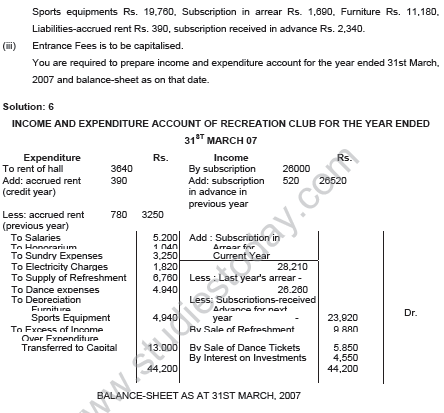

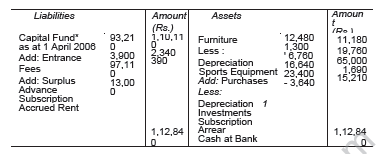

Refer to CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation. We have provided exhaustive High Order Thinking Skills (HOTS) questions and answers for Class 12 Accountancy Part 1 Chapter Accounting for Not-for-Profit Organisation. Designed for the 2026-27 exam session, these expert-curated analytical questions help students master important concepts and stay aligned with the latest CBSE, NCERT, and KVS curriculum.

Part 1 Chapter Accounting for Not-for-Profit Organisation Class 12 Accountancy HOTS with Solutions

Practicing Class 12 Accountancy HOTS Questions is important for scoring high in Accountancy. Use the detailed answers provided below to improve your problem-solving speed and Class 12 exam readiness.

HOTS Questions and Answers for Class 12 Accountancy Part 1 Chapter Accounting for Not-for-Profit Organisation

1. A non profit organisation follows hybrid system of accounting. Do you agree with this.

Ans.Yes. A non profit organisation follow the combina-tion of cash and accrual system ie, hybrid system.

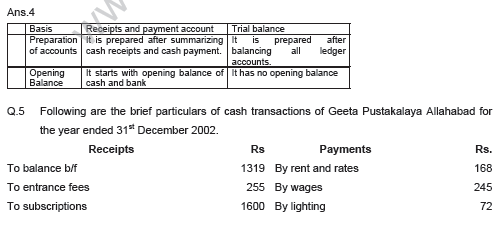

2. Receipts and Payments Account is similar to a cash book. Do you agree? Comment.

Ans Yes, it is similar to a cash book and hence it serves the purpose of a cash book. All cash transactions, whether revenue or capital in nature are accounted for. This accounts begins with opening balance of cash and gives the cash balance at the end of the pe-riod.

HOTS (HIGHER ORDER THINKING SKILLS)

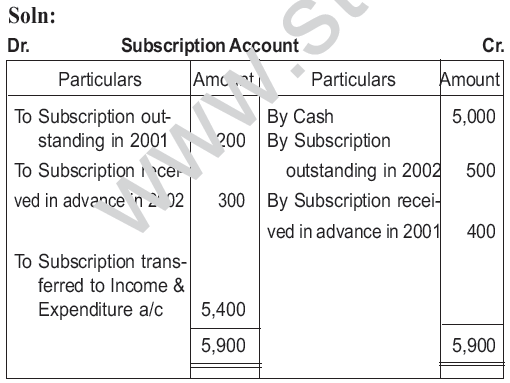

3. From the following particulars calculate the total amount of subscription to be credited to Income and Expenditure account for the year 2002.

Rs.

Subscription received during 2002 - 5,000

Subscription outstanding in 2001 - 200

Subscription outstanding in 2002 - 500

Subscription received in advance in 2001 - 400

Subscription received in advance in 2002 - 300

Solution:

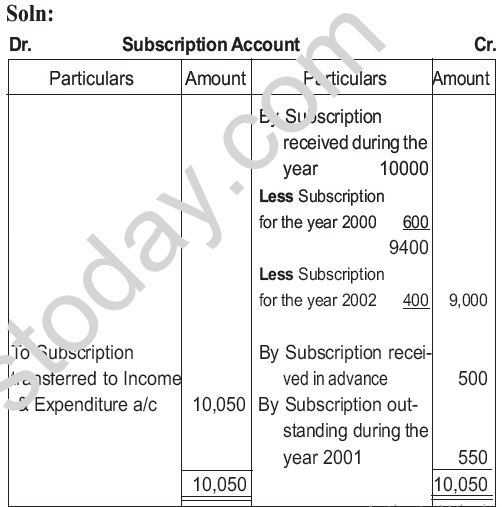

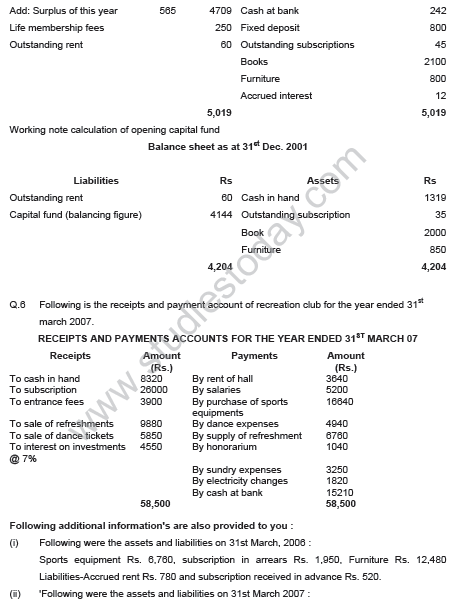

4. From the following particulars, prepare a sub-scription account for the year 2001, total subscription received during the year 2001 is Rs. 10,000 (including Rs. 600 for the year 2,000 and Rs. 400 for the year 2002). Subscription received in advance in the year 2000 for the year 2001 was amounted to Rs. 500. Subscriptions outstanding during the year 2001 is Rs. 550.

ACCOUNTING FOR – NOT FOR PROFIT ORGANISATIONS

1 Mark Questions

Free study material for Accountancy

HOTS for Part 1 Chapter Accounting for Not-for-Profit Organisation Accountancy Class 12

Students can now practice Higher Order Thinking Skills (HOTS) questions for Part 1 Chapter Accounting for Not-for-Profit Organisation to prepare for their upcoming school exams. This study material follows the latest syllabus for Class 12 Accountancy released by CBSE. These solved questions will help you to understand about each topic and also answer difficult questions in your Accountancy test.

NCERT Based Analytical Questions for Part 1 Chapter Accounting for Not-for-Profit Organisation

Our expert teachers have created these Accountancy HOTS by referring to the official NCERT book for Class 12. These solved exercises are great for students who want to become experts in all important topics of the chapter. After attempting these challenging questions should also check their work with our teacher prepared solutions. For a complete understanding, you can also refer to our NCERT solutions for Class 12 Accountancy available on our website.

Master Accountancy for Better Marks

Regular practice of Class 12 HOTS will give you a stronger understanding of all concepts and also help you get more marks in your exams. We have also provided a variety of MCQ questions within these sets to help you easily cover all parts of the chapter. After solving these you should try our online Accountancy MCQ Test to check your speed. All the study resources on studiestoday.com are free and updated for the current academic year.

FAQs

You can download the teacher-verified PDF for CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation from StudiesToday.com. These questions have been prepared for Class 12 Accountancy to help students learn high-level application and analytical skills required for the 2026-27 exams.

In the 2026 pattern, 50% of the marks are for competency-based questions. Our CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation are to apply basic theory to real-world to help Class 12 students to solve case studies and assertion-reasoning questions in Accountancy.

Unlike direct questions that test memory, CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation require out-of-the-box thinking as Class 12 Accountancy HOTS questions focus on understanding data and identifying logical errors.

After reading all conceots in Accountancy, practice CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation by breaking down the problem into smaller logical steps.

Yes, we provide detailed, step-by-step solutions for CBSE Class 12 Accountancy HOTs Accounting for Not-for- Profit Organisation. These solutions highlight the analytical reasoning and logical steps to help students prepare as per CBSE marking scheme.