Download CBSE Class 11 Syllabus for Accountancy 2023 2024. Refer to the latest syllabus provided below and free download latest curriculum of Class 11 for Accountancy issued by CBSE and NCERT, free download in pdf, get topic wise weightage, suggested readings and books based on latest syllabus and guidelines. The Accountancy Class 11 Syllabus curriculum has been developed and issued by CBSE and NCERT for Accountancy in Class 11. All students studying in Class 11 are suggested to go through latest syllabus to ensure that their preparation is as per the latest syllabus issued by CBSE NCERT KVS. Class 11 Accountancy students should do preparation for Accountancy exam strictly based on the latest curriculum and concentrate more on the topics with higher weightage to help them score higher marks in Class 11 Accountancy class tests and exams

Class 11 Accountancy Syllabus

It is important for students to study as per the latest Class 11 Accountancy curriculum and marks breakup as per important topics. This will help to prepare properly for the upcoming examination. You can click on the following links to download the latest and past year syllabus provided by us below.

Year Wise Accountancy Syllabus Class 11

Accountancy (Code No.055)

Course Structure

Class-XI (2023-24)

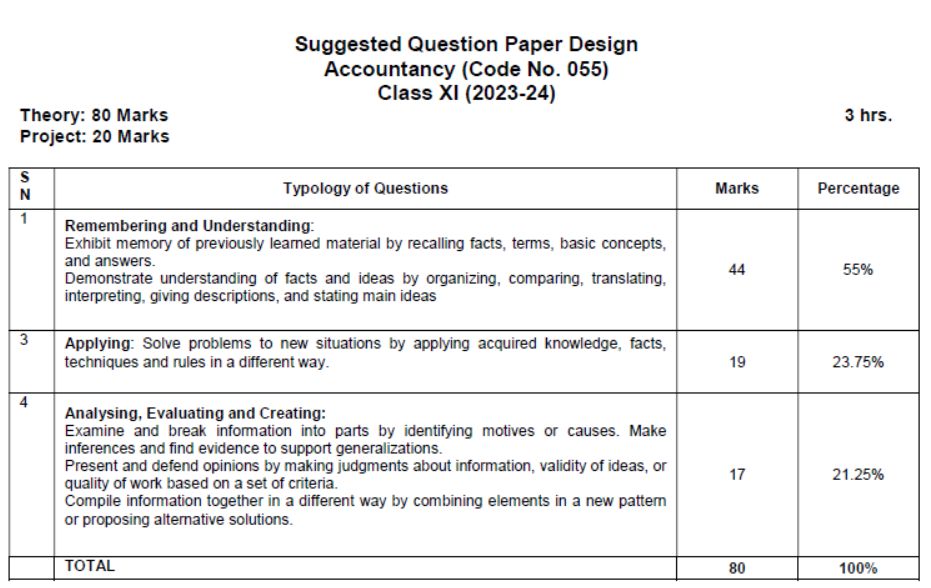

Theory: 80 Marks 3 Hours

Project: 20 Marks

Units Periods Marks

Part A: Financial Accounting-1

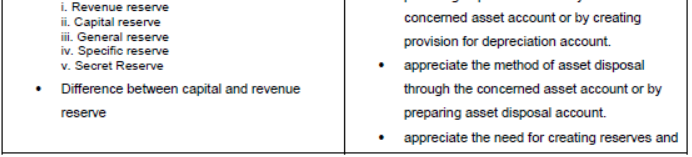

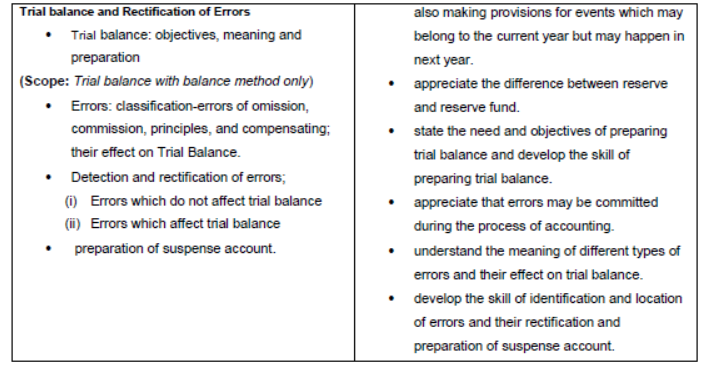

Unit-1: Theoretical Framework 25 12

Unit-2: Accounting Process 115 44

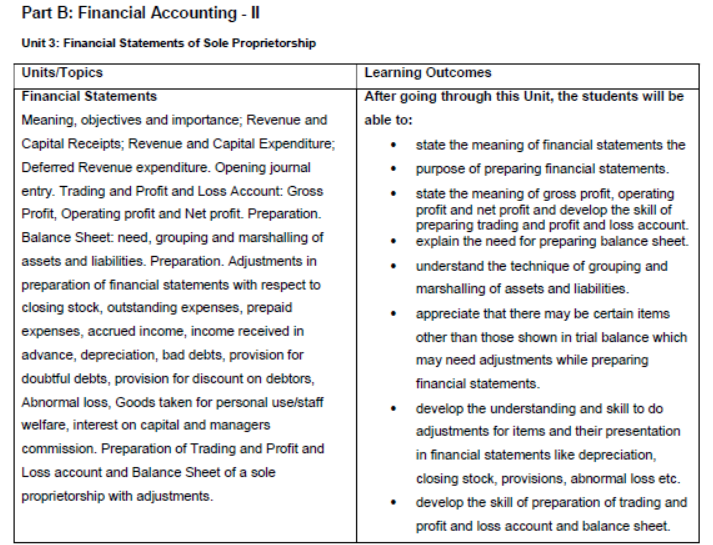

Part B: Financial Accounting-II

Unit-3: Financial Statements of Sole Proprietorship 60 24

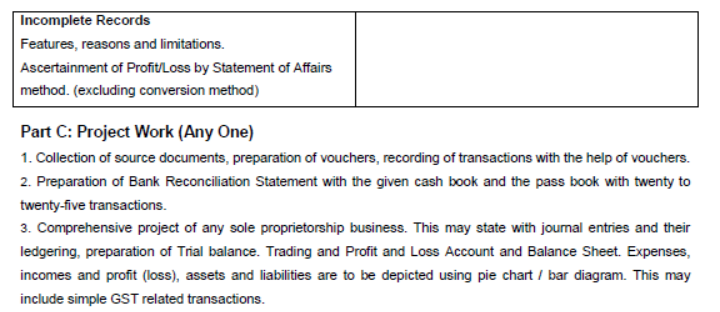

Part C: Project Work 20 20

PART A: FINANCIAL ACCOUNTING - I

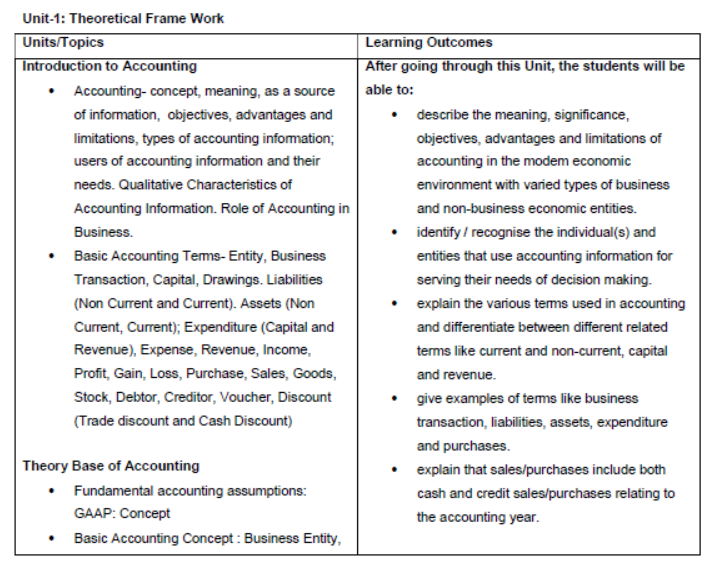

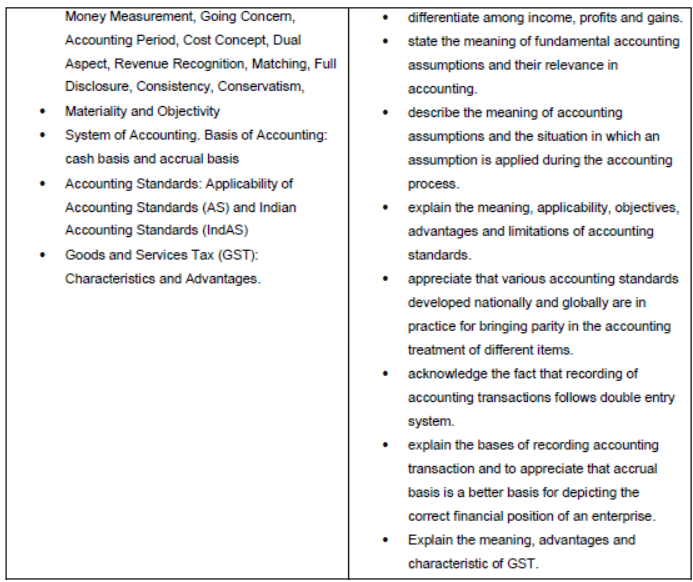

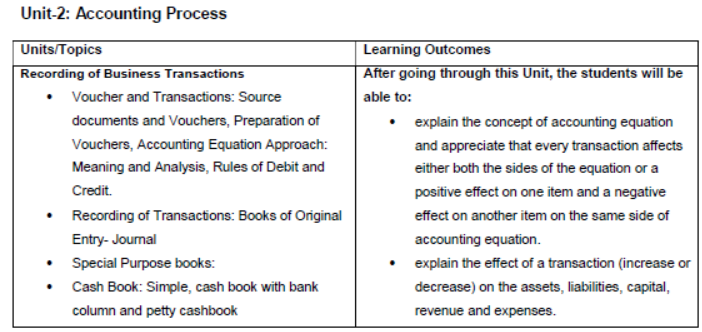

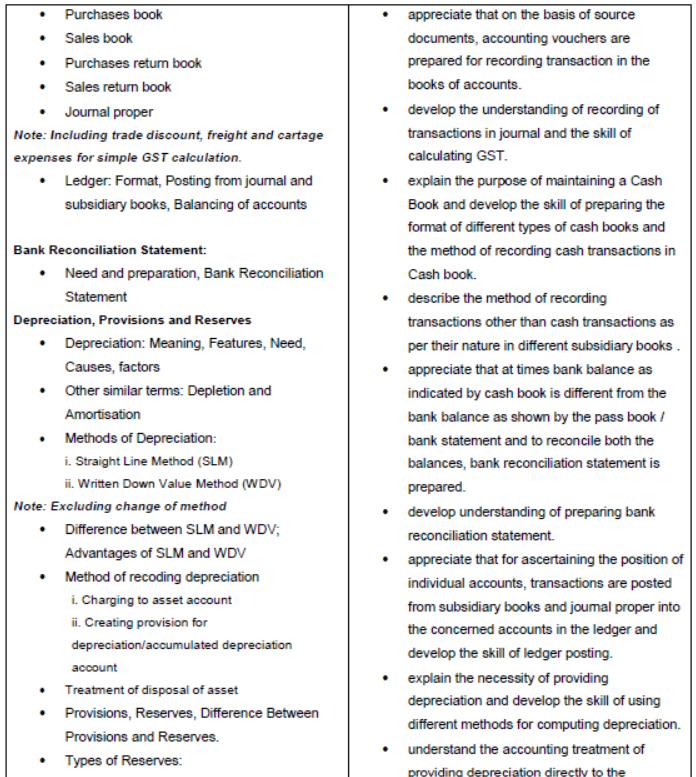

Unit-1: Theoretical Frame Work

PROJECT WORK

It is suggested to undertake this project after completing the unit on preparation of financial statements. The student(s) will be allowed to select any business of their choice or develop the transaction of imaginary business. The project is to run through the chapters and make the project an interesting process. The amounts should emerge as more realistic and closer to reality.

Specific Guidelines for Teachers

Give a list of options to the students to select a business form. You can add to the given list:

1. A beauty parlour 10. Men's wear 19. A coffee shop

2. Men's saloon 11. Ladies wear 20. A music shop

3. A tailoring shop 12. Kiddies wear 21. A juice shop

4. A canteen 13. A Saree shop 22. A school canteen

5. A cake shop 14. Artificial jewellery shop 23. An ice cream parlour

6. A confectionery shop 15. A small restaurant 24. A sandwich shop

7. A chocolate shop 16. A sweet shop 25. A flower shop

8. A dry cleaner 17. A grocery shop

9. A stationery shop 18. A shoe shop

After selection, advise the student(s) to visit a shop in the locality (this will help them to settle on a realistic amounts different items. The student(s) would be able to see the things as they need to invest in furniture, decor, lights, machines, computers etc.

A suggested list of different item is given below.

1. Rent 19. Wages and Salary

2. Advance rent [approximately three months] 20. Newspaper and magazines

3. Electricity deposit 21. Petty expenses

4. Electricity bill 22. Tea expenses

5. Electricity fitting 23. Packaging expenses

6. Water bill 24. Transport

7. Water connection security deposit 25. Delivery cycle or a vehicle purchased

8. Water fittings 26. Registration

9. Telephone bill 27. Insurance

10. Telephone security deposit 28. Auditors fee

11. Telephone instrument 29. Repairs & Maintenance

12. Furniture 30. Depreciations

13. Computers 31. Air conditioners

14. Internet connection 32. Fans and lights

15. Stationery 33. Interior decorations

16. Advertisements 34. Refrigerators

17. Glow sign 35. Purchase and sales

18. Rates and Taxes

At this stage, performas of bulk of originality and ledger may be provided to the students and they may be asked to complete the same.

In the next step the students are expected to prepare the trial balance and the financial statements.

You can download the CBSE 2025 Syllabus for Class 11 Accountancy for latest session from StudiesToday.com

Yes, you can click on the links above and download Syllabus in PDF for Class 11 for Accountancy

Yes, the syllabus issued for Class 11 Accountancy have been made available here for latest 2025 academic session

You can easily access the links above and download the Class 11 Syllabus Accountancy

There is no charge for the Syllabus for Class 11 CBSE Accountancy you can download everything free

Planning your studies as per syllabus given on studiestoday for Class 11 subject Accountancy can help you to score better marks in exams

Yes, studiestoday.com provides all latest CBSE Class 11 Accountancy Syllabus with suggested books for current academic session

Yes, studiestoday provides curriculum in Pdf for Class 11 Accountancy in mobile-friendly format and can be accessed on smartphones and tablets.

Yes, syllabus for Class 11 Accountancy is available in multiple languages, including English, Hindi