Access the latest CBSE Class 12 Accountancy Accounting For Companies Worksheet. We have provided free printable Class 12 Accountancy worksheets in PDF format, specifically designed for Part 2 Chapter 1 Accounting for Share Capital. These practice sets are prepared by expert teachers following the 2025-26 syllabus and exam patterns issued by CBSE, NCERT, and KVS.

Part 2 Chapter 1 Accounting for Share Capital Accountancy Practice Worksheet for Class 12

Students should use these Class 12 Accountancy chapter-wise worksheets for daily practice to improve their conceptual understanding. This detailed test papers include important questions and solutions for Part 2 Chapter 1 Accounting for Share Capital, to help you prepare for school tests and final examination. Regular practice of these Class 12 Accountancy questions will help improve your problem-solving speed and exam accuracy for the 2026 session.

Download Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital Worksheet PDF

VERY SHORT ANSWER TYPE QUESTIONS

Question. What is meant by issue of shares at premium?

Answer: Issue of shares at premium means issuing shares at a price higher than their face value (nominal value). The excess amount is called securities premium.

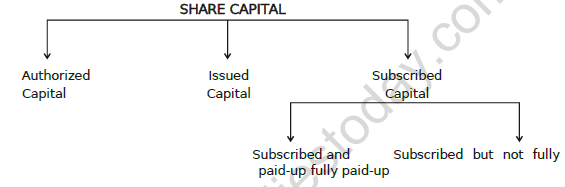

Question. What is meant by over-subscription? What options does a Company have to deal with over-subscription?

Answer: Over-subscription occurs when the number of applications received for shares is more than the number of shares offered for subscription. The company has three options: (i) Reject excess applications and refund money, (ii) Make pro-rata allotment, or (iii) A combination of both.

Question. Equity shareholders are ;

(a) Creditors

(b) Owners

(c) Customers of the company

(d) None of these

Answer: (b)

Question. A company issued 25,000 shares and received applications for 35,000 shares . company wants to allot shares to everyone who has applied. What will be the ratio for allotment

(a) \( 6:7 \)

(b) \( 7:5 \)

(c) \( 5:7 \)

(d) \( 7:6 \)

Answer: (c)

Question. In a Public Company the maximum number of members is :

(a) 50

(b) 1000

(c) 20

(d) Upto number of shares

Answer: (d)

Question. Premium received on issue of shares at :

(a) Liabilities side

(b) Assets side

(c) Credit side of profit and loss A/c

(d) Debit side of profit and loss A/c

Answer: (a)

Question. Which amongst the following shares confer voting rights on its holders ?

(a) Equity share

(b) Redeemable preferences shares

(c) participatory preference shares

(d) None of these

Answer: (a)

Question. A Company forfeited 60 shares of Rs. Rs. 10 each Rs. 8 per share called up on which X had paid application and Allotment money of Rs. 6 per share. Shares forfeiture a/c will be credited by the amount –

(a) 160

(b) 480

(c) 360

(d) 200

Answer: (c)

Question. Match Part – A with Part – B

Part - A

(i) Essential features of a company

(ii) Private company

(iii) Memorandum of Association

(iv) Govt. Company

(v) Company’s Preliminary Expense

Part - B

(a) Basic discount

(b) Restrict the right of transfer of shares

(c) Atleast \( 51\% \) shares on paid up capital with Govt.

(d) Underwriting commission

(e) Limited liability

Answer: (i)-(e), (ii)-(b), (iv)-(c)

Question. True or False Type Questions (state true or false)

1. Issued capital can be less than called up capital.

2. Share of a company is moveable asset.

3. Promoters are the owners of the company.

4. Capital reserve is made out of capital profits.

5. Ltd. Word is used for private companies.

Answer: 1. False, 2. True, 3. False, 4. True, 5. False

Question. Fill in the blanks.

1. Upon forfeiture of shares, share capital account is debited by ………………………….

2. The profit made on reissue of shares is transferred to …………………………………….

3. When shares are forfeited, Calls – in- arrear Account is…………………….

4. If a share Rs. 50 on which Rs. 40 has been called up and Rs. 30 is paid is forfeited, the capital account should be debited with………………………

5. If shares were issued at premium and such premium has been received then on forfeiture such premium is…………………………………..

Answer: 1. Called-up amount, 2. Capital Reserve, 3. Credited, 4. \( Rs. 40 \), 5. Ignored/Not cancelled

SHORT ANSWER TYPE QUESTIONS

Question. What is the difference between capital reserve and reserve capital?

Answer: Reserve Capital is that part of uncalled capital which a company decides to call only at the time of winding up. Capital Reserve is a reserve created out of capital profits (e.g., profit on sale of fixed assets or forfeiture of shares) and is not available for distribution as dividend.

Question. State the provisions of section 52 of companies act 2013. OR How security premium can be utilized by the company?

Answer: Under Section 52(2), Securities Premium can be used for: (i) Issuing fully paid bonus shares, (ii) Writing off preliminary expenses, (iii) Writing off expenses/commission/discount on issue of shares/debentures, (iv) Providing for premium payable on redemption of preference shares/debentures, (v) Buyback of own shares.

Question. ABC Ltd. issue 10,000 equity shares of Rs 100 each, payable as Rs 30 on application, Rs 40 on allotment and Rs 30 on first and final call. Pass necessary journal entries.

Answer: Journal entries involve: (1) Bank A/c Dr \( 3,00,000 \) to Share App A/c, (2) Share App A/c Dr \( 3,00,000 \) to Share Cap A/c, (3) Share Allot A/c Dr \( 4,00,000 \) to Share Cap A/c, (4) Bank A/c Dr \( 4,00,000 \) to Share Allot A/c, (5) Share First & Final Call A/c Dr \( 3,00,000 \) to Share Cap A/c, (6) Bank A/c Dr \( 3,00,000 \) to Share First & Final Call A/c.

Question. AB Ltd issues 5,00,000 equity shares of Rs 10 each at \( 20\% \) premium, payable as Rs 3 on Application, Rs 4 on allotment, Rs 2 on first call and balance on final call. Applications received for 6,00,000 Equity shares, 40,000 applicants rejected and rest allotted proportionately. All the calls were made and duly received. Pass necessary journal entries.

Answer: (1) Bank A/c Dr \( 18,00,000 \) to Share App A/c, (2) Share App A/c Dr \( 18,00,000 \) to Share Cap A/c (\( 15,00,000 \)), to Bank A/c (\( 1,20,000 \)), to Share Allot A/c (\( 1,80,000 \)), (3) Share Allot A/c Dr \( 20,00,000 \) to Share Cap A/c (\( 10,00,000 \)) and Securities Premium A/c (\( 10,00,000 \)), (4) Bank A/c Dr \( 18,20,000 \) to Share Allot A/c.

Question. XY Ltd purchased Land of Rs 8,00,000 and Machinery of Rs 3,00,000 from PQ Ltd. Purchase consideration satisfied by issue of equity shares of Rs 100 each. Pass necessary journal entries for above transactions.

Answer: (1) Land A/c Dr \( 8,00,000 \), Machinery A/c Dr \( 3,00,000 \) to PQ Ltd \( 11,00,000 \). (2) PQ Ltd Dr \( 11,00,000 \) to Equity Share Capital A/c \( 11,00,000 \) (Issue of 11,000 shares).

Question. MN Ltd. purchased Land of Rs 19, 00,000, Plant and Machinery of Rs 6,00,000 and also acquired creditors of Rs 3,00,000. Purchase consideration settled by issue of Equity shares of Rs 100 each at \( 10\% \) premium. Pass necessary journal entries

Answer: Net Assets = \( 19,00,000 + 6,00,000 - 3,00,000 = 22,00,000 \). Number of shares = \( 22,00,000 / 110 = 20,000 \). Entry: Vendor Dr \( 22,00,000 \) to Equity Share Cap \( 20,00,000 \) and Securities Premium \( 2,00,000 \).

Question. Pass necessary Journal entries for the following transaction in the books of Sachin Ltd. Sachin Ltd. purchased a running business from Deepak Ltd. for a sum of Rs.3,00,000 payable as Rs.2,50,000 in fully paid Equity shares and balance by a bank draft. The assets and liabilities consisted of the following :- Plant and Machinery Rs.72,000; Building Rs.80,000; Sundry Debtors Rs. 38,000; Stock Rs. 60,000; Sundry Creditors Rs.40,000.

Answer: (1) Plant & Machinery A/c Dr \( 72,000 \), Building A/c Dr \( 80,000 \), Debtors A/c Dr \( 38,000 \), Stock A/c Dr \( 60,000 \), Goodwill A/c Dr \( 90,000 \) to Creditors \( 40,000 \) and Deepak Ltd \( 3,00,000 \). (2) Deepak Ltd Dr \( 3,00,000 \) to Equity Share Cap \( 2,50,000 \) and Bank A/c \( 50,000 \).

Question. 100 shares of Rs 10 each(Rs 8 called up) cancelled as shareholder failed to pay first call of Rs 3. All the shares reissued for Rs 7 per share as fully paid up. Pass entries for forfeiture and re-issue

Answer: (1) Share Cap A/c Dr \( 800 \) to Share Forfeiture A/c \( 500 \) and First Call A/c \( 300 \). (2) Bank A/c Dr \( 700 \), Share Forfeiture A/c Dr \( 300 \) to Share Cap A/c \( 1000 \). (3) Share Forfeiture A/c Dr \( 200 \) to Capital Reserve A/c \( 200 \).

Question. Pass journal entries for the forfeiture and re-issue in the following cases:-

(a.) Z Limited forfeited 800 shares of Ashok of Rs. 10 each fully paid called up due to non-payment of Final Call of Rs. 3 per share. All these shares were re-issued to Mohan for Rs. 8 per share as fully paid up.

(b.) K Limited forfeited 80 shares of Rs. 100 each due to non-payment of First Call of Rs. 20 per share. Second and Final Call of Rs. 30 has not been yet called. Out of these 24 shares were re-issued for Rs. 60 per share.

Answer: (a) Cap Dr \( 8,000 \) to Forf \( 5,600 \) and Call \( 2,400 \). Reissue: Bank \( 6,400 \), Forf \( 1,600 \) to Cap \( 8,000 \). Cap Reserve \( 4,000 \). (b) Cap Dr \( 5,600 \) (\( 80 \times 70 \)) to Forf \( 4,000 \) and Call \( 1,600 \). Reissue: Bank \( 1,440 \), Forf \( 960 \) to Cap \( 2,400 \). Cap Reserve: \( (50 \times 24) - 960 = 240 \).

Question. 80 shares of Rs 10 each, cancelled due to nonpayment of final call of Rs 3. All the shares reissued at Rs 12 per share. Pass entries for forfeiture and re-issue.

Answer: (1) Share Cap Dr \( 800 \) to Forf \( 560 \) and Call \( 240 \). (2) Bank Dr \( 960 \) to Cap \( 800 \) and Sec Prem \( 160 \). (3) Forfeiture A/c Dr \( 560 \) to Capital Reserve \( 560 \).

Question. Axis Ltd. issues 60,000 Equity shares of Rs 100 each at \( 10\% \) premium, payable as follows: Application Rs 20, Allotment Rs 30, First call Rs. 30, second call - balance. Issue was oversubscribed by 40,000 shares. 20,000 applications rejected and rest alloted proportionately . All installments were duly received, except call money on 200 shares. Pass necessary journal entries.

Answer: Total app = \( 1,00,000 \). Rejected = \( 20,000 \). Pro-rata = \( 80,000:60,000 = 4:3 \). Excess app money = \( 20,000 \times 20 = 4,00,000 \) adjusted to allotment. Second call balance = \( 110 - (20+30+30) = 30 \). Calls in arrears on 200 shares on first and second call.

Question. On 1st April 2012 Ashwin Ltd. was formed with an authorized capital of 10,00,000 divided into 20,000 equity shares of Rs. 50 each. The company issued prospectus inviting applications for 18,000 shares. The issue price was payable as under: On application: Rupees 20. On allotment: Rupees 20 On call: balance amount. The issue was fully subscribed and the company allotted shares to all the applicants. The company did not make the call during the year, Chahal having 1,000 shares didn’t pay the allotment. Show the following: (a) Share capital in the balance sheet of the company as per schedule III, part 1 of the Companies Act, 2013. (b) Also prepare notes of accounts for the same.

Answer: Subscribed but not fully paid capital: \( 18,000 \times 40 = 7,20,000 \) less calls in arrears \( 1,000 \times 20 = 20,000 \). Net Share Capital = \( 7,00,000 \).

LONG ANSWER TYPE QUESTIONS

Question. A ltd invited applications for issuing 1,50,000 equity shares of Rs.10 each at a discount of \( 10\% \).The amount was payable as follows: On application Rs.2 per share, On allotment Rs.2 per share, On first and final call balance. Applications for Rs.3,00,000 shares were received. Applications for 50,000 shares were rejected and application money of these applicants was refunded. Shares were allotted on pro rata basis to the remaining applicants Excess money received with these applicants was adjusted towards sum due on allotment. Neha who had applied for 2,500 shares, failed to pay the allotment and first and final call money. Hemant did not pay the first and final call money on his 2000 shares. All these shares were forfeited and later on 2000 of these shares were reissued at Rs.17 per share fully paid up. The reissue shares included all the shares of Neha. Pass the necessary journal entries in the books of A ltd. For the above transactions.

Answer: Allotment ratio = \( 2,50,000 : 1,50,000 = 5:3 \). Neha allotted = \( 2,500 \times 3/5 = 1,500 \) shares. Hemant allotted = \( 2,000 \) shares. Total forfeited shares = \( 1,500 + 2,000 = 3,500 \). Reissue of \( 2,000 \) shares includes all \( 1,500 \) of Neha and \( 500 \) of Hemant. [Note: Discount on issue is no longer allowed per Companies Act 2013, entries to be made assuming it as a case study].

Question. Jk.ltd invited application for issuing 70,000 equity shares of Rs.10 each at a premium of Rs.2 per share the amount was payable as follows: On application Rs.3 per share, On allotment Rs.4(including premium Rs.2), On first and final call balance. Applications for 65,000 shares were received and allotment was made to all the applicants .A shareholder Ram who was allotted 2000 shares failed to pay the allotment money. His shares were forfeited immediately after the allotment. Afterwards the first and final call was made. Soham who had 3,000 shares failed to pay the first and final call his shares were also forfeited. Out of forfeited shares 4,000 were reissued at Rs.20 per share fully paid up.The reissued share included all the shares of Ram. Pass the necessary journal entries for the above transactions in the book of JK.ltd .

Answer: Ram's forfeiture: Share Cap Dr \( 10,000 \) (\( 2,000 \times 5 \)), Sec Prem Dr \( 4,000 \) to Share Forf \( 6,000 \) and Allot \( 8,000 \). Soham's forfeiture: Share Cap Dr \( 30,000 \) to Share Forf \( 15,000 \) and Call \( 15,000 \). Reissue: Bank Dr \( 80,000 \) to Share Cap \( 40,000 \) and Sec Prem \( 40,000 \). Capital Reserve: \( 6,000 \) (Ram) + \( 10,000 \) (Soham pro-rata) = \( 16,000 \).

Question. Garima Limited issued a prospectus inviting applications for 3,000 shares of Rs. 100 each at a premium of Rs.20 payable as follows: On Application Rs.20 per share, On Allotment Rs.50 per share (Including premium), On First call Rs.20 per share, On Second call Rs.30 per share. Applications were received for 4,000 shares and allotments made on prorata basis to the applicants of 3,600 shares, the remaining applications being rejected, money received on application was adjusted on account of sums due on allotment. Renuka whom 360 shares were allotted failed to pay allotment money and calls money, and her shares were forfeited. Kanika, the applicant of 200 shares failed to pay the two calls, her shares were also forfeited. All these shares were sold to Naman as fully paid for Rs.80 per share. Show the journal entries in the books of the company.

Answer: Renuka applied = \( 360 \times 3,600/3,000 = 432 \) shares. Kanika allotted = \( 200 \times 3,000/3,600 = 166.67 \) [Note: Numbers usually rounded in exam problems, assume 180]. Journalize application, allotment with pro-rata adjustment, forfeiture, and reissue at a discount of \( Rs. 20 \).

Question. Raja Ltd. Invited applications for 1,00,000 equity shares of Rs. 10 each . the shares were issued at a premium of Rs. 5 per share. The amount was payable as follows: On application and allotment Rs. 8 per share (including premium Rs. 3 ), The balance including premium on the first and final call . Applications for 1,50,000 shares were received . Applications for 10,000 shares were rejected and pro-rata allotment was made to the remaining applicants on the following basis. (i) Applicants for 80,000 shares were allotted 60,000 shares. (ii) Applicants for 60,000 shares were allotted 40,000 shares. (iii) P, who belonged to the first category and was allotted 300 shares, failed to pay first call money. Q, who belonged to the second category and was allotted 200 shares ,also failed to pay the first call money . their shares were forfeited . the forfeited shares were re-issued@ Rs. 12 per share fully paid –up . pass necessary journal entries and prepare cash book .

Answer: Application/Allotment = \( Rs. 5 + Rs. 3 \) premium. First/Final Call = \( Rs. 5 + Rs. 2 \) premium. P applied = \( 400 \) shares. Q applied = \( 300 \) shares. Calculate calls-in-arrears, forfeiture, and reissue profit to Capital Reserve.

Question. on 1st June , 2019, kartik Ltd. Offered for subscription 50,000 equity shares of Rs. 100 each at a premium of Rs. 20 per share payable as given below: On application Rs. 20 per share , on allotment (Including premium ) Rs. 50 per share and two month after allotment Rs. 50 per share . Application were received for 84,000 shares. On 1 st July , 2019 , the Directors processed to allot shares proportionately . of these, application for 4,500 shares were accompanied with full amount and hence, were accepted in full and the balance allotment was made on pro-rata basis. Excess amount paid by applicants was utilized towards allotment and call money due from them. One of the applicants to whom 300 shares were allotted proportionately , failed to pay the call money. His shares were forfeited on 30th November , 2019 and subsequently issued @ Rs. 130 per share. Record entries relating to these transactions in the journal of the company.

Answer: Total shares = \( 50,000 \). \( 4,500 \) full allotment. Remaining \( 45,500 \) shares allotted to \( 79,500 \) applicants. Pro-rata ratio = \( 79,500 : 45,500 \). [Note: Adjust excess money carefully to calls]. Reissue at Rs. 130 means premium of Rs. 30.

Question. CANDID Ltd. Invited applications for issuing 75,000 equity shares of Rs. 100 each at a premium of Rs. 30 per share . the amount was payable as follows . On application and allotment Rs. – Rs. 85 per share (including premium ), On first and final call- the balance account . Applications for 1,27,500 shares were received . Applications for 27,500 shares were rejected and shares were allotted on prorate basis to the remaining applicants. Excess money received on application and allotment was adjusted towards sum due on first and final call. The calls were made. A shareholder , who applied for 1,000 shares, failed to pay the first and final call money . his shares were forfeited . all the forfeited shares were re- issued at Rs. 150 per share fully paid –up. Pass necessary journal entries for the above transactions in the books of CANDID Ltd.

Answer: Pro-rata ratio = \( 1,00,000 : 75,000 = 4:3 \). Shareholder applied \( 1,000 \), allotted = \( 750 \) shares. Balance on call = \( 130 - 85 = 45 \). Reissue at \( Rs. 150 \) means \( Rs. 50 \) premium.

Question. The Director of X Ltd. issued for public subscription 50,000 equity shares of Rs. 10 each at Rs. 12 per share payable as to Rs. 5 on application (including premium), Rs. 4 on allotment and the balance on call. Applications for 70,000 shares were received. Of the cash received Rs. 40,000 was returned and Rs.60,000 was applied to the amount due on allotment, All the shareholders paid the call due with the exception of an allottee of 500 shares. These shares were forfeited and reissued as fully paid at Rs. 8 per share. The company, as a matter of policy, does not maintain a calls-in-arrears account. Give journal entries to record these transactions in the books of X. Ltd.

Answer: Total money received = \( 70,000 \times 5 = 3,50,000 \). \( 40,000 \) refunded (for 8,000 shares). Pro-rata on \( 62,000 \) shares to \( 50,000 \). Excess \( 12,000 \times 5 = 60,000 \) to allotment. 500 shares failed to pay call (\( Rs. 3 \)). Forfeit and reissue entries required.

Question. Sunrise Company Limited offered for public subscription 10,000 shares of Rs.10 each at Rs. 11 per share. Money was payable as follows: Rs. 3 on application, Rs. 4 on allotment (including premium), Rs. 4 on first and final call. Applications were received for 12,000 shares and the directors made prorate allotment. Mr. Ahmad, an applicant for 120 shares, could not pay the allotment and call money, and Mr. Basu, a holder of 200 shares, failed to pay the call. All these shares were forfeited. Out of the forfeited shares, 150 shares (the whole of Mr. Ahmad’s shares being included) were issued at Rs. 8 per share fully paid-up. Prepare Cash Book, Shares Capital Account and Share Forfeiture Account.

Answer: Ahmad applied \( 120 \), allotted \( 100 \). Basu allotted \( 200 \). Total forfeited = \( 300 \) shares. Reissue \( 150 \) shares. Ahmad's forfeiture = \( 360 \) (paid on app). Basu's forfeiture = \( 200 \times 6 = 1200 \). Capital reserve calculation based on shares reissued.

Question. A Ltd. Invited applications for issuing 1,00,000 shares of Rs.10 each at a premium of Rs. 1 per share . The amount was payable as follows: On application Rs. 3 per share, On allotment Rs. 3 per share (including premium ), On first call Rs. 3 per share, On second and final call Balance amount. Application for 1,60,000 shares were received . Allotment was made on the following basis: (i) To applicants for 90,000 shares 40,000 shares, (ii) To applicants for 50,000 shares 40,000 shares, (iii) To applicants for 20,000 shares Full shares. Excess money paid on application is to be adjusted against the amount due on allotment and call. Rishabh , a shareholder, who applied for 1,500 shares and belonged to category (ii) , did not pay allotment, first and second and final call money , Another shareholder, Sudha , who applied for 1,800 shares and belonged to category (i), did not pay the first and second and final call money. All the shares of Rishabh and Sudha were forfeited and were subsequently re- issued at Rs. 7 per share fully paid. Pass the necessary journal entries in the books of A Ltd. Open calls -in-arrears account and calls-in advance account wherever required.

Answer: Rishabh allotted = \( 1,500 \times 40/50 = 1,200 \). Sudha allotted = \( 1,800 \times 40/90 = 800 \). Second call = \( 11 - 9 = 2 \). Adjust excess application money to allotment and calls-in-advance.

Please click on below link to download CBSE Class 12 Accountancy Accounting For Companies Worksheet

Free study material for Accountancy

Part 2 Chapter 1 Accounting for Share Capital CBSE Class 12 Accountancy Worksheet

Students can use the Part 2 Chapter 1 Accounting for Share Capital practice sheet provided above to prepare for their upcoming school tests. This solved questions and answers follow the latest CBSE syllabus for Class 12 Accountancy. You can easily download the PDF format and solve these questions every day to improve your marks. Our expert teachers have made these from the most important topics that are always asked in your exams to help you get more marks in exams.

NCERT Based Questions and Solutions for Part 2 Chapter 1 Accounting for Share Capital

Our expert team has used the official NCERT book for Class 12 Accountancy to create this practice material for students. After solving the questions our teachers have also suggested to study the NCERT solutions which will help you to understand the best way to solve problems in Accountancy. You can get all this study material for free on studiestoday.com.

Extra Practice for Accountancy

To get the best results in Class 12, students should try the Accountancy MCQ Test for this chapter. We have also provided printable assignments for Class 12 Accountancy on our website. Regular practice will help you feel more confident and get higher marks in CBSE examinations.

FAQs

You can download the teacher-verified PDF for CBSE Class 12 Accountancy Accounting For Companies Worksheet from StudiesToday.com. These practice sheets for Class 12 Accountancy are designed as per the latest CBSE academic session.

Yes, our CBSE Class 12 Accountancy Accounting For Companies Worksheet includes a variety of questions like Case-based studies, Assertion-Reasoning, and MCQs as per the 50% competency-based weightage in the latest curriculum for Class 12.

Yes, we have provided detailed solutions for CBSE Class 12 Accountancy Accounting For Companies Worksheet to help Class 12 and follow the official CBSE marking scheme.

Daily practice with these Accountancy worksheets helps in identifying understanding gaps. It also improves question solving speed and ensures that Class 12 students get more marks in CBSE exams.

All our Class 12 Accountancy practice test papers and worksheets are available for free download in mobile-friendly PDF format. You can access CBSE Class 12 Accountancy Accounting For Companies Worksheet without any registration.