Dissolution of A partnership firm

Q.1 Distinguish between dissolution of partnership and dissolution of partnership firm on the basis of continuation of business.

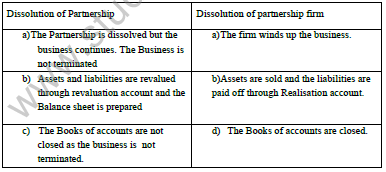

Ans. 1 In case of dissolution of partnership, the firm may continue its business operation but in case of dissolution of partnership firm, the business operations are discontinued.

Q.2 Why is Realisation Account prepared on dissolution of partnership firm?

Ans. 2 Realisation account is prepared to ascertain profit or loss on sale of assets and payment of liabilities.

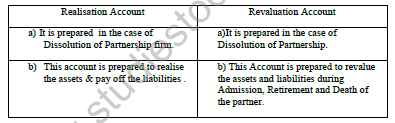

Q.3 State any one point of difference between Realisation Account and Revaluation Account.

Ans. 3 Realisation Account is prepared on dissolution of partnership firm and Revaluation account is prepared on reconstitution of partnership firm.

Q.4 All partners wish to dissolve the firm. Yastin, a partner wants that her loan of Rs. 2,00000 must be paid off before the payment of capitals to the partners. But, Amart, another partner wants that the capital must be paid before the payment of Yastin‘s loan. You are required to settle the conflict giving reasons.

Ans. 4 Yustin‘s claim is valid as according to section 48 (b) of partnership Act, partners loan are to be paid before any amount is paid to partners on account of their capitals

Q.5 On a firms dissolution debtors as shown in the Balance sheet were Rs. 17000 out of these Rs. 2000 became bad. One debtor of Rs. 6000 became insolvent and 40% could be recovered from him. Full recovery was made from the balance debtors. Calculate the amount received from debtors and pass necessary journal entry.

Ans. 5 Cash A/C Dr. 11400

To Realisation A/C 11400

(For debtors realized on dissolution of firm)

Q.6 On dissolution of a firm, Kamal‘s capital account shows a debit balance of Rs. 16000. His share of profit on realization is Rs. 11000. He has taken over firms creditors at Rs. 9000. Calculate the final payment due to /from him and pass journal entry.

Ans. 6 Kamal‘s capital A/C Dr. 4000

To cash A/C 4000

(for final payment to Kamal)

Q.7 A and B were partners in a firm sharing profits and losses equally. Their firm was dissolved on 15th March, 2004, which resulted in a loss of Rs. 30,000. On that date the capital A/C of A showed a credit balance of Rs. 20,000 and that of B a credit balance of Rs. 30000. The cash account has a balance of Rs. 20000. You are required to pass the necessary journal entries for the (i) Transfer of loss to the capital accounts and (ii) making final payment to the partners.

Ans. 7 (i) A‘s capital A/C Dr. 15000

B‘s capital A/C Dr. 15000

To realization A/C 30000

(For transfer of loss on dissolution)

(ii) A‘s capital A/C Dr. 5000

B‘s capital A/C Dr. 15000

To cash A/C 20000

(For final payment to partners)

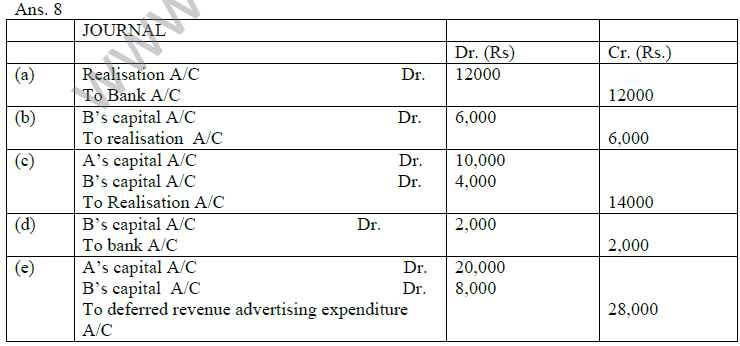

Q.8 What journal entries would be passed in the books of A and B who are partners in a firm, sharing profits in the ratio of 5:2, for the following transactions on the dissolution of the firm after various assets (other than cash) and third party liabilities have been transferred to Realisation Account?

(a) Bank loan Rs. 16,000 is paid.

(b) Stock worth Rs. 6000 is taken over by B.

(c) Loss on Realisation Rs. 14,000.

(d) Realisation expenses amounted to Rs. 2,000, B has to bear these expenses.

(e) Deferred Revenue Advertising Expenditure appeared at Rs. 28,000.

(f) A typewriter completely written off in the books of the firm was sold for Rs. 200.

Learning Objectives

After Studying this unit, the students will be able to understand:

*Meaning of Dissolution

* Distinction between Dissolution of Partnership and Dissolution of Partnership firm.

* Preparation of Realisation Account

* Procedure of settlement of accounts

* Preparation of Memorandum Balance sheet (to find out missing figures)

* Necessary journal entries to close the books of the firm.

SALIENT POINTS:

♦ Dissolution : Dissolution of the firm is different from Dissolution of Partnership.

♦ Realisation account : It is prepared to realize the various assets and pay off the liabilities.

♦ Closure of the Books of Accounts : When the firm is dissolved, finally all the books of accounts are closed through Bank Account.

1. Distinguish between Dissolution of Partnership and Dissolution of Partnership firm

2. State the provisions of Section 48 of the Partnership Act 1932 regarding settlement of Accounts during the Dissolution of Partnership firm.

Ans. According to section 48—

a) Losses including the deficiencies of Capitals are to be paid---

i) First out of profits

ii) Next out of Capitals of the partners

iii) Lastly if required, by the partners individually in their profit sharing ratio(as their liability is unlimited)

b) The Assets of the firm and the amount contributed by the partners to make up the deficiency of capital shall be applied for –

i) First to pay the debts of the firm to the third parties.

ii) Next, Partners Loan(Partner has advanced to the firm)

iii) Partners capitals

iv) The residue, if any shall be distributed among the partners in their profit sharing ratio.

3. Distinguish between Realisation account and Revaluation account.

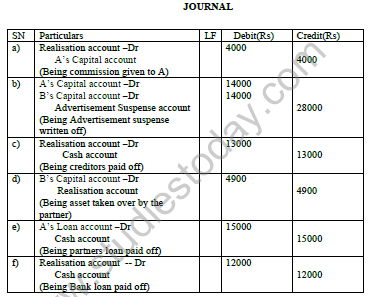

4. A and B are partners sharing profits and losses equally. They decided to dissolve their firm. Assets and Liabilities have been transferred to Realisation Account. Pass necessary Journal entries for the following.

a) A was to bear all the expenses of Realisation for which he was given a commission of Rs 4000.

b) Advertisement suspense account appeared on the asset side of the Balance sheet amounting Rs 28000

c) Creditors of Rs 40,000 agreed to take over the stock of Rs 30,000 at a discount of 10% and the balance in cash.

d) B agreed to take over Investments of Rs 5000 at Rs 4900

e) Loan of Rs 15000 advanced by A to the firm was paid off.

f) Bank loan of Rs 12000 was paid off.

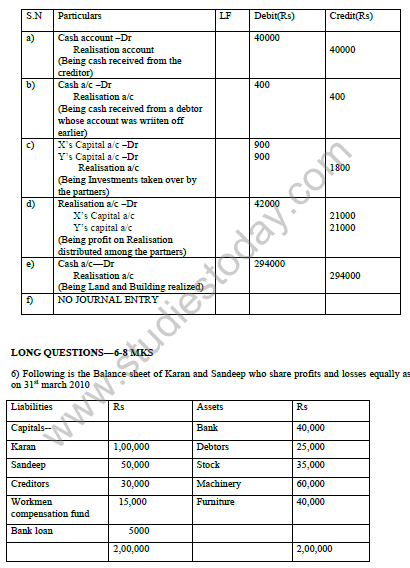

4. X and Y are partners in the firm who decided to dissolve the firm. Assets and Liabilities are transferred to Realisation account. Pass necessary journal entries—

a) Creditors were Rs 1,00,000. They accepted Building valued Rs 1,40,000 and paid cash to the firm Rs 40,000.

b) Aman, an old customer whose account of Rs 1000 was written off as bad in the previous year paid 40% of the amount.

c) There were 300 shares of Rs 10 each in ABC Ltd which were acquired for Rs 2000 were now valued at Rs 6 each. These were taken over by the partners in the profit sharing ratio.

d) Profit on Realisation Rs 42000 was divided among the partners.

e) Land and Building (Book value Rs 1, 60,000) was sold for Rs 3,00,000 through a broker who charged 2% commission on the deal.

f) Plant and machinery (Book value Rs 60,000) was handed over to the creditor in full settlement of his claim.

The firm was dissolved on the above date.

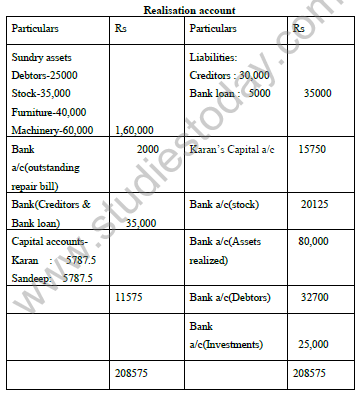

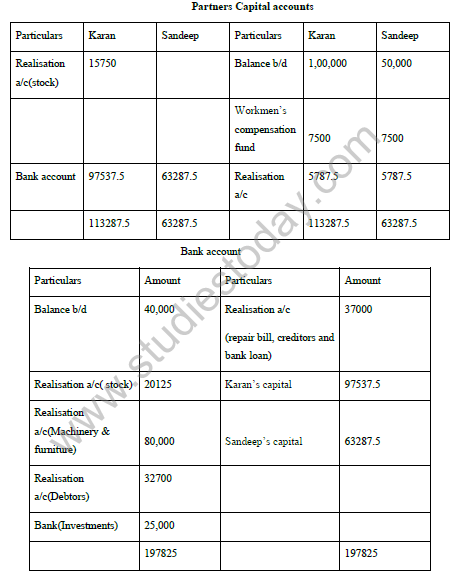

1. Karan agreed to take over 50% of the stock at 10% less on its book value, the remaining stock was sold at a gain of 15%. Furniture and machinery realized for Rs 30,000 and 50,000 respectively.

2. There was unrecorded Investments which was sold for Rs 25,000.

3. Debtors realized Rs 31,500 (with interest) and Rs 1200 was recovered for bad debts written off last year.

4. There was an outstanding bill for repairs which had to be paid Rs 2000. Prepare necessary Ledger accounts to close the books of the firm.

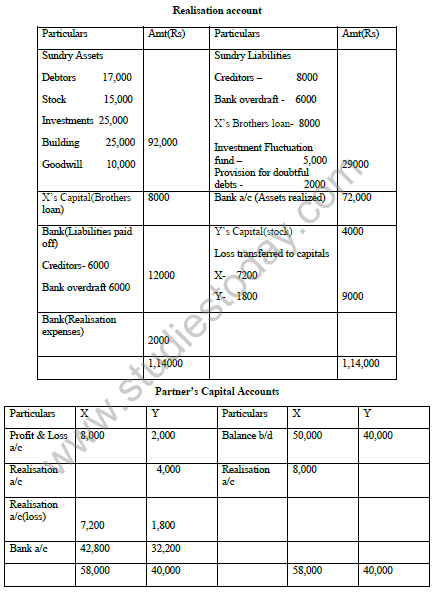

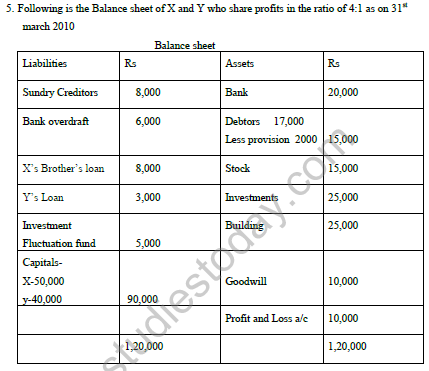

The firm wasdissolved on the above date and the following was decided—

a) X agreed to pay off his brother‘s loan

b) Debtors of Rs 5000 proved bad.

c) Other assets realized as follows—Investments 20% less, and Goodwill at 60%.

d) One of the creditors for Rs 5000 was paid only Rs 3000.

e) Building was auctioned for Rs 30,000 and the auctioneer‘s commission amounted to Rs 1000.

f) Y took over part of the stock at Rs 4000(being 20% less than the book value)Balance stock realized 50%

g) Realisation expenses amounted to Rs 2000.

Prepare Realisation account, Partners capital accounts and Bank account.

1. You are given the following particulars

Furniture of book value of Rs. 10,000

Loss on sale - Rs. 2,000

If it had been taken over by Anil, a partner what would

have been the journal entry on

(a) Dissolution (b) On reconstitution

Journal entry

Ans.(a) Anils capital a/c Dr. 8,000

Realisation a/c 8,000

(b) Anils capital a/c Dr. 8,000

Revaluation a/c Dr. 2,000

Furniture a/c 10,000

2. Complete the series

(a) Sacrificing ratio : admission

Gaining ratio : ?

(b) Dissolution : Realisation a/c

Reconstitution : ?

(c) Trading a/c : Profit and loss a/c

Profit & loss a/c : ?

(d) Balance of capital a/c : Balance sheet Balance of profit and loss appropriation a/c:?

Ans.(a) Retirement (b) Revaluation a/c

(c) Profit and loss appropriation a/c

(d) Capital accounts

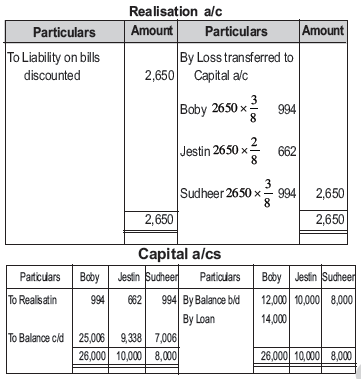

Q.3. Boby, Jestin and Sudheer are in partnership in the ratio of 3:2:3. They have decided to dissolve the firm.

On the date of dissolution total creditors were Rs. 16,000; Bills discounted Rs. 2,650 during the year, has become a real liability which has to be paid, though this has not been recorded anywhere in the books of accounts. Their capital account balances were Boby Rs. 12,000; Jestin Rs. 10,000; Sudheer Rs. 8,000 respectively. Boby advance Rs. 14,000 besides his capital account.

Find out: (a) Total Sundry Assets

(b) Realisation a/c

(c) Capital accounts of partners.

(a) Value of asset

Asset = Capital + Liability

= 12000 + 10000 + 8000 + 14000 + 16000

= Rs. 60,000

4. Should you pass any entry for the payment of creditors worth Rs. 5,000 on dissolution, if they accept stock of the same value? If yes, what is the journal entry?

Ans: No journal entry will be passed as they have accepted stock of same value.

5. What entry would you pass for the following transactions on the dissolution of a firm having partners Vishal and Rakesh.

(i) An unrecorded asset realised Rs. 6,200

(ii) Dissolution expenses amounted to Rs. 3,200

(iii) Creditors already transferred to realisation account were paid Rs. 88,000

(iv) Stock worth Rs. 5,400 already transferred to realisation account was sold for Rs. 4,100

(v) Profit on realisation Rs. 48,000 to be distributed between partners, Vishal and Rakesh? Passing Journal Entries

(i) Cash a/c Dr. 6,200

Realisation a/c 6,200

(ii) Realisation a/c Dr. 3,200

Cash 3,200

(iii) Realisation a/c Dr. 88,000

Cash 88,000

(iv) Cash a/c Dr. 4,100

Realisation a/c 4,100

(v)Realisation a/c Dr. 48,000

Vishal capital a/c 24,000

Rakesh capital a/c 24,000

Q.6. Richard and Gere, partners of Sun Chemicals decided to dissolve the firm. You are required to pass journal entries for the following transactions at the time of dissolution.

(i) Expenses of dissolution amounted to Rs. 500, paid by Mr. Richard.

(ii) Stock worth Rs. 3,000 which was already transferred to realisation account was taken over by Mr. Richard.

(iii) Profit on realisation Rs. 6,000 has to be distributed to Mr. Richard and Gere in the ratio 2:1.

Journal entry

(i) Realisation a/c Dr. 500

Richards capital a/c 500

(ii) Richards capital a/c Dr. 3,000

Realisation a/c 3,000

(iii) Realisation a/c Dr. 6,000

Richards capital a/c 4,000

Geres capital a/c 2,000

Q.7. Toya and Soya are partners sharing profits and losses equally. They decided to dissolve the firm on 15th March, 2005 which resulted in a loss of Rs. 30,000. The capital accounts of Toya and Soya was Rs. 20,000 and Rs. 30,000 respectively. The cash account showed a balance of Rs. 20,000.

You are required to pass journal entries for

(i) Transfer of loss to the capital account of partners

(ii) Making final payments to the partners.

Ans.(i) Journal entry for transfer of loss

Toyas capital a/c Dr. 15,000

Soyas capital a/c Dr. 15,000

Realisation a/c 30,000

(ii) Journal entry for final payment of partners

Toyas capital a/c Dr. 5,000

Soyas capital a/c Dr. 15,000

Cash a/c 20,000