Download the latest CBSE Class 11 Accountancy Recording Of Transaction Concepts And Illustrations in PDF format. These Class 11 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 11 students.

Revision Notes for Class 11 Accountancy Chapter 3 Recording of Transactions-I

To secure a higher rank, students should use these Class 11 Accountancy Chapter 3 Recording of Transactions-I notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Chapter 3 Recording of Transactions-I Revision Notes for Class 11 Accountancy

Accounting Equation : Total Assets = Total Liabilities Or Total Assets = Internal Liabilities + External Liabilities Or Total Assets = Capital + Liabilities Classification of Transactions Following are the nine basic transactions:

1. Increase in assets with corresponding increase in capital.

2. Increase in assets with corresponding increase in liabilities.

3. Decrease in assets with corresponding decrease in capital.

4. Decrease in assets with corresponding decrease in liabilities.

5. Increase and decrease in assets.

6. Increase and decrease in liabilities

7. Increase and decrease in capital

8. Increase in liabilities and decrease in capital

9. Increase in capital and decrease in liabilities.

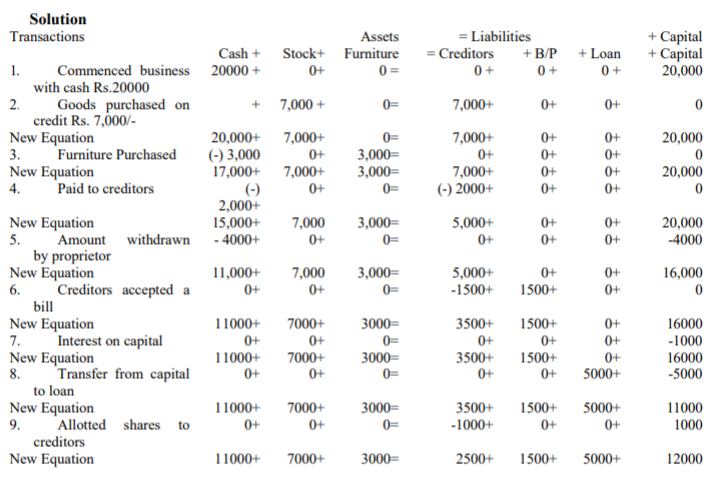

Illustration : Show the effect of the following business transactions on assets, liabilities and capital through accounting equations:

1. Commenced business with cash 20,000

2. Goods purchased on credit 7,000

3. Furniture purchased 3,000

4. paid to creditors 2,000

5. Amount withdrawn by the proprietor 4,000

6. Creditors accepted a bill for payment 1,500

7. interest on capital 1,000

8. Transfer from capital to loan 5,000

9. Allotted shares to creditors 1,000

Question for Practice:

Prepare Accounting equation on the basis of following information:

(1) Sohan started business with cash =80,000

Machinery =10,000

And stock =10,000

(2) Interest on the above capital was allowed @ 10%

(3) Money withdrew from the business for his personal use 10,000/-

(4) Interest on drawings 500/-

(5) Depreciation charged on machinery 2,000/-

Q. How the assets liabilities and capital will be affected under following cases:

(1) Purchase of building for cash

(2) Purchase of furniture on credit

(3) Receipt of commission

(4) Payment to creditors

Generally Students commit these mistakes please avoid :

• Treatment of adjustment in accounting equation

• Dual or triple effect of transaction

• Omission in recording amount

• Interest on capital and drawing

• Debit and credit should be done properly

• Depreciation must be treated properly.

RULES OF DEBIT AND CREDIT (I) Traditional or English Approach: This approach is based on the main principle of double entry system i.e. every debit has a credit and every credit has a debit. According to this system we should record both the aspects of a transaction whereas one aspect of a transaction will be debited and other aspect of a transaction will be credited.

(1) Personal Account: Debit the receiver and credit the giver.

(2) Real Account: Debit what comes in and credit what goes out.

(3) Nominal Account: Debit all expenses and losses credit all incomes and gains.

(2) Modern or American Approach: This approach is based on the accounting equation or balance sheet. In this approach accounts are debited or credited according to the nature of an account. In a summarised way the five rules of modern approach is as follows:

1. Increase in asset will be debited and decrease will be credited.

2. Increase in the liabilities will be credited and decrease will be debited.

3. Increase in the capital will be credited and decrease will be debited.

4. Increase in the revenue or income will be credited and decrease will be debited.

5. Increase in expenses and losses will be debited and decrease will be credited.

SOURCE DOCUMENTS

Meaning of Source documents: Business transactions are recorded in the books of accounts on the basis of some written evidence called source document.

Common Source documents are Cash Memo, Invoice or Bill, Receipts, Debit Note, Credit Note, Cheque, Pay in slip

Meaning of Voucher: Voucher is a source by which we record the transactions.

Meaning of Journal: Journal is a book of prime entry in which transactions are copied in order of date from a memorandum or waste book.

Illustration:

Journalise the following transactions in the books of Ravi:

1. Bought goods from Sonam Rs. 20,000 less trade discount 20% plus VAT @ 10%.

2. Sold goods costing Rs. 6,000 to Ram for Rs. 8,000 plus VAT @ 10%

3. Sold the balance goods for Rs. 16,000 and charged VAT @ 10% to Mohan against payment by cheque which was banked on the same day.

4. Deposited the VAT into government account by cheque.

Question for Practice:

Journalise the following transactions:

1. Paid sales tax Rs. 5,000.

2. Sold goods for Rs. 80,000 to Diwan for cash and charged 8% sales tax.

3. Purchased goods from Neelam for Rs. 50,000 plus VAT @ 10%

4. Sold goods to Punam worth Rs. 80,000 plus VAT @ 10%.

5. VAT was deposited into Government Account on its due date.

6. Paid Income Tax Rs. 7,000.

CASH BOOK Meaning: Cash book is a book in which all the transactions related to cash receipts and cash payments are recorded.

Please click the link below to download pdf file for CBSE Class 11 Accountancy Recording Of Transaction Concepts And Illustrations.

Free study material for Accountancy

CBSE Class 11 Accountancy Chapter 3 Recording of Transactions-I Notes

Students can use these Revision Notes for Chapter 3 Recording of Transactions-I to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 11. Our teachers always suggest that Class 11 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Chapter 3 Recording of Transactions-I Summary

Our expert team has used the official NCERT book for Class 11 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 11. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Chapter 3 Recording of Transactions-I Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Chapter 3 Recording of Transactions-I. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 11 Accountancy Recording Of Transaction Concepts And Illustrations from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 11 students get the best study material for Accountancy.

Yes, our CBSE Class 11 Accountancy Recording Of Transaction Concepts And Illustrations include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 11 Accountancy Recording Of Transaction Concepts And Illustrations provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 11 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 11 Accountancy Recording Of Transaction Concepts And Illustrations, Class 11 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 11 Accountancy Recording Of Transaction Concepts And Illustrations, are available for immediate free download. Class 11 Accountancy study material is available in PDF and can be downloaded on mobile.