Read and download the CBSE Class 11 Accountancy Financial Statements II Worksheet Set 01 in PDF format. We have provided exhaustive and printable Class 11 Accountancy worksheets for Chapter 9 Financial Statements - II, designed by expert teachers. These resources align with the 2026-27 syllabus and examination patterns issued by NCERT, CBSE, and KVS, helping students master all important chapter topics.

Chapter-wise Worksheet for Class 11 Accountancy Chapter 9 Financial Statements - II

Students of Class 11 should use this Accountancy practice paper to check their understanding of Chapter 9 Financial Statements - II as it includes essential problems and detailed solutions. Regular self-testing with these will help you achieve higher marks in your school tests and final examinations.

Class 11 Accountancy Chapter 9 Financial Statements - II Worksheet with Answers

Short Answer Type Questions :

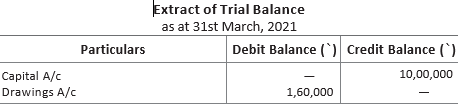

Question: Consider the following extract of trial balance from books of Prateek Limited.

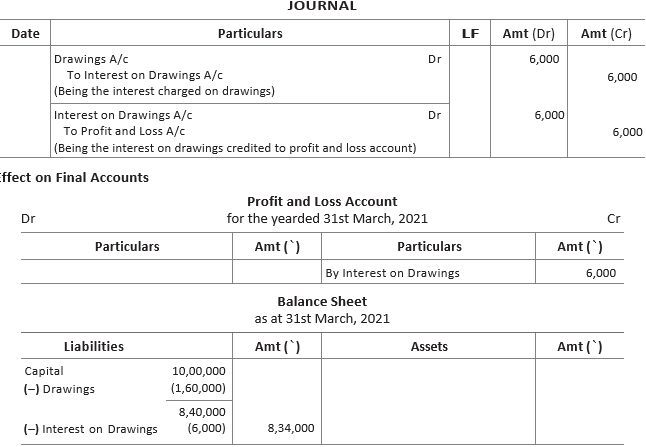

Adjustment Charge ₹ 6,000 as interest on drawings.

Pass an adjusting entry and show effect on financial statements.

Answer: Adjustment Entries

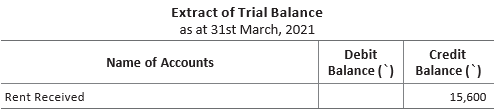

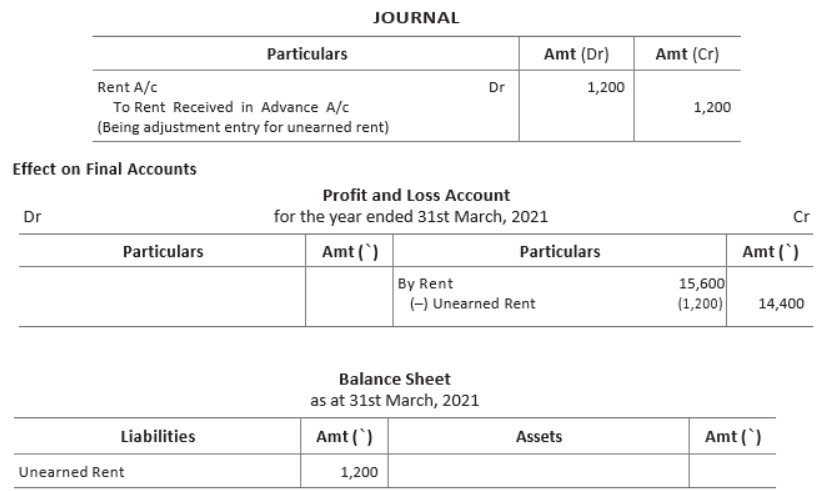

Question: Consider the following extract of trial balance taken from Prakhar’s Books

Additional Information

Rent received but not earned ₹ 1,200.

Pass an adjusting entry and show how will this appear in final accounts.

Answer: Adjustment Entry

Question: What is meant by closing stock? Show its treatment in final accounts.

Answer: Closing stock implies the value of unsold goods at the end of an accounting period. Closing stock is valued at cost or net realisable value, whichever is lower.

If closing stock is given in adjustment, it will be shown on the credit side of trading account and will also be shown on the assets side of balance sheet under current assets. If closing stock is given in trial balance, it will only be shown on the assets side of balance sheet under current assets.

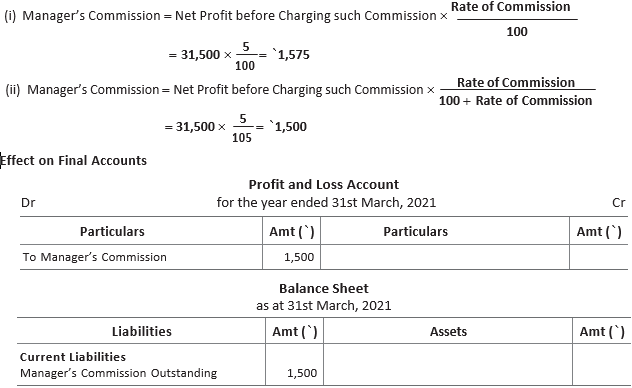

Question: The net profit of a firm amounts to ₹ 31,500 before charging commission. The manager of the firm is entitled to a commission of 5% on the net profits. Calculate the commission payable to the manager in each of the following alternative cases and also show its effect on final accounts.

(i) If the manager is allowed commission on the net profit before charging such commission.

(ii) If the manager is allowed commission on the net profit after charging such commission.

Also, show its treatment in final accounts ending on 31st March, 2021.

Answer:

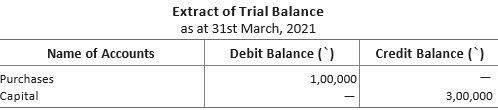

Question: Consider the following extract of trial balance taken from books of Mehta Limited.

Additional Information

During the year, the proprietor, Mr Mehta withdrew goods worth ₹ 5,000.

Pass an adjusting entry and show effect on financial statements.

Answer: Adjusting Entry

Question: What is meant by provision for doubtful debts? Why is it necessary to create a provision for doubtful debts at the time of preparation of final accounts?

Answer: The provision for doubtful debts is estimated amount of bad debts that will arise from amount receivable from debtors. In order to bring an element of certainty in amount of debtors, a provision for doubtful debts is created to cover the loss of possible bad debts as per the principle of prudence or conservatism.

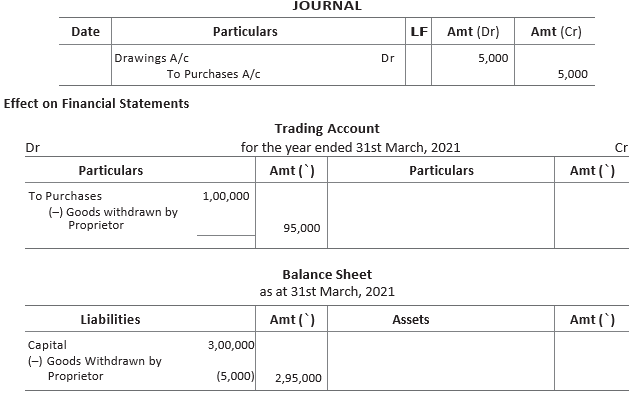

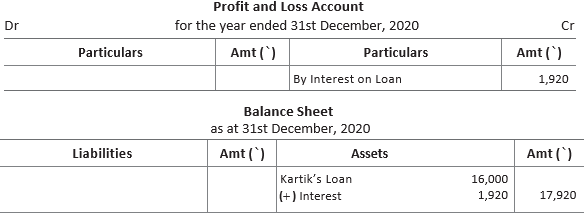

Question: Consider the following extract of trial balance of ABC Limited

Adjustment Interest on Kartik’s loan is due to be received @ 12% per annum for the whole year.

Pass an adjusting entry and show effect on financial statements.

Answer: Adjustment Entries

Working Note

Interest of Loan = 16,000 ×12/100 = ₹ 1,920

Effect on Final Accounts

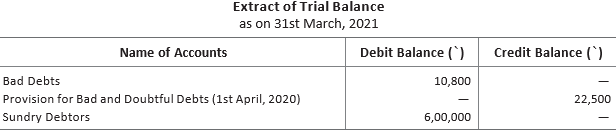

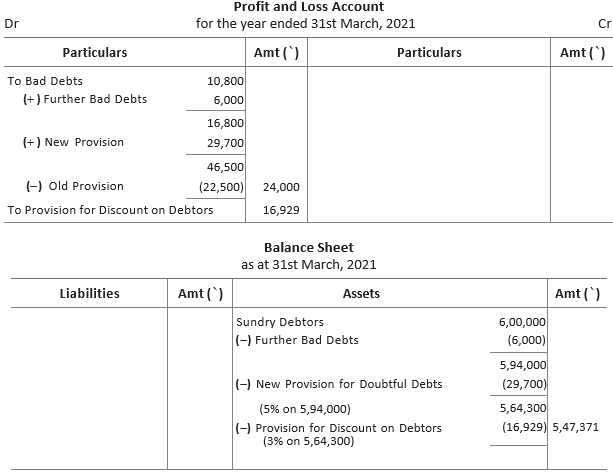

Question: Consider the following extract of trial balance taken from books of Harshit Enterprises.

Additional Information

(i) Write-off further bad debts ₹ 6,000.

(ii) Provision for doubtful debts to be maintained at 5% on sundry debtors.

(iii) Create a provision for discount on sundry debtors at 3%.

Show effect on profit and loss account and balance sheet.

Answer: Effect on Final Acccounts

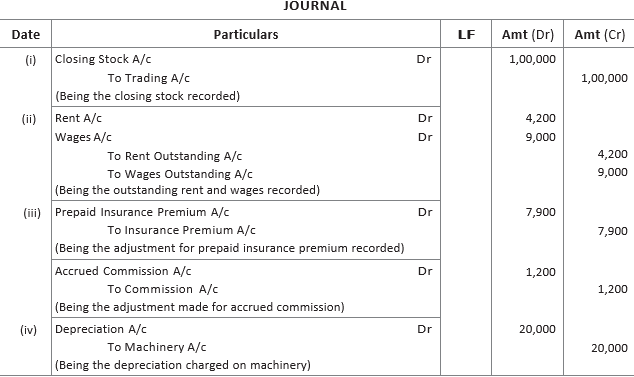

Question: Following trial balance is prepared on 31st March, 2019 from a trader’s book

Taking into consideration the adjustments given below. Pass the journal entries for the same.

(i) Closing stock ₹ 1,00,000

(ii) Outstanding rent ₹ 4,200 and outstanding wages ₹ 9,000

(iii) Prepaid insurance ₹ 7,900 and accrued commission ₹ 1,200

(iv) Charge depreciation on furniture @ 10% p.a.

Answer:

Working Note

Depreciation of Machinery = 2,00,000 ×10/100 = ₹ 20,000

Question: What are the adjusting entries? Why are they necessary for preparing final accounts?

Or

Why is it necessary to record the adjusting entries in the preparation of final accounts?

Answer: It is the entry passed to record expenses and incomes that relate to the accounting period but are yet to be paid or received.

The need of making various adjustments are stated below

(i) To ascertain the true profit or loss of the business.

(ii) To determine the true financial position of the business.

(iii) To make a record of the transactions earlier omitted in the books.

(iv) To rectify the errors committed in the books.

(v) To complete the incomplete transactions.

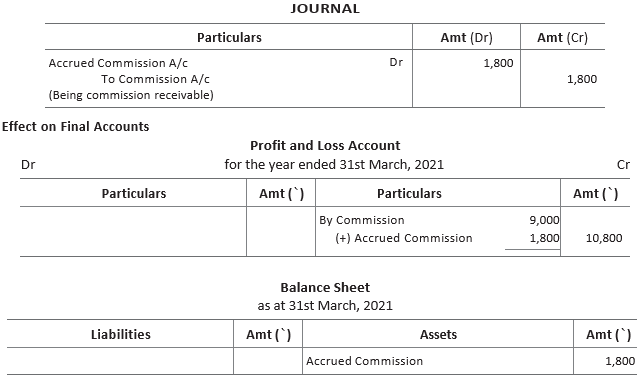

Question: Consider the following extract of trial balance

Additional Information

Commission earned but not received ₹ 1,800.

Pass an adjusting entry and show how will this appear in final accounts.

Answer: Adjustment Entry

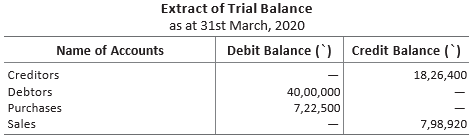

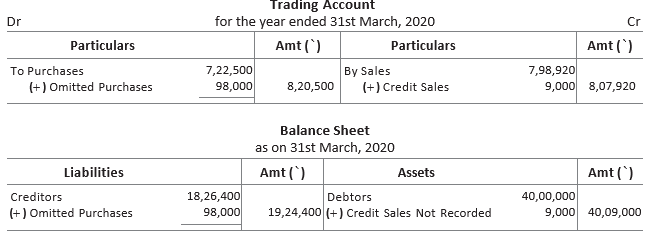

Question: Consider the following extract of trial balance taken from books of Manisha Enterprises.

Additional Information

(i) Credit sales of ₹ 9,000 were not recorded in books of accounts.

(ii) Received ₹ 98,000 worth of goods on 29th March, 2020 but the invoice of purchases was not recorded.

Answer:

Question: State the meaning of

(i) Outstanding expenses

(ii) Prepaid expenses

(iii) Income received in advance

Answer: (i) Outstanding Expenses Those expenses whose benefit have been derived during the current year but payment is not made at the end of the year are known as outstanding expenses.

(ii) Prepaid Expenses Those expenses which have been paid in current year but the benefit of which will be available in the next accounting year are known as prepaid expenses.

(iii) Income Received in Advance The income or portion of income which is received during the current accounting year but has not been earned is called unearned income.

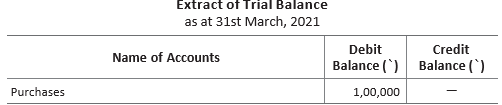

Question: Consider the following trial balance of Rohan Limited.

Additional Information

During the year the proprietor, Mr Rohan distributed goods worth ₹ 10,000 as free samples.

Pass an adjusting entry and show effect on financial statements.

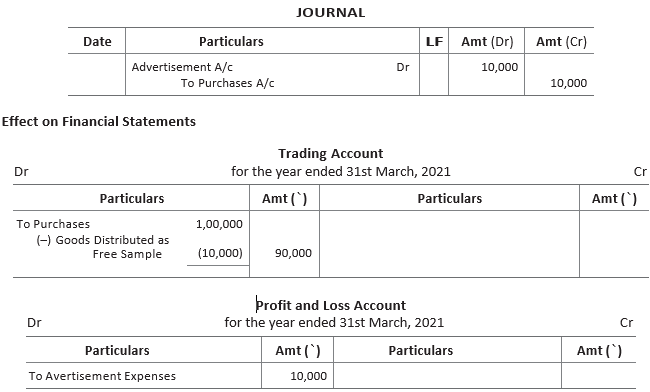

Answer: Adjusting Entry

Long Answer Type Questions :

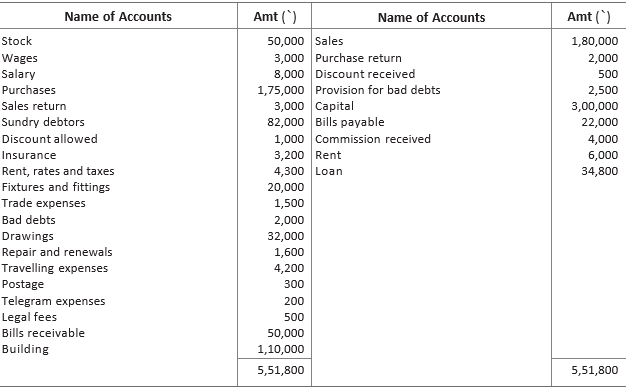

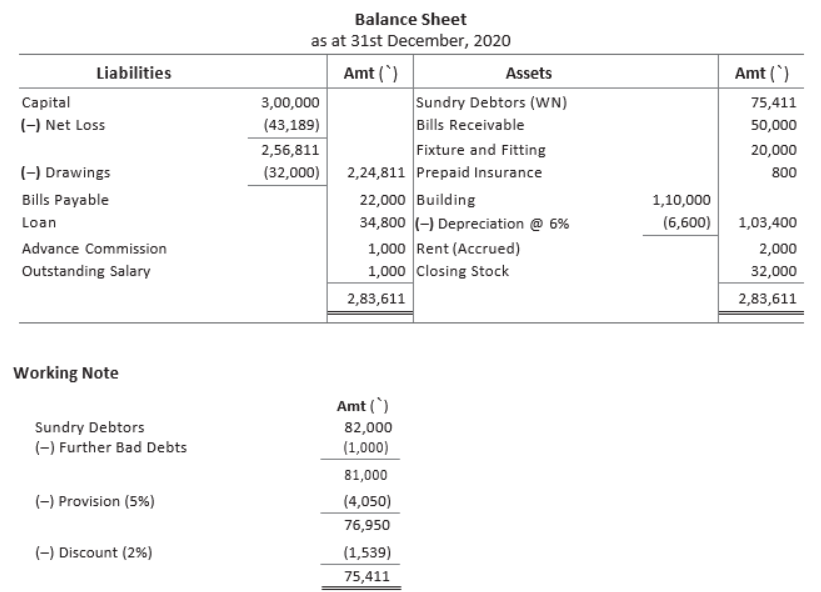

Question: Prepare a trading and profit and loss account for the year ending 31st December, 2020 from the balances extracted from M/s Rahul and Sons. Also prepare a balance sheet at the end of the year.

Adjustments

(i) Commission received in advance ₹ 1,000.

(ii) Rent received ₹ 2,000.

(iii) Salary outstanding ₹ 1,000 and insurance prepaid ₹ 800.

(iv) Further bad debts ₹ 1,000 and provision for bad debts@5% on debtors and discount on debtors@2%.

(v) Closing stock ₹ 32,000.

(vi) Depreciation on building @ 6% p.a.

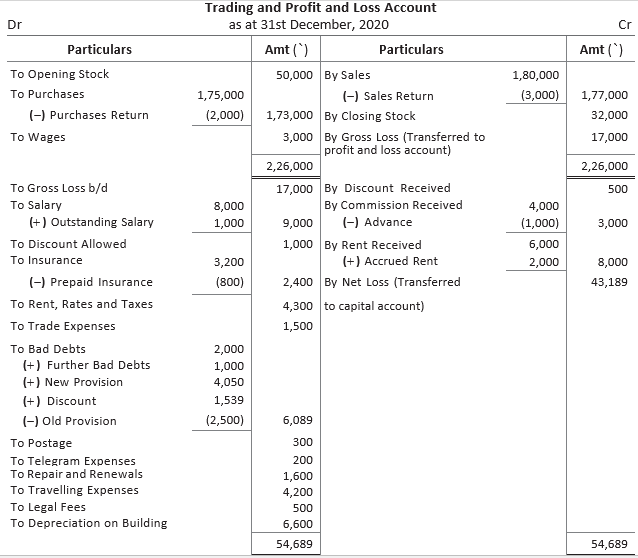

Answer:

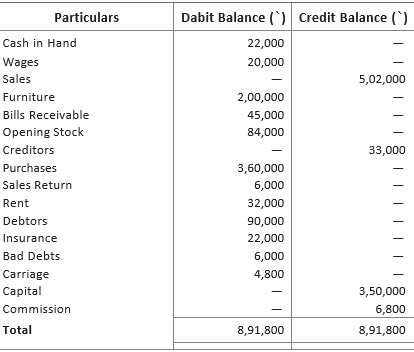

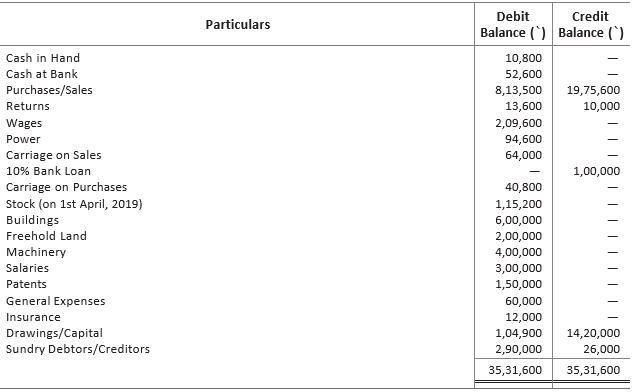

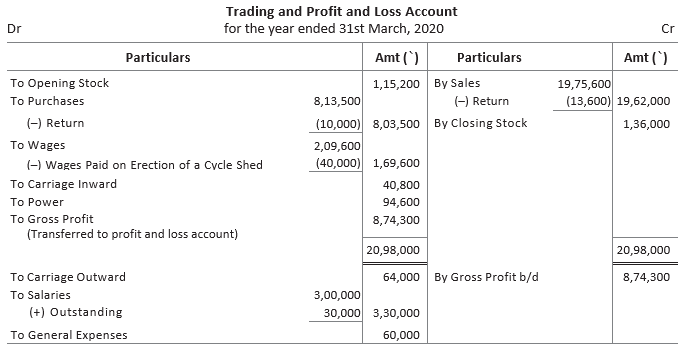

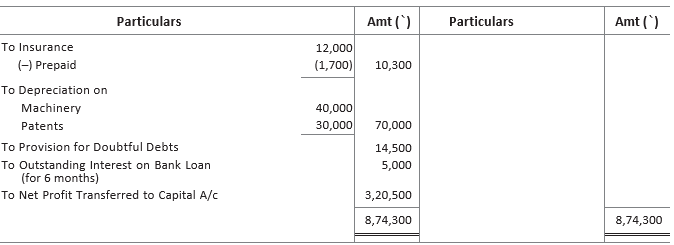

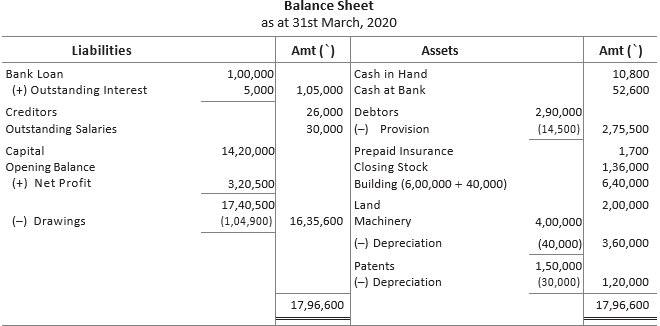

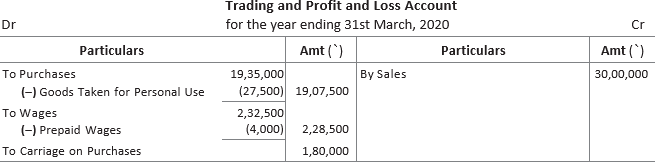

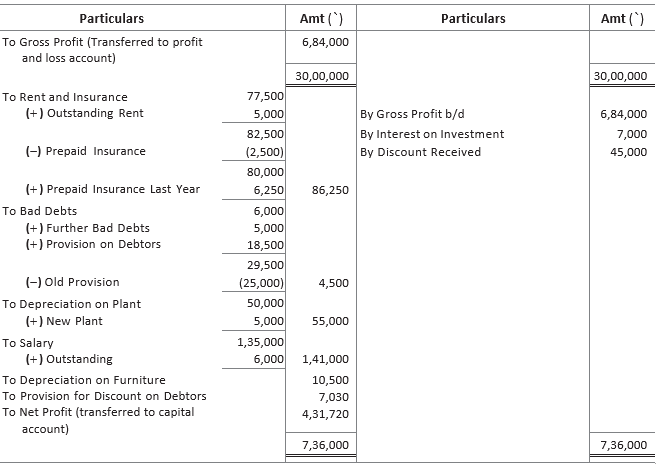

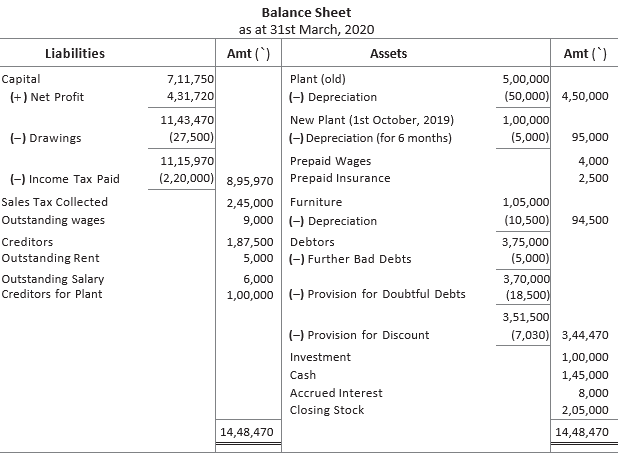

Question: The following is the trial balance of Mr Chidambram on 31st March, 2020.

Taking into account the following adjustments, prepare trading and profit and loss account and the balance sheet.

(i) Stock in hand on 31st March, 2020 is ₹ 1,36,000.

(ii) Machinery is to be depreciated at the rate of 10% p.a. and patent at the rate of 20% p.a.

(iii) Salaries for the month of March, 2020 amounting to ₹ 30,000 were unpaid.

(iv) Insurance includes a premium of ₹ 1,700 for 2020-21.

(v) Wages include a sum of ₹ 40,000 spent on the erection of a cycle shed for employees and customers.

(vi) A provision for doubtful debts is to be created to the extent of 5% on sundry debtors.

(vii) Bank loan was taken on 1st October, 2019.

Answer:

Question: From the books of M/s Aggarwal, the following trial balance has been prepared on 31st March, 2020

Prepare the trading and profit and loss account for the year ended 31st March, 2020 and the balance sheet as at that date, taking into consideration the adjustments given below

(i) On 1st October, 2019, plant worth ₹ 1,00,000 was purchased on credit but no entry has been passed.

(ii) Outstanding expenses rent ₹ 5,000 and salary ₹ 6,000.

(iii) Prepaid expenses insurance ₹ 2,500 and wages ₹ 4,000.

(iv) Goods worth ₹ 27,500 were taken for personal use by the owner but no entry has been made.

(v) Write-off depreciation on plant and furniture @ 10% p.a.

(vi) Write-off ₹ 5,000 from debtors as bad debts and create provision for doubtful debts @ 5% and 2% provision for discount on debtors.

Answer:

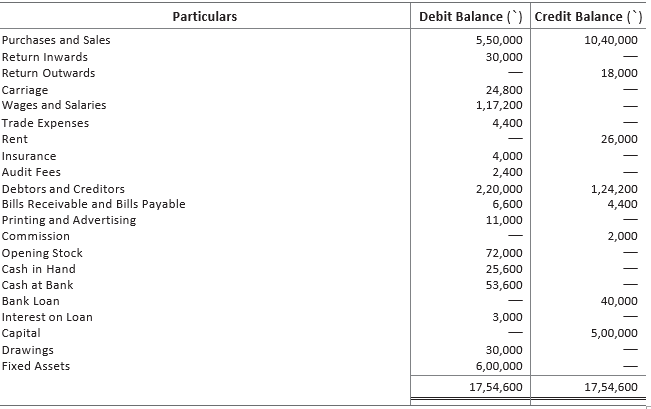

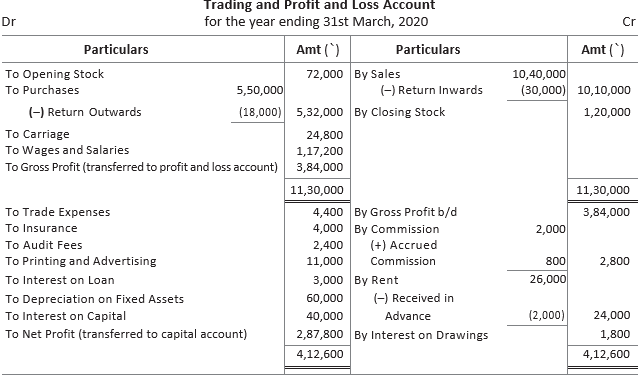

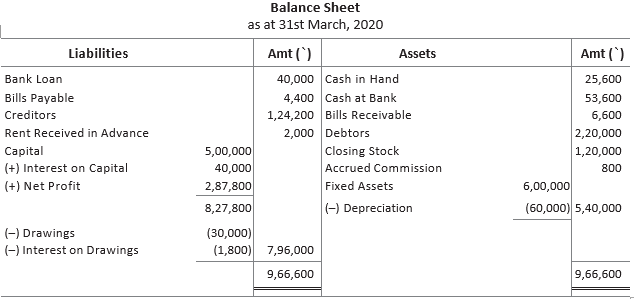

Question: From the following trial balance of Sh. Prakash, prepare trading and profit and loss account for the year ended 31st March, 2020 and balance sheet as at that date.

Additional Information

(i) Stock at the end₹1,20,000. (ii) Depreciation to be charged on fixed assets @10%.

(iii) Commission earned but not received amounting to ₹ 800.

(iv) Rent received in advance ₹ 2,000.

(v) 8% interest to be allowed on capital and ₹ 1,800 to be charged as interest on drawings.

Answer:

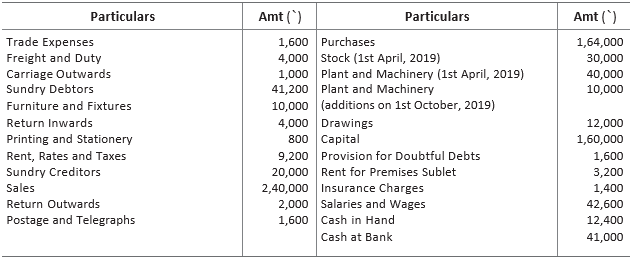

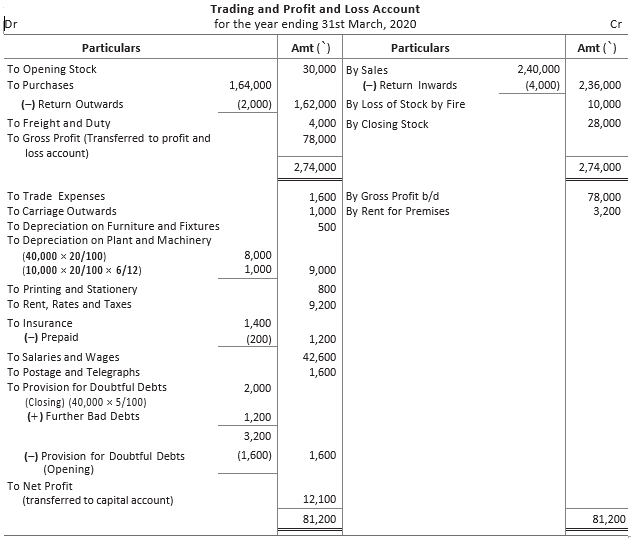

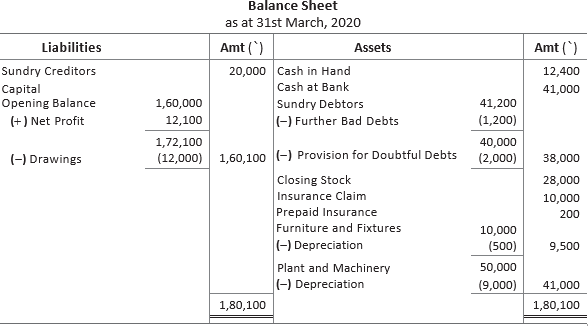

Question: From the following ledger balances of Mr Navjot Singh, prepare the trading and profit and loss account for the year ended 31st March, 2020 and the balance sheet as at that date after making the necessary adjustments.

Additional Information

(i) Stock on 31st March, 2020 was ₹ 28,000.

(ii) Write-off ₹ 1,200 as bad debts.

(iii) Provision for doubtful debts is to be maintained @ 5%.

(iv) Provision for depreciation on furniture and fixtures at 5% p.a. and on plant and machinery at 20% p.a.

(v) Insurance prepaid was ₹ 200.

(vi) A fire occurred in the godown and stock of the value of ₹ 10,000 was destroyed. It was insured and the insurance company admitted full claim.

Answer:

Note – Sometimes, the balance in the provision for doubtful debts account is more than sufficient to meet the bad debts and the new provision required. Thus, remaining amount is then credited to the profit and loss account.

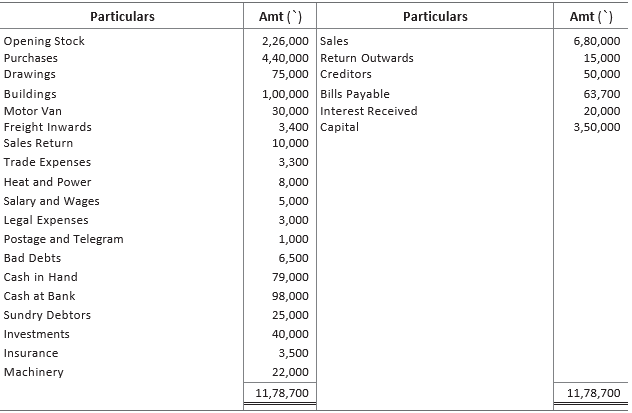

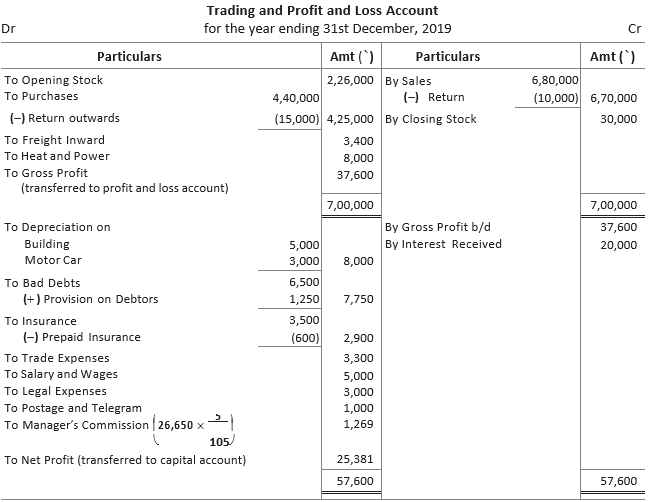

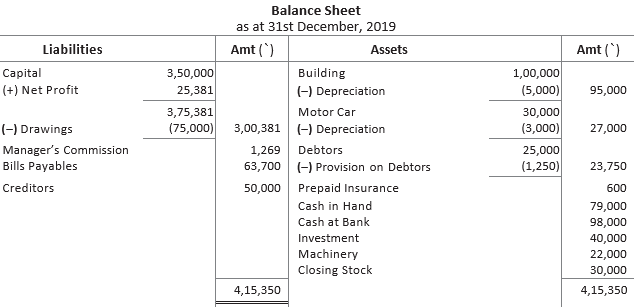

Question: Following balances have been extracted from the trial balance of M/s Keshav Electronics Ltd. You are required to prepare the trading and profit and loss account and balance sheet as on 31st December, 2019.

The following additional information is available

(i) Stock on 31st December, 2019 was ₹ 30,000.

(ii) Depreciation is to be charged on building @ 5% and motor van @ 10%.

(iii) Provision for doubtful debts is to be maintained @ 5% on sundry debtors.

(iv) Unexpired insurance was ₹ 600.

(v) The manager is entitled to commission @ 5% on net profit after charging such commission.

Answer:

Free study material for Accountancy

CBSE Accountancy Class 11 Chapter 9 Financial Statements - II Worksheet

Students can use the practice questions and answers provided above for Chapter 9 Financial Statements - II to prepare for their upcoming school tests. This resource is designed by expert teachers as per the latest 2026 syllabus released by CBSE for Class 11. We suggest that Class 11 students solve these questions daily for a strong foundation in Accountancy.

Chapter 9 Financial Statements - II Solutions & NCERT Alignment

Our expert teachers have referred to the latest NCERT book for Class 11 Accountancy to create these exercises. After solving the questions you should compare your answers with our detailed solutions as they have been designed by expert teachers. You will understand the correct way to write answers for the CBSE exams. You can also see above MCQ questions for Accountancy to cover every important topic in the chapter.

Class 11 Exam Preparation Strategy

Regular practice of this Class 11 Accountancy study material helps you to be familiar with the most regularly asked exam topics. If you find any topic in Chapter 9 Financial Statements - II difficult then you can refer to our NCERT solutions for Class 11 Accountancy. All revision sheets and printable assignments on studiestoday.com are free and updated to help students get better scores in their school examinations.

FAQs

You can download the latest chapter-wise printable worksheets for Class 11 Accountancy Chapter 9 Financial Statements - II for free from StudiesToday.com. These have been made as per the latest CBSE curriculum for this academic year.

Yes, Class 11 Accountancy worksheets for Chapter 9 Financial Statements - II focus on activity-based learning and also competency-style questions. This helps students to apply theoretical knowledge to practical scenarios.

Yes, we have provided solved worksheets for Class 11 Accountancy Chapter 9 Financial Statements - II to help students verify their answers instantly.

Yes, our Class 11 Accountancy test sheets are mobile-friendly PDFs and can be printed by teachers for classroom.

For Chapter 9 Financial Statements - II, regular practice with our worksheets will improve question-handling speed and help students understand all technical terms and diagrams.