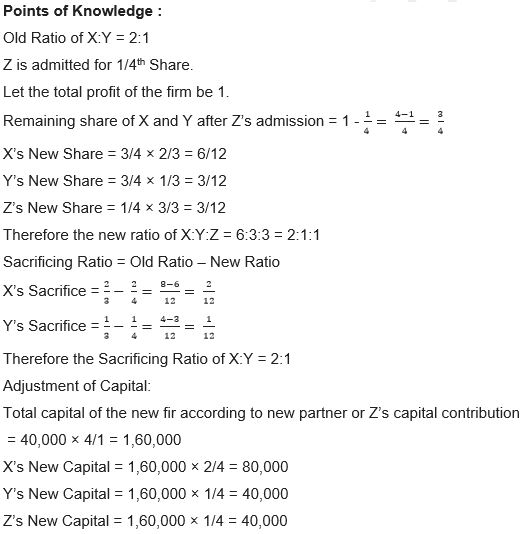

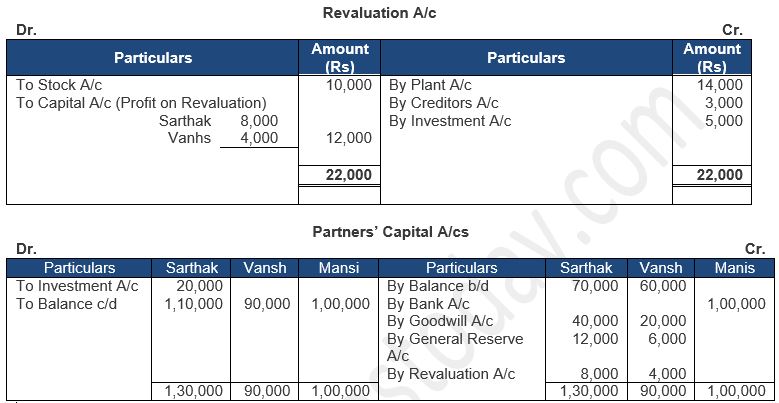

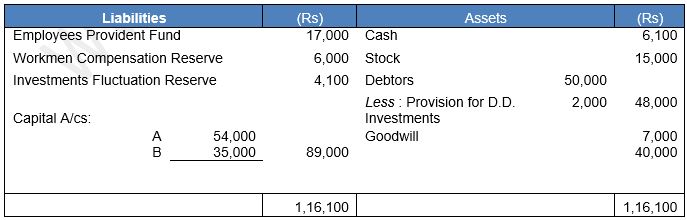

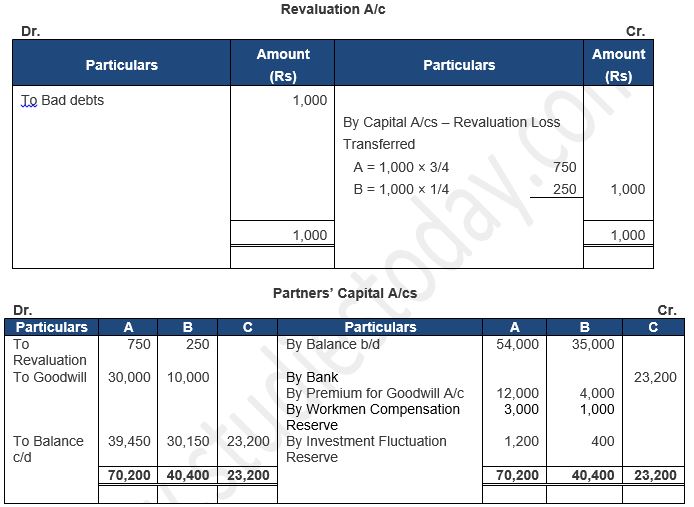

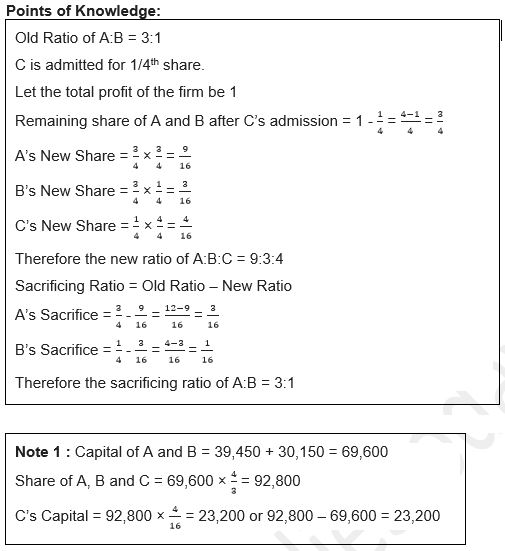

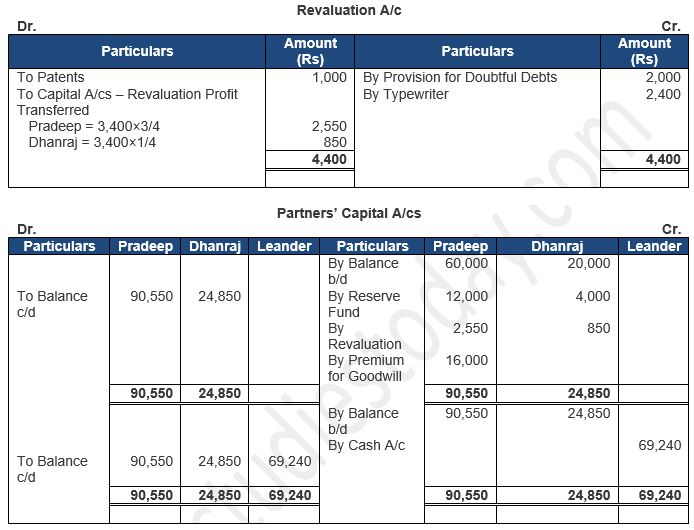

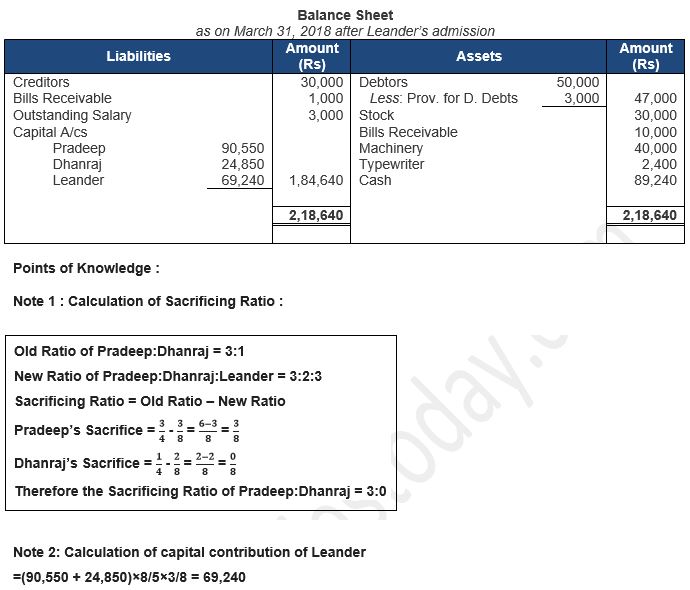

Question 53: Vimal and Nirmal are partners in a firm sharing profits and losses in the ratio of 5 : 3. They admit Kailash into the firm on 1st April 2023, when their Balance Sheet was as follows:

Term’s of Kailash’s admission were as follows:

(i) Kailash will bring ₹ 30,000 as his share of capital and will be entitled to 1/3rd share in the profits.

(ii) Kailash is not to bring goodwill in cash, Vimal and Nirmal raise the goodwill in the books.

(iii) Goodwill of the firm is valued on the basis of 2 year’s purchase of the average profit of the last three years. Average profit of the last three years is ₹ 6,000.

(iv) Machinery and stock are revalued at ₹ 45,000 and ₹ 8,000 respectively.

Prepare a Revaluation Account and Partner’s Capital Accounts incorporating the above adjustments.

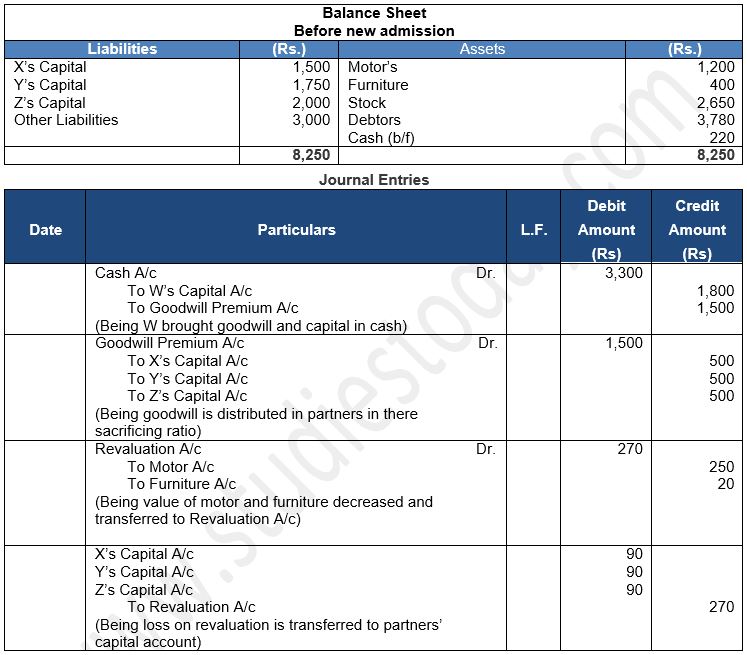

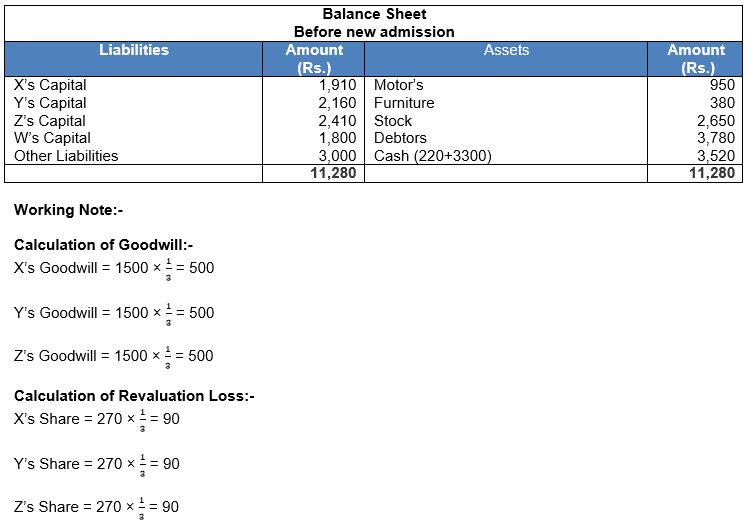

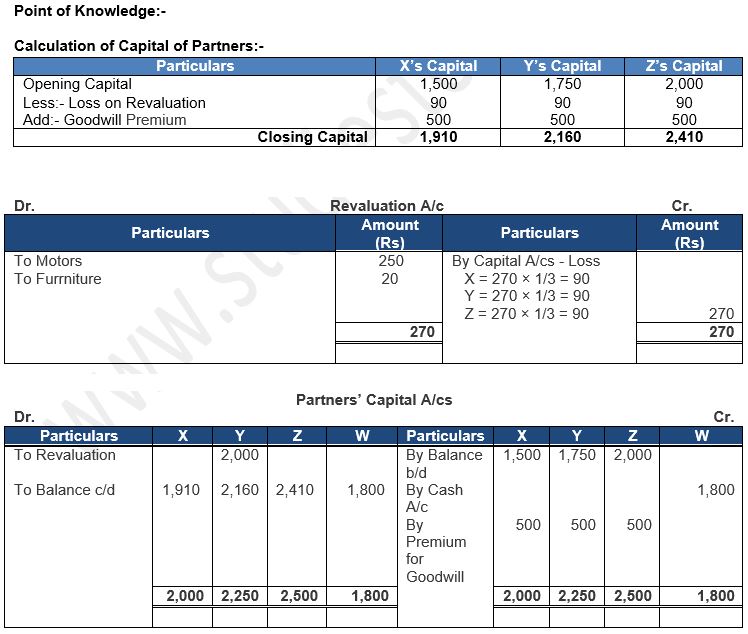

Answer:

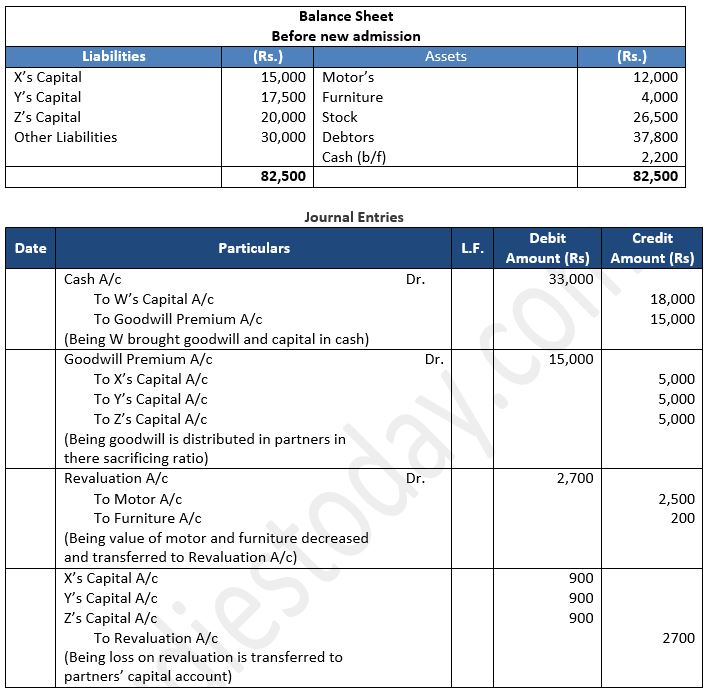

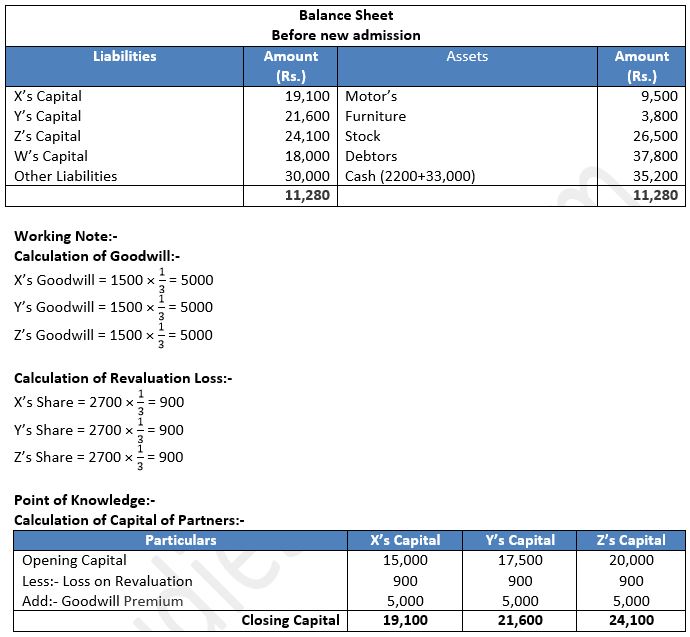

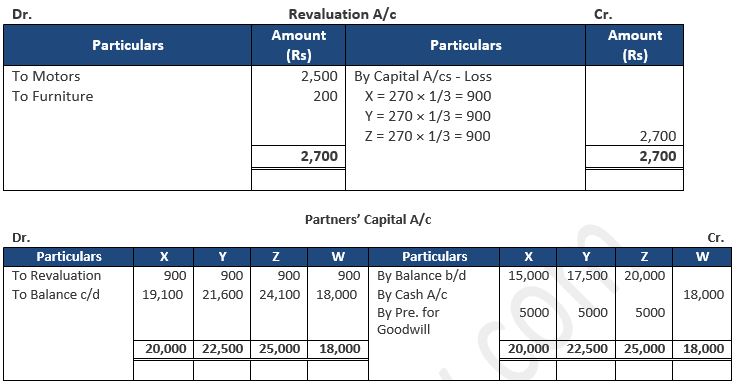

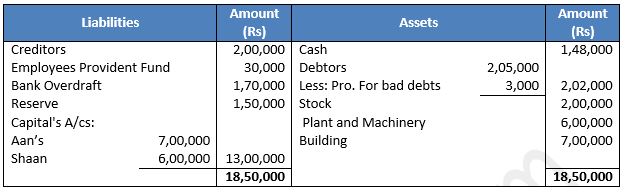

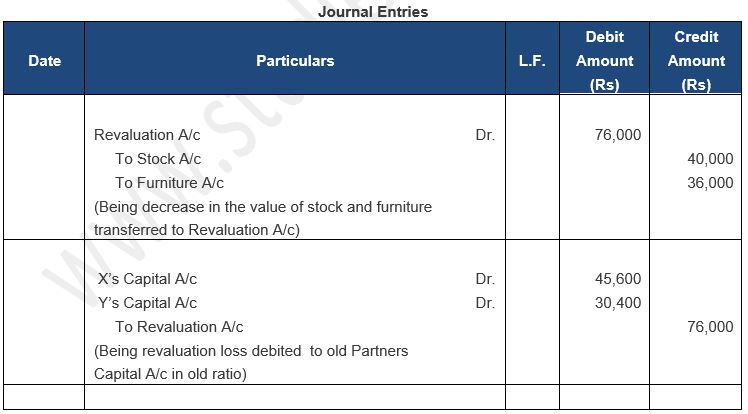

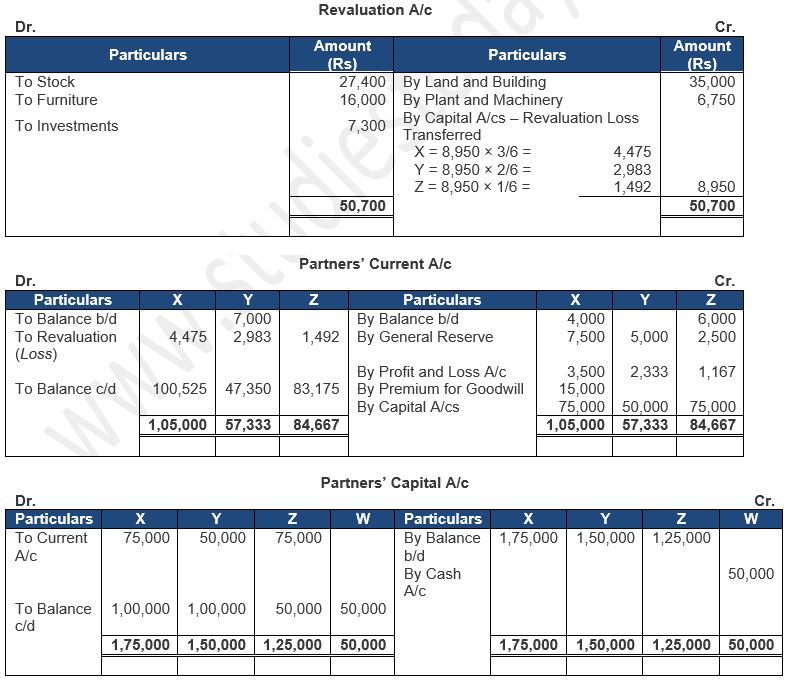

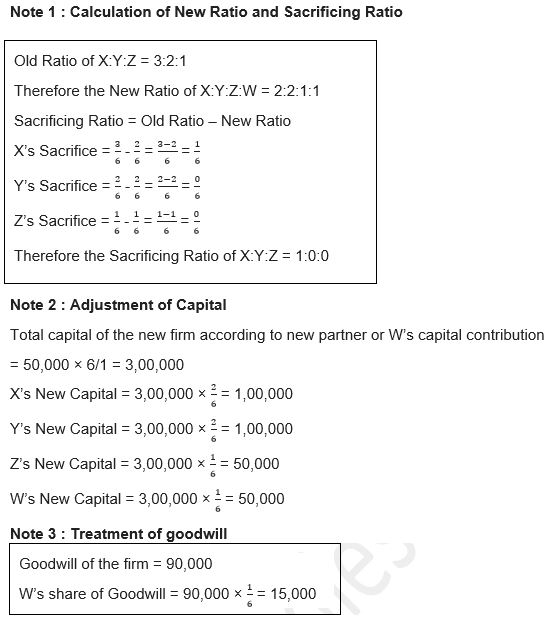

Question 54: X, Y and Z are equal partners with capital of Rs. 15,000; Rs. 17,500 and Rs. 20,000 respectively. They agree to admit W into equal partnership upon payment in cash Rs. 15,000 for 1/4th share of the goodwill and Rs. 18,000 as his capital, both sums to remain in the business. The liabilities of the old firm amounted to Rs. 30,000 and the assets, apart from cash, consist of Motors Rs. 12,000, Furniture Rs. 4,000, Stock Rs. 26,500 and Debtors Rs. 37,800. The Motors and Furniture were revalued at Rs. 9,500 and Rs. 3,800 respectively.

Answer:

About Solution:-

It is prepared to record the effect of revaluation of assets and liabilities when they are to appear at their revised new figures. If any reserves and accumulated profits or losses exist in the books of firm at the time of change in profit sharing ratio, they are to be transferred to the Partners' Capital Accounts or their Current Accounts in their old profit sharing ratio as such existing reserves and profits are earned before the reconstitution of the firm.

Things to Remember:

Adjustments required at the time of change in the profit sharing ratio: Various matters that need to be considered at the time of change in profit sharing ratio are:

(1) Determination of Sacrificing Ratio and Gaining Ratio

(2) Accounting for Goodwill

(3) Accounting Treatment of Reserves and Accumulated Profits

(4) Accounting for Revaluation of Assets and Liabilities

(5) Adjustment of Capitals

Important Notes:

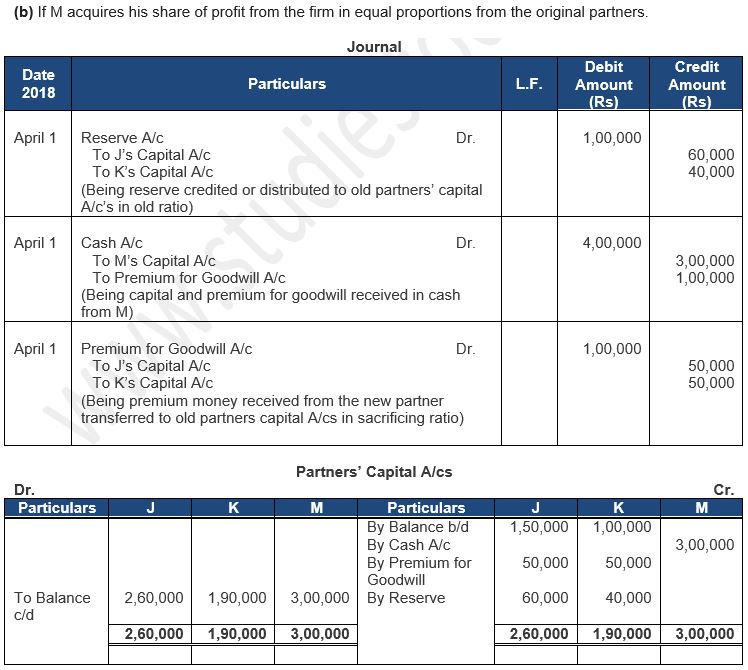

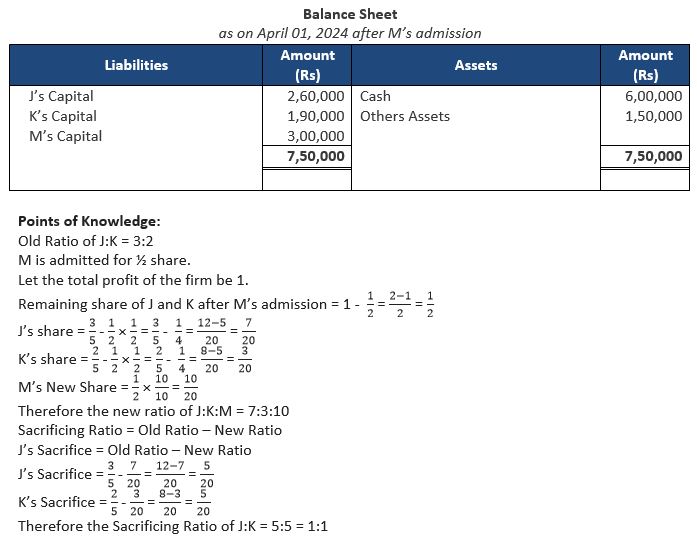

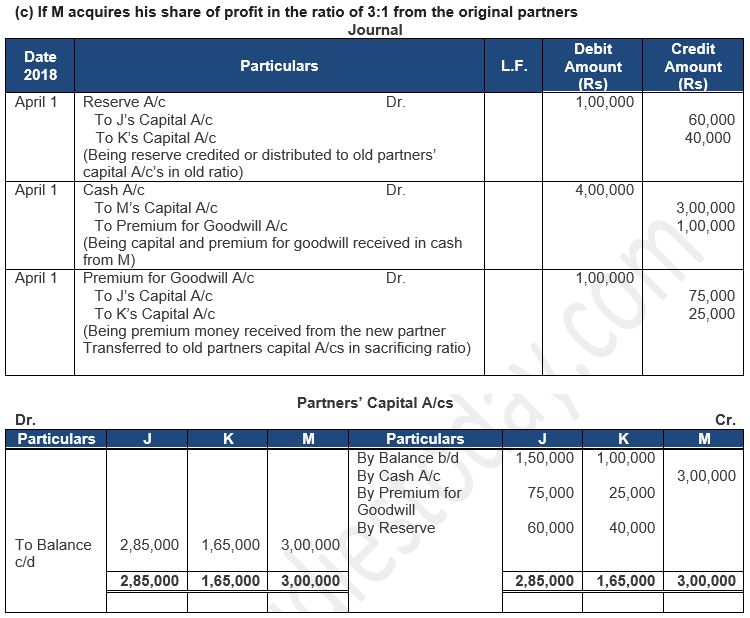

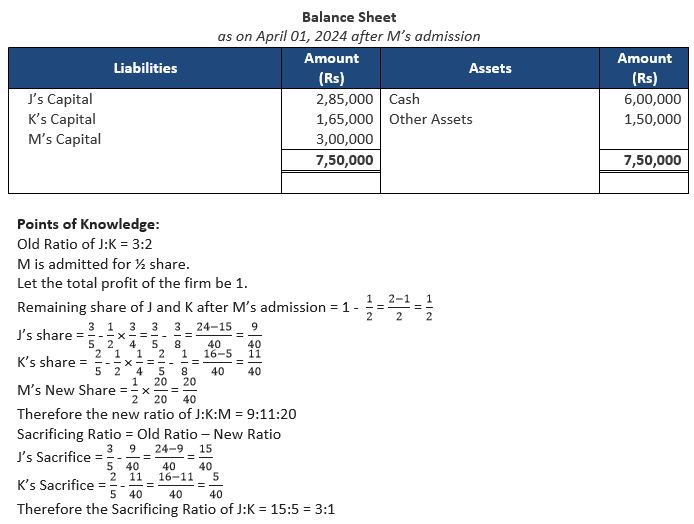

When claim against workmen compensation reserve does not exist: In this situation, amount of this reserve is transferred to Partners ' Capital Accounts in their old profit sharing ratio. Entry to be passed is:

Workmen Compensation Reserves A/c Dr.

To Partners' Capital (or Current) A/c

(Being workmen compensation reserves credited to partners' capital or current accounts in their old profit sharing ratio)

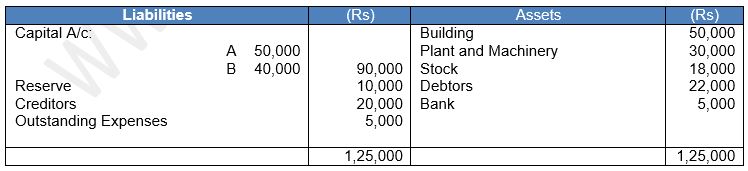

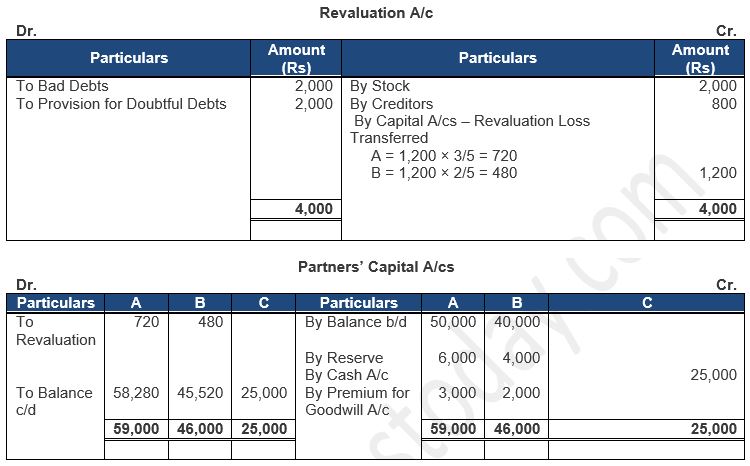

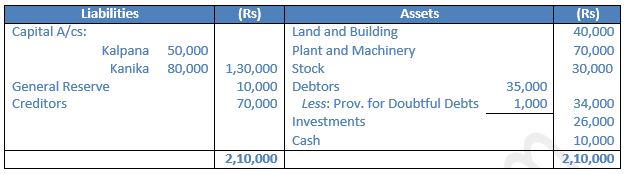

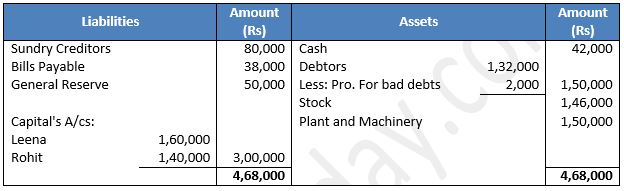

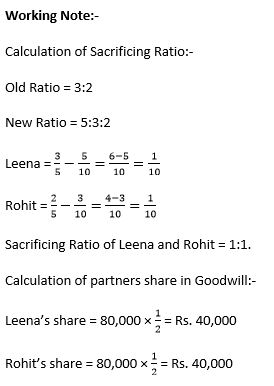

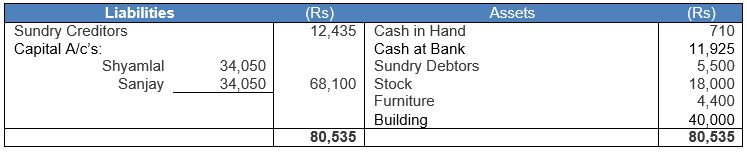

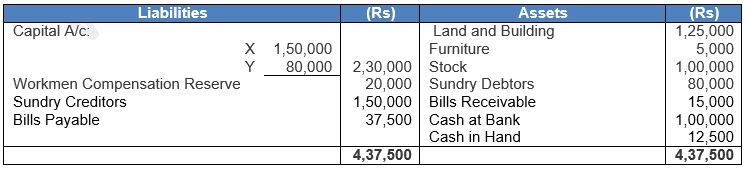

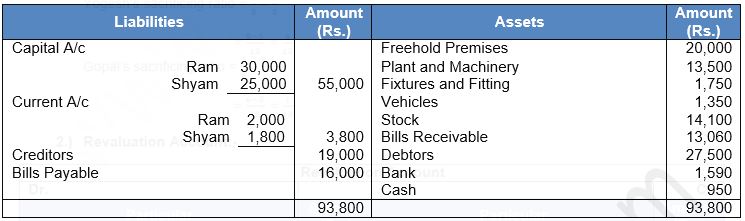

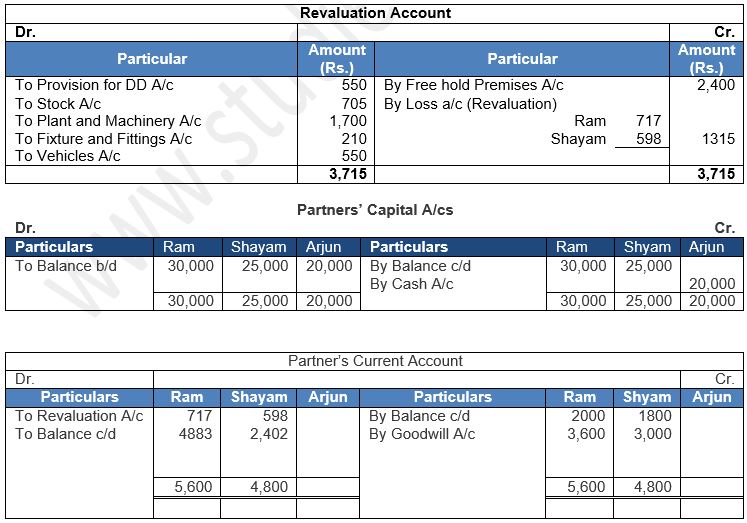

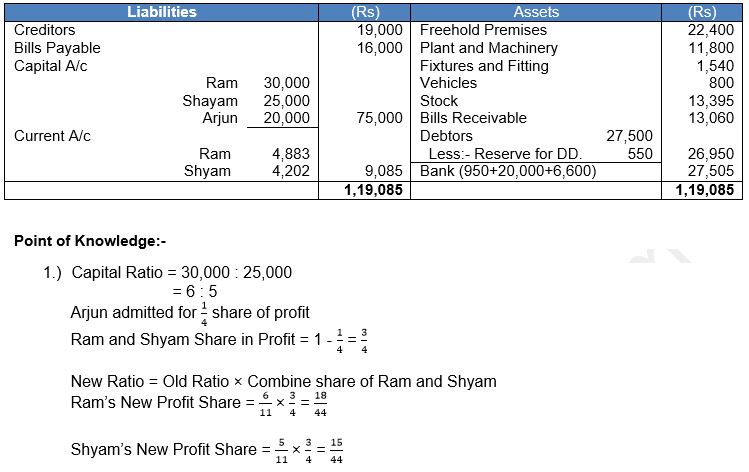

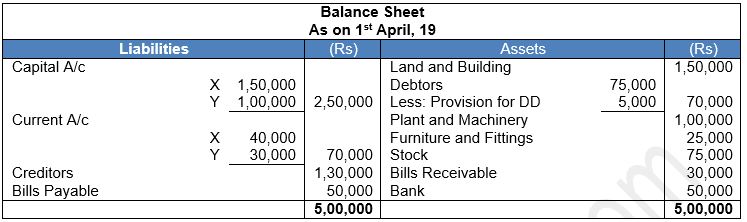

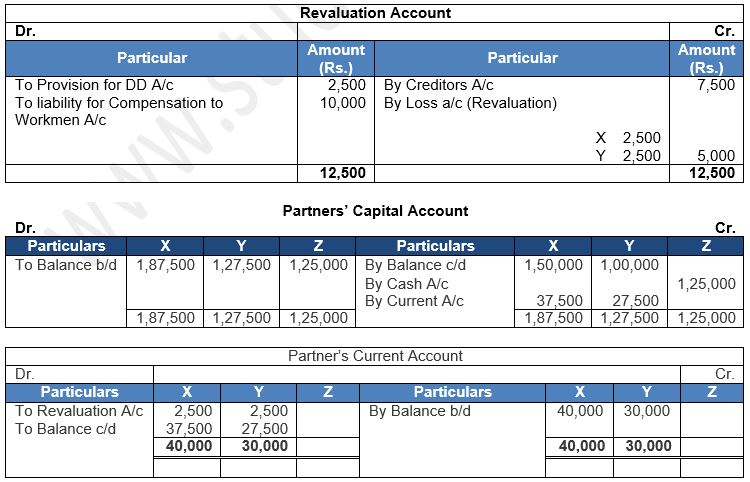

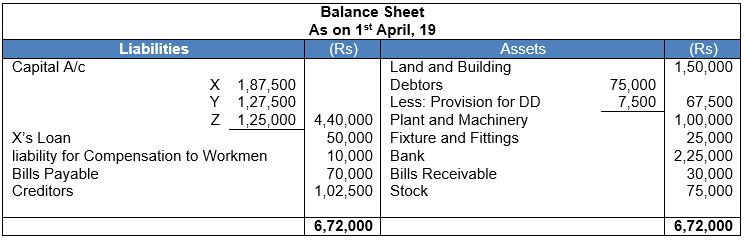

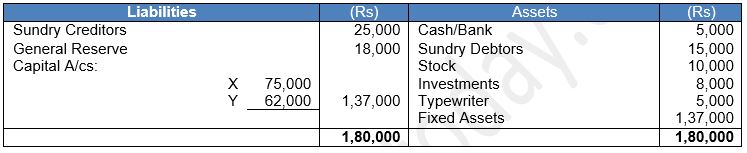

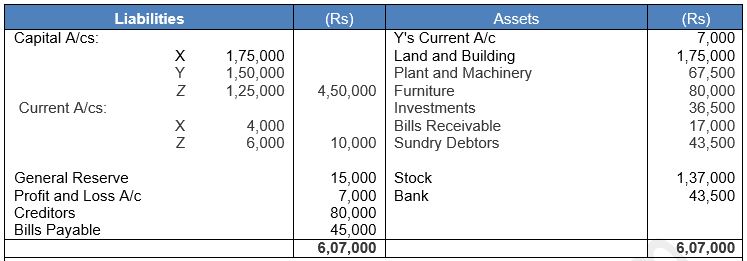

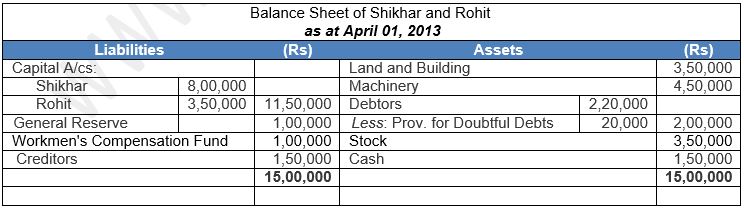

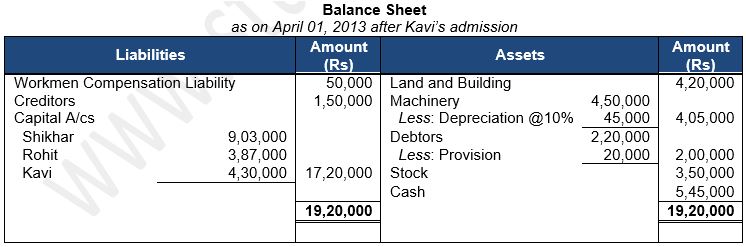

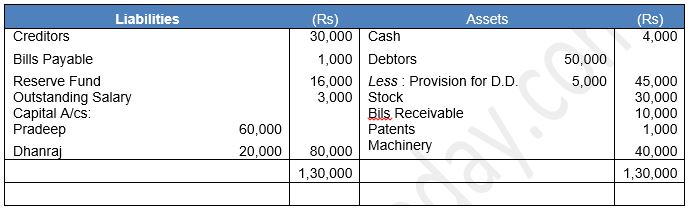

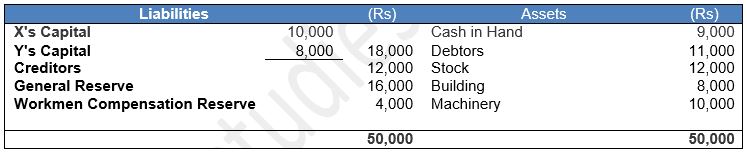

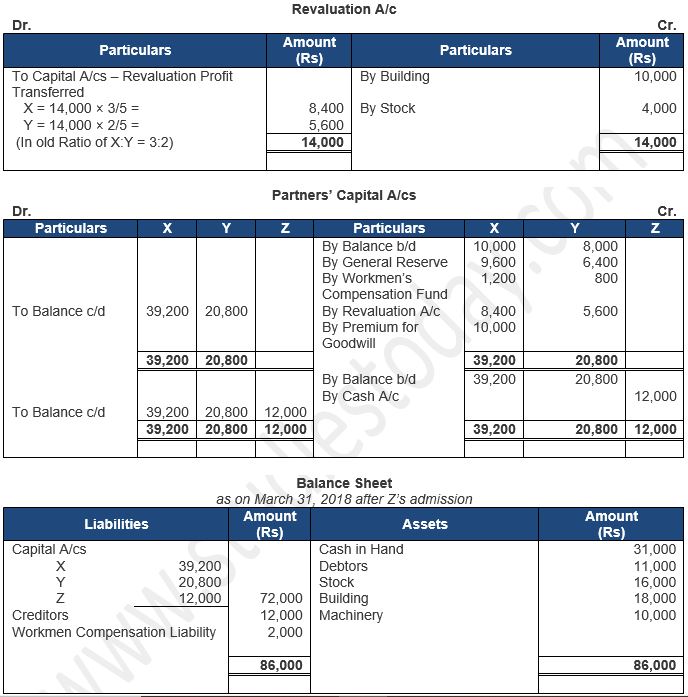

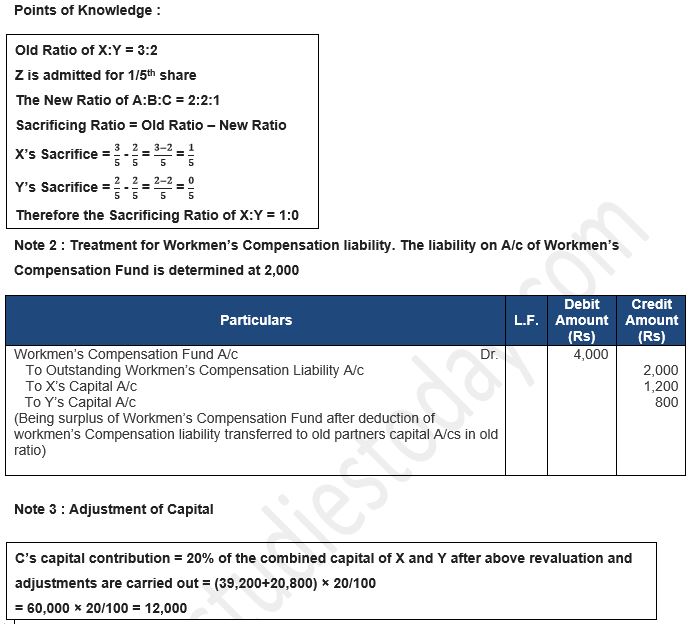

Question 55: Following was the Balance Sheet of A and B who were sharing profits in the ratio 2 : 1 as at 31st March, 2019:

They agree to admit C into the partnership on the following terms:

(a) C was to bring in Rs. 7,500 as his capital and Rs. 3,000 as goodwill for 1/4th share in the firm.

(b) Values of the Stock and Plant and Machinery were to be reduced by 5% .

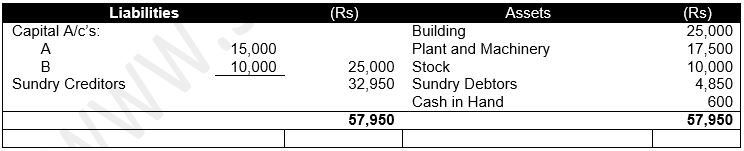

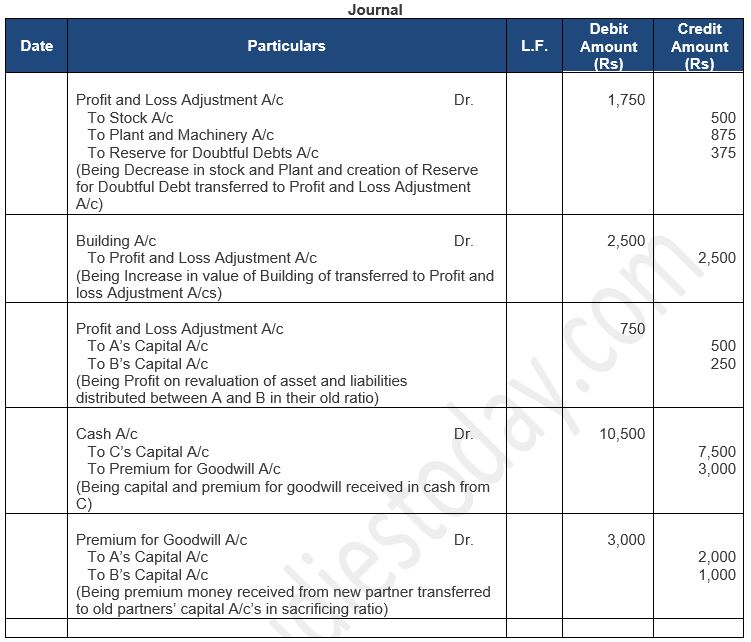

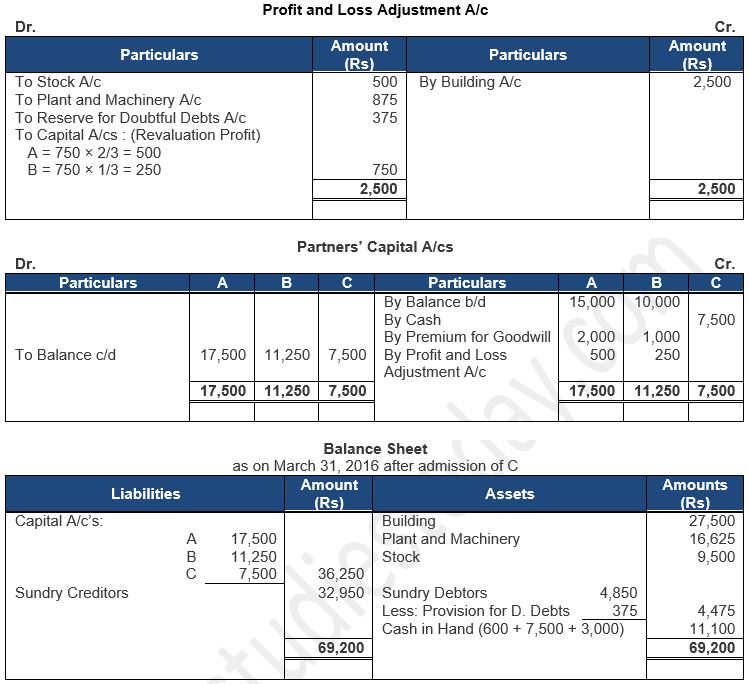

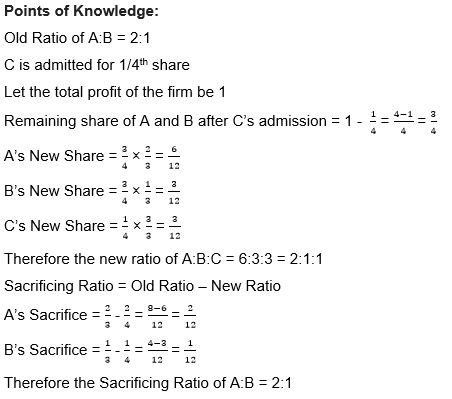

(c) A Provision for Doubtful Debts was to be created in respect of Sundry Debtor Rs 375.

(d) Building A/c was to be appreciated by 10%.

Pass necessary journal entries to give effect to the arrangements. Prepare Profit and Loss Adjustment A/c (or Revaluation A/c), Capital A/c’s and Balance Sheet of the new firm.

Answer:

About Solution:-

Determine surplus or deficit capital by comparing step

Present Capital > Proportionate Capital = Surplus and

If, Present Capital < Proportionate Capital = Deficit

Things to Remember:

In case a new or incoming partner is admitted in the firm during the year, profit for that year is to be divided between pre-admission and post-admission period on an agreed basis which can either be time basis or turnover basis.

Important Notes:

If no information is given, the profit of the firm should be divided on the basis of time assuming that the profit was earned evenly throughout the year.

Question 56: A and B, carrying on business in partnership and sharing profits and losses in the ratio of 3 : 2 , require a partner, when their Balance Sheet stood as:

They admit C into partnership and give him 1/8th share in the future profits on the following terms:

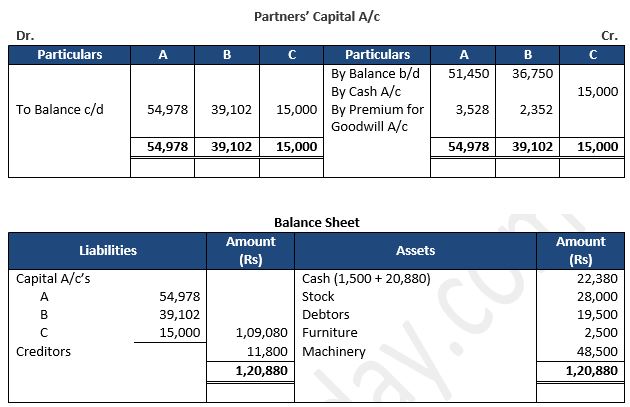

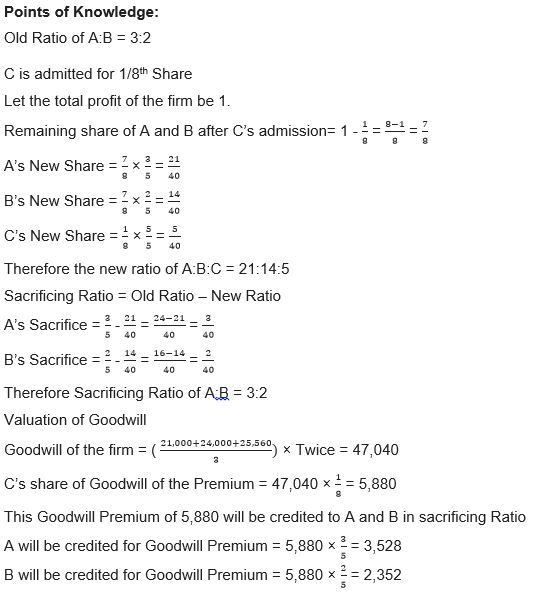

(a) Goodwill of the firm be valued at twice the average of the last three years' profits which amounted to Rs. 21,000; Rs. 24,000 and Rs. 25,560.

(b) C is to bring in cash for the amount of his share of goodwill.

(c) C is to bring in cash Rs 15,000 as his capital.

Pass journal entries recording these transactions, draw out the Balance Sheet of the new firm and state new profit-sharing ratio.

Answer:

About Solution:-

When there is an Increase in Market Value of Investment: In this case, total amount of Investment Fluctuation Reserve is distributed among partners and increase in value of investment is credited to Revaluation Account for which following entry is to be passed:

Investment Fluctuation Reserve A/c Dr.

To Partners' Capital (or Current) A/c [In Old Ratio]

Things to Remember:

If the partners of the firm decide that the existing balances of accumulated profits, losses and reserves should continue to appear at the same amount in the Balance Sheet of the reconstituted firm, then an adjustment entry for the net effect of accumulated profits, losses and reserves is passed since they were earned in past.

Important Notes:

Determine total capital of the firm on the basis of capital of new or incoming partner

Total capital of the firm = Capital of the or incoming partner / Share of profit of the new or incoming partner

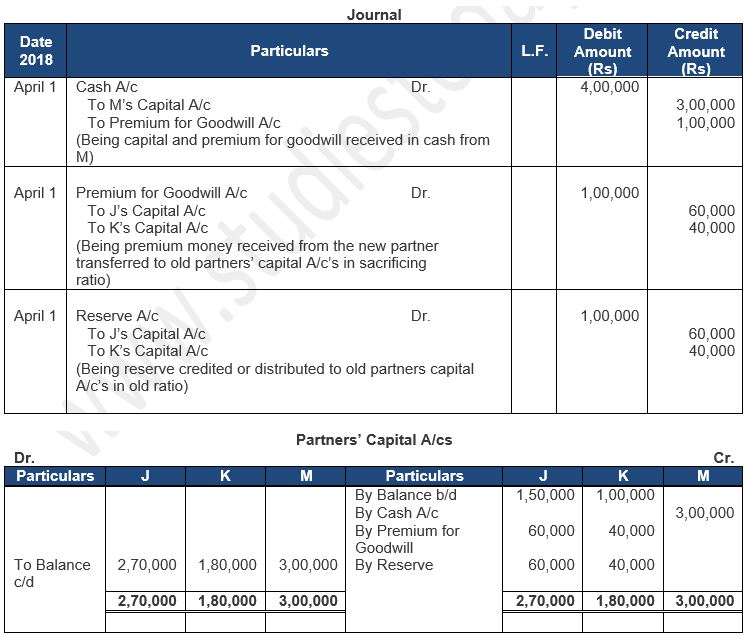

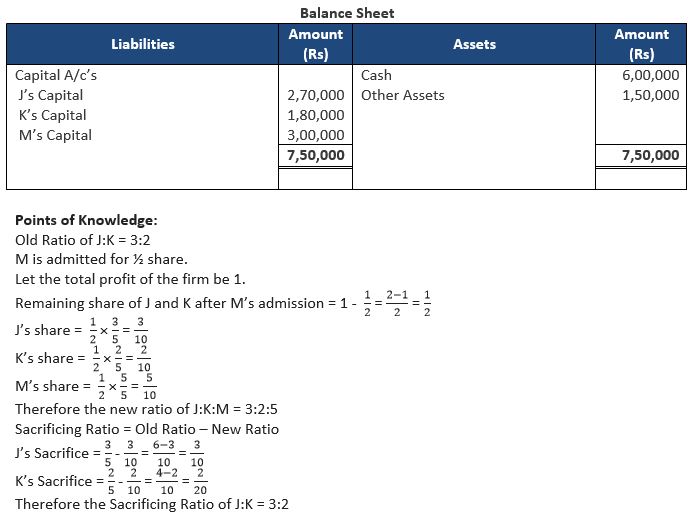

Question 57: Balance Sheet of J and K who share profits in the ratio of 3 : 2 is as follows: