Access free TS Grewal Solution Class 12 Chapter 1 Financial Statement of a Company 2026 below. Students can now access free TS Grewal Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 1 Financial Statement of a Company TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 1 Financial Statement of a Company Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 1 Financial Statement of a Company TS Grewal Class 12 Solved Exercises

About the chapter: TS Grewal Class 12 Chapter 1 Financial Statements of a Company is a very important chapter for class 12 students who are currently pursuing commerce and are studying accountancy. In this chapter, the students will be able to understand about various financial statements which are published by various organizations such as balance sheet profit and loss account, cash flow statements, trial balance and various other schedules which are prepared based on which the financial situation of a company and accuracy of accounting is understood. The financial statements are prepared as for the Companies Act 2013 which has also been explained in this chapter. it is very important for the students to understand this chapter as understanding of financial statements will be used throughout their life if they plan to pursue their career in accountancy. Lot of questions are asked in the Class 12 examinations relating to this chapter. Students are also required to solve lot of practical questions which have been given at the end of this chapter. Our expert accountancy teachers have solved all the questions and have given the answers below.

Solutions for T.S. Grewal's Analysis of Financial Statements

Textbook for CBSE Class 12 TS Grewal Solutions Class 12 Accountancy

Chapter 1 Financial Statement of Companies

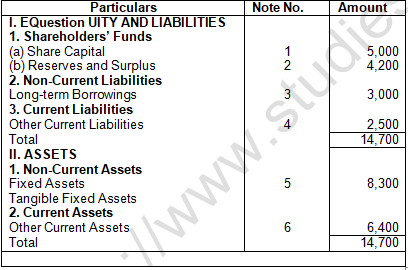

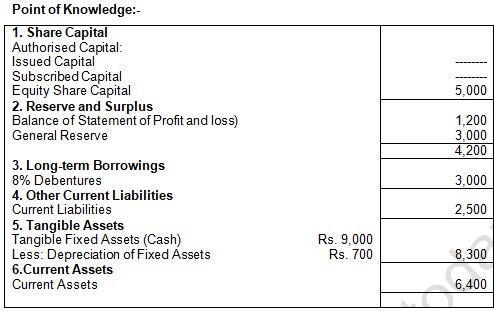

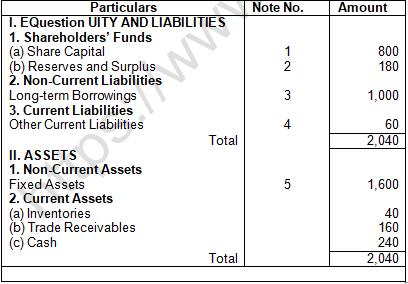

(a) Shareholder Fund

(b) Share Application Money Pending Allotment

(c) Non-current Liabilities

(d) Current Liabilities

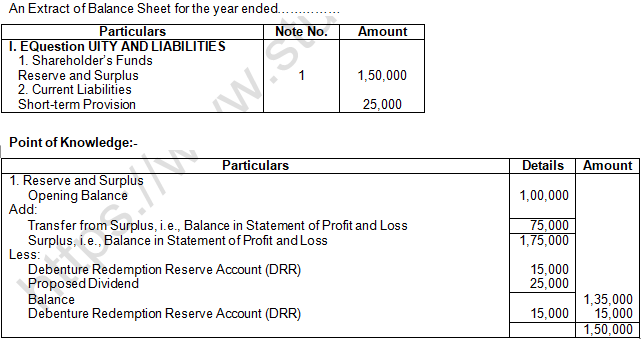

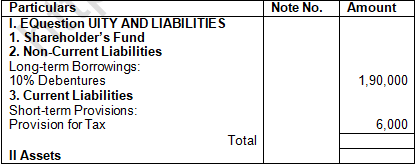

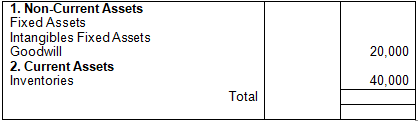

Question 6. A company has an opening credit balance in Surplus, i.e., Balance in Statement of Profit and Loss of Rs. 1,00,000. During the year, it earned a profit of Rs. 75,000. It decided to transfer Rs. 15,000 to Debentures Redemption Reserve (DRR) and also proposed to pay dividend of Rs. 25,000.

How will be the appropriations shown in the financial statements?

About solution:

Equity: It is the liability of the company towards its shareholders and is called as ‘Shareholders’ Funds’. It includes Share Capital, Reserves & Surplus and Money Received against Share warrants.

Things to remember:

Liabilities: It means external liabilities of the company or liabilities towards outsiders. In between Shareholders’ Fund and Liabilities, Application Money Pending Allotment is placed as per the prescribed form of the Balance Sheet. Liabilities have further been divided into (a) Non-current Liabilities and (b) Current Liabilities.

Important Note:

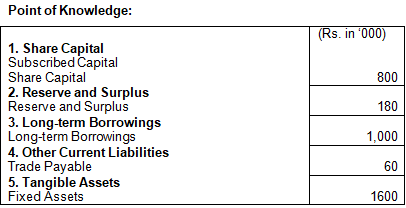

1. Shareholders’ Funds

(a) Share Capital

(b) Reserves and Surplus

(c) Money Received against Share Warrants

Question 7. State giving reason whether Trade Receivables are classified as Current Assets or Non-current Assets in the Balance Sheet of a Company as per Schedule III of the Companies Act, 2013 in the following cases.

The Trade Receivables are classified as Current Assets or Non-current Assets in the Balance Sheet of a Company as per Schedule III in the following cases are explained with reason:

Case1: Current Assets

Reason: They are realisable within the period of 12 months from the date of Balance Sheet.

Case 2: Current Assets

Reason: They are realisable within the period of 12 month from the date of Balance Sheet.

Case 3: Non-current Assets

Reason: They are realisable not within the period of 12 month from the date of Balance Sheet.

Case 4: Current Assets

Reason: They are realisable within the period of operating cycle of the business.

Case 5: Non-current Assets

Reason: They are realisable not within the period of 12 months from the date of Balance Sheet and also not within the operating cycle period.

Question 8. State giving reason whether Trade Payables are classified as Current Liabilities or Non-current Liabilities in the Balance Sheet of a Company as per Schedule III of the Companies Act, 2013 in the following cases:

The Trade Payable is classified as Current Liabilities or Non-current Liabilities in the Balance Sheet of a company as per Schedule III in the following cases are given with reasons.

Case-1: Current Liabilities

Reason: They are payable within the period of 12 months from the date of Balance Sheet.

Case-2: Current Liabilities

Reasons: They are payable within the period of 12 months from the date of Balance Sheet.

Case 3: Non – Current Liabilities

Reason: They are payable not within the period of 12 months from the date of Balance Sheet.

Case 4: Current Liabilities

Reason: They are payable within the period of operating cycle of the business.

Case 5: Non-current Liabilities

Reason: They are payable not within a period of 12 months from the date of Balance Sheet and also not within the period of operating cycle of the business.

Question 9. Under which head and how are the following items shown in the Balance Sheet of a company under Schedule III:

(i) Calls-in-Arrears; (ii) Share Application Money Pending Allotment; (iii) Unpaid Dividend; and (iv) Dividend not paid on Cumulative Preference Shares?

Below are the heads and adjustment:-

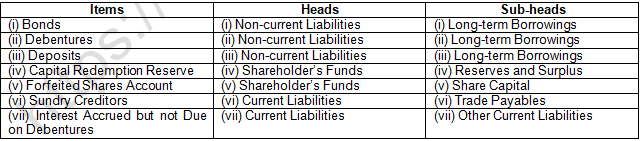

Question 10. Under which main head and sub-head of Equity and Liabilities part of the Balance Sheet are the following items classified or shown:

(i) Bonds; (ii) Debentures; (iii) Public Deposits; (iv) Capital Redemption Reserve; (v) Forfeited Shares Account; (vi) Sundry Creditors; and (vii) Interest Accrued but Not Due on Debentures?

Below are the head and sub-head:-

Question 11. State any two items that are included in the following major heads under which liabilities of a company are shown: (i) Reserves and Surplus; (ii) Long term Borrowings; (iii) Short-term Borrowings; (iv) Other Current Liabilities.

Below are the two items that are included in the following major heads under which liabilities of a company are shown:

(i) Reserve and Surplus:

(a) Capital Reserve

(b) Capital Redemption Reserve

(ii) Long-term Borrowings:

(a) Debentures

(b) Public Deposits

(iii) Short-term Borrowings

(a) Bank Overdraft

(b) Loan Repayable on Demand

(iv) Other Current Liabilities

(a) Interest accrued but not Due on Borrowings

(b) Unpaid Dividends

Question 12. Classify the following items under major head and sub-head (if any) in the Balance Sheet of a company as per Schedule III of the Companies Act, 2013:

(i) Capital Work-in-Progress; (ii) Provision for Warranties; (iii) Income received in Advance; and (iv) Capital Advances.

Below are the following main head and sub-head in the Balance Sheet:-

Question 13. Under which major head and sub-head of the Assets part of the Balance Sheet will the following be shown:

(i) Intangible Assets; (ii) Intangible Assets under Development; (iii) Investments (more than 12 months); (iv) Deferred Tax Assets (Net); (v) Stores and Spares; and (vi) Loose Tools?

Below are the following main head and sub-head in the Balance Sheet:-

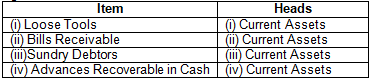

Question 14. Under which heads the following items are classified or shown on the Assets part of the Balance Sheet of a company: (i) Loose Tools; (ii) Bills Receivable; (iii) Sundry Debtors: and (iv) Advances Recoverable in Cash?

Below are the following main head in the Balance Sheet:-

Question 15. Under which heads the following items on the Assets part of the Balance Sheet of a company will be presented?

(i) Sundry Debtors; (ii) Patents and Trademarks; (iii) Shares in Question uoted Companies; (iv) Advances recoverable in cash; (v) Prepaid Insurance; and (vi) Work-in-Progress (Machinery)?

Below are the following main head and sub-head in the Balance Sheet:-

Question 16. Under which of the major heads will the following items be shown while preparing Balance Sheet of a company, as per Schedule III of the Companies Act, 2013:

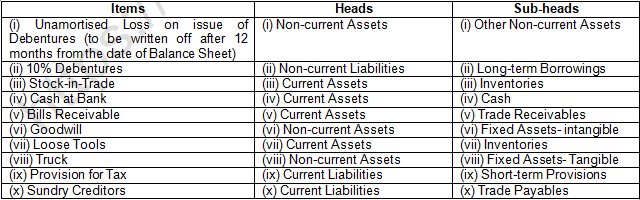

(i) Unamortised Loss on Issue of Debentures (To be written off after 12 months from the date of Balance Sheet); (ii) 10% Debentures; (iii) Stock-in-Trade; (iv) Cash at Bank; (v) Bills Receivable; (vi) Goodwill; (vii) Loose Tools; (viii) Truck; (ix) Provision for Tax; and (x) Sundry Creditors?

Below are the following main head and sub-head in the Balance Sheet:-

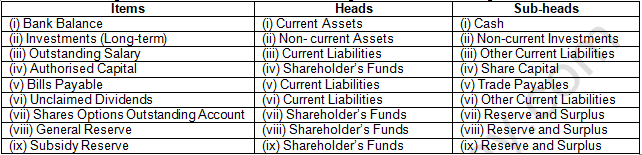

Question 17. Under which heads will the following items be shown in the Balance Sheet of a Company

(i) Bank Balance; (ii) Investments (Long-term); (iii) Outstanding Salary; (iv) Authorised Capital; (v) Bills Payable; (vi) Unclaimed Dividends; (vii) Shares Option Outstanding Account; (viii) General Reserve; and (ix) Subsidy Reserve?

Below are the following main head and sub-head in the Balance Sheet:-

Question 18. Under which heads the following items are shown in the Balance Sheet of a company:

(i) Calls-in-Arrears; (ii) Commission Received in Advance; (iii) Debentures; (iv) Stores and Spare Parts; (v) Land and Building; (vi) Forfeited Shares Account; (vii) Government Securities; and (viii) Uncalled Liability on parity paid Shares?

Under the following heads of the Balance Sheet the following items will be shown as given below:

Question 19. Under which heads the following are shown in a company's Balance Sheet:

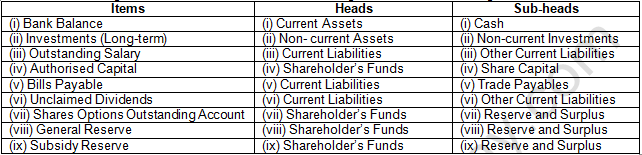

(i) Public Deposits; (ii) Office Furniture; (iii) Prepaid Rent; (iv) Outstanding Salaries; (v) Computer Software; (vi) Interest Accrued on Investment; (vii) Bills discounted but not matured; and (viii) Livestock?

Below are the following heads or Sub-head of the Balance Sheet:-

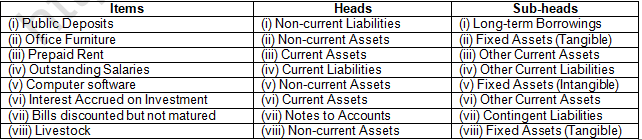

Question 20. Name the major heads under which the following items will be presented in the Balance Sheet of a company as per Schedule III of the Companies Act, 2013:

(i) Loose Tool.

(ii) Unpaid Dividend.

(iii) Copyrights and Patents.

(iv) Land and Building.

Below are the following main head in the Balance Sheet:-

Question 21. Identify the major heads under which the following items will be shown in the Balance Sheet of a company as per Schedule III of Companies Act, 2013:

(i) Provision for Tax

(ii) Loan payable on demand

(iii) Computer and related equipment

(iv) Goods acquired for trading

Below are the following main head in the Balance Sheet:-

Question 22. Under which heads and Sub-heads the following are shown in a company's Balance Sheet:

(i) Provision for Employee Benefits; (ii) Calls-in-Advance.

Below are the following main head and sub-head in the Balance Sheet:-

Question 23. How are the following items shown while preparing Balance Sheet of a company?

(i) Surplus, i.e., Balance in Statement of Profit and Loss (Dr.);

(ii) Interest accrued and due on Debentures;

(iii) Computer Software under development;

(iv) Interest accrued on Investment?

Under the following heads of the Balance Sheet the following items will be shown as given below:

About solution:

Balance Sheet as prescribed in schedule VI part I of the Companies Act 1956 is broadly divided into two parts:

(i) Equity and Liabilities and

(ii) Assets

Things to remember:

Non-current Liabilities have been defined as liabilities which are not current liabilities. Current liability is that liability which is:

i) Expected to be settled in the company’s normal operating cycle; or

ii) Due to be settled within 12 months after the reporting date i.e., Balance Sheet date; or

iii) Held primarily for the purpose of being traded; or

iv) There is no unconditional right to defer settlement for at least 12 months after the reporting date.

Important Note:

(a) Long-term Borrowings:

(i) Debentures;

(ii) Bonds;

(iii) Term Loans;

(iv) Public Deposits and

(v) Other loans and advances

About solution:

Like liabilities, assets are also divided into ‘non-current assets’ and ‘current assets’. Non-current assets have been defined as assets that are not current. Current assets have been defined in Schedule VI of the Companies Act, 1956 as follows:

Current Assets are those assets which are:

i) Expected to be realized in or intend for sale or consumption in the company’s normal operating cycle;

ii) Held primarily for the purpose of trading; or

iii) Expected to be realized within 12 months from reporting date i.e., Balance Sheet date;

iv) Cash and Cash equivalents unless they are restricted from being exchanged or used to settle a liability for at least 12 months after reporting date i.e., Balance Sheet date.

Things to remember:

Non-Current Assets are classified into the following five major heading as given below:

(a) Fixed Assets

(b) Non-Current Investments

(c) Deferred Tax Assets

(d) Long-term Loans and Advances

(e) Other non-current assets.

Important Note:

Current Liabilities:

(i) Short-term borrowings;

(ii) Trade Payables;

(iii) Other Current Liabilities and

(iv) Short-term Provision.

About solution:

Fixed Assets:

(i) Tangible Assets

(ii) Intangible Assets

(iii) Capital Work-in-Progress

(iv) Intangible Assets under Development

Things to remember:

Non-Current Investments:

(i) Investment in Property

(ii) Investment in Equity Investments

(iii) Investments in preference shares

(iv) Investment in Govt. or Trust Securities

(v) Investments in Debentures or Bonds

(vi) Investments in Mutual Funds

(vii) Investments in Partnership Firms

(viii) Other Non-Current Investments.

Important Note:

Long-Term Loans and Advances:

(i) Capital Advances;

(ii) Security Deposits;

(iii) Other Loans and Advances

Question 29. Under which head following revenue items of a non-financial company will be classified or shown:

(i) Sales; (ii) Revenue from Services Rendered; (iii) Sale of Scrap; (iv) Interest Earned on Loans; and (v) Gain (profit) on Sale of Investments?

Under the following head the following revenue items of a non-financial company will be classified or shown:

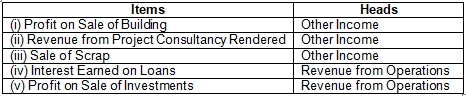

Question 30. Under which head following revenue items of a financial company will be classified or shown:

(i) Gain (Profit) on Sale of Building; (ii) Revenue from Project Consultancy Rendered; (iii) Sale of Scrap; (iv) Interest earned on Loans; and (v) Gain (Profit) on sale of Investments?

Under the following head the following revenue items of a financial company will be classified or shown:

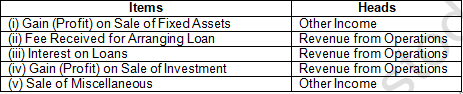

Question 31. Under which head following revenue items of non-financial company will be classified or shown: (i) Gain (Profit) on Sale of Fixed Asset; (ii) Fee Received for Arranging Loans; (iii) Interest on Loans Given; (iv) Gain (Profit) on Sale of Investments and (v) Sale of Miscellaneous Items?

Under the following head the following revenue items of a financial company will be classified or shown:

Question 32. Calculate Cost of Materials Consumed from the following:

Opening Inventory of Materials ₹5,00,000; Purchase of Materials ₹25,00,000; and Closing Inventory of Materials ₹4,00,000.

Cost of Materials Consumed = Opening Inventory of Materials + Purchase of Materials – Closing Inventory of Materials

= Rs. 5,00,000 + Rs. 25,00,000 – Rs. 4,00,000

= Rs. 26,00,000

About solution:

Formula for Cost of Material Consumed:-

Cost of Materials Consumed = Opening Inventory of Materials + Purchase of Materials – Closing Inventory of Materials

Things to remember:

Current Assets:

(i) Current Investments

(ii) Inventories

(iii) Trade Receivables

(iv) Cash and Cash Equivalents

(v) Short term loans and advances

(vi) Other Current Assets.

Important Note:

The main objective of a business is to earn a satisfactory return on the funds invested in it. Financial analysis helps in ascertaining whether adequate profits are being earned on the capital invested in the business or not. It also helps in knowing the capacity to pay the interest and dividend.

Question 33. Calculate Cost of Materials Consumed from the following:

Opening Inventory of Materials ₹2,50,000; Finished Goods ₹1,00,000; Closing Inventory of Materials ₹2,25,000; Finished Goods ₹75,000; Raw Material purchased during the year ₹15,00,000.

Cost of Materials Consumed = Opening Inventory of Materials + Purchases of Materials – Closing Inventory of Materials

= Rs. 2,50,000 + Rs. 15,00,000 – Rs. 2,25,000

= Rs. 15,25,000

About solution:

We know business is mainly concerned with the financial activities. In order to ascertain the financial status of the business every enterprise prepares certain statements, known as financial statements. Financial statements are mainly prepared for decision making purposes. But the information as provided in the financial statements is not adequately helpful in drawing a meaningful conclusion. Thus, an effective analysis and interpretation of financial statements is required.

Things to remember:

Analysis means establishing a meaningful relationship between various items of the two financial statements with each other in such a way that a conclusion is drawn.

Important Note:

The term financial analysis is also known as analysis and interpretation of financial statements. It refers to the establishing meaningful relationship between various items of the two financial statements i.e., Statement of Profit & Loss and Balance Sheet. It determines financial strength and weaknesses of the firm.

Question 34. Calculate Cost of Materials Consumed from the following:

Opening Inventory of Materials ₹3,50,000; Finished Goods ₹75,000; Stock-in-Trade ₹2,00,000; Closing Inventory of: Materials ₹3,25,000; Finished Goods ₹85,000; Stock-in-Trade ₹1,50,000; Purchases during the year: Raw Material ₹17,50,000; Stock-in-Trade ₹9,00,000.

Cost of Materials Consumed = Opening Inventory of Materials + Purchases of Materials – Closing Inventory of Materials

= Rs. 3,50,000 + Rs. 17,50,000 – Rs. 3,25,000

= Rs. 17,75,000

About solution:

Analysis of financial statements is an attempt to assess the efficiency and performance of an enterprise. Thus, the analysis and interpretation of financial statements is very essential to measure the efficiency, profitability, financial soundness and future prospects of the business units.

Things to remember:

Financial statements of the previous years can be compared and the trend regarding various expenses, purchases, sales, gross profits and net profit etc. can be ascertained. Value of assets and liabilities can be compared and the future prospects of the business can be envisaged.

Important Note:

Assessing the Growth Potential of the Business: The trend and other analysis of the business provide sufficient information indicating the growth potential of the business.

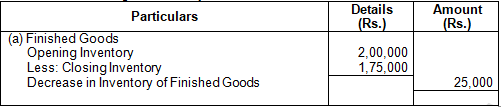

Question 35. From the following information, calculate Change in Inventory of Finished Goods: Opening Inventory and Closing Inventory of Finished Goods ₹2,00,000 and ₹1,75,000 respectively.

Calculation of Change in Inventory:

About solution:

The purpose of financial statements analysis is to help the management to make a comparative study of the profitability of various firms engaged in similar businesses. Such comparison also helps the management to study the position of their firm in respect of sales, expenses, profitability and utilizing capital, etc.

Things to remember:

Assess overall financial strength: The purpose of financial analysis is to assess the financial strength of the business. Analysis also helps in taking decisions, whether funds required for the purchase of new machines and equipment’s are provided from internal sources of the business or not if yes, how much? And also to assess how much funds have been received from external sources.

Important Note:

Assess solvency of the firm: The different tools of an analysis tell us whether the firm has sufficient funds to meet its short term and long term liabilities or not.

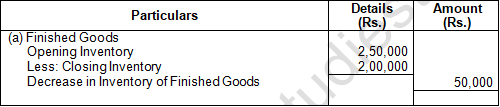

Question 36. From the following information, calculate Change in Inventory of Finished Goods: Opening Inventory and Closing Inventory of Finished Goods ₹2,50,000 and ₹2,00,000 respectively.

Calculation of Change in Inventory:

About solution:

Analysis of financial statements has become very significant due to widespread interest of various parties in the financial results of a business unit.

Things to remember:

Investors: Shareholders or proprietors of the business are interested in the well-being of the business. They like to know the earning capacity of the business and its prospects of future growth.

Important Note:

Management: The management is interested in the financial position and performance of the enterprise as a whole and of its various divisions. It helps them in preparing budgets and assessing the performance of various departmental heads.

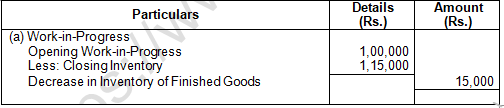

Question 37. From the following information, calculate Change in Inventory of Work-in-Progress: Opening and Closing Work-in-Progress ₹1,00,000 and ₹1,15,000 respectively.

Calculation of Change in Inventory of Work-in-Progress:

About solution:

Analysis of financial statements has become very significant due to widespread interest of various parties in the financial results of a business unit.

Things to remember:

Investors: Shareholders or proprietors of the business are interested in the well-being of the business. They like to know the earning capacity of the business and its prospects of future growth.

Important Note:

Management: The management is interested in the financial position and performance of the enterprise as a whole and of its various divisions. It helps them in preparing budgets and assessing the performance of various departmental heads.

Question 38. From the following information, calculate Change in Inventory of Work-in-Progress: Opening and Closing Work-in-Progress ₹1,50,000 and ₹1,45,000 respectively.

Calculation of Change in Inventory of Work-in-Progress:

About solution:

Work-in-Progress = Opening Work-in-progress – Closing Work-in-progress

Things to remember:

Limitations of Financial Statements: Financial analysis is based on financial statements. But financial statements themselves suffer from certain limitations; hence the limitations of financial statements are also the limitations of their analysis. For example, (a) sometimes the information given in financial statements are incomplete and not authentic, (b) financial Statements are based on accounting concepts and conventions. As such, the utility of financial analysis is decreased due to the shortcomings of financial statements.

Important Note:

Affected by Window-dressing: Some firms resort to window-dressing their financial statements to cover up bad financial position on the eve of accounting date. For example, they may not record the purchases made at the end of the year or they may overvalue their closing stock. In such cases, the results obtained by analysis of financial statements will be misleading.

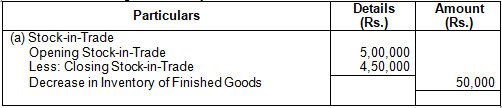

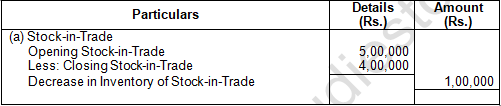

Question 39. From the following information, calculate Change in Inventory of Stock-in-Trade: Opening and Closing Stock-in-Trade ₹5,00,000 and ₹4,50,000 respectively.

Calculation of Change in Inventory of Stock-in-Trade:

About solution:

Calculation of Change in Inventory of Stock-in-trade:-

Change in Stock in Trade = Opening Stock in trade – Closing Stock in Trade

Things to remember:

Difficulty in Forecasting: Financial statements are a record of past events and historical facts. In the fast changing and developing modern business, the analysis of past information may not be of much use in future forecasting. Continuous changes take place in the demand of the product, policies adopted by the firm, the position of competition etc. As such, no estimate based on the analysis of historical facts can be made for future.

Important Note:

Different Accounting Policies: If two firms adopt different accounting policies, the comparison between the two will be unreliable. For example, one firm may provide depreciation on original cost method, whereas the other firm may adopt the written-down value method for providing the depreciation. Similarly, the method of valuation of closing stock may also differ from one firm to another. The results obtained from the comparison of the financial statements of such firms may give misleading picture.

Question 40. From the following information, calculate Change in Inventory of Stock-in-Trade: Opening and Closing Stock-in-Trade ₹5,00,000 and ₹4,00,000 respectively.

Calculation of Change in Inventory of Stock-in-Trade:

About solution:

Calculation of Change in Inventory of Stock-in-trade:-

Change in Stock in Trade = Opening Stock in trade – Closing Stock in Trade

Things to remember:

Financial statements record only those events and transactions which can be expressed in terms of money. Qualitative aspects of business units are omitted from the books at all as these cannot be expressed in monetary terms. Thus, changes in management, reputation of the business, cordial management-labour relations, firm’s ability to develop new products, efficiency of management, satisfaction of firm’s customers etc. which have a vital bearing on the profitability of the company are all ignored and omitted from being recorded because all of these are qualitative in nature.

Important Note:

Results obtained from financial analysis assume significance only when compared with the figures of previous periods. For example, the profit of a firm to sales is 12%, whether this is satisfactory or not, will depend upon the figures of previous years. If the firm earned 10% of sales as profit in the previous year, it may be considered to have done better this year. However, the financial statements of two years may not be comparable due to the changes in accounting policies.

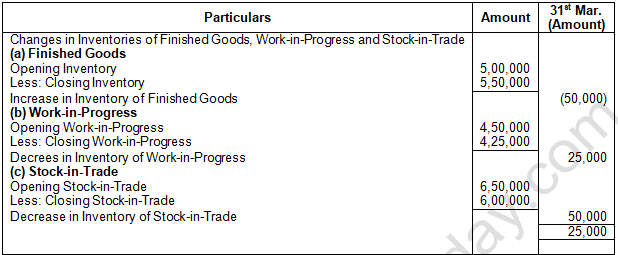

Question 41. From the following information of Hospitality Ltd. for the year ended 31st March, 2018, calculate amount that will be shown in the Note to Accounts on Changes in inventories of Finished Goods, WIP and stock-in-Trade:

Calculate the amount that will be shown in the Note to Accounts on Changes in Inventories of Finished Goods, Work-in-Progress and Stock-in-Trade from the following information of Hospitality Ltd. For the year ended 31st March……….

About solution:

Cross-sectional Analysis: It is also known as interring firm comparison. This analysis helps in analysing financial characteristics of an enterprise with financial characteristics of another similar enterprise in that accounting period. For example, if company A has earned 15% profit on capital invested. This does not say whether it is adequate or not. If we analyse further and find that a similar company has earned 16% during the same period, then only we can make a conclusion that company B is better than company A. Thus, it turns into a meaningful analysis.

Things to remember:

It is also called as intra-firm comparison. According to this method, the relationship between different items of financial statements is established, comparisons are made and results obtained.

Important Note:

Cross-sectional cum Time Series Analysis: This analysis is intended to compare the financial characteristics of two or more enterprises for a defined accounting period. It is possible to extend such a comparison over the year. This approach is most effective in analysing of financial statements.

Question 42. From the following information compute the amount to be shown in Note to Accounts on Employees Benefit Expenses: Wages ₹ 5,40,000; Salaries ₹ 7,20,000; bonus ₹ 1,05,000; Staff Welfare Expenses ₹ 60,000 and Business Promotion Expenses ₹ 50,000.

Computation of the amount to be shown in Note of Accounts on Employees Benefit Expenses:

About solution:

Calculation of Amount to be shown in the Statement of Profit

Employees Benefit Expenses = Wages + Salaries + Bonus + Staff Welfare Expenses

Things to remember:

Comparative financial Statements In brief, comparative study of financial statements is the comparison of the financial statements of the business with the previous year’s financial statements. It enables identification of weak points and applying corrective measures. Practically, two financial statements (balance sheet and income statement) are prepared in comparative form for analysis purposes

Important Note:

For studying current financial position or liquidity position of a concern one should examine the working capital in both the years. Working capital is the excess of current assets over current liabilities.

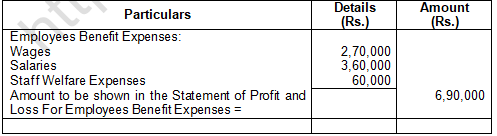

Question 43. From the following information, prepare Note to Accounts on Employees Benefit Expenses: Wages ₹ 2,70,000; Salaries ₹ 3,60,000; Staff Welfare Expenses 60,000; Printing and Stationery Expenses ₹ 20,000 and Business Promotion Expenses ₹ 50,000.

Computation of the amount to be shown in Note of Accounts on Employees Benefit Expenses:

About solution:

Calculation of Amount to be shown in the Statement of Profit

Employees Benefit Expenses = Wages + Salaries + Staff Welfare Expenses

Things to remember:

Common Size Balance Sheet: A statement where balance sheet items are expressed in the ratio of each asset to total assets and the ratio of each liability is expressed in the ratio of total liabilities is called common size balance sheet.

Important Note:

Thus the common size statement may be prepared in the following way.

1. The total assets or liabilities are taken as 100

2. The individual assets are expressed as a percentage of total assets i.e. 100 and different liabilities are calculated in relation to total liabilities.

Question 44. Out of the Following, identify the items that are shown in the Note to Accounts on Finance Costs:

(i) Interest paid on Borrowing from prince Finance Ltd.;

(ii) Interest paid on Term Loan to Bank;

(iii) Interest paid on Public Deposits;

(iv) Loss on Issue of Debentures Written off; and

(v) Bank Charges.

The items shown in the Note of Accounts of Finance Costs are:

(i) Interest paid on Borrowing from Prince Finance Ltd.;

(ii) Interest paid on Term Loan to Bank;

(iii) Interest paid on Public Deposits;

(iv) Loss on Issue of Debentures Written off; and

(v) Bank Charges.

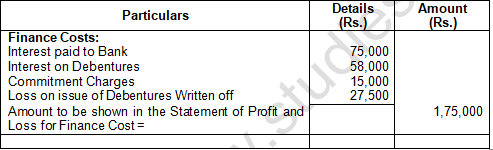

Question 45. From the following information, prepare Note to Accounts on Finance Costs: Interest paid to Bank ₹ 75,000; Interest on Debentures ₹ 58,000; Loss on issue of Debentures written off ₹ 27,500; and Commitment Charges ₹ 15,000.

Computation of the amount to be shown in Note of Accounts on Finance Costs:

About solution:

Calculation of Finance Costs: Interest paid to Bank + Interest of Debtors + Commitment Charges + Loss on issue of denture written off.

Things to remember:

t the preparation of financial statements i.e. Balance Sheet and Trading and Profit and Loss Account in the module titled ‘Financial Statements of Profit and Not for Profit Organisations’. In the case of a company the Trading and Profit & Loss Account is known as Statement of Profit and Loss. After preparation of the financial statements, one may be interested in analysing the financial statements with the help of different tools such as comparative statement, common size statement, ratio analysis, trend analysis, fund flow analysis, cash flow analysis, etc.

Important Note:

Balance Sheet as prescribed in schedule VI part I of the Companies Act 1956 is broadly divided into two parts:

(i) Equity and Liabilities

(ii) Assets

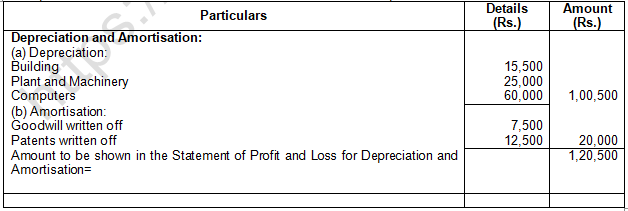

Question 46. From the following information of Best Marketing Ltd. for the year ended 31st March, 2018, prepare Note to Accounts on Depreciation and Amortisation Expenses:

Depreciation on: Building ₹15,500; Plant and Machinery ₹25,000; Computers ₹ 60,000; Goodwill written off ₹ 7,500; Patents written off ₹ 12,500.

Computation of the amount to be shown in Note to Accounts on Depreciation and Amortisation:

About solution:

Analysis of financial statement is a systematic process of dividing the financial information into simple and valuable elements, establishing relationships between inter-related elements and interpreting the same to understand the working and financial position of an enterprise from its financial statements.

Things to remember:

To Assess the Earning Capacity or Profitability: Earning Capacity and Profitability of the enterprise can be assessed from the financial statement analysis. It also facilitates forecasting of the same for the future years. External users are interested in earnings and hence, this is their prime objective of analysing financial statement. ii. To Assess the Managerial Efficiency: This assessment is possible because financial statement analysis identifies the areas where managers have been efficient and where not. Favorable and unfavorable variations can be identified to pinpoint the managerial inefficiency.

Important Note:

To facilitate Inter-firm Comparison: Inter-firm Comparison helps an enterprise to assess its own performance as well as that of others if mergers and acquisitions are to be considered.

Question 47. Identify which of the following items will be shown in the Note to Accounts on Other Expenses? (i) Salaries; (ii) Postage Expenses; (iii) Telephone and Internet Expenses; (iv) Rent for warehouse; (v) Carriage Inwards; (vi) Depreciation on computers; (vii) Computer Software amortised; (viii) Computer Hiring Charges; (ix) Audit fee; (x) Bonus.

The following items will be shown in the Note to Accounts on other Expenses Head:

(ii) Postage Expenses

(iii) Telephone and Internet Expenses

(iv) Rent for Warehouse

(v) Carriage Inwards

(viii) Computer hiring charges

(ix) Audit Fee.

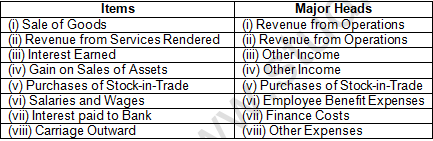

Question 48. Under which line item (major head) of the Statement of Profit and Loss of non-financial company will the following be shown:

(i) Sale of Goods; (ii) Revenue from Services Rendered; (iii) Interest Earned; (iv) Gain (Profit) on Sale of Assets; (v) Purchases of Stock-in-Trade; (vi) Salaries and Wages; (vii) Interest paid to Bank; (viii) Carriage Outward?

Question 49. Under which line item (major head) of the Statement of Profit and Loss of a financial company will the following be shown:

(i) Interest on Loans Given: (ii) Gain (Profit) on Sale of Securities; (iii) Loss on Sale of Fixed Assets; (iv) Interest paid on Deposits; (v) Depreciation on Computers; (vi) Goodwill Written off; (vii) Commission paid for Deposit Mobilisation; and (viii) Repairs Expenses?

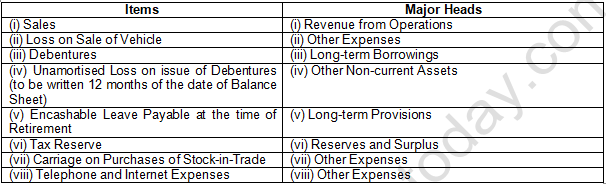

Question 50. Under which line item of the financial statements following items will be shown:

(i) Sales; (ii) Loss on Sale of Vehicle; (iii) Debentures; (iv) Unamortised Loss on Issue of Debentures (to be written off within 12 months of the date of Balance Sheet); (v) EnCashable Leave Payable at the Time of Retirement; (vi) Tax Reserve; (vii) Carriage on Purchases of Stock-in-Trade; and (viii) Telephone and Internet Expenses?

Question .51 Financial statements are prepared following the consistent accounting concepts, principles, procedures and also the legal environment in which the business organisations operate. These statements are the sources of information on the basis of which conclusions are drawn about the profitability and financial position of a company so that their users can easily understand and use them in their economic decisions in a meaningful way. From the above statement, identify any two values that a company should observe while preparing its financial statements. Also, state under which major headings and sub-headings the following items will be presented in the Balance Sheet of a company as per Schedule III of the Companies Act, 2013:

(i) Capital Reserve; (ii) Calls-in-Advance;

(iii) Loose Tools; and (iv) Bank Overdraft.

Under the following major headings and sub-headings in the Balance Sheet as per Schedule III of the Companies Act, 2013, the following items are presented:

The two identified values that a company should observe while preparing its financial statements are:

(i) Consistency

(ii) Transparency.