Read and download the CBSE Class 12 Economics Revenue Supply And Its Elasticity Worksheet in PDF format. We have provided exhaustive and printable Class 12 Economics worksheets for Revenue Supply And Its Elasticity, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 12 Economics Revenue Supply And Its Elasticity

Students of Class 12 should use this Economics practice paper to check their understanding of Revenue Supply And Its Elasticity as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 12 Economics Revenue Supply And Its Elasticity Worksheet with Answers

Question. _____refers to the quantity of goods or services that Producers are willing and able to offer to themarket at various prices during a period of time.

(a) Demand

(b) Supply

(c) Stock

(d) Sales

Answer: B

Question. Producing Firms are guided by —

(a) Service Motive

(b) Profit Motive

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: B

Question. Other things being equal, the supply quantity of a product is related to price of related goods.

(a) Directly

(b) Inversely

(c) Proportionally

(d) Not at all

Answer: B

Question. Contraction of Supply is the result of —

(a) Decrease in the number of Producers

(b) Decrease in the price of the product concerned

(c) Increase in the prices of other goods

(d) Decrease in the Outlay of Sellers

Answer: B

Question. Which of the following is the only determinant that the Law of Supply takes into account?

(a) Technology

(b) Price of the Product

(c) Qual ity of the Product

(d) Purchasing Power of Sel lers

Answer: B

Question. Other things being equal, if the price of the commodity is higher, quantities thereof will be supplied to the market.

(a) Equal

(b) Lower

(c) Greater

(d) Zero

Answer: C

Question. _ is the total volume of the commodity which can be brought into the market for sale at a short notice.

(a) Demand

(b) Supply

(c) Stock

(d) Sales

Answer: C

Question. ___ refers to the quantity which is actually brought in the market.

(a) Demand

(b) Supply

(c) Stock

(d) Sales

Answer: B

Question. Supply is different from Stock. This statement is

(a) True

(b) False

(c) Partially True

(d) None of the above

Answer: A

Question. Change in Quantity Supplied causes —

(a) a movement on the same Supply Curve

(b) shift of the Supply Curve

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: A

Question. Which of the following factors is not a determinant of Supply?

(a) Price of the Commodity

(b) Prices of Related Commodities

(c) Prices of Water and Salt

(d) Prices of Factors of Production

Answer: C

Question. Stock is potential supply.

(a) True

(b) False

(c) Partially True

(d) None of the above

Answer: A

Question. Stock refers to quantity _ into the market, whereas Supply refers to quantity __ into the market.

(a) Actually brought, actually brought

(b) Can be brought, actually brought

(c) Can be brought, actually brought

(d) Can be brought, can be brought

Answer: B

Question. When lower quantities are supplied, due to changes in factors other than price, it is called

(a) Contraction of Supply

(b) Expansion of Supply

(c) Decrease in Supply

(d) Increase in Supply

Answer: C

Question. Prices of Related Commodities are not a determinant of supply of a particular commodity. This statement is —

(a) True

(b) False

(c) Partially True

(d) None of the above

Answer: B

Question. The meaning of time element in economics is

(a) Calendar time

(b) Clock time

(c) Operational time which supply adjusts with the market demand

(d) None of these

Answer: C

Question. Supply refers to ________

(a) Stock of goods available for sale

(b) Stock of goods

(c) Quantity supplied at a various price during a period of time

(d) Actual production of the goods

Answer: C

Question. What would be the shape of the Supply Curve of the toys, if a Seller offers to sell any number of toys as 100?

(a) Vertical

(b) Downward sloping

(c) Horizontal

(d) Upward sloping

Answer: C

Question. Other things being equal, if the Cost of Production of a commodity is higher, quantities thereof will be supplied to the market.

(a) Equal

(b) Lower

(c) Greater

(d) Zero

Answer: B

Question. Supply of a Commodity is a —

(a) Stock Concept

(b) Flow Concept

(c) Both Stock and Flow Concept.

(d) None of these.

Answer: B

Question. Which of the following is the determinant in the Law of Supply?

(a) Technology

(b) Price of related goods

(c) Price of the product

(d) None of these

Answer: C

Question. Generally, Supply of a Product X will be if the prices of goods other than X increase.

(a) Equal

(b) Lower

(c) Greater

(d) Zero

Answer: B

Question. Generally, Supply of a Product X will be ___ if the prices of goods other than X decrease.

(a) Eq ual

(b) Lower

(c) Greater

(d) Zero

Answer: C

Question. When higher quantities are supplied, due to changes in factors other than price, it is called

(a) Contraction of Supply

(b) Expansion of Supply

(c) Decrease in Supply

(d) Increase in Supply

Answer: D

Question. Period in which supply cannot be increased is called

(a) Market Period

(b) Short Run

(c) Long Run

(d) None of these

Answer: A

Question. Supply can be referred as —

(a) Those goods which Firms offers for sale

(b) Amount of goods, Firms sells in the market

(c) Amount of goods all people want

(d) None of the above

Answer: A

Question. If there is an decrease in the Prices of Factors of Production, Cost of Production of that product will —

(a) Inc reas e

(b) Decrease

(c) Remain Constant

(d) Become Zero

Answer: B

Question. When more units of the product are supplied at a higher price, it is called —

(a) Contraction of Supply

(b) Increase in Supply

(c) Change in Supply

(d) Expansion of Supply

Answer: D

Question. Other things being equal, if the Cost of Production of a commodity is lower, quantities thereof will be supplied to the market.

(a) Equal

(b) Lower

(c) Greater

(d) Zero

Answer: C

Question. Inventions and Innovations lead to —

(a) Lower Cost of Production in existing products

(b) Production of more or better goods

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: C

Question. Other things being equal, if the State of Technology in re lat ion to a commodi ty inc reas es, quantities thereof will be supplied to the market.

(a) Equal

(b) Lower

(c) Greater

(d) Zero

Answer: C

Question. Supply refers to the quantity of goods or services, that are willing and able to offer to the market at various prices during a period of time.

(a) Producers

(b) Consumers

(c) Economists

(d) Accountants

Answer: A

Question. When there is a movement on the Supply Curve, we are referring to —

(a) Change in Supply

(b) Change in Quantity Supplied

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: B

Question. Generally, higher the prices of products, higher the

(a) Profits of Producing Firms

(b) Satisfaction Level of Consumers

(c) Tax Rates

(d) All of the above

Answer: A

Question. Supply refers to what Firms offer for sale, and not necessarily to what they succeed in selling. This statement is —

(a) True

(b) False

(c) Partially True

(d) None of the above

Answer: A

Question. Other things being equal, the supply quantity of a product is _____ related to the Cost of Production of that product.

(a) Directly

(b) Inversely

(c) Proportionally

(d) Not at all

Answer: A

Question. When there is a change in supply —

(a) Supply Curve shifts inward or outward

(b) There is a upward / downward movement on the same Supply Curve

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: A

Question. Generally, if there are incentives like Subsidies which reduce the cost of production, the supply quantity will —

(a) Increase

(b) Decreas e

(c) Remain Constant

(d) Become Zero

Answer: A

Question. When there is a movement of the Supply Curve, we are referring to —

(a) Change in Supply

(b) Change in Quantity Supplied

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: A

Question. Supply of a Product decreases when the prices of other related goods increase. This is because

(a) Customers start demanding more of other goods

(b) Those goods become relatively more profitable to the Firm to produce and sell

(c) Customers preferences and tastes will change

(d) Producing Firms' profit motive changes

Answer: B

Question. In case of failure of rains, floods, fires, etc. the supply of agricultural commodities will —

(a) Increase

(b) Decrease

(c) Remain Constant

(d) Become Zero

Answer: B

Question. In case of better rainfall, improvement in irrigation, improved seeds, etc. the supply of agricultural commodities will —

(a) Increase

(b) Decreas e

(c) Remain Constant

(d) Become Zero

Answer: A

Question. The Supply of a product refers to —

(a) Actual production of the product

(b) Total existing stock of the product

(c) Stock available for sale

(d) Amount of the product offered for sale at a particular price per unit of time

Answer: D

Question. As per Law of Supply, other things being equal, if the Price of a Commodity increases, its Supply Quantity will

(a) Increase

(b) Decrease

(c) Remain Constant

(d) Become Zero

Answer: A

Question. As per Law of Supply, other things being equal, if the Price of a Commodity decreases, its Supply Quantity will

(a) Increa se

(b) Decrease

(c) Remain Constant

(d) Become Zero

Answer: B

Question. To constitute Supply, the Producing Firms must have

(a) Ability, i.e. productive capacity

(b) Willingness, i.e. ready to supply

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: C

Question. Which of the following factors is not a determinant of Supply?

(a) Government's industrial and foreign policies

(b) Market Structure

(c) State of Technology

(d) Income Levels of Consumers

Answer: C

Question. Inventions and Innovations lead to —

(a) Increase in supply quantity of new products

(b) Reduction in the supply quantity of products that are displaced

(c) Both (a) and (b)

(d) Nei ther (a) nor (b)

Answer: C

Question. As per Law of Supply, other things being equal, there is a ____ between Price and Quantity Supplied.

(a) Direct relationship

(b) Inverse relat ionship

(c) Proportional relationship

(d) No relationship

Answer: A

Question. _____ shows the quantity of products a producer or seller wishes to sell at a given price level.

(a) Average Product Curve

(b) Supply Curve

(c) Marginal Product Curve

(d) Total Product Curve

Answer: B

Question. Generally, the Supply Curve —

(a) Slopes downwards from left to right

(b) Slopes upwards from right to left

(c) Slopes upwards from left to right

(d) Nothing can be said

Answer: C

Question. Generally, the Supply Curve —

(a) Positively sloped

(b) Negatively sloped

(c) Zero—sloped

(d) Nothing can be said

Answer: A

Question. Typically, the Supply Curve —

(a) Slopes upward

(b) Slopes downward

(c) Is horizontally straight

(d) Is vertically straight

Answer: A

Question. The Supply Curve —

(a) Is always a straight line

(b) Is always a curve

(c) Sometimes a straight line, sometimes a curve

(d) Nothing can be said

Answer: C

Question. Supply refers to theby Producing Firms.

(a) Quantities offered for sale

(b) Prices offered

(c) Sales achieved

(d) Profits earned

Answer: A

Question. Generally, the Supply Curve —

(a) Is negatively sloped.

(b) Is positively sloped.

(c) Has both positive and negative slopes

(d) Does not have a slope at all

Answer: B

Question. If the Demand of a commodity is perfectly inelastic, an increase in Supply will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Increase in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Increase in Equi l ibrium Price, Equi l ibrium Quantity remaining constant

Answer: D

Question. Other things being equal, as Supply increases, Quantity at the Equilibrium Price level —

(a) Increases

(b) Decreases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

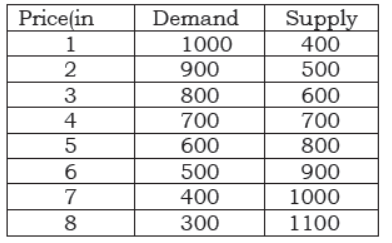

Question. In the table below, what will be Equilibrium Price?

(a) Z 2

(b) Z 3

(c) Z 4

(d) 7 5

Answer: C

Question. Other things being equal, as Demand increases, Quantity at the Equilibrium Price level —

(a) increases

(b) decreases

(c) does not change at all

(d) cannot be commented upon.

Answer: A

Question. Other things being equal, as Demand increases

(a) Equilibrium Price and Quantity both increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price increases and Quantity decreases.

(d) Equilibrium Price decreases and Quantity increases.

Answer: A

Question. Other things being equal, as Demand decreases, Equilibrium Price —

(a) decreases

(b) increases

(c) does not change at all

(d) cannot be commented upon

Answer: A

Question. Other things being equal, as Demand decreases, Quantity at the Equilibrium Price level —

(a) increases

(b) decreases

(c) does not change at all

(d) cannot be commented upon.

Answer: B

Question. Other things being equal, as Demand decreases —

(a) Equilibrium Price and Quantity bOth increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price increases and Quantity decreases.

(d) Equilibrium Price decreases and Quantity increases.

Answer: B

Question. If the Demand of a commodity is perfectly elastic, a decrease in Supply will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Decrease in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Decrease in Equilibrium Price, Equilibrium Quantity remaining constant

Answer: C

Question. Other things being equal, as Supply increases —

(a) Equilibrium Price and Quantity both increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price increases and Quantity decreases.

(d) Equilibrium Price decreases and Quantity increases.

Answer: D

Question. Market Forces refer to —

(a) Demand

(b) Supply

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: C

Question. Other things being equal, as Supply decreases, Quantity at the Equilibrium Price level —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

Question. If the Supply of a commodity is perfectly elastic, a decrease in Demand will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Decrease in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Decrease in Equilibrium Price, Equilibrium Quantity remaining constant

Answer: C

Question. If decrease in demand is greater than decrease in supply, then the Quantity at the Equilibrium Price level —

(a) Increases

(b) Decreases

(c) Does not change at all

( d) Cannot be commented upon.

Answer: B

Question. Other things being equal, as Supply decreases Equilibrium Price and Quantity both increase.

(a) Equilibrium Price and Quantity both decrease.

(b) Equilibrium Price increases and Quantity decreases.

(c) Equilibrium Price decreases and Quantity increases.

(d) None of the above

Answer: B

Question. Equilibrium price is where

(a) Market supply and market demand are equal

(b) Firm supply ad market demand are equal

(c) Firm demand and market supply are equal

(d) None of these

Answer: A

Question. Generally, the Demand Curve —

(a) Is parallel to X Axis

(b) Is parallel to Y Axis

(c) Slopes upward from left to right

(d) Slopes downward from left to right

Answer: D

Question. If increase in demand is greater than the increase in supply, then Quantity at the Equilibrium Price level —

(a) Increases

(b) Decreases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

Question. If increase in demand is greater than the increase in supply, then —

(a) Equilibrium Priced Quantity both increase.

(b) Equilibrium Price a annd Quantity both decrease.

(c) Equilibrium Price increases and Quantity decreases.

(d) Equilibrium Price decreases and Quantity increases.

Answer: A

Question. P Q.D. Q.S. 1 500 200 2 450 250 3 400 300 4 350 350 5 300 400 6 250 450 7 200 550 8 150 600 Whatis equilibrium price

(a) 1

(b) 2

(c) 3

(d) 4

Answer: D

Question. If the Supply of a commodity is perfectly elastic, an increase in Demand will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Increase in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Increase in Equilibrium Price, Equilibrium Quantity remaining constant

Answer: C

Question. If decrease in demand is greater than the decrease in supply, then —

(a) Equilibrium Price and Quantity both increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price increases and Quantity decreases.

(d) Equilibrium Price decreases and Quantity increases.

Answer: B

Question. Which of these refer to "Market Forces"?

(a) Price and Output

(b) Demand and Supply

(c) Cost and Revenue

(d) All of the above

Answer: B

Question. If increase in demand is equal to the increase in supply, then the Quantity at the Equilibrium Price level —

(a) Increases

(b) Decreases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

Question. Generally, the Demand Curve —

(a) Is positively sloped.

(b) Is negatively sloped.

(c) Has both positive and negative slopes

(d) Does not have a slope at all

Answer: B

Question. If increase in demand is equal to the increase in supply, then —

(a) Equilibrium Price and Quantity both increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price remains the same but Quantity increases.

(d) Equilibrium Price remains the same but Quantity increases.

Answer: C

Question. Other things being equal, as Demand increases, Equilibrium Price —

(a) decreases

(b) increases

(c) does not change at all

(d) cannot be commented upon.

Answer: B

Question. If decrease in demand is greater than the decrease in supply, then the Equilibrium Price —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

Question. If decrease in demand is equal to the decrease in supply, then —

(a) Equilibrium Price and Quantity both increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price remains the same but Quantity increases.

(d) Equilibrium Price remains the same but Quantity increases.

Answer: D

Question. If increase in demand is less than the increase in supply, then the Equilibrium Price —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

Question. Generally, the Supply Curve —

(a) Is parallel to X Axis

(b) Is parallel to Y Axis

(c) Slopes upward from left to right

(d) Slopes downward from left to right

Answer: C

Question. If increase in demand is greater than the increase in supply, then the Equilibrium Price —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: B

Question. If increase in demand is less than the increase in supply, then the Quantity at the Equilibrium Price level —

(a) Increases

(b) Decreases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

Question. With a given Supply Curve, a decrease in Demand causes —

(a) An overall decrease in price but an increase in equilibrium quantity

(b) An overall increase in price but a decrease in equilibrium quantity

(c) An overall decrease in price and a decrease in equilibrium quantity

(d) No change in overall price but a reduction in equilibrium quantity

Answer: C

Question. If decrease in demand is equal to the decrease in supply, then the Equilibrium Price —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: C

Question. Which of the following situation does not lead to an increase in Equilibrium Price?

(a) An increase in demand, without a change in supply.

(b) A decrease in supply accompanied by an increase in demand.

(c) A decrease in supply without a change in demand.

(d) An increase in supply accompanied by a decrease in demand.

Answer: D

Question. Demand & Supply interact in determining—

(a) Price and Output

(b) Cost and Revenue

(c) Both (a) and (b)

(d) Neither (a) nor (b)

Answer: A

Question. If decrease in demand is less than the decrease in supply, then the Equilibrium Price —

(a) decreases

(b) increases

(c) does not change at all

(d) cannot be commented upon.

Answer: B

Question. If the Supply of a commodity is perfectly inelastic, an increase in Demand will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Increase in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Increase in Equilibrium Price, Equilibrium Quantity remaining constant

Answer: D

Question. If the Supply of a commodity is perfectly inelastic, a decrease in Demand will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Decrease in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Decrease in Equilibrium Price, Equilibrium Quantity remaining constant

Answer: D

Question. If the Demand of a commodity is perfectly elastic, an increase in Supply will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Increase in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Increase in Equi l ibrium Price, Equi l ibrium Quantity remaining constant

Answer: C

Question. Other things being equal, as Supply decreases, Equilibrium Price —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: B

Question. Other things being equal, as Supply increases, Equilibrium Price —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: A

Question. If decrease in demand is less than the decrease in supply, then the Quantity at the Equilibrium Price level —

(a) Increases

(b) Decreases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: B

Question. If the Demand of a commodity is perfectly inelastic, a decrease in Supply will result in —

(a) Decrease in both Price and Quanti ty at equilibrium

(b) Increase in both Price and Quanti ty at equilibrium

(c) Decrease in Equilibrium Quantity, Equilibrium Price remaining constant

(d) Decrease in Equilibrium Price, Equilibrium Quantity remaining constant

Answer: D

Question. If decrease in demand is equal to the decrease in supply, then the Quantity at the Equilibrium Price level —

(a) increases

(b) decreases

(c) does not change at all

(d) cannot be commented upon.

Answer: B

Question. If decrease in demand is less than the decrease in supply, then —

(a) Equilibrium Price and Quantity both increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price increases and Quantity decreases.

(d) Equilibrium Price decreases and Quantity increases.

Answer: C

Question. If a fisherman must sell all of his daily catch before it spoils for whatever price he is offered once the fish are caught. The Fisherman's Price Elasticity of Supply for fresh fish is —

(a) Zero

(b) Infinity

(c) One

(d) Cannot be determined

Answer: A

Question. If increase in demand is equal to the increase in supply, then the Equilibrium Price —

(a) Decreases

(b) Increases

(c) Does not change at all

(d) Cannot be commented upon.

Answer: C

Question. If increase in demand is less than the increase in supply, then —

(a) Equilibrium Price and Quantity both increase.

(b) Equilibrium Price and Quantity both decrease.

(c) Equilibrium Price increases and Quantity decreases.

(d) Equilibrium Price decreases and Quantity increases.

Answer: D

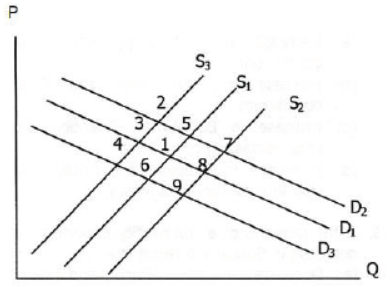

The Below 7 Questions are based on the demand and supply diagrams below. S1 and D1 are the original demand and supply curves. D2, D3, S2 and S3 are possible new demand and supply curves. Starting from initial equilibrium point (1) what point on the graph is most likely to result from each change?

Question. Assume that consumers expect the prices on new cars to significantly increase next year. What point in Figure is most likely to be the new equilibrium price and quantity?

(a) Point 6

(b) Po int 5

(c) Po int 3

(d) Po int 8

Answer: B

Question. Assume X is a normal good. Holding everything else constant, assume that income rises and the price of a factor of production also increases. What point in Figure 1 is most likely to be the new equilibrium price and quantity?

(a) Po int 9

(b) Po int 5

(c) Po int 3

(d) Point 2.

Answer: D

Question. When a market is in equilibrium:

(a) No shortages exist.

(b) Quantity demanded equals quantity supplied.

(c) A price is established that clears the market.

(d) All of the above are correct.

Answer: D

Question. The market of computers is not in equilibrium, then which of the following statements is definitely true?

(a) The prices of computer will rise

(b) The prices of computer will fall

(c) The prices of computers will change, but not enough information is given to determine the direction of the change.

(d) None of the above.

Answer: C

Question. We are analyzing the market for good Z. The price of a complement good, good Y, declines. At the same time, there is a technological advance in the production of good Z. What point Figure 1 is most likely to be the new equilibrium price and quantity?

(a) Point 4.

(b) Po int 5

(c) Po int 8

(d) Po int 7

Answer: C

Question. What combinations of changes would most likely decrease the equilibrium quantity?

(a) When supply increases and demand decreases.

(b) When demand increases and supply decreases

(c) When supply increases and demand increases.

(d) When demand decreases and supply decreases.

Answer: D

Question. Heavy rains in Maharashatra during 2005 and 2006 caused havoc with the rice crop. What point in Figure 1 is most likely to be the new equilibrium price and quantity?

(a) Po int 6

(b) Point 3

(c) Point 7

(d) Point 8

Answer: B

Free study material for Economics

CBSE Economics Class 12 Revenue Supply And Its Elasticity Worksheet

Students can use the practice questions and answers provided above for Revenue Supply And Its Elasticity to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 12. We suggest that Class 12 students solve these questions daily for a strong foundation in Economics.

Revenue Supply And Its Elasticity Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 12 Economics to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Economics to cover every important topic in the chapter.

Class 12 Exam Preparation Strategy

Regular practice of this Class 12 Economics study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in Revenue Supply And Its Elasticity difficult then you can refer to our NCERT solutions for Class 12 Economics. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

FAQs

You can download the latest chapter-wise printable worksheets for Class 12 Economics Revenue Supply And Its Elasticity for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 12 Economics worksheets for Revenue Supply And Its Elasticity focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 12 Economics Revenue Supply And Its Elasticity to help students verify their answers instantly.

Yes, our Class 12 Economics test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Revenue Supply And Its Elasticity, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.