Practice CBSE Class 12 Accountancy Case Study Questions Accounting For Share Capital MCQs provided below. The MCQ Questions for Class 12 Chapter 1 Accounting for Share Capital Accountancy with answers and follow the latest CBSE/ NCERT and KVS patterns. Refer to more Chapter-wise MCQs for CBSE Class 12 Accountancy and also download more latest study material for all subjects

MCQ for Class 12 Accountancy Chapter 1 Accounting for Share Capital

Class 12 Accountancy students should review the 50 questions and answers to strengthen understanding of core concepts in Chapter 1 Accounting for Share Capital

Chapter 1 Accounting for Share Capital MCQ Questions Class 12 Accountancy with Answers

Case Study

Read the following statement carefully and give the answer for the questions

Golden Firework Ltd is authorised to issue shares 5,00,000 of ₹ 100 each. Company raised the capital by issue of 2,00,000 shares through e-IPO. As per the decision of Managing Board of Directors ofcompany, company issued 75,000 shares to their parent company and 40,000 shares issued to existing employees of company as per their choice and option at the below price than the market price.

Question. “40,000 shares issued to existing employees of company as per their choice and option at the below price than the market price.” Is an example of _______

(a) Public Issue

(b) Private Placement

(c) ESOP

(d) Issue other than cash

Answer: B

Question. “Company issued 75,000 shares to their parent company” is an example of ______.

(a) Public Issue

(b) Private Placement

(c) ESOP

(d) Issue other than cash

Answer: B

Read the following statement carefully and give the answer for the questions

X Ltd issued 2,00,000 shares of ₹ 100 each. Amount to be paid on Application ₹ 30 per share; on allotment ₹ 40 per share and on first & final call ₹ 30 per share.

All money was duly subscribed and paid towards the nominal value of shares except on 9,000 shares who failed to pay allotment and calls money. These shares were forfeited. 5,000 shares were re-issued at ₹ 80 per share fully paid.

Question. Which amount the following will be called paid up share capital?

(a) ₹ 1,96,00,000

(b) ₹ 1,97,20,000

(c) ₹ 2,00,00,000

(d) ₹ 1,97,70,000

Answer: A

Question. Which amount of the following, balancein Share Forfeiture Account?

(a) ₹ 4,00,000

(b) ₹ 1,50,000

(c) ₹ 1,20,000

(d) ₹ 50,000

Answer: C

Question. Which amount of the following will be shown into the Balance Sheet of the company under the sub-head “Share Capital”?

(a) ₹ 1,96,00,000

(b) ₹ 1,97,20,000

(c) ₹ 2,00,00,000

(d) ₹ 1,97,70,000

Answer: B

Question. Which one of the following is a permanent representative personal account of share-holders?

(a) Share Application A/c

(b) Share Allotment A/c

(c) Share Application & Allotment A/c

(d) Share Capital A/c

Answer: D

Question. Which of the following is a temporary representative personal account of shareholders?

(a) Share Application A/c

(b) Share Allotment A/c

(c) Share Application & Allotment A/c

(d) All of these

Answer: D

Question. Which amount of the following will be transferred to Capital Reserve?

(a) ₹ 4,00,000

(b) ₹ 1,50,000

(c) ₹ 1,20,000

(d) ₹ 50,000

Answer: D

Question. Received share application money towards application & allotment of shares will be credited to which of the following account?

(a) Share Application & Allotment A/c

(b) Share Application A/c

(c) Share Capital A/c

(d) None of these

Answer: A

Question. Ashok a shareholder of a company allotted shares to whom 12,000 of ₹ 100 each, failed to pay allotment ₹ 30 per share and first & final call ₹ 30 per share. Ashok had paid only application money. Pro-rata allotment proportion is 5:6. What will be the amount of calls-in arrears on allotment, from the following:

(a) ₹ 3,60,000

(b) ₹ 2,64,000

(c) ₹ 96,000

(d) None of these

Answer: B

Question. A shareholder failed to pay share allotment money on 12,000 shares @ ₹ 30 per share. Which one of the following account will be taken into account?

(a) Debited to Share Capital A/c

(b) Debited to Calls-in Arrears A/c

(c) Credited to Calls-in Arrears A/c

(d) Credited to Share Capital A/c

Answer: B

Read the information given below and give the answer for the questions

X Ltd issued 50,000 shares of ₹ 100 per share for public subscriptions at 20% premium. Amount payable as under:

On Application : ₹ 40 per share (including 10% premium)

On Allotment : ₹ 40 per share (excluding 10% premium)

On First & Final Call : ₹ Balance

Application received for 75,000 shares. Allotment was made to 60,000 share applicants. All due money was duly received except from a shareholder (Ashok) allotted to whom 12,000 shares, failed to pay allotment and calls. These shares were forfeited.

Question. What the amount received on allotment?

(a) ₹ 15,96,000

(b) ₹ 21,00,000

(c) ₹ 5,04,000

(d) ₹ 4,00,000

Answer: A

Question. Which of the following amount did not receive on allotment?

(a) ₹ 15,96,000

(b) ₹ 21,00,000

(c) ₹ 5,04,000

(d) ₹ 4,00,000

Answer: C

Question. What the amount forfeited on 12,000 shares?

(a) ₹ 5,76,000

(b) ₹ 4,56,000

(c) ₹ 5,04,000

(d) ₹ 4,00,000

Answer: B

Question. Which of the following Excess application money adjusted on allotment?

(a) 10,00,000

(b) 6,00,000

(c) 4,00,000

(d) None of these

Answer: C

Question. Once, forfeited shares reissued, balance of share forfeiture money will be transferred to ___

(a) General Reserve

(b) Capital Reserve

(c) Reserve Capital

(d) Securities Premium Reserve

Answer: B

Question. The allowed amount of discount on re-issue of shares will be _____

(a) @ 10% of issue price

(b) Up to the amount of forfeited money

(c) Could not issue at discount

(d) None of these

Answer: B

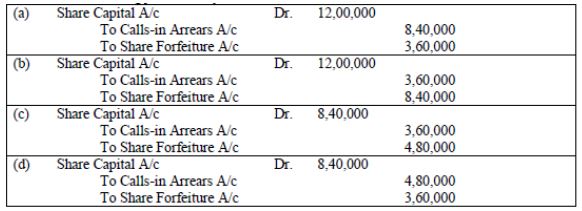

Question. 12,000 shares of ₹ 100 each forfeited due to nonpayment of ₹ 40 per share. First & final call of₹ 30 per share not yet made. These shares were reissued at ₹ 80 per share for ₹ 70 per share.Which of the following journal entry is correct for the forfeiture of shares?

Answer: A

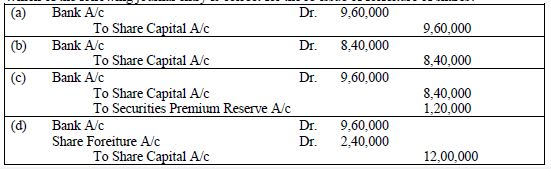

Question. 12,000 shares of ₹ 100 each forfeited due to nonpayment of ₹ 40 per share. First & final call of₹ 30 per share not yet made. These shares were reissued at ₹ 80 per share for ₹ 70 per share.Which of the following journal entry is correct for the re-issue of forfeiture of shares

Answer: C

Question. 12,000 shares of ₹ 100 each forfeited due to nonpayment of ₹ 40 per share. First & final call of₹ 30 per share not yet made. These shares were reissued at ₹ 80 per share for ₹ 70 per share.Which of the following forfeited amount will be transferred to Capital Reserve A/c?

(a) 4,80,000

(b) 3,60,000

(c) 1,20,000

(d) None of these

Answer: B

Question. If the premium on forfeited shares has already been received, then securities premium reserve account should be:

(a) Credited

(b) Debited

(c) No treatment

(d) Transferred to Capital Reserve A/c

Answer: C

Question. A company issued 40,000 preference shares of ₹ 100 per share at par payable as under:

On Application : 20%

On Allotment : 40%

On First & Final Call : balance

Applications were received for 50,000 shares. Allotment was made on pro-rata basis. How much amount will be received in cash on allotment?

(a) 14,00,000

(b) 16,00,000

(c) 18,00,000

(d) 20,00,000

Answer: A

Question. 12,000 shares of ₹ 100 each forfeited due to nonpayment of allotment of ₹ 40 per share and first & final call of ₹ 30 per share. Out of the forfeited shares, 9,000 shares were reissued at ₹ 80 per share fully paid.

Which of the following amount of share forfeiture account will be transferred to Capital Reservee Account? 1,80,000

(a) 90,000

(b) 1,80,000

(c) 3,60,000

(d) 2,70,000

Answer: A

Read the following information carefully and give the answer for the questions

AB Ltd issued 3,00,000 shares of ₹ 100 each at 20% premium through e-IPO, payable as under:

On Application : ₹ 40 (including 10% premium) per share

On Allotment : ₹ 40 (excluding 10% premium) per share

On First & Final Call : Balance

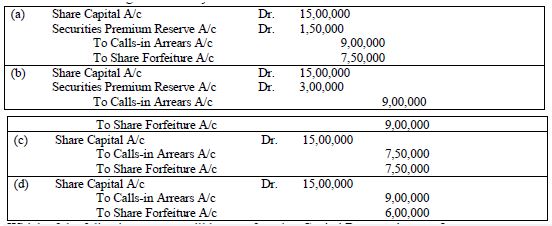

Share was subscribed for 5,00,000 shares. 50,000 share applications were rejected with letter of regret and pro-rata allotment was made to remaining share applicants. All money was duly received except from Raghav, allotted to whom 15,000 shares failed to pay allotment and calls.These shares were forfeited and out of which 9,000 shares reissued at ₹ 75 per share fully paid.

Question. Which of the following amount received on allotment of shares?

(a) ₹ 1,50,00,000

(b) ₹ 90,00,000

(c) ₹ 45,00,000

(d) ₹ 85,50,000

Answer: D

Question. Which of the following amount will be debited to calls-in arrears account on allotment?

(a) ₹ 6,00,000

(b) ₹ 4,50,000

(c) ₹ 3,00,000

(d) ₹ 7,50,000

Answer: B

Question. What the amount was called in first & final call per share?

(a) ₹ 20 per share

(b) ₹ 40 per share

(c) ₹ 30 per share

(d) None of these

Answer: C

Question. Which of the following Journal entry is correct for the forfeiture of shares?

Answer: A

Question. Which of the following amount will be transferred to Capital Reserve Account?

(a) ₹ 7,50,000

(b) ₹ 6,00,000

(c) ₹ 4,50,000

(d) ₹ 2,25,000

Answer: D

Question. Golden Fire Works Ltd took over assets worth ₹ 10,00,000 and liabilities of ₹ 3,00,000 of a company. Out of the purchase consideration of ₹ 12,00,000; ₹ 2,00,000 of bill payable accepted and the balance paid by issue of shares of ₹ 100 each at 25% premiumHow much amount will be credited to Securities Premium Reserve A/c?

(a) ₹ 1,75,000

(b) ₹ 2,50,000

(c) ₹ 3,00,000

(d) ₹ 2,00,000

Answer: B

Question. A, B and C are partners sharing profits in the ratio of 3:2:1. They are agreed to admit D into the partnership for 1/4th share. An extract of their balance sheet on 1st April, 2021 is as follows:

If the market value of Investments is ₹ 4,20,000 then the Investment Fluctuation Fund will be shown in the Balance Sheet of reconstituted firm at ₹ _____.

(a) 40,000

(b) 20,000

(c) Zero

(d) None of these

Answer: C

Question. Match the columns with reference to share capital of a company.

(a) (iii) (iv) (ii) (i)

(b) (ii) (iv) (i) (iii)

(c) (ii) (i) (iii) (iv)

(d) (i) (ii) (iii) (iv)

Answer: A

Question. AB Ltd purchased a Machinery from XY Ltd for ₹ 4,50,000. AB Ltd immediately paid ₹ 90,000 by Bank Draft and the balance by issue of preference share of ₹ 100 each at 20% premium for the purchase consideration of Machinery to XY Ltd. Shares issued by AB Ltd?

(a) 3,000 preference shares

(b) 30,000 preference shares

(c) 3,600 preference shares

(d) 36,000 preference shares

Answer: A

Case Study

Anant and his 10 friends formed a Whatsapp group to discuss the Covid situations and decided to help the society somehow. They thought of starting with a venture where they can help the affected persons required medicines and oxygen cylinders at genuine prices.

They wanted to make an App for Android as well as I-Phones as that the patients or their family members can fill their requirements quite easily.. They also need to make contacts with some genuine medical stores of the country so that the medicines to be supplied timely at genuine prices.

They need funds of Rs. 15,00,000 for IT work as well as working capital requirements. But they had only Rs.2,00,000 with them. They discussed the idea with their friend Varun who was Chartered Accountant. Varun suggested that they should start a public company and invite the general public to finance in their project. Since the project is profitable as well as beneficial for the masses, so good number of investors will be interested in buying the shares of such company. For all the necessary formalities of starting a company like applying for starting a company with Registrar of Companies as well as making important documents like Memorandum of Association, Articles of Association and Prospectus the amount they had i.e Rs.2,00,000 was sufficient. So these friends acted as promoters and suggested the name of company as Get Well Soon Ltd. which was approved by Registrar. Registrar approved the required authorised capital as filled by them in application form as Rs.50,00,000 divided in to 5,00,000 shares of Rs.10 each.

After incorporation, Get Well Soon Ltd. invited applications for 1,50,000 shares of Rs.10 each. The company also issued 10,000 shares to promoters for their services. Share was payable as Rs.3 on application, Rs.4 on allotment and balance on call. Since the project was social and beneficial for the society so their shares were over-subscribed and the company received applications for 2,40,000 shares. Pro-rata allotment was made to applicants in proportion of 4:3 and remaining applications were sent letter of regret.

Mr. Sultan holding 6,000 shares failed to pay allotment money and his shares were immediately forfeited. After this call was made and received by the company except by Mr. Baadshah holding 3,000 shares. Later on 4,000 shares were re-issued @Rs.12 per share as fully paid up.

Answer the following questions on the basis of above mentioned information.

Question. Money received at the time of allotment received was :-

(a) Rs.6,00,000

(b) Rs.4,50,000

(c) Rs.4,26,000

(d) Rs.4,32,000

Answer: D

Question. Amount to be refunded at the time of Application money utilised was :-

(a) Rs.2,70,000

(b) Rs.1,20,000

(c) Rs.1,50,000

(d) None of the above

Answer: B

Question. Amount forfeited of Mr. Sultan was :-

(a) Rs.18,000

(b) Rs.24,000

(c) Rs.32,000

(d) Rs.6,000

Answer: B

Question. Amount received on First call was :-

(a) Rs.4,50,000

(b) Rs.4,41,000

(c) Rs.4,32,000

(d) Rs.4,23,000

Answer: D

Question. Amount due on First call was :-

(a) Rs.4,50,000

(b) Rs.4,41,000

(c) Rs.4,32,000

(d) Rs.4,23,000

Answer: C

Question. Remaining 2,000 shares can be issued at a minimum re-issue amount/price of Rs.._____

(a) Rs.8,000 (Rs.4 per share)

(b) Rs.12,000 (Rs.6 per share)

(c) Rs.20,000 (Rs.10 per share)

(d) Rs.4,000 (Rs.2 per share)

Answer: B

Free study material for Accountancy

MCQs for Chapter 1 Accounting for Share Capital Accountancy Class 12

Students can use these MCQs for Chapter 1 Accounting for Share Capital to quickly test their knowledge of the chapter. These multiple-choice questions have been designed as per the latest syllabus for Class 12 Accountancy released by CBSE. Our expert teachers suggest that you should practice daily and solving these objective questions of Chapter 1 Accounting for Share Capital to understand the important concepts and better marks in your school tests.

Chapter 1 Accounting for Share Capital NCERT Based Objective Questions

Our expert teachers have designed these Accountancy MCQs based on the official NCERT book for Class 12. We have identified all questions from the most important topics that are always asked in exams. After solving these, please compare your choices with our provided answers. For better understanding of Chapter 1 Accounting for Share Capital, you should also refer to our NCERT solutions for Class 12 Accountancy created by our team.

Online Practice and Revision for Chapter 1 Accounting for Share Capital Accountancy

To prepare for your exams you should also take the Class 12 Accountancy MCQ Test for this chapter on our website. This will help you improve your speed and accuracy and its also free for you. Regular revision of these Accountancy topics will make you an expert in all important chapters of your course.

FAQs

You can get most exhaustive CBSE Class 12 Accountancy Case Study Questions Accounting For Share Capital MCQs for free on StudiesToday.com. These MCQs for Class 12 Accountancy are updated for the 2026-27 academic session as per CBSE examination standards.

Yes, our CBSE Class 12 Accountancy Case Study Questions Accounting For Share Capital MCQs include the latest type of questions, such as Assertion-Reasoning and Case-based MCQs. 50% of the CBSE paper is now competency-based.

By solving our CBSE Class 12 Accountancy Case Study Questions Accounting For Share Capital MCQs, Class 12 students can improve their accuracy and speed which is important as objective questions provide a chance to secure 100% marks in the Accountancy.

Yes, Accountancy MCQs for Class 12 have answer key and brief explanations to help students understand logic behind the correct option as its important for 2026 competency-focused CBSE exams.

Yes, you can also access online interactive tests for CBSE Class 12 Accountancy Case Study Questions Accounting For Share Capital MCQs on StudiesToday.com as they provide instant answers and score to help you track your progress in Accountancy.