Access the latest CBSE Class 12 Accountancy Accounting For Share Capital Worksheet. We have provided free printable Class 12 Accountancy worksheets in PDF format, specifically designed for Part 2 Chapter 1 Accounting for Share Capital. These practice sets are prepared by expert teachers following the 2025-26 syllabus and exam patterns issued by CBSE, NCERT, and KVS.

Part 2 Chapter 1 Accounting for Share Capital Accountancy Practice Worksheet for Class 12

Students should use these Class 12 Accountancy chapter-wise worksheets for daily practice to improve their conceptual understanding. This detailed test papers include important questions and solutions for Part 2 Chapter 1 Accounting for Share Capital, to help you prepare for school tests and final examination. Regular practice of these Class 12 Accountancy questions will help improve your problem-solving speed and exam accuracy for the 2026 session.

Download Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital Worksheet PDF

Question. Name the head of Capital Clause of Memorandum of Association of a company in which maximum amount of share capital mentioned is called .

(a) Reserve Capital

(b) Subscribed Capital

(c) Authorised Capital

(d) Issued Capital

Answer. C

Question. A shareholder allotted to whom 9,000 shares of ₹ 10 per share failed to pay first & final of ₹ 2 per share. ₹ 18,000 to be recorded in the books of company with

(a) Dr. to Calls-in Arrears A/c

(b) Dr. to Share Forfeiture

(c) Cr. to Calls-in Arrears A/c

(d) Cr. to Share Forfeiture A/c

Answer. A

Question. Arrange the following in proper sequence as types of “Share Capital”

a) Paid up capital

b) Issued capital

c) Subscribed capital

d) Authorised capital

a) a) ,c) , d) , b)

b) d), c) , b), a)

c) d), b), c),a)

Answer. C

Question. Shobha Limited was formed with share capital of Rs. 50,00,000 divided into 50,000 shares of Rs.100 each. 8,000 shares were issued to the vendor as fully paid for purchase consideration of a Machinery acquired. 30,000 shares were allotted in payment of cash on which Rs.70 per share was called and paid. State the amount of subscribed capital:

A) Rs. 50,00,000

B) Rs. 30,50,000

C) Rs. 29,00,000

D) Rs. 20,00,000

Answer. C

Question. Star Ltd forfeited 1,000 shares of Rs.10 each (which were issued at par )of Jeevan, a share holder of the company, for non payment of allotment money of Rs.4 per share. The called up value per share was Rs.7. On forfeiture, the amount debited to share capital:

a) Rs.3,000

b) Rs.7,000

c) Rs.4,000

d) Rs.10,000

Answer. B

Question. The allowed amount of discount on re-issue of shares will be

(a) 10% of issue price

(b) Up to the amount of forfeited money

(c) Could not issue at discount

(d) None of these

Answer. B

Question. Once, forfeited shares reissued, balance of share forfeiture money will be transferred to:

(a) General Reserve

(b) Capital Reserve

(c) Reserve Capital

(d) Securities Premium Reserve

Answer. B

Question. 12,000 shares of ₹ 100 each forfeited due to non-payment of allotment of ₹ 40 per share and first & final call of ₹ 30 per share. Out of the forfeited shares, 9,000 shares were reissued at ₹ 80 per share fully paid. Which of the following amount of share forfeiture account will be transferred to Capital Reserve Account?

(a) 90,000

(b) 1,80,000

(c) 3,60,000

(d) 2,70,000

Answer. A

Question. Which of the following statements is/are true?

(i) Authorized Capital < Issued Capital (ii) Authorized Capital ≥ Issued Capital

(iii) Subscribed Capital ≤ Issued Capital (iv) Subscribed Capital > Issued Capital

(a) (i) only

(b) (i) and (iv) Both

(c) (ii) and (iii) Both

(d) (ii) only

Answer. C

Question. Name the head of Capital Clause of Memorandum of Association of a company in which the maximum amount of share capital mentioned is called .

(a) Reserve Capital

(b) Subscribed Capital

(c) Authorised Capital

(d) Issued Capital

Answer. C

Question. The part of uncalled capital, to be called only in the liquidation of a company is called:

(a) Un-reserved Capital

(b) Reserve Capital

(c) Capital Reserve

(d) Calls-in Arrears

Answer. B

Question. Manisha ltd. had been allotted for 600 shares by a Gokul Ltd on pro rata basis which had

issued two shares for every three applied. He had paid application money of ₹3 per share and could not pay allotment money of ₹5 per share. First and final call of ₹2 per share was not yet made by the company. His shares were forfeited. the following entry will be passed:

Equity Share Capital A/c Dr ₹X

To share Forfeited A/c ₹Y

To Calls in Arrear A/c ₹Z

Here X, Y and Z are:

(a) ₹ 6,000; ₹2,700; ₹3,000 respectively.

(b) ₹ 9,000; ₹2,700; ₹4,500 respectively.

(c) ₹ 4,800; ₹2,700; ₹2,100 respectively.

(d) ₹ 7,200; ₹2,700; ₹4,500 respectively.

Answer. C

Question. A shareholder allotted to whom 9,000 shares of ₹ 10 per share failed to pay first & final of ₹ 2 per share. ₹ 18,000 to be recorded in the books of company with

(a) Dr. to Calls-in Arrears A/c

(b) Dr. to Share Forfeiture A/c

(c) Cr. to Calls-in Arrears A/c

(d) Cr. to Share Forfeiture A/c

Answer. A

Question. Read the following statement carefully and give the answer for the questions :

Kokun Ltd is authorised to issue shares 5,00,000 of ₹ 100 each. Company raised the capital by issuing 2,00,000 shares through e-IPO. As per the decision of the Managing Board of Directors of the company, the company issued 75,000 shares to their parent company and 40,000 shares issued to existing employees of the company as per their choice and option at the below price than the market price.“Company issued 75,000 shares to their parent company” is an example of .

(a) Public Issue

(b) Private Placement

(c) ESOP

(d) Issue other than cash

Answer. B

Question. 40,000 shares issued to existing employees of the company as per their choice and option at the below price than the market price.” Is an example of

(a) Public Issue

(b) Private Placement

(c) ESOP

(d) Issue other than cash

Answer. C

Question. Vibhuti Ltd. forfeited 20 shares of ₹10 each, ₹8 called up, on which John had paid application and allotment money of ₹5 per share, of these, 15 shares were reissued to Parker as fully paid up for ₹6 per share. What is the balance in the share Forfeiture Account after the relevant amount has been transferred to Capital Reserve Account?

(a) ₹0

(b) ₹5

(c) ₹25

(d) ₹100

Answer. C

Question. Which one of the following is a permanent representative personal account of share-holders?

(a) Share Application A/c

(b) Share Allotment A/c

(c) Share Application & Allotment A/c

(d) Share Capital A/c

Answer. D

Question. Which of the following is a temporary representative personal account of shareholders?

(a) Share Application A/c

(b) Share Allotment A/c

(c) Share Application & Allotment A/c

(d) All of these

Answer. B

Question. XYZ Ltd took over business of Bizare ltd and paid for it by issue of 30,000, Equity Shares of ₹100 each at a par along with 6% Preference Shares of ₹1,00,00,000 at a premium of 5% and a cheque of ₹8,00,000.

What was the total agreed purchase consideration payable to Bizare ltd.

(a) ₹1,05,00,000.

(b) ₹1,43,00,000.

(c) ₹1,40,00,000.

(d) ₹1,35,00,000.

Answer. B

Question. A shareholder failed to pay share allotment money on 12,000 shares @ ₹ 30 per share. Which one of the following account will be taken into account?

(a) Debited to Share Capital A/c

(b) Debited to Calls-in Arrears A/c

(c) Credited to Calls-in Arrears A/c

(d) Credited to Share Capital A/c

Answer. B

Question. Received share application money towards application & allotment of shares will be credited to which of the following account?

(a) Share Application & Allotment A/c

(b) Share Application A/c

(c) Share Capital A/c

(d) None of these

Answer. C

Question. Ashok a shareholder of a company allotted shares to whom 12,000 of ₹ 100 each, failed to pay allotment ₹ 30 per share and first & final call ₹ 30 per share. Ashok had paid only application money. Pro-rata allotment proportion is 5:6. What will be the amount of calls-in arrears on allotment, from the following:

(a) ₹ 3,60,000

(b) ₹ 2,64,000

(c) ₹ 96,000

(d) None of these

Answer. B

Question. The allowed amount of discount on re-issue of shares will be

(a) @ 10% of issue price

(b) Up to the amount of forfeited money

(c) Could not issue at discount

(d) None of these

Answer. B

Question. The allowed amount of discount on re-issue of shares will be

(a) @ 10% of issue price

(b) Up to the amount of forfeited money

(c) Could not issue at discount

(d) None of these

Answer. B

Question. 12,000 shares of ₹ 100 each forfeited due to non payment of allotment of ₹ 40 per share and first & final call of ₹ 30 per share. Out of the forfeited shares, 9,000 shares were reissued at ₹ 80 per share fully paid. Which of the following amount of share forfeiture account will be transferred to Capital Reserve Account?

(a) 1,80,000

(b) 90,000

(c) 3,60,000

(d) 2,70,000

Answer. A

Question. Match the columns with reference to share capital of a company:

Column I Column II

(A) Capital Reserve (i) Memorandum of Association

(B) Minimum Subscription (ii) Allotment / Calls due but did not receive (C)Calls-in Arrears (iii) Reserves & Surplus

(D)Authorised Capital (iv) SEBI Guidelines

A B C D

(a) (iii) (iv) (ii) (i)

(b) (ii) (iv) (i) (iii)

(c) (ii) (i) (iii) (iv)

(d) (i) (ii) (iii) (iv)

Answer. A

Question. As per SEBI guidelines application money should not be less than ...............of the issue price of each share.

a) 10%

b) 15%

c) 25%

d) 50%

Answer. C

Question. Minimum subscription amount of 90% is related to which share capital….

a) Authorised Capital

b) Issued Capital

c) Paid up Capital

d) Reserve capital

Answer. B

Question. Kaar Ltd forfeited 4,000 shares of ₹20 each, fully called up, on which only application money of ₹6 has been paid. Out of these 2,000 shares were reissued and ₹8,000 has been transferred to capital reserve. Calculate the rate at which these shares were reissued.

(a) ₹20 Per share

(b) ₹18 Per share

(c) ₹22 Per share

(d) ₹8 Per share

Answer. B

Question. AB Ltd purchased a Machinery from XY Ltd for ₹ 4,50,000. AB Ltd immediately paid ₹ 90,000 by Bank Draft and the balance by issue of preference share of ₹ 100 each at 20% premium for the purchase consideration of Machinery to XY Ltd. Shares issued by AB Ltd?

(a) 3,000 preference shares

(b) 30,000 preference shares

(c) 3,600 preference shares

(d) 36,000 preference shares

Answer. A

Question. Shares issued by a company to its employees or directors in consideration of ‘Intellectual Property Rights’(IPR) are called…….

a) Right equity Shares

b) Private Equity shares

c) Sweat Equity Share

d) Bonus Equity shares

Answer. C

Question. Krishan Ltd has Issued Capital of 20, 00,000 Equity shares of ₹10 each. Till Date ₹8 per share have been called up and the entire amount received except calls of ₹4 per share on 800 shares and ₹3 per share from another holder who held 500 shares. What will be amount appearing as ‘Subscribed but not fully paid capital’ in the balance sheet of the company?

(a) ₹ 2,00,00,000

(b) ₹ 1,95,99,000

(c) ₹ 1,59,95,300

(d) ₹ 1,99,95,300

Answer. C

Question. Reserve capital is a part of …

a) Paid up Capital

b) Forfeited share capital

c) Asset

d) Capital to be called up only on liquidation of company.

There are two statements marked as Assertion (A) and Reason (R).

Read the statements and choose the appropriate option from the options given below for the question:

(a) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A)

(b) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A)

(c) Assertion (A) is false, but Reason (R) is true

(d) Assertion (A) is true, but Reason (R) is false

Answer. D

Question. Assertion: (A) Received amount of securities premium will not debited to securities premium reserve account, on forfeiture of shares.

Reason (R) Received amount of securities premium will be debited while writing off of certain type of capital loss or expenditure

Answer. B

Question. Assertion (A) Equity shares does not carry fixed rate of dividend and they are the ultimate risk bearer.

Reason (R) Equity shareholders are getting dividend from residual part of profits and in the case of windup of the company, invested money will be refunded at the last.

Answer. A

Question. Assertion (A): A company must receive minimum subscription on public issue of shares.

Reason (R): In default to receive minimum subscription, company could not allot its shares.

Answer. A

Question. 6,000 shares of ₹ 100 each (applied for 7,500 shares) forfeited due to non-payment of allotment ₹ 40 per share. First & final call was not yet made. Company received only application money at ₹ 50 per share including premium of ₹ 20 per share. Which of the following amount will be forfeited by the company?

(a) ₹ 3,75,000

(b) ₹ 3,00,000

(c) ₹ 2,55,000

(d) 1,80,000

Answer. C

Question. As per Section 52 of Companies Act 2013, Securities Premium Reserve cannot be utilised for:

(a) Writing off capital losses.

(b) Issue of fully paid bonus shares.

(c) Writing off discount on issue of securities.

(d) Writing off preliminary expenses.

Answer. A

Question. Public subscription of shares include:

a) To issue prospectus

b) To receive Application

c)To make allotment

d) All of the above

Answer. D

Question. Kamesh Ltd offered 2,00,000 Equity Shares of ₹10 each, of which 1,98,000 shares were subscribed. The amount was payable as ₹3 on application, ₹4 an allotment and balance on first call. If a shareholder holding 3,000 shares has defaulted on first call, what is the amount of money received on first call?

(a) ₹9,000.

(b) ₹5,85,000.

(c) ₹5,91,000.

(d) ₹6,09,000.

Answer. B

Question. Calculate the amount of second & final call when Abhijit Ltd, issues Equity shares of ₹10 each at a premium of 40% payable on Application ₹3, On Allotment ₹5, On First Call ₹2.

(a) Second & final call ₹3.

(b) Second & final call ₹4.

(c) Second & final call ₹1.

(d) Second & final call ₹14.

Answer. B

Question. Anil Ltd, issued a prospectus inviting applications for 2,000 shares. Applications were received for 3,000 shares and pro- rata allotment was made to the applicants of 2,400 shares. If Dhruv has been allotted 40 shares, how many shares must he have applied for?

(a) 40

(b) 44

(c) 48

(d) 52

Answer. C

Question. ……………….is transferred to the Capital Reserve.

a) Profit from sale of fixed assets

b) Premium on issue of shares

c) Profit on forfeiture of shares

d) all of the above

Answer. D

Question. Equity shares cannot be issued for the purpose of :

a) Cash Receipts

b) Purchase of Assets

c) Redemption of Debentures

d) Distribution of Dividend

Answer. D

Question are based on the hypothetical situation given below.

Star Limited is engaged in the manufacture of high-end medical equipment. Considering the prospects of high growth in this segment the company has decided to expand and for this purpose additional investment of ₹50,00,00,000 is required. Directors have decided that 20% of this requirement would be financed by raising long term debts and balance by issue of Equity shares. As per memorandum of association of the company the face value of Equity shares is ₹100 each. Also, considering the market standing of the company these shares would be issued at a premium of 25%. Directors decided to issue sufficient shares to collect the desired amount (including premium). The prospectus was issued to the public, and the issue was oversubscribed by 2,00,000 shares which were issued letters of regret. Answer the below mentioned questions considering that the entire amount was payable on application.

Question. What is the total amount collected on application?

(a) ₹42,50,00,000

(b) ₹40,00,00,000

(c) ₹32,00,00,000

(d) None of the above

Answer. A

Question. How many Equity shares were offered for issue by Star Ltd?

(a) 40,00,000 shares.

b) 50,00,000 shares.

c) 35,00,000 shares.

(d) 32,00,000 shares.

Answer. D

Question. People who start a company are called………..

a) Shareholders

b) Directors

c) Promoters

(d) Auditors

Answer. C

Question. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R):

Assertion (A): In case of shares issued on Pro–rata basis, excess money received at the time of application can be utilised till allotment only.

Reason (R): Company has to pay interest on calls in advance @12% p.a. for amounts adjusted towards calls (if any). In the context of the above two statements, which of the following is correct?

(a) Both (A) and (R) are true, but (R) is not the explanation of working capital management.

(b) Both(A) and (R) are true and (R) is a correct explanation of (A).

(c) Both (A) and (R) are false.

(d) (A) is false, but (R) is true.

Answer. D

Question. Read the following statement and Mark Option a for true and option b for false.

According to the below given information the final call per share is ₹22. The subscribed capital of a company is ₹80,00,000 and the nominal value of the share is ₹100 each. There were no calls in arrear till the final call was made. The final call made was paid on 77,500 shares only. The balance in the calls in arrear amounted to ₹ 55,000.

Answer. True

Question. Read the following statement and Mark Option a for true and option b for false.

Securities premium received on issue of shares cannot be used for the purpose of Buy back of shares.

Answer. False

Question. Read the following statement and Mark Option a for true and option b for false.

Share application amount is in the nature of a Real account.

Answer. False

Question. Arrange the following in proper sequence as types of “Share Capital”

(i) Paid up capital

(ii.) Issued capital

(iii) Subscribed capital

(iv.) Called up capital

Answer. Issued,Subscribed,Called– up,Paid-up.

Question. Maximum limit of premium on shares is:

(A.) 32%

(B.) 20%

(C.) No limit

(D.) 100%

Answer. C

Question. Amount of money not received out of called up capital is:

(A.) Added to share capital

(B.) Subtracted from share capital

(C.) Shown as current liabilities

(D.) Shown as current asset

Answer. B

Question. Following amounts were payable on issue of shares by a company: Rs.3on application, ₹3 on allotment, ₹2 on first call and ₹.2 on final call. X holding 500 shares paid only application and allotment money whereas Y holding 400 shares did not pay final call. Amount of calls in arrear will be:

(A.) ₹3,800

(B.) ₹2,800

(C.) ₹1,800

(D.) ₹6,200

Answer. B

Question. Rajan Limited issued 50,000 shares at a price lower than the nominal value of the share. The shares issued are called:

A) Sweat equity shares

B) Redeemable Preference shares

C) Equity shares

D) Bonus shares

Answer. A

Question. ENGOY Ltd. had allotted 10,000 shares to the applicants of 14,000shares on pro rata basis, application money on another 6000 shares was refunded. The amount payable on the application was ₹.2. RAAF applied for 420 shares.The number of shares allotted to him will be:

(A.) 60 shares

(B.) 340 shares

(C.) 320 shares

(D.) 300 shares

Answer. D

Question. A company issued 4,000 equity shares of ₹ 10 each at par payable as under: On application ₹3, on allotment ₹2; on first call ₹4 and on final call ₹ 1 per share. Applicants were received for 16,000 shares. Applications for 6,000 shares were rejected and pro-rata allotment was made to the applicants for 10,000 shares. How much amount will be received in cash on first call, when excess application money is adjusted towards amount due on allotments and calls:

(A.) ₹6.000

(B.) nil

(C.) ₹16,000

(D) ₹10,000

Answer. A

Question. A company issued 4000 equity shares of ₹ 50 each at par payable as under: On application rupees 20%, on allotment 40%; on first call 10%; on final call-balance Applications were received for 10,000 shares. Allotment was made pro-rata. How much will be received in cash on allotment?

(A) ₹ 6.000

(B.) nil

(C.) ₹ 16,000

(D.) ₹ 20,000

Answer. D

Question. Which one of the following is not a part of subscribed capital:

A) Equity shares issued to vendor

B) Preference shares of convertible type

C) Forfeited shares

D) Bonus shares

Answer. C

Question. When nominal(face) value of a share is called up by the company but as some shareholders did not pay the money, the shares are forfeited. The share capital is shown in the balance sheet(notes) of a company under the following heading:

A) Subscribed and fully paid up

B) Subscribed but not fully paid up

C) Subscribed and called up

D) Subscribed but not called up

Answer. A

Question. Zee Ltd issued 15,000 equity shares of ₹.20 each at a premium of ₹5 payable

₹.5 on application, ₹10 on allotment (including premium)and the balance on first and final call. The company received applications for 22,500 shares and allotment was made pro rata. Bittoo to whom 1,200shares were allotted, failed to pay the amount due on allotment. All his shares were forfeited after the call was made. The forfeited shares were reissued to Dheeraj at par. Assuming that no other bank transactions took place, the bank balance of the company after the above transactions is:

A) ₹ 6,85,000

B) ₹. 3,60,500

C) ₹. 3,78,000

D) ₹ 6,34,000

Answer. C

Question. EREK Ltd purchased the sundry assets of M/s Surat Industries for ₹.28,60,000 payable in fully paid shares of Rs. 100each. State the number of shares issued to vendors when issued at a premium of10%.

A) ₹ 28,000

B) ₹31,778

C) ₹ 28,600

D) ₹26,000

Answer. D

Question. The subscribed share capital of GUL Ltd is ₹1,00,00,000 of ₹100 each. There were no calls in arrear till the final call was made. The final call was paid on 97,500 shares. The calls in arrear amounted to ₹ 87,500. The final call on share:

A) ₹.20

B) ₹35

C) ₹.25

D) ₹.45

Answer. B

Question. These shares which in addition to the fixed preference dividend, carry a right to participate in the surplus profits, if any, after dividend at a stipulated rate has been paid to the equity shareholders are called:

A) Participating preference shares

B) Convertible preference shares

C) Redeemable preference shares

D) Cumulative preference shares

Answer. A

Question. T Ltd had allotted 20,000 shares to the applicants of 24,000 shares on pro rata basis. The amount payable on application is ₹2. Babua applied for 450 shares. The number of shares allotted and the amount carried forward for adjustment against allotment money due from him is:

A) 150shares, ₹375

B) 375 shares, ₹.150

C) 400shares, ₹100

D) 300shares, ₹.300

Answer. B

Question. A company forfeited 3,000 shares of ₹.10each (which were issued at par) held by Kishore for non payment of allotment money of ₹.5pershare. The called up value per share was ₹.8. On forfeiture, the amount debited to share capital:

A) ₹ 30,000

B) ₹ 24,000

C) ₹15,000

D) ₹. 6,000

Answer. B

Question. VIRE limited is used shares of ₹.100 each at a premium of 10%. Mr. Q Purchased 500 shares and paid ₹ 20 on application but did not pay the allotment money of ₹.30. If the company forfeited his 30% shares, the forfeiture account will be credited by :

A) ₹.4500

B) ₹3500

C) ₹.1650

D) ₹.3000

Answer. D

Question. Daisy Limited forfeited 200 shares ₹10 each who had applied for 500 shares, issued at a premium of10% for non payment of final call of ₹3 per share.

Out of these 100 shares were issued as fully paid up for ₹.15. The profit on reissue is: A) ₹.700

B) ₹.6400

C) ₹.300

D) ₹.400

Answer. A

Question. KOLI Limited was formed with share capital of ₹50,00,000 divided into 50,000 shares of ₹.100 each. 9,000 shares were issued to the vendor as fully paid for purchase consideration of furniture acquired. 30,000 shares were allotted in payment of cash on which ₹70 per share was called and paid. State the amount of subscribed capital:

A) ₹50,00,000

B) ₹.30,50,000

C) ₹.30,00,000

D) ₹.20,00,000

Answer. C

Question. BEWI Limited invited application for 2,00,000 shares of ₹.10each These shares were issued at premium of ₹11each which was allowed at the time of allotment. All money was called and duly received except on 10,000 shares on which only application money of ₹3 per share was received. The company forfeited all the shares. 7000 of forfeited shares were re-issued at ₹.13 per share. State the amount of securities premium to be shown under the head-Reserve and surplus.

A) ₹.20,00,000

B) ₹.11,11,000

C) ₹.8,11,000

D) ₹.21,11,000

Answer. D

Question. MEME limited has an authorized capital of ₹.1,00,00,000 divided into 1,00,000 equity shares of ₹.100 each. If offered 90,000 equity shares ₹10 each at a premium of ₹8. The public applied for 81,000 equity shares. Till 31st March 2018, ₹17(including premium) was called. An applicant holding 5000 shares did not pay first call of ₹.2 per share.

As per the above given information:

………………. Is the amount of Share capital to be shown in the balance sheet of the company.

Answer. Rs.7,19,000

Question. Out of total face value, liability of a share holder is limited to .................... value of the share allotted to him.

Answer. Calledup

Question. Match the following:

a) Cumulative Pref. Share i) Repaid after some time

b) Participating Pref. Share ii) converts into equity shares

c) Redeemable Pref. shares iii) Dividend accumulates if not paid

d) Convertible Pref. shares iv) Gets share in surplus profit

The correct match is:

A) a-ii, b-i, c-iii, d-iv

B) a-iii, b-iv, c-i, d-ii

C) a-iii, b-iv, c-ii, d-i

D) a -ii, b-iv, c-iii, d-i

Answer. B

CASE STUDY BASED QUESTIONS

Read the following statement carefully and give the answer for the questions:

Shine Firework Ltd is authorised to issue shares 5,00,000 of ₹ 100 each. Company raised the capital by issue of 2,00,000 shares through e-IPO. As per the decision of Managing Board of Directors of company, company issued 75,000 shares to their parent company and 40,000 shares issued to existing employees of company as per their choice and option at the below price than the market price.

Question. “Company issued 75,000 shares to their parent company” is an example of .

(a) Public Issue

(b) Private Placement

(c) ESOP

(d) Issue other than cash

Answer. B

Question. “40,000 shares issued to existing employees of company as per their choice and option at the below price than the market price.” Is an example of

(a ) Public Issue

(b) Private Placement

(c) ESOP

(d) Issue other than cash

Answer. C

Read the following statement carefully and give the answer for the questions:

X Ltd issued 2,00,000 shares of ₹ 100 each. Amount to be paid on Application ₹ 30 per share; on allotment ₹ 40 per share and on first & final call ₹ 30 per share. All money was duly subscribed and paid towards the nominal value of shares except on 9,000 shares who failed to pay allotment and calls money. These shares were forfeited. 5,000 shares were re-issued at ₹ 80 per share fully paid.

Question. Which amount of the following will be shown into the Balance Sheet of the company under the sub-head “Share Capital”?

(a) ₹ 1,96,00,000

(b) ₹ 1,97,20,000

(c) ₹ 2,00,00,000

(d) ₹ 1,97,70,000

Answer. A

Question. Which of the following amount will be, balance in Share Forfeiture Account?

(a) ₹ 4,00,000

(b) ₹ 1,50,000

(c) ₹ 1,20,000

(d) ₹ 50,000

Answer. D

Question. Given below are two statements, one labelled as Assertion the other labelled as Reason (R):

Assertion(A): Preferential allotment means allotment of shares at a pre determined price to the identified people who are interested in taking shares in the company.

Reason(R): Employee Stock Option Plan is a category of sweat Equity In the context of the above two statements, which of the following is correct?

(A) Both (A) and (R) are correct and (R) is the correct reason of (A)

(B) Both (A) and (R) are correct but (R) is not the correct reason of (A).

(C) Only (R) is correct.

(D) Both (A) and (R) are wrong.

Answer. B

Question. Given below are two statements, one labelled as Assertion the other labelled as Reason (R):

Assertion (A): The forfeited shares may be reissued by the company at par, at premium or at discount.

Reason(R): Reissue of forfeited shares is not an issue of shares but is selling the shares that were issued earlier and were cancelled by the company. In the context of the above two statements, which of the follow-ing is correct?

(A) Both (A) and (R) are correct and (R) is the correct reason of (A).

(B) Both (A) and (R) are correct but (R) is not the correct reason of (A).

(C) Only (R) is correct.

(D) Both (A) and (R) are wrong.

Answer. A

Question. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R)

Assertion (A)The part of un-called capital, to be called only in the liquidation of a company is called Reserve Capital.

Reason (R) : It can be used for writing off capital losses.

In the context of the above two statements, which of the following is correct?

(A) is correct, but (R) is wrong.

(B) Both (A) and (R) are correct.

(C) (A) is wrong, but (R) is correct.

(D) Both (A) and (R) are wrong

Answer. A

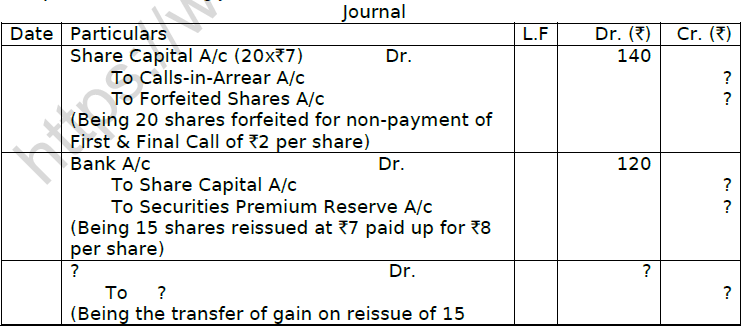

10 Complete the following journal entries for forfeiture and reissue.

![]()

Free study material for Accountancy

Part 2 Chapter 1 Accounting for Share Capital CBSE Class 12 Accountancy Worksheet

Students can use the Part 2 Chapter 1 Accounting for Share Capital practice sheet provided above to prepare for their upcoming school tests. This solved questions and answers follow the latest CBSE syllabus for Class 12 Accountancy. You can easily download the PDF format and solve these questions every day to improve your marks. Our expert teachers have made these from the most important topics that are always asked in your exams to help you get more marks in exams.

NCERT Based Questions and Solutions for Part 2 Chapter 1 Accounting for Share Capital

Our expert team has used the official NCERT book for Class 12 Accountancy to create this practice material for students. After solving the questions our teachers have also suggested to study the NCERT solutions which will help you to understand the best way to solve problems in Accountancy. You can get all this study material for free on studiestoday.com.

Extra Practice for Accountancy

To get the best results in Class 12, students should try the Accountancy MCQ Test for this chapter. We have also provided printable assignments for Class 12 Accountancy on our website. Regular practice will help you feel more confident and get higher marks in CBSE examinations.

FAQs

You can download the teacher-verified PDF for CBSE Class 12 Accountancy Accounting For Share Capital Worksheet from StudiesToday.com. These practice sheets for Class 12 Accountancy are designed as per the latest CBSE academic session.

Yes, our CBSE Class 12 Accountancy Accounting For Share Capital Worksheet includes a variety of questions like Case-based studies, Assertion-Reasoning, and MCQs as per the 50% competency-based weightage in the latest curriculum for Class 12.

Yes, we have provided detailed solutions for CBSE Class 12 Accountancy Accounting For Share Capital Worksheet to help Class 12 and follow the official CBSE marking scheme.

Daily practice with these Accountancy worksheets helps in identifying understanding gaps. It also improves question solving speed and ensures that Class 12 students get more marks in CBSE exams.

All our Class 12 Accountancy practice test papers and worksheets are available for free download in mobile-friendly PDF format. You can access CBSE Class 12 Accountancy Accounting For Share Capital Worksheet without any registration.