Refer to CBSE Class 12 Accountancy HOTs Accounting For Share Capital. We have provided exhaustive High Order Thinking Skills (HOTS) questions and answers for Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital. Designed for the 2026-27 exam session, these expert-curated analytical questions help students master important concepts and stay aligned with the latest CBSE, NCERT, and KVS curriculum.

Part 2 Chapter 1 Accounting for Share Capital Class 12 Accountancy HOTS with Solutions

Practicing Class 12 Accountancy HOTS Questions is important for scoring high in Accountancy. Use the detailed answers provided below to improve your problem-solving speed and Class 12 exam readiness.

HOTS Questions and Answers for Class 12 Accountancy Part 2 Chapter 1 Accounting for Share Capital

ACCOUNTING FOR SHARE CAPITAL & DEBENTURE

Case Based Question :

Anant and his 10 friends formed a Whatsapp group to discuss the Covid situations and decided to help the society somehow. They thought of starting with a venture where they can help the affected persons required medicines and oxygen cylinders at genuine prices.

They wanted to make an App for Android as well as I-Phones as that the patients or their family members can fill their requirements quite easily.. They also need to make contacts with some genuine medical stores of the country so that the medicines to be supplied timely at genuine prices.

They need funds of Rs. 15,00,000 for IT work as well as working capital requirements. But they had only Rs.2,00,000 with them. They discussed the idea with their friend Varun who was Chartered Accountant. Varun suggested that they should start a public company and invite the general public to finance in their project. Since the project is profitable as well as beneficial for the masses, so good number of investors will be interested in buying the shares of such company. For all the necessary formalities of starting a company like applying for starting a company with Registrar of Companies as well as making important documents like Memorandum of Association, Articles of Association and Prospectus the amount they had i.e Rs.2,00,000 was sufficient. So these friends acted as promoters and suggested the name of company as Get Well Soon Ltd. which was approved by Registrar. Registrar approved the required authorised capital as filled by them in application form as Rs.50,00,000 divided in to 5,00,000 shares of Rs.10 each.

After incorporation, Get Well Soon Ltd. invited applications for 1,50,000 shares of Rs.10 each. The company also issued 10,000 shares to promoters for their services. Share was payable as Rs.3 on application, Rs.4 on allotment and balance on call. Since the project was social and beneficial for the society so their shares were over-subscribed and the company received applications for 2,40,000 shares. Pro-rata allotment was made to applicants in proportion of 4:3 and remaining applications were sent letter of regret. .

Mr. Sultan holding 6,000 shares failed to pay allotment money and his shares were immediately forfeited. After this call was made and received by the company except by Mr. Baadshah holding 3,000 shares. Later on 4,000 shares were re-issued @Rs.12 per share as fully paid up.

Answer the following questions on the basis of above mentioned information.

Question. Amount due on First call was :-

(a) Rs.4,50,000

(b) Rs.4,41,000

(c) Rs.4,32,000

(d) Rs.4,23,000

Answer : C

Question. Amount to be refunded at the time of Application money utilised was :-

(a) Rs.2,70,000

(b) Rs.1,20,000

(c) Rs.1,50,000

(d) Nil

Answer : B

Question. Money received at the time of allotment received was :-

(a) Rs.6,00,000

(b) Rs.4,50,000

(c) Rs.4,26,000

(d) Rs.4,32,000

Answer : D

Question. Amount received on First call was :-

(a) Rs.4,50,000

(b) Rs.4,41,000

(c) Rs.4,32,000

(d) Rs.4,23,000

Answer : D

Question. Remaining 2,000 shares can be issued at a minimum re-issue amount/price of Rs.._____

(a) Rs.8,000 (Rs.4 per share)

(b) Rs.12,000 (Rs.6 per share)

(c) Rs.20,000 (Rs.10 per share)

(d) Rs.4,000 (Rs.2 per share)

Answer : B

Question. Amount forfeited of Mr. Sultan was :-

(a) Rs.18,000

(b) Rs.24,000

(c) Rs.32,000

(d) Rs.6,000

Answer : B

Accounting for Share capital & Debentures

Q.1 What do you mean by Private placement of shares?

Ans. Private Placement of shares implies issue and allotment of shares to a selected groups of persons privately and not to public in general through public issue. In order to place the shares privately, a company must pass a special esolution to this effect.

Q.2 What is Sweat Equity?

Ans. Sweat Equity shares means easily shares issued by the company to its employees or whole time directors at a discount or for consideration other then cash for providing know - how or making available right in the nature of intellectual properly rights or valve addition by whatever name called.

Q.3 What maximum amount of discount can be allowed on the reissue of forfeited shares?

Ans. The maximum amount of discount on reissue of forfeited shares is that the amount of discount allowed cannot exceed the amount that had been received on forfeited shares on their original issue and that the discount allowed on re issue of forfeited shares should be debited to the share forfeited account.

Q.4 State in brief, the SEBI Guidelines regarding Debenture Redemption Reserve.

Ans. At per SEBI Guidelines, an amount equal to 50% of the debenture issue must be transferred to DRR before the redemption begins. In other words, before redemption, at least an amount equal to 50% of the debenture issue must stand to the credit of DRR

Q.5 Name the head under which discount on issue of debentures appears in the Balance Sheet of "C" Company.

Ans. Discount on issue of debentures will appear under the heading Miscellaneous Expenditure.

UNIT 4: Company Accounts- Share capital

LEARNING OBJECTIVES

Understand the meaning and features of company

I) Classification of share capital

II) Understand the accounting treatment of over subscription, calls in arrears, premium and discount on issue of shares.

III) Understand the meaning of forfeiture of shares

IV) Pass journal entries regarding forfeiture and reissue of shares

V) Calculate capital reserve

VI) Differentiate between capital reserve and reserve capital

VII) Understand the disclosure of the share capital in the balance sheet

Salient Features

*A company is an artificial person having separate legal entity.

*A company is created by law and effected by law.

*A private company can be formed with minimum two members and maximum fifty.

*For a public company minimum members required are 7 and there is no maximum limit.

*The capital of the company is divided into units of small denominations which are called shares.

*Though the company is an artificial person, it has to perform all statutory obligation like a person association.

*A public company can allot shares in case of minimum subscription is received.

*Shares can be issued at par, premium, or even at discount.

*Preferences shareholder enjoy preference rights whereas equity share holder enjoy voting rights.

*When a shareholder fails to pay one or more installments due on the shares held by him, the company has the authority to forfeit such shares.

*A company can re-issue the forfeited shares in accordance with the provisions contained in the articles of the company.

(1 marks)

Q.1 Give the definition of a compnay as contained in the companies act,1956.

Ans section 3(1)(i) of companies act defines a company as "a company formed and registered under this act or an existing company." According to sec3(1)(ii),"An exisiting company means a company formed and registered under any of the former companies Acts."

Q.2 Can forfeited shares be issued at a discount ? If so to what extent?

Ans Re-issue of forfeited shares: Forfeited shares can be reissued at a discount. However, the In other words, amount received on received on re-issue plus amount already received on forfeited shares must not be less than the paid up value of shares.

Q.3 As a director of a company you had invited applications for 20,000 equity shares of Rs.10 each at a premium of Rs.2 each. The total applications money received at Rs.3/- per share was Rs.72,000. Name the kind of subscription. List the three alternatives for allotting these share.

Ans It is a case of over-subscription. Shares are said to be over-subscribed when the numbers of shares ar more than the number of shares offered:

(i) Allotment for 1st 20,000 shares and the rest can rejected

(ii) Allotment on prorata basis

(iii)Allotment of some application in full and some on prorata basis,and some refused.

4 What is an Escrow Account?

Ans. In order to fulfill certain obligations under the scheme of buy-back of securities an account is opened, which is known as escrow account.

Q.5 What do you mean by Private placement of shares?

Ans. Private Placement of shares implies issue and allotment of shares to a selected groups of persons privately and not to public in general through public issue. In order to place the shares privately, a company must pass a special resolution to this effect.

Q.6 What is Sweat Equity?

Ans. Sweat Equity shares means easily shares issued by the company to its employees or whole time directors at a discount or for consideration other then cash for providing know - how or making available right in the nature of intellectual properly rights or valve addition by whatever name called.

Q.7 What maximum amount of discount can be allowed on the reissue of forfeited shares?

Ans. The maximum amount of discount on reissue of forfeited shares is that the amount of discount allowed cannot exceed the amount that had been received on forfeited shares on their original issue and that the discount allowed on re issue of forfeited shares should be debited to the share forfeited account.

Q.8 State in brief, the SEBI Guidelines regarding Debenture Redemption Reserve.

Ans. At per SEBI Guidelines, an amount equal to 50% of the debenture issue must betransferred to DRR before the redemption begins. In other words, before redemption, at least an amount equal to 50% of the debenture issue must stand to the credit of DRR

Q.9 Name the head under which discount on issue of debentures appears in the Balance Sheet of "C" Company.

Ans. Discount on issue of debentures will appear under the heading Miscellaneous Expenditure.

Q.10 Can a company issue share of discount ? What conditions must a company comply with before the issue of such shares.

Ans. Section 79 of the companies Act, 1956 permits a company to issue shares at a discount only if the following conditions are fulfilled :

1) The shares are of a class already issued.

2) At least one year must have elapsed since the company become entitled to commence business.

3) The issue of shares at discount is authorised by a revolution passed by the company in its general meeting and sanctioned by the central Government.

The resolution specifies the maximum rate of discount at which the shares are to be issued. The rate must not exceed 10% unless sanctioned by the central Government.

Q.13 Employees stock option plan-"A right to buy and not an obligation". Comment

.

Ans. Employees stock option plan is the right granted to the employees of the company to purchases the shares lower than the market prices. It is worth mentioning the options provide a right and not the obligation to bur shares. It means that the employees under this plan are not necessarily required to purchase the shares. It is their wish to buy or not necessarily required to purchase the shares. It is their wish to buy or not.

Q.14 Write a short note on minimum subscription?

Ans Minimum subscription is the amount received from share holders which is sufficient from the point of view of directors‘ for following purposes:

(a) For purchasing necessary assets of the company.

(b) For paying preliminary expenses and commission on sales of shares.

(c) For paying loan if arranged for above two purposes.

(d) For working capital and for any other purposes which the directors agree upon.

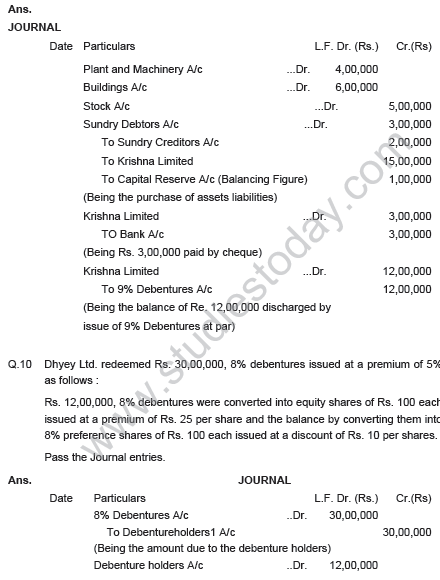

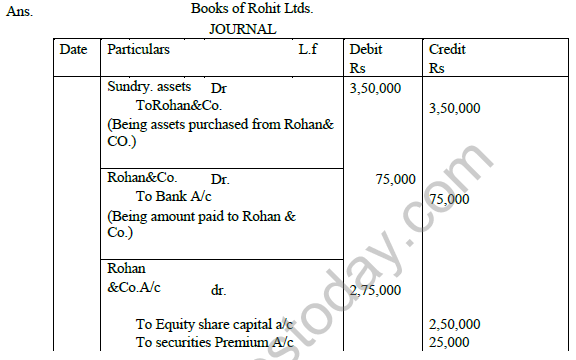

Q.15 Rohit Ltd. Purchased assets from Rohan & co. for Rs. 3,50,000. A sum of Rs. 75,000 was paid by the emans of a bank draft and for the balance due Rohit Ltd. Issued Equity shares of Rs. 10 each at a premium of 10% .Journalise the above transaction in the books of the company.

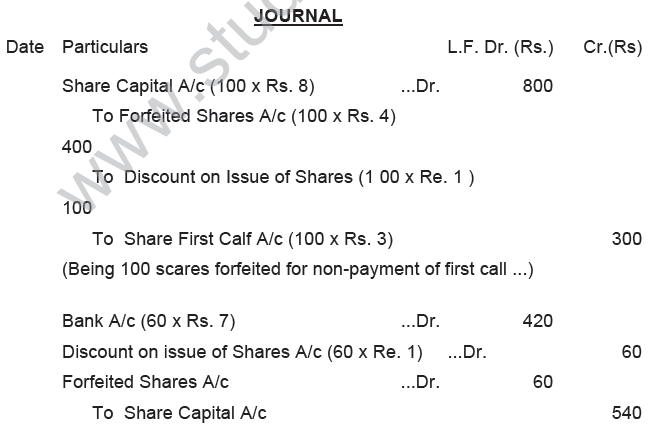

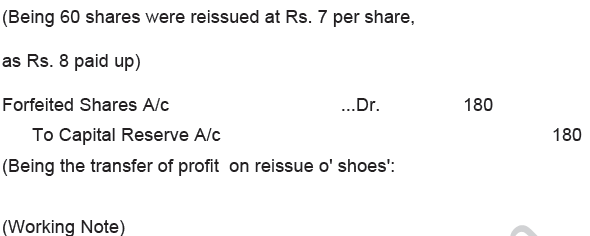

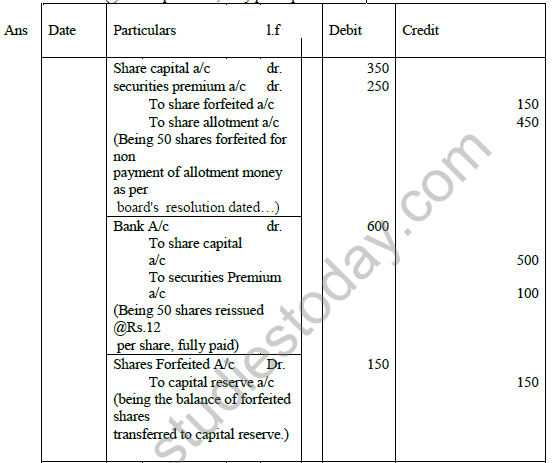

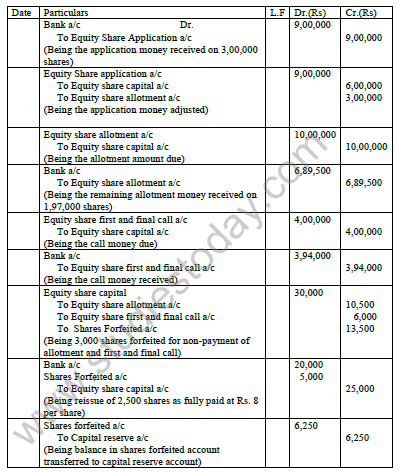

Q.16 50 shares of Rs. 10 each, issued at as premium of Rs. 5 per share, were forfeited by sohan Ltd. for the nonpayment of allotment money of Rs.9 per share (including premium). The first and final call on these shares at Rs. # per share was not made. Forfeited shares were re-issued @ Rs. 12 per share, fully paid up. Journalise

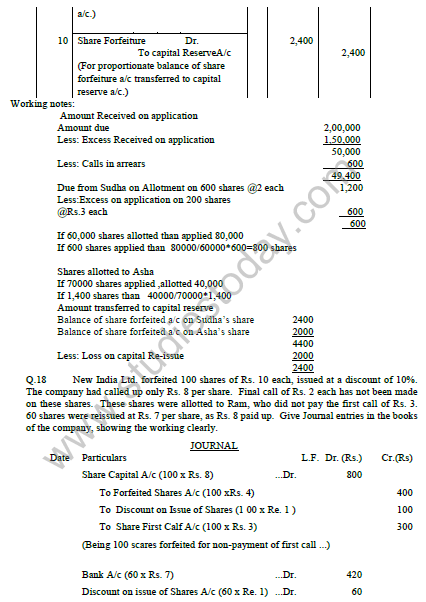

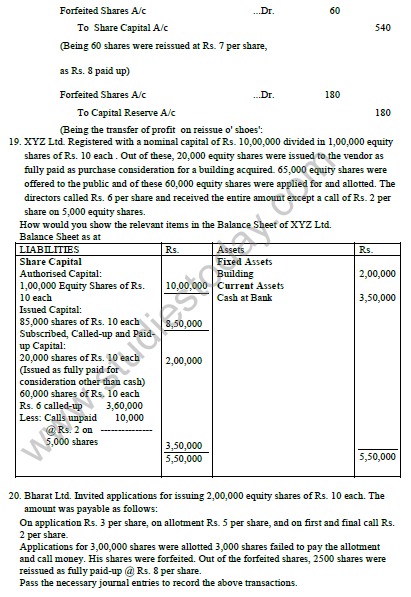

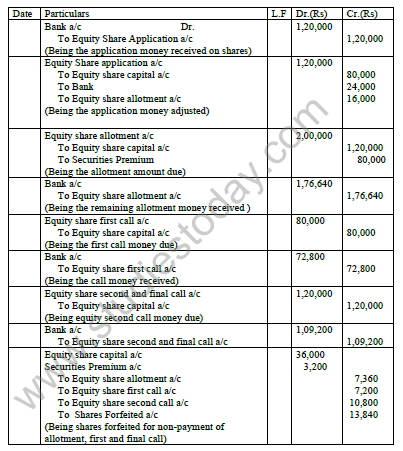

Q17 AB Ltd. Invited applications for issuing 1,00,000 equity shares of Rs. 10 each. The amount was payable as follows: On Application Rs.3 per share; On allotment Rs.2 per share; and on 1st and final call Rs.5 per share. Applications for 1,50,000 shares were received and prorata allotment was made to all applicants as follows: Application for 80,000 shares were allotted 60,000 shares on pro-rata basis ; Application for 70,000 shares were allotted 40,000 shares on pro-rata basis; Sudha to whom 600 shares were allotted out of the group 80,000 shares failed to pay allotment money. Her shares were forfeited immediately after allotment. Asha who had applied for 1,400 share out of the group 70,000 shares failed to pay the first and final call.Her shares were also forfeited. Out of forfeited shares 1,000 shares were reissued @ Rs.8 per share fully paid up The reissued shares included all the forfeited shares of Sudha. Pass necessary journal entries to record the above transaction

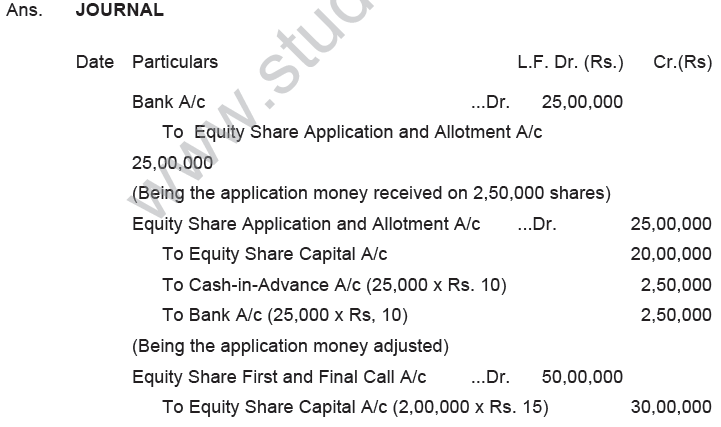

21. Alpha Ltd issued for public subscription 40,000 equity shares of Rs. 10 each. At a premium of Rs. 2 per share payable as under:

On application Rs. 2 per share, on allotment Rs. 5 per share (including premium), on first call Rs. 2 per share and on second call Rs. 3 per share. Applications were received for 60,000 shares. Allotment was made pro rata basis to the

applicants for 48000 shares, the remaining applications being refused. Money overpaid on application was applied towards sums due on allotment.

A, to whom 1,600 shares were allotted, failed to pay the allotment money and B, to whom 2,000 shares were allotted failed to pay the two calls. These were subsequently forfeited after the second call was made. Pass journal entries.

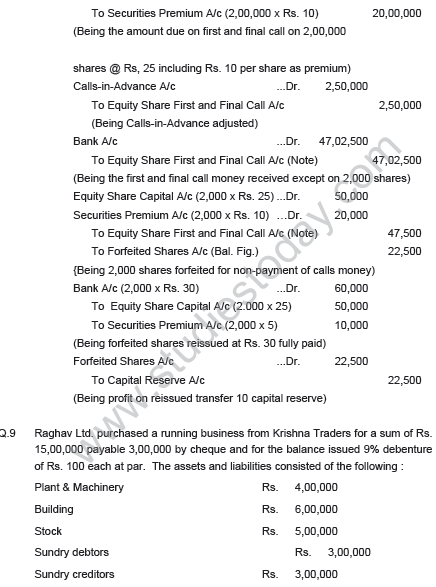

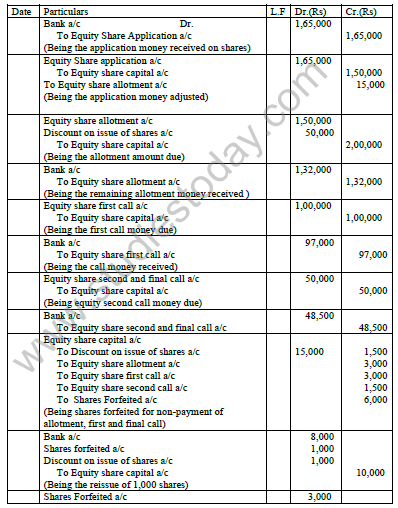

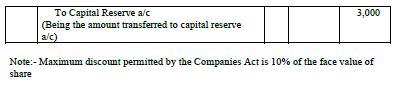

22. A limited company invites applications for 50,000 equity shares of Rs. 10 each, at a maximum discount by the Companies Act, payable as follows:

On application Rs. 3; on allotment Rs. 3; on first call Rs. 2; on final call the balance. Applications were received for 55,000 shares. Allotments were made on the following basis:

(i) To applicants for 35,000 shares- in full(ii) To applicants for 20,000 shares- 15,000 shares.

Excess money paid on application was utilized towards allotment money. A shareholder who was allotted 1,500 shares out of the group applying for 20,000 shares failed to pay allotment money and money due on calls. These shares were forfeited. 1,000 forfeited shares were reissued as fully paid on receipt of Rs. 8 per share. Show the journal in the books of the company

Free study material for Accountancy

HOTS for Part 2 Chapter 1 Accounting for Share Capital Accountancy Class 12

Students can now practice Higher Order Thinking Skills (HOTS) questions for Part 2 Chapter 1 Accounting for Share Capital to prepare for their upcoming school exams. This study material follows the latest syllabus for Class 12 Accountancy released by CBSE. These solved questions will help you to understand about each topic and also answer difficult questions in your Accountancy test.

NCERT Based Analytical Questions for Part 2 Chapter 1 Accounting for Share Capital

Our expert teachers have created these Accountancy HOTS by referring to the official NCERT book for Class 12. These solved exercises are great for students who want to become experts in all important topics of the chapter. After attempting these challenging questions should also check their work with our teacher prepared solutions. For a complete understanding, you can also refer to our NCERT solutions for Class 12 Accountancy available on our website.

Master Accountancy for Better Marks

Regular practice of Class 12 HOTS will give you a stronger understanding of all concepts and also help you get more marks in your exams. We have also provided a variety of MCQ questions within these sets to help you easily cover all parts of the chapter. After solving these you should try our online Accountancy MCQ Test to check your speed. All the study resources on studiestoday.com are free and updated for the current academic year.

FAQs

You can download the teacher-verified PDF for CBSE Class 12 Accountancy HOTs Accounting For Share Capital from StudiesToday.com. These questions have been prepared for Class 12 Accountancy to help students learn high-level application and analytical skills required for the 2026-27 exams.

In the 2026 pattern, 50% of the marks are for competency-based questions. Our CBSE Class 12 Accountancy HOTs Accounting For Share Capital are to apply basic theory to real-world to help Class 12 students to solve case studies and assertion-reasoning questions in Accountancy.

Unlike direct questions that test memory, CBSE Class 12 Accountancy HOTs Accounting For Share Capital require out-of-the-box thinking as Class 12 Accountancy HOTS questions focus on understanding data and identifying logical errors.

After reading all conceots in Accountancy, practice CBSE Class 12 Accountancy HOTs Accounting For Share Capital by breaking down the problem into smaller logical steps.

Yes, we provide detailed, step-by-step solutions for CBSE Class 12 Accountancy HOTs Accounting For Share Capital. These solutions highlight the analytical reasoning and logical steps to help students prepare as per CBSE marking scheme.