Read TS Grewal Solution Class 12 Chapter 3 Goodwill Nature and Valuation 2026. Students should study TS Grewal Solutions Class 12 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 12 Accountancy have been prepared by expert teachers. These TS Grewal Class 12 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 12 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 12 Accounts Chapter 3 Goodwill Nature and Valuation TS Grewal Solutions

TS Grewal Solutions for Chapter 3 Goodwill Nature and Valuation Class 12 Accounts have been provided below based on the latest TS Grewal Class 12 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 12 will help students to improve their concepts and easily solve accountancy questions for Class 12.

Chapter 3 Goodwill Nature and Valuation TS Grewal Class 12 Solutions

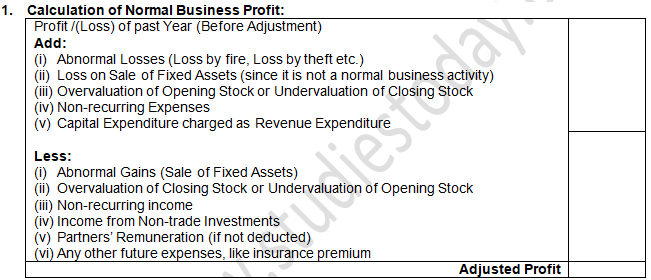

About this chapter: TS Grewal Class 12 Chapter 3 provides a detailed understanding relating to the concepts of Goodwill and different methods used to value goodwill. As valuing goodwill is crucial, especially during mergers and acquisitions, as it can impact the valuation of the entire business. The valuation of goodwill is an important part of any business. Though its an intangible asset but its valuation is very essential for all types of businesses. Correct accounting treatment is essential to make sure the books of account show correct amount of goodwill. Its important to understand that goodwill is an essential element of a company's value, and understanding its nature and valuation is important for students as its used by all businesses and accountants. As valuing goodwill is a complex process, therefore detailed explanation has been provided in TS Grewal's Class 12 Accountancy book so that students can understand how to calculate it and easily solve questions in exams. Our Class 12 accountancy teachers have provided detailed solutions to all questions given in this chapter.

Question 1. Define Goodwill.

Answer 1:

Goodwill is a thing very easy to describe, very difficult to define. It is the benefit and advantage of the good name, reputation and connections of a business. It is the attractive force which brings in customers. It is one thing which distinguishes an old established business from a new business at its first start.

Question 2. State any three circumstances other than (i) admission of a new partner, (ii) retirement of a partner and (iii) death of a partner, when need for valuation of goodwill of a firm may arise.

Answer 2:

The need for valuation of goodwill arises in the following circumstances:

1.) When there is a change in the profit sharing ratio.

2.) When partnership firm is sold as a going concern.

3.) When two or more firms amalgamate.

Question 3. Give any two features of Goodwill.

Answer 3:

Below are the features of Goodwill:-

1.) It is an intangible asset i.e. an asset which cannot be seen and touched.

2.) It does not have an existence separate from that of an enterprise. Thus, it has realisable value when business is sold.

Question 4. What is meant by Purchased Goodwill?

Answer 4:

Purchased Goodwill is that goodwill which is acquired by a firm for a consideration, whether paid in cash of kind. For example, when a business is purchased and purchase consideration is more than value of net assets (i.e. Assets – Liabilities), the difference amount is the value of purchased goodwill.

Question 5. What is meant by Self-generated Goodwill?

Answer 5:

Self-generated goodwill is that goodwill which is not purchased for a consideration but is earned by the efforts of the management (or partners). It is an internally generated goodwill which arises from a number of factors (such as favourable location, efficient management, good quality of products, etc.) that a running business possess due to which it is able to earn higher profit.

Question 6. What is meant by Average Profit?

Answer 6:

Goodwill under Average Profit Method can be calculated either by:

(i) Simple Average Profit Method: Under Simple Average Profit Method, normal business profits earned by the business for the specified number of years are considered. Profits earned are totalled and average is determined. Average profit as calculated is multiplied by a number of year’s purchase to determine the value of goodwill. In the form of formula, value of Goodwill = Average Profit ᵡ Number of year’s Purchase.

(ii) Weighted Average Profit Method: It is a method whereby weight is assigned to each year and thereafter, normal business profit of each year is multiplied by the assigned weight to determine the value. Recent year’s profit being more relevant in determining value of Goodwill is assigned higher weight.

Weighted Average Profit Method is considered better as compared to Simple Average Profit Method as it gives more weightage to the profit of recent year. This method is particularly effective when profit show rising or falling trends.

Question 7. What are 'Super Profits?

Answer 7:

Capital employed in a business yields profit. Some of the enterprises earn more profit, while other earn less profit or incur loss on the same amount of capital employed. When a similar type of business earns profit at a certain percentage of the capital employed it called normal return. But a buyer’s advantage lies in the excess of the normal return on capital employed. It is only such enterprises which enjoy goodwill. The excess of actual profit over the normal profit is known as super profit.

Question 8. What is meant by Capitalisation of Average Profit?

Answer 8:

In this method goodwill is calculated by deducting capital employed (i.e., Net Assets as on the date of valuation) in the business from the capitalised value of average profit on the basis of Normal Rate of Return.

![]()

Question 9. What is meant by Capitalisation of Super Profit?

Answer 9:

In this method, goodwill is calculated by capitalising super profit at the normal rate of return. Thus, as a first step Super Profit is determined on the same basis as is determined under Super Profit Method, which is capitalised at the Normal Rate of Return to determine the value of goodwill.

![]()

Question 10. Why is Goodwill considered as an intangible asset but not a fictitious asset?

Answer 10:

Goodwill is a valuable intangible asset like patents, trademarks, copyrights, etc. It is not depreciated like tangible assets but is amortised over its useful life. Intangible Assets prescribes that goodwill should not be recorded in the books of account unless consideration is paid for it.

Fictitious assets are the expenses of a firm such as expenditure on formation of business, debit balance of profit and loss account, deferred revenue expenditure, etc., which are still to be charged against the profits. They all have a debit balance and cannot be considered as assets of the firm.

Question 11. State any two factors affecting the value of Goodwill of a firm.

Answer 11:

Goodwill of a firm is affected by all the factors which increase the earning capacity of the firm. These factors are:

(i) Efficient Management:- If the management is experienced capable and competent, the firm will earn higher profit as compared to other firms. It will, thus, increase the value of goodwill.

(ii) Favourable Location:- If the business is located at a favourable place, resulting in increased customer walk-in and, therefore, sale, the value of goodwill will be higher.

Question 12. How does the factor 'efficiency of management' affect the Goodwill of a firm?

Answer 12:

If the management is experienced capable and competent, the firm will earn higher profit as compared to other firms. It will, thus, increase the value of goodwill.

Question 13. How does the factor 'quality of product' affect the Goodwill of a firm?

Answer 13:

If a firm enjoys good reputation for the quality of its products, there will be a ready sale and the value of its goodwill, therefore, will be high.

Question 14. How does location affect the Goodwill of a business?

Answer 14:

If the business is located at a favourable place, resulting in increased customer walk-in and, therefore, sale, the value of goodwill will be higher.

Question 15. How does the market situation affect the value of Goodwill of a firm?

Answer 15:

If a firm is in a business wherein demand for the products dealt in is higher than the supply, it will lead to lower capital requirement and higher profit. It will, thus, increase the value of its goodwill.

Question 16. How does the nature of business affect the value of Goodwill of a firm?

Answer 16:

It the business of a firm is of the nature where the products dealt in are in high demand although not short in supply, the profit will be higher. It will, thus, increase the value of its goodwill.

Question 17. Name any four factors which affect the Goodwill of a partnership firm.

Answer 17:

Below are the factors affecting the goodwill of a partnership firm:-

1.) Efficient Management

2.) Access to Supplies

3.) Market Situation

4.) Risk Associated with Business

Question 18. Give the formula for calculation of Goodwill by Capitalisation of Average Profit.

Answer 18:

![]()

Question 19. Give the formula for calculation of Goodwill by 'Capitalisation of Super Profit Method'.

Answer 19:

![]()

Question 20. Enumerate two main steps involved in valuing Goodwill according to Super Profit Method.

Answer 20:

Question 21. Suraj and Dilip are partners in a firm dealing in stationery items. The firm is well managed and advantage of being cost effective. It buys stationery items at reasonable cost from Dilip's relative manufacturer of stationery items. The firm's sale outlet is situated near a school. As a result, the firm h demand of stationery items and is earning good profits. The firm is donating 10% of its profits to the school for the education of the students of below poverty line. State any two factors affecting the goodwill of the firm. Also, identify any two values which the firm is trying to propagate.

Answer 21:

Two factors affecting the value of goodwill of the firm:

(a) Efficiency of management

(b) Favourable location

Two Values:

(a) Sensitivity towards promotion of education among the student of below poverty line.

(b) Promoting healthy trade practices in the society.

2021–Rs.12,000; 2022–Rs.18,000; 2023–Rs.16,000; 2024–Rs.14,000.

Calculate amount of Goodwill

Goodwill under Average Profit method = Average profit per year × Years Purchase

Goodwill under Average Profit method = 15,000 × 3

Goodwill under Average Profit method = 45,000

Working Note:-

Average profit = (Total Profit)/(Total Years)

Average profit = 12,000+18,000+16,000+14,000 / 4 Years

Average profit = 15,000

About Solution:

Change in profit sharing Ratio among the existing partners for example A and B are partners in a firm sharing ratio of 2:1 in future they decide to share profit in the ratio of 3:1 its amount to reconstitution of the firm.

Things to Remember:

Admission of a new partner for example Charu and Dinesh are partners sharing profit equally on April 1, 2019 they decided to admit Sudha as a new partners with ¼th share it result into reconstitution of the firm.

Important Notes:

Retirement of an existing partner for example Babita, Gita and Sita are partner sharing profit in the ratio of 1:2:3Sita retires from the firm on March 31 2019 it amounts reconstitution of the firm.

Year 2020–Rs 4,00,000 Year 2021–Rs 3,98,000; Year 2022–Rs 4,50,000; Year 2023–Rs 4,45,000; Year 2024–Rs 5,00,000.

Calculate goodwill of the firm on the basis of 4 years' purchase of 5 years' average profit

Goodwill under Average Profit method = Average profit per year × Years Purchase

Goodwill under Average Profit method = Rs. 4,38,600 × 4

Goodwill under Average Profit method = Rs. 17,54,400

Working Note:-

Average profit = Total Profit)/(Total Years

Average profit = (4,00,000+3,98,000+4,50,000+4,45,000+5,00,000 ) (5 Years

Average profit = 21,93,000/5

About Solution:

As a result of changing in profit sharing ratio one or more of the existing partners gain some portion of other partners share of profit the ratio of gain of profit sharing ratio is gain of profit sharing ratio is called gaining ratio it is calculated as follow:

Gaining ratio = New ratio – Old ratio

Things to Remember:

Amalgamation of two partnership firms for example A and B are partners in a firm sharing profit and ratio of 2:1 To eliminate compensation they amalgamate their firm with the firm of C and D who are sharing profit in the ratio of 3:1 they new ratio for A,B,C and D are agreed at 2:1:3:1 it amounts to recantation of the firm of A and B on the one hand and the firm C and D on the other hand and new reconstituted firm is formed.

Important Notes:

Sometimes the existing partner decide to change their profit sharing ratio the change is necessitated due to change in capital contribution or in active participation in management as a result of a change in profit sharing ratio one or more of the existing partner my acquire extra share in profit at the cost of one or more of other partners in such a case in order to maintain equality among the partner it is necessary to make adjustment for goodwill revaluation of assets and liabilities reserve accumulated profit and losses etc. these adjustment are similar to those made at the time of admission or retirement of a partner.

Question 3: Purav and Purvi are partners in a firm sharing profits and losses in the ratio of 2:1. They decide to take Purav into partnership for 1/4th share on 1st April, 2019. For this purpose, goodwill is to be valued at four times the average annual profit of the previous four or five years, whichever is higher. The agreed profits for goodwill purpose of the past five years are:

![]()

Answer 3:

Option 1:-

Goodwill under Average Profit method = Average profit per year × Years Purchase

Goodwill under Average Profit method = Rs. 14,100 × 4

Goodwill under Average Profit method = Rs. 56,400

Option 2:-

Goodwill under Average Profit method = Average profit per year × Years Purchase

Goodwill under Average Profit method = Rs. 14,125 × 4

Goodwill under Average Profit method = Rs. 56,500

Goodwill of the firm will be the higher value of the above two options i.e, 56,400 or 56,500. So the goodwill of the firm will be 56,500.

Working Note:-

Calculation of Average profit for Five Years:-

Average Profit = Total Profit / Total Years

Average Profit = 14,000 +15,500 +10,000 +16,000 + 15,000 / 5 Years

Average Profit = 70,500/5

Average Profit = 14,100

Calculation of Average profit for Four Years:-

Average Profit = Total Profit / Total Years

Average Profit = 15,500 +10,000 +16,000 + 15,000 / 4Years

Average Profit = 56,500/4

Average Profit = 14,125

About Solution:

It is valuable only when entire business is sold goodwill cannot be sold in part it can be sold with the entire business only the only exceptions is at the time of admission and retirement of a partner.

Things to Remember:

It is difficult to place and exact value of may fluctuate from time to time due to changing circumstances which are internal and external to business.

Important Notes:

Goodwill is an a intangible assets since it has not physical existence and cannot be seen or touched but it is not a fictitious assets do not have a value whereas goodwill has a value in case of profit making concerns it can be sold thought a sale will be possible along with the sale of the entire business.

Profit of 2020-21 was calculated after charging ₹ 25,000 for abnormal loss of goods by fire

Average Profit = (1,25,000+1,00,000+1,87,500-62,500+1,25,000)/5

Average Profit = 5,00,000/5

Average Profit = Rs. 1,00,000

Goodwill = Average Profit × Number of Year purchases

Goodwill = Rs. 1,00,000 × 3

Goodwill = Rs. 3,00,000

Q5: Madhu and Vidhi are partners sharing profits in the ratio of 3 : 2. They decided to admit Manu as a partner from 1st April 2023 on the following terms:

(i) Manu will be given a 2/5th share of the profit.

(ii) Goodwill of the firm will be valued at two years’ purchase of three years’ normal average profit of the firm.

Profits of the previous three years ended 31st March were:

2023 – Profit ₹ 30,000 (after the debiting loss of stock by fire ₹ 40,000).

2022 – Loss ₹ 80,000 (includes voluntary retirement compensation paid ₹ 1,10,000).

2021 – Profit ₹ 1,10,000 (including a gain (profit) of ₹ 30,000 in the sale of fixed assets).

Calculate the value of goodwill.

Answer 5:

Normal Profit after Adjustment-

Profit for the year 2024 = Rs. 30,000 + Rs. 40,000 = Rs. 70,000

Profit for the year 2023 = (Rs. 80,000) + Rs. 1,10,000 = Rs. 30,000

Profit for the year 2022 = Rs. 1,10,000 – Rs. 30,000 = Rs. 80,000

Average Profit of 3 Year = 70,000+30,000+80,000 / 3

Average Profit of 3 Year = 1,80,000 / 3

Average Profit of 3 Year = Rs. 60,000

Goodwill = Average Profit × 2 year of purchases

Goodwill = Rs. 60,000 × 2

Goodwill = Rs. 1,20,000

Q6: Tarang purchased Jyoti’s business with effect from 1st April 2024. Profits shown by Jyoti’s Business for the last three financial years ended 31st March were:

2022 : ₹ 1,00,000 (including an abnormal gain of ₹ 12,500).

2023 : ₹ 1,25,000 (after charging an abnormal loss of ₹ 25,000).

2024: ₹ 1,12,500 (excluding ₹ 12,500 as insurance premium on firm’s property – now to be insured).

Calculate the value of the firm’s goodwill on the basis of two years’ purchase of the average profit of the last three years.

Answer 6:

Normal Profit after Adjustment:-

Profit for the year 2022 – Rs. 1,00,000 – Rs. 12,500 = Rs. 87,500

Profit for the year 2023 – Rs. 1,25,000 – Rs. 25,000 = Rs. 1,50,000

Profit for the year 2024 – Rs. 1,12,500 – Rs. 1,25,000 = Rs. 1,00,000

Average profit = 87,500+1,50,000+1,00,000 / 3

Average profit = Rs. 1,12,500

Goodwill = Average Profit × Number of year purchases

Goodwill = Rs. 1,12,500 × 2

Goodwill = Rs. 2,25,000

Average Profit = Total Profit / Total Years

Average Profit = 1,50,000+3,50,000+5,00,000+7,75,000-6,00,000 / 5 Years

Average Profit = 11,75,000/5

Average Profit = Rs. 2,35,000

Goodwill = Average Profits × No. of years of Purchase

Goodwill = Rs. 2,35,000 × 4

Goodwill = Rs. 9,40,000

Working Note:-

Calculation of Normal Profits for the year 31st March, 2018:-

Normal Profit = Total Profits + Purchase of car wrongly debited - Depreciation on Car - Nontrade Investments

Normal Profit = Rs. 7,10,000 + Rs. 1,00,000 – Rs. 25,000 – Rs.10,000

Normal Profit = Rs. 7,75,000

Calculation of Normal Profits for the year 31st March, 2019:-

Normal Profit = Total Loss + Income from Non - Trade Investments

Normal Profit = Rs. 5,90,000 + Rs. 10,000

Normal Profit = Rs. 6,00,000

About Solution:

Nature of goods if a business deal in goods of daily use it will have steady profit as the demand for these goods will be stable such business will have more goodwill but if it deals in fancy goods its profit will uncertain and as such the value of the goodwill will be less.

Things to Remember:

Possession of license ifa firm holds an import license the goodwill of the firm will be more as it will be very difficult for other firm to enter this business in the absence of this license.

Important Notes:

Monopolistic and other rights if a business enjoy monopoly market it will have assured profit similarly if it holds some special rights such as partners trademarks copyrights or concessions etc. it will have more goodwill.

Books of Account revealed that:

(i) Abnormal loss of Rs. 20,000 was debited to Profit and Loss Account for the year ended 31st March, 2021.

(ii) A fixed asset was sold in the year ended 31st March, 2022 and gain (profit) of Rs. 25,000 was credited to Profit and Loss Account.

(iii) In the year ended 31st March, 2023 assets of the firm were not insured due to oversight. Insurance premium not paid was Rs. 15,000. Calculate the value of goodwill.

Answer 8:

Goodwill under Average Profit Method = Average Normal Profit per year × Years Purchase

About Solution:

There is no concrete a genuine basis of selecting the number of past year on which average profit is to calculate.

Things to Remember:

In average profit method average profit are multiplied by number of years (such as two or three) to find out the value of goodwill however the number of year of purchase used are based on estimation hence the value of goodwill cannot be stated as satisfactory there should be some concrete or genuine basis for determining the number of year of purchase rather than based on estimated.

Important Notes:

Capital employed is not considered while calculating average profit earned by two firm engaged in the same type business may be the same whereas capital employed by the two firms may be different hence average profit cannot be the proper base for calculation of goodwill.

Question 9: Profits of a firm for the year ended 31st March for the last five years were:

About Solution:

Capitalization of super profit method under this method first of all we calculate the super profit and then we assess the capital needed for earning some super profit on the basis of normal rate of return such capital is actually the amount of goodwill following formula is used to calculate goodwill

Goodwill= Super profit ×100/(normal rate of return )

Things to Remember:

Assets and liabilities of a firm must also be revalued at the time of change in profit sharing ratio of existing partners the reason is that the realizable or actual value of assets and liabilities may be different from those show in the balance sheet it is possible that with the passage of time some of assets might have appreciated in the value while the value of certain other assets might have decreased and no record has been made of such change in the books of accounts.

Important Notes:

For decrease in the value of assets:

Revaluation A/c Dr.

To Assets A/c

(Decrease in the value of assets)

Question 10: Raman and Daman are partners sharing profits in the ratio of 60:40 and for the last four years they have been getting annual salaries of Rs. 50,000 and Rs. 40,000 respectively. The annual accounts have shown the following net profit before charging partners' salaries:

Year ended 31st March, 2022 – Rs. 1,40,000; 2023 – Rs. 1,01,000 and 2024 – Rs. 1,30,000.

On 1st April, 2024, Zeenu is admitted to the partnership for 1/4th share in profit (without any salary). Goodwill is to be valued at four years' purchase of weighted average profit of last three years (after partners′ salaries); Profits to be weighted as 1,2 and 3, the greatest weight being given to the last year. Calculate the value of Goodwill.

Answer 10:

Weighted average profit = Total of weighted profit / Total of weights

Weighted average profit =1,92,000 / 6

Weighted average profit = Rs. 32,000

Goodwill = Weighted Average Profit × No. of Year Purchase

Goodwill = 32,000 × 4

Goodwill = Rs. 1,28,000

About Solution:

The partner whose share have decreased as a result of change in profit sharing ratio are called sacrificing ratio.

Things to Remember:

At the time of admission of a new partner, at the time of change in profit sharing ratio of existing partners.

Important Notes:

The partners whose share have increased as a result of change in profit sharing ratio are called gaining partners.

Important Notes:

The partners whose share have increased as a result of change in profit sharing ratio are called gaining partners

Question 11: The Capital of the firm of Anuj and Benu is ₹ 10,00,000 and the market rate of interest is 15%. The annual salary of the partners is ₹ 60,000 each. The profit for the last three years were ₹ 3,00,000; ₹ 3,60,000 and ₹ 4,20,000. The goodwill of the firm is to be valued on the basis of two years’ purchase of the last three years’ average super profit. Calculate the goodwill of the firm.

Answer 11:

Actual Profit after Salaries of Partners:-

For 1st Year = Rs. 3,00,000 – (Rs. 60,000 × 2) = Rs. 1,80,000

For 2nd Year = Rs. 3,60,000 – (Rs. 60,000 × 2) = Rs. 2,40,000

For 3rd Year = Rs. 4,20,000 – (Rs. 60,000 × 2) = Rs. 3,00,000

Average Profit = 1,80,000+2,40,000 +3,00,000 / 3

Average Profit = 1,80,000+2,40,000 +3,00,000 / 3

Average Profit = Rs. 2,40,000

Calculation of Normal Profit:-

Normal Profit = Capital Employed × Normal Rate of Return

Normal Profit = Rs. 10,00,000 × 15%

Normal Profit = Rs. 1,50,000

Calculation of Super Profit:-

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 2,40,000 – Rs. 1,50,000

Super Profit = Rs. 90,000

Calculation of Goodwill:-

Goodwill = Super Profit × Number of Year purchases

Goodwill = Rs. 90,000 × 2

Goodwill = Rs. 1,80,000

Question 12: Atul and Bipul had a firm in which they had invested ₹ 50,000. On average, the profits were ₹ 16,000. The normal rate of return in the industry is 15%. Goodwill is to be valued at four years’ purchase of profits in excess of profits @ 15% on the money invested. Calculate the value of goodwill.

Answer 12:

Calculation of Normal Profit:-

Normal Profit = Capital Employed × NRR

Normal Profit = Rs. 50,000 × 15%

Normal Profit = Rs. 7,500

Calculation of Super Profit:-

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 16,000 – Rs. 7,500

Super Profit = Rs. 8,500

Calculation of Goodwill:-

Goodwill = Super Profit × Number of Year Purchases

Goodwill = Rs. 8,500 × 4

Goodwill = Rs. 34,000

Question 13: The total capital of the firm of Sakshi, Mehak and Megha is Rs. 1,00,000 and the market rate of interest is 15%. The net profits for the last 3 years were Rs. 30,000; Rs. 36,000 and Rs. 42,000. Goodwill is to be valued at 2 years' purchase of the last 3 years' super profits. Calculate the goodwill of the firm.

Answer 13:

Normal Profit = Capital Employed × Normal Rate of Return / 100

Normal Profit = 1,00,000 × 15/100

Normal Profit = Rs. 15,000

Average Profit = Total Profit / Number of Year

Average Profit = 30,000+36,000+42,000 / 3

Average Profit = 1,08,000/3

Average Profit = Rs. 36,000

Super Profit = Actual Profit – Normal Profit

Super Profit = Rs. 36,000 – Rs. 15,000

Super Profit = Rs. 21,000

Goodwill = Super Profit × No. of year purchase

Goodwill = Rs. 21,000 × 2

Goodwill = Rs. 42,000

About Solution:

Purchased Goodwill: Purchased goodwill means goodwill for which a consideration has been paid e.g. when business is purchased the excess of purchase consideration of its net assets i.e. Assets – Liabilities is known as Purchased Goodwill It is separately recorded in the books because as it is purchased by payment in cash or kind.

Things to Remember:

Self-generated Goodwill: It is also called as inherent goodwill. It is an internally generated goodwill which arises from a number of factors that a running business possesses due to which it is able to earn more profits in the future.

Important Notes:

Simple Average Profit Method: This is a very simple and widely followed method of valuation of goodwill. In this method, goodwill is calculated on the basis of the number of past years. Average of such profits is multiplied by the agreed number of years (such as two or three) to find out the value of goodwill. Formula for calculation of goodwill is as follows: Goodwill = Average Profits x Number of years’ purchase.

Question 14: A and B were partners in a firm sharing profits equally. Their capitals were: A – ₹ 1,20,000 and B – ₹ 80,000. The annual rate of interest is 20%. Profits of the firm for the last three years were ₹ 34,000; ₹ 38,000 and ₹ 30,000. They admitted C as a new partner. On C’s admission the goodwill of the firm was valued at 2 year’s purchase of the super profits.

Calculate the value of goodwill of the firm on C’s admission.

Answer 14:

Calculation of Normal Profit:-

Capital Employed = Total Capital of A and B

Capital Employed = Rs. 1,20,000 + Rs. 80,000

Capital Employed = Rs. 2,00,000

Normal Profit = Capital Employed × NRR

Normal Profit = Rs. 2,00,000 × 20%

Normal Profit = Rs. 40,000

Calculation of Average Profit:-

Average Profit = Rs.34,000+Rs.38,000+Rs.30,000 / 3

Average Profit = 1,02,000 / 3

Average Profit = Rs. 34,000

Calculation of Super Profit:-

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 34,000 – Rs. 40,000

Super Profit = – Rs. 6,000

Here, Firm has negative super profit so the firm does not have goodwill.

Question 15: A business earned an average profit of Rs. 8,00,000 during the last few years. The normal rate of profit in the similar type of business is 10%. The total value of assets and liabilities of the business were Rs. 22,00,000 and Rs. 5,60,000 respectively. Calculate the value of goodwill of the firm by super profit method if it is valued at 21/2 years' purchase of super profits.

Answer 15:

Goodwill under Super Profit Method = Super Profit × Year’s Purchase

Goodwill = (Average Profit – Normal Profits) × Year’s Purchase

Goodwill = (Average Profit – (Assets – Liabilities) ×10%) × Years Purchase

Goodwill = (8,00,000 – (22,00,000 – 5,60,000) × 10%) × 2.5 Years Purchase

Goodwill = (8,00,000 – 16,40,000 × 10%) × 2.5 Years Purchase

Goodwill = (8,00,000 – 1,64,000) × 2.5 Years Purchase

Goodwill = Rs. 6,36,000 × 2.5 Years

Goodwill = Rs. 15,90,000

About Solution:

Location: A business will draw more clients and build more goodwill if it is situated in a handy or noticeable area.

Things to Remember:

The company's longevity: An older company is more well-known to its clientele and is therefore more likely to have greater goodwill. When a company has established a solid reputation over time, it will have a larger client base than competitors that have just entered the market. A business's ability to turn a profit can be determined by the number of consumers.

Important Notes:

Monopolistic and other Rights: A business will enjoy guaranteed earnings if it has a monopolistic market. Similar to this, it will have greater goodwill if it owns certain unique rights, such as patents, trademarks, copyrights, or concessions.

Question 16: Average net profit expected in the future by XYZ firm is ₹ 36,000 per year. The average capital employed in the business by the firm is ₹ 2,00,000. The normal rate of return from capital invested in this class of business is 10%. The remuneration of the partners is estimated to be ₹ 6,000 p.a. Calculate the value of goodwill on the basis of two years’ purchase of super profit.

Answer 16:

Calculation of Average Profit of the firm:-

Average Profit = Average Profit – Partners Remuneration

Average Profit = Rs. 36,000 – Rs. 6,000

Average Profit = Rs. 30,000

Calculation of Normal Profit:-

Normal profit = Capital Employed × NRR

Normal profit = Rs. 2,00,000 × 10%

Normal profit = Rs. 20,000

Calculation of Super Profit:-

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 30,000 – Rs. 20,000

Super Profit = 10,000

Calculation of Goodwill of the firm:-

Goodwill = Super Profit × Number of Year Purchases

Goodwill = Rs. 10,000 × 2

Goodwill = Rs. 20,000

Question 17: A partnership firm earned net profits during the last three years ended 31st March, as follows: 2022–Rs.17,000; 2023–Rs. 20,000; 2024–Rs. 23,000.

The capital investment in the firm throughout the above-mentioned period has been Rs 80,000. Having regard to the risk involved, 15% is considered to be a fair return on the capital. Calculate value of goodwill on the basis of two years' purchase of average super profit earned during the above-mentioned three years.

Answer 17:

Goodwill under Super Profit Method = Super Profit × Years Purchase

Super Profit Method = (Average Profit – Normal Profit) × Years Purchase

Super Profit Method = (Rs. 20,000 – Rs. 80,000 × 15%) × 2 Years

Super Profit Method = (Rs. 20,000 – Rs. 12,000) × 2 Years

Super Profit Method = Rs. 8,000 × 2 Years

Super Profit Method = Rs. 16,000

About Solution:

Capitalisation of Average Profit Method: Under this method first of all we calculate the average profits and then we assess the capital needed for earning such average profits on the basis of normal rate of return. Such capital is also called capitalised value of average profits. It is calculated as under.

Capitalised value of the firm = Average Profits x 100 Normal Rate of Return.

Things to Remember:

Capitalisation of Super Profit Method: Under this method first of all we calculate the super profits and then we assess the capital needed for earning such super profits on the basis of normal rate of return. Such capital is actually the amount of goodwill. Super profits are calculated in the same manner as calculated in super profits method.

Goodwill of the firm = Super Profits ×100 / Normal rate of return

Important Notes:

A company develops goodwill via the diligence and integrity of its owners, which is the good name or reputation of the business. When a business provides excellent customer service, happy customers are more likely to return and help the business make more money in the long run.

Question 18: On 1st April, 2024, an existing firm had assets of Rs 75,000 including cash of Rs 5,000. Its creditors amounted to Rs 5,000 on that date. The firm had a Reserve of Rs 10,000 while Partners' Capital Accounts showed a balance of Rs 60,000. If Normal Rate of Return is 20% and goodwill of the firm is valued at Rs 24,000 at four years' purchase of super profit, find average profit per year of the existing firm.

Answer 18:

Goodwill under Super Profit Method:-

Goodwill = Super Profit × Year’s Purchase

Goodwill = (Average Profit – Normal Profit) ×Years Purchase

24,000 = (Average Profit – 14,000) × 4 Years Purchase

24,000/4 = Average Profit – 14,000

6,000 = Average Profit – 14,000

Average Profit = 14,000 + 6,000

Average Profit = 20,000

About Solution:

Capitalization of Super Profit Method: In this technique, the super profits are first calculated, and then the capital required to produce such super profits is estimated based on the average rate of return. Indeed, the quantity of such capital is goodwill. The same formula used to compute super profits is used to calculate super profits.

Things to Remember:

The firm benefits from Goodwill's favourable positioning, which enables it to generate larger revenues without exerting additional effort. Goodwill is a feeling that cannot be seen. As a result, goodwill is referred to as an intangible asset.

Important Notes:

Average profit is the profit that a firm has generated on average over the course of preceding accounting periods. Given future estimates of the businesses' earning capability, goodwill is estimated using the average profit.

Question 19: A business earned an average profit of ₹ 1,80,000 during the last few years. Average capital employed by the firm is ₹ 12,50,000. If goodwill of the firm is valued at ₹ 1,60,000 at 2 year’s purchase of super profit, find normal rate of return.

Answer 19:

Calculation of Normal Profit of the firm:-

Goodwill = Super Profit × Number of Year Purchases

We know that,

Super Profit = Average Profit – Normal Profit

Rs. 1,60,000 = (Rs. 1,80,000 – Normal Profit) × 2

1,60,000/2 = (Rs. 1,80,000 – Normal Profit)

Normal Profit = Rs. 1,80,000 – Rs. 80,000

Normal Profit = Rs. 1,00,000

Calculation of Normal Rate of Return:-

Normal Profit = Capital Employed × Normal Rate of Return

Rs. 1,00,000 = Rs. 1,25,000 × Normal Rate of Return

1,00,000 / 1,25,000 = Normal Rate of Return

Normal Rate of Return = 1,00,000/1,25,000 × 100

Normal Rate of Return = Rs. 8%

Question 20: A business has earned average profit of ₹ 1,20,000 during the last four years and the normal rate of return of similar business is 15%. If goodwill of the firm is valued at ₹ 1,35,000 at 3 year’s purchase of average super profit, find the capital employed of the firm.

Answer 20:

Calculation of Normal Profit of the firm:-

Goodwill = Super Profit × Number of Year Purchases

We know that,

Super Profit = Average Profit – Normal Profit

Rs. 1,35,000 = (Rs. 1,20,000 – Normal Profit) × 3

1,35,000/3 = (Rs. 1,20,000 – Normal Profit)

Normal Profit = Rs. 1,20,000 – Rs. 45,000

Normal Profit = Rs. 75,000

Calculation of Normal Rate of Return:-

Normal Profit = Capital Employed × Normal Rate of Return

Rs. 75,000 = Capital Employed × 15%

75,000 / 15% = Normal Rate of Return

Normal Rate of Return = 75,000 / 15 × 100

Normal Rate of Return = Rs. 5,00,000

Question 21: Average profit earned by a firm is Rs. 1,00,000 which includes undervaluation of stock of Rs. 40,000 on an average basis. The capital invested in the business is Rs. 6,30,000 and the normal tare of return is 5%. Calculate goodwill of the firm on the basis of 5 times the super profit.

Answer 21:

Goodwill under Super Profit Method = Super Profit × Years Purchase

= Super Profit × Times Purchase

= (Average Profit + Under Valuation of Stock – Normal Profit)×Times Purchase

= (1,00,000 + 40,000 – 6,30,000 × 5%) × 5 Times Purchase

= (1,00,000 + 40,000 – 31,500 ) × 5 Times Purchase

= Rs. 1,08,500 × 5 Times Purchase

= Rs. 5,42,500

About Solution:

According to this technique, the company's capitalized value is determined using the average rate of return. Goodwill is the distinction between capitalized value and actual capital used.

Things to Remember:

Bought goodwill: Purchased goodwill refers to goodwill for which a consideration has been paid, for example, when a firm is purchased, Purchased Goodwill refers to the excess of the purchase consideration of its net assets, or Assets - Liabilities. Because it was paid for when it was acquired, it is individually recorded in the books in kind or money.

Important Notes:

Capitalization of Super Profit Method): In this technique, we first determine the super profits and then determine the capital required to generate such super profits based on the usual rate of return.

Indeed, the quantity of such capital is goodwill. The same formula used to compute super profits is used to calculate super profits.

Goodwill of the Company = 100 times Super Profits standard return rate.

Question 22: The average profit earned by a firm is Rs 7,50,000 which includes overvaluation of stock of Rs 30,000 on an average basis. The capital invested in the business is Rs 4,20,000 and the normal tare of return is 15%. Calculate goodwill of the firm on the basis of 3 time the super profit.

Answer 22:

Goodwill under Super Profit Method = Super Profit × Years Purchase

= Super Profit × Times Purchase

= (Average Profit – Over Valuation of Stock – Normal Profit) × Times Purchase

= (7,50,000 – 30,000 – 42,00,000 × 15%) × 5 Times Purchase

= (7,50,000 – 30,000 – 6,30,000) × 5 Times Purchase

= 90,000 × 3 Times Purchase

= Rs. 2,70,000

About Solution:

Whenever there is a change in the profit sharing ratio one and more of the existing partner have to surrender some of their old share in favour of one or more of other partner the ratio of surrender of profit sharing ratio is called sacrificing ratio it is calculated as fallow:-

Sacrificing ratio = Old ratio – New ratio

Things to Remember:

Goodwill means the good name or the reputation earned by an firm thought the hardwork and honestly of its owner if a firm renders good service to the customer the customer who feel satisfied will come again and again and the firm will able to earn more profit in future Thus, goodwill is value of the reputation of a firm which enable it to earn higher profit in comparison to the normal profit earned by other firm in the same trade.

Important Notes:

The term goodwill is generally used to donate the benefits arising from connection and reputation “goodwill is nothing more than the probability that the old c profit than customer will resort to the old place goodwill may be said to be that elements a raising from the reputation connection or other advantage possessed by a business which enable it to earn great profit then the return normally to be expected on the capital represented by the net tangible assets employed in business.

Question 23: Ayub and Amit are partners in a firm and they admit Jaspal into partnership w. e. f. 1st April, 2018. They agreed to value goodwill at 3 years' purchase of Super Profit Method for which they decided to average profit of last 5 years. The profit for the last 5 years were:

The firm has total assets of Rs 20,00,000 and Outside Liabilities of Rs 5,00,000 as on that date. Normal Rate of Return in similar business is 10%.

Calculate value of goodwill.

Answer 23:

Value of Goodwill under Super Profit Method

Good Will = Super Profit × Years’ Purchases

= 48,000 × 3Years

= Rs. 1,44,000

About Solution:

Goodwill is or touched it can only be felt hence it is treated as an intangible assets but it is no fictitious assets because fictitious assets do not have a value or it can be purchased or sold with any other assets.

Things to Remember:

If the manager is capable and competent the firm will earn high profit which will increase the value of goodwill better quality of product will increase the sale and profit which will increase the value of goodwill.

Important Notes:

A change in profit sharing implies purchase of share of profit by one or more partners from other partners or partners.

Question 24: From the following information, calculate value of goodwill of the firm by applying Capitalisation Method:

Total Capital of the firm Rs 16,00,000.

Normal rate of return 10%.

Profit for the year Rs 2,00,000.

Answer 24:

Goodwill under Capitalisation Method:-

Goodwill = Expected Capital – Actual Capital

Goodwill = Profit for the year × Reverse of Reasonable Rate of Return – Actual Capital

Goodwill = Rs. 2,00,000 × 100/10 – 16,00,000

Goodwill = Rs. 20,00,000 – 16,00,000

Goodwill = Rs. 4,00,000

About Solution:

As a result of changing in profit sharing ratio one or more of the existing partners gain some portion of other partners share of profit the ratio of gain of profit sharing ratio is gain of profit sharing ratio is called gaining ratio it is calculated as follow:

Gaining ratio = New ratio – Old ratio

Things to Remember:

Amalgamation of two partnership firms for example A and B are partners in a firm sharing profit and ratio of 2:1 To eliminate compensation they amalgamate their firm with the firm of C and D who are sharing profit in the ratio of 3:1 they knew ratio for A,B,C and D are agreed at 2:1:3:1 it amounts to recantation of the firm of A and B on the one hand and the firm C and D on the other hand and new reconstituted firm is formed.

Important Notes:

Sometimes the existing partner decide to change their profit sharing ratio the change is necessitated due to change in capital contribution or in active participation in management as a result of a change in profit sharing ratio one or more of the existing partner my acquire extra share in profit at the cost of one or more of other partners in such a case in order to maintain equality among the partner it is necessary to make adjustment for goodwill revaluation of assets and liabilities reserve accumulated profit and losses etc. these adjustment are similar to those made at the time of admission or retirement of a partner.

Question 25: A firm earned an average profit of ₹ 3,00,000 during the last few years. The normal rate of return of the industry is 15%. The assets of the business were ₹ 17,00,000 and its liabilities were ₹ 2,00,000.

Calculate the goodwill of the firm by Capitalisation of average profit.

Answer 25:

Total Capitalised value of the Firm as per Average profit:-

Total Capitalised value of the firm = Average profit / Normal Rate of Return

Total Capitalised value of the firm = Rs. 3,00,000 × 100 / 15

Total Capitalised value of the firm = Rs. 20,00,000

Calculation of Capital Employed:-

Capital Employed = Assets – Liabilities

Capital Employed = Rs.17,00,000 – Rs. 2,00,000

Capital Employed = Rs.15,00,000

Calculation of Goodwill of the firm:-

Goodwill = Total Capitalized value of the firm – Capital Employed

Goodwill = Rs. 20,00,000 – Rs. 15,00,000

Goodwill = Rs. 5,00,000

Question 26: A and B were partners in a firm with capitals of ₹ 3,00,000 and ₹ 2,00,000 respectively, The normal rate of return was 20% and the capitalised value of average profits was ₹ 7,50,000. Calculate the goodwill of the firm by capitalisation of the average profit method.

Answer 26:

Capital value of Average Profit = Rs. 7,50,000

Capital Employed = A’s Capital + B’s Capital

Capital Employed = Rs. 3,00,000 + Rs. 2,00,000

Capital Employed = Rs. 5,00,000

Calculation of Goodwill of the Firm:-

Goodwill = Capitalised value of the firm – Capital Employed

Goodwill = Rs. 7,50,000 – Rs. 5,00,000

Goodwill = Rs. 2,50,000

Question 27: Puneet and Tarun are in the restaurant business having credit balances in their fixed capital accounts as ₹ 2,50,000 each. They have credit balances in their Current Accounts of ₹ 30,000 and ₹ 20,000 respectively. The firm does not have any liability. They are regularly earning profits and their average profit for the last 5 years is ₹ 1,00,000. If the normal rate of return is 10%. Find the value of goodwill by Capitalisation of the Average Profit Method.

Answer 27:

Calculation of Capitalised value of Average Profit:-

Capitalised value of Average Profit = Average Profit / Normal Rate of Return

Capitalised value of Average Profit = 1,00,000 / 10%

Capitalised value of Average Profit = 1,00,000/10× 100

Capitalised value of Average Profit = Rs 10,00,000

Calculation of Capital Employed:-

Capital Employed = Capital of Partners + Current of Partners

Capital Employed = Rs. 2,50,000 + Rs. 2,50,000 + Rs. 30,000 + Rs. 20,000

Capital Employed = Rs. 5,50,000

Goodwill = Capitalised Value of Average profit – Capital Employed

Goodwill = Rs. 10,00,000 – Rs. 5,50,000

Goodwill = Rs. 4,50,000

Question 28: From the following particulars, calculate the value of goodwill of a firm by the Capitalisation of Average Profit Method. (i) Profits of last five consecutive years ending 31st March, are: 2024 – ₹ 54,000; 2023 – ₹ 42,000; 2022 – ₹ 39,000; 2021 – ₹ 67,000 and 2020 – ₹ 59,000.

(ii) Capitalisation rate 20%.

(iii) Net assets of the firm ₹ 2,00,000.

Answer 28:

Calculation of Average Profit of Last 5 years:-

Average Profit = 59,000+67,000+39,000+42,000+54,000 / 5

Average Profit = 2,61,000/5

Average Profit = Rs. 52,200

Capitalised value of Average Profit = Average Profit / Normal Rate of Return

Capitalised value of Average Profit = 52,200 / 20%

Capitalised value of Average Profit = 52,200 / 20 × 100

Capitalised value of Average Profit = Rs. 2,61,000

Calculation of Goodwill of the firm:-

Goodwill = Capitalised value of Average – Capital Employed

Goodwill = Rs. 2,61,000 – Rs. 2,00,000

Goodwill = Rs. 61,000

Question 29: A business has earned average profit of Rs. 4,00,000 during the last few years and the normal rate of return in similar business is 10%. Find value of goodwill by:

(i) Capitalisation of Super Profit Method.

(ii) Super Profit Method if the goodwill is valued at 3 years' purchase of super profits.

Assets of the business were Rs. 40,00,000 and its external liabilities Rs. 7,20,000.

Answer 29:

Actual or Average Profit Rs. 4,00,000

Capitalised Value of Average Profit = 4,00,000 × 100 / 10

Or Expected capital = 40,00,000

Actual Capital = Assets – Liabilities

= 40,00,000 – 7,20,000

= Rs. 32,80,000

Value of Goodwill under Capitalisation of Average Profit Method

Goodwill = Capitalised value of Average Profit – Actual Capital

= 40,00,000 – 32,80,000 × 10 / 100

= Rs. 7,20,000

Super Profit = Average Profit – Normal Profit

= 4,00,000 – 32,80,000 × 10 / 100

= 4,00,000 – 3,28,000

= Rs. 72,000

(1) Value of Goodwill under Capitalisation of Super Profit Method

= Super Profit × Reverse Rate of Return

= 72,000 × 100 / 10

= 7,20,000

(2) Value of Goodwill under Super Profit Method

= Super profit × Years purchase

= 72,000 × 3

= Rs. 2,16,000

About Solution:

Nature of goods if a business deal in goods of daily use it will have steady profit as the demand for these goods will be stable such business will have more goodwill but if it deals in fancy goods its profit will uncertain and as such the value of the goodwill will be less.

Things to Remember:

Possession of license if a firm holds an import license the goodwill of the firm will be more as it will be very difficult for other firm to enter this business in the absence of this license.

Important Notes:

Monopolistic and other rights if a business enjoy monopoly market it will have assured profit similarly if it holds some special rights such as partners trademarks copyrights or concessions etc. it will have more goodwill.

Question 30: A firm earns a profit of ₹ 5,00,000. The normal Rate of Return in a similar type of business is 10%. The value of total assets (excluding goodwill) and total outsider’s liabilities as on the date of goodwill are ₹ 55,00,000 and ₹ 14,00,000 respectively. Calculate the value of goodwill according to the Capitalisation of the Super Profit Method as well as the Capitalisation of the Average Profit Method.

Answer 30:

Goodwill Calculation by Capitalisation of Super Profit Method:-

Capital Employed = Total Assets – Outside Liabilities

Capital Employed = Rs. 55,00,000 – Rs. 14,00,000

Capital Employed = Rs. 41,00,000

Normal Profit = Capital Employed × NRR

Normal Profit = Rs. 41,00,000 × 10%

Normal Profit = Rs. 4,10,000

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 5,00,000 – Rs. 4,10,000

Super Profit = Rs. 90,000

Goodwill = Super Profit / NRR

Goodwill = 90,000 / 10%

Goodwill = 90,000 / 10×100

Goodwill = Rs. 9,00,000

Goodwill Calculation by Capitalisation of Average Profit Method:-

Capital Employed = Total Assets – Outside Liabilities

Capital Employed = Rs. 55,00,000 – Rs. 14,00,000

Capital Employed = Rs. 41,00,000

Capitalised Value of Average Profit = Average Profit / NRR

Capitalised Value of Average Profit = 5,00,000 / 10%

Capitalised Value of Average Profit = Rs. 50,00,000

Goodwill = Capitalised Value of Average Profit – Capital Employed

Goodwill = Rs. 50,00,000 – Rs. 41,00,000

Goodwill = Rs. 9,00,000

Question 31: On 1st April, 2018, a firm had assets of Rs. 1,00,000 excluding stock of Rs. 20,000. The current liabilities were Rs. 10,000 and the balance constituted Partner’s Capital Accounts. If the normal rate of return is 8%, the Goodwill of the firm is valued of Rs. 60,000 at four years’ purchases of super profit, find the actual profits of the firm.

Answer 31:

Total Assets = Sundry Assets + Stock

Total Assets = Rs. 1,00,000 + Rs. 20,000

Total Assets = Rs. 1,20,000

Current Liabilities = Rs. 10,000

Capital Employed = Total Assets – Current Liabilities

Capital Employed = Rs. 1,20,000 – Rs. 10,000

Capital Employed = Rs. 1,10,000

Normal Profit = Capital Employed × Normal rate of Return / 100

Normal Profit = Rs. 1,10,000 × 8/100

Normal Profit = Rs. 8,800

Goodwill = Super Profit × No. of Year Purchases

60,000 = (Actual Profit – Normal Profit) × 4

60,000 = (Actual Profit – 8,800) × 4

60,000 = 4× Actual Profit – (8,800 × 4)

60,000 = 4× Actual Profit – 35,200

60,000 + 35,200 = 4× Actual Profit

95,200 = 4× Actual Profit

95,000 / 4 = Actual Profit

Actual Profit = Rs. 23,800

About Solution:

There is no concrete a genuine basis of selecting the number of past year on which average profit is to calculate.

Things to Remember:

In average profit method average profit are multiplied by number of years (such as two or three to find out the value of goodwill however the number of year of purchase used are based on estimation hence the value of goodwill cannot be stated as satisfactory there should be some concrete or genius basis for determining the number of year of purchase rather than based on estimate.

Important Notes:

Capital employed is not considered while calculating average profit earned by two firm engaged in the same type business may be the same whereas capital employed by the two firms may be different hence average profit cannot be the proper base for calculation of goodwill.

Question 32: The average profit of a firm during the last few years is ₹ 1,50,000. In similar businesses, the normal rate of return is 10% of the capital employed. Calculate the value of goodwill by capitalisation of the super profit method if the super profits of the firm are ₹ 50,000.

Answer 32:

Goodwill Calculation by Capitalisation of Super Profit Method:-

Goodwill = Super Profit / NRR

Goodwill = 50,000 / 10%

Goodwill = 50,000 / 10 × 100

Goodwill = Rs. 5,00,000

Question 33: Raja Brothers earn an average profit of ₹ 30,000 with a capital of ₹ 2,00,000. The normal rate of return in the business is 10%. Using Capitalisation of super profit method. Workout the value of the goodwill of the firm.

Answer 33:

Calculation of Normal Profit:-

Normal Profit = Capital Employed × NRR

Normal Profit = Rs. 2,00,000 × 10%

Normal Profit = Rs. 20,000

Calculation of Super Profit:-

Super Profit = Average Profit – Normal Profit

Super Profit = Rs. 30,000 – Rs. 20,000

Super Profit = Rs. 10,000

Calculation of Goodwill by Capitalisation of Super Profit Method:-

Goodwill = Super Profit / NRR

Goodwill = 10,000 / 10%

Goodwill = 10,000 / 10 × 100

Goodwill = Rs. 1,00,000

Question 34: Rajan and Rajani are partners in a firm. Their capitals were Rajan Rs. 3,00,000; Rajani Rs. 2,00,000. During the year 2017-18, the firm earned a profit of Rs. 1,50,000. Calculate the value of goodwill of the firm by capitalisation of super profit assuming that the normal rate of return is 20%.

Answer 34:

Goodwill by Capitalisation of Super Profit Method = Super Profit × Reverse Rate of Return

(Actual Profit – Normal Profit) × Reverse of Rate of Return

(Actual Profit – Capital Employed × Normal Rate of Return) × Reverse of Rate of Return

(1,50,000 – 5,00,000 × 20/100) × Reverse of Rate of Return

(1,50,000 – 1,00,000) × 100 / 20

= Rs. 50,000 × 100 / 20

= Rs. 2,50,000

About Solution:

It is an intangible asset: As goodwill lacks a physical form and cannot be seen or felt, it falls under the same category as intangible assets like patents, trademarks, copyrights, etc.

Things to Remember:

Its value is subject to continual variations: Although goodwill does not lose value over time, its worth is subject to constant fluctuations. It always exists as a silent asset in a company that makes exceptional profits (i.e., more than usual), but its value decreases as earnings do.

Important Notes:

Goodwill can only be sold as a whole to be valued; it cannot be sold separately. It can only be sold along with the whole company. The partner's admission or retirement constitutes the lone exception.

Question 35: A business has earned average profit of Rs. 8,00,000 during the last few years and the normal rate of return in similar business is 10%. Find value of goodwill by:

(i) Capitalisation of Super Profit Method; and

(ii) Super Profit Method if the goodwill is valued at 3 years' purchase of super profit.

Assets of the business were Rs. 80,00,000 and its external liabilities Rs. 14,40,000.

Answer 35:

(i) Capitalisation of Super Profit = Super Profit × 100/(Normal Rate of Retur)

Capitalisation of Super Profit= 1,44,000 × 100/10

Capitalisation of Super Profit= Rs. 14,40,000

(ii) Goodwill = Super Profit × No. of Year Purchases

Goodwill = Rs. 1,44,000 × 3

Goodwill = Rs. 4,32,000

Working Note:-

Normal Profit = Capital Employed × Normal Rate of Retur / 100

Normal Profit = Rs. 65,60,000 × 10 / 100

Normal Profit = Rs. 6,56,000

Average Actual Profit = 8,00,000 (given)

Calculation of Capital Employed = Total Asset – External Liabilities

Capital Employed = Rs. 80,00,000 – Rs. 14,40,000

Capital Employed= Rs. 65,60,000

Super Profit = Average Actual Profit - Normal Profit

Super Profit = Rs. 8,00,000 – Rs. 6,56,000

Super Profit = Rs. 1,44,000

About Solution:

Purchased Goodwill: Purchased goodwill means goodwill for which a consideration has been paid e.g. when business is purchased the excess of purchase consideration of its net assets i.e. Assets – Liabilities is known as Purchased Goodwill It is separately recorded in the books because as it is purchased by payment in cash or kind.

Things to Remember:

Self-generated Goodwill: It is also called as inherent goodwill. It is an internally generated goodwill which arises from a number of factors that a running business possesses due to which it is able to earn more profits in the future.

Important Notes:

Simple Average Profit Method: This is a very simple and widely followed method of valuation of goodwill. In this method, goodwill is calculated on the basis of the number of past years. Average of such profits is multiplied by the agreed number of years (such as two or three) to find out the value of goodwill. Formula for calculation of goodwill is as follows:

Goodwill = Average Profits x Number of years’ purchase.

Question 36: Ajeet and Baljeet are partners in a firm. Their capitals are Rs. 9,00,000 and Rs. 6,00,000 respectively. During the year ended 31st March, 2019 the firm earned a profit of Rs. 4,50,000. Assuming that the normal rate of return is 20%, calculate value of goodwill of the firm:

(i) By Capitalisation Method; and

(ii) By Super Profit Method if the goodwill is valued at 2 years' purchase of super profit.

Answer 36:

(i) Capitalisation of Super Profit = Super Profit × 100 / Normal Rate of Retur

Capitalisation of Super Profit= Rs. 1,50,000 × 100 / 20

Capitalisation of Super Profit= Rs. 7,50,000

(ii) Goodwill = Super Profit × No. of Year Purchases

Goodwill = Rs. 1,50,000 × 2

Goodwill = Rs. 3,00,000

Working Note:-

Normal Profit = Capital Employed × Normal Rate of Retur / 100

Normal Profit = Rs. 15,00,000 × 20 / 100

Normal Profit = Rs. 3,00,000

It is given that,

Average Actual Profit = Rs. 4,50,000 (given)

Calculation of Capital Employed = Total Asset – Current Liabilities

Capital Employed = Rs. 9,00,000 – Rs. 6,00,000

Capital Employed = Rs. 15,00,000

Super Profit = Average Actual Profit - Normal Profit

Super Profit = Rs. 4,50,000 – Rs. 3,00,000

Super Profit = Rs. 1,50,000

About Solution:

Goodwill is difficult to quantify precisely: This is owing to the fact that its worth may occasionally change as a result of internal and external circumstances.

Things to Remember:

Bought goodwill is goodwill for which a consideration has been paid; for example, when a firm is purchased, the excess of the purchase consideration over its net assets, or (Assets - Liabilities), is the Purchased Goodwill. As it is purchased by paying in cash or kind, it is individually documented in the books.

Important Notes:

Inherent goodwill is another name for self-generated goodwill. It is an internally produced goodwill that results from a variety of elements that an operating firm has and that allows it to make more profits in the future.

Question 37: From the following information, calculate value of goodwill of the firm:

(i) At three years' purchase of Average Profit.

(ii) At three years' purchase of Super Profit.

(iii) On the basis of Capitalisation of Super Profit.

(iv) On the basis of Capitalisation of Average profit.

Information:

(a) Average Capital Employed is Rs 6,00,000.

(b) Net Profit/(Loss) of the firm for the last three years ended are: 31st March, 2108–Rs 2,00,000, 31st March, 2107–Rs 1,80,000, and 31st March, 2106–Rs 1,60,000.

(c) Normal Rate of Return in similar business is 10%.

(d) Remuneration of Rs. 1,00,000 to partners is to be taken as charge against profit.

(e) Assets of the firm (excluding goodwill, fictitious assets and not-trade investments) is Rs. 7,00,000 whereas Partners' Capital is Rs 6,00,000 and Outside Liabilities Rs 1,00,000.

Answer 37:

(i) Goodwill at three years purchase of Average profits = Average profit × Years Purchase

= (Total Profit)/(Total Years) × Years Purchase

=((2,00,000+1,80,000+1,60,000-3,00,000)/(3 Years))×3 years

=80,000 × 3years

= Rs.2,40,000

(ii) Goodwill by super profit method at three years purchase = Super Profit × Years Purchase

(Average Profit – Normal Profit) × Years Purchase

(Average Profit – Capital Employed × Normal Rate of return) × Years Purchase

=((2,00,000+1,80,000+1,60,000-3,00,000)/3 - 6,00,000 × 10/100) ×Years Purchase

= (80,000 – 60,000) × 3years purchase

= 20,000 × 3Years

= Rs. 60,000

(iii) Goodwill by Capitalisation Super Profit Method = Super Profit × reverse rate of return

(Average Profit – Normal Profit) × Reverse rate of return

(Average Profit – Capital Employed × Normal Rate of return) × reverse of rate of return

= ((2,00,000+1,80,000+1,60,000-3,00,000)/3 - 6,00,000 × 10/100) × 100/10

= (80,000 – 60,000) × 100/10

= 20,000 × 100/10

= 2,00,000

(iv) Goodwill by capitalisation of average profit method = Average Profit × reverse rate of return

= ((2,00,000+1,80,000+1,60,000-3,00,000)/3) × 100/10

= Rs. 80,000 × 100/10

= Rs. 8,00,000

About Solution:

The need to value goodwill arises from the fact that if the partners' respective rights change, the party who makes a sacrifice must get compensation. We must determine goodwill as it is the basis for compensation.

Things to Remember:

Goodwill belongs to the category of intangible asset such as partner trademarks, copy rights etc. It does not suffer wear and tear and as such the question of deprecation does not arise on it as is the case of the other assets.

Important Notes:

While goodwill does not depreciate its valve is liable to constant fluctuation it is always present as a silent asset in a business where there are super profit (i.e. more than the normal) but declines in value with the decline in meaning.

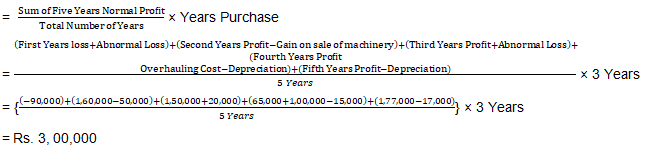

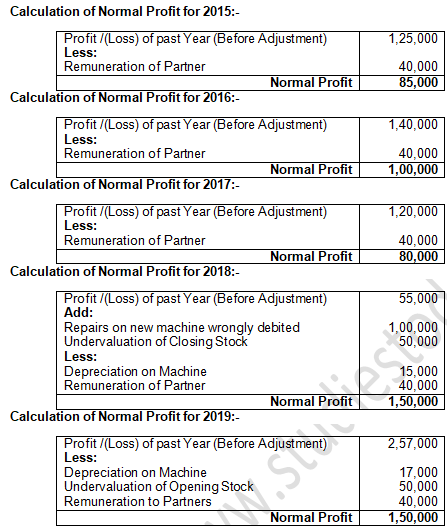

Old Quesrions

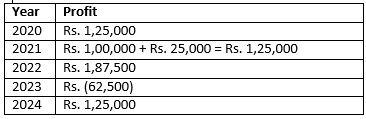

The annual profit for the purpose of goodwill for the past four years was:

![]()

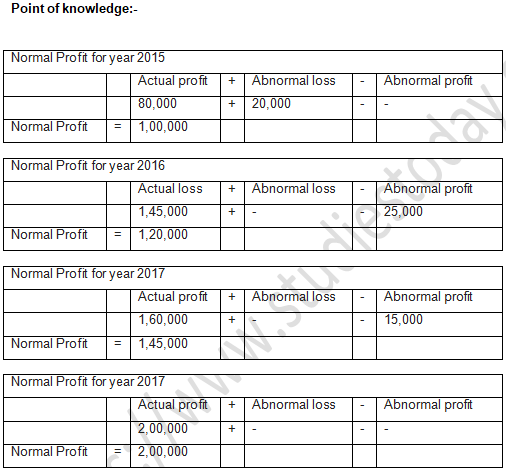

Books of Account of the firm revealed that:

(i) The firm had gain (profit) of Rs. 50,000 from sale of machinery sold in the year ended 31st March, 2016. The gain (profit) was credited in Profit and Loss Account.

(ii) There was an abnormal loss of Rs. 20,000 incurred in the year ended 31st March, 2017 because of a machine becoming obsolete in accident.

(iii) Overhauling cost of second hand machinery purchased on 1st July, 2017 amounting to Rs. 1,00,000 was debited to Repairs Account. Depreciation is charged @ 20% p.a. on Written Down Value Method.

Calculate the value of goodwill.

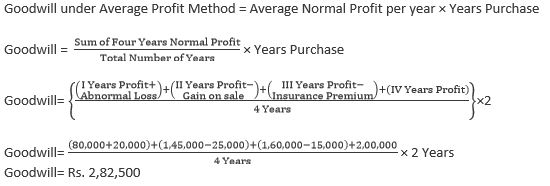

Answer :

Goodwill under Average Profit Method = Average Normal Profit per year × Years Purchase

Point of Knowledge:-

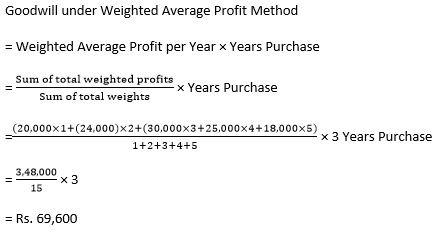

Goodwill under weighted Average Profit Method

= Weighted Average profit per year × Years Purchase

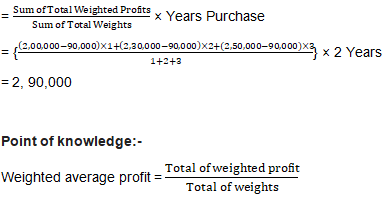

Question : Calculate goodwill of a firm on the basis of three years' purchase of the Weighted Average Profit of the last four years. The profits of the last four financial years ended 31st March, were: 2016 – Rs. 25,000; 2017 – Rs. 27,000; 2018 – Rs. 46,900 and 2019 – Rs. 53,810. The weights assigned to each year are: 2016 − 1; 2017 − 2; 2018 − 3; 2019 − 4. You are supplied the following information:

(i) On 1st April, 2016, a major plant repair was undertaken for Rs. 10,000 which was charged to revenue. The said sum is to be capitalised for goodwill calculation subject to adjustment of depreciation of 10% on Reducing Balance Method.

(ii) The Closing Stock for the years ended 31st March, 2017 and 2018 were overvalued by Rs. 1,000 and Rs. 2,000 respectively.

(iii) To cover management cost an annual charge of Rs. 5,000 should be made for the purpose of goodwill valuation.

Answer :

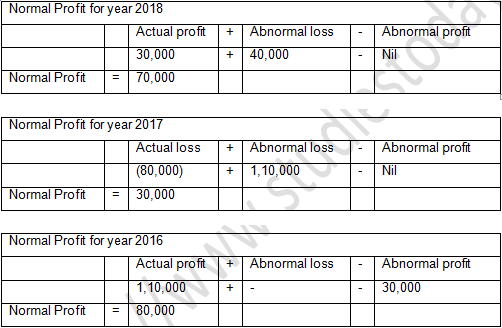

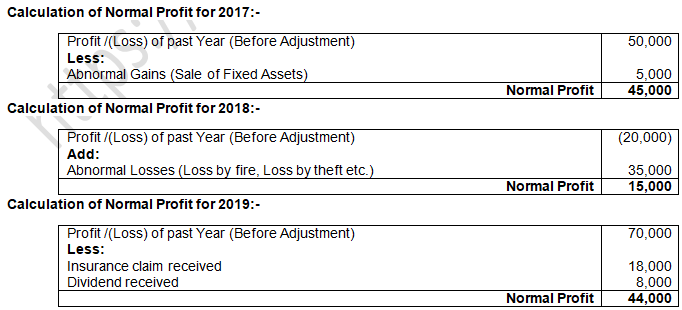

Question : Dinesh and Mahesh are partners sharing profits and losses in the ratio of 3:2. They admit Ramesh into partnership for 1/4th share in profits. Ramesh brings in his share of goodwill in cash. Goodwill for this purpose shall be calculated at two years' purchase of the weighted average normal profit of past three years. Weights being assigned to each year 2017−1; 2018−2 and 2019−3. Profits of the last three years were:

2017 − Profit Rs. 50,000 (including profits on sale of assets Rs. 5, 000.)

2018 − Loss Rs. 20,000 (including loss by fire Rs. 35, 000.)

2019 − Profit Rs. 70,000 (including insurance claim received 18,000 and interest on investments and dividend received Rs. 8, 000.)

Calculate the value of goodwill. Also, calculate the goodwill brought in by Ramesh.

Answer :

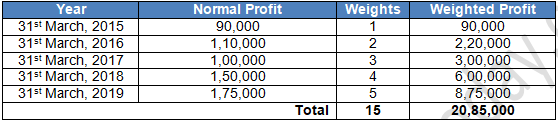

Question : Manbir and Nimrat are partners and they admit Anahat into partnership. It was agreed to value goodwill at three years' purchase on Weighted Average Profit Method taking profits of last five years. Weights assigned to each year as 1, 2, 3, 4 and 5 respectively to profits for the year ended 31st March, 2015 to 2019. The profits for these years were: Rs. 70,000, Rs. 1,40,000, Rs. 1,00,000, Rs. 1,60,000 and Rs.1,65,000 respectively.

Scrutiny of books of account revealed following information:

(i) There was an abnormal loss of Rs. 20,000 in the year ended 31st March, 2015.

(ii) There was an abnormal gain (profit) of Rs. 30,000 in the year ended 31st March, 2016.

(iii) Closing Stock as on 31st March, 2018 was overvalued by Rs. 10,000.

Calculate the value of goodwill.

Answer :

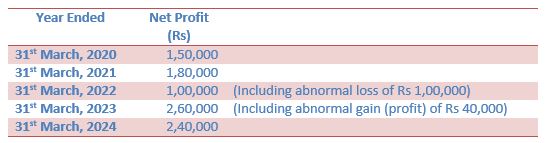

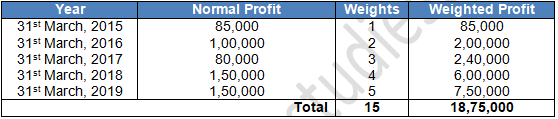

Question : Mahesh and Suresh are partners and they admit Naresh into partnership. They agreed to value goodwill at three years' purchase on Weighted Average Profit Method taking profits for the last five years. They assigned weights from 1 to 5 beginning from the earliest year and onwards. The profits for the last five years were as follows:

Scrutiny of books of account revealed the following:

(i) A second-hand machine was purchased for Rs. 5,00,000 on 1st July, 2017 and Rs. 1,00,000 were spent to make it operational. Rs. 1,00,000 were wrongly debited to Repairs Account. Machinery is depreciated @ 20% p.a. on Written Down Value Method.

(ii) Closing Stock as on 31st March, 2018 was undervalued by Rs. 50,000.

(iii) Remuneration to partners was to be considered as charge against profit and remuneration of Rs.20,000 p.a. for each partner was considered appropriate.

Calculate the value of goodwill.

Answer :

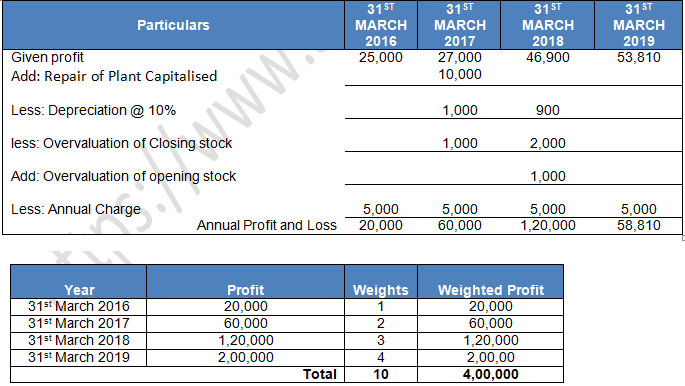

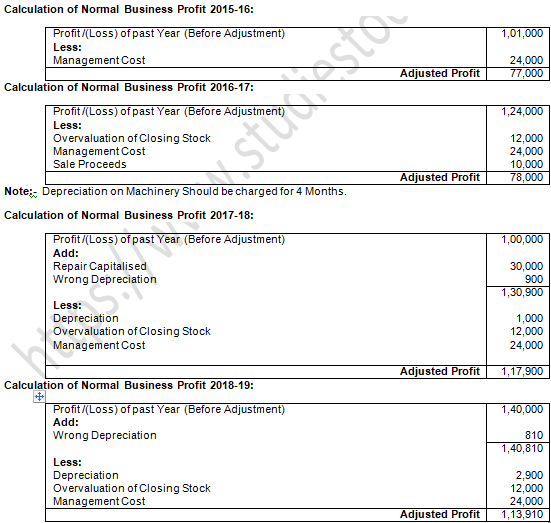

Question : Calculate the goodwill of a firm on the basis of three years' purchase of the weighted average profit of the last four years. The appropriate weights to be used and profits are:

![]()

On a scrutiny of the accounts, the following matters are revealed:

(i) On 1st December, 2017, a major repair was made in respect of the plant incurring Rs. 30,000 which was charged to revenue. The said sum is agreed to be capitalised for goodwill calculation subject to adjustment of depreciation of 10% p.a. on reducing balance method.

(ii) The closing stock for the year 2016-17 was overvalued by Rs. 12,000.

(iii) To cover management cost, an annual charge of Rs. 24,000 should be made for the purpose of goodwill valuation.

(iv) On 1st April, 2016, a machine having a book value of Rs. 10,000 was sold for Rs. 11,000 but the proceeds were wrongly credited to profit and loss account. no effect has been given to rectify the same.

Depreciation is charged on machine @ 10% p.a. on reducing balance method.

Answer :

Weighted average profit = (Total of weighted profit)/(Total of weights)

= 10,41,640/10

= Rs. 1,04,234

Goodwill = Weighted Average Profit × No. of Year Purchase

= 1,04,234 × 3

= Rs. 3,12,702

Working Note:-

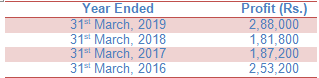

Question : A partnership firm earned net profits during the past three years as follows:

![]()

Point of Knowledge:-

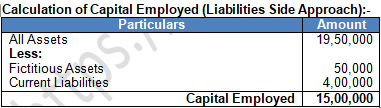

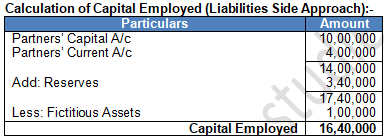

(a) Liabilities Side Approach:

Capital Employed = Capital + Reserve – Fictitious Assets – Non-trade Investments

(b) Assets Side Approach:

Capital Employed = All Assets (except goodwill, fictitious assets and non-trade investments) – Outside Liabilities.

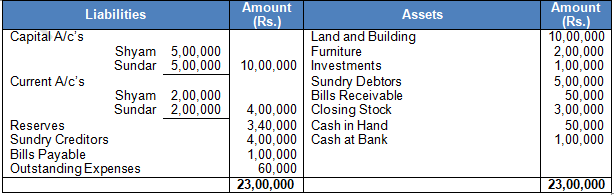

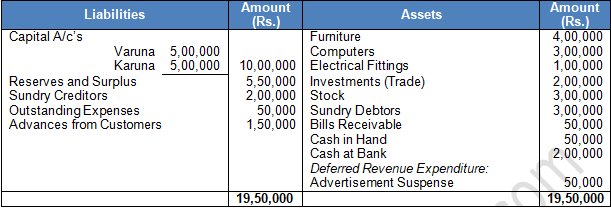

Question : Varuna and Karuna are partners for equal shares. They admit Lata into partnership for 1/4th share. It was agreed to value goodwill of the firm at 4 years' purchase of super profit. Normal rate of return is 15% of the capital employed. Average profit of the firm is Rs. 4,00,000. Balance Sheet of the firm as at 31st March, 2019 was as follows:

Average Profit = 4,00,000 (Given)

Super Profit = Actual Profit – Normal Profit