Practice CBSE Class 12 Accountancy Case Study Questions Financial Statements of a Company MCQs provided below. The MCQ Questions for Class 12 Chapter 3 Financial Statement Of Companies Accountancy with answers and follow the latest CBSE/ NCERT and KVS patterns. Refer to more Chapter-wise MCQs for CBSE Class 12 Accountancy and also download more latest study material for all subjects

MCQ for Class 12 Accountancy Chapter 3 Financial Statement Of Companies

Class 12 Accountancy students should review the 50 questions and answers to strengthen understanding of core concepts in Chapter 3 Financial Statement Of Companies

Chapter 3 Financial Statement Of Companies MCQ Questions Class 12 Accountancy with Answers

Question. Main limitation of analysis of financial statements is

(a) Affected by window dressing

(b) Difficulty in forecasting

(c) Do not reflect changes in price level

(d) All of the options

Answer: D

Question. ………appear in a Company’s Balance Sheet under the Sub-head Short-term Provision

(a) Interest Accrued but not due on Borrowings

(b) Provision for Tax

(c) Unpaid Dividend

(D) Calls in Advance

Answer: B

Question. Main objective of analysis of financial statements is:

(a) To know the financial strength

(b) To make a comparative study with other firms

(c) To know the efficiency of management

(d) All of the options

Answer: D

Question. Amount provided for any known liability whose amount as yet isuncertain is known as:

(a) Liability

(b) Reserve

(c) Provision

(d) None of the options

Answer: C

Question. The assets which cannot be realised incash or from which no further benefit can be derived are known as:

(a) Tangible asset

(b) Fictitious asset

(c) Intangible asset

(d) None of the options

Answer: B

Question. Financial analysis becomes significant because it:

(a) Ignores price level changes

(b) Measures the efficiency of business

(c) Lacks qualitative analysis

(d) Is effected by personal bias

Answer: B

Question. Change in Inventories means :

(a) Difference between Opening Inventories and Closing Inventories

(b) Difference between Closing Inventories and Opening Inventories

(c) Difference between Opening Inventories and Closing Inventories, if Opening Inventories are higher

(d) Difference between Closing Inventories and Opening Inventories, if Closing Inventories are higher.

Answer: A

Question. What will be the amount shown under the head current liabilities when the following data is given?

Short-term borrowings = ₹ 2,00,000

Trade Payables = ₹ 1,00,000

Other Current Liabilities = ₹ 1,50,000,

Short-term Provisions = ₹ 20,000

(a) ₹ 5,00,000

(b) ₹ 600,000

(c) ₹ 2,00,000

(d) ₹ 4,70,000

Answer: D

Question. Bank overdraft and cash credit are treated as ‘short-term borrowings’ in the balance sheet of a company.

(a) True

(b) False

(c) Partially true

(d) Can’t say

Answer: A

Question. Livestock is an item of……… under sub-head fixed asset and the major head non-current assets.

(a) tangible assets.

(b) inventories

(c) trade receivables

(d) intangible

Answer: A

Question. According to prescribed order of assets in a Company’s Balance Sheet ……………………… assets should be shown first of all.

(a) Non-Current Assets

(b) Current Assets

(c) Current Investments

(d) Loans and Advances

Answer: A

Question. Calls in advance appear in a Company’s Balance Sheet under ………………..

(a) Share Capital

(b) Current Liability

(c) Long-term Borrowings

(d) Reserve & Surplus

Answer: B

Question. Goodwill of a company amounting to 35,000 is shown on the assets side of the balance sheet under which of the following head?

(a) Non-current assets

(b) Current assets

(c) Non-current liabilities

(d) None of the options

Answer: A

Question. Which of the following points out nature of financial statements?

(i) Financial statements are prepared on the basis of recorded facts.

(ii) Certain accounting conventions are followed while preparing financial statements.

(iii) Financial statements are prepared on certain basic assumptions (pre-requisites) known as postulates.

(iv) Facts and figures presented through financial statements are based on personal opinion, esti-mates and judgements.

(a) Only (i)

(b) (i), and (ii)

(c) (i), (ii) and (iii)

(d) (i), (ii), (iii) and (iv)

Answer: D

Question. Assertion (A) Analysis of financial statements is done to assess the managerial efficiency.

Reason (R) Financial statement analysis helps to identify the areas where the managers have been efficient and the areas where they have been inefficient.

Options:

(a) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion(A)

(b) Both Assertion (A) and Reason (R) are true but Reason (R) is not the correct explanation of Assertion (A)

(c) Assertion (A)is false, but Reason (R) is true

(d) Assertion (A ) is true, but Reason (R) is false

Answer: A

Question. Assertion (A) Bills receivable are shown as trade receivables in the balance sheet of the company.

Reason (R) Debtors and bills receivable forms the part of trade receivables.

Options:

(a) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion(A)

(b) Both Assertion (A) and Reason (R) are true but Reason (R) is not the correct explanation of Assertion (A)

(c) Assertion (A)is false, but Reason (R) is true

(d) Assertion (A ) is true, but Reason (R) is false

Answer: A

Question. Assertion (A) The bank charges charged by the bank are included in finance cost.

Reason (R) Bank charges are an expense not incurred in connection with raising finance but for availing the services of the bank.

Options:

(a) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion(A)

(b) Both Assertion (A) and Reason (R) are true but Reason (R) is not the correct explanation of Assertion (A)

(c) Assertion (A)is false, but Reason (R) is true

(d) Assertion (A ) is true, but Reason (R) is false

Answer: C

Direction : Read the following case study and answer below questions on the basis of the same.

Care Ltd is a company that deals in manufacturing of pharmaceutical products. Dev has recently been hired as an assistant to the accountant of Care Ltd. The accountant of the firm Mr. Raj asks Dev to go for financial statement analysis to assess the financial position of the firm. To judge the knowledge and capabilities of Dev, Mr. Raj asked him to analyze the financial statements from the view point various parties interested in the firm like the management, the lenders, the inves-tors, government etc.

Question. If Dev is to analyse the financial statements for the short-term lenders, what should he consider?

(a) Short-term liquidity of the firm

(b) Long-term solvency of the firm

(c) The resources of the firm are used most efficiently and that the firm’s financial condition is sound

(d) None of the options

Answer: A

Question. Which of the following statements will primarily be utilised by Dev for the purpose of finan-cial statement analysis?

(a) Balance sheet and cash flow statement.

(b) statement of profit and loss and cash flow statement

(c) balance sheet and statement of profit and loss

(d) cash flow statement and fund flow statement.

Answer: C

Question. While analysing the financial statements, Dev should be conscious of which of the following?

(a) Changes in accounting policies of the firm

(b) Personal judgements

(c) Window dressing of financial statements

(d) All of the options

Answer: D

Question. If Dev is to analyse the financial statements for the top management, what should he consider?

(a) Short-term liquidity of the firm.

(b) Ability to pay its long-term lenders.

(c) The resources of the firm are used most efficiently and that the firm’s financial condition is sound.

(d) None of the options

Answer: C

Question. If Dev is to analyse the financial statements for the investors, what should he consider?

(a) Firm’s present and future profitability

(b) Ability to pay its long-term lenders

(c) Firm’s capital structure

(d) Both (a) and (c)

Answer: D

Question. Match the following:

(a) Interest paid on debentures (i) depreciation

(b) Fixed assets written off over their useful life (ii) other expenses

(c) cheques (iii) financial cost

(d) discount allowed (iv) other current liabilities

Answer: a (iii), b (i), c (iv), d (ii)

Question. State the importance of Financial Analysis?

Answer: Financial Analysis has great importance to various accounting users on various mat-ters. Income Statements, Balance Sheets and other financial data provides information about expenses and sources of income, profit or loss and also helps in assessing the financial position of a business. These financial data are not useful until they are ana-lysed. There are various tools and methods such as Ratio Analysis, Cash Flow State-ments that make the financial data to cater varying needs of various accounting users.

The following are the reasons that advocate in favour of Financial Analysis:

1. It helps in evaluating the profit earning capacity and financial feasibility of a business.

2. It helps in assessing the long-term solvency of the business.

3. It helps in evaluating the relative financial status of a firm in comparison to other competitive firms.

4. It assists management in decision making process, drafting various plans and also in establishing an effective controlling system.

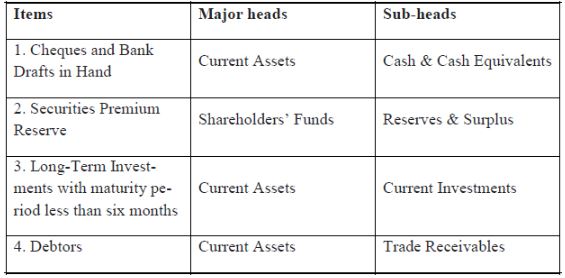

Question. Under which major heads and sub-heads will the following items be placed in the Balance Sheet of the company as per Schedule III, Part I of the Companies Act, 2013?

(i) Cheques and Bank Drafts in Hand

(ii) Securities Premium Reserve

(iii) Long-Term Investments with maturity period less than six months

(iv) Debtors

Answer:

Question. State any four limitations of analysis of financial statements.

Answer: Limitations of ‘Financial Statements Analysis’:

(a) Different Accounting Principles and Practices. Financial analysis is subject to lim-itations inherent in the financial statements like following different accounting princi-ples or practices regarding depreciation methods, inventory valuation and pricing, etc.

(b) Ignores the Quality Elements. Financial statements contain only financial data and exclude from the preview of qualitative information, which cannot be expressed in money terms. Thus, analysis of such financial statements will also lack quality ele-ment.

(c) Ignores Price Level Changes. Transactions, in financial statements, are recorded on historical cost basis and generally no adjustment is made for price level changes. Thus, the analysis of financial statement will not yield comparable results due to lack of ad-justments for the price level changes.

(d) Affected by Window Dressing. Some firms may resort to window dressing (show-ing better picture) to cover-up bad financial position. For example, closing stock may be overstated. In such case, the results of analysis will also be misleading.

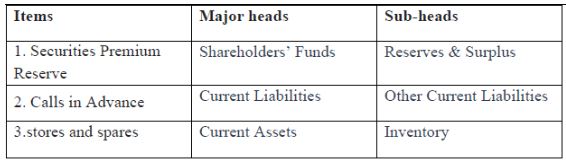

Question. K M Limited is a computer hardware manufacturing company. While preparing its accounting rec-ords it takes into consideration the various accounting principles and maintains transparency. At the end of the accounting year, the company follows the ‘Companies Act, 2013 and Rules there under’ for the preparation of its Financial Statements. It also prepares its Income Statement and Balance Sheet as per the format provided in Schedule III to the Act. Its Financial Statements depict its true & fair financial position. For the financial year ending March 31,2017, the accountant of the company is not certain about the presentation of the following items under relevant Major Heads & Sub Heads, if any, in its Balance Sheet: Present it correctly.

• Securities Premium Reserve

• Calls in Advance

• Stores & Spares

Answer:

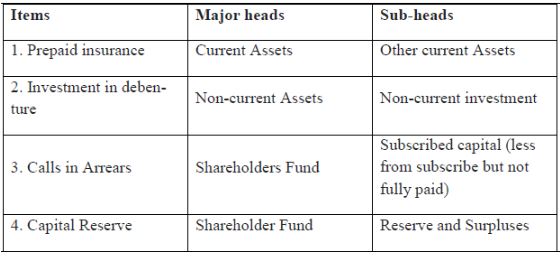

Question. State under which major headings and sub-headings will the following items be presented in the BalanceSheet of a company as per Schedule-Ill, Part-I of the Companies Act, 2013. (i) Prepaid Insurance

(ii) Investment in Debentures

(iii) Calls-in-arrears

(iv) Capital Reserve

Answer:

Question. State the objectives of ‘Analysis of Financial Statements’.

Answer: Objectives of‘Financial Statements Analysis’:

1. Assessing the earning capacity or profitability of the firm as a whole as well as its different departments so as to judge the financial health of the firm.

2. Assessing the managerial efficiency by using financial ratios to identify favourable and unfavourable variations in managerial performance.

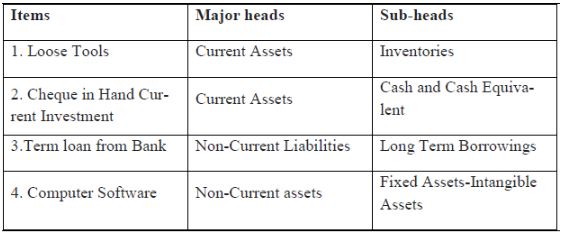

Question. W Ltd was a company manufacturing geysers. As a part of its long term goal for expansions, the company decided to identify the opportunity in rural area. Initial plan was rolled out for Bhiwani village in Haryana. Since, the village did not have regular supply of electricity, the company de-cided to manufacture solar geysers. The core team consisting of the Regional Managers, Account-ant and the Marketing Manager was taken from the Head office and the remaining employee were selected from the village and neighbourhood area. At the time of preparation of financial statement the accountant of the company fell sick and the company deputed a junior accountant temporarily from the village for two months. The Balance Sheet prepared by the junior accountant showed the following items against the Major heads and sub-head mentioned which were not as per Schedule III of the Companies Act 2013. Items Major Head

• Loose Tools -Trade Receivable

• Cheque in Hand- Current Investment

• Term Loan from Bank- Other long Term Liabilities

• Computer Software -Tangible Fixed Assets

Present the above items under the correct major head and sub-head as per the Schedule III of Companies Act 2013.

Answer:

Question. Explain the importance of financial analysis for

(i) labour unions, and

(ii) creditors

Answer: (i) Importance for Labour Unions: Labour unions analyse the financial statements to assess whether it can presently afford a wage increase and whether it can absorb a wage increase through increased productivity or by raising the prices.

(ii) Importance for Creditors: Creditors through an analysis of Financial Statements appraises not only the ‘ ability of the company to meet its short term obligations but also judges the probability of its continued ability to meet its financial obligations in future.

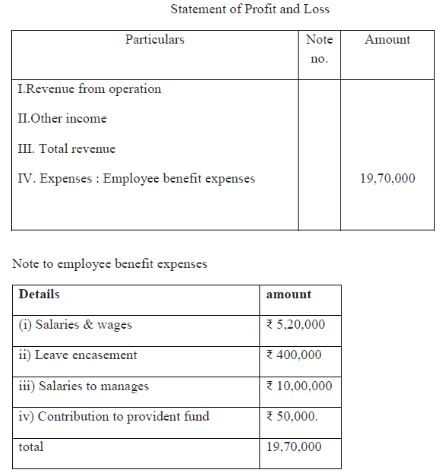

Question. How would you show ‘Employee Benefit Expenses with the help of Notes to Accounts in the Statement of Profit &Loss.

(i) Salaries & wages ₹ 5,20,000

(ii) Dividend received ₹ 5000,

(iii) Leave encasement ₹ 400,000

(iv) Salaries to manages ₹ 10,00,000

(v) Depreciation on fixed assets ₹ 200,000

(vi) Contribution to provident fund ₹ 50,000.

Answer:

Question. Which of the following is the element of financial statements?

(a) Balance Sheet

(b) Profit & Loss A/c

(c) Both (a) and (b)

(d) None of these

Answer: (c) Both (a) and (b)

Question. Which of the following is not required to be prepared under the Companies Act:

(a) Statement of Profit & Loss

(b) Balance Sheet

(c) Anditor’s Report

(d) Fund Flow Statement

Answer: (c) Anditor’s Report

Question. Equity \( Rs 90,000 \) Liabilities \( Rs 60,000 \) Profit of the year \( Rs 20,000 \). Then total assets will be :

(a) \( Rs 1,70,000 \)

(b) \( Rs 1,50,000 \)

(c) \( Rs 1,10,000 \)

(d) \( Rs 80,000 \)

Answer: (a) \( Rs 1,70,000 \)

Question. The reserve which is created for a particular (specific) purpose and which is a charge against revenue is called:

(a) Capital Reserve

(b) General Reserve

(c) Secret Reserve

(d) Specific Reserve

Answer: (d) Specific Reserve

Question. An Annual Report is issued by a company to its:

(a) Directors

(b) Authors

(c) Shareholders

(d) Management

Answer: (c) Shareholders

Question. The profit and loss disclosed by the accounts of a company is:

(a) Transferred to share capital account

(b) Shown under the head of ‘Current liabilities’ and provisions

(c) Shown under the head ‘Reserves and Surplus

(d) None of these

Answer: (c) Shown under the head ‘Reserves and Surplus

Question. The assets of a business can be classified as :

(a) Fixed and Non-fixed Assets

(b) Tangible and Intangible Assets

(c) Non-Current and Current Asset

(d) None of these

Answer: (c) Non-Current and Current Asset

Question. The term financial statements includes :

(a) Statement of Profit & Loss

(b) Balance Sheet

(c) Statement of Profit & Loss and Balance Sheet

(d) None of these

Answer: (c) Statement of Profit & Loss and Balance Sheet

Question. Balance Sheet is a :

(a) Account

(b) Statement

(c) Both (a) and (b)

(d) All the above

Answer: (b) Statement

Question. Financial statements are the product of accounting process.

(a) First

(b) Second

(c) End

(d) None of these

Answer: (c) End

Question. Financial statements disclose :

(a) Monetary information

(b) Qualitative information

(c) Non-monetary information

(d) All the above

Answer: (a) Monetary information

Question. Statement of Profit & Loss is also called………:

(a) Operating Profit

(b) Balance Sheet

(c) Income Statement

(d) Trading Account

Answer: (c) Income Statement

Question. Preliminary expenses are shown in the Balance Sheet under the head:

(a) Non-current assets

(b) Current assets

(c) Non-current liabilities

(d) Deducted from securities premium reserve

Answer: (d) Deducted from securities premium reserve

Question. Debit Balance of Profit & Loss Statement will be shown on:

(a) Assets Side of Balance Sheet

(b) Liabilities Side of Balance Sheet

(c) Under the head Reserve & Surplus

(d) Under the head Reserves and Surplus as a negative item

Answer: (d) Under the head Reserves and Surplus as a negative item

Question. Patents and copyrights fall under the category of:

(a) Current Assets

(b) Liquid Assets

(c) Intangible Assets

(d) None of these

Answer: (c) Intangible Assets

Question. Goodwill falls under which category of assets:

(a) Current Assets

(b) Tangible Assets

(c) Intangible Assets

(d) None of the above

Answer: (c) Intangible Assets

Question. Contingent Liabilities are exhibited under the heading:

(a) Fixed Liabilities

(b) Current Liabilities

(c) As a footnote

(d) None of these

Answer: (c) As a footnote

Question. Provision for Provident Funds is shown in the Balance Sheet of a company under the head :

(a) Reserves and Surplus

(b) Non-current Liabilities

(c) Provision

(d) Contingent Liabilities

Answer: (b) Non-current Liabilities

Question. Preliminary Expenses are shown in the Balance Sheet under which head ?

(a) Fixed Assets

(b) Reserves and Surplus

(c) Loans & Advances

(d) None of these

Answer: (d) None of these

Question. Financial Statements are :

(a) Anticipated facts

(b) Recorded facts

(c) Estimated facts

(d) None of these

Answer: (b) Recorded facts

Question. The term current assets includes :

(a) Stock

(b) Debtors

(c) Cash

(d) All of these

Answer: (d) All of these

Question. Which of the following is not a part of financial statement of a company ?

(a) Profit & Loss A/c

(b) Balance Sheet

(c) Ledger Account

(d) Cash Flow Statement

Answer: (c) Ledger Account

Question. Under which heading of Balance Sheet is general reserve shown:

(a) Miscellaneous Expenditure

(b) Share Capital

(c) Reserves & Surplus

(d) None of these

Answer: (c) Reserves & Surplus

Question. Current Assets on the Assets side of Balance Sheet of a Company includes:

(a) Sundry Debtors

(b) Cash in hand

(c) Stock

(d) All of these

Answer: (d) All of these

Question. As per provisions of Companies Act, 2013 under which Section, the final accounts of a company is prepard :

(a) 128

(b) 210

(c) 129

(d) 212

Answer: (c) 129

Question. According to which part of Schedule III of the Indian Companies Act, 2013, Indian companies have to prepare Balance Sheet:

(a) Part 1

(b) Part 2

(c) Part 3

(d) Part 4

Answer: (a) Part 1

Question. Balance sheet of companies is now prepared in :

(a) Horizontal Form

(b) Vertical Form

(c) Either (a) or (b) Form

(d) None of these

Answer: (b) Vertical Form

Question. Goodwill of a company is shown on the assets side of the Balance Sheet under the head.

(a) Current Assets

(b) Non-current Assets

(c) Miscellaneous Expenditure

(d) None of these

Answer: (b) Non-current Assets

Question. The form of Balance Sheet as per Companies Act, 2013 is:

(a) Horizontal

(b) Horizontal or Vertical

(c) Vertical

(d) None of these

Answer: (c) Vertical

Question. Which of the following assets is not shown undeer the head ‘Fixed Asset’ in the Balance Sheet ?

(a) Goodwill

(b) Bills Receivable

(c) Buildings

(d) Vehicle

Answer: (b) Bills Receivable

Question. Securities Premium Account is shown on the liabilities side in the Balance Sheet Under heading

(a) Reserves and Surplus

(b) Current Liabilities and Provisions

(c) Share Capital

(d) Contingent Liabilities

Answer: (a) Reserves and Surplus

Question. Debentures are shown in the Balance Sheet under the head of:

(a) Short-term Loan

(b) Secured Loan

(c) Current Liability

(d) Share Capital

Answer: (b) Secured Loan

Question. Divident is usually paid :

(a) On Authorised Capital

(b) On Ussued Capital

(c) On Paid-up Capital

(d) On Called-up Capital

Answer: (c) On Paid-up Capital

Question. Amount set aside to meet losses due to bad debts is called:

(a) Reserve

(b) Provision

(c) Liability

(d) None of these

Answer: (b) Provision

Question. Which Section of the Companies Act, 2013 requires that the Balance Sheet to be prepared in prescribed form ?

(a) Section 128

(b) Section 130

(c) Section 129

(d) Section 212

Answer: (c) Section 129

Question. The prescribe from the Balance Sheet has given in the Schedule:

(a) VI Part I

(b) VI Part II

(c) III Part I

(d) VII Part IV

Answer: (c) III Part I

Question. Share capital is shown in Balance Sheet under. the head ?

(a) Authorised Capital

(b) Issued Capital

(c) Paid-up Capital

(d) Shareholders’ Funds

Answer: (d) Shareholders’ Funds

Free study material for Accountancy

MCQs for Chapter 3 Financial Statement Of Companies Accountancy Class 12

Students can use these MCQs for Chapter 3 Financial Statement Of Companies to quickly test their knowledge of the chapter. These multiple-choice questions have been designed as per the latest syllabus for Class 12 Accountancy released by CBSE. Our expert teachers suggest that you should practice daily and solving these objective questions of Chapter 3 Financial Statement Of Companies to understand the important concepts and better marks in your school tests.

Chapter 3 Financial Statement Of Companies NCERT Based Objective Questions

Our expert teachers have designed these Accountancy MCQs based on the official NCERT book for Class 12. We have identified all questions from the most important topics that are always asked in exams. After solving these, please compare your choices with our provided answers. For better understanding of Chapter 3 Financial Statement Of Companies, you should also refer to our NCERT solutions for Class 12 Accountancy created by our team.

Online Practice and Revision for Chapter 3 Financial Statement Of Companies Accountancy

To prepare for your exams you should also take the Class 12 Accountancy MCQ Test for this chapter on our website. This will help you improve your speed and accuracy and its also free for you. Regular revision of these Accountancy topics will make you an expert in all important chapters of your course.

FAQs

You can get most exhaustive CBSE Class 12 Accountancy Case Study Questions Financial Statements of a Company MCQs for free on StudiesToday.com. These MCQs for Class 12 Accountancy are updated for the 2026-27 academic session as per CBSE examination standards.

Yes, our CBSE Class 12 Accountancy Case Study Questions Financial Statements of a Company MCQs include the latest type of questions, such as Assertion-Reasoning and Case-based MCQs. 50% of the CBSE paper is now competency-based.

By solving our CBSE Class 12 Accountancy Case Study Questions Financial Statements of a Company MCQs, Class 12 students can improve their accuracy and speed which is important as objective questions provide a chance to secure 100% marks in the Accountancy.

Yes, Accountancy MCQs for Class 12 have answer key and brief explanations to help students understand logic behind the correct option as its important for 2026 competency-focused CBSE exams.

Yes, you can also access online interactive tests for CBSE Class 12 Accountancy Case Study Questions Financial Statements of a Company MCQs on StudiesToday.com as they provide instant answers and score to help you track your progress in Accountancy.