Read and download the CBSE Class 12 Accountancy Accounting for Share Capital VBQs Set 01. Designed for the 2026-27 academic year, these Value Based Questions (VBQs) are important for Class 12 Accountancy students to understand moral reasoning and life skills. Our expert teachers have created these chapter-wise resources to align with the latest CBSE, NCERT, and KVS examination patterns.

VBQ for Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital

For Class 12 students, Value Based Questions for Part 2 Chapter 1 Accounting for Share Capital help to apply textbook concepts to real-world application. These competency-based questions with detailed answers help in scoring high marks in Class 12 while building a strong ethical foundation.

Part 2 Chapter 1 Accounting for Share Capital Class 12 Accountancy VBQ Questions with Answers

Very Short Answer Type Questions:

Question. State in brief, the SEBI guidelines regarding Debenture Redemption Reserve(DRR).

Answer : As per SEBI guidelines, an amount equal to 50% of the debenture issue, must be transferred to DRR before the redemption begins.

Question. X ltd. was formed with a capital of Rs. 500,000 divided into shares of Rs. 10 each out of these 2000 shares were issued to the vendors as fully paid as purchase consideration for a building acquired, 1000 shares were issued to signatories to the memorandum of association as fully paid. The directors offered 6500 shares to the public and called up Rs. 6 per and received the entry called up amount on share allotted. Show these transaction in the Balance sheet of a company.

Answer : Issued Capital Rs. 95000.

Question. As per latest guidelines governing the servicing of debentures a company is required to create on special account. Name that account.

Answer : Debenture Redemption Reserve Account.

Question. Sonu Ltd. company issued 15,000 shares of Rs. 10 each. Payment on there shares is to be made as follows:

On application Rs. 4 ( 1st Feb, 2003)

On allotment Rs. 3 (1st April, 2003)

On final call Rs. 3 (1st May, 2003)

Rakesh to whom 1000 shares were allotted paid the full amount on application and mohan to whom 200 shares were allotted paid the final call money on allotment. Interest @ 6% was paid on 1st May, 2003. Pass necessary journal entries.

Answer : Interest on Calls in advance = 15 + 3 = Rs. 18

Question. Name the method of redemption of debentures in which there is no requirement of creating Debenture Redemption Reserve.

Answer : Redemption of debentures by conversion.

Question. Why securities premium money can not be used for payment of cash dividend among shareholders?

Answer : It is restricted under section 78 of Indian Companies Act.

Question. 500 shares of Rs. 100 each issued at a discount of 10% were forfeited for the non-payment of allotment money of Rs. 50 per share. The first and final call of Rs.10 per share on these shares were not made. The forfeited shares were reissued at Rs. 80 per share fully paid-up.

Answer : Capital Reserve Rs. 10,000

Question. Gupta Ltd has incurred a loss of Rs. 8,00,000 before payment of interest on debentures. The directors of the company are of the opinion that interest on debentures is payable only when company earn profit. Do you agree?

Answer : No’ because Interest on debentures is a charge against profit and not an appropriation of profit.

Question. State with reason whether a company can issue its shares at a discount in its Initial Public Offer (IPO).

Answer : Section 79 Companies Act- the shares must be of a class already issued. So a company cannot issue shares at a discount in its Initial Public Offer.

Question. 200 shares of Rs. 100 each issued at a discount of 10% were forfeited for the non payment of allotment money of Rs. 50 per share. The first and final call of Rs. 10 per share on these shares were not made. The forfeited share were reissued at Rs. 14 per share fully paid up.

Answer : Capital Reserve Rs. 600

Question. Can a company issue shares at a premium in the absence of any express authority in its articles?

Answer : Yes. [ Hint See section 78]

Question. 800 Shares of Rs. 10 each issued at per were forfeited for the non-payment of final call of Rs. 2 per share. These shares were reissued at Rs. 8 per share fully paid-up.

Answer : Capital Reserve Rs. 4,800.

Question. A company forfeited 240 shares of Rs. 10 each issued to raj at a a premium of 20%. Raman had applied for 300 shares and had not paid anything after paying Rs 6 per share including premium on application. 180 shares were reissued at Rs. 11 per share fully paid up. Pass journal entries relating to forfeiture and reissue of shares.

Answer : Capital Reserve Rs. 990.

Question. Krishna Ltd. With paid-up share capital of Rs. 60,00,000 has a balance of Rs. 15,00,000 in securities premium account. The company management does not want to carry over this balance. You are required to suggest the method for utilizing this premium money that would achieve the objectives of the management and maximize the return to shareholders.

Answer : Mention the provisions of section 78.

Question. What is the restriction on reissue of forfeited shares at discount?

Answer : A Company can reissue forfeited shares at a discount not more than amount forfeited on these shares.

Question. What is the nature of receipt of premium on issue of shares?

Answer : Capital Nature.

Question. Distinguish between a share and a Debenture.

Answer : Basis of difference :

(i) Ownership

(ii) Return

(iii) Voting Right

(iv) Convertibility

Question. Can share premium be utilised for the purchase of fixed assets?

Answer : No.

Question. What is the maximum rate of interest which the board of directors of a company can normally pay on calls-in-advance if the articles are silent on the matter of such interest?

Answer : According to table ‘A’ not exceeding 6 % p.a.

Short Answer Type Questions:

Question. Which companies are exempted from the obligation of creating DRR by SEBI?

Answer : The following companies are exempted from the obligation of creating DRR –

(i) A company which has issued debentures with a maturity of 18 months or less.

(ii) Infrastructure companies, which are wholly engaged in the business of developing, maintaining and operating infrastructure facilities.

Question. X Ltd. issued 20,000 shares of Rs. 10 each at a premium of 10% payable as follows:-

On application Rs. 2 ( 1st Jan 2001), on allotment Rs. 4 (including premium) (1st April 2001), On first call Rs. 3 (1st June 2001), on second call & final call Rs. 2 (1st Aug. 2001).

Application were received for 18,000 shares and the directors made allotment in full. One shareholder to whom 40 shares were allotted paid the entire balance on his share holdings with allotment money and another shareholder did not pay allotment and 1st call money on his 60 shares but which he paid with final call.

Calculate the amount of interest paid and received on calls-in-advance and calls-in-arrears respectively on 1st Aug. 2001.

Answer : Interest on Calls in advance Rs. 2.80

Interest on Calls in arrears Rs. 5.50

Question. X Ltd. invited applications for 11,000 shares of Rs. 10 each issued at 10% premium payable as:

On application Rs. 3 (including Rs. 1 premium)

On allotment Rs. 4 (including Rs. 1 premium)

On 1st Call Rs. 3

On 2nd & final call Rs. 2

Application were received for 24000 shares.

Category I : One fourth of the shares applied for allotted 2000 shares.

Category II: Three fourth the shares applied for allotted 9000 shares.

Remaining applicants were rejected. Mr. Mohan holding 300 shares out of category II failed to pay allotment and two calls and his shares were re issued @ Rs. 11 fully paid-up. Pass necessary journal entries.

Answer : Hint-

(i) Amount received on allotment Rs. 26,100.

(ii) Amount transferred to share forfeited A/C Rs. 900

(iii) Amount transferred to Capital Reserve Rs. 600.

Question. On 01-04-1999, A Ltd., issued 2000, 7% debentures of Rs. 100 each at a discount of 10% redeemable at par after 4 years by converting them into equity shares of Rs. 100 each issued at a premium of 25%.

Pass journal entries in the following cases:

(i) If debentures are redeemed on maturity.

(ii) If debentures are redeemed before maturity.

Answer : Case (i) – No. of Equity shares to be issued 1,600.

Case (ii) – No. of Equity shares to be issued 1,440.

Question. The following balance appeared in the books of Z Ltd. on January 1, 2004.

12% Debentures A/C Rs. 1,50,000

Debenture Redemption Fund Rs. 1,25,000

Debenture Redemption Fund Investment Rs. 1,25,000

(Represented by Rs. 1,47,500, 3% Govt. Securities)

The annual installment added to the fund is Rs. 20,575. On December 31, 2004, the bank balance after the receipt of interest on investment was Rs. 39,100. On that date all the investment were sold at 83% and the debentures were duly redeemed. Show the necessary ledger accounts for the year 2004.

Answer : Hint : (i) Loss on sale of investment Rs. 2575.

(ii) Amount transferred to General Reserve Rs. 1,47,425.

Question. Virani Industries Ltd. issued 1,00,000, 10% Debentures of Rs. 10 each at a discount of 9% on April 1st, 2001 redeemable as follows:

31st March 2003 - 20,000 Debentures

31st March 2004 - 30,000 Debentures

31st March 2005 - 20,000 Debentures

31st March 2006 - Remaining Debentures

Calculate the amount of discount to be written off each year and prepare discount on issue of debentures account.

Answer : Amount of discount = Rs. 90,000

Discount to be written off:

2001-02 - Rs. 25,000

2002-03 - Rs. 25,000

2003-04 - Rs. 20,000

2004-05 - Rs. 12,500

2005-06 - Rs. 7,500

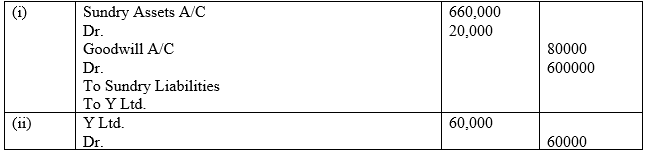

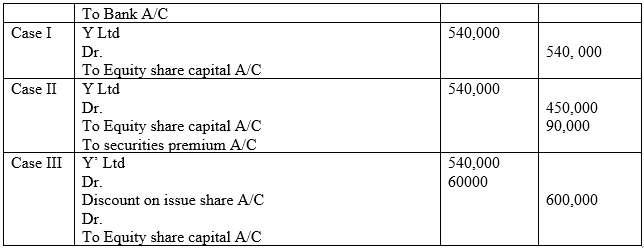

Question. X Ltd took over the assets of Rs. 6,60,000 and liabilities of Rs. 80,000, Y Ltd for Rs. 600,000. Show the necessary journal entries in the book of X Ltd. assuming that

Case-I : The consideration was payable 10% in cash and the balance in 54000 equity shares of Rs. 10 each.

Case-II : The consideration was payable 10% in cash and the balance in 45000 equity shares of Rs. 10 each.

Case-III : The consideration was payable 10% in cash and the balance in 60,000 equity shares of Rs. 10 each.

Answer : Solution:-

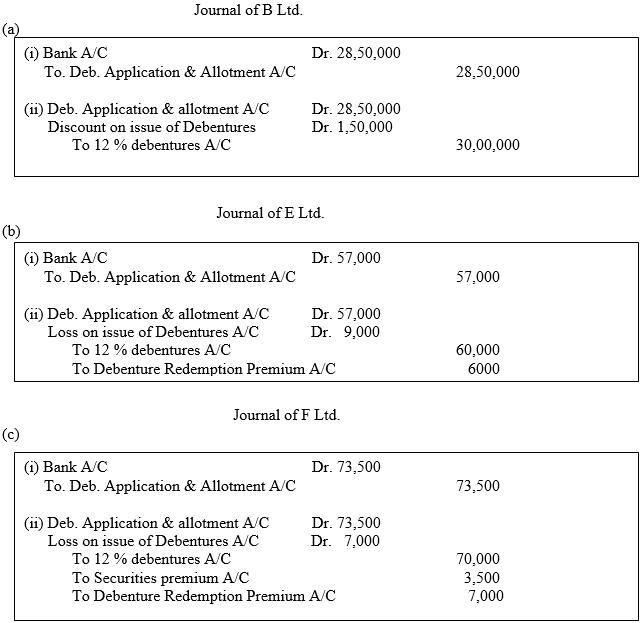

Question. Pass journal entries for the following at the time of issue of debentures:

(a) B Ltd. issues 30,000, 12% Debentures of Rs. 100 each at a discount of 5 % to be repaid at par at the end of 5 years.

(b) E Ltd. issues Rs. 60,000, 12% Debentures of Rs. 100 each at a discount of 5 % repayable at a premium of 10% at the end of 5 years.

(c) F Ltd. issues Rs. 70,000, 12% Debentures of Rs. 100 each at a premium of 5 % redeemable at 110%.

Answer :

Question. On 1st July 2007. A Ltd gave notice of their intention to redeem their outstanding Rs. 400,000 8% Debentures on 1st January, 2008 @ rs. 102 each and offered the holders the following options-

(a) To subscibe for (i) 6% cumulative preference shares of Rs. 20 each at Rs. 22.50 per share, accepted by debenture holders of Rs. 1,71,000 or (ii) 12% debentures were issued @96% accepted by the holders of Rs. 1,44,000 Debentures.

(b) Remaining debentures to be redeemed for cash if neither of the option under (a) was accepted. Pass necessary journal entries.

Answer : Hints-

(1) Case a (i) – No. of preference shares issued 7752.

(2) Case a (ii)- No. of debentures issued 1530.

(3) Remaining 85000 debentures paid in cash.

Question. TPT Ltd. invited applications for issuing 1,00,000 equity shares of Rs. 10 each at a premium of Rs. 3 per share. The whole amount was payable on application. The issue was over subscribed by 30,000 shares and allotment was made on pro-rata basis. Pass necessary journal entries in the books of the company.

Answer : (i) Dr. Bank A/C Rs. 16,90,000, Cr.Eq.share Application A/C Rs. 16,90,000.

(ii) Dr.Eq.Share Application A/C Rs. 16,90,000, Cr.Eq. share Capital A/C Rs.10,00,000, Cr. Security premium A/C Rs. 300,000, Cr. Bank A/C Rs. 3,90,000.

Partnership – Fundamentals

Values are the significant and fundamental dimensions of human life and indicate how one adheres, attaches and reacts in life situations or circumstances. They are the blue prints or action plan which orient and decide the thinking, action feelings and behavior itself.

• Values does not mean going back to the superstitions but to bring in harmony with the present social and cultural conditions,

which are acceptable to the society.

• Values Cannot be scientifically investigated or proven

• Values affect how we practice

CORE VALUES OF A BUSINESS:

• Accountability- Responsibility of our actions that influence the lives of our customers and fellow workers.

• Balance- Maintaining Healthy life and work balance for workers.

• Collaboration-Collaborating within and outside the company to give the best.

• Commitment- Commitment to roll great product, service and other initiatives that impact lives both within and outside the organization.

• Community- A sense of responsibility and contribution to society that define our existence.

• Consistency- Be consistent in offering the best for wonderful experience.

• Diversity- Respecting the diversity and giving the best of the composition.

• Efficiency- Being efficient and effective in our approach to give best solution each time.

• Empowerment- Empowering the employees to take initiative and give the best.

• Fun- Having fun and celebrating small successes in our journey to achieve big.

• Innovation- To come out with new creative ideas that have the potential to change the world.

• Integrity-To act with honesty and integrity without compromising the truth.

• Leadership- The courage to lead from front and shape future.

• Ownership- Taking ownership of the company and customer success.

• Passion-Putting the heart and mind in the work to get the best.

• Quality-Giving the best and unmatched results for all round satisfaction.

• Respect-Giving due respect to self and others and maintain the environment of team work and growth.

• Risk Taking- Encouraging self and others to take risk for a bright future.

• Safety- Ensuring the safety of people and making sure to give them trouble free experience.

• Service Excellence- Giving the best and world class service and achieving excellence each passing day.

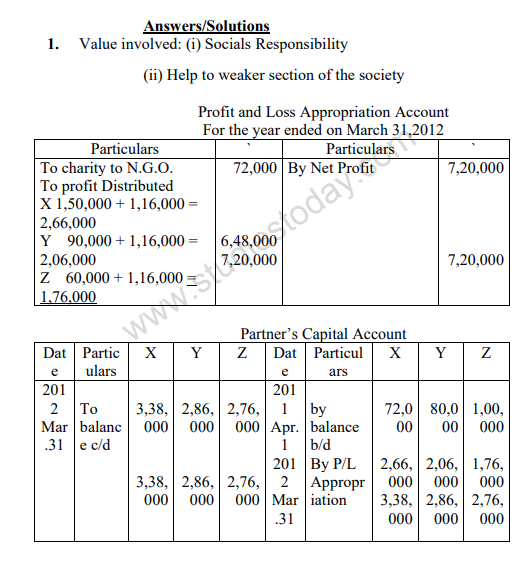

Question. X, Y and Z are partners with ₹ 72,000, ₹ 80,000 and ₹ 1,00,000 as their capitals respectively. The profit for the year ending March 31, 2012 was ₹ 7,20,000. Before distributing profits they donated 10% of profits to a 'Non-Govt. organization‘ as charity for welfare of educationally backward section of the society. Out of the remaining profit, ₹4,00,000 is divisible as 5:3:2 ratio and the remaining is to be divided amongst them equally.

Answer :

Identify the value involves by the partnership form of X,Y and Z. Prepare Profit and Loss appropriation Account and partner‘s Capital Account.

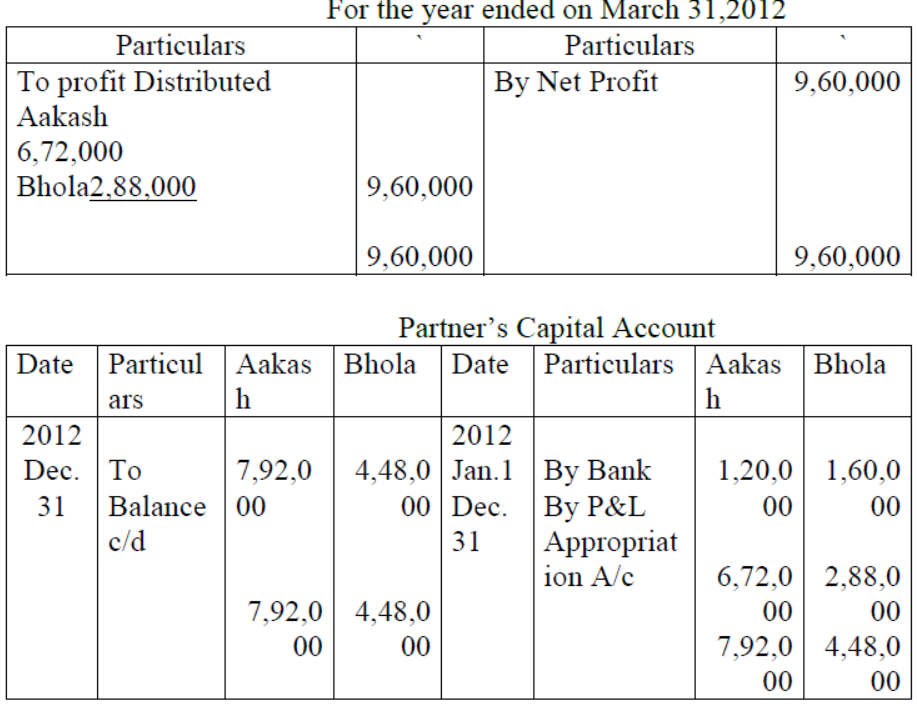

Question. Aakash and Bhola entered into partnership on January 1, 2012 contributing ` 1,20,000 and ` 1,60,000 as capitals respectively. Their partnership firm started the business of manufacturing shoes They decided to allow a discount of 30% on shoes for school going children. They share profits in the ratio of 7:3. The profits for the year were ` 9,60,000. Prepare Profit and Loss Appropriation Account and the partner‘s Capital Accounts. Also identify the value involved in this question.

Answer: Values : (i) Motivation to school going children

(ii) Help to increase the literacy rate.

Profit and Loss Appropriation Account

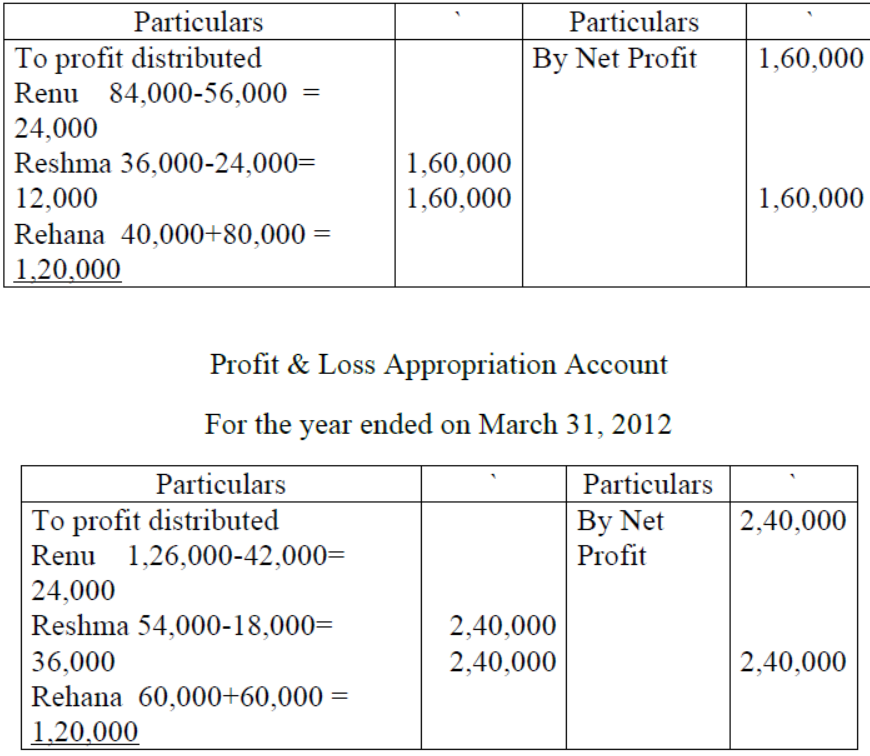

Question. Renu and Reshma shared profits as 7:3. Renu want to give admission to her friend Rehana as a new partner. Reshma agrees with this decision of Renu. Rehana is a physically challenged lady and admitted with a ¼th share in profits. Renu and Reshma gave her a guarantee that her share of profit will never be less than 1,20,000 p.a., the profits for the last two years ended March 31,

2011 and March 31, 2012 were ` 1,60,000 and ` 2,40,000 respectively. Identify the human value involved in this case and prepare Profit and Loss Appropriation Account for the two years.

Answer : Value involved:

(i) Good relations between persons of different religions.

(ii) Women empowerment

(iii) Welfare of differently abled persons.

(iv) Protection of the interest of differently abled

(v) National integration

Profit & Loss Appropriation Account

For the year ended on March 31, 2011

Question. Ramesh and Gurmeet are two friends belonging to Hindu and Sikh religion respectively. They started a business of wire manufacturing in the form of a partnership firm. They know that the factory of wire manufacturing pollutes the environment. Therefore there are two options available before them. First option is that the factory can be opened in rural area where local residents are poor and illiterate. Second option is that an advanced pollution control plant can be installed in their factory to control the pollution. They decided to choose the second option which involves an additional cost of ` 2, 00,000. To arrange this amount, they admitted their fast friend John as a new partner for equal share in the future profits.

John brought` 2,50,000 as his share of capital. Ramesh and Gurmeet gave him a guarantee that his share of profit will not be less than ` 60,000 p. a. At the end of first year the firm earns a profit of ` 1,50,000. Mention the value involved in this question. Write the effects of choosing option available before Ramesh and Gurmeet. Prepare the Profit and Loss Appropriation Account for the first year.

Answer : Value involved:

(i) Good relations between different religions

(ii) National integration

(iii) Development of minorities

(iv) Awareness about pollution control

(v) Use of advanced technology

Profit & Loss Appropriation Account

For the year ended on _ _ _ _ _ _ _ _ _

Question. A, B and C are in a partnership. A is appointed for carrying on the business of the firm by the other partners. A has decided to purchase the goods from a firm in which his wife and his son are partners at a double rate then the prevailing market rate without disclosing this fact to others partners of the firm.

State which values have been violated by A by not disclosing this information to B and C.

Answer : As A is working on behalf of the other partners, it is his moral duty to work for the benefit of the firm and not to earn any undisclosed profits.

By ignoring the interests of the firm and favoring his wife and son, A

has violated the following values:

• Honesty

• Integrity

• Truth

• Breach of mutual trust

Question. A, B and C are partners in a firm. C used firm‘s money to buy shares without disclosing it other partners. Which value C is violating and what will be the treatment of profit earned by C?

Answer : C has violated the following values:

• Honesty

• Integrity

• Truth

• Breach of mutual trust

C will have to return firm‘s money alongwith any profits earned.

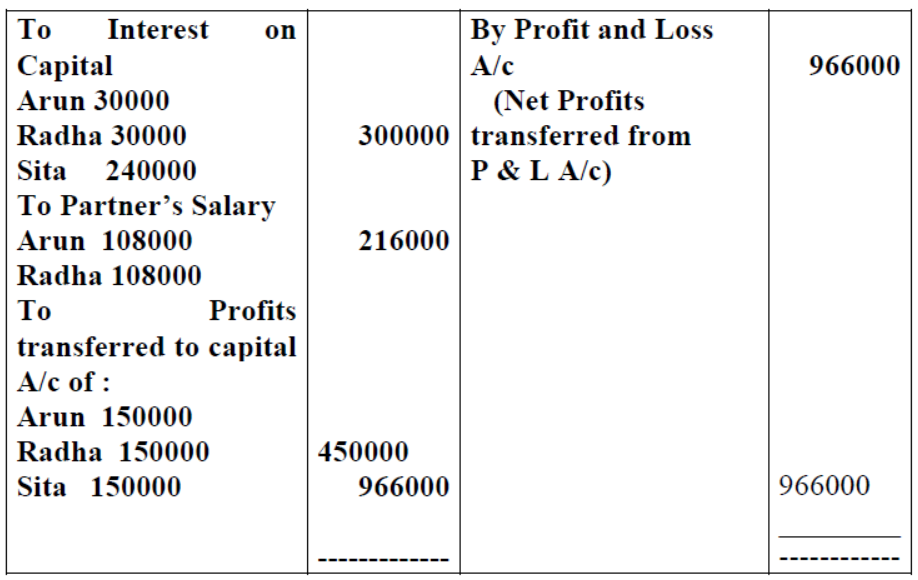

Question. After completing MBA, Arun and Radha want to start a new business but they don‘t have sufficient capital. They contacted their common friend Sita, a rich lady with low vision. They decided to form a partnership firm with a capital of Rs.25,00,000 with a ratio of 80% by Sita, 10% each by Arun and Radha respectively. The partnership deed provided as follows:-

• Interest on capital @12% p.a.

• Salary to active partners Arun and Radha @ 9,000 p.m. The firm earned a net profit of 9,66,000 during the year. Sita decided to donate half of her profits to a school for differently abled children. State which values are being reflected in the above case and also prepare Profit and loss appropriation a/c for the year.

Answer : Following values are being reflected :-

• Sensitivity towards differently abled individuals.

• Empowering women entrepreneurship.

• Efficient utilization of surplus funds.

• Mutual trust and co-operation

Profit and Loss Appropriation Account

For the year ending on

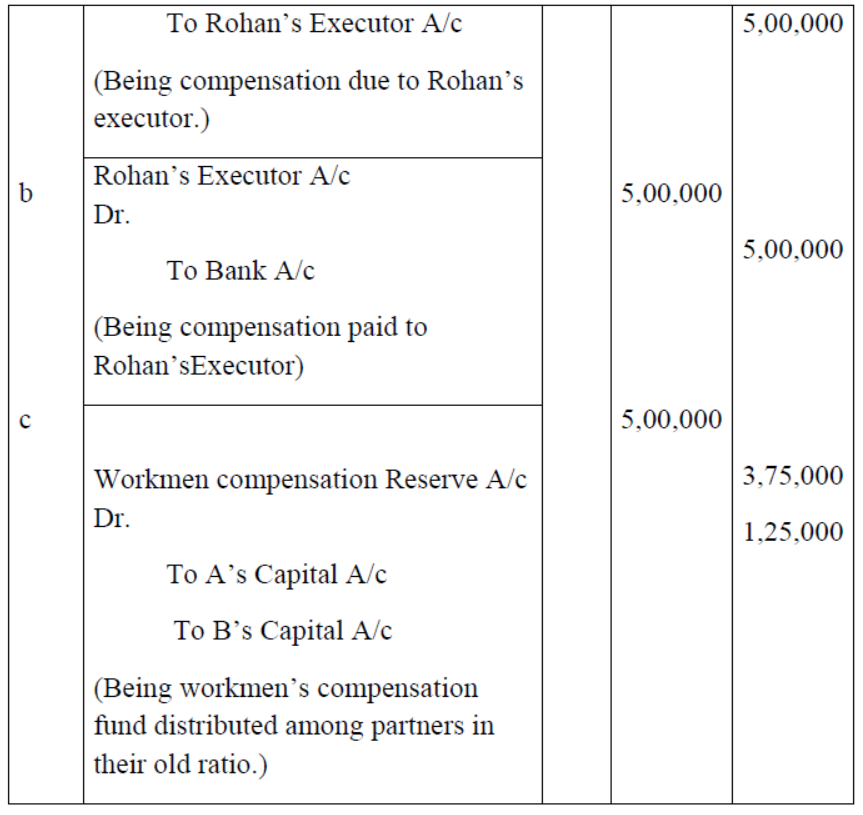

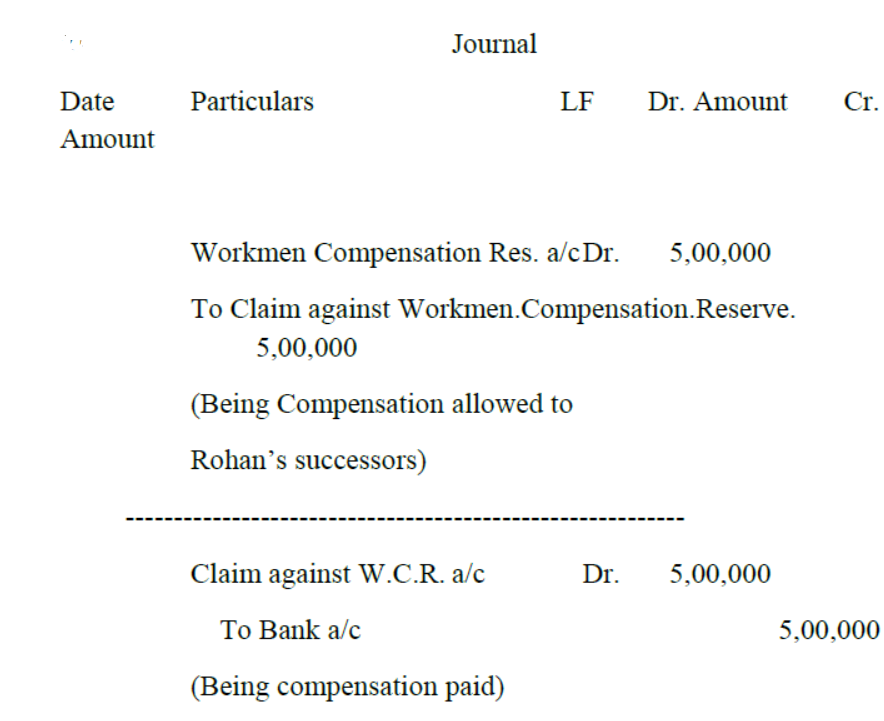

Question. A and B are partners in a firm having a workmen compensation reserve of 10,00,000. A worker, Rohan died in an accident while working for the firm. The firm paid 500,000 as compensation to his family and offered a job to his wife and also arranged for the education of his son. State which values are being reflected in the above case and also show the treatment of workmen compensation reserve if A and B now decide to change their profit haring ratio from 3:1 to equal ratio. Workmen compensation reserve will not be shown in the books of new firms.

Answer : Following values are being reflected :-

• Mutual trust and co-operation

• Fulfillment of social responsibility

• Sympathy

Question. A and B are partners in a firm. A manages all business as a representative of firm. For execution of a sales order to a valuable customer A incurred ` 5,000 for delivery in quick time. B is not agreeing to reimburse the above expenses from the firm‘s accounts.

Explain the treatment of above expense and describe which value is violatedby the partners.

• What are the values involved in the formation of a partnership firm?

Answer : It is the right of A to get indemnified against the payment which he paid for the firms business.

B violated the following values:

• Mutual trust and co-operation

• Integrity

• Truth

• Acknowledgement

Question. What are the values disclosed by a Partnership Deed?

Answer : Values

1. Unity

2. Pooling of Resources

3. Efficient use of resources

Question. In the absence of partnership deed, interest on Advances/Loan by a partner is to be paid @ 6% p.a. What value is depicted in this provision of Indian Partnership Act, 1932?

Answer : Values:

1. Transparancy

2. Evidence

3. Awareness

Question. A and B are partners in a firm. A manages all business as a representative of firm. For execution of a sales order a valuable customer A incurred Rs. 5,000 for delivery in quick time. B does not agree to reimburse the above expenses from the firm‘s accounts. Explain the treatment of above expense and describe which value is violated by the partners.

Answer : It is the right of A to get indemnified against the payment which he paid for the firms business. B violated the following values:

• Mutual trust and co-operation

• Integrity

• Truth

• Acknowledgement

Question. A, B and C are partners in a firm. C used firm‘s money to buy shares without disclosing it to other partners. Which value C is violating and what will be treatment of profit earned by doing so?

Answer : C has violated mutual trust/honesty. Firm‘s money will be refunded to the firm along with profits earned. In case there is any loss through this transaction it will be borne by the partner himself.

Question. A and B are partners in a firm having workmen compensation reserve of Rs.10, 00,000. A worker, Rohan, died with an accident. The firm paid his successors Rs.5, 00,000 and gave employment to his wife and arranged for his child education.

Which values are being indicated in the question and what will be the treatment of workmen compensation reserve if A and B decide to change their profit sharing ratio from 3:2 to 2:3

Answer :

B‘s Capital a/c Dr. 1,00,000

To A‘s Capital a/c 1,00,000

(Being adjustment made due to changes

In profit-sharing ratio)

Working notes:

B‘s Gaining ratio = New ratio-old ratio 3/5-2/5 =1/5

A‘s Sacrificing ratio = Old ratio-New ratio 3/5-2/5 =1/5

Adjustment for workmen compensation reserve 1/5 of Rs.5,00,000i.e

Rs.1,00,000.

Values involved—

1 Gratitute towards employees.

2.Promoting education

3.Concern for family

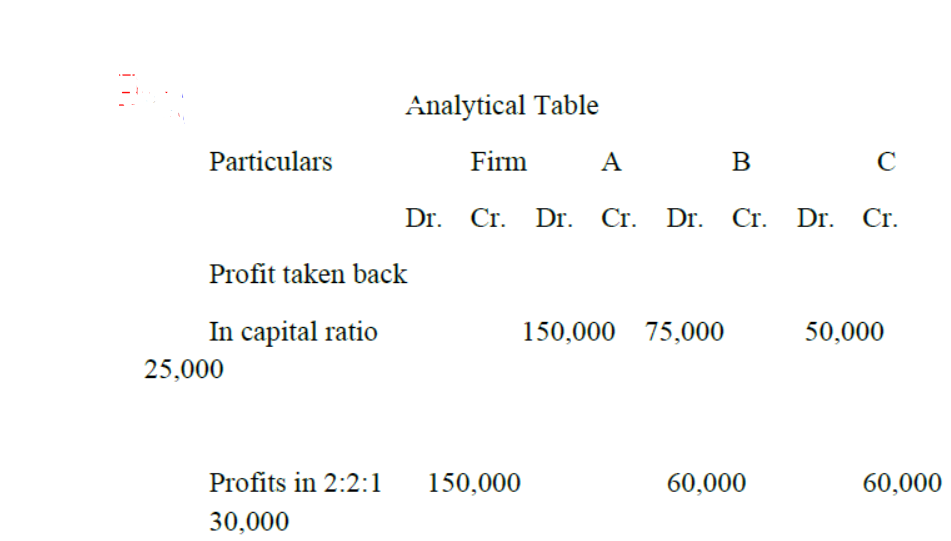

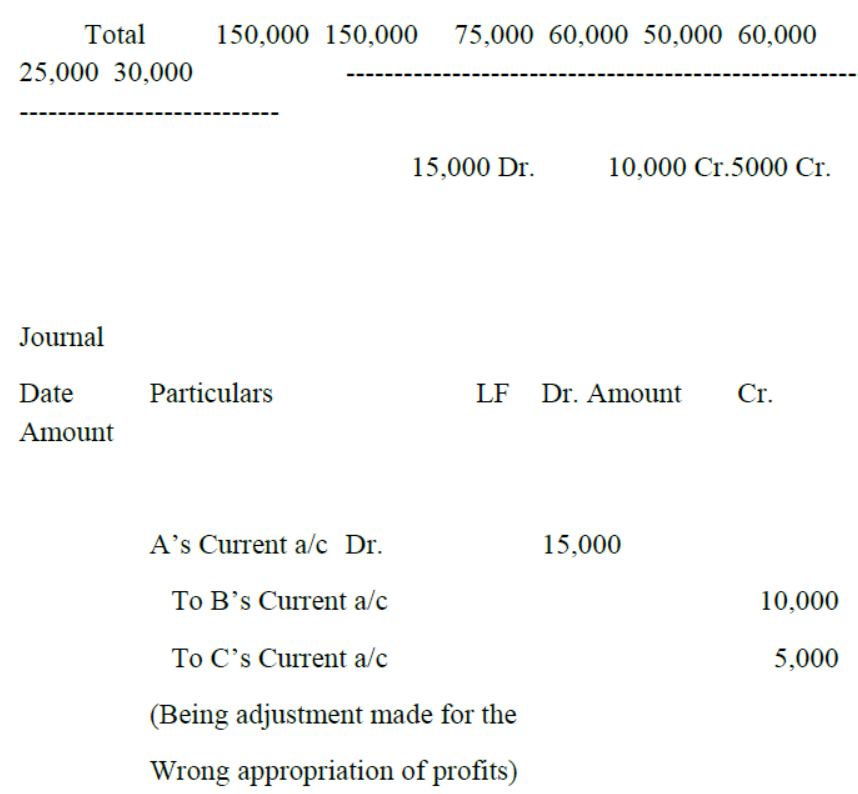

Question. A, B and C are partners in a firm having fixed capital of Rs.5lacs, 3lacs and 2lacs respectively. Firm earned profits of Rs.1, 50,000 during the year ending 31st march, 2011. These profits were divided in capital ratio instead of 2:2:1.

Answer :

Values involved-

1.Admitting mistakes

2.Rectifying one‘s mistakes

Reconstitution of Partnership- Admission of Partner

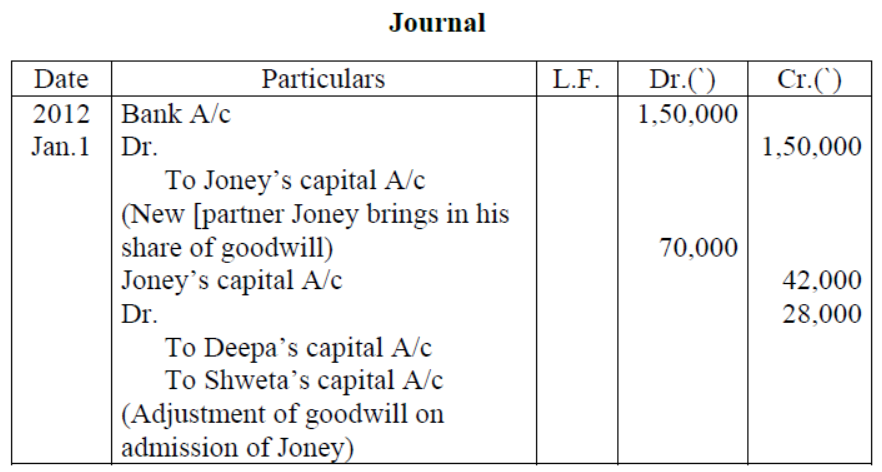

Question. Deepa and Shweta are friends and after completion of their study they started a business of readymade Garments by constituting a partnership firm with a profit sharing ratio as 3:2 respectively.

Their partnership firm earns huge profits during few years. They decided to start a scholarship of ` 10,000 p.a. for meritorious and poor students. On January 1, 2012 they admit Joney, their manager as a new partner with 1/5th share in future profits. The value of goodwill of the form is ` 3,50,000 and Joney is not able to bring his share of goodwill in cash. Joney belongs to a Religious minority community and isexpert in business management. He contributes ` 50,000 as his capital and old partners want to pass an adjusting entry for the treatment of goodwill.

Identify the value is involved in this question and pass the journal entries on admission of Joney. Also calculate the new profit sharing ratio.

1. Value involved: (i) Socials Responsibility

(ii) Help to weaker section of the society

Profit and Loss Appropriation Account

For the year ended on March 31,2012

Answer : Value involves:

(i) Women entrepreneurship

(ii) Women empowerment

(iii) Contribution for welfare of poor students

(iv) Welfare of minorities

(v) National integration

Deepa Shweta

3 2

Share of new partner Joney = 1/5

Remaining share for Deepa and Shweta = 1-1/5 = 4/5

New share of Deepa = 4/5*3/5 = 12/25

New share of Shweta = 4/5*2/5 = 8/25

Share of Joney = 1/5*5/5 = 5/25

New ratio = 12:8:5

Journal

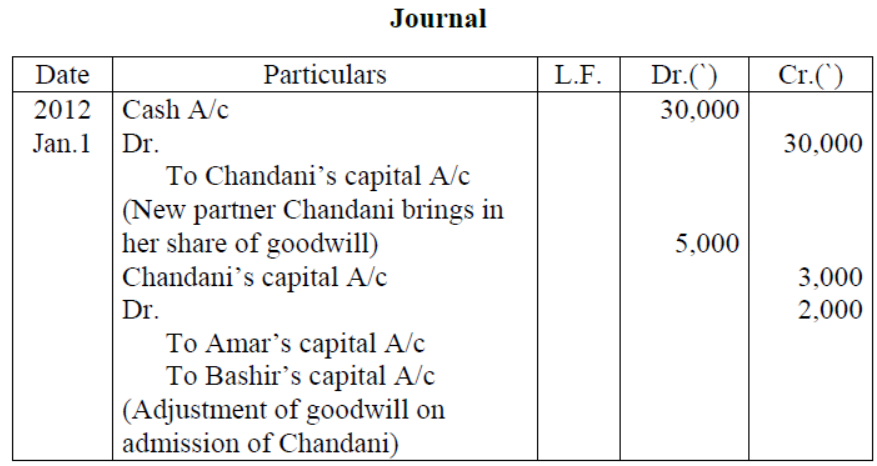

Question. Amar and Bashir are sharing profits in the ratio of 3:2 respectively.

They admit their friend Chandni with one fourth share in the future profits. Chandni belongs to economic weaker section of the society and not able to bring her share of goodwill. Goodwill of the firm is valued at ` 20,000. Chandni contributes ` 30,000 as her share of capital.

Identify the value involved in this question. Give Journal entries in the books of the firm to record the above transactions.

• X and Y were partners in a firm sharing profits in the ratio of 3:2.

On March 31, 2012, their Balance Sheet was as follows: (img)

Answer : Value involved-

(i) Help to economic weaker section of society

(ii) Women empowerment

(iii) National Integration

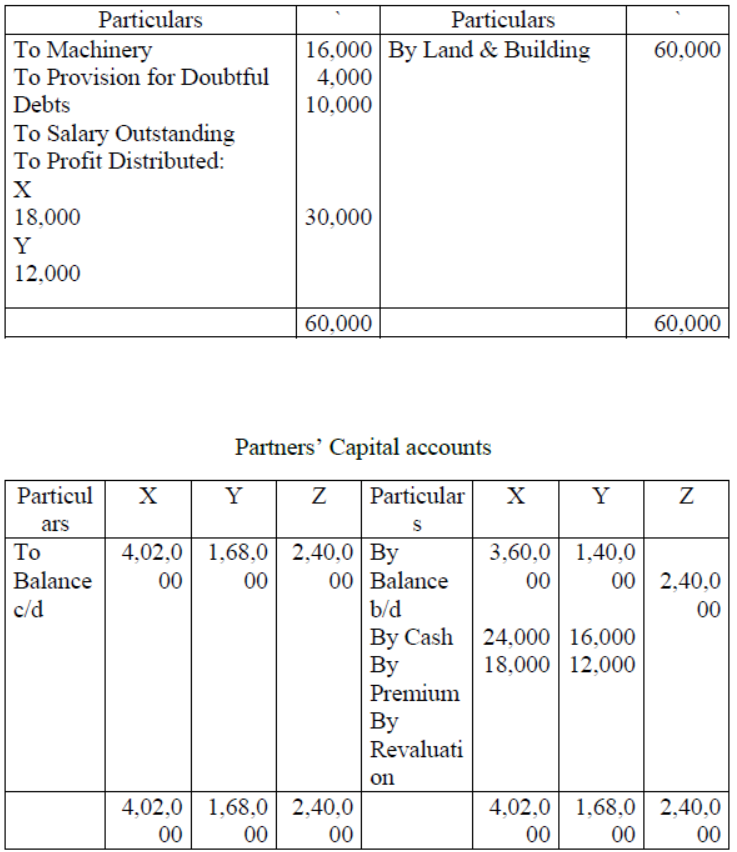

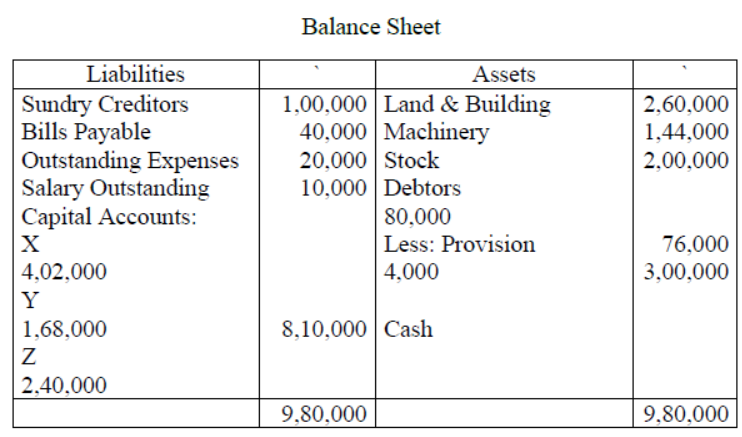

Question. On the above date, Z was admitted as a new partner in the firm for ¼ share in the profits on the following terms:

Z will bring ` 2, 40,000 for her capital and ` 40,000 for her share of goodwill. Machinery was to be depreciated by 10% and Land & Building was to be appreciated by ` 60,000. A provision of 5% was to be created for doubtful debts.

Salary outstanding was ` 10,000.

Prepare Revaluation Account, Partners‘ Capital Accounts and the

Balance Sheet of the new firm.

Which values of life does Revaluation Account signify?

Answer : Following values are being violated:-

• Mutual trust

• Honesty

• Revaluation account signifies Adaptability

according to changes in life.

• Transparancy

Revaluation Account

Dissolution of Partnership Firms

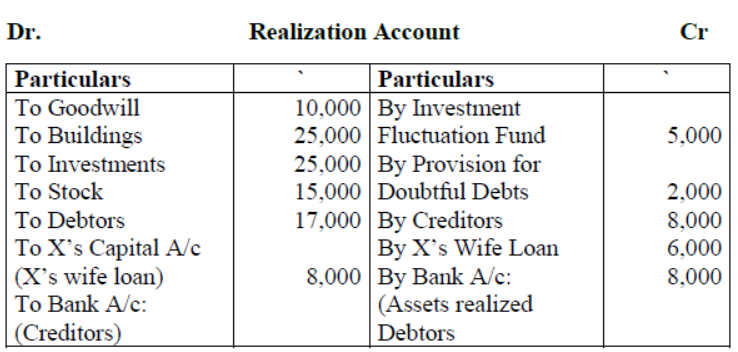

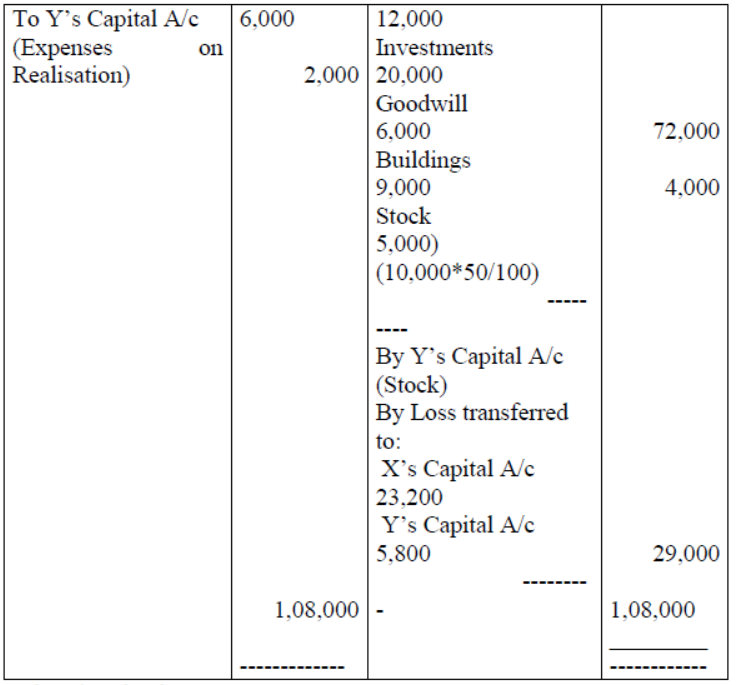

Question. Following is the Balance Sheet of X and Y, who share profits and losses in the ratio of 4:1, as at 31st March, 2011:

Balance Sheet

As on 31st March, 2011

The firm was dissolved on the above date and the following arrangements were decided upon:

(i) Y is authorized to sell the assets of the firm and he will get a fixed amount of ` 2,000 for his work.

(i) X agreed to pay off his wife‘s loan.

(ii) Debtors of ` 5,000 proved bad.

(iii) Y decided to sale the building for ` 9,000 to his brother.

Market value of the building was ˆ 80,000.

(iv) Others assets realized – Investments 20% less; and Goodwill at 60%. (v) One of the creditors for ˆ 5,000 was paid only ˆ 3,000.

(vi) Y took over part of Stock at ` 4,000 (being 20% less that the book valve).

Balance stock realized 50%.

(vii) Realization expenses amounted to ` 2,000.

State which value are being violated in the above question and also prepare Realization A/c.

Answer :

Values involved—

1.Mutual understanding

2 Transparancy

Company Account- Issue of Shares

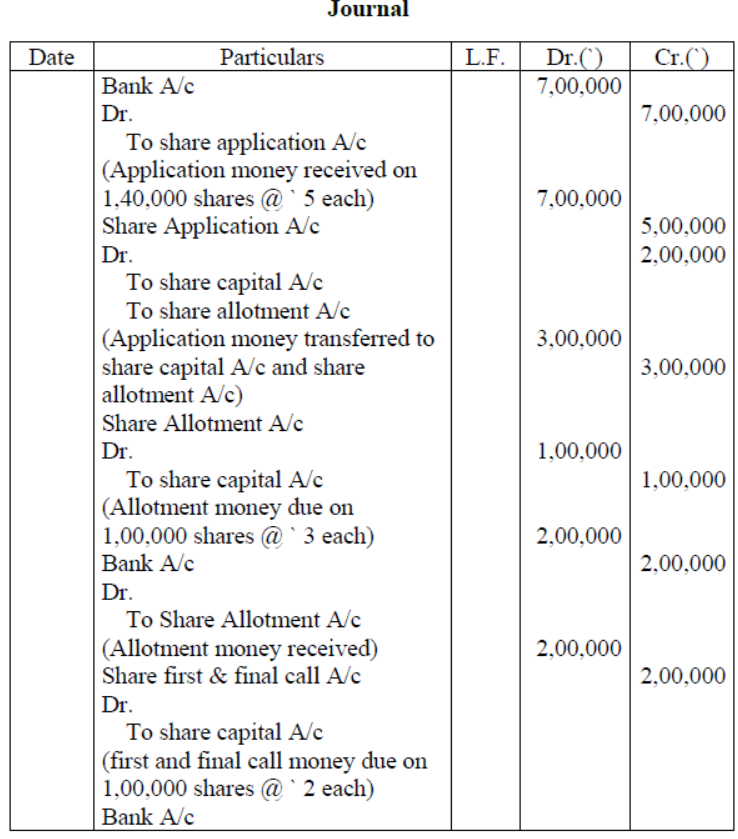

Question. Shiksha India Ltd. issues 1, 00,000 shares of ` 10 each payable ` 5 on application, ` 3 on allotment and ` 2 on first and final call.

Public applied for 1, 40,000 shares and the company made the allotment to all the applicants on pro-rata basis.

Identify the value involves in the decision of company regarding allotment of shares. Pass the journal entries in the books of the company.

Answer : Values:

(i) Equality

(ii) Equal opportunity to all members of public

Shiksha India Ltd.

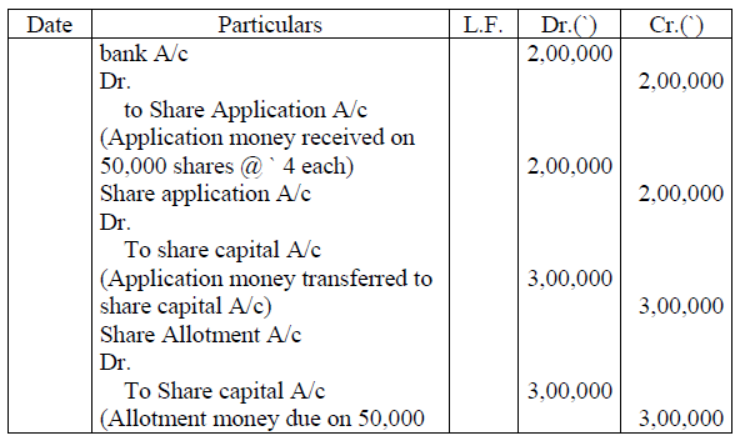

Question. Rehan Ltd. issues 50,000 shares of ` 10 each payable ` 4 on application and ` 6 on allotment. According to the SEBI guidelines, a minimum of the net offer should be reserved for small investors.

Therefore, out of these 50,000 shares, 50% portion is reserved for retail (small) investors. Issue has been fully subscribed. Identify the value involves in this question and pass the Journal entries in the books of Rehan Ltd.

Answer : Values Involves:

(i) protection of interest of small investors

(ii) Promoting the habit of saving in people

(iii) Helpful in capital formation

Rehan Ltd.

Journal

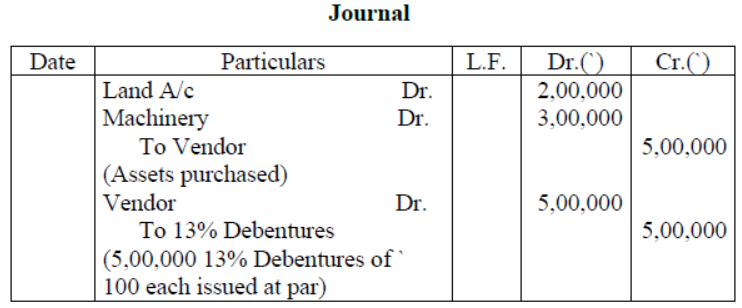

Question. Board of Directors of Pearl Global Industries Ltd. wants to start a new unit at a remote area of Assam. The new unit can be started in the form of labor intensive with a capital of ` 5 crore or in the form of automatic plant with a capital of ` 30 crore. Directors decided to start this unit in the form of labor intensive for generation of employment opportunities in remote areas. Therefore company purchased land for ` 2, 00,00,000 and machinery for ` 3,00,00,000.

In consideration of these assets Company issues 13% Debentures at par.

Identify the values involves in the decision of directors of Pearl

Global Ltd. and Journalize the transactions.

Answer : Value involved:

(i) Generation of employment opportunities

(ii) Balanced regional development

Question. According to the SEBI guidelines, Debentures can be secured by a charge on the assets of the company. A 'Debenture Trust Deed‘ is entered into between the company and the debenture holders. .

Identify the values involved in this decision of SEBI.

Answer : Value Involved

(i) Protection of interest of debenture holders.

Question. A Ltd. issued Rs. 10lacs 9% debentures of Rs. 100 each on 1st April, 2008 redeemable in five equal instalments through draw of lots beginning from the year ending 31st march 2011. Assume that Company has transferred sufficient amount to Debenture redemption reserve.

Pass journal entries for redemption of debentures for 1st year

and state the value symbolised by redeeming the debentures through draw of lots?

• Creation of Debenture Redemption Reserve by company indicates which value?

• INFRA Developers Ltd. (an infrastructure company) issued 5, 00,000 8% Debentures of Rs.100 each on April 1, 2008 redeemable

on April 1, 2012. How much amount of Debenture Redemption Reserve is required before the redemption of debentures?

Which value SEBI wants to promote by having special provision for Infrastructure Company?

Answer : Journal

Date Particulars LF Dr. Amount Cr.

Amount

2011

March 31 9% Debentures a/c Dr. 100,000

To Debenture holders 100,000

(Being payment due to Debenture

Holders on redemption)

March 31 Debenture holders a/c Dr. 100,000

To Bank a/c 100,000

(Being payment made)

By redeeming Debentures through draw of lots, Company is showing the following values:-

• Equal opportunity to every Debenture holder in redemption of Debentures.

• Judicious and rational decision making by the company to pay its debts in installments.

Question. The operating ratio of A ltd. is 55% and that of B Ltd. is 65%.

Which company is following the value of efficient utilization of resources and explain your answer?

Answer : No Debenture Redemption Reserve is to be created since SEBI has exempted infrastructure companies.

SEBI wants to promote National Development by exempting infrastructure companies so that it may utilise its funds in timely completion of the projects.

Question. Balance sheet of A Ltd. Showed a balance of Rs.25 Lacs as Cash and Cash equivalents while working capital requirement of Rs.

5Lacs on an average. Which value do you think is missing in the financial planning of the company?

Answer : A Ltd. is using the value of efficient utilization of resources because operating ratio shows the percentage of sales that is absorbed by the cost of sales and operating expenses. A lower operating ratio is always better.

Analysis of financial statements

Question. Prepare Comparative Statement from the following:

31st March, 2007 31st March, 2008

Revenue from Operations 10,00,000 12,50,000

Cost of Goods Sold 5,00,000 6,50,000

Operating Expenses 50,000 60,000

Interest on investments @ Rs.30.000 and taxes payable @ 50%. Identify the values involved in preparation of comparative statement.

Answer : Values: Estimation with due care

Analytical ability

Comparative income statement

for the year ended March 31, 2007 and March 31, 2008

Particulars 31-3-2007 31-3-2008 Absolute %

Increase Increase

or or

DecreaseDecrease

Revenue from Operations10,00,000 12,50,000 +2,50,000 + 25.00

Less: Cost of Goods sold 5,00,000 6,50,000 + 1,50,000 + 30.00

Gross Profit 5,00,00 6,00,000 + 1,00,000 + 20.00

Less: Operating Expenses 50,000 60,000 + 10,000 + 20.00

Operating Profit 4,50,000 5,40,000 + 90,000 + 20.00

Add: Other Income 30,000 30,000

N.P. before Tax 4,80,000 5,70,000 +90,000 + 18.75

Less: Income Tax @ 50% 2,40,000 2,85,000 + 45,000 + 18.75

N.P. After Tax 2,40,000 2,85,000 +45,000 +18.75

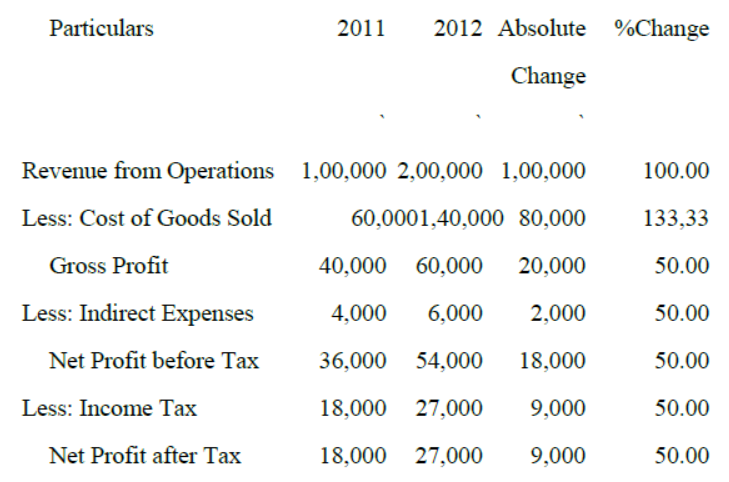

Question. Prepare a comparative income statement of X Ltd., with the help of the following information and identify the value involved in it-

2011 2012

Revenue from Operations 1, 00,000 2, 00,000

Cost of Goods Sold 60% of Sale 70% of sales

Indirect Expenses 10% of Gross Profit

Rate of Income Tax 50% of Net Profit before Tax

Answer :

Values: Estimation.

Analytical ability

Comparative Income Statement

Question. Following particulars are given to you:

Closing Inventory 2,00,000

Trade Receivables 1,08,000

Less: Provision for Doubtful Debts 8,000 1,00,000

Cash 30,000

Marketable Securities 20,000

Income Tax paid in Advance 10,000

Share Issue Expenses 15,000

Liability for Current Taxation 20,000

Liability for Future Taxation 30,000

Trade Payables 34,000

Outstanding Salaries 5,000

Bank Overdraft 25,000

Dividends Payable 36,000

Calculate the Liquidity Ratio and Comment on the short-term financial position of the company. Identify the values involved in this question.

Answer :

Values: Decision Making andForesightedness.

Liquidity Ratios include the following two ratios:

• Current Ratio, and (b) Quick Ratio

• Current Ratio = Current Assets/Current Liabilities

Current Assets = Closing Inventory + Trade Receivables + Cash +

Marketable Securities + Income Tax Paid in Advance

= ` 2,00,000 + ` 1,00,000 + ` 30,000 + ` 20,000 + `10,000

= `3,60,000

Current Liabilities = Taxation (Current) + Trade Payables +

Outstanding Salaries + Bank Overdraft + Dividents Payable

= `20,000 + `34,000 + `5,000 + `25,000 + `36,000

= `1,20,000

Current Ratio = 360000/120000 = 3:1

• Quick Ratio = Liquid Assets / Current Liabilities

Liquid Assets = Trade Receivables + Cash + Marketable Securities

= `1,00,000 + `30,000 + `20,000

= `1,50,000

Quick Ratio = 150000/120000 = 1.25:1

Comments: The short-term financial position of the company is sound because its current ratio is 3 : 1, which is more than the ideal ratio of 2 : 1. Liquid ratio o the company is 1.25 : 1, which is also more than the ideal ratio of 1 : 1. Therefore, it can be said that the company is in a position to pay its current liabilities instantly.

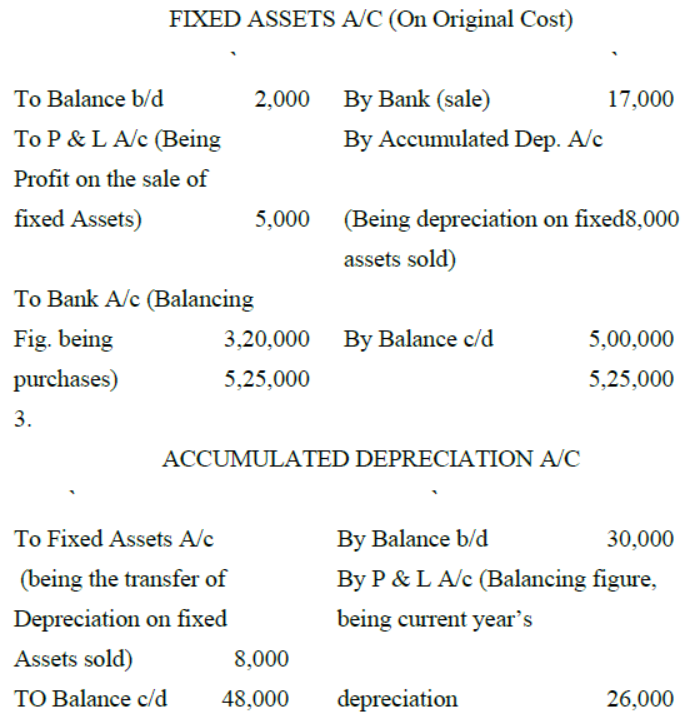

Question. From the following Balance Sheets of Surya Roshni Ltd., as on 31st March 2011 and 2012, prepare a statement of cash flow:

Particulars 2011 2012

• EQUITY AND LIABILITIES `

Equity Share Capital 3,00,000 4,00,000

Preference Share Capital 1,00,000 75,000

Securities Premium —

60,000

Profit & Loss Balance 10,000 72,000

15% Debentures 2,00,000 2,50,000

Trade Payables 50,000 1,10,000

TOTAL 6,40,000 9,67,000

• ASSETS:

Fixed Assets 2,00,000 5,00,000

Less: Accumulated Depreciation 30,000 48,000

1,70,000 4,52,000

Non-Current Investments 40,000 45,000

Inventory 1,50,000 2,00,000

2011 2012

Trade Receivables 1,76,00056,000

Less: Provision for

Doubtful Debts 10,000 16,000

1,66,00040,000 1,66,000 40,000

Bank 94,000 2,14,000

Discount on Issue of Debentures 20,000 16,000

TOTAL 6,40,000 9,67,000

Additional Information:

• Dividend paid during the year ` 36,000.

• Investment costing ` 10,000 were sold at a profit of 40%.

• Fixed Assets Costing ` 20,000 (accumulated depreciation ` 8,000) were sold for ` 17,000.

Additional debentures amounting to ` 50,000 were issued at par on 1st August 2011. Interest on debentures has been paid regularly.Mention the values involved in it.

Answer :

CASH FLOW STATEMENT

(Indirect Method)

• Cash flows from Operating Activities:

Net profit before taxation:

Profit during the year (1) 82,000

+Dividend paid 36,000 1,18,000

Adjustments for:

Depreciation on fixed assets(3) 26,000

Provision for doubtful debts 6,000

Discount on issue written off 4,000

Interest Paid 35,000

1,89,000

Less: Profit on sale of investments 4,000

Profit on sale of fixed assets 5,000 9,000

Operating profit before working 1,80,000

capital change

Add: Decrease in Current Assets:

Trade Receivables 1,20,000

Increase in Current Liabilities:

Trade Payables 60,000 1,80,000

3,60,000

Less: Increase in Current Assets:

Inventory 50,000

Net cash from operating activities 3,10,000 3,10,000

• Cash flows from Investing Activities:

Purchase of Fixed Assets (2) (3,20,000)

Sale of Fixed Assets 17,000

Purchase of Investments (4) (15,000)

Sale of Investments 14,000

Net cash used in investing activities (3,04,000)(3,04,000)

• Cash flows from financing activities:

Issue of Equity Shares 1,00,000

Premium received on issue of shares 60,000

Issue of Debentures 50,000

Redemption (Repayment) of Preference (25,000)

Shares

Dividend paid (36,000)

Interest paid (35,000)

Net cash from financing activities 1,14,000 1,14,000

Net increase in cash and cash equivalents 1,20,000

Cash and cash equivalents at the beginning

of the period 94,000

Cash and cash equivalents at the end of the

Period 2,14,000

Note: 1. Negative balance of Profit & Loss amounting to ` 10,000

appearing in the Balance Sheet on 31st March, 2011 represent an amount

of loss. In the current year, after covering this loss of ` 10,000, the Profit

~ Loss shows a profit of ` 72,000. It means that net profit during the

current year must have been ` 72,000 + ` 10,000 = ` 82,000.

Question. Jamshedji Tata conceived an idea of formation of company in 1908 when East India Company was ruling Indian market . He selected hilly region bordering three states Jharkhand(then part of Bihar ) ,Orissa and West Bengal All states were thickly populated and poor .Area he chose was rich in Iron ore so he decided to develop Iron and Steel Industry .

He wanted to tap unproductive savings of public and Issued capital of Rs. 5,00,000. Area was undeveloped so he decided to spend 10% of profits every year for providing Infrastructure to employees. To begin with he provided them accommodation and later he spent amount for schools, hospitals, development of playground and gardens and also contributed in road construction. He also built temples, mosques and churches. Employees were satisfied and worked hard as a result profit grew substantially 20% every year and more Industries were floated by him .Which values lead him to this road of success.

Answer : Because of following values he proved to be successful

• Courage – he was first Indian to start industry during British period

• entrepreneurship

• social issues---sensitivity towards education

sensitivity towards environment

• respect for all religions

• unity as people of all three states worked together happily

• channelizing saving leading to capital formation

• rural development

• motivation of employees

• best utilization of resources

• nation building

Question. Cadbury India Ltd. A chocolate company launched a factory in Baddi a small town of Himachal Pradesh .The workers who enter in factory have to wash their hands with sanitizer and wear overcoat, cap and shoes which are sterilized every day for which company spends Rs. 3,00,000 per month . All employees working in factory wear gloves and not allowed to touch directly either raw material or final product .

All employees irrespective of post have to take food in mess at the same place and same food for this company spends Rs.4,00,000 per month .Which values are taken care of ?

Answer :

• Equality all employees treated equally

• Health consciousness—use of sanitizer and sterilised clothes

• Balanced regional development

• Employment to people of hills raising their standard of living

Free study material for Accountancy

VBQs for Part 2 Chapter 1 Accounting for Share Capital Class 12 Accountancy

Students can now access the Value-Based Questions (VBQs) for Part 2 Chapter 1 Accounting for Share Capital as per the latest CBSE syllabus. These questions have been designed to help Class 12 students understand the moral and practical lessons of the chapter. You should practicing these solved answers to improve improve your analytical skills and get more marks in your Accountancy school exams.

Expert-Approved Part 2 Chapter 1 Accounting for Share Capital Value-Based Questions & Answers

Our teachers have followed the NCERT book for Class 12 Accountancy to create these important solved questions. After solving the exercises given above, you should also refer to our NCERT solutions for Class 12 Accountancy and read the answers prepared by our teachers.

Improve your Accountancy Scores

Daily practice of these Class 12 Accountancy value-based problems will make your concepts better and to help you further we have provided more study materials for Part 2 Chapter 1 Accounting for Share Capital on studiestoday.com. By learning these ethical and value driven topics you will easily get better marks and also also understand the real-life application of Accountancy.

FAQs

The latest collection of Value Based Questions for Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital is available for free on StudiesToday.com. These questions are as per 2026 academic session to help students develop analytical and ethical reasoning skills.

Yes, all our Accountancy VBQs for Part 2 Chapter 1 Accounting for Share Capital come with detailed model answers which help students to integrate factual knowledge with value-based insights to get high marks.

VBQs are important as they test student's ability to relate Accountancy concepts to real-life situations. For Part 2 Chapter 1 Accounting for Share Capital these questions are as per the latest competency-based education goals.

In the current CBSE pattern for Class 12 Accountancy, Part 2 Chapter 1 Accounting for Share Capital Value Based or Case-Based questions typically carry 3 to 5 marks.

Yes, you can download Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital VBQs in a mobile-friendly PDF format for free.