Read TS Grewal Solution Class 12 Chapter 1 Financial Statement of Not for Profit Organisations 2026. Students should study TS Grewal Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These TS Grewal Class 12 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 1 Financial Statement of Not for Profit Organisations TS Grewal Solutions

TS Grewal Solutions for Chapter 1 Financial Statement of Not for Profit Organisations Class 12 Accounts have been provided below based on the latest TS Grewal Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 1 Financial Statement of Not for Profit Organisations TS Grewal Class 12 Solutions

About this chapter: TS Grewal Class 12 Chapter 1 provides a detailed understanding of the concepts relating to the financial statements of not-for-profit organizations. Chapter 1 in Class 12 TS Grewal accountancy book mainly covers the different accounting topics relating to types of financial statements of not-for-profit organizations, such as income and expenditure account, balance sheet, and cash flow statements. The author has also explained in great detail the importance of each financial statement and how it helps the interested party in assessing the performance of not-for-profit organizations. The chapter also covers one of the most important topics which is the accounting treatment of different items such as donations received, legacies, and endowments. There are a lot of detailed concepts and questions given in the chapter, and our teachers have provided solutions to all unsolved questions in the book. With the help of TS Grewal Solution Class 12 Chapter 1, Class 12 students will be able to understand the concepts and principles of financial accounting and gain a detailed understanding of the financial statements of not-for-profit organizations.

Q1. Give three essential features of the Income and Expenditure Account.

Answer:

Features of Income and Expenditure Account:-

1.) Nature: It is a Nominal Account. Hence, it is debited with expenses and losses and it is credited with income and gains.

2.) Opening and Closing Balance: It does not have an opening Balance. Its Balance at the end is either surplus or deficit. It is transferred to Capital Fund in the Balance Sheet.

3.) Adjustment: This account is prepared on accrual basis of accounting and thus all adjustments relating to prepaid or outstanding expenses and income, provision for depreciation or doubtful debts are made.

Q2. Explain with illustration the concept of Fund Based Accounting.

Answer:

Fund means amount received or set aside by a Not-for-Profit Organisation for a Specific purpose. The fund amount along with the income earned on the fund cannot be used for purposes other than those for which it is received or set aside.

Donations received or funds set aside for specific purposes are credited to a separate Fund Account and are shown on the liabilities side of the Balance Sheet. The incomes from or donations for these funds are credited to respective Fund Account. On the other hand, expenses or Payments out of these funds are debited. Accounting when done on this basis is known as Fund Based Accounting.

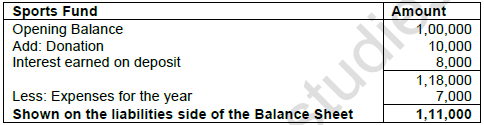

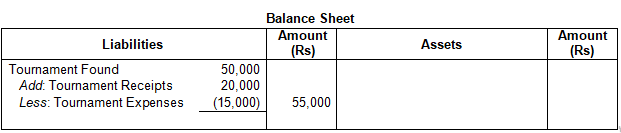

For example: The Sports Fund has a balance of Rs. 1,00,000 which is invested as fixed deposit in a bank earning 8% interest. Further donation of Rs. 10,000 is received towards it. Expenses incurred towards prizes are Rs. 7,000; Rs. 3,000 towards trophies and Rs. 4,000 towards distribution of cash prizes. In the accounts, it is shown as follows:

Q3. What are the essential features of the Receipts and Payments Account?

Answer:

Features of Receipts and Payments Account:

1.) Nature: It is an asset account since it is a summary of cash receipts and cash payments including bank balance.

2.) Basis of Preparing: It is prepared on cash basis i.e., transactions and events which have been received or paid in cash are shown in the account.

3.) Capital and Revenue: It records all receipts and payments whether they are of revenue nature or capital nature.

4.) Period: It records cash and bank transactions without distinguishing among current, previous or succeeding (next) accounting periods.

5.) Opening and Closing Balance: Opening balance of this account shows cash in hand and/or at bank in the beginning of the accounting period and closing balance shows cash in hand and/or at bank at the end of the accounting period.

Q4. Differentiate between the Receipts and Payments Account and the Cash Account.

Answer:

EXERCISE :->

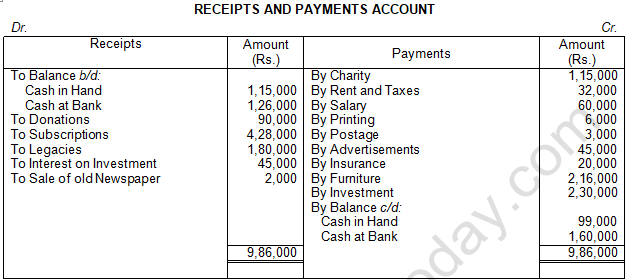

Question 1: From the information given below, prepare Receipts and Payments Account of Railway Club for the year ended 31st march, 2019:

Answer: 1:

Point of Knowledge:-

- Receipts and Payments Account is a summary of cash (including bank) receipts and Payments during and accounting period, receipts and payments being shown under appropriate heads of accounts.

Question 2: Bengal Cricket Club was inaugurated on 1st April, 2018. It had the following Receipts and Payments during the year ended 31st March, 2019:

Receipts: Entrance Fees Rs. 10,000; Subscriptions Rs. 60,000; Donations Rs. 10,000.

Payments: Rent Rs. 15,000; Postages Rs. 1,000; Newspapers and Magazines Rs. 8,000; Investments Rs. 30,000; Stationery Rs. 4,000; Entertainment Expenses Rs. 3,000; Miscellaneous Expenses Rs. 2,000.

Show the Receipts and Payments Account for the year ended 31st March, 2019.

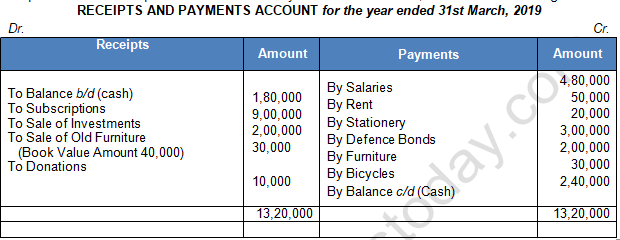

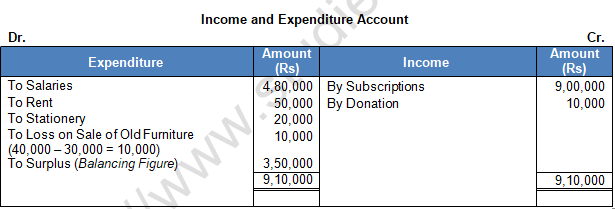

Answer: 2:

Point of Knowledge:-

Final accounts of a Not-for-Profit Organisation include:

1.) Receipts and Payments Account

2.) Income and Expenditure Account

3.) Balance Sheet

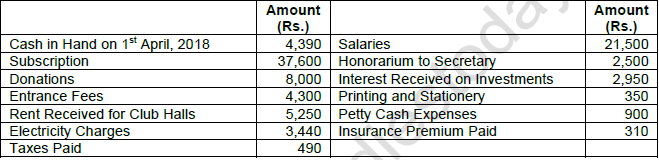

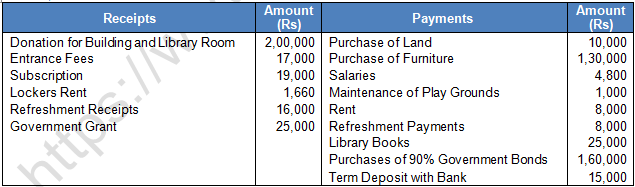

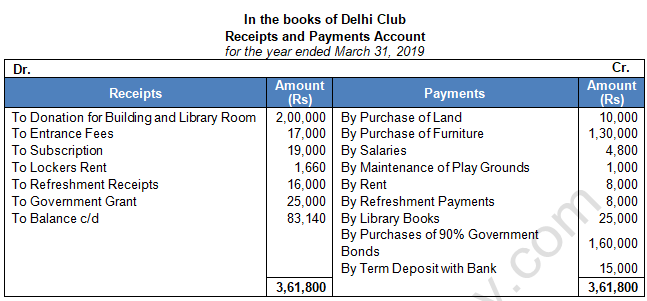

Question 3: The following information were obtained from the books of Delhi Club as on 31st March, 2019 at the end of the first year of the Club, prepare Receipts and Payment Account for the year ending 31st March, 2019:

Answer: 3:

Point of Knowledge:-

Limitations of Receipts and Payments Account:-

1.) It does not show expenses and income on accrual basis.

2.) It does not show whether the Not-for- Profit Organisation is able to meet its day-to-day expenses out of its income or not.

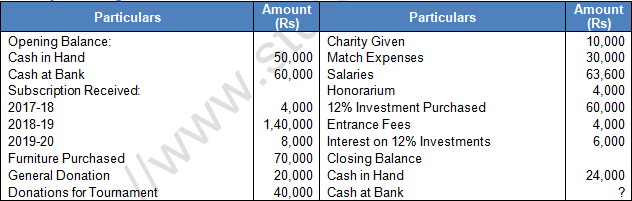

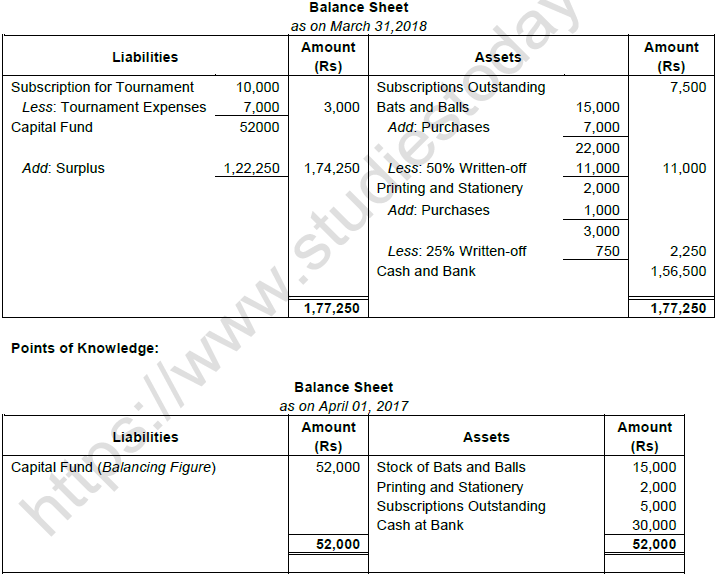

Question 4: From the following information, prepare Receipts and Payments Account of Long-town Sports Club for the year ending 31st March, 2019:

Answer: 4:

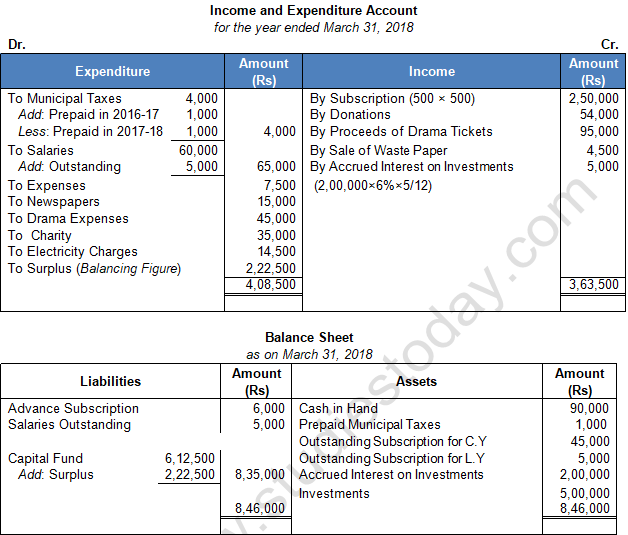

Point of Knowledge :- Cash at Bank = Receipts – Payments

= 3,32,000 – 2,61,600

= 70,400

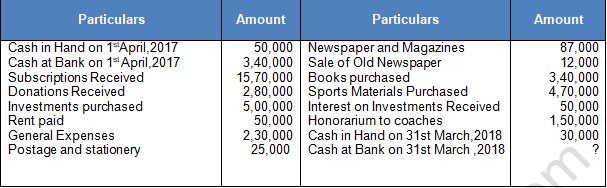

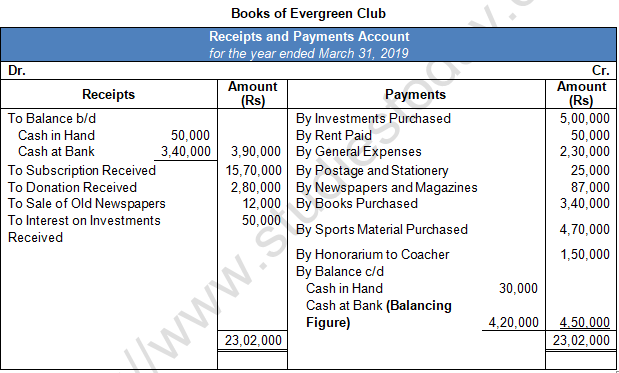

Question 5: From the following particulars of Evergreen club, prepare Receipts and payments Account for the year ended 31st March, 2019:

Answer: 5:

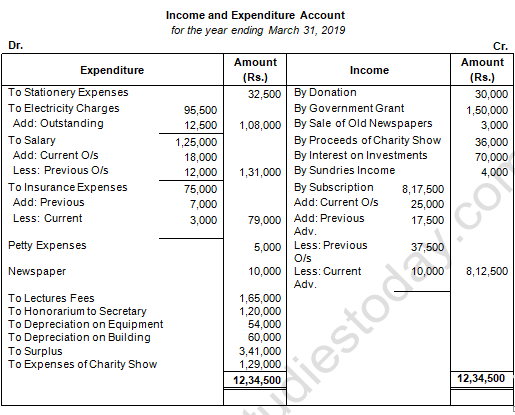

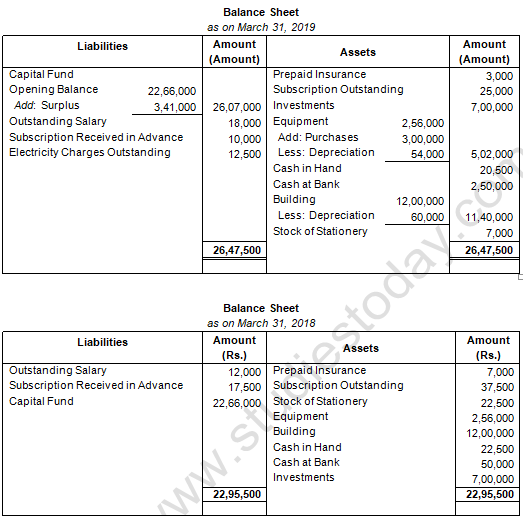

Fund Based Accounting

Question 6: How are the following items shown in the accounts of a Not-for-Profit Organisation?

Answer: 6:

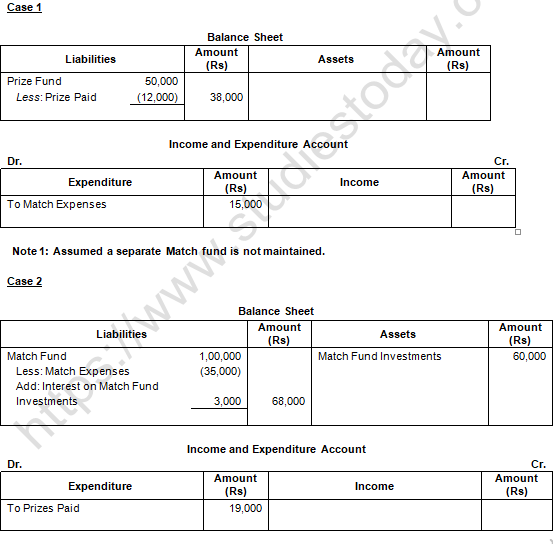

Question 7: How are the following dealt with in the accounts of a Not-for-Profit Organisation?

Answer: 7:

Note 1: Assumed a separate Prize fund is not maintained.

Question 8: How are the following dealt with while preparing the final accounts of a club?

Answer: 8:

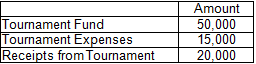

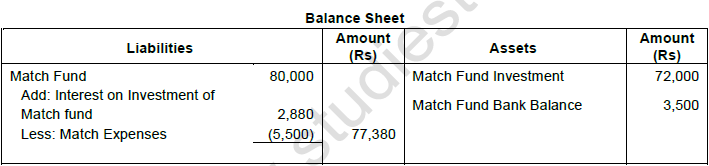

Question 9: From the following information of a club show the amounts of match expenses and match fund in the appropriate Financial Statements of the club for the year ended on 31st March, 2019:

Answer: 9:

Question 10: Show how are the following items dealt with while preparing the final accounts for the year ended 31st March, 2019 of a Not-for-profit Organisation:

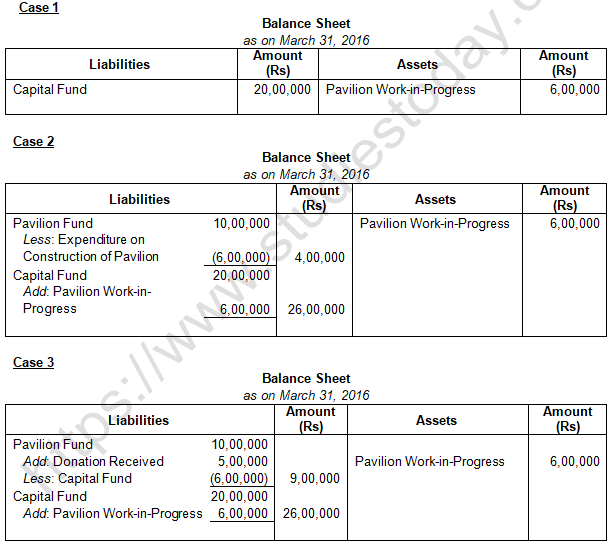

Case I Expenditure on construction of Pavilion is Amount 6,00,000. The construction work is in progress and has not yet completed. Capital Fund as at 31st March, 2017 is Amount 20,00,000.

Case II Expenditure on construction of Pavilion is Amount 6,00,000. The construction work is in progress and has not yet completed. Pavilion Fund as at 31st March, 2017 is Amount 10,00,000, and Capital Fund as at 31st March, 2017 is Amount 20,00,000.

Case III Expenditure on construction of Pavilion is Amount 6,00,000. The construction work is in progress and has not yet completed. Pavilion Fund as at 31st March, 2017 is Amount 10,00,000, and Capital Fund as at 31st March, 2017 is Amount 20,00,000. Donation Received for Pavilion on 1st January,2018 is Amount 5,00,000.

Answer 10:

Entrance Fees

Question 11: How is Entrance Fees dealt with while preparing the final accounts for the year ended 31st March, 2019 in each of the following alternative cases?

Case I: During the year ended 31st March, 2019, Entrance Fees received was Amount 1,00,000.

Case II: During the year ended 31st March, 2019, Entrance Fees received was Amount 1,00,000.Out of this, Amount 25,000 was received from individuals whose membership is not yet approved.

Answer 11:

Case 1: During the year 2018-19, Entrance fees received Rs 1,00,000 – Entrance fees received Rs 1,00,000 should be credited to the Income and Expenditure Account

Case 2: During the year 2018-19, Entrance Fees received Rs1,00,000. Out of this Rs25,000 pertains to the year 2018-19. The accounting policy of the club is to treat the Entrance fees as of revenue receipt. Entrance Fees received Rs75,000 should be credited to the Income and Expenditure Account and advance received Rs 25,000 for the year 2018-19 will be shown as advance entrance fees in the liabilities side of this year’s Balance Sheet.

Calculation of Amount of Subscriptions

Question 12: In the year ended 31st March, 2019, the subscriptions received by the Jaipur Literary Society were Amount 4,20,000. These subscriptions include Amount 14,000 received for the year ended 31st March, 2018. On 31st March, 2019, subscriptions due but not received were Amount 10,000. What amount should be credited to Income and Expenditure Account for the year ended 31st March, 2019 as subscription?

Answer 12:

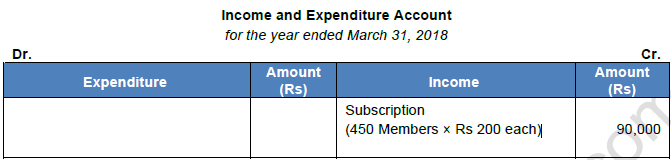

Question 13: Subscriptions received during the year ended 31st March, 2018 are:

There are 450 members, each paying an annual subscription of Amount 200; Amount 1,800 were in arrears for the year ended 31st March, 2018.

Calculate amount of subscriptions to be credited to Income and Expenditure Account for the year ended 31st March, 2019.

Answer 13:

Points of Knowledge:

Subscriptions to be credited to the Income and Expenditure Account for the year ended 31st March

= Rs. 450 × 200

= Rs. 90,000

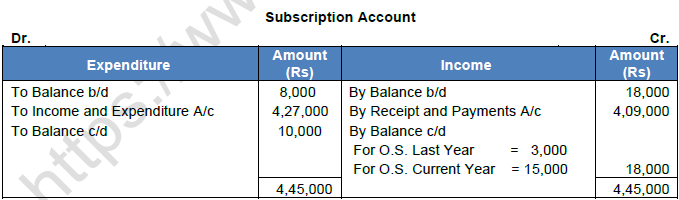

Question 14: In the year ended 31st March, 2019, subscriptions received by Kings Club, Delhi were Amount 4,09,000 including Amount 5,000 for the year ended 31st March, 2018 and Amount 10,000 for the year ended 31st March, 2020. At the end Amount 15,000. The subscriptions due but not received at the end of the previous year, i.e., 31st March, 2017 were Amount 8,000, while subscriptions received in advance on the same date were Amount 18,000.

Calculate amount of subscriptions to be credited to Income and Expenditure Account for the year ended 31st March, 2018.

Answer 14:

Question 15 :From the following information, calculate amount of subscriptions to be credited to the Income and Expenditure Account for the year ended 31st March, 2019:

Amount

1st April, 2018 Subscriptions in Arrears 50,000

Subscriptions Received in Advance 30,000

31st March, 2019 Subscriptions in Arrears 25,000

Subscriptions Received in Advance 70,000

Subscriptions received during the year ended 31st March, 2019 - Amount Rs. 3,00,000

Subscriptions still in arrears for the year 2017-18 Rs. 10,000

Answer 15:

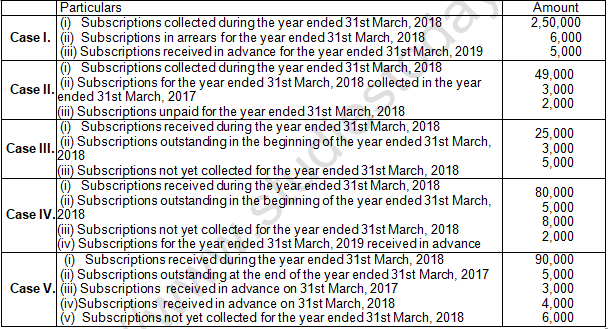

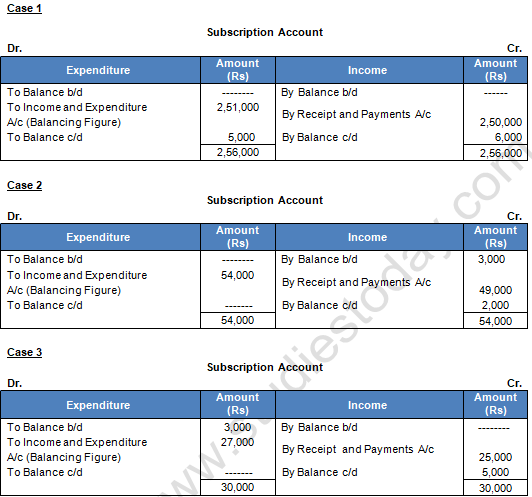

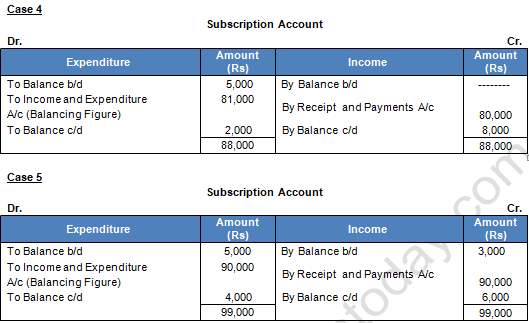

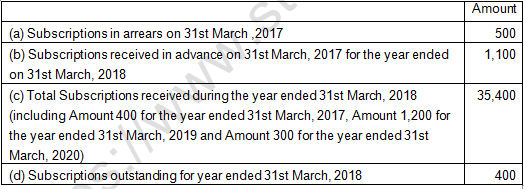

Question 16: Calculate amount of subscriptions which will be treated as income for the year ended 31st March, 2018 for each of the following cases:

Answer 16:

Question 17: From the following particulars, calculate amount of subscriptions to be credited to the Income and Expenditure Account for the year ended 31st March, 2019:

Answer 17:

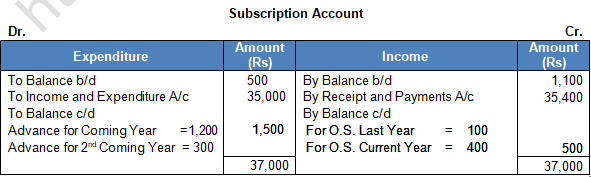

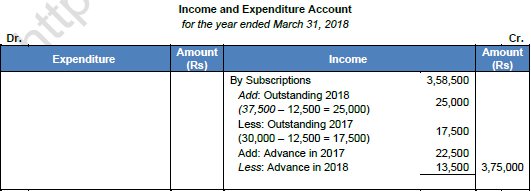

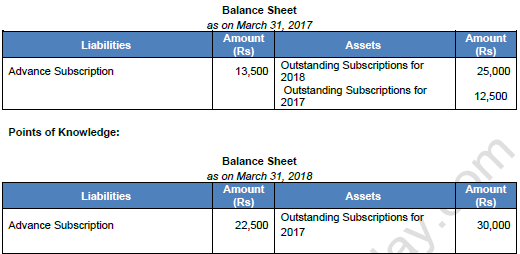

Question 18: How are the following items of subscriptions shown in the Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheets as at 31st March, 2018 and 2019?

Amount

Subscriptions received during the year ended 31st March, 2019 3,58,500

Subscriptions outstanding on 31st March, 2018 30,000

Subscriptions received in Advance on 31st March, 2018 22,500

Subscriptions received in Advance on 31st March, 2019 13,500

Subscriptions outstanding on 31st March, 2019 37,500

(including Amount 12,500 for the year ended 31st March, 2018)

Answer 18:

Question 19: From the following information, calculate amount of subscriptions outstanding for the year ended 31st March, 2019:

A club has 200 members each paying an annual subscription of Amount 1,000. The Receipts and Payments Account for the year showed a sum of Amount 2,05,000 received as subscriptions. The following additional information is provided:

Amount

Subscriptions Outstanding on 31st March, 2018 30,000

Subscriptions Received in Advance on 31st March, 2019 40,000

Subscriptions Received in Advance on 31st March, 2018 14,000

Answer 19:

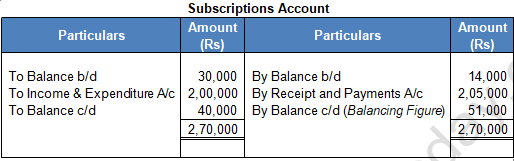

Question 20: From the following information, prepare Subscription Account for the year ending 31st March, 2019:

In the year ending 31st March, 2019, subscription received were Rs. 2,10,000 (including Rs. 6,000 of arrears from previous year) and subscription arrears of previous year were written off Rs. 4,000.

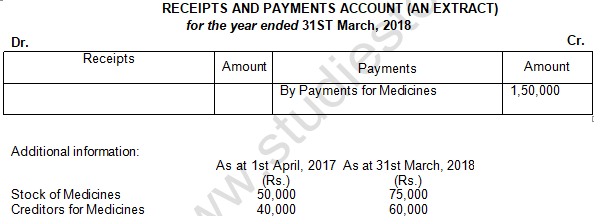

Answer 20:

Calculation of the Amount of Consumable items

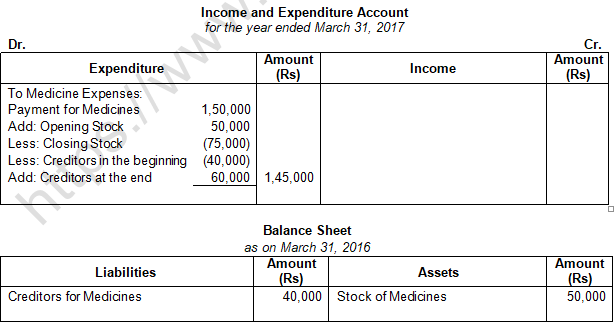

Question 21: On the basis of information given below, calculate the amount of medicines to be debited to the Income and Expenditure Account of Good Health Hospital for the year ended 31st March, 2018:

Medicines purchased during the year ended 31st March, 2018 were Amount 60,80,700

Answer 21:

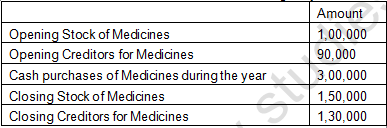

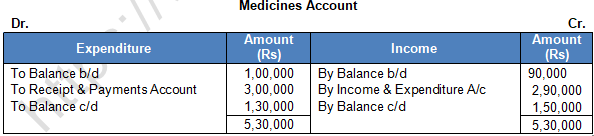

Question 22: Calculate amount of medicines consumed during the year ended 31st March, 2018:

Answer 22:

Calculation of medicine consumed during the year ended 31st March ;

Question 23: Calculate amount to be posted to the Income and Expenditure Account for the year ended 31st March, 2019:

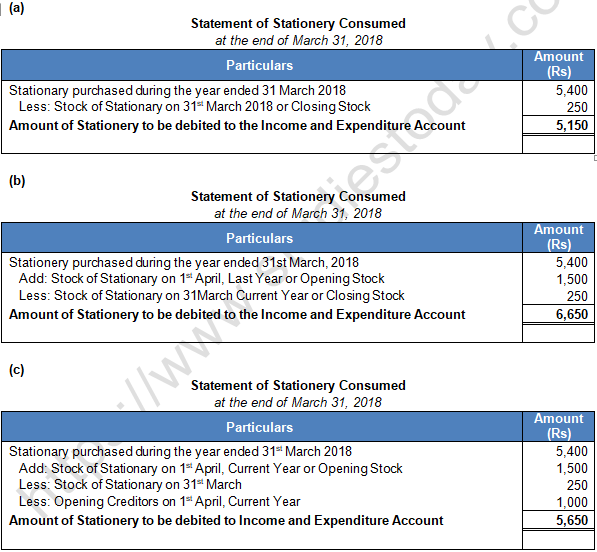

(i) Amount paid for stationery during the year ended 31st March, 2019 ——Rs. 5,400; Stock of Stationery in Hand on 31st March, 2019 ——Rs. 250.

(ii) Stock of Stationery in Hand on 1st April, 2018——Rs. 1,500; Payment made for Stationery during the year ended 31st March, 2019——Rs. 5,400; Stock of Stationery in Hand on 31st March, 2019 ——Rs. 250.

Answer 23:

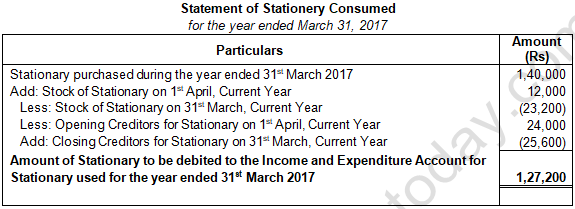

Question 24: On the basis of the following information, calculate amount that will appear against the term ' Stationery Used' in the Income and Expenditure Account for the year ended 31st March, 2018:

Answer 24:

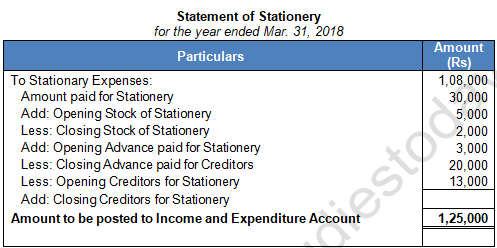

Question 25: Calculate the amount that will be posted to the income and Expenditure Account for the year ended 31st March, 2019:

Answer 25:

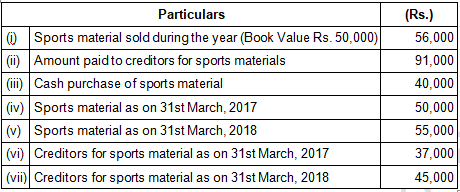

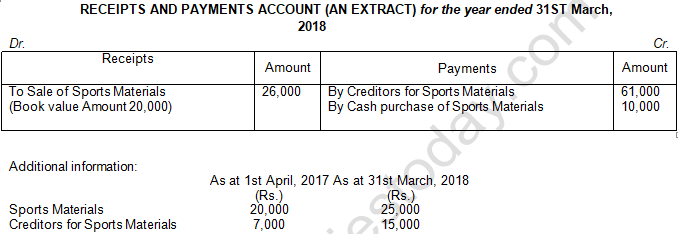

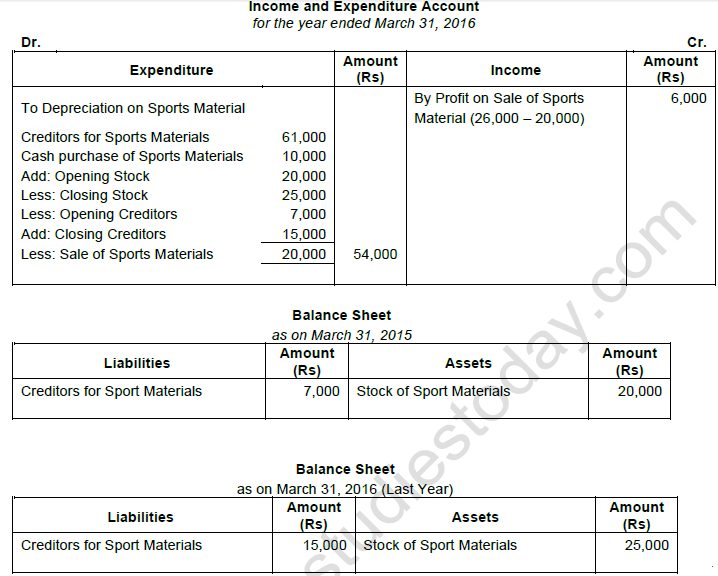

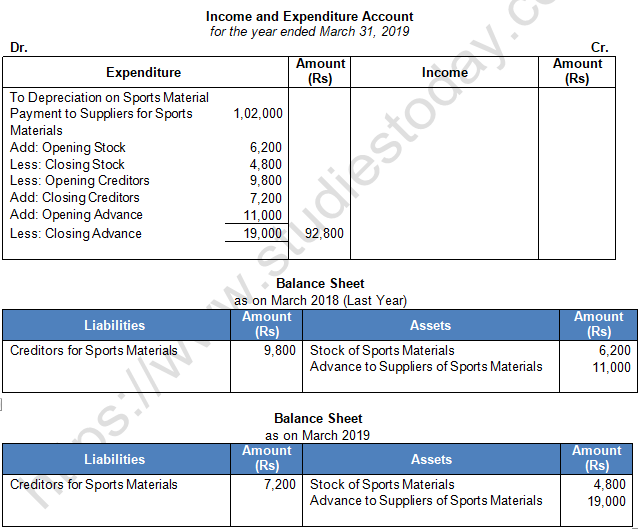

Question 26: Calculate the amount of sports material to be transferred to income and Expenditure Account of Raman Bhalla Sports Club, Ludhiana, for the year ended 31st March, 2018 :

Answer 26:

Question 27: How are the following dealt with while preparing the final accounts for the year ended 31st March, 2018?

Additional information:

(I) Sports Materials in Hand on 31st March, 2018——Amount 22,000

Answer 27:

Question 28: How are the following dealt with while preparing the final accounts for the year ended 31st March, 2018?

Answer 28:

Question 29: How are the following dealt with while preparing the final accounts of a sports club for the year ended 31st March, 2019?

Answer 29:

Question 30: From the following information of a Not-for-Profit Organisation, show the 'Sports Materials' item in the Income and Expenditure Account for the year ended 31st March, 2018 and Balance Sheets as at 31st March, 2019:

Answer 30:

Calculation of Gain (Profit) or Loss on Sale of Fixed Assets

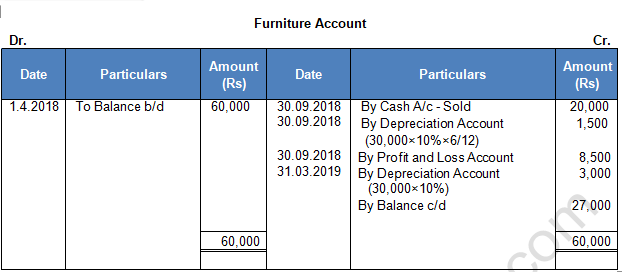

Question 31: The book value of furniture on 1st April, 2018 is Amount 60,000. Half of this furniture is sold for Amount 20,000 on 30th September,2017. Depreciation is to be charged on furniture @ 10% p.a.

Calculate loss on sale of furniture. Show how the loss on sale and depreciation on furniture will be shown in the Income and Expenditure Account for the year ended 31st March, 2019.

Answer 31:

Points of Knowledge:

Loss on Sale of furniture to be shown in the Income and Expenditure Account is Rs 8,500.

Depreciation on sale of furniture to be shown in the Income and Expenditure Account is

1,500 + 3,000 = 4,500

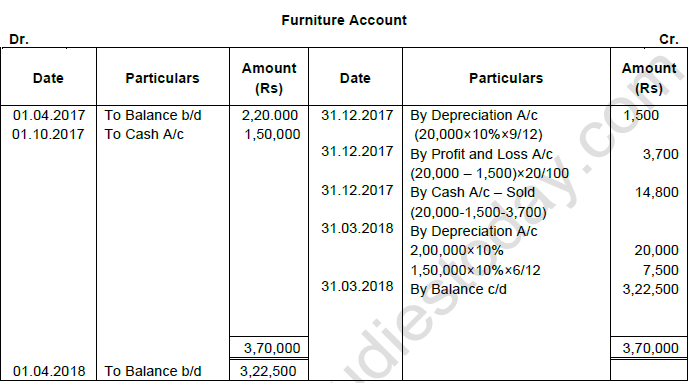

Question 32: Delhi Youth Club has furniture at a value of Amount 2,20,000 in its book on 31st March, 2018. It sold old furniture, having book value of Amount 20,000 as at 1st April, 2018 at a loss of 20% on 31st December, 2018. Furniture is to be depreciated @ 10% p.a. Furniture costing Amount 1,50,000 was also purchased on 1st October, 2018

Prepare Furniture Account for the year ended 31st March, 2019.

Answer 32:

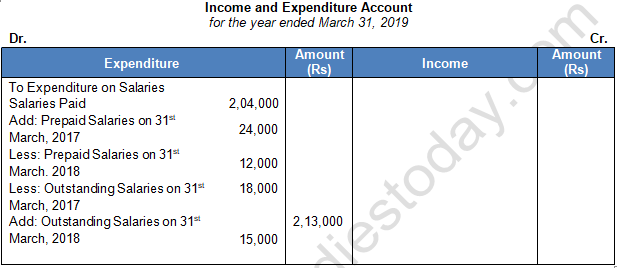

Question 33: In the year ended 31st March, 2018, salaries paid amounted to Amount 2,04,000. Ascertain the amount chargeable to the Income and Expenditure Account for the year ended 31st March ,2019 from the following additional information:

Answer 33:

Question 34: How are the following items dealt with while preparing Income and Expenditure Account of a club for the year ended 31st March, 2018? Locker Rent received during the year ended 31st March, 2018—— Amount 52,000.

Locker Rent received during the year ended 31st March, 2018—— Amount 52,000.

Answer 34:

Preparation of Income and Expenditure Account

Question 35: Prepare Income and Expenditure Account for the year ended 31st March, 2019 from the following:

Answer 35:

Donation of Rs. 10,000 received for Building Fund was wrongly included in the Subscriptions Account. A bill of medicines purchased during the year amounted to Rs. 12,800 was outstanding. Government Grant is not for a specific purpose.

Answer 36:

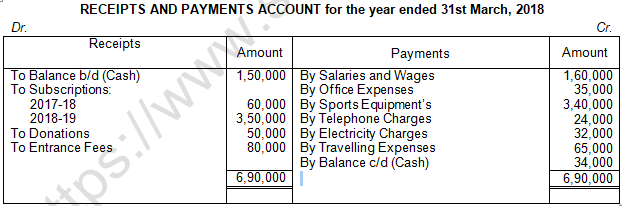

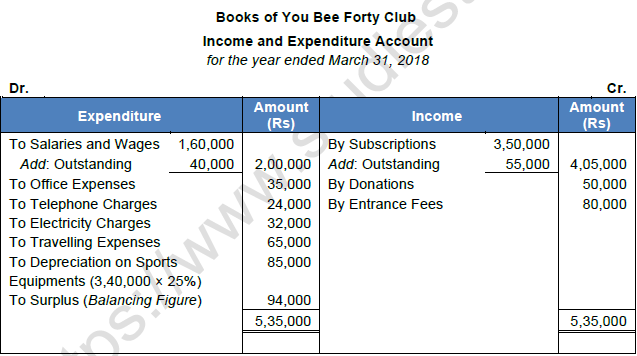

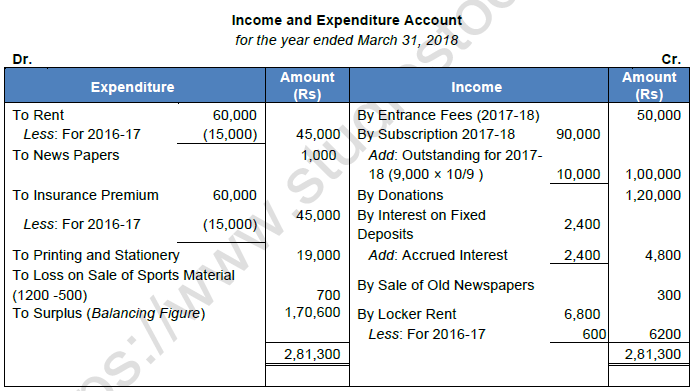

Question 37: Following is the Receipts and Payments Account of You Bee Forty Club for the year ended 31st March, 2018:

Additional Information:

(a) Outstanding Subscriptions for the year ended 31st March, 2018——Rs. 55,000.

(b) Outstanding Salaries and Wages——Rs. 40,000.

(c) Depreciate Sports Equipment’s by 25%.

Prepare Income and Expenditure Account of the club from the above particulars.

Answer 37:

Question 38: From the following Receipts and Payments Account of Jaipur Sports Club, prepare Income and Expenditure Account for the year ended 31st March, 2019:

Answer 38:

Question 39: Following is the information given in respect of certain items of a Sports club. Show these items in the Income and Expenditure Account and the Balance Sheet of the club as at 31st March, 2018:

Answer 39:

Question 40: Prepare Income and Expenditure Account from the following particulars of Youth Club for the year ended on 31st March, 2018:

Additional Information:

(i) Subscription outstanding as at 31st March, 2018 Rs. 16,200.

(ii) Rs. 1,200 is still in arrears for the year 2016-17 for subscription.

(iii) Value of sports material at the beginning and at the year was Rs. 3,000 and Rs. 4,500 respectively.

(iv) Depreciation to be provided @ 10% p.a. on Furniture.

Answer 40:

Question 41: Following is the Receipts and Payments Account of Delhi Football Club for the year ended 31st March, 2019:

Additional Information:

(i) During the year ended 31st March, 2019, the club had 550 members and each paying an annual subscription of Rs. 100.

(ii) Salaries Outstanding as at 1st April, 2018 were Rs. 10,000 and as at 31st March, 2019 were Rs. 5,000.

Prepare Income and Expenditure Account of the Club for the year ended 31st March, 2019.

Answer 41:

Preparation of the Income and Expenditure Account and Balance Sheet from Receipts and Payments Account with Additional Information

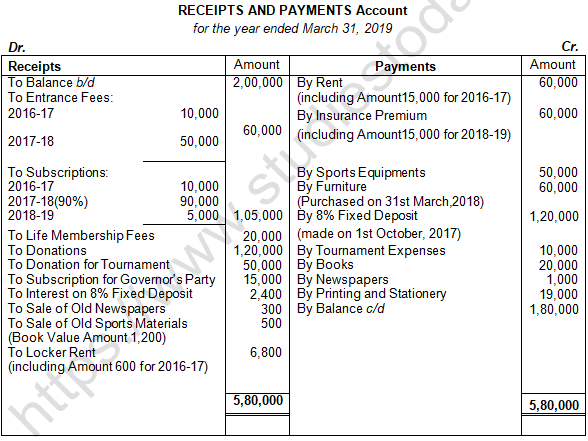

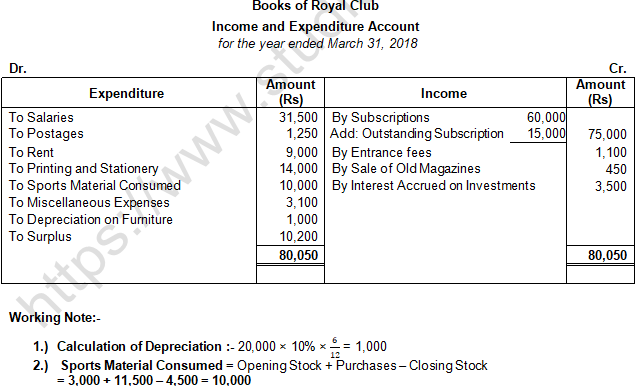

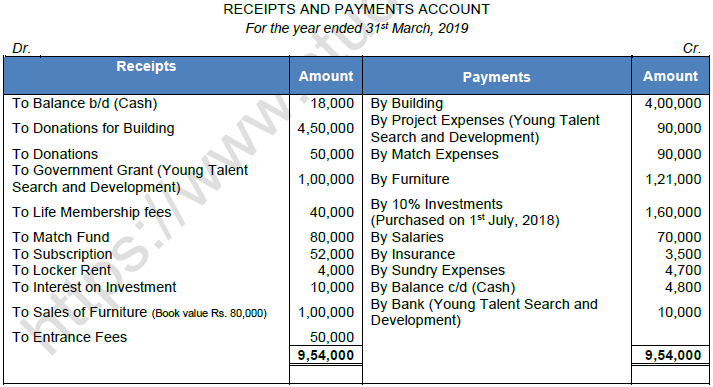

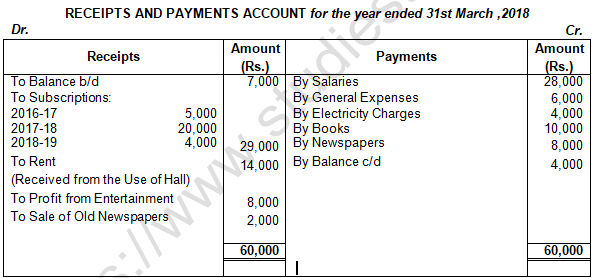

Question 42: Following is the summary of cash transactions of the Royal Club for the year ended 31st March, 2019:

In the beginning of the year, the club possessed Books of Rs. 2,00,000 and Furniture of Rs. 85,000. Subscriptions in arrears in the beginning of the year amounted to Rs. 3,500 and at the end of the year Rs. 4,500 and six month’s Rent Rs. 6,000 was due both in the beginning of the year and at the end of the year.

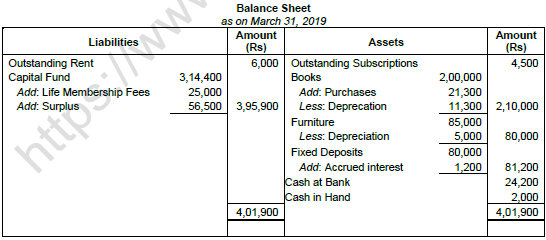

Prepare Income and Expenditure Account of the club for the year ended 31st March, 2019 and is Balance Sheet as at that date after writing off Amount 5,000 and Amount 11,300 on Furniture and books respectively.

Answer 42:

Question 43: From the following Receipts and Payments Account of City Club and from the information supplied, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date:

(a) The club has 50 members each paying an annual subscription of Amount 500. Subscriptions Outstanding on 31st March,2017 were Amount 6,000.

(b) On 31st March, 2018, Salaries Outstanding amounted to Amount 2,000. Salaries paid in the year ended 31st March, 2018 included Amount 6,000 for the year ended 31st March, 2017.

(c) On 1st April, 2017, the club owned Building valued at Amount 2,00,000; Furniture Amount 20,000 and Books Amount 20,000.

(d) Provide depreciation on Furniture at 10%.

Answer 43:

Question 44: From the following Receipts and Payments Account and additional information given below, prepare Income and Expenditure Account and Balance Sheet of Rural Literacy Society as on 31st March, 2018:

Additional information:

(i) Subscription outstanding as on 31st March, 2017 Amount 20,000 and on 31st March, 2018 Amount 15,000.

(ii) On 31st March, 2018, salary outstanding Amount 6,000 and one month rent paid in advance.

(iii) On 1st April, 2017, society owned furniture Amount 1,20,000 and books Amount 50,000.

Answer 44:

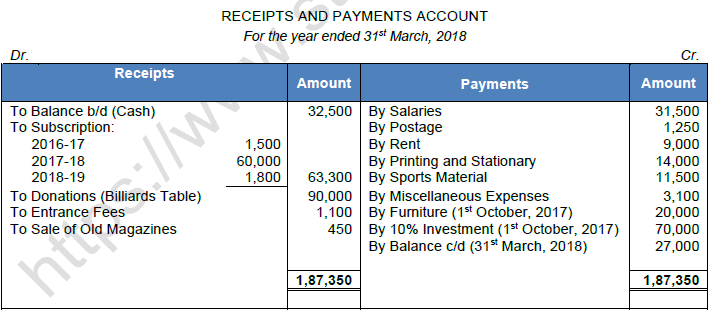

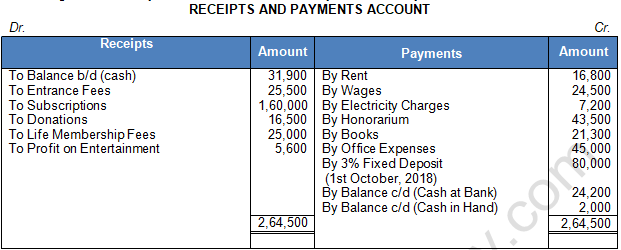

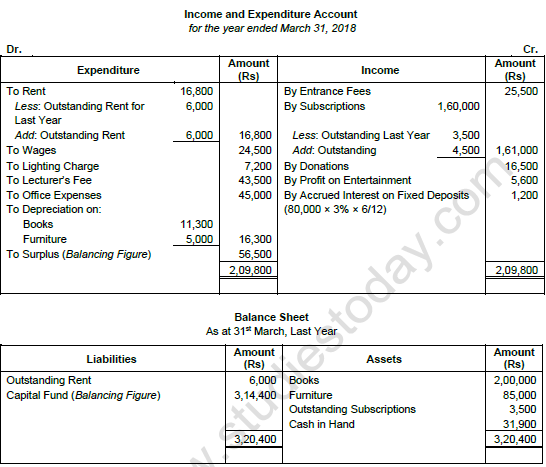

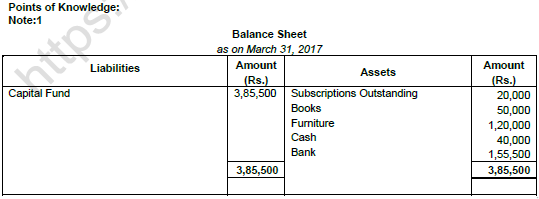

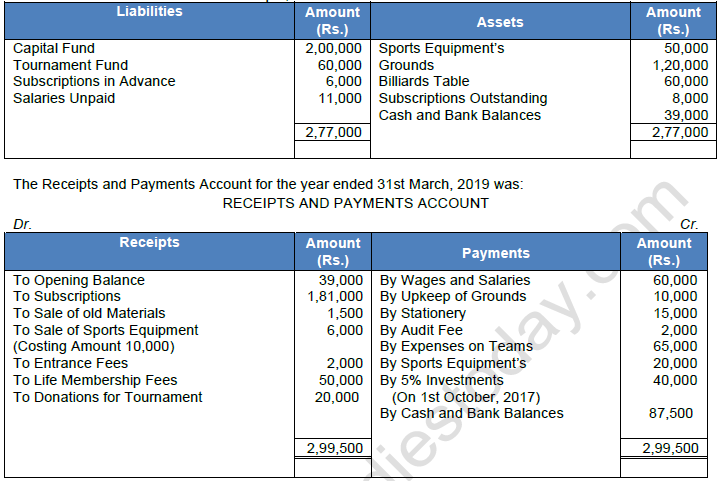

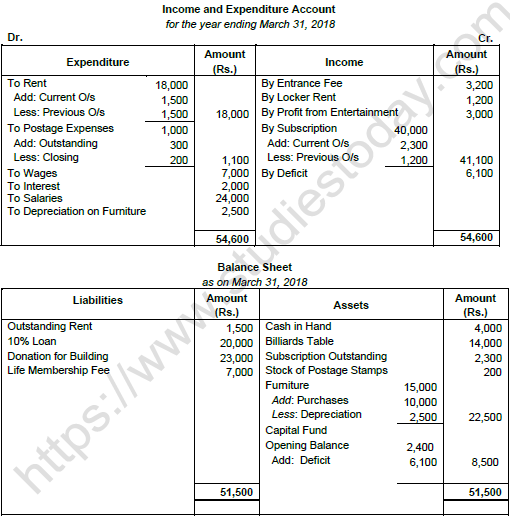

Question 45: Glaxo Club's Balance Sheet as at 1st April, 2018 was as under:

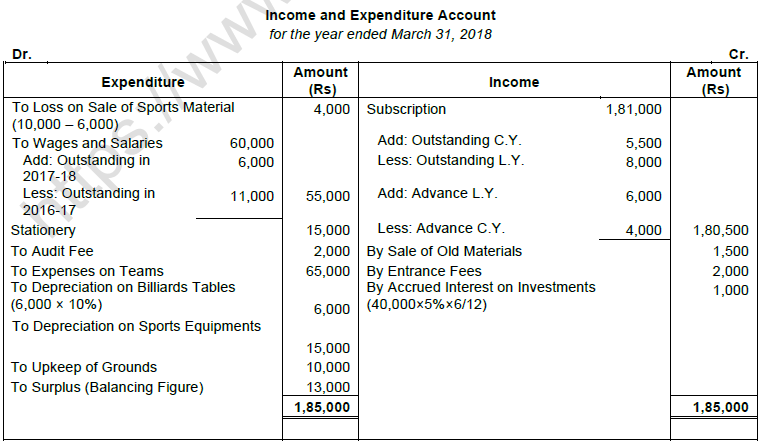

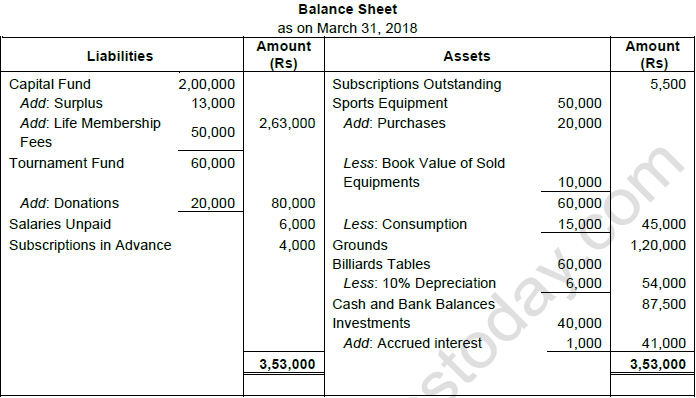

Subscriptions still to be received are Rs. 5,500 but subscriptions already received include Rs. 4,000 for next year. Salaries still unpaid are Rs. 6,000. Sports Equipment’s are now valued at Rs. 45,000. Prepare Income and Expenditure Account and the Balance Sheet, after charging 10% depreciation on Billiards Tables.

Answer 45:

Question 46: From the following information relating to the Star Cricket Club, prepare Income and Expenditure Account for the year ended 31st March, 2018 and Balance Sheet as at that date. The summary of cash transactions is:

Answer 46:

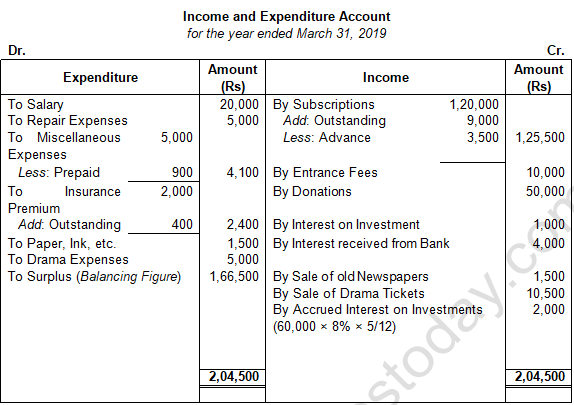

Question 47: From the following Receipts and Payments Account of Mumbai Theatre Club, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date.

Additional Information:

(i) Subscriptions in arrear for the year ended 31st March, 2019 Rs. 9,000 and subscriptions in advance for the year ended 31st March, 2019 Rs. 3,500.

(ii) Insurance Premium outstanding Rs. 400.

(iii) Miscellaneous expenses prepaid Rs. 900.

(iv) 8% interest has accrued on investment for five months.

(v) Billiard Table costing Rs. 3,00,000 was purchased during last year and Rs. 2,20,000 were paid for it.

Answer 47:

Prepare Income and Expenditure Account for the year ended 31st March, 2019, and Balance Sheet as on that date after the following adjustments:

(i) Insurance premium was paid in advance for three months.

(ii) Interest on investment Rs.11,000 accrued was not received.

(iii) Rent Rs. 6,000; Salary Rs. 9,000 and advertisement expenses Rs. 10,000 outstanding as on 31st March, 2019.

Answer 48:

Question 49: Given Below is the Receipts and Payments Account of a Mayur Club for the year ended 31st March, 2019:

Prepare club's Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date after taking the following information into account:

(i) There are 500 members, each paying an annual subscription of Rs. 500, Rs. 5,000 are still in arrears for the year ended 31st March, 2018.

(ii) Municipal Taxes amounted to Rs. 4,000 per year is paid up to 30th June and Rs. 5,000 are outstanding of salaries.

(iii) Building stands in the books at Rs. 5,00,000.

(iv) 6% interest has accrued on investments for five months.

Answer 49:

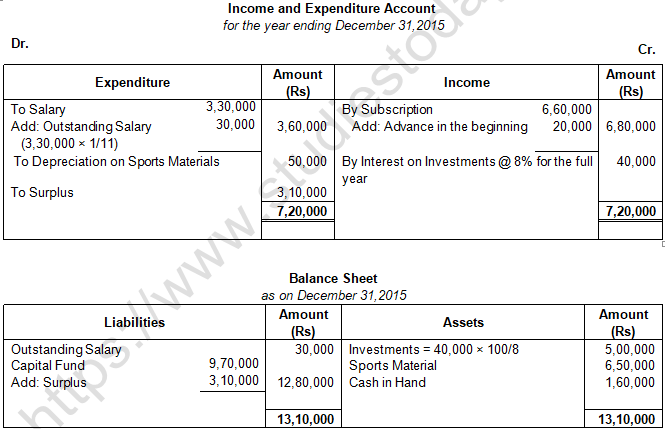

Question 50: From the following Receipts and Payments Account of Imran Khan club and from the given additional information, prepare Income and Expenditure Account for the year ending 31st December, 2015 and the Balance Sheet as at that date:

Additional Information:

(i) The club had received Amount 20,000 for subscription in 2017-18 for 2018-19.

(ii) Salaries had been paid only for 11 months

(iii) Stock of sports materials on 31st December, 2018 was Rs. 3,00,000 and on 31st December, 2015 Rs. 6,50,000

Answer 50:

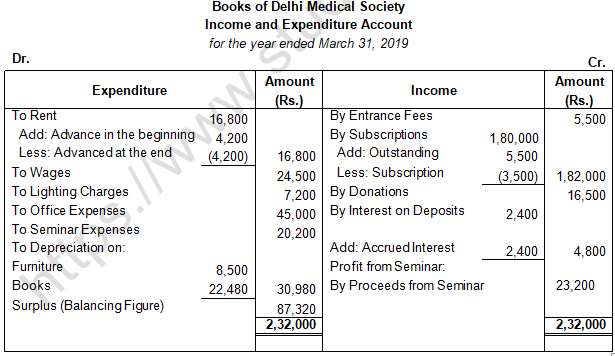

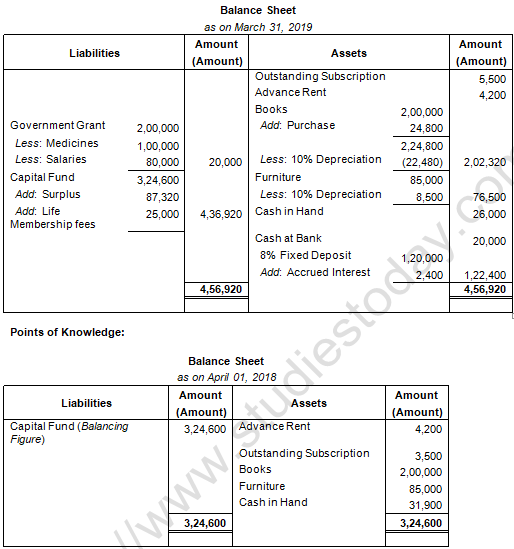

Question 51: From the following information and Receipts and Payments Account of Delhi Medical Society, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date.

Other information:

On 31st March, 2018, the club possessed books of Rs. 2,00,000 and Furniture of Rs. 85,000. Provide depreciation on these assets @ 10% including the purchases during the year.

Subscriptions in arrears in the beginning of the year amounted to Rs. 3,500 and at the end of the year Rs. 5,500 were outstanding.

The Club paid three months' rent in advance both in the beginning and at the end of the year.

Answer 51:

Question 52: Receipts and Payments Account of Shankar Sports Club is given below, for the year ended 31st March, 2019:

Prepare Income and Expenditure Account and Balance Sheet with the help of following information:

Subscription outstanding on 31st March, 2018 is Rs. 1,200 and Rs. 2,300 on 31st March, 2018; opening stock of postage stamps is Rs. 300 and closing stock is Rs. 200; Rent Rs. 1,500 related to the year ended 31st March, 2018 and Rs. 1,500 is still unpaid. On 1st April, 2018 the club owned furniture Rs. 15,000, Furniture valued at Rs. 22,500 on 31st March, 2018. The club has a loan of Rs. 20,000 (@10% p.a.) which was taken, in year ended 31st March,2018.

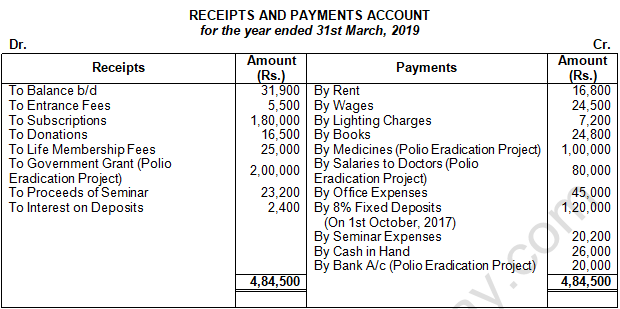

Answer 52:

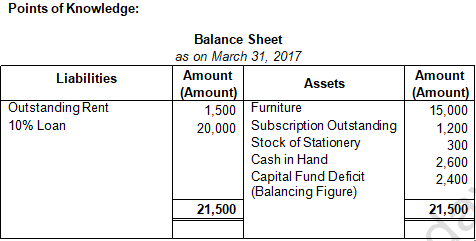

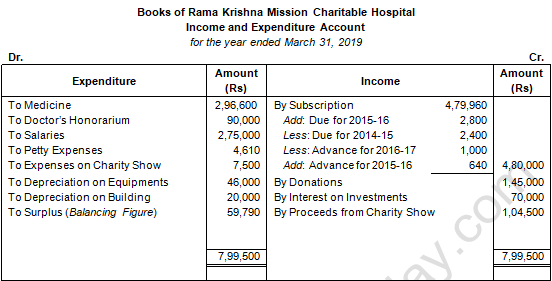

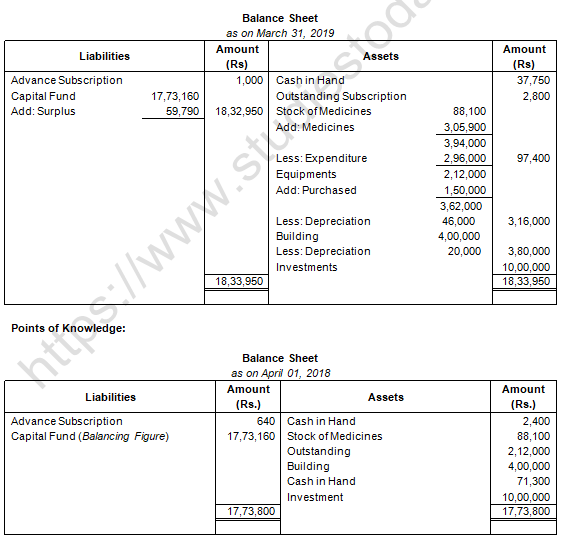

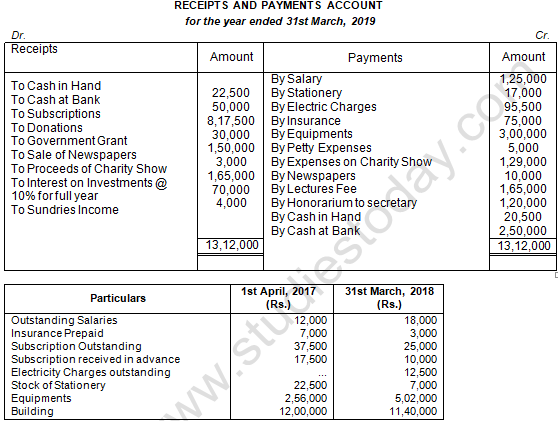

Question 53: From the following particulars relating to the Ramakrishna Mission Charitable Hospital, prepare Income and Expenditure Account for the year ended 31st March, 2019 and Balance Sheet as at that date.

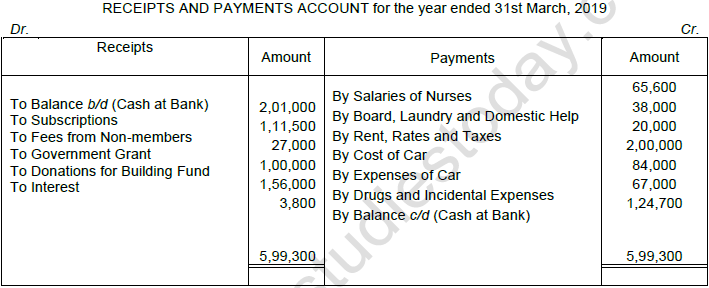

Answer 53:

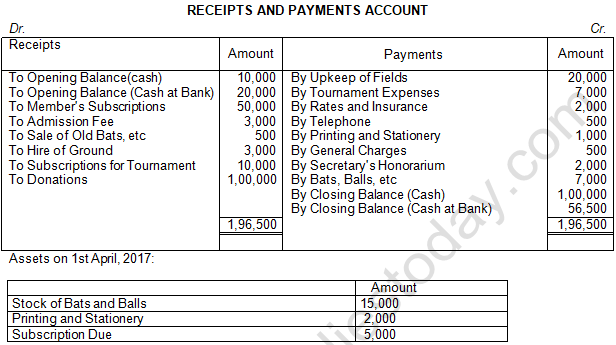

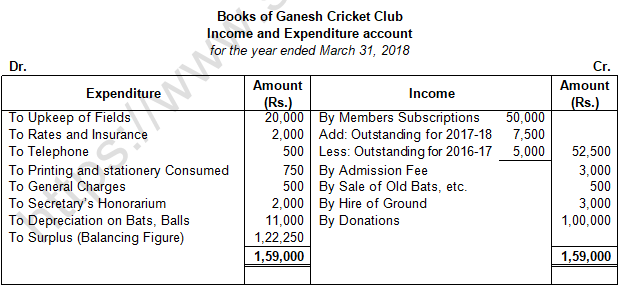

Question 54: Following is the Receipt and Payment Account of Women's Welfare Club for the year ended 31st March, 2019:

Prepare Income and Expenditure Account for the year ended 31st March, 2019, and Balance Sheet as on that date.

Answer 54:

Point to Remember:-

1) Calculate Opening Capital Fund: If opening balance of the Capital Fund is not given, Balance Sheet in the beginning of the year is prepared. It is prepared by taking the opening cash and bank balance as given in the Receipts and Payment Account, other assets and liabilities as given in the additional information.

2) Determine Items of Income from Receipts and Payment Account: Receipts and Payment Account records all receipts, whether they relate to current, previous or future periods and whether they are of revenue or capital nature.