Download the latest CBSE Class 11 Accountancy Introduction To Accounting Notes in PDF format. These Class 11 Accountancy revision notes are carefully designed by expert teachers to align with the 2026-27 syllabus. These notes are great daily learning and last minute exam preparation and they simplify complex topics and highlight important definitions for Class 11 students.

Revision Notes for Class 11 Accountancy Chapter 1 Introduction to Accounting

To secure a higher rank, students should use these Class 11 Accountancy Chapter 1 Introduction to Accounting notes for quick learning of important concepts. These exam-oriented summaries focus on difficult topics and high-weightage sections helpful in school tests and final examinations.

Chapter 1 Introduction to Accounting Revision Notes for Class 11 Accountancy

“There's no business like show business, but there are several businesses like accounting.

” Introduction:

Accounting has greater discipline than book keeping. It includes conceptual knowledge of the subject and applications also.

BOOK KEEPING:-

It involves journal, ledger, cash book and other subsidiary books, it cannot disclose the results of Business. Meaning of Accounting:-It is process of identifying, measuring, recording and communicating the financial information.

Difference between Bookkeeping and accountancy: Book keeping does not show the net result and accountancy shows net result of the business.

Economic Events:- All events which can be measured in monetary Terms are known as Economic events. (Salary paid to employees, Goods purchased from creditors, cash withdrew from bank)

CHANGING ROLE OF ACCOUNTANCY

1. As a language to communicate information an enterprises.

2. To provide valuable information for judging management ability.

3. To provide quantitative information this is useful in economic decision.

Process of accounting

1. Identification of the economic events. (Selection of important event)

2. Classification of the business transaction (Assets, liability, expenses, income).

3. Measurement in terms (Monetary value transaction.),

4. Recording of business transactions (As per accounting principal)

5. Summarizing the business transaction (Journal, ledger, trial balance and Balance sheet.)

6. Analysis and interpreting the business transactions. (Various reports, ratio etc.)

7. Communication (provide information to internal and external users.)

Users of financial statements:

1. Internal users :- (Owners, shareholders, investors, creditors, employees, customers, management.)

2 External users: - (Regulatory agencies, labor union, stock exchange, public and others)

BRANCHES OF ACCOUNTING

1. Financial accounting (Book Keeping + preparation of financial statement).

2. Cost accounting (Determines the unit cost at different level of production).

3. Management accounting (It blends financial and cost accounting to get maximum profit at maximum cost).

4. Tax accounting (Sales tax and income tax).

5. Social responsibility (Focus on social benefits)

Objectives of Accounting

1. Provides information in systematic way.

2. Enables to get profit or loss of business during certain profit.

3. Shows the actual position of the business.

BASIC ACCOUNTING TERMS

1. Entity:- It means existence of an individual which includes two things 1.Business entity 2. Non business entity.

2. Transactions: - Exchange of goods and services for consideration.

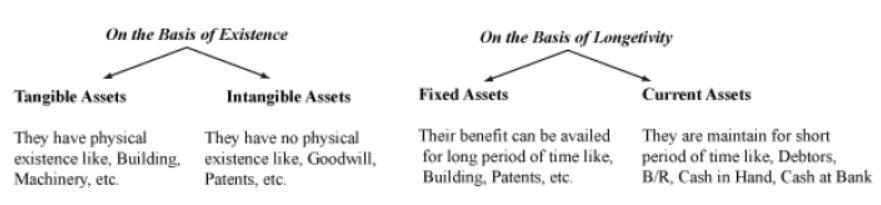

3.Assets:- These are properties or economic resources of an enterprises which can be expressed in monetary terms it can be divided in two parts 1.Fixed assets( more than 1 year period) 2. Current assets(less than 1 year period)

4. Liabilities:-These are certain obligations or dues which firm has to pay.

5. Capital: It is an essential investment for commencement of every business.

6. Sales: It can be credit or cash, in which goods are delivered to customers.

7. Revenues:-It is the amount which is earned by selling of products.

8. Expenses:-It is known as cost of assets consumed or services which used.

9. Expenditure:-It means spending money for some benefit.

10. Profit: - Excess of revenues over expenses is called profit.

11. Gain: - It generates from incidental transaction such as sales of fixed asset, winning of court case.

12. Loss: - Excess of expenses over income is termed as loss.

13. Discount:-It is defined as concession or deduction in price of goods sold.

14. Voucher:-It is known as evidence in support of a transaction.

15. Goods: - It refers all the tangible goods (Raw material, work in progress, finished goods.)

16. Drawings: - Amount of goods or cash which is withdrawn from business for personal use.

17. Purchases: - It means of procurement of goods on credit or cash.

18. Stock: - It is a part of unsold goods. It can be divided into two categories.

1.Opening stock

2. Closing stock.

19 Debtors: - There are persons who owe to an enterprise an amount for buying goods and services on credit.

20. Creditors: - These are persons who have to be paid by an enterprise an amount for providing the enterprise goods and services on credit.

Questions:

Question. Write any two users of financial statements.

Answer: 1.Public 2.Regulatory agencies

Question. Write any one advantage of accounting.

Answer: Provide information in systematic order

Question. Write any one example of voucher.

Answer: cash memo

Question. Write any two examples of current assets.

Answer: 1.Stock 2.Debtor

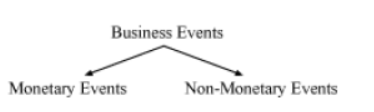

- Business Events – Those events which occur in the normal operation of a business like, sale and purchase of goods are called business events

- Types of Business Events – There are two types of business events.

- Monetary Events – Those business events that can be expressed in monetary terms are called monetary events. These affect the financial position of the business. For example, sale and purchase of goods.

- Non Monetary Events – Those events that cannot be expressed in monetary terms like, recruitment of an employee are called non-monetary events.

NOTE: In accountancy, only monetary events are recorded in the books of account, ignoring the non-monetary events.

- Business Transactions – Those financial transactions or events which are measured and recorded in monetary terms in the books of account are called business transactions. These transactions affect the financial position of an enterprise.

- Accounting– Accounting is an art of identifying, measuring, recording, classifying and summarising the transactions or events (in monetary terms) and analysing and communicating the financial results of business to the various interested parties.

Functions of Accounting

- Identifying the events to be recorded in the books of account

- Measuring the events in the monetary terms

- Recording the financial events in the books of accounts

- Classifying the recorded transaction into their respective groups (accounts) in the ledger (a book having different accounts). The transactions relating to the similar nature are posted under the same head. For example, all cash sales related transactions are recorded in the Sales Account.

- Summarising the classified event in such a manner (Trial Balance, Profit and Loss Account and Balance Sheet) which can be understood by different accounting users without any ambiguity.

- Analysing the summarised data by using different tools of analysis, according to the needs of different users of accounting information

- Communicating the accounting information to various users and the interested parties

Branches of Accounting

Depending on different accounting users’ interests vested in a business, accounting is subdivided into three branches:

- Financial Accounting primarily deals with identifying, recording, summarising the transactions and analysing and communicating the financial results to various users of accounting information.

- Cost Accounting is primarily concerned with estimating the cost of production by ascertaining cost of inputs and accordingly facilitating the pricing policy of the final output of the business. It helps in cost controlling and checking the viability of expenses incurred and reducing cost inefficiencies.

- Management Accounting basically caters to the managerial need of accounting information, i.e. gathering accounting information for the need of the management for designing various policy measures. Cash Flow Statements, Cash Budgeting and Ratio Analysis are the prime tools of Management Accounting.

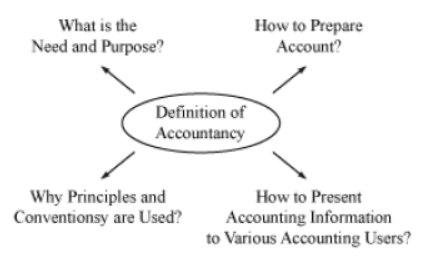

Accountancy

Accountancy is the science or study of accounting. It explains the need and purpose of accounting and also explains various principles and conventions that are used in the accounting process and imparts know-how of preparing accounts and presenting and communicating accounting information in a summarised form to various users of accounting information.

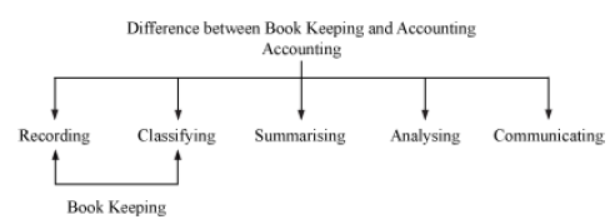

Difference Between Book Keeping and Accounting

- Book Keeping is an art of recording and classifying the transactions in a systematic manner, whereas accounting in addition to Book Keeping also includes summarising,

analyisng and communicating financial results to various interested parties.

Objectives of Accounting

- Recording of transaction in the chronological order

- Ascertaining profit and loss made during an accounting period

- Assessing the financial position of the business

- Communicating the accounting information and financial results to various users

- Locating, rectifying and preventing errors and frauds

- Assessing and analysing the progress of the business by conducting inter-firm and intrafirm comparisons

Advantages of Accounting

- Provides permanent records of transactions Helps in recalling the transactions Assists management to perform various activities like, planning and controlling

- Accounting records can be used as an evidence in the court of law

- Acts as ready source

- of accounting information to various interested parties and users

Limitations of Accounting

- Qualitative aspects like, quality, size, colour, etc. are not revealed by accounting records

- Window dressing (manipulation and misrepresentation) is possible in preparation and presentation of accounts

- Market value of assets are ignored

- Effects of inflation (price change) are ignored in the accounting records Some items like, anticipated losses and profits are based on estimation and past experiences

Accounting Information

Accounting information refers to the accounting data which are presented in such a manner that they are understandable to various accounting users.

Accounting information is in the form of financial statements, financial reports etc.

Qualitative Characteristics of Accounting Information

The accounting information besides being true and fair must also bear the following qualities:

- Reliable – All accounting information must be supported by verifiable evidences.

- Relevance – Accounting information must fulfill the legal requirements and should also disclose the items which are material.

- Understandability – Accounting information should be presented in such a manner that it is easily understood and interpreted without any ambiguity to all users of the accounting information.

- Comparable – Accounting information should be comparable, so that both inter-firm as well as intra-firm comparisons are possible to assess the progress of the business.

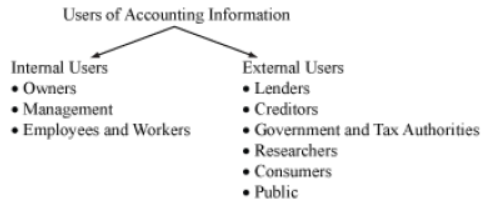

Users of Accounting Information

The parties, organisations and the individuals whose interests are vested in the performance of the business are called users of accounting information. These users can be internal and external users. In order to assess the performance of the business, they rely on the financial statements and other accounting information which are prepared and communicated by the business.

| Internal Users | Interest | Reasons |

| Owners | Return on capital and profit or loss made | To assess the profitability and viability of the capital invested by them in the business. |

| Management | Return on investment, expenditure, assets and liabilities | To draft various policies measures, facilitating planning and decision making process. Also helps the management for cost controlling and to remove inefficiencies. |

| Employees and Workers | Amount of profit earned | Timely payment of wages and salaries, bonus, increment in wages and salaries |

| External users | Interest | Reasons |

| Lenders | Profitability and solvency position | To assess the credit worthiness of the business and ensure timely repayment of loans from the business, |

| Creditors | Liquidity position | Timely repayment of amount lend to the business and ensuring the safety and security of their amount. |

| Future Investors | Return on investment | To ensure the safety of their funds and future returns of their investment. |

| Tax Authorities | Amount of profit earned | To levy tax proportionately to the profit earned. |

| Researcher | Accounting records and data | To conduct various researches. |

| Consumers | Price fixing policy and cost per unit of the product | To know whether the business is charging fair prices. |

| Public | Contribution to social welfare and upliftment projects | Proportion of the profit spent on development and welfare of the society |

Basic Terms in Accounting

- Assets– Assets are the right of ownership of the business on its physical properties (called tangible assets) or on non-physical properties (called intangible assets). Both the rights are measured and recorded in monetary terms in the books of account.

- Classification of Assets

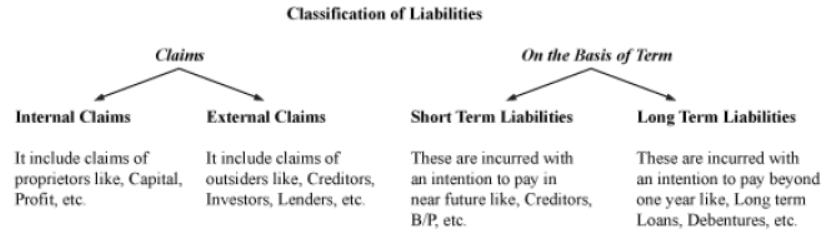

- Liabilities– Those amount which the business is liable to pay are called liabilities. For example, creditors, capital invested by the owner, bank overdraft, etc.

Classification of Liabilities

- Contingent Liabilities – Contingent liabilities refer to the amount that may or may not become liability depending on the outcome of a future event. In other words, these are potential liabilities. These liabilities are not shown in the Balance Sheet, but are shown as footnote of the Balance Sheet.

- Capital – The amount invested (either in form of cash or assets) by the proprietor in the business is called capital. Capital is a liability for the business, as the business is liable to pay back the amount of capital to the proprietor.

- Drawings– The amount withdrawn in cash or in form of other asset like, goods withdrawn from business by the proprietor is called drawings. Drawings reduce the amount of capital of the business.

- Sales– The sale of goods either in cash or in credit are called sales.

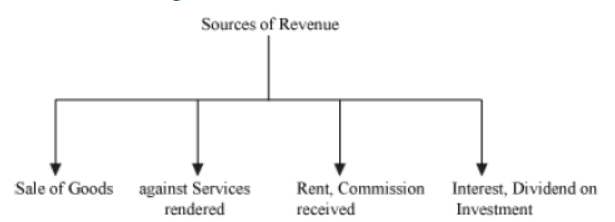

- Revenues– The amount which is either received or receivable from various business operations like, sale of goods, interest, dividend, rent etc. are called revenue.

- Expenses – The amount that are incurred for generating revenue are called expenses.

For example, purchase of goods, payment of wages, etc.

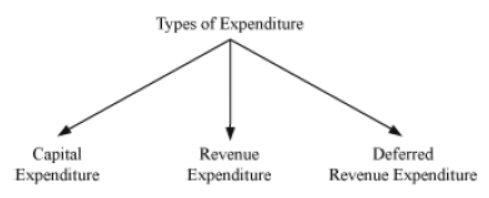

- Expenditure – Amount spent or liabilities incurred for the purchase of goods and services and for acquiring assets are called expenditure. For example, purchase of machinery on credit, or cash is expenditure for the business.

- Capital Expenditure – Expenditures that are incurred for the purchase of fixed assets like, machinery, building, land, etc. are called capital expenditure. This expenditure is of capital nature, as the benefits of these expenditures can be availed for a long period of time.

- Revenue Expenditure – Expenditure that are incurred during a normal operation of business, like rent paid, salaries, are called revenue expenditures. The benefits of this expenditure are availed only for one accounting period.

- Profit – Profit refers to the excess of revenue over its related expense. Algebraically, Profit = Revenue – Expense

- Gain – Gain refers to the profit from non-recurring business transaction. For example, profit on sale of machine of Rs 2,000 is considered as gain, as sale of machine is nonrecurring in nature.

- Loss – Loss refers to the excess of expense over its related revenue. For example, loss on sale of machinery.

Discount – It refers to:

- Deduction in the sale price of goods and services

- Deduction allowed on account of receiving quick payment from the debtors.

Trade discount – Generally this discount is allowed on the list price of the goods from whole seller to retailer or when goods are sold in bulk

Cash Discount – This discount is allowed for spontaneous payment. This discount is allowed only when the payment is made.

Discount Allowed – This discount is allowed when payment from the debtors is received.

Discount Received – This discount is received when payment is made to the creditors.

Voucher – Voucher is an evidential document containing details of a transaction.

Some examples of voucher are bill, receipt, cash memo, etc.

Goods – Those items which are produced or purchased with an intention to sell in the main course of a business are called goods. For example, furniture produced is considered as goods for a furniture company.

Stock – Goods which are held by a firm for the purpose of sale in the normal course of the business are called stock.

Debtors – Persons who owe amount to the business on account of credit sales of goods and services are called debtors.

Creditors – Person to whom business owe amount on account of credit purchases of goods and services are called creditors.

Introduction

According to the American Institute of Certified Public Accountants (AICPA), accounting is defined as the art of systematically recording, grouping, and summarizing financial transactions and events in monetary terms, and then interpreting the resulting data.

The Accounting Principles Board (APB) of AICPA (U.S.A.) describes it as a service-oriented activity designed to deliver quantitative financial details about economic entities, helping stakeholders make informed financial choices.

To put it simply, accounting involves collecting, documenting, grouping, summarizing, and presenting financial information to its users to support sound judgment and decision-making.

Objectives of Accounting

- Maintaining a systematic and complete log of all financial transactions within the books of accounts by adhering to established rules, which helps eliminate omissions and prevent fraud.

- Calculating the exact net profit generated or net loss suffered over a specific financial period to evaluate the enterprise's performance.

- Determining the overall financial health of the enterprise through a Balance Sheet, which displays assets on one side alongside capital and liabilities on the other.

- Supplying relevant accounting details to interested stakeholders such as investors, owners, creditors, banking institutions, employees, and state regulators for their analysis.

- Furnishing the internal management with financial data necessary for effective planning, budgeting, forecasting, and decision-making.

- Shielding the business against fraudulent activities through the regular and disciplined maintenance of accounting records.

Advantages of Accounting

- It arms management with vital financial inputs crucial for administrative decision-making.

- It facilitates year-on-year performance comparisons for owners to identify growth or decline factors.

- It details the financial stability of the enterprise via the Balance Sheet, which contrasts assets against capital and liabilities.

- It ensures systematic records of operations are kept, which are recognized and accepted by courts of law as valid evidence.

- It assists the enterprise in accurately evaluating tax liabilities, including income tax, sales tax, GST, and excise duties.

- It provides a clear track of financial valuation, which helps determine a fair business purchase price during mergers or acquisitions.

Limitations of Accounting

- Accounting is predominantly historical, meaning it reflects past transactions rather than the current real-time valuation of the business. Additionally, financial statements generally overlook the effects of price-level inflation.

- It solely records quantitative data measurable in monetary terms, completely disregarding qualitative aspects like employee morale, management efficiency, and customer satisfaction.

- It is vulnerable to window dressing, where accounts might be manipulated to project a more favorable financial health than what actually exists.

- It is prone to personal bias and subjective judgments, such as selecting depreciation rates or estimating provisions for bad and doubtful debts.

- It relies on rigid accounting conventions and assumptions that can sometimes obstruct realistic disclosures. For instance, assets are typically recorded at historical cost rather than current realizable market value.

Bookkeeping - The Basis of Accounting

Bookkeeping constitutes the primary record-recording stage of accounting, focusing on the systematic and orderly entry of financial events and transactions. It is important not to conflate bookkeeping with the broader scope of accounting. Bookkeeping covers the initial recording phase, whereas accounting encompasses the analytical and summarizing phases of the financial system.

| Bookkeeping | Accounting |

|---|---|

| 1. It is the recording phase of an accounting system. | 1. It is the summarizing phase of an accounting system. |

| 2. It is a primary stage and basis for accounting. | 2. It is a Secondary Stage which begins where the Bookkeeping process ends. |

| 3. It is routine in nature and does not require any special skill or knowledge. | 3. It is analytical in nature and requires special skill or knowledge. |

| 4. It is done by junior staff called bookkeepers. | 4. It is done by senior staff called accountants. |

| 5. It does not give the complete picture of the financial conditions of the business unit. | 5. It gives the complete picture of the financial conditions of the business unit. |

Types of Accounting Information

- Earnings Data: Details on profitability found within the Income Statement (Profit and Loss Account), highlighting the net operational results of a specific period.

- Financial Status Data: Insights into the firm's assets, capital, and liabilities presented through the Balance Sheet.

- Explanatory Notes: Detailed schedules, disclosures, and notes that clarify individual items on the balance sheet and income statement.

Branches or Subfields of Accounting

- Financial Accounting: The branch focused on systematically tracking, recording, and summarizing monetary transactions to calculate periodic profit/loss and present the financial health of the business to external stakeholders.

- Cost Accounting: The subfield dedicated to analyzing, tracking, and controlling the total and per-unit costs of manufacturing goods or delivering services.

- Management Accounting: The branch that processes and presents accounting data tailored specifically for internal managers to assist in planning, controlling, and operational decision-making.

Qualitative Characteristics of Accounting Information

- Reliability: Financial information must be factual, verifiable via source documents, and free from errors or personal bias.

- Relevance: The data must be timely and directly influence users' decisions by helping them evaluate past, present, or future events.

- Understandability: Information must be structured and presented in a clear, comprehensible manner for users who possess a basic knowledge of business.

- Comparability: Accounting disclosures must allow users to track performance over time (inter-period) and compare results against other enterprises (inter-firm).

Basic Accounting Terms

- Entity: Refers to a business unit or organization that possesses a distinct, independent existence (e.g., a partnership, sole proprietorship, or corporation).

- Transaction: An economic event involving an exchange of value between two or more independent entities.

- Assets: Economic resources or properties owned by a business that have monetary value and can yield future benefits, classified broadly into Non-Current (Fixed) Assets and Current Assets.

- Liabilities: Financial obligations or debts that a business owes to external parties, categorized into Long-term (Non-Current) Liabilities and Short-term (Current) Liabilities.

- Capital: The initial investment, either in cash or assets, made by the owners or partners to start and run the business enterprise.

- Sales: The total revenues generated by selling goods or rendering services to clients, consisting of both cash and credit sales.

- Revenues: The gross inflows of cash, receivables, or other consideration arising from the ordinary activities of an enterprise (like sales, interest, dividends, etc.).

- Expenses: The costs incurred by an enterprise in the process of generating revenue (such as salaries, rent, and utility bills).

- Expenditure: Any payment made or liability incurred to acquire assets, goods, or services. It is divided into Capital Expenditure (long-term benefits) and Revenue Expenditure (short-term benefits).

- Profit: The positive residual amount when total revenues exceed total matched expenses within an accounting year.

- Gain: A non-operating, monetary benefit or profit resulting from secondary transactions or events (such as the sale of a fixed asset or winning a court case).

- Loss: This term refers to either the negative net income of a period (where total expenses exceed total revenues) or an asset write-off from which no economic benefit is received (such as damage from fire or theft).

- Discount: A reduction allowed in the list price of goods, which is categorized into Trade Discount (given at the time of sale) and Cash Discount (given to encourage prompt payment).

- Voucher: The primary documentary evidence, such as a bill or receipt, that supports and validates a business transaction.

- Goods: Tangible commodities, merchandise, or products in which the business enterprise regularly trades or manufactures for sale.

- Drawings: Any withdrawal of cash or goods from the business by the owner for their personal or domestic use.

- Purchases: The total value of goods procured by an enterprise, whether on cash or credit, specifically meant for resale or manufacturing.

- Stock: The value of raw materials, work-in-progress, or finished goods remaining unsold or unused with a business at a given point in time.

- Debtors: Individuals or customer entities who owe money to the business for goods purchased or services rendered to them on credit.

- Creditors: Suppliers or other entities to whom the business owes money for goods or services purchased on credit.

Please click the link below to download pdf file for CBSE Class 11 Accountancy Introduction To Accounting Notes.

Free study material for Accountancy

CBSE Class 11 Accountancy Chapter 1 Introduction to Accounting Notes

Students can use these Revision Notes for Chapter 1 Introduction to Accounting to quickly understand all the main concepts. This study material has been prepared as per the latest CBSE syllabus for Class 11. Our teachers always suggest that Class 11 students read these notes regularly as they are focused on the most important topics that usually appear in school tests and final exams.

NCERT Based Chapter 1 Introduction to Accounting Summary

Our expert team has used the official NCERT book for Class 11 Accountancy to design these notes. These are the notes that definitely you for your current academic year. After reading the chapter summary, you should also refer to our NCERT solutions for Class 11. Always compare your understanding with our teacher prepared answers as they will help you build a very strong base in Accountancy.

Chapter 1 Introduction to Accounting Complete Revision and Practice

To prepare very well for y our exams, students should also solve the MCQ questions and practice worksheets provided on this page. These extra solved questions will help you to check if you have understood all the concepts of Chapter 1 Introduction to Accounting. All study material on studiestoday.com is free and updated according to the latest Accountancy exam patterns. Using these revision notes daily will help you feel more confident and get better marks in your exams.

FAQs

You can download the teacher prepared revision notes for CBSE Class 11 Accountancy Introduction To Accounting Notes from StudiesToday.com. These notes are designed as per 2026-27 academic session to help Class 11 students get the best study material for Accountancy.

Yes, our CBSE Class 11 Accountancy Introduction To Accounting Notes include 50% competency-based questions with focus on core logic, keyword definitions, and the practical application of Accountancy principles which is important for getting more marks in 2026 CBSE exams.

Yes, our CBSE Class 11 Accountancy Introduction To Accounting Notes provide a detailed, topic wise breakdown of the chapter. Fundamental definitions, complex numerical formulas and all topics of CBSE syllabus in Class 11 is covered.

These notes for Accountancy are organized into bullet points and easy-to-read charts. By using CBSE Class 11 Accountancy Introduction To Accounting Notes, Class 11 students fast revise formulas, key definitions before the exams.

No, all study resources on StudiesToday, including CBSE Class 11 Accountancy Introduction To Accounting Notes, are available for immediate free download. Class 11 Accountancy study material is available in PDF and can be downloaded on mobile.