Read TS Grewal Accountancy Class 11 Solution Chapter 20 Accounts from Incomplete Records Single Entry System 2026. Students should study TS Grewal Solutions Class 11 Accountancy available on Studiestoday.com with solved questions and answers. These chapter-wise answers for Class 11 Accountancy have been prepared by expert teachers. These TS Grewal Class 11 Solutions have been designed as per the latest accountancy TS Grewal Book for Class 11 and if practiced thoroughly can help you to score good marks in Accounts class tests and examinations.

Class 11 Accounts Chapter 20 Accounts from Incomplete Records Single Entry System TS Grewal Solutions

TS Grewal Solutions for Chapter 20 Accounts from Incomplete Records Single Entry System Class 11 Accounts have been provided below based on the latest TS Grewal Class 11 book. The answers have been prepared based on the latest 2026 book for the current academic year. TS Grewal Solutions Class 11 will help students to improve their concepts and easily solve accountancy questions for Class 11.

Chapter 20 Accounts from Incomplete Records Single Entry System TS Grewal Class 11 Solutions

About this chapter: As many companies maintain their books of accounts based on cash transactions therefore in order to maintain accurate financial statements it is important to convert single-entry records into double entry records. In this chapter the concept of how to prepare financial books on the basis of incomplete records which are using a single entry system. As this is an important topic the students should understand the methods of converting single entry records into double entry into records including the process of maintaining the financial statements based on this type of accounting. All the concepts have been explained very clearly in this chapter including all the techniques to maintain accurate books. The chapter also includes a lot of the articles and practical questions. Our accountancy teachers have solved all the questions in the chapter, you can refer to the answers below.

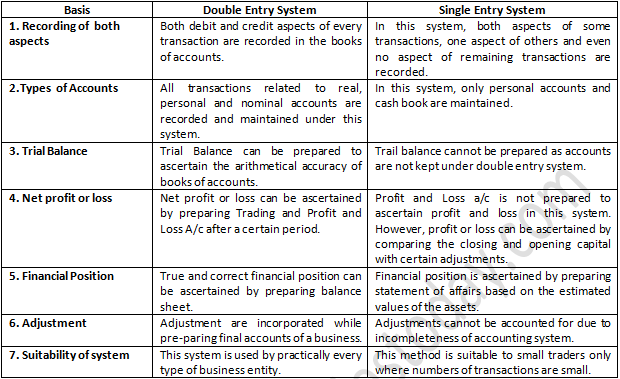

Question .1 Define Single Entry System. What are the defects of this system?

Answer 1.

According to Kohler, “Single Entry System is a System of book keeping in which as a rule only records of cash and of personal accounts are maintained, it is always incomplete double entry varying with the circumstances.

Below are the defects in Single Entry System:-

1. Absence of Trail Balance: Since accounts are not kept on double entry system so trail balance cannot be prepared to ascertain the arithmetical accuracy of the books of accounts.

2. Incomplete and unscientific system: Since the method is not based on the principal of double entry system so it cannot be called as scientific method.

3. True Profit and Loss cannot be ascertained: Trading and profit and loss account cannot be prepared as records of nominal accounts are kept. The Profit or Loss is ascertained by comparing the closing capital and opening capital with certain adjustments.

4. Difficulty I preparing Balance Sheet: Usually accounts of real accounts are not maintained so balance sheet cannot be prepared to exhibit a true and fair view of financial position of the business. However, statement of affairs is prepared based on estimated values of assets and liabilities.

Question .2 Mention three characteristics of single Entry System.

Answer 2.

Below are the characteristics of Single Entry System:-

1. Suitability:- This system of accounting is suitable only to small traders like sole trader or partnership firm. Companies are not allowed to follow this system of accounting as per provision of Companies Act, 1956.

2. Maintenance of Personal Accounts:- Under this system, only personal accounts are kept and maintained while real and nominal accounts are not kept.

3. Maintenance of Cash Book:- A Cash Book is maintained in this system containing the business and personal transaction of the owner.

Question .3 What is a Statement of Affairs? How does it differ from the Balance Sheet?

Answer 3.

A Statement of Affairs is a statement of assets and liabilities. The difference between the two represents capital of the owner.

Under this method, profit and loss is ascertained by comparing the capital at the end and at the beginning of the accounting period with some adjustments. The capital at the end and at the beginning is ascertained by preparing closing as well as opening statement of affairs. A statement of affairs is similar to balance sheet thought not exactly the same.

In the absence of records of real and nominal accounts, final accounts of a sole proprietorship firm can be prepared. However, Trading Accounts and Profit and Loss Accounts cannot be prepared by converting the available information into double entry records and by ascertaining the missing information. The amount of assets and liabilities can be computed based on estimates so balance sheet prepared under this system is called Statement of Affairs and not Balance Sheet.

Question .4 What is the difference between Single Entry System and Double Entry System?

Answer 4.

Question .5 How profit is calculated under Statement of Affairs Method?

Answer 5.

Calculation of Profit and loss:-

Following steps are followed to find out the profit and loss made during the accounting period:

Step 1. Prepare Statement of affairs at the beginning of the year to find out the opening capital.

Step 2. Also Prepare Statement of Affairs at the end to find out the capital at the end of the accounting period.

Step 3. Adjust the closing capital: Adjusted capital = Closing capital + Drawings – Additional capital introduced.

(a) Drawings is added on the logic that capital would be more if there was no drawing during the year.

(b) Further capital is deducted on the logic that capital would have not increased if there was no addition of the capital during the year.

Step 4. Profit or Loss = Adjusted closing capital – Opening capital

Question .6 “Single Entry System of book keeping is most incomplete, inaccurate, unscientific and unsystematic.” Discuss this statement.

Answer 6.

“Single Entry System of book keeping is most incomplete, inaccurate, unscientific and unsystematic.” Below are the defects in Single Entry System:-

1. Absence of Trail Balance: Since accounts are not kept on double entry system so trail balance cannot be prepared to ascertain the arithmetical accuracy of the books of accounts.

2. Incomplete and unscientific system: Since the method is not based on the principal of double entry system so it cannot be called as scientific method.

3. True Profit and Loss cannot be ascertained: Trading and profit and loss account cannot be prepared as records of nominal accounts are kept. The Profit or Loss is ascertained by comparing the closing capital and opening capital with certain adjustments.

4. Difficulty I preparing Balance Sheet: Usually accounts of real accounts are not maintained so balance sheet cannot be prepared to exhibit a true and fair view of financial position of the business. However, statement of affairs is prepared based on estimated values of assets and liabilities.

5. No use of internal Check system: Internal check system cannot be employed among employee of the business as accounts are not kept on double entry system so the chances of existence of errors and frauds are there in this system.

Question .7 Give any three advantages of Single Entry System of Accounting.

Answer 7.

Below are the advantages of Single Entry System:

1. Simple Method: Since accounts are not maintained on double entry system so no specialized knowledge for maintaining accounts is required.

2. Less Expensive: Only Cash Book and records of personal accounts are kept in this system so the method is less expensive in relation to double entry system.

3. Easy to compute profit and loss: At the end of the accounting period, only the statement of affairs is prepared to find out the closing capital. The comparison of closing capital with opening capital along with some adjustments reveals the profit and loss during the accounting period.

Practical Problems.....................

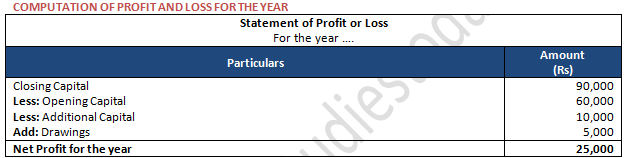

Question 1: Following information of an accounting year is given:

Opening Capital Rs 60,000; Drawings Rs 5,000; Capital added during the year Rs 10,000 and Closing Capital Rs 90,000. Calculate the Profit and Loss for the year.

Answer 1:

Net profit for the year is Rs. 25,000.

Point of Knowledge:-

Closing Capital = Opening Capital + Net Profit + Additional Capital – Drawings

Rs. 90,000 = Rs. 60,000 + Net Profit + Rs. 10,000 – Rs. 5,000

Rs. 90,000 = Rs. 65,000 +Net Profit

Net Profit = Rs. 90,000 – Rs. 65,000

Net Profit = Rs. 25,000

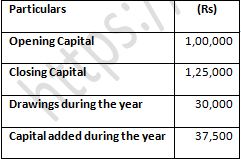

Question 2: Mayank does not keep proper records of his business; he gives you the following information:

Calculate the profit or loss for the year.

Answer 2:

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Net profit for the year is Rs. 17,500.

Point of Knowledge:-

Closing Capital = Opening Capital + Net Profit + Additional Capital – Drawings

Rs. 1,25,000 = Rs. 1,00,000 + Net Profit + Rs. 37,500 – Rs. 30,000

Rs. 1,25,000 = Rs. 1,07,500 +Net Profit

Net Profit = Rs. 1,25,000 – Rs. 1,07,500

Net Profit = Rs. 17,500

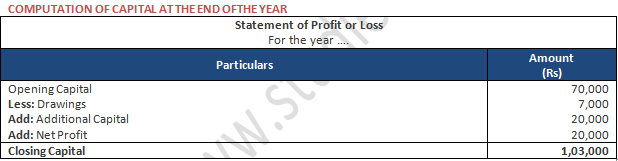

Question 3: Capital of Ganesh Gupta in the beginning of the year was Rs 70,000. During the year his business earned a profit of Rs 20,000, he withdrew Rs 7,000 for his persona use. He sold ornaments of his wife for Rs 20,000, and invested that amount into the business. Find out his Capital at the end of the year.

Answer 3:

Capital at the end of the year is Rs. 1,03,000.

Point of Knowledge:-

Closing Capital = Opening Capital + Net Profit + Additional Capital – Drawings

Closing Capital = Rs. 70,000 + Rs. 20,000 + Rs. 20,000 – Rs. 7,000

Closing Capital = Rs. 1, 03,000

Question 4: Pankaj maintains his books of account on Single Entry System. He provides following information from his books. Find out additional capital introduced in the business during the year 2023-24.

Opening Capital–Rs. 1,30,000

Drawing during the year Rs. 50,000

Closing Capital–Rs. 2,00,000

Profit made during the year Rs. 1,00,000

Answer 4:

COMPUTATION OF ADDITIONAL CAPITAL INTRODUCED DURING THE YEAR 2023–24

Additional capital for the year 2017-18 is Rs. 20,000.

Point of Knowledge:-

Additional Capital = Closing Capital – Opening Capital – Net Profit + Drawings

Additional Capital = Rs. 2,00,000 – Rs.1,30,000 – Rs. 1,00,000 + Rs. 50,000

Additional Capital = Rs. 20,000

Question 5: Vikas maintains books on Single Entry System. He gives you the following information:

You are required to calculate the Profit or Loss made by Vikas.

Answer 5:

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Net profit for the year is Rs. 4,500.

Point of Knowledge:-

Closing Capital = Opening Capital + Net Profit + Additional Capital – Drawings

Rs. 16,900 = Rs. 15,200 + Net Profit + Rs. 2,000 – Rs. 4,800

Rs. 16,900 = Rs. 12,400 + Net Profit

Net profit = Rs. 4,500

Question 6: Gurman who keeps his books on Single Entry System sells goods at Cost plus 50%. On 1st April, 2023 his Capital was Rs. 4,00,000 and on 31st March, 2024 it was Rs. 3,50,000. He had withdrawn Rs. 20,000 per month besides goods of the sale value of Rs. 60,000. How much did he earn in 2023-24?

Answer 6:

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Net profit for the year is Rs. 56,000.

Point of knowledge:-

Sales = Cost + Profit

Rs. 60,000 = COST + (COST × 50%)

Rs. 60,000 = COST + COST/2

Rs. 60,000 = 2COST + COST/2

Rs. 60,000 = 3COST/2

Rs. 1,20,000 = 3 cost

Cost = 1,20,000/3

Cost = Rs. 40,000

So, the amount of drawings is Rs. 40,000 as the drawings by the owner can’t be at sales price but at cost price.

Closing Capital = Opening Capital + Net profit + Additional Capital – Drawings

Rs. 3,50,000 = Rs. 4,00,000 + Net Profit + 0 - ( Rs. 20,000 × 12 + Rs. 40,000)

Rs. 3,50,000 = Rs. 4,00,000 + Net Profit + 0 - (2,40,000 + 40,000)

Rs. 3,50,000 = Rs. 4,00,000 + Net Profit - Rs. 2,80,000

Rs. 3,50,000 = Rs. 1,20,000 + Net Profit

Net Profit = Rs. 3,50,000 – Rs. 1,20,000

Net Profit = Rs. 2,30,000

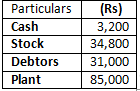

Question 7: Krishan started his business on 1st April, 2023 with a Capital of Rs 1,00,000. On 31st March, 2024, his assets were:

He owed Rs 12,000 to sundry creditors and Rs 10,000 to his brother on that date. He withdrew Rs 2,000 per month for the private expenses. Ascertain his profit.

Answer 7:

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Closing Capital = Opening Capital + Net Profit – Drawings

Rs.1,32,000 = Rs. 1,00,000 + Net Profit – Rs. 24,000

Rs.1,32,000 = Rs. 1,24,000 + Net Profit

Net Profit = Rs. 1,32,000 – Rs. 1,24,000

Net Profit = Rs. 56,000

Total Drawings during the year = Rs. 2,000 × 12 = Rs. 24,000

Question 8: Muneesh maintains his books on Single Entry System and from them and the particulars supplied, the following figures were gathered together on 31st March, 2024:

Book Debts Rs 10,000; Cash in Hand Rs 510; Stock-in-Trade (estimated) Rs 6,000; Furniture and Fittings Rs 1,200; Trade Creditors Rs 4,000; Bank Overdraft Rs 1,000; Muneesh stated that he started business on 1st April 2023 with cash Rs 6000 paid into bank but stocks valued at Rs 4,000. During the year he estimated his drawings to be Rs 2,400. You are required to prepare the statement, showing the profit for the year, after writing off 10% for Depreciation on Furniture and Fittings.

Answer 8:

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Net Profit = Closing Capital – Opening Capital + Drawings

Net Profit = Rs. 12,590 – Rs. 10,000 + Rs. 2,400

Net Profit = Rs. 4,990

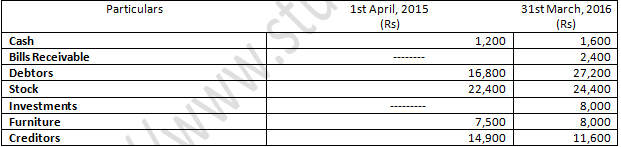

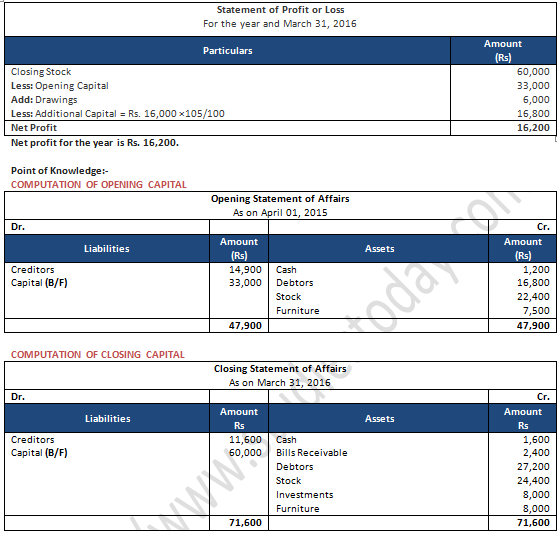

Question 9: Shruti maintains her books of account from Incomplete Records. Her books provide the following information:

She withdrew Rs 500 per month for personal expenses. She sold her Investments of Rs 16,000 at 5% premium and introduced the amount into business.

You are required to prepare a Statement of Profit or Loss for the year ending 31st March, 2016.

Answer 9:

Computation of profit and loss for the year

Net Profit = Closing Capital – Opening Capital + Drawings – Additional Capital

Net Profit = Rs. 60,000 – Rs. 33,000 + (Rs. 500×12) – Rs.16,000 × 105/100

Net profit = Rs. 60,000 – Rs. 33,000 + Rs. 6,000 – Rs. 16,800

Net Profit = Rs. 16,200

Question 10: Swastik maintains her books of account on Single Entry System. His books provide the following information:

His drawings during the year were Rs 5,000 Depreciate furniture by 10% and provide a reserve for Bad and Doubtful Debts at 10% on Sundry Debtors. Prepare the statement showing the profits for the year.

Answer 10:

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Net Profit = Closing Capital – Opening Capital + Drawings

Net Profit = Rs. 53,900 – Rs. 35,000 + Rs. 5,000

Net Profit = Rs. 23,900

Question 11: Mahesh commenced business on 1st April, 2023 with capital of Rs 10,000. He immediately bought Furniture and Fixtures for Rs 2,000. On 1st October, 2023, he borrowed Rs 5,000 from his wife @ 9% p.a. (interest not yet paid) and introduced a further capital of his own amounting to Rs 1,500. A drew @ Rs 300 per month at the end of each month for household expenses. On 31st March, 2024 his position was as follows:

Cash in Hand Rs 2,800; Sundry Debtors Rs 6,400; Stock Rs 6,800; Sundry Creditors Rs 500 and owing for Rent Rs 150. Furniture and Fixtures to be depreciated by 10%.

Ascertain the profit earned or loss incurred by Mahesh during the year ended 31st March, 2024.

Answer 11:

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Closing Capital = Opening Capital + Net Profit + Additional Capital – Drawings

Rs. 11,925 = Rs. 10,000 + Net Profit + Rs. 1,500 – Rs. 3,600

Rs. 11,925 = Rs. 15,100 + Net Profit

Net profit = Rs. 15,100 – Rs. 11,925

Net Profit = Rs. 4,025

Question 12: Kuldeep, a general merchant, keeps his accounts on Single Entry System. He wants to know the results, of his business on 31st March, 2024 and for that following information is available:

During the year, he had withdrawn Rs 5,00,000 for his personal use and invested Rs 2,50,000 as additional capital. Calculate his profits on 31st March, 2024 and prepare the Statement of Affairs as on that date.

Answer 12:

In the books of kuldeep

Net Profit = Closing Capital – Opening Capital – Additional Capital + Drawings

Net Profit = Rs. 16,25,000 – Rs. 14,00,000 – Rs. 2,50,000 + Rs. 5,00,000

Net Profit = 4,75,000

Question 13: From the following information relating to the business of Abhay who keeps books on Single Entry System, ascertain the profit or loss for the year 2023-24:

Abhay withdrew Rs. 4,100 during the year to meet his household expenses. He introduced Rs. 300 as fresh capital on 15th January, 2024. Machinery and Furniture are to be depreciated at 10% and 5% p.a. respectively.

Answer 13:

Question 14: Following information is supplied to you by a shopkeeper:

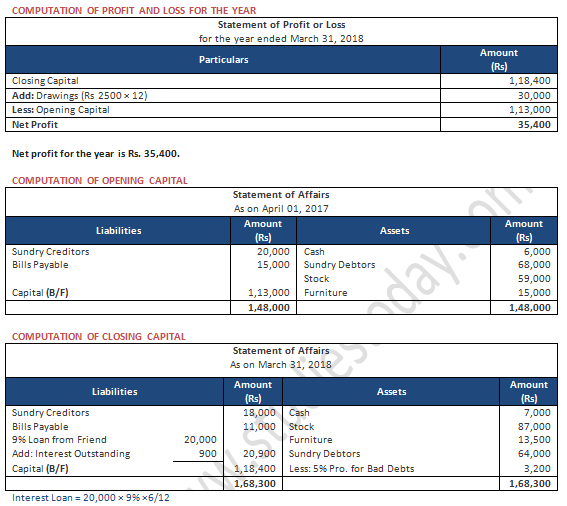

During the year, he withdrew Rs 2,500 per month for domestic purposes. He also borrowed from a friend at 9% a sum of Rs 20,000 on 1st October, 2017. He has not yet paid the interest. A provision of 5% on debtors for doubtful debts is to be made.

Ascertain the profit or loss made by him during the period.

Answer 14:

Question 15: Vikas is keeping his accounts according to Single Entry System. His capital on 31st March, 2023 was Rs. 2,50,000 and his capital on 31st March, 2024 was Rs. 4,25,000. He further informs you that during the year he gave a loan of Rs. 30,000 to his brother on private account and withdrew Rs. 1,000 per month for personal purposes. He used a flat for his personal purpose, the rent of which @ Rs. 1,800 per month and electricity charges at an average of 10% of rent per month were paid from the business account. During the year he sold his 7% Government Bonds of Rs. 50,000 at 1% premium and brought that money into the business. Prepare a Statement of Profit or Loss for the year ended 31st March, 2024.

Answer 15:

IN THE BOOKS OF VIKAS

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR

Net profit for the year is Rs. 1,90,260.

Point of Knowledge:-

Calculation of Total Drawings = Rs. 30,000 + (Rs. 1,000×12) + (1,800 × 12 × (100+10)/100 ) = 65,760

Calculation of Additional Capital = Rs. 50,000 × (100+01)/100 = Rs. 50,500

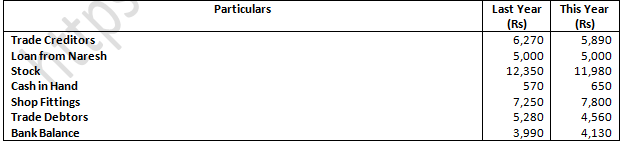

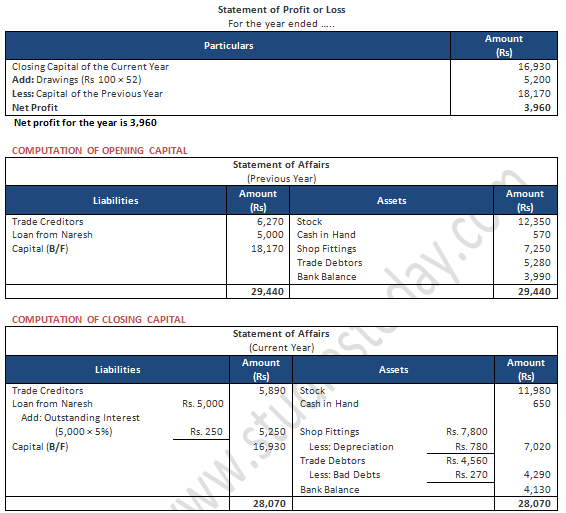

Question 16: Gurman, a retailer, has not maintained proper books of account but it has been possible to obtain the following details

Calculate the net profit for this year and draft the Statement of Affairs at the end of the year after noting that:

(a) Shop Fittings are to be depreciated by Rs 780.

(b) X has drawn Rs 100 per week for his own use.

(c) Included in the Trade Debtors is an irrecoverable balance of Rs 270.

(d) Interest at 5% p.a. is due on the loan from Naresh but has not been paid for the year.

Answer 16:

Computation of profit and loss for the year

Question 17: On 1st April, 2023, X started a business with Rs 40,000 as his capital. On 31st March, 2024, his position was as follows:

During the year 2023–24, X drew Rs 24,000. On 1st October, 2023, he introduced further capital amounting to Rs 30,000. You are required to ascertain profit on loss made by him during the year 2023–24.

Adjustments:

(a) Plant is to be depreciated at 10%.

(b) A provision of 5% is to be made against debtors, Also prepare the Statement of Affairs as on 31st March, 2024.

Answer 17:

Computation of profit and loss for the year

Net Profit = Closing Capital – Opening Capital – Additional Capital + Drawings

Net profit = Rs. 1,30,000 – Rs. 40,000 – Rs. 30,000 + Rs. 24,000

Net Profit = Rs. 84,700

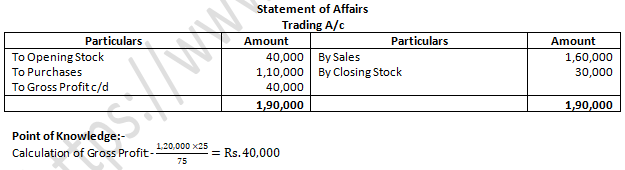

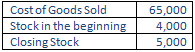

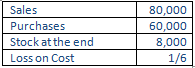

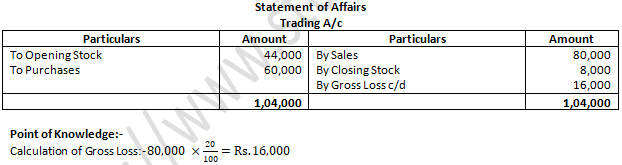

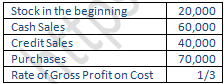

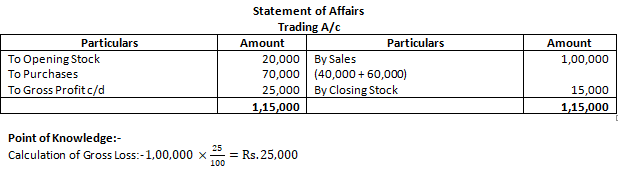

Question 18. A firm sells goods at a Gross Profit of 25% of sales. On 1st April, 2020 the Stock was Rs. 40,000; Purchases were Rs. 1,10,000 and the Stock on 31st March, 2021 was Rs. 30,000. What was the value of Sales?

Answer 18.

Question 19. A firm sells goods at Cost plus 25%. Sales to credit customers (3/4 of total) was Rs. 1,80,000. His Opening and Closing Stock were Rs. 20,000 and Rs. 15,000 respectively. Find out the value of Purchases.

Answer 19.

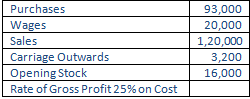

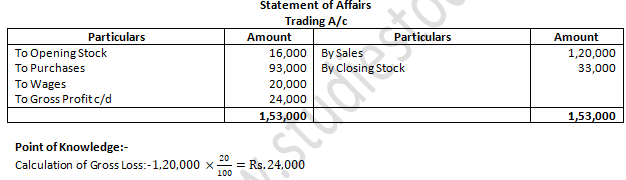

Question 20. Calculate Purchases:

Answer 20.

Calculation of Purchases:-

Purchases = Cost of Goods Sold – Opening Stock + Closing Stock

Purchases = Rs. 65,000 – Rs. 4,000 + Rs. 5,000

Purchases = Rs. 66,000

Question 21. Calculate Stock in the beginning:

Answer 21.

Question 22. Calculate Stock in the end:

Answer 22.

Question 23. Calculate at the value of Closing Stock from the following information:

Answer 23.

Question 24. Calculate Sales:

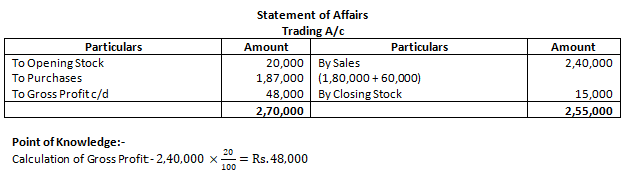

![]()

Answer 24.

Sales = Cost of goods sold + Gross Profit

Sales = 2,00,000 + 50,000

Sales = 2,50,000

Gross Profit = 2,00,000 × 25/100

Gross Profit = 50,000

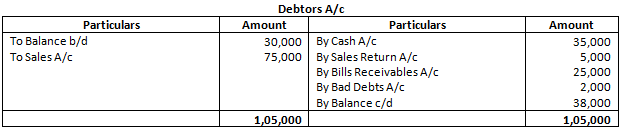

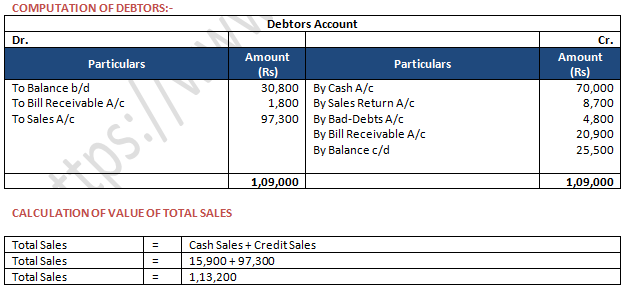

Question 25. Debtors in the beginning of the year were Rs. 30,000, Sales on Credit during the year were Rs. 75,000. Cash received from the Debtors during the year was Rs. 35,000, Returns Inward (regarding credit sales) were Rs. 5,000 and Bills Receivable drawn during the year were Rs. 25,000. Find the balance of Debtors at the end of the year, assuming that there were Bad Debts during the year of Rs. 2,000.

Answer 25.

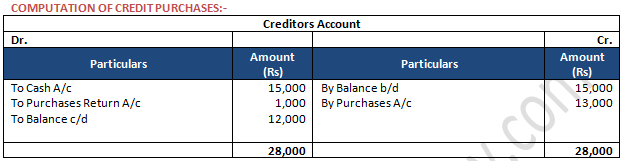

Question 26: Following information is given of an accounting year:

Opening Creditors Rs. 15,000; Cash paid to creditors Rs. 15,000; Returns Outward Rs. 1,000 and Closing creditors Rs. 12,000.

Calculate Credit Purchases during the year.

Answer 26:

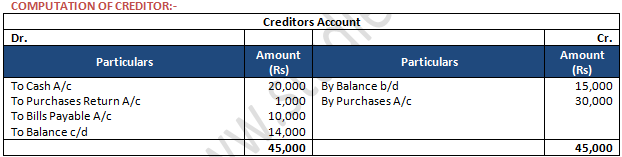

Question 27: Creditors on 1st April, 2018 were Rs. 15,000, Purchases on credit were Rs. 30,000, Cash paid to Creditors during 2018-19 was Rs. 20,000, Returns Outward (regarding credit purchases) was Rs. 1,000 and Bills Payable accepted during the year Rs. 10,000. Find the balance of Creditors on 31st March, 2019.

Answer 27:

Question 28. From the following information, calculate the amount to be shown in Profit and Loss Account in the following cases:

(i) Rent paid during the year Rs. 1,00,000. Rent Outstanding at the year-end Rs. 20,000.

(ii) Insurance premium paid during the year Rs. 50,000. Prepaid insurance Rs. 10,000.

(iii) Interest received during the year Rs. 30,000. Accrued Interest Rs. 5,000.

(iv) Commission received during the year Rs. 60,000. Unearned Commission Rs. 7,000.

Answer 28.

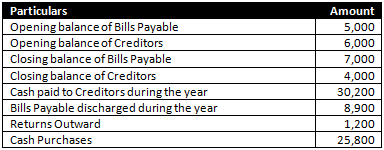

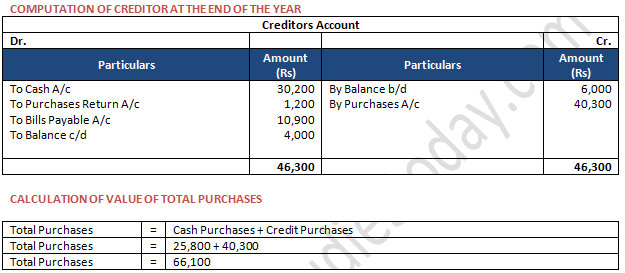

Question 29: From the following information supplied by X, who keeps his books on Single Entry System, you are required to calculate Total Purchases:

Answer 29:

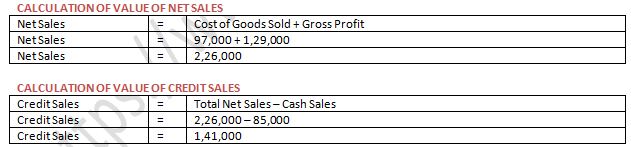

Question 30: Cash sales of a business in a year were Rs. 85,000, the Cost of Goods Sold (including direct expenses) was Rs. 97,000 and Gross Profit as shown by the Trading Account for the year was Rs. 1,29,000. Calculate Credit Sales during the year.

Answer 30:

Question 31: From the following information, calculate Total Sales made during the period:

Answer 31:

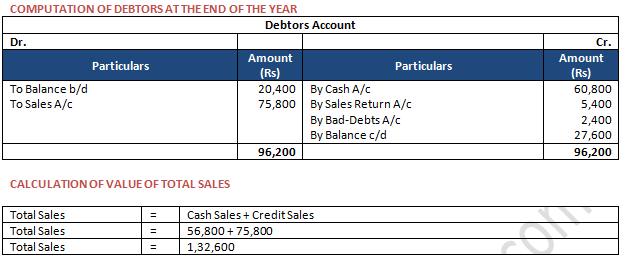

Question 32: Calculate Total Sales from the following information:

Answer 32:

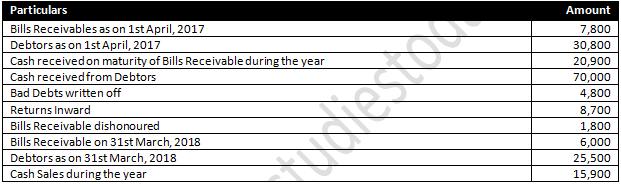

Question 33: From the following information, ascertain the opening balance of Sundry Debtors and the closing balance of Sundry Creditors:

Answer 33:

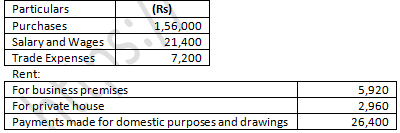

Question 34: Roshan, whose accounts are maintained by Single Entry System, acquired a retail business on 1st April, 2017. He had Rs40,000 of his own and he borrowed Rs 20,000 from his wife. He paid Rs15,000 for Goodwill, Rs5,000 for Furniture and Rs35,000 for Stock.

Total cash received by him during the financial year from the Debtors was Rs2,30,000. His payments were:

At the end of the year, the Stock was Rs37,500. He owed Rs13,500 to Creditors for goods and his customers owed to him Rs15,000. Provide 5% for Depreciation on Furniture, Interest at 5% on wife's Loan and Rs1,000 for Doubtful Debts.

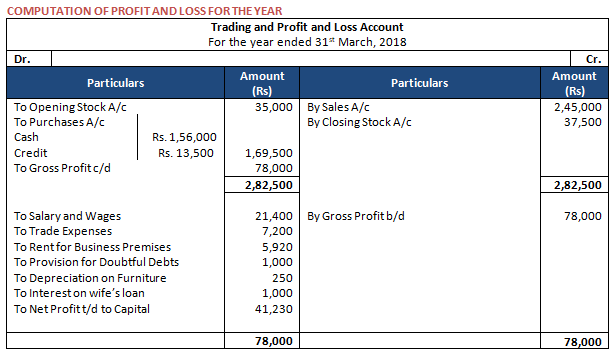

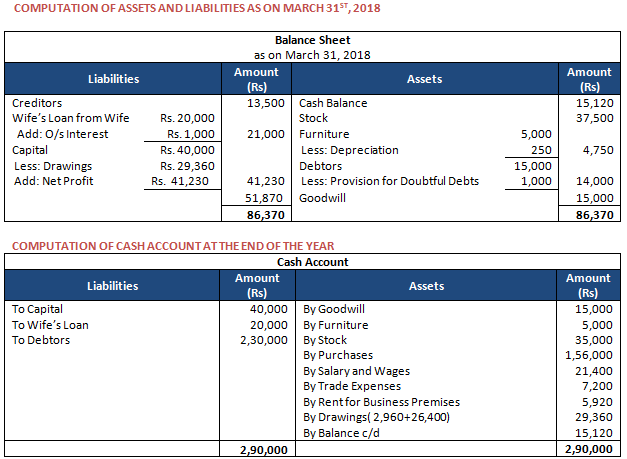

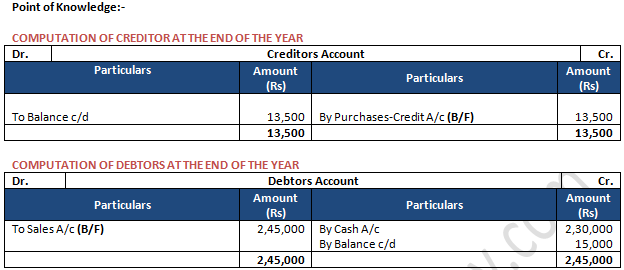

Prepare the Cash Account, the Profit and Loss Account for the year ended 31st March, 2018 and the Balance Sheet at the close of the year.

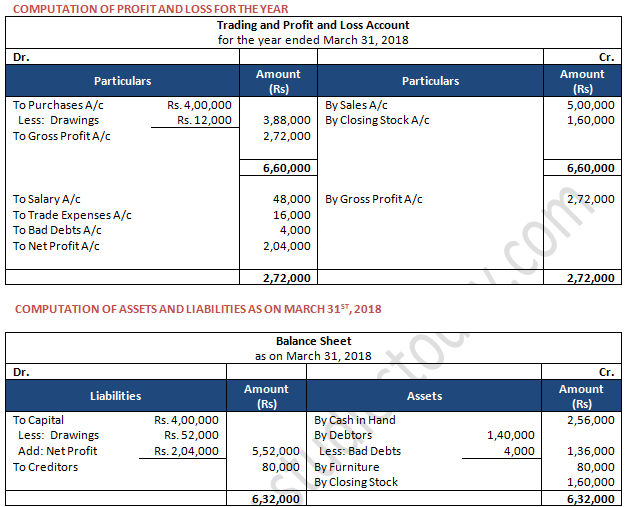

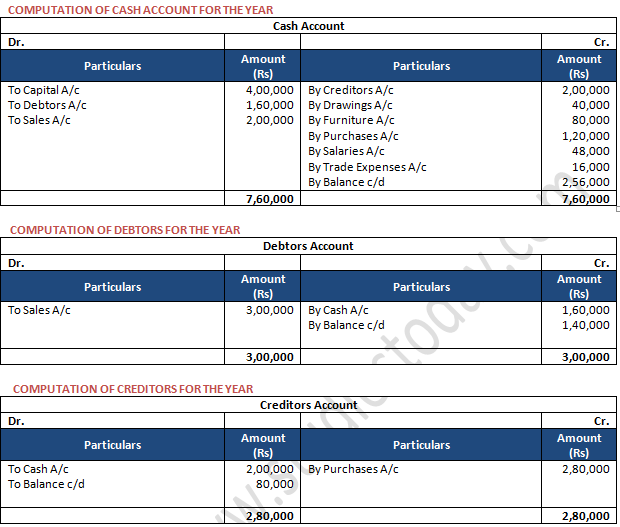

Answer 34:

Question 35: Vijay commenced business as foodgrains merchant on 1st April, 2017 with a capital of Rs4,00,000. On the same day, he purchased furniture for Rs80,000. From the following particulars obtained from his books which do not conform to Double Entry principles, you are required to prepare the Trading and Profit and Loss Account for the year ended 31st March, 2018 and the Balance Sheet as on that date:

Vijay used goods of Rs12,000 for private purposes during the year. On 31st March, 2018, his Debtors amounted to Rs1,40,000 and Creditors Rs80,000. Stock-in-Trade on that date was Rs1,60,000.

Answer 35:

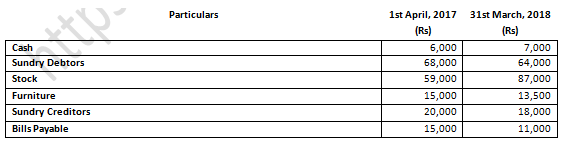

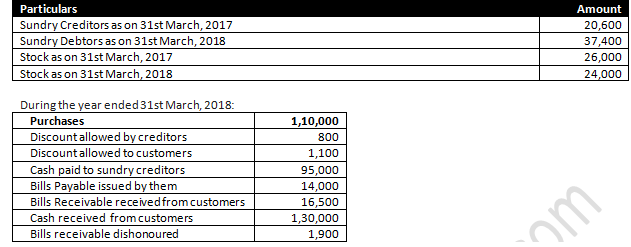

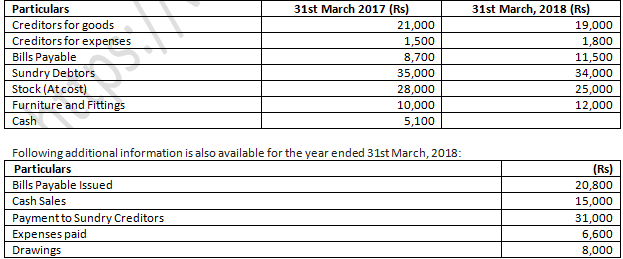

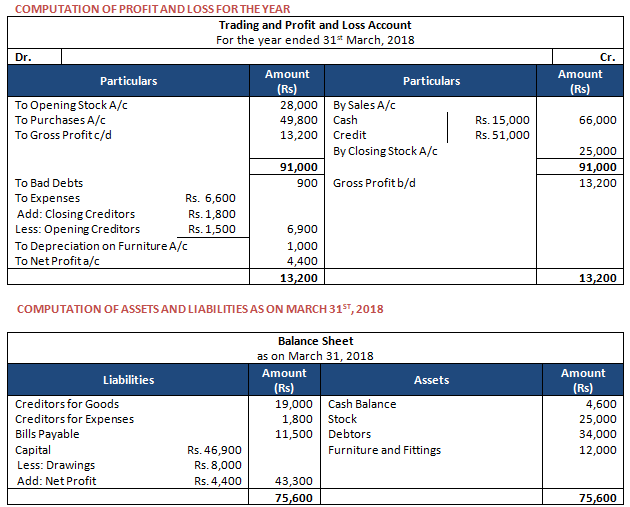

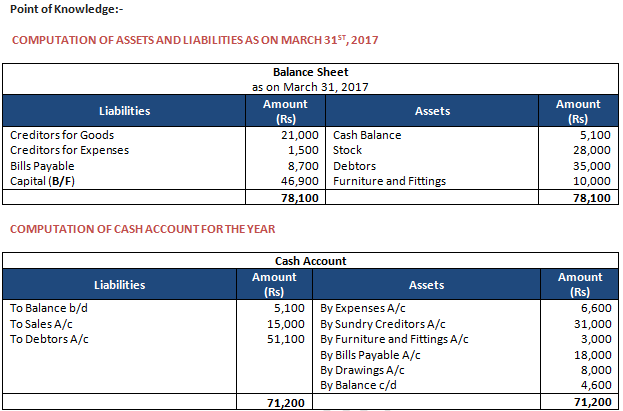

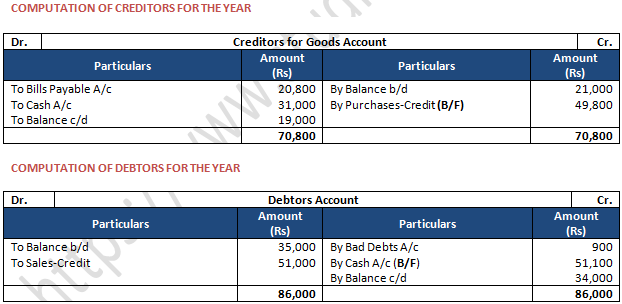

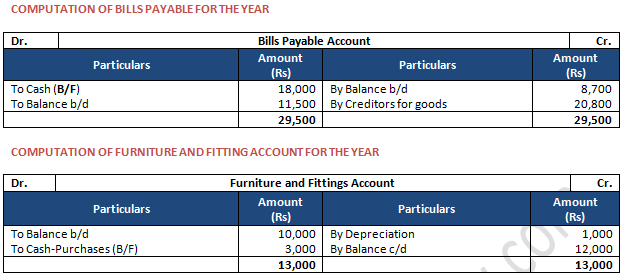

Question 36: Surya does not keep a systematic record of his transactions. He is able to give you the following information regarding his assets and liabilities:

Bad Debts during the year were Rs900. As regards sale, Surya tells you that he always sells goods at Cost plus 25%. Furniture and Fittings are to be depreciated at 10% of the value in the beginning of the year.

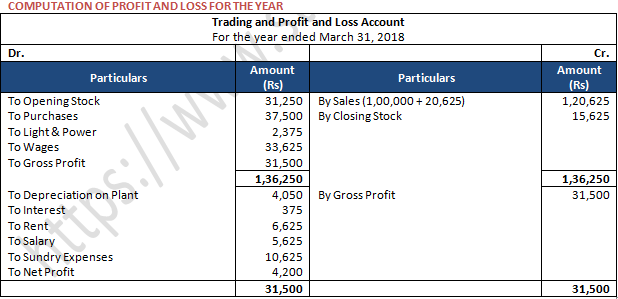

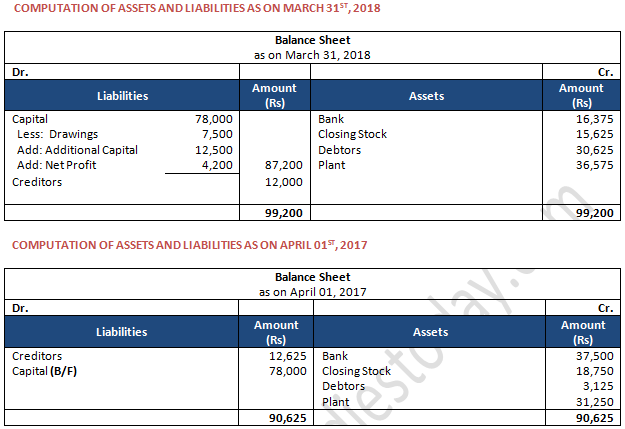

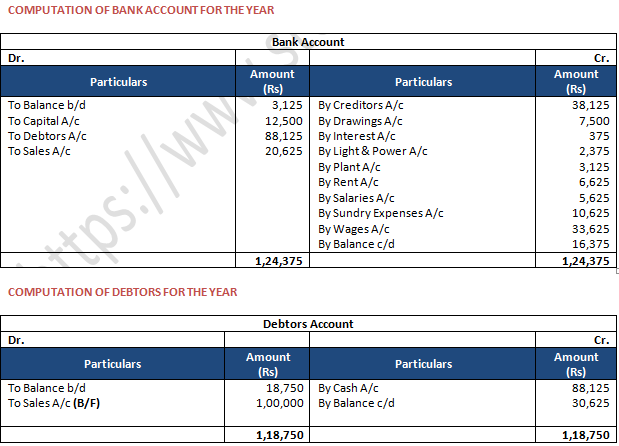

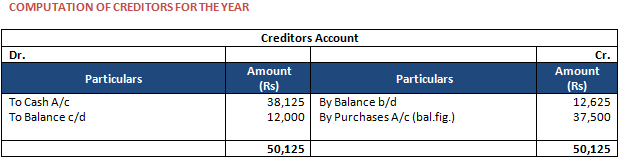

Prepare Surya's Trading and Profit and Loss Account for the year ended 31st March, 2018 and his Balance Sheet on that date.

Answer 36:

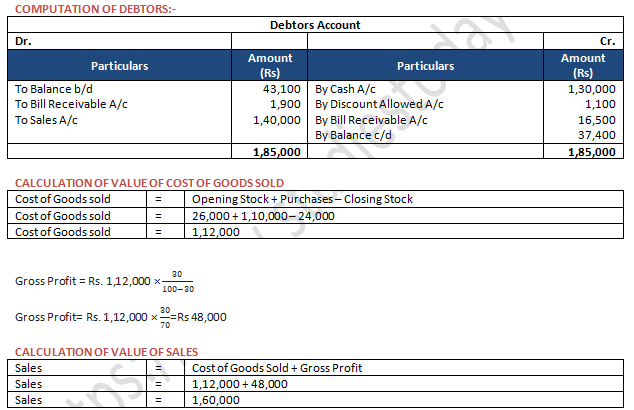

Computation of Cost of Goods Sold and Credit Sales

Cost of goods sold = Opening Stock + Purchases – Closing Stock

= Rs. 28,000 + Rs. 49,800 – Rs. 25,000

= Rs. 52,800

Gross Profit = 52,800 × 25%

= Rs. 13,200

Total Sales = COGS + Gross Profit

= Rs. 52,800 + Rs. 13,200

= Rs. 66,000

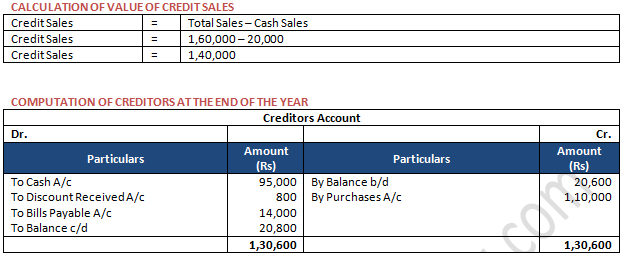

Credit Sales = Total Sales – Cash Sales

= Rs. 66,000 – Rs. 15,000

= Rs. 51,000

Points to Remember:-

1. Profit = Closing Capital + Drawings – Additional Capital – Opening Capital

2. Closing Capital = Opening Capital + Additional Capital + Profit / -loss - Drawings

3. Cost of goods sold = Opening Stock + Net Purchases + Direct Expenses – Closing Stock

4. Gross Profit = Net Sales – Cost of Goods sold

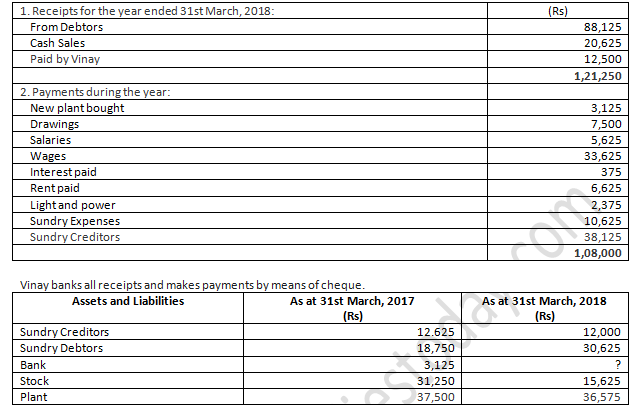

Question 37: Following information is obtained from the books of Vinay, who maintained his books of account under Single Entry System:

From the above information, prepare Trading and Profit and Loss Account for the year ended 31st March, 2018 and Balance Sheet as on that date.

Answer 37:

Question 38: Manu started business with a capital of Rs 4,00,000 on 1st October, 2005. He borrowed from his friend a sum of Rs1,00,000. He brought further Rs 75,000 as capital on 31st March, 2006, his position was:

Cash: Rs 30,000; Stock: Rs 4,70,000; Debtors: Rs 3,50,000 and Creditors: Rs 3,00,000.

He withdrew Rs 8,000 per month during this period. Calculate profit on loss, for the period.

Answer 38:

IN THE BOOKS OF MANU

Net Profit = Closing Capital – Opening Capital – Additional Capital + Drawings

Net Profit = Rs. 4,50,000 – Rs. 4,00,000 – Rs. 75,000 + Rs. 48,000

Net Profit = 23,000

COMPUTATION OF PROFIT AND LOSS FOR THE YEAR