Read and download the CBSE Class 12 Accountancy Accounting For Partnership Firms Worksheet Set 02 in PDF format. We have provided exhaustive and printable Class 12 Accountancy worksheets for Part 1 Chapter 1 Accounting for Partnership Basic Concepts, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts

Students of Class 12 should use this Accountancy practice paper to check their understanding of Part 1 Chapter 1 Accounting for Partnership Basic Concepts as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts Worksheet with Answers

MCQ Questions for NCERT Class 12 Accountancy Accounting For Partnership Firms

Question. Seeta and Geeta are partners sharing profits and losses in the ratio 4 : 1. Meeta was manager who received the salary of ₹4,000 p.m. in addition to a commission of 5% on net profits after charging such commission. Profit for the year is ₹6,78,000 before charging salary. Find the total remuneration of Meeta.

(a) ₹78,000

(b) ₹88,000

(c) ₹87,000

(d) ₹76,000

Answer: A

Question. If the Partners’ Capital Accounts are fixed ‘salary payable to partner’ will be recorded :

(a) On the debit side of Partners’ Current Account

(b) On the debit side of Partners’ Capital Account

(c) On the credit side of Partners’ Current Account

(d) None of the above

Answer: C

Question. For the firm interest on drawings is

(a) Capital Payment

(b) Expenses

(c) Capital Receipt

(d) Income

Answer: D

Question. Interest on Partner’s drawings will be debited to :

(a) Profit and Loss Account

(b) Profit and Loss Appropriation Account

(c) Partner’s Current Account

(d) Interest Account

Answer: C

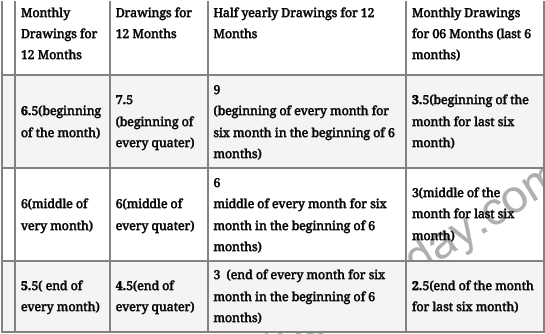

Question. If a fixed amount is withdrawn by a partner in each quarter, interest on the total amount is charged for ……………….. months

(a) 3

(b) 6

(c) 4.5

(d) 7.5

Answer: B

Question. A and B contribute ₹1,00,000 and RS₹60,000 respectively in a partnership firm by way of capital on which they agree to allow interest @ 8% p.a. Their profit or loss sharing ratio is 3 : 2. The profit at the end of the year was ₹2,800 before allowing interest on capital. If there is a clear agreement that interest on capital will be paid even in case of loss, then S’s share will be:

(a) Profit ₹6,000

(b) Profit ₹4,000

(c) Loss ₹6,000

(d) Loss ₹4,000

Answer: D

Question. Which of the following statement is true

(a) Fixed capital account will always have a credit balance

(b) Current account can have a positive or a negative balance

(c) Fluctuating capital account can have a positive or a negative balance

(d) All of the above

Answer: D

Question. When partners’ capital accounts are fixed, which one of the following items will be written in the partner’s capital account :

(a) Partner’s Drawings

(b) Additional capital introduced by the partner in the firm

(c) Loan taken by partner from the firm

(d) Loan Advanced by partner to the firm

Answer: B

Question. A, B and C are partners. A’s capital is ₹3,00,000 and B’s capital is ₹1,00,000. C has not invested any amount as capital but he alone manages the whole business. C wants RS30,000 p.a. as salary. Firm earned a profit of ₹1,50,000. How much will be each partner’s share of profit:

(a) A ₹60,000; B ₹60,000; C ₹Nil

(b) A ₹90,000; B ₹30,000; C ₹Nil

(c) A ₹40,000; B ₹40,000 and C ₹40,000

(d) A ₹50,000; B ₹50,000 and C ₹50,000.

Answer: D

Question. It the Partner’s Capital Accounts are fixed, interest on capital will be recorded:

(a) On the credit side of Current Account

(b) On the credit side of Capital Account

(c) On the debit side of Current Account

(d) On the debit side of Capital Account

Answer: A

Question. If a fixed amount is withdrawn by a partner in the middle of every month, interest on the total amount is charged for …………… months

(a) 6

(b) 6 1/2

(c) 5 1/2

(d) 12

Answer: A

Question. Sushil is a partner in a firm. He withdrew ₹4,000 per month in the middle of every month during the year ended 31st March, 2019. If interest on drawings is charged @ 8% p.a. the interest charged will be :

(a) ₹2,080

(b) ₹1,760

(c) ₹3,840

(d) ₹1,920

Answer: D

Question. On 1st April 2018, 2fs Capital was ₹2,00,000. On 1st October 2018, he introduces additional capital of ₹1,00,000. Interest on capital @ 6% p.a. on 31st March, 2019 will be :

(a) ₹9,000

(b) ₹18,000

(c) ₹10,500

(d) ₹15,000

Answer: D

Question. X and Y are partners in the ratio of 3 : 2. Their capitals are RS2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of RS60,000 for the year ended 31st March 2019. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) V ₹8.000; Y ₹4,000

(c) X ₹14,400; Y ₹9,600

(d) No Interest will be allowed

Answer: A

Question. X and Y are partners in the ratio of 3:2. Their capitals are ₹2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of ₹15,000 for the year ended 31st March 2019. As per partnership agreement, interest on capital is treated a charge on profits. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) X ₹9,000; Y ₹6,000

(c) X ₹10,000; Y ₹5,000

(d) No Interest will be allowed

Answer: A

Question. Bipasa is a partner in a firm. She withdrew ₹6,000 at the end of each quarter during the year ended 31st March, 2019. Interest on her drawings @ 10% p.a. will be :

(a) ₹900

(b) ₹600

(c) ₹1,500

(d) ₹1,200

Answer: A

Question. Partners are suppose to pay interest on drawing only when by the

(a) Provided, Agreement

(b) Permitted, Investors

(c) Agreed, Partners

(d) ‘A’ & ‘C’ above

Answer: D

Question. Where will you record interest on drawings :

(a) Debit Side of Profit & Loss Appropriation Account

(b) Credit Side of Profit & Loss Appropriation Account

(c) Credit Side of Profit & Loss Account

(d) Debit Side of Capital/Current Account only

Answer: B

Question. Vikas is a partner in a firm. His drawings during the year ended 31st March, 2019 were RS72,000. If interest on drawings is charged @ 9% p.a. the interest charged will be :

(a) ₹324

(b) ₹6,480

(c) ₹3,240

(d) ₹648

Answer: C

Question. X and Y are partners in the ratio of 3:2. Their capitals are RS2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm incurred a loss of ₹60,000 for the year ended 31st March 2019. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) A ₹8,000; Y ₹4,000

(c) X ₹14,400; Y ₹9,600

(d) No Interest will be allowed

Answer: D

Question. If a fixed amount is withdrawn by a partner on the last day of every month, interest on the total amount is charged for …………… months :

(a) 12

(b) 6 1/2

(c) 5 1/2

(d) 6

Answer: C

Question. X and Y are partners in the ratio of 3:2. Their capitals are ₹2,00,000 and ₹1,00,000 respectively. Interest on capitals is allowed @ 8% p.a. Firm earned a profit of ₹15,000 for the year ended 31st March 2019. Interest on Capital will be :

(a) X ₹16,000; Y ₹8,000

(b) X ₹9,000; Y ₹6,000

(c) X ₹10,000; Y ₹5,000

(d) No Interest will be allowed

Answer: C

Question. In a partnership firm, a partner withdrew ₹5,000 per month on the first day of every month during the year for personal expenses. If interest on drawings is charged @ 6% p.a. the interest charged will be :

(a) ₹3,600

(b) ₹1,950

(c) ₹1,800

(d) ₹1,650

Answer: B

Question. If fixed amount is withdrawn by a partner on the first day of each quarter, interest on the total amount is charged for …………….. months

(a) 4.5

(b) 6

(c) 7.5

(d) 3

Answer: C

Question. If a fixed amount is withdrawn by a partner on the last day of each quarter, interest on the total amount is charged for ……………… months

(a) 6

(b) 4.5

(c) 7.5

(d) 3

Answer: B

Short Answer questions :

Question. In the absence of Partnership deed, how are mutual relations of partners governed?

Answer: In the absence of |Partnership deed, mutual relations are governed by The Indian partnership Act 1932.

Question. A and B are partners in a firm sharing profit in the ratio of 3:2. They had advanced to the firm a sum of Rs. 30,000 as a loan in their profits sharing ratio on 1st Oct. 2014. The partnership deed is silent on the question of interest on loan for partners. Compute the interest payable by the firm to the partners, assuming the firm closes its books on 31st March.

Answer: A- Rs.540 B- Rs. 360. (Note: In the absence of Partnership deed, 6% p.a will be allowed as Interest on Loan)

Question. A,B and C are partners and decided that no interest on drawings is to be charged from any Partner. But after one Year ‘C’wants that interest on drawings should be charged from every partner. State how ‘C’ can do this?

Answer: He can do so only by changing the Partnership deed with the consent of all partners.

Question. If the partners’ capitals account are fixed where will you record drawings of partners?

Answer: Debit side of partners current A/c.

Question. Would a “Charitable Dispensary” run by 8 members be deemed a Partnership Firm? Give reason in support of your answer.

Answer: (i) In Partnership, there must be a business;

(ii) There must be sharing of profits from such business among the partners.

Question. Under fixed capital method, partner’s drawings are shown in which account?

Answer: Partners Current A/cs

Question. What is a legal status of a firm?

Answer: A firm is not a legal person it is merely a collection of partners.

Question. Mention two items that are recorded in Partners Fixed Capital Account.

Answer: i) Capital Withdrawal ii) Fresh Capital Introduced.

Question. What is meant by Partnership? / Define Partnership.

Answer: According to Section 4 of Indian Partnership Act 1932, “Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all”.

Question. A & B are two working partners whereas B is sleeping partner in the firm. B wants to inspect books of Accounts but A denies. What shall be done?

Answer: A is wrong, he cannot deny as B holds the right to inspect the accounts.

Question. Debit balance of Partners Current A/Cs is shown on which side of the balance sheet?

Answer: Assets side.

Question. What do you understand by Sacrificing Ratio?

Answer:_Sacrificing ratio is the ratio in which the partner or partners have agreed to sacrifice their share of profit in favour of one or more partners of the firm. Sacrificing ratio of each partner is calculated as follows: Sacrificing Ratio = Old Ratio – New Ratio

Question. How will you calculate interest on drawings when date of withdrawal is not given?

Answer: It will be calculated on the average basis of 6 months.

Question. In which account interest on partners loan is debited and why?

Answer: It is debited to Profit and Loss Account because it is a charge against theprofit

Question. Name the Act under which partnership is governed?

Answer: Partnership Act, 1932.

Question. What do you understand by Sacrificing Partners?

Answer:_The partners whose share stand decreased as a result of change in profit-sharing ratio are known as Sacrificing Partners. Sacrificing ratio shows the sacrifice of share of each sacrificing partner.

Question. Why is it preferable to have a written agreement between the partners?

Answer: To avoid all kinds of misunderstanding and disputes among the partners.

Question. Which Act of the Parliament specified the number of partners in Partnership?

Answer: Section 464 of Companies Act, 2013

Question. What share of profits would a “sleeping partner” who has contributed 75% of the total Capital get in the absence of Partnership Deed?

Answer: In the absence of Partnership Deed, a sleeping partner will get equal share of profits.

Question. Give the journal entry of P & L credit balance.

Answer: Profit and Loss A/c Dr

To Profit and Loss Appropriation A/c.

Question. What share of profits would a “sleeping partner” who has contributed 75% of the total Capital get in the absence of Partnership Deed?

Answer: In the absence of Partnership Deed, a sleeping partner will get equal share of profits.

Question. Anna and Bobby were partners sharing profits and losses in the ratio of 5 : 3. On 1st April 2014, their capital accounts showed balances of Rs 3,00,000 and Rs 2,00,000 respectively. Calculate the amount of profit to be distributed between the partners if the partnership deed provided for interest on capital @ 10% per annum and the firm earned a profit of Rs 45,000 for the year ended 31st March 2015.

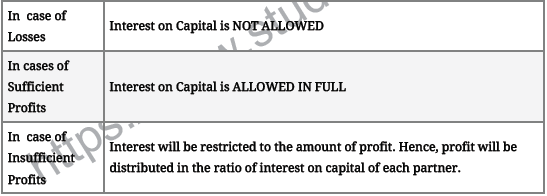

Answer:_No profit will be distributed as the amount of profit (i e., Rs 45,000) is not sufficient to pay the interest on capital (Rs 50,000),so Interest on capital i.e. Rs.45,000, to be provided in the interest ratio of the partners.

Question. What is the status of partnership firm from an accounting viewpoint?

Answer: From the accounting view point, Partnership is a separate business entity from the partners.

Question. Can a Partner be exempted from sharing the losses in a firm? If yes, under what circumstances?

Answer: Yes, if Partnership Deed provides so.

Question. What are the circumstances under which the balance of the ‘Fixed capitals Accounts’ may change?

Answer: i) Additional capital Introduced. ii) Capital Withdrawn.

Question. Why is that the Fixed Capital Account of a partner does not show “Debit Balance” in spite of regular and Consistent losses year after year?

Answer: When the capitals are fixed, the Capital Account of a partner will never show debit balance since, all transactions between the firm and the partner are recorded in Current Account.

Question. Can a Partner be exempted from sharing the losses in a firm? If yes, under what circumstances?

Answer: Yes, if Partnership Deed provides so.

Question. When fluctuating capital method is used, which of the following items are shown in debit side of partners’ capital account?

(a) Opening debit balance of capital account

(b) Drawings

(c) Interest on drawings

(d) All of these

Answer: d

Question. The capital balance of a partner at the end of the year (after adjusting for his drawings ₹ 3,500 and his share in the profit ₹ 2,300) is ₹ 12,000. Interest on capital is payable to him at 5% per annum. What will be the amount of interest on capital?

(a) ₹ 660

(b) ₹ 600

(c) ₹ 540

(d) None of these

Answer: a

Question. Aman and Vimal are partners in a firm. Aman says that goodwill is an asset so it has a realisable value. Vimal says that goodwill is an intangible asset, so it has no realisable value. Solve the issue.

(a) Aman is correct. Goodwill is asset, so it has realisable value.

(b) Vimal is correct. Goodwill is intangible asset, so it has no realisable value.

(c) Goodwill is an intangible asset, it may have some realisable value or it can be nil.

(d) Goodwill is a loss, it has negative value.

Answer: c

Question. If firm gives guarantee to a partner then who will sacrifice for this guarantee?

(a) All partners equally

(b) Only that partner who has maximum profit

(c) All partners in profit or loss sharing ratio

(d) All of the above

Answer: c

Question. Loan has been given by wife of a partner to the firm. Now partner wants interest @ 6% per annum as per Partnership Act, 1932 while partnership deed is silent. Solve this issue.

(a) Provide 6% per annum interest as Partnership Act says

(b) Provision of interest on loan @ 6% per annum of the Partnership Act does not apply

(c) Provide 10% interest to solve the issue

(d) None of the above

Answer: b

Question. A and B were partners in a firm. They share their profits in the ratio of 2:1. A withdraws an amount of ₹ 2,000 on 1st July, 2021. Journalise it.

(a) Profit and Loss Appropriation A/c Dr 2,000

To A’s Capital A/c 2,000

(b) A’s Capital A/c Dr 2,000

To Profit and Loss A/c 2,000

(c) A’s Drawings A/c Dr 2,000

To Cash/Bank A/c 2,000

(d) A’s Capital A/c Dr 2,000

To A’s Drawings A/c 2,000

Answer: c

Question. Asha and Bipasha are partners in a firm. They share profits in the ratio of 1:1. In this year, they suffered a loss. They maintain capital accounts under fluctuating account method. Pass journal entry to transfer the loss to the capital accounts of Asha and Bipasha.

(a) Profit and Loss Appropriation A/c Dr

To Asha’s Capital A/c

To Bipasha’s Capital A/c

(b) Asha’s Capital A/c Dr

To Bipasha’s Capital A/c

(c) Asha’s Capital A/c Dr

Bipasha’s Capital A/c Dr

To Profit and Loss A/c

(d) None of the above

Answer: c

CASE STUDY BASED QUESTIONS :

Amit and Mahesh were partners in a fast food corner sharing profits and losses in ratio 3:2. They sold fast food items across the counter and did home delivery too. Their initial fixed capital contribution was ₹ 1,20,000 and ₹ 80,000 respectively.

At the end of first year, their profit was ₹ 1,20,000 before allowing the remuneration of ₹ 3,000 per quarter to Amit and ₹ 2,000 per half year to Mahesh. Such a promising performance for first year was encouraging, therefore, they decided to expand the area of operations.

For this purpose, they needed a delivery van, a few scotties and an additional person to support. Six months into the accounting year, they decided to admit Sundaram as a new partner and offered him 20% as a share of profits along with monthly remuneration of ₹ 2,500.

Sundaram was asked to introduce ₹ 1,30,000 for capital and ₹ 70,000 for premium for goodwill. Besides this, Sundaram was required to provide ₹ 1,00,000 as loan for two years. Sundaram readily accepted the offer. The terms of the offer were duly executed and he was admitted as a partner.

Question. Remuneration will be transferred to …………… of Amit and Mahesh at the end of the accounting period.

(a) Capital account

(b) Loan account

(c) Current account

(d) None of these

Answer: c

Question. Upon the admission of Sundaram, the sacrifice for providing his share of profits would be done

(a) by Amit only

(b) by Mahesh only

(c) by Amit and Mahesh equally

(d) by Amit and Mahesh in the ratio of 3:2

Answer: d

PRACTICAL QUESTIONS :

Question. Raju and Jai commenced business in partnership on April 1, 2019. No partnership agreement was made whether oral or written. They contributed ₹4,00,000 and ₹1,00,000 respectively as capitals. In addtion, Raju advanced ₹2,00,000 as loan to the firm on October 1, 2019. Raju met with an accident on July 1, 2019 and could not attend the business up to september 30, 2019. The profit for the year ended March 31, 2020 amounted to ₹50,000 before charging interest on Raju’s loan. Disputes have arisen between them on sharing the profits of the firm. Raju Claims:

(i) He should be given interest at 10% p.a. on capital and so also on loan.

(ii) Profit should be distributed in the proportion of capitals. Jai Claims: (i) Net profit should be shared equally. (ii) He should be allowed remuneration of ₹1,000 p.m. during the period of Raju’s illness.

(iii) Interest on capital and loan should be given @ 6% p.a.

State the correct position on each issue as per the provisions of the Partnership Act, 1932.

Solution:

Settlement of disputes as per the provisions of the Partnership Act, 1932:

(i) No interest is payable on Partners’ capitals in the absence of partnership agreement.

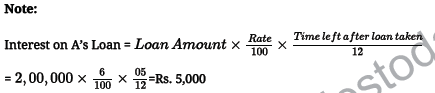

(ii) Interest on Raju’s loan is payable @6% p.a., i.e., 2,00,000 × 6% × 6/12 = `6,000

(iii) Jai’s claim for remuneration @ `1,000 p.m. is not valid since no remuneration is payable when there is no partnership agreement.

(iv) Profits should be distributed equally among the partners irrespective of their capital contributions.

Net profit after charging interest on Raju’s loan = 50,000 – 6,000 = `44,000, which will be distributed equally between Raju and Jai, i.e. RS `22,000 each.

According to Section -4 of the Indian Partnership Act, 1932:

Q.1. A and B are partners. A gave a loan of ₹ 8,000 to the firm on 1.4.12. The Partnership Deed is silent upon interest on loan. How much interest on loan will be provided to him?

Accounting year is calendar year

(a) ₹ 480

(b) ₹360

(c) ₹ 200

(d) none of the above

Answer : B

Q.2. On 31.3.12, after the close of books of accounts, the capital a/c of Ram, Shyam & Mohan showed a balance of ₹24,000, ₹ 18,000 and ₹ 12,000 respectively. The profits for the year ended 31.3.12 amounted to Rs. 36,000 and the partner’s drawings had been Ram-Rs. 3,600, Shyam-₹ 4,500 and Mohan-₹ 2,700. The Profit Sharing Ratio was 3:2:1. How much will be the opening capital?

(a) Ram-₹15,600, Shyam-₹10,500, Mohan-₹ 8,700

(b) Ram-₹15,650, Shyam-₹ 10,550, Mohan-₹ 2,750

(c) Ram-₹15,600, Shyam-₹10,500, Mohan-₹ 2,800

(d) None of the above

Answer : A

Q.3. If Partnership Deed is silent, how much salary will be provided to partners?

(a) Proportionate to capital contribution

(b) Proportionate to time spent

(c) Nil

(d) none of the above

Answer : C

Q.4. A, B and C are partners in a firm. They decided to share profits upto ₹ 10,000 in the ratio of 50%, 30% and 20% respectively. Above this amount, profits are shared equally. If the profits of the firm for the year was ₹25,600. Distribute the profits.

(a) A-₹10,000, B-₹8,500, C-₹7,500

(b) A-₹10,200, B-₹8,100, C-₹7,300

(c) A-₹10,200, B-₹8,200, C-₹7,200

(d) A-₹10,200, B-₹8,200, C-₹.7,500

Answer : C

Q.5. A, B and C are partners sharing profits and losses in the ratio of 2:1:2. Their capitals were ₹3,00,000, ₹1,00,000 and ₹2,00,000 respectively. Interest on capital for the year 2011 was credited to them @ 9% p.a. instead of 10% p.a. The profits for the year before charging interest was ₹ 2,50,000. Which of the following journal entry is correct?

(a) A’s Capital A/c Dr. 200

C’s Capital A/c Dr. 400

To B’s Capital A/c 600

(b) B’s Capital A/c Dr. 200

C’s Capital A/c Dr. 400

To A’s Capital A/c 600

(c) B’s Capital A/c Dr. 200

A’s Capital A/c Dr. 400

To C’s Capital A/c 600

(d) None of the above

Answer : B

Q.6. X and Y are partners. X drew regularly ₹400 at the beginning of every month for six months ending 30.6.12. Calculate interest on drawings @ 5% p.a.?

(a) ₹ 40

(b) ₹ 38

(c) ₹ 29

(d) ₹35

Answer : D

Free study material for Accountancy

CBSE Accountancy Class 12 Part 1 Chapter 1 Accounting for Partnership Basic Concepts Worksheet

Students can use the practice questions and answers provided above for Part 1 Chapter 1 Accounting for Partnership Basic Concepts to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 12. We suggest that Class 12 students solve these questions daily for a strong foundation in Accountancy.

Part 1 Chapter 1 Accounting for Partnership Basic Concepts Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 12 Accountancy to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Accountancy to cover every important topic in the chapter.

Class 12 Exam Preparation Strategy

Regular practice of this Class 12 Accountancy study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in Part 1 Chapter 1 Accounting for Partnership Basic Concepts difficult then you can refer to our NCERT solutions for Class 12 Accountancy. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

FAQs

You can download the latest chapter-wise printable worksheets for Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 12 Accountancy worksheets for Part 1 Chapter 1 Accounting for Partnership Basic Concepts focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 12 Accountancy Part 1 Chapter 1 Accounting for Partnership Basic Concepts to help students verify their answers instantly.

Yes, our Class 12 Accountancy test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Part 1 Chapter 1 Accounting for Partnership Basic Concepts, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.