Access free TS Grewal Solution Class 12 Chapter 5 Cash Flow Statement 2026 below. Students can now access free TS Grewal Solutions for Class 12 Mathematics. These chapter-wise exercises are designed by expert math teachers to help you understand complex formulas and score higher marks in your class tests.

Class 12 Math Chapter 5 Cash Flow Statement TS Grewal Solutions

Get step-by-step TS Grewal Solutions for Chapter 5 Cash Flow Statement Class 12 Math below. All answers are updated for the 2026 school curriculum, offering step by step methods to help you solve textbook problems easily.

Chapter 5 Cash Flow Statement TS Grewal Class 12 Solved Exercises

About this chapter: TS Grewal Class 12 Chapter 5 Cash Flow Statement explains about the various ways by which a cash flow statement of a company can be prepared. The chapter explains about the basic concepts of cash flow statement and the importance and process of preparing it and how to utilise it. Students will be able to understand the relationship between the cash flow statements and various other financial statements and how to interpret the statement properly. The questions in the exam will provide details about various cash transactions which a company does and the students will be required to prepare a cash flow statement. It is important for the students to understand the basic concepts of the topic as this will help them to understand the cash flow situation of a company. Once you have understood all the topics given in this chapter you should solve the questions which have been given at the end of the chapter and match your answers with the solutions which have been provided by our teachers. Please refer to the section below to access all the answers to various questions.

Solutions for T.S. Grewal's Analysis of Financial Statements

Textbook for CBSE Class 12

TS Grewal Solutions Class 12 Accountancy

Chapter 5 Cash Flow Statement

(a) Cash Sale of Goods

(b) Cash Received against Revenue from Services rendered

(c) Cash Purchases of goods

(d) Cash paid against Services Taken

(k) Commission Received

(o) Income Tax Paid

(q) Cash Received from Debtors

(r) Cash paid to Creditors

(ii) Below are the transaction are belong to Investing Activities:-

(e) Patents Purchased

(i) Purchases of Shares

(n) Interest on Investments

(p) Income Tax Paid in Gain on Sale of Asset

(iii) Below are the transaction are belong toFinancing Activities:

(g) Bank Overdraft

(h) Proceeds from issue of Debentures

(j) Repayment of Long-term Loan

(l) Repayment of Debentures

(m) Interest on Debentures

(iv) Below are the transaction are belong to Cash and cash equivalents

(f) Marketable Securities

(a) Purchase of Shares on a Stock Exchange

(b) Dividend received on Shares

(c) Loan Given

(d) Loan Taken

(f) Interest on Borrowings

There is no transactions are classified as Operating Activities for a non-financial company.

(b) Sale of goods against cash.

(c) Purchase of machinery for cash.

(d) Purchase of Land and Building for Rs. 10,00,000. Consideration paid by issue of debentures.

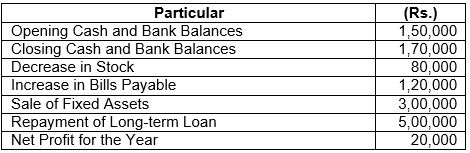

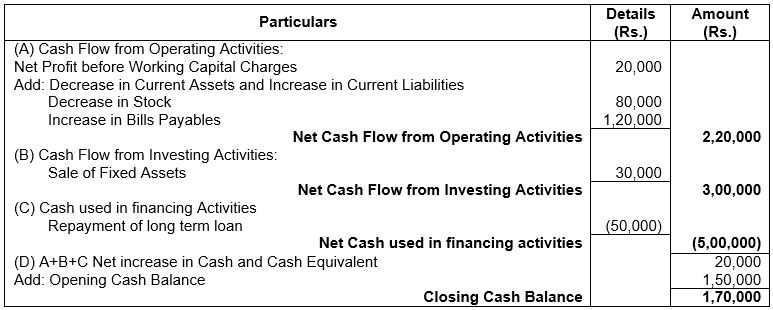

(e) Issued fully paid Bonus Shares.

(f) Cash withdrawn from bank.

(g) Payment of Interim Dividend

Below are the following result in inflow of Cash and Cash Equivalents:-

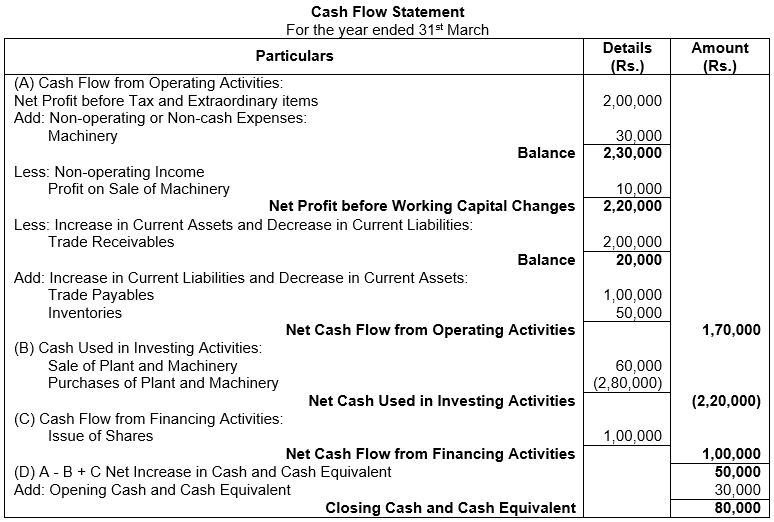

(a) Sale of Fixed Assets, Book Value Rs. 1,00,000 at a profit ofRs. 10,000.

(b) Sale of goods against cash.

Below are the following result in outflow of Cash and Cash Equivalents:-

(c) Purchase of Machinery of cash.

(g) Payment of interim Dividend.

Below are the following result in no flow of Cash and Cash Equivalents:

(d) Purchase of Land and Building for Rs. 10,00,000. Consideration paid by issue of debentures.

(e) Issue fully paid Bonus Shares.

(f) Cash withdrawn from bank.

Question 4. For each of the following transactions, calculate the resulting Cash Flow and state the nature of Cash Flow, i.e., whether it is Operating, Investing or Financing:

(a) Acquired machinery for Rs. 2,50,000 paying 20% by cheque and executing a bond for the balance payable.

(b) Paid Rs. 2,50,000 to acquire shares in Informa Tech Ltd. and received a dividend of Rs. 50,000 after acquisition.

(c) Sold machinery of original cost of Rs. 2,00,000 with an accumulated depreciation of Rs. 1,60,000 for Rs. 60,000.

Answer:

Below are the transactions of Cash Flow and there nature:-

(a) 20% payment by cheque that of Rs. 2,50,000 is Rs. 50,000 is an outflow of funds and an investing Activity due to purchases of machinery.

(b) Payment ofRs. 2,50,000 to acquire shares in informa Tech Ltd. is an Investing Activity and an out flow of cash. Whereas dividend received is an inflow of cash and an investing Activity. So the net outflow of cash due to investing Activity is Rs. 20,00,000.

(c) Sale of machinery for Rs. 60,000 is an inflow of cash due to investing activity. The cost price and accumulated depreciation has nothing to do with cash movement.

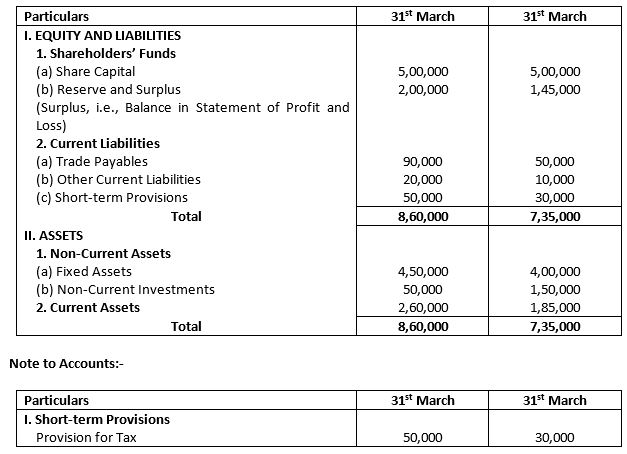

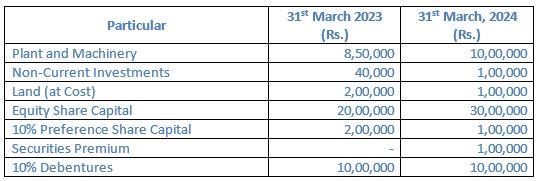

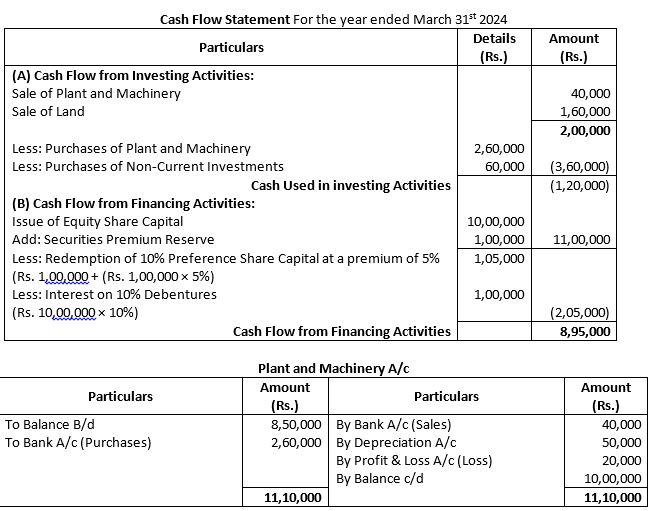

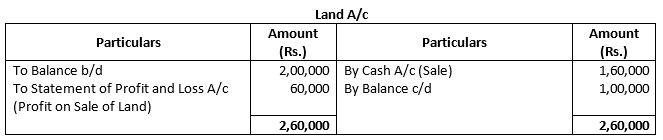

Question 5. Following are the extracts from the Balance Sheet of MAH Ltd. as at 31st March, 2024:

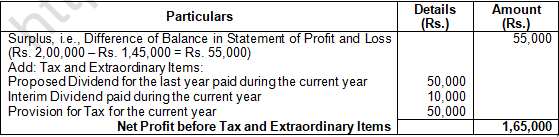

Additional Information: Proposed Dividend for the years ended 31st March, 2023 and 2024 are Rs. 4,00,000 and Rs. 5,00,000 respectively. Prepare the Note to show Net Profit before Tax and Extraordinary Items

Answer:

Following is the Note to show Net Profit before Tax and Extraordinary items of MAH Ltd. for the year ended 31st March.

About Solution:

Cash Flow: A cash flow is the inflow (receipt) and the outflow (payment) of Cash and Cash equivalents, where cash and cash equivalents include Cash, Bank Balance, Marketable Securities, etc. (unless specified otherwise, Current Investments are considered as Marketable Securities).

Things to Remember:

Cash Flow Statement: It is a statement that shows the inflows and the outflows Of Cash and cash Equivalents during the period. Inflows are those transactions that increase the Cash

Important Notes:

As per this accounting standard, cash flows are showed under the following 3 heads:

1. Cash Flow from Operating Activities.

2. Cash Flow from Investing Activities.

3. Cash Flow from Financing Activities.

Question 6. Following is the extract from the Balance Sheet of Zee Ltd.:

Additional Information:

(i) Proposed dividend on equity shares for the year 2017-18 and 2018-19 are Rs. 1,60,000 and Rs. 2,00,000 respectively.

(ii) An Interim Dividend of Rs. 40,000 on Equity Shares was paid.

Calculate Net Profit before Tax and Extraordinary Items.

Answer:

Following is the Note to show Net Profit before Tax and Extraordinary items of Zee Ltd. for the year ended 31st March.

About Solution:

Cash Flow from Investing Activities: Activities related to sale and purchase of long-term fixed assets and investments.

Cash Inflows:

1. Proceeds from sale Of Fixed Assets and Investments.

2. Interest and dividend received.

Things to Remember:

Cash Equivalents and outflows are those transactions that decrease the Cash and Cash Equivalents. Such statement is prepared in accordance with the Accounting Standard-3 (Revised) on Cash Flow Statement.

Important Notes:

Cash Flow from Operating Activities: Activities related to core or principal revenue generating activities of an enterprise.

1. Cash Sales

2. Debtors

3. Royalty

4. Commission

Q7. From the following extract of Balance Sheet of Universal Ltd., Calculate Net Profit before Tax and Extraordinary Items:

Additional Information:

Interim Dividend of ₹ 2,00,000 was paid on Equity Shares on 1st November, 2023

Answer:

Question 8. Calculate Net Profit before Tax and Extraordinary Items of Premier Sales Ltd. from its Balance Sheet as at 31st March, 2024:

Additional Information:

(i) Proposed Dividend for the years ended 31st March, 2023 and 2024 are Rs. 50,000 and Rs. 75,000 respectively.

(ii) Interim Dividend paid during the year was Rs. 10,000

Answer:

Following is the Note to show Net Profit before Tax and Extraordinary items of Premier Sales Ltd. for the year ended 31st March.

About Solution:

Cash Flow from Financing Activities: Activities related to capital or long term funds of an enterprise.

Cash Inflows:

1. Proceeds from Issue of Shares and Debentures for Cash.

2. Proceeds from Long-term Borrowings such as Bonds, Loans, etc.

Things to Remember:

Cash Outflows: Purchase of long term fixed assets such as Land & Building, Plant & Machinery, Investments, etc.

Important Notes:

To determine the sources of Cash and Cash Equivalents under operating, investing and financing activities of the enterprise.

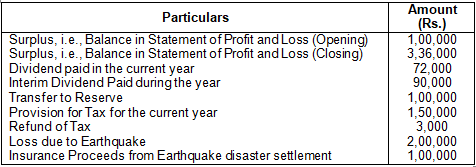

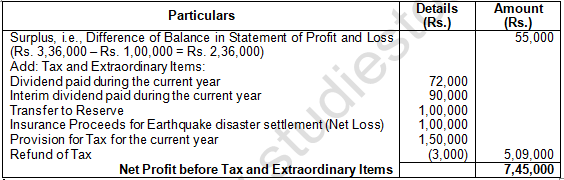

Question 9. From the following information, calculate Net Profit before Tax and Extraordinary Items:

Answer:

Following is the Note to show Net Profit before Tax and Extraordinary items of

About Solution:

To determine the applications of Cash and Cash Equivalents for operating, investing and financing activities of the enterprise.

Things to Remember:

To determine the net change in Cash and Cash Equivalents due to cash inflows and outflows for operating, investing and financing activities of the enterprise that take place between the 2 balance sheet dates.

Important Notes:

To facilitate Short-term Planning: It helps in planning investments and assessing the financial requirements of the enterprise based on information provided in the statement about the sources and applications of Cash and Cash Equivalents.

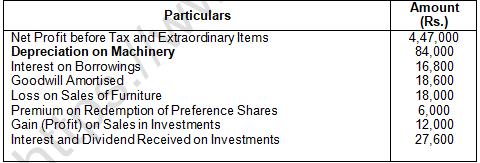

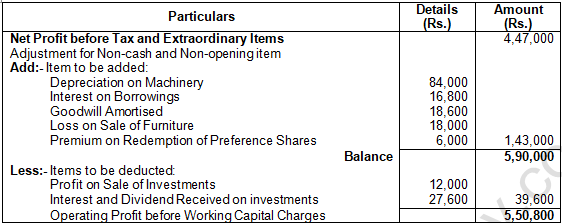

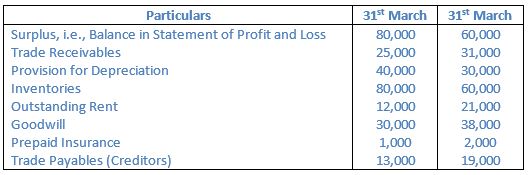

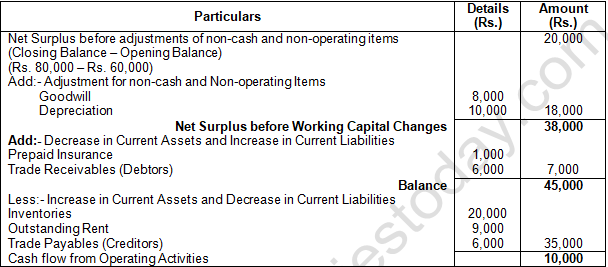

Question 10. From the following information, calculate Operating Profit before Working Capital Charges:

Answer:

Calculation of the Opening Profit before Working Capital Change

About Solution:

To manage Cash Efficiently: It provides information about the cash position by reflecting either a surplus of cash or a deficit of cash in the statement. This helps the enterprise to take decisions about the investment of surplus cash and the arrangement of deficit funds. iv. To facilitate Comparative Study: It facilitates the comparison of actual cash flows with the budgeted cash flows to identify whether the inflows and outflows of cash are moving as per the plan. Such comparison will also reflect deviations Of the actual cash flows from the budgeted cash flows for which necessary actions are then taken by the enterprise.

Things to Remember:

To justify Cash Position: Cash flow statement is prepared to record all the cash inflows and outflows which result in the surplus or deficit of cash for an enterprise. Since, all the cash transactions are presented in the statement, it becomes easy to identify the items which increase or decrease the cash balances.

Important Notes:

To evaluate Management Decisions: This statement classifies the cash transactions under 3 separate heads namely, operating, investing and financing. Such classification helps the users of the statement to evaluate whether the decisions taken by the management are appropriate from investing and financing point of view.

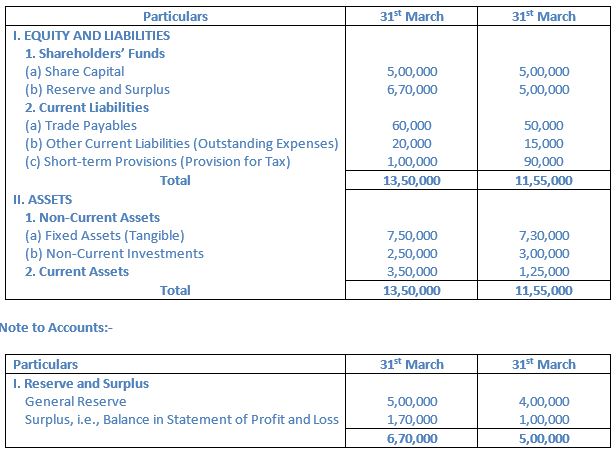

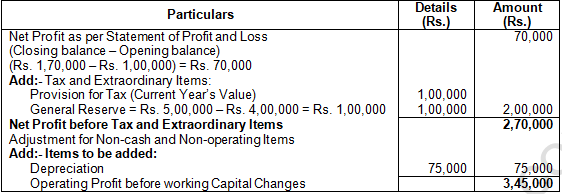

Question 11. From the following Balance Sheet of Double Tree Ltd. as at 31st March, 2024 and additional information, calculate Operating Profit before Working Capital Changes:

Additional Information: Depreciation for the year was Rs. 75,000.

Answer:

Calculate of the Operating Profit before Working Capital Changes of Double Tree Ltd. for the year ended 31st March

About Solution:

To take dividend decisions: In order to declare or approve the dividends, every enterprise should comply with the prescribed provisions e.g., depositing the amount of dividend in a separate bank, etc. Accordingly, to identify whether the enterprise has sufficient funds for such compliance cash flow statement is referred by the management. Also, it helps in deciding how much dividend the enterprise should pay during a particular year.

Things to Remember:

Non-cash transactions are not shown: It takes into consideration only cash inflows and cash outflows. Non-cash transactions are not considered for preparation of cash flow statement.

Important Notes:

Not a substitute for an Income Statement: Cash flow statement cannot be used as a substitute for an Income Statement because Income Statement is prepared on accrual basis of accounting whereas cash flow statement is prepared on cash basis. Also, it is not possible to compute net profit or loss from the cash flow statement.

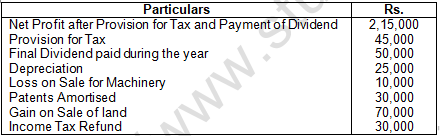

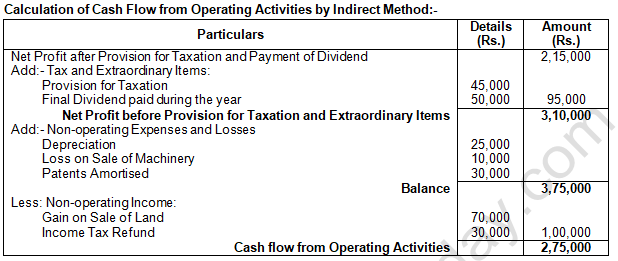

Question 12. Calculate Cash Flow from Operating Activities from the following details:

Answer:

Not a substitute for Balance Sheet: Cash flow statement do not show the financial position of the enterprise and therefore, cannot be used as a substitute for Balance Sheet.

Things to Remember:

Historical in Nature: Cash flow statement is prepared based on the cash inflows and outflows that have already taken place during the year and hence, it is historical in nature.

Important Notes:

Assessment of Liquidity: Cash flow statement takes into consideration all the transactions of cash and cash equivalents. This cash and cash equivalents is just one of the components in the current assets which determine the liquidity position of the enterprise. Therefore, cash flow statement alone cannot help in determining the liquidity position of the enterprise.

Question 13. Calculate Cash Flow from Operating Activities from the following details:

Answer:

About Solution:

Accuracy of Cash Flow Statement: Since, the cash flow statement is prepared from the financial statements of an enterprise; accuracy of the same shall depend upon how accurately the financial statements of the enterprise are prepared.

Things to Remember:

Cash: It includes Cash in hand and demand deposits with banks.

Important Notes:

Cash Equivalents: It includes highly liquid short-term investments that are readily convertible into cash and that are subject to an insignificant risk of change in value. It includes treasury bills, commercial papers, current investments and preference shares if these are redeemable within 3 months from the date of purchase and if they do not have any significant risk of change in its value.

Question 14. Calculate Cash Flow from Operating Activities from the following:

Answer:

Classification of Cash Flows as per Accounting Standard-3 (Revised): This standard on Cash Flow Statement requires that all the inflows and outflows of the cash and cash equivalent during a particular period should be classified under 3 different heads as per the nature of transactions.

Things to Remember:

Operating Activities: These are the principal revenue generating activities Of an entity. It includes all non-investing and non-financing activities. In a cash flow statement, net effect of all the inflows and outflows from operating activities is shown as Cash Flow from (or used in) Operating Activities.

Important Notes:

Financial Companies: It includes all transactions related to:

1. Purchase of securities.

2. Sale Of securities.

3. Interest on loans granted.

4. Interest on loans taken.

5. Dividends on securities.

6. Salaries, bonus and other employee benefits paid to employees.

7. Income tax paid and income tax refund received (unless such amounts are identified with investing or financing activities).

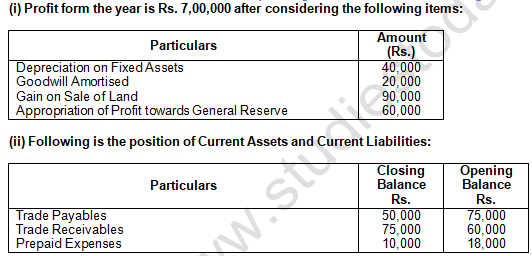

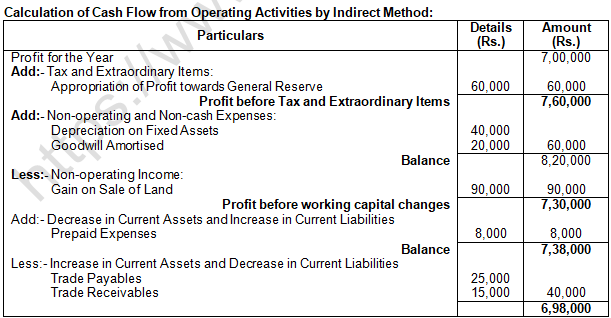

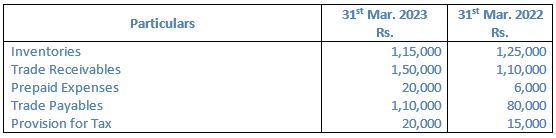

Question 15. Calculate Cash Flow from Operating Activities from the following information: (Old Question)

Answer:

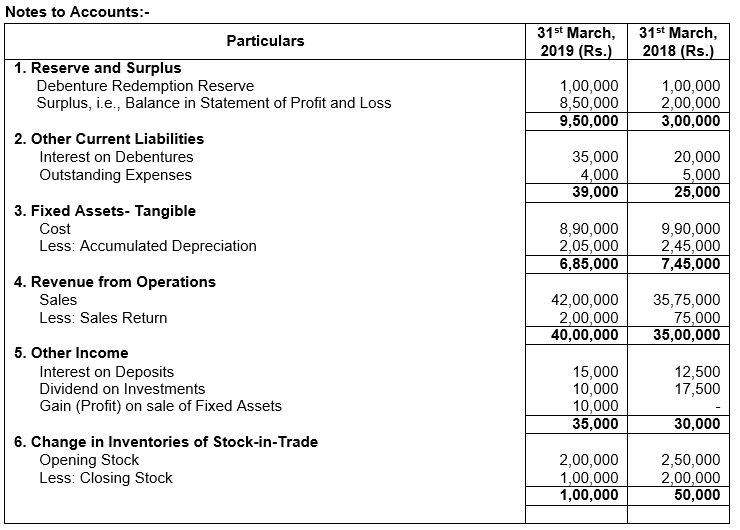

Depreciation charged on Plant and Machinery Rs. 55,000, insurance claim received Rs. 50,000, gain (profit) on sale of investment Rs. 20,000 appeared in the Statement of Profit and Loss for the year ended 31st March, 2019. Calculate Cash Flow from Operating Activities.

Answer:

About Solution:

Non-Financial Companies: It includes all transactions related to:

1. Purchase of goods and/or availing of services.

2. Sale of goods and/or rendering of services.

3. Amounts received from trade receivables.

4. Amounts paid to trade payables.

5. Royalties, fees and commission, etc.

6. Wages, salaries and other employee benefits paid to the workers and employees.

7. Payment of claims and receipt of premium (in case of Insurance Companies)

Things to Remember:

Investing Activities: These include all activities related to the acquisition and disposal Of Long-term Assets and other investments which are not classified as cash equivalents.

Important Notes:

Following is the list Of investing activities:]

1. Purchase of fixed assets.

2. Sale or disposal of fixed assets.

3. Purchase of securities (in case of non-financial companies).

4. Sale of securities (in case of non-financial companies).

5. Loans and advances made to third parties (other than those made by a financial enterprise)

6. Repayments received from loans and advances made to third parties (Other than those made by a financial enterprise).

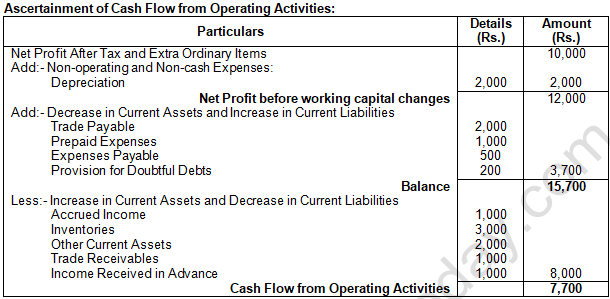

Question 16. Charles Ltd. earned a profit of Rs. 1,00,000 after charging depreciation of 20,000 on assets and a transfer to General Reserve of Rs. 30,000. Goodwill amortised was Rs. 7,000, and gain on sale of machinery was Rs. 3,000. Other information available is (changes in the value of Current Assets and Current Liabilities): trade receivables showed an increase of Rs. 3,000; trade payables an increase of Rs. 6,000; Prepaid expenses an increase of Rs. 200; and outstanding expenses a decrease of Rs. 2,000.

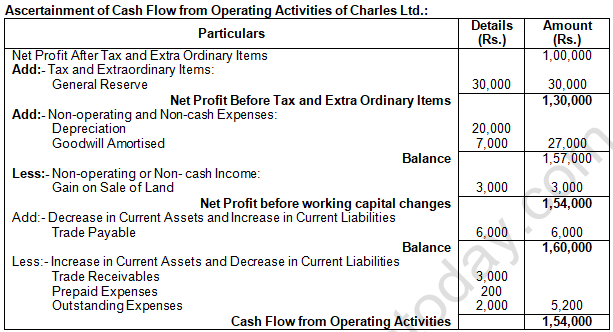

Ascertain Cash Flow from Operating Activities.

Answer:

About Solution:

Operating Activity helps in taking vital decisions with respect to use of cash for payment of dividends to shareholders, make new investments, expand projects, etc. o It helps in forecasting and projecting future cash flows.

Things to Remember:

Investing Activities: It represents the extent to which expenditure has been incurred to generate future revenue and cash flows.

Important Notes:

Financing Activities: It assists in assessing claims on future cash flows contributors Of funds to the enterprise.

Question 17. Compute Cash Flow from Operating Activities from the following: (Old Question)

An asset costing Rs. 40,000 having book value of Rs. 28,000 was sold for Rs. 36,000.

Answer:

Question 17. From the following information, Calculate Cash flow from Operating Activities:

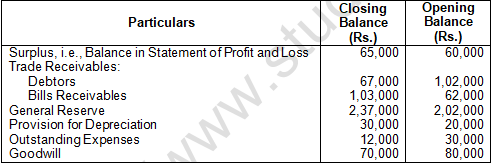

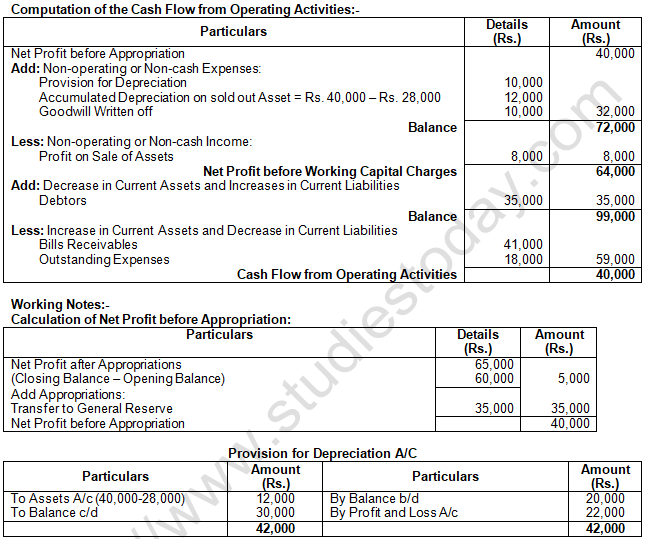

Additional Information:

(i) Preference Shares were redeemed on 31st March, 2023 at a premium of 5%.

(ii) Dividend on Equity Shares was paid @ 8%.

(iii) Fresh issue of Equity shares was made on 1st April 2022.

Answer:

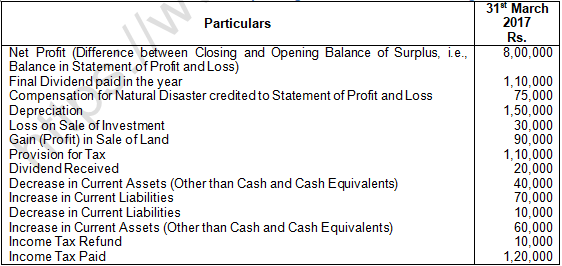

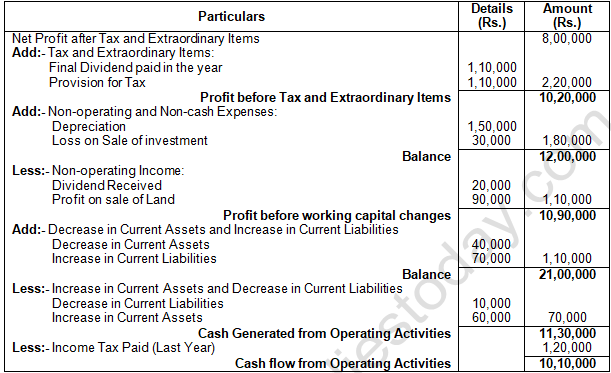

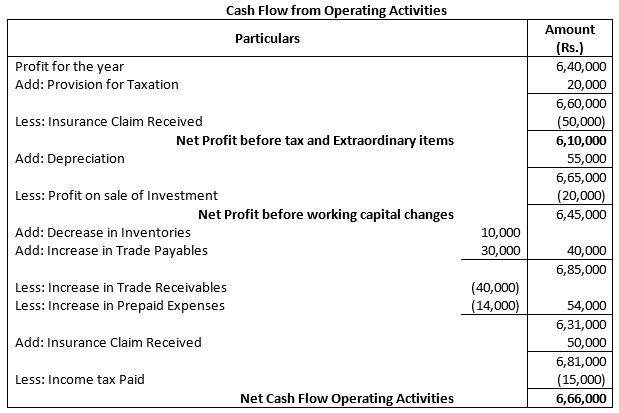

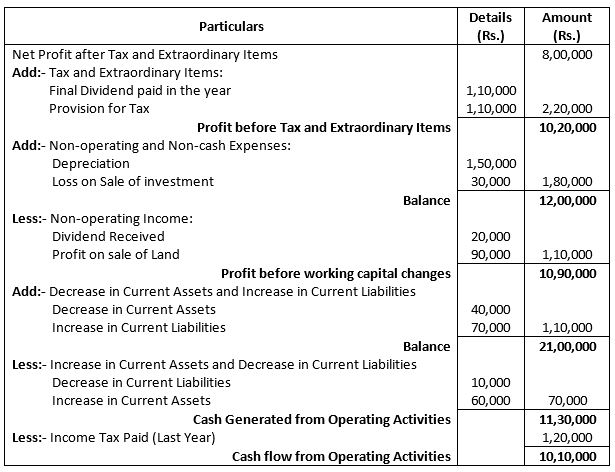

Question 18. Sunrise Ltd., reported Net Profit after Tax of ₹ 6,40,000 for the year ended 31st March, 2023. The relevant extract from Balance Sheet as at 31st March, 2023 is:

Depreciation charged on Plant and Machinery ₹ 55,000, insurance claim received ₹ 50,000, gain (Profit) on sale of investment ₹ 20,000 appeared in the Statement of Profit & Loss for the year ended 31st March, 2023. Calculate Cash flow from Operating Activities

Answer:

Question 19. Compute Cash Flow from Operating Activities from the following:

(i) Profit for the year ended 31st March, 2024 is Rs. 10,000 after providing for depreciation ofRs. 2,000.

(ii) Current Assets and Current Liabilities of the business for the year ended 31st March, 2023 and 2024 are as follows:

Answer:

All the incomes and expenses that arise from events or transactions that are clearly distinct from the ordinary course of business of the enterprise are termed as extraordinary items. o All such items are not expected to recur frequently or regularly.

Things to Remember:

It includes items such as payment shareholders in the event of buy back of shares, claim for damages received, etc.

Important Notes:

Indirect Method: In this method, Cash Flow from Operating Activity is calculated from statement Of Profit and Loss and Balance Sheet with the help Of following steps:

Step 1: Calculate the Net Profit before Tax and Extraordinary Items.

Step 2: Calculate the Operating Profit before Working Capital Changes.

Step 3: Compute the Cash generated from Operating Activities.

Step 4: Compute the Cash flow from Operating Activities before Extraordinary Items.

Step 5: Compute the Cash flow from (or used in) Operating Activity.

Question 20. Calculate Cash Flow from Operating Activities from the following information:

Answer:

About Solution:

Financing Activities: These are those activities that change the size and composition of the owner's capital (i.e., Equity and Preference Share Capital in case of a company) and borrowings of the enterprise.

Things to Remember:

Following is the list of financing activities:

a) Issue of shares or other similar instruments.

b) Issue Of debentures, loans, bonds, and other short-term borrowings.

c) Changes in bank overdraft and cash credit.

d) Buy-back of equity shares.

e) Repayment of borrowings including redemption of debentures.

f) Dividends on both equity and preference shares.

g) Interest on debentures and loans (both short and long-term loans).

Important Notes:

Transactions not regarded as Cash Flow: These are the transactions that are mere movements in between the items of Cash and Cash Equivalents. This includes cash deposited in bank, cash withdrawn from the bank and purchase or sale of marketable securities.

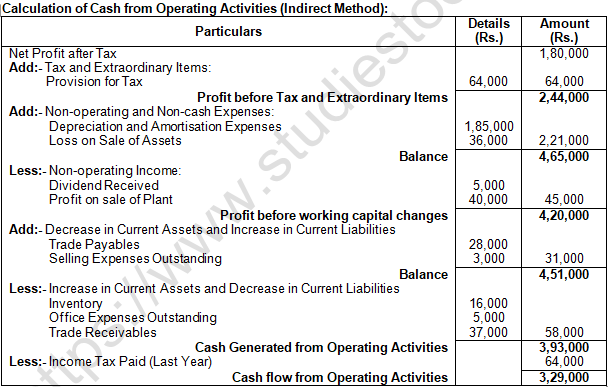

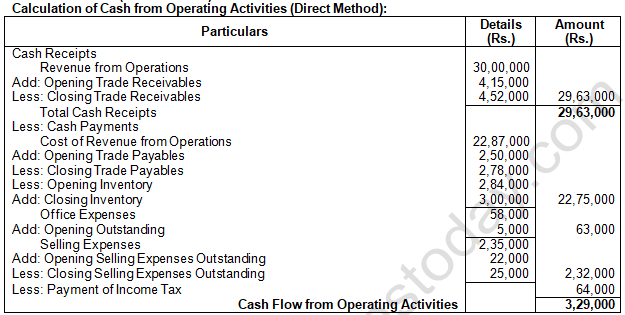

Question 21. Following information is related to ABC Ltd.:

Answer:

Alternate Method (Direct Method)

Calculation of Cash from Operating Activities (Direct Method):

About Solution:

There are two methods to solve cash flow:-

1. Direct Method

2. Indirect Method

Things to Remember:

Non-cash transactions: These are the transactions in which the inflow or outflow Of Cash or Cash Equivalent does not take place. Therefore, these non-cash transactions are not considered while preparing the Cash Flow Statements. These transactions include depreciation, amortization, issue of bonus, etc.

Important Notes:

Financial Enterprise: An enterprise that basically deals in lending (advancing loans) and borrowing Of funds (accepting deposits), such as Banks.

Question 22. From the following information, Calculate the amount of Cash Flow from Investing Activities:

Acquired Machinery for ₹ 10,00,000, paying 10% immediately in cash and accepting a draft for the balance in favour of the vendor, payable after three months.

Answer:

Computation of the Cash Flow from Investing Activities:-

About Solution:

1. Cash flow Statement helps in efficient and effective management of cash.

2. The management generally looks into cash flow statements to understand the internally generated cash which is best utilized for payment of dividends.

3. Cash Flow Statement based on AS-3 (revised) presents separately cash generated and used in operating, investing and financing activities.

4. It is very useful in the evaluation of cash position of a firm

Things to Remember:

Non-Financial Enterprise: An enterprise that basically deals in areas other than finance (purchase Of raw material and sale of goods.

Important Notes:

Operating Activities:

a) It acts an indicator of the extent to which the business operations successfully generate cash.

b) It determines operating efficiency of the entity

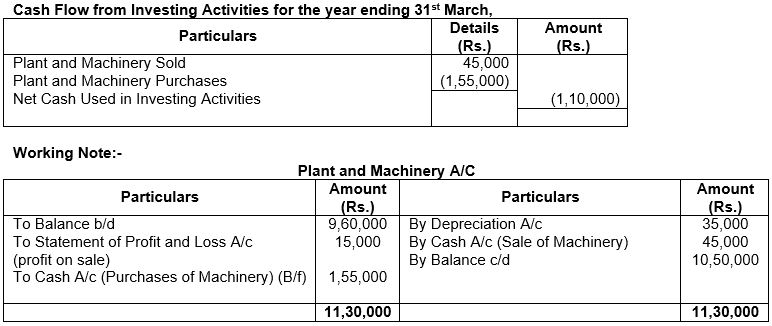

Question 23. Mars Ltd. has Plant and Machinery whose written down value on 1st April, 2017 was Rs. 9,60,000 and on 31st March, 2018 was Rs. 10,50,000. Depreciation for the year was Rs. 35,000. In the beginning of the year, a part of plant was sold for Rs. 45,000 which had a written down value of Rs. 30,000.

Calculate Cash Flow from Investing Activities.

Answer:

About Solution:

The statement of cash flow serves a number of objectives which are as follows:

1. Cash flow statement aims at highlighting the cash generated from operating activities.

2. Cash flow statement helps in planning the schedule for repayment of loan schedule and replacement of fixed assets, etc.

3. Cash is the centre of all financial decisions. It is used as the basis for the projection of future investing and financing plans of the enterprise.

4. Cash flow statement helps to ascertain the liquid position of the firm in a better manner. Banks and financial institutions mostly prefer cash flow statement to analyse liquidity of the borrowing firm.

Things to Remember:

It is determined by analyzing the changes in fixed assets, long-term investments in the beginning and at the end of the year for which specific accounts can be prepared using the values that are available.

Important Notes:

These are those activities that change the size and composition of the owner's capital (i.e., Equity and Preference Share Capital in case Of a company) and borrowings Of the enterprise.

Question 24. From the following details. Calculate Cash Flow from Investing Activities

Additional Information:

1. Half of the investment held in the beginning of the year were sold at 10% profit.

2. Depreciation on Land and Building was Rs. 50,000 for the year.

3. Interest received on investments Rs. 75,000.

Answer:

About Solution:

Cash Flows are inflows and outflows of cash and cash equivalents. The statement of cash flow shows three main categories of cash inflows and cash outflows, namely: operating, investing and financing activities.

(a) Operating activities are the principal revenue generating activities of the enterprise.

(b) Investing activities include the acquisition and disposal of long-term assets and other investments not included in cash equivalents.

(c) Financing activities are activities that result in change in the size and composition of the owner’s capital (including Preference share capital in the case of a company) and borrowings of the enterprise.

Things to Remember:

It does not take into consideration bonus issue as it is just a capitalization of reserves for which the company does not receive any cash for it. Similarly, conversion of debentures into new debentures or shares involves no cash flow and therefore not considered in a cash flow statement.

Important Notes:

Interim Dividend: The dividend declared and paid by the Board of Directors before its Annual General Meeting during the current year. (Always given as adjustment and is not affected by Proposed Dividend)

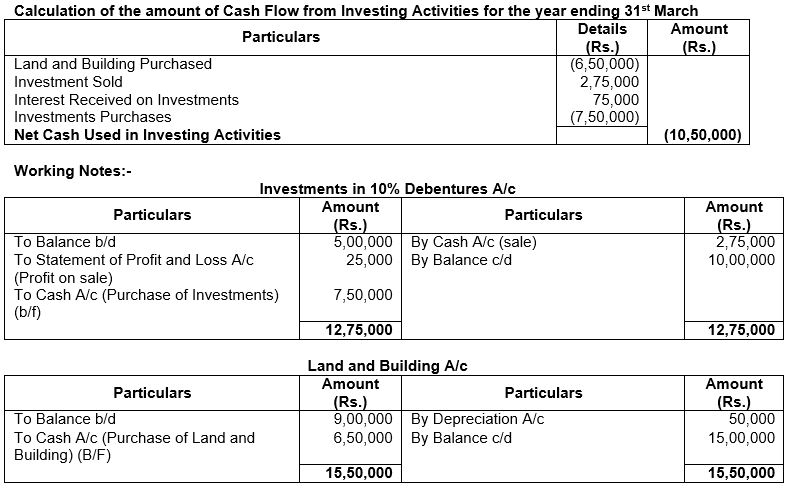

Question 25. From the following details. Calculate Cash Flow from Investing Activities.

Additional Information:

During the year, machine costing Rs. 90,000 with accumulated depreciation of Rs. 60,000 was sold for Rs. 50,000. Patents written off were Rs. 50,000 while a part of patents were sold at a profit of Rs. 40,000.

Answer:

Calculation of the amount of Cash Flow from Investing Activities:

About Solution:

Cash Flow Statement deals with flow of cash which includes cash equivalents as well as cash. This statement is additional information to the users of Financial Statements. The statement shows the incoming and outgoing of cash. The statement assesses the capability of the enterprise to generate cash and utilize it.

Things to Remember:

It is useful in estimating claims on cash flows by lenders of funds in future and therefore, are shown separately.

Important Notes:

It is computed by analyzing change in Equity and Preference Share Capital, Debentures and other borrowings. It also takes into consideration the amounts paid on account of interest (only in case Of non-financing companies) and dividend (all types of companies).

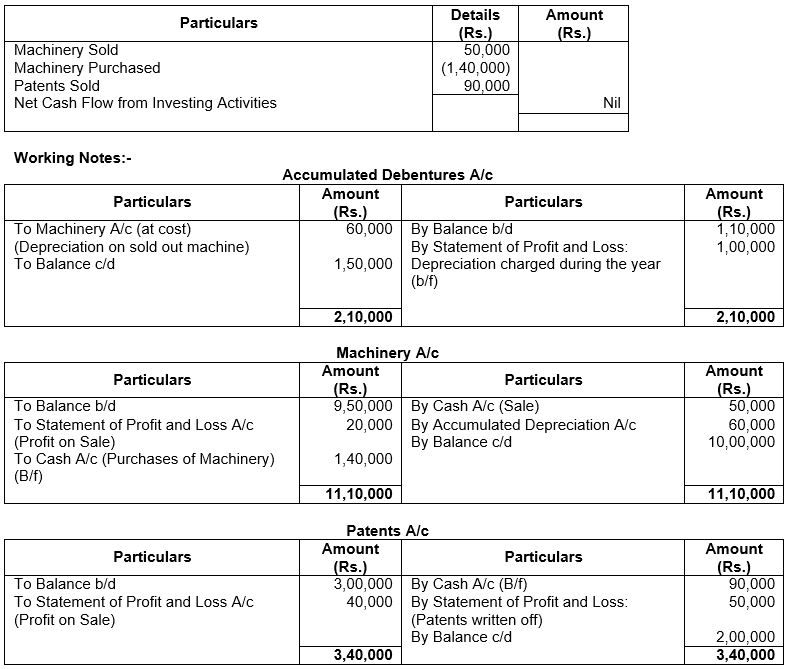

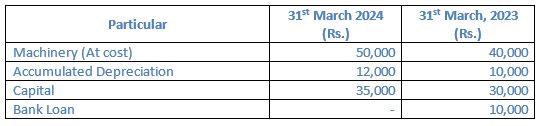

Question 26. Welprint Ltd. has given the following information:

Rs.

Machinery as on 1st April, 2023 50,000

Machinery as on 31st March, 2024 60,000

Accumulated Depreciation on 1st April, 2023 25,000

Accumulated Depreciation on 31st March, 2024 15,000

During the year, a machine costing Rs. 25,000 (accumulated depreciation thereon Rs. 15,000) was sold for Rs. 13,000. Calculate Cash Flow from Investing Activities on the basis of the above information.

Answer:

About Solution:

Cash and Relevant Terms as per AS-3 (Revised)

As per AS-3 (revised) issued by the Accounting Standards Board

(a) Cash fund:

Cash Fund includes

(i) Cash in hand (ii) Demand deposits with banks, and (iii) cash equivalents.

(b) Cash equivalents are short-term, highly liquid investments, readily convertible into cash and which are subject to insignificant risk of changes in values.

Things to Remember:

If shares or debentures are issued at a premium, Cash Flow Statement shows total cash received from the issue that includes both nominal value and the premium.

Important Notes:

Any amount of share issue expenses and underwriting commission is a cash outflow from financing activities

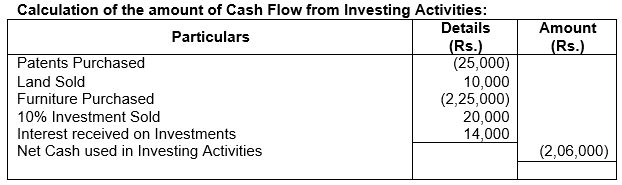

Question 27. From the following extracts of a company, calculate Cash Flow from Investing Activities:

Answer:

About Solution:

1. It has been assumed that investments have been sold at the end of the accounting year.

2. Interest received on Investments = 10% of Rs. 2,00,000 – Rs. 6,000 = Rs. 14,000

Things to Remember:

Interest on borrowings: Identify if the percentage Of interest on borrowings is given and add the amount of interest paid to compute Net Profit before Working Capital Changes and show it as an 'Outflow' under Cash Flow from Financing Activities.

Important Notes:

Interest on Investment: Identify if the percentage of interest on Investment is given and deduct the amount of interest received to compute Net Profit before Working Capital Changes and show it as an 'Inflow' under cash Flow from Investing Activities.

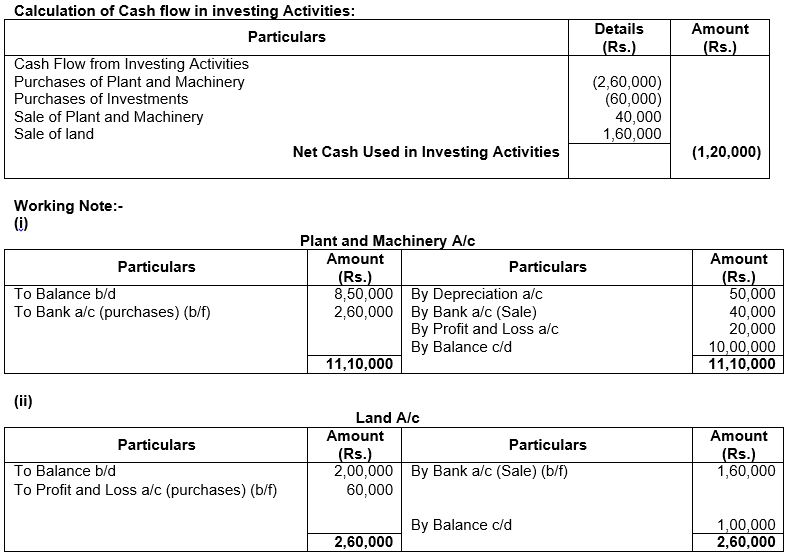

Question 28. From the following information, calculate Cash Flow from Investing Activities

Additional Information:

1. Depreciation charged on Plant and Machinery Rs. 50,000.

2. Plant and Machinery with a Book Value of Rs. 60,000 was sold for Rs. 40,000.

3. Land was sold at a profit of Rs. 60,000.

4. No investment was sold during the year.

Answer:

About Solution:

Cash outflow from investing activities are:

1. Purchase of fixed assets i.e. land, Building, furniture, machinery etc.

2. Purchase of Intangible assets i.e. goodwill, trade mark etc.

3. Purchase of shares and debentures.

4. Purchase of Government Bonds Loan made to outsiders.

Things to Remember:

Balance in Statement of Profit and Loss: Identify whether the balance in the Statement of Profit and Loss is positive or negative. When the opening balance is negative, it is to be added to the closing balance and when the opening balance is positive, it is to be deducted from the closing balance.

Important Notes:

Balance of Other Reserves: Identify whether the balances of other reserves have increased or decreased. When the increase is due to appropriation from Surplus, i.e., Balance in Statement of Profit and Loss, it is to be added to compute Net Profit before tax and Extraordinary Items.

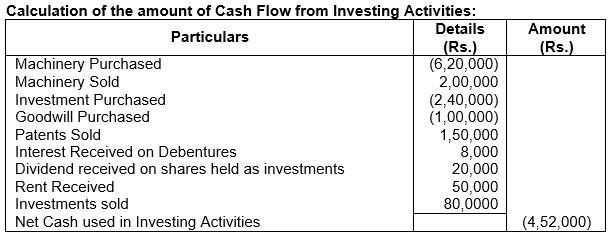

Question 29. From the following particulars, calculate Cash Flow from Investing Activities:

Additional Information:

1. Interest received on debentures held as investment Rs. 8,000.

2. Interest paid on debentures issued Rs. 20,000.

3. Dividend received on shares held as investment Rs. 20,000.

4. Dividend paid on Equity Share Capital Rs. 30,000.

5. A plot of land was purchased out of the surplus funds for investment purposes and was let out for commercial use. Rent received Rs. 50,000 during the year.

Answer:

About Solution:

Financing activities are those activities that are related to capital or long term funds of an enterprise. These activities results in the change in the capital and borrowed funds.

Things to Remember:

Receipt Of dividend can be an operating activity for a financial company as it is a principal revenue generating activity.

Important Notes:

A Cash Flow Statement is a statement that provides information about the historical changes in Cash & Cash Equivalents of an enterprise by classifying cash flows into Operating, Investing and Financing Activities.

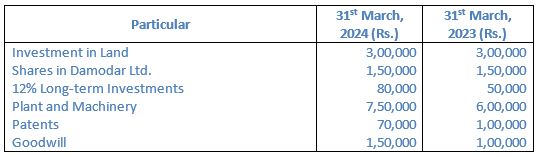

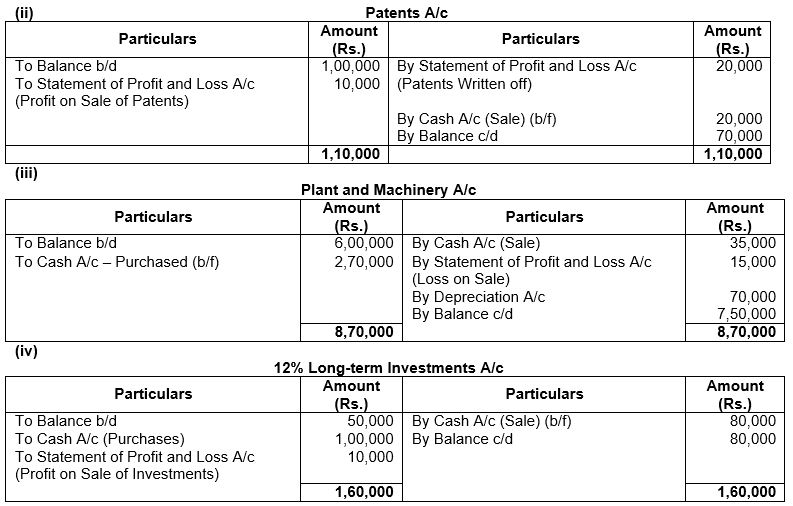

Question 30. Calculate Cash Flow from Investing Activities from the following information:

Additional Information:

1. A piece of land was purchased as an investment out of surplus. It was let out for commercial purpose and the rent received was Rs. 20,000.

2. Dividend received from Damodar Ltd. @ 12%.

3. Patents written off to the extent of Rs. 20,000. Some patents were sold at a profit of Rs. 10,000.

4. A machine costing Rs. 80,000 (depreciation provided thereon Rs. 30,000) was sold for Rs. 35,000. Depreciation charged during the year was Rs. 70,000.

5. During the year 12% investments were purchased for Rs. 1,00,000 and some investments were sold at a profit of Rs. 10,000. Interest on investments for the year was duly received.

Answer:

Things to Remember:

Non-cash Expenses: Identify if non-cash expenses are given and add them to compute Net Profit before Working Capital Changes.

Important Notes:

Non-operating Expenses: Identify if non-operating expenses are given and add them to compute Net Profit before Working Capital Changes. It will be shown as an outflow under appropriate head.

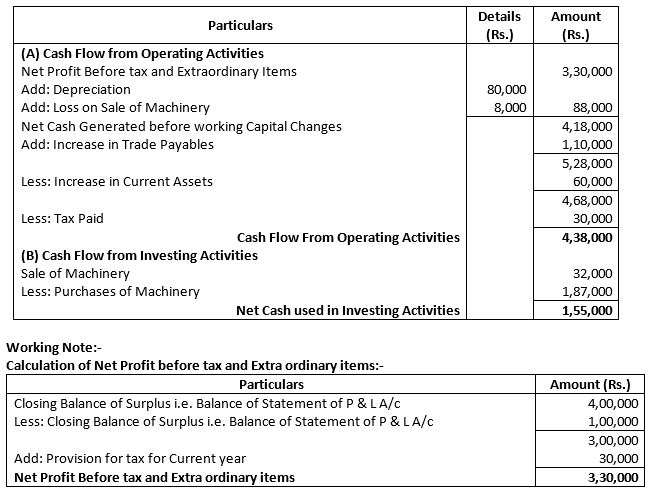

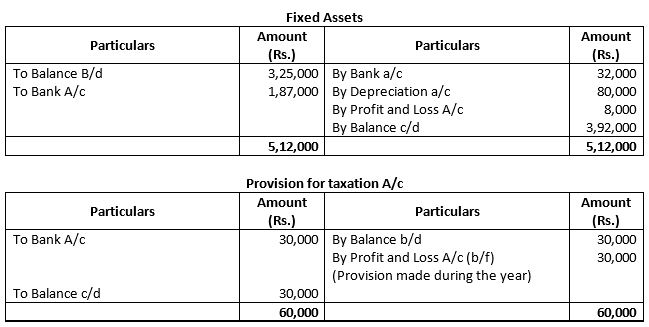

Question 31. From the following information, Calculate cash Flow from Operating Activities and Investing Activities:

Additional Information:

1. Depreciation of ₹ 80,000 was provided and a machine costing ₹ 1,05,000 (Depreciation provided thereon ₹ 65,000) was sold at a loss of ₹ 8,000.

2. Tax paid during the year ₹ 30,000

Answer:

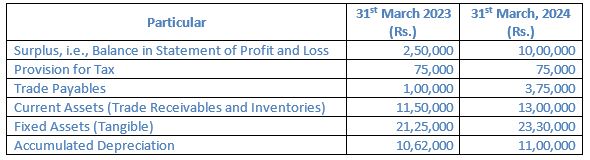

Question 32. From the following information, calculation Cash Flow from Operating Activities and Investing Activities:

Additional Information:

1. A machine having book value of Rs. 1,00,000 (Depreciation provided thereon Rs. 1,62,500) was sold at a loss of Rs. 20,000.

2. Tax paid during the year Rs. 75,000.

Answer:

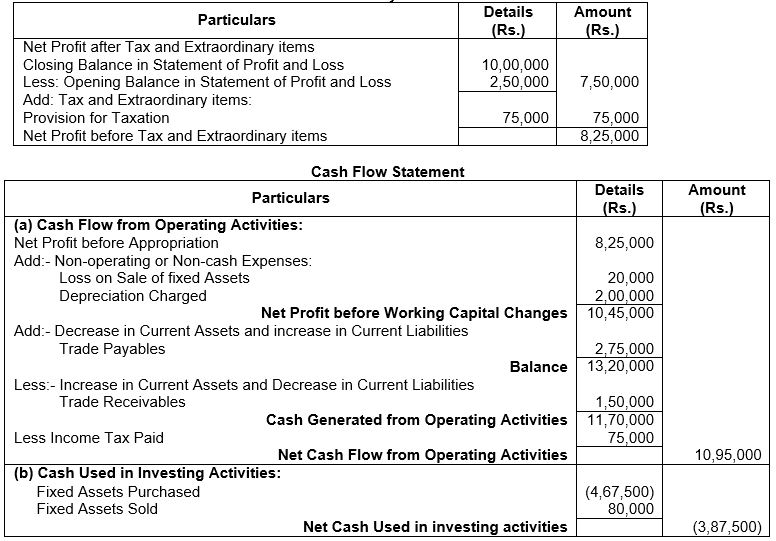

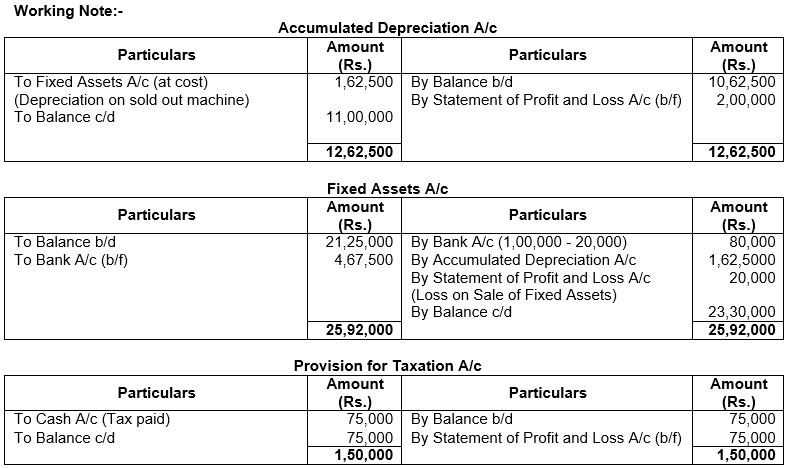

Calculation of Net Profit before tax and Extraordinary items:

About Solution:

Net Profit after Tax and Extraordinary items = Closing Balance of Surplus – Opening Balance of Surplus + Tax

Net Profit after Tax and Extraordinary items = 10,00,000 – 2,50,000 + 75,000

Net Profit after Tax and Extraordinary items = 8,25,000

Things to Remember:

Cash equivalents are investments that are highly liquid in nature and do not change value easily. Cash equivalents are essential for managing short term cash requirements or any such investments. For example:- treasury bills.

Important Notes:

Cash Flows: It is the inflow and outflow of cash and cash equivalents. Cash inflows boost cash balance and cash outflow has a negative impact on cash balance.

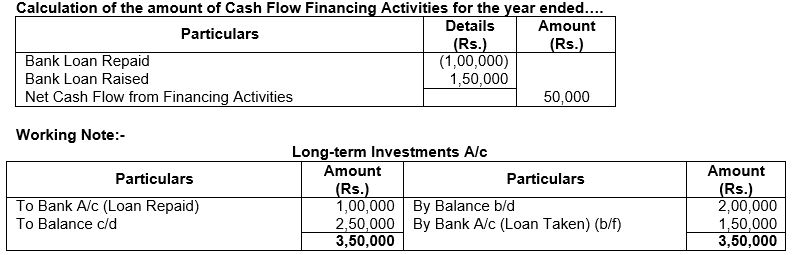

Question 33. From the following information, calculate Cash Flow from Financing Activities:

During the year, the company repaid a loan of Rs. 1,00,000.

Answer:

Things to Remember:

"Cast equivalents" means short term highly liquid investments that are readily convertible into known amount of cash & which are subject to an in significant risk of changes in value.

Important Notes:

The primary purpose of the statement of cash flows is to provide information about cash receipt, cash payments, and the net change in cash resulting from the operating, investing and financing activities of a company during the period.

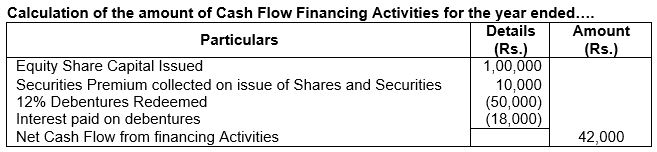

Question 34. From the following information, calculate Cash Flow from Financing Activities:

Additional Information: Interest paid on debentures Rs. 18,000.

Answer:

About Solution:

(i) Equity Share Capital Issued = Rs. 10,00,000 – Rs. 9,00,000 = Rs. 1,00,000

(ii) Securities Premium collected on issue of Shares and Securities = Rs. 2,60,000 – Rs. 2,50,000 = Rs. 10,000

(iii) 12% Debentures = Rs. 1,00,000 – Rs. 1,50,000 = Rs. (50,000)

Things to Remember:

A financial statement that represents the inflow and outflow of cash and cash equivalents of a company is called a cash flow statement. It shows how well a company can manage its cash position and generates enough cash to pay the obligations in the form of debt and also run the operational expenses.

Important Notes:

Three types of activities are defined:

1. Operating Activities

2. Financing Activities

3. Investing Activities

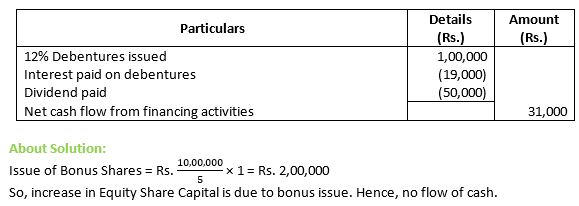

Question 35. XYZ. Ltd. provided the following information, calculate Net Cash Flow from Financing Activities:

Additional Information:

1. Interest paid on debentures Rs. 19,000.

2. Dividend paid in the year Rs. 50,000.

3. During the year, XYZ Ltd. issued bonus shares in the ratio of 5 : 1 by capitalising reserve.

Answer:

Cash Flow from Financing Activities of XYZ Ltd. for the year ending:-

Things to Remember:

There are two methods which are used for preparation of cash flow statement:

1. Direct Method

2. Indirect Method.

Important Notes:

Preparation of Cash Flow Statement using Direct Method has been excluded from the prescribed syllabus. The format is given since the question has not specified the method explicitly. Students can refer to the direct method for the knowledge purpose.

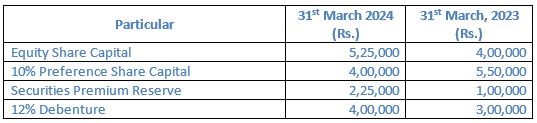

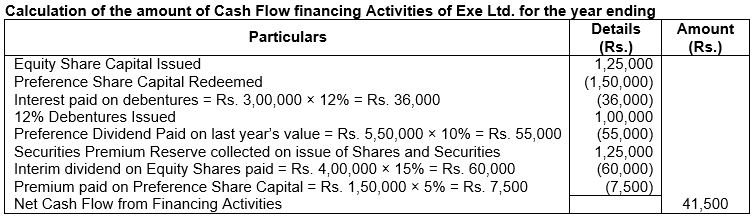

Question 36. From the following extracts of Balance Sheet of Exe Ltd., calculate Cash Flow from Financing Activities:

Additional Information:

1. Equity Shares were issued on 31st March, 2024.

2. Interim dividend on Equity Shares was paid @ 15%.

3. Preference Shares were redeemed on 31st March, 2024 at a premium of 5%. Premium paid was debited to Statement of Profit and Loss.

4. 12% Debentures of face value Rs. 1,00,000 were issued on 31st March, 2024

Answer:

About Solution:

(i) Equity Share Capital = 5,25,000-4,00,000=1,25,000

(ii) 10% Preference Share Capital = 4,00,000-5,50,000=(1,50,000)

(iii) Securities Premium Reserve = 2,25,000-1,00,000=1,25,000

12% Debenture = Rs. 4,00,000 – Rs. 3,00,000=Rs. 1,00,000

Things to Remember:

To determine inflow and outflow of cash and the cash equivalents obtained from the different kind of activities.

Important Notes:

To seek out various reasons responsible for change in cash balances during the accounting period.

Question 37. From the following information, calculate Cash Flow from Investing and Financing Activities:

During the year, a machine costing Rs. 10,000 was sold at a loss ofRs. 2,000. Depreciation on machinery charged during the year amounted to Rs. 6,000.

Answer:

Things to Remember:

It helps in depicting the position of the company in terms of liquidity and solvency.

Important Notes:

It also helps in determining the requirement and the corresponding availability of cash for business in future.

Question 38. From the following information, Calculate (a) Cash Flow from Investing Activities; and (b) Cash Flow from Financing Activities:

Additional Information:

1. Depreciation charged on Plant and Machinery was ₹ 50,000.

2. Plant and Machinery of book value ₹ 60,000 was sold for ₹ 40,000.

3. Land was sold at a gain of ₹ 60,000.

4. Preference Shares were redeemed on 31st March, 2024 at a premium of 5%.

5. Dividend on Equity Shares and Preference Shares for the year ended 31st March, 2023 was Nil and for the year ended 31st March, 2024 Proposed Dividend on Equity Shares was 10%.

6. Fresh issue of Equity Shares was on 1st April, 2023.

Answer:

About Solution:

Cash Flow from Investing Activities: These include all activities related to the acquisition and disposal of Long-term Assets and other investments which are not classified as cash equivalents.

Things to Remember:

All cash inflows and outflows relating to the fixed assets, shares and related instruments of other enterprise including loans and advances to third parties and their repayments are classified under Investing Activities.

Important Notes:

It shows the extent to which investments have been made for resources that generate revenue and cash flows in future.

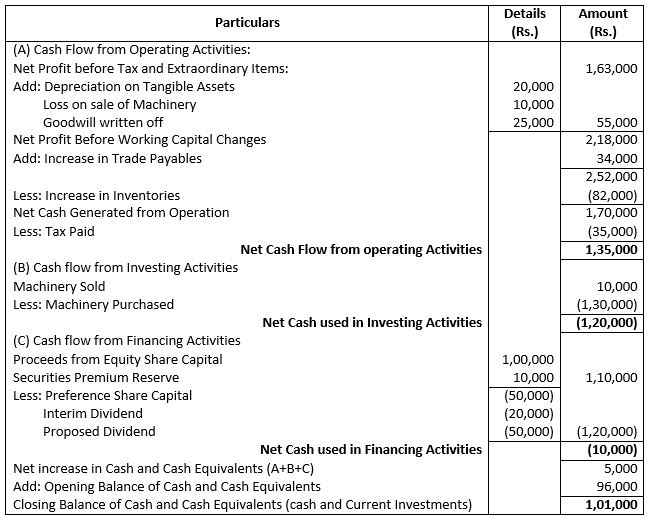

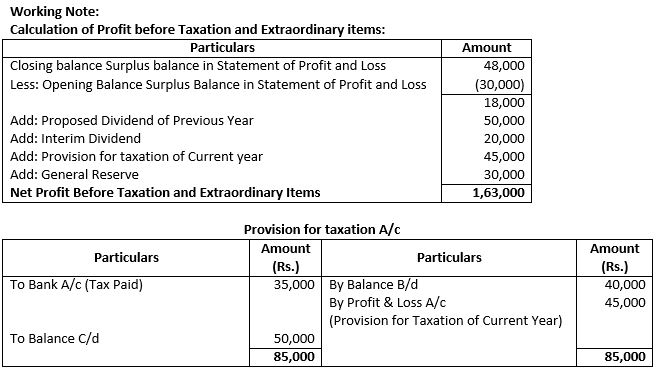

Question 39. From the following information, prepare Cash Flow Statement:

Answer:

About Solution:

Preparation of Cash Flow Statement using Direct Method has been excluded from the prescribed syllabus. The format is given since the question has not specified the method explicitly. Students can refer to the direct method for the knowledge purpose.

Things to Remember:

Loans and cash advances that are made to third parties (does not includes loans and advances made by financial enterprises.

Important Notes:

Cash receipts obtained from any insurance company for a property that is involved in accident.

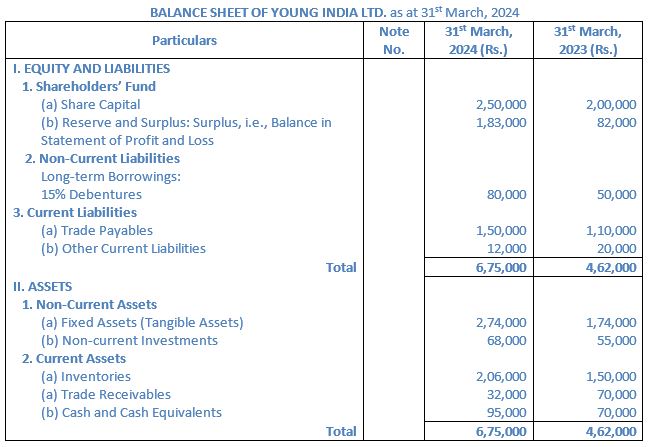

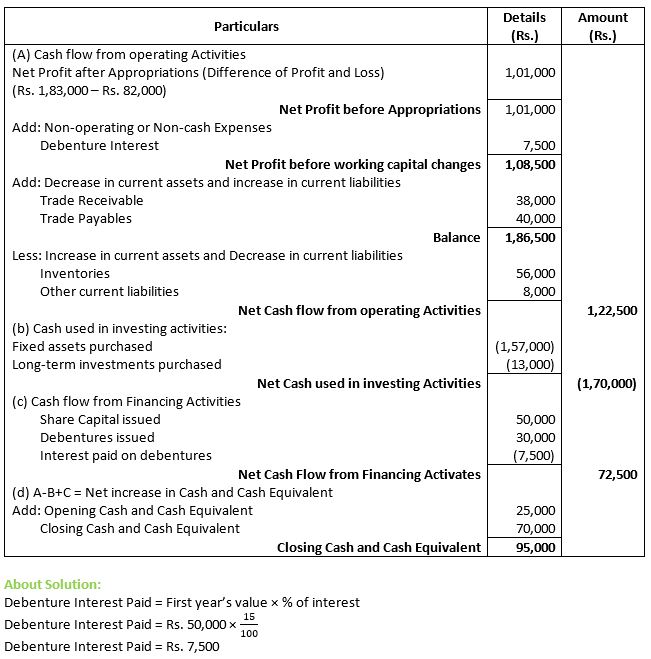

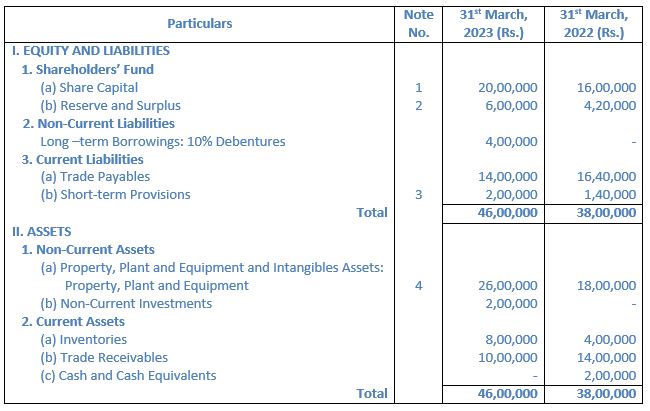

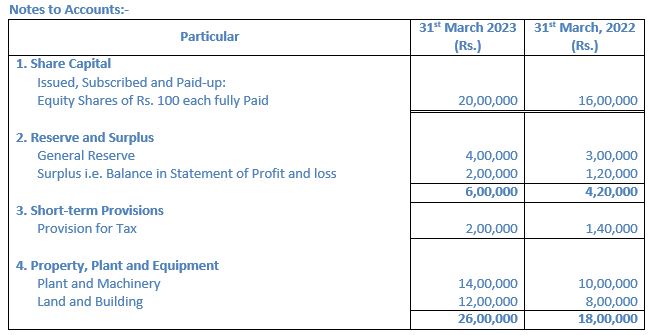

Question 40. From the following Balance Sheet of Young India Ltd., prepare Cash Flow Statement:

Answer:

Cash Flow Statement for the year ended 31st March

Things to Remember:

Cash receipts that are obtained for repayment of loans and cash advances made to third parties.

Important Notes:

Any type of income that is obtained from fixed assets like interest, dividend and rent (not in case of financial enterprises).

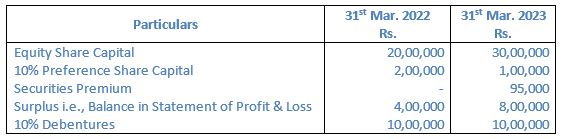

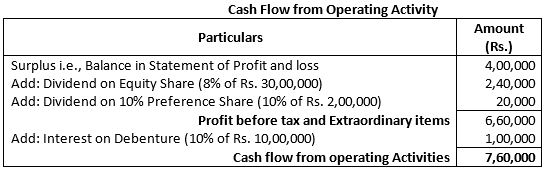

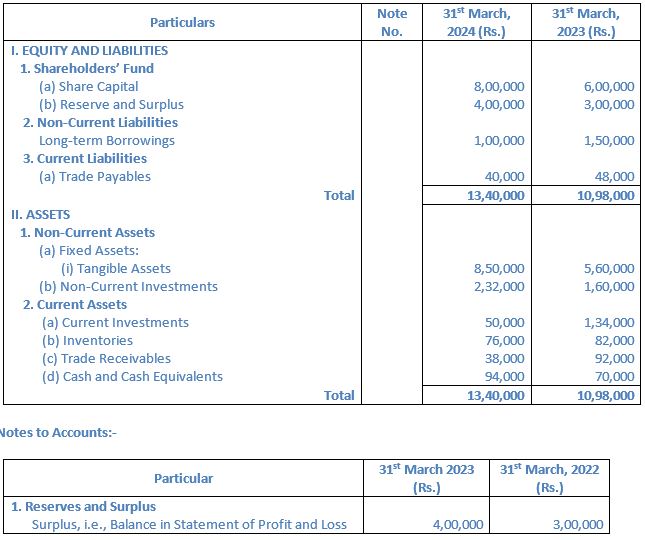

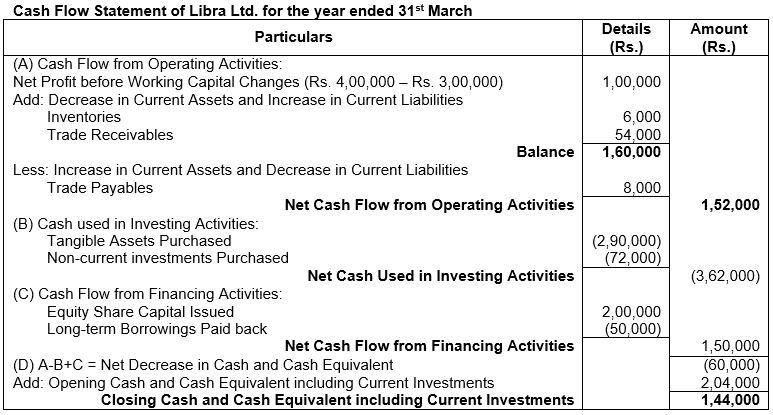

Question 41. Prepare a Cash Flow Statement on the basis of the information given in the Balance Sheet of Libra Ltd. as at 31st March, 2022 and 31st March 2023:

Answer:

About Solution:

Cash Flow: A cash flow is the inflow (receipt) and the outflow (payment) of Cash and Cash equivalents, where cash and cash equivalents include Cash, Bank Balance, Marketable Securities, etc. (unless specified otherwise, Current Investments are considered as Marketable Securities).

Things to Remember:

Cash Flow Statement: It is a statement that shows the inflows and the outflows Of Cash and Cash Equivalents during the period. Inflows are those transactions that increase the Cash

Important Notes:

Cash Equivalents and outflows are those transactions that decrease the Cash and Cash Equivalents. Such statement is prepared in accordance with the Accounting Standard-3 (Revised) on Cash Flow Statement.

Question 42. The Balance Sheet of Bright Ltd. as at 31st March, 2023 is as follows:

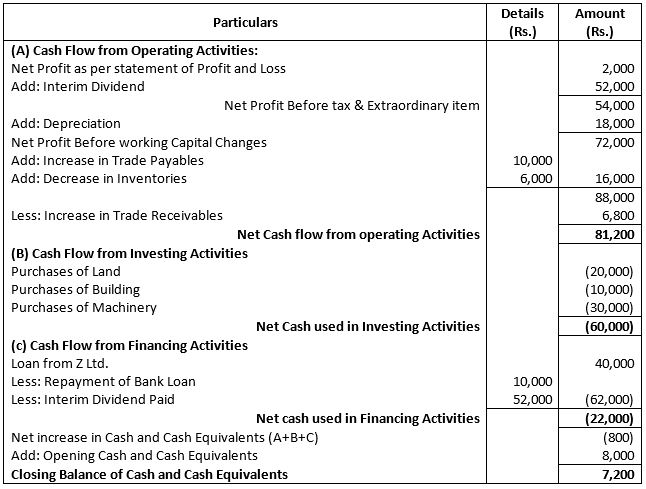

Additional Information: During the year Rs. 52,000 were paid as interim dividend.

Prepare Cash Flow Statement.

Answer:

Cash Flow Statement of Solar Power Limited for the year ended 31st March

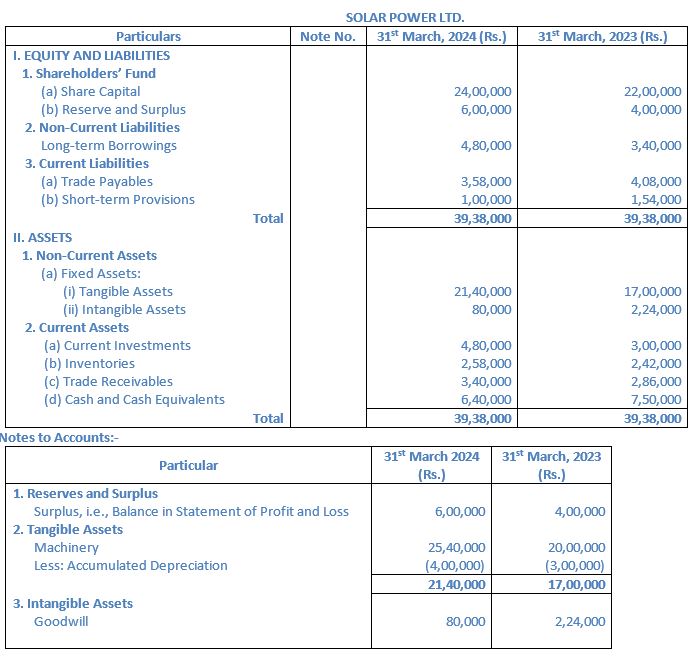

Question 43. Following are the Balance Sheets of Solar Power Ltd. as at 31st March, 2014 and 2013:

Additional Information:

During the year, a piece of machinery costing Rs. 48,000 on which accumulated depreciation was Rs. 32,000 was sold for Rs. 12,000. Prepare Cash Flow Statemen

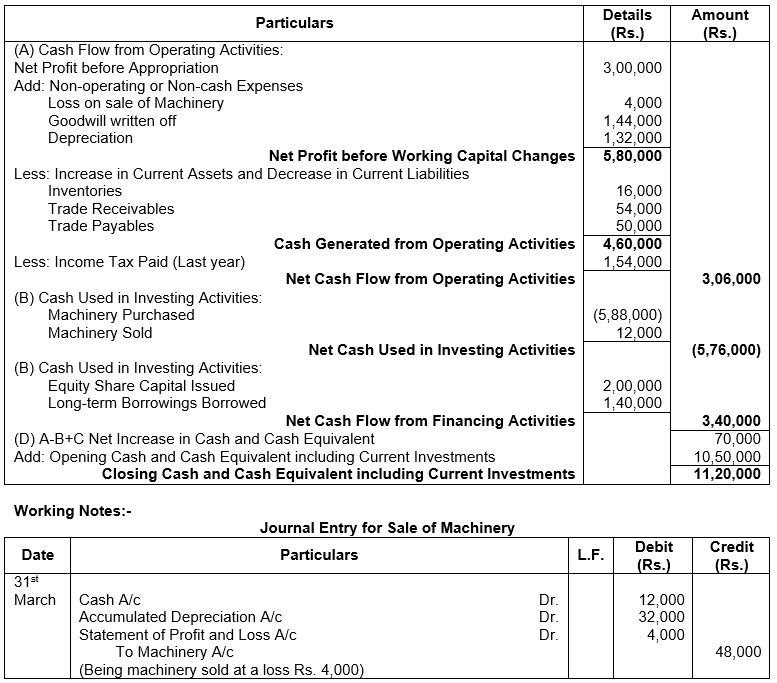

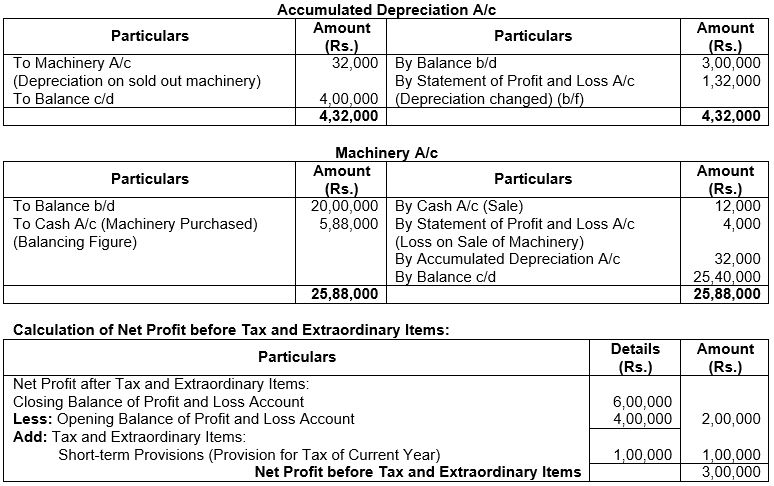

Answer:

About Solution:

Net Profit after Tax and Extraordinary Items = Closing Balance of Profit and Loss – Opening Balance of Profit and Loss + Tax

Net Profit after Tax and Extraordinary Items = Rs. 6,00,000 – Rs. 4,00,000 + Rs. 1,00,000

Net Profit after Tax and Extraordinary Items = Rs. 3,00,000

Things to Remember:

As per this accounting standard, cash flows are showed under the following 3 heads:

a) Cash Flow from Operating Activities.

b) Cash Flow from Investing Activities.

c) Cash Flow from Financing Activities.

Important Notes:

Cash Flow from Operating Activities: Activities related to core or principal revenue generating activities of an enterprise.

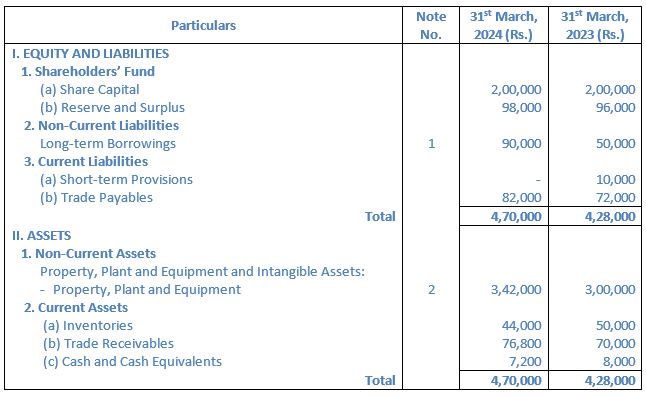

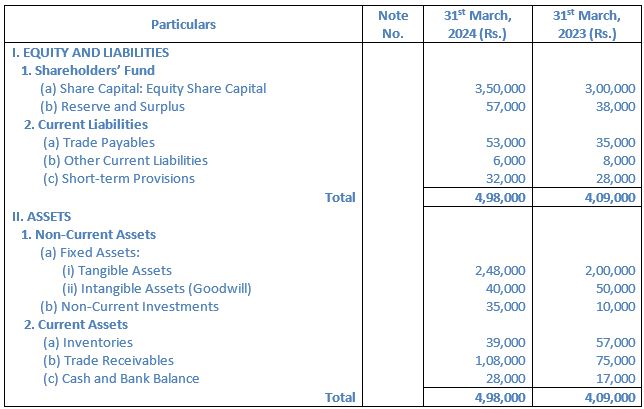

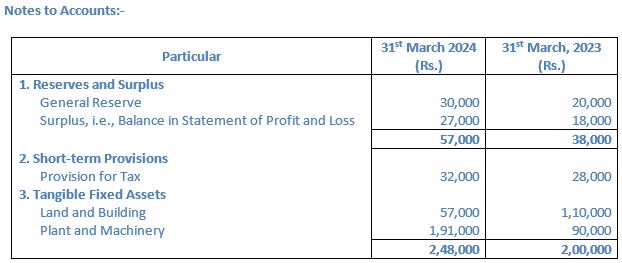

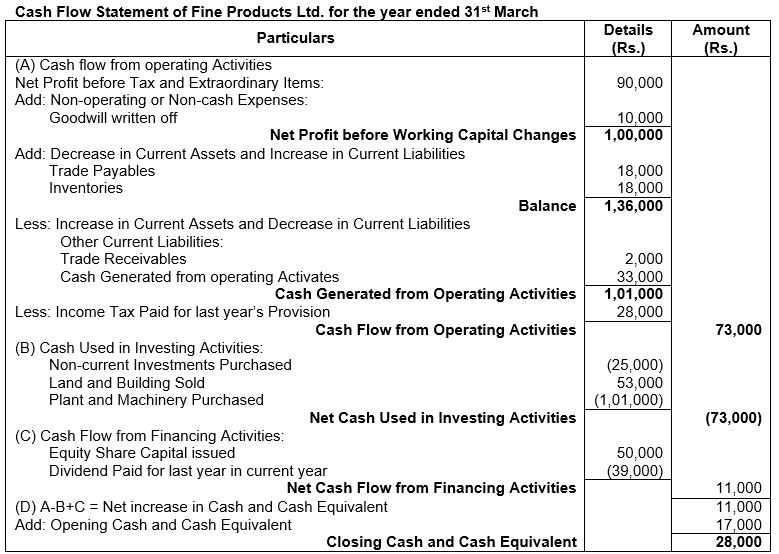

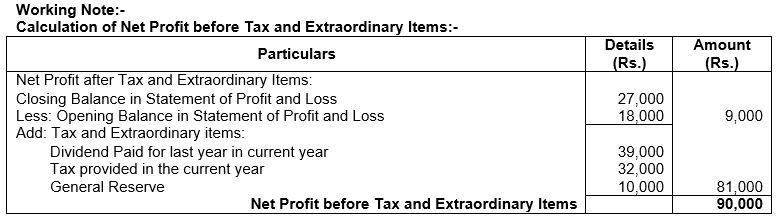

Question 44. Following is the Balance Sheet of Fine Products Ltd. as at 31st March, 2024:

Note: Proposed dividends on equity for the years ended 31st March, 2023 and 2024 are Rs. 39,000 and Rs. 45,000 respectively. You are required to prepare Cash Flow Statement for the year ended 31st March, 2024.

Answer:

About Solution:

Net Profit after Tax and Extraordinary Items = Closing Balance in Profit and Loss – Opening Balance in Profit and Loss + Tax + Dividend Paid + General Reserve

Net Profit after Tax and Extraordinary Items = Rs. 27,000 – Rs. 18,000 + Rs. 32,000 + Rs. 39,000 + Rs. 10,000

Net Profit after Tax and Extraordinary Items = Rs. 90,000

Things to Remember:

Cash repayments of the amount borrowed in form of debentures, loans, notes bonds, and other short and long-term borrowings.

Important Notes:

An important point that must be noted is that the purchase and sale of securities, interest paid or received and dividend received is treated as cash flow from operating activities for an investment company. But dividend paid is treated as cash flow from financing activities.

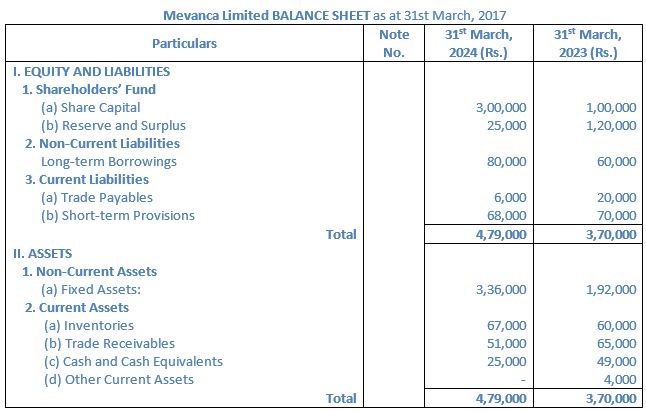

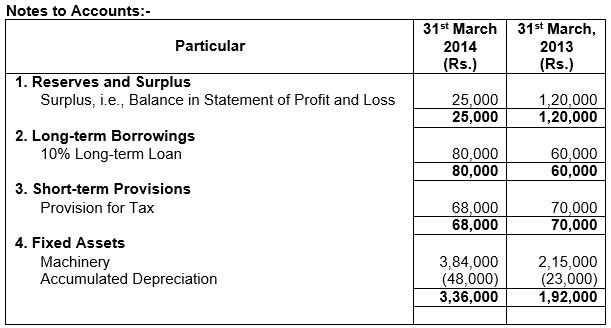

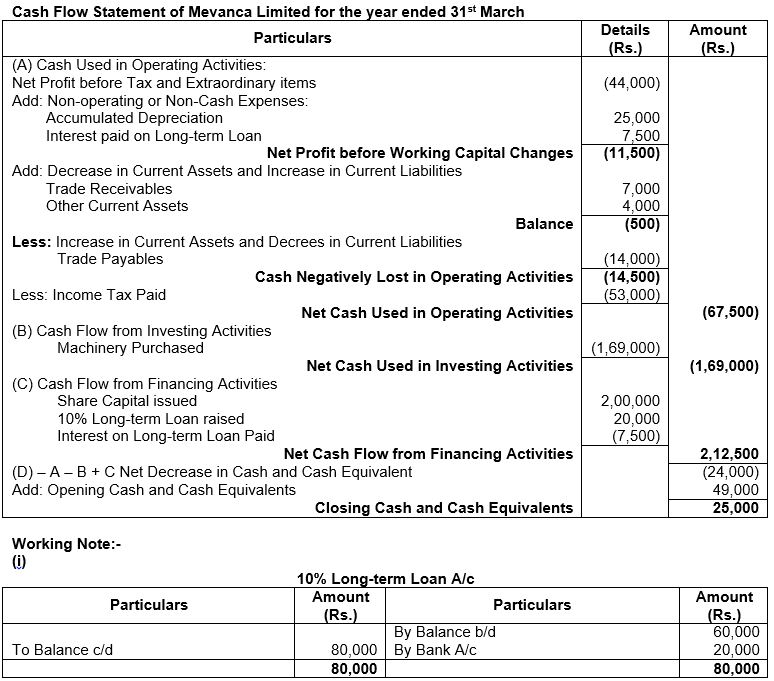

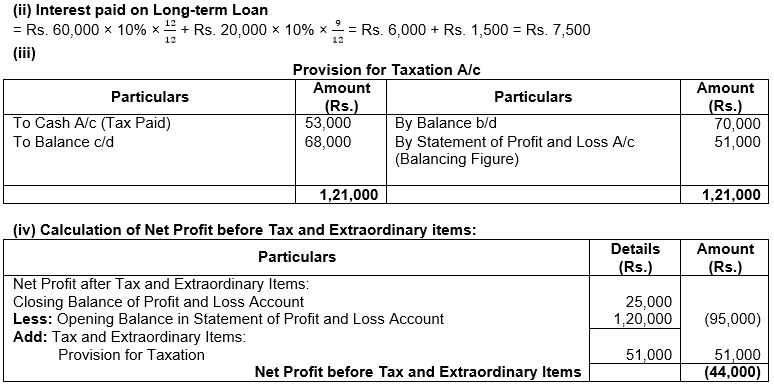

Question 45. Following is the Balance Sheet of Mevanca Limited as at 31st March, 2017:

Additional Information:

(i) Additional loan was taken on 1st July, 2016.

(ii) Tax of Rs. 53,000 was paid during the year.

Prepare Cash Flow Statement

Answer:

About Solution:

Cash Flow from operating Activities:-

(a) Cash sale of goods: Normal business activity of selling Inventories or goods (Cash inflow)

(b) Cash paid to suppliers of raw materials Routine payments for purchasing the goods (Cash outflow)

(c) Cash payment of salaries and wages: Cash payments to employees for their services in the office (Cash outflow)

Things to Remember:

Cash Flow from Investing Activities: Activities related to sale and purchase of long-term fixed assets and investments.

Important Notes:

Cash Flow from Financing Activities: Activities related to capital or long term funds of an enterprise.

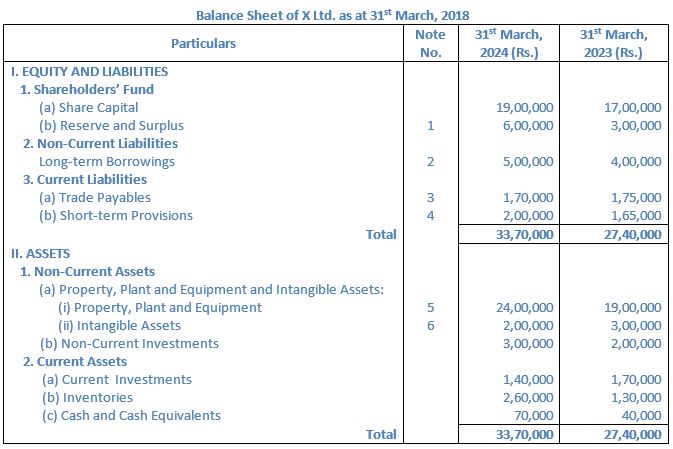

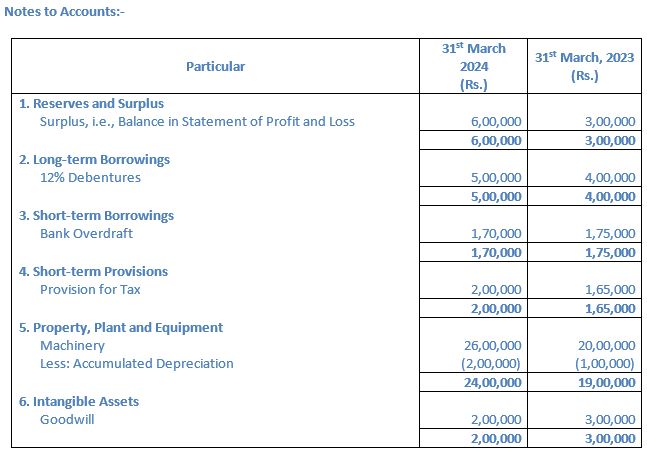

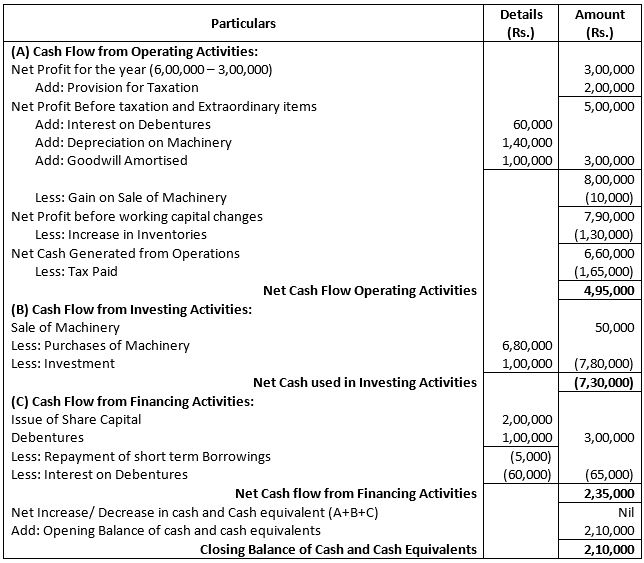

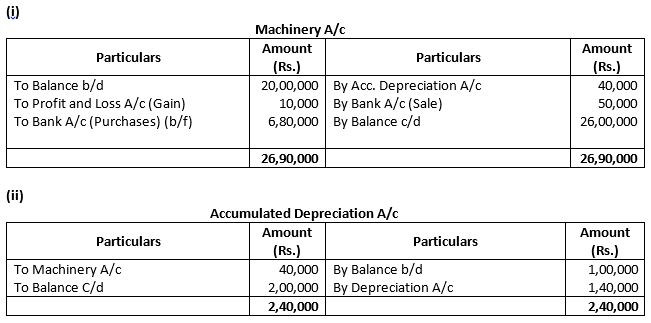

Question 46. Following is the Balance Sheet of X Ltd as at 31st March, 2018:

Additional Information:

(i) Rs. 1,00,000, 12% debentures were issued on 1st April, 2017.

(ii) During the year, a piece of machinery costing Rs. 80,000 on which accumulated depreciation was Rs. 40,000 was sold at a gain of Rs. 10,000.

Prepare a Cash Flow Statement.

Answer:

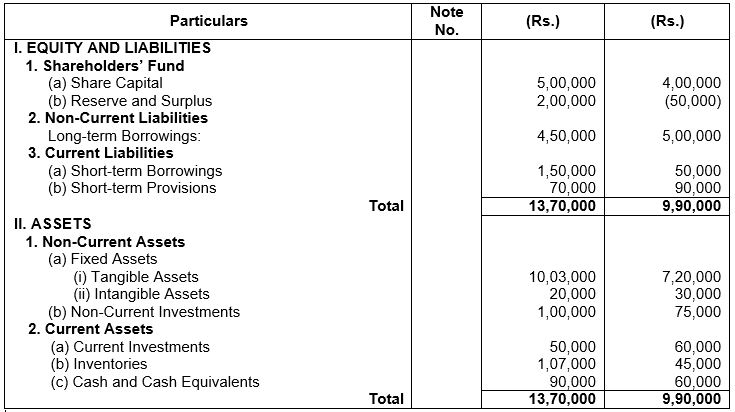

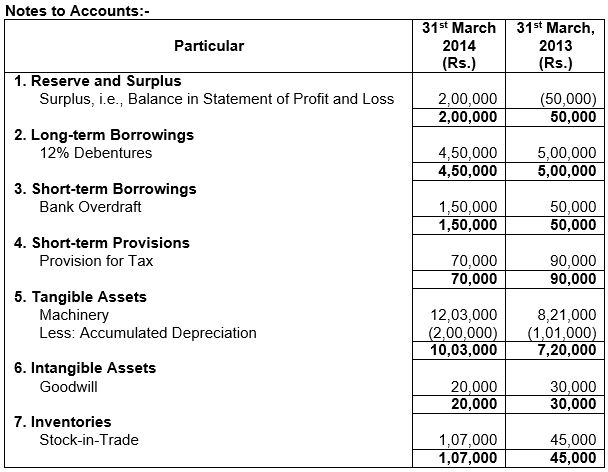

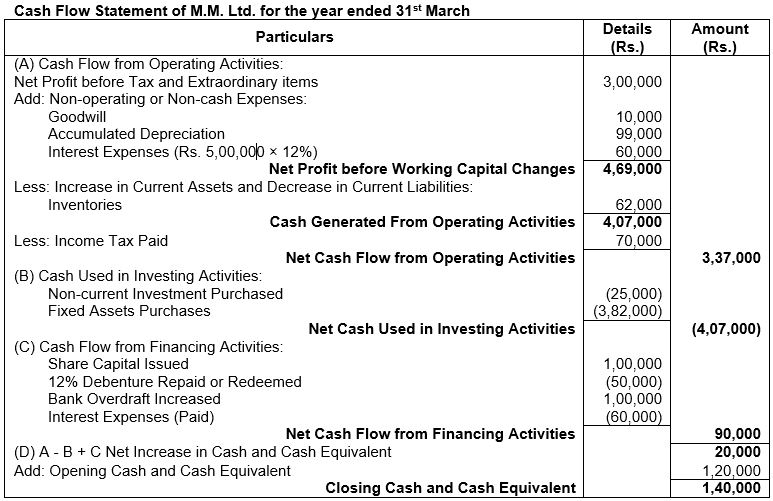

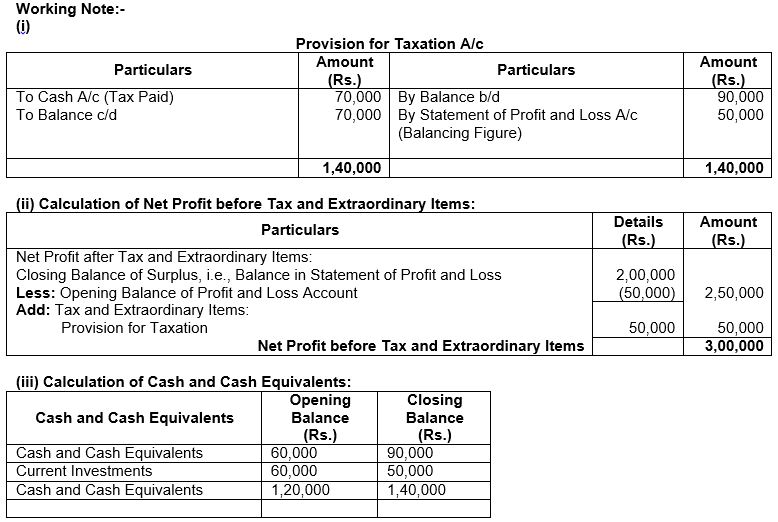

Cash Flow Statement of M.M. Ltd. for the year ended 31st March

About Solution:

Some facts about cash flow statement:

(i) Only listed companies are required to prepare and present Cash flow statement.

(ii) The Accounting period for the Cash Flow Statement is the same for which Profit and Loss Account and Balance Sheet are prepared.

(iii) Cash flow items are as

(a) Cash flow from operating activities

(b) Cash flow from investing activities

(c) Cash flow from financing activities.

Things to Remember:

Income Tax Refund: Deducted from Profits in Operating Activities and Deducted from Income Tax paid.

Important Notes:

Discount Written-off: Added back to Current Year's Profits in Operating Activities

Question 47. Following was the Balance Sheet of M.M. Ltd. as at 31st March, 2015:

Additional Information:

1. 12% Debentures were redeemed on 31st March, 2015.

2. Tax Rs. 70,000 was paid during the year.

Prepare Cash Flow Statement

Answer:

About Solution:

Cash Flow from financing Activities

(a) Cash proceeds from issuing shares at premium: (Cash inflow)

(b) Payment of dividends: It is related to issue of share capital, a (Cash outflow)

(c) Interest paid on debentures: Payment associated with loan capital (Cash outflow)

Things to Remember:

To determine the applications of Cash and Cash Equivalents for operating, investing and financing activities of the enterprise.

Important Notes:

To determine the net change in Cash and Cash Equivalents due to cash inflows and outflows for operating, investing and financing activities of the enterprise that takes place between the 2 balance sheet dates.

Question 48. From the following Balance Sheet and the additional information as at 31st March, 2019, Prepare a Cash Flow Statement when Cash Flow from Financing Activities is ₹ 2,32,000:

Additional Information: Tax Rs. 1,50,000 was paid during the year.

Answer:

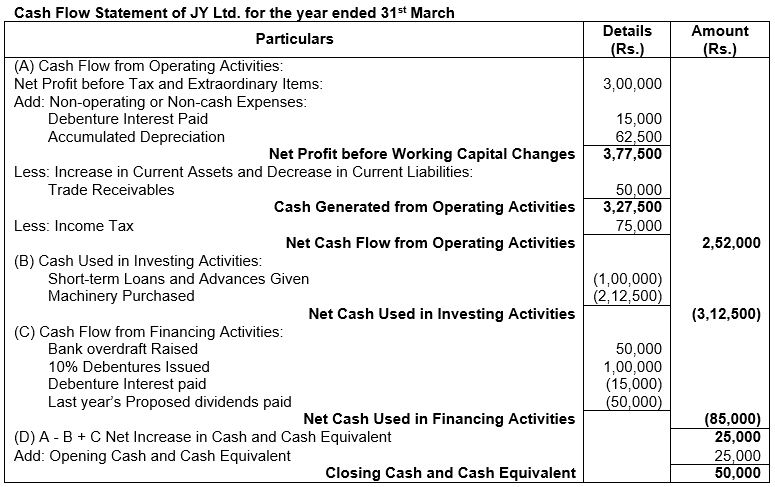

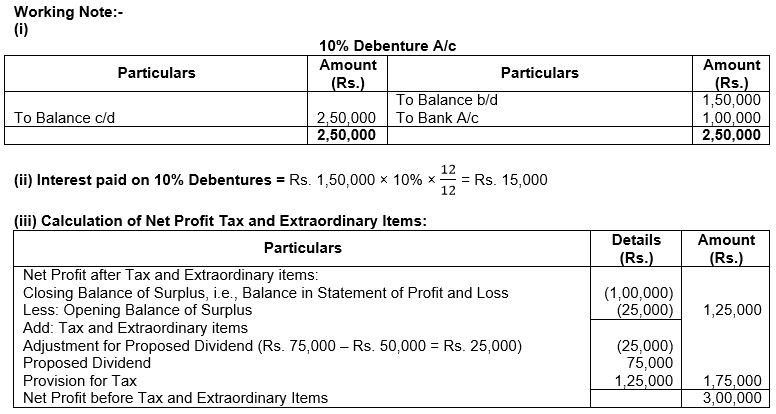

Cash Flow Statement of JY Ltd. for the year ended 31st March

Question 49. From the following Balance Sheet of JY Ltd. as at 31st March 2023, prepare a Cash Flow Statement:

Note: Proposed Dividend for the years ended 31st March, 2016 and 2017 are Rs. 50,000 and Rs. 75,000 respectively.

Additional Information: Rs. 1,00,000, 10% Debentures were issued on 31st March, 2017

Answer:

About Solution:

Provision for Taxation is a non-operating expenses or an item of appropriation in the Income statement/Profit and Loss Account and therefore should not be allowed to reduce the cash provided from operating activities. Hence, if the profit is given after tax and the amount of the provision for tax made during the year is given, the same would be added back to the current year profit figure.

Things to Remember:

To take dividend decisions: In order to declare or approve the dividends, every enterprise should comply with the prescribed provisions e.g., depositing the amount of dividend in a separate bank, etc. Accordingly, to identify whether the enterprise has sufficient funds for such compliance cash flow statement is referred by the management. Also, it helps in deciding how much dividend the enterprise should pay during a particular year.

Important Notes:

Non-cash transactions are not shown: It takes into consideration only cash inflows and cash outflows. Non-cash transactions are not considered for preparation of cash flow statement.

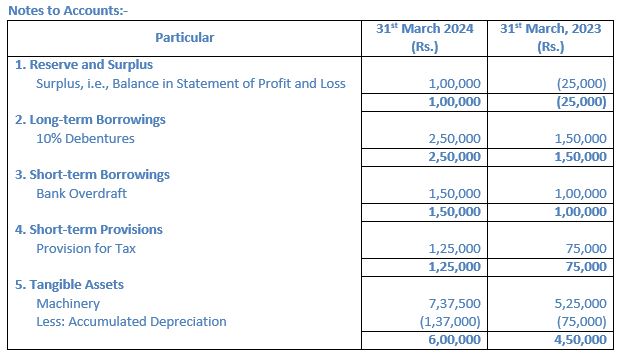

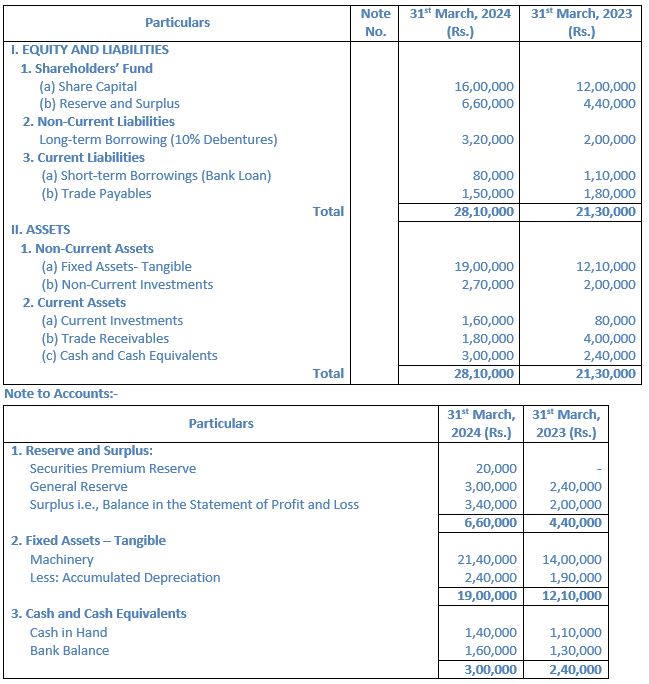

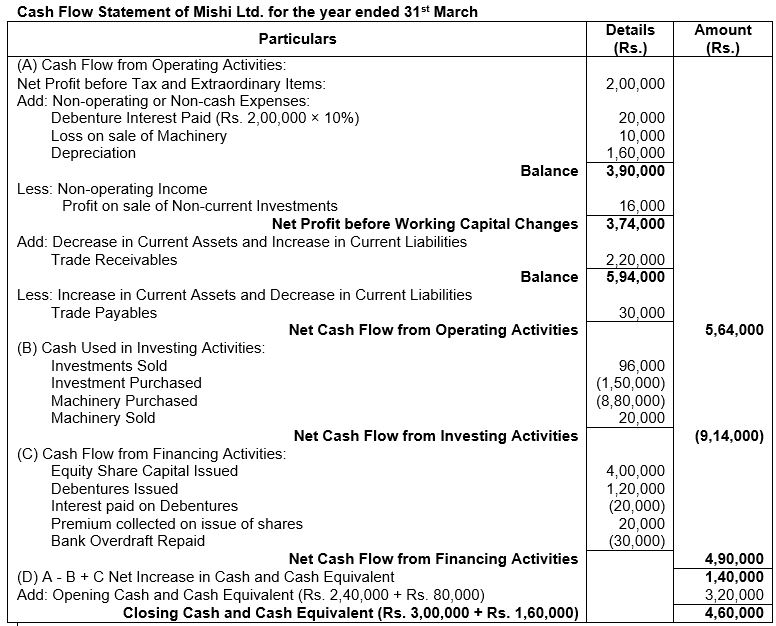

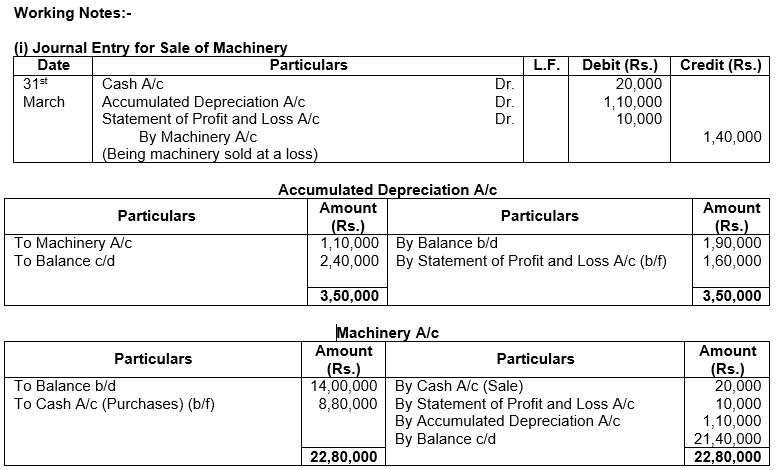

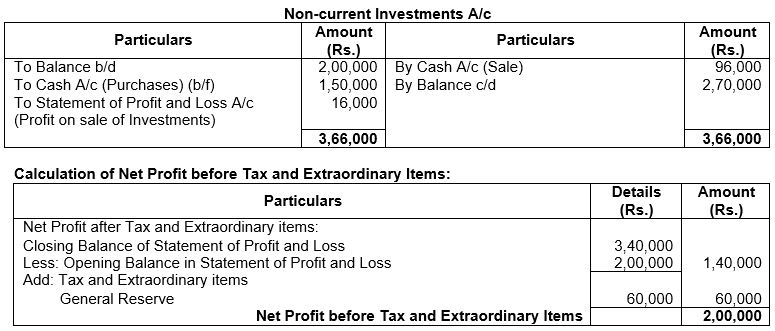

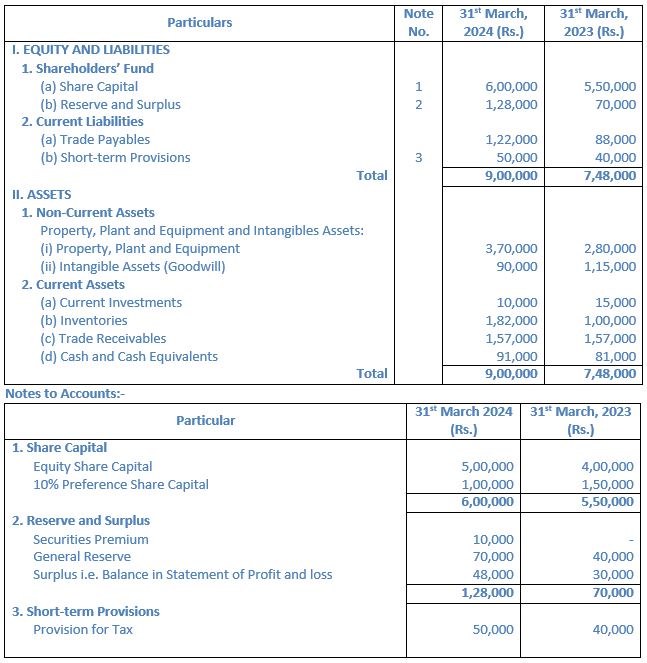

Question 50. From the following Balance Sheet of Mishi Ltd. as at 31st March, 2024, prepare Cash Flow Statement:

Additional Information:-

(i) During the year, Machinery costing Rs. 1,40,000 (accumulated depreciation provided thereon Rs. 1,10,000) was sold for Rs. 20,000.

(ii) During the year, Non-current Investments costing Rs. 80,000 were sold at a profit ofRs. 16,000

Answer:

About Solution:

Calculation of Net Profit before tax and extraordinary items:-

Net Profit before Tax and Extraordinary Items = Closing Balance of Statement of Profit and Loss – Opening Balance in Statement of Profit and Loss + Tax and Extraordinary items

Net Profit before Tax and Extraordinary Items =Rs. 3,40,000 – Rs. 2,40,000 + Rs. 60,000

Net Profit before Tax and Extraordinary Items =Rs. 2,00,000

Things to Remember:

Transactions not regarded as Cash Flow: These are the transactions that are mere movements in between the items of Cash and Cash Equivalents. This includes cash deposited in bank, cash withdrawn from the bank and purchase or sale of marketable securities.

Important Notes:

Non-cash transactions: These are the transactions in which the inflow or outflow Of Cash or Cash Equivalent does not take place. Therefore, these non-cash transactions are not considered while preparing the Cash Flow Statements. These transactions include depreciation, amortization, issue of bonus, etc.

Question 51. Following is the Balance Sheet of Sonal Ltd:

Additional Information:

1. Proposed dividend for the years ended 31st March, 2023 and 2022 were ₹ 60,000 and ₹ 50,000 respectively.

2. A machine costing ₹ 50,000 (depreciation provided thereon ₹ 30,000) was sold for ₹ 10,000.

3. Depreciation charged during the year was ₹ 20,000.

4. Interim dividend paid ₹ 20,000.

5. Income Tax paid ₹ 35,000

Answer:

About Solution:

Cash flow from operating activities are primarily derived from the principal revenue generating activities of the enterprise. A few items of cash flows from operating activities are:

(i) Cash receipt from the sale of goods and rendering services.

(ii) Cash receipts from royalties, fee, Commissions and other revenue.

(iii) Cash payments to suppliers for goods and services.

(iv) Cash payment to employees

(v) Cash payment or refund of Income tax.

Things to Remember:

Discount Allowed During the Year: Net Proceeds (after discount) Shown as Cash from Financing Activities.

Important Notes:

Steps for Preparing Cash Flow Statement:

Step 1: Compute cash flow from Operating Activities.

Step 2: Compute cash flow from Investing Activities.

Step 3: Compute cash flow from Financing Activities.

Step 4: Adding Step 1, Step 2 and Step 3 above, compute the net increase or decrease in Cash and Cash Equivalents.

Step 5: Amount computed in Step 4 is to be added to the balance Of Cash and Cash Equivalents in the beginning of the year.

Step 6: Adding Step 4 and Step 5 will give the balance of Cash and Cash Equivalents at the end of the year which will match the balance as per Balance Sheet.

Question 52. Balance Sheet of Grow More Ltd. as at 31st March, 2023:

Additional Information:

1. Depreciation @ 25% was charged on the opening value of Plant and Machinery.

2. During the year one old machine costing ₹ 1,00,000 (written Down Value ₹ 40,000) was sold for ₹ 70,000.

3. ₹ 1,00,000 was paid as income tax during the year.

4. Proposed dividend for the year ended 31st March, 2023 was ₹ 4,00,000 and for the year ended 31st March, 2022 was ₹ 2,00,000.

5. During the current year new debentures were issued on 1st October, 2022.

Answer:

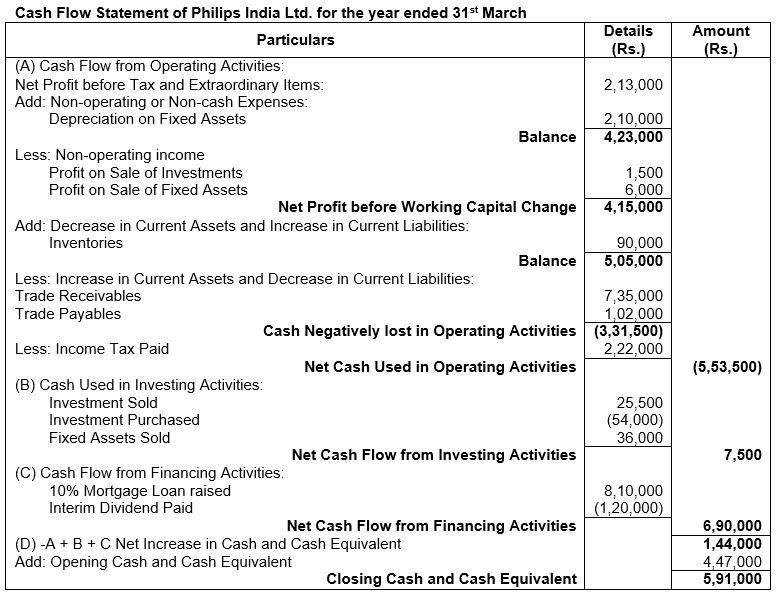

Question 53. Following is the summarised Balance Sheet of Philips India Ltd. as at 31st March 2018:

Additional Information:

1. Investments costing Rs. 24,000 were sold during the year for Rs. 25,000.

2. Provision for Tax made during the year was Rs. 27,000.

3. During the year, a part of the Fixed Assets costing Rs. 30,000 was sold for Rs. 36,000. The profits were included in the Statement of Profit and Loss.

4. The Interim Dividend paid during the year amounted to Rs. 1,20,000.

You are required to prepare Cash Flow Statement.

Answer:

About Solution:

Cash outflow from financing activities are:

a) Payment of dividends to shareholders

b) Redemption or repayment of loans i.e. debentures and bonds

c) Redemption of preference share capital

d) Buy back of equity shares.

Things to Remember:

Historical in Nature: Cash flow statement is prepared based on the cash inflows and outflows that have already taken place during the year and hence, it is historical in nature.

Important Notes:

Assessment of Liquidity: Cash flow statement takes into consideration all the transactions of cash and cash equivalents. This cash and cash equivalents are just one of the components in the current assets which determine the liquidity position of the enterprise. Therefore, cash flow statement alone cannot help in determining the liquidity position of the enterprise.

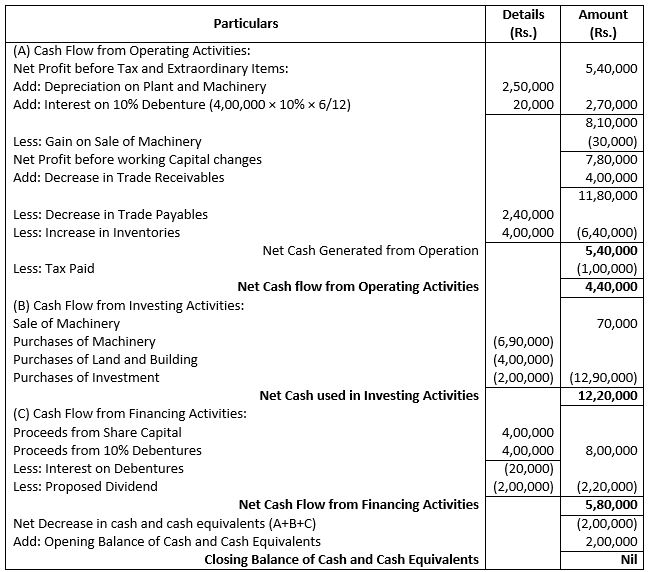

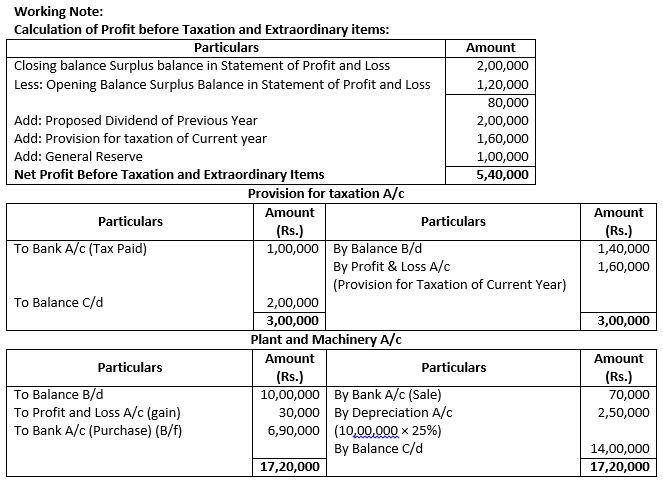

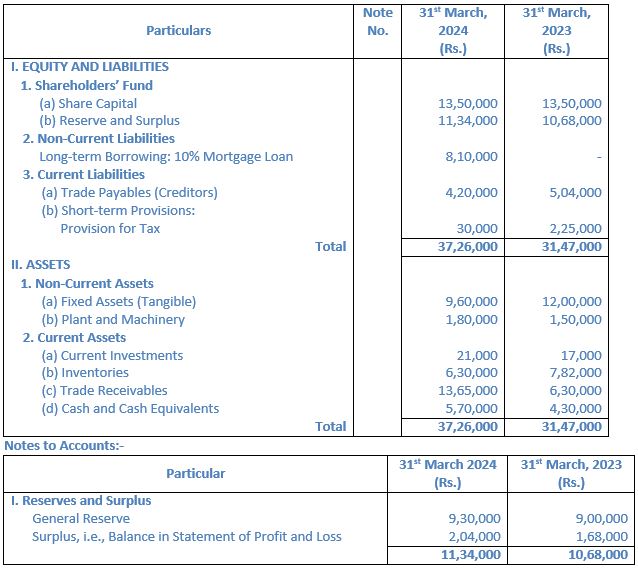

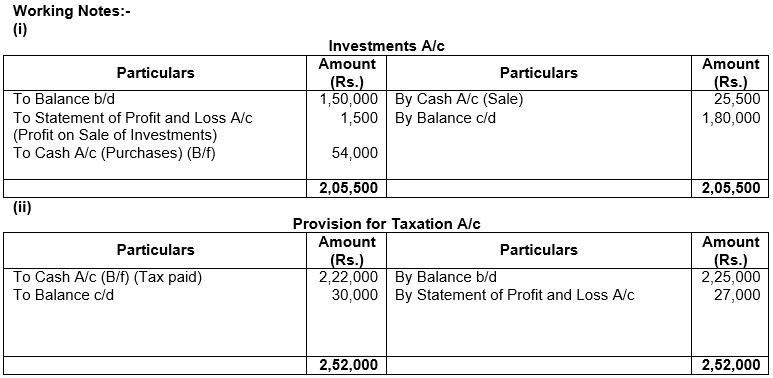

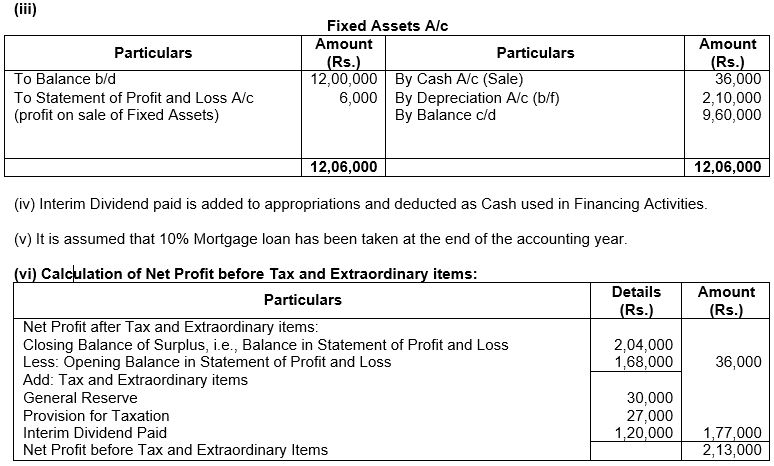

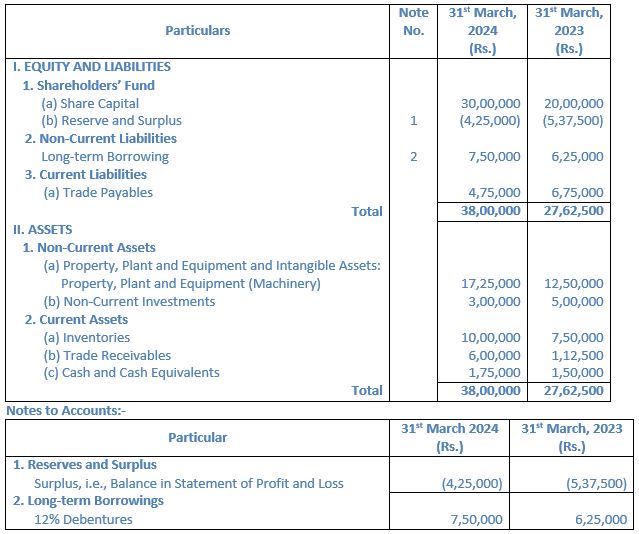

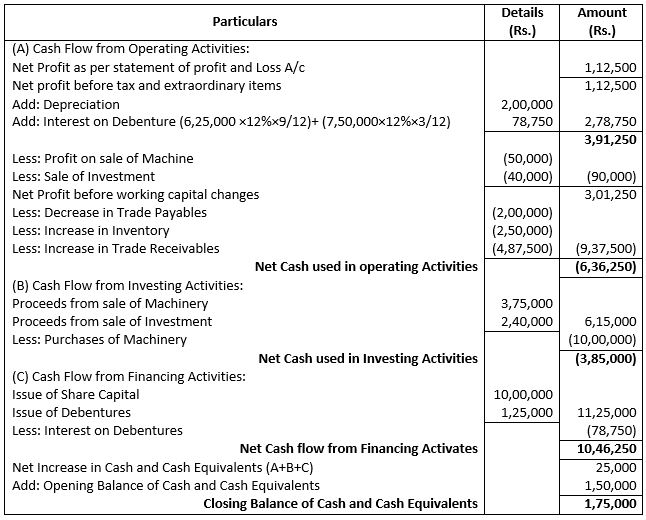

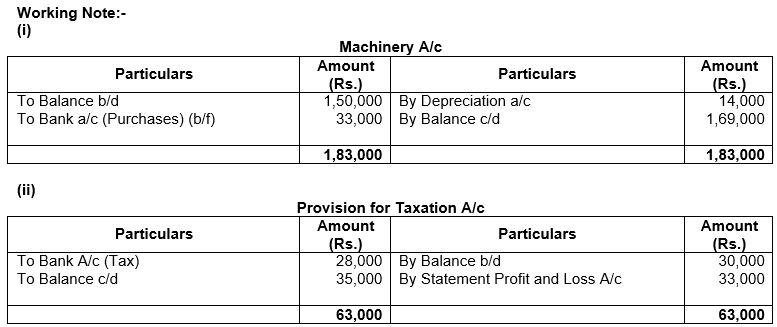

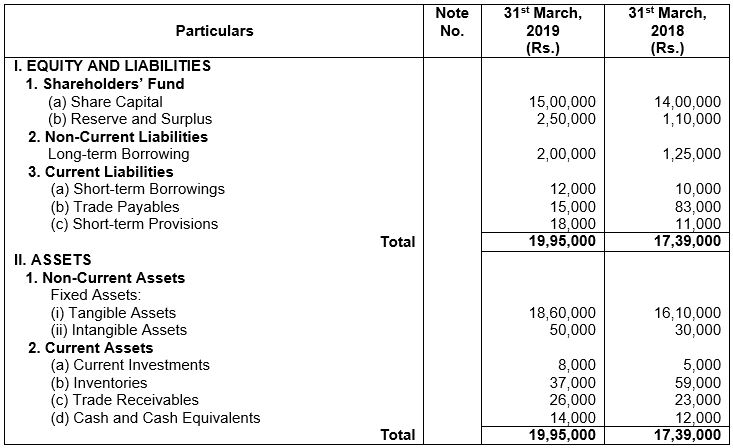

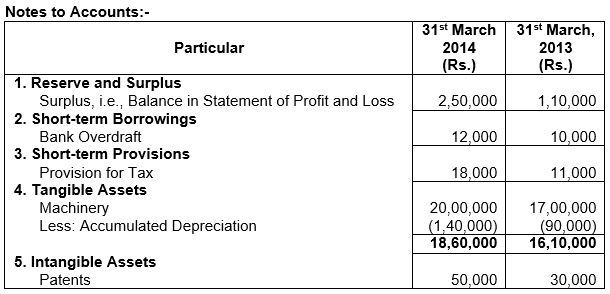

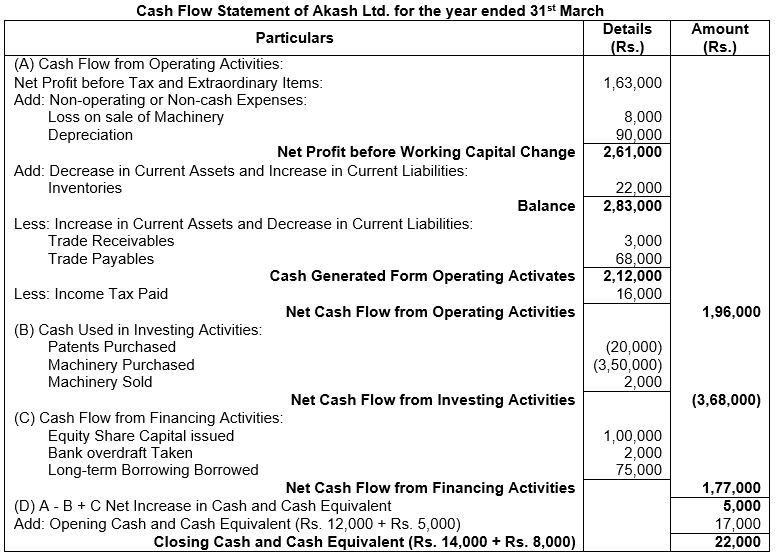

Question 54. Following is the Balance Sheet of Akash Ltd. as at 31st March, 2023, prepare Cash Flow Statement

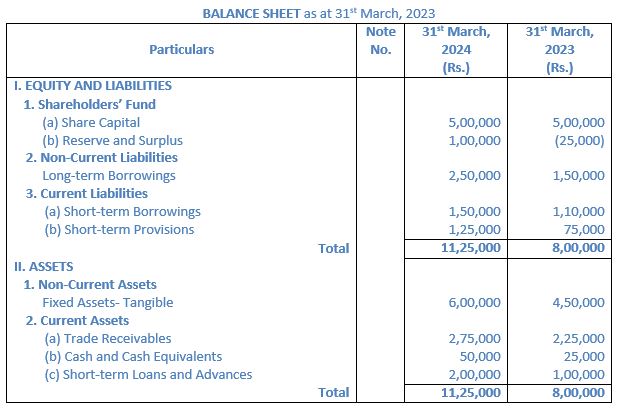

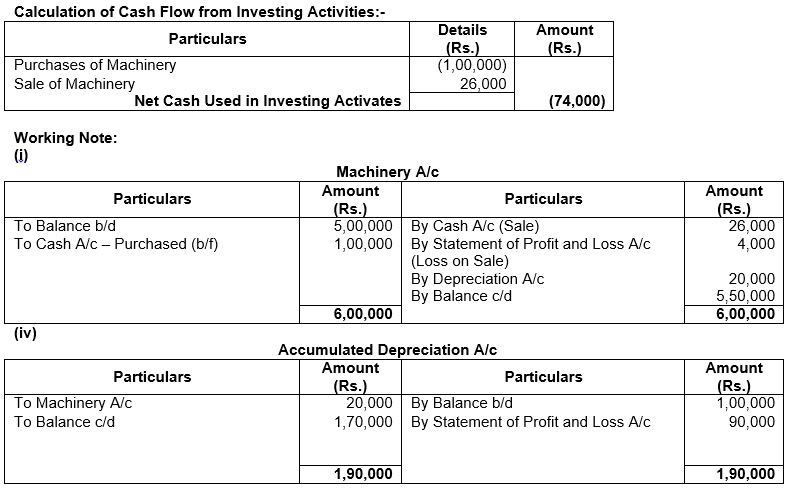

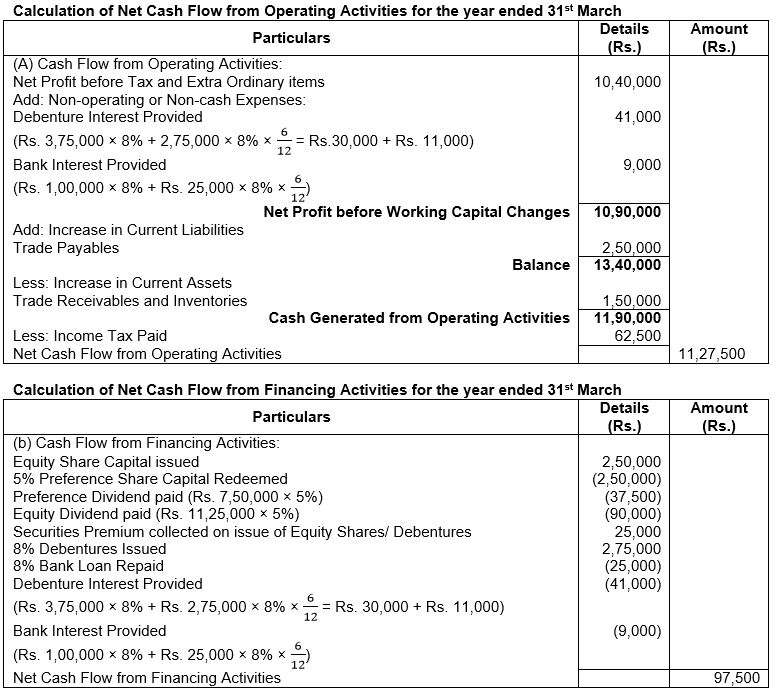

Additional Information:

(i) Debentures were issued on 1st January, 2023.

(ii) Machinery costing ₹ 5,00,000 on which depreciation charged was ₹ 1,75,000 was sold for ₹ 3,75,000.

(iii) Depreciation charged during the year amounted to ₹ 2,00,000.

(iv) Non-Current Investments were sold at a profit of 20%.

Prepare Cash Flow Statement.

Answer:

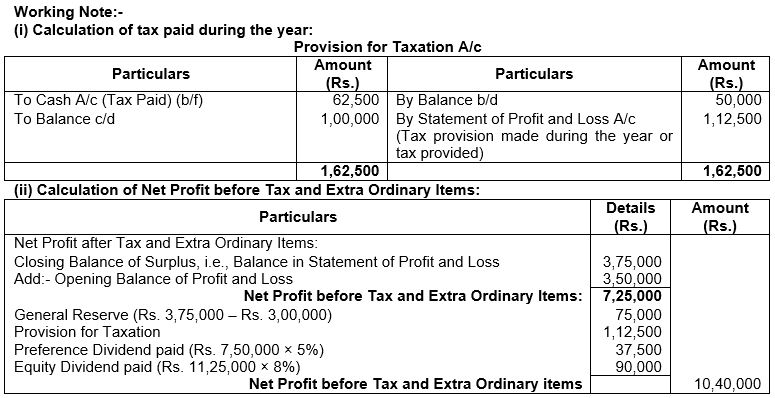

About Solution:

Net Profit after Tax and Extra Ordinary Items = Closing Balance of Surplus – Opening Balance of Surplus + Transfer to General Reserve + Provision for Taxation + Preference Dividend Paid + Equity Dividend Paid

Net Profit after Tax and Extra Ordinary Items = 3,75,000 + 3,50,000 + 75,000 + 1,12,500 + 37,500 + 90,000

Net Profit after Tax and Extra Ordinary Items = Rs. 10,40,000

Things to Remember:

In indirect method cash flow statement begins with net income or loss, and thereafter the additions or deductions from that amount for non-cash expense and revenue items, which results in cash flow from operating activities.

Important Notes:

Investing activities consist of sales and purchase of fixed assets that are long term in nature, like building, land, furniture and plant and machinery etc. It also includes sale and purchase of items that are not cash equivalents. If any income is received from these assets it is regarded as a part of investing activities.

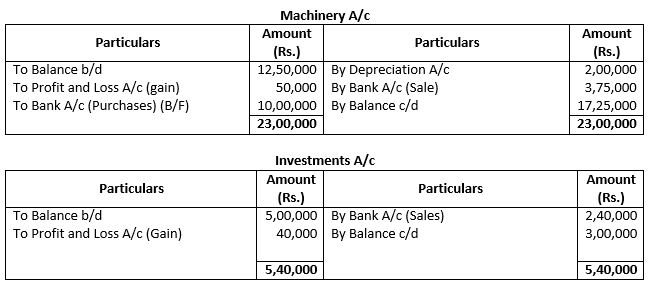

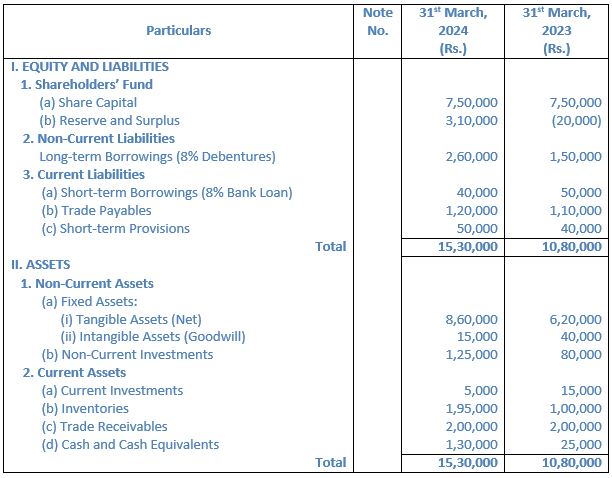

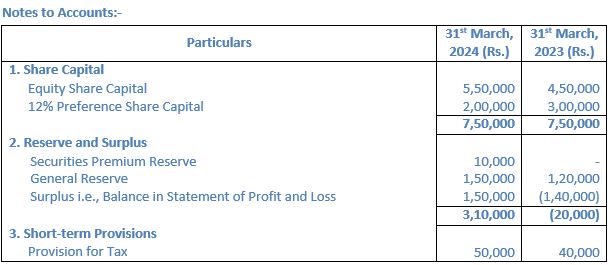

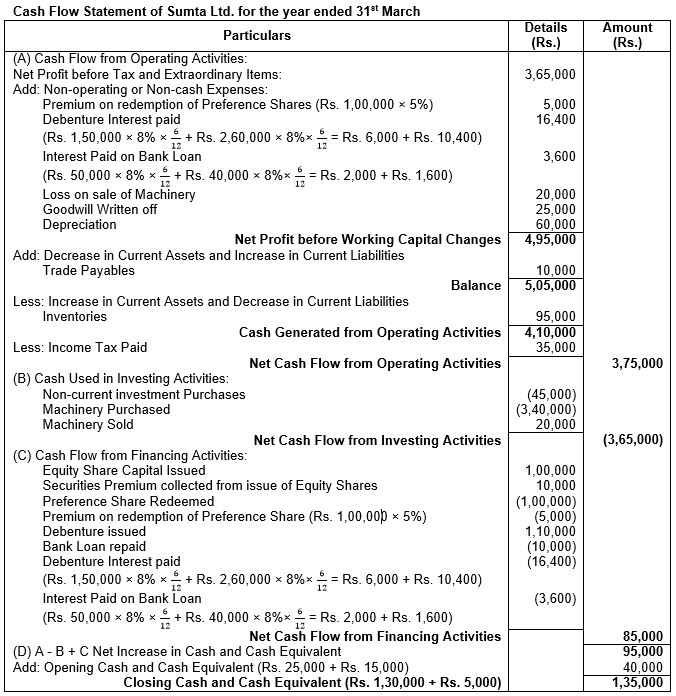

Question 55. From the following Balance Sheet of Samta Ltd., as at 31st March, 2024, prepare Cash Flow Statement:

Additional Information:

(i) During the year a piece of machinery costing Rs. 60,000 on which depreciation charged was Rs. 20,000 was sold at 50% of its book value. Depreciation provided on tangible Assets Rs. 60,000;

(ii) Income tax Rs. 45,000 was provided;

(iii) Additional Debentures were issued at par on 1st October, 2023 and Bank Loan was repaid on the same date;

(iv) At the end of the year Preference Shares were redeemed at a premium of 5%

Answer:

About Solution:

Net Profit before tax and extraordinary items = Closing Balance – Opening Balance + Provision for Tax + General Reserve

Net Profit before tax and extraordinary items = Rs. 1,50,000 – Rs. 1,40,000 + Rs. 45,000 + Rs. 30,000

Net Profit before tax and extraordinary items = Rs. 75,000

Things to Remember:

Investing Activity: These include all activities related to the acquisition and disposal of Long-term Assets and other investments which are not classified as cash equivalents.

Important Notes:

All cash inflows and outflows relating to the fixed assets, shares and related instruments of other enterprise including loans and advances to third parties and their repayments are classified under Investing Activities.

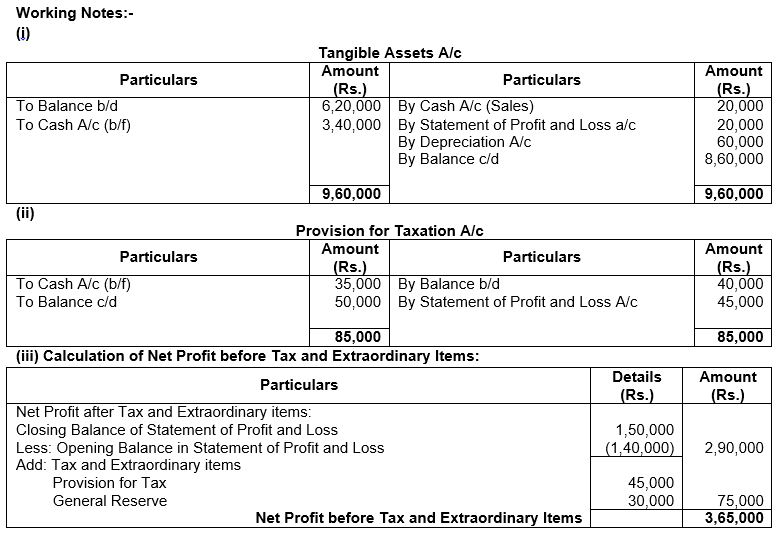

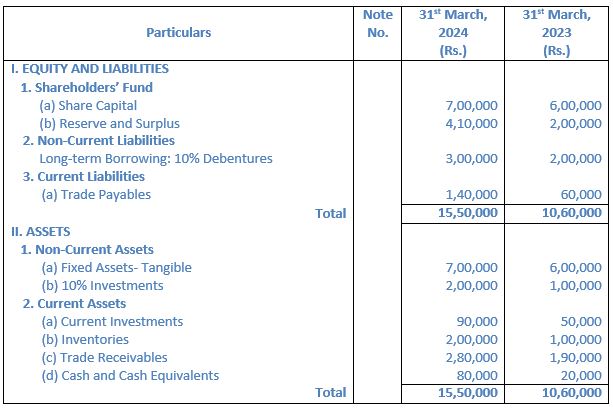

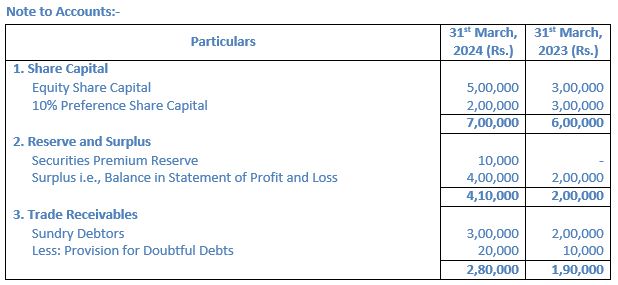

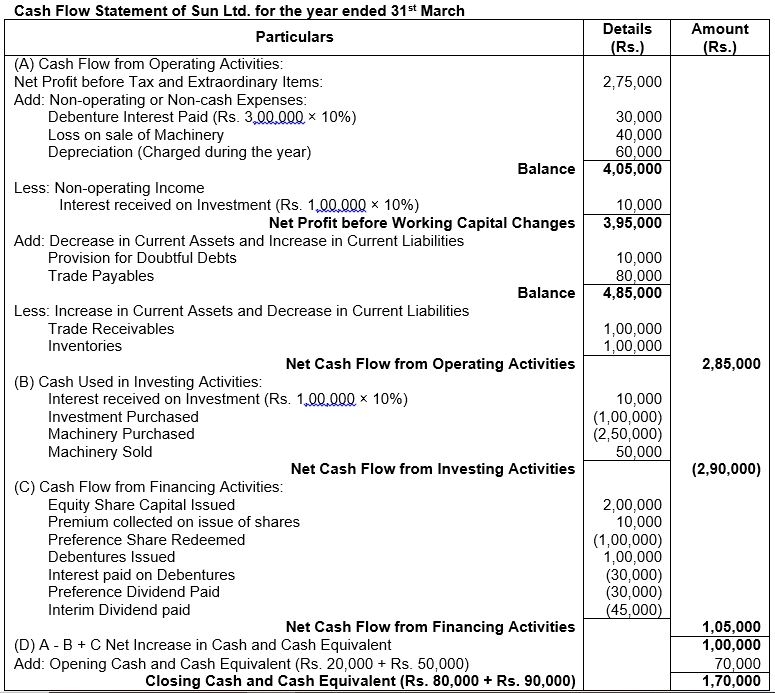

Question 56. From the following Balance Sheet and information of Sun Ltd., prepare Cash Flow Statement:

You are informed that during the year:

(i) Proposed Dividend: 31st March, 2024 31st March, 2023

Equity Share Capital Nil Nil

Preference Share Capital 10% 10%

(ii) A machine with a book value of Rs. 90,000 was sold for Rs. 50,000;

(iii) Depreciation charged during the year Rs. 60,000;

(iv) Debentures were issued on 1st April, 2023;

(v) Investments were purchased on 31st March, 2024;

(vi) Preference shares were redeemed on 31st December, 2023;

(vii) An interim dividend @ 15% was paid on equity shares on 31st December, 2023;

(viii) Fresh equity shares were issued at a premium of 5% on 31st March, 2024.

Answer:

About Solution:

Cash flow arising from Investing activities are:-

1. Cash payments to acquire fixed Assets

2. Cash receipts from disposal of fixed assets

3. Cash payments to acquire shares, or debenture as investment.

4. Cash receipts from the repayment of advances and loans made to third parties

Things to Remember:

Financial Enterprise: An enterprise that basically deals in lending (advancing loans) and borrowing of funds (accepting deposits), such as Banks.

Important Notes:

Non-Financial Enterprise: An enterprise that basically deals in areas other than finance (purchase of raw material and sale of goods).

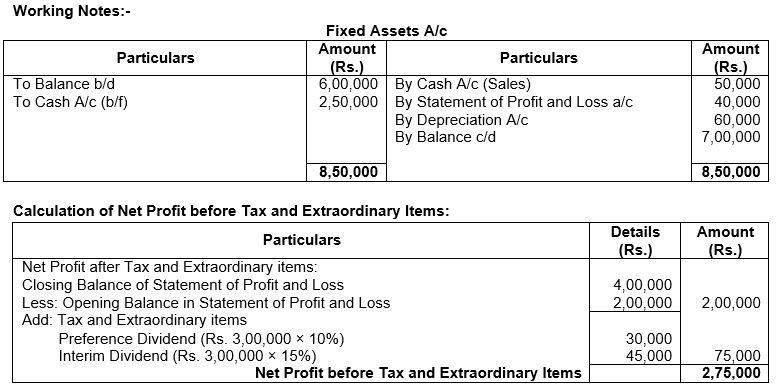

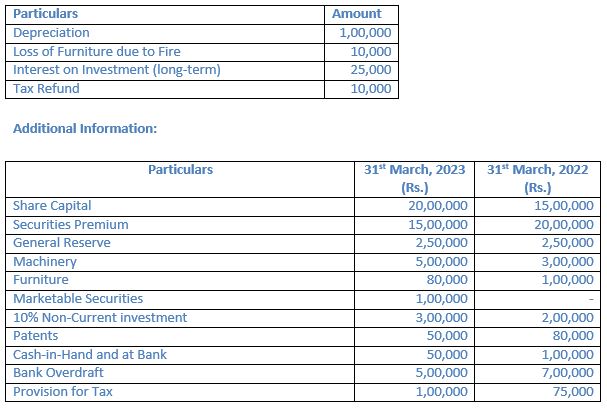

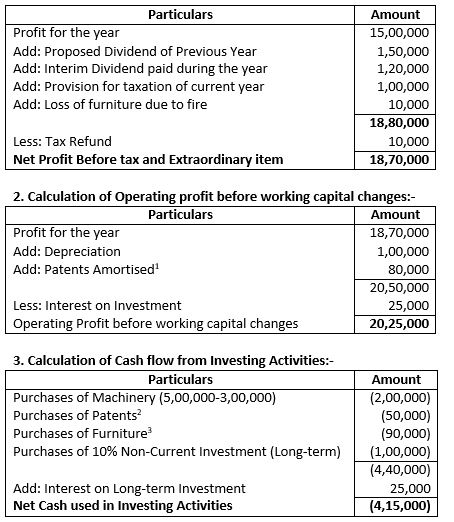

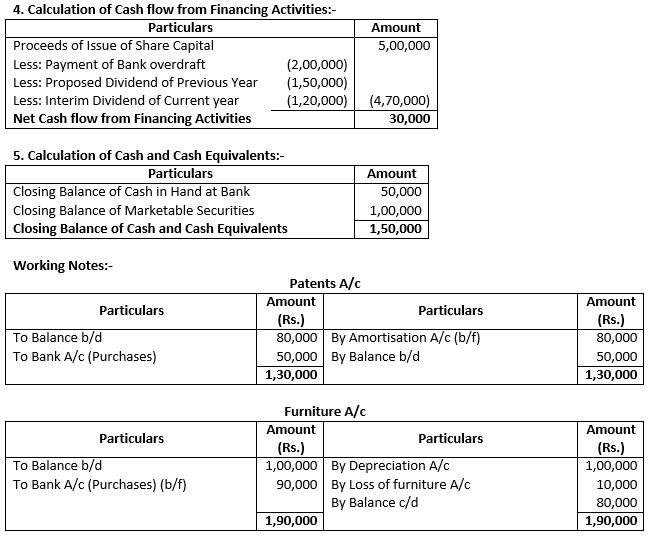

Question 57. Read the following hypothetical text and answer the given questions on its basis. Profit for the year ended 31st March, 2023 of iPay (a payment processing start up) was ₹ 15,00,000 after accounting the following:

(i) Patents purchased during the year was ₹ 50,000.

(ii) Proposed Dividend for the year ended 31st March, 2022 and 2023 was ₹ 1,50,000 and ₹ 2,00,000 respectively.

(iii) Interim Dividend during the year ended 31st March, 2022 and 2023 was ₹ 50,000 and ₹ 1,20,000 respectively.

You are required to:

1. Determine Net Profit before Tax and Extraordinary Items.

2. Determine Operating Profit before Working Capital Changes

3. Determine Cash Flow from Investing Activities.

4. Determine Cash Flow from Financing Activities

5. Determine Cash and Cash Equivalents.

Answer:

1. Calculation of Profit before taxation and Extraordinary Item:-

About Solution:

(i) An increase in an item of current assets causes a decrease in cash inflow because cash is blocked in current assets.

(ii) A decrease in an item of current assets causes an increase in cash inflow because cash is released from the sale of current assets.

Things to Remember:

It does not take into consideration bonus issue as it is just a capitalization of reserves for which the company does not receive any cash for it. Similarly, conversion of debentures into new debentures or shares involves no cash flow and therefore not considered in a cash flow statement.

Important Notes:

If shares or debentures are issued at a premium, Cash Flow Statement shows total cash received from the issue that includes both nominal value and the premium.

Old Questions

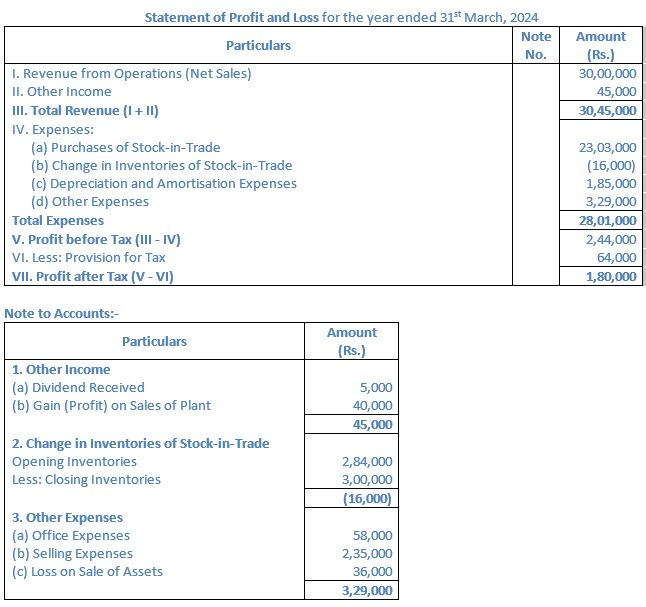

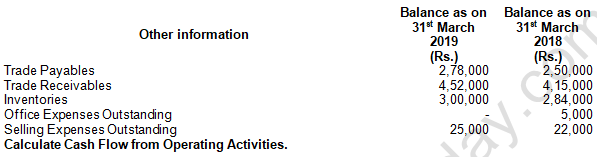

Question. Calculate Cash Flow from Operating Activities from the following information:

Answer:

Question. From the following information, calculate Cash Flow from Investing Activities:

A building was purchased as investment out of surplus which was let out for commercial purposes. Rent Received Rs. 20,000.

Answer:

Question. From the following Balance Sheet of Combiplast Ltd. for the year ended 31st March, 2019 and additional information, calculate Cash Flow from Investing Activities:

Additional Information: During the year the company sold machinery at Book Value of Rs. 1,50,000.

Answer:

Question. From the following information, calculate Cash Flow from Investing Activities:

During the year, a machinery costing Rs. 50,000 (accumulated depreciation provided thereon Rs. 20,000) was sold for Rs. 26,000.

Answer

:

Question. From the following information, calculate Net Cash Flow from Operating Activities and Financing Activities:

Additional Information:

(i) During the year additional debentures were issued at par on 1st October and Bank Loan was repaid on the same date.

(ii) Dividend on Equity Shares @ 8% was paid on Opening Balance.

(iii) Income tax Rs. 1,12,500 has been provided during the year.

(iv) Preference shares were redeemed at par at the end of the year.

Answer:

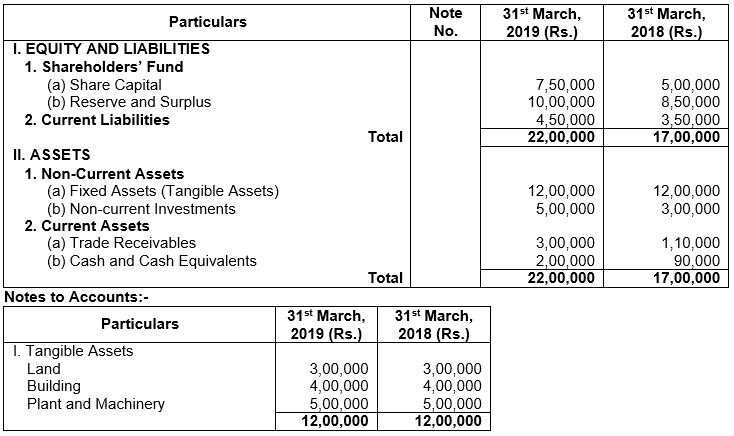

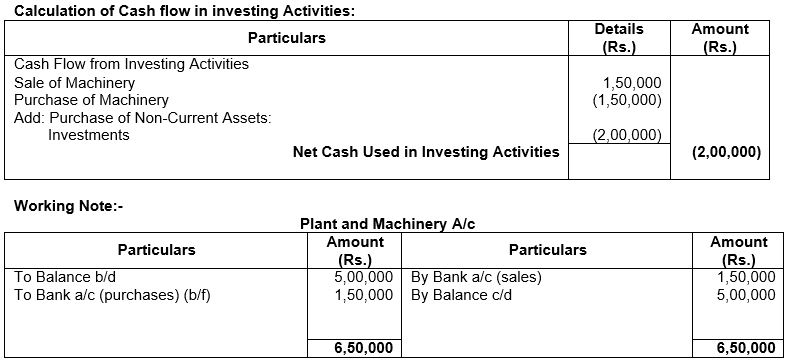

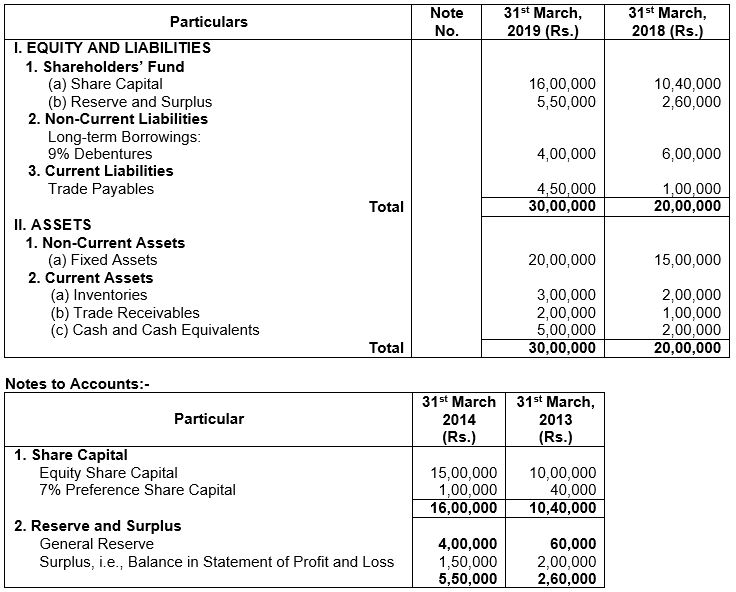

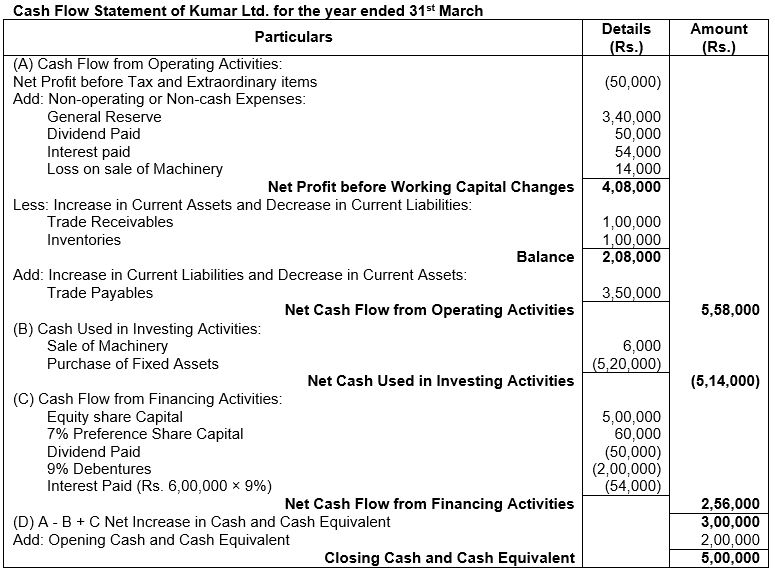

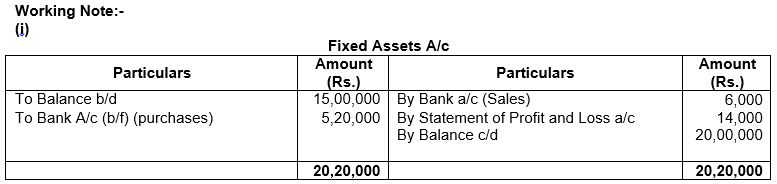

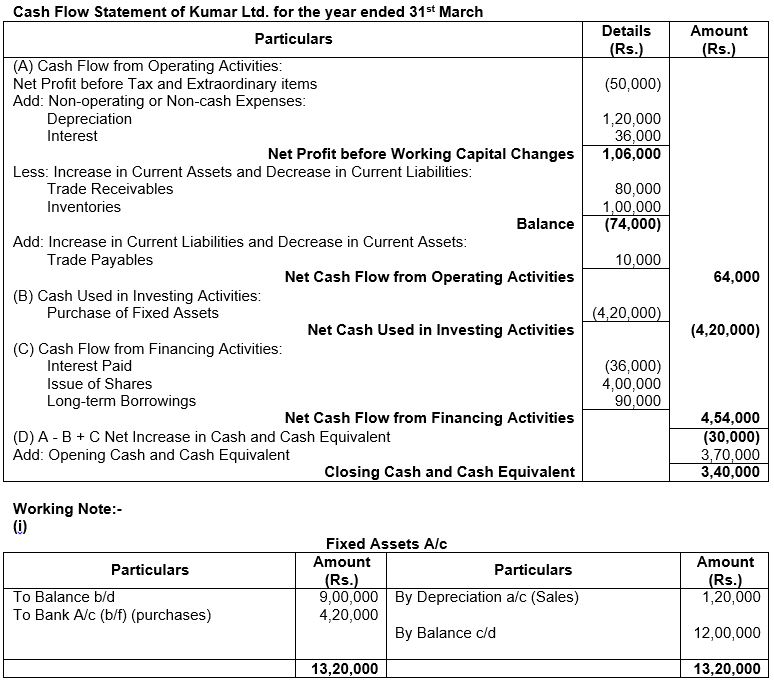

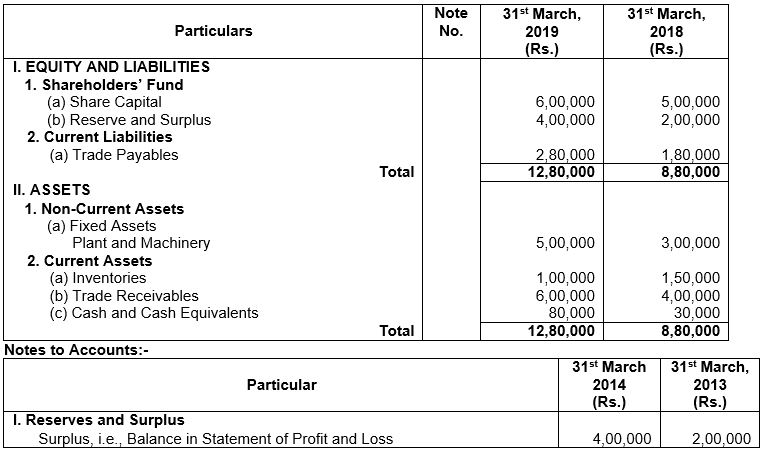

Question. From the following Balance Sheet of Kumar Ltd. as at 31st March, 2019, prepare Cash Flow Statement:

Additional Information:

1. During a year, a machinery costing Rs. 20,000 was sold for Rs. 6,000.

2. Dividend paid during the year Rs. 50,000.

Answer:

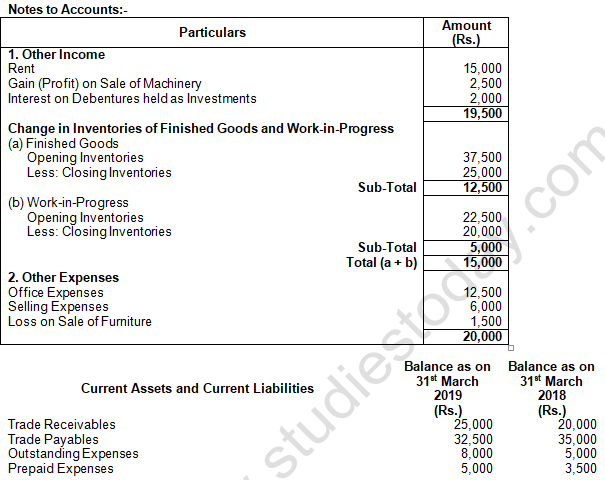

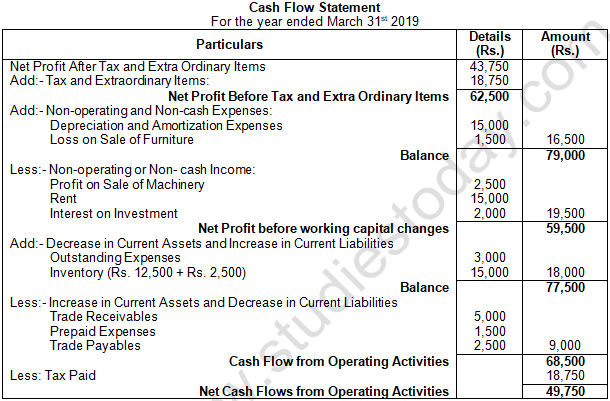

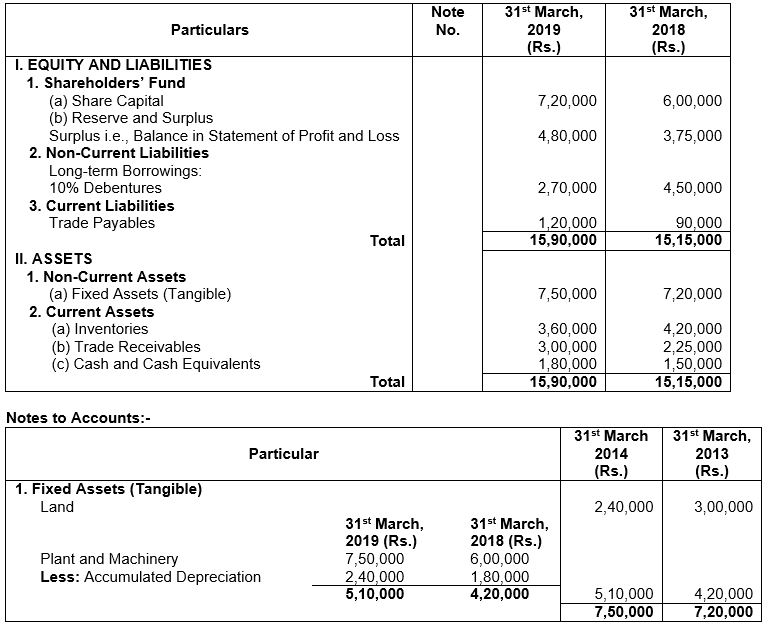

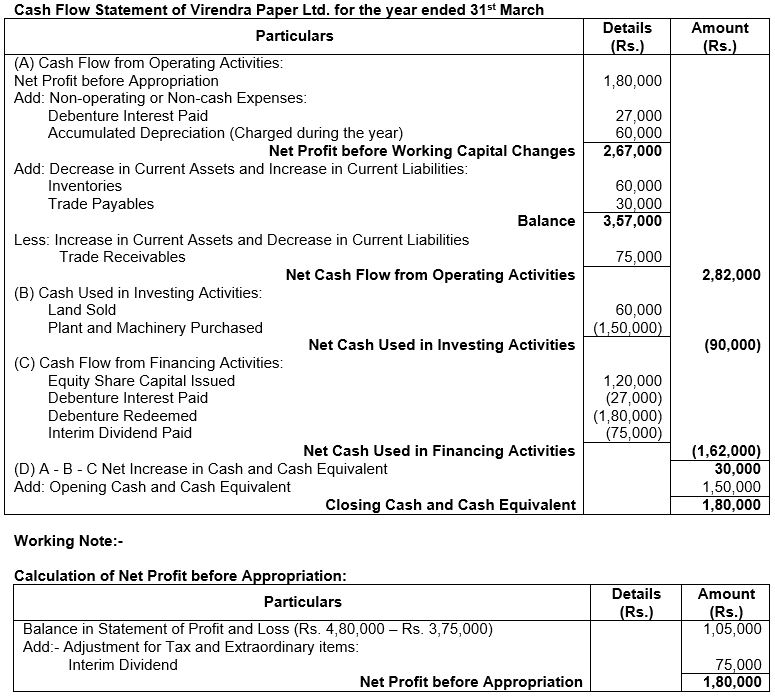

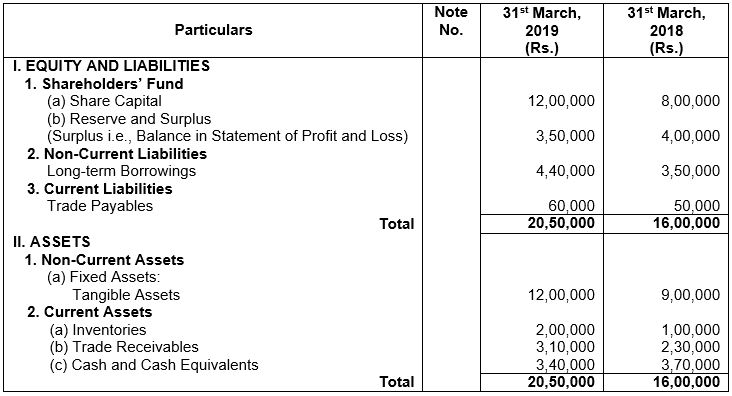

Question. The Balance Sheet of Virendra Paper Ltd. as at 31st March, 2019 is given below:

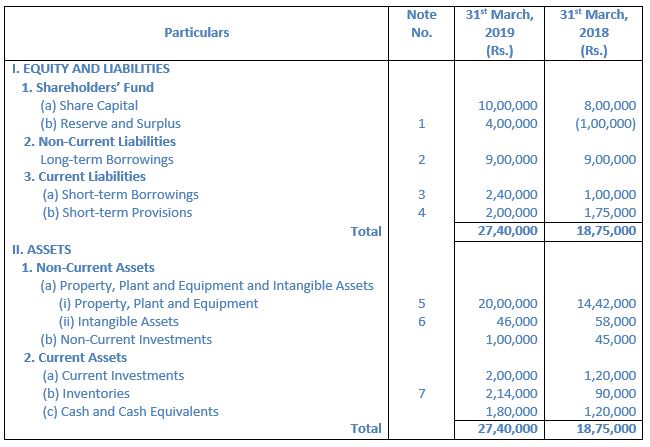

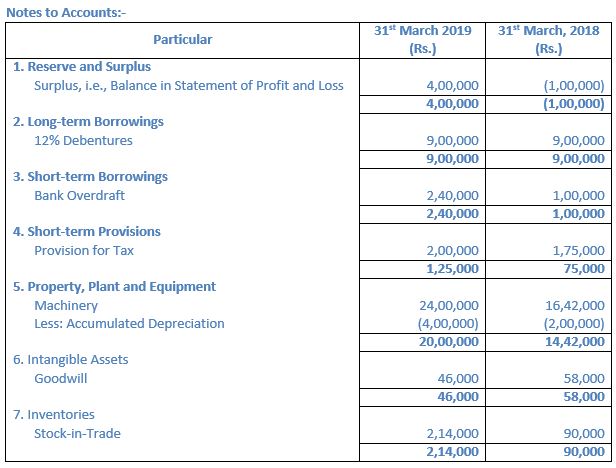

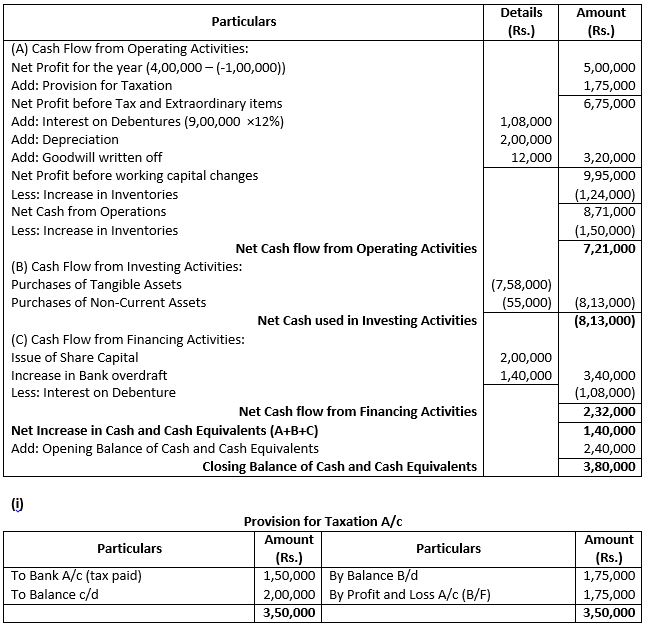

Additional Information:

1. Interim Dividend of Rs. 75,000 has been paid during the year.

2. Debenture Interest paid during the year Rs. 27,000.

You are required to prepare Cash Flow Statement.

Answer:

Question. Following are the Balance Sheets of Krishtec Ltd. for the years ended 31st March 2012 and 2011:

Prepare a Cash Flow Statement after taking into account the following adjustments:

(a) The company paid Interest Rs. 36,000 on its long-term borrowings.

(b) Depreciation charged on tangible fixed assets was Rs. 1,20,000.

Answer:

Question. Prepare Cash Flow Statement from the following Balance Sheet:

Additional Information:

(i) An old machinery having book value of Rs. 50,000 was sold for Rs. 60,000.

(ii) Depreciation provided on Machinery during the year was Rs. 30,000.

Answer:

Question. From the following Balance Sheet, prepare Cash Flow Statement:

Additional Information:

1. Proposed Dividend for the year ended 31st March, 2019 was Rs. 25,000 and for the year ended 31st March, 2018 was Rs. 14,000.

2. Interim Dividend paid during the year was Rs. 9,000.

3. Income Tax paid during the year was Rs. 28,000.

4. Machinery was purchased during the year Rs. 33,000.

5. Depreciation to be charged on machinery Rs. 14,000 and building Rs. 10,000.

Answer:

Question. From the following Balance Sheet of Akash Ltd. as at 31st March 2014:

Additional Information:

(i) Tax paid during the year amounted to Rs. 16,000.

(ii) Machine with a net book value of Rs. 10,000 (Accumulated Depreciation Rs. 40,000) was sold for Rs. 2,000.

Prepare Cash Flow Statement.

Answer:

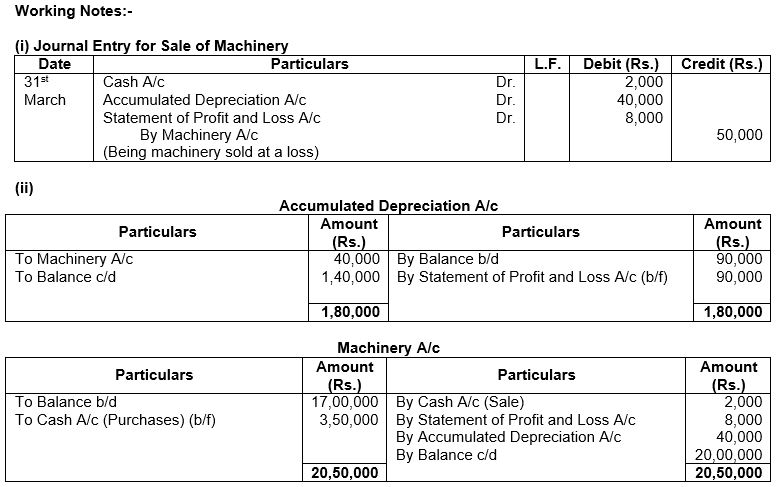

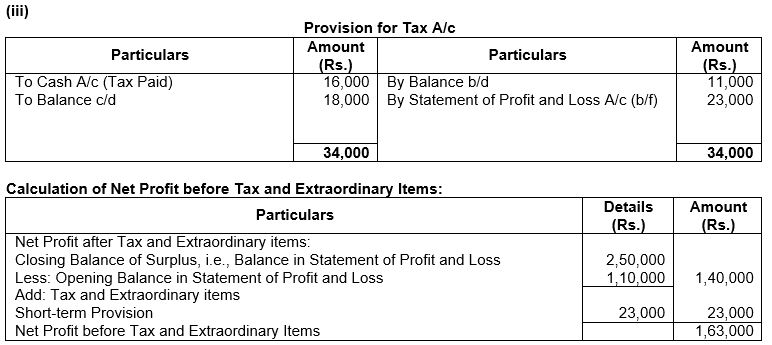

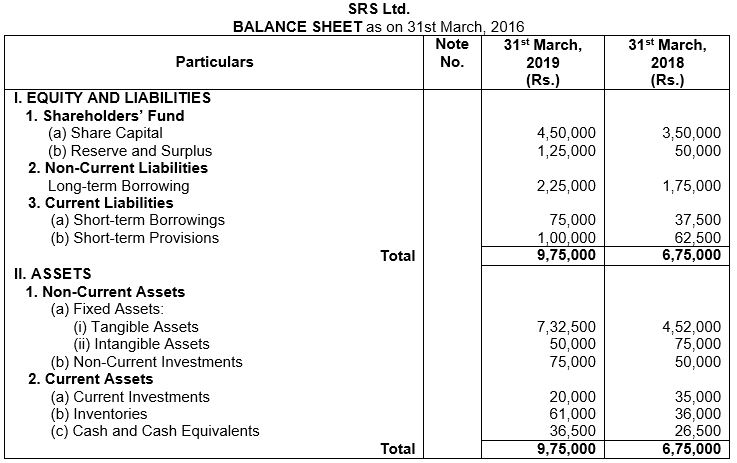

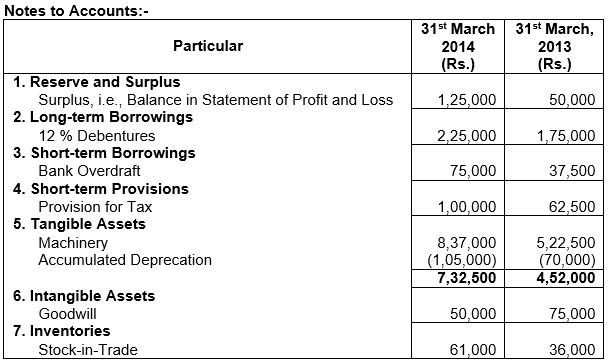

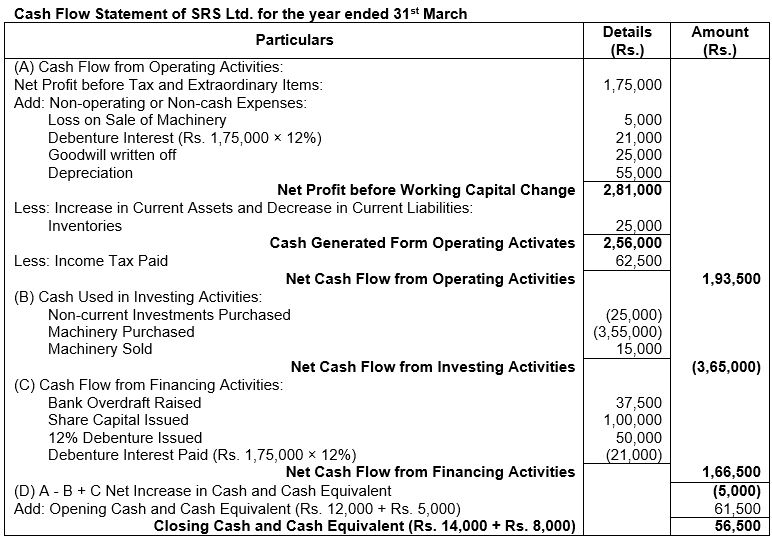

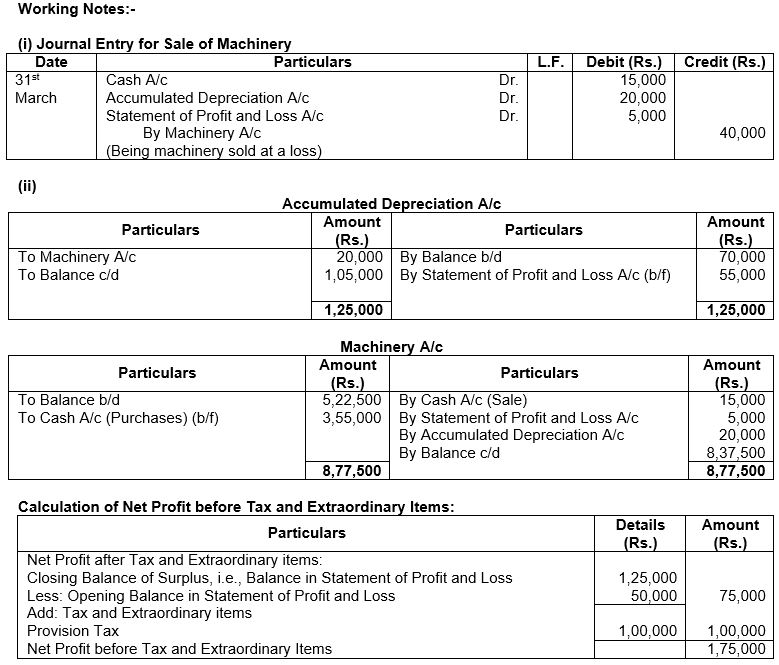

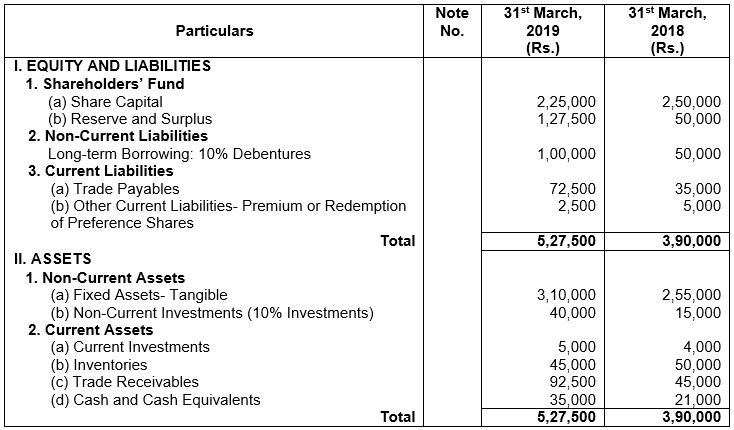

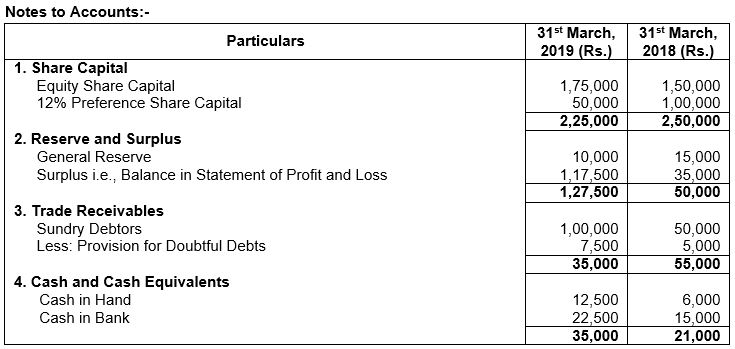

Question. From the following Balance Sheet of SRS Ltd. and the additional information as on 31st March, 2016, prepare a Cash Flow Statement:

Additional Information:

(i) Rs. 50,000, 12% Debentures were issued on 31st March, 2016.

(ii) During the year, a piece of machinery costing Rs. 40,000, on which accumulated depreciation was Rs. 20,000, was sold at a loss of Rs. 5,000.

Answer:

Question. From the following Balance Sheet and information of Volvo Ltd., prepare Cash Flow Statement:

Additional Information:

(i) You are informed during the year:

Proposed Dividend: 31st March, 2019 31st March, 2018

Equity Share Capital Nil Nil

Preference Share Capital 12% 12%

(ii) A machine with a book value of Rs. 20,000 was sold for Rs. 12,500;

(iii) Depreciation charged during the year was Rs. 35,000;

(iv) Preference shares were redeemed on 31st March, 2018 at a premium of 5%;

(v) An Interim dividend of Rs. 5,000 was paid on equity shares on 31st March, 2019 out of General Reserve;

(vi) Fresh equity shares were Issued on 31st March, 2019; and

(vii) Additional Investments were purchased on 31st March, 2019.

Answer:

Question. Prepare Cash Flow Statement from the following:

Answer:

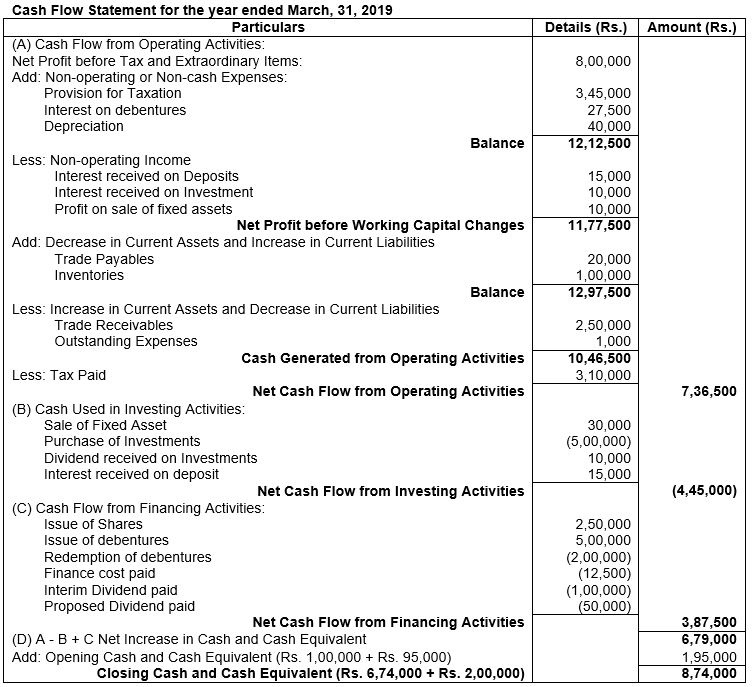

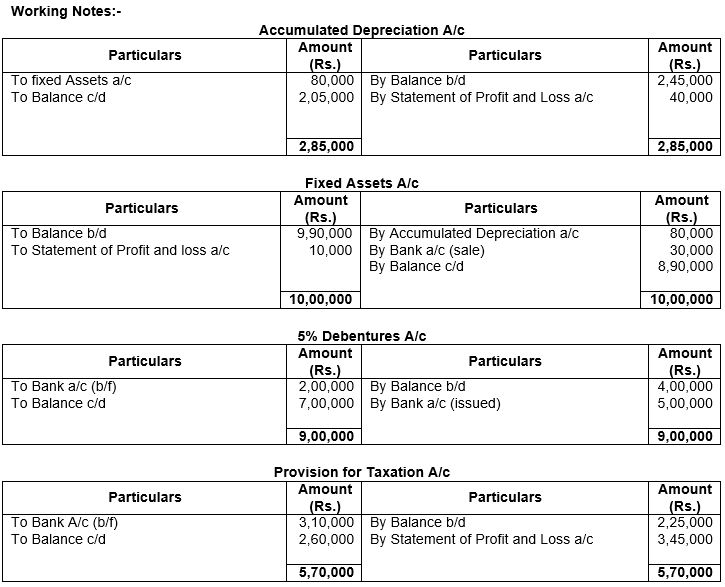

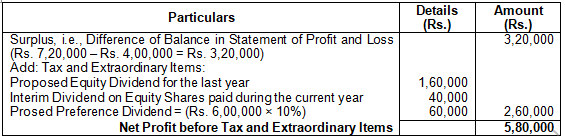

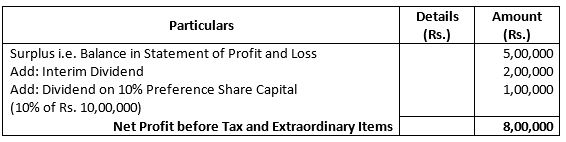

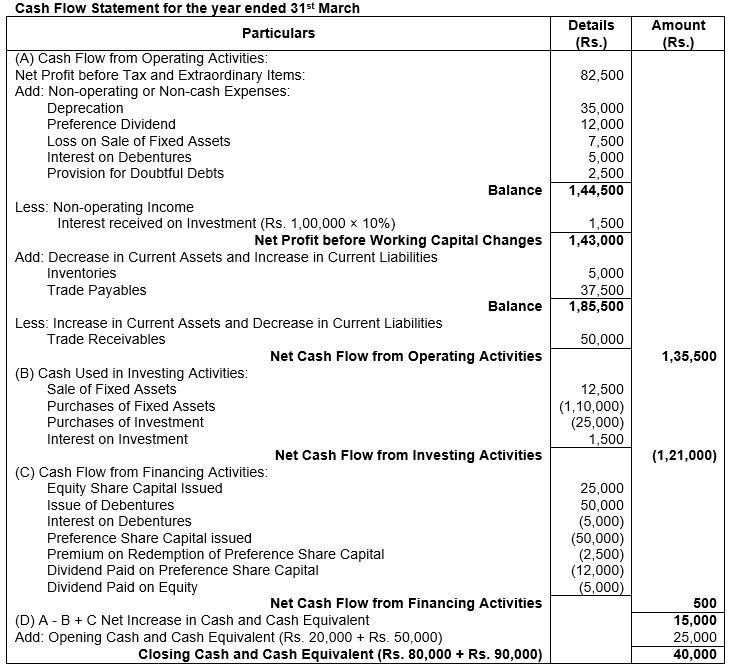

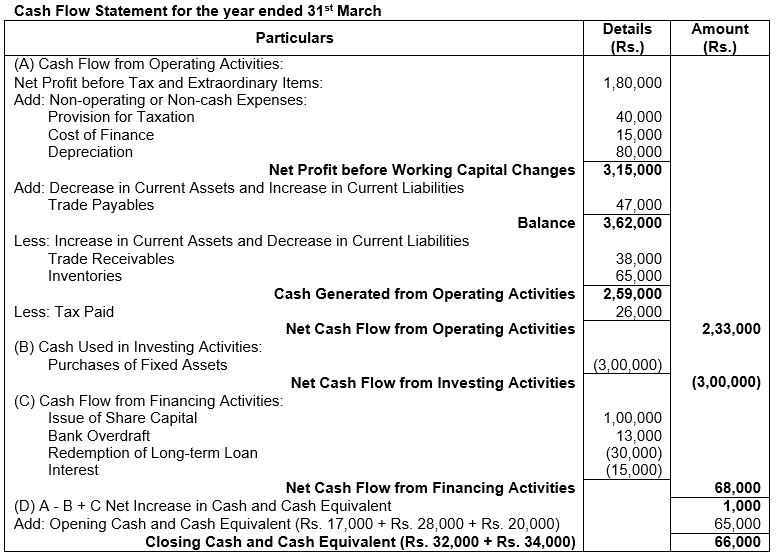

Question. From the following Balance Sheet as at 31st March, 2019 and Statement of Profit and Loss for the year ended 31st March, 2019 of RSB Ltd. and additional information, prepare Cash Flow Statement:

Additional Information:

(i) Additional debentures were issued on 1st October, 2018 of Rs. 5,00,000. On the same date, part of outstanding debentures was redeemed and interest was paid, whereas interest on outstanding debentures was paid on 10th April, 2019.

(ii) Board of Directors proposed dividend in both the years @ 10%.

(iii) Interim Dividend of Rs. 1,00,000 was paid during the year.

(iv) A fixed asset with original cost of 1,00,000, on which depreciation till date was provided of Rs. 80,000 was sold at a profit of Rs. 10,000.

Answer: